Crypto World

Why Nexo Is Reentering the US After the 2023 Crypto Lending Crackdown

Key takeaways

-

After paying a $45-million settlement in 2023 and exiting the market, Nexo has reentered the US with a redesigned product model focused on regulatory alignment rather than direct yield issuance.

-

The 2023 crackdown centered on unregistered securities concerns. The SEC alleged that Nexo’s Earn Interest Product functioned as an unregistered security, raising questions about retail yield marketing, transparency, custody practices and counterparty risk.

-

The new model relies on licensed US partners. Instead of directly offering yield products, Nexo now operates through regulated US intermediaries, including licensed entities and, where required, SEC-registered investment advisers.

-

The Bakkt partnership anchors the compliance strategy. By collaborating with Bakkt, a publicly traded US crypto firm with regulatory licenses, Nexo shifts from a direct issuer model to a partner-delivered framework embedded within regulated infrastructure.

Three years after departing the US and paying a $45-million settlement to federal and state regulators, Nexo has formally reentered the US market. But this is not a straightforward relaunch. Rather, it is a structural overhaul.

What changed is not merely the timing or the political climate; it is how the product is designed, delivered and regulated.

This article examines why Nexo exited in 2023, what regulators objected to and how its 2026 return is structured differently. It also explores what US users should watch before engaging with crypto-backed loans or yield-style products.

The 2023 crackdown: Why Nexo left the US

Nexo, co-founded by former Bulgarian lawmaker Antoni Trenchev, developed much of its initial US footprint through its Earn Interest Product (EIP), which enabled users to deposit crypto and earn yield.

In January 2023, the US Securities and Exchange Commission (SEC) accused Nexo of offering and selling unregistered securities through this product. The SEC contended that the EIP met the legal definition of a security and, therefore, required proper registration.

Nexo consented to a settlement:

-

It paid a total of $45 million in fines to the SEC and various state regulators.

-

It neither admitted nor denied the allegations.

-

It ceased offering the product to US investors.

Soon after, Nexo withdrew from the US retail market.

Why regulators targeted “earn” products

The enforcement action stemmed from a wider post-2022 crypto lending fallout. Major failures across the lending industry had revealed liquidity mismatches, rehypothecation risks and retail exposure to opaque yield structures.

Regulators were particularly concerned about:

-

The promotion of yield products to retail investors

-

Transparency regarding how returns were generated

-

Custody practices and credit counterparty risks

-

Whether these offerings functioned as investment contracts.

The crackdown extended beyond Nexo and signaled a broader regulatory overhaul for centralized crypto yield offerings.

Did you know? Borrowing against volatile assets is not a new concept. Traditional stock margin lending has existed for decades, but crypto’s 24/7 trading makes liquidation mechanics far more dynamic and automated.

What changed in 2026

Nexo’s 2026 comeback rests on a core claim: The product is now structured differently and provided through licensed US partners.

Instead of directly delivering yield-like products to US investors under its former approach, Nexo states that its updated structure:

-

Relies on properly licensed US partners

-

Incorporates an SEC-registered investment adviser when required

-

Has phased out the product addressed in the 2023 order.

This difference is significant: Rather than operating as an independent provider of an earn program, Nexo is now positioned within a regulated infrastructure framework.

According to Nexo, it will offer crypto-backed loans and yield-generating products. These services will be provided through licensed US partners.

Crypto-backed loans differ from the unsecured lending models that failed in 2022. Users deposit digital assets as collateral and borrow against them. Liquidation occurs if the collateral falls below set loan-to-value thresholds.

The Bakkt partnership: Compliance by design

A key factor in the relaunch is Nexo’s collaboration with Bakkt, a publicly traded US crypto firm.

Bakkt provides regulated trading infrastructure and holds multiple US licenses. By channeling US operations through regulated entities, Nexo is effectively moving from a direct issuer model to a partner-delivered model.

In practical terms, this means:

-

Trading, custody or advisory services could reside with regulated entities.

-

Product elements may be distributed across licensed intermediaries.

-

Supervision may occur across multiple regulatory layers.

This framework is designed to address the regulatory objections that led to the 2023 settlement.

Did you know? Unlike banks, most crypto lending platforms do not benefit from federal deposit insurance, meaning customer protections depend heavily on custody structures and legal agreements rather than government backstops.

A shifting regulatory landscape

Timing is a factor in Nexo’s return to the US. Under President Donald Trump’s administration, the SEC has terminated or scaled back multiple crypto enforcement actions. The enforcement environment has shifted from an intense crackdown to a period of readjustment.

For instance, the SEC moved to drop a lawsuit involving the Gemini Earn program following investor recoveries. This does not indicate that crypto lending issues are entirely resolved, but it points to a more adaptable regulatory stance than in early 2023.

Nevertheless, the US regulatory framework remains fragmented. Federal agencies, state securities regulators, money transmitter statutes and consumer lending rules may all apply depending on the structure.

What US users need to watch

Even if products are offered through regulated intermediaries, users should assess:

-

Who is your legal counterparty? Is the agreement with Nexo, with a US-licensed entity or with multiple entities?

-

Where does custody sit? Are assets held by a qualified custodian? Under which regulatory regime?

-

How are returns generated? Are yields derived from lending, staking, market-making or other activities?

-

What are the liquidation terms for crypto-backed loans?

What is the loan-to-value (LTV) threshold?

How quickly can liquidation occur?

Are there additional fees?

-

What disclosures exist? Look for:

Risk disclosures

Rehypothecation clauses

Conflict-of-interest statements

Jurisdiction clauses.

“Compliant structure” does not equal “risk-free product.”

Did you know? Money transmitter licensing in the US is state-based, which means a crypto company may need approvals in dozens of jurisdictions. This is one reason partner-led models are gaining popularity.

Why this comeback matters for the industry

Nexo’s return could indicate a wider transformation in US crypto lending:

-

Phase 1 (Pre-2023): Direct-to-consumer yield models with minimal registration

-

Phase 2 (2023-2025): Regulatory enforcement, withdrawals and reorganization

-

Phase 3 (2026 onward): Partner-led models employing licensed intermediaries and segregated functions.

If this framework proves viable, other international crypto companies may reenter the US through comparable compliance layers instead of direct issuance models.

The real shift: It is about the wrapper, not just the product

The primary takeaway from Nexo’s return is structural.

The fundamental economic idea of generating yield on digital assets or borrowing against crypto remains intact. What has evolved is the regulatory framework surrounding it.

Rather than pushing the limits of securities law, the updated model integrates into licensed infrastructure.

Whether this method satisfies regulators over the long term will hinge on:

-

Disclosure quality

-

Risk management practices

-

Transparency of revenue sources

-

Ongoing federal and state coordination.

For now, Nexo’s comeback reflects a more prudent crypto industry that recognizes that in the US, structure dictates survival.

Cointelegraph maintains full editorial independence. The selection, commissioning and publication of Features and Magazine content are not influenced by advertisers, partners or commercial relationships.

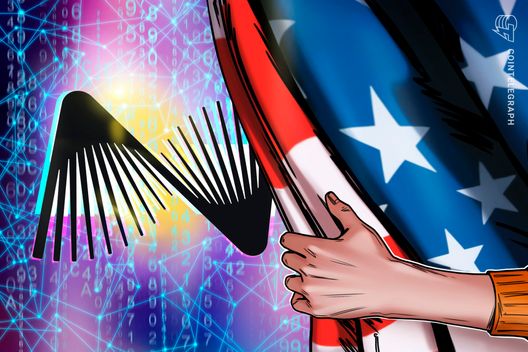

Michael Saylor’s Strategy, the world’s largest public holder of Bitcoin (BTC), bought another 1,031 Bitcoin last week in a much smaller purchase than its previous two weekly buys, funding the acquisition with sales of Class A common stock.

Strategy acquired 1,031 Bitcoin for $76.6 million last week, according to an 8-K filing with the US Securities and Exchange Commission on Monday.

The purchases were made at an average price of $74,326 per coin, below the company’s overall average acquisition price of $75,694. Bitcoin averaged around $70,871 for the week of March 16-22, based on daily closing prices.

The new acquisitions bring Strategy’s holdings to 762,099 BTC, acquired for a total cost of roughly $57.69 billion, the company said.

Common stock funded the latest buy

Strategy’s relatively modest purchase follows larger Bitcoin acquisitions recently, including a 22,337 BTC buy reported last Monday and a 17,994 BTC buy a week earlier.

The 22,337 BTC ($1.6 billion) purchase ranks among Strategy’s largest on record and was largely funded through sales of its perpetual preferred equity, Stretch (STRC). The stock generated approximately $1.2 billion, accounting for about 75% of the total purchase.

Related: Strategy records biggest STRC issuance day with estimated 1,420 BTC buy

Unlike the prior week’s funding mix, the latest purchase appears to have been funded through sales of Strategy’s Class A common stock rather than preferred equity.

Strategy has bought 41,362 Bitcoin for around $2.93 billion in March. With Bitcoin trading at $70,430 at the time of writing, the company is down around 7% on its BTC holdings, now worth around $54 billion, according to data from CoinGecko.

Related: Strategy halts Bitcoin buying via STRC: Will BTC price dip again?

Strategy’s holdings are roughly 3% below the Bitcoin holdings of BlackRock’s iShares Bitcoin Trust ETF (IBIT), which held about 785,300 BTC on behalf of its clients after the close of trading on Friday.

US spot Bitcoin ETFs collectively held nearly 1.3 million BTC as of March 20, representing roughly 6.1% of the 21 million maximum Bitcoin supply, according to data from WalletPilot.

Magazine: Metaplanet’s Japan Bitcoin bet, Bithumb ordered suspension: Asia Express

Arkham data shows a wallet cluster holding 644 million SIREN, about 88% of the 728 million circulating supply, raising manipulation concerns.

Crypto token Siren surged 340% in the last week, amid claims that a large portion of the circulating supply may be concentrated among a small group of wallets.

Siren markets itself as the “first AI analyst agent deployed on BNB Chain.” At the time of writing, CoinGecko data shows SIREN trading at $2.81, up over 340% from $0.63 on March 16. In the past month, the token exploded by nearly 1,300% from $0.22. The rally drew scrutiny after analysts said a large share of the token’s supply may be concentrated in a small group of wallets, a dynamic that could amplify volatility if confirmed.

Citing an unverified custom entity created by Arkham Intelligence, onchain analyst EmberCN said the party cornered nearly all spot supply to profit off contracts. He said this was the secret behind the token’s surge in the past month.

According to the Arkham Intelligence page, the entity holds 644 million SIREN (worth around $1.8 billion). The amount accounts for 88% of the entire circulating supply of 728 million tokens.

Crypto analysts point to wallet clustering

On X, pseudonymous crypto analyst Mlmabc warned his followers on Sunday to be careful trading the token, adding that “supply is heavily cornered.” Mlmabc said a cluster of wallets is currently sitting on $950 million in unrealized profit, implying that it could dump the tokens on potential buyers.

Citing his own Dune Analytics dashboard, Bitcoin Strategy analyst Gerhard Kuschnik said most of the Siren token trading activity over the last month, when SIREN surged, was not from new users. Kuschnik said these were trading activities by existing holders, arguing that the token is not gaining new interest.

Related: ‘Hawk Tuah’ girl Haliey Welch says memecoin implosion ‘traumatized’ her

“The vast majority of trading happens by returning users,” adding that the average new user that bought into the token during its surge averaged between 100 and 200.

Magazine: Sex robots, agent contracts a hitman, artificial vaginas: AI Eye goes wild

Key takeaways

-

This $3.4 million scam shows how modern crypto fraud increasingly relies on social engineering rather than technical exploits.

-

Scammers used a gradual grooming process, engaging victims in friendly conversations over time to build emotional trust before introducing any financial discussion. It closely resembled the pig-butchering model.

-

The investment pitch combined Ether’s growth potential with the perceived stability of gold. This created a compelling but fraudulent narrative that convinced victims they were gaining access to an exclusive, low-risk opportunity.

-

Victims were told to buy Ether themselves on legitimate platforms and transfer it to provided wallets. This gave them a false sense of control and legitimacy.

This scam did not begin with a phishing link or hacked wallet. It started with a simple message: “Sorry, wrong number.”

According to US prosecutors, the interaction evolved into a social engineering scheme that defrauded victims of millions and led to the seizure of $3.4 million in USDt (USDT).

From innocent messages to multimillion-dollar fraud

Federal prosecutors in Boston have initiated a civil forfeiture proceeding to recover approximately $3.44 million in USDt linked to a suspected online investment fraud.

According to authorities, the funds were seized in early 2025 as part of an investigation launched in late 2024 after complaints from victims in multiple US states who reported significant financial losses.

The operation did not involve sophisticated technical exploits. Instead, it relied on a well-known yet remarkably effective tactic: social engineering. Fraudsters used ordinary, everyday interactions to deceive unsuspecting victims.

Victims received texts or chat messages that appeared to have been sent by mistake. Fraudsters used apps like WhatsApp and Telegram to send these messages.

On the surface, the communication appeared completely ordinary. There was no pressure, no immediate request and no clear warning signs.

This lack of an obvious threat is one reason the method can be so effective.

Unlike crypto scams that trigger immediate suspicion, the “wrong number” approach:

-

Appears natural and socially appropriate

-

Encourages polite replies

-

Creates an opportunity for ongoing dialogue

In this case, as in similar ones, what begins as an apparent mistake soon evolves into an opening for further contact.

The grooming stage: Gradually establishing trust

Following the initial exchange, scammers avoid rushing the process. They cultivate trust gradually through friendly conversations, the sharing of seemingly personal information and the maintenance of a consistent, reliable persona.

Rather than introducing financial topics too early, the scammers:

-

Create a sense of emotional ease

-

Make regular communication feel normal

-

Foster the appearance of a genuine personal connection

This strategy aligns with a broader category of fraud commonly known as pig-butchering, in which victims are methodically “groomed” before being targeted for financial gain.

By the time money becomes part of the discussion, victims often believe they are interacting with someone familiar rather than an unknown fraudster.

Did you know? The “wrong number” scam technique evolved from earlier email scams in which fraudsters pretended to contact the wrong person. Messaging apps have made this tactic more effective by enabling real-time, casual conversations that feel more authentic.

The pitch: A fake Ether investment tied to gold

After building initial trust, scammers subtly shifted the discussion toward lucrative investment opportunities. Victims were presented with what appeared to be a privileged Ether (ETH) investment opportunity, supposedly tied to tangible gold holdings.

This pairing appears to have been deliberate.

It merged:

Together, these elements created an attractive narrative: the promise of substantial returns while minimizing perceived risk.

Victims were told they were being given access to a rare, exclusive opportunity that was not available to the general public.

The transaction method: Why victims purchased Ether

Instead of requesting direct transfers, the fraudsters instructed victims to:

-

Buy Ether through established, legitimate exchanges

-

Send the purchased Ether to designated wallet addresses

This approach had a significant psychological impact.

Victims felt reassured because they:

-

Conducted transactions on genuine, well-known platforms

-

Personally handled and authorized the purchase

-

Could observe and verify the funds in their own wallets before the transfer

As a result, the process never felt like directly giving money to fraudsters. Instead, it appeared to be genuine participation in a legitimate investment opportunity.

Did you know? In many fraud cases, scammers appear to operate in organized groups using scripted playbooks. Some teams specialize only in the “conversation phase,” while others handle crypto transactions, showing how modern fraud has become structured like a business operation.

What occurred after the Ether transfer

After victims sent their Ether to fraudsters:

-

The funds were routed through various intermediary wallet addresses

-

They were then converted into USDt, a stablecoin pegged to the US dollar

-

Finally, the stablecoins were transferred to unhosted wallets controlled by the perpetrators

This sequence was designed to:

-

Conceal the transaction path

-

Disconnect the funds from their original source

-

Significantly complicate efforts to recover them

Nevertheless, blockchain records, combined with investigative tools, helped authorities trace the money trail. The process ultimately resulted in the seizure of assets.

Part of a larger fraud pattern

This prosecution fits into a broader wave of cryptocurrency-related fraud cases. Authorities across the US have taken action against pig-butchering frauds and romance scams. They have also launched crackdowns on laundering operations involving stablecoins.

Across these incidents, common traits appear:

-

Initial outreach through social media, dating apps or informal platforms

-

A slow, deliberate process of cultivating trust

-

A pivot toward cryptocurrency “investment” opportunities

-

Fund transfers through layered transactions

While the specific methods and technologies may vary, the intent and strategy remain consistent.

Did you know? Crypto scams often use multiple blockchains to move funds, not just one. After converting assets into stablecoins, scammers may bridge them across networks to make tracking and recovery efforts even more difficult.

Why this scam proved effective

The core reason these schemes succeed is that they are rooted in psychology rather than in any technological flaw.

The perpetrators did not exploit vulnerabilities in the system itself. Instead, they targeted and manipulated predictable patterns of human behavior.

Several critical psychological elements contributed:

-

Politeness bias: Individuals tend to reply politely even to messages that appear accidental.

-

Trust formation: Consistent, repeated contact creates a growing sense of familiarity and comfort.

-

Perceived control: Victims personally handled the purchase and transfer of funds.

-

Credibility: Linking the high-growth promise of cryptocurrency with the time-tested stability of gold gave the proposal greater believability.

By the time the fraud unraveled, the victim had already become deeply committed both emotionally and financially.

The legal response: Moving from seizure to permanent forfeiture

The US government initiated a civil forfeiture proceeding to recover the seized assets.

Through this legal mechanism, authorities are able to:

-

Assert ownership over property suspected of being linked to criminal conduct

-

Obtain judicial authorization for the permanent forfeiture of those assets

-

Allow victims or other third parties an opportunity to file legitimate claims to the property

Unlike criminal prosecutions, civil forfeiture proceedings focus on the assets themselves and do not necessarily require a criminal conviction to move forward.

Warning signs to recognize

Scams of this nature tend to follow well-established patterns. Important red flags to watch for include:

-

Unsolicited messages claiming to have been sent in error

-

The rapid development of rapport and trust by previously unknown individuals

-

Discussions that gradually shift toward investment suggestions

-

Promises of exclusive access or guaranteed high returns in cryptocurrency

-

Instructions to send funds or cryptocurrency to external wallet addresses

Any investment proposal that arises from a random conversation should be approached with the highest level of skepticism.

What to do if you receive similar messages

If you receive an unsolicited message about a lucrative crypto investment, you should:

-

Refrain from responding to or engaging with unfamiliar contacts

-

Resist the urge to continue the conversation simply to be polite

-

Never transfer money or cryptocurrency to wallet addresses provided by strangers

-

Immediately block and report suspicious phone numbers, accounts or profiles

-

Promptly notify law enforcement and the relevant platforms or exchanges if any funds have already been sent

Prompt action can sometimes improve the chances of authorities tracing the funds or freezing them.

Cointelegraph maintains full editorial independence. The selection, commissioning and publication of Features and Magazine content are not influenced by advertisers, partners or commercial relationships.

One of Switzerland’s most prominent banking dynasties has officially fractured. Marc Syz has walked away from his family’s CHF 24 billion legacy at Banque Syz to bet the firm’s future on a Bitcoin treasury strategy that his father rejected.

The split centers on Future Holdings AG, a corporate treasury vehicle holding 5,000 BTC. Marc Syz and partner Richard Byworth pushed to integrate the $450 million position directly into the bank’s alternative asset arm.

Eric Syz refused.

Now Marc is taking the unit public independently. The move exposes a deep fault line in Swiss wealth management between capital preservation and digital asset adoption. The window for compromise has closed.

- The Asset: Future Holdings AG holds over 5,000 BTC in its corporate treasury, valued at approximately $450 million as of March 2026.

- The Event: Marc Syz has filed regulatory papers for a dual listing on Nasdaq and SIX Swiss Exchange to raise CHF 500 million later this year.

- The Friction: While 28% of private banks plan crypto allocations by 2027, CRD VI compliance deadlines are forcing institutions to choose between integration and exclusion.

The Mechanics of the Syz Separation Explained

This is not a simple resignation. It is a fundamental divergence on how value is stored. Marc Syz previously led Syz Capital, managing CHF 1.2 billion in alternative assets. His proposal was to absorb Future Holdings AG and its Bitcoin stack directly into the bank’s offering.

The structure was modeled explicitly on MicroStrategy. With 5,000 BTC on the balance sheet, the entity acts as a high-beta proxy for Bitcoin price action. Richard Byworth, a former HSBC and Ripple executive, joined as co-founder to build the infrastructure.

Banque Syz leadership balked at the volatility. The bank, founded in 1995, prioritizes the stability required by its private banking clientele.

While major US institutions like Morgan Stanley advance Bitcoin ETF applications to capture fee revenue, holding physical Bitcoin on a family bank’s balance sheet remains a bridge too far for the older guard.

Marc responded by filing for an IPO. Regulatory filings submitted to FINMA on March 15 confirm the plan for a dual listing on Nasdaq and the SIX Swiss Exchange. The goal is to raise CHF 500 million to expand the treasury further. The split is now administrative reality.

Can Old Money Survive the Bitcoin Transition?

The Syz family split is bigger than a boardroom disagreement.

Swiss wealth managers are staring down a relevance crisis. PwC data shows 28% plan to allocate 5-10% to crypto by 2027. Execution is stalling because of exactly this kind of internal governance clash.

Marc Syz is taking the corporate treasury route. 5,000 BTC in custody. Future Holdings heading for a public listing. The thesis is straightforward: Bitcoin is the only real hedge against monetary debasement available to family offices.

At completion, this deal sees @H100Group become the #1 BTCTC in Europe. — Richard Byworth ∞/21M (@RichardByworth) March 23, 2026

Then Switzerland

Then tackling the 800bln bond market with zero yield

Just like Bitcoin: tick tock next block

Quiet continuous execution with @Sanderandersenn, @Wiik_Johannes, @HUGESKY852, @SYZCAP  https://t.co/1xq5PKOXAv

https://t.co/1xq5PKOXAv

Eric Syz and the main Banque Syz branch are not following. They are sticking to traditional digitization, modernizing without putting the balance sheet anywhere near crypto volatility.

The market is moving faster than both of them.

By taking Future Holdings public, Marc Syz is not just making a bet. He is forcing the market to price his vision against his father’s. The prospectus is with FINMA. The split is official.

The dynasty is no longer hedging. It is dividing.

Discover: The best new crypto in the world

The post Switzerland Private Banking Dynasty Is Tearing Itself Apart Over Crypto appeared first on Cryptonews.

Bitcoin moved back above $71,000 after US President Donald Trump postponed Iran strike for five days, sending oil price crashing below $100.

Bitcoin (BTC) broke back toward $71,000 during Monday’s European trading session as US President Donald Trump said attacks on Iran’s power infrastructure would be postponed.

Key takeaways:

-

Bitcoin bounces 5% to $71,000 after President Trump said US attacks on Iran’s infrastructure would be postponed.

-

$270 million in short positions were liquidated in an hour.

-

Focus now shifts to $72,000–$75,000 liquidity zones to see if BTC price will rise further to grab these.

Bitcoin erases weekend losses with 5% rebound

Data from TradingView showed BTC price rose as much as 4.7% within 60 minutes to an intraday high of $71,500, recouping all the losses made over the last three days. The last time BTC/USD traded above $71,000 was on March 19.

The price reacted to President Trump’s announcement of a five-day pause on planned US military strikes against Iranian power plants and energy infrastructure after “very good and productive” discussions with Tehran.

“And this shall henceforth be known as the ‘TACO PUMP,’” Coinbureau CEO Nic Puckrin said in response to Bitcoin’s reaction following the news.

The move in Bitcoin was accompanied by $270 million in short liquidations within an hour, with BTC short liquidations accounting for $120 million.

This brought the total liquidations across the crypto market over the last 24 hours to $781 million.

Gold erased almost all its earlier losses, now down just 1% on the day and rebounding to $4,440 per ounce, while the dollar index (DXY) has slipped to 99.3.

Related: Gold bear market and sub-$50K BTC: Five things to know in Bitcoin this week

Oil, a key macro risk factor, dropped as much as 16% to $92 from an intraday high of $110, while WTI crude dropped below $85 — the steepest single-day decline since late 2025.

However, Iranian officials quickly denied the reports of substantive productive talks, insisting no meaningful concessions had been made and reiterating demands for a complete halt to US and Israeli actions before any broader resolution.

Bitcoin price fills CME gap at $70,000

Bitcoin started the week with a significant CME gap around $70,000. This gap has now been filled with the latest price rise. Traders will now focus on the next one near the $80,000 region.

Meanwhile, the liquidation heatmap showed BTC price eating away ask orders below $72,000. A close above this level would push the BTC/USD pair toward $75,000, where the next major liquidity cluster sits.

On the downside, “the $64K-$65K region is interesting,” analyst Daan Crypto Trades said, adding:

“Currently there’s a lot of fear for the latter which is why most markets have been selling off a lot the past few trading days.“

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

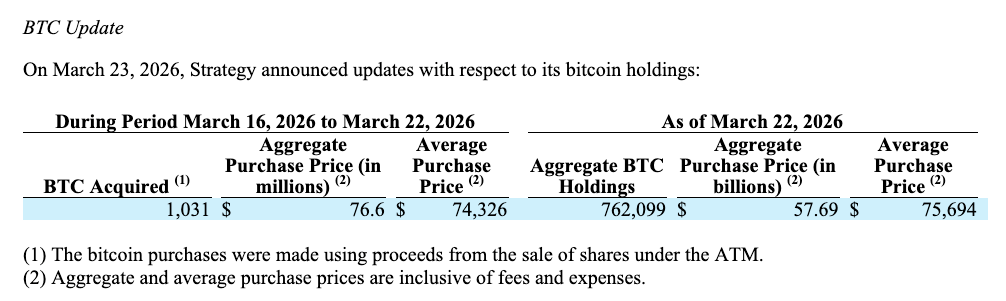

Crypto investment products maintained their inflow streak last week but momentum slowed amid ongoing Middle East tensions and a “hawkish pause” interpretation of the US Fed’s meeting.

Crypto exchange-traded products (ETPs) recorded $230 million in inflows last week, with $405 million in outflows following the Federal Open Market Committee (FOMC) meeting in the US, CoinShares reported Monday.

The inflows extended the streak to four consecutive weeks, but the latest total was sharply lower than the previous week’s $1.06 billion.

CoinShares head of research James Butterfill largely attributed the slowdown to the market’s “hawkish pause” interpretation of the US Federal Reserve’s Wednesday meeting, rather than broader geopolitical tensions.

“The intra-week data supports this,” Butterfill said, referring to strong inflows in the first two days of the week before reversing sharply in the wake of the FOMC meeting.

Bitcoin funds lead inflows, while Ether reverses

Bitcoin (BTC) accounted for nearly all of last week’s crypto ETP inflows, posting $219.2 million in gains. Ether (ETH) funds saw $27.5 million in outflows, ending a three-week inflow streak.

Solana (SOL) saw $17 million in inflows for the seventh straight week, bringing the total to $136 million and making it one of the most popular ETP assets in recent months.

Additionally, notable gains came from Chainlink (LINK) and Hyperliquid (HYPE), with inflows netting $4.6 million and $4.5 million, respectively.

Related: NYSE exchanges scrap crypto options cap on 11 Bitcoin, Ether ETFs

Crypto ETPs have clocked $1.4 billion of inflows year-to-date, with Bitcoin ETPs leading at $1.2 billion. Total assets under management stand at $138 billion, according to CoinShares.

US spot Bitcoin ETFs account for 43% of gains

About half of Bitcoin ETP inflows were driven by the US spot Bitcoin exchange-traded funds (ETFs) last week, which ended the week with $95.2 million in inflows.

The inflows marked four consecutive weeks of gains totaling $2.2 billion, according to SoSoValue data. Despite the gains, spot Bitcoin ETFs remain underwater year-to-date, with roughly $400 million in outflows.

Similar to broader investment products, US spot Ether ETFs failed to maintain the inflow streak after three weeks of inflows, with last week’s outflows totaling around $60 million.

The US spot Ether ETFs have seen $599 million in outflows year-to-date, while broader ETPs were roughly $50 million underwater.

Magazine: Google flags crypto malware, retiree loses $840K in ‘expert’ scam: Hodler’s Digest, Mar. 15 – 21

XRP is trading at the $1.40 price level, down just 1% over 24 hours, as the prediction says crypto markets will pull back further despite new U.S. regulatory clarity classifying the token as a digital commodity.

The classification, confirmed by the SEC and CFTC, handed bulls a headline victory, but the rally fizzled fast. We hit a wall of macro aggression: a hawkish Federal Reserve stalling rate cuts and a geopolitical oil spike to above $100 per barrel, before dropping this hour to under $90.

The $1.40 level, once a floor, has turned into a ceiling and a battleground for the week ahead.

XRP Price Prediction: Will Ripple Reclaim $1.50 Amid Macro Headwinds?

The technical landscape for Ripple’s native token is precarious. While the asset benefits from established support following the May 2025 SEC settlement, the failure to hold above $1.45 suggests buyer exhaustion. Trading volumes have thinned as capital rotates into commodities; oil prices above $112 act as a liquidity sponge, soaking up risk capital.

If bulls cannot reclaim $1.45 within 48 hours, the next logical support sits significantly lower. Conversely, a clean break above $1.45, fueled perhaps by institutional flows into spot ETFs, could target $1.55.

On-chain data signals XRP may be near a bottom, but the macro environment demands caution. With rates stuck at 3.50%-3.75%, the cost of capital remains high, dampening the leverage needed for a sustained breakout.

BREAKING: — Watcher.Guru (@WatcherGuru) March 18, 2026

Federal Reserve leaves interest rates unchanged, remains at 3.50% – 3.75%.

Federal Reserve leaves interest rates unchanged, remains at 3.50% – 3.75%.

Traders should watch the $1.30 support level closely. A breakdown here validates the pressure seen since the start of 2026, potentially exposing the asset to a deeper flush toward $1.30. Is the market pricing in a delay to altcoin season? The data points to a temporary risk-off sentiment.

Maxi Doge Targets Early Mover Upside as XRP Tests Key Levels

While major cap assets like XRP wrestle with interest rate realities and oil shocks, a subset of traders is rotating into high-velocity presales unaffected by Brent crude charts. Capital is seeking volatility in new narratives. Enter Maxi Doge ($MAXI), a new entrant aggressively targeting the “degen” trading subculture with a distinct leverage-king aesthetic.

The project has raised more than $4,6 million thus far, priced at $0.000281 per token and a staking reward bonus of 66%. Unlike standard meme tokens that rely solely on cute imagery, Maxi Doge integrates holder-only trading competitions and a “Maxi Fund” treasury designed for liquidity injections. It appeals to the high-risk demographic with the tagline “Never skip leg-day, never skip a pump.”

Meme coin liquidity is thinning elsewhere, yet $MAXI continues to attract inflows due to its specific market fit: a 240-lb canine juggernaut embodying a 1000x leverage trading mentality. For traders exhausted by XRP’s slow grind against the $1.40 resistance, this presale offers a high-variance alternative built for the current volatility. However, early-stage tokens carry inherent risks; dynamic APY staking provides an incentive for holding, but market timing remains critical.

The post XRP Price Prediction: SEC Clarity Meets Fed and Oil Shock as We Watch 1.40 appeared first on Cryptonews.

Crypto fear index slumps as investors dump XRP, SOL and AAVE, rotate into cash and stables, and test whether extreme fear sets up the next recovery leg.

Summary

- Crypto Fear & Greed Index falls to 8, locking in one of the deepest “extreme fear” readings of this cycle as traders dump risk across majors like XRP, SOL and DeFi plays such as AAVE.

- Total crypto market cap holds around $2.36 trillion even as investors aggressively de‑risk and rotate out of high‑beta altcoins into cash and stablecoins.

- Analysts warn that “extreme fear grips the market,” but note that structurally, such levels have historically preceded major recovery phases in both Bitcoin and large altcoins.

Crypto investors woke up to a sharply darker mood as the Crypto Fear & Greed Index fell to 32, cementing the market’s return to “extreme fear” territory after weeks of mounting macro and geopolitical pressure. The single‑digit reading underscores how quickly sentiment has flipped from cautious optimism to outright risk aversion, even though the total cryptocurrency market capitalization still hovers near $2.36 trillion.

According to data provider Alternative.me, a score of 8 sits at the bottom of the index’s 0–100 range and signals that “investors are extremely worried” about near‑term downside. A flash note from CoinEx described the latest move bluntly: “Crypto Fear & Greed Index drops to 8, extreme fear grips the market,” highlighting that selling has been broad‑based across spot and derivatives venues, with names like XRP and SOL now firmly in correction territory.

Despite the collapse in sentiment, several trackers show aggregate market cap holding or even rising slightly, with some estimates pointing to roughly $2.36 trillion in total crypto value after a modest 2–3% 24‑hour gain. As one March market recap put it, “the total cryptocurrency market capitalization has actually increased by about +2.87% in the last 24 hours, reaching approximately $2.36 trillion,” suggesting that fear and flows are no longer perfectly aligned.

Within that headline number, however, rotation has been brutal under the surface. Large‑cap altcoins such as XRP (XRP) and SOL (SOL) have seen outsized intraday swings as traders shed beta, while DeFi bellwether AAVE (AAVE) has become a high‑conviction short for some funds concerned about leverage and protocol risk. Milk Road’s composite sentiment gauge echoes that bifurcation: the market has spent roughly 62% of the past eight years in “fear” or “extreme fear,” yet major assets have still trended structurally higher over that period. “The boilerplate interpretation,” the site notes, is simple – “be greedy when others are fearful, and be fearful when others are greedy.”

The latest plunge to 8 extends what some analysts describe as one of the longest “fear streaks” since at least 2019, with social metrics now matching the kind of stress last seen during mid‑2022 liquidations. In an early‑March note titled “The Heartbeat of the Crypto Market,” one strategist wrote that escalating conflict and the effective closure of key oil chokepoints have pushed investors into “capital preservation mode,” driving the index down from 22 to low‑teens readings in a matter of days.

For traders, the key question is whether this 8 print marks a capitulation low or just another step down in a longer deleveraging cycle that continues to pressure altcoins and DeFi names like AAVE. While history offers no guarantees, previous extreme fear clusters have often coincided with discounted entry points for long‑term capital — a dynamic that some institutional desks are already watching closely as they weigh when to step back into XRP, SOL and the broader market.

Crypto World

Stablecoin yield in crypto Clarity Act won’t allow rewards on balances, latest text says

Crypto industry insiders got their first look at the revised market structure bill in the Senate, and the opening impression was that the language on allowable stablecoin yield was overly narrow and unclear, according to a person familiar with the current draft.

The new language, which was announced Friday by Senators Angela Alsobrooks and Thom Tillis, would ban yield payments for simply holding a stablecoin. It would also restrict any approach that makes the program in any way equivalent to a bank deposit, and it applies further limits to other potentially allowed activities, the person said, adding that the mechanics of determining activities-based stablecoin rewards is left uncertain.

The crypto industry got this first look at the revised section of the Digital Asset Market Clarity Act on Monday in a closed-door review on Capitol Hill in Washington, representing an attempt to clear a roadblock in the effort to get a hearing in the Senate Banking Committee. Bankers had insisted that stablecoin rewards look nothing like interest-bearing bank deposits, because they argued the competing product could hamstring the industry and strangle lending. So, the compromise will allow rewards programs on users’ stablecoin activities but not balances.

A similar version of the Clarity Act passed in the House of Representatives last year, and another version cleared a markup hearing in the Senate Agriculture Committee. The banking panel represents a big step that would get the legislation to a place where lawmakers could prepare a final, combined version that would get a vote of the overall Senate.

The stablecoin yield lobbying fight between the crypto sector and the banking industry had stifled progress on the legislation for a while. But it’s not the only sticking point. The industry will still need to see the final approach to oversight of the decentralized finance (DeFi) space, which had remained an area of concern for Democrats who had wanted to ensure illicit finance protections. And the Democrats have also insisted on a need for a ban on senior government officials profiting personally from the crypto industry — a provision aimed squarely at President Donald Trump.

Though the industry recorded a tremendous win last year when the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act became the first major U.S. law to govern a segment of the crypto industry, it was meant as the less important first step of a one-two policy approach that concludes with the Clarity Act.

That full-fledged arrival of crypto into the U.S. financial system will eliminate regulatory uncertainty for any investors who have been hesitant about involvement in the sector. Digital assets insiders believe it will open flood gates among institutional investors and developers who want to build atop the technology.

TLDR

- Aave DAO approved the Request for Comment proposal to begin discussions on deploying Aave V4 on Ethereum mainnet.

- The governance vote closed after four days with 100% support from participating members.

- The ARFC marks the first non-binding stage before a formal onchain Aave Improvement Proposal vote.

- Aave V4 introduces a modular Hub and Spoke architecture to unify liquidity and isolate risk.

- The Liquidity Hub will consolidate supplied assets while Spokes will set individual lending and collateral rules.

Aave DAO has approved a Request for Comment proposal to start discussions on deploying Aave V4 on Ethereum mainnet. The vote closed after four days with 100% support on Aave’s governance platform. The measure now moves the protocol closer to a binding onchain proposal and eventual rollout this year.

Aave DAO Backs Initial Governance Stage for V4

Aave DAO used its governance platform to pass the non-binding Aave Request for Comment proposal. The vote recorded full support after a four-day voting period. As a result, the process now advances to the next governance phase.

The ARFC serves as the first step in Aave’s decentralized governance framework. It allows contributors and token holders to refine technical and risk details before a binding vote. After community feedback, Aave Labs will submit an Aave Improvement Proposal for onchain approval.

Aave Labs, led by Stani Kulechov, will coordinate the next submission. The team will work with security and risk advisors to define final risk parameters. The snapshot proposal states that deployment preparations will continue during this review period.

Aave V4 Introduces Modular Hub and Spoke Architecture

Aave V4 represents the next major upgrade of the onchain lending protocol. The upgrade introduces a modular Hub and Spoke architecture to improve liquidity efficiency. The design aims to unify liquidity while isolating risk profiles.

According to official documentation, the Liquidity Hub will consolidate supplied assets into a single unified pool. Individual Spokes will connect to the Hub under distinct lending rules and collateral policies. Each Spoke will define its own risk parameters and user conditions.

The new structure addresses the issue of siloed liquidity within the protocol. It also allows markets to operate under separate risk frameworks while sharing liquidity depth. The snapshot proposal states, “Liquidity depth is maximized, risk is priced with precision, and a wider range of lending activity can be supported onchain.”

The documentation also confirms deeper integration of Aave’s native GHO stablecoin within V4. The upgrade will introduce a revamped liquidation engine to improve efficiency. Together, these changes aim to expand supported market structures within one framework.

Governance Changes and Security Review Shape Deployment

The governance move follows internal changes among core contributors. BGD Labs and Aave Chan Initiative announced plans to step back when their contracts expire. Their announcements followed Kulechov’s “Aave Will Win” proposal on governance restructuring.

Kulechov’s proposal calls for greater DAO control over Aave Labs’ revenue and intellectual property. In exchange, the DAO would manage a defined budget for operations and development. The proposal also urges stakeholders to prioritize Aave V4 deployment.

Kulechov has also called for streamlined governance procedures within the protocol. He has encouraged faster coordination between contributors and token holders. These proposals remain under discussion within the community.

Aave V4 has completed roughly 345 days of cumulative security review. The process included manual audits, formal verification, invariant testing, fuzzing, and a public security contest. The DAO ratified a $1.5 million security budget to support these efforts.

BITCOIN ALERT!!!!!!!!

US attacks on Cuban medical missions risk damaging healthcare for poor people in developing countries

Strategy Buys 1,031 Bitcoin Using MSTR Stock Sales

-

Crypto World3 days ago

Crypto World3 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Adidas – Corporette.com

-

Politics3 days ago

Politics3 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Tech6 days ago

Tech6 days agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Crypto World2 days ago

Crypto World2 days agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

News Videos5 days ago

News Videos5 days agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Crypto World2 days ago

Crypto World2 days agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Politics6 days ago

Politics6 days agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Tech4 days ago

Tech4 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

Politics6 days ago

Politics6 days agoReal-time pollution monitoring calls after boy nearly dies

-

Crypto World5 days ago

Crypto World5 days agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

Sports14 hours ago

Sports14 hours agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

NewsBeat5 days ago

NewsBeat5 days agoResidents in North Lanarkshire reminded to register to vote in Scottish Parliament Election

-

News Videos5 days ago

News Videos5 days agoPARLIAMENT OF MALAWI – PAC MEETING WITH REGISTRAR OF FINANCIAL ON AMARYLLIS HOTEL – INQUIRY LIVE

-

Business1 day ago

Business1 day agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Politics4 days ago

Politics4 days agoGender equality discussions at UN face pushbacks and US resistance

-

Business5 days ago

Business5 days agoWho Was Alex Pretti? 5 Key Facts About the ICU Nurse Killed by Federal Agents in Minneapolis

-

Sports13 hours ago

Sports13 hours agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Tech1 day ago

Tech1 day agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Sports3 days ago

Sports3 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who nailed 12 Derby-Oaks Doubles enters picks

You must be logged in to post a comment Login