Crypto World

What is a digital commodity? CLARITY Act explained

Whether a token is a security or a commodity decides almost everything about how it can be traded, listed, and held in the U.S. In March 2026 regulators called sixteen major tokens “digital commodities,” but only on interpretive footing a future administration could undo. The CLARITY Act would turn that label into law. Here is what a digital commodity actually is, and how the bill would reclassify crypto.

Summary

- A digital commodity is a crypto asset whose value comes from the workings of a functional blockchain and from supply and demand, not from the expectation of profit from a company’s managerial efforts.

- The distinction matters enormously: a security falls under the securities regulator’s heavy registration and disclosure regime, while a commodity falls under the commodities regulator’s lighter-touch oversight.

- In March 2026 the SEC and CFTC jointly classified sixteen major tokens, including Bitcoin, Ethereum, XRP, and Solana, as digital commodities, but that was an interpretation, not a law, and a future administration could reverse it.

- The CLARITY Act would write the digital-commodity category into federal statute, making the classification durable, and create a maturity test that lets a token move from security to commodity as its network decentralizes.

- Reclassification changes what products can be built, especially exchange-traded funds, how exchanges list assets, how institutions hold them, and how much investor protection applies.

A digital commodity is a crypto asset whose value comes from the workings of its blockchain and from supply and demand, rather than from the promised efforts of a company or team, which is the legal distinction that places it under the lighter-touch oversight of the commodities regulator instead of the heavier hand of the securities regulator. That sentence contains the entire stakes of one of the most consequential questions in crypto: for any given token, is it a security or a commodity. The answer determines which federal agency has authority over it, what financial products can be built around it, how exchanges can list it, whether large institutions can comfortably hold it, and how aggressively the government can act against the people who issue and trade it. For more than a decade, the U.S. had no clear way to answer that question for most tokens, leaving the entire industry in a gray zone, and the fight over how to draw the line, and who gets to draw it, has shaped the regulation of crypto in America more than any other issue.

In 2026 that long-running question reached a turning point on two fronts at once, and understanding both is essential to understanding what a digital commodity is and why it matters. On the regulatory front, the two relevant agencies, the securities regulator and the commodities regulator, took the unprecedented step of jointly declaring sixteen major tokens to be digital commodities, ending years of ambiguity for those specific assets. On the legislative front, Congress has been working on the CLARITY Act, a bill that would take the digital-commodity concept and write it into permanent federal law, with a mechanism for deciding which tokens qualify and how a token can move from one category to another over time. This guide explains what a digital commodity actually is, why the security-versus-commodity distinction decides so much, the test at the heart of classification, what the 2026 regulatory interpretation did and why it was not enough on its own, how the CLARITY Act would reclassify crypto by statute, the clever maturity mechanism that lets a token change categories, what reclassification practically changes, and the real limits and risks that remain.

What a digital commodity actually is

Start with the precise definition, because the legal language is doing specific work. A digital commodity, in the formulation regulators have adopted, is a crypto asset that is intrinsically linked to and derives its value from the programmatic operation of a functional crypto system, as well as from supply and demand dynamics, rather than from the expectation of profits from the essential managerial efforts of others. That is a dense sentence, so it helps to unpack it: the key idea is the source of the asset’s value. A digital commodity is valuable because of how its blockchain works and because of ordinary market forces of supply and demand, not because some company is promising to do work that will make the token go up.

Crucially, regulators have added that a digital commodity does not carry intrinsic economic rights such as generating a passive yield or conveying a claim on the future income, profits, or assets of a business, which is exactly the kind of feature that would make something look like a security. The contrast that makes this concrete is the traditional commodity. Think of oil, wheat, or gold: these are produced by many different parties around the world, not issued by a single company to raise money for itself, and one unit is interchangeable with another, so one barrel of a given grade of oil is worth the same as any other. Their value comes from supply and demand and from their inherent usefulness, not from anyone’s promise of profit.

Regulators have long treated Bitcoin the same way, reasoning that it is produced by many disparate miners around the world, is fungible, and has no central issuer making promises, which makes it commodity-like rather than security-like. The digital-commodity category extends that logic to other tokens whose networks are sufficiently decentralized and functional that no central enterprise is driving their value through promised efforts. A digital commodity, then, is the crypto equivalent of gold or oil instead of the crypto equivalent of a company’s stock. That single distinction is what determines how it is regulated.

Security or commodity: the question that decides everything

To see why this classification carries such weight, you have to understand how differently the two categories are regulated. Securities, which include stocks and bonds, fall under the securities regulator, whose regime is built around investor protection through heavy obligations: companies issuing securities must register their offerings, provide extensive ongoing disclosures, and operate within a tightly controlled system of registered broker-dealers and exchanges, all backed by the threat of enforcement for non-compliance. The logic is that when people invest money expecting profit from someone else’s efforts, they need protection and information, so the law imposes a demanding framework. Commodities, by contrast, fall under the commodities regulator, whose regime is far lighter.

The commodities regulator oversees the derivatives markets for commodities, such as futures and options, and can pursue fraud and manipulation, but it does not impose the same registration-and-disclosure burden on the underlying asset. It also has limited direct authority over spot markets where commodities are bought and sold for immediate delivery, which is why the jurisdictional split codified by the CLARITY Act matters so much. The practical consequences of which bucket a token lands in are enormous, which is why the industry has fought over classification for years. If a token is a security, its issuer faces registration and disclosure requirements, the exchanges listing it face securities-law obligations, and institutions weighing whether to hold it confront the heavier compliance and restrictions that come with securities.

If the same token is a commodity, those burdens largely lift: listing is easier, compliance is lighter, and the path to building products around it, especially exchange-traded funds, becomes far more direct. Classification also determines which regulator writes the rules, who pays which fees, how custody is handled, and how much room institutions have to participate. Calling a token a security or a commodity is not a technicality; it is a decision that shapes whether a project can operate smoothly in the U.S. or faces a wall of regulatory friction. It also influences the token’s accessibility to the institutional capital that can move its price, which is why the definition of a digital commodity, and the process for deciding which tokens qualify, became one of the central battles in crypto policy.

The Howey test and the efforts of others

At the heart of the security-versus-commodity question sits a legal test that has governed it for decades: the Howey test. Derived from a Supreme Court case, the Howey test defines an investment contract, which is a type of security, as an investment of money in a common enterprise with an expectation of profits derived from the efforts of others. That last phrase, the efforts of others, is the crux. If you buy a token primarily because you expect a company or team to do work that will increase its value, the arrangement looks like a security, because your profit depends on their efforts.

If, instead, the token’s value comes from a decentralized network and market forces with no central party whose efforts you are relying on, it looks more like a commodity. The Howey test is why the same token can be treated differently depending on how it is sold and how mature its network is. This is also where one of the most important and confusing features of crypto classification comes from: a token’s status is not necessarily permanent. The Howey analysis depends on facts that can change as a project evolves.

A token might begin its life as a security, sold by a founding team to raise money for a network that does not yet exist, where buyers are clearly relying on the team’s efforts. Over time, if the network becomes genuinely functional and decentralized, with no central team driving its value, the same token can stop looking like a security and start looking like a commodity, because the efforts-of-others element fades away. This transition is the key conceptual move that everything else builds on, and it explains why regulators and lawmakers have struggled to draw clean lines: the line itself moves as a project matures. The 2026 regulatory interpretation adjusted the Howey analysis for crypto by requiring that an issuer affirmatively make representations or promises about its essential managerial efforts for there to be an investment contract, which sharpened the test in a way favorable to treating mature, decentralized tokens as commodities.

The March 2026 interpretation: a label, not a law

In March 2026 the security-versus-commodity question got its most significant answer yet, though an incomplete one. The securities regulator and the commodities regulator, which had spent years disagreeing over jurisdiction, jointly issued a formal interpretation that, for the first time, set out an agreed framework for classifying crypto assets. The interpretation sorted crypto into a taxonomy of categories, most of which are not securities: digital commodities, digital collectibles such as certain non-fungible tokens, digital tools that perform a utility function like membership or access, stablecoins, which sit in their own lane governed by separate stablecoin legislation, and digital securities, the one category that clearly is a security. Within that framework, the agencies named sixteen major tokens as examples of digital commodities, including Bitcoin, Ethereum, Solana, and XRP, alongside others such as Cardano, Litecoin, and even some memecoins, explicitly declaring that these assets are not securities and that their spot trading falls primarily under the commodities regulator.

This was a landmark moment, the first time the two top financial regulators agreed in writing on how to treat these assets, and it brought real clarity to the named tokens. But it carried a critical limitation that defines why the story does not end there. The interpretation is exactly that, an interpretation: a statement of how the agencies read existing law, binding on the agencies themselves in how they administer the law, but not a new statute passed by Congress. That distinction matters enormously, because an interpretation issued by agencies can be modified or reversed by those same agencies under a future administration.

The clarity it provides is real but conditional, resting on the current regulators’ chosen reading instead of on durable law. This is precisely why, even as the industry welcomed the interpretation, many participants, and even one of the regulators involved, called for Congress to act, because only legislation can turn a reversible interpretation into permanent law. Stablecoins sit in their own separate lane, which is why the law governing the stablecoin category matters alongside the CLARITY Act rather than inside the same commodity bucket. Digital securities, meanwhile, remain a separate class, and the rise of the digital-securities category shows why not every on-chain asset belongs under commodity-style treatment.

How the CLARITY Act reclassifies crypto

The CLARITY Act, formally the Digital Asset Market Clarity Act, is the legislative effort to take the digital-commodity concept and write it into federal statute, giving it the permanence the 2026 interpretation lacks. The bill would create a statutory framework that sorts digital assets into categories and assigns them to regulators, with digital commodities placed under the commodities regulator and securities remaining with the securities regulator. In doing so, it would codify the jurisdictional split that the interpretation expressed, so that the division of authority between the two agencies rests on law instead of on an agreement that could be undone. A companion measure moving through the agriculture committee, sometimes called the Digital Commodity Intermediaries Act, would give the commodities regulator formal jurisdiction over the spot markets for digital commodities, addressing the long-standing gap in which that regulator could oversee derivatives but had limited authority over everyday spot trading.

The conceptual heart of how the CLARITY Act reclassifies crypto is a principle of separating the asset from the way it is offered and sold. Under this approach, the act recognizes that a token can be sold in a transaction that is an investment contract, and therefore a security at the point of that sale, while the underlying token itself can be a digital commodity. This separation is what allows the law to handle the awkward reality that the same token can look like a security in one context and a commodity in another. It means the securities regulator retains authority over primary-market fundraising, when a project first sells tokens to raise capital and buyers are relying on the team’s efforts, as well as over assets that truly function as investment contracts, while the commodities regulator takes over the secondary-market trading of digital commodities once a token’s network is mature.

By writing this structure into statute, the CLARITY Act would replace the case-by-case, lawsuit-driven approach of the past, in which classification was fought out one enforcement action at a time, with a predictable framework that issuers and exchanges can read in advance. That shift, from regulation by enforcement to regulation by clear rule, is what the industry treats as the bill’s central promise. It is also why the bill’s contested path matters so much: until the bill becomes law, the digital-commodity framework remains partly dependent on agency interpretation rather than statutory permanence. The category may now be easier to understand, but it still needs Congress to make it durable.

The maturity test: how a token moves from security to commodity

The cleverest and most important mechanism in the CLARITY Act is the one that lets a token change categories as its network matures, because it directly addresses the moving-line problem that Howey created. The bill creates a maturity test, a set of criteria for determining when a blockchain system has become decentralized and functional enough that its token should be treated as a digital commodity instead of as part of a securities offering. The underlying idea follows directly from the efforts-of-others principle: a token sold early in a project’s life, when a central team is building the network and buyers are betting on that team’s success, fits the securities framework. Once the network is truly up and running and no longer dependent on a central group’s managerial efforts, the justification for securities treatment fades, and the token can graduate to commodity status.

This creates what is sometimes called a maturity on-ramp, a path by which a token can begin under securities oversight and, as its network decentralizes and meets the maturity criteria, transition to commodity oversight. The criteria for maturity center on decentralization: roughly, whether the system operates without any single person or affiliated group exercising outsized control over the network or its value, whether it is functional, and whether its governance and operation are truly distributed. A blockchain that meets the test is treated as mature, and its native token is treated as a digital commodity. This mechanism is what makes the CLARITY Act more sophisticated than a simple fixed list of which tokens are commodities.

Instead of freezing classifications in place, it provides a rule for how a token earns commodity status by becoming the kind of decentralized network that commodity treatment is meant for. It is also, as the limits section notes, one of the most contested parts of the bill, because deciding exactly how decentralized is decentralized enough is truly difficult, and the definition the bill uses has been criticized from multiple directions. But the basic design, a test that lets status follow the reality of a network’s maturity instead of being fixed at launch, is the conceptual engine of how the CLARITY Act would reclassify crypto. It gives projects a legal path from fundraising-stage oversight to mature-network treatment, rather than forcing every dispute into the courts.

What reclassification actually changes

For everyday holders and for the market, the abstract question of classification translates into concrete consequences, so it is worth being specific about what changes when a token is treated as a digital commodity. The most immediate effect is on financial products, above all exchange-traded funds. An asset classified as a commodity follows a far more direct regulatory path to a spot ETF than a security does, which is why the digital-commodity designation has been linked to a surge of pending ETF applications across many tokens. For an investor, this matters because spot ETFs are often the most convenient and trusted way for both retail and institutional money to gain exposure to an asset, so commodity status can widen access and bring in new demand.

Reclassification also eases how exchanges list a token, since listing a commodity does not carry the securities-law obligations that listing a security does, and it lowers the compliance burden across the board. The change extends to institutions and to specific crypto activities. Large institutions, including asset managers and pension funds, generally face fewer restrictions holding commodity-classified assets than security-classified ones, so commodity status can unlock institutional participation that securities treatment would discourage. The 2026 interpretation also clarified that certain activities long shadowed by securities-law uncertainty, including protocol staking and the wrapping of tokens, are not in themselves securities transactions when conducted within defined boundaries, which removed legal risk that had pushed some platforms to suspend staking services.

To make the journey concrete, consider a token’s path under this framework: it might launch through a sale that is an investment contract, a security at that moment, with its issuer subject to securities obligations. Then, as its network grows decentralized and functional and meets the maturity test, the token itself comes to be treated as a digital commodity, its spot trading moves under the commodities regulator, exchanges can list it more easily, an ETF becomes feasible, and institutions grow more comfortable holding it. That arc, from security at birth to commodity at maturity, is the practical shape of what the CLARITY Act’s reclassification is designed to enable. It is why the industry views statutory clarity as the gateway to the next phase of adoption.

Limits, risks, and what is still unsettled

For all its significance, the digital-commodity framework comes with real limits and unresolved tensions that an honest account must address. The first and most important is the gap between interpretation and law. The 2026 classification of sixteen tokens as digital commodities is an agency interpretation, binding on the agencies but reversible by a future administration, which means the clarity it provides is conditional instead of permanent until Congress acts. And the legislation meant to make it durable, the CLARITY Act, has not become law; it has advanced through the House and a Senate committee but still faces a contested path, so the statutory permanence the industry wants is not yet secured.

Beyond the interpretation-versus-statute problem, several substantive concerns persist. The definition of decentralization at the core of the maturity test is truly hard to pin down, and critics argue the version in play is too narrow or too vague, which could lead to inconsistent or contestable classifications. There is a meaningful investor-protection tradeoff: moving an asset out of the securities regime and into the commodity regime means lighter disclosure requirements and fewer of the protections securities law provides, which supporters see as appropriate for decentralized assets but critics warn could leave holders more exposed, particularly because crypto can be more susceptible to manipulation than registered securities and direct crypto holdings do not carry the same regulatory safeguards. Classification can also remain context-dependent: even a token treated as a commodity in secondary trading could be part of a securities transaction if it is later sold subject to an investment-contract arrangement promising profits.

The whole area remains politically contested, with the CLARITY Act facing objections over its decentralized-finance provisions, its treatment of stablecoin yield, and ethics questions, any of which could reshape or stall it. The honest summary is that the digital-commodity category represents real and welcome progress toward clarity, but it currently stands on reversible interpretive ground, depends on legislation that has not passed, relies on a maturity test that is hard to define, and carries genuine investor-protection tradeoffs. It is a meaningful step in defining how crypto is regulated, not a finished or settled answer.

Frequently asked questions

What is a digital commodity in simple terms?

A digital commodity is a crypto asset whose value comes from how its blockchain works and from ordinary supply and demand, instead of from a company promising to do work that makes the token go up. That makes it the crypto equivalent of gold or oil instead of a company’s stock. Because no central enterprise is driving its value through promised efforts, it is treated like a commodity under the lighter-touch commodities regulator instead of as a security under the heavier securities regulator. Regulators have long treated Bitcoin this way and, in 2026, extended the label to other sufficiently decentralized tokens such as Ethereum, XRP, and Solana.

Why does it matter whether a token is a security or a commodity?

Because the two are regulated completely differently, and the difference shapes nearly everything. A security falls under the securities regulator’s heavy regime of registration, disclosure, and trading restrictions designed to protect investors. A commodity falls under the commodities regulator’s far lighter regime, which oversees derivatives and pursues fraud but imposes much less burden on the underlying asset. Commodity status makes a token easier to list, lighter to comply with, more accessible to institutions, and far closer to qualifying for a spot exchange-traded fund.

Which cryptocurrencies are digital commodities?

In March 2026 the securities and commodities regulators jointly named sixteen major tokens as examples of digital commodities, including Bitcoin, Ethereum, Solana, and XRP, along with others such as Cardano, Litecoin, Stellar, and some memecoins. The list was described as not closed, meaning other assets could qualify. The common thread is that these tokens derive their value from decentralized, functional networks instead of from a central team’s promised efforts. It is important to note this came from an agency interpretation instead of a law, so while it gave real clarity to those tokens, the classification rests on interpretive footing that could change until Congress passes durable legislation.

How does the CLARITY Act reclassify crypto?

The CLARITY Act would write the digital-commodity category into federal statute, placing digital commodities under the commodities regulator and securities under the securities regulator, codifying the jurisdictional split so it rests on law instead of a reversible interpretation. Its key mechanism is separating the asset from how it is sold: a token can be sold in a securities transaction while the underlying token is a digital commodity. The securities regulator keeps authority over fundraising and genuine investment contracts, while the commodities regulator takes over secondary trading of mature digital commodities. This replaces the old case-by-case enforcement approach with a predictable, statutory framework.

What is the maturity test?

The maturity test is the CLARITY Act’s mechanism for letting a token move from security to commodity as its network matures. The idea follows from the principle that a token sold early, when a central team is building the network and buyers rely on that team’s efforts, fits the securities framework, but once the network is truly decentralized and functional, no longer dependent on a central group, the token can graduate to digital-commodity status. The criteria center on decentralization: whether any single person or group exercises outsized control, whether the system is functional, and whether its operation is truly distributed. It creates a maturity on-ramp instead of freezing a token’s status at launch, though defining decentralization precisely remains contested.

Is a digital commodity safer or less regulated than a security?

It is less heavily regulated, which cuts both ways. Commodity status means lighter compliance, easier listing, and broader access, which the industry views as appropriate for decentralized assets and a driver of adoption. But it also means fewer of the disclosure requirements and investor protections that securities law provides, so holders may be more exposed, particularly because crypto can be more susceptible to manipulation than registered securities and direct crypto holdings lack the same safeguards. Commodity status is also not a permanent, blanket shield, since a token could still be part of a securities transaction if later sold with profit promises.

This article is educational information, not legal, financial, or tax advice. The classification of crypto assets, the status of the 2026 regulatory interpretation, and the progress of the CLARITY Act reflect information available as of June 28, 2026, and can change. Regulatory classifications can be modified, and the legal treatment of any specific token may differ by context and jurisdiction. Verify current details from primary sources and consult a qualified professional before making any decision.

Nvidia stock price keeps sliding, yet the usual dip buyers are missing. Institutional money flow on the stock is the most negative of any major chip name, which means big investors are stepping back instead of loading up.

That single fact reframes the whole selloff. A falling price normally pulls in bargain hunters. This time, the money is leaving Nvidia and moving elsewhere inside the same sector, and the reasons explain why the dip keeps failing.

Institutions are Leaving Nvidia, Not the Chip Sector

Across the major semiconductor names, Nvidia (NVDA) shows the deepest negative reading on the 20-day Chaikin Money Flow, near -0.19. Micron (MU) is one of the few stocks in the group still being accumulated.

In plain terms, this indicator works as a proxy for institutional money. Nvidia’s deep negative score means institutional money isn’t choosing this chip stock.

Because the selling is specific to Nvidia, the price split is stark. The stock is up only about 2.6% so far in 2026 and has slipped roughly 18% from its May peak.

Measured against the semiconductor index, Nvidia scores just 52.9 on relative strength, where 100 means keeping pace with the sector.

In plain terms, the chip index has nearly doubled over the past six months while Nvidia has gone almost nowhere. So the sector is not breaking. One company is, which is why its chart signals turned bearish while peers rose.

Positioning agrees. In early June, Nvidia director Mark Stevens sold about 1 million shares worth roughly $221 million, one of several insider sales that month. That is the setup. The next question is: where did the money go?

Why the Money is Rotating Elsewhere

The capital from Nvidia went mostly into the memory sector. Micron recently posted record revenue of $41.46 billion, up 346% in a year, and the stock jumped about 15% immediately after.

It also guided next-quarter sales near $50 billion, well above forecasts. The Micron stock forecast is now one of the hottest on Wall Street.

Here is the simple version. Micron makes the memory chips that feed Nvidia’s processors, and that memory is in short supply. Its entire HBM (specialized AI memory) is sold out, and prices keep climbing. So big money chased it.

The Micron stock price has roughly tripled this year, and Micron even briefly passed Meta in value. Investors did not quit chips. They moved one step over, from Nvidia to its supplier.

Nvidia’s Biggest Customers Are Now Its Rivals

The second reason runs deeper. Nvidia’s largest buyers are building their own chips. Alphabet now sells its in-house AI chips to outside customers, and Anthropic plans to spend about $200 billion with Alphabet over five years.

In short, the giant cloud firms that buy the most Nvidia chips need fewer of them once they make their own. Citizens analyst Andrew Boone estimates Alphabet’s chip business could grow from about $3 billion in 2026 to $25 billion in 2027.

That is why investors doubt Nvidia can keep charging top prices, a worry tied to the wider AI spending surge and Wall Street’s caution on the stock.

Why Wells Fargo Cutting Its Nvidia Target Makes Sense Now

Put those causes together and one earlier move suddenly fits. The buy ratings have not changed. Nvidia still holds a Strong Buy consensus, with 37 buy ratings, one hold, and no sells over the past month, and an average target near $309.

But the ceiling is dropping. On June 1, Wells Fargo analyst Aaron Rakers cut his Nvidia target from $375 to $315 while keeping his buy rating. Across the desk, the Wall Street price target picture shows buyers stepping aside even as ratings stay green.

That combination is the rotation in a single data point. Analysts still like the business, so they hold the rating. They no longer trust the premium, so they cut the number. A target trim that looked odd in isolation makes sense once you see the money already leaving.

What It Takes for Institutions to Come Back

None of this means Nvidia is broken. Revenue is still growing fast, Blackwell demand looks strong, and the forward price-to-earnings (P/E) has slipped to roughly 20 times earnings, cheap next to several AI peers.

In plain terms, that means investors pay about $20 for every $1 of profit the company is expected to earn over the next year, a low price for a top AI name.

Wedbush keeps a $330 target and calls the selloff a buying chance.

That is the tension. Fundamentals look excellent, yet the flow points the other way, and flow is what moves price now. While the money flow stays this negative, each dip is more likely to meet sellers than buyers.

The first real signal of a turn would be Chaikin Money Flow returning to accumulation. Until that happens, Nvidia is no longer the default chip stock, and the smart money is shopping elsewhere in the aisle.

The post Smart Money is Leaving Nvidia for This AI Chip Stock appeared first on BeInCrypto.

Breez, a Bitcoin-focused infrastructure company, has updated its developer toolkit with a capability to send stablecoins—specifically USDC and USDT—across more than 30 blockchain networks while using a Bitcoin balance as the only funding source.

The integration, described in an announcement shared with Cointelegraph, combines Lightning Network routing with automated conversion so users can effectively pay in stablecoins without separately acquiring or holding USDC/USDT on the destination chain.

Key takeaways

- Breez’s new SDK feature routes payments from a Bitcoin balance to USDC or USDT on over 30 networks without requiring users to hold stablecoins.

- The system uses the Lightning Network plus automated conversion to move value into stablecoins before delivering it to the recipient’s chosen chain.

- Breez says the approach is non-custodial and currently supports only outbound stablecoin payments.

- Lightning addresses and supported stablecoin networks are handled via “interoperability,” according to Breez.

- Liquidity providers named by Breez include Flashnet and Boltz, which perform the conversion and settlement on the target blockchain.

How Breez enables stablecoin payments from Bitcoin

In practice, developers using the Breez SDK can prompt users to enter a recipient’s wallet address. Breez’s tooling then determines the destination blockchain, computes a conversion route to USDC or USDT, and presents the user with the expected amount, network, and fees before confirming the payment.

Once confirmed, the payment is routed through liquidity providers—Breez specifically mentions Flashnet and Boltz. Those providers convert the sender’s Bitcoin into the selected stablecoin and deliver it to the recipient on the blockchain chosen by the receiver.

Breez CEO Roy Sheinfeld told Cointelegraph that the feature does not depend on USDT or USDC being issued on Lightning. Instead, he characterized the design as relying on interoperability that lets users “spend from a Bitcoin balance while recipients receive stablecoins” on supported networks.

Under this approach, the user continues to hold Bitcoin until initiating a payment. Recipients receive stablecoins on their preferred chain, and the sender is not required to manage separate stablecoin balances for different ecosystems.

Why this matters for developers and payment flows

Stablecoin distribution across many chains is often the hardest part of designing modern crypto payment experiences. Developers typically need to handle multiple destination networks, stablecoin balance management, and the user experience that comes with switching between payment assets.

Breez’s framing is that the new SDK functionality is meant to remove those frictions. It allows developers to add stablecoin payments without implementing separate integrations for each blockchain or forcing users to pre-position USDC/USDT across networks.

This distinction is especially relevant for applications that start from a Bitcoin-first user base—such as wallets, payment apps, or service providers that want stablecoin output for settlement, accounting, or recipient preferences, but can’t assume users will hold stablecoins.

Non-custodial scope and what’s next

Breez describes the feature as non-custodial. It also states that it is initially limited to outbound stablecoin payments, meaning users can send USDC/USDT to recipients on other networks, rather than receiving stablecoins that originate from external chains.

Support for receiving stablecoins from external blockchain networks is planned for a future release, according to Breez. For users and developers, that roadmap matters because it defines whether a single application can fully unify both sides of the payment experience—or if it will need to keep receiving logic separate until the bidirectional capability arrives.

Lightning and Bitcoin infrastructure keep broadening beyond simple transfers

While Breez’s stablecoin routing focuses on improving how Bitcoin can be used for payments, the launch lands in a broader trend: companies are extending Lightning Network capabilities into higher-value and more complex financial workflows.

Earlier this year, Secure Digital Markets completed a $1 million Bitcoin payment to Kraken over Lightning in under half a second, as Cointelegraph previously reported. The transaction was highlighted as an example of Lightning being tested for uses beyond small retail payments.

Lightning is also being embedded into business-oriented products. Voltage introduced a US dollar-settled revolving credit line that embeds business credit into Lightning payment flows, allowing repayments to be settled in US dollars or Bitcoin—an approach aimed at giving companies working capital options without requiring crypto holdings on their balance sheets.

Outside finance, event infrastructure is another direction. Cointelegraph reported that Satlantis launched a Bitcoin-native ticketing platform with embedded Lightning wallets, designed to let organizers sell tickets while accepting BTC alongside traditional payment methods.

And in the stablecoin ecosystem, Cointelegraph previously covered funding for technology aimed at stablecoin issuance and settlement on Bitcoin, noting a $5.2 million round backing Tether-supported Ark Labs.

Adoption signals continue to appear in network metrics. A February report from River estimated that Lightning surpassed $1 billion in monthly transaction volume in late 2025, up from roughly $12 million in 2021, according to the figures River shared with Cointelegraph’s reporting.

River’s public post referenced by Cointelegraph showed Lightning Network transaction volume growth over time.

For investors and builders, the underlying message is consistent: Lightning is being positioned as more than a faster Bitcoin transfer rail. It is increasingly treated as an infrastructure component that can connect Bitcoin to stablecoin settlement and to application-specific payment requirements.

Going forward, the key thing to watch is whether Breez’s planned receiving support arrives as stated and how developers respond to the outbound-only limitation—because bidirectional stablecoin flows could meaningfully change how Bitcoin-first applications handle balances, reconciliation, and user onboarding across multiple chains.

British far-right activist Tommy Robinson — real name Stephen Yaxley-Lennon — says he feels like a “wanker” after shilling his son’s “patriotic” Pump Fun-based cryptocurrency.

Yaxley-Lennon promoted the Patriotic Bull token on his X account with an image of an AI-generated minotaur wearing tight jeans and standing in front of the Palace of Westminster.

He then shared the token’s address and claimed his own Pump Fun account would use collected fees “to make the UK a better place.”

However, as he later clarified, this project wasn’t his doing. Indeed, the whole thing was his son’s idea. “I’ve not been hacked I’m just letting my son pump his crypto,” he said.

“I feel like a wanker writing these posts 😂😂 I am the patriotic bull 😂😂.”

The post upset numerous right-wing accounts, who described it as a “grift” and “crypto scam.”

One such account called him the “lowest form of pond scum imaginable,” while another claimed they would be unfollowing him for “pumping sloppy crypto scams” while the country is supposedly “being decimated.”

Yaxley-Lennon’s Pump Fun account has received tokens from three different, but similarly named, “The Patriotic Bull” tokens.

The Pump Fun account that created the token and shared Yaxley-Lennon’s X account, “Carefulsquid838, is presumably run by his son, Spencer Yaxley-Lennon.

Who is Tommy Robinson’s son?

Spencer Yaxley-Lennon has previously been spotted sharing posts on Instagram in which he boasts about a luxurious lifestyle of private jets and designer clothes.

The account was later tweaked from public to private once his posts began to circulate. Spencer’s Instagram promotes FX trading, and Trade Informer reports that his promotions link to the website Ghost Trades.

This site relies on offshore broker “Vantage Markets” for its trading, which has also been promoted by Yaxley-Lennon Senior.

Read more: Nigel Farage accused of undervaluing Christopher Harborne jet loan by $666K

Spencer’s online activity appears to contradict his father’s image of himself as a struggling activist in need of financial support.

In 2018, Stephen Yaxley-Lennon received £20,000 ($26,500) worth of BTC donations while in prison for contempt of court.

In 2022, court documents revealed that he was receiving anywhere between £1,000 ($1,300)and £4,000 ($5,300) a month from supporters while also gambling £100,000 ($132,600) in casinos and online.

More recently, his self-proclaimed journalism firm, Urban Scoop, called for donations so that it could re-equip its team and expand operations.

He then shared footage of himself on holiday.

UK right-wing backed by tech trillionaires and billionaires

The political activist has been emboldened by the likes of Tesla trillionaire Elon Musk, who frequently supports Stephen Yaxley-Lennon’s posts on X. Earlier this month, Yaxley-Lennon met up with Musk’s father, Errol, in Russia.

Yaxley-Lennon claims “Russia is not the enemy of Britain.” The hostile nation often covertly stirs up right-wing UK citizens and is responsible for a crypto-paying sabotage network that led to the fire bombing of property owned by Prime Minister Sir Keir Starmer.

Musk also supports Restore UK and Rupert Lowe. The right-wing member of Parliament formed the party after he was suspended from Reform UK following a dispute with its leader Nigel Farage and chairman Zia Yusuf.

Farage and his party, meanwhile, are backed by Christopher Harborne, a 12% shareholder in multi-billion-dollar stablecoin firm Tether.

He has given the party £25 million ($33 million) over the years, and personally gave Farage another £5 million ($6.6 million) before his reentry into politics in 2024. This sum was kept a secret until recently, and is now being probed by the Parliamentary Standards Commissioner.

Read more: Tether shareholder was Boris Johnson’s advisor in Ukraine, report

Over the weekend, it was reported that Harborne has recently registered to vote in the UK. He was previously listed as an overseas UK voter, and was affected by the overseas political donations cap of £100,000 ($132,600).

The limit was introduced by the Labour government as part of a deterrent against foreign political interference.

Also this weekend, The Nerve reported that the UK’s former Conservative prime minister, Boris Johnson, may not have declared a trip to Ukraine in Harborne’s private jet back in 2023.

His jet has also been loaned out to Farage. While declared on the register of interests, Labour Chair Anna Turley has accused Farage of undervaluing the trip by hundreds of thousands of pounds.

She has threatened to report him to parliamentary authorities unless he provides the full details of his trip.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Key takeaways:

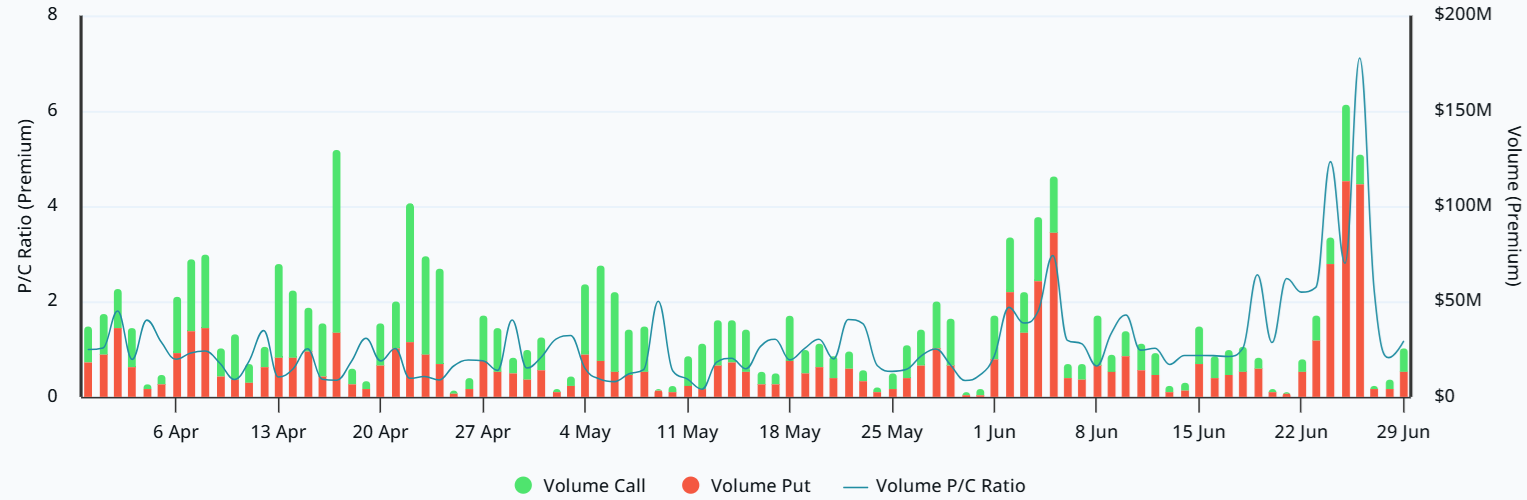

- An extreme Bitcoin put-call options imbalance and a 19% delta skew reveal heavy hedging against downside price swings.

- Strategy’s cash hoard eases short-term debt fears but does not hold back a broader capital rotation into tech stocks.

Bitcoin has failed to reclaim the $61,000 mark since Thursday, despite optimism fueled by lower crude oil prices following the US and Iran’s 60-day ceasefire agreement. Demand for downside Bitcoin price protection jumped to unusually high levels, prompting traders to question whether $55,000 is the next target.

Deribit Bitcoin options premium put-to-call ratio. Source: Laevitas

The premium paid on Bitcoin put (sell) options on Deribit totaled $115 million on Friday, 7 times the $16 million paid on call (buy) options. The imbalance was the highest in over 12 months, signaling extremely low demand from bulls. However, such data does not necessarily signal conviction from bears.

Bitcoin 30-day options delta skew (put-call) at Deribit. Source: Laevitas

The Bitcoin options delta skew stood at 19% on Monday, meaning market makers are unwilling to hold downside price exposure. This setup hints at fear, although that has been the norm for the past 4 weeks. Data aligns with growing demand for bearish hedging as Bitcoin price struggles to sustain levels above $60,000.

Bitcoin’s weakness can be partially pinned to investors’ discomfort with MicroStrategy (MSTR US) ability to pay dividends and debt maturing in 2027. The company reacted on Monday by announcing an additional $1.2 billion in cash from recent share sales and setting aside $1.25 billion in Bitcoin for eventual sale.

The measures taken by Strategy ease some short-term concerns but also create anxiety about Bitcoin’s supply and demand dynamics. Even if no sales occur over the next couple of months, bears are more comfortable knowing that Strategy has no incentives to issue MSTR shares given the current 17 months of dividend coverage.

Related: Grayscale’s Pandl says Strategy should sell $3B Bitcoin to restore confidence

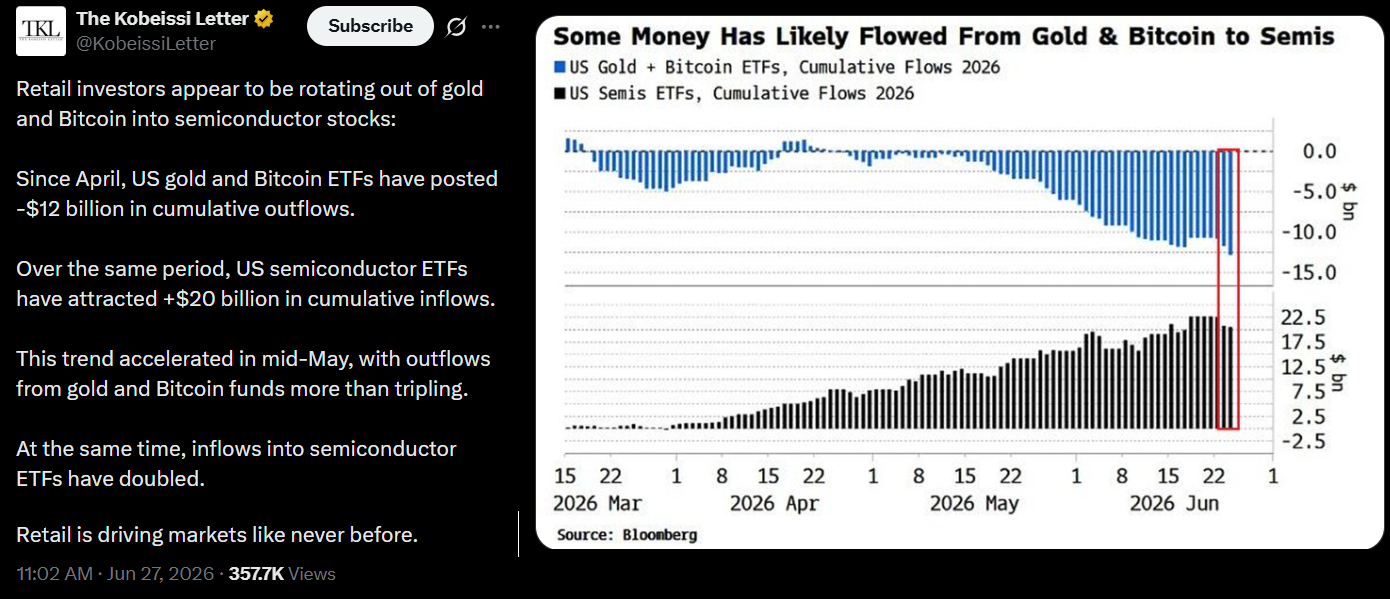

Rotation from Bitcoin and gold into semiconductor stocks

In contrast to Bitcoin investors’ pessimism, momentum in the US stock market has shifted favorably after inflationary pressure eased, with crude oil prices dropping to their lowest levels in 4 months. Additionally, a Goldman Sachs report projected 22% annual earnings growth for S&P 500 companies, easing concerns about excessive valuations.

Source: X/KobeissiLetter

Retail investors appear to be rotating out of gold and Bitcoin into semiconductor stocks, according to ‘The Kobeissi Letter’ analysis. Data collected by Bloomberg has shown over $20 billion in cumulative inflows in semiconductor exchange-traded funds (ETFs), triggering an 81% rally in iShares Semiconductor ETF (SOXX US) and 60% gains in VanEck Semiconductor ETF (SMH).

US-listed Bitcoin spot exchange-traded funds weekly net flows, USD. Source: SoSoValue

The 7 consecutive weeks of net outflows from the US-listed Bitcoin spot ETFs have shattered bulls’ hopes of a strong bounce from the $58,050 lows on June 25. Regardless of whether the sell-off can be attributed to the rotation into tech stocks, sentiment is unlikely to improve while Bitcoin spot ETFs continue to see strong net outflows.

A retest of $55,000 should not be dismissed, but the increased demand for downside hedging in Bitcoin options should not be interpreted as growing confidence among bears.

TLDR:

- XRP Ledger Foundation and VS1 Finance are building an open-source compliant lending reference application for XRPL.

- The project combines Credentials, Permissioned Domains, Vaults and Lending Protocol into one institutional framework.

- Developers will be free to fork, study and extend the reference application for regulated lending use cases.

- The initiative focuses on permissioned lending infrastructure designed for institutions operating on XRP Ledger.

The XRP Ledger Foundation has partnered with VS1 Finance to develop an open-source reference application for compliant lending on the XRP Ledger. The initiative focuses on regulated lending by combining native XRP Ledger features with permissioned access controls.

The project aims to provide developers with a reusable framework for building institutional lending products. It also highlights the network’s growing focus on compliance-ready blockchain infrastructure for financial markets.

XRP Ledger Foundation expands compliant lending infrastructure on XRP Ledger

The new application will use several native XRP Ledger building blocks designed for regulated financial activity. These include Credentials, Permissioned Domains, Single Asset Vaults, and the Lending Protocol.

According to the XRP Ledger Foundation’s announcement on X, the application will serve as an open-source reference implementation rather than a closed commercial product. Developers will be able to examine its architecture and adapt it for their own use cases.

The framework targets permissioned lending environments where participants must satisfy compliance requirements before accessing financial services. That approach allows institutions to operate within predefined identity and authorization rules.

The project reflects continued development around institutional blockchain infrastructure. Instead of introducing new protocol features, the application combines existing XRP Ledger primitives into a practical lending workflow.

XRP Ledger lending app targets institutional crypto finance

VS1 Finance said the collaboration focuses on creating infrastructure that institutions can readily adopt for compliant capital deployment. The company stated on X that permissioned lending can help bridge traditional financial firms with blockchain-based markets.

Rather than limiting access to a single platform, the partners intend to publish the application as open source. Development teams will have the option to fork, modify, or extend the codebase for different lending products.

The announcement places strong emphasis on transparency and ecosystem growth. Open-source reference applications often reduce development time by providing tested implementation examples for builders across the network.

Neither organization disclosed a launch date or technical roadmap alongside the announcement. The initial statements instead centered on the application’s design goals and its role within the broader XRP Ledger ecosystem.

The collaboration arrives as blockchain networks continue developing compliance-focused infrastructure for regulated financial institutions. By combining permissioned access with native lending components, the project seeks to provide a standardized foundation for future XRP

Ledger lending applications, according to updates shared separately by both the XRP Ledger Foundation and VS1 Finance on X.

The crypto market enters the final stretch of the month in a perilous position with bitcoin still below $60,000 and ether (ETH) less than $1,600.

The bitcoin price has now lost more than 50% of its value since October’s record high, with analysts suggesting that more downside is on the cards over the coming months.

On Monday, the largest cryptocurrency is marginally in the black, rising by 0.6% since midnight UTC to $59,800 despite the broader market structure and chart formation skewing bearish.

Solana (SOL) has recovered after tumbling to its lowest point since late 2023 early this month. It has advanced by more than 13% since Thursday and 2% since midnight.

U.S. equities rose overnight as Nasdaq 100 futures traded up 1% while S&P 500 futures added 0.75%. Both indexes remain in a downtrend since setting record highs on June 15.

Derivatives positioning

- Over $200 million in futures positions have been forcibly closed, or liquidated, by exchanges in the past 24 hours, with longs accounting for the bulk of the amount.

- There are signs of a turnaround over the past four hours: the nearly $20 million in liquidations included $13 million in shorts. That shows how BTC’s bounce to $60,000 caught some bears off guard.

- BTC’s futures market offers little excitement. Open interest (OI) is back in ranges seen earlier this month, erasing the minor pop to 775K BTC seen on Friday. Traders seem less willing to take on risk.

- The same is true for ether, where OI remains locked at around 14.2 million ETH.

- Open interest positioning in SOL feels relatively elevated at 72.70 million SOL, just short of the record high of over 76 million SOL set on June 24. That suggests potential for more volatility in Solana’s native token.

- AVAX rose over 5% last week, decoupling from market leader BTC’s weakness. But that hasn’t been enough to draw traders into leveraged bets. OI continues to decline, standing at 38.07 million tokens, the lowest since April 1. That raises questions about the sustainability of the price gains.

- The 24-hour OI-adjusted cumulative volume delta (CVD) remains bearish. Most top 25 tokens, except TRX, XMR and ZEC, show negative values, a sign that bears are leading price action by selling via market orders rather than limit orders.

- Volatility indexes, though, offer some good news. The BVIV, which tracks BTC’s 30-day implied volatility, dropped 5% to 47% today, pausing its two-week upswing. That suggests a renewed bet on market calm, typically a feature of grinding upswings in spot prices.

- On Deribit, BTC and ETH options continue to show a bias for puts, or downside protection. In BTC’s case, the $60,000 put now has notional open interest of nearly $1 billion, almost rivaling the $1.11 billion sitting in the $80,000 call. These two have been the key option levels for at least two months. Should prices slide below $60,000, the next big options cluster is at $50,000, with notional OI of $712 million.

- Over the weekend, traders sold strangles in the July 10 expiry on HYPE options on the decentralized platform Derive, according to data tracked by Laevitas. Shorting a strangle is a bet on price consolidation.

Token talk

- The altcoin market is little changed, trading in line with the biggest cryptocurrencies as traders appear apathetic toward more speculative assets until bitcoin confirms its next move.

- Privacy coins dash (DASH) and zcash (ZEC) are up by more than 2% on Monday. The move comes after both assets lost between 18% and 30% in the past two weeks alone, suggesting it is more of a relief rally than a meaningful recovery.

- lost 1.5% since midnight, joining AI token FET in the red.

- CoinMarketCap’s “Altcoin Season” indicator is at 49/100, a level it has held for most of June as investors focus on bitcoin’s next move.

Crypto World

DraftKings Launches Proprietary Prediction Markets Exchange With $3.4B Annualized Consumer Volume

Sports betting giant DraftKings has launched a proprietary prediction markets exchange called DKeX, entering a space dominated by Polymarket and Kalshi as the company reports $3.4 billion in annualized consumer volume. DraftKings announced DKeX on Tuesday as a "vertically integrated foundation" for… Read the full story at The Defiant

The path of the Digital Asset Market Clarity (CLARITY) Act, a bill intended to establish comprehensive guidelines for cryptocurrency regulation, remains uncertain with the US Congress set to break for another state work period in a matter of weeks.

Since passage in the US House of Representatives in July 2025, the CLARITY Act has faced several hurdles advancing in Congress, from industry pushback on stablecoin rewards to lawmakers’ concerns about ethics. The bill passed the Senate Agriculture Committee in January and the Senate Banking Committee in May along party lines, setting it up for consideration in the full chamber.

However, US President Donald Trump on Wednesday cancelled the signing ceremony for the 21st Century ROAD to Housing Act, a housing bill that received bipartisan support in both chambers and contained a ban on a central bank digital currency (CBDC). Trump said that he would not sign the bill until Republicans in Congress passed the SAVE America Act, legislation requiring voters to provide proof of US citizenship in person to register, adding in March that he would “not sign other bills” until it was passed.

The move by the president leaves the future of the CLARITY Act in doubt despite earlier statements signaling he supported the bill. If Trump vetoes the legislation, Congress could override him with a two-thirds majority vote in both chambers. According to the US Constitution, if a president doesn’t sign or veto a bill within 10 days while Congress is in session, the bill automatically becomes law.

Related: Galaxy cuts CLARITY Act odds to 50% as Senate floor time narrows

On Monday, Republican leaders in the Senate, including banking committee chair Tim Scott and majority leader John Thune, said that they were pushing for the chamber to pass CLARITY in July. Lawmakers are scheduled to be out of Washington, DC and on state work periods until July 13, giving them four weeks to address the bill before a monthlong state work period in August.

Source: Senator Tim Scott

“We’ve been negotiating on the CLARITY Act hardcore since last Labor Day, and it’s been an arduous process,” said Senator Cynthia Lummis, one of the bill’s proponents, in a Fox Business interview last week, adding:

“We’re still working a little bit on DeFi, we’re working [on] illicit finance, we’re working a little bit on ethics [..] We’re finally to the point where we’re going to put out the text over the July 4th, and give people one last really thorough look at the bill, and then we’re moving in July.”

What happens if lawmakers face more delays on CLARITY?

Republicans hold a slim majority in the US Senate, where they will need some support from Democrats should they hold a vote on CLARITY next month. Many Democratic lawmakers have been pushing for ethics provisions in the bill, citing the Trump family’s ties to the crypto industry through the president’s memecoin and his sons’ involvement in the World Liberty Financial platform and a Bitcoin mining company.

Should Republicans not meet the 60-vote threshold in the Senate before August, many experts expect that lawmakers dealing with reelection campaigns could delay the passage of CLARITY, potentially pushing the legislation to the next session of Congress in 2027.

Magazine: AI is banking the unbanked in Africa… faster than crypto

The Commodity Futures Trading Commission is conducting a broad investigation into Polymarket that reportedly covers staged trades and fabricated winning bets, Bloomberg reported Friday, extending federal scrutiny beyond the platform's previously reported influencer scheme. CNBC also reported Friday… Read the full story at The Defiant

With the EU’s Markets in Crypto-Assets (MiCA) framework set to start on July 1, several major cryptocurrency exchanges that are already licensed are stepping up efforts to keep— and win—European users. At the same time, companies that missed (or withdrew) their MiCA authorization are beginning to scale back access for customers in the EU and wider European Economic Area (EEA).

The push is becoming unusually direct: executives at platforms including Coinbase, OKX, and others have taken to social media to offer incentives ahead of the enforcement date, as regulators approve licenses under MiCA and unlicensed firms prepare for restrictions.

Key takeaways

- MiCA enforcement begins July 1 for crypto-asset services offered to users across 27 EU countries, requiring authorization as a Crypto-Asset Service Provider (CASP).

- Binance said it would restrict services for EU-based users after withdrawing its MiCA application, while Bybit said EEA access will be progressively limited from July 1.

- As of Monday, EU regulators had approved 244 MiCA crypto licenses, with Germany’s BaFin accounting for 57 of them, and several member states reporting no approvals as of Friday.

- Licensed exchanges are using time-bound promotions—such as deposit offers and transfer bonuses—to move users away from platforms facing MiCA limits.

Why MiCA is triggering a scramble for EU users

Under MiCA, firms offering crypto-asset services to people in the EU must hold a license as a Crypto-Asset Service Provider (CASP), granted by a regulator in an EU member state. This structure means that authorization is not merely a compliance checkbox—it determines whether customers can legally access services after the rules take effect.

Many exchanges, including Coinbase, FalconX, Kraken, and OKX, have obtained MiCA approval to continue operating following the June 30 deadline. But gaps in approvals across the bloc could still reshape the market quickly: users on platforms without the necessary permissions may face narrowed or removed access once enforcement starts.

Binance withdraws, Bybit limits—licensed rivals move first

Binance, the largest cryptocurrency exchange by market presence, signaled a turning point for EU users after it withdrew its MiCA application last week, according to Cointelegraph’s reporting. The company said it would restrict services for EU-based users following that withdrawal, a move that effectively frames MiCA as a forced migration event rather than a gradual transition.

Bybit’s approach is also restrictive, but with a more time-phased description. According to a statement reported by Cointelegraph, Bybit said access to services for users in the EEA “will be progressively limited” starting July 1. The same coverage notes that Bybit EU is authorized to operate under MiCA through its Austrian licensee, suggesting that users’ experience may vary depending on the jurisdiction and corporate entity providing services.

The licensing landscape is still uneven. As of Monday, EU regulators had approved 244 total licenses for crypto companies under MiCA, Cointelegraph reported, citing regulatory updates. Of those approvals, about a quarter—57—came from Germany’s Federal Financial Supervisory Authority, BaFin. The reporting also states that authorities in Greece, Hungary, Poland, Portugal, and Romania had not issued any licenses as of Friday.

Incentives and migration tactics: bonuses tied to the July 1 deadline

As access rules tighten, executives at licensed exchanges are trying to convert uncertainty into customer transfers. Erald Ghoos, CEO of OKX Europe, said OKX would offer 8% on new deposits, using the approaching MiCA date as a clear incentive window. (Ghoos made the comments publicly via X, as linked in Cointelegraph’s write-up.)

Coinbase CEO Brian Armstrong similarly pointed to a time-bound benefit: Coinbase would provide a 5% transfer bonus for users before July 13, about two weeks after MiCA takes effect, according to Armstrong’s post referenced by Cointelegraph.

Kraken, another exchange already authorized under MiCA, announced a promotional draw for euro deposits, described in the source coverage as a $1.1 million prize pool. While the specific mechanics weren’t detailed in the article, the thrust is clear: licensed firms are leveraging the compliance transition to strengthen their position in the EU.

For users, these campaigns matter because they may reduce the financial friction of moving funds during a period when account access and eligibility can change quickly. For the market, they also raise the stakes for exchanges that are not fully authorized in relevant jurisdictions—because the competition is effectively marketing compliance.

MiCA compliance and the business shift beyond Europe

MiCA’s enforcement date is also influencing where exchanges place growth efforts. The source coverage highlights Bybit’s decision to limit certain services for EU users while expanding in the Middle East and North Africa (MENA).

Cointelegraph reports that Derek Dai, Bybit’s head for the Middle East and North Africa, discussed the company’s strategy at a Tel Aviv event on Sunday. Dai said Bybit was stepping up efforts in the region as it restricted services for EU customers. He framed the approach as tailoring marketing and product offerings to different customer groups.

According to the quoted remarks, Bybit aims to build “halal products” designed for more conservative customers in some Arabic countries, while also focusing on derivative products for younger investors in Morocco who are developing trading skills and interest.

This split strategy reflects a broader pattern visible across crypto markets: when regulatory clarity tightens in one region, growth often shifts to jurisdictions where compliance requirements may be different or where the firm already has operational footing. Whether that will mitigate churn from EU limits depends on how smoothly users can transition their activity across platforms and regions.

Going forward, the key thing to watch is how quickly the remaining MiCA approvals—or the lack of them—translate into actual service limits for unlicensed firms, and whether user migration continues once July 1 arrives and incentives end. The licensing numbers show how far the framework has progressed, but the experience for customers will ultimately depend on how each exchange implements access controls across specific jurisdictions and corporate entities.

Cause of Antalya Shawarma, Middlesbrough fire revealed

Bristol Waste’s new managing director pledges to deliver ‘reliable services’

Smart Money is Leaving Nvidia for This AI Chip Stock

-

Sports6 days ago

Sports6 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics4 days ago

Politics4 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics4 days ago

Politics4 days agoPotential 2028er World Cup attendee leaderboard

-

News Videos1 day ago

News Videos1 day agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Business4 days ago

Business4 days agoAsia stock markets slide as tech shares slump

-

Tech4 days ago

Tech4 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World4 days ago

Crypto World4 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World2 days ago

Crypto World2 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Crypto World6 days ago

Crypto World6 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Business6 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World3 days ago

Crypto World3 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports3 days ago

Sports3 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Tech2 days ago

Tech2 days agoRussian hackers now target Signal backup recovery keys

-

Tech2 days ago

Tech2 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Crypto World4 days ago

Crypto World4 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Crypto World3 days ago

Crypto World3 days agoRTX holders must register wallets before token distribution begins

-

Crypto World3 days ago

Hyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World5 days ago

Crypto World5 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

You must be logged in to post a comment Login