Crypto World

why Sui is betting on a native stablecoin

On March 4, 2026, the Sui blockchain launched USDsui, a US dollar stablecoin issued by Bridge (a Stripe-acquired firm) through its Open Issuance platform.

Summary

- USDsui routes reserve yield into SUI buybacks and DeFi liquidity instead of issuer-only revenue.

- Sui’s prior $1T stablecoin volume gives the model a real base to test adoption.

- Bridge’s Stripe-backed Open Issuance platform gives USDsui enterprise rails and cross-network potential.

- The model’s success depends on market share migration from USDC and USDT.

The launch was treated by most coverage as a routine product announcement. The structural reality is more consequential. USDsui is the first major Layer-1 native stablecoin where the reserve yield flows back to the underlying network rather than to the issuer. Sui processed over $1 trillion in cumulative stablecoin transfers before launching its own, including $111 billion in January 2026 alone. The yield generated on those reserves, under the traditional Circle and Tether model, would have gone to the issuer. Under USDsui, it goes to SUI token buybacks and DeFi liquidity. This is a structural shift in how blockchain economics work, and it may matter more than the launch headlines suggested.

What USDsui actually is

The Sui blockchain launched USDsui on March 4, 2026, after announcing the product in November 2025. The stablecoin is issued by Bridge, which Stripe acquired for $1.1 billion in February 2025. Bridge runs the Open Issuance platform, which launched September 30, 2025, and provides infrastructure for launching network-aligned stablecoins. The custodians for USDsui’s reserves are BlackRock, Fidelity, and Superstate. The underlying backing consists of US Treasury bonds and other liquid financial instruments.

In the simplest terms, USDsui is a dollar-pegged stablecoin like USDC, USDT, RLUSD, or PYUSD. The same basic mechanics apply: one USDsui equals one US dollar, the issuer holds reserves equal to the circulating supply, users can mint and redeem for dollars through approved channels, and the token works as a payment and trading instrument on the Sui blockchain.

What makes USDsui structurally different from the dominant stablecoin models is what happens to the reserve yield. The issuer holds the reserves in interest-bearing instruments (mostly short-term US Treasury bonds). Those instruments generate yield. Under the traditional model, that yield goes to the issuer as revenue. Under USDsui’s model, the yield flows back to the Sui network through two channels: SUI token buybacks and capital deployed into DeFi protocols and automated market makers.

This is the structural innovation. The yield that would have gone to Bridge as issuer revenue under a Circle or Tether model instead goes back to the network whose blockchain the stablecoin runs on. The arrangement is enabled by Bridge’s Open Issuance platform, specifically designed to support this kind of yield-sharing structure with networks rather than retain all reserve income for Bridge itself.

The result is a stablecoin where the economic incentives align with the underlying blockchain rather than against it. The more USDsui circulates on Sui, the more reserve income flows back to the Sui ecosystem. The arrangement creates a positive feedback loop that does not exist with USDC on Solana, USDT on Tron, or any other dominant stablecoin-blockchain pairing where the issuer captures all the economic upside.

Why this matters more than it looks

To understand why USDsui’s yield redistribution model is structurally significant, you need to understand the scale of money being captured by stablecoin issuers in the traditional model.

Tether, the largest stablecoin issuer, reportedly generated over $13 billion in profit in 2024 alone. The vast majority of that profit came from yield on the reserves backing USDT. Tether holds approximately $130 billion in reserves, mostly in short-term US Treasuries that yield around 4 to 5 percent annually. The math is straightforward: $130 billion at roughly 5 percent yield produces $6.5 billion in annual reserve income, before considering Tether’s other investments and trading activities.

Circle, the issuer of USDC, follows a similar model. Circle’s recent IPO disclosed that the company’s revenue is overwhelmingly driven by reserve yield, with management fees representing a relatively small portion of total revenue. The structure is the same: USDC circulates, Circle holds the reserves, the reserves generate yield, Circle keeps the yield.

The question USDsui asks is: why should the issuer capture all of that yield when the blockchain provides the rails that make the stablecoin usable?

Under the traditional model, the answer is “because the issuer takes on the regulatory and operational risk.” That answer is partially accurate. Stablecoin issuers do bear meaningful regulatory burdens, operational costs, and reputational risk. But the answer also obscures the reality the blockchain provides essential infrastructure (settlement, transaction processing, smart contract integration) that makes the stablecoin commercially valuable. Without the blockchain, the stablecoin would be a database entry with no utility.

Bridge’s Open Issuance platform, which Stripe inherited through its acquisition, is built around the premise this revenue split has been unbalanced. The platform offers networks the ability to launch stablecoins where the reserve yield is shared with the underlying network rather than retained entirely by the issuer. Sui is one of the first major networks to use this structure at scale, and USDsui is the proof of concept.

If the model works as designed, the implications are significant. Every Layer-1 blockchain that hosts substantial stablecoin volume would, in principle, prefer a native stablecoin arrangement where the network captures some of the reserve yield. The dominance of USDC and USDT across the industry would, over time, face structural pressure from native alternatives offering better economics to the underlying networks.

This is the broader competitive question USDsui raises. Whether the answer plays out in Sui’s favor depends on adoption, integration, and whether other networks follow with similar native stablecoin strategies.

The numbers that make Sui specifically a logical launch network

USDsui is not the first attempt at a network-aligned stablecoin. Earlier projects, including USDH on Hyperliquid, have tried similar structures with varying success. What makes Sui a particularly logical platform for this experiment is the scale of stablecoin activity the network was already supporting before USDsui launched.

Sui processed over $1 trillion in cumulative stablecoin transfers as of early 2026. In January 2026 alone, the network handled $111 billion in stablecoin transfer volume. Between August and September 2025, Sui processed a combined $412 billion in stablecoin transfers. These numbers, sourced from Sui’s own reporting, place the network among the larger stablecoin transfer venues globally.

The math implies meaningful potential yield capture. If even a fraction of that transfer activity flows through USDsui rather than USDC or USDT, the network captures yield that previously went to Circle or Tether. The exact percentage of yield that flows back to Sui under the USDsui structure has not been publicly disclosed in precise terms, but the general framework distributes a substantial share to the Sui ecosystem.

The activity is real and growing. The network’s stablecoin throughput has scaled materially over the past 18 months, driven by DeFi protocols (Suilend, NAVI, Bluefin, Scallop, Cetus, Turbos), decentralized exchange volume (DeepBook), and growing institutional integration. USDsui launches into an ecosystem that already has the stablecoin activity to justify the structure, rather than launching into a hypothetical future demand.

This is the practical reason Sui chose to move first on the native stablecoin strategy. The volume already exists. The yield capture is real. The question is whether USDsui can capture meaningful share from the dominant stablecoins now operating on the network.

How the yield loop actually works

The mechanics of USDsui’s yield redistribution are worth understanding in detail, because they determine whether the structural promise translates into operational reality.

When a user mints USDsui by depositing dollars, those dollars are sent to Bridge, which manages the reserves through its custodial relationships with BlackRock, Fidelity, and Superstate. Bridge invests the deposited dollars in US Treasury bonds and other liquid instruments that generate yield. The reserves are held one-to-one against circulating USDsui supply, ensuring the stablecoin can be redeemed at any time for the face value of one dollar.

The yield generated by the reserves accumulates as Bridge holds the Treasuries. Under the traditional model, this yield would flow to the issuer as revenue. Under the USDsui structure, the yield is redirected through Bridge’s Open Issuance platform back to the Sui Foundation, which then deploys it through two channels.

The first channel is SUI token buybacks. The yield is used to buy SUI from the open market, which reduces circulating supply and supports the token’s price through structural demand. This is similar to the buyback mechanism Hyperliquid runs with HYPE, though smaller in absolute scale because USDsui is newer and the reserve base is smaller than Hyperliquid’s protocol revenue.

The second channel is DeFi liquidity provision. The yield is deployed into automated market makers, lending protocols, and other DeFi infrastructure on Sui to deepen on-chain liquidity. This is meant to improve the trading experience on Sui-based DeFi, reduce slippage for users, and incentivize further DeFi development on the network.

Both channels are designed to create a positive feedback loop. More USDsui circulation produces more reserve yield. More reserve yield produces more SUI buybacks and deeper DeFi liquidity. Higher SUI price and better DeFi infrastructure attract more users and activity to Sui. More activity drives more USDsui adoption, which produces more reserve yield. The loop, if it holds, is self-reinforcing.

What the loop requires to hold is consistent USDsui adoption growing relative to other stablecoins on the network. If USDC keeps dominating Sui’s stablecoin activity, the yield captured by USDsui is limited to the share of activity that migrates to the native option. The faster USDsui captures market share from existing stablecoins on the network, the larger the yield loop becomes.

This is the operational question that will determine USDsui’s success. The structural framework is in place. The technical infrastructure works. The economic incentives align. Whether users, developers, and DeFi protocols actually migrate to USDsui in meaningful volume is the empirical question the next 12 to 18 months will answer.

The Stripe and Bridge connection

The infrastructure behind USDsui deserves more attention than it gets in most coverage. Bridge, the issuer, was acquired by Stripe for $1.1 billion in February 2025. The acquisition gave Stripe a foothold in stablecoin issuance infrastructure that complements its core payments business.

Stripe is one of the largest payment processors in the world, handling hundreds of billions of dollars in annual transaction volume across millions of businesses. The company has been gradually expanding into crypto-adjacent infrastructure, including stablecoin payments, on-chain settlement, and now stablecoin issuance through Bridge.

The strategic implications of Stripe-as-issuer are substantial. Stripe brings institutional credibility, regulatory relationships, payment processing infrastructure, and a global customer base traditional crypto-native stablecoin issuers cannot easily match. For USDsui specifically, Stripe’s involvement signals the product is being built to enterprise standards rather than as a crypto-experimental project.

Bridge’s Open Issuance platform, which launched September 30, 2025, is the technical infrastructure that makes the USDsui structure possible. The platform is designed to let networks like Sui launch custom stablecoins with yield-sharing arrangements traditional issuance models do not support. Open Issuance is, in effect, the productized version of the network-aligned stablecoin concept.

If Open Issuance proves successful with USDsui, the platform is positioned to launch similar native stablecoins for other major Layer-1 networks. The competitive implications extend beyond Sui. If networks like Avalanche, Aptos, NEAR, or others adopt similar native stablecoin strategies through Bridge’s platform, the broader market share calculus for USDC and USDT shifts. The question for Circle and Tether becomes whether they can match the yield-sharing terms network-native alternatives can offer.

The Bridge platform also brings regulatory compliance built into the structure. USDsui is compliant with the GENIUS Act, which President Trump signed into law on July 18, 2025. The legislation established the federal payment stablecoin framework, and Bridge’s infrastructure is designed to work within that framework from launch. This is a meaningful difference from earlier network-aligned stablecoin attempts that operated in regulatory gray areas.

What this means for other stablecoins on Sui

USDC, USDT, and other dominant stablecoins still run on Sui. The launch of USDsui does not eliminate them. The question is how the competitive dynamics play out over time.

For users, the differences between USDsui and other stablecoins on Sui are subtle. All major stablecoins maintain the one-to-one peg with the US dollar. All are usable for payments, trading, and DeFi participation. The user experience of holding USDsui versus USDC versus USDT is, at the transaction level, nearly identical.

The differences become more visible when you look at where the value flows. Using USDC on Sui generates reserve yield that goes to Circle. Using USDsui on Sui generates reserve yield that goes back to the Sui ecosystem. For sophisticated users who care about the broader economic implications of their stablecoin choices, USDsui offers a structural alignment the other options do not.

For DeFi protocols, the calculation is more direct. Protocols that build liquidity around USDsui benefit from the DeFi liquidity deployment channel in the yield loop. The Sui Foundation can deploy yield-generated capital into specific protocols that use USDsui as their primary stablecoin. This creates direct economic incentives for protocols to prioritize USDsui integration over competing stablecoins.

For institutional users, the choice depends on existing relationships, regulatory considerations, and operational preferences. Institutions that have built infrastructure around USDC will not switch easily. Institutions evaluating new digital asset infrastructure may consider USDsui as a structurally aligned option with strong regulatory framework support through Bridge’s GENIUS Act-compliant structure.

The realistic outcome is probably gradual market share migration rather than dramatic displacement. USDC and USDT are deeply entrenched, have first-mover advantage on most networks, and benefit from network effects in trading pair liquidity and exchange listings. USDsui starts at zero market share and needs to grow through organic adoption rather than network displacement.

The pace of that growth will determine whether USDsui becomes a significant player in Sui’s stablecoin landscape or stays a niche option with structural advantages that fail to translate into market dominance.

The competitive question for other Layer-1s

The most interesting implication of USDsui is not what it means for Sui specifically. It is what it means for every other major Layer-1 blockchain that hosts substantial stablecoin activity.

Solana processes more stablecoin transfer volume than Sui. Ethereum hosts the largest absolute stablecoin supply. Tron is the dominant network for USDT transfers globally. Each of these networks generates substantial stablecoin activity that produces reserve yield. Each of those reserve pools is captured by Tether, Circle, or other issuers rather than by the underlying networks.

Under the USDsui model, each of these networks would have economic incentive to launch native stablecoins that capture some of the reserve yield rather than ceding it entirely to external issuers. The infrastructure to do this (Bridge’s Open Issuance platform, or competing platforms that may emerge) is now available. The regulatory framework (GENIUS Act in the US, MiCA in the EU) provides structural clarity. The economic logic is straightforward.

The constraints are also real. Solana, Ethereum, and other major networks have deep integration with existing stablecoins that would be expensive and disruptive to migrate away from. Network effects in stablecoin liquidity make it difficult for new entrants to displace established players. The user experience switching costs are substantial. And Circle, Tether, and other issuers are not passive participants. They will compete aggressively to maintain their positions.

But the structural pressure USDsui creates is real. If the model proves successful on Sui, other networks face a choice: accept that they cede billions of dollars in potential annual yield to external stablecoin issuers, or pursue similar native stablecoin strategies. The first choice is the status quo. The second choice is a meaningful shift in how blockchain economics work.

This is the broader competitive question USDsui raises that goes beyond Sui specifically. The model may or may not succeed for Sui. The model existing and being operationally proven changes the strategic calculus for every other network that hosts substantial stablecoin activity.

For Tether and Circle, the structural threat is similar to the one the CLARITY Act’s stablecoin yield provisions create. Both developments push toward a world where the reserve yield captured by stablecoin issuers is increasingly shared with networks, exchanges, or end users rather than retained entirely by the issuer. The era of issuers capturing all the yield, which has produced extraordinary profits for Tether specifically, may be entering a structural decline.

What could go wrong

A fair assessment of USDsui has to name the conditions under which the strategy could fail.

The first risk is adoption. The yield loop only works if USDsui captures meaningful market share from existing stablecoins on Sui. If users and DeFi protocols keep defaulting to USDC and USDT despite the structural advantages of USDsui, the reserve base stays small and the yield loop is too modest to drive meaningful network effects. This is a real possibility because stablecoin adoption is sticky and the user experience differences between options are subtle.

The second risk is operational complexity. The yield-sharing arrangement between Bridge, the Sui Foundation, and the underlying SUI buyback and DeFi liquidity channels requires sophisticated coordination. Operational failures, accounting disputes, or governance disagreements over how the yield is deployed could undermine the structure’s credibility and adoption.

The third risk is regulatory. While USDsui is structured to comply with the GENIUS Act, the broader regulatory environment for yield-sharing stablecoin structures is still evolving. The CLARITY Act’s provisions on stablecoin yield and the ongoing fight between banking interests and crypto on this question create uncertainty about how regulators will treat USDsui’s structure long-term. A future regulatory change could require modifications that weaken the model.

The fourth risk is competitive response. Circle and Tether are not going to passively accept market share loss to network-aligned stablecoins. Both companies have substantial resources and could match USDsui’s yield-sharing structure for specific networks if they choose to do so. Circle’s banking license pursuit and operational scaling are partly defensive moves against exactly this kind of competitive threat. If Circle introduces a USDC variant with yield-sharing for major networks, USDsui’s structural advantage narrows.

The fifth risk is broader market conditions. USDsui’s yield loop depends on Treasury yields staying high enough to generate meaningful reserve income. If interest rates fall significantly, the absolute yield captured shrinks, and the buyback and DeFi liquidity channels become less impactful. The current rate environment is favorable. A return to near-zero rates would weaken the model.

None of these risks invalidate the structural innovation USDsui represents. They are the conditions under which the model could fail or be diluted. The honest read is that USDsui is a meaningful experiment in network-aligned stablecoin design whose success depends on factors largely outside Sui’s direct control.

What to watch over the next 12 months

For readers tracking USDsui’s progress and the broader native stablecoin question, three things are worth watching over the coming year.

The first is USDsui’s market share on Sui. If USDsui captures 20 to 30 percent of Sui’s stablecoin volume within a year, the model is working as designed and the yield loop becomes structurally meaningful. If USDsui stays under 10 percent, the model is struggling against network effects and user inertia.

The second is whether other Layer-1 networks follow with similar native stablecoin launches through Bridge’s Open Issuance platform or competing infrastructure. If Avalanche, Aptos, or NEAR launches a similar arrangement in 2026 or 2027, the structural shift toward network-aligned stablecoins becomes a sector-wide pattern rather than a Sui-specific experiment. If no major network follows, USDsui remains an isolated case study.

The third is competitive response from Circle and Tether. Both companies will likely respond to the structural threat in some form, whether through their own yield-sharing arrangements, aggressive partnership deals with major networks, or regulatory advocacy that constrains the network-aligned stablecoin model. The shape of that response will determine how much of the structural shift USDsui represents actually translates into broader market change.

The bottom line

USDsui is more interesting than it looks. The launch was treated as a routine product announcement by most coverage. The structural reality is USDsui represents one of the first serious attempts to break the dominant stablecoin business model where issuers capture all the reserve yield while networks provide the infrastructure that makes the stablecoin valuable.

The math is genuinely consequential. Tether generated over $13 billion in profit in 2024 from reserve yield. Circle’s revenue is overwhelmingly driven by the same source. The blockchains that provide the rails for these stablecoins captured none of that economic value. USDsui changes the equation by routing reserve yield back to the underlying network through SUI buybacks and DeFi liquidity deployment.

Whether the model succeeds depends on adoption, competitive dynamics, and regulatory evolution. The structural framework is in place. The infrastructure works. The economic incentives align. The empirical question is whether users, developers, and DeFi protocols actually migrate to USDsui in meaningful volume on the network, and whether other major Layer-1 networks follow with similar strategies.

For Sui specifically, USDsui is a long-term structural positive that supports the network’s positioning as a payments and DeFi platform. The yield captured will compound over time, supporting SUI’s price and the network’s DeFi infrastructure. The impact in the first 12 months will be modest. The impact over 24 to 36 months could be substantial if adoption follows the structural framework.

For the broader stablecoin market, USDsui is a meaningful test case. If the model proves successful, the structural pressure on Circle and Tether’s business models intensifies. If it fails, the dominant model goes unchallenged. The outcome will shape how stablecoin economics evolve across the industry for the rest of the decade.

For readers, the practical lesson is native stablecoins are no longer just a theoretical concept. USDsui is operational, regulated, backed by enterprise-grade infrastructure through Stripe’s Bridge, and integrated across Sui’s major DeFi protocols. The model is being tested in real conditions, with real adoption metrics that will tell us within 12 to 18 months whether the structural innovation translates into competitive market share.

The Stripe and Bridge backing matters because it brings institutional credibility purely crypto-native stablecoin alternatives have struggled to match. The Open Issuance platform matters because it productizes the network-aligned stablecoin model for replication across other networks. The Sui Foundation’s commitment matters because it shows major Layer-1 networks are willing to bet on this structural approach.

USDsui is not going to displace USDC or USDT in the next 12 months. The question is whether USDsui shows a different model is viable, and whether that demonstration changes the strategic calculus for every other major blockchain network that currently lets its stablecoin yield flow entirely to external issuers.

That is the bet Sui is making with USDsui. The bet is rational. The execution is in place. The outcome will be visible in the adoption metrics over the next year.

What this all comes down to is a simple question: should the reserve yield from blockchain stablecoin activity go to the issuer or to the network that provides the infrastructure? The traditional answer has been the issuer. USDsui is the first serious attempt to give a different answer at scale.

The answer to that question, however it plays out, will define a significant piece of how blockchain economics work for the next decade.

This article is for informational purposes and does not constitute financial or investment advice. Stablecoin structures and adoption metrics evolve quickly; the figures and milestones described reflect reporting available as of late May 2026. Always do your own research.

TLDR:

- Major U.S. banks are building tokenized deposit networks for interbank settlement and clearing.

- DTCC plans tokenized equity and Treasury trades before a broader platform launch in October.

- Tokenized stocks surpassed $1.5 billion in value after growing more than 3,300% since 2024.

- SEC discussions around tokenized stock rules signal growing regulatory engagement with the sector.

Tokenization is moving deeper into mainstream finance as major banks, asset managers, and regulators advance new blockchain-based initiatives.

Recent developments span tokenized deposits, securities settlement, stablecoin reserve funds, and tokenized equities.

The activity comes as tokenized stocks continue to record rapid growth across digital asset markets. Together, the moves highlight how traditional financial institutions are increasing their involvement in tokenized finance.

Tokenization Expands Across Banks and Financial Infrastructure

Several of the largest U.S. banks are pushing forward with tokenized payment infrastructure.

According to information shared by Ondo Finance, The Clearing House is developing a shared tokenized deposit network for interbank clearing and settlement.

The initiative involves major institutions including JPMorgan, Citi, Bank of America, and Wells Fargo. The proposed network aims to streamline transfers between participating banks through tokenized deposits.

Momentum is also building in securities infrastructure. The Depository Trust & Clearing Corporation, commonly known as DTCC, plans to begin limited production trades involving tokenized Russell 1000 equities, major ETFs, and U.S. Treasuries in July.

DTCC expects a broader platform launch in October. The organization stated that more than 50 firms have participated in development efforts, including BlackRock, JPMorgan, and Ondo Finance.

Asset managers are also expanding their presence in tokenized markets. According to data highlighted by Ondo Finance, State Street launched a dedicated money market fund designed for stablecoin issuers.

The fund launched with approximately $121 million in assets under management. State Street joins BlackRock, Goldman Sachs, and BNY in offering products aimed at supporting stablecoin reserve requirements.

Tokenized Stocks Growth Draws SEC Attention

Tokenized stocks continue to emerge as one of the fastest-growing sectors in digital assets. Data from RWA.xyz shows the market exceeded $1.5 billion in value by mid-June.

The sector has expanded more than 3,300% since January 2024. That growth has pushed tokenized equities and ETFs into a more prominent position within crypto markets.

Regulators are increasingly examining the trend. According to Reuters, the U.S. Securities and Exchange Commission is evaluating an innovation exemption that could create a modified framework for tokenized stock platforms.

The proposal faced delays after exchanges raised concerns during discussions earlier this year. Reuters reported that revisions to the framework are expected in the coming months.

At the same time, Ondo Finance continues expanding access to tokenized securities. Ondo Global Markets recently added 173 tokenized stocks and ETFs.

The expansion increased the platform’s offering to more than 430 tokenized stocks and ETFs. The assets are available across Ethereum, Solana, and BNB Chain, further broadening access to blockchain-based financial products.

BitGo CEO Mike Belshe has rejected a viral claim that Anthropic’s Mythos model breached nearly all of the National Security Agency’s classified systems, calling the story false as it spread across X this weekend.

His pushback targets posts that recast the government shutdown of a three-day-old model as a real-world hack. The fuller record is less dramatic.

Where the Mythos NSA Breach Claim Came From

The claim originated with Senator Mark Warner, vice chair of the Senate Intelligence Committee. The Economist reported his account of what the NSA director told him.

Warner said General Joshua Rudd, who leads the NSA and US Cyber Command, described the tool in stark terms.

“This tool broke into almost all of our classified systems, not in weeks, but in hours,” the Economist wrote, citing Warner.

Warner raised the example while praising Anthropic, not condemning it. He used it to argue for faster pre-release testing of frontier models.

The detail that went missing online is simple. This was an authorized red-team test on the agency’s own networks, not an outside intrusion.

Shashank Joshi, the Economist editor who published the quote, later cautioned it should not be read literally. He said it depended on Mythos working alongside other tools in particular conditions.

The US government was already a Mythos partner. Anthropic had deployed the model to government cyber defenders through Project Glasswing since April.

Belshe and Others Question the Framing

Belshe, the co-founder and chief executive of digital-asset custodian BitGo, answered one of the threads bluntly.

“I’m calling BS on this,” he challenged.

Follow us on X to get the latest news as it happens

He was not alone. Zack Korman mocked how the claim moved from senator to journalist to social media unchecked.

Analyst Kyle Chase noted the break-in was a test. He said a separate jailbreak flagged by Amazon was the real trigger.

Anthropic’s own statement supports them. It said the flagged jailbreak simply asked the model to read a codebase and fix flaws.

The technique surfaced a few minor, already-known bugs that rival models like OpenAI’s GPT-5.5 can also find.

The company disabled both models on June 12 to meet a US export-control directive, not because of any battlefield breach. It objected to recalling a model used by hundreds of millions of people over one narrow flaw.

Whether the test justified pulling the models is still contested. AI researcher Pedro Domingos argued the export controls were responsible, given the model’s powerful hacking capabilities.

Anthropic itself calls Mythos the strongest cyber model in the world. Yet it says recalling a tool over one flaw would freeze new releases across the industry.

The company is now working to restore access, and is drafting a shared risk framework with the White House.

The post Crypto Executive Disputes Claims Anthropic’s Mythos Breached NSA Systems appeared first on BeInCrypto.

CME is arguing that perps are harmful to its long-dated futures products. The lawsuit alleges that the CFTC did not consider the ramifications of approving perps, and that these products are actually “swaps” as defined by the Dodd-Frank Act, and not “futures.”

Each term carries implications for how the products themselves are to be regulated and what the requirements are for the companies issuing them are. CME CEO Terrence Duffy, who recently announced he’s stepping down next year, told CNBC last week that the distinction mandates different rules for participants.

“The CFTC did not engage in its own analysis of whether its approval of Kalshi’s Bitcoin perpetual as a future is consistent with law,” CME’s lawsuit said. “The CFTC did not even mention the relevant Dodd-Frank provision defining ‘swap.’ Indeed, the word ‘swap’ appears nowhere in the Order.”

The CFTC instead just “rubberstamped Kalshi’s application,” the lawsuit claimed.

What’s interesting is that the actual landscape of companies securing designated contract market (DCM) approvals and moving into perps is growing quite rapidly. On the same day the CFTC granted Kalshi’s application, it sent a no-action letter to Coinbase, seemingly opening the door for that exchange to list perps as well — albeit through an offshore intermediary.

TLDR:

- Sui’s reported 1M operations per second milestone sparked fresh discussion around blockchain scalability.

- Community posts highlighted Sui’s focus on supporting large-scale AI agent activity on-chain.

- CoinMarketCap data showed SUI gaining 0.79% over the past 24 hours amid rising attention.

- Network throughput claims intensified competition among high-performance blockchain platforms.

Sui is drawing fresh attention after claims that its network reached one million operations per second, adding momentum to discussions around blockchain scalability and AI-driven activity.

The milestone surfaced through posts from prominent members of the Sui ecosystem and quickly spread across crypto markets.

Network performance has become a key focus as developers prepare for growing machine-to-machine interactions on-chain. Meanwhile, SUI posted a modest price increase over the past 24 hours despite broader market uncertainty.

Sui Network Scalability Claims Put AI Agent Demand in Spotlight

Discussion around Sui accelerated after posts from the Sui Community account highlighted the network’s reported ability to process 300,000 transactions per second.

The post stated that the network has no hard scalability ceiling and was designed for a future where AI agents could outnumber human users on-chain.

The claim referenced comments from Sui co-founder Adeniyi Abiodun and research discussions involving Grayscale’s research team. According to the shared information, Sui’s architecture was built with large-scale autonomous activity in mind.

Attention intensified after Crypto Banter shared separate comments attributed to Abiodun.

The post stated that the network had reached one million operations per second and that activity from stablecoin systems and automated agents appeared among the earliest indicators of the increased throughput.

The distinction between operations and transactions remains important. However, the figures quickly became a talking point across crypto social media as traders evaluated the implications for future blockchain demand.

Sui has increasingly positioned itself as a network focused on high-speed execution and scalable infrastructure. Those features have become more relevant as AI-powered applications begin interacting directly with blockchain networks.

SUI Price Edges Higher Following Throughput Milestone

The scalability discussion arrived alongside a positive move in the SUI token price. According to CoinMarketCap data, SUI traded at approximately $0.7087 at the time of reporting.

The token recorded a 0.79% gain over the previous 24 hours. The move was relatively modest, yet it coincided with heightened attention around the network’s performance claims.

Trading activity remained active as market participants reacted to the reports circulating across social platforms. The throughput figures generated significant engagement among developers, investors, and infrastructure-focused projects.

Interest in AI-related blockchain infrastructure has expanded throughout the digital asset sector. As a result, claims involving large-scale processing capacity often attract immediate attention from traders.

Posts from the Sui Community account and Crypto Banter helped amplify the discussion, placing network performance at the center of the conversation. The reported milestones also arrived as competition among high-throughput blockchain networks continues to intensify across the crypto market.

Abu Dhabi Global Market (ADGM) has approved the first admission of tokenized digital securities to its Official List, alongside permission for the instruments to trade on a recognized exchange venue. The development signals that tokenized assets can be structured and regulated within an established securities framework, rather than operating only as over-the-counter products or experimental pilots.

The legal filing and regulatory steps were guided by law firm Gibson Dunn, which advised Btech Holdings Limited. According to the firm, the Financial Services Regulatory Authority (FSRA) of ADGM approved the relevant prospectuses on 11 June 2026 under the market and financial services rules that apply to securities listings.

What ADGM approved, and why it matters

ADGM’s announcement centers on the admission of tokenized securities referred to as bStocks. The instruments were characterized under ADGM regulation as securities for the purposes of the Financial Services and Markets Regulations 2015 (FSMR). They were structured as Certificates over Shares, a design choice intended to fit the tokenized product into conventional securities categories.

After FSRA approval of the prospectuses, the securities were admitted to ADGM’s Official List of Securities with effect from the same date, and they were also set to be traded on the Recognized Investment Exchange (RIE) operated by Nest Exchange Limited.

In institutional capital markets, listing and trading rules are critical for liquidity, investor protections, and market integrity. By tying tokenized securities to an official listing process and prospectus approval, ADGM is effectively aligning part of the tokenization market with the same regulatory benchmarks used for traditional listings.

Regulatory pathway: prospectus approval and admission to the Official List

Per Gibson Dunn’s account, FSRA approval was granted for prospectuses drafted by the firm. The approval was described as being provided pursuant to section 61 of FSMR and Rule 4.6 of the Market Rules (MKT), including a reference to meeting requirements under MKT 4.5.

This matters because prospectus regimes are typically designed to ensure disclosures are comprehensive and consistent, covering issuer details, the nature of the instrument, risk factors, and other information required for public market participation. For tokenization to move into mainstream financing channels, regulators and exchanges generally need to ensure tokenized structures still satisfy disclosure and governance expectations.

How the product is structured: certificates over shares

The tokenized instruments were described as securities that fall under FSMR, structured as certificates over shares. The certificate-over-share structure is relevant in regulatory terms because it can help define the rights embedded in the tokenized instrument, including the economic linkage to the underlying shares.

While tokenization often involves distributed ledger infrastructure, the key regulatory question is how the product maps to existing legal definitions. ADGM’s approach, as reflected in this admission, indicates a willingness to treat tokenized securities as regulated securities when the instrument’s legal characteristics are clear and the issuer complies with disclosure and admission requirements.

Implications for tokenization in the UAE and beyond

Institutional tokenization is still searching for scalable market infrastructure and consistent regulatory standards. Regions that can demonstrate repeatable pathways for approvals, listing, and regulated trading have an advantage when issuers and financial intermediaries decide where to deploy tokenized capital markets activity.

ADGM’s step also points to a broader industry trend: regulators are increasingly focused on whether tokenized assets can meet established securities principles, including transparency, market conduct expectations, and investor protections.

In this case, the admission to ADGM’s Official List and the ability to trade on the RIE operated by Nest Exchange potentially reduce operational uncertainty for market participants evaluating tokenized instruments. It may also encourage other issuers considering tokenization to pursue structured, regulated listings rather than limiting activity to private placements.

Role of legal counsel

Gibson Dunn stated it advised on multiple phases of the mandate, including structuring the issuance, preparing prospectuses approved by FSRA, and handling the applications for admission to the Official List and to trading on the RIE.

The firm said the team was led by partners Sameera Kimatrai and Jade Chu, supported by associates Aliya Padhani and Holly Alderton. The matter was also described as involving other partners including Hagen Rooke, Mellissa Duru, and Lauren Cook Jackson.

What to watch next

This admission provides a regulatory reference point for tokenized securities that aim to be integrated into exchange-based trading. Going forward, market observers will likely focus on whether additional tokenized issuances follow the same pathway, how liquidity develops on the trading venue, and whether the market structure attracts issuers and intermediaries at scale.

For investors, the practical value of tokenized securities will depend on execution quality, transparency, custody and settlement mechanics, and ongoing compliance. For issuers, the central question will be whether regulated listing and trading can reduce barriers to issuance while still supporting innovation in how assets are tokenized and distributed.

Crypto World

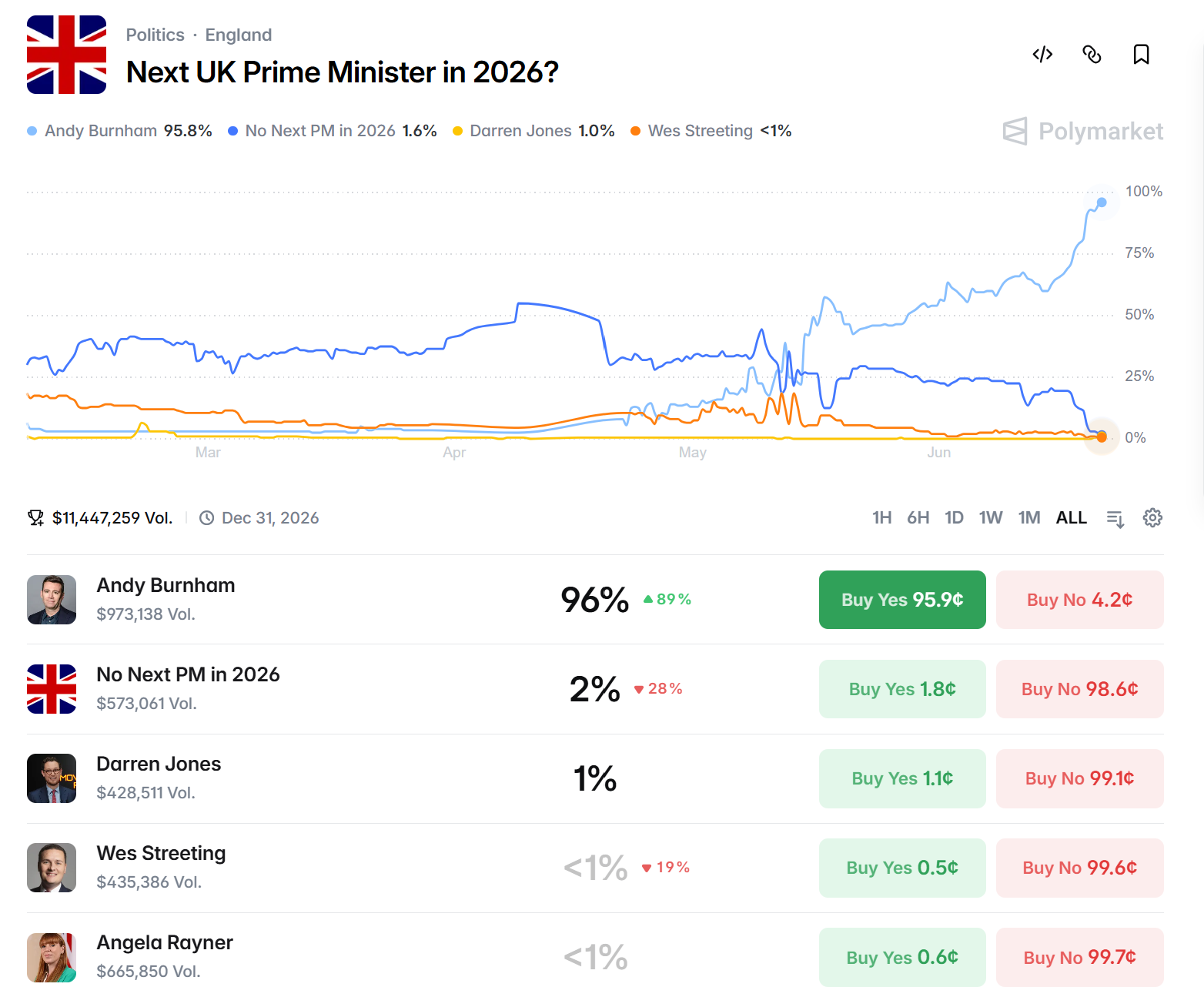

Could Keir Starmer’s Exit Open the Door to Britain’s Most Crypto-Friendly Labour Leader?

Andy Burnham’s landslide by-election win has handed Labour’s most crypto-friendly figure a clear route to challenge Keir Starmer for the party leadership.

The Greater Manchester mayor will be sworn in as an MP this week, removing the last barrier to a leadership bid. His enthusiasm for Web3 sits awkwardly beside Starmer’s recent crackdown on crypto.

Burnham’s Win Reopens the Leadership Question

Burnham took the Makerfield seat on June 18 with 54.8% of the vote. He beat Reform UK by a majority of more than 9,200, on a turnout that climbed to almost 59%.

By-election turnouts usually fall, so the result reads as a genuine mandate.

He is due to be sworn in within days. On Polymarket, the crypto-settled prediction market, traders have wagered more than $11 million on the succession and make Burnham the clear favorite to take over.

Starmer insists he will fight any challenge.

Weekend reports suggested the prime minister was weighing his future, though his office dismissed talk of an imminent exit.

Cabinet ministers, union leaders and party donors have all joined talks about the timing of a handover.

A Pro-Web3 Voice Against a Crypto Crackdown

Burnham ranks among the few senior Labour figures to openly back digital assets. He told about 100 Web3 founders at a Stand With Crypto event that he was “bought in.”

“Manchester was the home of the Industrial Revolution. Let’s make it the home of the web3 revolution,” Andy Burnham, Mayor of Greater Manchester, in remarks to crypto founders.

That tone clashes with the national party. In March, Starmer’s government imposed a moratorium on crypto donations to political parties.

The independent Rycroft Review had warned that crypto’s anonymity could mask foreign money entering UK politics.

Even so, Burnham’s support looks regional and pragmatic, tied to Manchester jobs rather than markets.

Reform UK is Britain’s most crypto-forward party, and one of only three that had agreed to accept crypto at all.

Its leader, Nigel Farage, has bought Bitcoin (BTC) himself and pitched a national reserve.

Markets Watch the Handover

The political risk has already reached bond markets. The 10-year gilt yield rose to about 4.8% on Friday.

Investors are weighing a Burnham government they expect to borrow and spend more freely, and sterling weakened alongside it.

For crypto, the signal is fainter. Bitcoin traded near $63,900, up less than 1% on the day but down about 17% over the month and 38% on the year.

It sits well below its October record near $126,000, so the turmoil has produced no clear safe-haven bid.

Any read-through also depends on a retail base that is shrinking. Crypto ownership among UK adults has slipped to about 8%, down from 12% a year earlier, the FCA found.

A Burnham premiership could still soften the tone toward Web3 after a year of tighter UK crypto rules, though bond investors look more worried about his spending than his digital-asset views.

His swearing-in and any leadership timetable this week will set the near-term direction. A warmer crypto stance surviving Britain’s fiscal squeeze is the real question for a shrinking crypto electorate.

The post Could Keir Starmer’s Exit Open the Door to Britain’s Most Crypto-Friendly Labour Leader? appeared first on BeInCrypto.

In times when investors are pulling funds out of the spot exchange-traded funds tracking ETH and especially BTC, their behavior toward XRP, HYPE, and SOL has been entirely contrasting.

The ETFs following the three altcoins’ performances continue to see more net inflows even as the market stagnates and uncertainty builds.

XRP, SOL, HYPE ETFs Keep Gaining Capital

CryptoPotato has repeatedly reported on the Ripple ETFs’ impressive performance over the past several weeks, in which most assets, including XRP, recorded fresh losses and dipped to multi-year lows. However, investors using the Wall Street-trading financial vehicles have remained active, with net inflows dominating for months. In fact, there have been only two weeks in the red since mid-March.

The last one, which had only four trading days, also ended in the green. The ETFs attracted $2.82 million on Monday, $5.30 million on Tuesday, and $2.55 million on Thursday. Since Wednesday was a $0.00 day, according to SoSoValue data, that means that the week ended with net inflows of $10.66 million. The cumulative net inflows have tapped a new all-time high of $1.45 billion.

The Solana ETFs also attracted over $7 million in net inflows in the past week, following a red one with $2.58 million in net outflows. HYPE and its ETFs continue to be the current market superstar. The funds saw their third-best week to date, with almost $28 million entering. Moreover, the HYPE ETFs have been on a six-week streak of net inflows since their inception in mid-May.

Their performance has been particularly promising since they have attracted nearly $185 million in net inflows in six weeks. The same six weeks have been highly emotional and full of FUD for the entire crypto market, especially June’s start when most assets tumbled to multi-year lows.

BTC, ETH ETFs Deep in Red

And while the aforementioned altcoins continue to enjoy fresh ETF capital, the same cannot be said for the funds tracking the two largest cryptocurrencies by market cap. As reported earlier, the spot BTC ETFs bled more than $226 million in the past week, and are down by roughly $5 billion in the same six weeks in which the HYPE and XRP ETFs have been only in the green.

The spot Ethereum ETFs are in no better shape. In fact, they are on the same six-week negative streak, pushing the total inflows down by nearly $1 billion. So the question now is whether investors are simply seasonally rotating from larger-cap digital assets into smaller altcoins, or have they completely abandoned BTC and ETH for the new kids on the block.

The post Why Capital Is Flowing Into XRP, SOL, and HYPE Instead of BTC and ETH appeared first on CryptoPotato.

Bitcoin’s downside risks are again back in focus as analyst Jesse Olson laid out a worst-case technical scenario that could send BTC sharply lower if a broader macro shock hits US markets. In a Sunday post, Olson pointed to a multi-week chart setup that, in his view, leaves Bitcoin vulnerable to a move toward $23,980—a level he frames as a key target in the event of a severe stock-market sell-off.

The bearish case is not only technical. Olson’s outlook aligns with what multiple market indicators have been signaling so far in 2026: institutional participation appears muted, with a persistently weak Coinbase premium reading and ongoing spot Bitcoin ETF outflows described by market data providers. Together, these factors suggest that when risk appetite falls, Bitcoin could face stronger selling pressure than what retail alone might typically drive.

Key takeaways

- Olson’s chart work suggests BTC could fall toward $23,980 if US equities undergo a macro downturn of roughly 50%+.

- A negative Coinbase premium is consistent with weaker professional demand rather than aggressive institutional accumulation.

- Since May, SoSoValue data shows US spot Bitcoin ETFs have logged $4.68 billion in net outflows.

- On-chain analyst Darkfost argues institutions tend to wait for confirmation and performance, making them less likely to “buy the bottom” prematurely.

Olson’s worst-case BTC level and the macro trigger

Olson shared a two-week Bitcoin chart outlining a potential pathway for downside under stress conditions. His level is derived from a proprietary Market Sniper Pro VWAP indicator, using a long-term support line based on an anchored, volume-weighted average price (aVWAP) concept.

In the chart framing Olson used, the line appears anchored from the 2022 bear-market bottom. As the chart progresses, that methodology effectively creates a sloping reference zone that traders can watch for whether price is respecting a longer-term “average” support framework—or breaking away from it.

Olson presented $23,980 as a base-case target in a “severe macro sell-off” scenario that includes a US stock market drop of more than 50%. The implication is straightforward: Bitcoin has often traded like a high-risk asset during periods when leveraged positions are unwound and liquidity becomes expensive.

The macro timing risk Olson warns about is not confined to crypto technicals. The article context also references calls from established market observers who have warned about speculative excess or heightened recession risk. For example, GMO co-founder Jeremy Grantham has argued the current AI-led market surge resembles a major speculative bubble, while economist Gary Shilling has warned a US recession is “almost inevitable” by year-end, with stocks potentially declining by 20%–30%. (Those perspectives are cited via links embedded in the original reporting.)

Against that backdrop, the logic for Bitcoin is that a broad equity shock could accelerate crypto de-risking. In practical trading terms, that can mean earlier longs are forced to reduce exposure, and new dip-buying interest—particularly institutional—may take longer to reappear.

Coinbase Premium stays negative, signaling weak “professional” appetite

Beyond chart levels, the report highlights the Coinbase Premium Index—a metric that compares Bitcoin’s price on Coinbase versus Binance. The underlying idea is that when the premium is positive, it often reflects stronger US institutional demand (or at least more aggressive buying pressure on regulated venues). When the reading stays negative, it can point to weaker professional accumulation or heavier selling on Coinbase relative to Binance.

According to the report’s description, the Coinbase premium has been largely negative so far in 2026. That matters because it suggests that, at least in this period, institutional-style demand has not stepped in with the same urgency seen during stronger risk-on phases.

The key tension for traders is that BTC’s price can still rise without sustained premium strength—especially if retail-driven flows dominate. But if the market later shifts into “risk-off,” a lack of steady institutional bid can make drawdowns more abrupt, because there is less natural demand to cushion sell pressure.

Spot Bitcoin ETFs record $4.68B in outflows since May

The institutional-demand picture is reinforced by spot Bitcoin ETF flow data cited from SoSoValue. The report states that since May, US-based spot Bitcoin funds have accumulated $4.68 billion in net outflows.

ETF flow trends are closely watched by many participants because they aggregate buying and selling behavior across traditional brokerage accounts and investment platforms. Net outflows, in that sense, can be read as ongoing caution from professional allocators and advisers rather than a one-off profit-taking event.

While the report doesn’t attempt to forecast ETF flows forward, the combination of negative Coinbase premium and ETF outflows fits the same broader narrative: there isn’t clear evidence, at least in the period referenced, that major institutional channels are actively leaning against weakness.

Why institutions may wait for “confirmation,” not a potential bottom

One reason analysts often provide for institutional behavior under stress is that these players may not buy based on technical “support” signals alone. Instead, they may wait for confirmation—whether that’s stabilization in broader markets, improved volatility conditions, or sustained improvements in inflows.

In a Sunday post cited in the report, Darkfost, a CryptoQuant-associated on-chain analyst, said: institutions “don’t act like retail” and typically operate under “permanent risk management logic.” Darkfost’s point, as quoted, was that institutions are “not looking to buy a potential bottom” but rather for confirmation and performance—adding that the conditions for that are “not the case yet.”

This helps explain why Olson’s downside framing could matter even if the $23,980 area is technically meaningful. If institutional demand is missing—or if ETF outflows continue—then market moves toward lower support zones may be driven less by “buying opportunity” narratives and more by positioning adjustments and liquidity constraints.

Earlier coverage referenced in the report also aligns with the idea that a stock-market crash could push Bitcoin below $30,000. While those earlier remarks are not elaborated in detail here, they strengthen the broader theme: macro shocks can overwhelm crypto’s internal narratives and magnify downside through forced de-risking.

For readers, the key watch items are straightforward: whether BTC’s technical structure actually breaks toward the $23,980 target, and whether institutional indicators change character—specifically the Coinbase premium trend and whether spot Bitcoin ETFs shift from net outflows to inflows. If those signals remain weak, the market may continue to treat rallies as temporary while waiting for broader risk conditions to improve.

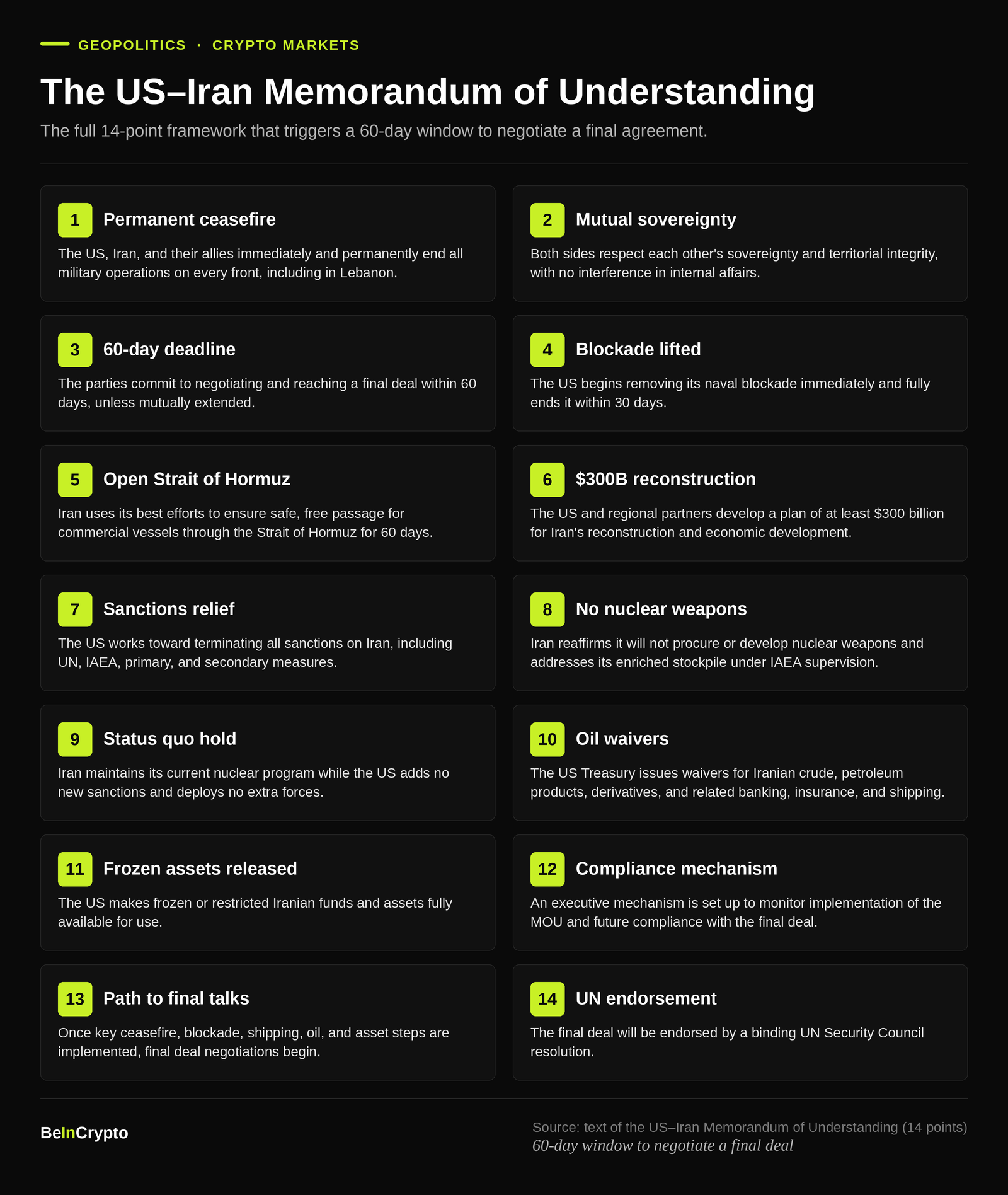

US Vice President JD Vance opened direct US-Iran talks at Switzerland’s Bürgenstock resort on Sunday, even as President Donald Trump threatened fresh military strikes if Tehran fails to rein in Hezbollah.

The talks implement a 14-point memorandum that Trump and Iranian President Masoud Pezeshkian signed on June 17. It set a 60-day ceasefire to end a war that began on February 28 and to reopen the Strait of Hormuz.

US-Iran Talks Open Under Pressure

Vance leads the US side, with Iranian chief negotiator Mohammad Bagher Ghalibaf heading Tehran’s team. Pakistan and Qatar are mediating in a four-way format.

The talks nearly fell apart first. Iran suspended them on Friday over Israel’s strikes in Lebanon, then agreed to meet on Sunday. Vance expects only a couple of days of negotiations.

Washington wants fast movement on Iran’s nuclear program. Tehran wants the fighting in Lebanon to stop first. It is also seeking sanctions relief, the unfreezing of assets, and an end to the US naval blockade.

The truce is fraying. Israeli strikes killed dozens in Lebanon over the weekend, and five Israeli soldiers have died since the deal. The turmoil has even split crypto traders over whether the ceasefire holds.

Bitcoin (BTC) could swing again if the war reignites, a risk analysts have already war-gamed for crypto. Trump, meanwhile, escalated on Truth Social, warning Tehran over its Lebanese proxies.

“Iran must immediately stop their highly paid PROXIES in Lebanon from causing trouble. If they don’t, we’ll hit Iran very hard again, just like we did last week, only harder!!!” Donald Trump, US president, via post.

Follow us on X to get the latest news as it happens

Why Crypto Markets are Watching Hormuz

The Strait of Hormuz is the reason markets care. About 20 million barrels of oil cross it daily. That is close to a fifth of global supply and more than a quarter of seaborne trade.

Iran’s Revolutionary Guard declared the waterway shut on Saturday, citing Israel’s attacks. Yet US Central Command said 55 tankers still passed through that day, carrying more than 17 million barrels.

After the signing, oil fell sharply, and equities set records. Brent crude slipped to about $78 a barrel, and US gas hit $3.99 a gallon, its lowest since March. GasBuddy analyst Patrick De Haan expects sub-$3 gas by early 2027 if the truce holds.

For crypto, the signal runs through oil. Cheaper energy cools inflation and revives rate-cut bets, the script Bitcoin has followed all year.

Yet Bitcoin barely reacted to the deal, holding near $64,000. Last June, a similar Iran ceasefire sent it above $105,000.

The next few days of talks will test whether the ceasefire survives in Lebanon. For crypto, the bigger tell may be oil, not the nuclear file.

The post Trump Issues Fresh Iran Threat as US-Iran Talks Enter Critical Phase appeared first on BeInCrypto.

HIVE Digital Technologies, a Nasdaq-listed infrastructure provider, says it has received approval from the municipal council of Boden to acquire the 32 megawatt Big Boden data centre in northern Sweden. The purchase, focused on long-term control of a key Nordic site, is designed to support HIVE’s plans to expand high-performance computing and AI workloads from within its existing Swedish footprint.

The Big Boden facility has supported HIVE’s operations since 2018. With the approval in place, the company moves from tenant arrangements to ownership, a shift that typically gives data centre operators greater flexibility over long-term capital planning, infrastructure upgrades, and operational resilience targets.

From tenant to owner at Big Boden

Municipal approval is a common procedural step in real estate and infrastructure transactions, particularly where utilities, permitting, and local planning requirements are involved. For HIVE, the significance is practical as well as strategic: a controlled asset can be upgraded on a longer horizon than leased capacity.

In its announcement, HIVE framed the acquisition as a milestone in its commitment to Sweden as a location for “sovereign” AI and sustainable digital infrastructure. The company has previously positioned its compute infrastructure around sustainability and green power sourcing, an increasingly important topic for enterprise AI buyers who face pressure to disclose and manage energy use.

Upgrade path toward Tier III-style capabilities

HIVE said it plans to bring the Boden site toward Tier III infrastructure standards. In data centre terms, that typically relates to higher expectations for redundancy and uptime, including design approaches meant to reduce the risk of unplanned outages. While the company did not provide a detailed timeline in the email update, it indicated the work is intended to strengthen security, redundancy, and uptime capabilities for enterprise-scale AI and high-performance computing workloads.

The company also referenced support for next-generation NVIDIA GPU architectures, pointing to a market demand shift across the industry. Data centre operators are increasingly competing not only on raw power capacity, but also on operational readiness for GPU-intensive deployments, including performance, reliability, and power delivery capabilities suitable for large-scale AI training or inference.

Why data centre ownership matters for compute strategy

In the broader market, many compute infrastructure firms rely on a mix of owned and contracted capacity. Ownership can reduce uncertainty when demand rises, but it also shifts execution risk to the operator, including capex planning, construction timelines, and regulatory compliance.

For companies pursuing AI-related workloads, the reliability dimension is critical. GPU clusters generally require steady power availability, robust cooling, and predictable uptime to maintain service quality for customers and internal deployments. Moving toward a higher tier standard can therefore be an operational necessity rather than a branding exercise.

HIVE’s move to own the Big Boden asset also aligns with a trend in which governments, enterprises, and regulated sectors seek local compute options. Whether referred to as “sovereign” compute, data residency, or strategic infrastructure, the underlying idea is the same, greater control over where workloads run and how infrastructure is governed.

Sustainability and local impact in the background

The email update included figures and context intended to show continuity of investment in the Boden region since HIVE’s earlier entry. It stated that HIVE has invested more than SEK 960 million in the region through local contractors and renewable energy procurement, and that it has contributed more than SEK 575 million in taxes to the Swedish Tax Authority. HIVE also pointed to local community involvement through initiatives such as support for youth and women’s hockey, sponsorship activity, and work linked to heat recovery projects.

While these points are not directly tied to the municipal approval itself, they help explain how data centre operators often build long-term social and regulatory relationships, particularly in markets where energy consumption, land use, and grid impact are recurring political topics.

Implications for HIVE and the Nordic AI infrastructure market

If HIVE executes its upgrade plan as described, the Big Boden facility could strengthen the company’s ability to serve enterprise and institutional customers looking for AI compute capacity in northern Europe. In practice, the key question for investors and customers will be how quickly capacity can be upgraded to the desired operational standard and how performance targets translate into usable capacity for GPU-based deployments.

HIVE also indicated the project fits into a broader strategy aimed at developing renewable-powered AI infrastructure across multiple jurisdictions. For the Nordic region specifically, the acquisition underscores ongoing competition among compute operators to secure energy-backed capacity and to position their facilities for AI workloads with higher reliability expectations.

For now, the municipal approval clears the way for the transaction and subsequent development plans. The next milestones will likely involve the deal completion process and disclosure around the scope and timing of upgrades at the 32 MW site.

Note: This update is based on information provided in the announcement circulated to the media.

Wall Street’s Tokenization Race Heats Up as SEC Reviews New Rules

I Will Find You EPs Reveal If David Will Date His Sister-in-Law

Sudden financial luck

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Miami – Corporette.com

-

Crypto World7 days ago

Zimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Business2 days ago

Business2 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Entertainment7 days ago

Entertainment7 days agoMatt Damon’s Viral Sci-Fi Thriller Has Taken Over HBO Max

-

Crypto World2 days ago

Crypto World2 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Business7 days ago

Business7 days agoAnthropic staff to meet White House officials next week, Axios reports

-

Crypto World7 days ago

Crypto World7 days agoBitcoin could crash to $48,000, if this historical pattern is triggered

-

NewsBeat7 days ago

NewsBeat7 days agowhat doctors are seeing in ebike crashes

-

NewsBeat7 days ago

NewsBeat7 days agoWarning of disruption as Cardiff Crossrail works to start

-

NewsBeat7 days ago

NewsBeat7 days agoTributes to former deputy head teacher at Cambridge school among death and funeral notices

-

Entertainment7 days ago

Entertainment7 days agoKate Middleton Glare Goes Viral After Kids Booed At Royal Event

-

Politics7 days ago

Politics7 days ago“Israel’s” ban on ICRC visits ruled illegal, but Knesset moves to stop them permanently

-

Crypto World7 days ago

Crypto World7 days agoXRP ETFs Outperform As Bitcoin And Ethereum Funds Extend Outflow Trend

-

Tech7 days ago

Tech7 days agoOver 400 Arch Linux packages compromised to push rootkit, infostealer

-

News Videos7 days ago

News Videos7 days agoFinancial Accounting | Last Day Revision Strategy and Booster | CMA Inter – June 2026

-

Sports7 days ago

Sports7 days agoDick Advocaat’s Curacao scores first-ever World Cup goal against Germany

-

Business7 days ago

Business7 days agoInvesco Quality Income Fund Q1 2026 Commentary

-

NewsBeat7 days ago

NewsBeat7 days agoSinger Oliver Tree dies aged 32 in helicopter crash in Brazil

-

Tech5 days ago

Tech5 days agoThe Adder At The Heart Of Intel’s 8087 FPU

-

Tech7 days ago

Tech7 days agoMicrosoft Updates Six Windows’ Apps. ‘Photos’ Gets Watermarks for Copilot Images (Off by Default)

You must be logged in to post a comment Login