Crypto World

What is a multisig wallet? How crypto’s biggest treasuries get secured, and robbed

Multisignature wallets guard most of the serious money in crypto: DAO treasuries, exchange cold storage, protocol funds, and the savings of the security-conscious. They are also at the center of the industry’s biggest heists, from Bybit’s $1.5 billion to this year’s UXLINK breach, because attackers stopped picking locks and started fooling the people holding the keys. This guide explains how multisig actually works, the M-of-N design choices, how the famous multisig hacks really happened, and how to run one without becoming a case study.

Summary

- Multisig wallets protect crypto funds by requiring multiple approvals, reducing the risk of a single compromised key.

- Major breaches such as Bybit and Ronin exposed human error and interface attacks rather than weaknesses in multisig technology itself.

- Strong operational practices including independent verification and separate key management remain essential for multisig security.

Ask where crypto’s serious money lives, and the answer, overwhelmingly, is behind multiple signatures. A majority of institutional custodians run multisignature arrangements; DAO treasuries holding billions coordinate through them; exchanges guard cold storage with them; custody chains behind institutional products depend on them; and protocols park their upgrade keys and reserve funds inside them, most commonly in Safe, the contract system formerly known as Gnosis Safe, which alone secures values rivaling large banks. The idea is old, borrowed from bank vaults and nuclear launch protocols: no single person, key, or machine should be able to move what matters. Require M signatures out of N keys, 2-of-3, 3-of-5, and a thief must compromise several independent guardians instead of one.

And yet the largest theft in crypto’s history, Bybit’s $1.5 billion, walked out through a multisig. So did this year’s $11.3 million UXLINK breach, and the Ronin bridge’s $600 million before them. The pattern is the most instructive fact in modern crypto security: the multisig math has never been broken; the humans and interfaces around it are broken constantly. Multisig eliminates the single point of failure and replaces it with a subtler question, whether your several points of failure are actually independent, and the industry’s disaster record is a catalog of discovering they were not.

This guide covers the mechanism and its failure modes with equal seriousness: how multisignature schemes actually work on Bitcoin and on smart-contract chains, how to choose M and N and what each choice trades, the anatomy of the great multisig heists and the blind-signing problem at their core, multisig against its modern rivals, MPC and smart accounts, and the operational playbook that separates the treasuries that survive from the ones that headline.

The mechanism: M-of-N, on two architectures

A multisig wallet requires a threshold of signatures, M, from a set of authorized keys, N, before any transaction executes. A 2-of-3 personal setup might split keys across a hardware wallet at home, a second device in a bank box, and a trusted relative; a 4-of-7 DAO treasury spreads keys across council members on different continents. The threshold is the design’s dial: security against compromise rises with M, resilience against key loss rises with the gap between N and M, and operational friction rises with both.

Under the hood, two architectures implement the idea. On Bitcoin, multisig is native to the protocol’s scripting: an address encodes the M-of-N requirement itself, and spending requires the signatures to be presented and verified by the network. It is minimal, battle-tested, and rigid, changing signers means moving funds to a new address. On Ethereum and similar chains, multisig lives in smart contracts: a program, such as a Safe, holds the funds and enforces the policy, collecting signatures until the threshold is met and then executing. The contract approach is vastly more flexible, signers can be rotated, thresholds changed, daily limits and timelocks and module extensions added, and that flexibility is double-edged: the policy is code, code can have flaws, and, as the disaster section will show, the richness of what a contract wallet can execute is exactly what modern attackers exploit.

The transaction flow in both worlds follows the same rhythm. Someone proposes a transaction, recipient, amount, and, on contract wallets, arbitrary program calls. The proposal circulates to signers, each of whom reviews and cryptographically approves it with their own key, on their own device. When approvals reach the threshold, the transaction becomes executable and is broadcast. Every step is auditable: the chain records exactly which keys approved what, creating the accountability trail that makes multisig the governance tool of choice for DAO treasuries whose control is otherwise contested through token votes, for corporate funds requiring officer sign-off, and for escrow arrangements where a neutral third key arbitrates disputes, the human-governed cousin of the time-locked contracts that automate escrow on-chain.

Choosing M and N: the design space

The threshold choice is a risk allocation, and the standard configurations each answer a different question. 2-of-2 is a partnership with no tiebreaker and no recovery, one lost key strands the funds, and is mostly used with one key held by a service. 2-of-3 is the individual’s workhorse: it survives the loss of any one key, resists the compromise of any one key, and keeps signing friction tolerable; the classic personal build spreads three hardware keys across locations, and the classic collaborative-custody build gives one key to a professional service that can co-sign recovery but can never move funds alone. 3-of-5 and up is institutional territory, tolerating multiple losses and requiring multiple corruptions, at the price of coordination overhead that, in practice, tempts organizations into the worst sin of the genre: concentration, several keys held by one person, one office, one laptop, or one cloud account. A 3-of-5 whose keys live in three browsers and two drawers of the same office is a 1-of-1 with extra steps, and post-mortems of real losses find this shape constantly. The rule the design space reduces to: the security of a multisig is the security of its most correlated keys, and independence, of people, devices, software, and geography, is the entire point of the exercise.

Key-holder policy matters as much as the numbers. Every signer is a target the moment the arrangement is visible on-chain, and large treasuries are visible by definition, tracked by the same wallet-attribution lens that maps every whale. Serious operations therefore treat signers as an attack surface: hardware keys only, dedicated signing devices, no signer identities published unnecessarily, and procedures rehearsed before they are needed, because the day a treasury must move funds under pressure is the worst day to discover the third signer’s key is in a safe nobody can open.

How multisigs actually get robbed

The heist record is where this subject earns its place in a security curriculum, because the attacks share an anatomy and it is not the one intuition expects. No major multisig loss has come from breaking the cryptography. They come from making the right people sign the wrong thing.

The Bybit theft, $1.5 billion, the largest in industry history, is the canonical case. The exchange’s cold storage sat behind a multisig with executives as signers, exactly as best practice prescribes. Attackers, attributed to North Korea’s Lazarus Group, compromised the infrastructure of the wallet interface the signers used, so that when the executives performed a routine, scheduled transfer, their screens showed the legitimate transaction while their hardware keys signed a different payload, one that handed the attackers control of the wallet’s logic. Every signature was genuine. Every signer was diligent by the standard of what they could see. The vault held; the vault’s window lied. The Ronin bridge before it fell differently but rhymes: a 5-of-9 arrangement whose keys were insufficiently independent, with one organization controlling enough of them that compromising it, via a social-engineered employee, crossed the threshold, the key-compromise pattern behind the largest bridge disasters. And this year’s UXLINK breach showed the small-scale version: attackers who gain threshold control do not just drain, they use the wallet’s own administrative powers, adding themselves as signers, ejecting the owners, because on a contract multisig, governance of the wallet is itself just another transaction.

The common thread is blind signing. A hardware key protects the signature; it does not tell the signer, in honest human terms, what they are signing, and complex contract-wallet payloads are unreadable hashes on a tiny screen. Attackers therefore aim at the layer between intention and signature: the web interface, the signer’s laptop, the proposal pipeline, the human’s routine. The defenses that address this are specific and increasingly standard: independent verification of every payload on a second channel before signing, signing devices that decode and display transaction meaning, simulation tools that preview a transaction’s actual effects, timelocks that delay large movements long enough for review, and the simple institutional rule that no transaction is routine, because routine is precisely the state of mind the Bybit attackers were waiting for.

From Bitcoin script to Safe: how the standard was built

Multisig’s history is the history of crypto custody growing up, and its milestones explain today’s defaults. The capability is nearly as old as Bitcoin itself, formalized in the protocol’s early years through pay-to-script-hash addresses that let spending conditions, including M-of-N signature requirements, be encoded on-chain. The first institutional era was built directly on it: the early exchange and custody pioneers ran Bitcoin multisig vaults, and the first collaborative-custody businesses sold 2-of-3 arrangements to individuals a decade ago. The idea crossed to Ethereum as smart-contract wallets, where the flexibility of code produced both the triumphs and the scars: an infamous 2017 library bug in a widely used contract wallet froze hundreds of millions permanently, the formative lesson that flexible custody code is itself an attack surface, and the survivor of that era’s consolidation, Gnosis Safe, hardened through years of audits and adversarial value into the default it is now.

Today Safe-style contracts secure treasuries whose combined value rivals major banks, the DAO era having made the multisig council crypto’s standard governance executive, and Bitcoin’s own multisig lineage continues in parallel, favored for deep cold storage precisely because its rigid, minimal script surface offers so little to exploit.

The standardization has a consequence worth naming: concentration of a different kind. When one contract system secures the majority of on-chain treasuries, its code, its interface, and its upgrade process become systemic infrastructure, and the Bybit attack’s compromise of interface infrastructure was, among other things, a demonstration that the ecosystem’s eggs share more baskets than the M-of-N math suggests. The response, interface diversity, independent transaction verification services, signing-device decoding, is effectively the community rebuilding independence one layer up the stack, the same principle the wallets encode, applied to the tooling around them.

Setting one up: the individual’s path

For an individual reader, the practical on-ramp deserves concreteness. A personal 2-of-3 today is a weekend project: three hardware keys, ideally from two different vendors to avoid a shared firmware flaw; a contract wallet on an inexpensive network or a native Bitcoin multisig, depending on holdings; owner addresses triple-checked before deployment, because a mistyped owner is a permanent stranger with signing power; and the three keys distributed across genuinely separate locations, home, bank box, trusted party, with recovery instructions that someone other than you can follow.

The recurring costs are minor, deployment gas and slightly larger transaction fees, and the recurring disciplines are not: test the setup with small amounts first, rehearse a lost-key migration before losing one, keep a small gas balance where the contract needs it, and revisit the arrangement whenever a signer, device, or living situation changes. The friction is real, every transaction becomes a small ceremony, and the friction is the feature: a wallet that requires deliberation cannot be drained by one bad click, which, given that a single mistaken approval is how most individual losses now happen, is the entire value proposition in one sentence.

Multisig and its rivals: MPC and smart accounts

Two adjacent technologies answer the same single-point-of-failure problem, and choosing among them is a real decision, not branding.

Multi-party computation, MPC, splits one key into mathematical shares held by different parties, who jointly compute a signature without the full key ever existing anywhere. To the blockchain, the result looks like an ordinary single signature: cheaper, private, chain-agnostic, and revealing nothing about the policy behind it. The trade is opacity and dependence: the threshold logic lives in the providers’ off-chain software rather than in public code, there is no on-chain trail of who approved what, and the institutional MPC market is dominated by vendors whose systems must be trusted. Institutions increasingly use both, MPC for operational hot flows, multisig for deep cold governance.

Smart accounts, account abstraction, generalize the contract-wallet idea: programmable accounts with recovery guardians, spending policies, session keys, and multisig as merely one available policy among many. They are the likely long-term home of these ideas for individuals, folding multisig-grade protection into interfaces normal users can operate. For treasuries today, the audited, battle-hardened dedicated multisig remains the standard, precisely because its decade of scars, documented above, produced a decade of hardening.

Between the architectures sits a question every treasury eventually asks: how many signers is too many? The coordination cost of thresholds grows faster than linearly, five signers across five time zones can turn a routine payment into a week, and organizations respond with delegation structures that deserve scrutiny because they quietly re-centralize. Common patterns include a small operational multisig with spending limits for daily flows, governed by a larger cold council for everything above the limit; module systems that pre-authorize specific recurring actions; and role separation between proposers, who prepare transactions, and signers, who approve them, narrowing what any single compromised seat can initiate. Each pattern trades purity for function, and the honest evaluation standard is the same one the thresholds themselves answer to: enumerate what the compromise of each seat, device, and interface enables, and check that no enumeration ends in everything. Treasury security is not a product purchased once; it is that enumeration, repeated, forever, against adversaries who read the same post-mortems.

One misconception deserves explicit correction before the playbook: multisig does not protect against approving a bad idea unanimously. If all required signers are deceived by the same forged interface, the same fraudulent counterparty, or the same internal fraudster’s paperwork, the threshold is met and the mathematics executes the mistake faithfully. Signature independence protects against compromised keys; only verification independence, different signers checking the payload through different tooling and channels, protects against compromised information, and the great heists were failures of the second kind wearing the confidence of the first.

The operational playbook

Everything in this guide compresses into a practice list, and the list is the difference between the mechanism and its reputation. Choose thresholds for both compromise and loss: 2-of-3 personal, 3-of-5 or higher institutional. Make independence real: different people, devices, vendors, physical locations, and no key in a browser. Verify what you sign: second-channel confirmation of every payload, simulation before approval, and a standing suspicion of anything urgent. Add time as a defense: timelocks on large transfers turn a successful deception into a recoverable one. Rehearse recovery: a lost-key drill and a signer-rotation drill, run before either is needed. And treat the wallet’s own governance, adding or removing signers, changing thresholds, as the crown jewels, because the UXLINK lesson is that whoever can edit the signer set owns everything the signatures guard.

Multisig, honestly summarized, is the most successful security primitive crypto has deployed: it moved the industry’s treasuries from single hackable keys to arrangements that require conspiracies to rob, and the conspiracies, note, have had to grow to nation-state sophistication to succeed. Its failures are not refutations but curriculum, each one converting a blind spot into a checklist item, and the checklist is public. The vault works. Guard the window.

Two closing perspectives round out the subject. The first is the defender’s asymmetry, and it is encouraging: every major multisig loss has produced a specific, adoptable countermeasure, payload verification after Bybit, key-independence audits after Ronin, signer-set timelocks after the takeover breaches, and the countermeasures compound while the attacks must be reinvented. A treasury running the current playbook is not facing the same odds its predecessors did; it is facing adversaries who must now defeat every lesson previous victims paid for. Security in this domain is cumulative, and the cumulation is public.

The second is the philosophical point hiding in the mechanism, worth one paragraph because it explains multisig’s cultural weight in crypto. A multisignature arrangement is a constitution in miniature: a written rule about who may act, enforced by mathematics instead of courts, visible to everyone it governs. That is why the technology became the executive branch of the DAO era, why its failures feel like institutional scandals rather than mere thefts, and why its steady hardening matters beyond the funds it guards. Crypto’s founding claim was that agreements could be enforced without trusted enforcers, and the multisig, requiring humans to agree while preventing any of them from betraying the agreement, is the claim’s most widely deployed, most thoroughly attacked, and most durably successful embodiment. The vaults hold more than money.

For further orientation, the study list is mercifully practical: the post-mortems of the major incidents named above, each a free masterclass in one failure mode; the documentation of the dominant contract systems, whose security recommendations encode the industry’s accumulated scar tissue; the transaction-simulation and payload-decoding tools that address blind signing directly; and, for organizations, the published treasury-operations frameworks that DAOs and custodians have converged on. Multisig is the rare corner of crypto where the best practices are written down, battle-tested, and free, and where the distance between the average outcome and the best outcome is almost entirely a matter of reading them.

And if this guide leaves a single instinct behind, let it be this one: in multisig, the question is never whether the mathematics will hold, because it will. The question, every time, for every transaction, is whether the humans holding the keys know what they are signing, and every practice in the playbook above is, in the end, a different way of making sure the answer is yes.

Disclaimer: This article is for educational purposes only and does not constitute investment or security advice. Digital asset custody carries significant risk, and no arrangement eliminates it. Details are current as of July 9, 2026. Always do your own research.

Frequently asked questions

What is a multisig wallet in simple terms?

A multisig wallet is a crypto wallet that requires multiple private keys to approve any transaction, following an M-of-N rule such as 2-of-3 or 3-of-5. No single person or device can move the funds alone: a proposal must collect the threshold number of signatures, each from an independent key, before it executes. This removes the single point of failure that defines ordinary wallets.

How does a 2-of-3 multisig work?

Three keys are created and stored independently, for example on a hardware wallet at home, a second device in another location, and with a trusted party or service. Any two of the three must sign for a transaction to execute. One key being lost does not strand the funds, and one key being stolen does not endanger them, which is why 2-of-3 is the standard personal configuration.

Are multisig wallets actually safe if Bybit lost $1.5 billion through one?

The mathematics has never been broken; the famous losses came from deceiving the signers. In the Bybit case, attackers compromised the signing interface so executives approved a malicious payload their screens displayed as routine. The lesson is that multisig secures the signatures, while operational discipline, verifying payloads independently, using devices that decode transactions, adding timelocks, must secure what gets signed.

What happens if I lose one of my keys?

If your threshold still allows it, for example losing one key of a 2-of-3, the remaining keys can move the funds, and best practice is to migrate promptly to a fresh setup with a full key set. If losses exceed the tolerance, the funds are permanently inaccessible, which is why the gap between N and M exists and why recovery drills matter.

What is the difference between multisig and MPC?

Multisig uses several complete keys with the threshold enforced on-chain, visible and auditable. MPC splits a single key into shares that jointly produce one ordinary-looking signature, with the policy enforced in off-chain software. Multisig offers transparency and battle-tested public code; MPC offers privacy, lower fees, and chain flexibility at the cost of trusting provider infrastructure. Institutions commonly use MPC for hot operations and multisig for cold governance.

Who should use a multisig wallet?

Anyone holding more crypto than they could bear to lose to a single mistake: individuals with significant savings, and, essentially without exception, organizations, DAOs managing community treasuries, companies with crypto on the balance sheet, protocols holding upgrade keys, and groups needing escrow. For small everyday balances, the coordination friction usually outweighs the benefit.

What is blind signing and why is it dangerous?

Blind signing is approving a transaction whose true contents you cannot read, typically a complex smart-contract payload shown as an opaque hash. It is the vector behind the largest multisig heists: attackers compromise the interface so signers see a legitimate transaction while approving a malicious one. Defenses include devices that decode payloads, independent second-channel verification, and simulation tools that preview effects.

Can the signers of a multisig be changed?

On smart-contract multisigs, yes: adding or removing signers and changing the threshold are themselves transactions requiring threshold approval. That flexibility enables rotation and recovery, and it is also a target, since an attacker reaching the threshold can eject the rightful owners entirely, as recent breaches showed. Treat signer-set changes as the most sensitive operation the wallet performs.

Phantom and the Hyperliquid Policy Center have asked the US Commodity Futures Trading Commission (CFTC) to clarify that blockchain protocol developers and non-custodial wallet providers should not be treated like traditional financial intermediaries.

The request was submitted in response to a CFTC request for information on how fintech regulations apply in the digital-assets era, urging the agency to codify exemptions and provide guidance tailored to onchain systems where users transact directly rather than relying on a firm to hold customer assets or execute orders.

Key takeaways

- Phantom and the Hyperliquid Policy Center want the CFTC to confirm that building onchain software and contributing to open protocols does not, by itself, trigger registration obligations meant for custodial intermediaries.

- The groups argue that regulations should target entities that actually handle customer funds or execute trades, not developers who do not control how software is used.

- They ask for explicit guidance that regulated derivatives exchanges, clearinghouses, and intermediaries may use blockchain infrastructure for execution, clearing, settlement, margining, and recordkeeping while staying within existing requirements.

- They also request an exemption framework so non-custodial wallet providers are not classified as introducing brokers.

Why the CFTC is being pressed on fintech rules

In the letter, the companies contend that much of the CFTC’s regulatory framework was built around intermediaries that operate as gatekeepers—typically taking custody of customer assets and routing trades through centralized processes. In contrast, onchain protocols can be designed so that users conduct transactions without any intermediary exercising control over funds or placing orders on their behalf.

From that premise, Phantom and the Hyperliquid Policy Center argue that applying registration rules designed for custodians and trade executors to protocol developers and infrastructure contributors would misalign legal obligations with actual operational roles in an onchain environment.

The filing specifically requests CFTC confirmation that protocol developers do not have to register solely for creating onchain software, alongside guidance that preserves the ability of regulated market participants to use blockchain-based infrastructure for core post-trade functions.

Exempting developers and addressing non-custodial wallets

Phantom and the Hyperliquid Policy Center also ask the CFTC to formalize exemptions to prevent non-custodial wallet providers from being treated as introducing brokers.

The argument centers on responsibility and control: the groups say registration should attach to firms that manage customer funds or execute trades, while entities that provide access to non-custodial tools and software—without holding assets or directing trade decisions—should not be forced into categories meant for intermediaries that perform those actions.

They further emphasize that the regulatory baseline, as it stands, leaves US users without comparable pathways into onchain derivatives markets, while related innovation continues elsewhere. Their position is that clarity and targeted exemptions would reduce friction and allow legitimate participation without stretching existing rules beyond their original intent.

Letter to the CFTC. Source: Hyperliquidpolicy.org

What regulated exchanges and clearing firms should be able to do onchain

Beyond exemptions for developers and wallet providers, the letter seeks to remove uncertainty for established, regulated derivatives actors. Phantom and the Hyperliquid Policy Center ask the CFTC to clarify that regulated derivatives exchanges, clearinghouses, and intermediaries can use blockchain infrastructure for functions such as trade execution, clearing, settlement, margining, and recordkeeping.

Crucially, they frame this request as compatible with continuing compliance: the groups say the ability to use onchain infrastructure should be preserved as long as firms continue to meet the requirements already applicable to their regulated roles.

This is an important distinction for market participants because it positions blockchain integration as an implementation choice rather than a substitute for regulatory oversight—potentially affecting how exchanges design matching engines, how clearing systems manage accounts and obligations, and how margining and audit trails are maintained.

Broader onchain derivatives pressure on US regulators

The letter lands amid an increasingly public debate over how US regulators should approach blockchain-based derivatives. According to earlier coverage, Intercontinental Exchange (ICE) and CME Group have also pushed for how the CFTC should evaluate risks tied to onchain platforms.

In May, reporting noted that ICE and CME urged regulators to scrutinize Hyperliquid’s move into commodity-linked perpetual futures, arguing that onchain derivatives in the energy space raise market integrity and manipulation concerns. Two weeks later, ICE CEO Jeffrey Sprecher called for a “level playing field” that would allow regulated exchanges to compete with onchain perpetual futures platforms, saying existing regulation can prevent traditional firms from offering 24/7 onchain products. Sprecher also said ICE had exploratory discussions with Hyperliquid to better understand how onchain derivatives markets operate.

Meanwhile, CME has continued expanding its regulated derivatives footprint. This year, the exchange announced futures tied to Avalanche and Sui, launched CFTC-regulated Bitcoin volatility futures, and introduced Nasdaq CME Crypto Index futures—a market-cap-weighted contract tracking seven digital assets. Separately, CME also pursued legal action: in June, the exchange sued the CFTC regarding the agency’s approval of crypto perpetual futures, arguing that the regulator exceeded its authority under the Commodity Exchange Act.

Taken together, the Phantom and Hyperliquid Policy Center letter reflects the same tension seen across the sector: regulated exchanges want pathways to use onchain infrastructure without giving up compliance obligations, while innovators and infrastructure providers want exemptions that reflect how onchain systems function when users retain control and firms do not custody funds or execute trades in the traditional sense.

Readers should watch how the CFTC responds to the specific exemption requests—particularly whether it will draw clearer lines between developer activity, non-custodial tooling, and intermediary conduct, and whether it provides explicit guidance on what regulated entities may do with blockchain infrastructure while staying within existing derivatives rules.

Coinbase and Grayscale, two of crypto’s largest firms, both saw a top executive step down this week. Coinbase Chief Legal Officer Paul Grewal and Grayscale Chief Financial Officer Edward McGee announced their exits hours apart.

Both are leaving on good terms after multi-year tenures, and each firm quickly named internal successors. Neither cited any dispute.

Coinbase Legal Chief Steps Down After Six Years

Grewal notified Coinbase on July 8 that he would leave as chief legal officer and secretary, effective July 31. He joined in 2020 from Facebook, where he served as deputy general counsel. Before that, he spent more than five years as a federal magistrate judge.

During his tenure, Grewal helped take Coinbase public in April 2021. The Nasdaq direct listing made Coinbase the first major US crypto exchange to trade publicly.

He then led its defense after the Securities and Exchange Commission (SEC) sued Coinbase in 2023. The agency dropped the case with prejudice in early 2025, without any fine.

Grewal also backed Coinbase’s move to Texas from Delaware and its push for federal crypto rules. He summed up those fights in his farewell note.

“After helping to take the company public, fighting the SEC and winning, moving us from Delaware to Texas, working to get GENIUS and soon CLARITY passed into law… now is my time for new adventures,” wrote Grewal.

Follow us on X to get the latest news as it happens

Molly Abraham, a vice president of legal, will become general counsel. Grewal also named Ryan VanGrack as vice chairman. Grewal will advise Coinbase through October and stay on its trust company board.

Grayscale CFO Exits After Seven Years

McGee stepped down as chief financial officer on July 2, ending seven years with the Digital Currency Group-owned firm. Grayscale said he left for personal reasons and thanked him for his service.

His tenure covered a turning point for the firm. In August 2023, a federal appeals court ruled that the SEC had wrongly rejected Grayscale’s application. The decision led the SEC to approve spot Bitcoin (BTC) exchange-traded funds (ETFs) in January 2024.

Grayscale converted its flagship Grayscale Bitcoin Trust (GBTC) that month. The fund held about $26.5 billion at the time.

Its 1.5% fee is six times the 0.25% that BlackRock’s iShares Bitcoin Trust charges. That gap has cut the total to about $10.5 billion by the end of March 2026.

McGee also supported Grayscale’s confidential IPO filing in 2025, which the firm has since paused.

Kathryn Masci and Daniel Plourde, both senior finance executives, will serve as interim co-chief financial officers. Masci also joins the board of managers and becomes principal financial and accounting officer.

What the Coinbase and Grayscale Exits Signal

Both departures land as Washington moves toward clearer crypto rules. The GENIUS Act became law in July 2025, while the CLARITY Act still awaits a full Senate vote.

By promoting from within, both firms signaled continuity rather than a change in direction. The coming months will show how their new leaders handle the next stage.

The post Coinbase and Grayscale Executives Step Down After Major Crypto Wins appeared first on BeInCrypto.

Bitcoin mining stocks that briefly caught a bid on hopes of an AI-driven pivot are now facing a more skeptical market backdrop, according to Blocksbridge Consulting. In its Miner Weekly update, the research firm says the AI infrastructure theme—centered on data centers, power assets, and partnerships with hyperscalers—helped re-rate valuations across parts of the sector, but momentum has cooled as broader AI and chip equities have pulled back.

Blocksbridge points to the TEM AI Infrastructure Growth Index, which tracks Bitcoin miners alongside AI cloud providers, power suppliers, and other AI infrastructure-linked businesses. The index has fallen 16% over the past month, a move that has shifted investor attention toward corporate governance and whether insiders and major shareholders benefited from the earlier rally.

Key takeaways

- Blocksbridge links the prior stock re-ratings in Bitcoin mining names to an AI infrastructure narrative, which has since lost traction.

- The TEM AI Infrastructure Growth Index is down 16% over the past month, reflecting weaker sentiment across AI-adjacent equities.

- Insider selling at TeraWulf, Cipher Digital, Riot Platforms, and Core Scientific has drawn more attention, even though many transactions were reportedly executed under Rule 10b5-1 plans.

- Strategic investors are also trimming exposure, including Tether’s stake reduction in Bitdeer after Bitdeer’s AI-related rebound.

AI’s pullback changes what investors scrutinize

Blocksbridge says the AI transition initially buoyed the market’s outlook for miners that are repositioning their operations toward compute-related infrastructure. The pitch is straightforward: mining companies already control or access large-scale power generation and can leverage data-center assets, making them potential suppliers of capacity for AI-related demand.

However, when AI and semiconductor stocks retreat, the trade-off becomes harder to ignore. With fewer investors willing to underwrite optimistic long-term narratives in the face of near-term uncertainty, governance questions tend to resurface—particularly around whether insiders sold shares during periods when the story was most compelling.

In that context, Blocksbridge highlights that executives and major stakeholders have disclosed stock sales. Many of these trades were reportedly carried out using prearranged Rule 10b5-1 trading plans, which are commonly used to reduce the risk of accusations that insider information influenced transactions. Even so, Blocksbridge argues that the same routine mechanism can look less neutral when the sector narrative cools after a rapid re-rating.

Insider and strategic selling comes into focus

The Blocksbridge report draws a direct line between the easing AI sentiment and increased scrutiny of insider activity. It points to disclosed stock sales by executives at TeraWulf, Cipher Digital, Riot Platforms, and Core Scientific. Rule 10b5-1 plans are designed to create a predetermined trading schedule so that sales can occur without discretionary timing based on nonpublic information.

Blocksbridge says the sales are now attracting more attention because investors are reassessing the durability of the AI-linked valuation premium. Rather than asking only whether miners can transition into AI infrastructure providers, the market is increasingly asking whether public shareholders ultimately capture the value created by these pivots.

That skepticism also extends to non-executive investors. Blocksbridge notes that stablecoin issuer Tether reduced its stake in Bitdeer following Bitdeer’s AI-driven rebound. While the reasons for any individual investor’s changes in exposure may be complex, the broader pattern—strategic capital trimming risk as sentiment fades—adds another layer to governance and alignment concerns.

TeraWulf singled out after a high-profile AI infrastructure deal

Blocksbridge describes TeraWulf as the clearest example of how insider activity can become especially visible when a company is viewed as a leading beneficiary of the AI infrastructure shift. It says CEO Paul Prager and Beowulf E&D Holdings, an entity the CEO manages, sold roughly 1.59 million WULF shares.

The timing becomes notable in the report’s framing because it occurred ahead of, or around the period of, a deal widely viewed as validation of TeraWulf’s AI strategy. Blocksbridge ties the spotlight to the company’s announcement of a 20-year AI infrastructure lease with AI developer Anthropic, referenced in earlier reporting from Cointelegraph: “Terawulf shares rise after 19B Anthropic AI lease, JV sale”.

For investors, this kind of juxtaposition matters because it forces a hard question: are insiders reflecting a long-term conviction in the transition, or are they de-risking after the stock has already priced in a meaningful portion of the upside? Rule 10b5-1 plans don’t eliminate that interpretive tension—they simply shape the legal and compliance framework around how the trades occur.

The valuation problem behind AI infrastructure spending

Blocksbridge’s report also broadens the discussion beyond Bitcoin miners to the AI sector itself. Many miners have moved into AI data-center positioning as traditional mining economics have grown tougher, particularly after Bitcoin’s 2024 halving tightened industry margins.

But the AI infrastructure trade is no longer empty space. Blocksbridge argues it has become crowded and is facing mounting pressure from investors to justify large capital expenditures against uncertain payoffs. In a report published by Deloitte in October, AI was described as a “paradox of rising investment and elusive returns,” reflecting the view that many organizations may need more time than expected to turn AI spending into measurable value.

Additional perspective in the Blocksbridge update comes from Teneo research based on a survey of more than 350 public company CEOs. That work suggested fewer than half of AI initiatives delivered returns exceeding their costs.

These findings don’t negate the long-term demand thesis for compute capacity—but they do highlight why miners attempting to capture AI-related demand may face a harder path to convincing equity markets. The sector may benefit from access to power and existing infrastructure, yet the equity valuation mechanism still depends on credible timelines for monetization and measurable returns.

In this environment, investors appear to be shifting from the simplicity of the AI pivot story toward a more demanding checklist: execution milestones, evidence of customer pull-through, and whether governance signals align with shareholders’ long-term interests.

Going forward, the market’s key question will likely be whether miners can translate their AI infrastructure positioning into durable, shareholder-visible returns—while insiders and major investors’ selling patterns remain an unavoidable data point during periods of weakening AI sentiment.

Crypto World

Hyperliquid Policy Center, Phantom Urge CFTC To Ease Onchain Software Registration Rules

TLDR:

- HPC and Phantom filed a joint letter urging CFTC to clarify registration rules for developers.

- The letter asks CFTC to give registered exchanges a path to adopt onchain infrastructure.

- HPC and Phantom want the Phantom no-action letter codified into a permanent formal rule.

- The filing responds directly to a CFTC request on rules hindering market participants.

Hyperliquid Policy Center and Phantom have urged the CFTC to clarify that publishing onchain protocol software does not require registration.

The two firms submitted a joint comment letter this week addressing onchain market infrastructure. Their filing asks regulators to modernize outdated rules built around custodial intermediaries.

It calls for a clear registration pathway for exchanges adopting onchain systems. The letter also pushes to codify the existing Phantom no-action letter into formal policy.

HPC And Phantom Detail Registration Concerns

Hyperliquid Policy Center and Phantom compare software developers to internet service providers. The letter states “no one confuses either person for the other” between builders and brokers.

An internet provider supplies cables that let brokers take customer orders. The letter argues protocol developers deserve the same clear distinction under CFTC rules.

Digital asset builders have not received consistent treatment from past CFTC leadership. The letter notes developers were left “guessing whether they may be treated as operating an unregistered exchange.”

This ambiguity pushed many companies to build their products offshore instead. HPC and Phantom credit current leadership under Chairman Selig with shifting this approach.

Onchain markets differ structurally from traditional custodial trading systems, the letter notes. Legacy markets pass customer funds through brokers, exchanges, and clearinghouses sequentially.

The filing states onchain systems “let users hold their own funds and trade directly with one another.” Hyperliquid Policy Center and Phantom say regulation should reflect this fundamental difference.

Three recommendations anchor the joint submission to the Commission. Confirm first that publishing protocol software alone does not require registration.

Second, create pathways for registered exchanges to adopt onchain infrastructure directly. Third, convert the Phantom no-action letter into what the filing calls “a formal rule.”

Firms Frame Request As Path To Onshore Growth

HPC and Phantom present their proposal as a route to bring innovation onshore. The letter states protections can be built in “by design rather than by decree.”

Regulated intermediaries would continue handling responsibilities that code alone cannot resolve. This structure preserves protections while modernizing infrastructure for onchain derivatives markets.

The letter responds to a CFTC request asking which rules hinder market participants. HPC and Phantom write, “this is our answer, and it is within the Commission’s own authority to act on.”

They state the requested changes fall within the Commission’s existing regulatory authority. No new legislation would be required to implement these clarifications.

Codifying the Phantom no-action letter would benefit smaller non-custodial wallet providers broadly. The filing notes such firms would gain “durable certainty rather than having to ask, one at a time, for relief.”

Firms would gain lasting certainty instead of requesting individual relief repeatedly. This reduces friction for developers building non-custodial financial technology tools.

Existing registrants also stand to benefit from the proposed regulatory pathway. Exchanges and clearinghouses could retire legacy systems for transparent onchain alternatives instead.

Compliance obligations would remain intact under the new registration framework. HPC and Phantom describe this transition as advantageous for American consumers.

The joint letter reflects continued engagement between digital asset firms and federal regulators.

Paul Grewal has announced that he will step down as Coinbase’s chief legal officer on July 31, handing over leadership of the exchange’s legal team just days before the US Senate is expected to resume work on the CLARITY Act.

Summary

- Paul Grewal will leave his role as Coinbase chief legal officer on July 31 and become an adviser.

- Molly Abraham will become general counsel as Congress prepares to revisit the CLARITY Act.

- Coinbase continues pushing for crypto market structure legislation after its SEC lawsuit was dismissed.

According to posts Grewal published on X and LinkedIn, he will move into an advisory role at Coinbase after serving as the company’s chief legal officer since 2020. The announcement also confirmed that legal vice presidents Molly Abraham and Ryan VanGrack will take on expanded responsibilities, with Abraham becoming general counsel and VanGrack serving as vice chair.

In a separate LinkedIn post, Abraham said she would take charge of Coinbase’s legal organization following the transition.

During Grewal’s tenure, Coinbase navigated one of the most closely watched legal battles in the US crypto industry. As chief legal officer, he led the company’s response after the US Securities and Exchange Commission sued Coinbase in 2023, alleging that the exchange had operated as an unregistered securities exchange, broker, and clearing agency.

The lawsuit was later dismissed under the Trump administration, ending one of the regulator’s highest-profile enforcement actions against a crypto company.

Before leaving the role, Grewal also said in his social media posts that he would reveal his next professional position “in due course,” without providing additional details.

Coinbase leadership changes arrive as Congress debates crypto rules

The timing of Grewal’s departure coincides with renewed attention on digital asset legislation in Washington. Coinbase executives, including chief executive Brian Armstrong, have repeatedly urged lawmakers to pass the Digital Asset Market Clarity Act (CLARITY), arguing that the legislation would establish clearer regulatory responsibilities for the crypto industry.

The proposed bill would move much of the oversight of digital asset markets from the Securities and Exchange Commission to the Commodity Futures Trading Commission. The US Senate is currently on a state work period and is expected to return on Monday, when lawmakers could resume consideration of the legislation.

The leadership transition also comes after Coinbase strengthened its presence in US policy discussions over the past two years. Following the dismissal of the SEC case, the exchange expanded its engagement with lawmakers and government officials while continuing to advocate for digital asset legislation.

Coinbase has expanded its political engagement during regulatory debates

Coinbase has also increased its involvement in US political advocacy during the ongoing debate over crypto regulation. The company is among the largest contributors to the Fairshake political action committee, which supports candidates it considers favorable toward digital asset policies.

Separately, Armstrong has met with US President Donald Trump and has publicly called on Congress to pass legislation establishing a clearer legal framework for cryptocurrencies. Those efforts have continued alongside Coinbase’s participation in policy discussions surrounding the CLARITY Act and other crypto-related proposals.

Although Grewal will no longer oversee Coinbase’s legal department after July 31, the company’s legal strategy will remain in the hands of executives who have worked alongside him through recent regulatory disputes.

Abraham’s appointment as general counsel places her in charge of legal operations as Congress prepares for another round of debate over market structure legislation that could reshape how digital assets are regulated in the United States.

Coinbase chief legal officer Paul Grewal will transition to an advisory role at the exchange starting July 31, according to an announcement he shared on X and LinkedIn.

In the same update, Grewal said Coinbase’s current legal vice presidents—Molly Abraham and Ryan VanGrack—will move into expanded leadership roles as general counsel and vice chair after his departure at the end of the month. Abraham added that she will “take the helm” of the company’s legal team.

Key takeaways

- Paul Grewal is leaving Coinbase’s day-to-day legal leadership on July 31, shifting to an advisory capacity.

- Molly Abraham and Ryan VanGrack are set to take over top legal governance roles as Coinbase reorganizes internally.

- Grewal previously led Coinbase’s legal response to the SEC’s 2023 enforcement action alleging unregistered exchange, broker, and clearing activity.

- Coinbase executives continue to press Congress on legislation that would move major digital-asset oversight from the SEC toward the CFTC.

A leadership handoff in Coinbase’s legal department

Grewal’s announcement marks a notable change at the center of Coinbase’s legal strategy. He has served as the exchange’s chief legal officer since 2020, overseeing the company’s engagement with regulators during a period when US crypto policy and enforcement have repeatedly shifted.

Under the plan Grewal described, Abraham will assume responsibility for directing Coinbase’s legal team as general counsel, while VanGrack will take on a vice-chair role. Grewal indicated that he would announce a potential new position “in due course,” but did not provide further specifics at the time of his post.

Why Grewal’s role carried regulatory weight

As CLO, Grewal played a prominent part in Coinbase’s legal posture during the SEC’s 2023 case. In that action, the SEC alleged that Coinbase operated as an unregistered securities exchange, broker, and clearing agency. Coinbase and its executives challenged the claims, and the lawsuit was later dismissed under the Trump administration.

The significance of a CLO at a major exchange extends beyond courtroom strategy: it often shapes how a company navigates evolving enforcement theories, responds to regulator guidance, and supports legislative engagement. Grewal’s move to advisory status therefore raises an obvious question for the market—how much influence will shift with the leadership change, even if Coinbase’s broader policy approach remains constant.

Coinbase has long portrayed its policy efforts as aligned with clearer regulatory boundaries for digital asset markets, and Grewal’s involvement has historically been a part of the exchange’s public-facing legal narrative.

Coinbase’s push for market-structure legislation continues

Even as Grewal transitions roles, Coinbase’s policy priorities appear unchanged. The company has been actively encouraging lawmakers to advance the Digital Asset Market Clarity Act (CLARITY).

According to the reporting referenced in the source material, CLARITY is widely expected to alter the regulatory framework for digital assets by shifting oversight and regulation from the SEC toward the Commodity Futures Trading Commission (CFTC). That framework change would matter to market participants because it could redefine which regulator is responsible for key aspects of crypto market supervision.

The source also notes that the US Senate is in a state work period until Monday, when lawmakers are expected to return and potentially take up a vote on the bill. For traders, issuers, and exchanges, the timing of committee movement and floor consideration can influence expectations around compliance costs and the likelihood of future regulatory certainty.

What investors should watch next

Grewal’s transition doesn’t automatically signal a policy pivot—Coinbase’s top leadership has continued to emphasize legislative clarity, and the exchange’s legal structure is being redistributed rather than dismantled. Still, the appointment and influence of whoever effectively holds the reins after the July 31 transition will be closely watched by anyone tracking US crypto regulatory risk.

With the Senate schedule potentially affecting CLARITY’s near-term momentum, the key question is how Coinbase’s legal leadership will shape engagement with lawmakers and regulators as the political process moves forward. Readers should monitor any further updates from Coinbase regarding Grewal’s advisory responsibilities and any concrete legislative or regulatory developments that follow the Senate’s return.

Key Takeaways

- CoreWeave shares declined 3.4% to close at $83.53, touching an intraday bottom of $79.46, while volume trailed the daily average by 20%

- Analysts hold a Moderate Buy rating with a consensus price target of $135, with bullish forecasts reaching as high as $250

- Investor anxiety is mounting over Meta’s reported plans to enter the AI cloud computing space, potentially challenging CoreWeave’s market position

- Company insiders have offloaded more than $3 billion in shares over the last three months, primarily through tax withholding arrangements

- The company’s Q1 results fell short of expectations with EPS of -$1.40 versus the -$1.17 estimate, despite revenue jumping 111.6% annually to $2.08 billion

CoreWeave (CRWV) experienced a 3.4% pullback on Tuesday, settling at $83.53 following an intraday descent to $79.46. The previous trading session had concluded at $86.46.

CoreWeave, Inc. Class A Common Stock, CRWV

Trading activity registered approximately 23 million shares, falling roughly 20% short of typical volumes — indicating the downturn wasn’t fueled by mass liquidation.

Year-to-date, the stock maintains a 26% gain, though it’s nursing a 41% decline over the trailing twelve months and trading considerably beneath its 50-day moving average of $106.86.

Tuesday’s weakness reflected mounting investor apprehension centered on two key issues: Meta’s reported AI computing infrastructure ambitions and persistent insider share dispositions.

A Bloomberg piece highlighted Meta’s exploration of commercializing AI computing services and infrastructure capacity to external clients — a strategic direction that would place it squarely against CoreWeave’s primary revenue streams.

Rosenblatt upheld its Buy stance with a $250 target, contending the Meta threat is exaggerated. Both Wolfe Research and Evercore ISI confirmed Outperform positions with matching $150 targets.

Executive Stock Dispositions Draw Attention

Insider transactions have become a focal point. Throughout the preceding 90 days, company insiders have divested more than $3 billion in CRWV shares.

Most recently, General Counsel Kristen J. McVeety disposed of 22 shares for $1,889 on July 6, conducted under a Rule 10b5-1 arrangement established in May 2025.

Prior to that, insider Brian Venturo unloaded 76,912 shares on July 1 at an average price of $86.99, generating approximately $6.69 million. This transaction trimmed his holdings by 21%.

Insider Brannin McBee divested 56,707 shares on June 30 at $95.69, totaling roughly $5.43 million — reducing his stake by 14.9%.

Both transactions occurred through predetermined Rule 10b5-1 arrangements designed to satisfy tax liabilities on equity compensation vesting. While this represents standard practice, the magnitude has nonetheless attracted market attention.

Recent Earnings Disappointment Lingers

CoreWeave’s most recent quarterly disclosure on May 7 added to sentiment headwinds. The firm recorded EPS of -$1.40, falling short of the -$1.17 consensus projection by $0.23.

Revenue reached $2.08 billion, representing 111.6% year-over-year expansion. While top-line momentum remains robust, profitability challenges persist — the net margin currently registers at -25.57%.

Wall Street’s consensus forecast anticipates full-year EPS of -$4.57.

Notwithstanding the earnings shortfall, multiple analysts contend the sell-off is excessive. BNP Paribas holds the Street’s most optimistic target at $192, with Cantor Fitzgerald at $167. Wells Fargo elevated its objective to $155 in May.

Among 35 analysts tracking the equity, 21 assign Buy ratings, 12 recommend Hold, and 2 suggest Sell.

The company’s debt-to-equity ratio registers at 3.68, accompanied by a current ratio of merely 0.31 — a financial structure that introduces meaningful risk alongside the growth narrative.

CoreWeave’s market capitalization hovers between approximately $37–45 billion, fluctuating with market conditions. The company unveiled ARIA, an AI-powered research assistant, earlier this week — though analysts view it as lacking immediate catalytic potential.

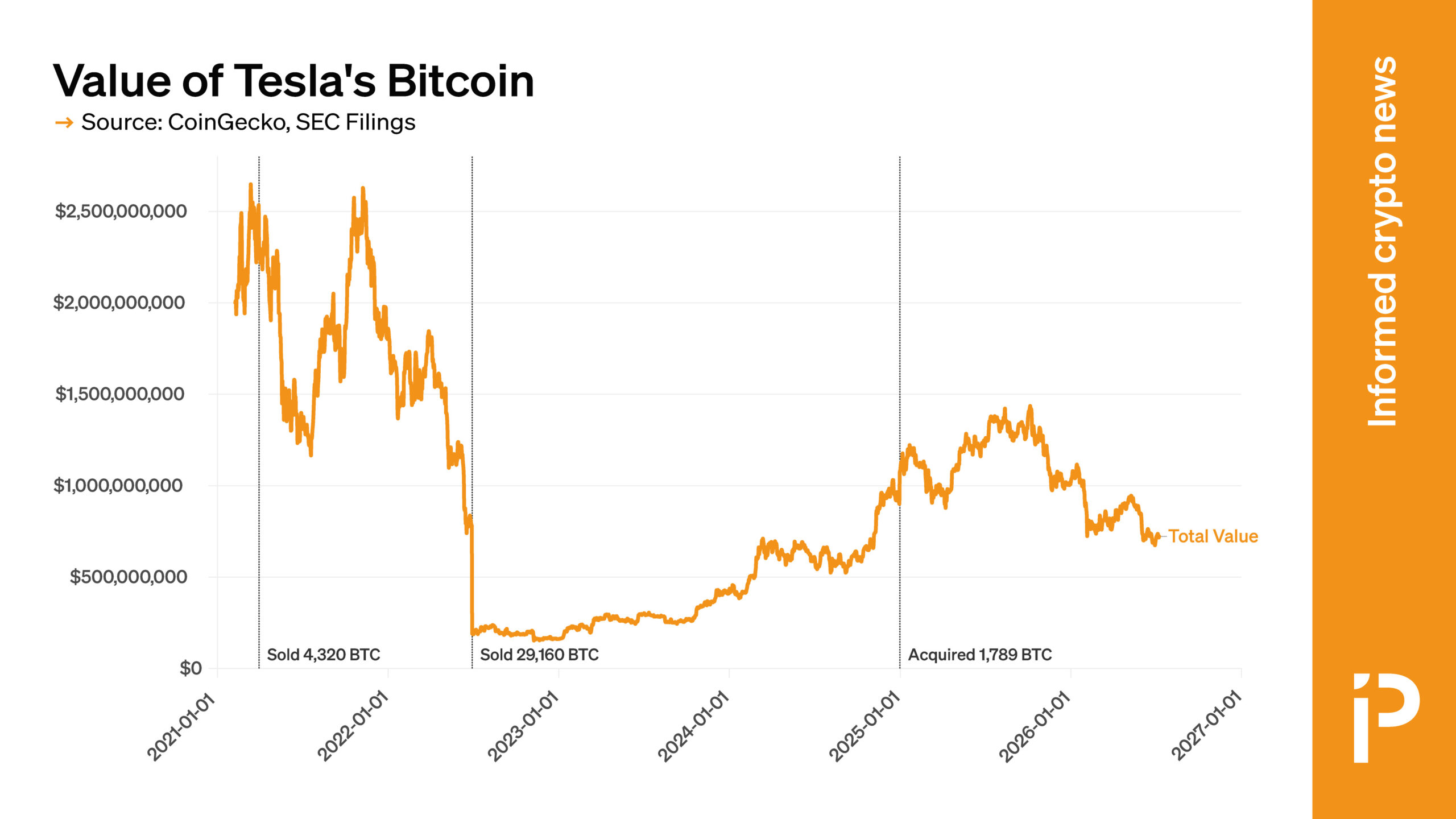

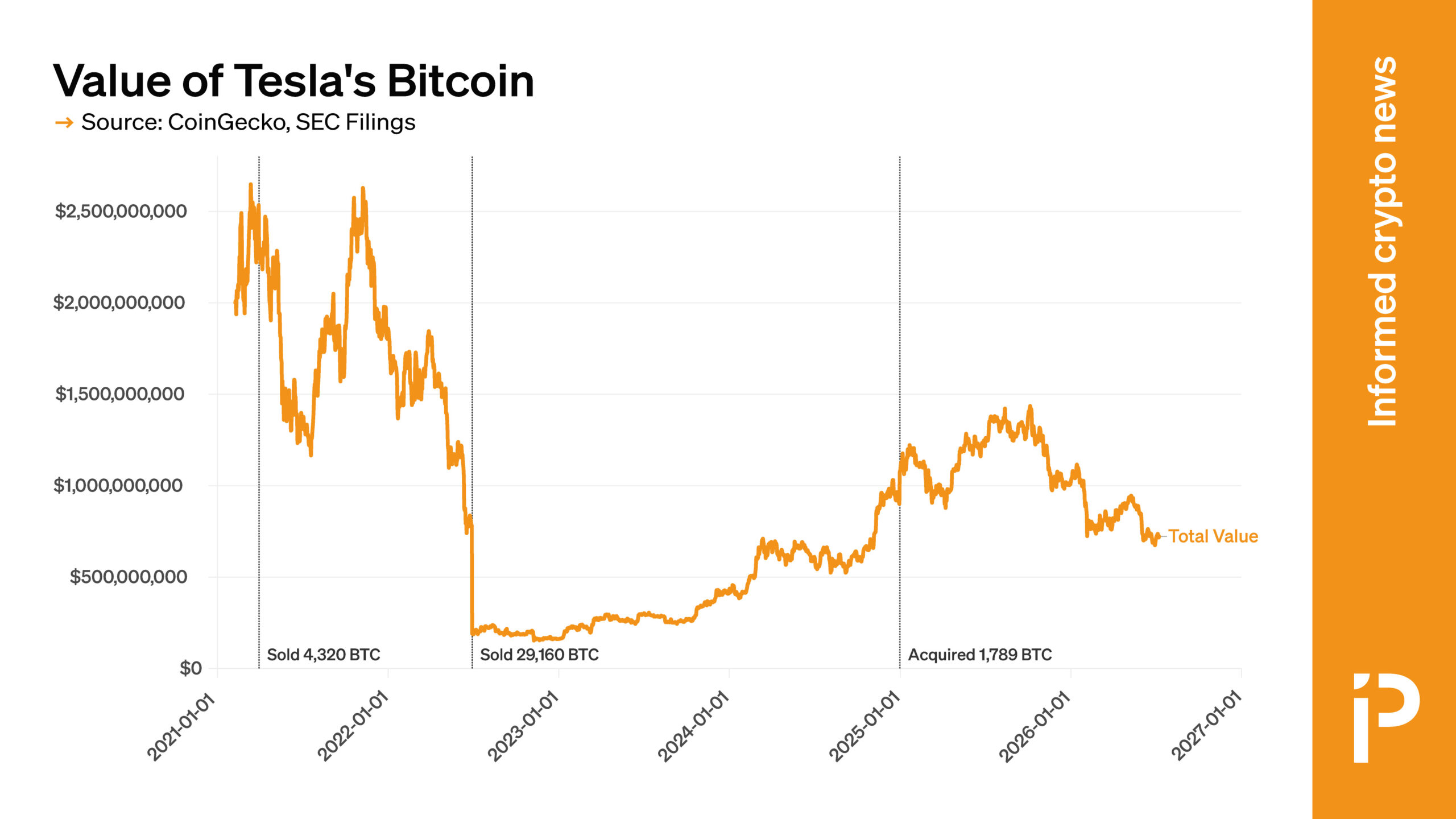

Tesla became one of the early firms to embrace BTC, adding it to its balance sheet in 2021; however, it all but abandoned this initiative, and the total value of its holdings has fallen by two-thirds, despite BTC appreciating by more than 30%.

During this same period Elon Musk, the founder and leader of Tesla, has gone from a frequent cryptocurrency promoter to someone who rarely mentions or endorses it.

This depression in value has occurred despite the fact that Musk had unprecedented access to the federal government early in Donald Trump’s second administration through the so-called “DOGE” initiative.

This access also coincided with a period when the administration was rapidly trying to shift its regulatory stance to support Trump’s vision of himself as a supporter of the crypto industry, which has embraced him.

Read more: Elon Musk now worth more than 200 Donald Trumps

In 2021 Tesla originally acquired 43,200 BTC and announced that it expected “to begin accepting BTC as a form of payment for our products.”

Around this same time, Musk had added “#bitcoin” to his Twitter bio, after which the asset briefly surged. He also appeared on a voice chat on social media site Clubhouse to say that he was a supporter of BTC.

However, Musk’s Tesla didn’t maintain this stash of BTC indefinitely.

Read more: Elon Musk promised to fund Dogecoin, now the foundation accounts are overdue

Less than two months after this acquisition, Musk took to Twitter to explain that Tesla had to start selling in order “to prove liquidity of BTC as an alternative to holding cash on balance sheet.”

Two months after that initial sale, Musk again took to Twitter to announce that Tesla would no longer be accepting BTC payments.

He cited concerns “about rapidly increasing use of fossil fuels for BTC mining” and added that Tesla would use it for transactions again once “mining transitions to more sustainable energy.”

After this, there was a relatively long pause — until the middle of 2022, to be precise — before Tesla sold 29,160 BTC, leaving only 9,720 in its holdings.

This remained the stable amount for over two years until it was revealed at the end of 2024 that the company had purchased an additional 1,789 BTC, bringing its total to 11,509.

However, Tesla’s holdings have continued to lose value since then as the price of BTC has suffered.

It described this purchase as an “immaterial amount.”

Musk has not wholly moved on from Bitcoin.

Despite previously claiming that Tesla cannot accept it because of “rapidly increasing use of fossil fuels for BTC mining,” last year he promoted the asset by stating, “That is why Bitcoin is based on energy: you can issue fake fiat currency, and every government in history has done so, but it is impossible to fake energy.”

BTC has fallen by over 40% since Musk made this point.

Broadly, it’s not entirely clear what Musk or Tesla thinks of BTC, whether it is a powerful alternative to fiat or a threat to the environment.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

At the last moment, New Hampshire has turned its back on a groundbreaking effort to establish what was expected to be the first rated, bitcoin-backed bond issued under a state’s authority, with a governmental body there canceling the project.

Just a few months after Moody’s Ratings gave the bond a Ba2 rating, the New Hampshire Executive Council, which reviews major state financial actions, slammed the door with a 3-2 decision that sided with those concerned about the state’s financial reputation.

The financial instrument was to be issued by the Business Finance Authority of the State of New Hampshire, backing a private-sector bond of up to $100 million tied to Bitcoin mining and datacenter firm CleanSpark. The council’s vote was the final step.

“It was an extremely short-sighted decision,” Keith Ammon, a longtime crypto advocate and the majority floor leader in the New Hampshire House of Representatives, posted on social media site X. “They should gather all relevant facts and information and reconsider their vote at a future meeting.”

Ammon told CoinDesk that it’s an election year for council members, and it only takes one to swing the vote, adding, “We’re not giving up.”

Bitcoin reclaimed the $63,000 level on Thursday, but traders are approaching Friday’s $1.4 billion Bitcoin options expiry on Deribit with caution. The central debate is whether macro pressure—particularly rising US Treasury yields—will undermine BTC’s rebound and put the $62,000 support zone to the test.

While US bond yields pushing toward 4.6% have kept risk appetite cautious, Deribit positioning appears to be more balanced than outright bearish. That mix is setting up a weekend-or-later decision point for BTC’s short-term direction.

Key takeaways

- US 10-year Treasury yields nearing 4.6% are weighing on risk assets, reinforcing fears about debt concerns and tighter financial conditions.

- Deribit’s balanced put-to-call activity suggests downside demand is not dominating ahead of Friday’s large options expiry.

- Open interest and strike concentration point to key levels around $62,000, $61,000, and $63,500 for near-term price behavior.

- For bulls to extend their edge, BTC needs to hold above key expiry-related thresholds; otherwise, the market may remain rangebound.

Treasury yields and risk appetite: why BTC is stuck near $63K

The move in US government bond yields is driving much of the near-term caution. With the US 10-year yield approaching 4.6%, investors appear increasingly concerned about the expansion of government debt and the likelihood that additional monetary policy support may be needed to avoid a recessionary slowdown.

That backdrop has influenced Bitcoin’s trading behavior. BTC has largely been moving sideways, while equities—at least in the Nasdaq-100—have been holding relatively close to record levels. On Thursday, technology momentum continued to attract capital, supported by market-moving activity in semiconductors.

According to the article, SK Hynix’s US initial public offering was oversubscribed, contributing to strength across parts of the AI-linked chip complex. The result was a risk-on bid in equities, with Arm Holdings up about 10%, Advanced Micro Devices higher by roughly 7%, and Micron gaining around 7% intraday.

Still, equities strength does not automatically translate into sustained BTC upside when bond yields are rising. Bitcoin tends to react to shifts in global liquidity expectations, and bond yield pressure can quickly change the market’s risk calculus.

ETF flow worries cool off—options demand looks more balanced

Spot Bitcoin ETF flows briefly came back into focus on Wednesday, when the market saw $85 million in net outflows, ending a short run of three consecutive days of inflows. Earlier coverage by Cointelegraph linked that outflow episode to broader selling pressure in spot ETF markets.

However, the presence of outflows alone does not clarify whether institutions have shifted structurally bearish. More importantly for the near-term trade is how derivatives positioning has evolved into Friday’s expiry.

Deribit activity has been described as “balanced” between calls and puts, implying that demand for downside exposure has not surged. The key point is that options volumes over the past few days did not show a clear stampede into protective puts.

As cited in the piece, Laevitas data shows the put-to-call volumes relationship remains supportive of range stability. Even though call activity has outpaced put volume over four days—suggesting traders have trimmed urgency around downside—this is not the same as a market that is fully discounting volatility.

Deribit expiry setup: where the market’s incentives cluster

Friday’s weekly options expiry involves a large notional figure of $1.4 billion on Deribit, and the strike distribution matters for how price can “pin” near certain levels. The article highlights an interesting imbalance in the immediate strike zones.

Calls up to the $62,500 region amount to about $137 million, while puts above $61,000 total roughly $121 million. That does not imply an outright one-sided bet, but it does indicate that there is meaningful positioning both for upside continuation and for defense just below the middle of the range.

Open interest and strike placement also shape traders’ expectations for pinning behavior. With BTC positioned around the $63,000 area heading into expiry, the next move could be influenced by how market makers and hedgers respond to gamma exposure across key strikes. The article references Deribit open interest data for July 10 BTC, underscoring that the market is not operating without “gravity” around specific prices.

Within this framework, the piece outlines conditional outcomes: bulls would strengthen their position materially with a move above $63,500 by the 8:00 AM UTC expiry on Friday, while bears maintain a smaller edge below $61,000. Without additional macro or catalyst-driven volatility, the market may not deliver a decisive breakout purely from derivatives positioning.

Oil, geopolitics, and bond yields: what could break the range

Beyond crypto-native signals, the article points to two macro variables that could shift demand between fixed income and risk assets: energy and Treasury yields. A temporary truce in the Middle East could ease recession fears, encouraging capital rotation into higher-risk markets—an environment that typically supports BTC.

On the other hand, the piece also notes an ongoing counterweight. It argues that persistent uncertainty in the macro outlook, including the risk of additional large Treasury issuance to cover debt growth, could keep pressure on yields and dampen crypto upside attempts.

Traders are also asked to watch crude oil direction. A renewed escalation around Iran could push oil higher, worsening inflation fears and potentially forcing a less favorable policy outlook—conditions that tend to complicate liquidity for risk assets.

Crucially, the article ties these macro considerations back to options behavior: with put-option buying remaining restrained in recent sessions, BTC appears positioned to defend the $62,000 support level, at least in the immediate term. Still, that defense is not guaranteed. The market’s stability depends on whether bond yields ease and whether geopolitical risk stops feeding into inflation and rate expectations.

For now, the near-term picture is conditional: a successful expiry resolution above $63,500 could deliver short-term relief, but sustained upward progress would likely require a more supportive macro shift. Until then, traders may have to manage expectations for a range that can hold—but also revert quickly if yields keep climbing.

As Friday’s options expiry approaches, the key variables to watch are whether Treasury yields cool off and how price reacts around $63,500 and $62,000 into the settlement window—levels that derivatives positioning is effectively steering toward.

Stock Market Explained! #shorts #trendingshorts #trending

Canada’s Carney defends his trip as he visits Saudi Arabia

Micron CEO details $250 billion US investment amid chip, memory shortage

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: High Hopes

-

NewsBeat5 days ago

NewsBeat5 days agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Crypto World6 days ago

Crypto World6 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

Fashion3 days ago

Fashion3 days agoOpen Thread: What Great Books Have You Read Recently?

-

Politics6 days ago

Politics6 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Fashion12 hours ago

Fashion12 hours agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

News Videos3 days ago

News Videos3 days agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Tech3 days ago

Tech3 days agoAnthropic’s new “J-lens” reveals a silent workspace inside Claude that mirrors a leading theory of consciousness

-

Crypto World6 days ago

ESMA Expands Crypto Register by 37 Firms Following MiCA Transition Period

-

Business3 days ago

Business3 days agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Sports2 days ago

Sports2 days agoJoshua Pacio ‘more complete’ ahead of ONE rematch vs Malachiev

-

Crypto World4 days ago

Crypto World4 days agoSouth Africa proposes crypto tax guidance under existing rules

-

Crypto World3 days ago

SK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

News Videos3 days ago

News Videos3 days agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

Tech4 days ago

Tech4 days agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

Business7 days ago

Business7 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Sports2 days ago

We have punished the disrespect

-

News Videos3 days ago

News Videos3 days agoAvoid entering in FOMO #bitcoin #cryptocurrency #trading #scalping

-

Crypto World7 days ago

Crypto World7 days agoAlibaba bans Claude Code over alleged backdoor security concerns

-

Tech5 days ago

Tech5 days agoNeuralink Threads Its Way Straight Through the Brain’s Armor

You must be logged in to post a comment Login