Crypto World

What is ISO 20022? The banking standard behind the XRP, XLM, and ALGO hype

A wave of cryptocurrencies are marketed as “ISO 20022 compliant,” with the promise that banks will adopt them and send prices soaring. This guide explains what the standard actually is, why it matters for global payments, and why the “compliant coin” label is mostly a myth.

Summary

- ISO 20022 is a global standard for the messages financial institutions send one another, defining a common, data-rich language for payments and securities, not a rule about cryptocurrencies.

- Major systems including SWIFT and the United States Fedwire have adopted it, replacing older, simpler message formats with structured data that carries far more information.

- A group of tokens, including XRP, XLM, ALGO, HBAR, and others, are widely marketed as “ISO 20022 compliant,” fueling a belief that banks will adopt them and lift their prices.

- That label is largely a myth: there is no certification or registry for compliant coins, and being aligned with the standard does not mean a token is endorsed, validated, or destined for bank adoption.

- The standard genuinely matters for connecting traditional finance and blockchain, but the investment thesis built on the compliance label rests on a misunderstanding of what ISO 20022 actually is.

ISO 20022 is an international standard that defines a common, structured language for the electronic messages financial institutions send one another, covering payments, securities trades, and other financial transactions. That is the whole of it: it is a messaging standard, a shared format that lets banks, payment systems, and market infrastructures exchange information in a consistent, data-rich way. It says nothing, in itself, about cryptocurrencies. And yet ISO 20022 has become one of the most hyped terms in certain corners of the crypto market, attached to a list of tokens, XRP, Stellar’s XLM, Algorand’s ALGO, Hedera’s HBAR, and several others, that are marketed as “ISO 20022 compliant,” with the implication that this compliance makes them special, bank-ready, and poised to soar once financial institutions adopt the standard.

The reality is more mundane and more important to understand, because the gap between what ISO 20022 is and what the hype claims it means is exactly where investors get misled. This guide explains the standard plainly, why the financial world is adopting it, where crypto genuinely fits, and why the “compliant coin” label is largely a marketing myth rather than a meaningful endorsement.

The reason this matters is that ISO 20022 sits at the intersection of a real, significant trend and a layer of misleading marketing, and telling the two apart is essential. The real trend is that the global financial system is upgrading the language it uses to move money, a genuine modernization with real consequences for how payments work and how easily traditional finance can connect to blockchains. The misleading layer is the claim that certain tokens are validated or endorsed by the standard, a claim that has fueled speculative buying based on a misunderstanding.

This guide covers what ISO 20022 actually is, why institutions are switching to it, what richer messaging buys them, where the crypto angle comes from, why the compliance label is a myth, what alignment truly means, the specific case of XRP, and how to read the whole phenomenon honestly. The goal is to leave you understanding both the substance and the spin.

The standard that runs the world’s payment messages

Start with what ISO 20022 fundamentally is, because its name makes it sound more mysterious than it is. When a bank sends money to another bank, no physical cash travels; instead, the banks exchange messages instructing each other to debit one account and credit another. For decades, those messages used older, rigid formats that packed limited information into terse codes, formats designed in an era of expensive bandwidth and simple transactions. ISO 20022 is the modern replacement: a standardized, structured language for these financial messages that can carry far more information in a consistent, machine-readable form. Think of it as a shared grammar that every institution agrees to speak, so that a message sent by a bank in one country can be understood automatically by a system in another without translation or guesswork.

The power of ISO 20022 lies in two qualities: it is standardized, meaning everyone uses the same format, and it is rich, meaning each message can carry detailed, well-organized data rather than cramped codes. A useful way to picture it is the difference between a tightly abbreviated telegram and a properly structured digital form. The old formats were like telegrams, squeezing essential facts into minimal space and leaving much to interpretation. ISO 20022 is like a structured form with clearly labeled fields for every relevant detail: who is paying, who is receiving, the purpose of the payment, the parties involved, and the regulatory information attached. This is not a small upgrade. It changes what financial systems can do with a payment message, because a message that carries clean, structured, comprehensive data can be processed, screened, and reconciled automatically in ways that the old cramped formats never allowed.

Why the financial world is switching to it

The migration to ISO 20022 is one of the largest coordinated upgrades in the history of financial infrastructure, and it is happening because the old messaging formats had become a serious bottleneck. The legacy formats carried so little structured data that banks constantly had to deal with incomplete information, manual intervention, and errors, all of which slow payments down and raise costs. When a payment message lacks clear, structured fields, a human often has to step in to interpret it, check it against sanctions lists, or chase missing details, and every such intervention is friction. As global payments grew in volume and as regulatory demands for transparency and screening intensified, the limitations of the old formats became untenable. ISO 20022 solves this by carrying the rich, structured data that lets far more of the process happen automatically and accurately.

The adoption has been sweeping. The global messaging network that connects most of the world’s banks has been migrating its cross-border payments to ISO 20022, phasing out the legacy formats. Major domestic payment systems have moved as well, including the United States’ main real-time settlement system, which adopted ISO 20022 for its operations, joining systems in Europe and elsewhere that had already transitioned. The direction is unmistakable: the world’s core payment rails are converging on this single standard, because the benefits, richer data, better automation, improved compliance, and smoother interoperability between systems, are compelling enough to justify an enormous, multi-year coordinated effort. For the financial industry, ISO 20022 is simply the new common language of money movement, and the migration to it is a genuine, consequential modernization. None of this, it is worth stressing again, has anything inherent to do with cryptocurrencies. It is about how banks and payment systems talk to each other.

A worked example: what richer data actually buys

To make the value concrete, picture a single cross-border payment under the old system and under ISO 20022, because the difference shows why institutions care.

Under a legacy format, a bank sending a payment abroad might transmit a message with a sender, a receiver, an amount, and a short, cramped reference field, with much of the contextual detail abbreviated, omitted, or jammed into free-text notes that no automated system can reliably read. When that message arrives, the receiving bank may not have enough structured information to automatically confirm the purpose of the payment, verify the parties against regulatory lists, or match it to the right account, so a staff member has to intervene, slowing the payment and introducing the possibility of error. Multiply that friction across millions of payments and the cost in time, money, and risk is enormous.

Now picture the same payment under ISO 20022. The message arrives with clearly labeled, structured fields: the full identities of the sender and receiver, the precise purpose of the payment, the regulatory and compliance information, and the references needed to match it automatically to the correct account. Because the data is structured and comprehensive, the receiving bank’s systems can process it without human intervention, screen it against sanctions and fraud checks automatically, and reconcile it instantly. The payment moves faster, costs less to handle, and carries less risk of error or of slipping past compliance controls. This is the real, unglamorous value of ISO 20022: it turns payment messages from cramped telegrams that often need human interpretation into structured data that machines can handle end to end. That improvement in automation, compliance, and interoperability is why the entire financial world is undertaking the switch, and it is a truly significant upgrade to the plumbing of global finance. It is also, notably, an upgrade about messages, not about money itself, and certainly not about any particular token.

Where crypto enters the picture

So how did a banking messaging standard become a crypto buzzword? The connection runs through the idea of interoperability between traditional finance and blockchain. As ISO 20022 became the language banks use, some blockchain projects, particularly those focused on payments and settlement, positioned themselves as able to work with that language, to structure their own messaging or data in ways compatible with the standard that banks were adopting. The thinking was reasonable on its surface: if banks are standardizing on ISO 20022, then a blockchain that can speak the same data language might integrate more easily into bank workflows, which could be an advantage for a payments-focused crypto network.

From that reasonable starting point grew a much larger and much shakier narrative. A list of tokens came to be labeled “ISO 20022 compliant” across crypto media and social channels, typically including XRP, Stellar’s XLM, Cardano’s ADA, Algorand’s ALGO, Hedera’s HBAR, and a handful of others associated with payments or enterprise use. Around this list formed a popular investment thesis: that because these tokens are ISO 20022 compliant, banks adopting the standard will naturally adopt these tokens, driving massive demand and sending prices soaring. The thesis is seductive because it connects a real, sweeping trend, the global migration to ISO 20022, to a specific set of assets, implying that those assets are uniquely positioned to benefit from the trend. Entire communities and marketing campaigns have been built around the “ISO 20022 coin” label, treating it as a mark of quality and a catalyst for price appreciation. The trouble is that the label means far less than the hype suggests, and in important respects it is simply false.

The “compliant coin” myth, explained

Here is the core fact that punctures the hype: there is no such thing as official ISO 20022 certification for a cryptocurrency, because no certification process or registry for compliant coins exists. The standard is a messaging format used by financial institutions, and it has no mechanism for validating, endorsing, or registering tokens. When you see a coin described as “ISO 20022 certified” or “endorsed by ISO,” that language is marketing, and it is misleading or outright false. No authority hands out a compliance badge to cryptocurrencies, no list of approved tokens is maintained by the standards body, and being included on a community-circulated “ISO 20022 coin” list confers no official status whatsoever. The label that has driven so much speculative interest does not correspond to any real certification.

This matters because the entire investment thesis rests on a misreading of what the standard is. ISO 20022 governs how financial institutions format the messages they send each other; it does not validate the assets those messages might reference, and it does not bless particular blockchains as bank-ready. A bank using ISO 20022 messaging to interact with a crypto-related service is using the standard to communicate, which says nothing about whether the underlying token is approved, valuable, or destined for adoption. The conflation of “this token’s project works with ISO 20022 data formats” and “this token is officially compliant and therefore bank-endorsed” is the heart of the myth. The first may be true in a narrow technical sense for some projects; the second is not a real category. An investor buying a token because it appears on an “ISO 20022 compliant” list is buying based on a designation that does not officially exist, which is precisely the kind of misunderstanding that marketing language is designed to exploit.

What “aligned” actually means for a token

To be fair and precise, there is a real kernel beneath the myth, and understanding it keeps this guide honest. A blockchain project truly can do engineering work to make its systems compatible with ISO 20022 data, structuring the information its network handles so that it maps cleanly onto the standard’s fields, or building tools that let institutions using ISO 20022 messaging interact with the blockchain more easily. This is real work, and for a project aiming to serve banks and payment providers, being able to speak the same data language as the institutions it wants as customers is a sensible and potentially useful capability. So when a project says it is “aligned with” or “built for” ISO 20022, it may be describing genuine technical compatibility, which is not nothing.

But notice how far that real kernel is from what the hype claims. Technical compatibility with a messaging standard is a feature a project chooses to build, not a certification it receives, and it does not make the project’s token special, validated, or guaranteed adoption. Plenty of capability can be ISO 20022 compatible without any of it translating into demand for a token, because, as with so much in crypto infrastructure, the usefulness of a network to institutions is a separate question from demand for its native asset. A project can do excellent work making its systems speak the standard’s language and still see no particular benefit flow to its token, because banks using that compatibility are using the technology, not buying the coin. So “aligned with ISO 20022” should be read as a modest, real technical claim about a project’s engineering, never as an official stamp of approval or a reason to expect price appreciation. The distance between the honest version of the claim and the hyped version is enormous.

The XRP case specifically

Because XRP sits at the center of the ISO 20022 hype, it is worth examining its actual relationship to the standard, which illustrates the whole confusion neatly. Ripple, the company associated with XRP, has genuine ties to the world of financial messaging standards; as a company building payment infrastructure for institutions, Ripple participates in the relevant standards bodies and works with the messaging formats that banks use. That corporate level engagement is real and is part of why XRP appears at the top of most “ISO 20022 coin” lists. But here the crucial distinction between Ripple the company and XRP the token reasserts itself, the same distinction that runs through so much of the XRP story.

Ripple’s involvement with financial messaging standards as a company does not mean that XRP the token is “ISO 20022 compliant” in any meaningful sense. Ripple’s own chief technology officer has stated plainly that XRP has nothing to do with ISO 20022, clarifying that while Ripple as a company may engage with the standards world, that engagement does not translate into the token itself being compliant or endorsed. The standard is about how institutions message each other; XRP is a digital asset that can serve as a bridge in settlement. Those are different things, and a company working with messaging standards does not make its associated token a certified ISO 20022 instrument. The persistence of the XRP ISO 20022 conflation, despite direct clarification from the people who would know, shows how powerful the marketing narrative has become and how readily a real corporate fact, Ripple engages with standards bodies, gets transformed into a false token level claim, XRP is officially ISO 20022 compliant and therefore bank bound. The honest position is that Ripple’s standards work is real and XRP’s “compliance” is a myth, and both can be true at once.

What ISO 20022 does and does not mean for prices

Pulling it together, the right way to think about ISO 20022 is to separate its genuine significance from its mythologized one, because both exist and they point in very different directions. Truly, ISO 20022 is a meaningful, long-term tailwind for the convergence of traditional finance and blockchain.

As the entire financial system standardizes on a rich, structured data language, it becomes technically easier for blockchain networks that can speak that language to integrate with bank workflows, and over a long horizon that interoperability supports the broader adoption of blockchain-based settlement and tokenization. For payments-focused crypto projects, being able to work with the standard banks use is a real and sensible capability that may help them win institutional business over time. That is a slow, structural benefit to the ecosystem, and it is worth understanding.

What ISO 20022 is not is a catalyst that validates specific tokens or that should be expected to pump particular coins. There is no certification, no registry, no official “compliant coin” status, and no mechanism by which the standard endorses or guarantees adoption of any asset. The investment thesis that says “this token is ISO 20022 compliant, so banks will adopt it and the price will soar” rests on a designation that does not officially exist and a causal chain that does not hold, because banks adopting a messaging standard does not mean banks buying tokens.

The disciplined reading is to treat ISO 20022 as what it is, an important modernization of financial messaging that gently supports long-term blockchain interoperability, and to treat the “compliant coin” label as what it is, a marketing narrative untethered from any official meaning. A project’s genuine technical work with the standard can be a small point in its favor. The compliance badge that crypto marketing waves around is not a reason to buy anything.

Red flags and scams to watch

Because the ISO 20022 narrative is so heavily marketed and so widely misunderstood, it has become fertile ground for misleading promotion and outright scams, and knowing the warning signs protects you. The danger is not the standard itself, which is a legitimate piece of financial infrastructure, but the way its name is used to lend false authority to speculative pitches. Treat the following as red flags whenever you encounter ISO 20022 in a crypto context:

• Any claim that a token is “ISO 20022 certified,” “approved by ISO,” or “officially compliant.” No such certification or registry exists for cryptocurrencies, so this language is always misleading, and a project or promoter using it is either confused or deliberately exploiting the confusion.

• Price predictions that treat the standard as a guaranteed catalyst, such as promises that a coin will surge “once ISO 20022 goes live” or “when banks switch.” Banks adopting a messaging standard is not the same as banks buying tokens, and anyone presenting it as a sure path to gains is selling a misunderstanding.

• “ISO 20022 coin list” promotions that bundle a group of tokens as uniquely positioned to benefit, often used to pump lower-quality assets by association with the more credible names on the list. The list has no official status, and inclusion confers nothing.

• Urgency and exclusivity, such as claims that you must buy before a specific adoption date or miss a once-in-a-lifetime window. Genuine infrastructure modernization unfolds over years and does not create the kind of dated price triggers these pitches invent.

• Sources that conflate Ripple’s corporate standards work, or any company’s, with token-level compliance. A company engaging with standards bodies is real; the leap to “therefore the token is endorsed” is the exact sleight of hand to distrust.

The broader risk is financial. People have bought tokens primarily because of the ISO 20022 label, expecting bank adoption to drive prices, and that thesis rests on a designation that does not officially exist. If you are considering an asset associated with the standard, evaluate it on its actual fundamentals, its technology, adoption, team, and tokenomics, exactly as you would any other, and disregard the compliance badge entirely, because it carries no real weight. As with anything in crypto, never invest money you cannot afford to lose, be skeptical of any pitch that promises certainty, and remember that the louder a narrative is marketed, the more carefully it deserves to be checked.

Frequently Asked Questions

What is ISO 20022 in simple terms?

ISO 20022 is an international standard that defines a common, structured language for the electronic messages financial institutions send one another, covering payments, securities, and other transactions. It replaces older, rigid message formats with richer, machine-readable data, so that a payment message can carry detailed, clearly labeled information that systems can process automatically. It is a messaging standard for banks and payment systems, not a rule about cryptocurrencies, and it has nothing inherent to do with any token.

Why are banks adopting ISO 20022?

Because the older message formats carried so little structured data that they created constant friction: incomplete information, manual intervention, errors, and difficulty with automated compliance screening. ISO 20022 carries rich, structured data that lets far more of the payment process happen automatically and accurately, improving speed, cost, fraud and sanctions screening, and reconciliation. The world’s core payment rails, including the main global bank messaging network and major domestic settlement systems like the United States Fedwire, have migrated to it because the benefits justify the enormous coordinated effort.

What are “ISO 20022 coins”?

It is a label, circulated across crypto media and social channels, applied to a list of tokens, commonly XRP, XLM, ADA, ALGO, HBAR, and a few others, that are marketed as being compatible with or “compliant” with the standard. Around this label grew an investment thesis claiming that because banks are adopting ISO 20022, they will adopt these tokens, driving prices up. The label has fueled significant speculative interest, but it does not correspond to any official certification or status, which is the central problem with it.

Is the “ISO 20022 compliant” label real?

Largely no. There is no certification process or registry for compliant cryptocurrencies, because the standard is a messaging format for institutions and has no mechanism for validating or endorsing tokens. Language like “ISO 20022 certified” or “endorsed by ISO” is marketing and is misleading or false. A project can do genuine engineering to make its systems compatible with ISO 20022 data, which is a real but modest technical capability, but that is very different from an official compliance badge. No authority approves or registers tokens under the standard.

Is XRP actually ISO 20022 compliant?

Not in the way the hype implies. Ripple, the company, truly engages with financial messaging standards bodies as part of building institutional payment infrastructure, which is why XRP tops most “ISO 20022 coin” lists. But Ripple’s own chief technology officer has stated plainly that XRP, the token, has nothing to do with ISO 20022. The standard concerns how institutions message each other; XRP is a separate digital asset. A company working with messaging standards does not make its associated token a certified ISO 20022 instrument, so the token level compliance claim is a myth, even though Ripple’s standards work is real.

Should ISO 20022 affect which tokens I buy?

Not on the basis of the compliance label, which does not officially exist. ISO 20022 is a genuine, long-term tailwind for connecting traditional finance and blockchain, and a payments project’s real technical compatibility with the standard can be a small point in its favor. But the standard does not validate, endorse, or guarantee adoption of any token, and banks adopting a messaging standard does not mean banks buying coins. Treating an “ISO 20022 compliant” label as a reason to expect price appreciation means relying on a designation that does not exist and a causal chain that does not hold.

This article is educational information, not investment advice. It aims to clarify a widely misunderstood topic, and details reflect reporting available as of June 26, 2026. Verify current information from primary sources, and be especially cautious of marketing language that implies official certification where none exists.

Ripple CTO Emeritus David Schwartz has settled a renewed debate over XRP (XRP) origins, confirming that a precursor payment network concept predated Bitcoin (BTC) by five years, but that XRP itself did not.

Schwartz responded on X after a social post claimed XRP predated Bitcoin by decades. The post called XRP the oldest digital asset, a label Schwartz addressed directly, drawing a sharp line between an early concept and the coin Ripple manages today.

What Ryan Fugger Designed in 2004

Ryan Fugger conceptualized a decentralized payment and settlement network around 2004. That placed his concept roughly five years before Satoshi Nakamoto published the Bitcoin white paper.

Schwartz confirmed the timeline on X but flagged a crucial omission. Fugger’s design included no decentralized assets. His system, later known as RipplePay, functioned as a trust-based credit network.

Users routed value through pre-existing trust relationships rather than a shared cryptographic ledger. There was no native token and no open asset that could be traded independently.

Schwartz addressed the distinction on X.

However, that separation matters. Bitcoin introduced open bearer assets secured by proof of work. The XRP Ledger brought its own model for decentralized value transfer, but it arrived after Bitcoin, not before.

XRP Launched Three Years After Bitcoin

The XRP Ledger went live in 2012, three years after Bitcoin’s genesis block was mined in January 2009. Jed McCaleb, Arthur Britto, and Schwartz built the protocol together before Ripple assumed stewardship.

That timeline directly dismantles the 1988 claim. Fugger’s concept may predate Bitcoin, but a concept is not a coin. The XRP Ledger and the XRP token both trace their launch to 2012.

The distinction carries weight beyond historical accuracy. Ripple’s CEO has also criticized Bitcoin’s corporate strategy, reflecting broader tensions between the two communities.

The debate reflects a pattern seen across the crypto industry. Origin stories often conflate an idea with its execution. Earlier this year, the Bitcoin CIA creation claim drew broad pushback through a similar dynamic.

XRP Holds Near $1 as Ripple Expands Into Europe

The token recently tested the $1 psychological level amid a sharp slide from earlier highs. Some investors still treat the coin as a long-term inflation hedge, though analysts have found the math difficult to support at current prices.

Schwartz has stayed active in the community beyond the origins question. He recently discussed investing versus gambling in a post that generated its own round of debate among holders.

How far back XRP’s roots run may be less relevant than where Ripple is heading. The company recently obtained European MiCA approval via a Luxembourg license, broadening its regulatory footprint across the continent.

The post XRP Origins Debate Reignites as Ripple’s EX CTO Says Concept Came Before Bitcoin appeared first on BeInCrypto.

Crypto venture activity continued to narrow in 2026 as the number of investors participating in the sector fell sharply from previous cycle highs.

In its latest findings, CryptoRank revealed that the number of unique investors participating in crypto funding activity declined to 651 during the second quarter of 2026, down significantly from the record high of 2,564 investors recorded in 2022.

Crypto Funding Boom Is Fading

According to the data, the only period with lower participation was in 2020, when the quarterly number of active investors ranged between 250 and 450. The analytics firm said the decline points to a venture market that is becoming increasingly concentrated among a smaller group of specialized investors.

Monthly data also showed that investor participation remained weak and uneven over the past year. The number of unique investors stood at 436 in September 2025 and increased to 451 in October before dropping to 316 in November.

The figure recovered slightly to 354 in December but fell again to 273 in January and 224 in February. March saw a brief rebound to 389 investors, although the increase did not last as the figure declined to 229 in April.

Participation rose to 314 in May before falling to 222 in June, the lowest monthly level during the period.

Intense Competition for Investor Capital

The findings also come as Galaxy Research previously reported a slowdown in crypto venture activity. It had reported that crypto venture firms invested around $4 billion across 355 blockchain and crypto deals in the first quarter of 2026, representing a 50% decline in invested capital compared with the previous quarter and a 16% drop in deal count.

Galaxy attributed the slowdown largely to the absence of large late-stage financings that had supported activity in late 2025, although early-stage and seed funding remained relatively stable. The report also found that later-stage startups captured 57% of invested capital during the quarter, while larger and more established companies continued to attract a greater share of funding.

At the same time, fundraising conditions remained challenging as venture firms faced macroeconomic pressures, effects from the crypto downturn, growing investor interest in artificial intelligence, and increased competition from spot crypto ETFs and digital asset treasury companies.

The post Crypto Venture Activity Narrows as Investor Participation Hits 6-Year Low appeared first on CryptoPotato.

Fidelity Digital Assets has pushed back on worries that Bitcoin’s security will weaken as block subsidies shrink through future halvings. In a research report authored by Daniel Gray, Fidelity argues that Bitcoin’s long-term protection is supported by a broader set of economic incentives beyond new coin issuance—particularly transaction fees and the costliness of mounting sustained attacks.

The debate matters because Bitcoin’s issuance schedule mechanically reduces the block reward every four years, eventually turning the network into one primarily funded by fees. Critics have long argued that if transaction fees fail to rise enough to replace falling subsidies, miners’ incentives could weaken and the security budget for the chain could erode.

Key takeaways

- Fidelity says Bitcoin’s security depends on more than block rewards, emphasizing transaction fees and broader incentives that make attacks prohibitively expensive.

- Gray highlights that miner incentives have historically strengthened alongside Bitcoin’s price, even as issuance falls across halving cycles.

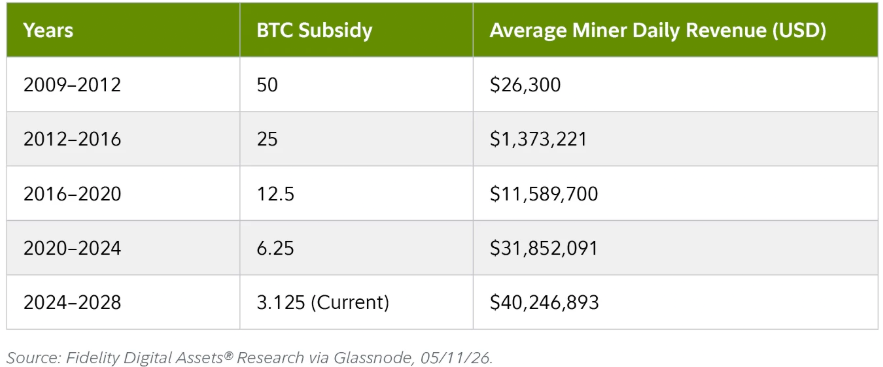

- Since the April 20, 2024 halving, the block subsidy is 3.125 BTC per block, down from 6.25 BTC previously.

- Average daily miner revenue has increased across cycles—from about $26,300 early in the prior halving era to more than $40.2 million today, according to the report.

- Despite Fidelity’s long-term view, publicly traded miners still face near-term funding and operational pressures, contributing to an AI and HPC shift.

Fidelity’s argument: security isn’t only about subsidies

Fidelity’s report challenges a core criticism of Bitcoin’s halving design: that each quadrennial cut reduces miners’ income and could ultimately impair the network’s ability to sustain high levels of mining participation. The concern typically centers on the idea that lower block rewards must eventually be offset by higher transaction fees—or else miners’ profitability could drop to a level that discourages security spending.

Gray’s conclusion is that this framing understates how Bitcoin’s incentive system works in practice. According to Fidelity, the network is not secured by issuance alone. Transaction fees, market dynamics, and other economic forces can keep miners motivated to invest in and maintain the infrastructure needed to protect the blockchain.

In other words, the report argues that declining subsidies do not automatically translate into declining incentives. If the total revenue miners earn—issuance plus fees—holds up or grows, then the security that depends on miners’ willingness to keep operating remains supported.

The post-halving revenue picture

Fidelity anchors its case in the latest halving mechanics and the observed changes in miner income. Since April 20, 2024, Bitcoin miners have received a subsidy of 3.125 BTC per block, compared with 6.25 BTC during the prior cycle.

Gray argues that the reduction in issuance has not weakened miner incentives, largely because Bitcoin’s market price has risen enough to more than compensate. Fidelity points to growth in average daily miner revenue, stating it increased from roughly $26,300 during Bitcoin’s first halving cycle to more than $40.2 million at present.

“Despite declining issuance, miner incentives — and by extension, network security — historically strengthened alongside Bitcoin’s price,” Gray wrote, according to the report.

This is a meaningful distinction for investors and builders: it implies the pathway from subsidies to fee-based security may be less abrupt than critics assume. Instead of treating the halving as an immediate security stress test, Fidelity frames the outcome as dependent on how fees and market conditions evolve relative to the declining reward schedule.

Why transaction fees are central—and why uncertainty remains

Even with Fidelity’s argument, the question of how Bitcoin transitions to fee-led security is still the focal point of long-term risk analysis. The network’s supply schedule is fixed, meaning new issuance will continue to shrink until it eventually disappears. The open uncertainty is whether transaction fees, in combination with other economic forces, will reliably sustain miner incentives through that transition.

Fidelity’s report does not remove that uncertainty; it addresses the claim that halving alone inevitably damages security incentives. By pointing to historical patterns—where miner incentives rose despite declining issuance across previous halving cycles—the report suggests the market has previously adjusted in ways that preserved or strengthened miner profitability.

For readers, the practical takeaway is that monitoring should extend beyond the headline halving reward. The combination of fee levels, total miner revenue, and the broader price trend will likely be more informative indicators of whether security spending remains well supported over time.

Near-term pressure for miners: AI and HPC expansion

While Fidelity frames Bitcoin’s long-term security economics as resilient, the near-term reality for many publicly traded miners has been more difficult. Multiple analysts and industry narratives cited in the broader coverage describe a challenging environment shaped by reduced mining rewards, higher costs, and intense competition.

That pressure has helped drive diversification strategies. Some miners have moved toward artificial intelligence and high-performance computing, leveraging existing power infrastructure and data center assets rather than relying only on Bitcoin mining revenues.

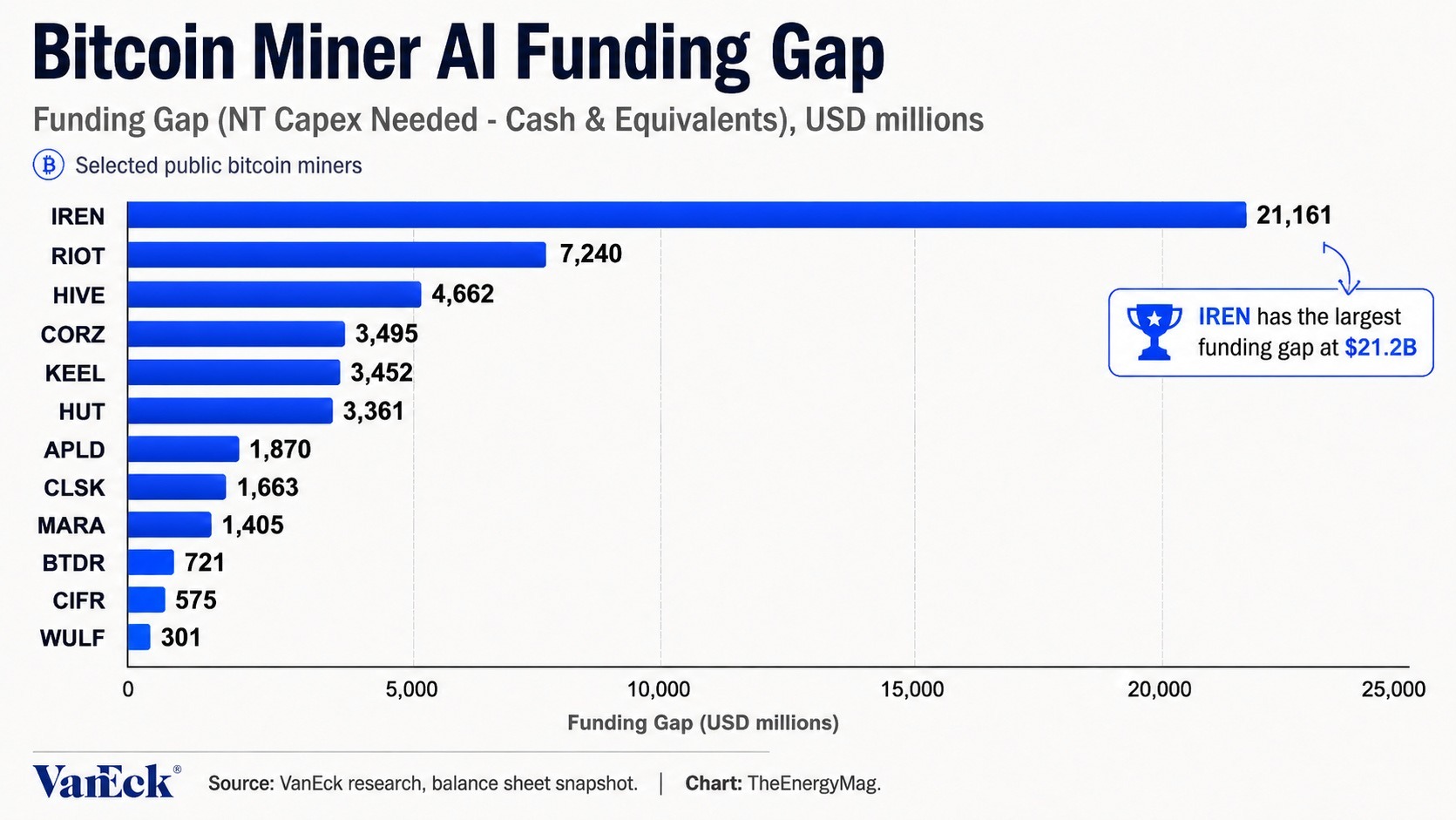

Earlier coverage referenced in the article noted that several miners have been pursuing these alternatives, including a shift towards AI-oriented infrastructure. Separately, a report by VanEck estimated publicly traded miners could require up to $50 billion in additional capital to fully transition to AI infrastructure—an illustration of how large the investment hurdle can be when expanding beyond crypto mining.

Blocksbridge Consulting, quoted in a Miner Weekly publication, highlighted operational differences that matter for business planning: it argued that Bitcoin mining can often be supported with modular infrastructure and ASIC fleets that tolerate fast curtailment, while AI and HPC facilities require higher standards for uptime, cooling, redundancy, networking, and customer support.

This creates an asymmetry investors should pay attention to. Even if Bitcoin’s security budget holds up in the long run, individual mining companies may still face financing constraints and execution risk while they adapt to changing economics and technology demands.

Readers should watch how miners balance these two tracks—supporting Bitcoin’s security today while making capital-heavy bets on future revenue streams. The timing of that pivot, and the ability to raise funds without impairing balance sheets, may become an increasingly important variable for equity holders as the industry continues adjusting to post-halving economics.

The FBI is urging victims of the OneCoin cryptocurrency fraud to apply for government compensation before the June 30, 2026, deadline, with more than $40 million in forfeited assets still available.

The Department of Justice (DOJ) launched the remission claims process on April 13, making funds accessible to eligible investors. Victims can file petitions online, by mail, or by email through onecoinremission.com, the only authorized claims portal.

The $4 Billion Fraud Built on False Promises

OneCoin launched in 2014 out of Sofia, Bulgaria, with its founders marketing it as the next major cryptocurrency. Co-founders Ruja Ignatova and Karl Sebastian Greenwood pitched it as a ground-floor rival to Bitcoin (BTC), drawing in investors across dozens of countries.

Unlike genuine cryptocurrencies, OneCoin had no real blockchain, and its tokens were effectively worthless.

Ignatova and Greenwood drove growth through a multi-level marketing network. Existing investors earned commissions by recruiting new buyers, who then recruited more. As a result, victims worldwide collectively lost more than $4 billion.

Thai authorities arrested Greenwood in July 2018, and U.S. officials extradited him shortly after. He received a 20-year prison sentence in September 2023, with a court order to forfeit $300 million. Ignatova, however, has evaded capture since 2017 and remains on the FBI’s Ten Most Wanted list.

Furthermore, identity change reports suggest she may have altered her appearance, complicating the manhunt.

FBI New York Assistant Director in Charge James C. Barnacle Jr. described the scale of the harm.

“Misled by falsified statements and empty promises, many unknowingly depleted their savings for a fraudulent investment scheme in an emerging financial ecosystem that would never pay out.”

DOJ Warns of New Fraud Targeting Victims

The program covers individuals who purchased OneCoin between Q4 2014 and Q4 2019 and suffered a net financial loss. However, filing a petition does not guarantee compensation.

BeInCrypto covered the DOJ remission program launch in April, when the petition window first opened. Filing is entirely free. The DOJ warned that any third party charging a fee is running a secondary scam. The US State Department offers a $5 million reward for information leading to the arrest of Ignatova.

With June 30 now days away, eligible victims face a narrow filing window. The DOJ’s wider crypto fraud crackdown signals continued enforcement focus, and broader warnings about crypto fraud infrastructure show why this remission fund remains a direct recovery path for OneCoin investors.

The post FBI Urges OneCoin Victims to File for DOJ Compensation Before June 30 appeared first on BeInCrypto.

Crypto World

SpaceX to join the Nasdaq-100 in a fast-tracked process that will drive huge ETF buying demand

The stock of SpaceX continues its consolidation phase on the New York Stock Exchange one week after its Nasdaq listing.

Samuel Boivin | Nurphoto | Getty Images

SpaceX became one of the quickest additions ever to the Nasdaq-100 index, setting up a fresh wave of buying from passive investors less than a month after the company’s blockbuster public debut.

Nasdaq announced after the close Friday that SpaceX qualifies for inclusion in the benchmark technology index. Assuming the company meets the requirements, index-tracking funds and other product sponsors would begin purchasing shares after the market closes on July 6, with SpaceX officially joining the Nasdaq-100 before trading begins on July 7.

More than $800 billion tracks the index, including the Invesco QQQ Trust (QQQ), which is one of the most popular securities traded each day and is seen as a barometer for the artificial intelligence bull market.

The aerospace and satellite company is expected to enter the index with a weighting of less than 1%.

Adding SpaceX this quickly would make the Elon Musk company one of the first beneficiaries of Nasdaq’s recently adopted fast-track inclusion framework for newly public companies. The changes allow some large IPOs to become eligible for the Nasdaq-100 after just 15 trading days, dramatically shortening what had historically been a far longer waiting period.

Under the previous framework, investors tracking the Nasdaq-100 could be forced to wait months before gaining exposure to newly listed market giants.

The inclusion could create another source of demand for SpaceX, which has been one of the most actively traded stocks since its June 12 debut. Index funds and exchange-traded funds tied to the Nasdaq-100 would need to buy shares to match the benchmark’s new composition, while active managers who track the index closely might also adjust positions.

Because SpaceX’s publicly tradable float remains small compared with its total market capitalization, even a modest index weighting could require meaningful purchases from passive investment vehicles.

Earlier this month, S&P Dow Jones Indices declined to create a similar fast-track process for the S&P 500. Therefore, SpaceX remains ineligible for inclusion in the S&P 500 because of that index’s separate profitability and seasoning requirements.

— CNBC’s Leslie Picker contributed reporting.

TLDR:

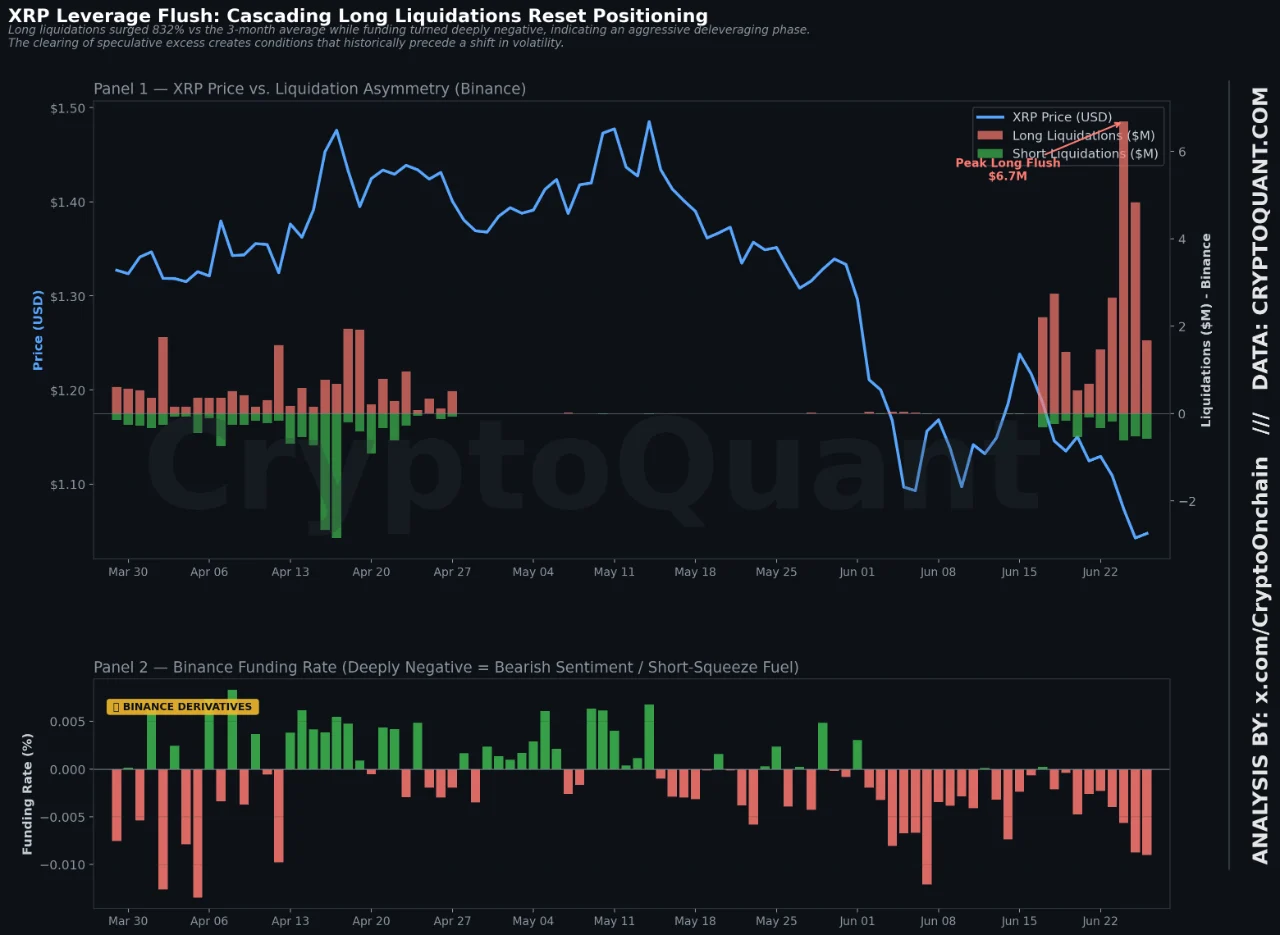

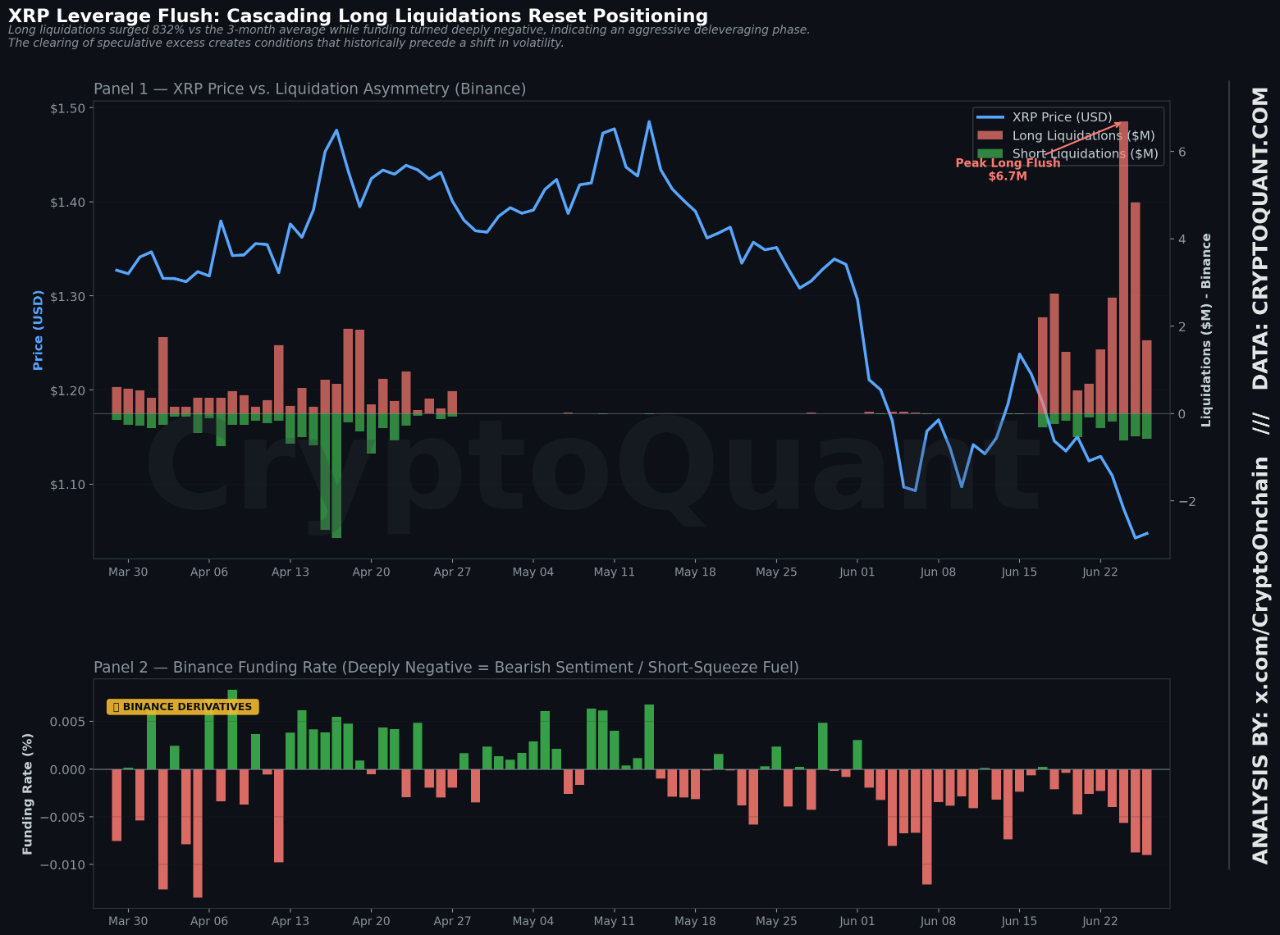

- XRP long liquidations surged 832% over the past week, reaching nearly $3.0 million in forced exits.

- Open Interest dropped from $1.18B to $1.04B, reflecting an 11.1% monthly decline in leveraged exposure.

- Binance XRP reserves fell just 0.35% weekly, showing spot holders remained calm amid futures turmoil.

- A Tom DeMark “9” buy signal and Morning Star Doji pattern suggest XRP could rebound toward $1.30.

XRP derivatives markets recorded a sharp deleveraging episode over the past week, with long liquidations surging 832% versus the prior month.

Open Interest fell from roughly $1.18 billion to approximately $1.04 billion. Funding rates turned deeply negative, registering a -463% shift against the quarterly baseline.

The data points to a forced exit of leveraged long positions rather than an orderly rollover, resetting the market’s overall risk structure.

Cascading Liquidations Clear Speculative Excess From XRP Futures

Long liquidations reached nearly $3.0 million over the seven-day period, far outpacing short liquidations. This imbalance confirms that upside-positioned traders bore the brunt of the selloff. The scale of exits reflects a systematic purge rather than isolated margin calls across the derivatives market.

Open Interest declining by 11.1% on a monthly basis reinforces this interpretation. When OI falls alongside deeply negative funding rates, it typically means leveraged longs are being closed, not transferred. The market is shedding speculative weight accumulated during the prior uptrend.

Source: CryptoQuant

Despite the futures turmoil, spot-side behavior told a different story. Binance XRP reserves remained relatively stable, down just 0.35% on the week.

That restraint among holders suggests limited appetite to deposit tokens for immediate sale, even as price weakened noticeably.

The divergence between panicked futures positioning and composed spot holders is notable. Historically, this kind of split often marks a transitional phase rather than an outright bearish continuation. Whether that transition resolves bullishly depends on how sellers respond next.

Technical Signals and Utility Developments Add Context to XRP’s Next Move

On the technical side, analyst Ali Charts flagged two reversal patterns forming on the daily chart. The Tom DeMark Sequential printed a “9” buy signal, which historically anticipates a one-to-four candle relief rebound.

Additionally, the past three sessions completed a Morning Star Doji formation, a pattern traditionally associated with localized price bottoms.

Ali Charts noted that if buying volume accelerates, XRP could move toward the $1.30 level from current prices near $1.05.

These signals do not guarantee a sustained trend change, but they do indicate potential short-term momentum shifts worth watching.

On the fundamental side, Ripple’s launch of RLUSD in Japan through SBI VC Trust adds a longer-range utility layer to the XRP ecosystem.

Stablecoin infrastructure tied to regulated partners in a major market could support broader adoption over time.

The immediate focus, however, remains on Open Interest recovery. A rebound in OI alongside normalizing funding rates would confirm that fresh demand is entering the market.

Until that happens, the question is whether short-sellers press their advantage or negative funding triggers a short-covering rally.

Fidelity Digital Assets has pushed back against concerns that Bitcoin’s long-term security will deteriorate as mining rewards decline, arguing in a new research report that the network’s economic incentives remain sufficient to secure the blockchain over time.

The report, authored by Fidelity research analyst Daniel Gray, reiterated the view that Bitcoin’s security depends on more than block rewards. Transaction fees, market incentives and other economic forces continue to encourage miners to secure the network and make sustained attacks prohibitively expensive, it said.

The findings challenge a longstanding criticism that each quadrennial halving weakens Bitcoin’s security by reducing the issuance of new coins. Critics argue that declining block rewards could eventually erode miners’ incentives unless transaction fees grow enough to offset the shortfall.

The issue has become one of the most closely watched long-term questions surrounding Bitcoin (BTC), whose fixed supply schedule gradually reduces new issuance until block subsidies eventually disappear. Whether transaction fees and other incentives can sustain network security remains a central debate among developers and market participants.

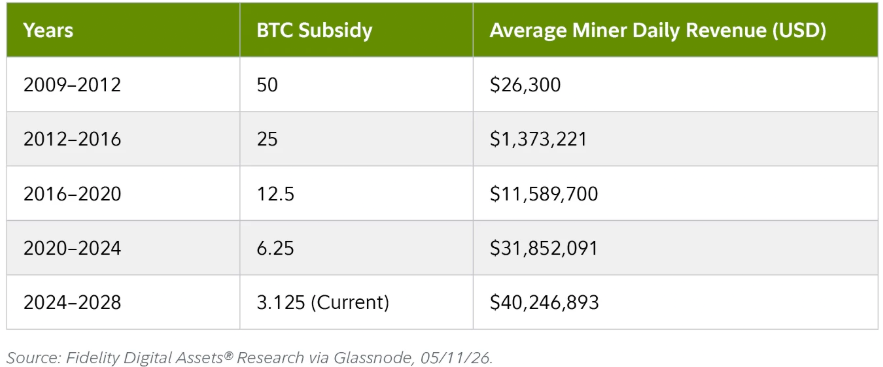

Since April 20, 2024, Bitcoin miners have received a subsidy of 3.125 BTC for each block they mine, down from 6.25 BTC during the previous halving cycle. However, Gray argued that lower issuance has not translated into weaker incentives for miners because Bitcoin’s rising price has more than offset the decline in block rewards.

He pointed to the growth in average daily miner revenue, which increased from roughly $26,300 during Bitcoin’s first halving cycle to more than $40.2 million today. “Despite declining issuance, miner incentives — and by extension, network security — historically strengthened alongside Bitcoin’s price,” Gray wrote.

Bitcoin’s average daily miner revenue has increased substantially across halving cycles. Source: Fidelity Digital Assets

Related: Nvidia’s $20 billion debt boom reinforces Bitcoin miners’ AI pivot

Public Bitcoin miners face mounting financial pressure

While Fidelity argues that Bitcoin’s long-term incentive structure remains intact, many publicly traded mining companies continue to face near-term financial pressure. Some industry analysts have described the current environment as one of the most challenging on record, citing lower mining rewards, rising costs and growing competition.

In response, several miners have diversified into artificial intelligence and high-performance computing, leveraging existing power infrastructure and data center assets to meet growing demand for AI workloads rather than relying solely on Bitcoin mining.

A recent report by VanEck estimated that publicly traded miners could require up to $50 billion in additional capital to fully transition to AI infrastructure, underscoring the scale and cost of the shift.

Public miners face a large funding gap in realizing their AI ambitions. Source: Miner Weekly

“A Bitcoin mine can run with relatively simple buildings, modular infrastructure and ASIC fleets that tolerate fast curtailment,” Blocksbridge Consulting wrote in a recent Miner Weekly publication. “AI and HPC facilities require higher standards for uptime, cooling, electrical redundancy, networking and customer support.”

Digital Currency Group-backed investment firm Yuma has launched the Yuma Total Market Fund, a pooled product designed to give institutional investors diversified exposure to the Bittensor ecosystem—without requiring them to pick individual subnet tokens.

Announced on Thursday, the fund is structured to provide exposure to Bittensor’s native TAO token alongside a basket of AI-focused subnets. Yuma says the aim is to package participation in Bittensor’s decentralized AI infrastructure economy into a single vehicle, with seed capital provided by an undisclosed anchor investor.

Key takeaways

- Yuma’s new fund targets broad exposure to Bittensor via TAO plus a basket of AI subnet assets in one pooled strategy.

- The firm positions the approach as simpler than selecting and managing individual subnet tokens directly.

- Network “subnet value” figures vary materially depending on the tracker used—Yuma cites $900M+ across 128 subnets, while Taostats points to roughly $300M.

- Institutional interest in Bittensor-linked assets has been rising, reflected in Grayscale’s evolving TAO weighting and filings for TAO exchange-traded products.

- Renewed attention to decentralized AI follows US Commerce Department actions impacting access to Anthropic models, underscoring the debate over reliance on centralized providers.

A fund built around Bittensor’s subnet economy

Bittensor is a decentralized network for building AI infrastructure and applications, operating through specialized subnets. These subnets focus on different areas such as compute, marketplaces, and identity. Rather than betting solely on the performance of TAO as a single token, Yuma’s strategy blends exposure to TAO with additional subnet-related assets.

According to Yuma, Bittensor’s 128 subnets collectively represent more than $900 million in combined value. However, data from network tracker Taostats suggests a lower combined subnet value—closer to $300 million. For investors, this gap matters because the “size” of the subnet economy can be measured differently depending on the methodology behind network trackers, and those assumptions influence how meaningful “diversification across subnets” really is.

Yuma did not disclose the anchor investor that provided seed capital. Still, the launch signals a shift in how asset managers are structuring access to decentralized AI systems: instead of treating Bittensor as a single-token theme, they are increasingly packaging it as an ecosystem.

How institutional allocations are changing for TAO

Institutional exposure to Bittensor-linked assets has broadened alongside the network’s expanding subnet economy, and TAO allocations within established funds offer a window into how managers are rebalancing their decentralized AI theses.

In April, Grayscale increased TAO’s weighting in its Grayscale Decentralized AI Fund to 43% during the fund’s quarterly rebalance. Since then, TAO’s allocation has fallen to about 20%, while Near Protocol’s NEAR has become the largest holding at roughly 44%.

That evolution highlights a familiar dynamic in crypto asset management: even when a thesis is “decentralized AI,” the portfolio can still rotate as managers weigh relative opportunities across tokens they view as part of the same broader category. For readers, it suggests that TAO may remain central to decentralized AI exposure, but it is not immune to shifting portfolio construction as other ecosystem players gain weight.

ETF momentum: filings for TAO exposure

Beyond private funds, the push to bring TAO exposure into more traditional investment wrappers is also accelerating. Asset managers have been filing with US regulators to create exchange-traded products tied to Bittensor.

In April, Bitwise filed for a TAO Strategy ETF with the US Securities and Exchange Commission (SEC). Grayscale, meanwhile, submitted an amended registration statement aimed at converting its existing Bittensor Trust into a spot TAO exchange-traded fund that would be listed on NYSE Arca, if approved.

These filings reflect growing demand from investors who want exposure to decentralized AI through regulated market infrastructure. If regulators approve spot TAO structures, it could reduce friction for institutional allocators who prefer standardized instruments over bespoke crypto holdings.

Why decentralized AI is back in focus

The interest in Bittensor’s model is occurring amid renewed scrutiny of centralized AI access. The case for decentralized AI—where AI infrastructure and computing are distributed across blockchain-based networks rather than relying on a single provider—has gained traction after the US Commerce Department suspended public access to Anthropic’s Fable 5 and Mythos 5 models over national security and export control concerns.

Grayscale head of research Zach Pandl argued that the restrictions underscored the risks of centralized control of AI. According to Pandl, investors may seek alternatives such as Bittensor and its TAO token as they look for ways to avoid single-provider chokepoints.

While the restrictions initially tightened, the situation appears to be easing. The Commerce Department restored access to Mythos 5 on Friday, and Axios reported Saturday that the Trump administration is expected to allow Anthropic to resume public access to Fable 5 as soon as next week.

Even if access returns quickly, the episode has already reframed parts of the conversation around decentralized AI. For market participants, it raises a practical question: are investors buying “decentralized AI” as a speculative crypto theme, or as a hedge against policy-driven disruptions that can affect availability and control of AI models?

What to watch next

With Yuma’s fund now live and multiple managers pursuing TAO-linked ETF pathways, the next signal to monitor is how these products structure their exposure to TAO versus subnet baskets—and whether regulatory outcomes for spot listings translate into broader institutional demand for Bittensor ecosystem exposure.

Chinese AI models are gaining ground on Anthropic and OpenAI after Z.ai released GLM-5.2, an open-source system running at roughly one-sixth the cost of US frontier labs. The launch arrived as Washington tightened access to American models.

The timing reshaped the entire competitive picture across the global AI industry in just one week.

How GLM-5.2 is Reshaping the Chinese AI Race

An open-source AI model is a system whose weights can be freely downloaded, fine-tuned, and run on any infrastructure without the original developer’s permission. GLM-5.2 belongs to that category, and its release has triggered the loudest reaction from Silicon Valley since DeepSeek’s debut last year.

The model carries serious technical credentials. Z.ai, formerly known as Zhipu AI, designed GLM-5.2 with 750 billion parameters and a 1-million-token context window.

Furthermore, the system runs entirely on domestic Chinese chips, a critical detail given the ongoing United States export restrictions.

Benchmarks tell the story. GLM-5.2 now sits within a single percentage point of Anthropic’s Opus 4.8 on a closely watched agentic evaluation.

As a result, the gap between Chinese open models and the very top closed US systems has shrunk faster than most industry forecasts had anticipated.

Follow us on X to get the latest news as it happens.

The release timing was anything but accidental. GLM-5.2 launched a day after Anthropic disabled global access to its most advanced models, including Fable 5 and Mythos. Moreover, OpenAI moved to limit access to GPT-5.6 following a separate government request that same week.

Co-founder Tang Jie addressed the contrast directly. He called the Anthropic suspension “deeply regrettable” and said frontier intelligence should not belong to a few people or be subject to sudden rule changes.

Furthermore, his framing positioned Chinese open weights as the safer institutional bet.

Markets responded immediately. Z.ai shares surged more than 30% in Hong Kong trading and now sit up over 800% since debuting in January. JP Morgan projects Z.ai revenue to expand by more than 534% this year, with profitability arriving by 2028.

Why the Chinese AI Push Now Hits Anthropic and OpenAI

The cost advantage is the most damaging factor for US labs. DeepSeek V4 Pro charges $3.48 per million output tokens. Anthropic’s Fable 5 charged $50 for the same output. As a result, enterprise buyers are now openly rethinking their entire AI vendor relationships.

Adoption metrics support the shift. OpenRouter, a popular AI aggregator platform, now shows that Chinese models hold the top four positions among the most widely used systems globally. DeepSeek, MiniMax, Tencent, and Xiaomi have collectively passed every major US frontier provider by token traffic.

The rotation also extends well beyond price. Open-source models can be downloaded, fine-tuned, and run permanently. As a result, neither developers nor governments can revoke access to a system already running on a customer’s own servers, a quality now suddenly more valuable than raw frontier performance.

The competitive picture remains nuanced. DeepSeek itself estimates that Chinese models trail leading US systems by 3 to 6 months in terms of pure capability.

However, that gap matters less when access becomes the primary risk factor, and pricing determines whether production is viable or token economics are prohibitive.

The broader policy backdrop favors the Chinese push. Washington’s restrictions on Anthropic and OpenAI may end up vindicating China’s broader tech self-sufficiency vision, which accelerated after the 2022 Biden administration chip controls landed.

Furthermore, demand for Chinese open models is rising fastest across developing economies worldwide.

Z.ai also plans a dual listing in Shanghai to fund a long-term push toward artificial general intelligence. The next model, GLM-5.5, is expected to launch in August.

The post China’s AI Models Gain Ground on Anthropic and OpenAI appeared first on BeInCrypto.

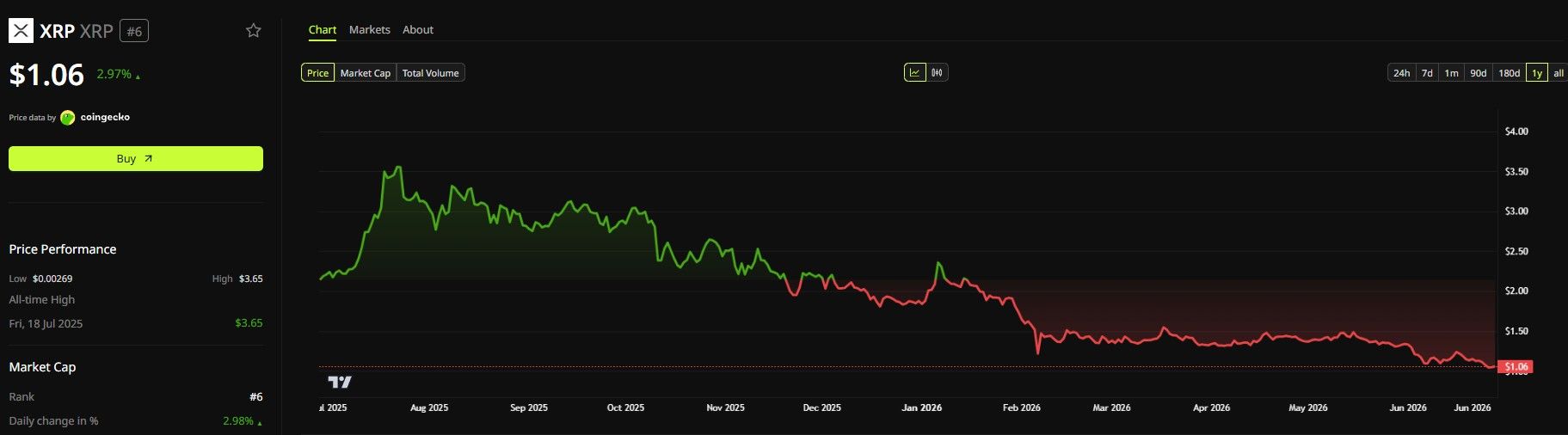

ChatGPT AI just made the case that XRP price prediction worst chapter is finally closing even though the chart has not caught up yet. The model predicts a climb to $3.50 to $5.00 by the end of 2026, with an extreme scenario stretching as far as $6.50.

The bull case treats XRP as a coin whose fundamentals have quietly outrun its price for months. With XRP sitting at $1.05 today, the model leans on the SEC battle being largely behind the asset now, which removes the single biggest overhang that kept institutional money on the sidelines for years.

Expanding institutional adoption of the XRP Ledger is another pillar, alongside growing real world asset tokenization activity that gives the network genuine utility beyond speculation.

RLUSD continues strengthening the broader Ripple ecosystem, and increasing institutional access through spot XRP ETFs adds a fresh on ramp for capital that previously had no clean way into the asset.

The timing piece matters too, since the model expects the broader crypto bull market to regain momentum around November as liquidity improves and US crypto legislation keeps advancing.

If that broader momentum shows up alongside these fundamental improvements, XRP could finally start closing the gap between its improving fundamentals and its lagging price, with an extreme upside scenario opening up if ETF inflows materially exceed expectations and usage accelerates faster than expected.

The bear case zeroes in on something subtle but important. The biggest risk is that Ripple’s enterprise success keeps benefiting RLUSD and its payment network more than it benefits direct XRP demand, meaning the token itself could lag even if the broader ecosystem thrives.

Macro weakness or slower adoption could also keep capital sitting on the sidelines rather than flowing into XRP specifically.

Even with that risk on the table, the model still frames the risk reward as favorable for investors willing to accept volatility, since much of the historical regulatory discount has already been priced out while several real catalysts still lie ahead.

XRP Price Prediction: XRP Waits For Its Fundamentals To Finally Catch The Chart

The daily chart shows XRP at $1.05422 after a brutal, sustained decline from highs above $3.65 set back in July of last year.

That drop has been one of the longest grinding downtrends in this entire series, briefly interrupted by a bounce toward $2.40 in November before sellers took back control completely.

The most recent leg lower in June pushed price to a fresh cycle low near $1.04, right where it sits today. That kind of extended slide with very few meaningful relief rallies suggests sellers have remained firmly in control for the better part of a year.

Resistance sits first near $1.20, the level price keeps failing to hold above during recent bounce attempts, then a much heavier ceiling near $1.60 where multiple rejections piled up earlier this year. Support is being tested right at current levels near $1.04, with no clear floor visible below that on this chart.

The overall pattern here is a textbook descending staircase, similar to what showed up on XRP’s own chart a few weeks back, with each rally attempt landing lower than the one before it.

Momentum on the daily candles looks weak and still pointed down, without much sign yet of the kind of stabilization that usually comes before a real reversal.

Given how far price would need to travel just to reach the low end of this prediction, XRP likely needs to reclaim $1.60 and hold it before the fundamental story ChatGPT is describing starts showing up on the chart instead of just in the headlines.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Discover: The best crypto to diversify your portfolio with

Here is What ChatGPT AI Predicts For LiquidChain Near Future, Very Bullish

Sitting at resistance waiting for a breakout is not positioning. It is standing in line.

Bitcoin, Ethereum, and XRP have been pressing against the same ceilings for weeks. The catalyst that unlocks the next leg is perpetually one data print away.

The institutional inflows are perpetually next quarter. Every large-cap trader waiting for a breakout is waiting on a decision that belongs to someone else’s balance sheet.

Early-stage infrastructure plays by completely different rules, Copilot AI predicts. Capital that would vanish as statistical noise at Bitcoin’s scale moves a small undiscovered project by multiples.

The asymmetric return lives in one place only: the gap between what something is genuinely worth and what the market currently thinks it is worth. That gap exists because the project has not been found yet. The moment it gets found, the gap is gone.

Cross-chain fragmentation has been extracting value from DeFi participants since the first bridge went live and nobody has eliminated it. Bitcoin, Ethereum, and Solana were engineered as independent systems with no shared architecture and no intent to interoperate.

Every transaction that crosses those boundaries pays the price of that design in fees, slippage, and execution failures. Bridges were supposed to be the solution. They became the mechanism through which the problem collects its fee.

LiquidChain eliminates the fee entirely. Three networks inside a single execution layer. One deployment reaches all of them. No cross-chain tax on any interaction anywhere.

ChatGPT AI flagged it as worth watching. The presale is at $0.01454 with just over $860,000 raised.

Execution is unproven. Adoption is unknown. Established assets offer a predictable ride toward a ceiling that is already fully visible. LiquidChain is an entry point that disappears once the market finds it.

The post Sam Altman ChatGPT AI Predicts Crazy XRP Price by End of 2026 appeared first on Cryptonews.

England vs Panama LIVE: World Cup 2026 latest score, match stream, goal updates and fan reaction

Argentina cabinet chief resigns after corruption allegations

XRP Origins Debate Reignites as Ripple’s EX CTO Says Concept Came Before Bitcoin

-

Sports4 days ago

Sports4 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech5 days ago

Tech5 days agoMicrosoft accidentally kills epic Outlook email threads

-

Fashion1 day ago

Fashion1 day agoWeekend Open Thread: Staud – Corporette.com

-

Politics2 days ago

Politics2 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics2 days ago

Politics2 days agoPotential 2028er World Cup attendee leaderboard

-

Business2 days ago

Business2 days agoAsia stock markets slide as tech shares slump

-

Tech2 days ago

Tech2 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World4 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World4 days ago

Crypto World4 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World2 days ago

Crypto World2 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Business4 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Sports1 day ago

Sports1 day agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World18 hours ago

Crypto World18 hours agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Crypto World1 day ago

Crypto World1 day agoRTX holders must register wallets before token distribution begins

-

Crypto World1 day ago

Crypto World1 day agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Sports2 days ago

Sports2 days agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

-

Tech6 days ago

Tech6 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Crypto World2 days ago

The DATA Foundation Launches to Tackle AI’s Multi-Billion Dollar Training Data Bottleneck

-

Crypto World2 days ago

Crypto World2 days agoStrategy (MSTR) has a 10-month cash runway for dividends, but retail investors are losing faith

-

Crypto World2 days ago

Crypto World2 days agoAAVE price tests 9-month trendline after 17% rebound as breakout hopes build

You must be logged in to post a comment Login