Crypto World

What is a transfer agent in tokenized securities?

Crypto spent fifteen years arguing the ledger is the truth. Tokenized securities quietly reversed it. The token in your wallet is a receipt, and a company you have never heard of keeps the record that actually decides who owns what.

Summary

- A transfer agent maintains the official register of who owns a security, processes subscriptions and redemptions, issues and cancels shares, and pays out distributions. In the United States they must register with the SEC.

- In tokenized securities, the transfer agent’s off-chain register remains the authoritative legal record of ownership. The token is a digital representation that enables on-chain mobility, not the source of truth.

- If the blockchain and the register disagree, the register wins. Administrators including JPMorgan retain authority to correct the on-chain ledger against the legal record.

- Transfer agents run the allow-list. They screen identity, add approved wallets to an on-chain list, and the token contract blocks transfers to any address that is not on it.

- This inverts crypto’s founding assumption. Whether that is a betrayal or the precise reason institutions will tokenize anything at all is the argument worth having.

Every crypto explainer starts from the same premise: the blockchain is the record, possession of the key is ownership, and no intermediary can reverse it. That premise is true for Bitcoin. It is false for essentially every tokenized security in existence, including the ones BlackRock and JPMorgan are issuing right now. In those products, the authoritative record of who owns what is a database maintained by a company called a transfer agent, and the token in your wallet is a mirror of that database. If the two diverge, the database is right, and the chain gets corrected. Understanding this is not a technicality. It is the difference between understanding what tokenized securities are and repeating a marketing claim about them.

What a transfer agent does

The transfer agent is one of the least glamorous and most load-bearing roles in traditional finance. It exists because a company issuing shares needs someone to answer a deceptively hard question: who owns them right now?

The core functions are these. The transfer agent maintains the register of security holders, the official list of names and balances. It processes transfers when securities change hands, updating that register. It issues new shares when investors subscribe and cancels them when investors redeem. It distributes dividends, interest, and other payments to the holders on the register. And it handles corporate actions, communications, and the reconciliation that keeps everything consistent.

In the United States, transfer agents must register with the SEC under the Exchange Act and operate under its rules. This is not an informal bookkeeping role. It is a regulated function with legal consequences, because the register the agent maintains is what a court would consult to determine ownership.

Traditionally, shares in most listed securities are recorded through a central securities depository, with the Depository Trust and Clearing Corporation performing that function in the US. Each institution keeps its own books, and post-trade steps such as confirmation, clearing, and settlement require multiple intermediaries and repeated reconciliation between those books. The transfer agent sits inside that architecture as the issuer’s official record-keeper.

What changes when a security gets tokenized

The pitch for tokenization is that a shared, consensus-validated ledger replaces fragmented books and eliminates the reconciliation. Instead of every institution maintaining a separate record that must be checked against every other record, all participants read one ledger.

In practice, tokenized securities did not do that. They did something more modest and more interesting.

Tokenized funds use distributed ledger technology to issue and maintain their shares instead of recording them solely through a central depository. That is a real change: settlement collapses from a T+1 or T+2 cycle to minutes, and the share becomes programmable. But the transfer agent did not disappear. It moved.

The structure now looks like this. The transfer agent still maintains the official ownership record. A tokenization platform, most prominently Securitize and also Tokeny, runs the smart contracts that mint tokens on subscription and burn them on redemption. An oracle, typically Chainlink, publishes the fund’s net asset value on-chain. And the token contract enforces the transfer restrictions that the transfer agent’s compliance rules require.

Securitize Transfer Agent LLC is the reference example. It is an SEC-registered transfer agent and broker-dealer, and it maintains the official record for BlackRock’s BUIDL fund. BlackRock’s filing for its OnChain Shares describes Securitize Transfer Agent as maintaining the official record through a permissioned system connected to multiple public, permissionless blockchains, with wallets linked to off-chain identity records.

Franklin Templeton’s structure works the same way: one FOBXX share links to one BENJI token, while the transfer agent maintains the official ownership record through the Benji platform.

Read those descriptions carefully and the architecture becomes clear. A permissioned system, connected to public blockchains, with wallets linked to off-chain identity. The chain is a distribution and mobility layer bolted onto a conventional register. It is not the register.

The token is not the record

This is the single most important idea here, and it is stated backwards in most coverage.

The beneficial ownership of tokenized fund shares remains recorded in the transfer agent’s official register. The token acts as a digital receipt that enables on-chain movement. When a token transfers between two authorized wallets, the system updates the off-chain ownership record to reflect the change. The chain does not replace the register; it triggers an update to it.

And when they disagree? The register wins. JPMorgan, among others, retains the authority to correct discrepancies between the on-chain ledger and the legal record, so that the technological holding never diverges from the legal reality. There is a company with a button that can change what your wallet says, because your wallet was never the authority.

Holding the token does not, by itself, prove ownership. The exact rights depend on the fund’s legal documents, the official ownership record maintained by the transfer agent, and the product’s wallet and transfer rules. The official record is generally the authoritative source.

Consider what that means for a scenario crypto users take for granted. You send tokens to a friend’s wallet. In Bitcoin, that is final and your friend owns them. In a tokenized security, either the transfer fails because the wallet is not allow-listed, or it succeeds and the transfer agent updates the register to reflect the new holder, which happens only because the wallet was pre-approved and identity-linked. There is no version of that transaction where a stranger acquires the security by receiving the token.

Who controls the allow-list

The transfer agent’s most consequential power in tokenized securities is not record-keeping. It is the gate.

Before any subscription, the transfer agent runs know-your-customer and sanctions screening on the wallet owner. The wallet address is then added to an on-chain allow list maintained by the token contract. Smart contracts enforce restrictions from that list: any transfer to an address that is not allow-listed reverts. The BIS has noted that these products rely on the allow-listing of blockchain wallets to constrain peer-to-peer trading and meet regulatory compliance requirements.

The enforcement lives in the token standards. Where stablecoins typically use plain fungible standards such as ERC-20 with unrestricted transfers, tokenized securities often employ security token standards such as ERC-1400 or ERC-3643. Under ERC-3643, a function called isVerified confirms that a recipient appears in the register of allow-listed investors, and canTransfer enforces any additional conditions required before a transfer proceeds. As compliance needs evolve, programmable checks let more complex rules be applied in code.

That is the whole architecture in one sentence: compliance rules, written by a regulated intermediary, enforced automatically by a smart contract, on a public blockchain that anyone can read and almost nobody can transact on.

The practical consequences are worth spelling out. Moving a token to a wallet not on the allow list may be blocked at the protocol or transfer agent level, which is why verifying transfer eligibility before attempting to move a position is not optional. Access through secondary markets or unapproved wallets may not carry the same rights as subscribing directly through the fund or its authorized platform. And restrictions vary sharply by product: some funds are limited to qualified purchasers, some exclude US persons entirely, some impose institutional minimums.

Why this exists

It would be easy to read all of this as institutions gutting the point of a blockchain. The steelman is stronger than that, and it deserves stating properly.

Securities law does not care what technology you use. If an instrument is a security, then rules about who may hold it, how ownership is evidenced, what disclosures are owed, and how sanctions screening works all apply regardless of whether the record sits in Oracle or Ethereum. A tokenized fund that let anonymous wallets hold shares would not be an innovation. It would be an unregistered securities offering with an anti-money-laundering failure attached.

The allow-list model is what makes tokenized funds work inside existing securities and AML frameworks. Without it, none of these products would exist, because no regulated manager would issue them and no regulator would permit it. The choice was never between a permissioned tokenized fund and a permissionless one. It was between a permissioned tokenized fund and no tokenized fund.

And the benefits are real even with the gate in place. Settlement in minutes instead of days. Around-the-clock operation. Shares usable as collateral without leaving the fund, which is why crypto prime brokers accept BUIDL as margin. Real-time auditable records for regulators. Programmability that lets a share do things a book entry cannot. None of that requires the ledger to be the final authority. It only requires the ledger to be fast, shared, and honest about what it is.

The counterargument is equally real. If an intermediary maintains the authoritative record, screens participants, and can reverse the chain, then the blockchain is performing the role of a message bus, and a permissioned database could deliver most of the benefits with less complexity. The transparency argument weakens too, since the interesting record is off-chain. What you are left with is faster settlement and composability with other on-chain assets, which is genuinely valuable but a long way from disintermediation.

Where the two worlds are colliding

The most interesting developments sit exactly at this seam.

The DTCC, the central node in US securities infrastructure, ran its Smart NAV pilot with Chainlink, showing how mutual fund net asset value data can be published on-chain using cross-chain interoperability infrastructure, with multiple global asset managers participating. It has also unveiled a platform for real-time tokenized collateral management. The depository is not being disintermediated. It is tokenizing.

Meanwhile some tokenized funds are pushing the other way. Products including Superstate’s short-duration government securities fund and Franklin’s OnChain US Government Money Fund enable peer-to-peer transactions among approved holders, and BUIDL has been listed on Uniswap’s decentralized exchange for eligible traders. Each step widens the set of things an allow-listed holder can do without going through the issuer, which is a slow migration of function toward the chain without ever surrendering the register.

The tension shows up plainly in retail products. Robinhood’s Stock Tokens are structured as tokenized debt securities that track a stock’s economic performance but confer no voting rights, no shareholder rights, and no direct legal ownership claim on the shares, and they are unavailable to US persons. That is a different structure from a tokenized fund share, and it exists because building a token that conveys actual equity ownership across borders runs straight into the transfer agent and registrar architecture that governs real shares. It is easier to issue a derivative of a stock than to tokenize the stock.

What a failure would look like

A useful way to test whether you understand an architecture is to ask how it breaks, and the transfer agent model has failure modes that differ sharply from the ones crypto users are trained to watch for.

The register and the chain diverge. This is the mundane one and it will happen. A subscription is recorded off-chain but the mint fails. A transfer succeeds on-chain but the register update does not process. For a period, the two records disagree about who owns what. In a permissionless system this would be a crisis with no resolution path. Here it is a reconciliation task, because the hierarchy is defined in advance: the register is authoritative, the chain gets corrected, and administrators such as JPMorgan hold explicit authority to do exactly that. The failure is contained precisely because the system is not decentralized. That is the trade in one sentence.

The transfer agent itself fails. This is the interesting one, and it has no on-chain answer.

If the entity maintaining the register suffers an outage, an insolvency, or a compromise, the authoritative record of ownership is impaired. The tokens still sit in wallets, still display balances, still move between allow-listed addresses. And none of that settles what anyone owns, because the record that decides ownership is the impaired register. Traditional finance has procedures for transfer agent succession, because this risk predates blockchains by a century. But the crypto instinct, which is to point at the chain and say the record is right there, is precisely wrong here. The chain is a mirror. A mirror does not help when the original is gone.

The allow-list becomes the attack surface. Whoever controls which addresses may hold the token controls the asset in a way no key holder does. A compromised allow-list could add unauthorized addresses or, more disruptively, remove legitimate ones, freezing holders out of transfers they are entitled to make. The smart contract will faithfully enforce whatever the list says, because faithful enforcement is its only job. Decentralization does not protect you here; it is what is being enforced against.

Composability breaks at the edge. Tokenized fund shares are increasingly used as collateral across DeFi. But a permissioned token cannot be liquidated to an arbitrary buyer, because arbitrary buyers are not allow-listed. A lending protocol that accepts BUIDL as collateral must have a liquidation path that terminates in an approved wallet, which means its liquidation mechanism depends on a whitelist maintained by a company that has no obligation to that protocol. The composability that makes these tokens attractive is conditional on a permission layer sitting outside the protocol using them, and that dependency has not been tested during a genuine stress event.

None of these are arguments against the model. They are the actual risk register, and it is a different register from the one crypto is used to reading. Nobody is going to lose a tokenized fund position because they mismanaged a seed phrase. They would lose it because an intermediary’s database, an approval list, or a reconciliation process failed, which are exactly the risks tokenization was supposed to have removed and instead relocated.

The question underneath

Strip away the mechanics and one question remains, and it is the one that decides whether tokenization matters.

If the transfer agent’s register is the truth, and the token is a receipt, what exactly has been tokenized? The optimistic answer: the settlement layer, and that alone is worth billions in operational savings and unlocks collateral mobility that did not previously exist. The skeptical answer: nothing important, because the trust assumptions are identical to the ones we had, and we added a blockchain to a system that already worked.

The honest answer is probably that this is a transitional architecture. Right now the register is authoritative and the chain is a mirror, because the law requires a registered intermediary to keep the record and the law has not changed. If it ever does, if a properly regulated on-chain register were permitted to be the record itself, the transfer agent function would not vanish. It would become code plus a compliance oracle, and something would be genuinely different.

Until then, the useful discipline for anyone touching tokenized securities is to hold the correct mental model. The wallet shows you a balance. The register decides whether that balance is yours. Those are two different claims, and only one of them is enforceable in a courtroom.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or legal advice. Tokenized securities are subject to access restrictions and securities regulation, and eligibility, rights, and terms vary by product and jurisdiction. Nothing here is a recommendation to buy any product. Always do your own.

Frequently Asked Questions

What is a transfer agent?

A transfer agent maintains the official register of who owns a security, processes transfers between holders, issues shares on subscription and cancels them on redemption, distributes dividends and interest to registered holders, and handles corporate actions and reconciliation. In the United States, transfer agents must register with the SEC and operate under its rules, making it a regulated function rather than informal bookkeeping.

What does a transfer agent do in tokenized securities?

The same things, plus two more. It maintains the authoritative off-chain ownership register that the tokens mirror, and it controls the allow-list: screening investor identity, adding approved wallets to an on-chain list, and thereby determining which addresses can legally hold the token. The smart contract enforces those decisions automatically, blocking transfers to addresses that have not been approved.

If I hold the token, do I own the security?

Not by itself. The authoritative record is the register maintained by the transfer agent. The token functions as a digital receipt enabling on-chain mobility, and when it moves between approved wallets the off-chain record updates to match. Your actual rights flow from the fund’s legal documents, the register, and the product’s transfer and redemption rules.

What happens if the blockchain and the official record disagree?

The official record wins. Administrators including JPMorgan retain authority to correct discrepancies between the on-chain ledger and the legal record, so the technological holding never diverges from the legal reality. This inverts the usual crypto assumption that the ledger is the final source of truth, and it is the defining characteristic of tokenized securities as currently structured.

Why can I not send tokenized fund shares to any wallet?

Because the token contract enforces an allow-list maintained by the transfer agent. Security token standards such as ERC-1400 and ERC-3643 build the restrictions into the token itself. Under ERC-3643, isVerified checks whether a recipient appears in the register of allow-listed investors and canTransfer enforces additional conditions. A transfer to an unapproved address reverts at the contract level.

Who are the major transfer agents in tokenization?

Securitize is the most prominent. Securitize Transfer Agent LLC is an SEC-registered transfer agent and broker-dealer and maintains the official record for BlackRock’s BUIDL and its OnChain Shares filing. Tokeny is another tokenization platform operating in this space. Franklin Templeton maintains the official record for BENJI through its own Benji platform.

Does this defeat the purpose of using a blockchain?

That is the genuine argument. Critics note that if an intermediary keeps the authoritative record, screens participants, and can reverse the chain, a permissioned database could deliver similar benefits more simply. Supporters note that securities law requires a registered record-keeper regardless of technology, that the allow-list is what makes these products legal at all, and that faster settlement, continuous operation, and collateral mobility are real gains that do not require the ledger to be authoritative.

How does this differ from Robinhood’s Stock Tokens?

Considerably. Robinhood’s Stock Tokens are structured as tokenized debt securities that track a stock’s economic performance but confer no voting rights, no shareholder rights, and no direct ownership claim on the underlying shares, and they are unavailable to US persons. A tokenized fund share represents an actual registered fund position recorded by a transfer agent. It is easier to issue a derivative referencing a stock than to tokenize the stock itself, precisely because of registrar architecture.

The second-largest meme coin boosted its worldwide popularity thanks to a major initiative from Japan. However, the SHIB Army was left disappointed after previously expecting a global money manager would launch a SHIB exchange-traded fund (ETF).

The token’s price has been sliding sharply over the past several months, and certain factors suggest that the sell-off may intensify in the near future.

The Latest Developments

Earlier this week, Rakuten Wallet (a crypto exchange run by the Japanese e-commerce giant Rakuten Group) officially added a physical SHIB coin to its “Real Coin” series. Shiba Inu’s official X account celebrated the effort, saying:

“The fifth release in the collection and the first to feature a premium blast finish.”

Nonetheless, that’s about it with the good news surrounding the meme coin. T. Rowe Price’s crypto ETF has just gone live, yet despite expectations that SHIB would be among the underlying assets, the meme coin was ultimately excluded.

Another development comes from the United States. Arkham revealed that the American government recently transferred $250,000 worth of Shiba Inu seized from FTX and Alameda Research.

“This SHIB will be held by the US government and presumably used to repay creditos in the FTX case,” the post reads.

Total Ecosystem Setback

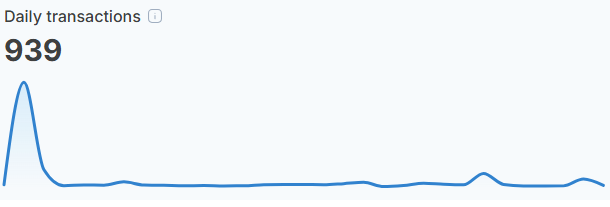

Shiba Inu has been going through a rough period lately; interest from traders and investors has dropped significantly, while overall ecosystem activity is barely visible.

The layer-2 scaling solution Shibarium, for instance, which once processed millions of daily transactions, is now in a much weaker condition. The figure has dropped to the mere hundreds, reflecting waning activity and interest among users.

Shiba Inu’s burning program is another worrying factor, with the rate down 54% over the past week, signaling a notable decline in network participation.

SHIB Price Outlook

As of press time, SHIB is worth roughly $0.000004078 (per CoinGecko), a 17% decline on a monthly scale and a colossal 95% collapse from the all-time high registered in late 2021.

The token’s market capitalization has slipped below $2.5 billion, and at one point this year Shiba Inu even fell to the third-biggest meme coin, overtaken by MemeCore (M). Shortly after, it reclaimed the second position, but only thanks to the double-digit collapse that MemeCore (M) experienced.

Despite the negative environment and multiple bearish factors, the community continues to grow. As CryptoPotato reported, the total number of SHIB wallets recently surged to a fresh peak of nearly 1.7 million after an explosive one-day influx of around 75,000 new holders.

The post Shiba Inu (SHIB) News Today: July 17th appeared first on CryptoPotato.

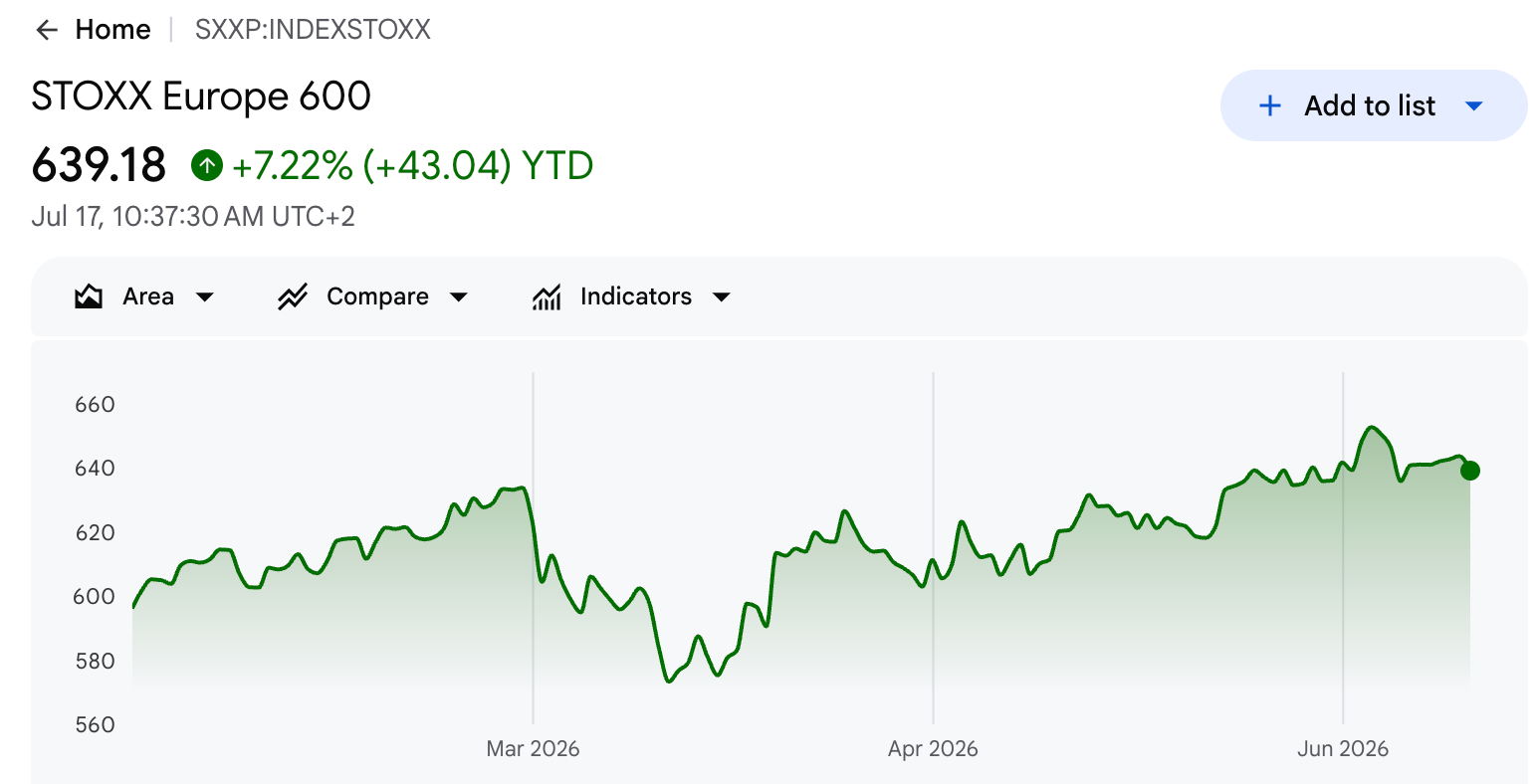

UBS forecast about 8% upside for the Stoxx Europe 600 by year-end, raising its target to 690 points from 630.

It reflects confidence that Europe’s earnings growth and stock rally can hold through geopolitical strain.

Why Banks Raised Their European Stock Target

European stocks have climbed back to record territory this year after a volatile first half. The index set a record close near 652 points on July 3.

It has since eased to about 639, but remains up more than 7% for the year. Worries about the Iran war faded after a ceasefire, and the rally held even as tensions flared again.

UBS strategists Gerry Fowler and Sutanya Chedda raised their target to 690 from 630, Bloomberg reported. The multinational investment bank and financial services firm expects the rally to run into 2027. It set a 760 target, which implies a 19% gain over the next 18 months.

“There’s probably more upside than downside risk at this point,” Fowler said.

Their 2026 forecast sits above JPMorgan’s 680, the previous highest target. Bank of America, Deutsche Bank, and Kepler Cheuvreux also lifted their targets.

The analysts pointed to stronger AI-related upgrades, steady bank revisions, and less drag from large defensive sectors.

Follow us on X to get the latest news as it happens

Strategists Split on What Comes Next

Across the July poll, the 18 strategists put the index at 647 on average by the end of 2026. That sits less than 1% above current levels, yet bearish calls are thinning out.

Only 5 of the 18 strategists expect the index to fall by year-end. Just 2 see declines steeper than 5%.

TFS is the most bearish, projecting a 9% drop to 585 points. Societe Generale ranks next, with strategist Roland Kaloyan calling for a slide of about 6% to 600. He warned that high expectations leave little room for disappointment.

“In our view, the main risk is not the absence of earnings growth, but that the recovery falls short of what is already priced in,” Kaloyan said.

The next test comes with the second-quarter results. More than 45% of firms have already beaten estimates, while 27% have missed.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Banking Giants Predict a 8% Rally for This European Stock appeared first on BeInCrypto.

The UK’s National Crime Agency (NCA) and the Metropolitan Police’s City of London Police have announced prison sentences for two men tied to the “Scattered Spider” cybercrime group. Both defendants entered guilty pleas at their first court appearance and were later sentenced at Woolwich Crown Court.

According to an NCA press release, the men pleaded guilty on June 22 and were sentenced on Thursday to a combined term of five years and six months in prison. Authorities said the case underscores how ransomware operators increasingly use cryptocurrency to monetize intrusions and extort victims.

Key takeaways

- The NCA and City of London Police say two Scattered Spider affiliates received five years and six months for hacking-related offenses.

- UK investigators linked the group to ransomware and cryptocurrency extortion activity affecting companies in both the UK and the US.

- US prosecutors previously associated Scattered Spider with large-scale crypto ransom collection, including at least $115 million from US companies.

- The group has also been tied to major incidents such as a public transport intrusion in London and separate claims involving Caesars Entertainment.

UK sentencing in the Scattered Spider case

The NCA said the two men were convicted in connection with cybercriminal activity associated with Scattered Spider, a group investigators have linked to ransomware and extortion schemes that use cryptocurrency payments.

In the court process described in the NCA update, both defendants pleaded guilty at their first appearance on June 22. The sentencing then took place on Thursday at Woolwich Crown Court, as reported in the NCA’s release.

For crypto-focused observers, the significance is less about the jail terms alone and more about how law enforcement continues to connect real-world extortion campaigns to digital asset flows—an area where blockchain analytics and custody investigations often determine whether perpetrators can be financially disrupted.

London transport network intrusion and reported losses

British authorities said the Scattered Spider group was involved in the infiltration of London’s public transport network in September 2024. The incident was reported to have resulted in losses and recovery costs of about £29 million (roughly $38.9 million).

While the sentencing announcement is specific to the two defendants, the underlying allegations tie back to a broader campaign pattern: gaining access to high-value targets, disrupting operations, and demanding payments—often in cryptocurrency—under time-sensitive pressure.

Investors and builders watching these cases generally look for a clear signal on enforcement priorities: when high-profile systems are targeted, governments typically respond with both criminal prosecution and efforts to trace and seize assets connected to extortion.

US DOJ links: crypto extortion at large scale

In a separate Department of Justice statement from September, US prosecutors said Scattered Spider was tied to collecting $115 million in cryptocurrency ransom payments from at least 47 US companies. That same DOJ release also described broader disruptions attributed to the group, including attacks impacting critical infrastructure and the federal court system.

The scale described by the DOJ matters because it suggests Scattered Spider is not a one-off operation. Instead, prosecutors portrayed it as a campaign capable of repeatedly compromising organizations and converting the resulting leverage into crypto-linked revenue.

The DOJ statement also described a broader investigation into the group’s activities, including repeated network intrusions. In such cases, sentencing outcomes in one jurisdiction can be interpreted as pieces of a larger enforcement strategy, where cases in the UK and US collectively strengthen the evidentiary record around the same actors and methods.

FBI seizure and earlier crypto ransom allegations

According to the DOJ’s September release, the FBI seized approximately $36 million worth of cryptocurrency from wallets linked to Scattered Spider in July 2024. Prosecutors said investigators traced and seized digital assets allegedly controlled by members of the group as part of the wider case.

US prosecutors further said Scattered Spider was accused of breaching Caesars Entertainment and stealing a large customer database in September 2023. Prosecutors said Caesars ultimately paid a $15 million ransom in Bitcoin (BTC). That earlier allegation fits the same overall pattern of using crypto as the payments mechanism for extortion demands.

The combination of wallet-linked seizures and later courtroom sentences highlights the practical leverage of crypto intelligence for law enforcement: tracking transfers and correlating wallet activity with criminal conduct can support both asset recovery and prosecution.

In the DOJ’s account, investigators said the group was responsible for at least 120 computer network intrusions. The NCA sentencing announcement does not enumerate those numbers, but it aligns with the DOJ’s broader framing of an expanding threat. For victims and compliance teams, the message is consistent: crypto-enabled ransomware operations continue to attract coordinated international responses, even when the extortion attempts cross borders.

“These malicious attacks caused widespread disruption to US businesses and organizations, including critical infrastructure and the federal court system, highlighting the significant and growing threat posed by brazen cybercriminals,” said Matthew Galeotti, then acting assistant attorney general of the Justice Department’s Criminal Division.

What to watch next

With Scattered Spider affiliates now facing prison time in the UK and prosecutors having described large crypto-related seizures and ransom totals in the US, the next key question is whether additional defendants—along with more wallet-linked assets—will be identified and targeted across jurisdictions. For companies and crypto traders alike, continued enforcement can meaningfully shape how ransomware groups attempt to move funds and how quickly investigators can disrupt those flows.

Crypto World

Inside Robinhood’s high-stakes bet to ‘democratizing’ its 10 million casual users onto blockchain finance

Tokenized real-world assets (RWAs) account for just $12.66 million in active market capitalization despite the recent spike in trading activity.

Much of that larger activity, instead, came from memecoin traders piling into a new token, CASHCAT, named after Robinhood’s former company mascot. The token rallied by more than 2,100% in its first week, briefly reaching a $156 million market cap, which is 12 times larger than the chain’s entire tokenized real-world asset market.

It’s worth noting, though, that memecoins are volatile and hype-driven by nature, often lacking durable growth. That lack of sustainability was evident on Wednesday, when Noxa, the token launcher that spawned CashCat, announced it had stopped operating while directing all revenue to creators. The shutdown does not determine the fate of Robinhood Chain, but it underscores how quickly activity built around memecoin launches can disappear.

Ironically, Robinhood CEO Vlad Tenev told CNBC on July 2 that memecoins were a dead end – assets with no utility that serve no purpose. Six days later, he posted that Robinhood Chain “works great for memes too,” presumably after seeing CASHCAT’s success.

Asked about the apparent contradiction, the company did not directly address it. “The early activity on Robinhood Chain is exciting: developers are building, users are engaging, and the chain is performing as designed,” Lee said.

Bitcoin slipped below $62,500 at the Wall Street open on Friday, extending a fresh dose of volatility as risk sentiment deteriorated. The move came as US markets reacted to renewed tensions tied to the US–Iran war, pulling down equities and—by extension—crypto.

Traders described BTC’s behavior as “very choppy,” with buyers and sellers repeatedly failing to establish direction after earlier strength. On the technical side, analysts flagged that Bitcoin’s long-running downtrend may be nearing an important phase, after the asset flipped a key long-term moving average into resistance.

Key takeaways

- BTC fell under $62,500 during the US open as US stocks turned lower amid escalated US–Iran headlines.

- Trading data referenced from TradingView indicated up to about 2% downside on the day for BTC/USD.

- Market participants say BTC is repeating prior patterns: local highs are being rejected, and price remains rangebound.

- Analysts including Rekt Capital pointed to Bitcoin flipping its 50-month EMA to resistance, which historically has preceded a move toward a long-term floor.

BTC weakens as equities take another hit

According to TradingView data cited in the report, BTC/USD extended losses into the session, with the move described as reaching as much as roughly 2% downside on the day. The timing aligned with a broad risk-off turn in US markets.

At the time of writing, US stocks had opened in the red, and the Nasdaq Composite was down nearly 2%. Fresh military strikes on Iran were highlighted as a catalyst behind the retreat in risk assets, with tech shares continuing to face selling pressure.

Additional pressure came from company-specific news. The Kobeissi Letter flagged weakness tied to earnings disappointments, noting that Netflix was down more than 10% at the start of the US session and citing a longer-view performance mark: the stock is down about 50% over the last 12 months and trading at its lowest level since August 2024, as stated in the outlet’s X post.

After three-week highs, traders face a familiar rhythm

Bitcoin’s decline followed a rebound period in which the asset had tapped three-week highs. After that push, traders reportedly saw “copycat” selling as the market returned to the same range conditions.

One market commentator, Exitpump, suggested on X that the pattern was repeating: a “dump into passive demand,” increased open interest with shorts building while spot buying begins to reappear—an imbalance that often produces sharp bounces rather than smooth trending.

Another trader, Daan Crypto Trades, characterized the broader tape as seasonal and directionless, describing recent weeks as “very choppy,” with alternating runs up and down and limited follow-through. That view fits with the overall picture of rangebound trading: peaks get sold, support gets tested, and the market appears to oscillate rather than commit to a new trend.

Bear-market “milestones” and the 50-month EMA flip

Beyond short-term price action, attention in the crypto market has also remained focused on the longer-term shape of Bitcoin’s bear-market cycle. Analyst Rekt Capital argued that Bitcoin has moved closer to a key technical milestone by flipping the 50-month exponential moving average (EMA) to resistance.

Rekt Capital said that BTC/USD’s interaction with the 50-month EMA is repeating bear-market history and that this change sets up the next phase of the decline toward a long-term floor. In his X update, he wrote that “the necessary technical milestone has been achieved,” adding that the milestone “technically indicates that the majority of the anticipated move has already happened.”

While such signals are often discussed as evidence that the market is maturing through the bear phase, they also leave plenty of uncertainty for traders. Even if the downtrend is in a late stage, timing can still be volatile—especially when external drivers such as macro headlines and geopolitical developments repeatedly shift risk appetite.

What to watch next for traders and investors

With BTC currently trading in a highly reactive environment—tied to equity sentiment while also reflecting recurring technical behavior—readers should watch how quickly support near recent range lows holds or breaks, and whether BTC’s resistance reactions around major longer-term levels persist. The next swing will likely be shaped as much by risk sentiment as by BTC-specific technical conditions.

The Bank of England approved HSBC Orion to go live in its Digital Securities Sandbox, with the first Digital Gilt Instrument transaction expected in the first quarter of 2027.

SBI Holdings has acquired a majority stake in Coinhako after securing regulatory approval for the Singapore crypto exchange deal on July 16.

Summary

- SBI Holdings acquired a majority stake in Coinhako after receiving approval from Singapore’s financial regulator.

- Coinhako gives SBI a licensed base for expanding digital asset services across Southeast Asia.

- The deal complements SBI’s JPYSC stablecoin, Ondo partnership, and Solana-based JX equity token

According to SBI Holdings, the transaction involved a capital injection through SBI Ventures Asset Pte. Ltd. and the purchase of shares from Coinhako’s existing investors. Coinhako will now operate as a consolidated subsidiary of the Japanese financial group.

Approval from the Monetary Authority of Singapore allowed the deal to close on July 16. SBI did not disclose the size of the investment, the percentage of shares acquired, or Coinhako’s valuation under the transaction.

Established in 2014, Coinhako is operated by Hako Technology Pte. Ltd. and holds a Major Payment Institution licence from MAS. Its affiliate, Alpha Hako Ltd., is registered as a virtual asset service provider with the British Virgin Islands Financial Services Commission.

Coinhako gives SBI a regulated Singapore base

Through the acquisition, SBI plans to combine Coinhako’s customers, regional network and crypto operations with the Japanese group’s financial products and international reach. The company identified Singapore as a key market because of its established digital asset regulations and position within Southeast Asia.

SBI Chairman and President Yoshitaka Kitao described the purchase as part of the group’s plan to connect exchanges across multiple countries. According to Kitao, such a network could let investors trade without being limited by national borders or currency differences.

Coinhako’s local presence and regulatory status were central to the decision, Kitao added. SBI expects the exchange to support new services involving stablecoins, tokenized assets, cross-border trading and on-chain finance between Japan and Southeast Asia.

For Coinhako, joining SBI provides access to a financial group with operations across banking, securities and digital assets. Commenting on the acquisition, Coinhako co-founder and CEO Yusho Liu described the deal as the company’s next stage after a decade of operating in Singapore.

“Joining the SBI Group is a natural step for Coinhako to move to the next stage of growth.”

Tokenized assets deepen SBI’s regional strategy

Alongside the Coinhako purchase, SBI has been developing a yen-backed stablecoin called JPYSC with blockchain company Startale. SBI plans to explore its use within the combined group, including possible links to Coinhako’s services and regional customer network.

As previously reported by crypto.news, SBI has also partnered with Ondo Finance to bring tokenized financial products into its ecosystem. Under the agreement, the companies plan to use JPYSC for settlement and collateral while connecting Japanese securities with overseas tokenized markets.

Ondo’s products are expected to reach investors through SBI’s customer network, according to the companies. The partnership also gives SBI another route for using its stablecoin beyond conventional transfers, including transactions involving tokenized securities.

One day before the Coinhako deal closed, SBI Global Asset Management launched the SBI Japan High Dividend Equity Strategy Token, or JX token, with regulated real-world asset exchange DigiFT. Issued on Solana, the product gives accredited and institutional investors blockchain-based exposure to a Japanese high-dividend equity strategy managed by SBI Asset Management Co.

Taken together, SBI’s announcements show how the group is assembling regulated exchanges, tokenized investment products and stablecoin infrastructure across Asia. Coinhako adds a licensed Singapore distribution point to that network, while the Ondo and DigiFT agreements provide financial products that SBI could connect to it.

Morgan Stanley has completed the rollout of Bitcoin, Ethereum, and Solana trading on E*TRADE, charging eligible clients a 0.50% fee on each transaction.

Summary

- E*TRADE now allows eligible clients to trade Bitcoin, Ethereum, and Solana for a 0.50% fee.

- Morgan Stanley plans crypto transfers and a move to its Digital Trust bank later this year.

- The rollout complements Morgan Stanley’s Bitcoin holdings, crypto ETFs and Galaxy Digital lending arrangement.

E*TRADE announced in a press release that supported customers can now buy, sell and hold the three digital assets directly through its brokerage platform. Zerohash provides the underlying crypto infrastructure and holds the assets in linked customer accounts.

Each transaction carries a 50-basis-point fee, according to E*TRADE. While the current service covers trading and custody, the brokerage expects to introduce crypto transfers later this year, allowing clients to move supported assets into and out of their accounts.

Following a pilot launched in May, the completed rollout makes the service available to all eligible E*TRADE customers. Morgan Stanley had first disclosed plans to add direct spot crypto trading in 2025.

Morgan Stanley is expanding several crypto services at once

E*TRADE’s launch comes as Morgan Stanley prepares to add two exchange-traded funds tied to Ethereum and Solana. As previously reported by crypto.news, amended S-1 filings for both products indicated that their launches were approaching, although the filings did not provide a confirmed trading date.

Earlier this year, Morgan Stanley also launched a spot Bitcoin ETF, becoming the first bank to offer such a product, according to the original report. SoSoValue data showed that the fund had accumulated $384 million in net assets at the time of reporting.

Direct trading gives E*TRADE customers another route to crypto exposure alongside Morgan Stanley’s investment funds. Unlike ETF shares, the new service allows eligible users to hold the underlying Bitcoin, Ether and Solana through Zerohash, while the planned transfer feature would give customers more control over moving those assets.

Morgan Stanley had also increased its tracked Bitcoin balance by nearly 1,000 BTC over the two weeks preceding July 11, according to a crypto.news report published that day. The purchases lifted its reported holdings above 5,700 BTC at the time.

Digital Trust is set to take over the crypto service

Later this year, E*TRADE expects to move the crypto offering from Zerohash to Morgan Stanley Digital Trust, the group’s planned national trust bank. The brokerage linked that transition to the introduction of transfer services but did not provide a specific launch date.

Morgan Stanley applied to the Office of the Comptroller of the Currency earlier this year for a crypto-focused national trust bank charter. Its application placed the firm alongside Coinbase, Crypto.com and Ripple, while the OCC has already granted Ripple conditional approval.

Circle has also received OCC approval to establish a national trust bank focused on digital assets. The USDC issuer had secured conditional approval in 2025 alongside BitGo, Fidelity and Paxos.

Morgan Stanley Wealth Management added another crypto route in June through a referral agreement with Galaxy Digital. Under the arrangement, eligible high-net-worth clients can lend Bitcoin, Ether and Solana to Galaxy and receive shares in spot crypto investment products, including the Morgan Stanley Bitcoin Trust.

Taken together, the ETRADE rollout, pending ETF launches and Digital Trust application place trading, investment products, lending referrals and custody infrastructure within Morgan Stanley’s disclosed crypto plans. Each service remains subject to separate eligibility rules, fees and regulatory arrangements set by the companies involved.

Bitcoin remains trapped inside a broader corrective structure after its sharp drop from the mid-$80K region. While buyers have managed to defend the $60K support multiple times, the inability to reclaim key resistance levels continues to favor a cautious outlook in the short term.

Bitcoin Price Analysis: The Daily Chart

On the daily timeframe, BTC is trading around $63K after stabilizing above the major support zone at $60K. This area has repeatedly attracted demand since the early June selloff and continues to serve as the market’s most important defensive level.

Despite the recent consolidation, the broader structure remains bearish. The price is still trading below both the 100-day and 200-day moving averages, which are positioned around the $70K and $73K regions, respectively. Both moving averages are sloping downward, reinforcing the prevailing downtrend.

The recent recovery attempt also failed to reclaim the previous breakdown area around $66K, leaving that zone as the first major resistance. Above it, another significant supply area sits near $74K, aligning closely with the declining 200-day moving average. As long as BTC remains below these levels, rallies are likely to face renewed selling pressure. Should the $60K support fail, the next major downside target appears around $55K, where another higher-timeframe demand zone is located.

BTC/USDT 4-Hour Chart

The 4-hour chart shows that BTC has been consolidating following its sharp decline from the $74K region. The price continues to trade within the broad descending channel while forming a series of higher lows above the $61K support zone.

The immediate resistance remains at $66K, where horizontal resistance intersects with the channel’s descending trendline. This confluence makes it a critical area for bulls to overcome before any stronger recovery can develop.

On the downside, the $61K support has held multiple retests and currently serves as the first line of defense. Losing this level would likely expose the $58K demand zone. The RSI has also been fluctuating around the neutral 50 level, suggesting that bearish momentum has eased and indecision is ruling the market.

A confirmed breakout above both the descending trendline and the $66K resistance zone would improve the short-term outlook and could trigger a move toward the $72K to $74K region. Until then, the market remains vulnerable to another rejection within the prevailing downtrend.

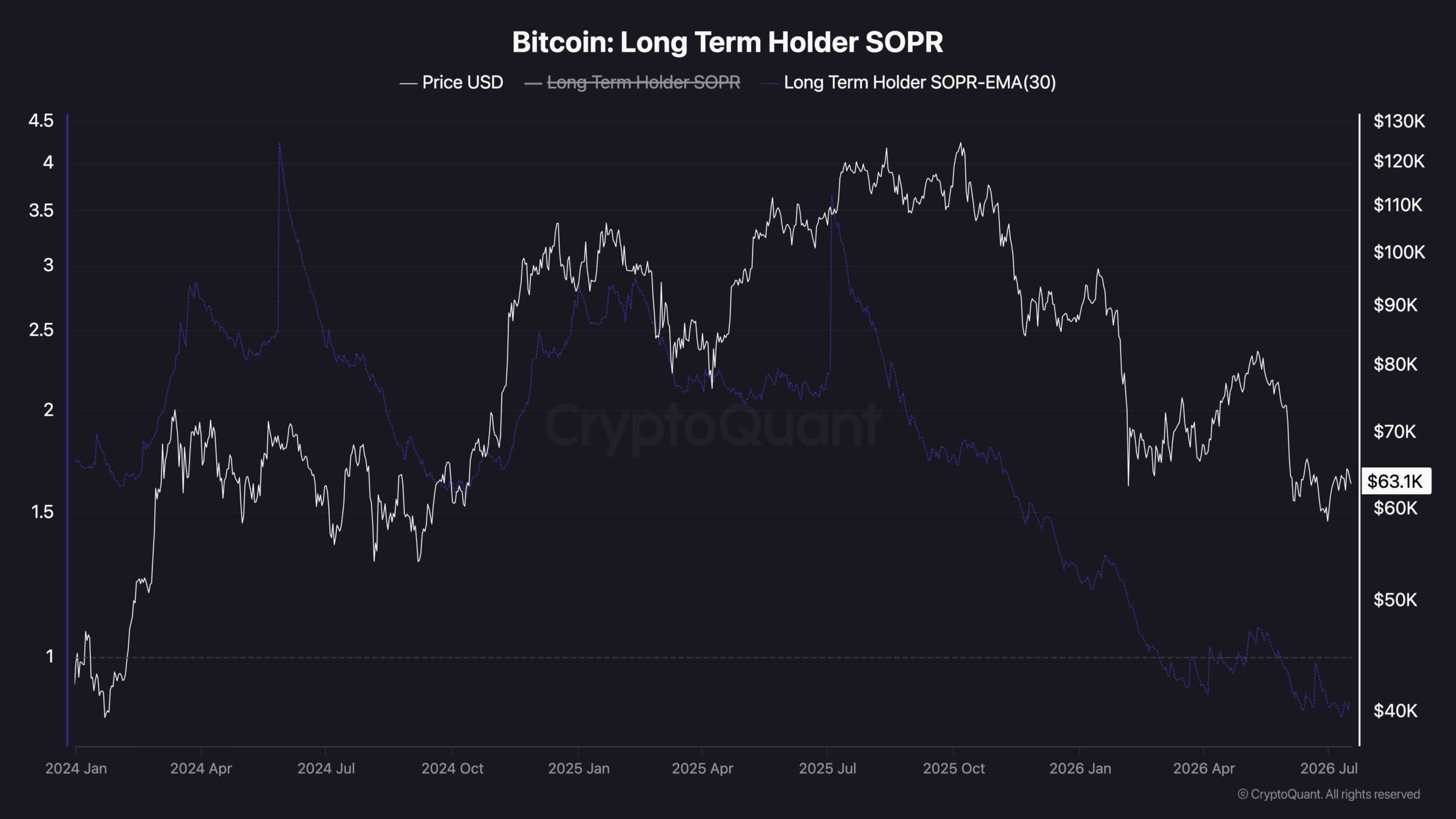

On-Chain Analysis

The 30-day exponential moving average of the Long-Term Holder SOPR (Spent Output Profit Ratio) has continued to decline and is now trading below the critical 1.0 threshold. This metric measures whether long-term holders are spending their coins at a profit or a loss, with readings below 1 indicating that coins are being realized at a loss on average.

The breakdown below 1 suggests that a growing portion of long-term investors (who have held their coins for over 6 months) has entered capitulation, choosing to sell despite being underwater. Historically, prolonged periods below this level have coincided with the late stages of corrective phases, when selling pressure from experienced holders intensifies before the market establishes a more durable bottom.

While this shift reflects deteriorating sentiment among long-term participants, it also suggests that the market is moving deeper into a redistribution phase. If the indicator quickly recovers above 1, it would imply that the recent capitulation was temporary. However, a sustained stay below this threshold would signal continued weakness and increase the likelihood of further downside, particularly if Bitcoin loses the key $60K support zone.

The post Bitcoin Price Analysis: Is BTC Headed Below $60K After $65.5K Rejection? appeared first on CryptoPotato.

Bitcoin (BTC) dipped below $62,500 at Friday’s Wall Street open as stocks took a fresh hit from the US-Iran war.

Key points:

- Bitcoin gives traders a sense of deja-vu as local highs spark rejection and rangebound moves continue.

- The US-Iran war pushes stocks and crypto lower.

- A bear-market trend line is now in place as resistance, copying historical patterns.

BTC price action stays “very choppy”

Data from TradingView showed BTC/USD extending losses with up to 2% daily downside.

BTC/USD one-hour chart. Source: Cointelegraph/TradingView

US stocks opened in the red, with the Nasdaq Composite Index also down nearly 2% at the time of writing. Fresh military strikes on Iran fueled the risk-asset retreat, while tech stocks continued to see selling pressure.

Trading resource The Kobeissi Letter also flagged weakness arising from earnings disappointments, with Netflix shedding over 10% to start the US session.

“The stock is now down -50% over the last 12 months and trading at its lowest level since August 2024,” it noted in a post on X.

Netflix stock one-day chart. Source: Cointelegraph/TradingView

After hitting three-week highs, BTC price action fell back into its established range as traders saw copycat moves.

“Market just keeps repeating same things,” commentator Exitpump wrote on X.

“Dump into passive demand, OI increases with shorts piling up while spot starts buying which leads to bounce.”

BTC/USDT five-minute chart with order-book data. Source: Exitpump/X

Trader Daan Crypto Trades argued that current behavior was “typical” of summer.

“Very choppy few days up, few days down kind of price action the last few weeks. No real action anywhere really,” he summarized.

BTC/USD four-hour chart. Source: Daan Crypto Trades/X

Bitcoin seals key bear-market repeat

Trader Jelle, meanwhile, remained optimistic, seeing range lows holding.

Related: Bitcoin bottom countdown nears 50 days after BTC supply in loss passed 50%

“Still think this looks good for a relief rally in the next weeks – which would give the market room to drop into October without nuking much deeper,” he told X followers.

BTC/USD one-day chart. Source: Jelle/X

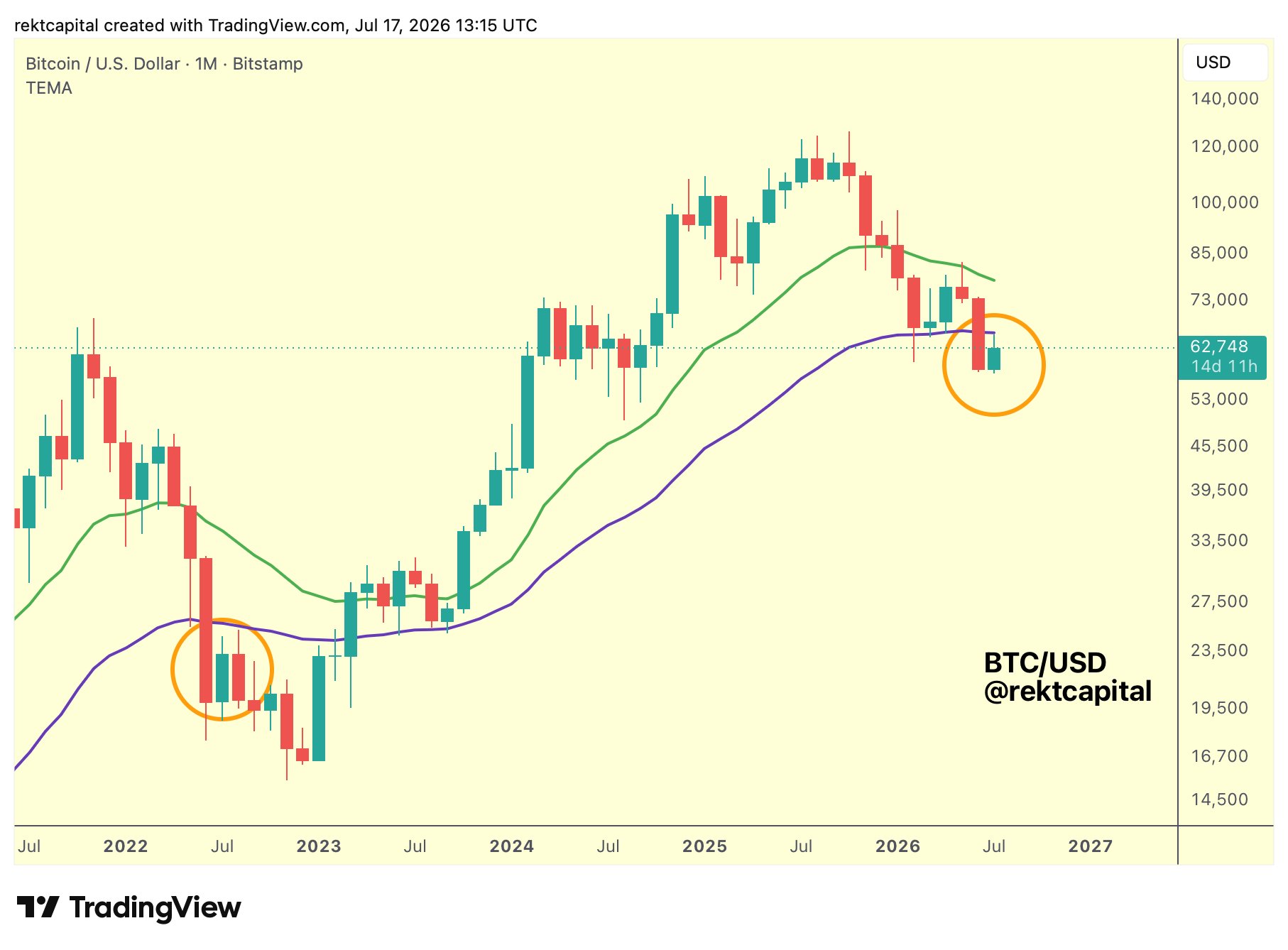

In updates on the bear market’s progress, trader and analyst Rekt Capital suggested that Bitcoin’s long-term downtrend was now in its final stages.

BTC/USD, he wrote, had flipped its 50-month exponential moving average (EMA) to resistance, repeating bear-market history to set up its drop to a long-term floor.

“The necessary technical milestone has been achieved,” he confirmed.

“Which technically indicates that the majority of the anticipated move has already happened.”

BTC/USD one-month chart with 21, 50EMA. Source: Rekt Capital/X

As Cointelegraph reported, Rekt Capital saw the July relief bounce ending with the onset of next month.

Apple Reclaims Title as World’s Most Valuable Company, Overtaking Nvidia for First Time Since April 2025

Shiba Inu (SHIB) News Today: July 17th

Szoboszlai agrees to new five-year contract with Liverpool

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

NewsBeat1 day ago

NewsBeat1 day agoLondon Mayor Sadiq Khan handed a peerage by Keir Starmer alongside 15 other Labour figures… just days before the PM leaves No10

-

Crypto World2 days ago

Crypto World2 days agoCFTC blocks Kalshi from unwinding Michigan trades after court order

-

Business2 days ago

Business2 days agoNvidia Stock Slips After Big Tuesday Rally as Huang Confirms Vera Rubin Chip Is Now in Production Today

-

Politics2 days ago

Politics2 days agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

Entertainment2 days ago

Entertainment2 days agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

News Videos3 days ago

News Videos3 days agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech3 days ago

Tech3 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Crypto World19 hours ago

Crypto World19 hours agoInjective Submits SEC Transfer-Agent Registration to Onchain Ownership Records

-

NewsBeat4 hours ago

NewsBeat4 hours agoRegistration is now open for March for Men with Kev 2026

-

Tech3 days ago

Tech3 days agoDark Secrets Emerge When Jailbreaking LLMs

-

Business2 days ago

Business2 days agoPalantir Shares Rise After Expanded Nvidia Partnership and Fresh Analyst Upgrades Ahead of Earnings Day

-

News Videos9 hours ago

News Videos9 hours agoMoney | Class 12 Economics | CBSE Board Exam 2026-27

-

Sports2 days ago

Sports2 days agoNew Cornerback Enters Vikings Trade Rumor Mill

-

Business15 hours ago

Business15 hours agoBanco Bilbao Vizcaya Argentaria, S.A. (BBVA) Discusses Global Macro Environment and Economic Outlook for Core Markets Transcript

-

Tech4 days ago

Tech4 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

News Videos4 days ago

News Videos4 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Entertainment2 days ago

Entertainment2 days agoVicki Gunvalson Defends Discussing Heather Dubrow’s Money

-

Crypto World3 days ago

Ripple, Coinbase, Circle Join Linux x402 Foundation to Help Shape AI Payments

-

Crypto World18 hours ago

Crypto World18 hours agoClaude Fable 5 Slips to Second in AI Coding Leaderboard

You must be logged in to post a comment Login