Anthony Norman is your typical Gen Z worker: 25, a little wayward, and struggling to find a full time job.

You can’t exactly fault him for the position he’s in. Unemployment rates are high. AI is creating a crisis for young people trying to enter the workforce. Hiring has slowed. And several companies—including Amazon, Block, and Meta—have embraced tech’s latest era of layoffmaxxing, with some cutting their staff by 20 percent.

So when Anthony lands a temp position at Rockin’ Grandma’s Hot Sauce, a small business in Southern California, he’s just happy for what he assumes is a regular gig: assisting with odd jobs and helping plan the annual retreat.

What Anthony doesn’t know is that he is actually the mark of Jury Duty Presents: Company Retreat, the second season of Prime Video’s experimental docu-comedy where one person unwittingly participates in a staged sitcom (the first season, which blew up on TikTok and snagged three Emmy nominations, was about a fake jury trial). Everyone is an actor except for him.

Advertisement

Anthony joins the team during a moment of transition. The founder, Doug Womack, is preparing to step down. His son, Dougie Jr, is next in line, and because not everyone thinks he’s fit to run the family business, he wants to prove that he’s more than an unqualified nepo baby—“the Bronny of hot sauce,” he says. Having just returned from a four-year stint in Jamaica “jamming” with a hotel lobby ska band called the Jive Prophets, the retreat is meant to be a test for Dougie Jr.

The season trades in the monotony of cubicles and watercooler talk for Oak Canyon Ranch, a cozy resort and recreation center nestled in the grassy suburb of Agoura Hills—about an hour drive northwest of Los Angeles—where the staff convenes for various activities: team building, a client cookout, motivational speakers, and a talent contest. Desperate for “one week without Cocomelon” and her three kids, Jackie Angela Griffin, the distribution and logistics rep, is ready to get away.

Like all offices, Rockin’ Grandma’s is a circus of eccentricity and ego. Accountant and bourbon enthusiast Helen Schaffer has been “cooking the books for 26 years.” Receptionist PJ Green has dreams of being a snack influencer. Sourcing manager Anthony Gwinn, who at one point confuses a flesh light for a water thermos, is jokingly nicknamed “Other Anthony” despite working at the company longer. Kevin Gomez, head of HR, has flashes of Michael Scott: He’s an overeager, comically delusional, hopeless romantic who loves his job and Amy Patterson, the customer relations coordinator. “Hot Sauce is having a moment,” he tells Anthony during the onboarding process. “You don’t see this kind of thing happening with ketchup.”

On day two, eager to demonstrate his instincts as CEO, Dougie Jr. calls an audible and brings in an “emotions and vulnerability expert”—she’s the Walmart version of academic Brené Brown—who confusingly leads the group through a conversation on how to navigate uncomfortable scenarios.

Advertisement

It’s good practice for Kevin’s failed proposal to Amy—they’ve actually never been on a real date minus her birthday, which included eight of her other girlfriends. After a humiliated Kevin makes a quick exit from the retreat center, to the sound of tin cans rattling as he speeds off in his car, Anthony is forced to step up.

“I got a promotion,” he says, improvising on the fly to lift morale and take on the role of “Captain Fun.”

Even as people have struggled to find meaning in their work—or simply find work—TV’s fixation with the American workplace has always been popular with viewers. Mad Men examined the existential toils of advertising executives. Severance has contemplated autonomy, in addition to a lot of other very weird shit. And no series has explored the delightful chaos of workplace hijinks better than NBC’s The Office, which followed the oddball staff of Dunder Mifflin, a Pennsylvania paper company.

Mundi Ventures’ EU-backed Kembara fund has made its first major investment by co-leading a $160m round with DCVC in the UK’s Quantum Motion.

The UK-based Quantum Motion specialises in silicon transistor-based quantum computing, and said it will use the Series C investment “to commercialise its scalable and energy-efficient approach to quantum computing” and to help deliver “utility-scale and commercially viable quantum computers that fit inside existing standard data centres and racks”.

Since its last funding round in 2023, the company has expanded internationally, with new offices and labs in Spain and Australia, and has deepened its manufacturing partnership with GlobalFoundries as part of its bid to tie directly into commercial semiconductor supply chains, it said.

“Quantum computing will only achieve its full potential if it can be built on a platform that scales, and we believe silicon is the strongest route to achieving that,” said Dr James Palles-Dimmock, CEO of Quantum Motion. “We are pleased to be joined by investors who share our vision and understand what it takes to build a foundational company in this field.”

Advertisement

Yann de Vries, partner and co-founder of Kembara, said: “If you believe quantum computing is going to be world-changing, as we do, then the obvious next question is which of the many ways of building one will actually work at scale? This investment signals our strong belief in where the answer lies.”

With an ultimate target of €1bn, Spain’s Mundi Ventures closed on €750m in February for its Kembara fund for deep tech and climate start-ups. The fund aims to address the scaling gap in European deep tech funding with its focus on Series B and C funding of €15m-€40m, and beyond, for European companies.

“Quantum is critical infrastructure for the next century of computing, AI and security, and leadership will go to whoever can industrialise it,” said Dr Prineha Narang, operating partner at DCVC. “DCVC led this investment in Quantum Motion because silicon is the foundation that scales, and this team is building on the CMOS advantage to turn quantum from a demonstration into a commercial success story.”

According to the Kembara team, Europe produces 28pc of global deep tech innovation, but only 3pc of European deep tech companies successfully raise Series B or C rounds. It is that very gap that the Kembara fund is hoping to bridge using “€1bn dedicated to backing Europe’s deep tech champions at the exact moment when technology is proven and global scale becomes possible”.

Advertisement

“Quantum Motion’s unique approach that combines cutting-edge quantum physics with established silicon manufacturing provides a distinct global edge,” said Charlotte Lawrence, managing director of direct equity at the British Business Bank, a new investor in the company with this round. “We are no longer just theorising about quantum computing but are actively starting to build the platforms to deliver it here in the UK.”

The European Investment Fund (EIF) is a lead backer of Kembara, announcing in July last year that it would invest €350m in Kembara Fund 1. At the time, the EIF said it was the experience of the Kembara management team and its “differentiated strategy” that were key to offering its support.

Don’t miss out on the knowledge you need to succeed. Sign up for the Daily Brief, Silicon Republic’s digest of need-to-know sci-tech news.

Financial analysts at Wedbush have consistently been bullish about Apple, but now has raised its target price by a whopping $50 to $400, making its greatest jump in at least the last five years.

Back in April 2025 when Trump’s tariffs first struck, Wedbush did cut its Apple price target $325 down to $250, but that was a rare drop. Now it’s made a similarly large increase, taking its price target from the $350 it set in December 2025, to $400.

This is the highest price target ever set for Apple by any investment firm, and in a note to investors seen by AppleInsider, the company’s analysts attribute it very much to AI. They believe that what Apple will reveal at WWDC 2026 in June will lead to around a fifth of the entire world’s population using AI via Apple devices over the next few years.

Key to this belief is the recent news that Apple’s forthcoming iOS 27 will give users the option of multiple different AI models. Wedbush also expects that ultimately hundreds of AI-based apps will take advantage of improvements to Apple Intelligence.

Advertisement

While the $50 target increase is the largest Wedbush has made since at least 2021, the firm has consistently predicted that 2026 will be a significant year for Apple Intelligence. It has also previously predicted that Apple will charge for some AI features, and its latest report doubles down on that.

Wedbush expects that over the next few years, Apple will monetize is AI services. Including its partnership in China with Alibaba, Wedbush predicts that Apple’s AI monetization could bring it $15 billion annually.

The investor note says little further about China, other than that Apple’s AI partnership is part of it aiming to greatly increase its user base in the country. In Apple’s latest earnings call, Tim Cook called out the fact that he was “thrilled” with how the company has seen “strong double-digit growth in Greater China.”

In that same call, Cook also stressed that how with Apple Intelligence, this “is not AI as a standalone feature, but AI as an essential, intuitive part of the experience across our devices.” That fits with Wedbush’s belief that Apple will become what it calls the consumer hub of AI.

Advertisement

CEO handover and WWDC

These expectations around AI, though, are not Wedbush’s only reasons to increase its price target. The firm’s analysts also expect the incoming CEO John Ternus to have an impact on Apple’s hardware moves.

Wedbush believes that WWDC 2026 will be particularly significant, but is already describing this as a golden age for Apple.

Most analysts have been positive about Apple following its recent earnings announcement, but Wedbush appears to be the first to raise its target price.

WWDC 2026 takes place in the week of June 8 to June 12, with the spotlight as ever being on the opening keynote speech.

Cloudflare beat Q1 earnings estimates, cut 1,100 employees because AI agents now do their work, and saw its stock fall 24 per cent. It is the most explicit case of a company attributing layoffs directly to AI replacing human roles.

Advertisement

Cloudflare beat Wall Street’s revenue and earnings estimates on Wednesday, announced it would cut 1,100 employees because artificial intelligence agents now do their work, and watched its stock fall 24 per cent on Thursday. The sequence is becoming the template for the technology industry in 2026: record revenue, record layoffs, record doubt about what comes next.

First-quarter revenue was 639.8 million dollars, up 34 per cent year over year, beating the consensus estimate of 622 million. Adjusted earnings per share were 25 cents against expectations of 23 cents. Free cash flow was 84.1 million dollars. The company added a record number of customers paying more than five million dollars per year and saw a 73 per cent year-over-year increase in deals worth more than a million. By every traditional metric, the quarter was strong.

The 💜 of EU tech

The latest rumblings from the EU tech scene, a story from our wise ol’ founder Boris, and some questionable AI art. It’s free, every week, in your inbox. Sign up now!

Advertisement

Then the company said it was eliminating one in five jobs.

The model

CEO Matthew Prince and co-founder Michelle Zatlyn announced in a blog post that Cloudflare is transitioning to what they called an “agentic AI-first operating model.” The company said its internal use of AI had increased more than 600 per cent in three months. Staff across engineering, human resources, finance, and marketing are running thousands of AI agent sessions per day. The framing was not that AI would assist employees. It was that AI has made certain categories of employee unnecessary.

Prince was specific about which roles are disappearing. “A lot of the support roles” behind customer-facing and engineering staff “are not going to be the roles that drive companies going forward,” he said. The language distinguished between people who build the product, people who sell the product, and people who support the people who build and sell the product. The third group is being replaced.

The financial results that accompanied the layoff announcement were not the results of a company in distress. Cloudflare now has 4,416 customers paying more than 100,000 dollars per year. It estimates that approximately 80 per cent of leading AI companies use its products. Its Workers developer platform, which runs code at the edge of Cloudflare’s network across data centres in 330 cities, is positioned as infrastructure for the AI agent economy the company says is replacing the roles it just eliminated.

Full-year revenue guidance was 2.805 to 2.813 billion dollars, narrowly beating the consensus estimate of 2.8 billion. Full-year adjusted earnings guidance was 1.19 to 1.20 dollars per share, ahead of the 1.14 expected. Prince called AI “the biggest tailwind we’ve ever seen in Cloudflare’s history” and said the re-platforming of the internet around AI agents represents the company’s largest growth opportunity.

The stock market disagreed, or at least disagreed with the timing. Shares fell 24 per cent on Thursday, erasing billions in market capitalisation. The sell-off reflected not the earnings, which were strong, but the uncertainty about whether a company that just fired 20 per cent of its workforce can execute a business model transition while maintaining the growth trajectory investors had priced in.

The cuts

The 1,100 affected employees will receive base pay through the end of 2026, continued healthcare coverage through year end in the United States, and equity vesting extended to 15 August 2026. The restructuring is expected to be substantially complete by the end of the third quarter. Prince said, “Today is a hard day.”

Advertisement

The company’s headcount will fall from approximately 5,156 to around 4,000. The restructuring charges of 140 to 150 million dollars break down to 105 to 110 million in cash severance and benefits and 35 to 40 million in non-cash equity-related expenses. The savings are projected at a pace that Cloudflare expects to reinvest into the AI infrastructure and hiring it says will drive the next phase of growth.

Cloudflare framed the cuts as structural rather than cyclical. This is not a company reducing headcount because revenue is declining. Revenue grew 34 per cent. This is a company reducing headcount because it believes the work those employees performed is now performed by software. The distinction matters because it implies the jobs are not coming back.

Cloudflare’s announcement is notable because it was the most explicit in attributing the layoffs to AI replacing human work rather than AI requiring capital reallocation. Meta’s Zuckerberg said the layoffs were about freeing capital for AI infrastructure. Cloudflare’s Prince said the layoffs were about AI doing the work. The difference is between “we need your salary to buy GPUs” and “we no longer need you because the GPUs are doing your job.”

Cloudflare’s position is coherent but uncomfortable. The company reported its strongest quarter, told investors the AI opportunity is transformational, cut a fifth of its workforce to pursue it, and then saw a quarter of its market value disappear because investors were not sure the transformation would work. The 600 per cent increase in AI usage over three months is either evidence that the transition is already delivering results or evidence that the company is moving faster than it can manage.

Prince’s statement that certain support roles “are not going to be the roles that drive companies going forward” is a prediction about the entire industry, not just Cloudflare. If he is right, the 1,100 people losing their jobs at Cloudflare are early casualties of a restructuring that will reach every technology company and eventually every company that employs people to do work that AI agents can approximate. If he is wrong, Cloudflare just fired 20 per cent of its workforce during its best quarter, and the 24 per cent stock drop is the market’s way of saying so.

The earnings beat. The layoffs are real. The stock is down. The AI agents are running. The question Cloudflare cannot yet answer, and that no company in its position has answered, is whether a 600 per cent increase in AI usage produces a proportional increase in the value of the work, or whether it produces a proportional increase in the confidence that the work is being done without anyone checking whether it is being done well.

The music gear super-company inMusic is purchasing Native Instruments. This is a big deal for a number of reasons. First and foremost, the acquisition puts Native Instruments under the same umbrella as long-time hardware and software rival Akai. The US-based inMusic also owns Moog, M-Audio, Denon, Numark and several other high-profile brands.

Native Instruments owns several popular digital brands like Plugin Alliance, iZotope and Brainworx, all of which will now be run by inMusic. The acquisition also puts an end to the Native Instruments bankruptcy saga, which had left its future uncertain. The company will continue on, which is encouraging for those tied to NI’s ecosystem of products. This does, however, create a massive juggernaut in the industry.

Advertisement

The deal isn’t exactly unsurprising. Someone had to buy Native Instruments and inMusic had already partnered up with the company to bring some of its plugins to Akai devices. The acquisition will likely lead to more NI software popping up on stuff like the Akai MPC XL. Native Instruments makes some of the most respected software in the industry, as synths like Reaktor and Massive are regularly used in music across multiple genres.

There are some questions regarding hardware. Akai makes multiple standalone grooveboxes. We aren’t sure where Native Instruments’ standalone Maschine+ fits in there, if anywhere. There will also be some major product overlap in the world of MIDI controllers. Akai and Native Instruments both make popular controllers and the same goes for other inMusic-owned brands like M-Audio.

Advertisement

Native Instruments CEO Nick Williams wrote in a blog post that the business will continue to operate normally as the transaction completes in the coming weeks. The company did just launch Komplete 26, the latest iteration of its music production bundle. This includes over 190 digital instruments with 180,000 presets. The latest release features a new version of the popular Abysynth synthesizer, along with updated pianos, vocal soundscapes and more.

If you’ve been thinking of getting into self-hosting generative AI, but don’t have a big budget for hardware, you might want to check out [Hardware Haven]’s latest video on an unusually cheap GPU option — but you’ll have to do so quickly, before the market realizes the chance for arbitrage and prices rise accordingly.

He’s gotten a hold of a 16 GB NVidia V100 card for only about a hundred bucks, mostly because it’s not easy to plug in, being on an SXM2 socket rather than the PCIe bus. SXM is a server architecture, and not something you’re likely to get on your motherboard. Another hundred got him an adapter board to fit this enterprise GPU on a consumer motherboard. That’s still a lot less than the PCIe version of the same card, which will likely set you back a thousand or more unless you get very lucky on eBay.

It’s not the newest card, dating back from 2017, but that doesn’t mean it can’t run the latest open models. After 3D printing a fan shroud for the thing so it didn’t cook itself, adding very slightly to the build cost, [Hardware Haven] set to work seeing what it could do. Going head-to-head against an RTX 3060 12 GB, the older V100 delivered more tokens per second at a slightly higher efficiency — but much higher idle power.

It’s hard to imagine modern life without glycols. They are used in cosmetics, fog machines, and food. As you read this, you’re almost certainly wearing or drinking from something they were used to produce — polyester fabric or plastic bottles, for example. If you brush your teeth with toothpaste or top your salad with bottled dressing, you’ve come into contact with these manmade chemical compounds.

Manufactured at industrial scales from crude oil and natural gas, glycols are a common antifreeze ingredient. They are also useful for refrigeration, allowing cooling systems to maintain colder temperatures than water alone allows.

But there’s something more they could do for us: When glycols are vaporized into indoor air, they rapidly inactivate viruses, bacteria, and fungal spores — even while the glycol vapors remain at low enough concentrations to be invisible, odorless, and tasteless. It’s a property that could reduce the spread of the seasonal flu, and maybe even help stop airborne pandemics before they begin. We’ve known about their disease-fighting properties for almost a century, and new research might allow us to deploy them at scale soon.

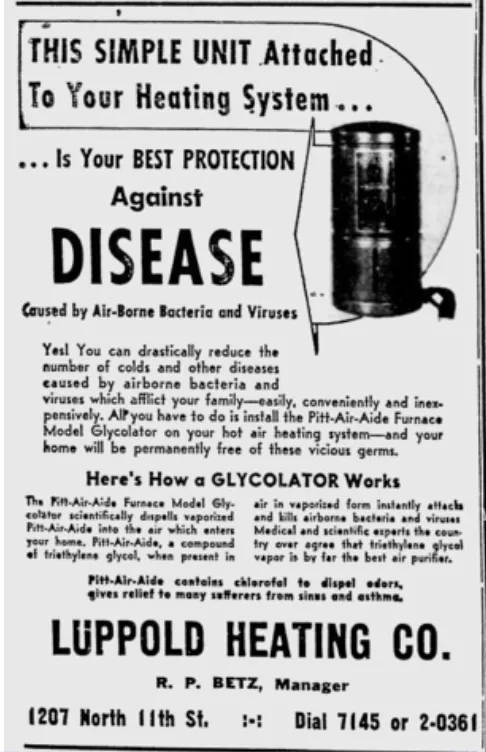

A glycolator ad from 1950.Reading Eagle, October 9, 1950

Chemically speaking, glycols are organic compounds that belong to the alcohol family. Propylene glycol (PG), dipropylene glycol (DPG), and triethylene glycol (TEG) vapors specifically seemsafe for humans to breathe. TEG vapors in particular would be cheap to deploy — costing only about 10 to 50 cents per day to protect a 1,000-square-foot room. While it’s not exactly clear how they combat pathogens, they’ve been shown to inactivate both air- and surface-borne viruses and prevent respiratory disease transmission. According to Curtis Donskey, an infectious disease physician and researcher at the Cleveland VA Medical Center, glycol vapors are particularly effective against enveloped viruses — think SARS-CoV-2, influenza, and Ebola.

Advertisement

There’s a bodyofevidence supporting their use for infection prevention dating back to the mid-20th century. One study conducted over three winters between 1941 and 1944 in a pediatric hospital demonstrated a 96 percent reduction in colds in wards that were disinfected with glycol vapors, compared to those that weren’t. Patients in the glycol-treated wards also had 90 percent fewer total cases of tracheobronchitis, middle ear infections, and acute pharyngitis than the controls.

That research is many decades old, of course, and even similar studies would employ different methodologies today. “Different times [mean] different research standards,” Jacob Swett, the executive director and founder of Blueprint Biosecurity, a nonprofit focused on pandemic prevention, told me. “But I think this shows where the potential could be.”

People in the mid-20th century saw a market opportunity in glycol vapors’ ability to reduce disease transmission. Newspaper advertisements touted “glycolators” and “glycolizers” to protect homes and office spaces.

Interest in glycol vapors for disinfection peaked in the 1940s, falling off with the advent of widely available antibiotics. There was a spike in peer-reviewed papers on glycols in the 1980s, mostly focused on their use in cooling systems and antifreeze agents as disinfectants, but broader interest remained minimal.

Advertisement

The Covid-19 pandemic brought renewed interest in glycol vapors’ antimicrobial properties, and the Environmental Protection Agency (EPA) issued an emergency approval in six states for a TEG-based product series to disinfect occupied indoor spaces. But scientific research on the subject remained relatively limited. Public health agencies were often skeptical about using glycol vapors for disinfection during the Covid-19 pandemic, when the safety profiles of other mitigation measures were better understood. Public health bodies were working with the information they had — some of which turned out to be outright incorrect, like the insistence that SARS-CoV-2 was spread only by droplets rather than being airborne. Hence the stronger focus, especially in the early phases of the pandemic, on measures such as social distancing, practices that are less effective for diseases in which pathogens travel farther and remain suspended in the air.

But even if early speculation about droplet-based transmission of Covid had been correct, there would have been plenty of other good reasons to take the pathogen-negating properties of glycol vapors seriously. “Whether it’s tuberculosis, SARS-CoV-2, the seasonal flu [that] threatens us every year or the next pandemic, which is likely to be airborne, having this evidence around glycol vapors will put us in a much better position to be able to make informed decisions about countermeasures,” Swett told me. With that possibility in mind, Blueprint awarded $4.5 million in grants to the recipients of its Glycol Vapors for Infection Suppression: Efficacy and Safety Research (GlycolISER) program in March.

The grantees will study how glycol vapors inactivate pathogens, their effectiveness during emergency deployment, real-world efficacy in healthcare settings, and how the vapors interact with air filter media. The researchers will also study glycol vapors’ safety profile, especially with potentially sensitive populations, such as people with asthma.

“Being ready to fight the next pandemic means we need to robustly evaluate a wide range of possible interventions,” Brian Renda, a program director at Blueprint Biosecurity, said in a press release. “Through this program, we’re supporting multidisciplinary research to better understand the potential and limitations of glycol vapors as a tool to reduce airborne disease transmission.”

Advertisement

Initial findings are expected by early to mid-2027. “We want to know more about how well it works and we want to make sure that it doesn’t have unintended consequences,” Delphine Farmer, a professor of atmospheric chemistry at Colorado State University who is one of the grantees, told me. Her research will examine how best to get glycol vapors into the air in a quick and affordable way, and how much would come out in gases and particles once vaporized, since those factors impact how effective they are at removing and destroying different microbes that might be in the air. “We want to make sure that if people start adding glycol vapors to air, that this doesn’t cause unknown or new chemistry that might negatively impact people. So the third aspect of what we’re doing is to look at polyethylene glycol chemistry and see if it’s going to produce anything or react with surfaces in ways we should be concerned about.”

Donskey is another of the grantees, and his project has multiple aims. Using a commercially available glycol-based product currently approved for use in unoccupied spaces and for control of mold and mildew, his work will assess whether glycol vapors can reduce the concentration of pathogens in various healthcare settings with different degrees of ventilation. His research will also, among other things, examine whether glycol vapors can reduce airborne pathogen dispersal in medical procedure rooms. The researchers will start testing in unoccupied rooms and transition to populated spaces after the products receive EPA registration for use in occupied spaces.

As Swett suggests, the next pandemic will very, very likely come at us through the air, but there are already numerous other illnesses circulating that we could prevent before they take root. The potential benefits — for reducing work and school absenteeism, healthcare costs, and avoidable suffering — are enormous.

Why we need a multilayered arsenal against airborne disease

Advertisement

If the Covid-19 pandemic taught us anything, however, it’s that airborne disease is still a threat as long as we breathe. But six years on, it’s not clear if we took that lesson to heart. “It seems like we didn’t really learn much from Covid-19 and [as a society] are actively ignoring the ongoing effects,” Miles Griffis, the co-founder of The Sick Times, a publication covering long Covid, told me. “I think we could be in a much better place than we are now.”

A study from 2024 found that 400 million people around the world have had long Covid — almost certainly an undercount. In the next 10 years, long Covid could cost health systems $11 billion annually. Up to 35 percent of people infected by Covid-19 develop lingering symptoms that can be profoundly disabling.

And Covid is only one disease you can catch through the air, nor is it the only one that can have dire consequences. Influenza costs the US almost $29 billion in a single season from healthcare costs and lost productivity — and it kills up to 650,000 people worldwide every year. Childcare centers, schools, and workplaces would be significantly safer and more productive with better ways to prevent the spread of airborne illness.

It’s impossible to say how many cold or flu or Covid-19 infections glycol vapors could prevent. But, like other technologies such as germicidal ultraviolet light, they are notable in part because they don’t require people to “opt in” the way donning a mask does — their distribution mechanisms could be built into the environment itself. William and Mildred Wells, a husband-and-wife duo, were thinking along these lines in the 1930s, advocating for governments to install germicidal ultraviolet lights in public places to protect everyone from airborne pathogens. The Wellses saw that people were developing ways to purify water, pasteurize milk, and ensure food wasn’t contaminated, and asked “‘What about the air? Don’t we deserve pure air as well?’” Carl Zimmer, a science columnist for the New York Times and the author of Air-Borne: The Hidden History of the Life We Breathe, told me.

Advertisement

Blueprint Biosecurity thinks so, and is also advancing work on far-UVC light and better personal protective equipment to protect against airborne pathogens. Better ventilation and filtration could, of course, also improve indoor air quality, which would significantly reduce respiratory disease transmission.

“In many ways, the kind of changes to buildings today [compared to the 1940s and ’50s when earlier studies were done] potentially make them more amenable to glycol vapors where you have centralized HVAC systems,” Swett told me. “[And] depending on how the evidence comes back, there’s a number of environments where you could imagine deploying them.”

An ad for a glycol vaporizer.The Pittsburgh Press, March 14, 1949

“I think we’ve got a little bit of testing to go before we know how well they work,” Farmer said. “As an atmospheric chemist, I always think about clean air…as the absence of any pollutant. So the moment I hear about adding anything to air, I have some notes of caution. But on the flip side, we do add things to our indoor air all the time, so it doesn’t necessarily mean it’s a dealbreaker.”

No matter how safe and effective glycol vapors prove to be, there’s likely to be resistance of one kind or another. People will be wary of adding substances to the air, and entering spaces where they don’t know if glycol vapors will be used. But Donskey doesn’t anticipate that this will be a major issue: “If a product has an EPA registration indicating that they believe it’s safe for use in occupied areas, I think most people will be comfortable. There may be some people who are less comfortable, but again, I think it’ll go through more safety evaluations.”

Advertisement

Once a regulatory agency says this is safe to use in occupied areas, the rest will follow. We would still need commercial products to disseminate them; people can’t just put glycol vapors into their home humidifier. “But if it’s EPA-registered, relatively inexpensive, easy to use, and doesn’t involve a lot of labor, I could easily envision a lot of healthcare facilities taking this up,” Donskey said.

There are many potential use cases for glycol vapors, and “we definitely need some good strategies that allow for safe indoor environments,” Farmer told me. After all, we spend about 90 percent of our time indoors, and we always have to breathe.

Dario Amodei is not the kind of CEO who talks loosely about numbers. The Anthropic co-founder and chief executive, a former VP of research at OpenAI with a PhD in computational neuroscience from Princeton, has built a reputation for measured public statements — particularly around the financial performance of a company that, until recently, disclosed almost nothing about its business.

So when Amodei took the stage at Anthropic’s Code with Claude developer conference on Wednesday and offered a genuinely striking piece of financial candor, the room paid attention.

“We tried to plan very well for a world of 10x growth per year,” Amodei said during a fireside chat with Anthropic’s chief product officer, Ami Vora. “And yet we saw 80x. And so that is the reason we have had difficulties with compute.”

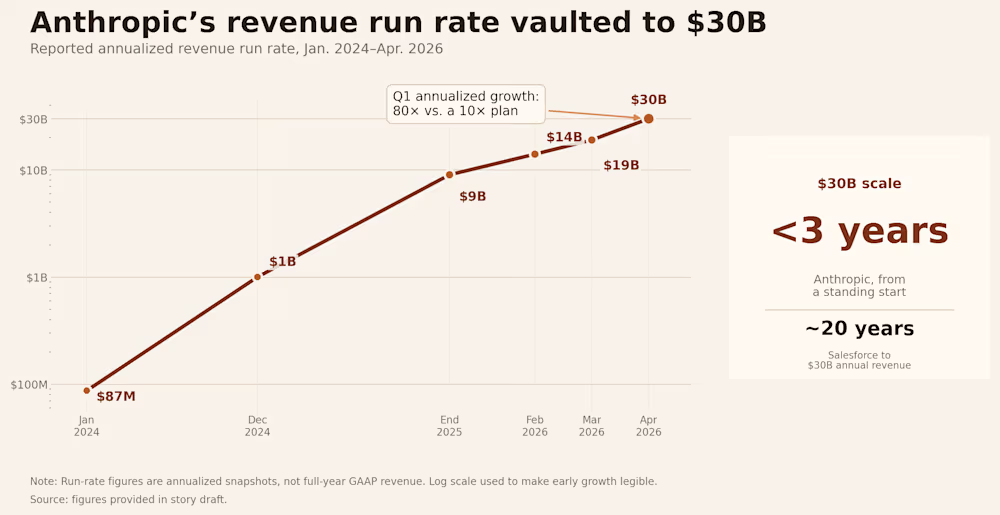

Anthropic had planned for tenfold growth. But revenue and usage increased 80-fold in the first quarter on an annualized basis, a rate Amodei described as “just crazy” and “too hard to handle.”

Advertisement

The number demands context. Annualized growth rates can overstate sustained performance — a single strong quarter, extrapolated across a full year, can paint a picture that doesn’t hold. Amodei knows this. But the underlying trajectory is not a mirage. Anthropic has crossed a $30 billion annualized revenue run rate, up sharply from roughly $9 billion at the end of 2025, and that growth is being driven largely by enterprise demand. The company’s revenue trajectory has been relentless: $87 million run rate in January 2024, $1 billion by December 2024, $9 billion by end of 2025, $14 billion in February 2026, $19 billion in March, and $30 billion in April.

For context: Salesforce took about 20 years to reach $30 billion in annual revenue. Anthropic did it in under three years from a standing start.

Anthropic’s annualized revenue run rate surged from $87 million in January 2024 to $30 billion by April 2026 — a pace that CEO Dario Amodei said outstripped the company’s own forecasts by a factor of eight. Note: Run-rate figures are annualized snapshots, not full-year GAAP revenue. Log scale used. (Image Credit: Michael Nunez / VentureBeat)

Claude Code became the fastest-growing product in enterprise software history

The growth story at Anthropic is, to a remarkable degree, a single-product story. Claude Code, the company’s agentic AI coding tool launched publicly in mid-2025, has become the fastest-growing product in the company’s history — and, by several measures, one of the fastest-growing software products ever built.

Advertisement

Claude Code hit $1 billion in annualized revenue within six months of launch, and the growth hasn’t slowed down. By February 2026, the product was generating over $2.5 billion in run-rate revenue. The company also said Claude Code’s weekly active users had doubled since January 1 and that business subscriptions had quadrupled since the start of 2026.

The mechanics of the product are straightforward. Claude Code is not a chatbot that suggests snippets. It reads a codebase, plans a sequence of actions, executes them using real development tools, evaluates the result, and adjusts its approach. The developer sets the objective and retains control over what gets committed, but the execution loop runs independently. The average developer using Claude Code now spends 20 hours per week working with the tool.

At Anthropic itself, the majority of code is now written by Claude Code. Engineers focus on architecture, product thinking, and continuous orchestration: managing multiple agents in parallel, giving direction, and making the decisions that shape what gets built.

That last point may be the most revealing detail Amodei disclosed at the conference: this is the first year Anthropic’s own internal pull requests have inflected upward due to Claude’s work on the company’s own codebase. The tool that Anthropic sells to developers is now a material contributor to Anthropic’s own engineering output. That creates a feedback loop that is almost impossible for competitors without a comparable product to replicate — the company is using its own product to build the next version of its own product.

Advertisement

The enterprise numbers tell the same story. The company now counts over 1,000 enterprise customers spending more than $1 million per year on Claude services, a figure that has doubled since February. Much of this increase has been fueled by a wave of corporate customers including Uber and Netflix.

Amodei framed the adoption curve in economic terms. “Software engineers are the ones who are fastest to adopt new technology,” he said on stage. “It’s a foreshadowing of how things are going to work across the economy, and how the economy is going to be transformed by AI.”

Anthropic’s 80x growth created a compute crisis it couldn’t solve alone

Hypergrowth creates its own category of problem. When demand outstrips supply by an order of magnitude, the constraint is not go-to-market strategy or product-market fit. The constraint is physics.

The company is growing so fast that its infrastructure has struggled to keep up, forcing Anthropic into what may be the most unexpected partnership in the current AI cycle. Amodei’s comments came hours after Anthropic announced a deal with Elon Musk’s SpaceX to use all of the compute capacity at his company’s Colossus 1 data center in Memphis, Tennessee. As part of the agreement, Anthropic will get access to more than 300 megawatts of capacity — over 220,000 Nvidia GPUs, including dense deployments of H100, H200, and next-generation GB200 accelerators.

Advertisement

The deal is remarkable for several reasons. Musk has been, until very recently, one of Anthropic’s most vocal critics. He has said Anthropic is “doomed to become the opposite of its name” and wrote in February that “Anthropic hates Western Civilization.” But on Wednesday, Musk changed his tune, saying he spent a lot of time with senior members of the Anthropic team over the past week and that he was “impressed.” “Everyone I met was highly competent and cared a great deal about doing the right thing. No one set off my evil detector,” Musk wrote.

The strategic logic on both sides is clear. xAI’s Colossus 1 ended up with capacity that Grok’s user base never grew into, while Anthropic needs compute immediately. Anthropic has been signing deals with Amazon, Google, Nvidia, and Microsoft for more compute capacity, but most of that isn’t expected to come online until late 2026 or early 2027. The SpaceX deal gives Anthropic a significant boost now — the key word being “now.”

Last month, Anthropic said demand for Claude has led to “inevitable strain on our infrastructure,” which has impacted “reliability and performance” for its users, particularly during peak hours. The company admitted in a postmortem from late April that three bugs had affected Claude Code since March 4, and that internal tests hadn’t caught them, leading to several weeks of degraded performance. Amodei said at the Code with Claude conference that the company is “working as quickly as possible to provide more” capacity and will “pass that compute on to you as soon as we can.”

Advertisement

A near-trillion-dollar valuation makes Anthropic’s IPO the most anticipated debut in years

The growth figures arrive at a moment when Anthropic’s valuation is itself becoming one of the defining financial stories of the AI era.

Anthropic has begun weighing a fresh funding round that would value the company at more than $900 billion, according to people familiar with the matter, potentially leapfrogging its longtime rival OpenAI as the world’s most valuable AI startup. The velocity of the escalation is difficult to overstate. From $61.5 billion in March 2025, to $183 billion by its Series F in September, to $380 billion in February, to, if the current discussions proceed, more than $900 billion in May. Anthropic’s shares were already trading at an implied $1 trillion valuation on secondary markets earlier this month.

Instead of cashing out, many existing investors are waiting to potentially exit during Anthropic’s anticipated IPO later this year. The company is raising what is likely to be its last private round before going public to fund its massive computing needs. Bloomberg has reported that the company is weighing an IPO as early as October 2026, with Goldman Sachs, JPMorgan, and Morgan Stanley already in early discussions.

Anthropic is also building out infrastructure on longer time horizons. Amazon has agreed to invest up to $25 billion in Anthropic, securing up to 5 gigawatts of compute capacity for training and deploying Claude models. Anthropic also secured 5 gigawatts of computing capacity as part of a separate deal with Google and Broadcom that will start to come online next year. The total commitment is staggering — tens of gigawatts of compute across three separate hardware ecosystems: Amazon’s Trainium chips, Google’s TPUs via Broadcom, and Nvidia GPUs through SpaceX and Microsoft Azure.

Advertisement

For perspective: Anthropic’s $30 billion run rate exceeds the trailing twelve-month revenues of all but approximately 130 S&P 500 companies. A company that was essentially pre-revenue in early 2024 now out-earns most of the Fortune 500.

At a $30 billion annualized run rate, Anthropic would out-earn roughly three quarters of S&P 500 companies by revenue — a striking milestone for a company that was essentially pre-revenue in early 2024. Note: Anthropic figure is an annualized run rate, not trailing twelve-month GAAP revenue. (Image Credit: Michael Nunez / VentureBeat)

That comparison comes with caveats. Private-market revenue run rate is not the same thing as audited GAAP revenue, gross margin, free cash flow, or public float. OpenAI has internally argued that Anthropic’s $30 billion figure is overstated by roughly $8 billion, pointing to questions about whether revenues from AWS and Google Cloud should be reported at gross value or net of the partner’s cut. The accounting question will ultimately be resolved when both companies file IPO prospectuses — but even on a net basis, Anthropic’s growth rate is unlike anything in enterprise software history.

Dario Amodei’s vision for AI extends far beyond coding — and he’s given himself a deadline

The financial story — 80x growth, a near-trillion-dollar valuation, a scramble to secure enough GPUs to meet demand — is dramatic on its own terms. But Amodei used his time on stage to place it inside a larger thesis about where AI is headed.

Advertisement

He described a progression from single agents to multiple agents to what he called whole organizational intelligence — from “a team of smart people in a room” to “a country of geniuses in the data center.” The framing is deliberately expansive. What Anthropic is selling today is a coding tool. What Amodei is describing is a future in which entire categories of knowledge work are performed by fleets of AI agents operating in parallel, supervised by humans who define objectives and review outputs.

He reiterated a prediction he made roughly a year ago: that 2026 would see the first billion-dollar company run entirely by a single person. “Hasn’t quite happened yet,” he said. “But we’ve got seven more months.”

The company has also been navigating political headwinds. The Pentagon declared Anthropic a supply chain risk in March, blacklisting it from work with the military. The company has warned the designation could result in billions in lost revenue, with over one hundred enterprise customers reportedly expressing doubts about continuing their relationships.

And yet — as that scuffle makes its way through the legal system, Anthropic is only getting more popular. Amodei said this week he’s eventually hoping for “more normal” expansion.

Advertisement

There is a temptation, when covering a company growing at this rate, to let the numbers speak for themselves. They shouldn’t. Growth at 80x annualized is not a business plan — it’s an emergency. It means demand has outrun infrastructure, that customers want something the company cannot yet reliably deliver at scale, and that every week of constrained capacity is a week during which competitors can close the gap.

The investors funding Anthropic — including SoftBank, Amazon, Nvidia, Google, a16z, Lightspeed, and ICONIQ — are making a specific bet: that compute costs continue to fall per unit of intelligence, that revenue keeps compounding faster than burn, and that whoever owns the AI infrastructure layer in 2029 will generate returns that make the interim losses irrelevant.

Amodei’s candor at Code with Claude was not a victory lap. It was a diagnostic — an admission that his company is running faster than it can steer. He planned for a world of 10x growth and got 80x instead. Now he has seven months to prove that the infrastructure, the organization, and the vision can catch up to the demand. The country of geniuses in the data center is getting crowded. The question is whether anyone remembered to build enough rooms.

According to insider sources, Microsoft engineers are working on a new feature called “Low Latency Profile” (LLP) aimed at improving Windows 11’s performance in certain critical, system-wide tasks. The change is already present in recent preview builds distributed to Windows Insider participants, meaning enthusiast users can enable and test it… Read Entire Article Source link

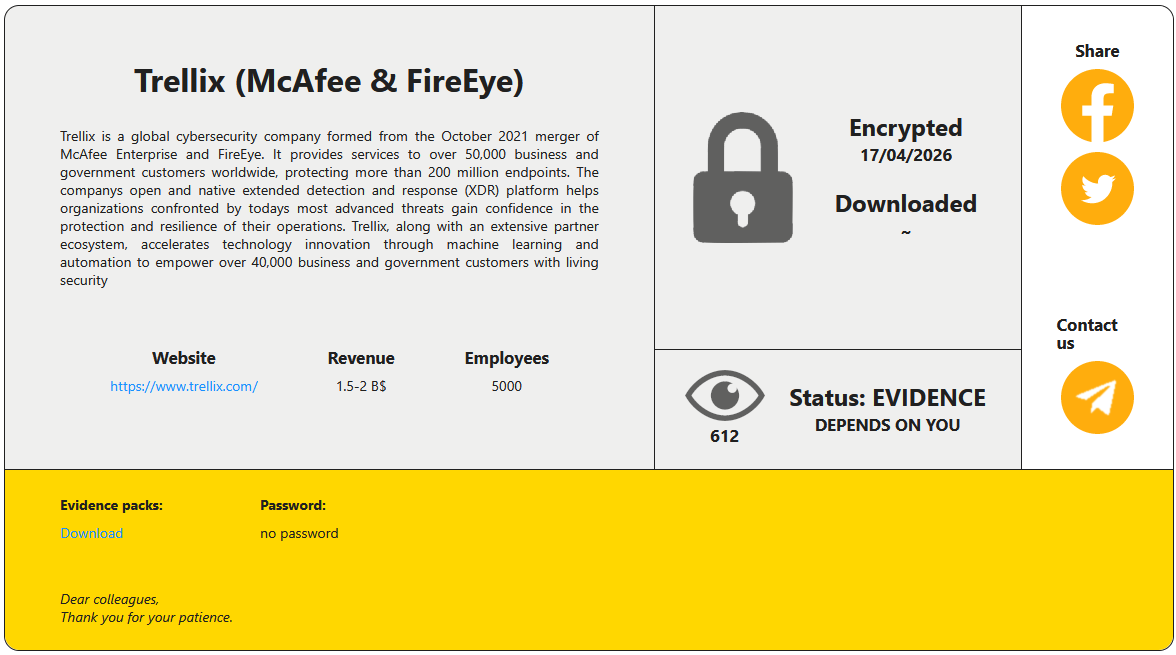

The attack on the Trellix source code repository disclosed last week has been claimed by the RansomHouse threat group, which leaked a small set of images as proof of the intrusion.

Yesterday, the threat actor published on their data leak site screenshots indicating access to the cybersecurity company’s appliance management system. However, BleepingComputer could not confirm the authenticity of the data.

Trellix is an international cybersecurity firm with global Fortune 100 customers. In 2025, the company had more than 53,000 customers in 185 countries and 3,500 employees.

The company confirmed the breach in a statement on May 1st and said that it was investigating the incident. “Trellix recently identified unauthorized access to a portion of our source code repository. Upon learning of this matter, we immediately began working with leading forensic experts to resolve it,” stated Trellix.

Advertisement

“We have also notified law enforcement. Based on our investigation to date, we have found no evidence that our source code release or distribution process was affected, or that our source code has been exploited.”

At the time, BleepingComputer’s request for details went unanswered, and the company did not disclose any information about the perpetrators.

Following a new request for comments after RansomHouse’s disclosure, Trellix told BleepingComputer that it was “aware of claims of responsibility for the attack and are looking into it.”

According to the threat actor, the intrusion occurred on April 17 and resulted in data encryption.

Advertisement

Trellix listed on the RansomHouse extortion portal Source: BleepingComputer

RansomHouse is a cybercrime group that launched in 2022 as a data-extortion operation, listing victims on a darkweb portal and leaking or selling data stolen from their corporate networks.

Over time, the threat actor added more advanced encryption utilities to their toolkit, such as ‘Mario,’ which performs a dual-encryption pass with two keys on target files, and ‘MrAgent,’ which automates the deployment of encryptors on VMware ESXi hypervisors.

A recent high-profile case involving RansomHouse was that of Japanese e-commerce giant Askul Corporation, from which the threat group stole 740,000 customer records, among other sensitive information.

Trellix’s investigation is still underway, and the company previously promised to share more details once they become available.

AI chained four zero-days into one exploit that bypassed both renderer and OS sandboxes. A wave of new exploits is coming.

At the Autonomous Validation Summit (May 12 & 14), see how autonomous, context-rich validation finds what’s exploitable, proves controls hold, and closes the remediation loop.

Helion Energy is building Tiny Merge, a fusion device that is one-eighth the size of its seventh generation prototype and will serve as a testbed for faster iterations of its designs. (Helion Photo)

EVERETT, Wash. — With just three years left on a hard deadline to prove its fusion approach works, Helion Energy is still wrestling with fundamental questions — and it’s building a new, smaller machine to help find answers faster.

Since launching more than a decade ago, Helion has built increasingly larger prototype devices to test and refine its fusion technology as it races to deliver a source of nearly limitless clean energy. But by 2028, Helion is contractually obligated to have a commercial facility producing energy from fusion reactions, essentially replicating the physics that power the sun.

So now it’s going small.

The company is building a downsized testbed device called “Tiny Merge,” a machine less than one-eighth the size of Polaris, its seventh-generation and final prototype. The decision reflects the reality that key issues remain that Helion’s larger, more expensive prototypes haven’t fully resolved. These concerns must be addressed before final designs for a power plant can be locked in.

“With this agile testbed, we will be able to test new ideas with much less energy and far fewer resource requirements, meaning we can iterate faster than we can on full-scale machines such as Polaris,” said Michael Hua, Helion’s senior director of radiation safety and nuclear science.

Advertisement

GeekWire got a sneak peek at Tiny Merge during a recent tour of the company’s sprawling R&D facility north of Seattle. Behind massive curtains in a cordoned-off section of the building sits the gleaming, tubular fusion device measuring roughly 8 feet long.

Running parallel to the machine are two rows of tall shelving — heavy-duty versions of what you’d find at a home improvement store — that will eventually hold hundreds of mini-fridge-sized capacitors to store power flowing into and out of the device. Helion plans to have Tiny Merge up and running by the end of the summer, leaving roughly two years to incorporate what it learns into final designs.

The stakes couldn’t be higher. Over in Eastern Washington, Helion has broken ground on Orion, a facility that it hopes will be the first to produce fusion energy at a commercial scale. It’s a feat no one has yet accomplished, though more than 45 companies are trying.

Helion has made the sector’s most aggressive timeline commitment through a deal with Microsoft to supply electricity from Orion for a data center development starting in 2028. Miss that deadline, and Helion faces financial penalties from Microsoft and partner Constellation.

Advertisement

The company is counting on Tiny Merge to help make that big bet pay off.

Fusion works by heating matter and compressing it into a plasma, a superheated state in which atoms are stripped of their electrons. In those extreme conditions, atomic nuclei collide, fuse and release energy. The process holds enormous promise for abundant clean power, but achieving it at scale remains a formidable scientific challenge.

The team’s first tests with Tiny Merge will focus on the formation and merging of plasma rings, said Manav Singh, Helion’s director of electrical engineering. The company has researched this with previous prototypes, Singh said, but new results have prompted further questions. “There’s a few much more deep investigations we want to do,” he added.

Helion and the broader fusion industry have made measurable progress in recent years, with devices hitting new records in temperature and pressure. Companies have poured significant funding into the pursuit, with Helion alone raising more than $1 billion from investors including OpenAI CEO Sam Altman.

Advertisement

But plenty of skeptics remain, arguing that grid-scale fusion energy is still many years away — if it ever arrives.

You must be logged in to post a comment Login