Crypto World

Zcash price prediction 2026-2030: the privacy renaissance test

Zcash (ZEC) hit $642.18 on May 9, 2026, marking the peak of a 650-1,000% rally from 2024 lows that crowned it the largest privacy coin by market cap, overtaking Monero. The catalysts driving this performance are different in kind from previous Zcash cycles. Grayscale filed Form S-3 to convert its Zcash Trust into the first US spot privacy coin ETF (ticker ZCSH) on NYSE Arca on May 12, 2026. The SEC closed its nearly two-year investigation into the Zcash Foundation on January 15, 2026, without enforcement action, removing the regulatory overhang that suppressed institutional participation for years.

Summary

- Zcash’s May 2026 rally to $642 was tied to Grayscale’s ETF filing, SEC clearance, Multicoin Capital’s position, and shielded pool growth.

- The bull case sees ZEC reaching $800 to $1,800 by 2030 if ETF approval, institutional demand, and FCMP++ deployment align.

- The bear case puts ZEC at $180 to $350 by 2030 if ETF rejection, regulatory pressure, or privacy coin competition weighs on adoption.

Multicoin Capital disclosed a “significant position” in (ZEC) on May 5, accumulated quietly since February 2024. Approximately 30% of the ZEC supply is now locked in shielded pools, up from 8% in 2024. The November 2024 halving cut inflation from 4% to 2% annually. The FCMP++ upgrade, promising 300% throughput improvement, is targeted for 2026 deployment. The “Privacy is Normal” narrative has shifted institutional perception from privacy coins as evasion tools to privacy coins as essential infrastructure for compliant commercial confidentiality. ZEC is currently trading around $522 after cooling from the May peak.

The honest read is Zcash is one of the more interesting setups in crypto for 2026-2030: real structural catalysts (ETF filing, shielded pool growth, FCMP++ upgrade, SEC clearance), real institutional interest (Grayscale, Multicoin Capital, growing whale accumulation), real risks (ETF approval uncertainty, governance disputes, competitive pressure from Monero and Railgun). This piece walks through actual mechanics, the bull case ($800-$1,800 by 2030), the base case ($400-$700), and the bear case ($180-$350), with the specific variables determining outcome.

Why Zcash is at $522 right now

The current Zcash price reflects a narrative shift that competitors keep missing. Most price prediction articles treat ZEC as just another privacy coin with generic supply-and-demand dynamics. The actual story is more specific and analytically important.

The starting point: ZEC traded around $20 in early 2024, having declined steadily from 2021 highs as the broader crypto market shifted away from privacy coins amid regulatory pressure. Multiple major exchanges delisted privacy coins through 2023-2024 in response to MiCA’s pending deployment in the EU and broader regulatory caution. The Zcash narrative was widely considered structurally damaged.

The rally that produced the current $522 price (and the May peak of $642) wasn’t speculation. It was driven by five specific catalysts arriving in sequence:

The November 2024 halving cut block rewards in half, reducing ZEC inflation from approximately 4% annually to approximately 2%. This is a big deal for a 21-million-supply asset where shielded pool accumulation removes supply from liquid markets. The halving plus shielded growth created the supply dynamics for the subsequent rally.

The shielded pool grew from approximately 8% of total supply in 2024 to approximately 30% of total supply by mid-2026. This is approximately 4.5 million ZEC moved from transparent (liquid) to shielded (illiquid for trading purposes) pools. The shielded pool growth represents both ideological commitment to privacy use and supply reduction in liquid markets. Most analyses treat shielded pool growth as a usage metric. It’s also a supply absorption mechanism comparable in effect to corporate Bitcoin treasury accumulation.

The SEC closed its nearly two-year investigation into the Zcash Foundation on January 15, 2026 without recommending enforcement action. The foundation had received a subpoena in August 2023 related to crypto asset offerings inquiries. The investigation closure removed a regulatory overhang that had suppressed institutional participation for years.

The immediate market response was a 3+ percent rally with ZEC briefly exceeding $427. The longer-term impact was institutional investors gaining confidence that Zcash specifically would not face SEC enforcement.

Multicoin Capital’s position disclosure on May 5, 2026 was the catalyst that triggered the May rally to $642. Co-founder and Managing Partner Tushar Jain disclosed via X that the firm had built a “significant position” in ZEC, accumulated quietly since February 2024. Jain framed the thesis as “a return to the cypherpunk ideals crypto was founded on” and argued that growing government scrutiny of visible crypto holdings makes Bitcoin’s transparent balances increasingly problematic for sophisticated holders. The Multicoin disclosure gave institutional validation that compounded the broader privacy narrative.

Grayscale’s Form S-3 filing on May 12, 2026 to convert its Zcash Trust into a spot ETF (ticker ZCSH) on NYSE Arca represents the first US spot privacy coin ETF filing in history. The trust currently holds approximately 391,103 ZEC ($99.4 million as of March 31, 2026 quarter-end). If approved, the ETF would provide regulated institutional access to ZEC similar to how spot Bitcoin and Ethereum ETFs changed those assets’ accessibility. The filing alone validated the institutional thesis even before approval is decided.

The combined effect of these five catalysts arriving in sequence produced the rally from approximately $20 in early 2024 to the May 2026 peak of $642 (a 30x+ move). The post-peak consolidation to current $522 levels reflects normal post-rally profit-taking and futures market unwinding (futures open interest fell 30% from peak to approximately $1.05 billion) rather than a fundamental thesis breakdown.

What the rally is fundamentally signaling: the “Privacy is Normal” narrative has gained genuine institutional traction. The same regulatory environment that pressured privacy coins in 2023-2024 (MiCA deployment, SEC enforcement concerns) has evolved through 2025-2026 (SEC enforcement pullback under Atkins, CLARITY Act framework, institutional adoption of crypto generally). Privacy infrastructure that was institutionally radioactive 18 months ago is becoming institutionally palatable for specific use cases (corporate confidentiality, regulatory compliance with selective disclosure, protected commercial transactions).

The bull case: $800-$1,800 by 2030

The bull case for Zcash requires specific catalyst conditions and represents the scenario where the “Privacy is Normal” narrative achieves full institutional acceptance.

The ETF approval catalyst: Grayscale’s ZCSH ETF approval is the single most important bull case variable. The pathway: SEC review completes by Q3 2026, exchange listing approval secured, ETF begins trading with $500M-$2B in initial inflows over the first 12 months. The precedent from Bitcoin and Ethereum ETF launches suggests this level of institutional capital flowing into a smaller asset like ZEC could produce a significant price impact. With a circulating supply of approximately 16 million ZEC and 30% already in shielded pools (effectively illiquid), the liquid float available for ETF accumulation is constrained.

The shielded pool supply absorption: continued growth from 30% to 40-50% of total supply removes another 1.5-3 million ZEC from liquid markets over the bull scenario timeframe. Plus ETF accumulation, the supply reduction would be significant. The bull case assumes shielded pool growth accelerates as FCMP++ deployment improves throughput and reduces the costs of shielded transactions.

The FCMP++ deployment: the upgrade targeting 300% throughput improvement for shielded transactions, planned for 2026 deployment, would address one of Zcash’s persistent technical limitations. Reduced shielded transaction costs would enable broader use cases (institutional settlements, commercial transactions, DeFi integrations) currently constrained by performance. A successful FCMP++ deployment would unlock the institutional use cases the privacy narrative requires.

The privacy narrative expansion: the bull case assumes the broader “Privacy is Normal” narrative gains traction beyond just crypto-native investors. Specific developments that would support this: major corporations adopting privacy infrastructure for commercial transactions, traditional finance integrating privacy-preserving technologies, regulators developing frameworks distinguishing compliant privacy from illicit use, and growing public awareness of financial surveillance concerns driving demand for privacy options.

The competitive positioning: Zcash bull case assumes it holds its position as the institutionally-preferred privacy coin, while Monero and Railgun serve different (less institutional) use cases. The differentiation: Zcash offers selective disclosure (institutions can prove compliance while keeping commercial details private), Monero offers mandatory privacy (which institutional investors find harder to navigate), and Railgun offers DeFi-native privacy (which serves different use cases). Zcash’s institutional positioning would be reinforced by ETF approval and Grayscale’s institutional distribution.

The Midnight integration: the Midnight Cardano privacy companion chain (covered in the Midnight long read) creates additional institutional infrastructure leveraging privacy primitives. While Midnight is technically separate from Zcash, the broader privacy ecosystem maturation benefits all institutional privacy infrastructure, including Zcash. Successful Midnight deployment with major partners (Google Cloud, MoneyGram) validates the broader privacy infrastructure investment thesis.

If all bull case conditions materialize, the price targets are:

2026 year-end: $700-1,000

2027 year-end: $850-1,300

2028 year-end: $1,000-1,500

2029 year-end: $1,200-1,700

2030 year-end: $800-1,800

The wide range at 2030 reflects uncertainty about how aggressively institutional adoption scales and whether broader market dynamics support sustained altcoin appreciation. The lower end of the bull range ($800) represents successful ETF launch with moderate institutional adoption. The upper end ($1,800) requires the privacy narrative achieving mainstream institutional acceptance comparable to how Bitcoin achieved mainstream institutional acceptance over 2024-2025.

The base case: $400-$700 by 2030

The base case assumes mixed outcomes across the catalyst variables, with Zcash maintaining institutional relevance but not achieving big adoption.

The ETF approval scenario: in the base case, Grayscale’s ZCSH ETF is eventually approved but the approval is delayed beyond initial Q3 2026 expectations. The SEC review process extends into 2027 or 2028. When approved, initial inflows are more modest ($200-500M rather than the bull case $500M-2B). The institutional adoption pathway opens but the impact is gradual rather than big.

The shielded pool growth scenario: continued moderate growth from 30% to 35-40% of total supply. The growth provides ongoing supply absorption but not the dramatic supply shock the bull case envisions. The shielded pool serves both privacy users and structural HODLers without achieving the broader commercial adoption the bull case requires.

The FCMP++ deployment outcome: the upgrade deploys successfully but the throughput improvement is more modest than projected, or deployment is delayed. The technical capability improvement happens but doesn’t unlock the dramatic institutional use case expansion the bull case requires.

The competitive landscape: Zcash holds its position as the largest institutional-grade privacy coin but faces growing competition from Monero (for non-institutional privacy users), Railgun (for DeFi-native privacy), and emerging privacy infrastructure (Midnight, Aztec, others). The competitive pressure limits Zcash’s pricing power without fundamentally undermining its position.

The regulatory environment: the broader crypto regulatory environment continues evolving under CLARITY Act deployment, but specific regulatory clarity for privacy coins stays ambiguous. Exchange delistings continue in some jurisdictions while listings expand in others. The mixed regulatory picture limits institutional adoption acceleration without forcing a Zcash-specific crackdown.

The “Privacy is Normal” narrative: the narrative continues developing but doesn’t achieve the mainstream institutional acceptance the bull case requires. Specific use cases (compliant corporate confidentiality, regulatory selective disclosure) gain traction in niche applications without becoming default institutional infrastructure. The narrative supports continued ZEC relevance without driving big growth.

Base case targets:

2026 year-end: $500-700

2027 year-end: $450-650

2028 year-end: $400-600

2029 year-end: $400-650

2030 year-end: $400-700

The base case represents moderate price appreciation from current levels plus periodic volatility around specific catalyst developments. The structural floor is meaningfully higher than pre-2026 levels because the SEC investigation closure and institutional accumulation have shifted the asset’s investor base toward longer-term holders.

The bear case: $180-$350 by 2030

The bear case requires either specific Zcash setbacks or broader privacy coin headwinds disrupting the thesis.

The ETF rejection scenario: the SEC rejects Grayscale’s ZCSH application, citing concerns about privacy coin oversight, market manipulation potential, or insufficient surveillance-sharing agreements. The rejection would close the institutional pathway that the bull case requires. Without ETF access, institutional accumulation would be limited to direct purchases through more cumbersome processes, reducing the capital pool available for ZEC investment.

The regulatory crackdown scenario: privacy coins broadly face renewed regulatory pressure as governments respond to growing crypto adoption. Specific risks: CLARITY Act deployment includes explicit privacy coin restrictions, EU MiCA enforcement targeting Zcash beyond current scope, US regulatory action restricting exchange listings, or major jurisdictions deploying privacy coin bans. Any of these would directly impact ZEC accessibility and adoption.

The exchange delisting cascade: in 2023-2024, multiple major exchanges delisted privacy coins amid regulatory uncertainty. A renewed cascade triggered by new regulatory pressure or specific privacy coin incidents could reduce ZEC trading liquidity and accessibility. The bear case assumes this dynamic returns and intensifies, with exchanges including some currently listing ZEC choosing to delist.

The competitive disruption: Monero, Railgun, or emerging privacy infrastructure captures the use cases Zcash currently serves. Monero retains hardcore privacy users who view selective disclosure as a compromise. Railgun captures DeFi-native privacy demand. New entrants (potentially Midnight, Aztec, others) capture institutional use cases through different technical approaches. Zcash’s positioning between institutional and crypto-native privacy could fail to capture either segment effectively.

The shielded pool stagnation: shielded pool growth slows or reverses as users find shielded transaction costs prohibitive or move to alternative privacy infrastructure. Without continued shielded pool expansion, the supply absorption mechanism weakens. ZEC becomes more liquid in markets, removing one of the key supply-side supports for current price levels.

The FCMP++ failure: the upgrade encounters technical problems, is significantly delayed, or fails to deliver projected throughput improvements. The technical limitations that have constrained Zcash’s broader adoption would persist, limiting institutional use case expansion.

The governance and foundation issues: Zcash has faced periodic governance disputes between the foundation and broader community. A major governance crisis or foundation funding shortfall could disrupt development momentum and institutional confidence. The Q1 2026 operating expenses of approximately $817K and treasury of $36.7M provide near-term stability but represent ongoing burn rates requiring sustainable funding mechanisms.

Bear case targets:

2026 year-end: $250-400

2027 year-end: $200-350

2028 year-end: $180-320

2029 year-end: $180-340

2030 year-end: $180-350

The bear case represents significant downside from current levels but assumes ZEC retains some institutional and crypto-native investor base. Complete failure scenarios (price below $100) would require more severe disruption than even the bear case envisions.

The five variables that determine outcome

Five specific variables determine which scenario materializes. Readers can monitor these directly rather than relying on price action alone.

Variable 1: Grayscale ZCSH ETF approval status.

The single most important variable. Approval timeline expectations: Q3 2026 (bull case), late 2026-2027 (base case), 2028+ or rejection (bear case).

Monitor: SEC docket updates for ZCSH filing, Grayscale public statements on approval expectations, related crypto ETF approval patterns (Solana ETF dynamics provide useful precedent), and CFTC-SEC coordination on privacy coin oversight.

Variable 2: Shielded pool supply percentage.

Currently 30% of total ZEC supply. Bull case requires growth to 40-50%. Base case assumes 35-40%. Bear case assumes stagnation or decline.

Monitor: Zcash shielded pool dashboard, FCMP++ deployment status (which would reduce shielded transaction costs and likely accelerate growth), and institutional accumulation patterns (institutions may shield holdings for both privacy and supply absorption purposes).

Variable 3: FCMP++ deployment timeline and success.

Targeted for 2026 deployment, promising 300% throughput improvement. Successful deployment unlocks institutional use cases requiring better performance.

Monitor: Zcash development updates, testnet performance data, deployment timeline announcements, and post-deployment shielded transaction volume metrics.

Variable 4: Privacy coin regulatory environment.

The broader regulatory framework for privacy coins continues evolving.

Specific developments to monitor: CLARITY Act deployment details affecting privacy coins, MiCA enforcement actions in EU, US Treasury or SEC privacy coin guidance, exchange listing/delisting patterns, and major jurisdictional decisions (UK, Singapore, Japan privacy coin policies).

Variable 5: Competitive positioning vs Monero, Railgun, and emerging privacy infrastructure.

ZEC’s bull case assumes it captures institutional use cases, while Monero serves hardcore privacy users and Railgun serves DeFi-native applications.

Monitor: Monero adoption metrics, Railgun TVL and transaction volume, emerging privacy projects (Midnight, Aztec) development progress, and institutional preference signals (which privacy infrastructure major institutions choose for specific use cases).

The five variables interact in important ways. ETF approval would likely accelerate shielded pool growth as institutions accumulate. FCMP++ deployment success would strengthen competitive positioning vs Monero. Regulatory clarity favoring compliant privacy would benefit ZEC specifically. Successful competitive positioning would justify higher institutional valuations. Readers monitoring all five variables get a more complete picture than focusing on price action alone.

What this means for Zcash holders and traders

For current ZEC holders, the practical implication is the thesis has shifted from speculative to fundamentally supported. The May 2026 rally to $642 wasn’t driven primarily by speculation. It was driven by specific institutional catalysts (Grayscale filing, Multicoin Capital position, and SEC investigation closure). The current $522 level reflects post-rally consolidation rather than thesis breakdown. The five variables framework provides a way to evaluate whether holding makes sense based on which scenario is materializing.

For potential ZEC buyers, the practical implication is current entry levels are significantly higher than pre-2026 levels, but the institutional thesis is more developed than at any previous point. The risk-reward calculation depends on the assessment of whether ETF approval and continued institutional adoption will materialize. The five variables provide objective signals to monitor rather than relying on price-based timing decisions.

For traders specifically, the practical implication is ZEC’s volatility profile combines structural support (institutional accumulation, shielded pool growth) with catalyst-driven moves (ETF approval news, regulatory developments, competitor dynamics). The support provides a downside cushion that purely speculative privacy coins lack. The catalyst-driven moves create asymmetric upside opportunities around specific events.

For institutional investors evaluating privacy coin allocation, the practical implication is that ZEC offers a more conventional risk-reward profile than alternative privacy coins. Selective disclosure capability addresses regulatory compliance concerns that mandatory privacy (Monero) makes difficult to navigate. Institutional infrastructure (Grayscale Trust, eventual ETF) provides accessibility that DeFi-native privacy (Railgun) lacks. The institutional positioning is the structural differentiation.

For the broader privacy coin ecosystem, the practical implication is that Zcash’s success or failure influences institutional perception of privacy infrastructure generally. ETF approval would validate institutional privacy investment broadly. ETF rejection would reinforce institutional caution. The outcome affects not just ZEC price but also Monero, Railgun, Midnight, and other privacy infrastructure development trajectories.

Connection to broader market dynamics

Zcash’s price story connects to several broader narratives we have previous covered on crypto.news.

The institutional-driven crypto dynamics explain why ZEC has performed strongly during a period of broad retail capitulation. Multicoin Capital’s institutional accumulation, Grayscale’s ETF filing, and the SEC investigation closure are all institutional dynamics that drive price action independently of retail attention.

The CLARITY Act framework provides regulatory clarity that distinguishes compliant privacy infrastructure from illicit use. Zcash’s selective disclosure capability fits this framework better than mandatory privacy alternatives. The framework’s deployment timeline (2027-2028 compliance deadlines) creates ongoing regulatory development that benefits ZEC’s positioning.

The Midnight Cardano privacy companion chain represents a broader institutional infrastructure for privacy primitives. While technically separate, Midnight’s success with Google Cloud and MoneyGram partnerships validates the institutional thesis for privacy infrastructure generally, which benefits ZEC by extension.

The Zcash shielded pool growth is one of the structural variables on which this prediction depends. The continued shielded pool expansion is both a usage metric and a supply absorption mechanism that supports ZEC price levels.

The Grayscale Zcash ETF dynamics represent the institutional pathway that determines whether the bull case materializes. The ETF approval pathway, fee structures, distribution mechanisms, and competitive dynamics all affect ZEC’s institutional adoption trajectory.

The honest bottom line

Zcash spent five years as a structurally damaged privacy coin. Then four things happened in twelve months: the SEC closed its Foundation probe with no enforcement, Multicoin Capital disclosed a quiet 15-month accumulation, Grayscale filed the first US privacy-coin ETF, and the shielded pool quietly grew from 8% to 30% of supply. The May rally to $642 wasn’t speculation. It was the market pricing in a thesis that no longer requires hand-waving.

The catalysts that drove the May 2026 rally are real: Grayscale’s ZCSH ETF filing, Multicoin Capital’s accumulated position disclosure, the SEC investigation closure, shielded pool growth to 30% of supply, the November 2024 halving’s inflation reduction, and the broader “Privacy is Normal” institutional narrative shift.

The main risks are real and material: ETF approval uncertainty, broader privacy coin regulatory pressure, exchange delisting risks, competitive pressure from Monero and Railgun, governance and foundation funding sustainability, and FCMP++ deployment execution risk.

The 2030 price range across scenarios is wide: $180-1,800, depending on how the structural variables resolve. The base case ($400-700) represents the most probable outcome assuming mixed catalyst outcomes. The bull case ($800-1,800) requires sustained institutional adoption plus ETF approval. The bear case ($180-350) assumes adverse regulatory or competitive developments.

ZEC holders own a different asset than they owned 18 months ago, and that’s the part that matters. Pre-2026 ZEC was a speculative privacy coin with limited institutional access. Post-Grayscale filing ZEC is an institutional privacy coin candidate with a clear regulatory pathway. The shift is significant even if specific outcomes (ETF approval, adoption magnitude) remain uncertain.

The ETF approval question is the most important catalyst variable. Approval would likely produce significant price appreciation through institutional capital flows colliding with constrained liquid supply (70% of ZEC is not in shielded pools, but a substantial portion of that is held by long-term holders rather than actively traded). Rejection would limit but not remove the institutional thesis.

The competitive positioning vs Monero and Railgun is the most important strategic variable. Zcash’s selective disclosure capability is fundamentally differentiated for institutional use cases. The competitive dynamics determine whether ZEC captures the institutional privacy market or whether different infrastructure (potentially Midnight, potentially Aztec, potentially others) becomes the institutional standard.

The shielded pool growth is the most important supply variable. Continued growth removes ZEC from liquid markets, supporting price levels. The pool’s growth from 8% to 30% over 2024-2026 represents supply absorption. Future growth depends on FCMP++ deployment, improving transaction economics.

For 2026 specifically, expect ZEC to continue trading in elevated ranges relative to historical levels, with significant volatility around ETF approval news, regulatory developments, and broader privacy coin dynamics. The $400-700 range represents the support given current institutional positioning. The upside ($700-1,000) depends on ETF approval timing. The downside ($300-450) depends on adverse regulatory or competitive developments.

For 2027-2030, the structural variables compound. Sustained execution across ETF launch, shielded pool growth, FCMP++ deployment, and competitive positioning produces the bull case trajectory. Deterioration across these variables produces the bear case. The base case assumes mixed outcomes producing moderate price appreciation.

The Zcash story is ultimately about whether privacy infrastructure can be institutionally palatable in 2026 and beyond. The early evidence is strongly positive. The structural catalysts are real. The institutional capital is positioning. The remaining variables are largely external (regulatory developments, competitive dynamics) and partially within Zcash’s control (development execution, governance stability, ecosystem development).

The “Privacy is Normal” narrative is being tested in real-time. Zcash is the asset whose price action provides the clearest signal of whether the narrative succeeds. The next 18-24 months will likely determine whether privacy infrastructure achieves institutional acceptance or remains a specialized crypto-native use case.

Frequently asked questions

- What is driving Zcash’s 2026 rally?

Five specific catalysts: the SEC closing its investigation of the Zcash Foundation on January 15, 2026 without enforcement action; Grayscale filing Form S-3 on May 12, 2026 for the first US spot privacy coin ETF (ZCSH); Multicoin Capital’s May 5 disclosure of a “significant position” accumulated since February 2024; shielded pool growth to 30% of total supply; and the November 2024 halving cutting inflation from 4 to 2%.

- Will Grayscale’s Zcash ETF actually get approved?

The approval is uncertain but the filing itself is a big deal. Form S-3 filings for crypto ETFs have a track record of approval over time (Bitcoin and Ethereum ETFs followed similar pathways). The SEC’s January 2026 closure of the Zcash Foundation investigation suggests reduced regulatory friction. Potential approval timeline: Q3 2026 (bull case) to 2028+ (bear case). Approval would likely produce $500M-$2B in initial institutional inflows.

- Can Zcash reach $1,000 by 2030?

$1,000 is within the bull case range ($800-$1,800 by 2030). Required conditions: ETF approval with substantial institutional adoption, FCMP++ successful deployment, shielded pool growth to 40-50% of supply, sustained “Privacy is Normal” narrative driving institutional acceptance, and Zcash keeping position as the largest institutional-grade privacy coin. The base case for 2030 is $400-$700.

- What is the FCMP++ upgrade and why does it matter?

FCMP++ is a planned Zcash upgrade targeting 300% throughput improvement for shielded transactions. The upgrade matters because shielded transaction performance has been a persistent limitation that has constrained Zcash’s broader institutional adoption. Successful deployment would reduce shielded transaction costs and enable broader use cases (institutional settlements, commercial transactions, DeFi integrations). Deployment is targeted for 2026.

- How does Zcash compare to Monero in 2026?

Zcash has overtaken Monero as the largest privacy coin by market cap, having risen 650-1,000% from 2024 lows. The differentiation: Zcash offers selective disclosure (institutions can prove compliance while keeping commercial details private), Monero offers mandatory privacy (which institutional investors find harder to navigate). Zcash is positioned for institutional adoption (ETF filing, Grayscale Trust), Monero stays positioned for crypto-native privacy users. Different use cases, different investor bases.

- What are the main risks to the Zcash thesis?

Five primary risks: (1) Grayscale ZCSH ETF rejection or extended delay, (2) broader privacy coin regulatory crackdown under CLARITY Act or MiCA, (3) exchange delisting cascade similar to 2023-2024, (4) competitive disruption from Monero, Railgun, or emerging privacy infrastructure (Midnight, Aztec), (5) FCMP++ deployment failure or significant delay, (6) Zcash governance or foundation funding sustainability issues.

- Should I buy Zcash now or wait for a pullback?

This piece does not provide investment advice. The structural analysis suggests ZEC’s current price reflects substantial institutional thesis development, but the asset carries specific risks that buyers should evaluate against their risk tolerance. The five variables framework provides objective signals to monitor. Current $522 level reflects post-rally consolidation from $642 May peak rather than thesis breakdown. ETF approval timing is the most important near-term catalyst variable.

- How does the CLARITY Act affect Zcash?

The CLARITY Act framework distinguishes compliant privacy infrastructure from illicit use, which structurally favors Zcash’s selective disclosure capability over mandatory privacy alternatives. The Act’s deployment through 2027-2028 will determine specific regulatory clarity for privacy coins. Zcash’s positioning between institutional adoption and crypto-native privacy use makes CLARITY deployment generally favorable, though specific provisions targeting privacy coins could create either bullish or bearish dynamics depending on how the framework develops.

This article is for informational purposes and does not constitute financial or investment advice. Cryptocurrency markets are highly volatile, and price predictions are inherently speculative. The figures and analysis described reflect data available as of late May 2026. Always do your own research and consult with qualified financial professionals before making investment decisions.

Crypto World

CME Group to Sue CFTC Over Perpetual Futures Approval, Citing Dodd-Frank Swaps Definition

CME Group plans to sue the Commodity Futures Trading Commission over the agency's approval of crypto perpetual futures, the world's largest derivatives exchange operator announced Wednesday evening on CNBC. Outgoing Chief Executive Terrence Duffy said the case would be filed as soon as Thursday and… Read the full story at The Defiant

At the start of June, the two largest cryptocurrencies by market capitalization tumbled to their lowest levels in years. However, many analysts believe the cycle bottoms have not occurred yet.

The big question now appears to be whether Bitcoin (BTC) or Ethereum (ETH) will find its floor first, and here’s the take of one popular market observer.

Is ETH First in Line?

X user Ted argued that the second-biggest cryptocurrency is more likely to bottom before the industry’s undisputed leader. He claimed that most of the downside liquidity has been taken out, projecting a plunge to $1,300-$1,400.

“But after that, upside liquidity will start to look more interesting,” he added.

Shortly after, Ted noted ETH’s drop below the critical $1,700 mark and warned that the asset could post a further 5-6% decline if it doesn’t reclaim this level.

There are plenty of other analysts who believe the worst for Ethereum is ahead. Ali Martinez said the asset is breaking down from its channel and is trading below the 200-hour SMA. That said, he expects a drop toward $1,580.

Niels also claimed that ETH hasn’t bottomed for this cycle, predicting a crash to as low as $1,200 sometime this year. At the same time, they see the current price level as a great buying opportunity.

How About BTC?

Earlier in June, the primary cryptocurrency plummeted to nearly $59,000 for the first time since late 2024. Ted, like many other industry participants, thinks this was not the bottom.

He spotted a massive liquidity cluster around $50,000-$60,000, describing it as the same zone with large BTC buy orders on exchanges. With that in mind, Ted said that the price will likely sink to $50K “with a possible wick.”

X users bee and Crypto Lens have also made bearish forecasts. The former opined that BTC is “on the verge of the final flush,” expecting a drop to $51,000-$52,000, while the latter envisioned a downturn to $43,000 by August this year.

However, it’s not all doom and gloom. Certain factors, such as the declining amount of BTC held on exchanges, suggest a rebound is also possible. As CryptoPotato reported, the figure recently dipped to a six-year low, meaning that investors have abandoned centralized platforms in favor of self-custody, thereby reducing immediate selling pressure.

Meanwhile, whales scooped up more than 30,000 BTC in a week: a strong signal that they are positioning for the next rally and something that could encourage retail investors to jump on the bandwagon, too.

The post Bitcoin (BTC) or Ethereum (ETH): Which Will Bottom First? appeared first on CryptoPotato.

Ethereum may be heading toward a funding crisis that could begin to emerge within the next three to nine months, according to former Ethereum Foundation contributor Trent Van Epps.

In a recent article on X, Van Epps, who recently ended his five-year stint at EF, said the risk is not simply the result of a temporary funding gap but originates from deeper structural changes taking place across the ecosystem.

Funding Crunch

Van Epps spoke about EF’s long-standing philosophy of “Subtraction,” a strategy that aims to gradually reduce the Foundation’s influence and encourage the broader Ethereum community to take on a larger role in supporting the network.

While he said the approach has been successful in conveying that the EF does not want to remain Ethereum’s sole center of power, he believes it has been less effective at ensuring other institutions step in to fill the gaps left behind.

According to Van Epps, the Ethereum Foundation still occupies a unique position within the ecosystem due to factors such as its reputation, historical role in leading the protocol, connection to Ethereum co-founder Vitalik Buterin, ownership of major communication channels and trademarks, as well as its long-standing support of core developers and researchers.

However, he added that one of the Foundation’s most important resources, its treasury, is becoming increasingly constrained.

The EF has spent much of its ETH holdings over the last decade helping bootstrap Ethereum’s growth and has already begun reducing spending to preserve remaining funds. He highlighted the Foundation’s treasury plan announced in June 2025, which outlined a gradual reduction in annual spending from 15% to a 5% endowment-style level by 2030.

Van Epps also pointed to the expiration of Ethereum’s Client Incentive Program (CIP) in April 2026. The four-year initiative provided funding to client teams through staking rewards, and no replacement program has been announced so far.

Shrinking Resources

Based on conversations across Ethereum’s core development community, he said these developments have created a real risk that funding pressures could start building over the coming months. He estimated that maintaining Ethereum’s current development capacity requires roughly $30 million per year to support client teams, researchers, and coordination efforts across the ecosystem.

Without stable funding, Van Epps warned that Ethereum could lose contributors who have accumulated years of critical expertise, which makes it harder to tackle major challenges such as scaling the network and preparing for future threats like quantum computing. According to the former contributor, the consequences of underinvestment may not be immediately visible but could become apparent within the next 12 to 18 months, when reversing the damage would be significantly more difficult and expensive.

Van Epps believes the Ethereum Foundation is unlikely to remain the network’s primary steward over the next decade, as he echoed recent comments from Vitalik Buterin that the organization was never intended to serve as Ethereum’s permanent caretaker. He called for new institutions and sustainable funding mechanisms capable of supporting Ethereum’s long-term development and maintaining the shared resources the ecosystem depends on.

The post Ethereum’s Biggest Risk May Be a Funding Crunch, Former EF Contributor Warns appeared first on CryptoPotato.

Nikita Bier, head of product at X, targeted Meta workers with a public recruitment pitch this week. He promised to match or beat any corporate snack budget the company could offer.

Meta CTO Andrew Bosworth admitted on an internal call that employee morale is near its worst ever. The May 2026 layoffs cut 8,000 jobs. Meta also forced roughly 7,000 more workers into AI units, giving them little say in the transition.

X Sees an Opening in Meta’s Morale Problem

Bier announced open roles for web and data engineers and data scientists. He aimed the message directly at workers he described as “neglected.”

His pitch was a direct dig at Meta’s crisis response. Rather than leading with salary, he zeroed in on the snack budget. That was the same perk Meta had scrambled to expand after morale collapsed. He pledged X would match or exceed whatever Meta could offer.

Workers on internal forums described Meta’s culture as “dead and depressing.” The core issue runs deeper than office perks, however. Applied AI, a division formed in March, absorbed around 6,500 engineers and product managers with little input from those transferred. Some employees compared it to a labor camp.

Meanwhile, 2026 tech layoff odds on prediction market Polymarket sit at 67%, with Meta’s situation among the factors traders cite. The Meta job cuts wiped out roughly 10% of its workforce in a single round.

Bier is no stranger to weighing in on Meta. He previously defended Mark Zuckerberg after backlash over a whistleblower documentary trailer. That move showed a pattern of engaging publicly with debates around Meta’s leadership and culture.

The post Who Needs Salary? X’s Nikita Bier Is Poaching Meta Talent With Better Snacks appeared first on BeInCrypto.

Amazon Web Services on Monday turned on AI traffic monetization inside AWS WAF, letting any site behind Amazon CloudFront charge AI agents per request in stablecoins through Coinbase's x402 protocol. It is the first time a hyperscale cloud has wired onchain settlement directly into its… Read the full story at The Defiant

Crypto World

CLARITY Act Reaches Senate Floor With House Ready to Move Fast; Seven-Democrat Math Becomes the Gate

The Digital Asset Market Clarity Act sits on the Senate Legislative Calendar as Calendar No. 423, eligible for a floor vote at any time leadership chooses to schedule one. House Agriculture digital-assets subcommittee chair Dusty Johnson said Thursday the House will move fast on a companion if the… Read the full story at The Defiant

Reform UK leader Nigel Farage has been threatened with a referral to the UK’s parliamentary authorities after he allegedly under-declared a private jet donation from billionaire crypto investor Christopher Harborne.

The threat came from Labour Chair Anna Turley, who wrote to Farage claiming that the donation he declared doesn’t match the market rates of private jet flights.

Farage took the private jet to the Chagos Islands earlier this year, where he attempted to undermine a UK sovereignty deal. He originally declared Harborne’s donation as £12,500 ($16,500), but later adjusted it to £25,000 ($33,500).

Turley claims that the cost of hiring the jet, and the 23-hour duration of his flight, mean his trip should’ve cost anywhere between £189,000 ($250,000) and £529,000 ($700,000).

She told Farage, “If you fail to provide anything less than a full and accurate account, I will be obliged to raise the matter with the Parliamentary authorities.”

Farage lobbied the Bank of England on crypto regulation

Turley then went after the controversial right-wing politician again, reportedly referring him to a UK financial regulatory body.

In this case, during a private meeting in September 2025, he allegedly urged Bank of England Governor Andrew Bailey to shelve plans for a state-backed stablecoin dubbed “Britcoin.”

One month later, Farage said at the crypto event Zebu Live that he would be “prepared to go to prison” in order to stop Britcoin, describing the plans for a state-backed stablecoin as “total and utter horror.”

The introduction of a state-backed stablecoin would dilute the private stablecoin market and, in doing so, reduce the value of Harborne’s 12% stake in multi-billion-dollar stablecoin giant Tether.

Read more: Nigel Farage aide George Cottrell bets US war will last four more months

Harborne’s lawyers told the Guardian that the story contained “a number of unsupported insinuations, hallucinations, and conspiracy theories bearing no basis in reality.”

Harborne has altogether given Reform UK a whopping £25 million ($33 million). By September 2025, Harborne had already donated £19 million ($25 million).

Reform UK loses key local election

One particular £5 million sum from Harborne, which Farage kept a secret, has already led to parliamentary authorities investigating the Reform UK leader.

This gift was made weeks before Farage U-turned and decided to stand in the general election. He claims he didn’t have to declare the sum as it was a personal gift given to him for security reasons and Brexit campaigning.

Farage has also been facing pressure this week outside of crypto.

Newsletter Democracy For Sale reported on Tuesday that his personal firm, Thorn in the Side Ltd, was breaking British company law by failing to file a confirmation statement and verify Farage’s ID.

To top it off, a Reform UK candidate lost in a key UK local election yesterday to Labour MP and Manchester Mayor Andy Burnham.

Read more: Reform UK isn’t sharing crypto wallets with UK regulators, report

It’s believed that Burnham may challenge Sir Keir Starmer’s position as prime minister and spark a leadership contest.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

The CLARITY Act has entered another round of Senate negotiations, with Senate Agriculture Committee Chairman John Boozman saying that limited understanding of the bill among lawmakers remains one of the biggest obstacles to its progress.

Summary

- John Boozman says many senators still do not fully understand the CLARITY Act.

- David Nage estimates lawmakers and industry participants are 80%–85% aligned on the bill.

- Cynthia Lummis believes a Senate vote before the August recess is more likely than before July 4.

According to a report from Punchbowl News, senators met on Thursday, June 18, to discuss the next phase of work on the crypto market structure legislation. Much of the proposal falls under the jurisdiction of the Senate Agriculture Committee, placing the panel at the center of efforts to move the bill toward a floor vote.

Speaking after the meeting, Boozman said discussions were advancing but acknowledged that many lawmakers are still unfamiliar with the legislation. He stated that most members do not fully understand the bill, describing that knowledge gap as a challenge as negotiators attempt to build support across the Senate.

The comments arrive as congressional leaders face increasing pressure to resolve remaining issues before lawmakers leave Washington for the August recess. Several last-minute meetings have been scheduled as Senate offices continue working through outstanding provisions tied to digital asset regulation.

Senate support appears stronger than public debate suggests

While Boozman highlighted concerns about member awareness, separate discussions on Capitol Hill suggest that disagreements over the substance of the legislation may be narrower than they appear.

As previously reported by crypto.news, David Nage, managing director and portfolio manager at Arca, said conversations with Senate offices led him to conclude that lawmakers and industry participants are roughly 80% to 85% aligned on the core elements of the bill.

In Nage’s assessment, stablecoin yield provisions no longer rank among the most contentious issues, despite continued criticism from JPMorgan CEO Jamie Dimon. Instead, Nage said attention has increasingly turned toward ethics and conflict-of-interest rules governing government officials involved in crypto-related business activities.

Following discussions with congressional staff, Nage stated that lawmakers are largely debating how such restrictions should be implemented rather than whether they should exist. He described the remaining divide as a political and enforcement matter rather than a disagreement over digital asset market structure itself.

Under Nage’s base-case scenario, lawmakers would settle the ethics language and reconcile competing proposals in the coming weeks, allowing the legislation to reach the Senate floor after Congress returns from recess on July 13.

Senate timeline remains the key uncertainty

Despite growing optimism from some supporters, the expected timing of passage remains unsettled.

During a recent interview with FOX Business, Senator Bill Hagerty said he hopes Congress can complete work on the legislation before the July 4 recess. Hagerty argued that the measure would provide the regulatory certainty needed for the U.S. digital asset sector to expand domestically rather than abroad.

Earlier, White House crypto advisor Patrick Witt also expressed optimism that lawmakers could approve the bill by Independence Day.

Other lawmakers have pointed to a longer timeline. Senator Cynthia Lummis has said a Senate floor vote before the August recess appears more likely than passage before July 4. Lummis has also noted that the legislation includes $150 million in funding intended to combat illicit cryptocurrency activity.

Supporters of the proposal contend that the bill would define the responsibilities of the Securities and Exchange Commission and the Commodity Futures Trading Commission while establishing compliance standards for digital asset firms.

Lummis has further warned that if Congress fails to advance market structure legislation during the current legislative window, meaningful action on the issue could be postponed until 2030.

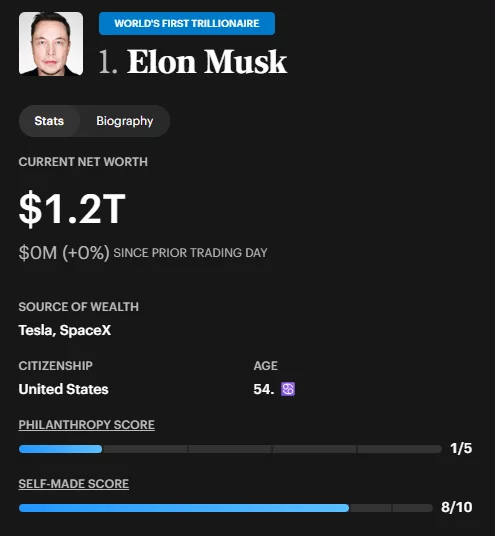

SpaceX’s blockbuster public debut has pushed Elon Musk’s net worth above $1 trillion while creating a new class of billionaires among the company’s earliest investors, executives, and institutional backers.

Summary

- Elon Musk’s fortune climbed above $1 trillion after SpaceX’s IPO, briefly surpassing Bitcoin’s market value.

- Early investors, including Valor Equity, Founders Fund, Alphabet, and Sequoia recorded tens of billions in gains.

- SpaceX executives and employees also benefited, while the company explores a potential $20 billion bond sale.

According to CNBC, SpaceX shares remained about 37% above their $135 IPO price even after retreating from post-listing highs, leaving the company with a market capitalization of roughly $2.43 trillion. The valuation surge briefly lifted SpaceX above Amazon and, for a short period, Microsoft, dramatically increasing the value of long-held stakes across its shareholder base.

Before the listing, crypto.news reported that retail investors rushed to secure allocations in the offering, with some reportedly seeking personal and bank loans as demand for shares far exceeded available supply. The scramble unfolded while SpaceX was preparing to enter public markets at a valuation of roughly $1.75 trillion.

For Musk, who controlled about 42% of SpaceX at the time of the offering, the gains were historic. Estimates cited by multiple reports place the value of his SpaceX holdings at more than $750 billion following the IPO. When combined with his interests in Tesla and xAI, several wealth trackers estimated Musk’s net worth briefly reached nearly $1.4 trillion on June 16 before falling back to roughly $1.2 trillion, making him the first person to surpass the trillion-dollar mark.

During the rally, Yahoo Finance data showed SpaceX shares reaching an intraday high of about $225.84 on June 16, pushing the company’s valuation close to $3 trillion. As crypto.news reported earlier, the surge briefly lifted the value of Musk’s holdings above Bitcoin’s market capitalization of roughly $1.31 trillion at the time.

The jump in wealth later drew political attention after Senator Elizabeth Warren argued that the financial system disproportionately rewards the wealthiest Americans while many households continue facing rising costs.

Early investors have emerged as the biggest winners

Among the largest beneficiaries is Antonio Gracias, founder of Valor Equity Partners and a longtime SpaceX board member. CNBC reported that Valor’s SpaceX stake is worth approximately $96.6 billion, although most of those holdings belong to the firm’s clients. Gracias, who has backed Musk’s ventures for years, has seen the value of his investment rise alongside SpaceX’s rapid growth.

Another major winner is Peter Thiel’s Founders Fund. The venture firm became SpaceX’s first institutional investor in 2008, investing while the company was recovering from multiple Falcon launch failures. According to investment records cited in reports following the IPO, Founders Fund invested roughly $600 million across several funding rounds and built a stake of around 3%, which is now worth more than $50 billion.

Alphabet has also recorded one of the largest gains. Google invested approximately $900 million in SpaceX alongside Fidelity in 2015, acquiring a stake that was later diluted to about 6%. Based on SpaceX’s post-IPO valuation, reports estimate Alphabet’s holding at roughly $132 billion, representing a return of nearly 147 times its original investment.

Several other investors also benefited from the listing. Reports indicate that Sequoia Capital’s roughly 1.5% stake has grown to more than $20 billion after investments totaling around $2 billion, while Kingdom Holding, controlled by Saudi Prince Alwaleed bin Talal, holds approximately 42.4 million shares valued at nearly $7 billion.

Executives and employees have shared in the windfall

Beyond institutional investors, the IPO has substantially increased the wealth of long-serving executives. CNBC estimates that SpaceX President and CEO Gwynne Shotwell holds a stake worth about $2.4 billion, making her one of the company’s largest individual shareholders.

Speaking to CNBC on the day of the IPO, Shotwell described her role as supporting Musk’s vision through operational execution while he focuses on strategy and engineering. Former SpaceX engineer Nathan Silvernail told CNBC that Shotwell has played a central role in managing customers, contracts, and daily business operations.

Chief Financial Officer Bret Johnsen has also joined the billionaire ranks. CNBC reported that the executive, who joined SpaceX in 2011 and oversees the company’s financial strategy, holds shares worth roughly $1.2 billion.

The gains have extended well beyond senior leadership. Reports on employee compensation programs indicate that thousands of current and former workers benefited from stock options accumulated over years of private ownership. One example cited in post-IPO coverage involved welder Juan Hernandez, whose employee stock awards reportedly grew from an initial value of about $10,000 to nearly $1 million after the listing.

While the IPO created substantial wealth for investors and employees, some of the initial gains have moderated. SpaceX shares later fell more than 9% from their post-listing highs, trimming Elon Musk’s fortune from its peak as the stock retreated from record levels.

Even as the stock pulled back, Bloomberg reported that SpaceX has explored a bond offering worth as much as $20 billion to refinance a bridge loan due in September 2027. According to Bloomberg, the proposed transaction could become one of the largest corporate debt offerings in recent years, although its final size and timing remain under discussion.

Despite the retreat from peak valuations, SpaceX’s market debut remains one of the largest wealth-creation events in recent corporate history. The listing generated billions of dollars in gains for early venture investors, institutional backers, executives, and employees who accumulated shares during the company’s years as a private business.

A smart contract is not smart, and it is barely a contract. It is a small program that lives on a blockchain and runs itself when its conditions are met, with no person to enforce it and no way to undo it. Understanding this one idea unlocks almost everything in crypto.

Summary

- Smart contracts are self executing programs on a blockchain that carry out predefined actions without requiring a middleman or central authority.

- Ethereum turned the concept into a practical technology, enabling applications such as DeFi platforms, NFTs, tokens, and decentralized apps.

- While smart contracts offer automation, transparency, and reliability, coding flaws or faulty external data can lead to irreversible losses.

A smart contract is a program stored on a blockchain that automatically executes when certain conditions are met, with no person, company, or middleman needed to carry it out. That is the whole concept, and it is simpler than the intimidating name suggests, because a smart contract is not artificial intelligence and it is not really a legal contract in the traditional sense.

It is code, a set of instructions that says “if this happens, then do that,” running on a network that no single party controls, in a way that cannot be stopped, censored, or reversed once it is set in motion. Almost everything interesting in crypto beyond simply sending coins, decentralized finance, NFTs, tokens, decentralized applications, runs on smart contracts, which makes understanding them the key that unlocks how the modern crypto world actually works.

This guide explains smart contracts in plain English, from the ground up, with no coding or technical background assumed. It covers what a smart contract actually is and where the idea came from, the vending-machine analogy that makes it click, how smart contracts actually work under the hood, what they are used for across crypto, their real advantages, and, just as importantly, their serious risks and limitations, because the same properties that make smart contracts powerful also make them dangerous when they go wrong.

By the end you will understand not just the definition but the deeper idea, why “code is law” is both the promise and the peril of smart contracts, and why this single invention reshaped what blockchains could do.

What a smart contract actually is

The name causes more confusion than the concept deserves, so it helps to take it apart before building it back up.

A smart contract is “smart” only in the sense that it executes automatically; the word does not imply intelligence or any kind of thinking, and the person who coined the term was careful to say so. It is a “contract” only in the loose sense that it encodes an agreement, a set of conditions and the actions that follow from it, but it is not a legal document sitting in a drawer waiting for a court to enforce it.

The clearest way to describe it is what it actually is: execution logic, a small computer program that lives on a blockchain and runs by itself when its predefined conditions are satisfied. It takes an input, checks whether the conditions are met, and if they are, it performs the actions it was programmed to perform, moving funds, updating records, transferring ownership, issuing a token, without any human stepping in to make it happen.

The idea is older than blockchain. A computer scientist and legal scholar named Nick Szabo proposed the concept in the 1990s, defining a smart contract as a set of promises specified in digital form and the protocols within which the parties perform on those promises, and he was explicit that “smart” did not mean intelligent.

For years the idea was theoretical, because there was no platform on which such self-executing agreements could run reliably without a trusted party to host them. Bitcoin, launched in 2009, introduced a limited form of programmability, but it was the launch of Ethereum in 2015 that made fully featured smart contracts a practical reality, providing a blockchain designed from the start to run arbitrary programs.

Ethereum turned Szabo’s theoretical idea into working infrastructure, and most of the smart contracts in use today run on Ethereum or on networks built on the same model. The concept waited two decades for a platform that could run it without anyone in charge, and the blockchain was that platform.

The vending machine: the analogy that makes it click

The single best way to understand a smart contract is through an analogy that the concept’s own inventor used, because it captures the essential idea perfectly.

Think of a vending machine. You walk up, insert the right amount of money, press the button for your selection, and the machine dispenses your item, all without a cashier, a clerk, or any human involved in the transaction. The machine enforces the agreement automatically: if you put in enough money and make a valid selection, you get the product, and if you do not put in enough, you get nothing.

The rules are built into the machine, they execute on their own when the conditions are met, and there is no person you need to trust or negotiate with, because the machine simply does what it was built to do. A smart contract is the digital, blockchain-based version of exactly this: a mechanism that holds a set of rules, checks whether the conditions are satisfied, and automatically delivers the outcome, with no intermediary required.

The analogy illuminates the key properties. The vending machine is automatic, it acts without a human; it is deterministic, the same input always produces the same output; and it is trustless in the sense that you do not need to trust the machine’s owner to be honest, because the machine’s behavior is fixed by its mechanism, not by anyone’s goodwill in the moment. A smart contract shares all three properties and adds the powers of a blockchain: it can hold and move large amounts of value, it runs on a network no single party controls so no one can secretly alter its rules, and its actions are permanently recorded and visible.

Where a vending machine dispenses a candy bar, a smart contract can release thousands of dollars, transfer ownership of an asset, or trigger a chain of further actions, all on the same simple principle of automatic execution when conditions are met. The vending machine is the intuition; the smart contract is that intuition scaled up to handle money, ownership, and complex agreements with no one in charge.

How a smart contract actually works

Going one level deeper, it helps to understand the mechanics, because the way a smart contract runs explains both its power and its dangers.

A smart contract is written as code, typically in a programming language designed for the purpose, and then deployed onto a blockchain, where it is stored at a specific address much like a wallet has an address. Once deployed, the contract lives on the blockchain permanently, its code visible to anyone and its rules fixed, and it sits there waiting to be used.

When someone wants to interact with it, they send a transaction to the contract’s address, providing whatever input the contract requires, and the network’s computers, the thousands of nodes that maintain the blockchain, all run the contract’s code with that input. Because every node runs the same code on the same input, they all arrive at the same result, which is how the network agrees on the outcome without any central authority, and that agreed result, the funds moved, the ownership transferred, the record updated, is written permanently to the blockchain.

Several features of this process are worth understanding because they shape everything about how smart contracts behave. First, execution costs money: running a contract’s code consumes computational resources, and the user pays a fee, often called gas, to compensate the network for that work, which means complex contracts that do more cost more to run. Second, execution is deterministic and verifiable: because every node runs the same code and reaches the same answer, anyone can verify that the contract did exactly what its code specifies, with no hidden behavior.

Third, and most consequentially, once a contract is deployed, its code generally cannot be changed: the rules are fixed at deployment, and the contract will do exactly what it was programmed to do, forever, which is a strength when the code is correct and a catastrophe when it contains a flaw. This combination, code that runs automatically across a decentralized network, costs a fee to execute, produces verifiable results, and cannot be altered after deployment, is what makes smart contracts both remarkably powerful and unforgiving of error. The machine does precisely what it was built to do, whether or not that is what its creators intended.

What smart contracts are used for

The abstract concept becomes concrete when you see what smart contracts actually do, because they are the engine behind nearly every crypto application beyond simple payments.

Decentralized finance, or DeFi, is where smart contracts found their fullest expression. Decentralized exchanges like Uniswap run entirely on smart contracts, handling the pools of capital that enable trading and settling trades automatically through code rather than through a traditional order book or a company.

Lending protocols like Aave use smart contracts to let people borrow against crypto collateral with no manual approval and no loan officer, with the contract automatically enforcing the loan terms, holding the collateral, and liquidating it if the borrower’s position falls below the required threshold. Stablecoins rely on smart contracts to manage the issuance and redemption of tokens and to maintain their peg. In each case, the smart contract replaces the bank, the broker, or the clearinghouse, performing the function that an institution would traditionally perform, but doing it automatically through code that anyone can inspect.

Beyond DeFi, smart contracts power much of the rest of crypto. Every NFT, a token representing ownership of a unique digital item, is governed by a smart contract that defines the token, tracks who owns it, and handles transfers when it is bought or sold on a marketplace. Tokens of all kinds, the thousands of assets that run on networks like Ethereum, are themselves smart contracts that define the token’s supply and rules.

Decentralized applications, or dApps, are built from smart contracts that provide their backend logic, enabling everything from games to social platforms to run without a central server. Decentralized autonomous organizations use smart contracts to manage shared funds and to execute the outcomes of member votes automatically. The common thread is that wherever crypto replaces a trusted intermediary, a bank, an exchange, a registrar, a voting authority, with automatic, transparent code, a smart contract is doing the work. They are the building blocks from which the entire programmable-money ecosystem is constructed, which is why understanding them illuminates so much of crypto at once.

The advantages: why smart contracts matter

The reasons smart contracts have become foundational come down to a set of real advantages over the traditional way agreements are made and enforced.

The first advantage is the removal of intermediaries. Traditional agreements often require trusted third parties, banks to hold and transfer money, brokers to execute trades, lawyers and courts to enforce terms, and each intermediary adds cost, delay, and the need to trust that party. A smart contract performs the enforcement itself, automatically and without a middleman, which can make transactions faster and cheaper and removes the dependence on any single trusted party.

The second advantage is transparency and verifiability: a smart contract’s code is visible on the blockchain, so anyone can inspect exactly what it will do, and its execution is verifiable, so anyone can confirm it did what it was supposed to, which is a level of openness traditional agreements rarely offer. You do not have to trust a promise; you can read the code that will keep it.

The third advantage is automation and reliability. A smart contract executes exactly as written, every time, without the delays, errors, or discretion of human processing, which means an agreement encoded in a smart contract carries itself out the moment its conditions are met, with no waiting and no possibility of a party simply refusing to perform.

This combination, no intermediary, full transparency, and automatic reliable execution, is what makes smart contracts powerful, because it lets people transact and cooperate without needing to trust each other or any central authority, relying instead on code that anyone can verify and that runs itself. For the first time, agreements can enforce themselves across a global network with no one in charge, and that capability is the foundation on which the entire world of decentralized applications is built. The advantages are real and significant, and they explain why smart contracts moved from a theoretical idea to the engine of an industry.

The risks: why “code is law” cuts both ways

Here is where honesty matters most, because the same properties that make smart contracts powerful make them truly dangerous, and anyone using them needs to understand the risks as clearly as the benefits.

The central risk follows directly from a central strength: smart contracts are immutable and self-executing, which means that if the code contains a bug or a vulnerability, that flaw executes automatically too, and there is often no way to stop it or reverse the damage. A traditional contract with a mistake can be renegotiated, and a fraudulent transaction at a bank can sometimes be reversed, but a smart contract does exactly what its code says, and if its code says to send all the funds to an attacker who found a loophole, it sends all the funds, irreversibly.

The history of crypto is full of expensive examples: hundreds of millions of dollars have been lost to smart-contract bugs and exploits, where attackers found flaws in the code and the contracts dutifully executed the attackers’ will because that is what the code, as written, permitted. The phrase “code is law” captures this: the code is the final authority, and it will enforce whatever it actually says, not what its creators meant it to say.

Several specific risks flow from this. Smart-contract bugs are flaws in the code that attackers can exploit, and because the code cannot easily be changed after deployment, these flaws can be catastrophic and permanent. Bad inputs and faulty external data are another danger, since many contracts rely on outside information delivered by oracles, and if that data is wrong or manipulated, the contract executes on false premises, which can trigger cascading liquidations or other harm.

Complexity compounds the problem, because the more a contract does, the more places a flaw can hide, and the harder it is to verify that the code is safe. And scams exploit the trust people place in code, with malicious contracts written to look legitimate while containing hidden behavior that drains the funds of anyone who interacts with them. The lesson is not that smart contracts are bad, but that “trustless” does not mean “riskless”: you no longer have to trust a person, but you do have to trust that the code is correct, and code written by humans contains human errors. Auditing, caution, and using well-tested, battle-hardened contracts instead of unknown ones are the practical defenses, but the underlying truth remains that a smart contract will do precisely what it is written to do, and getting that writing exactly right is hard.

The limitations worth knowing

Beyond the risks, smart contracts have inherent limitations that shape what they can and cannot do, and understanding these prevents overestimating them.

A smart contract can only see and act on information that exists on its own blockchain. It cannot natively know anything about the outside world, a price, a weather reading, the result of an event, because it is sealed inside the blockchain, which is why oracles exist to feed external data in, and that dependence on oracles is itself a source of risk and limitation.

A smart contract also cannot reach out and act in the physical world; it can move digital assets and update digital records, but it cannot make a physical delivery or enforce a real-world outcome on its own. And a smart contract is only as good as its code: it has no judgment, no ability to interpret intent, and no capacity to handle situations its programmers did not anticipate, so it executes the letter of its code with no understanding of the spirit behind it, which is why an unforeseen edge case can produce an outcome no one wanted.

These limitations matter because they define the boundary between what smart contracts are genuinely good for and where they fall short. They excel at automating clear, well-defined, on-chain agreements where the conditions and outcomes can be precisely specified in code, which is why they work so well for financial applications like trading, lending, and token transfers.

They struggle with anything requiring judgment, interpretation, real-world enforcement, or reliable outside information, because those need capabilities a self-contained piece of code does not have. Understanding the limitations keeps the technology in perspective: a smart contract is a powerful tool for automating precise digital agreements without a middleman, not a magical replacement for all human agreements, and its strengths and weaknesses both flow from the same root, that it is rigid, automatic code running on a sealed, decentralized network. Knowing where that root helps and where it hinders is the difference between using smart contracts well and expecting more from them than they can deliver.

The code that changed crypto

A smart contract is, in the end, a simple idea with profound consequences: a small program that lives on a blockchain and runs itself when its conditions are met, enforcing an agreement automatically with no person, company, or court required. The vending machine captures the intuition, money in, product out, no cashier, and the blockchain scales that intuition up to handle money, ownership, and complex agreements across a global network that no one controls. From this single concept flows nearly everything in crypto beyond simple payments: the decentralized exchanges, the lending protocols, the stablecoins, the NFTs, the tokens, the decentralized applications, all of them built from smart contracts doing automatically what institutions used to do.

The power and the peril come from the same source. Because a smart contract executes exactly as written, automatically and irreversibly, it can replace trusted intermediaries with verifiable code, which is the breakthrough that made decentralized finance and the rest of the ecosystem possible. But that same rigidity means a flaw in the code executes just as faithfully as a feature, with no one to stop it and no way to reverse it, which is why hundreds of millions have been lost to bugs and exploits and why “code is law” is a warning as much as a promise. Smart contracts removed the need to trust people and replaced it with the need to trust code, and code, written by humans, is only as good as the humans who wrote it.

Understanding that tradeoff, the extraordinary power of self-executing agreements and the real danger of their unforgiving precision, is understanding the invention that turned blockchains from simple ledgers into the programmable foundation of an entire industry. The contract is not smart, and it is barely a contract, but it changed what money and agreements could be.

Frequently Asked Questions

What is a smart contract in simple terms?

A smart contract is a program stored on a blockchain that automatically executes when certain conditions are met, with no person or middleman needed to carry it out. It works like a vending machine: provide the right input, and the code automatically delivers the outcome, moving funds, transferring ownership, or updating records. It is “smart” only in that it runs automatically, not because it is intelligent, and it is “code, not a legal document,” which executes itself across a decentralized network.

Who invented smart contracts?

The concept was proposed by computer scientist and legal scholar Nick Szabo in the 1990s, who defined a smart contract as a set of promises in digital form and was explicit that “smart” did not mean intelligent. The idea was theoretical until a platform existed to run it. Bitcoin introduced limited programmability in 2009, but Ethereum, launched in 2015, made fully featured smart contracts a practical reality, and most smart contracts today run on Ethereum or similar networks.

How does a smart contract actually work?

A smart contract is written as code and deployed to a blockchain at a specific address, where it lives permanently with its rules fixed. When someone sends a transaction to interact with it, the network’s many computers all run the contract’s code on the input and agree on the result, which is written permanently to the blockchain. Execution costs a fee called gas, the result is verifiable by anyone, and once deployed the code generally cannot be changed.

What are smart contracts used for?

They power nearly all of crypto beyond simple payments. In decentralized finance, they run exchanges like Uniswap and lending protocols like Aave, replacing brokers and banks. Every NFT and most tokens are smart contracts defining ownership and rules. Decentralized applications use them for backend logic, and decentralized organizations use them to manage funds and execute votes. Wherever crypto replaces a trusted intermediary with automatic, transparent code, a smart contract is doing the work.

What are the risks of smart contracts?

Because smart contracts are immutable and self-executing, a bug or vulnerability in the code executes automatically too, often with no way to stop or reverse it, and hundreds of millions of dollars have been lost to such exploits. Risks include code bugs, manipulated oracle data feeding false information, complexity hiding flaws, and malicious contracts disguised as legitimate ones. “Trustless” does not mean “riskless”: you no longer trust a person, but you must trust that the code is correct, and code contains human errors.

What does “code is law” mean?