Crypto World

Will crypto market dip as USDT exchange reserves decline?

The crypto market has faced sustained pressure in February, with prices struggling to build momentum amid declining stablecoin exchange reserves.

Summary

- CryptoQuant reports USDT reserves fell from $60B to $51.1B in two months, reducing market liquidity.

- Daily trading volumes are modest and active on-chain wallets have been declining.

- Analysts are split: VanEck calls it orderly deleveraging, while others warn of deeper losses if support breaks.

Bitcoin (BTC) has dropped by nearly 50% from its peak in October 2025 and by roughly 30% since the year began. Alongside the decline, there has been slower stablecoin growth, cautious interest rate signals from the Federal Reserve, and weaker U.S. manufacturing data.

Total market capitalization has fallen to around $2.3 trillion. At the same time, the Fear and Greed Index has slipped to cycle lows. Continued exchange-traded fund outflows have added to investor caution and reduced fresh capital entering the market.

Liquidity drain raises downside risks

On Feb. 26, CryptoQuant analyst TopNotchYJ warned that shrinking stablecoin reserves are becoming a major risk factor. Data shows that Tether (USDT) exchange balances fell from $60 billion to $51.1 billion in two months, a $9 billion decline that has tightened trading liquidity since January.

TopNotchYJ described the drop in USDT reserves as clear evidence of capital moving out of crypto markets. Stablecoins are the main source of trading activity, and falling balances usually signify a drop in investor confidence. Moving below $50 might put more selling pressure on major assets like XRP, ETH, and BTC.

The number of active wallet addresses has also rapidly decreased, from about 376,000 to 263,000. This shows that retail investors and institutional investors are taking a backseat. Price rebounds typically lose strength when there are fewer market participants, as demand naturally softens.

A similar pattern is visible in trading behavior. The daily volume has dropped by more than 6% to roughly $339 million. This indicates little speculative activity in the market, but it does not suggest widespread panic selling.

Short-term outlook and analyst views

Analysts remain divided, although most expect high volatility in the near term. Some warn that Bitcoin could slide another 20% to 30% if economic pressure continues, especially if support near $60,000 breaks. The $70,000 level continues to act as a major barrier to recovery.

Matthew Sigel of VanEck has described the recent decline as “orderly deleveraging.” He argues that leverage has cooled and that the market is adjusting rather than entering a full collapse.

Researchers at K33 Research see parallels with the late-2022 bottom. They point to fragile economic conditions and stagnant stablecoin supply as limits on short-term upside.

More positive views come from Bitwise Asset Management, which manages more than $15 billion. Their analysts continue to highlight Bitcoin’s long-term potential and see recent pullbacks as possible accumulation opportunities.

Several technical levels remain are now in focus. Support lies between $64,000 and $66,000, followed by $60,000 and the $50,000–$55,000 zone. Resistance is clustered near $70,000 and $80,000.

Until stablecoin reserves recover and user activity improves, analysts expect the market to stay vulnerable, with downside risks likely to persist in the coming weeks.

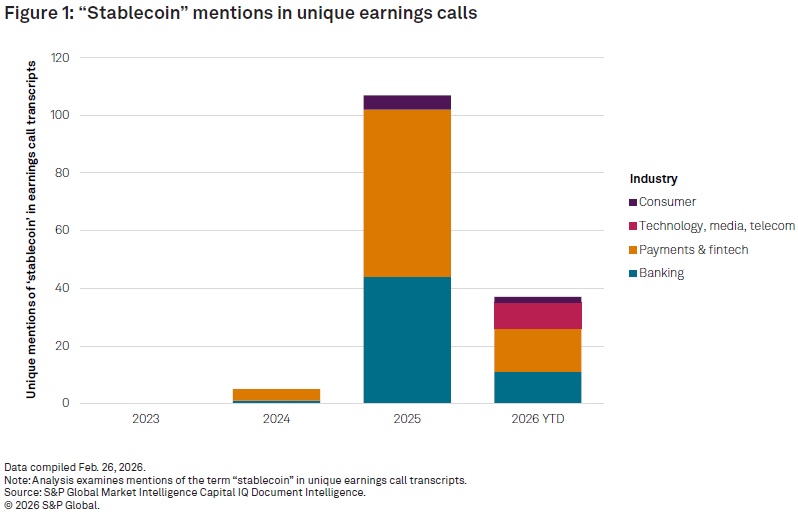

Stablecoins are rapidly evolving beyond their original role in crypto trading, emerging as a key layer of financial infrastructure, according to new research from S&P Global Market Intelligence.

The report highlights a growing shift toward institutional use cases, particularly in cross-border payments, treasury operations, and capital markets, while traditional banks continue to take a cautious, exploratory approach.

Stablecoins Move Beyond Trading

“Stablecoins are evolving beyond a crypto trading tool into a new layer of financial infrastructure,” said Jordan McKee, Director of Fintech Research at S&P Global Market Intelligence.

According to the report, the most meaningful adoption is happening behind the scenes, where stablecoins are improving settlement speed, capital efficiency, and liquidity movement rather than being widely used at the consumer level.

Market Growth Accelerates

The stablecoin market is expanding rapidly:

- Circulation reached approximately $269 billion in 2025

- Projected to grow to around $434 billion by 2028

- Mentions in earnings calls surged to 107 in 2025, up from just five in 2024

This sharp increase reflects rising interest from banks, fintech firms, and payment providers exploring the role of stablecoins in modern financial systems.

Institutional Use Cases Lead Adoption

Adoption remains concentrated in infrastructure-level applications, including:

- Cross-border payments

- Treasury and liquidity management

- Tokenized capital markets

In these areas, stablecoins are helping reduce settlement times and improve capital mobility across global markets.

Consumer Adoption Still Limited

Despite the growing institutional interest, consumer adoption remains low, especially in developed markets.

Only 12% of U.S. consumers report familiarity with stablecoins, with concerns around security, fraud, and lack of clear use cases acting as key barriers.

Banks Take a Wait-and-See Approach

The report also reveals a significant gap between infrastructure development and institutional readiness.

Among 100 primarily smaller U.S. financial institutions surveyed:

- Only 7% are developing internal stablecoin frameworks

- None are actively piloting stablecoin initiatives

This suggests that while the technology is advancing quickly, many banks are still evaluating how and when to engage.

Regulation and Competition to Shape the Future

Since the start of 2025, at least 19 applications for banking charters related to digital asset services have been submitted to the Office of the Comptroller of the Currency (OCC).

As the market matures, S&P Global Market Intelligence expects adoption to be driven less by consumer usage and more by:

- Institutional integration

- Regulatory frameworks

- Competition across issuance, liquidity, and distribution

The report concludes that stablecoins are entering a critical infrastructure buildout phase, which will likely define their role in the global financial system over the coming years.

A crypto card can look simple. You tap to pay, shop online, or withdraw cash, and it works much like a regular card.

Still, the total cost is not always obvious. Depending on the provider, users may pay blockchain fees, conversion costs, foreign exchange charges, ATM fees, or merchant markups. Some of those costs appear clearly. Others are built into the rate or show up only at checkout.

That is why the real cost of a crypto card is not one single fee. It is the total cost of moving funds, converting them, and spending them.

Network fees can start before you even spend

The first cost can appear when a user moves crypto into a wallet or account linked to the card. In that case, the blockchain may charge a network fee, often called a gas fee.

That fee usually does not come from the card provider. Instead, it comes from the network that processes the transaction. As a result, the cost can change depending on which blockchain the user picks and how busy that network is.

So even before the card is used for a purchase, the funding step may already carry a cost.

The exchange rate can include a hidden conversion cost

Many crypto cards convert crypto into fiat at the moment of payment. In some cases, that conversion cost appears as a stated fee. In other cases, it sits inside the exchange rate itself.

That difference matters. A card may look cheap on paper, but the user may still pay more through the rate used to convert crypto into dollars, euros, or another currency.

So when comparing cards, users should not look only at the fee page. They should also look at how the provider handles conversion.

Foreign purchases can trigger FX fees

When a card is used in a different currency, foreign exchange fees can apply. That is common when users travel, shop on foreign websites, or withdraw cash abroad.

In some cases, the card network sets one rate and the issuer adds its own FX fee on top. That means the final cost can rise even when the transaction goes through normally.

This is one reason why cross border spending often costs more than a domestic purchase.

DCC is one of the clearest ways to overpay

Another common cost appears at the terminal. When a user pays abroad, the merchant or ATM may ask whether to charge the card in the user’s home currency instead of the local one. That is Dynamic Currency Conversion, or DCC.

It often looks convenient, but it usually costs more. BEUC, the European Consumer Organisation, said consumers are financially worse off in “practically every single case” when they accept DCC. The same paper cited research showing DCC was on average 7.6% more expensive in one study, while the highest markup reached 12.4%.

So the cleaner option is usually the local currency, not the home currency shown on the screen.

A simple DCC example

|

Option |

What happens |

Typical result |

| Pay in your home currency through DCC | The merchant or ATM converts the purchase | Often a worse rate than letting the card network handle it |

| Pay in the local currency | The card network and issuer handle the conversion | Usually the more standard and lower cost route |

That difference may look small on one purchase. Still, it adds up across repeated payments and withdrawals. BEUC’s paper also found examples where payment markups in stores ranged from 2% to 5%, while ATM DCC increases ran from 2.6% to 12% in one dataset.

ATM withdrawals can stack several fees at once

Cash withdrawals are another area where costs can pile up fast. First, the ATM operator may charge its own fee. Then the card issuer may add a withdrawal fee. If the withdrawal is in a foreign currency, an FX fee may apply as well.

So one ATM transaction can combine several charges in a single step. That is why withdrawing cash is often one of the more expensive ways to use a crypto card.

Users should check both the card provider’s fee schedule and the ATM screen before confirming the transaction.

Card holds are not fees, but they still affect spending

Card holds are not fees, but they still affect spending

Not every unexpected charge is a fee. Hotels, fuel stations, car rentals, and some online merchants often place a temporary hold on the card before the final charge settles.

That hold reduces the available balance for a period of time. Later, the merchant posts the final amount and releases the unused part.

So while a hold is not a direct cost, it can still confuse users and make the card balance look lower than expected.

Other small charges can still matter

Some crypto cards also charge for physical card shipping, replacement cards, premium plans, or inactivity. These costs are not the same across the market, so they should not be treated as universal.

That is why the fee page matters as much as the headline promise. A provider may advertise low spending fees while charging in other places.

In short, the total cost depends on the full structure, not one line in the marketing copy.

What cost can look like in practice

A user may pay one fee to move crypto onchain, another cost through the conversion rate, another fee on a foreign purchase, and another markup if DCC is accepted by mistake. Then, if the same user withdraws cash abroad, ATM and FX charges may come on top.

KAST’s public fee page offers one example of how that structure can work. It says non-USD card purchases carry a foreign exchange fee of 0.5% to 1.75%, depending on the countries involved. It also says ATM withdrawals cost $3 plus 2% of the withdrawal amount, with the same 0.5% to 1.75% FX fee added for non-USD withdrawals.

That example does not make crypto cards unusually expensive. It simply shows that the total cost often comes from several layers, not one headline fee.

If you want to see how a real fee schedule is laid out before you travel or spend abroad, take a minute to explore KAST.

The main point on cost

Crypto cards are easier to understand when each cost is separated clearly. The main ones to watch are network fees, conversion costs, FX fees, DCC markups, ATM charges, and temporary holds.

Among them, DCC remains one of the clearest traps because it can make a transaction more expensive without adding any real benefit for the cardholder. BEUC’s findings underline that point.

So the simplest rule is this: check how the card handles conversion, read the fee page before using it abroad, and choose the local currency when a terminal gives you the choice.

Enhanced Labs raised a $1 million pre-seed led by Maximum Frequency Ventures to expand options-based yield strategies across on-chain and tokenized real-world assets.

Summary

- Enhanced Labs secures $1 million pre-seed round led by Maximum Frequency Ventures.

- Backers include GSR, Selini, Flowdesk and several angel investors.

- Funds will expand options-based yield strategies to more on-chain and tokenized real-world assets.

U.S.-based DeFi infrastructure startup Enhanced Labs has closed a $1 million pre-seed funding round to expand its options-based yield products across a wider range of on-chain assets, including tokenized real-world assets. The round was led by Maximum Frequency Ventures, with market-making and trading firms GSR, Selini and Flowdesk joining alongside a group of undisclosed angel investors. According to the company, the capital will be used to support product development, operations and go-to-market efforts.

Enhanced Labs positions itself as a provider of “options-based yield strategies” designed to sit on top of existing DeFi and tokenization rails, rather than competing directly with spot lending or simple staking. By extending these structured strategies to tokenized real-world assets, the firm is effectively betting that on-chain treasuries, credit, commodities and other RWAs will need the same kind of yield engineering and risk-transfer mechanisms that already exist in traditional markets. The goal is to package those exposures in a way that can be deployed programmatically, but still remain accessible to institutions that need clearer risk parameters than typical DeFi products offer.

Backing from names like GSR, Selini and Flowdesk suggests Enhanced Labs is targeting the intersection of market-making, derivatives and on-chain liquidity rather than retail-facing savings products. For these investors, options-based yield on tokenized assets is not just a new narrative but a potential source of structured flow if RWAs continue to move on-chain. The pre-seed size is modest by bull-market standards, but at this stage the more important signal is that specialized trading firms are willing to seed infrastructure aimed at making RWAs behave more like fully featured, hedgeable collateral.

If Enhanced Labs executes, it could help close one of the gaps in today’s tokenization pitch: plenty of projects can put a bond or a real-estate claim on-chain, but far fewer can offer a robust menu of ways to hedge, lever or generate predictable income on top of those assets. Whether a $1 million war chest is enough to build those tools—while navigating the regulatory and risk constraints that come with engineering yield on real-world exposures—remains an open question.

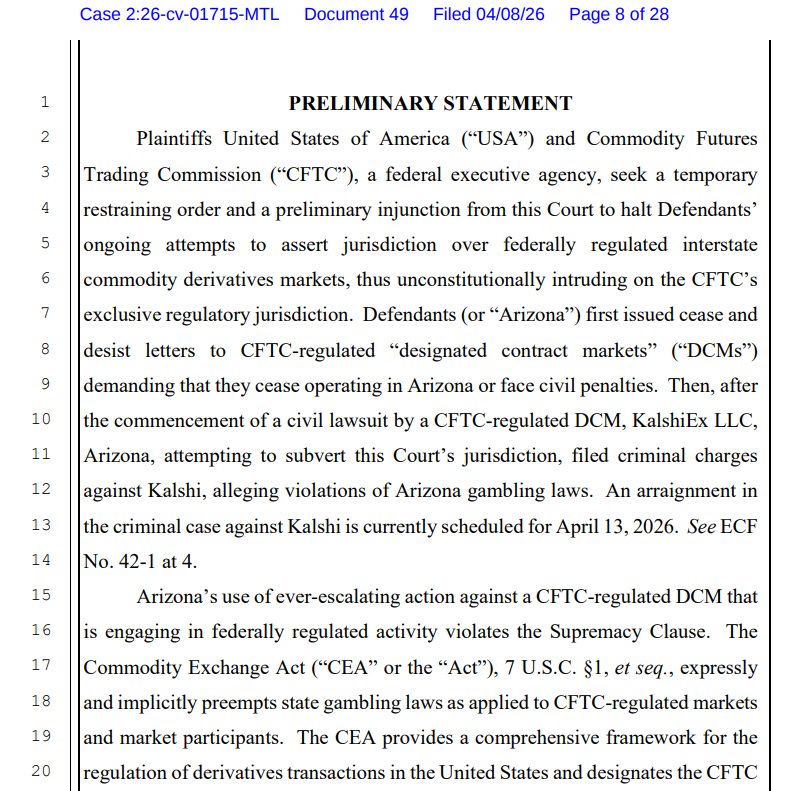

The US Department of Justice (DOJ) and Commodities and Futures Trading Commission (CFTC) asked a federal court to block Arizona from enforcing state gambling law against Kalshi’s event contracts, arguing that they fall under the CFTC’s exclusive authority over swaps markets.

The Wednesday filing argues that event contracts listed on federally regulated platforms such as Kalshi are swaps under the Commodity Exchange Act and therefore fall within the CFTC’s exclusive jurisdiction.

The filing says Arizona’s enforcement effort unlawfully intrudes on the CFTC’s exclusive jurisdiction over federally regulated event-contract markets.

If granted, the order would block Arizona from applying its gambling laws to prediction markets that are listed as federally regulated event contracts. An arraignment in the criminal case against Kalshi is currently scheduled for Monday.

Arizona Attorney General Kris Mayes announced charges against the companies behind Kalshi on March 17, accusing them of operating an “illegal gambling business in Arizona without a license” and offering illegal election wagering.

Kalshi co-founder and CEO, Tarek Mansour, claimed the charges were a “total overstep” and “not about gambling.”

Federal and state regulators clash over prediction markets

The dispute has become a major test of whether prediction market contracts belong under federal commodities law or state betting rules.

On April 2, the CFTC filed three separate lawsuits against the gaming regulators of Illinois, Connecticut and Arizona, claiming that the event contracts offered by the platforms violated state gambling laws and licensing requirements.

In those suits, the CFTC says it has exclusive jurisdiction over CFTC-registered designated contract markets that list lawful event contracts. Kalshi is the clearest example in the current litigation.

Related: Kalshi, Polymarket face trading halt in Nevada after court rulings

Prediction markets are facing growing regulatory pressure in the US, where 11 states have pursued legal action against them.

Prediction market activity has been rising since the beginning of the US and Israeli military conflict with Iran, fueling renewed insider trading allegations, after six Polymarket traders netted $1 million by accurately betting when the US would strike Iran.

In response to insider trading concerns, Democratic Party Senator Adam Schiff has introduced legislation seeking to ban prediction markets on war, death and terrorism.

Magazine: Train AI agents to make better predictions… for token rewards

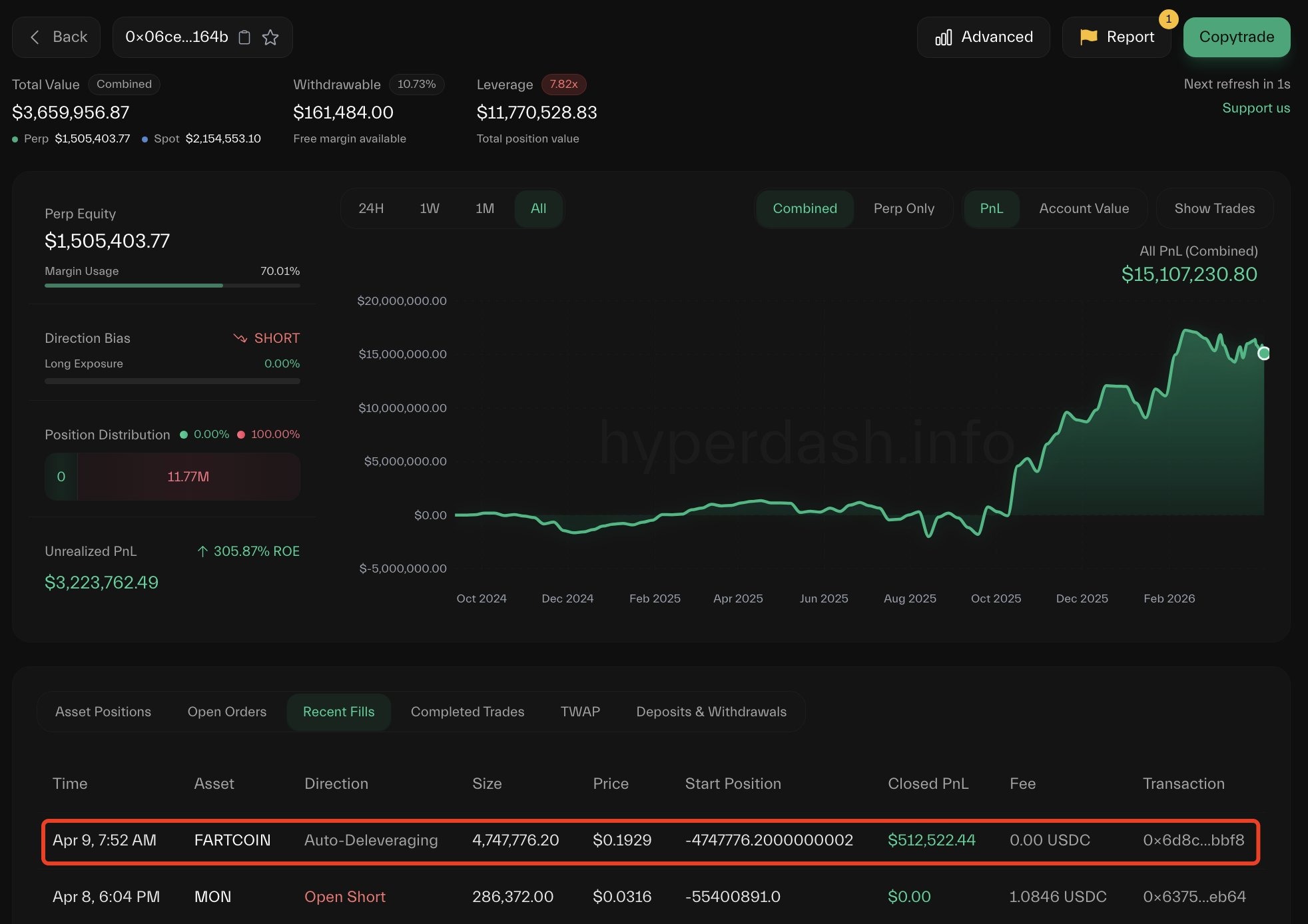

A trader lost about $3 million after building a large leveraged Fartcoin position on Hyperliquid that unraveled in thin liquidity, triggering the platform’s auto-deleveraging (ADL) mechanism.

Hyperliquid data flagged by Lookonchain shows that the trader accumulated about 145 million tokens across multiple wallets before being liquidated. The liquidation redistributed gains to opposing traders, with at least two wallets seeing around $849,000 through ADL.

PeckShield said the unwind produced about $3 million in accounting losses and left Hyperliquid’s HLP vault down roughly $1.5 million over 24 hours, though Hyperliquid had not publicly confirmed those figures by publication.

The episode highlighted how ADL can crystallize gains for traders on the other side of a collapsing position, while raising fresh questions about how Hyperliquid’s liquidation and vault structure behave in low-liquidity markets.

PeckShield said the activity appeared structured to trigger liquidations in low-liquidity conditions, potentially pushing losses onto Hyperliquid’s liquidity pool while being offset by positions elsewhere.

Cointelegraph reached out to Hyperliquid for comments, but had not received a response before publication.

Past trades exposed similar pressure on Hyperliquid’s liquidity system

This is not the first time Hyperliquid’s liquidity system has come under pressure from large, concentrated positions.

On March 13, 2025, the platform’s Hyperliquidity Provider (HLP) vault took a roughly $4 million hit after an oversized Ether (ETH) position was unwound, triggering liquidations under thin market conditions. After the incident, the team said that losses stemmed from market dynamics rather than a protocol exploit.

Related: Onchain perp DEX volumes fall for five straight months after October peak

A similar episode occurred later that month involving the JELLY memecoin. On March 27, 2025, a trader used multiple leveraged positions to exploit the platform’s liquidation system.

However, the final outcome remained unclear, with Arkham saying the trader withdrew about $6.26 million but may still have ended up down nearly $1 million.

On Nov. 13, 2025, a similar pattern occurred when a trader built large leveraged positions in the POPCAT market, triggering cascading liquidations that left a $5 million hole in the HLP vault. Community members said the strategy appeared designed to create and then remove liquidity to force the vault to absorb the impact.

Magazine: Solana exec trolls crypto gamers, Pixel tackles play-to-earn issues: Web3 Gamer

Authorities in the United States, United Kingdom and Canada have frozen millions of dollars tied to crypto scams in a joint enforcement operation called Operation Atlantic.

The operation, focused on phishing attacks, took place in March and was coordinated by the UK’s National Crime Agency (NCA), the US Secret Service, the Ontario Provincial Police and the Ontario Securities Commission.

Operation Atlantic identified more than 20,000 victims across the US, Canada and the UK, securing and freezing more than $12 million in suspected criminal proceeds, the NCA said Thursday. It also identified “more than $45 million stolen in cryptocurrency fraud schemes,” the agency added.

“Operation Atlantic is a powerful example of what is possible when international agencies and private industry work side by side,” NCA Deputy Director of Investigations Miles Bonfield said.

The operation involved assistance from major cryptocurrency exchange Binance, according to a separate statement by the company.

What is an approval phishing scam?

Approval phishing scams trick users into signing malicious permissions that allow attackers to access and drain crypto wallets.

Unlike typical scams, where perpetrators trick victims into sending them crypto, approval phishing misleads victims into unknowingly authorizing malicious transactions that allow scammers to spend specific tokens inside the victim’s wallet.

“Approval phishing is one of the most damaging types of scams targeting crypto users today,” said Flavio Tonon, Binance’s senior regional advisor for the Europe, Middle East and Africa region.

Related: Drift explains $280M exploit as critics question Circle over USDC freeze

He noted that the operation underscores how effective crime fighting is possible when private and public partners work together, adding that blockchain transparency makes it difficult for criminals to get away with phishing exploits.

No funds were frozen on Binance as part of the operation

Operation Atlantic included on-site investigations at the NCA’s London headquarters, where Binance said its Special Investigations team provided support, including live account screening and scam intelligence.

The company also provided insights on potential bad actors in order to assist with asset seizure efforts, and conducted research that identified scam websites that were still actively defrauding victims at the time of the operation.

Binance said no funds were frozen on Binance accounts.

Magazine: AI agents will kill the web as we know it: Animoca’s Yat Siu

Stablecoins are on track to become a foundational layer of global finance, with adjusted transaction volumes projected to reach $719 trillion by 2035, according to a new report by blockchain research firm Chainalysis on Wednesday.

The growth, driven by organic adoption alone, signals a structural shift in how value moves across borders and through everyday commerce, the research firm added.

Stablecoins moved more than $35 trillion on blockchain rails last year, noting that only roughly 1% was for real-world payments, according to a March report by McKinsey and blockchain data firm Atermis Analytics.

A key catalyst is the looming generational wealth transfer, with as much as $100 trillion expected to pass from Baby Boomers to Millennials and Gen Z over the coming decades. These younger cohorts, far more likely to use crypto as a financial instrument by default, are set to redefine payment preferences at scale, embedding digital assets into mainstream economic activity.

“When crypto becomes the default for the next generation of capital, the question is no longer if stablecoins compete with traditional rails, but how quickly they replace them,” Chainalysis said in its report.

At the same time, stablecoin transaction volumes are quickly converging with traditional payment networks. Chainalysis said that current trends suggest onchain payments could match Visa and Mastercard’s volumes no later than 2039, placing direct competitive pressure on legacy rails long defined by intermediaries, fees and delayed settlement.

Unlike card networks, stablecoins enable near-instant, 24/7 settlement and programmable transactions, reducing friction across remittances, business payments, and treasury operations. As merchant adoption expands, paying with stablecoins is increasingly shifting from a deliberate choice to invisible infrastructure, the firm added.

Chainalysis is also introducing a new category of blockchain intelligence agents, aimed at helping institutions navigate and operationalize this transition as digital assets move from the margins to the core of global finance.

“The institutions that build for onchain payments now will define the next era of global finance, while those that wait risk settling on someone else’s rails,” Chainalysis said.

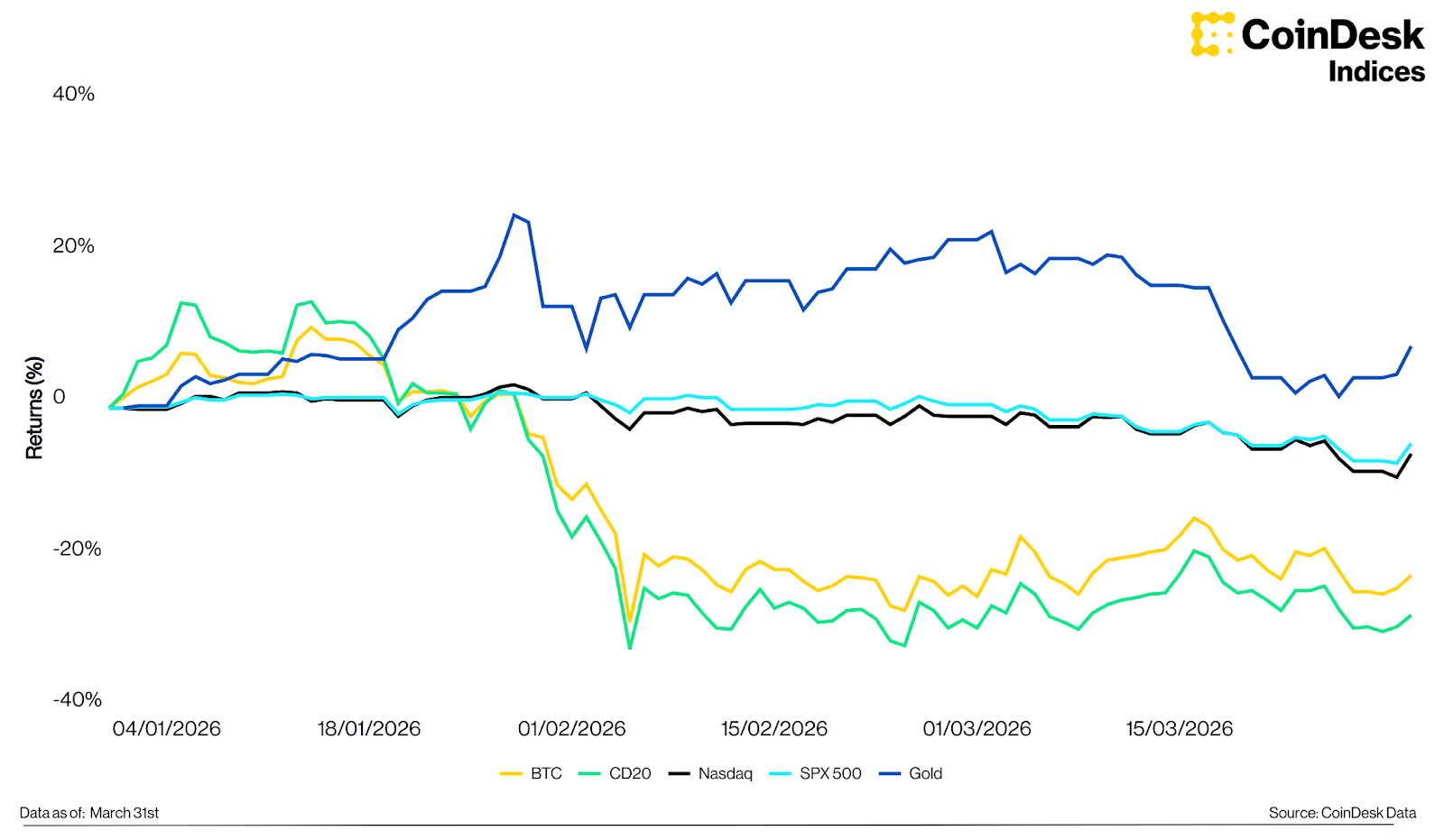

In today’s newsletter, Joshua de Vos from CoinDesk breaks down cryptos performance in the first quarter, highlighting shifting institutional demand and new regulatory clarity setting the stage for Q2.

Q1 2026 Digital Asset Review

Digital assets closed Q1 2026 under meaningful pressure, extending a downturn that began in late 2025. As presented in CoinDesk’s latest “Quarterly Review and Outlook,” the quarter was shaped by escalating geopolitical tensions, a cautious Federal Reserve, and institutional flows that turned sharply negative before partially recovering into month-end.

Q1 in review

The CoinDesk 20 Index declined 27.4% to 1,952, while bitcoin fell 22.1% to $68,228; its second-largest quarterly decline since Q2 2022. Escalating tensions in the Middle East pushed crude oil above $100 per barrel, while the Federal Reserve held rates steady at 3.5%–3.75% following its March meeting. The S&P 500 and Nasdaq declined 4.63% and 5.98% respectively; gold was the standout, rising 8.19% to $4,671.

BTC vs gold vs SPX vs Nasdaq vs the CD20 Index, Q1 2026

A notable dynamic emerged in the quarter’s second half. Bitcoin had already declined roughly 30% from its February peak before geopolitical tensions escalated sharply in late February, suggesting much of the fear and forced liquidations had been priced in before the event. Since tensions intensified, bitcoin returned 3.54%, while the S&P 500 and Nasdaq fell 5.09% and 4.89%. The CoinDesk Memecoin Index was the weakest performer at -41.7%; the CoinDesk 80 outperformed bitcoin, declining 16.5%, with Hyperliquid (+43.8%) and Morpho (+40.9%) leading positive returns among its constituents.

BTC and CD20 Index vs selected assets, returns since Feb 28th

Institutional flows in focus

Among U.S. spot bitcoin ETFs, net outflows of $1.81B across January and February erased much of the institutional demand built during the prior year. Although March saw a recovery of $1.32B in inflows, Q1 closed with net redemptions of approximately $496M. Bitcoin’s stabilisation in March coincided with the return of positive net inflows, suggesting institutional positioning had begun to rebuild before the quarter ended.

Bitcoin ETF flows and BTC price, Q1 2026

In the spot ETF era, institutional flow data provides a real-time signal of sentiment unavailable in prior cycles. The March recovery sets a baseline worth watching for Q2, particularly as Morgan Stanley reportedly prepares a spot bitcoin ETF ($MSBT) at a 0.14% fee, designed to integrate into its network of over 16,000 advisors.

The regulatory picture clarifies

A joint SEC–CFTC ruling on March 17 designated 16 assets, including SOL, XRP and DOGE, as digital commodities and thus outside the securities definition. This removes a key regulatory overhang and opens the pathway for spot ETF approvals across a broader range of assets. Basket and index-based ETPs now rank second only to bitcoin-focused products by number of pending filings, with CoinDesk indices including the CD20 and CD100 increasingly referenced as natural benchmarks for these vehicles.

Number of pending crypto ETP applications, 2025

Looking ahead to Q2

Market direction in Q2 will be shaped by two variables: the trajectory of the Middle East conflict and the Federal Reserve’s response to inflation data. A de-escalation would ease energy price pressure and creates conditions for recovery; prolonged conflict would keep financial conditions tight. Bitcoin’s October 2025 peak near $126,000 and the subsequent correction are broadly consistent with the historical halving cycle, which typically produces an 18–24 month post-ATH drawdown. This cycle’s structural difference is institutionalised ETF demand; on peak days in 2024, inflows topped $1 billion, equivalent to absorbing over 30 days of mining supply in a single session. Combined with a more supportive regulatory environment and a deepening institutional product suite, the structural foundation entering this correction is meaningfully more durable than in prior cycles.

Constituent highlights

Ether declined 29.1% in Q1, with U.S. spot ether ETFs recording net outflows of $758 million. The more significant forward-looking development is Ethereum’s structural position in tokenised assets; 59.4% of total real-world asset supply resides on Ethereum as of Q1 2026. BlackRock’s ETHB staking ETF, launched on March 12 with a projected 3–7% annual yield, introduces an income-generating dimension to ETH that could broaden its appeal to yield-oriented allocators.

Solana declined 33.2% but registered a notable milestone: peer-to-peer stablecoin transaction volume reached a new all-time high of $832 billion in Q1 2026, reflecting a shift toward payments infrastructure. Solana’s real-world asset holder count also surpassed Ether for the first time, driven by platforms such as Ondo Global Markets and xStocks.

XRP declined 27.1%, but the narrative is increasingly centred on Ripple’s expanding institutional infrastructure. RLUSD reached a market capitalization of $1.42 billion by quarter-end, and Ripple’s acquisition strategy, spanning prime brokerage through Hidden Road ($1.25 billion, clearing $3 trillion annually) and treasury management through GTreasury ($1 billion), points toward a comprehensive financial ecosystem built around XRP and RLUSD. The key catalyst for Q2 is whether these integrations translate into measurable on-chain activity.

This summary was created based on CoinDesk Research’s latest report “Digital Assets: Quarterly Review and Outlook, Featuring CoinDesk 5 and CoinDesk 20.”

– Joshua de Vos, research team lead, CoinDesk

Keep Reading

- JP Morgan CEO Jamie Dimon says the bank must “move faster” with its blockchain efforts due to the threats banking faces from blockchain technology.

- Morgan Stanley’s own bitcoin ETF opened this week creating competition on Wall Street.

- The U.S. Treasury is pitching new rules for stablecoin issuers to treat them like every other financial firm that must maintain armor against illicit uses.

Bitcoin (BTC) circled $71,000 at Thursday’s Wall Street open after US inflation data conformed to expectations.

Key points:

-

Bitcoin waits for new catalysts as US PCE inflation data conforms to market expectations.

-

Friday’s CPI release will be the first to show any impact of the US-Iran war.

-

$80,000 remains in play as a BTC price target, a trader says.

PCE data avoids surprises for risk assets

Data from TradingView showed cooling BTC price volatility after local highs near $73,000 the day prior.

Relief over a US-Iran ceasefire combined with favorable readings from the Federal Reserve’s “preferred” inflation gauge, the Personal Consumption Expenditures (PCE) index.

Core PCE year-on-year came in at 3% for February. On a monthly basis, core PCE was at 0.4%, per data from the US Bureau of Economic Analysis (BEA).

Reacting, trading resource The Kobeissi Letter noted that the impact of the US-Iran war and oil-supply squeeze were not yet reflected in PCE.

“This marks the final pre-Iran War PCE inflation datapoint,” it wrote on X.

Markets remained cautious about future Fed policy, with data from CME Group’s FedWatch Tool continuing to show no expectations of interest-rate cuts in 2026.

While Bitcoin offered no obvious reaction to the latest data, meanwhile, economist Mohamed El-Erian argued that Friday’s March Consumer Price Index (CPI) release was more important.

“While PCE inflation is widely regarded as the Fed’s favorite measure, the bigger inflation focus this week will be on tomorrow’s CPI data, as PCE covers February and not March,” he told X followers.

As Cointelegraph reported, CPI is particularly susceptible to fallout from oil-price swings.

Trader: $80,000 BTC price push “on the horizon”

BTC price action thus left traders guessing as to when and where the next move would be.

Related: Bitcoin RSI ‘nearly perfectly’ copying end of 2022 bear market: Analysis

In their latest market commentary, pseudonymous trader LP leveraged liquidation clusters to give potential targets.

“On the HTF, some upside low-leverage liquidation clusters have been cleared, but sizeable liquidity still remains around 73K and above the highs near 76K. Meanwhile, liquidity is starting to build on the downside, mainly around 69K and 64K,” an X post stated.

“With price still range-bound, both sides remain in play. If the 69–68K level holds, price is likely to push higher and target the remaining upside liquidity around 73K.”

Crypto trader Michaël Van de Poppe was more optimistic, keeping the $80,000 mark in play.

“As long as Bitcoin continues to hold these ranges, there’s a strong new upwards leg on the horizon towards $80K,” he summarized on the day.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

Crypto World

Bitmine Immersion (BMNR) uplists to NYSE and boosts share buyback program to $4 billion

Bitmine Immersion Technologies (BMNR) began trading on the New York Stock Exchange on Thursday, moving from the NYSE American as it scales its crypto-focused treasury strategy.

The company paired the uplisting with an increase in its share repurchase program, raising the authorization to $4 billion from $1 billion. The buyback ranks among the largest announced this year, according to the company. BMNR’s stock has plunged roughly 90% since peaking last summer amid the height of the digital asset treasury mania. Shares are lower by 2.8% in early Thursday trading.

Bitmine now holds about 4.8 million ETH, equal to 3.98% of total supply, and continues to target 5%, or what it calls the “Alchemy of 5%.”

The macro backdrop could play a role. Fundstrat co-founder Tom Lee, who also chairs Bitmine, has argued that U.S. equities may have found a bottom following a ceasefire tied to tensions in Iran. Stocks, oil and volatility shifted sharply in response, a pattern that has also lifted crypto markets.

Bitcoin recently moved above $72,000 alongside gains in equity futures, reflecting a broader “risk-on” trade. Ether may benefit as well, with recent inflows into spot exchange-traded funds and increased staking activity reducing selling pressure, according to Lee.

For Bitmine, the link is direct. Each 1% rise in ether’s price adds roughly $100 million to the value of its holdings. A sustained rebound in crypto could support its balance sheet and stock.

A stubborn inflation gauge stayed hot in February, even before Iran war gas spike

Cha Eun-woo Apologizes for 13 Billion Won Tax Burden After Paying Massive Bill Amid Fan Backlash

Stablecoins Emerge as Financial Infrastructure, but Banks Remain Cautious: S&P Report

-

NewsBeat7 days ago

NewsBeat7 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business7 days ago

Business7 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Spanx – Corporette.com

-

Business5 days ago

Business5 days agoExpert Picks for Every Need

-

Business4 days ago

Business4 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports5 days ago

Sports5 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Tech2 days ago

Tech2 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business4 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Fashion3 days ago

Fashion3 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Fashion2 days ago

Fashion2 days agoLet’s Discuss: DEI in 2026

-

Politics6 days ago

Wings Over Scotland | The quality of mercy

-

Business5 days ago

Business5 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Fashion7 days ago

Fashion7 days agoStatement Sunglasses: The Accessory Shaping Modern Fashion

-

Crypto World1 day ago

Crypto World1 day agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Politics7 days ago

Politics7 days agoEast Jerusalem Palestinian families eviction orders

-

Fashion7 days ago

Fashion7 days agoCoffee Break: Santa Croce Tote

-

Fashion7 days ago

Fashion7 days agoFor Love & Lemons’ Spring 2026 Line is for the Romantics

-

Politics6 days ago

Politics6 days agoWhy so many children are now classified as ‘disabled’

-

Politics7 days ago

Politics7 days agoNuclear rockets, moon bases and NASA’s Mars plan

-

Tech6 days ago

Tech6 days agoThe Threadless Ball Screw Never Took Off, But Don’t Write It Off

You must be logged in to post a comment Login