Crypto World

Would a Ripple IPO actually move XRP?

The assumption is simple: Ripple goes public, XRP moons. The reality is that Ripple equity and the XRP token are different assets, and the channels connecting them are weaker than the hype suggests.

Summary

- Ripple remains private with no S-1 on file, but a $750 million buyback fixed its valuation near $50 billion and private secondary shares have surged to about $136.90, keeping IPO speculation loud.

- Ripple equity and the XRP token are legally separate: owning XRP gives no claim on the company, and a public listing would not hand shareholders or token holders any automatic link between the two.

- The plausible transmission channels are sentiment, Ripple’s escrow and sell behavior, institutional validation, and value accrual, and each is weaker or more two-sided than the “IPO equals XRP moon” story assumes.

- There is a real counter-case that an IPO could pull capital away from XRP, by giving investors who want Ripple exposure a way to buy the stock instead of the token.

- The evidence so far is mixed: XRP briefly re-coupled to Ripple’s rising private valuation, yet the token is still down about 26% on the year, which points to weak, not strong, transmission.

The reflex in the XRP community is automatic. Ripple goes public, the story goes, and XRP rockets alongside it. The logic feels obvious, because Ripple and XRP are wrapped together in the same brand, the same headlines, and the same decade of shared history. But an initial public offering sells shares in a company, and XRP is a token that confers no ownership of that company.

Whether a Ripple listing would actually move the token is not a matter of sentiment or loyalty. It is a question of mechanism: through what channels, if any, would value flow from a Ripple equity event into the XRP price? This piece examines those channels one by one, and finds them thinner than the hype implies. The XRP holder payout question has already become a separate community obsession, but the XRP holder payout question is not the same as a price-transmission mechanism.

The starting point: Ripple equity and XRP are different assets

Everything begins with a distinction the excitement tends to blur. Ripple Labs is a private company. XRP is a digital asset that trades on public exchanges. There is no mechanism that entitles an XRP holder to Ripple shares, dividends, or any slice of the company’s profits, and a public listing would not create one.

If Ripple lists tomorrow, an XRP holder owns exactly what they owned the day before: a token, not a piece of the business. The one concrete link runs the other direction. Ripple is itself one of the largest holders of XRP, with tens of billions of tokens held in escrow that it releases on a schedule and uses, in part, to fund operations. So the company’s relationship to the token is that of a giant holder and periodic seller, not a value conduit that passes equity gains down to token holders.

That asymmetry matters for the whole analysis. When people say an IPO would help XRP, they are really claiming that something about Ripple becoming public would change demand for, or supply of, the token. The rest of this piece tests each version of that claim. Until then, Ripple equity and XRP should be treated as related but legally separate assets, not two versions of the same exposure.

Channel one: sentiment and attention

The first and most immediate channel is psychological. An IPO would be a media event, a wave of coverage, analyst notes, and credibility that reframes Ripple from a litigation-scarred crypto firm into a public company vetted by underwriters and public markets. In a market where attention is a real driver of price, that halo could spill onto XRP, lifting the token on narrative even without any mechanical connection. That is the channel the community understands instinctively, because XRP has always traded partly on Ripple headlines.

There is some evidence this channel is live. When Ripple’s private secondary shares surged, one analysis linked the move to XRP briefly re-coupling with the company’s rising valuation, as the market started treating the private-share price near $136.90 as a fundamental signal for the token. That is the sentiment channel working in real time: a Ripple equity data point moving XRP through association rather than mechanics. It is also why where XRP could go from here depends partly on whether traders treat corporate news as a catalyst or just another temporary headline.

The limit is that sentiment is fickle and shallow. It can lift a token into an event and drop it just as fast afterward, and it does not build the sustained demand that holds a price up. A narrative bump around an IPO is plausible. A durable re-rating on sentiment alone is not, which is why this channel, while real, is the weakest foundation for a lasting move.

Channel two: Ripple’s escrow and sell behavior

The most underappreciated channel runs through Ripple’s own balance sheet. Because Ripple holds a vast XRP escrow and sells tokens to help fund itself, anything that changes the company’s need to sell XRP changes the supply hitting the market. This is where an IPO could actually matter mechanically. A successful listing would raise cash and give Ripple a public currency, its own stock, to fund acquisitions and operations.

A cash-rich, publicly funded Ripple might lean less on programmatic XRP sales, easing a source of sell pressure that has weighed on the token for years. That is a genuine, if indirect, bullish path. Less selling from the single largest holder is a supply-side positive that does not depend on sentiment. It is the most concrete way an IPO could help XRP.

The two-sided catch is disclosure. Going public subjects Ripple to far heavier reporting requirements, which means the escrow, the sales, and the token’s role in Ripple’s finances would face new scrutiny from public-market investors and regulators. Greater transparency could reassure the market, or it could surface uncomfortable details about how much the company depends on token sales, which would cut the other way. The escrow channel is the strongest mechanical link, but its direction is not guaranteed.

Channel three: institutional access and validation

The third channel is legitimacy. A public Ripple would sit inside the regulated financial system in a way it does not today, and that validation could radiate outward to the whole XRP ecosystem. The backdrop already leans this way: XRP was recognized as a commodity in March, and seven spot XRP exchange-traded funds are trading with roughly $1.43 billion in cumulative inflows. A high-profile Ripple listing would add another layer of institutional acceptance, potentially making allocators more comfortable holding XRP through regulated products.

The argument is that validation compounds. Each step that moves XRP from contested asset toward accepted infrastructure lowers the barrier for the next institution, and a Ripple IPO would be a large step. In a world where the token already has ETF access, a public parent company strengthens the case that the ecosystem is durable. That is also why XRP’s regulatory status matters more than the IPO hype itself: institutions care less about community excitement than about whether the asset can be held cleanly under durable rules.

The weakness is that validation of the company is not the same as demand for the token. Institutions can conclude that Ripple is a fine investment and express that view by buying the stock, which does nothing for XRP. Legitimacy is a soft tailwind, helpful at the margin, but it does not force anyone to buy the token. For a durable move, validation has to become measurable token demand, not just a better story around the issuer.

Channel four: the value-accrual problem

This is the channel that breaks the simple story, and it is the most important. For an IPO to lift XRP durably, Ripple’s commercial success has to translate into demand for the token. But Ripple’s business and XRP’s value are only loosely coupled. Many of Ripple’s bank and payment partners use its software without touching XRP at all, and the company earns revenue from services, licensing, and acquisitions that do not route through the token.

Ripple can thrive as a company while XRP stagnates, because the token’s value depends on settlement usage and demand for XRP itself, instead of on Ripple’s profit and loss. This value-accrual gap explained is the reason a Ripple IPO is not the guaranteed catalyst holders imagine. An IPO rewards equity holders for the company’s success. It does not, by itself, create the on-chain demand that would lift the token.

Unless a listing changes how much XRP is actually used to move value, the mechanical link from Ripple’s public-market performance to the XRP price is faint. The token needs its own demand story, and the IPO does not write one. It may make Ripple more visible, more credible, and more valuable. None of that automatically makes XRP more scarce or more necessary.

The counter-case: an IPO could hurt XRP

The overlooked possibility is that a Ripple listing works against the token. For years, buying XRP was one of the only ways for a public investor to express a view on Ripple’s success. An IPO removes that constraint by offering the pure play: if you want exposure to Ripple, you buy the stock, which actually owns the business, the revenue, and the growth. The token, which owns none of that, becomes the inferior vehicle for a Ripple bet.

That substitution could siphon capital and attention away from XRP toward the equity. Some of the speculative demand that flowed into the token as a Ripple proxy would rationally rotate into shares once shares exist. In this reading, the IPO does not transmit value to XRP at all. It competes with it.

The very event the community treats as the catalyst could turn out to be a drain, redirecting the Ripple trade into a security that leaves the token behind. That does not mean XRP must fall on a Ripple IPO. It means the direction is not obvious, because the listing creates both a halo effect and a substitute asset. The market would have to decide whether XRP remains the best way to trade Ripple’s ecosystem once Ripple stock exists.

What the evidence shows so far

The cleanest test available is how XRP has behaved as Ripple’s private valuation has climbed. The answer is telling. Ripple’s secondary shares surged to about $136.90 and its valuation was fixed near $50 billion, and while XRP did briefly re-couple to that move on sentiment, the token still trades near $1, down roughly 26% on the year. If the transmission were strong, a 376% surge in Ripple’s private-share price should have dragged XRP sharply higher.

It did not. The token acknowledged the news and kept falling with the broader market. That is the empirical verdict: transmission exists, but it is weak. Ripple getting more valuable has not made XRP more valuable in any durable way, which is exactly what the value-accrual analysis predicts.

An actual IPO would be a bigger event than a private-share revaluation, so the sentiment bump could be larger. But the underlying mechanics that limited the private-market spillover would still apply to a public one. The stock would price Ripple’s business, while XRP would still need regulatory clarity, ETF flows, settlement usage, and broader market support. The link is real enough for traders to chase, but not strong enough to treat as automatic.

What would actually move XRP

If the IPO is a weak lever, what is a strong one? The catalysts that genuinely drive XRP are the ones that change token demand or supply directly. Regulatory outcomes rank first: whether crypto market-structure legislation codifies XRP’s status cleanly, which affects how freely institutions can hold it. ETF flows rank second, because sustained inflows into the seven XRP funds are real, measurable demand for the token.

Settlement usage ranks third: whether XRP is actually used to move value at scale, against the escrow supply that keeps entering the market. That is where XRP fits in settlement becomes more important than the IPO narrative. XRP needs recurring use as a bridge asset or liquidity tool, not just Ripple’s name in public-market headlines. And the direction of Bitcoin and the broader market ranks alongside all of them, since XRP rarely fights the tape.

Against those, a Ripple IPO sits at the edge of the picture. It could add a sentiment bump, it could ease Ripple’s XRP selling, and it could burnish the ecosystem’s legitimacy. Each is a real but modest channel, and at least one plausible effect points the wrong way. The honest conclusion is that a Ripple IPO would be a meaningful corporate event that most likely moves XRP far less than the community expects, and possibly not in the direction they assume.

The Coinbase and Circle precedent

The clearest way to test the transmission question is to look at crypto-adjacent companies that already trade publicly, because they show what happens when a company and the tokens around it are separated on public markets. Coinbase is the obvious case. Its stock gives investors exposure to the exchange’s revenue, which rises and falls with trading volume, but owning the stock is not the same as owning the assets that trade on it. When crypto rallies, Coinbase revenue tends to rise, so there is a loose correlation, yet the stock and the broader token market frequently move apart, because the equity is priced on the business and the tokens are priced on their own supply and demand.

Circle offers a sharper version of the lesson. Circle issues the USDC stablecoin, but USDC is a dollar-pegged token that does not float, so Circle equity captures the value of the issuing business, the reserves, the yield, the growth, while the token itself is designed to stay at a dollar. The company can be worth a great deal while the token it issues, by construction, accrues none of that equity value. That is the extreme illustration of the point: a token and its issuer’s stock can be almost entirely decoupled.

XRP sits somewhere between these cases. It is not a dollar peg, so it can appreciate, but it is also not an equity claim on Ripple, so it does not capture the company’s growth the way shares would. Even when Ripple-linked infrastructure appears in real capital-markets events, such as stablecoin settlement using RLUSD on the XRP Ledger, the immediate value still tends to accrue to the rails, the issuer, or the company before it accrues to XRP itself. The precedent from public crypto companies is that the market prices the business and the token separately, and a listing that rewards the equity does not automatically reward the associated token.

A Ripple IPO would most likely follow the same script, with the stock absorbing the value of the business while XRP continues to trade on its own drivers. That does not make the IPO irrelevant. It makes it indirect. The market would finally have a clean way to buy Ripple, and that could clarify how much demand for XRP was really token demand versus company-proxy demand all along.

What a realistic IPO scenario looks like for XRP

It helps to walk through how an actual Ripple listing would probably play out for the token, stage by stage, because the timeline reveals where the modest effects concentrate. In the announcement phase, when Ripple confirms an S-1 or a date, expect a sentiment spike: headlines, community excitement, and a short-term bid in XRP as traders position for the event. This is the sentiment channel firing, and it could produce a sharp but shallow move that fades as the news is absorbed.

In the run-up to the listing, attention would build, and XRP could trade with elevated volatility as speculation swings between the “IPO lifts XRP” and “IPO competes with XRP” theses. Some capital that had been using XRP as a Ripple proxy might already begin rotating toward the anticipated equity, capping the token’s upside even amid the excitement. The listing itself would be an equity event: shares price, the stock trades, and the value of Ripple’s business gets marked by the market. XRP would react mostly to the tone, a strong debut lifting sentiment, a weak one dampening it, rather than to any mechanical flow.

In the aftermath, the durable question resurfaces: does anything about a public Ripple change token demand or supply? If a cash-rich Ripple eases its XRP selling, that supply relief could support the token over time, the most concrete lasting benefit. If investors conclude the stock is the better Ripple bet, capital could keep rotating out of XRP into shares. The realistic net is a sentiment-driven spike around the event that mostly fades, a possible modest supply-side benefit if Ripple sells less XRP, and an ongoing competitive pull from the equity.

That is a meaningful corporate story with a muted and two-sided token effect, which is a long way from the moonshot the community pictures. The IPO could matter. It just would not erase the legal separation between the company and the token. XRP would still need its own demand engine.

Frequently asked questions

Does owning XRP give you a stake in Ripple?

No. XRP is a digital token that trades on public exchanges and confers no ownership of Ripple Labs, no shares, no dividends, and no claim on the company’s profits. Ripple the company and XRP the token are legally separate. A Ripple IPO would sell shares in the business, and holding XRP would give you no automatic right to those shares or their gains.

Has Ripple actually filed to go public?

Not as of late June 2026. Ripple remains private with no S-1 on file and no confirmed date, and executives have repeatedly downplayed the urgency of a listing. The speculation is driven by signals such as a $750 million share buyback that fixed the valuation near $50 billion and a surge in private secondary shares to about $136.90, not by an official filing. That distinction matters because IPO speculation can move sentiment long before any legal filing exists.

Could a Ripple IPO raise the XRP price?

It could, through weak and indirect channels. A listing could lift XRP on sentiment, could ease sell pressure if a cash-rich public Ripple relies less on XRP sales, and could add legitimacy to the ecosystem. None of these is a mechanical guarantee, and the evidence so far shows only faint transmission from Ripple’s rising valuation to the token. The stronger catalysts are still regulatory clarity, ETF flows, and actual XRP settlement usage.

How could an IPO hurt XRP?

By offering a substitute. An IPO would let investors who want Ripple exposure buy the stock, which actually owns the business, instead of the token, which does not. Some speculative capital that flowed into XRP as a Ripple proxy could rotate into the equity once it exists, redirecting demand away from the token rather than toward it. That is why a Ripple IPO is not automatically bullish for XRP.

What is the value-accrual problem?

It is the gap between Ripple’s success and XRP’s value. Many Ripple partners use its software without touching XRP, and much of its revenue does not route through the token. So Ripple can prosper as a company while XRP stagnates, because the token’s value depends on settlement usage and its own demand, not on Ripple’s profit and loss. This is why an IPO is not a guaranteed catalyst.

Did XRP move when Ripple’s private valuation rose?

Briefly and weakly. When Ripple’s secondary shares surged to about $136.90, one analysis linked it to XRP re-coupling with the valuation on sentiment. But XRP still trades near $1, down about 26% on the year, so a large rise in Ripple’s private-share price did not drag the token durably higher. That points to weak transmission between the two.

What actually drives the XRP price?

The strongest drivers are regulatory clarity on XRP’s status, sustained ETF inflows into the seven spot XRP funds, real settlement usage against the escrow supply, and the direction of Bitcoin and the broader market. These change token demand or supply directly. A Ripple IPO sits at the edge of that list, a modest and two-sided factor instead of a primary catalyst. The event may affect attention, but attention is not the same as recurring demand.

Would Ripple sell more or less XRP after an IPO?

Possibly less, which would be the most concrete bullish channel. A listing would raise cash and give Ripple a public stock to fund operations and deals, potentially reducing its need to sell XRP from escrow. The offsetting risk is that going public brings heavier disclosure of the escrow and token sales, which could reassure or unsettle the market depending on what it reveals. The direction depends on what the filings show and whether Ripple actually changes its sell behavior.

Disclaimer: This article is for information purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency prices are highly volatile, and corporate plans such as an IPO are speculative and can change. Nothing here is a recommendation to buy or sell any asset. Always do your own research and consider consulting a licensed professional before making financial decisions. Figures are accurate as of July 1, 2026, and will change.

Edel said it detected and contained the exploit, then paused all of its version-one contracts, which remain frozen, and warned users not to interact with them.

The team added it had traced the attacker’s transactions and is coordinating with exchanges, and that it has offered the attacker a whitehat settlement, a deal that lets a hacker return most of the funds in exchange for a fee and no legal pursuit, within a set window.

No depositor will take a loss, Edel noted, with the team absorbing the bad debt and restoring balances one for one. It is deploying a version two with a redesigned pricing setup meant to block this kind of manipulation, and promised a full technical breakdown to follow.

While the amount is small, the method sits in one of DeFi’s most persistent categories of exploit.

Manipulating the price a protocol reads, rather than breaking into it, ranks as the second most common smart-contract vulnerability in the OWASP Smart Contract Top 10 vulnerabilities for 2025, and security researchers at CertiK describe oracle price manipulation as one of the field’s most common attack vectors.

Alongside cross-chain bridges, which produced the year’s largest single thefts, including the $292 million drained from Kelp DAO in April, price manipulation is where much of the money keeps going, and in most of these, the code works as written.

Key Takeaways

- Shares of SanDisk tumbled 9.44% during Tuesday’s session even as Bank of America issued an optimistic price target increase

- Bank of America elevated its SNDK price objective from $2,100 to $2,500 while reiterating its Buy recommendation

- BofA’s Wamsi Mohan anticipates average selling prices could surge as much as 35%, while bit growth may increase 13% sequentially

- The memory maker has soared 800% in 2024 and an eye-popping 4,755% over the trailing year, reaching a $323 billion market capitalization

- Valuation concerns include a forward price-to-earnings ratio of 33 — exceeding both Nvidia and Micron — alongside troubling technical indicators

SanDisk shares experienced a steep decline on Tuesday, surrendering 9.44% of their value during the trading session. The selloff occurred paradoxically on the very day that Bank of America Securities announced an upward revision to its price target, moving from $2,100 to $2,500.

Bank of America’s equity analyst Wamsi Mohan maintained his Buy recommendation on the shares. His optimistic thesis centers on the persistent mismatch between NAND flash memory supply and demand, a condition he anticipates will persist through 2027.

Mohan’s research indicates SanDisk’s average selling prices could experience gains of up to 35%. Additionally, he projects bit growth — representing the total volume of memory units delivered — will expand by 13% on a sequential quarter basis.

Using these assumptions as a foundation, Bank of America now forecasts that SanDisk will report $9.1 billion in revenue for the June quarter alongside earnings per share of $37.01. These projections exceed the Street’s current consensus estimates of $8.35 billion in revenue and $34.26 in EPS.

For the subsequent quarter, BofA’s model anticipates revenue reaching $11.5 billion with EPS climbing to $48.55.

Multi-Year NAND Supply Deals Enhance Earnings Predictability

A critical element supporting Mohan’s optimistic outlook involves SanDisk’s strategic emphasis on securing long-term NAND supply agreements, referred to as NBMs. These multi-year commitments guarantee future revenue streams and provide greater clarity for investors modeling future profitability.

Bank of America anticipates widespread adoption of these contractual arrangements among cloud infrastructure providers and enterprise clients. The investment bank also highlighted that these agreements are designed to preserve gross margin levels within SanDisk’s established target parameters.

This strategic pivot has contributed significantly to SanDisk’s extraordinary market performance. The stock has skyrocketed 800% since the beginning of the year and an astonishing 4,755% over the past twelve months. This explosive growth has transformed what began as a Western Digital spinoff into a company valued at $323 billion.

The bullish sentiment extends beyond Bank of America. Mizuho Securities increased its target from $1,825 to $2,200. Cantor Fitzgerald established an even higher objective at $2,900. Susquehanna Financial Group represents the most aggressive bull case with a $3,250 price target.

The analyst community’s consensus rating stands at Strong Buy — featuring 14 Buy ratings, two Hold ratings, and zero Sell recommendations over the most recent three-month period. The mean price target across all analysts sits at $1,979.38, suggesting approximately 3% downside from present trading levels.

Growing Concerns About Valuation and Market Dynamics

Notwithstanding the widespread analyst enthusiasm, multiple risk factors deserve consideration — and Tuesday’s sharp decline serves as a cautionary reminder.

SanDisk’s forward price-to-earnings multiple has expanded to 33 times, surpassing Nvidia at 22 times and Micron Technology at 18 times. This valuation premium has begun attracting scrutiny from market participants.

Supply-side dynamics present another concern. Elevated memory pricing could incentivize rival manufacturers including Micron, Kingston Technology, and Kioxia Holdings to accelerate production capacity, which would ultimately exert downward pressure on pricing.

From a technical analysis perspective, the weekly chart reveals a bearish divergence in the Relative Strength Index. The RSI has been declining even as the stock price has continued advancing — a formation that frequently precedes price corrections.

The equity currently trades at $2,238, substantially above its 50-day moving average of $1,458.

Bitcoin has climbed back above $60,000 after Federal Reserve Chair Kevin Warsh declined to signal the direction of future interest rate decisions during an ECB policy discussion.

Summary

- Bitcoin rebounded above $60,000 after Fed Chair Kevin Warsh declined to signal the future path of interest rates.

- CME FedWatch shows markets still expect rates to remain unchanged in July despite lingering inflation concerns.

- Polymarket continues to price in a chance of a 2026 rate hike, while Morgan Stanley expects rates to stay on hold this year.

According to data from crypto.news, Bitcoin (BTC) traded around $60,175 at the time of writing after rebounding about 3% from an intraday low below the key $58,000 level. The move followed comments from Warsh, who again avoided offering forward guidance on monetary policy while reiterating that future decisions will depend on incoming economic data.

Bitcoin rebounds as Warsh avoids policy signals

Speaking during an ECB Forum panel, Warsh declined to say whether the Federal Reserve would raise interest rates at the July Federal Open Market Committee meeting. Instead, he repeated the position he adopted after taking office that the central bank would not pre-commit to future policy moves and would continue responding to economic data as it becomes available.

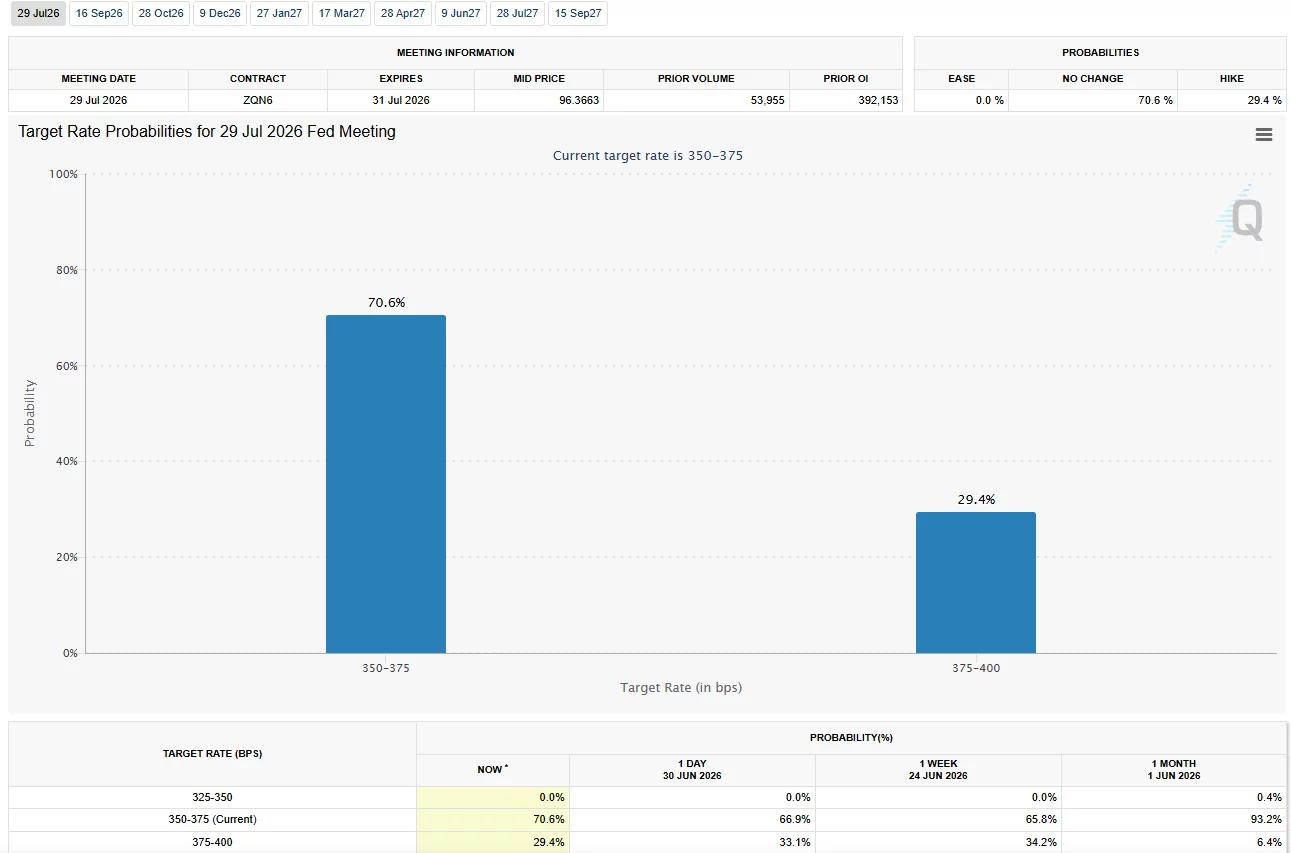

His remarks came as traders largely continued to expect no change in interest rates later this month. According to CME FedWatch data, markets currently assign a 70.6% probability that the Federal Reserve will leave rates unchanged at the July FOMC meeting.

Warsh also addressed inflation, saying expectations had declined during the first four weeks of the recent period despite concerns tied to the U.S.-Iran conflict. He added that inflation risks had eased while reaffirming the Federal Reserve’s commitment to returning inflation to its 2% target.

As crypto.news reported after the June FOMC meeting, Warsh also left rates unchanged at that gathering. Bitcoin fell to around $65,430 following the decision, while Ethereum traded near $1,770. The Federal Reserve’s updated projections at the time showed that nine policymakers expected at least one rate increase before the end of the year.

Those projections have continued to shape market expectations even after Warsh reiterated at the ECB Forum that future policy decisions would depend on incoming economic data.

Rate hike expectations continue to pressure crypto

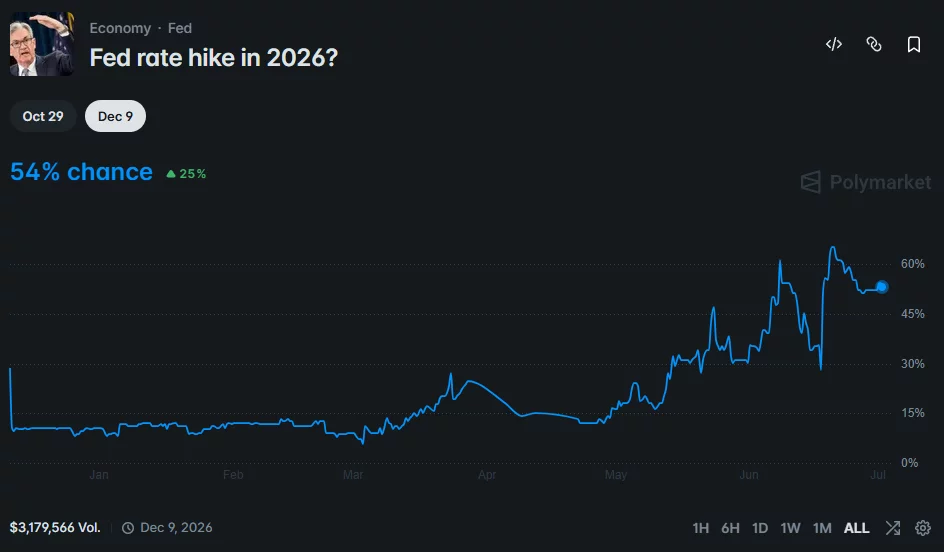

Although traders see little chance of a July rate increase, expectations for additional tightening later this year have not disappeared. According to Polymarket data, there is currently a 54% probability that the Federal Reserve will raise interest rates before the end of 2026.

Higher borrowing costs have generally remained a headwind for cryptocurrencies because elevated interest rates tend to support demand for cash and short-term fixed-income assets over riskier investments such as Bitcoin.

Separate reporting by crypto.news also noted that Morgan Stanley expects the Federal Reserve to keep rates unchanged through the rest of the year. The bank nevertheless warned that rate hikes could return if inflation remains persistent or if the unemployment rate falls further.

Outside monetary policy, another source of uncertainty for Bitcoin has come from corporate supply. As previously reported by crypto.news, the possibility that Strategy could sell as much as $1.25 billion worth of Bitcoin has remained one factor contributing to selling pressure in the market.

Political attention has also stayed on Federal Reserve policy. Before Warsh became chair, President Donald Trump repeatedly called for lower interest rates. After the June decision to keep rates unchanged, however, Trump responded without strong criticism and continued to praise the new Fed chair while receiving no timeline for future rate cuts.

The downgrade marks a sharp reversal from Citi’s previous outlook, which assumed passage of U.S. digital asset market structure legislation would spur adoption among financial advisors and traditional investors. The bank now believes that timeline has slipped, leaving the market without a meaningful catalyst.

Saunders said ETF flows continue to be the main force behind crypto prices, with recent demand turning negative as investors pulled back from risk.

According to the bank’s analyst, sentiment has also been hurt by concerns that digital asset treasury (DAT) companies could become net sellers of bitcoin. Recent corporate actions by Strategy amplified those fears despite involving relatively modest BTC sales.

The report noted that bitcoin and ether both remain below key technical levels, including their 200-day moving averages, while speculative capital has shifted toward AI-related investments.

The bank’s revised forecasts assume flat ETF flows in its base case. In its bull case, stronger retail and institutional adoption lifts bitcoin to $108,000 and ether to $2,932. Its bear case, based on recessionary macro conditions and continued ETF outflows, sees BTC falling to $53,000 and ETH to $1,094.

While the bank’s equity strategists have become more constructive on U.S. stocks, providing some support through crypto’s equity correlation, the report said that positive macro factors are insufficient to offset weakening flows.

A new independent non-profit, Ethereum Institutional, has launched with the goal of accelerating institutional adoption of Ethereum, its layer-2 networks and the broader ecosystem.

The organization is led by David Walsh, Marius Smith and Matthew Dawson. Walsh previously led the Ethereum Foundation’s enterprise efforts, while the organization said its leadership brings experience spanning institutional engagement, capital markets and Ethereum ecosystem development. It said its mission is to provide institutions with a neutral, independent point of contact as they evaluate Ethereum for tokenization, stablecoins and other onchain financial infrastructure.

In announcing the initiative on X, Ethereum Institutional said institutions need “a credible, independent front door” to the Ethereum ecosystem. While Ethereum’s neutrality is one of its defining strengths, the group argued, that neutrality has often left enterprises without a clear organization to engage as they make long-term infrastructure decisions.

The launch comes as the Ethereum Foundation continues to narrow its role to stewarding the core protocol, with ecosystem participants increasingly spinning up independent organizations focused on specific areas such as business development, institutional outreach and developer support. The shift follows broader changes at the foundation, including leadership restructuring and longstanding community calls for greater transparency.

Investment bank Standard Chartered has initiated coverage of Morpho, calling the lending protocol a dual-play on decentralized finance (DeFi) that combines a lending market with infrastructure for onchain banks and asset managers.

The bank has a $60 price target for MORPHO by the end of 2030, implying roughly 33x upside from its current price. This would see the token outperform both bitcoin and ether (ETH) over the same period.

MORPHO was more than 13% higher over 24 hours, trading around $2.13 at publication time.

“Given its status as one of the largest DeFi lending protocols and its comfortable financial position (it just raised $175 million in VC funding), we think Morpho can scale to meet the expanding base of assets deployed in DeFi,” wrote Geoff Kendrick, head of digital assets research at Standard Chartered, in the Wednesday report.

Decentralized finance has rebounded sharply over the past year as institutional interest in tokenized real-world assets and onchain lending accelerated. Lending protocols have benefited from rising stablecoin adoption and renewed demand for crypto credit, while infrastructure providers that enable asset managers and financial institutions to deploy capital onchain have emerged as one of the sector’s fastest-growing segments.

The European Union has completed its MiCA transition, leaving Tether’s $186 billion USDT without a compliant route onto regulated crypto exchanges across the bloc from July 1, 2026.

Summary

- EU MiCA rules have removed USDT from regulated exchanges after Tether chose not to seek authorization.

- Circle’s USDC and EURC are now the leading MiCA-compliant stablecoins across licensed EU platforms.

- Tether remains active through Hadron-powered partners as global USDT markets adjust to regional regulations.

According to the European Union’s Markets in Crypto-Assets (MiCA) framework, the transition period has now ended, requiring regulated crypto platforms to support only compliant stablecoins.

As a result, MiCA-licensed exchanges including Coinbase, Kraken, and Crypto.com have removed USDT trading for European users, ending the stablecoin’s presence on regulated order books despite its position as the world’s largest stablecoin by market capitalization.

Tether rejected MiCA authorization over reserve requirements

Rather than applying for authorization as an electronic money token (EMT), Tether decided not to pursue MiCA approval. CEO Paolo Ardoino previously argued that the regulation’s reserve rules create systemic risk because issuers must keep at least 60% of reserves in European bank deposits.

Tether’s reserve strategy instead relies heavily on U.S. Treasury securities and other globally diversified assets, making the MiCA framework incompatible with its existing model.

The company’s withdrawal from the European market had been unfolding well before the final deadline. Tether discontinued its euro-pegged EURT stablecoin in 2024, while exchange support for USDT gradually disappeared over the following months.

Coinbase Europe delisted the token in December 2024, Crypto.com followed in January 2025, Binance restricted European USDT trading pairs in March 2025, and Kraken first moved users to a sell-only model before later ending support entirely.

Data on MiCA adoption also illustrates how selective the licensing process has been. Before the July 1 deadline, only 244 MiCA licenses had been issued across the European Union, while several crypto companies opted to expand operations from jurisdictions such as Dubai instead of seeking authorization under the bloc’s new framework.

USDC strengthens its position while Tether keeps European partnerships

As Tether stepped away from the licensing process, Circle took the opposite approach by securing an Electronic Money Institution (EMI) license in France. The authorization can be passported across all 27 European Union member states, allowing both USDC and EURC to operate under MiCA. Their compliant status has made them the primary dollar- and euro-backed stablecoins available on licensed European trading platforms.

The transition has also forced liquidity providers to adjust. According to the report, market makers that previously quoted USDT pairs have begun rebuilding liquidity around USDC because regulated exchanges can no longer offer USDT trading within the European Union.

Even so, Tether has not completely exited the region’s digital asset ecosystem. Companies including StablR and Oobit have launched MiCA-compliant stablecoins, EURR and USDR, using Tether’s Hadron tokenization platform, allowing the company to maintain technology partnerships without issuing a MiCA-approved stablecoin itself.

Elsewhere in Europe, 37 banks including BNP Paribas and ING are developing a common euro stablecoin known as Qivalis, according to the report. The project seeks to provide a regulated euro-denominated alternative as financial institutions increase their participation in the digital asset market.

Recent exchange data also points to changing user behavior beyond Europe. As previously reported by crypto.news, Bybit and OKX disclosed higher user Bitcoin holdings in their latest Proof of Reserves reports, while USDT balances declined on both platforms, suggesting some users are holding less stablecoin liquidity.

In a separate crypto.news report, India’s USDT premium climbed above 8.5% after enforcement action against crypto remittance firms disrupted domestic supplies of the stablecoin, highlighting how regional regulations continue to reshape USDT markets in different ways.

Key Highlights

-

Security Matters shares advanced 6.90% following increased interest in its verification technology.

-

The company’s digital passport system connects plastic materials with authenticated documentation.

-

Stricter U.S. recycling regulations are driving demand for robust verification infrastructure.

-

Security Matters focuses on supply-chain transparency, regulatory compliance, and material authentication.

-

Authenticated recycled plastics could achieve competitive parity with virgin materials.

Security Matters (SMX) stock advanced 6.90% to reach $14.33 following the opening bell, driven by heightened interest in its recycling authentication technology. The stock experienced early gains, softened briefly, then held steady near peak levels. This movement came as investors focused on the company’s material verification platform and evolving U.S. recycling regulations.

SMX (Security Matters) Public Limited Company, SMX

Security Matters Advances Recycling Authentication Technology

SMX has centered its business model on verification-driven recycling rather than general environmental messaging. The company’s Digital Material Passport Platform creates connections between physical plastics and protected digital documentation. Consequently, plastic materials can carry information about source, composition, handling history, lifecycle phase, and regulatory alignment.

The firm employs molecular tagging to establish permanent material identification. This methodology enables brands, producers, and oversight bodies to authenticate recycled plastic throughout every phase. Recycled components can progress through distribution networks supported by enhanced documentation and transparent oversight.

Growing media coverage has elevated Security Matters’ visibility within the recycling technology sector. Numerous prominent publications featured its contributions to plastic authentication and data-driven environmental solutions. The organization’s primary emphasis continues to center on regulatory alignment, supply-chain transparency, and quantifiable recycling results.

Tightening U.S. Regulations Drive Verification System Adoption

The American recycling sector has transitioned toward more rigorous verification requirements. Individual states persistently broaden regulations covering recycled content mandates, collection programs, and producer responsibility frameworks. Consequently, organizations require more definitive documentation when reporting or substantiating environmental commitments.

Corporations encounter intensified oversight as regulatory authorities examine sustainability assertions more thoroughly. Producers require validated information before establishing pricing, purchasing, funding, or disclosing recycled material usage. Municipal governments demand stronger confirmation that collected plastics return to beneficial applications.

SMX addresses this requirement through authentication systems, passport documentation, and compliance-oriented analytics. The platform facilitates recycled-content validation, custody chain records, origin tracking, and lifecycle reporting. Collectively, these capabilities transform scattered recycling assertions into organized datasets.

Security Matters Connects Material Documentation With Market Value

Security Matters’ operational reach extends nationally and touches multiple recycling system components. The organization integrates physical marking, digital documentation, compliance analytics, and marketplace functionality. Accordingly, the platform can facilitate sourcing, capital access, plastic credit systems, and brand authentication.

The firm additionally advances its Plastic Cycle Token and recycled plastic registry framework. These instruments seek to align validated recycling operations with quantifiable financial value. Subsequently, certified materials can compete more effectively against virgin feedstock.

SMX has articulated this transformation through its Age of Parity initiative. The initiative contends that authenticated recycled plastic can emerge as a viable economic alternative. As supply constraints and regulatory pressure intensify, Security Matters presents its verification platform as essential recycling infrastructure.

“Large groups of large companies coordinate poorly, have misaligned incentives, slow things down and rarely create the space for real durable innovation,” he wrote.

Test for the consortium model

That skepticism is shared by Lorenzo Valente, director of digital asset research at ARK Invest, who noted that crypto has seen several consortium-backed stablecoin initiatives over the years, including Meta’s Diem project and Paxos-led Global Dollar Network.

“Every year we get our consortium-style initiative around a stablecoin,” Valente wrote in an X post. “While the set of players here is obviously potent, I remain highly skeptical any of these initiatives can hit scale.”

He said Open Standard’s biggest challenge may be coordinating more than 140 participants with competing interests.

“A consortium of hundreds of rivals has no precedent for working,” he said. “The pace of decision-making across competitors is going to be glacial.”

Valente likened the model to decentralized autonomous organizations, or DAOs, whose governance structures often struggled to make timely decisions.

“‘Owned by everyone’ almost always means accountable to no one,” he said. “I’d bet on the two operators who can ship unilaterally over a committee that has to ask hundreds of rivals for permission.”

He also questioned whether large banks, payment networks and technology companies would remain committed if the project encounters regulatory pressure. Circle and Tether, he noted, have spent years building global regulatory infrastructure and licensing, while a consortium could find it harder to stay aligned if conditions become more challenging.

Cuts of beef are displayed at Handy Market on May 14, 2026 in Burbank, California.

Justin Sullivan | Getty Images

With oil and gas prices falling in the wake of the detente between the U.S. and Iran, prediction market traders now think inflation has peaked.

Speculators on prediction market platform Kalshi think there’s only a 28% chance that headline inflation this year peaks above 4.2%, which was the annual rate of increase in the Consumer Price Index in May.

The next CPI report, measuring inflation in June, is due for release by the Bureau of Labor Statistics (BLS) on July 14.

The contract on Kalshi asks if traders think CPI will deliver a reading above various percentages in 2026. Contracts are resolved using the CPI data released each month by the BLS.

The inflation outlook has eased primarily due to recent declines in its main driver: energy prices. After shooting higher after the start of the U.S.-Iran war jn late February and the subsequent closure of the Strait of Hormuz, gas and oil prices have started to retreat after the partial reopening of the waterway.

Average national gasoline prices as of Wednesday stood at $3.84, according to AAA, down from more than $4.50 at their peak. That reflects weaker U.S. crude oil prices, which have fallen below $70 per barrel for the first time since the war began.

Energy prices in May accounted for 60% of CPI’s month-over-month increase.

Now the decline in gas prices is leading Kalshi traders to think that CPI in June will show prices falling by 0.2% compared with May, in-line with Wall Street consensus estimates.

Danny Glover Reveals He Has Alzheimer’s Disease in Emotional Interview Just Weeks Before His 80th Birthday

Prices of tokenized Google stock inflated 7,700% in rare DeFi lending exploit

Why traditional email security is no longer enough

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics5 days ago

Politics5 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World2 days ago

Crypto World2 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics6 days ago

Politics6 days agoPotential 2028er World Cup attendee leaderboard

-

Business5 days ago

Business5 days agoAsia stock markets slide as tech shares slump

-

News Videos3 days ago

News Videos3 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech6 days ago

Tech6 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World4 days ago

Crypto World4 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business2 days ago

Business2 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World5 days ago

Crypto World5 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports5 days ago

Sports5 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World6 days ago

Crypto World6 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech4 days ago

Tech4 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech4 days ago

Tech4 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World5 days ago

Hyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World5 days ago

Crypto World5 days agoRTX holders must register wallets before token distribution begins

-

Crypto World7 days ago

Crypto World7 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

-

Tech2 days ago

Tech2 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Sports4 hours ago

Sports4 hours agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

You must be logged in to post a comment Login