Crypto World

What is a crypto launchpad? Fair launches explained

Somewhere on the internet right now, a token that did not exist ninety seconds ago is being traded by strangers. It cost its creator about two dollars to launch, required no code, no company, and no permission, and it will most likely be worthless by dinner.

The machine that makes this possible is called a launchpad, and in the current market cycle, launchpads have become the single busiest category of application in all of crypto, minting millions of tokens, generating hundreds of millions of dollars in fees, and hosting both the fastest fortunes and the fastest wipeouts anywhere in the market.

A crypto launchpad is a platform where new tokens are created, distributed, and first sold. That one sentence covers two radically different worlds. The older world is the curated launchpad, a gatekept venue where vetted projects raise capital from early investors through structured sales. The newer world is the permissionless memecoin launchpad, where anyone can deploy a token instantly and the market sorts survivors from corpses in real time. Understanding both models, and the fair launch versus presale divide that separates them, is now basic literacy for anyone touching new tokens.

This guide covers what launchpads are and why they exist, how the curated model works step by step, how the ICO era created and nearly destroyed the category, how Pump.fun rewrote the rules with bonding curves and one click deployment, how fair launches differ from presales in mechanics and in incentives, the competitive war now running across chains, the risk landscape from rug pulls to sniping, and a practical checklist for evaluating any launch before putting money in.

What a launchpad is and the problem it solves

Every new token faces the same cold start problem. It needs a price, but prices come from markets, and markets need liquidity and participants, which a brand new asset has none of. It needs distribution, because a token held entirely by its creator is not a market but an inventory. And if the project behind it needs funding, it needs a way to sell tokens before any of the above exists. Launchpads are infrastructure built to solve the cold start: they provide the venue, the mechanics, and the initial audience that turn a token from a contract deployment into a trading asset.

The earliest solution was no solution at all. Projects in the initial coin offering era of 2017 and 2018 simply published a whitepaper and a deposit address, and money flowed in on trust. The results were catastrophic often enough, exit scams, vaporware, outright theft, that the market demanded intermediaries, and launchpads emerged as exactly that: platforms that would screen projects, structure the sale, hold the process to rules, and lend their reputation to launches that passed. Binance Launchpad’s 2019 debut set the template for the exchange hosted version, the initial exchange offering, and dozens of platforms followed across chains and niches.

Between those poles sits a spectrum of hybrids: launchpads with light vetting but open access, curated venues that added instant launch products, and exchange platforms that bolted bonding curves onto their listing pipelines. The taxonomy matters less than the underlying trade: every launchpad design chooses a point on the line between safety and openness, and every point on that line has a failure mode.

The intermediary model dominated until January 2024, when a Solana application called Pump.fun asked a heretical question: what if the launchpad screened nothing, structured nothing, and simply let anyone launch instantly into an automated market? The answer turned out to be the most prolific token factory in crypto history, and it split the launchpad world permanently in two.

How curated launchpads work

The traditional pipeline runs in recognizable stages. A project applies, submitting its documentation, team credentials, tokenomics, and roadmap. The platform vets, with the serious venues running identity checks, code audits, and economic review, and rejecting most applicants; the vetting is the product, since it is the reason investors trust the venue at all. An accepted project then announces its sale terms: price, allocation sizes, dates, and the vesting schedule governing when purchased tokens actually become tradable.

Participation mechanics vary by platform. The simplest model is first come, first served at a fixed price. More common is tiered access, where users must hold or stake the launchpad’s own native token to qualify, with larger stakes buying larger allocations, a design that conveniently creates permanent demand for the platform’s token. Lottery systems randomize access among registrants. Auctions let demand set the price. Whatever the format, buyers in these sales are getting in before public listing, usually at a discount to the expected listing price, and usually subject to vesting: a portion at the token generation event, the rest released over months. Some platforms add refund windows that let participants back out before claiming tokens, a feature that emerged after enough listings traded below their sale price to make guarantees a selling point.

After the sale, the platform typically coordinates the listing, on its own exchange in the IEO model or on a decentralized exchange in the IDO model, where the sale proceeds seed the first liquidity pools. The launch is complete when the token trades freely and the launchpad moves on to the next cohort. At their best, curated launchpads function as a hybrid of underwriter, accelerator, and quality filter. At their worst, they are pay to play listing machines whose vetting is a press release, and the category has produced plenty of both.

Pump.fun and the permissionless revolution

Pump.fun deleted every stage of that pipeline. Launched on Solana in January 2024, it reduced token creation to a form: name, ticker, image, and roughly two dollars in fees, with the token live and tradable in under a minute. No application, no vetting, no presale, no team allocation, no liquidity to raise. The mechanism that makes this possible is the bonding curve, an automated pricing formula that acts as the token’s first market.

The curve works like a vending machine that raises its prices as stock sells. A fixed portion of the new token’s supply is placed into the curve contract. Buyers purchase directly from the curve, and each purchase pushes the price higher along the formula; sellers sell back into it, pushing the price down. There is no order book, no market maker, and no counterparty except the contract, which means every token has instant, guaranteed liquidity from its first second, priced purely by net demand.

Graduation is the second innovation. When a token’s bonding curve fills to a threshold market value, originally around 69,000 dollars, later revised alongside the platform’s move to its own exchange, the accumulated funds are deposited automatically into a liquidity pool on an open decentralized exchange, and the token leaves the nursery to trade in the wild. Most tokens never graduate. That is the design, not a flaw: the curve stage is a cheap, contained arena where thousands of ideas can fail without wasting anyone’s liquidity but their buyers’.

The numbers the model produced are difficult to overstate. More than eleven million tokens have launched through the platform, cumulative revenue has run toward a billion dollars, and at peak the platform accounted for the large majority of all new token launches on Solana. In July 2025 the platform sold its own PUMP token, raising six hundred million dollars in twelve minutes as part of a sale exceeding a billion dollars, a fundraising event that would have ranked among the largest ICOs of the previous era, executed by a company whose product exists to make fundraising unnecessary. The irony was widely noted and changed nothing about the demand.

Inside the bonding curve: a worked example

The mechanics become intuitive with numbers. Suppose a new token launches with 800 million of its 1 billion supply placed into the curve, the standard structure on Pump.fun’s original design. The first buyer spends a small amount of SOL and receives tokens at the curve’s floor price, fractions of a cent. Each subsequent buy delivers fewer tokens per SOL, because the formula raises the price as the curve’s token reserve depletes. A buyer arriving after 100 SOL of net inflows pays a visibly higher price than the first; a buyer arriving after 400 SOL pays multiples of it.

Selling reverses the flow. A holder sells tokens back into the curve and receives SOL out of the accumulated reserve, pushing the price back down the formula. The reserve can never be emptied below what the formula requires, which is what makes the liquidity guaranteed: unlike a traditional pool that a creator can drain, the curve’s funds are locked in the contract and only move along the formula or, at graduation, into the public pool.

The design has an underappreciated psychological property. Because early positions on the curve are mathematically cheapest, every launch is a race, and the race is the product. The interface shows live buys, holder counts, and a progress bar to graduation, gamifying the climb. Critics describe the result as a slot machine with extra steps; users describe it as the purest price discovery in crypto, a market with no fundamentals to argue about, only flows. The two descriptions are not in conflict.

What the curve does not do is protect anyone after the music stops. When attention moves on, the same formula that escalated the price on the way up marks it down just as smoothly, and the last buyers hold the loss. The curve guarantees a market. It has no opinion about the price.

Fair launch versus presale: the real dividing line

Underneath the platform war sits a deeper design question: who gets tokens before the public does, and at what price. A presale model answers: insiders do. Investors, the team, and early allocations buy at preferential prices before public trading, with vesting schedules governing when they can sell. The presale is how projects fund development, and it is also how the low float, high valuation structure gets built, with all the delayed sell pressure that implies. Buying at public listing in a presale token means buying above the price every insider paid.

A fair launch answers: nobody does. All supply enters the market through the same mechanism at the same starting price, with no presale, no team allocation, and no vesting, because there is nothing to vest. The bonding curve launchpads made fair launches operationally trivial, and the model’s appeal is exactly its symmetry: the creator has no privileged tokens to dump, so the archetypal insider rug is structurally impossible.

The honest comparison cuts both ways. Fair launches remove insider pricing but replace it with a speed game, where the earliest seconds of the curve capture the cheapest tokens, and being early is its own privilege, one that trading bots enjoy far more than humans. Snipers buy in the launch block, bundlers split purchases across wallets to disguise concentration, and a nominally fair curve can be quietly cornered before an ordinary buyer ever sees the ticker. Presales, for all their asymmetry, at least fund something: a team with capital, obligations, and a vesting schedule has reasons to build, while a fair launched memecoin has no treasury, no roadmap, and no one accountable. Fairness at the starting line does not imply anything about the race.

The practical synthesis most of the market has settled on: fair launch mechanics suit tokens that are pure attention assets, meme coins whose only product is the crowd itself, while structured sales with vesting still dominate for projects that need funded teams. The mechanisms sort the assets.

The launchpad wars

Success invited siege. LetsBonk arrived in April 2025 from the BONK community in collaboration with Raydium, Solana’s largest decentralized exchange, differentiating itself by recycling a share of fees into buying BONK, a value return the community contrasted pointedly with Pump.fun’s extraction of fees. The same BONK ecosystem later provided a darker lesson in what community infrastructure can cost when its treasury governance failed spectacularly in a twenty million dollar attack, a reminder that the money launchpads generate has to live somewhere, and that somewhere has to be secured.

Competition then went cross chain. Four.Meme rose on BNB Chain and, in one signal moment, flipped Pump.fun in daily revenue as Binance ecosystem memecoins caught their own wave. SunPump ran the model on Tron. Moonshot courted safety conscious users with audited contracts. Raydium, watching its former partner build a competing exchange, shipped its own LaunchLab. Every general purpose chain now has at least one bonding curve launchpad, because the model is simple to copy and the fees are irresistible: the platform earns on every trade in every casino game, win or lose.

The economics explain the durability. A launchpad monetizes activity, not quality. Creation fees, trading fees on the curve, and graduation fees add up across millions of launches into revenue that rivals the largest protocols in crypto, all without the platform taking token risk itself. Critics call the model extractive, a house that profits from churn while the overwhelming majority of its tokens go to zero. Defenders answer that the platform sells exactly what it advertises, instant markets, and that no one is misled about the odds. Both descriptions are accurate.

What the launchpad era changed about token launches

Zoom out and the permissionless model altered three structural facts about crypto markets. First, it collapsed the cost of asset creation to effectively zero, which moved the scarce resource from capital to attention. When anyone can mint a token in a minute, tokens themselves are worthless by default, and value concentrates in whatever can gather and hold a crowd: a meme, a personality, a moment. The launchpad era is the attention economy with a price feed attached.

Second, it inverted the disclosure model. The curated era tried to make issuers trustworthy through vetting; the permissionless era abandoned trust and substituted transparency, publishing every wallet, every trade, and every creator action on chain and letting buyers do their own forensics. The tooling ecosystem that grew around launchpads, holder scanners, bundler detectors, creator wallet trackers, is the market’s answer to a world where nobody checks anything before launch, so everyone must check everything after.

Third, it turned launch mechanics into a competitive product category. Fee structures, creator revenue sharing, buyback programs, graduation thresholds, and anti sniping features now iterate week by week across competing platforms, the way exchanges once competed on maker fees. Some experiments push value back to communities, like fee recycling into ecosystem tokens. Others push it to creators, paying them a share of trading fees to keep launching. The direction of the iteration matters more than any single feature: launch infrastructure has become a business in its own right, larger by revenue than most of the projects that launch on it.

The risk landscape

The launchpad world’s risks divide by model. On permissionless platforms, the headline number tells the story: analyses of Pump.fun activity found that around 98.6 percent of launched tokens exhibited rug pull characteristics or died worthless, and the platform’s own founders concede that soft rugs, where a creator simply abandons a token and sells whatever they hold, cannot be prevented technically. Add sniping, bundled wallet accumulation, coordinated pump groups, copycat tickers designed to catch fat fingered buyers, and livestream stunts engineered for attention, and the picture is clear: the permissionless arena is adversarial by default, and every participant should assume the other side of their trade knows something they do not.

Curated platforms carry subtler risks. Vetting varies from rigorous to cosmetic, and a platform paid by projects to launch has a structural conflict when deciding what passes review. Allocation tiers push users to buy and stake platform tokens, concentrating risk in the venue itself. Vesting schedules on presale tokens defer insider supply into the future, where it lands on whoever is holding at unlock time. And the legal environment remains live: the category has drawn class action lawsuits, and the United Kingdom’s regulator blocked access to Pump.fun outright, part of a broader regulatory reckoning over whether instant token factories fit inside any existing framework. Distribution methods sit on a spectrum of scrutiny, from structured sales at one end to free airdrops at the other, and launchpads occupy the most commercially aggressive part of that spectrum.

None of this makes the category untouchable. It makes it a venue where risk is priced by attention, and where the checklist below does more work than in any other corner of crypto.

How to evaluate any launch

Before touching a curated sale, read the token’s full vesting table and compute what percentage of supply insiders hold, at what cost basis, unlocking on what dates. Check who audited the contracts and whether the audit is public. Investigate the launchpad’s track record: how did its last ten launches trade after listing, and after the first major unlock? Confirm what the raised funds are contractually committed to. If the answers are missing, the answers are bad.

Two universal habits complete the toolkit. Verify everything at the contract level, because interfaces lie more easily than chains: the vesting table that matters is the one enforced in code, and the holder distribution that matters is the one visible on chain right now. And watch what launches around you, because launchpad markets move in narrative waves, and a token’s fate usually has more to do with the wave it rides than with anything specific to the token.

Before touching a bonding curve token, check holder concentration first, since a token where a handful of connected wallets hold most of the supply is a trap regardless of its chart. Look at whether the creator’s wallet is accumulating or distributing. Treat graduation as a checkpoint, not a guarantee, because plenty of tokens rug after reaching open trading. Size positions on the assumption of total loss, because the base rate says that assumption will usually be correct. And treat social proof as a manufactured commodity, because on launchpads, it is: engagement, holders, and volume can all be bought for less than the profit of one successful exit.

The meta lesson spans both worlds. A launchpad organizes access to new tokens; it does not underwrite them. The most polished launch process on the most reputable platform still delivers an asset whose value depends entirely on what it is and who wants it. The machine that creates markets in ninety seconds is real, impressive, and permanently indifferent to whether any particular buyer walks away richer.

Frequently asked questions

What is a crypto launchpad?

A crypto launchpad is a platform where new tokens are created, distributed, and first sold. Curated launchpads screen projects and run structured early sales for investors, while permissionless launchpads such as Pump.fun let anyone create a token instantly and trade it through an automated bonding curve.

What is the difference between an ICO, an IEO, and an IDO?

All three are token sale formats. An ICO is a direct sale by the project itself, an IEO is a sale hosted and vetted by a centralized exchange, and an IDO is a sale conducted through a decentralized exchange or launchpad, with tokens typically becoming tradable on chain immediately after.

What is a bonding curve?

A bonding curve is a pricing formula inside a smart contract that acts as a token’s first market. Buyers purchase from the curve and each purchase raises the price; sellers sell back into it and lower the price. It gives new tokens instant liquidity without an order book or market maker.

What does graduation mean on Pump.fun?

Graduation is the moment a token’s bonding curve reaches its target value and the accumulated funds move automatically into a liquidity pool on an open exchange. The token then trades freely outside the launchpad. Most tokens never reach graduation.

What is a fair launch?

A fair launch distributes all supply through the same public mechanism at the same starting terms, with no presale, no team allocation, and no vesting. It removes insider pricing advantages, though bots and early snipers still gain an edge in the opening moments.

Are launchpad tokens safe to buy?

They carry elevated risk in both models. Analyses have found that the overwhelming majority of tokens on permissionless launchpads end up worthless or exhibit rug pull behavior, while presale tokens carry insider unlock overhangs. Position sizing that assumes total loss is the prudent baseline.

How do launchpads make money?

Primarily through fees: token creation fees, trading fees on bonding curve activity, graduation or listing fees, and in curated models, charges to projects and revenue tied to the platform’s own token. Launchpads earn on activity regardless of whether individual tokens succeed.

Why do some launchpads require staking their token?

Tiered access models grant larger sale allocations to users who hold or stake the platform’s native token. The design rations scarce allocations and, by requiring the stake, creates ongoing demand for the launchpad’s own token.

This article is for educational purposes only and does not constitute financial or investment advice. Launchpad mechanics, fees, and platform details change frequently. Details are accurate as of July 14, 2026.

South Korea plans to include crypto under a new National Asset Basic Act, a sweeping law that will modernize how the state manages roughly 1,400 trillion won in assets.

The reform, the first in 76 years, treats digital assets as long-term national wealth rather than a risk.

The National Asset Basic Act Redefines State Wealth

The National Asset Basic Act is a proposed South Korean law that expands the definition of state assets to include cryptocurrencies, virtual assets, and intellectual property.

The Ministry of Economy and Finance unveiled the plan on July 15 during a policy briefing in Seoul. The announcement formed part of the government’s economic strategy for the second half of 2026.

The legislation will replace a management system anchored in the State Property Act of 1950. That framework focused almost entirely on real estate and preservation, leaving no room for emerging asset classes. Officials described the current rules as outdated for a modern digital economy.

Follow us on X to get the latest news as it happens.

The scale involved is enormous. The law will govern about 1,400 trillion won in state holdings, equivalent to nearly $940 billion. According to the ministry, the new model prioritizes value creation over simple custody of public property.

The government also plans to tokenize state-owned real estate through security tokens, allowing citizens to invest and share returns. A pilot for tokenized government bonds linked to the Bank of Korea’s CBDC infrastructure is scheduled for 2027.

What Does the Law Mean for Korea’s Crypto Market

The proposal marks a philosophical shift. Previous crypto rules in the country concentrated on investor protection and exchange oversight.

Recognizing digital assets as national property integrates them into the country’s long-term financial infrastructure rather than treating them as pure speculation.

The context amplifies the signal. South Korea handles an estimated 15% to 20% of global crypto trading volume, with more than 18 million local participants. Few governments manage a retail base of that size anywhere in the world.

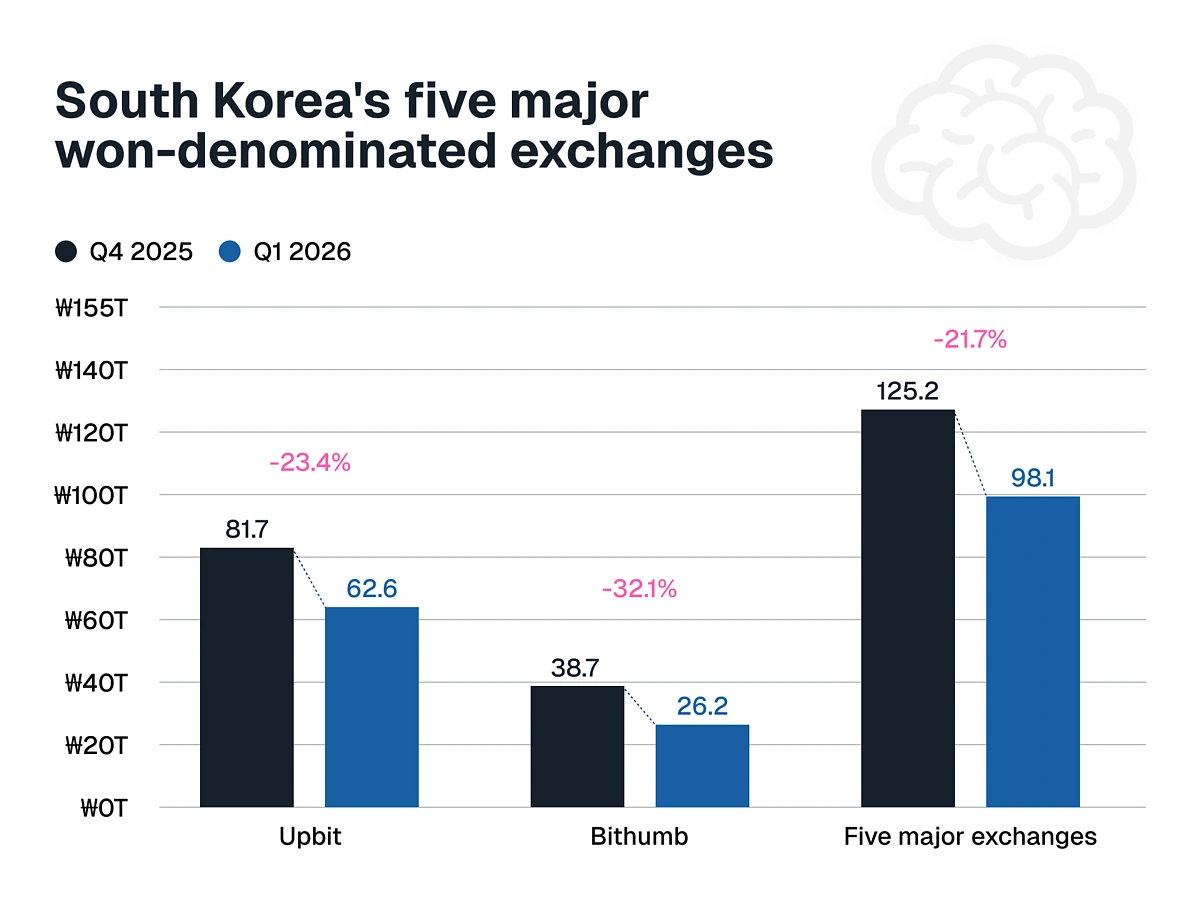

According to CoinGecko data, average monthly trading volume in KRW fell by 21.7% from Q4 2025 (125.2 trillion won) to Q1 2026 (98.1 trillion won). This doesn’t mean capital is leaving the market; it’s simply rotating. Funds are shifting away from retail speculation and toward institutional settlement infrastructure.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights.

The measure also arrives within a broader digital agenda. Authorities are advancing the Digital Asset Basic Act, which will set rules for won-pegged stablecoins, and reviewing Capital Markets Act amendments to enable the first spot crypto ETFs.

A legal basis for cross-border stablecoin transactions is also in the works, easing international payments with digital assets.

Implementation details remain pending, including how the state would acquire, custody, or value its future digital holdings over time.

Still, the direction seems clear. One of the world’s most active crypto markets now wants its government balance sheet to speak the same language.

The post South Korea Moves to Treat Crypto as National Wealth Under New Law appeared first on BeInCrypto.

Investment giant Cantor Fitzgerald and cryptocurrency-focused broker-dealer Securitize (SECZ), are revamping initial public offerings (IPOs) with tokenization and blockchain technology, the companies said on Wednesday.

Under the agreement, Cantor will leverage its equity capital markets and trading capabilities, while Securitize will provide the tokenization infrastructure used to issue, distribute, and service tokenized securities, according to a press release.

Large traditional finance players are taking rapid steps towards the tokenization of capital markets. This week the Depository Trust & Clearing Corporation (DTCC) announced further plans to tokenize stocks with a range of partners including JPMorgan, Goldman Sachs, BlackRock and Vanguard.

The collaboration will enable public companies to raise capital and issue securities onchain with improved operational efficiency and modernized ownership records, while still operating within the established capital markets framework of traditional public offerings, the companies said.

Rather than focusing on tokenized funds or secondary trading, this partnership extends blockchain infrastructure directly into IPOs and follow-on offerings, a Securitize spokesperson said in an email.

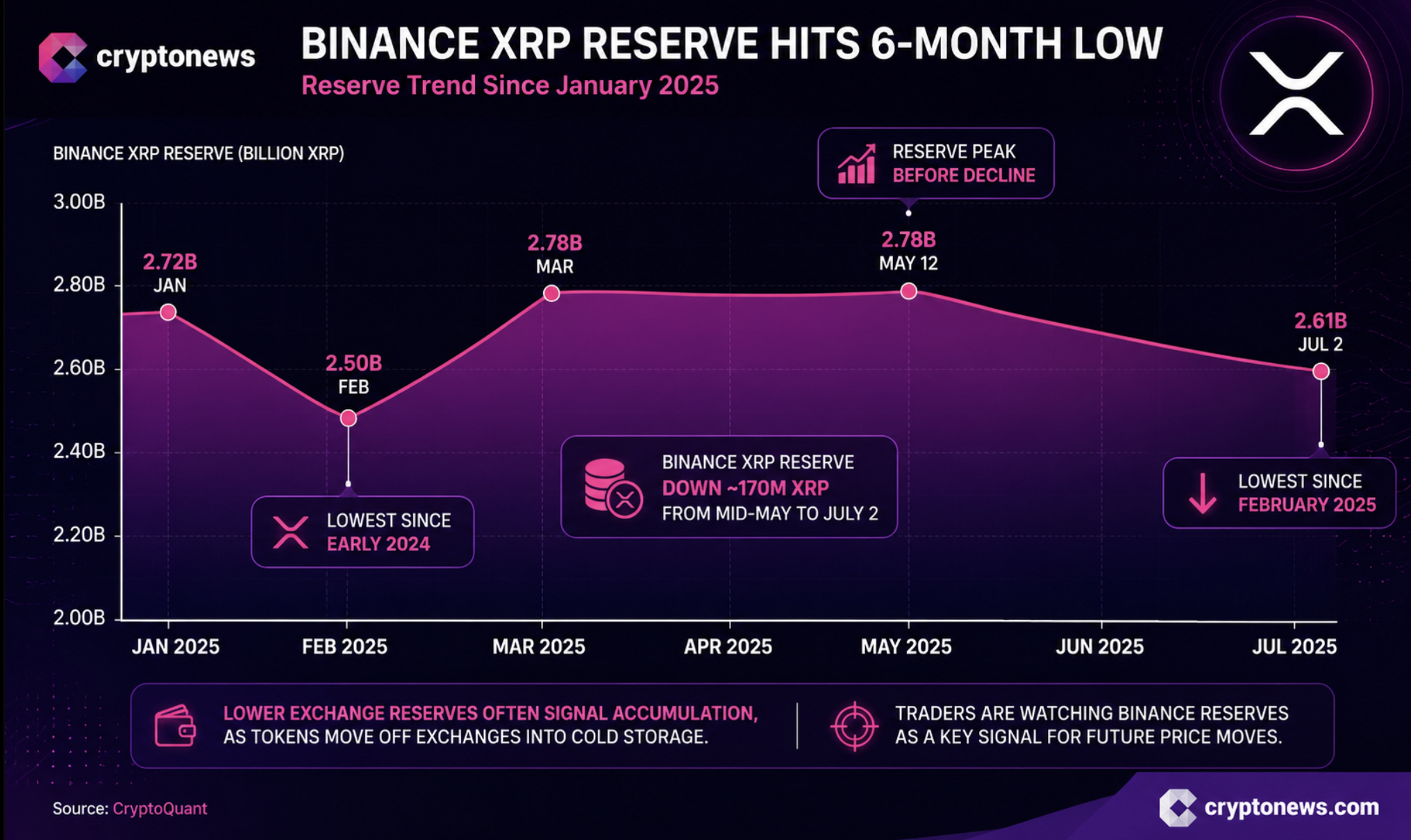

Binance’s XRP reserve just hit its lowest level since February as its price prediction turns slightly bullish. XRP price is hovering near $1.11 after gaining about 4% over the past 24 hours. That bounce ended several sluggish sessions, but the next move still needs proof.

According to CryptoQuant contributor Arab Chain, Binance’s XRP holdings have dropped to roughly 2.61 billion tokens, the lowest level in six months. Even better for bulls, meaningful inflows have yet to refill those reserves since early July. Coins leaving exchanges often hint at accumulation, although the market does not always reward patience immediately.

That said, XRP slipped toward $1.06 while reserves kept shrinking. In other words, weak sentiment and thin liquidity outweighed the bullish on-chain signal. Now that buyers have returned, those reserve trends may finally matter. Markets love showing up late to the party, but they usually bring plenty of noise.

Meanwhile, the Binance CVD Confirmation Score remains at negative 6.93 million, showing sellers have controlled order flow since XRP traded above $2.00 earlier this year. For now, Binance reserve data remains a closely watched signal as traders look for the next decisive move.

Discover: The Best Crypto to Diversify Your Portfolio

XRP Price Prediction: Break $1.15 and Reverse The Slide?

Technically, the $1.06 to $1.07 zone has continued to attract buyers, helping absorb the latest pullback. Immediate resistance remains between $1.12 and $1.15, where previous rallies have repeatedly stalled. That makes this area the first real test if buyers want to keep control.

The Binance CVD Confirmation Score remains at negative 6.93 million, showing sellers have dominated order flow since XRP traded above $2.00 earlier this year. A convincing break above $1.15 needs more than a single green candle. It also needs sustained buying pressure to shift the market’s balance.

If buyers defend current support and reclaim $1.15, momentum could extend toward the $1.30 to $1.40 region. Otherwise, XRP may continue moving between $1.07 and $1.12 while traders wait for the next catalyst. A daily close below $1.06 would weaken the setup and could expose the $0.95 to $1.00 area.

Despite the recent recovery, XRP still trades about 70% below its all-time high near $3.65. That leaves plenty of room for upside, but patience remains part of the game.

Trade XRP on BYBIT now, and Don’t Miss Out on Our $1,000 USDT Airdrop

LiquidChain Targets Early-Mover Upside as XRP Tests Key Resistance

XRP’s rebound is real, but the ceiling from $1.12 to $1.15 is equally real, and with a market cap already in the tens of billions, even a clean breakout delivers percentage gains that dwarf what early-stage infrastructure plays can offer. That asymmetry is exactly where traders rotating for higher upside exposure have been looking.

LiquidChain ($LIQUID) is a Layer 3 infrastructure project with a specific structural angle: it fuses Bitcoin, Ethereum, and Solana liquidity into a single execution environment. Liquid uses one deployment, three ecosystems.

An L3 crafted by LiquidChain? — LiquidChain (@getliquidchain) July 6, 2026

That is the most powerful type of Magic.  ⟁https://t.co/vqvBcdSQYC pic.twitter.com/7Rwd3fVOGc

⟁https://t.co/vqvBcdSQYC pic.twitter.com/7Rwd3fVOGc

The architecture centers on a Unified Liquidity Layer, Single-Step Execution, and Verifiable Settlement, targeting the fragmentation problem that still costs DeFi users real money on every cross-chain interaction.

The presale is currently priced at $0.0148, with $900K raised to date. LiquidChain has continued attracting capital even through recent macro-driven volatility, which says something about conviction at this stage.

Research LiquidChain here before the next pricing tier moves.

Discover: The Best Token Presales

The post XRP Price Prediction: Binance Reserve Hits 6 Months Low appeared first on Cryptonews.

XRP Ledger has entered the final two-week activation countdown for its fixCleanup3_2_0 amendment after validator support exceeded the network’s required 80% approval threshold.

Summary

- XRP Ledger’s fixCleanup3_2_0 amendment has entered its two-week activation countdown.

- The upgrade bundles protocol fixes for lending, permissioned domains, and the Permissioned DEX.

- Activation is scheduled for July 29 if validator support stays above the 80% threshold.

According to XRP Ledger governance data, the bundled maintenance amendment currently has 85.71% validator support, with 30 validators voting in favor and five against.

Under the network’s governance rules, an amendment must maintain at least 80% support for two consecutive weeks before it can be activated on the mainnet. If support drops below that level during the countdown, the activation timer resets.

Validator approval has moved the amendment into its final activation stage

With the voting threshold now secured, the amendment has entered its activation phase and is currently scheduled to go live on July 29, 2026, at 09:57 UTC, provided validator backing remains above the required level throughout the waiting period.

XRPL validator Vet shared the update on X, noting that fixCleanup3_2_0 is now in its two-week activation window. Vet also said node operators will need to update their software before the amendment becomes active to ensure compatibility with the protocol changes.

Unlike feature-focused upgrades, fixCleanup3_2_0 combines several maintenance fixes into a single amendment. The package addresses precision and rounding issues affecting Single Asset Vaults and the Lending Protocol while also correcting behavior in Permissioned Domains and the Permissioned DEX introduced alongside XRPL v3.2.0.

Additional protocol changes validate non-canonical Multi-Purpose Token (MPT) amounts, introduce zero DomainID verification for permissioned domains, and correct an invariant governing valid Permissioned DEX offer deletions. The amendment also adds another ledger invariant designed to prevent account deletions from leaving directly accessible artifacts behind.

By grouping multiple maintenance updates into one amendment, the XRP Ledger governance process requires validators to approve a single package instead of voting on several independent protocol changes.

Recent ecosystem growth has expanded activity around the network

The maintenance vote comes as development activity on XRP Ledger continues to expand beyond core protocol updates. Earlier, the network surpassed 1 million AI-powered payments processed through the x402 protocol, highlighting increasing use of AI-enabled payment applications.

Ripple-backed t54.ai recently launched the XRPL AI Hub, a platform that brings together AI projects, autonomous agents, developer tools, payment services, and technical documentation in one place.

According to t54.ai, the hub was introduced with support from Ripple developers and the XRP Ledger Foundation to help developers discover and build AI applications on the XRP Ledger.

Although the AI Hub launch is separate from the fixCleanup3_2_0 amendment, both developments arrive as the network continues improving infrastructure for decentralized finance, tokenization, permissioned trading, and AI-powered payment services.

If validator support remains above the required threshold until the end of the activation window, fixCleanup3_2_0 will become the latest protocol update added to the XRP Ledger without requiring another round of governance voting.

Dario Amodei, co-founder and CEO of Anthropic, during the company’s Builder Summit in Bengaluru, India, Feb. 16, 2026.

Samyukta Lakshmi | Bloomberg | Getty Images

Anthropic is lining up meetings with investors ahead of a potential initial public offering later this year, a person with knowledge of the plans told CNBC.

Bankers leading the offering are scheduling meetings between prospective investors and executives of the artificial intelligence firm behind the popular Claude models, said the person, who declined to be identified speaking about the process.

The meetings suggest Anthropic’s IPO preparations are advancing, as bankers begin sounding out investor demand before a formal roadshow and eventual share sale. Anthropic confidentially filed its IPO prospectus with the Securities and Exchange Commission last month, but hasn’t disclosed when it plans to debut.

The giant AI startup could hit the public markets as soon as October, though the timing could change, according to Bloomberg, which first reported the investor meetings. An Anthropic spokesperson declined to comment.

An Anthropic listing would build on momentum from June’s massive SpaceX IPO and further open the public markets to companies at the center of the AI boom. It follows years in which the industry’s biggest names remained private while raising hundreds of billions of dollars from investors.

Anthropic appears poised to beat rival OpenAI to the public markets, which could be an advantage for the startup if AI enthusiasm later wanes. OpenAI also confidentially filed for an IPO with the SEC in June, but it has not disclosed any additional details.

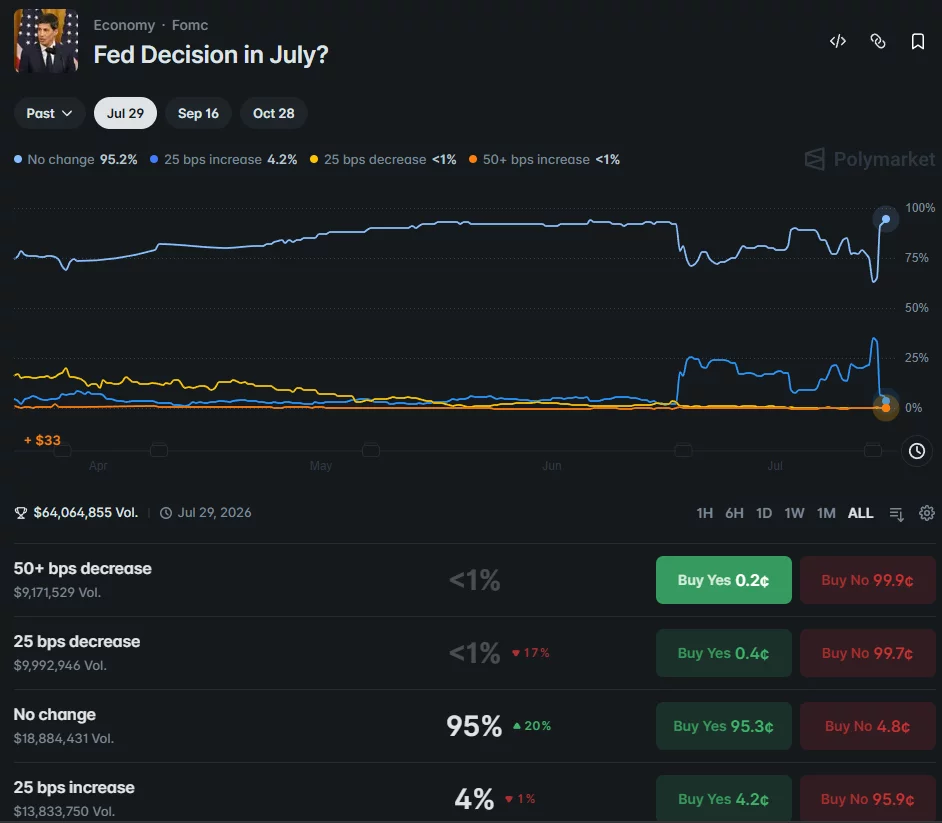

Bitcoin has climbed above $65,000 after softer-than-expected U.S. producer inflation reduced expectations of a Federal Reserve rate hike later this month.

Summary

- Bitcoin climbed above $65,000 after weaker-than-expected U.S. PPI data boosted risk appetite.

- Cooling inflation reduced expectations of a July Fed rate hike in both traditional and crypto markets.

- Ethereum topped $1,900 as the total crypto market capitalization rose above $2.3 trillion.

According to data from the U.S. Bureau of Labor Statistics, June’s Producer Price Index (PPI) added fresh momentum to risk assets after inflation came in below economists’ forecasts.

The total crypto market gained more than 2% to climb above $2.3 trillion, while Bitcoin reclaimed the $65,000 level and Ethereum moved above $1,900 for the first time since early June. The latest move extends the rally that began after June’s Consumer Price Index (CPI) report also surprised to the downside.

Softer inflation cuts expectations for a July Fed rate hike

The Bureau of Labor Statistics reported that headline PPI fell 5.5% year over year in June, below the 6.2% consensus estimate. On a monthly basis, producer prices declined 0.3%, the sharpest monthly drop since April 2025. Core PPI, which excludes food and energy, rose 4.7% from a year earlier, also below the expected 5.1%, while the monthly increase slowed to 0.2%, missing expectations of 0.3%.

Coming one day after a softer CPI report, the latest inflation figures strengthened investor confidence that price pressures continue to ease. The June CPI release had already lifted Bitcoin and the wider crypto market after recording the largest monthly decline in consumer prices since April 2020.

Analysts have linked part of last month’s cooling inflation to lower energy costs following the now-ended ceasefire agreement between the United States and Iran.

The combination of weaker CPI and PPI readings has encouraged traders to reassess the Federal Reserve’s next policy move, with markets increasingly expecting policymakers to keep interest rates unchanged at their July meeting.

Rate markets and prediction platforms scale back tightening bets

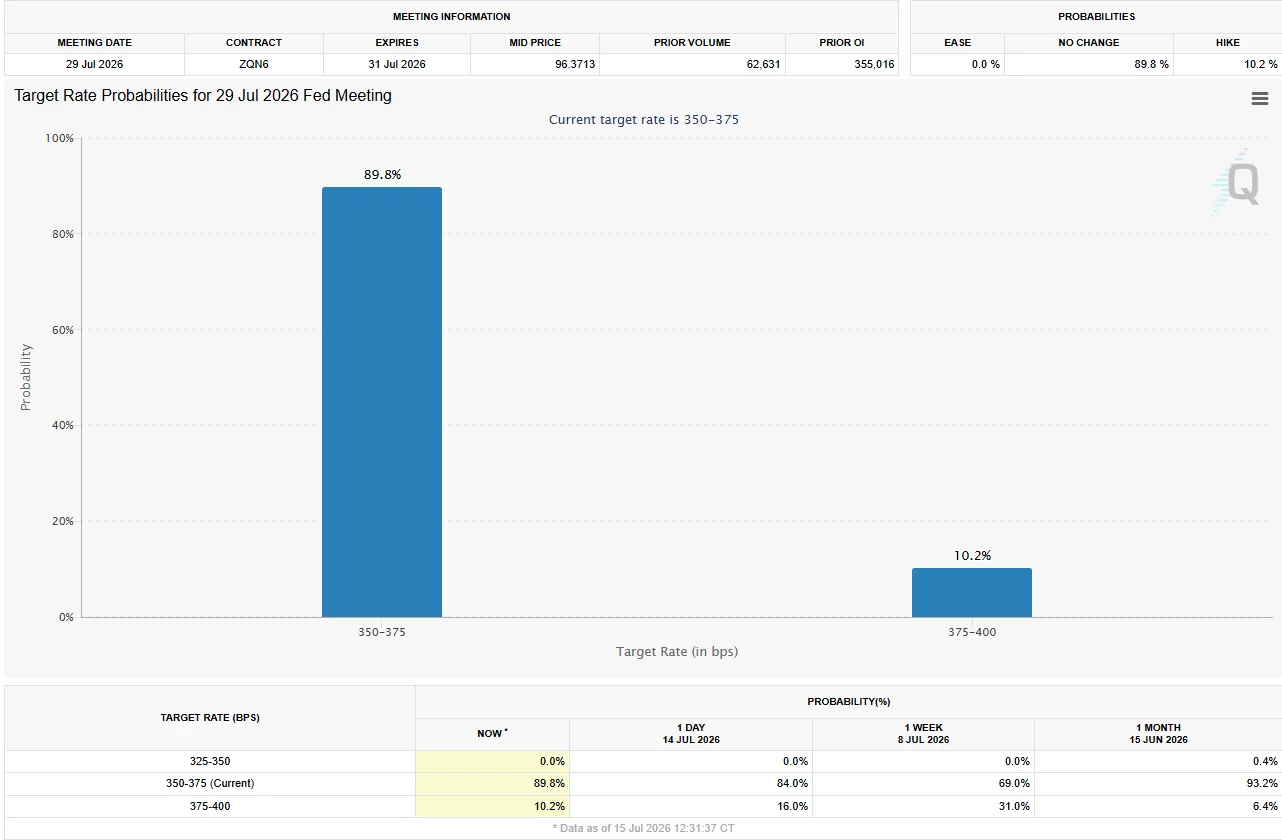

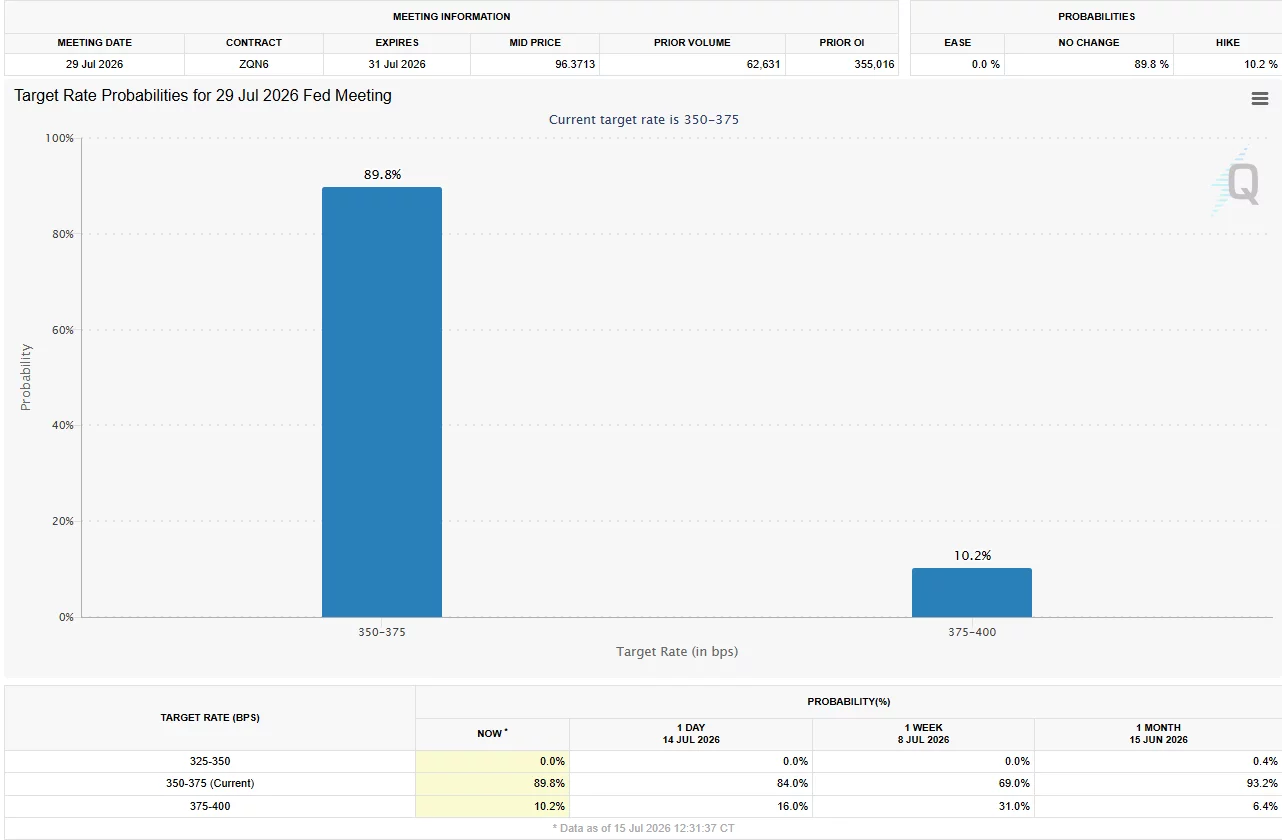

Expectations for another Federal Reserve rate increase dropped further after the PPI report. According to the CME FedWatch Tool, traders now assign only a 10.2% probability of a rate hike at the July 29 Federal Open Market Committee meeting, down from roughly 16% following the CPI release and well below levels above 30% seen last week.

Crypto-based prediction markets have become even more confident that policymakers will stay on hold. Data from Polymarket places the probability of a July rate hike at just 4%, showing a wider gap between crypto traders and traditional interest-rate markets.

Markets have also lowered the probability of an additional rate hike before the end of 2026. CME FedWatch data shows those odds have eased to about 51%, compared with around 55% a day earlier and roughly 71% at last week’s peak.

Even with inflation data moving in a favorable direction, Federal Reserve Chair Kevin Warsh has urged caution. During testimony before the House on Tuesday, Warsh warned that one encouraging inflation report does not mean the central bank has completed its work.

According to his remarks, the Federal Reserve remains committed to returning inflation to its long-term 2% target before declaring victory over price pressures.

For crypto investors, however, the latest inflation releases have shifted attention back toward monetary policy. With both CPI and PPI surprising to the downside in consecutive sessions, digital assets have benefited from renewed expectations that borrowing costs may remain unchanged in the near future, supporting demand for risk-sensitive assets including Bitcoin and Ethereum.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Securitize and Cantor Fitzgerald have partnered to support blockchain-based initial public offerings (IPOs) and follow-on equity offerings for listed companies, a move that could further expand the use of tokenized securities in traditional capital markets.

The companies said Wednesday that they are developing a framework for primary issuances that would allow companies to raise capital through tokenized securities while remaining within the existing regulatory framework for public offerings. The framework would support both IPOs and follow-on, or secondary, offerings, in which already public companies issue additional shares to raise capital.

Under the agreement, Securitize will provide the tokenization infrastructure used to issue, distribute and service the digital securities. Its SEC-registered broker-dealer affiliate, Securitize Markets, will participate in the offering and settlement process. Cantor will contribute its equity capital markets and trading capabilities typically associated with public offerings.

The announcement comes as tokenized securities gain traction across traditional finance. While tokenization has largely focused on private credit and Treasurys, companies are increasingly exploring blockchain-based infrastructure for public equities as well.

The collaboration builds on an existing relationship between the companies. Securitize, which provides blockchain infrastructure for tokenized real-world assets, went public through a merger with a special purpose acquisition company (SPAC) backed by Cantor Fitzgerald.

Related: Kraken acquires tokenization platform Magna ahead of potential IPO

Tokenized stocks attract Wall Street interest

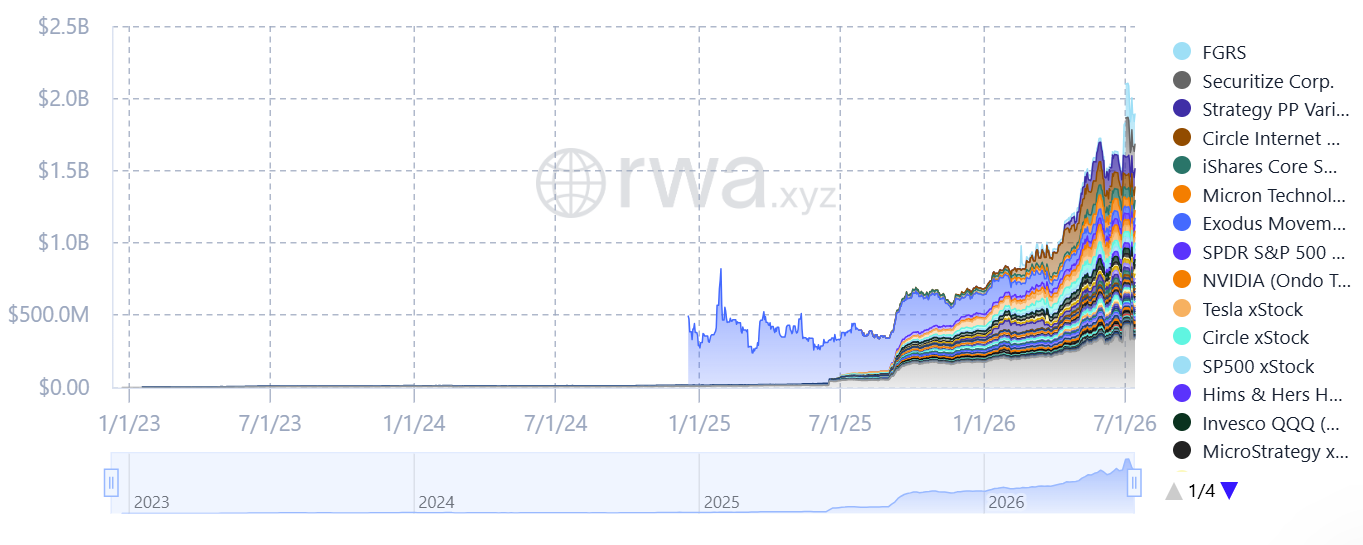

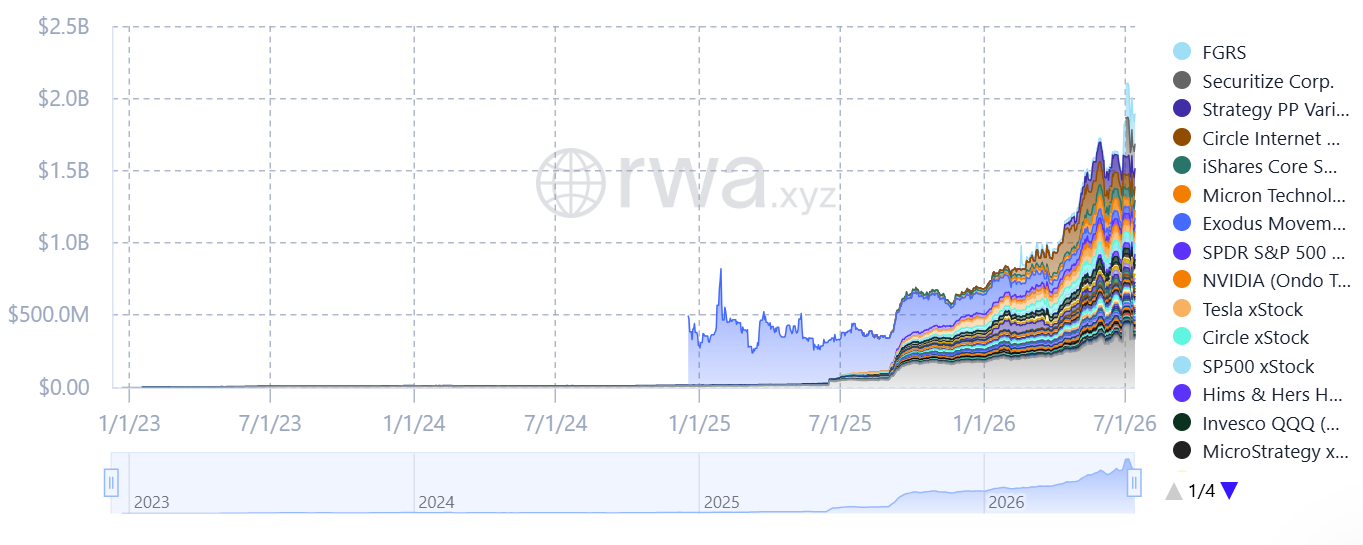

The market for tokenized stocks has expanded rapidly over the past year, outpacing much of the broader digital asset market. The value of tokenized stocks onchain has increased 16% over the past 30 days to nearly $1.9 billion, according to RWA.xyz.

The value of tokenized stocks has grown rapidly over the past year.

Source: RWA.xyz

The growth is drawing established financial institutions deeper into the sector. As The Wall Street Journal reported Wednesday, the Depository Trust & Clearing Corp. (DTCC) plans to pilot the tokenization of stocks and US Treasurys with nearly 40 financial companies, including JPMorgan and Goldman Sachs. The trial follows DTCC’s May announcement that it aims to roll out tokenized trading services by October.

Assets slated for tokenization include shares of Microsoft (MSFT) and stablecoin issuer Circle (CRCL), as well as exchange-traded funds tracking the S&P 500 index, the Nasdaq 100 index and short-term US Treasury bonds.

Related: US, UK treasuries to align transatlantic rules on tokenization and stablecoins

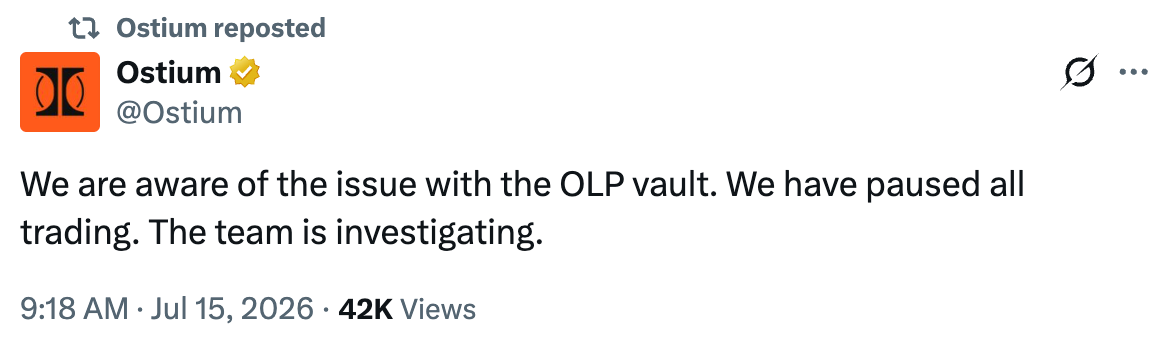

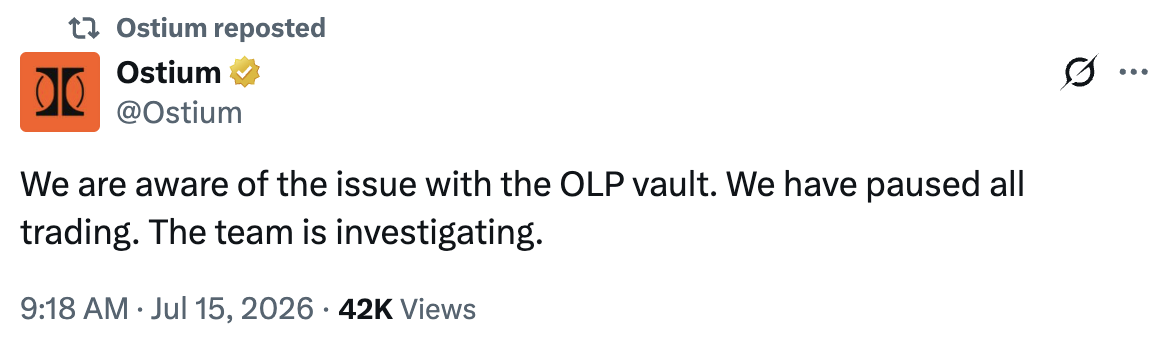

Decentralized trading protocol Ostium paused trading Wednesday after blockchain security firms Blockaid and CertiK reported an apparent exploit of its OLP liquidity vault.

Blockaid estimated the exploit resulted in roughly $18 million in losses, while CertiK placed the figure at about $22 million. Both firms attributed the incident to an apparent compromise of Ostium’s oracle system, which supplies external price data to the protocol.

Source: Ostium

Ostium announced on X that it paused all trading after identifying an issue affecting the vault. It subsequently said: “With user security being our first concern, we recommend that all users temporarily revoke approvals for our contracts until we can further investigate the recent incident.”

The protocol said its team is investigating and has not yet confirmed the cause of the incident or the estimated losses reported by blockchain security firms.

Built on Arbitrum, Ostium is an onchain perpetuals trading platform offering leveraged exposure to 75 trading pairs spanning stocks, ETFs, commodities, indices, foreign exchange and cryptocurrencies.

Source: CertiKAlert

Related: Crypto hacks fell 47% in H1 but ecosystem is no safer: CertiK

DeFi hacks remain persistent challenge

The incident is the latest in a series of high-profile attacks targeting decentralized finance protocols this year, despite broader efforts to strengthen security across the sector.

According to DeFiLlama, crypto hacks resulted in nearly $630 million in losses during April, the highest monthly total since February 2025. DeFi protocols accounted for the vast majority of those losses, with exploits at KelpDAO and Drift Protocol making up more than 80% of the month’s total.

Security researchers have said recent DeFi attacks increasingly target offchain infrastructure such as oracle systems, privileged access and key management rather than exploiting flaws in smart contracts alone.

The attacks have also fueled concerns about DeFi’s readiness for institutional adoption. In an April research note, JPMorgan analysts said bridge security remains a key challenge for the sector, raising questions about whether DeFi can scale to support broader institutional participation.

Industry executives have warned that shrinking DeFi yields are making security risks harder to justify. Speaking to Cointelegraph in May, the CEO of smart contract security firm Statemind and Symbiotic co-founder, Misha Putiatin, said institutions increasingly struggle to quantify hack risk, making them less willing to accept the sector’s returns despite growing interest in blockchain-based finance.

Magazine: Strategy became a symbol of the dot-com crash: Could history repeat?

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Institutional crypto OTC markets are evolving beyond block trades as firms demand liquidity, settlement, and cross-border infrastructure services.

Summary

- Institutional crypto OTC desks are evolving beyond block trades into full-service execution and settlement infrastructure.

- Growing institutional demand is reshaping crypto OTC desks into providers of execution, settlement, and treasury infrastructure.

- Crypto OTC markets are expanding beyond large trades as institutions seek integrated execution and liquidity solutions.

For most of its early history, the institutional crypto OTC market was defined by a single problem: how to move large blocks of Bitcoin or Ethereum without those orders moving the market against themselves. OTC desks existed to solve that problem, and the mechanics were straightforward. A desk aggregated liquidity across venues, quoted a price, and settled the transaction off-exchange. That was the value proposition, and for the institutions active in the market at the time, it was sufficient.

The market that exists today is considerably more complex. The institutions using OTC infrastructure now range from payment companies running millions of stablecoin conversions per month to sovereign wealth funds building digital asset exposure to regional exchanges managing fiat liquidity across multiple jurisdictions simultaneously. Their requirements go well beyond block execution, and the desks serving them have had to evolve accordingly. Understanding how that evolution unfolded and what it means for institutions evaluating OTC partners today is increasingly important as off-exchange activity accounts for a larger share of total institutional crypto volume.

From block trading to execution infrastructure

The original institutional OTC use case was straightforward: an investor wanted to acquire or liquidate a significant position in Bitcoin or Ethereum, and the depth available on public exchange order books at any given moment was insufficient to absorb the order without meaningful price impact. OTC desks solved this by aggregating liquidity from multiple venues simultaneously, executing the full position off-exchange at a single blended rate. The client received a cleaner outcome than exchange execution could deliver at a comparable size, and the desk managed the inventory risk.

As institutional participation broadened, the use cases multiplied faster than most desks anticipated. Payment companies discovered that stablecoin-to-fiat conversion at scale required the same off-exchange execution logic as block trades, but at far higher frequency and with much tighter settlement timing requirements. Mining operations needed to convert consistent production volumes without compressing spot prices on public markets. Funds allocating across a broader digital asset universe needed OTC access to assets with limited exchange liquidity. Each of these use cases placed different demands on OTC infrastructure, and the desks that grew with their clients were the ones that treated execution as a starting point rather than an end product.

The shift from block trading to execution infrastructure represents the most significant structural change in the institutional OTC market over the past several years. A desk operating as execution infrastructure is not just quoting prices on large orders. It involves managing settlement rails, maintaining credit relationships, operating compliance frameworks across multiple jurisdictions, and providing the reporting and operational integration that institutional treasury functions require. The technical and operational gap between a desk capable of this and one that handles only straightforward block trades is substantial.

Settlement as the real differentiator

Among the structural changes in institutional OTC, none has been more consequential than the shift in how clients evaluate settlement capability. For the first generation of institutional OTC clients, settlement was binary: did the transaction complete, and did it complete accurately? Speed was a secondary consideration because the use cases did not require it.

For the current generation of institutional users, settlement infrastructure is often the primary criterion for evaluation. Payment companies and fintechs running real-time stablecoin conversion flows cannot absorb settlement delays lasting hours. Treasury operations managing liquidity across multiple jurisdictions in different time zones need finality that is reliable rather than probabilistic. Regional exchanges facilitating local fiat pairs need settlement rails that are actually present in their markets rather than routing through correspondent banking chains that add latency and introduce clearing risk.

The desks that have responded to this have built onshore banking infrastructure across the regions where their clients operate, rather than relying on cross-border correspondent relationships to approximate regional settlement. The operational investment required to do this genuinely, with actual banking licenses, compliance infrastructure, and local operational presence, is one of the more significant barriers to entry in the institutional OTC market today. Recent developments reinforce why this matters: central banks moving to blockchain-based settlement rails is raising the baseline of what institutional settlement infrastructure is expected to deliver, making the gap between desks with genuine regional presence and those with nominal coverage more consequential. It is also one of the reasons that headline spread comparisons between desks are increasingly insufficient as an evaluation framework. A desk offering tight spreads with slow or uncertain settlement is, in practice, more expensive than one offering slightly wider spreads with second-level finality across all relevant markets.

The role of multi-venue aggregation in modern OTC execution

Multi-venue aggregation has always been part of the OTC value proposition, but how it is executed and the depth at which it operates have changed considerably as the crypto market structure has matured. In the early institutional OTC market, aggregation across a handful of major exchanges was sufficient to source competitive pricing on the assets clients needed. As the asset universe expanded and trading activity was distributed across more venues globally, connectivity requirements grew accordingly.

The practical implication is that the quality and quantity of multi-venue aggregation have become a primary differentiator among OTC desks, rather than just a baseline capability. A desk with deep connectivity across a broad network of exchanges can source liquidity and lock pricing for a wide range of digital assets simultaneously, giving clients certainty on the rate before execution begins, regardless of where the underlying liquidity happens to be distributed at that moment. The infrastructure required to deliver this, low-latency connections to a large number of venues, real-time pricing engines operating across all of them, and price-locking mechanisms that hold the rate through execution, represents a meaningful operational investment that separates the leading desks from the rest of the market.

Counterparties offering crypto OTC trading at this level of infrastructure depth provide a fundamentally different execution environment than lighter-touch alternatives. The difference is not primarily visible in a standard spread comparison. It shows up in execution consistency across a wide range of assets, in settlement reliability during volatile market conditions, and in the operational continuity that high-frequency clients depend on when their own business processes are built around it.

Emerging market demand and what it requires

One of the more underappreciated developments in institutional crypto OTC over the past few years has been the expansion in demand from emerging-market participants. Exchanges operating in Southeast Asia, Latin America, and MENA now represent a significant and growing share of institutional OTC activity, and their requirements are specific enough to constitute a distinct market segment rather than a geographic variation of the same use case.

The core challenge for emerging market participants is not execution pricing. Spreads on major pairs are competitive across most institutional desks. The challenge is regional settlement: reliably getting fiat in and out of local markets at speed, without the correspondent banking dependencies that introduce unpredictable latency. An exchange in Southeast Asia managing local fiat pairs needs a counterparty that can settle in the local market in seconds, not one that routes through a chain of correspondent banks and delivers settlement on the following business day.

This requirement has pushed institutional OTC desks toward genuine regional operational presence as a competitive necessity rather than a growth aspiration. The desks with onshore banking infrastructure and compliance frameworks in the markets where their emerging-market clients operate can serve this segment in ways those without it simply cannot replicate at the service levels these clients require. As emerging market institutional participation continues to grow, this regional operational depth is likely to become one of the most important factors in OTC counterparty selection.

How institutional clients are evaluating OTC desks today

The evaluation framework that institutional clients apply to OTC desks has become considerably more sophisticated as their use of OTC infrastructure has deepened. The clients who are now moving the most volume through OTC desks, payment companies, active trading operations, exchanges, and large fund managers have developed detailed views of what genuinely capable infrastructure looks like, and they apply those views when selecting or reviewing counterparties.

Settlement speed and regional coverage have already been discussed, but two additional dimensions are worth examining. Capital structure, specifically whether the desk operates on its own balance sheet or relies on borrowed inventory, shapes how risk is distributed within the arrangement and has direct implications for same-day settlement capability and credit availability. Desks operating on their own institutional capital can hold inventory, extend credit facilities to eligible counterparties, and absorb the timing differences between client execution and position management. These capabilities underpin the kind of operational reliability that high-frequency clients require.

Reporting and integration capability have also emerged as significant evaluation criteria for institutional treasury operations. Clients running high transaction volumes need real-time, granular visibility into execution quality, API integration that removes manual steps from the execution workflow, and operational transparency that enables their finance teams to accurately account for every transaction. Desks that treat reporting as an afterthought are increasingly unsuitable for the more sophisticated segment of the institutional OTC market, regardless of how competitive their pricing appears.

Where the institutional OTC market is heading

Several structural trends are likely to shape institutional crypto OTC over the coming years. Stablecoin adoption by major financial institutions is already changing the settlement economics of cross-border institutional flows, and OTC desks positioned within that infrastructure are likely to see volume growth that differs structurally from traditional block-trading demand. Visa’s CFO recently outlined how stablecoin settlement is reshaping institutional payment infrastructure, a signal that stablecoin-denominated settlement is moving from an emerging capability to an operational expectation across a significant segment of institutional payment flows, with direct implications for the OTC desks serving those clients.

Regulatory development across key markets is creating both clarity and new compliance requirements for institutional OTC operations. Desks with the compliance infrastructure to operate across multiple regulated jurisdictions are better positioned to serve the institutional segment as regulatory frameworks mature, while those without it face increasing friction in markets where institutional participation is growing fastest.

The consolidation dynamic evident in the institutional OTC market over the past few years is likely to continue. The operational investment required to maintain competitive execution infrastructure across a broad asset universe, genuine regional settlement capability, and the compliance frameworks that institutional clients now require is substantial. The desks that have built this infrastructure are pulling further away from those that have not, and the evaluation gap between them is becoming more visible to institutional clients with each passing cycle.

What this means for institutions evaluating OTC partners

The evolution of institutional crypto OTC from a block-trading service to a genuine financial infrastructure has significant implications for how institutions should approach counterparty evaluation. A framework built around spread comparison was adequate when OTC desks were doing a simpler job. It is insufficient for evaluating the kind of operational relationships that institutional crypto participation now requires.

The institutions best positioned in this market have treated their OTC counterparty decision as a strategic infrastructure choice rather than a transactional one, selecting partners with the settlement depth, regional presence, capital structure, and operational integration capability to support their business as it scales. The quality of that decision tends to compound over time. The desks with the right infrastructure today are the ones whose clients transact the most volume, and the gap between them and lighter alternatives is becoming harder to close from the outside.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Peter Schiff renewed his long-running criticism of Bitcoin (BTC) on the July 15 episode of “The Peter Schiff Show,” arguing that investors who hold the asset near its current price will eventually regret not selling, as he expects another major decline.

He also questioned Strategy’s decision to sell $450 million in common stock rather than touch its BTC holdings, saying it shows how boxed Michael Saylor’s company has become.

Schiff Lays Out His Bitcoin Case, and Takes Another Shot At Saylor

In the podcast, Schiff admitted that Bitcoin has been surprisingly resilient despite what he believes are growing risks beneath the surface. The economist said that he regretted not buying BTC when he first heard of it 15 years ago, but watching the asset in the last few years had tempered that regret.

“I don’t regret not buying it three, four, five years ago,” he told listeners. “But yeah, 15 years ago, sure, I should have bought it.”

However, he claimed that those who currently hold the OG crypto and still refuse to sell will soon rue their choice. Referring to the cryptocurrency’s current trading range, he argued that there is resistance around $65,000 while support is near $58,000. According to him, if that level fails, Bitcoin could fall below $50,000 before eventually hitting rock bottom at $30,000 or even $20,000.

‘The people who don’t sell it now, they’re going to be the ones that are going to have a lot of regrets,” he warned.

At the time of writing, CoinGecko data showed that BTC was trading a couple hundred bucks under $65,000, having gone up nearly 4% following the release of lower-than-expected US CPI numbers.

The economist then turned to another of his pet subjects, Strategy, which he noted had gone three straight weeks without buying Bitcoin and hadn’t sold any either since disposing of 3,588 BTC last week. Instead, Saylor’s firm raised $450 million through a common stock sale, pushing up its cash reserves to $3 billion, all while the stock traded at a huge discount to the value of its Bitcoin.

Schiff called it a needless dilution and argued that Strategy had avoided selling BTC only because doing so would tank the cryptocurrency’s price.

“Saylor knows if he starts really selling Bitcoin, the price is going to crash,” he claimed. “Now, the problem is it’s going to crash anyway because the market realizes the bind he’s in, and even if he doesn’t sell the market is going to crash out from under him.”

Corporate Treasury Debate In Focus

Schiff’s criticism has come at a time when analysts are reassessing the corporate Bitcoin accumulation story, of which Strategy is the biggest player. According to a recent report from QCP Capital, when Saylor’s firm sold some of its Bitcoin for the first time in late May, the amount, though small (32 BTC out of an over 847,000 BTC stash), still changed the way investors looked at such companies.

Many of them are now paying more attention to their cash reserves, equity issuances and the funding conditions of such operations to determine whether future purchases remain sustainable instead of just being swept away by the latest headline-grabbing buys.

The post Peter Schiff: Bitcoin Holders Will Soon Regret Not Selling at Current Levels appeared first on CryptoPotato.

South Korea Moves to Treat Crypto as National Wealth Under New Law

England-Argentina live: Kane and Messi battle for World Cup final spot

Concept of new indian plastic note of 50 rupees #money #moneysavingidea #shorts

-

Fashion6 days ago

Fashion6 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Sports6 days ago

Sports6 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports5 days ago

Sports5 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Tech6 days ago

Tech6 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

Politics6 hours ago

Politics6 hours agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

News Videos23 hours ago

News Videos23 hours agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech2 days ago

Tech2 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Tech22 hours ago

Tech22 hours agoDark Secrets Emerge When Jailbreaking LLMs

-

News Videos7 days ago

News Videos7 days agoCrypto Just Entered Its Most Important 6-Month Candle (Could Decide Everything!)

-

Tech6 days ago

Tech6 days agoLevel Infinite Launches Gangstar Mirage City in India with Pre-Registrations

-

NewsBeat6 days ago

NewsBeat6 days agoMajor update after Huntingdon train attack as man enters plea

-

News Videos2 days ago

News Videos2 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Tech2 days ago

Tech2 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

Entertainment1 hour ago

Entertainment1 hour agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

Tech7 days ago

Tech7 days agoEntra passkey enrollment vishing targets Microsoft 365 users

-

Crypto World7 days ago

Crypto World7 days agoDeFi Dashboard Zapper to Shut Down After 7 Years

-

Crypto World1 day ago

Ripple, Coinbase, Circle Join Linux x402 Foundation to Help Shape AI Payments

-

Crypto World7 days ago

Crypto World7 days agoMark Cuban-Backed DeFi Dashboard Zapper Shuts Down After 7 Years

-

Tech6 days ago

Tech6 days agoClaude’s New Reflect Dashboard Wants To Help You Log Off Of Claude

You must be logged in to post a comment Login