Crypto World

What is Lighter? Robinhood’s perps DEX

Lighter is the exchange running perpetual futures inside Robinhood Wallet. It is also the clearest attempt yet to rebuild payment for order flow on a blockchain, backed by the company that made the practice famous.

Summary

- Lighter is a decentralized perpetual futures exchange built as an Ethereum layer 2 using custom zero-knowledge circuits, founded in 2022 by Vladimir Novakovski and live on mainnet since October 2025.

- It is the official perpetuals partner of Robinhood Chain. Eligible users trade perps inside Robinhood Wallet, with USDG as collateral and quote asset, and Robinhood and Lighter split the revenue 50/50.

- The relationship runs deep. Robinhood Ventures joined a $68 million round in November 2025 at roughly $1.5 billion, Tenev serves as an advisor, and Novakovski mentored Tenev early in his career.

- The business model is payment for order flow, rebuilt on-chain: zero fees for retail, with revenue coming from selling access to that order flow to sophisticated firms through premium accounts.

- Americans cannot use it. Perps through Robinhood Wallet are unavailable to residents of the US, UK, Canada, Switzerland, UAE, and Singapore.

Most people encountering Lighter will not encounter it by name. They will open Robinhood Wallet, tap into perpetual futures, and trade. Underneath that tap is a separate company running a zero-knowledge rollup, taking half the revenue, and executing a strategy that would be familiar to anyone who followed the GameStop hearings. Lighter is not simply a venue Robinhood integrated. It is a bet that the most valuable thing in trading is not fees but order flow, and that the way to win the perpetual futures market is to give the trading away and sell what the trading reveals. That idea has a name in traditional finance, and the company whose name is synonymous with it is the one funding this.

What Lighter is

Lighter is a decentralized exchange specializing in perpetual futures, built as an Ethereum layer 2 using custom zero-knowledge circuits. It was founded in 2022 by Vladimir Novakovski, and launched its public mainnet in October 2025 after an extended beta.

The technical pitch addresses a real tension in on-chain derivatives. Perpetual exchanges historically had to choose: sacrifice decentralization for speed, or sacrifice speed for trustlessness. Centralized venues match orders fast and ask you to trust them. Fully on-chain venues are verifiable and slow. Lighter uses zero-knowledge rollup architecture to attempt both, processing transactions off-chain for speed while posting cryptographic proofs on-chain, which produces verifiable order matching and liquidations at latency competitive with centralized exchanges.

That matters more for perps than for most products. A perpetual futures position is leveraged and margined, which means liquidation is automatic and mechanical. If you cannot verify that a liquidation was executed correctly, you are trusting the venue at the exact moment the venue has the least incentive to be honest with you. Verifiable liquidation is not a marketing feature. It is the point.

Its token is LIT. The market has valued the project in the region of $2.75 billion fully diluted, which is a valuation built on distribution rather than on current fee revenue, for reasons the rest of this article explains.

The Robinhood relationship

The integration went live with Robinhood Chain’s mainnet on July 1, 2026, announced at the company’s The World is Flat livestream from the Old Royal Naval College in London.

The mechanics: a revamped Robinhood Wallet gives eligible users access to perpetual futures through Lighter. USDG, a dollar stablecoin, serves as both the collateral and the quote asset. Users can deposit Robinhood Chain assets into Lighter’s smart contracts as margin, and the whole experience sits inside Robinhood Wallet, so users never navigate an unfamiliar DeFi interface. When Lighter added Robinhood Chain collateral support, LIT rose roughly 15%.

Two details tell you this is a partnership and not a vendor arrangement. The revenue splits 50/50 between Robinhood and Lighter. And Lighter committed $11 million of its LIT tokens to the Robinhood community, with eligible users earning points on perp trades and double points when trading through Robinhood.

The history behind it runs further than the deal. Robinhood Ventures participated in Lighter’s $68 million funding round in November 2025, which valued the company at roughly $1.5 billion. Tenev serves as an advisor to Lighter and has publicly called it a step forward for decentralized infrastructure. And Novakovski and Tenev share a professional history stretching back over a decade, with Novakovski having mentored Tenev early in his career. Novakovski described the deal as twelve years in the making, which reads as hyperbole until you notice that Robinhood picked a perps partner run by the person who mentored its CEO.

Lighter frames the Robinhood integration as its first Domain, a template for how the exchange plans to scale: rather than acquiring users directly, it becomes the engine underneath someone else’s front end.

The order flow model

Here is the part that makes Lighter interesting instead of merely well-connected.

Lighter offers zero fees to retail traders. That is not a promotional rate. It is the business model. The revenue comes from the other side: sophisticated firms and high-frequency traders pay for premium accounts that give them access to the venue’s order flow.

Anyone who followed the 2021 retail trading hearings will recognize this immediately. In traditional equity markets, Robinhood does not charge commissions. It routes its customers’ orders to market makers such as Citadel and Virtu, who pay for the privilege. The industry term is payment for order flow, and the economic logic is that retail orders are valuable precisely because they are uninformed. A market maker filling a retail order is unlikely to be trading against someone who knows something. Filling an order from a sophisticated fund is dangerous, because that fund may well know something the market maker does not. Uninformed flow is profitable to intermediate. Informed flow is toxic.

Lighter reproduces that structure on-chain. Aggregate uninformed retail flow by making it free, then monetize access to it. The valuation logic follows: at a multibillion-dollar fully diluted value, the bet is not that Lighter will eventually raise fees. It is that if Lighter becomes the default engine behind Robinhood Wallet’s crypto users, the value of that order flow to market makers rises accordingly. Retail flow crossing over from stock trading is generally less sharp than crypto-native flow, which makes it more valuable to the firms buying access.

That is a genuinely coherent strategy and it is also the reason Lighter’s current fee generation looks thin against competitors running conventional models. The company is not trying to earn on volume. It is trying to own the pipe.

A worked example of the flow trade

The order flow argument is abstract until you price it, so walk the logic the way a market maker would.

Imagine two venues, each routing $200 billion of monthly perpetual futures volume. The first is crypto-native, populated by professional traders, arbitrage desks, and funds running systematic strategies. The second is retail crossover, populated by people who mostly trade equities and take directional views on Bitcoin when it is in the news.

To a market maker, those two order books are not remotely the same asset, and the identical volume figure conceals the difference. On the professional venue, a large share of incoming orders carry information. When a systematic fund lifts your offer, there is a meaningful chance it knows something about the next few seconds that you do not, and you are now holding inventory that is about to move against you. The industry term is toxic flow, and market makers price it by widening spreads, which is the cost of being adversely selected.

On the retail venue, the incoming orders are largely uninformed in the technical sense. Not stupid, and not badly intentioned, simply not carrying private information about the immediate direction of price. A market maker filling those orders can hedge calmly and earn the spread with far less adverse selection. That flow is worth substantially more per dollar of volume, and firms will pay for access to it.

Now the business model resolves. Lighter gives retail trading away for free, because the free trading is what aggregates the valuable flow. It sells premium access to the firms that want to interact with that flow. The more retail volume it aggregates, and the less contaminated that volume is by professional activity, the more the access is worth. Robinhood’s distribution is the input: millions of retail stock traders crossing into perps are close to the ideal population for this model, which is precisely why the partnership exists and why the revenue splits evenly.

That also explains a valuation that looks strange against current fees. At a fully diluted value in the billions, the market is not pricing Lighter’s fee revenue, which is thin by design. It is pricing the possibility that Lighter becomes the default engine behind Robinhood Wallet, at which point the flow it controls becomes considerably more valuable to the firms buying it. The bet is on distribution, not on eventually charging.

The honest counterpoint is that this model has been tested before, at scale, in equities, and it works commercially while generating a permanent argument about whether the customer is the buyer or the product. Nothing about a zero-knowledge proof settles that argument. It only proves that whatever happened, happened as described.

Where it sits in the market

Context matters here, because the perpetuals market is not empty.

Hyperliquid dominates the decentralized perpetuals category and has for some time, having built its position by serving crypto-native traders with high-performance execution. Aster competes on similar ground. Both are fighting for the same audience: sophisticated on-chain traders who care about latency, depth, and fee structure. For more context on the venue Lighter competes against, crypto.news has also examined why HYPE is different inside Hyperliquid’s buyback.

Lighter has explicitly chosen not to fight there. Its positioning is the traditional finance bridge, and its distribution advantage is a pipeline to millions of retail stock traders that no crypto-native competitor can access. That is a defensible strategic choice: the crypto-native segment is contested and price-sensitive, while the retail crossover segment is large, uncontested, and, for the reasons above, more commercially valuable per unit of volume.

The wider context is that fees across perpetual decentralized exchanges are trending toward zero. In a market where nobody can charge, whoever captures the most valuable flow wins. Lighter is not making an unusual bet so much as making the traditional finance bet earlier than its competitors.

Robinhood has expanded the surface around it, offering commodity, ETF, and foreign exchange perpetuals with up to 10x leverage to European users, while its Earn product pays roughly 7% APY on USDG through Morpho infrastructure. USDG therefore does double duty: yield when idle, margin when deployed.

Who cannot use it

The restriction list is long and it includes the country where Robinhood has most of its customers.

Perpetual futures through Robinhood Wallet are unavailable to residents of the United States, United Kingdom, Canada, Switzerland, the United Arab Emirates, and Singapore, along with other restricted jurisdictions.

The American exclusion is the one worth understanding, because it is the same wall that blocks Stock Tokens. Perpetual contracts occupy an unresolved zone in US financial law. The CFTC has historically treated perps as swaps, which places them under derivatives regulation that most crypto platforms are not structured to satisfy. That question is live: the CME is currently litigating against the CFTC over precisely how a perp should be classified, and the CLARITY Act would hand the agency primary authority over digital commodity spot markets while the agency itself operates with a single commissioner.

So an American Robinhood customer can hold the stock of the company that co-owns the revenue from a perps exchange they are legally barred from using. That is not an accident. It is a map of where American crypto regulation currently stands.

The questions worth asking

Three things about this arrangement deserve more scrutiny than they have received.

Whether on-chain payment for order flow attracts the same criticism. The traditional practice drew sustained regulatory attention on the argument that free trading is not free, that customers pay through worse execution, and that the arrangement creates a conflict between a broker’s duty to its customers and its revenue from the firms buying their orders. None of those critiques become less true because the venue posts zero-knowledge proofs. Verifiable matching proves the trade executed as stated. It does not prove the trade was routed to your benefit.

Whether the relationships are disclosed clearly enough. Robinhood Ventures is an investor in Lighter. Tenev is an advisor to Lighter. Novakovski mentored Tenev. Robinhood takes half the revenue. Each of those is individually unremarkable and publicly reported. Together they describe a venue selected through a network of overlapping interests, integrated as the default option inside an app used by millions, and a retail user tapping the perps tab is unlikely to know any of it.

Whether the traffic is real. Robinhood Chain ran a 90-day gas fee subsidy from launch, which inflates transaction counts and makes comparisons with other chains unreliable during the subsidy window. Perps activity routed through the wallet during that period should be read with the same caution. The honest test arrives when the subsidy expires and the flow either persists or does not.

None of this makes Lighter a bad product. The zero-knowledge architecture is a real answer to a real problem, and verifiable liquidation is worth having. It makes Lighter a product whose economics are worth understanding before you use it, which is a different claim and a more useful one. The trade is free. Something is still being sold.

What to watch

Three concrete signals will settle whether this integration is infrastructure or a distribution experiment.

Whether flow persists after the subsidy. Robinhood Chain ran a 90-day gas fee subsidy from launch. Perps routed through the wallet during that window are trading in artificially cheap conditions. The honest measurement of whether retail crossover users actually want perpetual futures arrives when they start paying real costs, and any volume figure quoted before then carries an asterisk.

Whether premium accounts materialize. The entire valuation thesis rests on sophisticated firms paying for access to Robinhood’s retail order flow. That is a testable claim. If market makers commit at scale, the model works and Lighter’s fully diluted value makes sense. If they do not, Lighter is a zero-fee exchange with no revenue and a large token supply, which is a considerably worse business.

Whether the regulatory position moves. Americans are barred from perps through the wallet because perpetual contracts sit in an unresolved zone of US law, where the CFTC has historically treated them as swaps. Two things could change that: the CME’s litigation against the CFTC over how a perp is classified, and the CLARITY Act, which would hand the agency primary authority over digital commodity spot markets. If perps come onshore, Robinhood’s largest customer base becomes addressable overnight and this integration stops being a foreign product.

The last one is the real prize and it explains the patience. Building the perps rail now, with a partner run by the CEO’s mentor, in jurisdictions where it is already legal, means that on the day American rules change the distribution is already wired. Robinhood is not building for the market it has. It is building for the one it expects, which is either foresight or an expensive bet on Congress. Worth noting that the agency holding the decision, the CFTC, currently operates with a single confirmed commissioner out of five seats and has lost roughly a fifth of its staff, while simultaneously writing perps rules, asserting jurisdiction over prediction markets, and preparing to inherit crypto spot markets if the CLARITY Act passes. The timeline for American perps therefore depends less on what Robinhood or Lighter build than on whether one understaffed regulator can produce a rulebook. For a user, the practical takeaway is narrower and more useful: the product exists, it works, it is free, and the reason it is free is that something about your trading is being sold to someone. That is not a scandal. It is the deal, and it is worth knowing you are in it.

Frequently asked questions

What is Lighter?

A decentralized perpetual futures exchange built as an Ethereum layer 2 using custom zero-knowledge circuits, founded in 2022 by Vladimir Novakovski and live on mainnet since October 2025. Its architecture processes trades off-chain for speed while posting cryptographic proofs on-chain, producing verifiable order matching and liquidations at latency competitive with centralized venues. Its token is LIT.

How is Lighter connected to Robinhood?

It is the official perpetuals partner of Robinhood Chain, live since the July 1, 2026 mainnet launch. Eligible users trade perps inside Robinhood Wallet using USDG as collateral and quote asset, and the two companies split revenue 50/50. Robinhood Ventures invested in Lighter’s $68 million round in November 2025 at roughly $1.5 billion, and Vlad Tenev serves as an advisor to the company.

Why does Lighter charge retail nothing?

Because the order flow is the product. Lighter offers zero fees to retail traders and generates revenue by selling sophisticated firms access to that flow through premium accounts. This mirrors payment for order flow in traditional equity markets, where uninformed retail orders are valuable to market makers precisely because they are unlikely to be trading on superior information.

Can Americans use Lighter through Robinhood?

No. Perpetual futures through Robinhood Wallet are unavailable to residents of the United States, United Kingdom, Canada, Switzerland, the United Arab Emirates, and Singapore, among other restricted jurisdictions. Perpetual contracts sit in an unresolved area of US law, where the CFTC has historically treated them as swaps subject to derivatives regulation.

How does Lighter differ from Hyperliquid?

Positioning. Hyperliquid dominates the decentralized perpetuals category by serving crypto-native traders with high-performance execution, and Aster competes on the same ground. Lighter has explicitly chosen not to fight there, positioning itself as a bridge to traditional finance retail through Robinhood’s distribution. Its advantage is access to millions of retail stock traders that crypto-native venues cannot reach.

What is USDG’s role?

It is both the collateral and the quote asset for perpetual futures on the Lighter integration. Users deposit USDG from Robinhood Wallet into Lighter’s smart contracts as margin. The same stablecoin also earns roughly 7% APY through Robinhood Earn’s lending product, built on Morpho infrastructure, giving it a dual purpose: yield when idle, margin when deployed.

What is the LIT token for?

LIT is Lighter’s native token. Lighter committed $11 million of LIT to the Robinhood community as a partner incentive, with eligible users earning points on perpetual trades and double points when trading through Robinhood. LIT rose roughly 15% when Lighter added support for Robinhood Chain collateral. It is a Lighter token, not a Robinhood Chain token, which does not exist.

What are the risks?

Perpetual futures are leveraged instruments and positions can be liquidated rapidly. Beyond that, the order flow model raises the same questions that payment for order flow attracts in equities: free trading may be paid for through execution quality, and the arrangement creates a conflict between routing decisions and revenue. The overlapping relationships between Robinhood and Lighter are publicly reported but unlikely to be visible to a retail user tapping a tab. Traders should also understand reading positioning on perp venues and how collateral works across positions before using leveraged products.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. Perpetual futures are leveraged products carrying substantial risk of loss, including losses exceeding the margin posted, and availability varies sharply by jurisdiction. Nothing here is a recommendation to trade any instrument or use any platform. Always do your own research. Information is accurate as of July 17, 2026.

SBI Holdings has acquired a majority stake in Coinhako after securing regulatory approval for the Singapore crypto exchange deal on July 16.

Summary

- SBI Holdings acquired a majority stake in Coinhako after receiving approval from Singapore’s financial regulator.

- Coinhako gives SBI a licensed base for expanding digital asset services across Southeast Asia.

- The deal complements SBI’s JPYSC stablecoin, Ondo partnership, and Solana-based JX equity token

According to SBI Holdings, the transaction involved a capital injection through SBI Ventures Asset Pte. Ltd. and the purchase of shares from Coinhako’s existing investors. Coinhako will now operate as a consolidated subsidiary of the Japanese financial group.

Approval from the Monetary Authority of Singapore allowed the deal to close on July 16. SBI did not disclose the size of the investment, the percentage of shares acquired, or Coinhako’s valuation under the transaction.

Established in 2014, Coinhako is operated by Hako Technology Pte. Ltd. and holds a Major Payment Institution licence from MAS. Its affiliate, Alpha Hako Ltd., is registered as a virtual asset service provider with the British Virgin Islands Financial Services Commission.

Coinhako gives SBI a regulated Singapore base

Through the acquisition, SBI plans to combine Coinhako’s customers, regional network and crypto operations with the Japanese group’s financial products and international reach. The company identified Singapore as a key market because of its established digital asset regulations and position within Southeast Asia.

SBI Chairman and President Yoshitaka Kitao described the purchase as part of the group’s plan to connect exchanges across multiple countries. According to Kitao, such a network could let investors trade without being limited by national borders or currency differences.

Coinhako’s local presence and regulatory status were central to the decision, Kitao added. SBI expects the exchange to support new services involving stablecoins, tokenized assets, cross-border trading and on-chain finance between Japan and Southeast Asia.

For Coinhako, joining SBI provides access to a financial group with operations across banking, securities and digital assets. Commenting on the acquisition, Coinhako co-founder and CEO Yusho Liu described the deal as the company’s next stage after a decade of operating in Singapore.

“Joining the SBI Group is a natural step for Coinhako to move to the next stage of growth.”

Tokenized assets deepen SBI’s regional strategy

Alongside the Coinhako purchase, SBI has been developing a yen-backed stablecoin called JPYSC with blockchain company Startale. SBI plans to explore its use within the combined group, including possible links to Coinhako’s services and regional customer network.

As previously reported by crypto.news, SBI has also partnered with Ondo Finance to bring tokenized financial products into its ecosystem. Under the agreement, the companies plan to use JPYSC for settlement and collateral while connecting Japanese securities with overseas tokenized markets.

Ondo’s products are expected to reach investors through SBI’s customer network, according to the companies. The partnership also gives SBI another route for using its stablecoin beyond conventional transfers, including transactions involving tokenized securities.

One day before the Coinhako deal closed, SBI Global Asset Management launched the SBI Japan High Dividend Equity Strategy Token, or JX token, with regulated real-world asset exchange DigiFT. Issued on Solana, the product gives accredited and institutional investors blockchain-based exposure to a Japanese high-dividend equity strategy managed by SBI Asset Management Co.

Taken together, SBI’s announcements show how the group is assembling regulated exchanges, tokenized investment products and stablecoin infrastructure across Asia. Coinhako adds a licensed Singapore distribution point to that network, while the Ondo and DigiFT agreements provide financial products that SBI could connect to it.

Morgan Stanley has completed the rollout of Bitcoin, Ethereum, and Solana trading on E*TRADE, charging eligible clients a 0.50% fee on each transaction.

Summary

- E*TRADE now allows eligible clients to trade Bitcoin, Ethereum, and Solana for a 0.50% fee.

- Morgan Stanley plans crypto transfers and a move to its Digital Trust bank later this year.

- The rollout complements Morgan Stanley’s Bitcoin holdings, crypto ETFs and Galaxy Digital lending arrangement.

E*TRADE announced in a press release that supported customers can now buy, sell and hold the three digital assets directly through its brokerage platform. Zerohash provides the underlying crypto infrastructure and holds the assets in linked customer accounts.

Each transaction carries a 50-basis-point fee, according to E*TRADE. While the current service covers trading and custody, the brokerage expects to introduce crypto transfers later this year, allowing clients to move supported assets into and out of their accounts.

Following a pilot launched in May, the completed rollout makes the service available to all eligible E*TRADE customers. Morgan Stanley had first disclosed plans to add direct spot crypto trading in 2025.

Morgan Stanley is expanding several crypto services at once

E*TRADE’s launch comes as Morgan Stanley prepares to add two exchange-traded funds tied to Ethereum and Solana. As previously reported by crypto.news, amended S-1 filings for both products indicated that their launches were approaching, although the filings did not provide a confirmed trading date.

Earlier this year, Morgan Stanley also launched a spot Bitcoin ETF, becoming the first bank to offer such a product, according to the original report. SoSoValue data showed that the fund had accumulated $384 million in net assets at the time of reporting.

Direct trading gives E*TRADE customers another route to crypto exposure alongside Morgan Stanley’s investment funds. Unlike ETF shares, the new service allows eligible users to hold the underlying Bitcoin, Ether and Solana through Zerohash, while the planned transfer feature would give customers more control over moving those assets.

Morgan Stanley had also increased its tracked Bitcoin balance by nearly 1,000 BTC over the two weeks preceding July 11, according to a crypto.news report published that day. The purchases lifted its reported holdings above 5,700 BTC at the time.

Digital Trust is set to take over the crypto service

Later this year, E*TRADE expects to move the crypto offering from Zerohash to Morgan Stanley Digital Trust, the group’s planned national trust bank. The brokerage linked that transition to the introduction of transfer services but did not provide a specific launch date.

Morgan Stanley applied to the Office of the Comptroller of the Currency earlier this year for a crypto-focused national trust bank charter. Its application placed the firm alongside Coinbase, Crypto.com and Ripple, while the OCC has already granted Ripple conditional approval.

Circle has also received OCC approval to establish a national trust bank focused on digital assets. The USDC issuer had secured conditional approval in 2025 alongside BitGo, Fidelity and Paxos.

Morgan Stanley Wealth Management added another crypto route in June through a referral agreement with Galaxy Digital. Under the arrangement, eligible high-net-worth clients can lend Bitcoin, Ether and Solana to Galaxy and receive shares in spot crypto investment products, including the Morgan Stanley Bitcoin Trust.

Taken together, the ETRADE rollout, pending ETF launches and Digital Trust application place trading, investment products, lending referrals and custody infrastructure within Morgan Stanley’s disclosed crypto plans. Each service remains subject to separate eligibility rules, fees and regulatory arrangements set by the companies involved.

Bitcoin remains trapped inside a broader corrective structure after its sharp drop from the mid-$80K region. While buyers have managed to defend the $60K support multiple times, the inability to reclaim key resistance levels continues to favor a cautious outlook in the short term.

Bitcoin Price Analysis: The Daily Chart

On the daily timeframe, BTC is trading around $63K after stabilizing above the major support zone at $60K. This area has repeatedly attracted demand since the early June selloff and continues to serve as the market’s most important defensive level.

Despite the recent consolidation, the broader structure remains bearish. The price is still trading below both the 100-day and 200-day moving averages, which are positioned around the $70K and $73K regions, respectively. Both moving averages are sloping downward, reinforcing the prevailing downtrend.

The recent recovery attempt also failed to reclaim the previous breakdown area around $66K, leaving that zone as the first major resistance. Above it, another significant supply area sits near $74K, aligning closely with the declining 200-day moving average. As long as BTC remains below these levels, rallies are likely to face renewed selling pressure. Should the $60K support fail, the next major downside target appears around $55K, where another higher-timeframe demand zone is located.

BTC/USDT 4-Hour Chart

The 4-hour chart shows that BTC has been consolidating following its sharp decline from the $74K region. The price continues to trade within the broad descending channel while forming a series of higher lows above the $61K support zone.

The immediate resistance remains at $66K, where horizontal resistance intersects with the channel’s descending trendline. This confluence makes it a critical area for bulls to overcome before any stronger recovery can develop.

On the downside, the $61K support has held multiple retests and currently serves as the first line of defense. Losing this level would likely expose the $58K demand zone. The RSI has also been fluctuating around the neutral 50 level, suggesting that bearish momentum has eased and indecision is ruling the market.

A confirmed breakout above both the descending trendline and the $66K resistance zone would improve the short-term outlook and could trigger a move toward the $72K to $74K region. Until then, the market remains vulnerable to another rejection within the prevailing downtrend.

On-Chain Analysis

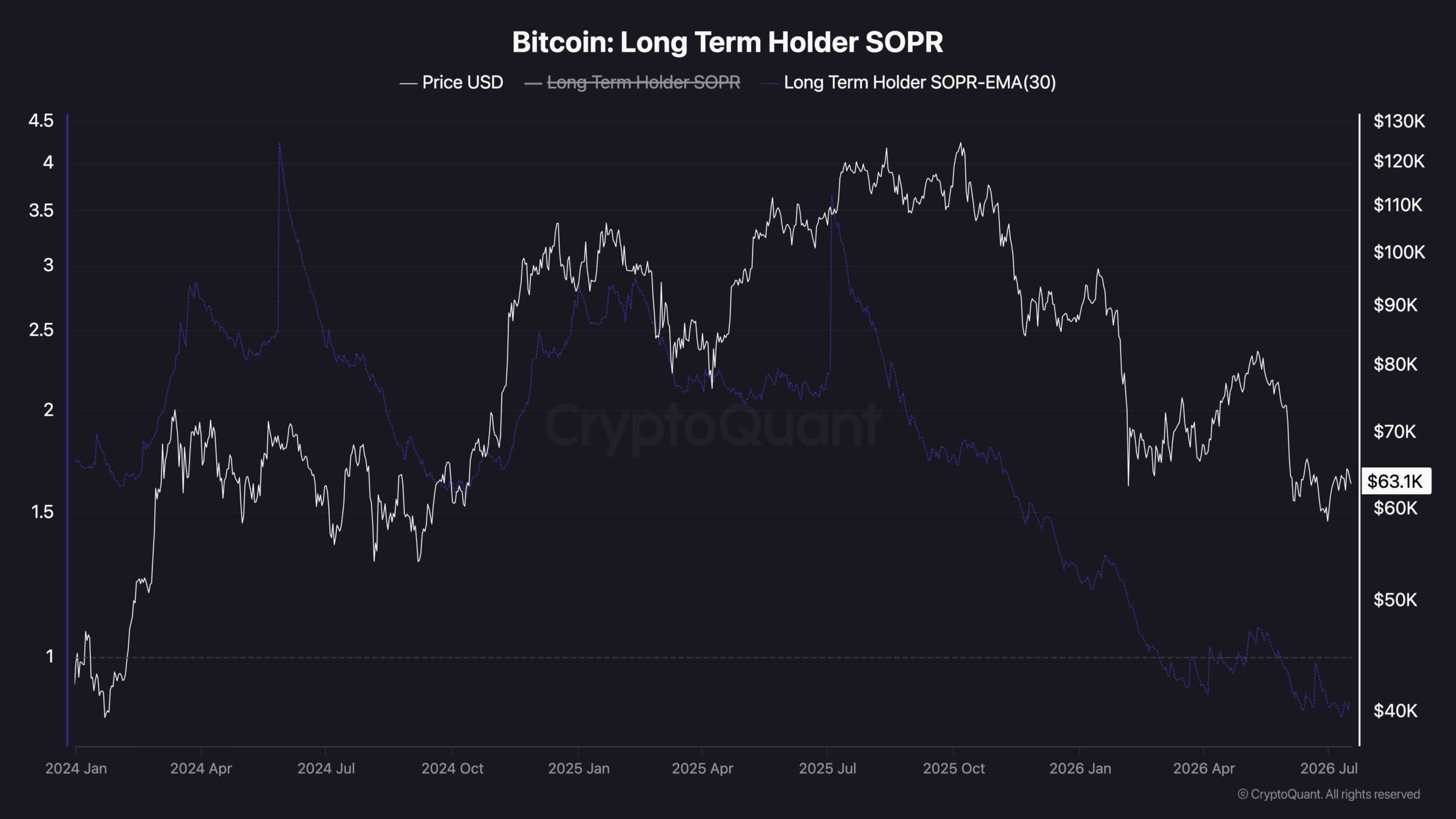

The 30-day exponential moving average of the Long-Term Holder SOPR (Spent Output Profit Ratio) has continued to decline and is now trading below the critical 1.0 threshold. This metric measures whether long-term holders are spending their coins at a profit or a loss, with readings below 1 indicating that coins are being realized at a loss on average.

The breakdown below 1 suggests that a growing portion of long-term investors (who have held their coins for over 6 months) has entered capitulation, choosing to sell despite being underwater. Historically, prolonged periods below this level have coincided with the late stages of corrective phases, when selling pressure from experienced holders intensifies before the market establishes a more durable bottom.

While this shift reflects deteriorating sentiment among long-term participants, it also suggests that the market is moving deeper into a redistribution phase. If the indicator quickly recovers above 1, it would imply that the recent capitulation was temporary. However, a sustained stay below this threshold would signal continued weakness and increase the likelihood of further downside, particularly if Bitcoin loses the key $60K support zone.

The post Bitcoin Price Analysis: Is BTC Headed Below $60K After $65.5K Rejection? appeared first on CryptoPotato.

Bitcoin (BTC) dipped below $62,500 at Friday’s Wall Street open as stocks took a fresh hit from the US-Iran war.

Key points:

- Bitcoin gives traders a sense of deja-vu as local highs spark rejection and rangebound moves continue.

- The US-Iran war pushes stocks and crypto lower.

- A bear-market trend line is now in place as resistance, copying historical patterns.

BTC price action stays “very choppy”

Data from TradingView showed BTC/USD extending losses with up to 2% daily downside.

BTC/USD one-hour chart. Source: Cointelegraph/TradingView

US stocks opened in the red, with the Nasdaq Composite Index also down nearly 2% at the time of writing. Fresh military strikes on Iran fueled the risk-asset retreat, while tech stocks continued to see selling pressure.

Trading resource The Kobeissi Letter also flagged weakness arising from earnings disappointments, with Netflix shedding over 10% to start the US session.

“The stock is now down -50% over the last 12 months and trading at its lowest level since August 2024,” it noted in a post on X.

Netflix stock one-day chart. Source: Cointelegraph/TradingView

After hitting three-week highs, BTC price action fell back into its established range as traders saw copycat moves.

“Market just keeps repeating same things,” commentator Exitpump wrote on X.

“Dump into passive demand, OI increases with shorts piling up while spot starts buying which leads to bounce.”

BTC/USDT five-minute chart with order-book data. Source: Exitpump/X

Trader Daan Crypto Trades argued that current behavior was “typical” of summer.

“Very choppy few days up, few days down kind of price action the last few weeks. No real action anywhere really,” he summarized.

BTC/USD four-hour chart. Source: Daan Crypto Trades/X

Bitcoin seals key bear-market repeat

Trader Jelle, meanwhile, remained optimistic, seeing range lows holding.

Related: Bitcoin bottom countdown nears 50 days after BTC supply in loss passed 50%

“Still think this looks good for a relief rally in the next weeks – which would give the market room to drop into October without nuking much deeper,” he told X followers.

BTC/USD one-day chart. Source: Jelle/X

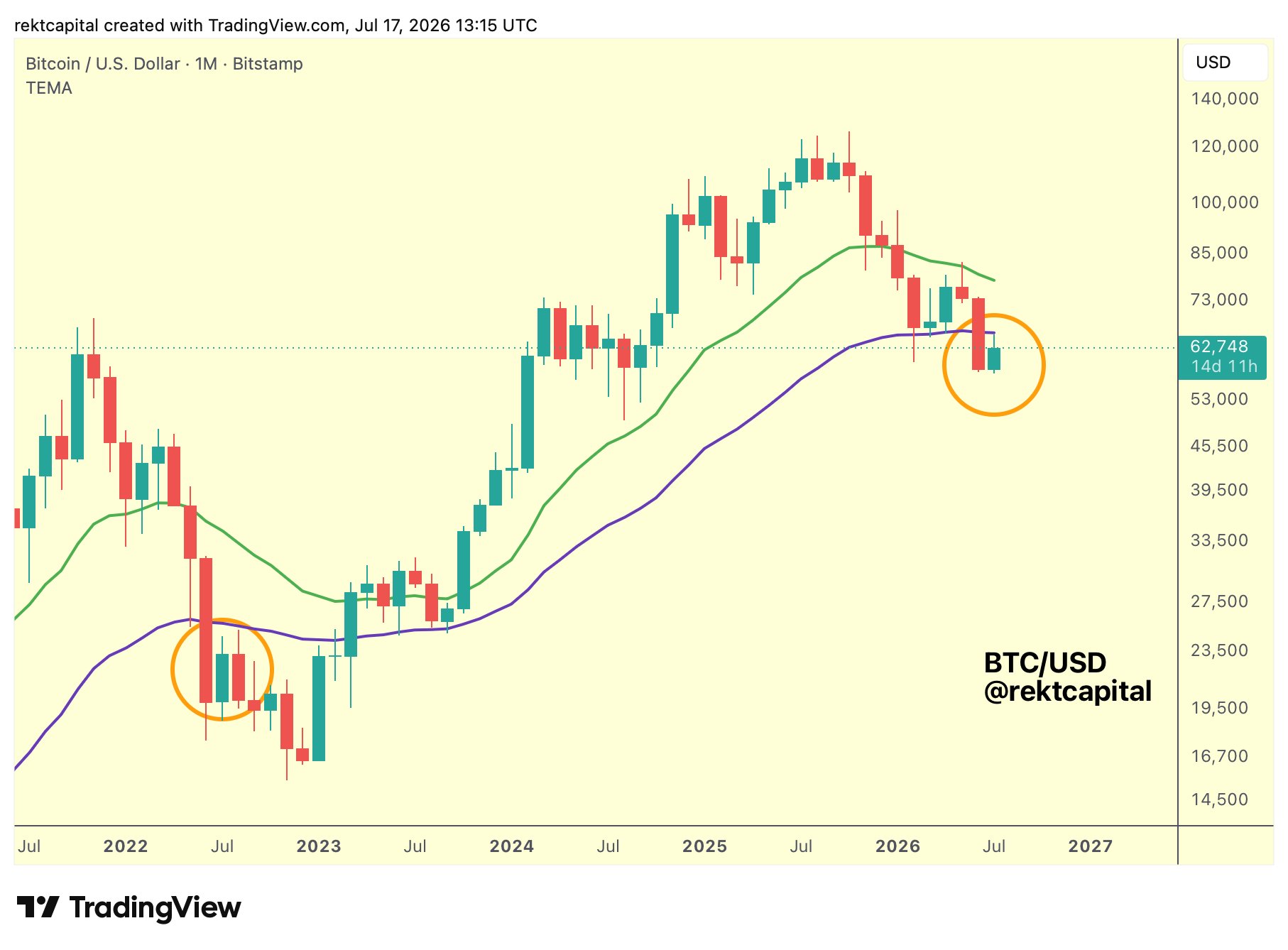

In updates on the bear market’s progress, trader and analyst Rekt Capital suggested that Bitcoin’s long-term downtrend was now in its final stages.

BTC/USD, he wrote, had flipped its 50-month exponential moving average (EMA) to resistance, repeating bear-market history to set up its drop to a long-term floor.

“The necessary technical milestone has been achieved,” he confirmed.

“Which technically indicates that the majority of the anticipated move has already happened.”

BTC/USD one-month chart with 21, 50EMA. Source: Rekt Capital/X

As Cointelegraph reported, Rekt Capital saw the July relief bounce ending with the onset of next month.

Benjamin Cowen’s July memo puts the next Bitcoin bottom in the fourth quarter of 2026. His seasonal math implies a floor near $44,000, and his framework has formally shifted into bottom-watch mode.

Cowen, a member of BeInCrypto’s Market Intelligence experts council, argues the reset now depends on time rather than a single price level. His projection lands inside the $44,000 to $47,000 zone that BeInCrypto’s models identified one week earlier.

The 2019 Analog Runs Out of Time

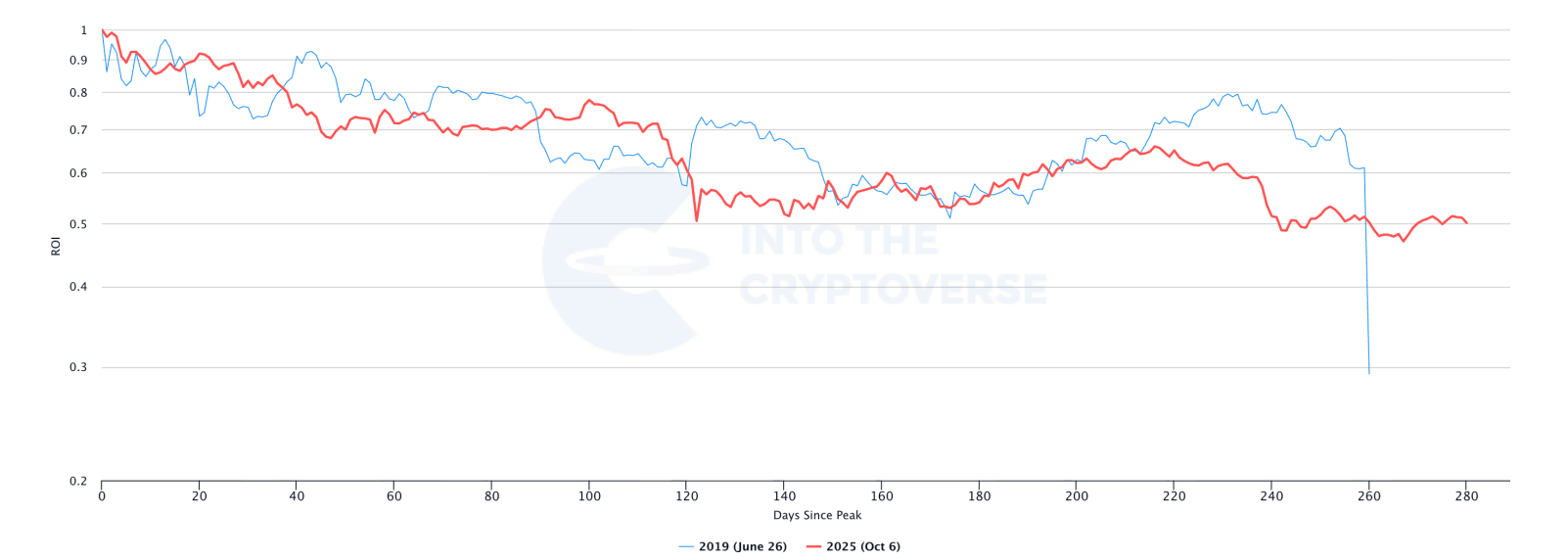

The core thesis of the memo compares the October 2025 top with the June 2019 top. Both peaks arrived on apathy rather than euphoria, and both printed weeks before quantitative tightening formally ended.

Bitcoin (BTC) has now spent 282 days in its drawdown. The 2019 analog bottomed at day 261, when the March 2020 pandemic crash reset every indicator at once.

Cowen treats that flush as an external shock, not a cycle mechanism. Because the analog expired without a similar event, he expects this reset to complete through time instead.

The current path sits at 0.520 of the October 2025 record above $126,000, a 48% decline. Meanwhile, retail attention never returned. New views across major crypto YouTube channels sit near 389,000, an order of magnitude below the 2021 peak near four million.

That reading fits the broader picture of washed-out crypto sentiment that BeInCrypto reported this week. Cowen calls it the apathy signature, and it separates this cycle from the euphoric tops of 2017 and 2021.

Midterm Years Save the Worst for Last

2026 is a midterm election year, historically the weakest of Bitcoin’s four-year cycle. The prior midterms in 2014, 2018, and 2022 all decayed through the second half, and none rallied into year-end.

July has typically been constructive in those years, and 2026 is tracking that tendency. However, August and September turned negative in all three prior midterms, with August losses between 15% and 18%.

Cowen’s year-to-date measure has bounced to 0.731, back above the midterm average. Applying the historical decay path would drag that reading to roughly 0.49 by year-end, which implies a price near $43,800.

He stresses the figure is an illustrative projection from three observations, not a target. Still, the direction was consistent across all three prior midterms.

Two of those cycles bottomed inside the midterm year itself, in December 2018 and November 2022. The 2014 cycle spilled into January 2015, which keeps early 2027 on the table.

The macro backdrop adds pressure. The Warsh Fed removed its easing bias while the energy-led disinflation fades, a combination that keeps real rates elevated into the same fourth-quarter window.

Why the On-Chain Reset Isn’t Done

On-chain data explains why Cowen doubts the low is already in. The MVRV Z-Score reads 0.395, and prior cycle bottoms formed only after the metric reset below zero.

That reset requires price to trade beneath the realized price; the market’s aggregate cost basis is near $53,000. The early-summer low of about $57,000 approached that level without reaching it.

His $43,800 estimate, therefore, sits inside the corridor between realized price and balanced price at $37,700. Cowen’s broader risk scorecard supports that read. On-chain risk sits at 0.188 and Bitcoin risk at 0.311, both far below their readings near the top one year ago.

Yet the valuation reset remains less advanced than the distressed July 2022 phase. BeInCrypto’s models reached the same region one week earlier.

BeInCrypto’s analysis of the final 91-day window projected a bottom between $44,000 and $47,000 by early October. A regression on past drawdowns and a logarithmic Fibonacci retracement converged on that zone.

The log Fibonacci midpoint sits at $44,428, within roughly $700 of Cowen’s figure. Two independent frameworks now point to the same floor and the same quarter.

Institutional forecasts frame a similar range. The wider Bitcoin bottom debate spans Standard Chartered’s $59,000 floor and Galaxy’s $40,000 scenario, and both reject a deeper crash this cycle.

Bitcoin Bottom Watch Is On, But Confirmation Is Far Away

The supply profit and loss cross gives Cowen his trigger. Supply in loss briefly exceeded supply in profit at the summer low, a condition that historically preceded entry into bottoming windows.

The bounce has since lifted supply in profit back to 56.83%. Cowen reads the whipsaw as typical of a bottoming window measured in months rather than a single clean event.

Cowen wrote:

“The framework is in bottom-watch mode, with the low most likely a matter of months rather than weeks away.”

Structural demand has also cooled. ETF holdings peaked above 1.25 million BTC in late 2025 and have since rolled over, with the decline steepening in recent weeks. The marginal bid that absorbed supply on the way up has faded.

Price structure tells the same story. Bitcoin reclaimed its 200-week SMA near $63,100, yet the identical break-and-reclaim sequence appeared in 2022 before the final low arrived.

Confirmation, in his framework, requires two consecutive weekly closes above the 50-week SMA near $86,500. Bitcoin’s current price of about $63,158, down 2.7% in 24 hours, sits roughly 37% below that level.

Cowen also assembles the bull case. Price sits on the first percentile of his long-run quantile model, ETF-era demand could lift the floor, and the absent crowd leaves few forced sellers for a final flush.

For now, the calendar, the on-chain reset, and BeInCrypto’s own models point to the same window. The next test comes quickly, as August will show whether the midterm pattern repeats or finally breaks.

The post Benjamin Cowen’s New Memo Points to Q4 Bitcoin Bottom Near $44,000 appeared first on BeInCrypto.

Crypto World

Bitcoin, Ethereum Reverse CPI-Fueled Gains as Strategy Stays Quiet: Your Weekly Crypto Recap

Bitcoin dipped on a couple of occasions below $62,000 during the previous business week, prompted by Strategy’s largest sale to date and the renewed attacks in the Middle East. However, it recovered a lot of ground by the weekend and spent it trading sideways at around $64,000.

Monday began with another nosedive to under the aforementioned level as the market priced in the new attacks between the US and Iran from Saturday and Sunday. Nevertheless, the bulls showed strong conviction and managed to defend that level.

All eyes turned to the US CPI data for June, which went live on Tuesday. Most market experts believed there would be a significant reduction from the May multi-year record, from 4.2% to somewhere around 3.8%-3.9%. However, the actual data was even more promising, showing a drop to 3.5%.

The primary cryptocurrency reacted immediately to the seemingly slowing inflation, rocketing to $64,000 within hours and up to $65,500 on Wednesday. The latter became its highest price tag in approximately three weeks.

However, BTC’s rally came to a halt at that point. The cryptocurrency started a gradual decrease, which pushed it south to $62,400 earlier today. Although it has recovered about a grand since then, it’s still down by more than 2% weekly. Many altcoins have shown even more profound losses, with HYPE leading this adverse trend.

Hyperliquid’s native token has plunged by more than 12% since this time last Friday, followed by SOL’s 6.5% drop and ADA’s near 6% decrease. In contrast, ONDO has jumped by almost 12%, while ZEC is up by 3.7%.

Market Data

Market Cap: $2.254T | 24H Vol: $61B | BTC Dominance: 56.5%

BTC: $63,210 (-2.45%) | ETH: $1,825 (+0.74%) | XRP: $1.08 (-3.2%)

This Week’s Crypto Headlines You Can’t Miss

Trump’s New Iran Strategy Revealed: Will Bitcoin Pay the Price Again? After the ceasefire breakdown, reports emerged during the past week outlining Trump’s new strategy against Iran. The new wave of attacks will reportedly involve strikes with a wider scope than the previous ones, which increases the pressure on risk-on assets like BTC.

CRO Surges as Crypto.com Secures $400M in Citadel Securities-Led Funding. In its first-ever institutional funding round, the popular crypto exchange secured a $400 million investment from Citadel Securities. Its native token jumped immediately by 25%, but it was quickly halted and returned to its starting point.

Ripple (XRP) Peaked at $3.65 Exactly a Year Ago: What Went Wrong? It was a year ago today that the cross-border token flew to $3.65 to set a new all-time high. The following 12 months, though, have been quite painful, with the asset dumping by 70%. Nevertheless, the company behind it continues to make major moves. Here are many of them.

Jesse Pollak Leaves Base Leadership After Failed Social Strategy. Base creator Jesse Pollak admitted to adopting the wrong strategy when developing the network, focusing mainly on the social side of the market. Consequently, he decided to step down from his leadership position.

Peter Schiff: Bitcoin Holders Will Soon Regret Not Selling at Current Levels. The full-time BTC critic did in the past week what he has been doing for many years. He used the opportunity to urge bitcoin investors to offload their positions at current levels, as they might regret not doing so soon.

Saylor’s Strategy Boosts USD Reserves by $450M Without Selling BTC: Here’s How. Mondays have become quite intriguing lately due to Strategy’s pivot. After the previous week’s sale, investors expected new controversial announcements from the largest corporate holder of bitcoin. Instead, the firm simply boosted its USD reserve and refrained from making any BTC-related moves.

The post Bitcoin, Ethereum Reverse CPI-Fueled Gains as Strategy Stays Quiet: Your Weekly Crypto Recap appeared first on CryptoPotato.

Japan’s SBI Holdings has moved to tighten its grip on the Asian crypto market after regulators in Singapore cleared its planned takeover of Coinhako. The financial services group said it has acquired a majority stake in Holdbuild, the parent company of the Singapore-based crypto exchange Coinhako, following approval from the Monetary Authority of Singapore (MAS).

In an announcement made Thursday, SBI stated that MAS authorization allowed it to acquire shares from existing shareholders via a capital injection. As a result, Coinhako will become a consolidated subsidiary of SBI, giving the Japanese company direct control over a regulated trading platform operating in one of Asia’s most important financial hubs.

Key takeaways

- SBI acquired a majority stake in Holdbuild, the parent of Coinhako, after MAS approval.

- MAS authorization enabled the deal through a capital injection, making Coinhako a consolidated SBI subsidiary.

- Coinhako operates under a Major Payment Institution license via its subsidiary, Hako Technology Pte. Ltd.

- SBI says it will combine Coinhako’s customer base and regional footprint with its own financial services and digital asset initiatives, including JPYSC.

- Financial terms were not disclosed, and SBI did not provide immediate additional details about the transaction.

Singapore regulator clears SBI’s majority stake

SBI’s move centers on Coinhako’s corporate structure in Singapore. The exchange is held through Holdbuild, and Coinhako itself operates with a Major Payment Institution license granted by MAS through Hako Technology Pte. Ltd. That licensing context matters because it ties the exchange’s activities to the regulatory framework governing payment-related services in Singapore.

According to SBI’s announcement, the key gating item was MAS approval. Once granted, SBI proceeded with a share acquisition from existing shareholders through a capital injection rather than disclosing other transaction mechanics. With the approval now complete, SBI’s ownership shift enables Coinhako to be brought into SBI’s consolidation scope.

SBI previously outlined its intention to buy a majority stake in February, setting up expectations that the acquisition would require regulatory confirmation before finalization. Thursday’s update effectively marks the transition from planned consolidation to execution.

Why the Coinhako platform fits SBI’s regional strategy

SBI framed Singapore as a core part of its digital asset strategy and presented the Coinhako acquisition as a way to strengthen its presence in Southeast Asia. In practical terms, SBI said it wants to combine Coinhako’s customer base and regional network with its own financial services and digital asset business lines.

That includes SBI’s JPYSC stablecoin initiative. While the announcement does not provide new technical details in the material provided, SBI’s stated intent signals that it sees value in connecting a regulated exchange footprint with settlement and collateral workflows tied to its stablecoin effort.

For investors and market participants, the consolidation of Coinhako matters because it can accelerate SBI’s ability to deploy its digital asset ambitions beyond Japan. It also reduces the friction of building distribution from scratch in an already regulated environment where local partners and compliance infrastructure often determine speed to market.

SBI also pointed to operational steps following the acquisition, including plans to hold its first overseas branch managers’ meeting in Singapore this summer. The company’s emphasis on on-the-ground leadership suggests it intends to treat the Singapore expansion as more than a passive investment.

SBI’s rapid build-out: acquisitions, tokenization, and infrastructure

The Coinhako deal lands amid a broader push by SBI to expand its digital asset footprint through acquisitions, partnerships, and blockchain-focused projects. Earlier in the same month, SBI led a $76 million Series C funding round for institutional crypto exchange EDX Markets, according to the information in the source material. SBI also said it plans to acquire Bitbank for $289 million, a strategy aimed at positioning the combined operations among Japan’s largest crypto exchanges.

That pattern—buying regulated or institution-facing platforms and then layering in SBI’s technology and financial products—appears to be consistent across markets. In addition to the Coinhako acquisition, SBI has been pursuing tokenization initiatives. This week, SBI partnered with Ondo Finance to bring tokenized Japanese stocks to market while integrating JPYSC stablecoin into settlement and collateral workflows, as referenced in the source material via an Ondo-related announcement.

In February, SBI and Startale Group unveiled Strium, a layer-1 blockchain designed around tokenized securities and real-world assets. The source material describes the network as intended to support 24/7 trading and tokenized equity settlement, as SBI expands its infrastructure for institutional financial applications.

Taken together, these moves show SBI trying to connect three parts of the crypto stack: regulated market access (via exchanges), asset tokenization (via security and RWA initiatives), and settlement infrastructure (via stablecoins and blockchain rails). The Coinhako acquisition fits that blueprint by bringing a Southeast Asian user base and trading operation into SBI’s consolidated structure.

What remains unclear and what to watch next

While SBI confirmed the majority stake acquisition and the regulatory basis for it, the company did not disclose financial terms in the announcement. SBI also did not immediately provide additional details when the source attempted to contact the company for transaction information.

For the weeks ahead, readers should watch for how SBI integrates Coinhako into its product roadmap—particularly whether the exchange’s operations become more directly tied to JPYSC settlement or other SBI-linked digital asset services. With Coinhako now positioned as a consolidated subsidiary, the next sign of progress may be changes to operational structure, regional expansion plans, or partnerships that leverage SBI’s institutional and tokenization efforts.

Key takeaways

- Solana (SOL) is down nearly 2% over the past 24 hours after failing to break above the crucial $78 resistance.

- Spot Solana ETFs have recorded net outflows, signaling weaker institutional demand.

- A break below $74 could send SOL toward $64, while a breakout above $78 may trigger a rally to $90.

Solana (SOL) extended its recent pullback on Friday, falling nearly 2% over the past 24 hours as buyers once again failed to overcome the key resistance level at $78.

Although cooling U.S. inflation briefly boosted risk appetite earlier this week, the rally lacked enough momentum to sustain a breakout. At the same time, declining trading volumes and renewed ETF outflows have added to the cautious outlook.

Trading activity cools after recent rally

Market participation has slowed noticeably in recent sessions. Daily trading volume has fallen from a short-term peak of approximately $4 billion on July 2 to around $2 billion, suggesting reduced buying interest following the recent rebound.

The inability to break above the $78 resistance despite improving macroeconomic sentiment indicates that bullish momentum may be weakening.

Institutional sentiment has also softened. According to CoinGlass, Solana-focused exchange-traded funds (ETFs) have recorded approximately $700,000 in net outflows this week.

The reversal contrasts with recent weeks, when Solana ETFs attracted more than $1.1 million in inflows and accumulated nearly $3 million since the beginning of the month.

The shift suggests institutional investors remain cautious as uncertainty surrounding interest rates and broader market conditions continues to weigh on risk assets.

Despite weaker price action, Solana’s network fundamentals continue to improve.

Data from Santiment shows that daily active addresses (DAAs) have continued to climb, indicating growing user activity across the network.

Notably, the 30-day moving average of daily active addresses has crossed above the 50-day moving average, with the gap widening in recent days.

Historically, similar crossovers have preceded significant price movements for Solana, although they do not indicate whether the move will ultimately be bullish or bearish.

The increase in active wallets suggests investors are positioning ahead of the token’s next major directional move.

SOL faces a critical technical crossroads

Technically, Solana remains trapped below the important $78 resistance level. The repeated rejection at this price has reinforced it as a key barrier that bulls must overcome before a sustained recovery can develop.

On the downside, the immediate focus shifts to the ascending trendline support near $74. This level represents a crucial defense for buyers.

If $74 fails to hold, Solana could accelerate lower toward the next major support around $64.

Momentum indicators are beginning to favor the bears. The Relative Strength Index (RSI) has slipped to around 49, falling below its signal line and indicating weakening bullish momentum.

A move toward 40 would strengthen the bearish outlook and suggest sellers have gained greater control.

Conversely, a decisive breakout above $78 could trigger a wave of short covering, as a significant number of stop-loss orders are believed to be positioned above that level.

Such a move could accelerate buying momentum and open the door for a rally toward $90.

For now, Solana remains at a pivotal technical level, with declining institutional flows contrasting against strengthening on-chain activity. The next breakout or breakdown is likely to determine the token’s short-term direction.

Crypto World

Following Ripple’s European regulatory approval, EX DeFi enabled XRP investors to earn $15,000 daily

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

As XRP ETF expectations rise, investors are exploring platforms like EX DeFi that offer alternative ways to participate in the digital asset ecosystem.

Summary

- EX DeFi expands its cloud mining platform as growing interest in XRP ETFs boosts attention on digital asset services.

- EX DeFi highlights cloud mining and platform security as XRP ETF optimism drives interest in crypto infrastructure.

- Rising XRP ETF expectations fuel interest in EX DeFi’s cloud mining platform and digital asset infrastructure.

With Ripple obtaining a crypto asset services license under the European MiCA (Crypto Asset Market Regulation) framework, market attention on the XRP ecosystem has surged again.

Simultaneously, Ripple continues to advance its RLUSD stablecoin, institutional-grade cross-border payments, asset tokenization (RWA), and XRP Ledger ecosystem development, further expanding its global digital finance footprint.

ETFs, regulation, and institutional funding remain key variables

As European regulations gradually take effect and digital asset regulatory frameworks such as the US Clarity Act continue to advance, market attention on XRP ETFs is constantly increasing. Some market institutions believe that if XRP ETFs continue to attract institutional inflows and more banks adopt XRP for cross-border payment settlements, its long-term prospects are likely to improve further.

Meanwhile, Ripple is continuously improving its digital financial infrastructure, including expanding its global payment network, promoting asset tokenization (RWA) applications, and supporting digital settlement in financial markets. As blockchain technology matures, more and more investors are focusing on diversified participation methods beyond directly holding digital assets.

EX DeFi offers digital asset investors more ways to participate.

Against the backdrop of the evolving digital asset ecosystem, EX DeFi has launched a data center cloud mining platform based on green energy. Users can choose different digital asset computing power solutions according to their needs without purchasing mining rigs or maintaining equipment themselves. The platform provides users with a more convenient and efficient digital asset service experience through automated management, a transparent profit settlement mechanism, and a multi-layered security architecture.

Ripple ecosystem development drives market attention, and EX DeFi continues to improve its platform

With Ripple obtaining regulatory approval in Europe, the compliance process in the digital asset industry has been further advanced, increasing market attention to the development of related ecosystems. Against this backdrop, EX DeFi continues to improve its platform infrastructure, security system, and service capabilities, committed to providing global users with more stable and transparent digital asset services.

The platform states that it currently covers over 180 countries and regions globally, serving more than 2 million users. It utilizes green energy data centers, multi-layered data encryption, automated computing power management, and a transparent profit settlement mechanism to provide users with a long-term, stable cloud mining experience.

How EX DeFi ensures user asset security

Fund security has always been a crucial component of the EX DeFi platform. The platform employs a cold and hot wallet separation management mechanism, with most digital assets stored in offline cold wallets. Combined with multi-signature, real-time risk monitoring, and an intelligent risk control system, it continuously monitors abnormal transactions and potential risks.

Simultaneously, the platform incorporates multiple security measures, including Cloudflare enterprise-grade network protection, the McAfee® security system, and two-factor authentication (2FA), and continuously optimizes network security and infrastructure construction to constantly improve the platform’s stability and digital asset security capabilities.

How to Participate in EX DeFi

The participation process is relatively simple:

2. Deposit Digital Assets: Supports multiple mainstream digital assets including XRP, BTC, ETH, BNB, USDC, SOL, DOGE, LTC, and USDT.

3. Choose a Mining Plan: Select the appropriate mining contract based on the budget. The system will automatically allocate computing power and start operation.

4. Automatic Profit Settlement: The platform operates 24/7, and profits will be automatically settled to the account. Users can choose to withdraw or reinvest to increase their returns.

Examples of popular mining contracts:

BTC (Beginner Trial Contract): Investment of $100, Term: 2 days, Daily Yield: $4, Total Profit: $100 + $8

DOGE (Golden Shell Mini Dogecoin Pro): Investment of $500, Term: 6 days, Daily Yield: $6.5, Total Profit: $500 + $39

BTC (Canaan-Avalon-A1466): Investment of $1000, Term: 10 days, Daily Yield: $13.4, Total Profit: $1000 + $134

LTC (Bitmain Antminer L7): Investment of $5000, Term: 20 days, Daily Yield: $73.5, Total Profit: $5000 + $1470

BTC (Bitmain S19K-Pro): Investment of $10,000, Term: 30 days, Daily Yield: $161, Total Profit: $10,000 + $4,830

For more details on popular mining yield contracts, please visit the EX DeFi official website.

Summary

Ripple’s receipt of MiCA regulatory approval in Europe marks a significant step forward in its global compliance strategy and further enhances market attention to the long-term development of the XRP ecosystem.

As the digital asset industry matures, more and more investors are focusing on digital asset participation methods that combine compliance, security, and convenience. EX DeFi stated that it will continue to improve its platform infrastructure and security system, and provide more stable and efficient cloud mining services to global users by continuously optimizing product experience and operational capabilities.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Washington has spent a year arguing about which agency should regulate a $2.2 trillion market. Nobody checked whether that agency has anyone in the building. It has one person, four empty chairs, and a plan involving artificial intelligence.

Summary

- The CLARITY Act would hand the CFTC primary oversight of spot trading in digital commodities. The commission is designed to hold five seats and currently has one confirmed member, Chairman Michael Selig.

- The agency ran fiscal 2025 with roughly 556 staff against the SEC’s 4,200, and has since lost between 21% and 25% of its workforce. Its enforcement division sits around 108 positions, about 23% below the 140 it had on record in 2025.

- While shrinking, its remit has expanded: crypto market structure, exclusive jurisdiction over prediction markets, perpetual futures rules, DeFi guidance, and a joint initiative with the SEC. Each competes for the same attorneys.

- Selig’s answer is automation. The CFTC plans to use artificial intelligence to review registration applications and assist market surveillance.

- The surprise in the data is that a one-person commission is moving faster, not slower, because there is nobody to dissent. Whether speed without dissent produces durable rules is the actual question.

For a year, the entire American crypto policy debate has been a jurisdictional argument. Should the SEC or the CFTC supervise digital asset markets? The CLARITY Act answers CFTC, and the industry has spent enormous energy and money trying to get that answer written into law. Somewhere in that year, almost nobody stopped to ask a more basic question about the agency on the receiving end of the handoff. The Commodity Futures Trading Commission is designed to hold five commissioners. It currently has one. Four seats sit empty, including both minority-party positions. The body that Congress is preparing to make the primary regulator of a $2.2 trillion market is, at this moment, a single person, a shrinking staff, and a plan to have software pick up the difference.

The arithmetic

Start with the headcount, because it is the least arguable part.

The CFTC ran fiscal 2025 with roughly 556 employees. The SEC runs about 4,200. That gap existed before crypto and made sense when the CFTC supervised agricultural futures and interest rate swaps, which are large markets with a small number of sophisticated participants. It makes considerably less sense as a description of an agency preparing to police spot markets for tokens held by tens of millions of retail buyers.

Since January 2025, under the federal workforce reduction drive, the agency has lost somewhere between 21% and 25% of its people. The enforcement division, the part that actually pursues fraud, sits at roughly 108 positions following a budget request for three new hires, which leaves it about 23% below the 140 enforcement employees it had on record in 2025. So the agency shrank the function most relevant to the mandate it is about to receive.

Then leadership. The commission is statutorily five seats. Selig, confirmed in December 2025, is the only sitting commissioner. This is not new: his predecessor, acting chair Caroline Pham, was also the agency’s sole commissioner during her tenure, which means the CFTC has functioned as a one-person body across two administrations’ worth of leadership. Four vacancies, including both seats reserved for the minority party, on a commission designed for bipartisan balance.

Selig himself is not an accidental appointment. He is a former CFTC official who most recently served as chief counsel to the SEC’s Crypto Task Force, which makes him arguably the best-credentialed person in Washington for the job he holds. That is precisely why the vacancy math is worth taking seriously instead of reading as partisan noise. The problem is not the person in the chair. It is the four chairs with nobody in them.

What keeps getting added to the plate

Now the workload, which has moved in the opposite direction from the headcount.

Crypto market structure. CLARITY would give the CFTC primary oversight of spot trading in digital commodities, meaning Bitcoin, Ether, XRP, Solana, and the rest of the assets named in the March joint taxonomy. That is rulebooks, registration, examinations, supervision, and custody standards for an entirely new market.

Prediction markets. The agency is asserting exclusive federal jurisdiction over a sector that has grown from millions of dollars a year to multiple billions, and it is litigating that claim: the CFTC has sued Illinois, Arizona, and Connecticut over state efforts to regulate sports prediction markets. Selig has confirmed numerous ongoing investigations in the space, with lawmakers pressing him about trades on Polymarket and Kalshi in which small numbers of anonymous accounts appear to have profited on bets tied to US military actions and government announcements, a pattern suggesting possible access to non-public information.

Perpetual futures. The agency is writing rules for a product that generated tens of trillions in annual volume offshore and is now arriving onshore, while simultaneously being sued by the CME over what a perp legally is.

DeFi guidance and Project Crypto, the joint initiative with the SEC that produced the March taxonomy.

At an April House Agriculture Committee oversight hearing, Chairman Glenn Thompson put the contradiction to Selig directly, observing that Congress is putting a lot on your plate with digital assets while also pushing the agency down the prediction markets path, and asked him to request more staff if operations required it. Selig agreed he would.

Thompson and Representative Craig then said they would write to the White House encouraging prompt appointment of commissioners from both parties. That letter is the tell: the committee overseeing the agency is publicly lobbying the executive to staff it.

Selig’s public answer to the resource question is technology. He has said artificial intelligence and automation can compensate for the personnel cuts, and that the agency is pushing to use it for reviewing registration applications and assisting market surveillance. He has also warned that enforcement remains a top priority and that participants should be on notice.

Read that plainly. The agency about to inherit crypto plans to review its registration applications with software because it does not have the people.

The bull case: one voice moves faster

Here is the part that inverts the obvious reading, and it comes from the reporting rather than from the agency’s spin.

A one-person commission is not slower. It is faster. Bloomberg Law’s reporting on the CFTC’s recent output describes an agency accelerating its rulemaking on prediction markets and crypto precisely because there is nobody to argue with. No minority commissioners drafting dissents. No negotiating a majority. No scheduling votes around four other calendars. A chairman who wants a proposal out can put it out.

That speed is visible. The agency has moved on prediction market rulemaking with unusual pace, in part as a deliberate strategy to preempt state claims by putting a federal framework in place quickly. It ran a crypto sprint, updated regulatory language for blockchain-based markets, formally approved spot crypto trading, and co-authored the March taxonomy with the SEC, which Selig has called the most important action taken to date, saying simply that now there is clarity. For an agency supposedly paralyzed by vacancies, the output is substantial.

There is a resource argument on the same side. The Trump administration is seeking more money and a larger headcount for the CFTC, so the staffing hole is at least acknowledged and being addressed through the budget process. And the automation case is not absurd on its face: reviewing registration applications is exactly the kind of structured, document-heavy work where software genuinely helps, and an agency that automates intake can point its scarce attorneys at enforcement instead of paperwork.

The strongest version of the bull case is simply this: the CFTC has, over the past year, produced more usable crypto policy than Congress has, with one commissioner and a quarter fewer staff. Whatever the org chart says, the output is real.

The bear case: fast is not durable

The rebuttal is that speed achieved by removing dissent is not a feature of a regulatory body. It is the absence of one.

Multi-member commissions exist because financial regulation benefits from adversarial internal review. A dissenting commissioner forces the majority to answer the strongest objection before a rule publishes instead of after, in court. Remove the dissent and you do not get better rules faster; you get rules that have never been stress-tested by anyone with the standing to stress-test them. Former CFTC leaders have publicly doubted the agency can juggle crypto and prediction markets simultaneously, and Selig’s Democratic predecessor Rostin Behnam argued routinely that the agency lacked the people to police crypto and prediction markets as they spread.

The durability problem is worse, and it connects directly to the wider argument the industry keeps having. A rule written by a single commissioner is a rule a future five-member commission can revisit with ease and with a ready-made rationale: that it was adopted without the deliberative process the statute contemplates. The industry wants permanence. It is currently getting output from the least permanent possible configuration of a regulator. Selig himself acknowledged the point in a different context, noting that the joint taxonomy does not yet carry the full force of permanent policy.

Then the examination gap, which is where the theory meets the market. Writing a rulebook is the cheap part. Supervising a market means examiners: people who visit registrants, review books, test controls, and catch problems before they become enforcement matters. An enforcement division 23% below its 2025 level is not a division that can absorb spot supervision of every crypto exchange, custodian, and broker seeking dual registration.

Crypto-native exchanges, traditional broker-dealers, asset managers building tokenization platforms, custodians, and futures commission merchants would all queue for the same application reviews at an agency of roughly 550 people. Artificial intelligence does not conduct an examination.

And the prediction market investigations sharpen the point. Selig has confirmed the agency is investigating well-timed trades that lawmakers suspect involved non-public information, in a market that has grown into the billions. Those are exactly the labor-intensive cases that a shrunken enforcement division struggles to bring. Asserting exclusive jurisdiction over a sector is a claim about authority. Policing it is a claim about capacity, and the two have diverged.

There is a historical pattern worth naming here, because the industry has watched it before and drew the wrong lesson. Regulators handed a new market without the resources to supervise it do not simply fail quietly. They fail loudly and late, after something breaks, and the political response is invariably an overcorrection that lands harder than the original rules would have. The agency does not have the examiners to catch problems early, so problems surface as scandals instead of as findings, and scandals produce legislation written in anger. An industry that wants light-touch supervision should be the loudest voice demanding the supervisor be adequately staffed, because the alternative to competent oversight is not an absence of oversight. It is delayed oversight, imposed after a failure, by people who are no longer in a listening mood.

That is the argument the crypto lobby has not made and probably will not, because it sounds like asking for a bigger regulator. It is worth making anyway. The industry spent a year insisting that the CFTC is the right home for digital assets, largely on the theory that the agency is smaller, more pragmatic, and less litigious than the SEC. Every one of those qualities is downstream of the same fact: the CFTC is small. The thing that makes it attractive as a regulator is the thing that makes it questionable as a supervisor of a market this size, and nobody has reconciled the two.

The fight over the empty chairs

The vacancies are not an accident of paperwork. They are a live political dispute with documents on both sides, and it broke into the open this month.

On June 10, twelve Senate Democrats, led by Chris Van Hollen and Raphael Warnock, wrote to the White House complaining about staffing at federal financial regulators including the SEC and CFTC. Their argument was procedural: the administration had broken with the customary practice of consulting Senate Democrats on minority-party nominees to independent agencies, and vacancies weaken agency independence.

On July 9, the White House fired back in a letter to Majority Leader John Thune and Minority Leader Chuck Schumer, signed by Director of Presidential Personnel Dan Scavino and Director of Legislative Affairs James Braid, saying it wanted to set the record straight. The administration said it had already asked Senate Democrats to recommend candidates for the vacant Democratic seats at both agencies and had not received names in response. It argued that Senate Democrats have blocked essentially every civilian nominee, and pointed out that Trump has nominated Democrats to other independent bodies including the National Labor Relations Board and the International Trade Commission. It also invoked the Supreme Court’s decision in Trump v. Slaughter, which expanded presidential removal powers, a citation that does not obviously help the bipartisanship argument.

The history is messier than either letter admits. The administration withdrew Brian Quintenz’s nomination for the CFTC chairmanship in September 2025 before nominating Selig in October, a sequence documented in the White House’s own list of nominations and withdrawals. So the seat that is filled took two attempts, and the four that are empty have generated a blame exchange instead of names.

The SEC is in comparable shape and receives a fraction of the attention. It has two vacant Democratic seats against three Republican commissioners, and Hester Peirce, one of the three, is expected to leave by November. Which produces the fact that ought to be the headline of the entire CLARITY debate: both of the agencies that would divide American crypto oversight are short-staffed at the commissioner level, and one of them is a single person.

The provision nobody is reading

There is a clause in the bill that turns all of this from a governance complaint into a market-structure problem, and it is Section 106.

CLARITY does not simply hand the CFTC authority and walk away. It contemplates a window in which the agency must finalize rulebooks, hire examiners, build supervision teams, and stand up a digital asset custody framework. If the CFTC cannot do those things inside that window, the industry operates under provisional status.

Sit with what that means. The bill the industry has spent a year fighting for, on the theory that regulatory certainty is the prize, contains a fallback in which firms operate provisionally because the regulator could not staff up in time. Provisional status is not certainty. It is uncertainty with a statutory basis, which may be marginally better than the status quo and is nothing like what the lobbying promised.

That is the risk almost nobody in the vote-counting coverage has priced. The failure mode of CLARITY is not only that it dies in the Senate. It is that it passes, hands a $2.2 trillion market to a one-person commission with 550 employees and a quarter of its enforcement staff gone, and the handoff does not work on schedule. The bill can pass and still not deliver certainty for years.

What to watch

Three things.

Whether any commissioner gets nominated before the recess. The House Agriculture leadership is already writing to the White House about it, and both parties say the agencies should have full benches before major crypto rules advance. If CLARITY reaches a floor vote while the CFTC still has one commissioner, that fact becomes an argument for opponents and a genuine operational problem for supporters.