Crypto World

US Job Market Flashes Warning Signs Last Seen During 2020 Pandemic

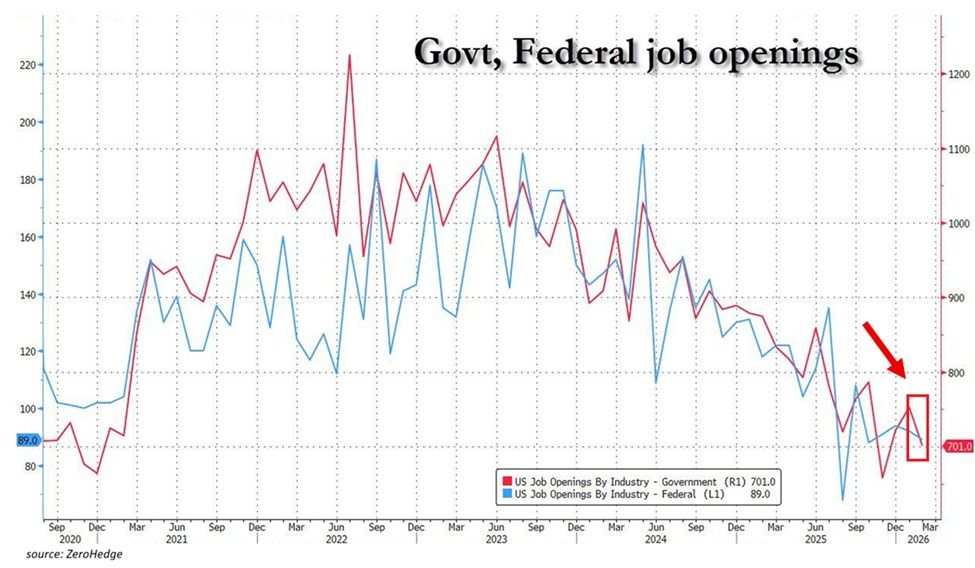

The US job market is showing alarming deterioration. According to The Kobeissi Letter, government job openings dropped 51,000 in February to 701,000.

This marked the second-lowest reading since December 2020. Available government vacancies have fallen 524,000 since their 2022 peak and now sit at pre-pandemic levels.

In addition, federal government openings fell to 89,000, the second-lowest since the pandemic low. This level is also in line with readings from 2017 and 2018.

Follow us on X to get the latest news as it happens

“Meanwhile, the government hiring rate stood at 1.4%, one of the lowest levels since mid-2020 and matching the 2016 and 2017 lows. Government hiring is frozen,” the post read.

Meanwhile, the private sector is shedding jobs at scale. Oracle reportedly laid off up to 30,000 employees on March 31. Amazon cut 16,000 corporate roles in January, and Block eliminated over 4,000 positions. These were just some of the many companies that made job cuts.

Consumer Sentiment Signals Trouble Ahead

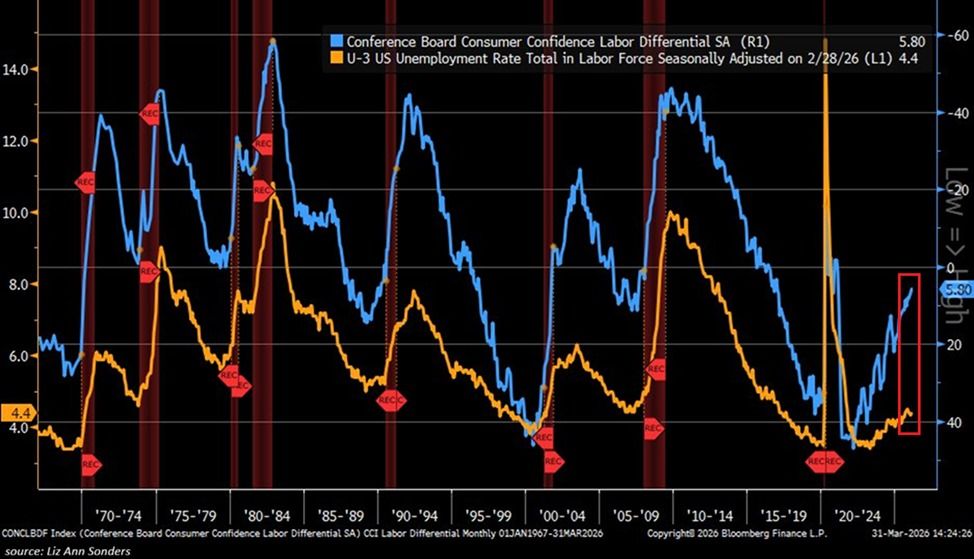

In a separate post, The Kobeissi Letter suggested that forward-looking indicators” point to a further increase in US unemployment.” The Conference Board’s March survey showed that only 27.3% of consumers described jobs as “plentiful.”

This was a marginal uptick from 26.7% in February, but still well below the roughly 55% who felt that way in 2022. At the same time, 21.5% said jobs were “hard to find,” up from approximately 10% over the same period.

The gap between these two readings, known as the labor market differential, fell to just 5.8 points. That represents the lowest level since the 2020 pandemic.

The Kobeissi Letter noted that historically, this indicator has been one of the most reliable leading signals of rising unemployment.

“Furthermore, current levels in this indicator have only been seen prior to or during a US recession since the 1990s. The job market is set for even more weakness,” the analysts added.

With these indicators pointing in the same direction, the March jobs report will be closely watched to determine whether underlying deterioration is cyclical or marks a deeper shift.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post US Job Market Flashes Warning Signs Last Seen During 2020 Pandemic appeared first on BeInCrypto.

Japanese and South Korean equities advanced on Friday after a late rebound on Wall Street, as traders bet that tensions in the Iran war may be edging closer to a managed outcome.

Summary

- Nikkei 225 and Kospi rose 1.4% and 2.7% respectively after a late rebound in US stocks on hopes of easing tensions in the Iran war.

- Oil prices stayed elevated above $110 despite easing from highs, as fresh US strikes on Iranian infrastructure intensified geopolitical risks.

- Crypto equities were mixed, with mining stocks gaining while Coinbase, Robinhood, and Strategy shares declined.

Japan’s Nikkei 225 rose 1.4%, while South Korea’s Kospi climbed 2.7%, following a turnaround in the S&P 500, which erased a 1.5% intraday loss to finish 0.1% higher. The shift in sentiment came as oil prices pulled back from recent highs after reports that Iran is working with Oman on a protocol to monitor shipping through the Strait of Hormuz, which has remained effectively shut since the conflict began.

Currency markets reflected the improving tone, with the US dollar weakening against major peers as demand for safe-haven assets eased. Treasury futures in Asia traded largely flat, with the US cash market set to reopen later for a shortened trading session.

Several Asia-Pacific markets, including Australia, New Zealand, Hong Kong, Singapore, the Philippines, and Indonesia, remained closed for the Good Friday holiday. US equities will also be shut, though key economic releases, including the March nonfarm payrolls report, are still due.

Risk sentiment weakened earlier in the week after remarks from US President Donald Trump did little to ease concerns about a near-term resolution to the conflict. Although he had previously outlined a two-to-three-week timeline, Trump signaled that military operations would continue and warned of “extremely aggressive” action.

Subsequent strikes on Iranian infrastructure, including a century-old medical research centre in Tehran, steel facilities, and a bridge near the capital, have drawn criticism. Iranian officials and several analysts argue that these targets qualify as civilian infrastructure, raising concerns about further escalation and humanitarian consequences.

Oil markets reacted sharply to the heightened rhetoric. Prices surged above $110 per barrel on Thursday, with West Texas Intermediate jumping around 12% to $112 and Brent settling near $109. Europe’s diesel benchmark climbed past $200 per barrel for the first time since 2022, underscoring supply fears tied to disruptions in the Strait of Hormuz.

Despite the volatility in energy markets, traditional safe-haven assets such as gold showed limited movement on Friday, indicating a cautious, wait-and-watch stance among investors as the geopolitical situation remains fluid.

Crypto-linked equities delivered a mixed performance amid the escalating war in the Middle East. Coinbase shares fell 0.9% at the end of Thursday, while Robinhood declined 1.73%. Galaxy Digital bucked the trend, gaining 1.5% by the close.

Crypto mining stocks saw much better gains. Notably, Marathon Digital rose 8.3%, while Riot Platforms, Hut 8 Mining, and Bitfarms were up by 2.47%, 1.5%, and over 1%, respectively.

However, accumulation-focused firms did not follow the same trend. Strategy, the Bitcoin-focused treasury company led by Michael Saylor, dropped 2.4%, while Bitmine Immersion Technologies (BNMR) fell 1.2%.

The divergence suggests investors favoured mining firms, which tend to track Bitcoin price movements more closely, amid ongoing geopolitical uncertainty.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

A small group of collections has moved beyond crypto-native speculation and into consumer-facing brands. Pudgy Penguins has continued to present itself as a broader IP business, with recent CoinDesk Research describing more than $13 million in retail sales and over 2 million units sold, while Doodles now frames itself less as a pure collection and more as a creative platform built around content, AI, and brand expansion.

Indeed, the NFT sector has become more selective, with utility-led and gaming-linked activity holding up better than the broad speculative frenzy that defined the earlier cycle.

While a handful of projects are trying to build durable intellectual property, the long tail of profile-picture collections continues to fade.

BeInCrypto asked three industry experts how the NFT market is restructuring, and what will determine which projects survive.

Brand Equity vs. On-Chain Scarcity

The divide now sits at the center of the NFT market’s recovery: whether value can be sustained through real-world brand equity, or whether it still depends on on-chain scarcity.

Federico Variola, CEO of Phemex, is skeptical that most projects can successfully make that transition.

“There are still some difficulties in tying the value of NFTs to brand equity in the physical world when there isn’t a clear revenue or distribution funnel.”

In his view, the core issue is that many NFT brands have yet to prove they generate meaningful business outcomes outside of crypto.

“Because of that, I think the real value of NFTs has always been rooted in on-chain scarcity.”

As market sentiment around scarcity weakened, projects began searching for alternative narratives, from media expansion to merchandise, but often without a clear product-market fit.

“As a result, many of these brands are now stuck trying to pivot from on-chain scarcity toward real-world positioning without having a product-market fit.”

That helps explain why a large share of collections remain significantly below their peak valuations.

Fernando Lillo Aranda, Marketing Director at Zoomex, takes the opposite view. For him, the market has already moved past scarcity as a primary driver of value.

“Most NFTs won’t recover – and they probably shouldn’t. Scarcity alone was never a sustainable value proposition.”

He argues that verification on-chain does not create demand on its own.

“The market learned the hard way that being ‘on-chain’ doesn’t make something valuable – it just makes it verifiable. And verification without demand is irrelevant.”

Instead, he sees the surviving projects as those building real businesses around their IP.

“The only NFTs that have a real future are the ones evolving into actual businesses and IP engines.”

“If your project can’t live outside of crypto, in retail, media, gaming, or culture, then it’s not an asset, it’s a speculation artifact from the last cycle.”

The disagreement relates to execution. The move toward IP-driven value is already underway.

The open question is how many NFT projects can operate as real businesses rather than speculative assets.

Gaming’s Reset: From Play-to-Earn to Play-to-Own

The failure of early NFT gaming models made the speculation versus sustainability debate impossible to ignore.

Play-to-Earn was built to reward users with tokens for activity. In practice, it depended on constant inflows of new players to support token prices. Once growth slowed, the model began to break down. Rewards turned into emissions, emissions turned into sell pressure, and in-game economies collapsed under their own weight.

The recent migration is toward what many describe as Play-to-Own – a model that treats NFTs less as yield-generating assets and more as ownership layers within a game.

Anton Efimenko, co-founder at 8Blocks, sees this as a necessary correction in how value is structured.

“The core issue with Play-to-Earn was that it tried to financialize gameplay too early. When rewards are driven by token emissions rather than real demand, the system becomes inherently unstable.”

Instead of promising returns, newer models focus on utility and persistence. Assets are meant to retain relevance inside the game environment, rather than function as extractive instruments.

“Play-to-Own shifts the focus from extracting value to owning something that has utility within a functioning ecosystem. That reduces sell pressure and aligns players more closely with the long-term health of the game.”

This does not eliminate speculation, but it changes where it sits. Value is no longer tied to how quickly rewards can be realized, but to whether the underlying game can sustain engagement without relying on constant token incentives.

Gaming has become one of the clearest testing grounds for this transition. If NFT-based ownership can hold value without emissions-driven rewards, it may offer a path forward. If not, the same issues are likely to resurface under a different name.

Tokenizing IP: Liquidity vs. Loyalty

As projects search for new ways to unlock value, one emerging direction is the tokenization of NFT IP itself.

In theory, that can broaden access, increase liquidity, and give communities a more direct stake in the commercial upside of a brand. But it also raises harder questions about governance, alignment, and loyalty.

Efimenko says the structure can create opportunities, but it also changes the incentives around ownership.

“The moment NFT IP becomes more liquid, you invite a different class of participant. Some will care about the brand, but many will care mainly about price exposure and short-term upside.”

Of course, communities built around identity and culture do not function like ordinary token markets. The more tradable the asset becomes, the more likely decision-making is to shift toward actors with weaker long-term attachment to the project.

“Liquidity can help expand participation, but it can also fragment governance. If too much influence moves to holders who are financially motivated but not operationally aligned, brand direction becomes harder to manage.”

This leaves NFT projects in a difficult position. Broader financial access may strengthen the balance sheet, but it can also dilute the kind of committed holder base that many successful brands rely on.

Ultimately, a highly liquid community asset may be easier to trade, yet harder to build around over time.

Fixing Crypto-Native Gaming

Our analysis so far leaves one more question hanging: whether blockchain mechanics can restore trust in crypto-native gaming and gambling after years of broken incentives, opaque systems, and user fatigue.

This is potentially where blockchain still offers a real advantage. Game logic, reward flows, and outcomes can be made transparent in ways that traditional platforms often cannot match. Provably fair mechanics give users a way to verify that systems are functioning as claimed, rather than simply trusting the operator.

But transparency alone is not enough to rebuild confidence.

As Lillo Aranda puts it:

“The market learned the hard way that being ‘on-chain’ doesn’t make something valuable – it just makes it verifiable. And verification without demand is irrelevant.”

The same logic applies to gaming. Verifiable mechanics can help solve the trust problem, especially in areas like crypto gambling or reward distribution, but they do not solve the product problem. If the game is weak, the economy is extractive, or the user experience feels designed around monetization rather than entertainment, transparency will not save it.

The sector’s next phase may well be a test of whether crypto products can combine fair mechanics with actual player retention. In that sense, blockchain may help restore trust, but only if the game itself is worth trusting.

Final Thoughts

The NFT market is being forced into a more selective phase, where value has to come from something more durable than hype alone.

Variola’s comments point to the limits of the current pivot. Many projects are trying to move from scarcity-led speculation into real-world branding without a clear business model or product-market fit.

Lillo Aranda furthers the argument, suggesting that only the collections capable of operating as actual IP businesses are likely to retain relevance over time.

Efimenko, meanwhile, highlights the challenge underneath both views: ownership design, token incentives, and governance all shape whether a project can remain stable as it grows.

NFTs are not disappearing, but they are becoming harder to justify as pure collectibles. The projects that endure are more likely to be the ones that can build beyond the chain, sustain user demand, and give digital ownership a function that lasts longer than a speculative cycle.

The post NFTs After the Hype: IP, Utility and the Fight to Stay Relevant appeared first on BeInCrypto.

Crypto World

Circle’s cirBTC Takes Aim at Coinbase’s $6 Billion cbBTC Months Before Key Deal Renewal

Circle announced cirBTC on April 2, 2026, a wrapped Bitcoin (BTC) token backed 1:1 by native BTC with real-time onchain reserve verification, marking the firm’s first expansion beyond stablecoins into tokenized BTC infrastructure.

The announcement puts Circle in direct competition with its largest distribution partner at a commercially sensitive moment.

A Trust Problem Worth $1.7 Trillion

Circle, the issuer of USDC stablecoin, frames cirBTC as a neutral, institution-grade alternative to existing wrapped BTC products. It is built on the same compliance and issuance foundations that support USDC and EURC.

“Bitcoin is sitting on the sidelines of DeFi. Not because people don’t want yield or liquidity — it’s because they don’t trust the wrapper,” said Circle VP of Product Rachel Mayer, identifying the core market thesis behind cirBTC.

The wrapped BTC sector has faced sustained credibility issues. In August 2024, BitGo’s Wrapped Bitcoin (WBTC) drew criticism after its custodian partnered with BiT Global, a firm linked to Tron founder Justin Sun.

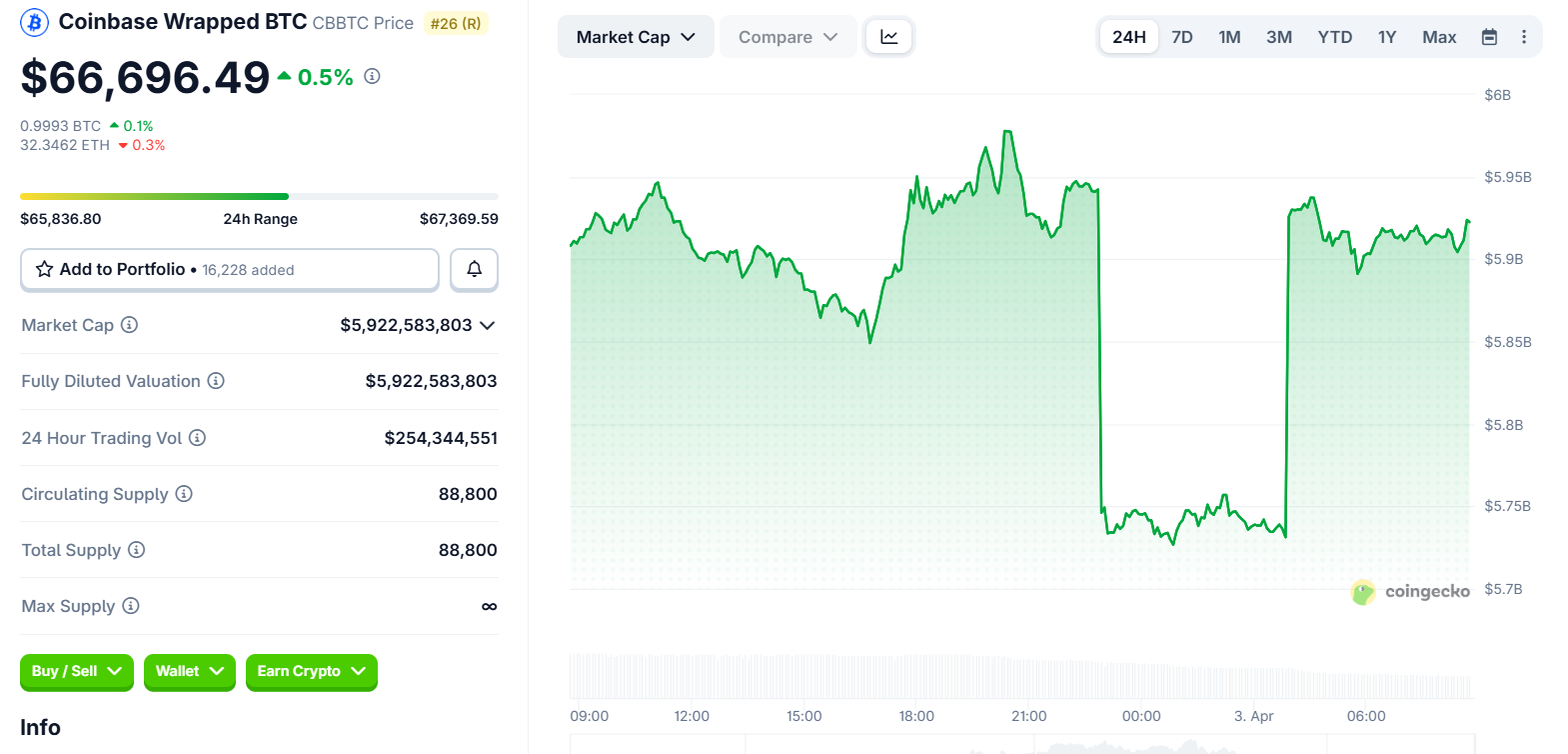

Coinbase launched cbBTC (Coinbase Wrapped BTC) shortly after, and currently holds roughly $6 billion in circulating supply according to CoinGecko data.

Circle is positioning cirBTC as a more transparent option. Reserves will be independently verifiable onchain in real time, with no reliance on third-party attestations.

The token launches first on Ethereum and Arc, Circle’s Layer-1 blockchain, with multichain support planned. Target users include OTC desks, market makers, lending protocols, and derivatives platforms.

Partnership Tension Ahead of August Renewal

The timing carries weight beyond product competition. Circle and Coinbase operate under a revenue-sharing agreement tied to USDC reserve income, up for renewal in August 2026.

Under the current deal, Coinbase receives 100% of interest on USDC held on its platform and a 50/50 split on off-platform holdings.

Analysts estimate that Coinbase collects over $900 million annually from this arrangement.

Crypto analyst Omar flagged the competitive signal directly, noting that Circle targeting cbBTC “feels like a direct shot” at Coinbase ahead of that renewal.

Circle CEO Jeremy Allaire described cirBTC as infrastructure rather than rivalry, saying the product extends the same foundations supporting USDC to “the largest digital asset.”

“cirBTC is coming. We are bringing the same infra that supports USDC, EURC, and USYC to the largest digital asset, creating a neutral infrastructure for new applications for onchain BTC,” wrote Allaire.

Still, no launch date has been confirmed, and the product page notes that availability depends on regulatory approvals.

Whether cirBTC gains institutional traction before cbBTC further entrenches its $6 billion lead may shape how much leverage Circle holds when the two companies return to the negotiating table in August.

The post Circle’s cirBTC Takes Aim at Coinbase’s $6 Billion cbBTC Months Before Key Deal Renewal appeared first on BeInCrypto.

The price that underpins real-world oil cargo transactions surged to its highest level since 2008. Dated Brent hit $141.37 per barrel, reaching an 18-year high.

Meanwhile, Brent crude futures traded near $107, still below 2022 levels. Thus, it’s clear that the benchmark for actual crude cargoes now trades more than $34 above Brent futures.

“The last time Dated Brent touched such heights was 18 years ago, when the global financial crisis that had been brewing for months was on the cusp of puncturing a historic crude rally,” Bloomberg wrote. “The surge is a sign of the growing disconnect between futures contracts and various pockets of physical markets that are pricing increasingly scarce supplies.”

This isn’t just a price difference. It’s a stress signal. The physical oil market is under acute strain, with immediate demand far outpacing available supply.

Follow us on X to get the latest news as it happens

Recently, Chevron CEO Mike Wirth warned that futures are not reflecting the true scale of the oil supply disruption. He stated that the market is trading on “scant information” and “perception.” According to him,

“There are very real, physical manifestations of the closure of the Strait of Hormuz that are working their way around the world and through the system that I don’t think are fully priced into the futures curves on oil.”

Energy Aspects founder Amrita Sen also told CNBC that the futures market is obscuring the real stress.

“You are seeing it, but the financial market is almost masking the true tightness that everywhere else is showing up,” Sen remarked.

Trump’s Shifting Stance Deepens Uncertainty

The Strait of Hormuz, which handles roughly one-fifth of global crude flows, has been closed for over a month. Gulf producers have cut output by at least 10 million barrels per day, as tanker traffic has dropped by 95%.

President Trump has sent conflicting messages on the Strait. In a prime-time address on April 2, he declared Iran “essentially decimated” and said the waterway would reopen “naturally” once the conflict ends.

Meanwhile, he told other nations they should “grab it and cherish it.” However, his shifting timelines and statements have layered uncertainity onto an already fractured supply picture.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Paper vs. Physical: The $34 Gap Exposing the True Cost of the Iran Oil Shock appeared first on BeInCrypto.

The International Monetary Fund has highlighted both the promise and the peril of tokenization in finance. In a 23-page assessment released this week, the IMF said tokenization could reduce friction and increase transparency across issuance, trading, settlement and asset management. Yet it warned that the same technology could also introduce risks that might affect financial stability, especially as speed and automation enable rapid, automated flows that leave less room for traditional oversight.

The IMF’s analysis stresses that while atomic settlement and enhanced visibility can mitigate some longstanding dangers, the accelerated pace of tokenized markets could give rise to new systemic stress if controls aren’t aligned with legal and supervisory clarity. A central finding remains: “The net effect of tokenization on financial stability is uncertain,” the IMF wrote, underscoring the delicate balance between improved efficiency and new risk vectors.

Key takeaways

- Tokenization reduces some traditional risks through faster settlement and greater transparency, but speed and automation introduce new financial-stability challenges.

- On-chain tokenization of real-world assets has surpassed $27.6 billion, excluding stablecoins, according to RWA.xyz data, highlighting growing industry activity.

- Long-run forecasts for the tokenization market vary widely—BCG in 2022 projected up to $16 trillion by 2030, while McKinsey in 2024 offered a more conservative $2 trillion—the gap reflecting differing assumptions about liquidity, regulation and adoption.

- Legal clarity over ownership records and settlement finality remains a bottleneck; the IMF notes fragmented markets could hamper widespread use unless governance keeps pace with technology.

The economic arc of tokenized real-world assets

The IMF’s report acknowledges that tokenization expands how securities and other financial products are issued, traded, settled and managed. But it also cautions that the technology effectively shifts some systemic risk from traditional banking rails to shared ledgers and smart contract code. In a phrase that captures the urgency for policymakers, the IMF warned that “stress events in tokenized markets are likely to unfold faster than in traditional systems, leaving less time for discretionary intervention.”

On the demand side, tokenization is being seen as a means to accelerate cross-border payments, broaden financial inclusion and unlock new channels for capital flow in emerging markets. Yet, the IMF also flags potential downsides: greater volatility in capital moves, rapid currency substitution and a perceived erosion of monetary sovereignty if participants rely on programmable money without adequate supervisory guardrails.

While the IMF is cautious, market participants are moving ahead. Real-world asset (RWA) tokenization has already drawn substantial traction. As of early April, data from RWA.xyz show more than $27.6 billion of real-world assets tokenized on-chain, excluding stablecoins. The scale of this segment points to a broader appetite among institutions to digitize assets like receivables, property interests and other non-tokenized holdings.

In the broader market outlook, the debate centers on scalability and liquidity. Industry studies have delivered mixed signals about the ultimate size of the opportunity. Boston Consulting Group estimated in 2022 that the tokenization market could swell to as much as $16 trillion by 2030, while McKinsey & Co. offered a notably more cautious projection of around $2 trillion for the same horizon. The IMF’s assessment sits between these bounds, emphasizing potential but underscoring the need for robust risk management as the ecosystem grows.

Industry momentum and notable players

Interest from Wall Street has been a key driver. High-profile figures such as BlackRock CEO Larry Fink have signaled support for tokenizing a broad spectrum of assets—from equities and bonds to money market funds and real estate—marking a shift in institutional attitudes toward on-chain representations of traditional instruments.

Within the on-chain asset category, Securitize has emerged as a leading platform by total value locked (TVL) in real-world asset tokenization. Securitize powers the BlackRock USD Institutional Digital Liquidity Fund, a major RWA project with reported TVL around $3.38 billion, per CryptoDep’s April data. Closely following are Tether Gold and Ondo Finance, with roughly $3.35 billion and $3.21 billion in TVL, respectively, underscoring a crowded field of tokenized wealth vehicles aimed at institutional investors.

Beyond tokenized assets themselves, the traditional exchanges are signaling their intent to bring tokenization into mainstream trading and settlement. Intercontinental Exchange, the parent company of the New York Stock Exchange, announced in January that it would launch a tokenization platform designed for 24/7 trading and instant settlement of stocks and exchange-traded funds via a blockchain-based post-trade system. The move indicates a direction where tokenized securities could become an integrated, continuous-source of liquidity rather than a niche, off-hours exercise.

Standards, regulation and practical controls

One of the IMF’s pointed critiques centers on legal and regulatory clarity. Without well-defined ownership records and settlement finality, tokenized markets risk becoming fragmented and peripheral to the broader financial system. In response, the industry has begun embracing standards and access controls to align technology with regulatory expectations.

Among the notable technical developments is the Ethereum ecosystem’s ERC-3643 standard, which enables permissioned access to tokenized assets and imposes identity and eligibility checks for holders. In practice, this standard is already being applied by some tokenized products to ensure compliance with investor requirements. A concrete example cited in the industry press is Coinbase Asset Management’s tokenized shares for the Coinbase Bitcoin Yield Fund, issued on the Base network (an Ethereum Layer 2). The fund leverages ERC-3643 to verify holder identity and eligibility during tokenization and post-trade processes.

The IMF also points to the broader regulatory architecture around stablecoins, cross-border flows and monetary sovereignty as areas that require ongoing attention as tokenized markets scale. The balance between enabling innovation and preserving monetary policy effectiveness will be a central theme for policymakers over the coming years.

What to watch next

As tokenization marches from pilot projects to greater market participation, investors and builders will be watching several key dynamics. First, whether legal frameworks and settlement finality standards crystallize in a way that reduces fragmentation and reassures traditional market participants. Second, whether liquidity continues to grow in real‑world asset tokens to the point where they rival or surpass traditional offline channels. Third, which infrastructure—clearing, custody, identity verification, and cross-border rails—will emerge as the de facto backbone for scalable tokenized markets. And finally, whether central banks and regulators adopt a calibrated stance that supports innovation without sacrificing financial stability.

In the near term, a handful of large players and platforms—creators of RWA markets, major asset managers experimenting with tokenized funds, and exchange operators expanding tokenized trading—will likely shape the pace and direction of adoption. The IMF’s findings suggest this is not a one-off tech experiment but a continental shift in how assets are created, traded and settled—one that demands careful risk governance as the ecosystem matures.

Readers should monitor developments around legal clarifications for tokenized ownership, concrete liquidity metrics for tokenized assets, and the progression of compliant standards like ERC-3643 as the market seeks a balance between efficiency and resilience.

Polymarket has partnered with oracle provider Pyth Network to launch traditional asset markets on its platform.

Summary

- Polymarket partnered with Pyth Network to introduce equity, commodity, and stock-linked contracts.

- The new markets include daily up or down and closing price contracts that reset at the end of each trading session.

- Pyth Network is providing real-time price feeds from trading firms and market makers to serve as the resolution layer for the new contracts.

According to an Apr. 2 announcement, the latest addition brings daily up-or-down and closing price contracts for major equity indexes, alongside commodities such as gold and oil, and US-listed stocks. Outcomes on these contracts are determined using Pyth’s real-time price feeds, and the markets reset at the end of each trading session.

Pyth Network will act as the resolution layer for these markets, replacing manual or exchange-specific references with a standardized data source aggregated from trading firms and market makers.

Simultaneously, Pyth has launched a data interface called Pyth Terminal, allowing users to track live price feeds and the reference values used to settle markets on Polymarket.

Oracle networks like Pyth bring off-chain data such as prices, foreign exchange rates, and commodities onto blockchains. These feeds are widely used across decentralized finance, prediction markets, and tokenized asset platforms, and have seen growing adoption, including by US government agencies.

PYTH price rallied over 70% after the announcement, while its market capitalization moved past $1 billion.

The latest products on Polymarket were launched as the platform continues to cement its position as a leading prediction market operator.

Last month, the project secured a $600 million investment from Intercontinental Exchange, the parent company of the New York Stock Exchange, as part of a broader multibillion-dollar commitment.

Meanwhile, Polymarket made investments of its own by acquiring DeFi infrastructure startup Brahma for an undisclosed sum.

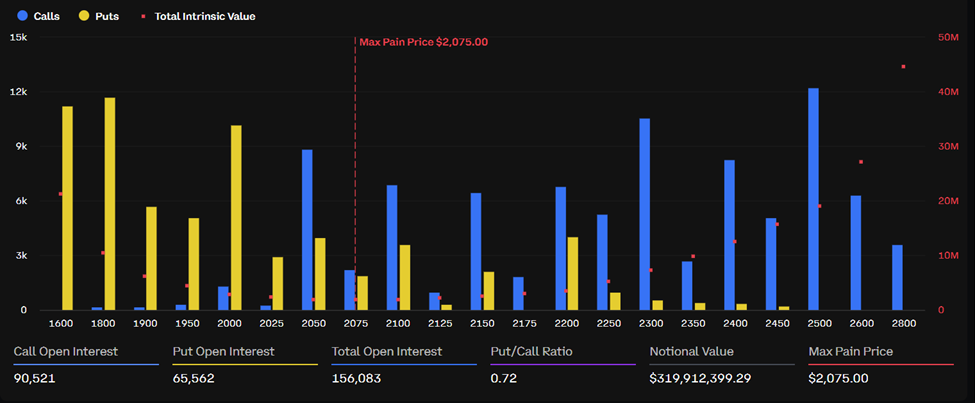

A whale accumulated more than 2,000 Bitcoin (BTC) put contracts overnight, targeting a move below $66,000, just as over $2.15 billion in Bitcoin and Ethereum (ETH) options settle on Deribit today, April 3.

The back-to-back repositioning signals that at least one large player sees downside risk in BTC’s current price range, even as call open interest still outnumbers puts across both assets.

Why the Whale Trade Matters

Options analytics platform Greeks.live flagged the position shift on April 2, noting the same whale had closed a profitable long trade hours earlier before pivoting bearish.

Per the analysts, the whale entered a long position at $66,000 and exited above $68,000, booking a confirmed profit.

Within hours, a trader of comparable size began accumulating put contracts, this time betting on a move lower.

The rapid reversal is notable. A whale exiting a winning trade and immediately loading the opposite direction suggests a view that the $66,000–$68,000 zone is a resistance ceiling, not a launchpad.

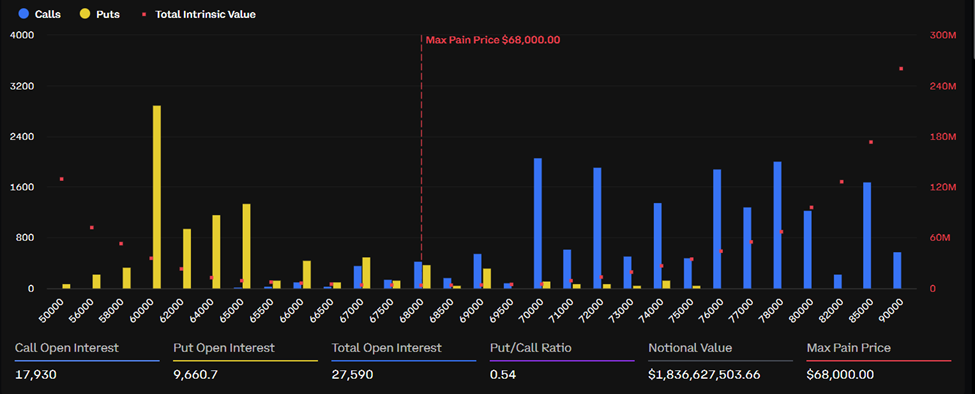

With BTC trading at $66,575 and its max pain level set at $68,000, the spot price sits $1,425 below the level where options sellers profit most. If BTC fails to close that gap before settlement at 08:00 UTC, the bearish whale’s puts gain value.

The Expiry Data

Bitcoin accounts for $1.84 billion of today’s total notional value, with 27,590 contracts outstanding. Call open interest stands at 17,930 against 9,600 puts, giving a put-to-call ratio of 0.54.

The call skew still leans bullish in aggregate, but the whale’s 2,000-contract put position adds concentrated downside weight near the $66,000 strike.

Ethereum’s expiry is smaller but similarly structured. With $319.9 million in notional value and 156,083 total contracts, ETH trades at $2,052 against a max pain level of $2,075. Its put-to-call ratio of 0.72 points to heavier downside hedging than BTC’s.

“Yesterday, the whale closed out the two positions on the right side… The whale entered the position at 66K and closed it out above 68K — this trade was a resounding success. Starting late last night, a whale of similar size began buying put options again, with over 2,000 contracts expiring today, targeting a price below 66K,” the analysts stated.

What Comes Next

Options settle at 08:00 UTC on Deribit. The hours leading up to that window typically generate the sharpest gamma hedging activity, pulling prices toward max pain.

For BTC, that means a potential drift toward $68,000 if bulls hold ground, or a break below $66,000 if the whale’s put bet plays out.

The post Whale Turns Bearish Ahead of $2 Billion Bitcoin and Ethereum Options Expiry appeared first on BeInCrypto.

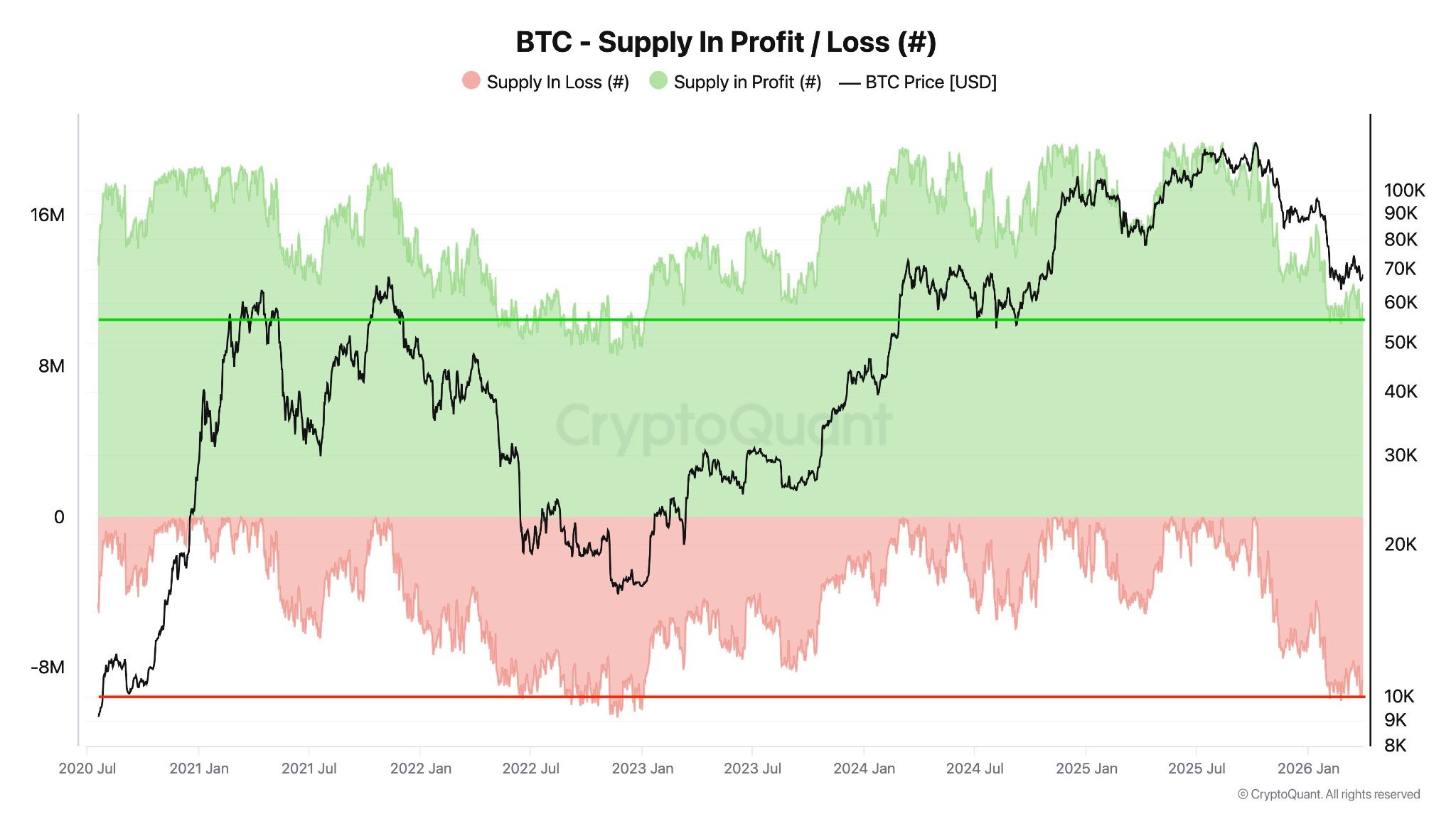

The amount of Bitcoin supply in profit and loss is now getting closer to levels typical of a bear market, according to a CryptoQuant analyst.

There are currently about 11.2 million Bitcoin (BTC) in profit. The previous bear market recorded 9 million BTC in profit at its lowest point, CryptoQuant analyst “Darkfost” said Thursday.

CryptoQuant data also shows there are about 8.2 million Bitcoin at a loss, with Glassnode data confirming it’s at levels not seen since late 2022.

“This is quite significant, considering that during the last bear market this figure reached about 10.6 million BTC,” Darkfost said.

Analysts have been debating whether Bitcoin has further to fall this year amid growing global turmoil. Bitcoin metrics that show a movement toward previous cycle lows could suggest that a market bottom is getting closer.

“This suggests that the market is reaching a notable level of undervaluation, comparable to the conditions observed during the previous bear market,” the analyst added.

Analyst sees increasing market stress, not undervaluation

However, Andri Fauzan Adziima, research lead at the Bitrue exchange, argued the data signals “increasing market stress, not immediate undervaluation.”

True capitulation bottoms saw deeper pain, he told Cointelegraph. The supply in loss in 2022 was greater than 50% and the supply in profit was around 45% or lower, while metrics such as net unrealized profit/loss (NUPL) and market value to realized value ratio (MVRV) were at “extremes.”

“Current data points to early/mid-bear transition (potential structural bottom near $55,000), with more downside or consolidation likely before a full reset.”

Related: Bitcoin’s drawdown is ‘less dramatic’ this cycle, Fidelity says

Data also shows Bitcoin has declined by about 52% from its all-time high this cycle, much less than previous bear markets, which saw 77% to 84% drawdowns from their cycle highs.

Strong dollar hampering recovery

Bitcoin author Timothy Peterson commented on X that Bitcoin “tends to struggle when the dollar is strong, and the Chinese yuan is weak.”

He added that this was due to tighter global liquidity, with higher dollar yields attracting capital into cash and bonds and cautious investor sentiment as China eases policy.

That only changes when US interest rates fall and “dollar yield loses its attractiveness,” which is not likely until the second half of 2026 or more likely 2027, he said.

The US dollar index (DXY) has gained about 5% over the past two months, according to TradingView.

For years, decentralized finance sold a simple, powerful idea: anyone, anywhere, can access financial services without gatekeepers. No banks, no approvals, no identity checks—just code and capital.

But beneath the surface, something is changing.

A growing number of protocols are quietly introducing permissioned layers—KYC-gated pools, whitelisted participants, and compliance-driven infrastructure. It’s subtle. Gradual. Easy to miss.

Yet it may redefine what DeFi actually is.

The Shift No One’s Loudly Talking About

Permissioned DeFi doesn’t arrive with headlines. It slips in through features like:

- KYC Pools – Liquidity pools restricted to verified users

- Whitelisted Access – Only approved wallets can interact with certain products

- Compliance Layers – Protocol-level rules aligning with regulatory frameworks

At first glance, these look like optional features. In reality, they signal a deeper evolution:

DeFi is adapting itself to fit inside the traditional financial system.

Why This Is Happening

Let’s be blunt—pure permissionless systems make regulators nervous.

Institutions want exposure to DeFi yields, but they need:

- Legal clarity

- Counterparty accountability

- Risk controls

Permissioned layers act as a bridge:

- They let institutions participate without violating compliance rules

- They give regulators something to work with

- They reduce the “wild west” perception of DeFi

In short, capital is forcing compromise.

What Changes (And What Breaks)

This shift isn’t just technical—it’s philosophical.

1. Participation Is No Longer Universal

The original promise of DeFi was inclusion.

Permissioned systems introduce exclusion by design.

If access requires:

- Identity verification

- Jurisdiction checks

- Approval from a governing entity

Then DeFi starts to look a lot like the system it aimed to replace.

2. “Open Finance” Becomes Conditional

DeFi assumed:

If you have a wallet, you’re in.

Permissioned DeFi changes that to:

If you meet the criteria, you’re in.

That’s a massive shift. It replaces code-based neutrality with policy-based access.

3. Liquidity Fragmentation

Instead of one unified pool of capital, we get:

- Public pools (permissionless)

- Private pools (permissioned)

This can lead to:

- Uneven yields

- Reduced efficiency

- Insider advantages for approved participants

Basically, the market starts splitting into tiers.

4. Power Starts Re-centralizing

Whitelists don’t manage themselves.

Someone decides:

- Who gets access

- Who gets removed

- What rules apply

Even if governance is “decentralized,”

Control creeps back in through decision-making layers.

The Trade-Off: Growth vs Principles

Let’s not pretend this is entirely bad.

Permissioned DeFi enables:

- Institutional capital inflows

- Regulatory survival

- Scalable adoption

Without it, DeFi risks staying niche—or getting shut out entirely.

But there’s a cost:

- Less openness

- Less censorship resistance

- Less equality

So the real question isn’t whether permissioned DeFi is good or bad.

It’s this:

How much of DeFi’s core ethos are we willing to trade for growth?

The Future: Two DeFis?

We may not end up with one unified ecosystem.

Instead, expect a split:

Permissionless DeFi

- Open to everyone

- Higher risk, higher innovation

- Resistant to control

Permissioned DeFi

- Regulated and compliant

- Institution-friendly

- Controlled access

They’ll coexist—but not as equals.

One maximizes freedom.

The other maximizes scale.

Final Thoughts

Permissioned DeFi isn’t sudden; it’s a slow drift.

No dramatic announcements.

No clear line crossed.

Just small changes… that quietly redefine everything.

And if you blink, you might miss the moment when “open finance” stops being fully open.

REQUEST AN ARTICLE

OpenAI has acquired technology talk show TBPN as it looks to refine how it communicates with audiences beyond its core products.

Summary

- OpenAI has acquired TBPN, a Silicon Valley-focused tech talk show, as it expands its role in shaping public conversations around artificial intelligence.

- TBPN will continue operating with editorial independence while also contributing to OpenAI’s communications and marketing efforts.

According to an Apr. 2 announcement, the deal brings the Los Angeles-based program under OpenAI’s umbrella. Financial terms of the deal were not disclosed.

TBPN, hosted by John Coogan and Jordi Hays, streams live for three hours each weekday and features interviews with founders, venture capitalists, and senior technology executives. Guests in recent months have included Mark Zuckerberg, Satya Nadella, and Sam Altman, underscoring the show’s growing influence within the tech ecosystem.

OpenAI’s leadership framed the acquisition as part of a push to shape how conversations around artificial intelligence unfold.

In an internal memo, Fidji Simo, OpenAI’s chief of strategy, said the company sees a need for “real, constructive conversation” as AI systems become more embedded in society. The company believes TBPN can help create that space while also expanding its reach.

Despite the ownership change, OpenAI has emphasized that TBPN will retain full editorial control.

Behind the scenes, the show is expected to contribute to OpenAI’s communications and marketing efforts beyond its daily broadcasts. Simo noted that TBPN’s track record in brand storytelling and its close view of industry trends played a role in the decision.

Founded in October 2024, TBPN began daily livestreaming in March 2025 and has since carved out a niche audience. Each episode draws roughly 70,000 viewers across platforms such as X, YouTube, and Spotify.

While modest compared to traditional financial media, the show has gained traction among technology leaders who see it as more aligned with industry perspectives than legacy outlets like Bloomberg or CNBC.

The acquisition comes shortly after OpenAI closed a $122 billion funding round led by Amazon, Nvidia, and SoftBank.

Asia markets rise led by Nikkei and Kospi, how are crypto equities faring?

Tony Pulis column: What Roberto de Zerbi needs to do to turn Tottenham around

30% Off Samsung Promo Code | April 2026

-

NewsBeat6 days ago

NewsBeat6 days agoThe Story hosts event on Durham’s historic registers

-

NewsBeat12 hours ago

NewsBeat12 hours agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Sports6 days ago

Sports6 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment4 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment5 days ago

Entertainment5 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World3 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Crypto World1 day ago

Crypto World1 day agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech4 days ago

Tech4 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Sports3 days ago

Sports3 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech3 days ago

Tech3 days agoEE TV is using AI to help you find something to watch

-

Business7 hours ago

Business7 hours agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion5 days ago

Fashion5 days agoAmazon Sundays: Soft Spring Layers

-

Business1 day ago

Business1 day agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech3 days ago

Tech3 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Tech4 days ago

Tech4 days agoApple will hide your email address from apps and websites, but not cops

-

Politics3 days ago

Politics3 days agoShould Trump Be Scared Strait?

-

Crypto World3 days ago

Crypto World3 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Tech3 days ago

Tech3 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Tech4 days ago

Tech4 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Tech5 days ago

Tech5 days agoElon Musk’s last co-founder reportedly leaves xAI

You must be logged in to post a comment Login