Crypto World

Trump Administration Secures $10 Billion Payment From TikTok Deal Investors

TLDR

- Investors acquiring TikTok’s U.S. operations will pay approximately $10 billion to the Trump administration

- Major investors include Oracle, Silver Lake, and Abu Dhabi’s MGX fund

- Initial payment of $2.5 billion has been transferred to Treasury, with additional installments scheduled

- The U.S. TikTok entity carries a valuation of approximately $14 billion, though experts debate whether this is accurate

- The transaction stems from legislation mandating ByteDance divest its stake in TikTok’s American business

The Trump administration negotiated an agreement that allowed TikTok to continue operating across the United States. Under the terms of this arrangement, the investors who assumed control of TikTok’s American operations committed to paying approximately $10 billion to the federal government.

This substantial fee comes in addition to the capital invested to establish a new domestically-based entity operating the popular social media platform. Key investors such as Oracle, Silver Lake, and MGX from Abu Dhabi transferred approximately $2.5 billion to the U.S. Treasury upon completion of the transaction in January. Additional payments are scheduled until the full $10 billion amount is satisfied.

ByteDance, TikTok’s parent company based in China, completed the transaction in January. The deal established a joint venture with majority American ownership called TikTok USDS Joint Venture LLC. This newly formed entity oversees U.S. user information, mobile applications, and proprietary algorithms.

ByteDance retains close to 20% ownership in the restructured entity and has licensed its algorithmic technology to the venture. The American entity must also distribute profits back to ByteDance.

Vice President JD Vance stated the restructured U.S. TikTok entity holds a valuation near $14 billion. Technology industry analysts have challenged this figure, suggesting it significantly underestimates the company’s true worth.

How the Fee Compares to Typical Deal-Making

The $10 billion government fee represents an almost unparalleled arrangement for a government facilitating a private sector transaction, according to business historians. To put this in perspective, investment banking fees on standard deals typically amount to less than 1% of total transaction value. Bank of America expects to collect approximately $130 million for its advisory services on Norfolk Southern’s $71.5 billion acquisition — representing one of the largest individual banking fees ever recorded.

Administration representatives defend the fee structure as appropriate. They emphasize Trump’s critical role in preserving TikTok’s presence in America and navigating complex negotiations with Chinese authorities while satisfying national security requirements from Congress.

The transaction was mandated by legislation enacted during Trump’s initial presidential term. That statute compelled ByteDance to significantly reduce its ownership position in TikTok’s American operations or face a complete shutdown. Congressional leaders had expressed significant concerns about a Chinese-owned corporation maintaining access to personal information of more than 200 million American citizens.

Earlier this month, Trump and Attorney General Pam Bondi faced legal action from retail shareholders of competing social media platforms. These investors are attempting to overturn the government’s approval of the ByteDance joint venture transaction.

The Broader Pattern of Government Stakes in Private Companies

The TikTok deal represents one element of a larger trend. The Trump administration has similarly secured nearly 10% ownership in Intel. It negotiated to receive a portion of chip sales to China from Nvidia as consideration for granting export authorization. The administration has also acquired equity positions in additional corporations and maintains a “golden share” in U.S. Steel after Nippon Steel’s acquisition.

The Wall Street Journal initially disclosed the $10 billion fee amount on March 13, 2026.

Meanwhile, the other community member believes the patience of XRP investors is “genuinely a psychological phenomenon.”

Ripple and its native non-stablecoin have a substantial community, but also a fair share of critics due to some of the core implementations. Its growth in popularity over the past several years has been quite astonishing, which sometimes even surpasses its market rise.

As such, whenever someone, especially a high-profile figure within the crypto industry, speaks against XRP in some form, there’s usually backlash.

A Bank Wearing a Hoodie?

Davinci Jeremie is among the OG crypto influencers and analysts, famously advising people to buy BTC when it was worth $1. In a recent post on X, he criticized XRP for several of its key features that could actually be making it a “bank wearing a hoodie.”

He outlined that these factors could be hidden leverage, fake decentralization, pausable exits, insider advantages, and users locked in wrapped IOUs. Instead, he commented that bitcoin does not have any of these.

Your favorite crypto project is just a bank wearing a hoodie.

*cough* $XRP

Hidden leverage ✓

Fake decentralization ✓

Pausable exits ✓

Insider advantages ✓

Users locked in wrapped IOUs ✓#Bitcoin has none of these.Name one other project that doesn’t. I’ll wait. 👇

— Davinci Jeremie (@Davincij15) March 11, 2026

Somewhat expectedly, most comments below the posts lashed out at Jeremie, with one saying, “That’s the dumbest thing I’ve ever read from you. XRP is everything that they wanted Bitcoin to be. That’s a fact.” Naturally, Jeremie disagreed. Others, though, agreed with his initial comments, saying that “XRP is a s**t and not a match” to bitcoin.

Finally, XRP’s Moment?

In contrast to the aforementioned statement, XRP Bags, among the vocal members of the XRP community on X, outlined what it feels like to be a holder of the cross-border token. They believe every year so far has begun with big promises but seemingly have failed to deliver, or at least until 2023, when it was the first big break in the lawsuit against the SEC.

You may also like:

More promisingly, though, the user noted that 2025 was an “I told you so” year for XRP, while 2026 shows that they are “just getting started.”

the XRP holder experience:

2017 — “this is going to change banking forever”

2018 — “just wait”

2019 — “keep stacking”

2020 — “SEC who?”

2021 — “SEC lawsuit, this is actually bullish”

2022 — “just wait”

2023 — “WE WON (partially)”

2024 — “Keep accumulating”

2025 — “told you”

2026…— XRP Bags💰👨🏽🚀 BagMan (@XRPBags) March 13, 2026

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

Opinion by: Ana Carolina Oliveira, chief compliance officer at Venga

Crypto doesn’t have a money laundering problem on its own. At least, not when compared to traditional finance, where the practice is at least twice as prevalent and over 90% of which is believed to go undetected. Money laundering is a general problem wherever we see the transfer of funds. That’s the good news.

Blockchain records everything for posterity. When money laundering does occur, an indelible record is created that allows the illicit financial flows to be traced from end to end.

Just because crypto doesn’t have a particular money laundering problem doesn’t mean that money laundering has been eradicated. The anti-money laundering system needs to evolve as a whole to strengthen preventive and investigative measures across traditional finance as well as centralized and decentralized finance (CeFi and DeFi) environments.

This evolution requires greater communication within the sector, improved feedback mechanisms, a deeper understanding of emerging typologies and more effective dissemination of new trends.

The recently published European Union AML Regulation (Regulation EU 2024/1624) sets some rules on this matter, but more needs to be done in practice. Achieving this calls for regulators and industry leaders to create the kind of guardrails that go beyond “box-checking” compliance.

Crypto must do better

It’s not enough to have AML procedures in place. These need to be constantly enhanced to ensure that crypto overcomes its misunderstood reputation as a high-risk money-laundering environment and strengthens its barriers to keep aggressively combating this practice.

This demands a cultural change in how we approach money laundering, with an emphasis on greater information sharing. Otherwise, criminals will simply shift operations from high AML venues to softer crypto targets where they can continue to ply their trade.

Crypto “enables” money laundering in exactly the same manner as fiat. The architecture may be different, but the outcome is the same: bad actors doing bad things with funds that facilitate everything from ransomware to, in the most egregious cases, terrorism.

Blockchain’s pseudonymity may be a feature, not a bug, but it makes it hard to know who you’re dealing with when it comes to self-hosted wallets, exacerbated when mixers are used to obfuscate the source of funds.

When you can’t easily identify the origin or owner of the funds, you will struggle to prevent money laundering.

Related: Universal blockchains buckle under real-world demands

That is the reality for fiat and crypto alike. A single exchange, no matter how robust its AML and Know Your Transaction tooling, lacks the visibility into everything that’s taking place onchain. Collectively, however, all crypto platforms possess vast knowledge of who’s doing what onchain, and when that “what” strays into the realm of suspected criminality, that information must be shared.

At present, initiatives like the Travel Rule, wallet screening and onchain analytics form a powerful AML barrier, but responsibility and the costs associated with creating the pathways to combat illicit activity, are delegated to individual entities. To give just one example, the Travel Rule mandates a SWIFT/IBAN-style identification system, but the industry has been left alone to create the technology and integration to facilitate this exchange of information.

In other words, regulators have delegated the implementation of a “crypto SWIFT system” to the industry. In a sector characterized by multi-jurisdictional companies that are subject to different geo-specific regulations, this compliance burden is colossal and labyrinthine. The ideal solution is for a global compliance standard to be implemented industry-wide.

Given the difficulties of getting different regulators and regions to agree to such a framework, the onus falls to the crypto industry, once more, to self-regulate. States and other national competent authorities must do better in regulating and setting the path for the industry to comply.

Fewer loopholes, more freedom

The biggest crypto money-laundering challenge at present is the difficulty of identifying who owns the wallets, and not the technology itself. Because the United States, EU and Asia have different thresholds and rules when it comes to sharing information, performing due diligence and enforcing the Travel Rule, there are loopholes that bad actors exploit.

Closing off these loopholes won’t just curtail money laundering; it will also empower legitimate users to enjoy the financial freedom that crypto provides. The freedom to transact, to trade and to tokenize without running into brick walls every time they change exchanges or switch regions. Because crypto is borderless, compliance needs to follow suit. Compliance needs to work everywhere, every time.

That’s why the industry needs to collaborate to share information, adopt best practices and signal to the world that blockchain is open for business but closed to criminals who have nowhere to hide their ill-gotten gains.

We’ve mastered the AML tools. Now we need to master the art of talking. Exchange to exchange. Platform to platform. Region to region. FIU to obliged entities. TradFi with CeFi. That’s how crypto’s stance on money laundering goes from low-tolerance to no-tolerance.

If we can achieve that, the industry will flourish.

Opinion by: Ana Carolina Oliveira, chief compliance officer at Venga.

This opinion article presents the author’s expert view, and it may not reflect the views of Cointelegraph.com. This content has undergone editorial review to ensure clarity and relevance. Cointelegraph remains committed to transparent reporting and upholding the highest standards of journalism. Readers are encouraged to conduct their own research before taking any actions related to the company.

XRP transactions jump 3x year-over-year, but price stays muted as daily network activity surges from approximately 1 million to nearly 3 million transactions.

Summary

- XRP Ledger activity surged to nearly 3M daily transactions.

- Growth is driven by RWAs, stablecoins, and institutional flows.

- XRP price remains muted, down 39% year-over-year.

The ledger data from XRPScan shows February 2026 posting 1.3 million average daily transactions, up from roughly 800,000 in May 2025.

XRP traded at $1.39 with a 24-hour range of $1.39 to $1.45, posting losses of 2.4% over 24 hours and 39.3% over one year.

The disconnect between surging network usage and stagnant price action has drawn attention from analysts who note the growth comes from real-world asset settlement, stablecoins, and institutional payment flows.

XRP transactions jump 3x year-over-year

XRP Brasil posted on X that the ledger jumped from 1 million to almost 3 million daily transactions in less than a year, calling the data “surgical” and stating “this isn’t noise, it’s real adoption.”

The account noted that while markets focus on price, the network processes real-world assets, stablecoins, and institutional flows behind the scenes.

Analyst PassingAnt identified three major drivers for the transaction growth: real-world assets, tokenized assets, and institutional payment rails.

The shift from 1 million to nearly 3 million daily transactions is the kind of growth that usually comes from on-chain financial activity rather than retail speculation.

September 2025 posted the lowest activity at approximately 700,000 daily transactions before the surge began.

January 2026 reached 1.05 million daily transactions, with February 2026 climbing to 1.3 million. The acceleration occurred while XRP price remained range-bound between $1.30 and $1.50 for most of the period.

Price remains muted with 39.3% yearly drop

XRP posted gains of 2.0% over seven days, 8.5% over 14 days, and 1.1% over 30 days, showing short-term recovery from recent lows.

The one-year performance of -39.3% shows the overall crypto market drawdown following Bitcoin’s October 2025 all-time high and subsequent drop.

Analyst Maxi noted XRP broke resistance levels but has yet to confirm with a daily candle close, calling Friday price moves “fake out Fridays.” The first short-term checkpoint sits at $2.36 and is a 70% gain from current levels.

The market value of USDC, the Circle-issued dollar-pegged stablecoin, is edging toward a new peak of roughly $80 billion as demand intensifies in the Middle East. Data from CoinMarketCap show USDC circulating supply at about $79.2 billion, a fresh all-time high that eclipses the previous peak just shy of $79 billion logged last December. The climb follows weeks of sustained supply growth, with the metric standing above $70 billion in early February and around $75 billion earlier this month. The widening footprint underscores how liquidity needs are shifting in a landscape where investors seek stable on-ramps and off-ramps amid global macro uncertainty.

In a post on X, Dubai-based analyst Rami Al-Hashimi attributed the surge to a broad appetite for moving funds out of conventional markets, saying over-the-counter desks in Dubai have struggled to keep pace with demand for USDC. The assertion dovetails with a broader narrative about stablecoins increasingly serving as a bridge for cross-border flows in regions facing FX volatility or capital controls. While the UAE’s property markets have drawn headlines for softness, the liquidity angle emphasizes a different use case for stablecoins: a readily accessible, dollar-linked liquidity layer that can be deployed with relatively low friction compared with traditional banking rails.

Dubai property slump may be driving USDC surge

Al-Hashimi connected the surge in stablecoin activity to turmoil in the United Arab Emirates’ real estate market. He argued that Dubai property prices have fallen by roughly 27% this month, fueling a rush among investors to reposition capital into digital assets. He framed the shift as a form of “war panic” and capital flight, suggesting a growing pattern of investors seeking liquidity and exit routes amid local real estate distress. The broader market backdrop is echoed by TradingView data, which show the Dubai Financial Market (DFM) Real Estate Index declining sharply from a peak around 16,800 to roughly 11,516, a slide near 31% in a compressed period. The correlation between real assets and a pivot to on-chain assets reflects a broader risk-off dynamic in which digital currencies are positioned as an escape hatch or hedge in uncertain times.

There are signs that the real estate slowdown is influencing pricing dynamics in the on-chain space as well. Some property listings have begun advertising discounts for buyers who pay with cryptocurrency, with Bitcoin (CRYPTO: BTC) cited as a preferred settlement option in certain corners of the market. The trend, while not universal, illustrates how digital assets are increasingly being used as a shopping tool for large-ticket purchases, even as the broader macro environment remains unsettled. The co-movement of real estate activity and crypto liquidity highlights how capital floods can reallocate quickly across asset classes when traditional channels tighten or become expensive to access.

Beyond the Dubai-specific story, market observers noted a notable shift in stablecoin usage on a global basis. In a development that has captured attention from traders and analysts, USDC is reported to have overtaken USDt (CRYPTO: USDT) in adjusted transaction volume for the year to date, according to Mizuho. The bank’s note indicates USDC handling roughly $2.2 trillion in adjusted transaction volume versus about $1.3 trillion for USDt, equating to roughly 64% of the combined volume. While USDt remains the dominant stablecoin by market capitalization—about $184 billion—the leap in on-chain throughput for USDC points to evolving user preferences and liquidity patterns within the stablecoin sector. The dynamic underscore is that liquidity is not static; it migrates as market participants seek efficiency, settlement speed, and regulatory clarity in different venues.

Taken together, the numbers paint a complex portrait of a market that is increasingly dependent on stable liquidity but is also becoming more sensitive to regional macro events. The growth in USDC supply and the related uptick in on-chain activity suggest that investors are prioritizing predictable settlement and cross-border transfer capabilities. At the same time, the continued magnitude of USDt’s market cap serves as a reminder that the stablecoin landscape remains fragmented, with different assets occupying distinct roles within portfolios and trading desks. While some observers point to a reshuffling of flows toward newer stablecoins, others caution that the sector’s regulatory and counterparty risk remains a central concern for market participants who rely on these digital currencies for everyday payments and liquidity provisioning.

Why it matters

For users and builders, the sustained expansion of USDC’s market footprint reinforces the role of stablecoins as a core liquidity layer in crypto markets. As demand for efficient settlement and cross-border transfers grows, stablecoins offer a familiar, dollar-linked settlement mechanism that can operate 24/7, reducing reliance on traditional financial rails. This can lower friction for institutions and retail traders alike, particularly in regions where FX controls or capital flight concerns drive preference for digital assets.

From a market structure perspective, the shift in transaction volumes toward USDC relative to USDt signals a potential recalibration of liquidity provision and exchange dynamics. If the trend persists, it could influence liquidity strategies on centralized and decentralized venues, affect funding rates, and alter risk premia across stablecoin-enabled pairs. Regulators are closely watching such developments, given ongoing scrutiny around stablecoin reserves, disclosures, and settlement practices. The evolving balance between stability, transparency, and efficiency will shape how market participants price and manage risk in the coming quarters.

For investors and traders, the Dubai-linked narrative adds a tangible example of how macro shocks in one region can ripple through crypto markets elsewhere. It reinforces the view that stablecoins remain a barometer of risk sentiment and capital mobility. As the ecosystem debates the merits of different stablecoins, users will increasingly evaluate not only collateral reserves and mint-and-burn mechanics but also the practical realities of liquidity access, regulatory alignment, and the speed of settlement across borders.

What to watch next

- Monitor USDC supply and market cap updates on CoinMarketCap to gauge whether the $79–$80 billion threshold remains a ceiling or becomes a new floor.

- Track Dubai real estate data and related price movements to see if the recent downturn persists or stabilizes, potentially affecting capital allocation choices.

- Observe any shifts in real-world asset adoption for crypto payments, particularly for large-ticket purchases where discounts could incentivize crypto settlement.

- Follow regulatory developments around stablecoins in major jurisdictions, including disclosures, reserve requirements, and cross-border settlement standards.

- Watch on-chain volume trends for USDC versus USDt to confirm whether the broader volume leadership persists and how that translates to liquidity depth across venues.

Sources & verification

- CoinMarketCap — USDC circulating supply and market cap data: https://coinmarketcap.com/currencies/usd-coin/

- Rami Al-Hashimi, X post discussing Dubai OTC demand for stablecoins: https://x.com/rami_hashimi/status/2032440070976819590

- DFM Real Estate Index performance data via TradingView: https://www.tradingview.com/chart/?symbol=DFM%3ADFMREI

- Mizuho analysis on USDC vs USDt adjusted transaction volumes: https://cointelegraph.com/news/circle-usdc-tether-usdt-adjusted-ytd-volume-mizuho

TLDR:

- NEAR approaches a major resistance zone after forming higher lows, suggesting momentum may be shifting toward a potential breakout scenario.

- Market analysts indicate that reclaiming resistance could accelerate price movement toward the $2 region if buying pressure continues building.

- Research projections place long-term NEAR targets between $6 and $18, depending on adoption, tokenomics shifts, and ecosystem growth.

- NEAR breakout momentum is gaining attention as the asset approaches a crucial resistance area following months of downward pressure.

NEAR breakout momentum is gaining attention as the asset approaches a crucial resistance area following months of downward pressure. Market participants are monitoring whether improving structure could trigger the next expansion phase.

NEAR Tests Key Technical Resistance

Recent market activity shows a strengthening price structure for NEAR Protocol after an extended decline. Price movement has gradually shifted toward higher lows. That pattern often appears when selling pressure weakens.

Market data indicates NEAR as of writing trades around $1.34. The asset recorded roughly 3.93% growth in 24 hours. Weekly performance shows a smaller 1.58% increase.

Technical observers note that the price is approaching an important horizontal resistance band. This level previously acted as support before the broader market breakdown. Recovering that area could reshape the current trend.

According to commentary shared by Michaël van de Poppe on X, momentum continues strengthening. The analyst stated that NEAR is attacking a crucial resistance region. He added that a breakout could open the path toward the $2 level.

Market Structure Shows Signs of Reversal

The earlier market structure displayed a prolonged series of lower highs and lower lows. That pattern defined a persistent downtrend during previous months. Several recovery attempts failed to reclaim lost support levels.

More recent trading behavior suggests a different pattern is emerging. The price stabilized after forming a clear base near recent lows. From that point, buyers began producing consistent upward moves.

Short-term moving averages also shifted direction during the recovery phase. The price moved above the indicator after several months of rejection. That development can indicate a transition in market momentum.

Chart annotations further suggest that reclaiming resistance could accelerate price expansion. Traders often interpret such moves as confirmation of a trend shift. Increased participation can follow when those levels break.

Long-Term Projections Draw Attention

Beyond short-term trading signals, broader research reports also discuss future growth scenarios. Commentary referencing analysis from Vini Barbosa discussed projections from SVRN. The report outlines possible valuation ranges through 2026.

The research suggests a base case price between $6 and $10. A more optimistic projection places the token between $12 and $18. Those targets dep`end on adoption and ecosystem expansion.

SVRN’s thesis focuses partly on infrastructure capabilities within the NEAR network. The platform competes among Layer-1 blockchain systems supporting decentralized applications. Developer tools and scalability remain key areas of focus.

The report also references network tokenomics and an inflation reduction decision approved previously. Lower token issuance could gradually tighten the circulating supply. Analysts suggest that reduced inflation may influence long-term valuation trends.

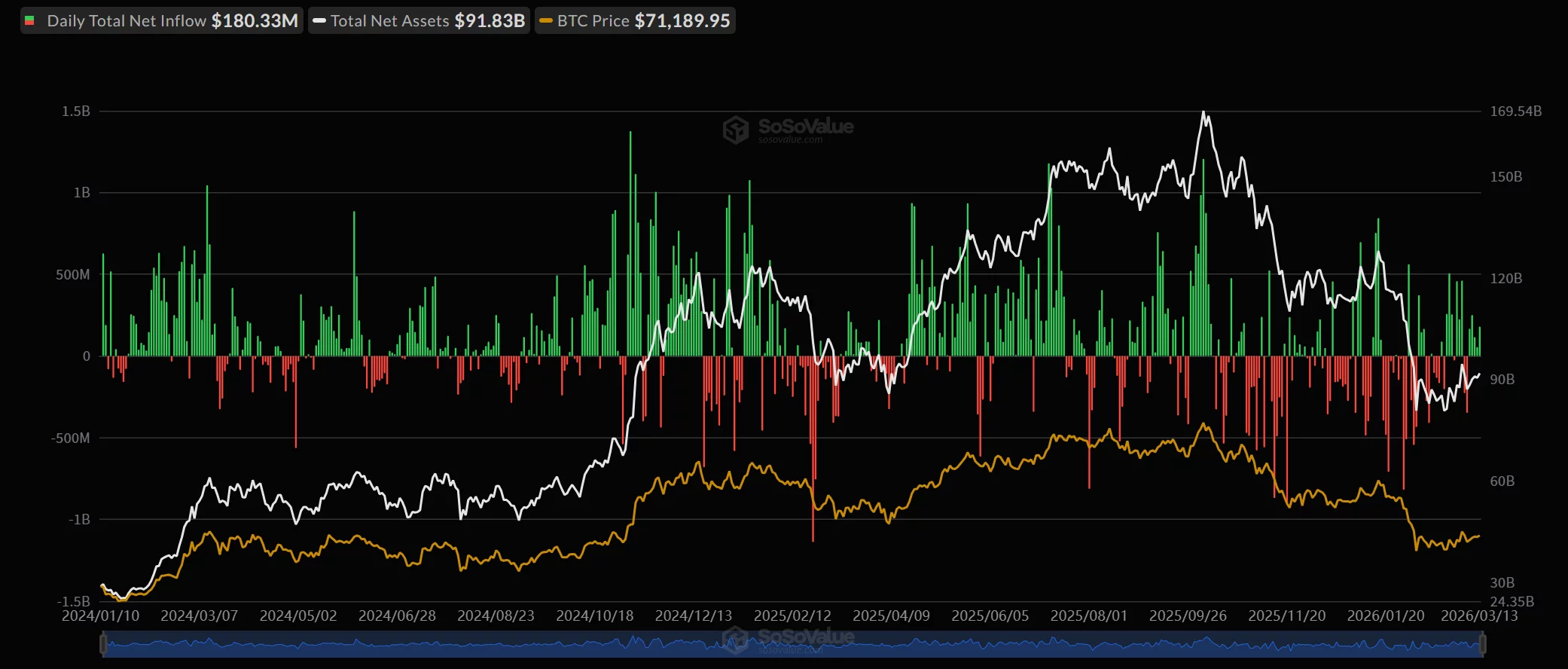

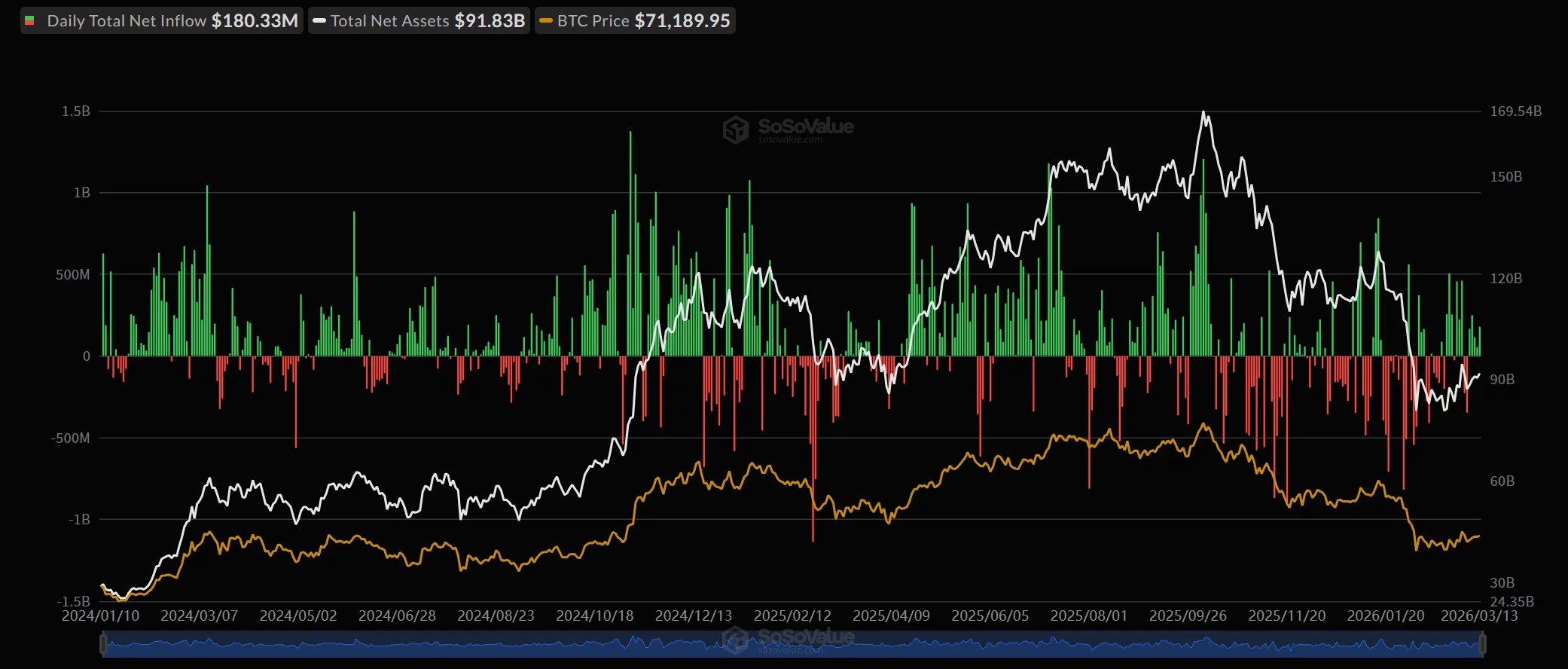

Spot Bitcoin ETFs recorded strong inflows on March 13, adding fresh momentum to institutional demand as market analysts pointed to key resistance and support levels for BTC price. Data shared by Farside Investors shows that U.S. spot Bitcoin ETFs attracted $180.4 million in net inflows on March 13, 2026.

Spot Bitcoin ETFs continue inflow streak

The funds extended a streak of positive flows after several volatile sessions earlier in the month.The largest share of inflows came from BlackRock’s IBIT, which added $143.6 million. Fidelity’s FBTC followed with $23.2 million, while Bitwise’s BITB recorded $3.1 million. ARK Invest’s ARKB posted $2.4 million, and VanEck’s HODL brought in $8.1 million.

Other Bitcoin ETFs reported no daily inflows, including Grayscale’s GBTC, Invesco’s BTCO, and Franklin Templeton’s EZBC. The latest figures from Farside UK reflect a rebound in ETF demand after significant outflows earlier in March. On March 6, spot Bitcoin ETFs collectively recorded $348.9 million in outflows.

The flows later turned positive, with $167.1 million in inflows on March 9 and $246.9 million on March 10, before moderating to $53.8 million on March 12. Since launch, cumulative inflows remain heavily concentrated in a few products. BlackRock’s IBIT has attracted more than $63 billion, while Fidelity’s FBTC has gathered nearly $11 billion, according to the totals displayed in the dataset.

Analysts remain optimistic on BTC price

At the same time, analysts are closely watching Bitcoin’s technical structure. Crypto analyst Ali Martinez said Bitcoin has entered a “low-resistance zone,” suggesting the asset could move higher with relatively limited selling pressure.

“Bitcoin $BTC has entered a low-resistance zone, with little standing in the way until $82,045,” Martinez wrote. He added, “Meanwhile, the key support floor sits at $66,898.”

A chart shared by crypto analyst Michaël van de Poppe shows Bitcoin trading around $71,720 on the 4-hour timeframe after rebounding from earlier March lows. The chart highlights a higher-low structure forming near $65,117, which Poppe described as a support level the market continues to hold.

Above the current price range, the chart marks a potential resistance band between $76,604 and $79,127, while a broader upside target zone sits near $80,646. The technical setup also shows Bitcoin reclaiming a short-term moving average after a series of consolidations.

Poppe described the recent price move as typical end-of-week volatility.“Classic price action on a Friday afternoon on #Bitcoin,” Poppe wrote on X. He noted, “Runs all the way towards the recent high, takes liquidity and inverses.”

Poppe added that he would be watching the next few sessions closely as he expects fresh highs soon. “Would be interested to see how this develops coming days, but would suggest that we’re going to attack the highs again in next two weeks.”

BlackRock digital assets head Robert Mitchnick said Bitcoin and Ethereum remain the only two cryptocurrencies attracting meaningful investor demand.

Summary

- BlackRock says Bitcoin and Ethereum dominate investor demand.

- IBIT saw $26B inflows in 2025 despite Bitcoin’s price decline.

- ETH staking ETF aims to add yield to ether exposure.

This comes as the asset manager evaluates future ETF products. Speaking on CNBC following the launch of BlackRock’s ETHB staked ether ETF, Mitchnick stated Bitcoin commands approximately 60% of crypto market share while Ethereum holds the low teens.

The comments come as BlackRock’s IBIT Bitcoin ETF recorded $26 billion in inflows during 2025 despite Bitcoin falling nearly 50% from its October all-time high.

IBIT ranked fourth globally for ETF inflows last year, becoming the only product in the top 20 to post positive flows while delivering negative price returns.

Year-to-date flows for IBIT remain slightly positive, with approximately 90% of the investor base maintaining steady accumulation patterns through the drawdown.

Bitcoin and Ethereum dominate investor allocation decisions

Mitchnick described Bitcoin as a “digital gold emerging monetary alternative” while calling Ethereum as “a technology centric bet around blockchain innovation and the various use cases of ether and digital assets.”

The distinction decides how investors approach portfolio allocations, with Ethereum exposure aligning more closely with technology and venture equity allocations.

BlackRock’s ETHA became the third-fastest ETF in history to reach $10 billion in assets under management, trailing only IBIT and Fidelity’s FBTC.

The newly launched ETHB adds staking yield to spot ether exposure, addressing what Mitchnick called a “limitation” in original ether ETF products that lacked yield capture mechanisms.

The staking feature makes ETHB “much closer, like the Bitcoin ETPs were, to a silver bullet for a lot of investors in terms of a super convenient exposure vehicle,” Mitchnick said.

Long-term investors drive Bitcoin and Ethereum ETF flows

Retail investors and financial advisors comprise the majority of ETF demand, with both segments showing opportunistic buying during price declines.

Hedge funds account for roughly 10% of flows, primarily running basis trades that go long ETFs while shorting futures contracts. These trades remain neutral for Bitcoin’s price but create flow volatility when basis spreads compress.

Mitchnick noted BlackRock sees “pockets of interest” in other crypto assets but maintains a “discerning approach” to product expansion.

The firm continues evaluating assets as liquidity, scale, and use cases develop, but Bitcoin and Ethereum remain where investor interest concentrates overwhelmingly.

The market capitalization of the USDC stablecoin is approaching a record high near $80 billion as demand surges in the Middle East, with one analyst linking the spike to capital flight from the United Arab Emirates.

According to data from CoinMarketCap, USDC (USDC)’s circulating supply has risen to roughly $79.2 billion, marking a new all-time high for the dollar-pegged stablecoin. The stablecoin’s market cap previously hit a high of below $79 billion in December last year.

The increase comes after supply expanded by billions of dollars in recent weeks. The stablecoin’s market cap stood at just over $70 billion in early February and at $75 billion earlier this month.

Self-proclaimed Dubai-based analyst Rami Al-Hashimi claimed the surge reflects growing demand from investors seeking to move funds out of traditional markets. In a Friday post on X, Al-Hashimi said over-the-counter (OTC) desks in Dubai have struggled to meet demand for the stablecoin.

Related: Stablecoins could form backbone of global payments in 10 years: Billionaire

Dubai property slump may be driving USDC surge

Al-Hashimi tied the surge in stablecoin demand to turmoil in the UAE’s real estate market. The analyst claimed property prices in Dubai have fallen roughly 27% this month, sparking a rush among investors to move capital into digital assets.

“War panic. Capital flight. Sellers are bleeding,” he wrote, describing what he said was a rapid shift in investor behavior.

Data from TradingView also shows that the DFM Real Estate Index, which tracks the performance of listed real estate and construction companies in Dubai, has suffered a sharp sell-off, with the index falling from around 16,800 at its recent peak to about 11,516, a decline of roughly 31%.

Al-Hashimi claimed the situation has also led some property sellers to accept cryptocurrency payments directly. He said certain real estate listings now advertise discounts for buyers who pay using Bitcoin (BTC).

“Pay in BTC, get 5–10% off,” he wrote, adding that the trend reflects growing demand for digital assets during periods of financial uncertainty.

Related: Crypto Biz: Circle stock defies Wall Street and digital asset selloff

USDC overtakes USDt in adjusted transaction volume

Japanese investment bank Mizuho says USDC has surpassed Tether’s USDt (USDT) in adjusted transaction volume for the first time since 2019. According to the bank’s research note, USDC recorded about $2.2 trillion in adjusted transaction volume year-to-date, compared with $1.3 trillion for USDt, giving USDC roughly 64% of combined transaction share.

Despite the shift in activity, USDt remains the largest stablecoin by market capitalization at about $184 billion, far ahead of USDC’s $79 billion.

AI Eye: IronClaw rivals OpenClaw, Olas launches bots for Polymarket

TLDR:

- Bitcoin marked its 2025 cycle top at $126,230 on October 6, starting a 159-day correction phase.

- The 2017 cycle took 1,180 days to reach a new ATH, while 2021 required 1,093 days to recover.

- For the first time ever, Bitcoin reached a new ATH in 2025 without a halving event preceding it.

- Spot Bitcoin ETFs launched in January 2024 disrupted historical halving-driven market cycle patterns.

Bitcoin correction timelines have historically tested investor patience across multiple market cycles. The most recent cycle top was marked on October 6, with Bitcoin reaching approximately $126,230.

Since then, the asset has been in a correction phase spanning 159 days. Market analysts are comparing this period against previous Bitcoin bear markets and recovery timelines.

Historical data shows earlier cycles required far longer before a new all-time high was reached. Long-term investors continue to track these patterns for perspective.

Bitcoin’s 159-Day Correction in Historical Context

The cycle top for Bitcoin was recorded on October 6 at approximately $126,230. Since that date, the correction has extended to 159 days based on current market data.

Many investors view this period as prolonged, though historical comparisons offer a contrasting view. Prior Bitcoin cycles consistently required far longer recovery timelines before reaching new highs.

Crypto analyst Darkfost published comparative data spanning Bitcoin’s most notable market cycles. In the 2017 cycle, it took 1,180 days before Bitcoin achieved a new all-time high.

The 2021 cycle required 1,093 days to reach that same milestone. The current 2025 cycle, by comparison, has so far lasted only 849 days from its peak.

Looking at these numbers, a clear trend toward shorter cycle durations becomes apparent. The time between Bitcoin’s all-time highs has been consistently shrinking across each major cycle.

This pattern points to Bitcoin’s continued maturation as a widely held global financial asset. For long-term holders who accumulate steadily rather than trade short-term moves, this trend is encouraging. It also suggests that Bitcoin’s recovery pace may continue to accelerate in future cycles.

Halvings, ETFs, and Bitcoin’s Long-Term Supply Dynamics

A key observation in the current Bitcoin cycle is the break from the established halving pattern. Historically, a Bitcoin halving had always come before a new all-time high in each prior cycle.

The 2025 cycle broke that precedent for the first time in Bitcoin’s recorded history. This departure has prompted analysts to revisit traditional assumptions around halving-driven market cycles.

Darkfost directly linked this pattern disruption to the launch of spot Bitcoin ETFs in January 2024. These financial products introduced institutional demand that did not follow traditional halving-driven market cycles.

The ETFs altered the timing dynamics that many traders and analysts had previously relied on. As a result, Bitcoin reached a new all-time high without waiting for a halving event to serve as a catalyst.

Despite the disrupted pattern, the halving continues to play a role in Bitcoin’s broader supply picture. Each halving reduces the rate of new Bitcoin issuance, gradually cutting the selling pressure from miners.

Over extended periods, this steady reduction in supply decreases Bitcoin’s overall inflation rate. This mechanism remains a structural support for Bitcoin’s long-term price performance, independent of short-term cycle behavior.

A US federal appeals court has rejected Custodia Bank’s final attempt to challenge the Federal Reserve’s authority over granting master accounts, bringing an end to the crypto-focused bank’s five-year legal fight for direct access to the central bank’s payment infrastructure.

Key Takeaways:

- A US appeals court refused to hear Custodia Bank’s final appeal, ending its five-year fight for a Federal Reserve master account.

- Courts ruled the Federal Reserve has discretion to decide which institutions can access its payment system.

- The case comes as more fintech and crypto firms pursue US bank charters and direct access to the banking system.

The US Court of Appeals for the Tenth Circuit said in a filing on Friday that it would not hear Custodia’s final appeal in a 7–3 vote, effectively closing the case and reinforcing the Federal Reserve’s discretion over who can access its banking services.

Custodia Argued Fed Must Grant Master Account to State-Chartered Banks

Custodia first applied for a Federal Reserve master account in October 2020.

Such accounts allow financial institutions to hold reserves directly at the central bank and connect to its payment rails, enabling banks to settle transactions without relying on intermediary institutions.

After its application was denied, Custodia took the dispute to court, arguing that the Monetary Control Act requires the Fed to provide services to state-chartered banks and therefore entitles it to a master account.

The bank maintained that access to the central bank’s payment system was critical to its operations as a digital asset-focused institution.

However, courts reviewing the case repeatedly sided with the Federal Reserve, concluding that the central bank retains discretion when deciding whether to grant master accounts.

denial of @custodiabank’s fed membership & master account on concerns of “safety and soundness” looks a bit absurd right now

custodia was to be a non-lending fully reserved depository with its cash in a fed account. no asset-liability mismatch, no duration risk@CaitlinLong_

— Alex Thorn (@intangiblecoins) March 10, 2023

The decision arrives shortly after crypto exchange Kraken secured a limited form of direct access to the Federal Reserve system.

On March 4, Kraken became the first crypto platform to obtain a master account from the Federal Reserve Bank of Kansas City.

Kraken’s account allows the firm to connect to the Fedwire payments network, though it does not grant the full suite of services typically available to traditional banks.

The development sparked speculation that US regulators might consider issuing “skinny” or restricted master accounts to crypto firms seeking closer integration with the banking system.

Despite the ruling against Custodia, one judge offered a forceful dissent. Judge Timothy Tymkovich argued that access to a master account is “indispensable” for banks and said denying one is “akin to a death sentence.”

Tymkovich noted that shortly after Custodia submitted its application in 2020, the Federal Reserve initially indicated that the proposal had “no showstoppers.”

He added that he disagreed with the majority’s view that reserve banks have broad discretion over such applications.

Revolut Files Second Bid for US Bank Charter to Expand Nationwide

Fintech company Revolut has filed a new application for a US national bank charter, marking its second attempt to obtain a banking license in the country.

The London-based firm submitted the application to the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corporation (FDIC) to establish “Revolut Bank US, N.A.”

If approved, the charter would allow Revolut to operate under a single federal regulatory framework across all 50 US states.

Revolut’s move comes as more fintech and crypto firms seek US bank charters through the OCC.

Recent applicants for national bank charters include Nubank, Crypto.com, Circle, Ripple, BitGo, Fidelity Digital Assets and Paxos, signaling growing interest among fintech and digital asset firms in gaining direct access to the US banking system.

The post Custodia Bank Loses Final Court Appeal Over Federal Reserve Master Account appeared first on Cryptonews.

Horror as two decapitated human heads found near Sinaloa bank just hours apart

Goldman warns S&P 500 could decline to 6300 if growth weakens

Sebastian Bach Issues Apology For Christina Applegate And Brad Pitt Drama

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Crypto Gold Live Trading| 13 MARCH #vinbullindia #livetrading #vinbulllive #live #trading

XRP: SOMETHING CRAZY IS HAPPENING | REVERSE CARRY TRADE & PARABOLIC OIL

Monetary and Financial Economics Now available on App. Micro and Macro notes are also available.

-

Tech3 days ago

Tech3 days agoA 1,300-Pound NASA Spacecraft To Re-Enter Earth’s Atmosphere

-

News Videos5 days ago

News Videos5 days ago10th Algebra | Financial Planning | Question Bank Solution | Board Exam 2026

-

Crypto World5 days ago

Crypto World5 days agoParadigm, a16z, Winklevoss Capital, Balaji Srinivasan among investors in ZODL

-

Business4 days ago

Business4 days agoExxonMobil seeks to move corporate registration from New Jersey to Texas

-

Crypto World9 hours ago

HYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

Fashion19 hours ago

Fashion19 hours agoWeekend Open Thread: Addict Lip Glow

-

Tech4 days ago

Tech4 days agoChatGPT will now generate interactive visuals to help you with math and science concepts

-

Sports7 days ago

Sports7 days agoThree share 2-shot lead entering final round in Hong Kong

-

Sports6 days ago

Sports6 days agoBraveheart Lakshya downs Lai in epic battle to enter All England Open final | Other Sports News

-

NewsBeat3 days ago

NewsBeat3 days agoResidents reaction as Shildon murder probe enters second day

-

Business6 days ago

Business6 days agoSearch for Nancy Guthrie Enters 37th Day as FBI Probes Wi-Fi Jammer Theory

-

Business3 days ago

Business3 days agoSearch Enters Sixth Week With New Leads in Tucson Abduction Case

-

NewsBeat5 days ago

NewsBeat5 days agoPagazzi Lighting enters administration as 70 jobs lost and 11 stores close across Scotland

-

Tech5 days ago

Tech5 days agoDespite challenges, Ireland sixth in EU for board gender diversity

-

Business5 days ago

Business5 days agoSearch Enters 39th Day with FBI Tip Line Developments and No Major Breakthroughs

-

NewsBeat3 days ago

NewsBeat3 days agoI Entered The Manosphere. Nothing Could Prepare Me For What I Found.

-

Sports5 days ago

Sports5 days agoSkateboarding World Championships: Britain’s Sky Brown wins park gold

-

Crypto World4 days ago

Crypto World4 days agoWill Chainlink price reclaim $10 amid volatility squeeze?

-

Business48 minutes ago

Business48 minutes agoCountry star Brantley Gilbert enters growing non-alcoholic beer market

-

Sports3 days ago

Sports3 days agoPWHL, Senators discussing plan to keep Charge in Ottawa