Crypto World

xStocks launches on-chain private-shares fund

Late-stage private-market exposure is moving on-chain as tokenized equity platforms expand their coverage of prominent technology companies. xStocks announced a collaboration with Fundrise to tokenize the Fundrise Innovation Fund, a closed-end vehicle whose portfolio includes private stakes in Anthropic, Databricks and SpaceX. The plan centers on a new single-token asset, VCXx, slated to go live on the xStocks platform in the coming days, bringing late-stage private tech exposure onto a blockchain-based trading layer.

The Fundrise Innovation Fund has been public for only a short time. It began trading on the New York Stock Exchange earlier this month, delivering a portfolio that includes private shares in several high-profile tech names. In its first days of trading, the fund’s share price swung dramatically, rising from an initial offering around $31 to a late-week peak near $575 before retreating to close the week near $173. The move underscores both the appetite for private-market access and the volatility that can accompany fresh listings in a novel asset class.

Key takeaways

- The Fundrise Innovation Fund is expanding on-chain exposure to its private-tech holdings via the tokenized asset VCXx on the xStocks platform.

- NYSE trading of the fund generated dramatic intraday moves, with a surge from about $31 at debut to a high of roughly $575, before finishing the week around $173; after-hours trading extended the decline by about 6%.

- Regulatory scrutiny looms: Citron Research flagged alleged past SEC charges against Fundrise Advisors LLC for paid solicitation in 2023 and urged regulators to scrutinize whether influencers are being compensated to promote VCX.

- Tokenized stocks as a space surpassed $1 billion in on-chain value, driven by a small group of operators led by Ondo and xStocks, indicating a nascent but rapidly consolidating market for real-world assets on the blockchain.

- Industry observers point to regulatory barriers, liquidity advantages and different tokenization models as key drivers shaping competition and consolidation in tokenized equities.

Fundrise’s on-chain expansion and VCXx

In a move that blends traditional private equity with decentralized finance rails, the tokenized asset VCXx will embody Fundrise’s late-stage private holdings on the blockchain. The collaboration with xStocks positions Fundrise’s Innovation Fund to offer on-chain access to a portfolio that features private stakes in Anthropic, Databricks and SpaceX, among others. Fundrise’s closed-end nature means investors gain exposure to a curated slate of private tech equities, while the tokenization layer aims to unlock on-chain liquidity and potentially broader participation in private markets that have historically been out of reach for many retail investors.

According to the platform’s disclosure, VCXx is expected to launch in the coming days, enabling a tokenized representation of the Fundrise portfolio that traders can access through on-chain settlement, custody and trading workflows. This is part of a broader trend in which real-world assets (RWAs) are being tokenized to provide liquidity, price discovery and programmable access to private-market exposures that were once the sole domain of accredited investors and institutions.

The broader context for this shift is a market increasingly comfortable with on-chain representations of traditional assets, even as it grapples with valuation challenges and the need for robust risk controls. Fundrise’s on-chain push mirrors a wave of tokenized private-market vehicles that have sought to translate the appeal of venture portfolios into a more liquid, transparent format on blockchain rails. Investors are watching not only the potential for improved liquidity but also how governance, custody, and regulatory compliance will evolve in this hybrid space.

NYSE debut, volatility and the regulatory backdrop

The Fundrise Innovation Fund’s public listing on the NYSE was a milestone for asset tokenization and the integration of private-market strategies with traditional equity markets. Yet the initial price action also highlighted the fragility of sentiment around newly listed vehicles tied to private tech. After an opening near $31, the stock surged to a high of around $575, a trajectory that underscored intense investor interest but also the risk of rapid de-rating as the market digested fundamental signals and liquidity dynamics.

By week’s end, the shares had retreated to about $173, a decline of roughly 34% from the intraweek peak, with further after-hours selling compounding the pressure. This sequence has roiled some observers who had expected more orderly price discovery for a vehicle that blends private-market exposure with a listed platform. The volatility prompted scrutiny from market watchers and commentators alike, especially as concerns about valuation practices and the fund’s governance surfaced in public discussions.

In this environment, Citron Research published a report raising questions about Fundrise’s past regulatory interactions. The short-seller asserted that Fundrise Advisors LLC faced SEC charges in 2023 related to paid solicitation activities and urged regulators to examine whether promotions of VCX involve paid influencers. The report fed into broader debate about the governance and transparency of tokenized private-market products, even as Fundrise’s leadership pushed back. Ben Miller, Fundrise’s co-founder and CEO, told CNBC that defenders of the strategy see it as expanding access to high-growth tech companies while critics are pursuing an unfounded smear campaign. Miller emphasized that the firm remains committed to its long-term vision of widening private-market participation through regulated vehicles.

For investors, the headlines carry both risk and potential. A publicly traded vehicle linked to a private-capital portfolio offers a route to exposure that was once out of reach for many, but it also introduces a complex mix of pricing, liquidity and regulatory risk that participants must navigate. The on-chain tokenization layer adds another dimension: it promises faster settlement and programmable features but must establish robust custody, compliance and market-making ecosystems to sustain trust over time.

Tokenized stocks: a growing but concentrated market

Beyond Fundrise, the tokenized-stocks space has been gaining traction as a way for investors to gain crypto-native exposure to traditional equities. Data from RWA.xyz shows that tokenized stocks crossed the $1 billion mark in total on-chain value earlier this month, underscoring growing demand for real-world assets within the crypto ecosystem. While the aggregate figure is sizeable, the activity is currently concentrated among a few operators. RWA.xyz notes that Ondo handles roughly 58% of market activity, with xStocks accounting for about 24% through its tokenized stock offerings. This implies a nascent duopoly in an industry that is still laying down the rules for liquidity, price discovery and regulatory compliance.

In a March 10 report, Foresight Ventures highlighted the market’s consolidation dynamics, pointing to regulatory barriers, liquidity gaps and the varying models used to tokenize assets as key factors shaping competition. The report suggests that the field is moving toward a handful of dominant platforms that can offer deeper liquidity and clearer governance, while smaller players struggle to maintain scale in a fragmented landscape. The evolving regulatory backdrop, including how securities laws apply to tokenized assets and the disclosure standards expected by investors, will continue to define who can participate and under what terms.

For participants in the space, these signals matter. A rising on-chain value for tokenized equities indicates healthy demand for real-world asset exposure in crypto-native infrastructure. Yet the concentration in a few players also raises questions about counterparty risk, platform dependence and the capacity for on-chain markets to deliver durable liquidity in stressed conditions. Observers will be watching how Fundrise’s VCXx deployment interacts with broader on-chain trading, what valuation regimes emerge for tokenized private-market exposures, and how regulators respond to the growing integration of traditional equities with blockchain-based settlement and custody mechanisms.

What investors and builders should watch next

Two threads are especially relevant for market participants. First, the timeline and mechanics of VCXx’s launch will be a focus. If the single-token representation of Fundrise’s Innovation Fund can deliver reliable liquidity and transparent pricing on xStocks, it may become a test case for how other private-market funds approach tokenization. Second, the regulatory dimension remains unsettled. The Citron report and subsequent coverage raise questions about sponsorship, disclosures and the safeguards around influencer-driven promotions in tokenized offerings. Regulators’ forthcoming guidance or enforcement actions could significantly shape how quickly and how broadly on-chain private-market products scale.

Beyond regulation, traders and investors should monitor platform-level dynamics. The tokenized-stocks market’s concentration around Ondo and xStocks will influence liquidity risk and price reliability. The size of the on-chain market—already exceeding $1 billion in value—suggests a tipping point where on-chain and off-chain price signals begin to interact more tightly. As more funds like Fundrise bring private-market assets onto a tokenized layer, the industry will need to demonstrate consistent governance, robust custody solutions and resilient market-making to sustain confidence during periods of volatility or macro stress.

In the near term, market participants should watch the VCXx launch timeline and any updates from Fundrise or xStocks on how the tokenized asset will be structured, priced and traded. They should also keep an eye on regulatory developments and any further disclosures around sponsorship and marketing practices for tokenized products. The convergence of private markets with on-chain infrastructure is still in a discovery phase, but the early momentum suggests a broader rethinking of how private capital can reach a wider investor base—provided the risks are managed with clear, enforceable standards.

As this space evolves, it will be essential to balance the promise of improved access and liquidity with the need for robust governance, transparent disclosures and prudent risk controls. The Fundrise on-chain initiative marks another milestone in that ongoing experiment, one that will likely shape how both traditional asset managers and blockchain-native platforms approach the increasingly blurred line between private markets and digital finance.

Readers should monitor updates from Fundrise and xStocks, regulatory filings and ongoing market data to gauge how the VCXx token performs relative to the underlying private portfolio and how the on-chain execution rails cope with real-world liquidity demands. The coming weeks could show whether this experiment translates into meaningful, durable access to late-stage tech exposure or merely reflects a volatile moment in the early days of tokenized private equities.

Canada’s federal government has unveiled a broad proposal to outlaw cryptocurrency donations to political parties and related election processes, part of a wider package designed to curb anonymous and hard-to-trace contributions. The Strong and Free Elections Act was introduced on Thursday to amend the Canada Elections Act, preventing parties and third parties involved in elections from accepting crypto, money orders, and prepaid cards as political contributions.

Stepping up the push against foreign interference and other election threats, the bill’s sponsor, Steven MacKinnon, said the measures aim to “block foreign interference and other threats to elections.” He noted that the legislation expands government coordination and investment in countering such risks, with the goal of preserving free, fair, and secure elections at all times.

Key takeaways

- The bill would prohibit political parties and election-process third parties from accepting donations in cryptocurrency, money orders, and prepaid cards, citing anonymity and traceability concerns.

- If enacted, contributions made via any of the banned methods must be returned, destroyed, or delivered to the chief electoral officer, with penalties up to twice the amount contributed plus fixed fines of $25,000 for individuals and $100,000 for corporations.

- Beyond donations, the legislation expands rules to address deepfakes that impersonate electoral candidates, adding an extra layer of protection for voters.

- The move follows a 2024 recommendation from the chief electoral officer to ban crypto political donations outright due to difficulties in identifying contributors.

- Canada has previously experimented with crypto campaign funding rules since 2019, but a similar ban attempt in 2024 stalled in Parliament before dying on the floor of the House of Commons.

What changes with the Strong and Free Elections Act?

The proposed amendments would revise the Canada Elections Act to close a notable loophole around fundraising. Under current practice, crypto donations have been permitted and treated similarly to property donations, a framework that many policymakers now view as insufficient for ensuring transparency. The new provisions would explicitly bar political actors from receiving crypto, money orders, or prepaid cards, tools often highlighted as vehicles for anonymous funding.

Enforcement provisions are designed to be concrete. Any prohibited contribution would need to be returned to the donor, destroyed, or passed to the chief electoral officer for appraisal and disposition. The penalties attached to violations reflect a deterrent approach: up to twice the amount of the contribution, in addition to statutory penalties of up to $25,000 for individuals and $100,000 for corporate entities.

In tandem with the fundraising clampdown, the bill broadens protections against disinformation by extending the prohibition on realistic political deepfakes that could mislead voters ahead of elections. The inclusion of deepfake safeguards reflects a broader concern raised in the lead-up to recent elections elsewhere, emphasizing the growing intersection of technology and electoral integrity.

Context, history, and what comes next

Canada’s stance on crypto political donations has evolved since the practice was permitted in 2019. If enacted, the Strong and Free Elections Act would mark a decisive shift in how digital assets are treated within the political finance framework. The current proposal follows earlier momentum in 2024, when a prior version of the bill—introduced by then-public-safety minister Dominic LeBlanc—failed to advance beyond the second reading in the House of Commons and ultimately died in that session.

Supporters point to the broader regulatory environment around crypto fundraising in other jurisdictions. For instance, the United Kingdom has signaled a similar intent to cap or pause crypto donations in political campaigns, following independent reviews and political pressure. The cross-border dimension underscores a shared concern among Western democracies about the potential for crypto-based contributions to bypass traditional oversight and donor-identification requirements.

Legislation must progress through the standard parliamentary process to become law. After first reading, the bill would require committee scrutiny, a second and third reading in the House of Commons, passage through the Senate, and finally royal assent from the Governor General. As of the introduction, observers will be watching for committee studies, proposed amendments, and any coalition dynamics that shape the bill’s fate in Canada’s Parliament.

For investors and participants in the crypto space, the proposal signals a continued emphasis on regulatory clarity for political fundraising. While the bill targets a narrow channel—donations to parties and election processes—it sits within a broader pattern of tightening controls around crypto-enabled political influence. Market participants should monitor how lawmakers weigh the balance between transparency, donor privacy, and the need to prevent foreign interference as the legislative process unfolds.

As the debate unfolds, readers should watch for updates on parliamentary progress, potential amendments to the scope of prohibited methods, and any alignment or divergence between Canada’s approach and developments in other major democracies. The coming months will clarify whether crypto fundraising becomes a regulated, clearly defined channel or a fully closed one in Canada’s political financing landscape.

Canada’s federal government has proposed a total ban on cryptocurrency donations to political parties, citing concerns that foreign entities could exploit the technology to interfere in elections.

Known as the Strong and Free Elections Act, the bill was introduced on Thursday and proposed to amend the Canada Elections Act to prohibit political parties and third parties involved in the election process from accepting donations in crypto, money orders and prepaid cards to prevent anonymous and “hard to trace contributions.”

The bill’s sponsor, Steven MacKinnon, the leader of the government in the House of Commons, said in an X statement on Thursday that the measures are intended to block foreign interference and other threats to elections.

“With the introduction of the Strong and Free Elections Act, new investments to counter foreign threats and stronger government coordination, we are acting to ensure our elections remain free, fair and secure at all times,” he said.

Canada is not alone in its concerns. The UK government also announced plans for a moratorium on crypto donations on Thursday, following an independent review and pressure from senior politicians.

First attempt at banning crypto donations failed

The current Strong and Free Elections Act had its first reading in the House of Commons on Thursday. To become law, it must progress through several readings and a committee stage in that chamber, then pass through the Senate before reaching the Governor General of Canada for royal assent.

A similar bill was proposed in 2024 by Dominic LeBlanc, then minister of public safety, but it failed to advance past the second reading in the House of Commons and ultimately died.

Crypto political donations in Canada have been permitted since 2019 and are treated similarly to property donations.

Related: Kalshi legal woes grow with Washington state gambling suit

However, a 2024 report by Stéphane Perrault, the chief electoral officer, recommended a ban on crypto political donations altogether on the grounds that it “poses challenges in identifying a contributor.”

Penalties could be up to twice the amount contributed

If the proposed legislation becomes law, contributions made using any of the banned payment methods must be returned, destroyed or delivered to the chief electoral officer.

Penalties for violations could include up to twice the amount contributed, plus $25,000 for individuals and $100,000 for corporate entities.

The bill also proposes expanding existing bans on realistic deepfakes that impersonate electoral candidates to mislead voters. The issue gained attention in the lead-up to the 2024 US elections, with one reported case involving a deepfake of then-President Biden urging voters not to participate.

Magazine: How crypto laws changed in 2025 — and how they’ll change in 2026

TLDR:

- Washington state sued Kalshi on Friday, alleging its prediction market products violate state online gambling laws.

- Nevada secured a temporary restraining order forcing Kalshi to halt sports, election, and entertainment contracts statewide.

- Coinbase, a Kalshi partner, received a preliminary injunction and 60 days to comply with Nevada’s court order.

- Legal experts say the federal versus state jurisdiction clash over prediction markets may reach the U.S. Supreme Court.

Prediction markets platform Kalshi is facing growing legal pressure from multiple U.S. states. Washington state filed a lawsuit against the company on Friday, alleging violations of state gambling laws.

The filing came just one week after Nevada secured a temporary restraining order against Kalshi. Nevada also won a preliminary injunction against Coinbase’s prediction market offerings.

Legal experts now say this dispute could eventually reach the U.S. Supreme Court.

Washington State Targets Kalshi Over Gambling Law Violations

Washington state’s attorney general filed the complaint, arguing that Kalshi operates gambling products in disguise.

According to the state, Washington maintains a tightly regulated gambling market, including a ban on online gambling. The lawsuit alleges that Kalshi bypasses these regulations through its platform.

The attorney general’s office stated that Kalshi’s app displays events and corresponding odds for consumer payouts. Officials argued this model mirrors how traditional gambling operations function.

The state press release noted that Kalshi “advertises that they allow consumers to ‘bet on anything’ by simply calling their service a ‘prediction market‘ rather than ‘gambling.’”

The lawsuit further claimed that Kalshi’s products promoted gambling addiction and specifically targeted college students.

Kalshi responded by filing to move the case to federal court. The company said it was already litigating similar issues in other federal courts at the time.

Kalshi’s head of communications, Elisabeth Diana, addressed the attorney general’s claims directly. “If AG [Nicholas] Brown hadn’t sued us ahead of our scheduled meeting with him, he would have known better than to say we offer war markets. We don’t,” she said.

Diana added that the suit itself only named a contract about when Iran’s former Supreme Leader would leave office, not a war market.

Nevada Courts Move Against Both Kalshi and Coinbase

Nevada’s legal actions against prediction market providers came ahead of Washington’s filing. An appeals court victory allowed Nevada to obtain a temporary restraining order against Kalshi.

Under the order, Kalshi was required to remove sports, entertainment, and election contracts from the state for at least two weeks.

A hearing is scheduled for Friday, April 3, where a state judge will decide on extending those restrictions. Trade publication Gambling Insider reported that Kalshi’s Nevada users could still access the platform after the order took effect. This raised questions about enforcement of the temporary restraining order.

Nevada also secured a preliminary injunction against Coinbase, which partners with Kalshi on prediction market offerings.

District Judge Kristin Luis noted that Coinbase did not dispute offering event-based contracts tied to sporting events and elections. The court gave Coinbase 60 days to make technological changes to comply with the order.

Diana maintained that Kalshi’s legal standing remains firm across jurisdictions. “As other courts have recognized, Kalshi is a regulated, nationwide exchange for real-world events, and it is subject to exclusive federal jurisdiction,” she said. “We are confident in our legal arguments,” she added.

Stablecoins have returned to the forefront of crypto discourse, but the reasons behind the attention have split into starkly different trajectories. Circle’s sharp sell-off this week highlights how regulatory headlines can swing crypto equities even when the underlying business remains intact. At the same time, Canada is quietly laying the groundwork for stablecoin integration into traditional finance, signaling a more deliberate, institution-forward path. Against that backdrop, prediction markets face growing regulatory scrutiny, while a fresh Forrester thesis argues that AI-enabled agents could finally unlock a viable micropayments economy.

Taken together, the week’s developments illustrate a market where regulation, automation, and institutional adoption are reshaping how value moves across crypto rails—and where the implications extend beyond traders to users, issuers, and the builders carving out the next phase of the ecosystem.

Key takeaways

- Circle’s roughly 20% share decline followed reports that a draft CLARITY Act could curb stablecoin rewards. Bernstein analysts argue the market’s reaction may be overstated, noting the bill targets reward distribution rather than the issuer’s core revenue model.

- Circle’s main earnings come from reserve income on USDC, not yield paid to users. Bernstein estimates reserve income could reach about $2.6 billion in 2025, suggesting the draft legislation may have limited direct impact on issuer economics.

- Canada accelerates institutional readiness for stablecoins through Deloitte Canada’s partnership with Stablecorp to pilot QCAD integration, signaling a pathway for fiat-backed digital assets within existing payment and settlement frameworks.

- Polymarket is overhauling its rules to address insider trading and manipulation concerns, tightening design criteria, outcome-resolution standards, and surveillance across both its decentralized platform and US-regulated exchange.

- Forrester signals a turning point for micropayments as AI agents automate small transactions. Stripe’s Machine Payments Protocol (MPP) is cited as an early model, with agent-enabled payments potentially enabling new pay-per-use models and a stronger appetite for low-cost, high-frequency rails—including stablecoins.

Regulatory headlines put stability to the test

The current cycle of regulation-focused headlines has put stablecoins back in the spotlight, with Circle bearing the brunt of market concern. A draft version of the CLARITY Act—intended to regulate crypto platforms and their handling of user-generated yields—has stirred speculation that passive stablecoin holdings could be restricted from earning yields. Analysts at Bernstein argue, however, that the market is conflating “who earns yield” with “who distributes yield.” In their view, the draft would primarily target platforms that pass yield to users, while the issuer’s own economics remain anchored in reserve income on USDC rather than yield distributions.

Circle’s revenue model centers on the interest earned from reserves backing USDC, much of which is invested in short-term U.S. Treasuries. Bernstein’s takeaway is that even with potential pressure on reward structures, the core reserve-income stream could remain robust enough to cushion any policy-induced changes. They estimate that reserve income for 2025 could reach around $2.6 billion, a figure that underscores the resilience of issuer economics in a more restrictive yield environment.

As policymakers weigh the balance between consumer protections and the growth of digital money, the sector will be watching closely how carve-outs in such legislation might preserve certain incentive structures tied to user activity, such as payments or trading, without undermining the fundamental reserve-backed model that underpins major stablecoins.

Canada moves to anchor stablecoins in traditional finance

In a sign of growing institutional appetite, Deloitte Canada has teamed up with Stablecorp to bring stablecoin infrastructure into Canada’s financial system. The collaboration centers on integrating QCAD, a Canadian dollar–pegged stablecoin, into payment and settlement workflows, a move aimed at helping financial institutions prepare for broader adoption even as formal regulatory parameters take shape.

QCAD is designed as a fully backed digital version of the Canadian dollar, aligning with expected regulatory standards around reserves, compliance, and risk management. By weaving stablecoins into backend settlement and real-time payment rails, the initiative envisions around-the-clock settlement, enhanced transparency, and streamlined cross-border workflows once regulatory guardrails become clearer.

The Deloitte-Stablecorp initiative signals a pragmatic approach: build the rails inside regulated institutions first, then scale to broader use cases as rules evolve. If Canada’s formal framework materializes as anticipated, institutions may begin pilot programs that demonstrate how fiat-backed digital assets can augment efficiency and resilience in traditional finance—without sacrificing the protections and oversight that markets expect.

Prediction markets tighten controls amid manipulation concerns

Polymarket, a notable player in the prediction market space, is overhauling its rulebook in response to intensified scrutiny over insider trading and market manipulation. The updates apply to both its decentralized platform and its US-regulated exchange, signaling a broader industry push toward stricter compliance standards.

Key elements of the reform include tighter market design rules, clearer criteria for resolving outcomes, and expanded surveillance systems designed to detect suspicious activity. The platform is also curbing certain markets deemed highly manipulable or ethically sensitive, reflecting regulators’ concerns that prediction markets can blur the line with traditional financial markets and gambling.

The changes come at a moment when lawmakers and observers worry that privileged information could disproportionately influence event outcomes, particularly in geopolitical or political contexts. By sharpening governance and risk controls, Polymarket aims to bolster legitimacy with regulators while preserving the core value proposition of forecast markets—transparent price discovery informed by collective intelligence.

AI-enabled micropayments: engineers’ next frontier

A new Forrester analysis argues that the long-promised micropayments economy could finally gain traction through AI agents. The report highlights Stripe’s Machine Payments Protocol (MPP) as an early example of this trend, showing how a coordination layer can enable machine-to-machine payments across existing systems rather than requiring a brand-new network.

According to Forrester, micropayments have historically stalled due to user friction: repeatedly approving small transactions becomes a tedious barrier. AI agents change that dynamic by performing payments automatically as tasks are completed, removing the need for manual authorization at checkout. This could unlock pay-per-use services and automated digital commerce, expanding demand for low-cost, high-frequency payment rails—including stablecoins as a practical settlement layer.

Analyst Meng Liu notes that prior attempts to realize micropayments faltered for structural reasons, but the emergence of agent-driven models could finally deliver a workable pathway. If these systems achieve scale, they could reshape business models that rely on microtransactions—ranging from content and software access to on-demand services—while reinforcing the role of stablecoins and other near-zero-fee, high-speed payment rails in everyday commerce.

As these threads converge, investors and builders should watch regulatory clarity in key markets, the pace of institutional pilots for fiat-backed digital assets, and the practical adoption of AI-powered payments in real-world workflows.

—

Washington sues Kalshi amid widening crackdown on prediction markets

Washington state filed a civil complaint on Friday accusing Kalshi Inc. of violating the state’s gambling laws by operating its online prediction-market platform without proper licensing. The case relies on Washington’s prohibition on online gambling and stringent gaming oversight, arguing that Kalshi’s offerings fall squarely within the state’s definition of gambling. The complaint was filed in King County Superior Court.

In its announcement, the Washington Attorney General’s office described Kalshi’s platform as showing “a range of events that they can bet on and the odds for those various events, which dictate how much the bettor will be paid out if the event occurs.” The AG’s office argued that Kalshi markets itself as a mechanism to “bet on anything,” and that labeling the service a “prediction market” does not remove it from gambling classifications. Announcement.

Kalshi promptly sought to remove the suit to federal court, arguing that the issues are already the subject of ongoing federal litigation and that Washington provided no prior warning before filing the complaint.

The action in Washington reflects a broader push by state prosecutors to police what they view as online wagering activities disguised as non-traditional markets. Kalshi’s platform advertises a slate of events with associated odds and payouts, which the AG’s office says mirrors conventional gambling operations even when framed as a prediction market.

Key takeaways

- The Washington complaint asserts Kalshi violated the Washington Consumer Protection Act, Gambling Act, and Recovery of Money Lost at Gambling Act; Kalshi has moved to transfer the case to federal court.

- A Nevada judge issued a 14-day temporary restraining order blocking Kalshi from operating in the state, following a motion from the Nevada Gaming Control Board. The ruling cited the likelihood that Kalshi’s event contracts could breach state gambling laws.

- Arizona Attorney General Kris Mayes announced criminal charges against the companies behind Kalshi, alleging the platform operated an “illegal gambling business in Arizona without a license” and offered illegal election wagering. Report.

- The evolving enforcement landscape shows regulators in multiple states scrutinizing prediction-market operators, complicating whether such platforms should be regulated as gambling or under different statutory regimes. Kalshi has argued that federal oversight via the CFTC should apply, given its interpretation of the platform’s contracts as beyond state gambling definitions.

- For investors and users, the string of state actions underscores ongoing uncertainty around the legality and governance of prediction markets in the United States, with outcomes potentially shaping how similar platforms operate going forward.

Washington’s case, Nevada’s ruling, and the broader regulatory backdrop

Washington’s complaint frames Kalshi’s product as a traditional betting market in disguise. The attorney general’s filing emphasizes that Kalshi’s contracts “risk money, rely in part on chance, and promise a payout to winners,” characteristics the state argues align with gambling behavior under Washington law. The state’s action also notes that Kalshi markets itself as a platform where users can “bet on anything,” bolstering the case that the activity falls outside the bounds of a mere educational or informational tool.

Kalie’s response to the Washington action centers on jurisdiction. By seeking federal transfer, Kalshi contends that the core issues are already being litigated in federal venues and that the state’s suit lacks sufficient warning or dialogue prior to filing. The dispute taps into a broader legal debate about whether prediction-market contracts should be regulated exclusively by the Commodity Futures Trading Commission (CFTC) or by state gambling authorities.

In Nevada, the temporary restraining order illustrates how state regulators are ready to curb Kalshi’s activities while litigation continues. Nevada’s decision aligns with a broader trend in which state authorities have pressed cases against Kalshi to determine whether its event contracts violate local gambling statutes. The court’s action underscores the friction between state-level enforcement and Kalshi’s insistence on federal jurisdiction.

Arizona’s criminal charges amplify the sense that Kalshi faces a sprawling, multi-jurisdictional legal challenge. The state’s action, described by authorities as targeting an “illegal gambling business” and unlicensed betting on elections, adds to the pressure on Kalshi’s operations across the country. This constellation of cases comes as lawmakers scrutinize prediction markets for potential insider-information risks tied to government actions, particularly bets on military events or policy moves.

Looking ahead, observers will be watching how the Washington case intersects with Nevada’s TRO and Arizona’s charges. A key question is whether federal courts or state authorities will prevail in defining Kalshi’s legal footing, and how much of the regulatory burden may shift onto operators of prediction markets. The outcome could establish a precedent for how prediction markets are regulated in the United States and influence whether other platforms adapt, relocate, or modify their products to comply with state gaming statutes.

Readers should monitor forthcoming court filings and state-agency updates as regulators continue to test the boundaries of what counts as gambling in the context of modern, online, and market-based prediction tools. The evolving stance across jurisdictions will likely determine the near-term viability of Kalshi’s business model and shape the regulatory playbook for similar platforms.

TLDR:

- Bitcoin has closed red for five straight months, from October 2024 through February 2025.

- A sixth red monthly close would tie the longest losing streak ever recorded in Bitcoin’s history.

- Analyst van de Poppe identifies $60K as the ideal long entry if Bitcoin continues sweeping lower

- A clear break above $71K is the key level analysts say could fully reverse Bitcoin’s bearish trend.

Bitcoin is facing one of its most closely watched monthly closes in recent memory. The leading cryptocurrency has recorded red monthly closes for five straight months, from October through February.

March is on course to extend that run to six months. Currently trading at $66,000, the asset remains down on the month.

A sixth red monthly close would tie the longest streak in Bitcoin’s history. That record was last set between August 2018 and January 2019.

Bitcoin’s Longest Losing Streak on Record Within Reach

The asset closed red in October, November, December, January, and February, marking five straight losing months. Trader Jeremy, known as @Jeremybtc on X, noted the historic nature of this run.

He pointed out that six consecutive red closes would match a record set between August 2018 and January 2019. March closes on Tuesday, with the price still sitting below its monthly open.

That prior streak bottomed with Bitcoin near $3,400 at its lowest point. The asset then rallied roughly 300% over the following five months.

The 2018–2019 cycle remains one of the most referenced periods in the cryptocurrency’s short trading history. Many traders continue using it as a framework for reading current price behavior.

Bitcoin’s current level of $66,000 sits well above those earlier lows. The present correction, therefore, operates from a much higher base than the 2018 example.

Even so, the pattern of consecutive losing months draws clear comparisons between both periods. Traders are watching closely whether March confirms the sixth consecutive red monthly close.

The monthly close carries weight for both short-term traders and long-term holders. Any price movement before Tuesday could still shift the overall outcome.

For now, the current trajectory keeps a record-tying sixth red month firmly in view. Market sentiment has grown cautious as that deadline approaches.

Analysts Outline Key Price Levels to Watch

Crypto analyst Michaël van de Poppe, known as @CryptoMichNL on X, shared his near-term outlook. He described the price action as following the same path seen during a prior consolidation phase.

He added that the asset would likely hold its range briefly before sweeping lower. Van de Poppe identified $60,000 as the ideal entry point for long positions if prices fall further.

The analyst also outlined what could shift his cautious view toward the upside. He stated that a clear break above $71,000 would change the overall perspective on Bitcoin.

Without that breakout level being reached, further downside remains his base case. His stance reflects a measured approach to reading the present market structure.

Van de Poppe further disclosed his personal trading plan heading into April. He said he would dollar-cost average into his altcoin portfolio on April 1st.

Lower prices, in his words, would actually work in favor of that strategy. This method is widely used among experienced traders who treat market dips as accumulation opportunities.

Taken together, both viewpoints place the market at a clear inflection point this week. Lower prices could draw fresh buyers in, while a push higher may restart an upward trend.

Traders remain divided on which outcome emerges next. The Tuesday monthly close may provide the most telling directional signal yet.

TLDR:

- Canada’s Bill C-25 bans crypto, money order, and prepaid card donations across Canada’s political system.

- Canada’s Chief Electoral Officer shifted from tighter regulation to a full ban by November 2024.

- No major federal party has ever disclosed a crypto donation in either the 2021 or 2025 elections.

- Violators face penalties up to twice the contribution’s value, plus $100,000 fines for corporations.

Crypto donations to political campaigns in Canada may soon be prohibited entirely. The federal government introduced Bill C-25, the Strong and Free Elections Act, on March 26, 2026.

The bill proposes a full ban on cryptocurrency, money order, and prepaid card donations across the political system.

This move follows years of concern from Canada’s Chief Electoral Officer about risks to electoral transparency.

A Rarely Used Channel Under Heavy Scrutiny

Canada first permitted crypto donations in 2019 under an administrative framework. That framework classified digital assets as non-monetary contributions, similar to property.

However, no major federal party has ever publicly accepted cryptocurrency donations. Neither the 2021 nor the 2025 elections recorded any disclosed crypto contributions.

Under the original framework, contributions were not eligible for tax receipts. That was a strong disincentive in a system where donors routinely claim tax credits.

Contributors of more than $200 had to be identified publicly by name and address. Only cryptocurrencies with verifiable public blockchains were permitted, excluding privacy coins like Monero and ZCash.

Despite low actual use, Canada’s Chief Electoral Officer grew increasingly concerned over time. In a June 2022 post-election report, the CEO recommended tighter regulation of crypto contributions.

By November 2024, the position had shifted from regulation to a full ban. The CEO stated that contributor identification is “fundamentally difficult,” pointing to cryptocurrency’s pseudo-anonymity as a core transparency challenge.

Bill C-25 is not the first attempt to introduce such a ban in Canada. Its predecessor, Bill C-65, contained identical provisions but died when Parliament was prorogued in January 2025.

The new bill was reintroduced to close what the CEO described as a transparency gap in the electoral financing system. It is currently at first reading in the House of Commons.

Penalties, Deadlines, and a Broader Global Trend

Bill C-25 sets clear deadlines for handling any prohibited contributions already received. Recipients have 30 days to return, destroy, or convert and remit any banned crypto contributions.

Proceeds from converted contributions must be forwarded to the Receiver General. This process covers all registered parties, candidates, and third parties engaged in election advertising.

The penalties for violations are firm and clearly outlined. Maximum administrative penalties can reach twice the value of the offending contribution.

Corporations face an additional penalty of up to $100,000. These measures are intended to discourage any attempt to bypass the ban.

Canada is not acting alone on this issue. The United Kingdom recently announced an immediate moratorium on cryptocurrency donations to political parties.

The UK cited concerns that digital assets could be used, in its own words, to “hide the origins of foreign money” in British politics. Both countries are responding to similar transparency challenges in the evolving digital finance space.

In contrast, the United States continues to permit crypto donations to political campaigns. The Federal Election Commission has offered guidance on disclosing Bitcoin and other crypto contributions since 2014.

Canada’s approach marks a clear departure from the American model. Whether other nations will follow Canada and the UK on this path remains to be seen.

TLDR:

- Tech’s valuation premium compresses to near +4%, the lowest since 2019, signaling weaker growth pricing.

- Rising rates and tighter liquidity reduce the appeal of long-duration tech assets and compress multiples.

- Market leadership is rotating as investors diversify into other sectors and alternative asset classes.

- Broader S&P 500 valuation levels are normalizing, reflecting a shift in risk appetite and positioning.

The S&P 500 Information Technology Index is undergoing a valuation reset as the premium over the broader index compresses.

The decline reflects a shift in investor expectations, driven by macroeconomic conditions and evolving market dynamics.

Valuation Compression and Macroeconomic Pressures

The S&P 500 tech forward P/E premium is near +4%. This marks the lowest level since 2019 and a sharp decline from previous highs above 30%.

The adjustment reflects a more cautious market stance. Earlier in the cycle, tech valuations were supported by low interest rates and strong earnings growth.

However, rising yields and tighter financial conditions have reduced the appeal of long-duration assets. Investors are now demanding higher returns for growth exposure.

The broader S&P 500 forward P/E has also moved closer to long-term averages. This indicates that valuation compression is not limited to technology alone.

Instead, it reflects a broader normalization across equity markets as conditions adjust.

Market Structure, Rotation, and Capital Positioning

The S&P 500 is currently trading within a consolidation range near 6,450–6,700. This range reflects a balance between bullish and bearish positioning as investors respond to macroeconomic data.

The market remains sensitive to shifts in sentiment. Technical indicators suggest short-term weakness alongside long-term stability.

The index is trading below short-term moving averages while remaining above longer-term averages. This structure supports a corrective phase rather than a full reversal.

Capital flows are adjusting in response to the S&P 500 tech valuation compression. Institutional portfolios are exploring sectors with different risk exposures as tech multiples compress.

This has contributed to increased diversification across asset classes. At the same time, alternative assets are gaining attention as part of portfolio strategies.

Bitcoin and related digital assets are being considered for their distinct drivers, including liquidity conditions and monetary trends. This reflects a broader search for diversification.

The current environment shows a transition in market leadership. While technology remains a key driver of innovation and earnings growth, its valuation profile has shifted. Investors are adapting to new pricing dynamics across the equity landscape.

Crypto World

Best Crypto Presale: Claude Mythos Leak Crashes BTC as Pepeto Exchange Draws Buyers While ADA and DOGE Slide

Euro stablecoins now command over 80% of the non USD stablecoin market with supply hitting $1.2 billion, and Visa and Mastercard have expanded settlement support across their networks. But the real story is what happens underneath that growth: every new settlement pathway that opens is another surface where dangerous contracts can intercept transactions.

Investors are trying to enter the best crypto presale before the window closes, and more than $8 million has been raised in the Pepeto presale with analysts projecting 100x as the Binance listing approaches. The exchange is live, and the final hours before listing are where the biggest returns are secured.

Best Crypto Presale: Claude Mythos Leak Crashes BTC as Pepeto Exchange Draws Buyers While ADA and DOGE Slide

Anthropic’s leaked AI model Claude Mythos crashed Bitcoin to $66,000 after internal documents revealed a model capable of rapidly exploiting software vulnerabilities according to CoinDesk. Cybersecurity stocks dropped 4 to 6% while the tech software sector fell nearly 3%. According to Investing.com, the leak heightened concerns about AI driven attacks on crypto infrastructure. The best crypto presale is the entry where verified security is already running, not a feature on a roadmap.

What Is Trending in the Presale Market and Where Real Returns Are Building

Pepeto: The Exchange That Scans Every Contract Before the Reader’s Capital Moves

Pepeto represents the opposite end of the risk timeline from the Claude Mythos leak. Investors are deeply interested in the exchange tools it provides because they give every trader a clear edge in a market where on chain threats are growing. What exists right now is a working platform, a presale closing when the Binance listing opens, and a chance that is measured in days rather than months.

The exchange does something that becomes more valuable as stablecoin volumes grow and on chain activity increases. Every new settlement pathway that Visa and Mastercard open is another surface area where malicious contracts can intercept funds. PepetoSwap processes orders without taking any trading fee so capital stays fully intact, the cross chain connector delivers tokens between networks at zero cost, and the contract scanner confirms every project is clean before a dollar commits, confirmed by a SolidProof audit.

The same person who took the original Pepe token from zero to $11 billion without any products constructed this exchange, and it does all this without requiring the reader to understand what is happening at the code level.

The same person who took the original Pepe token from zero to $11 billion without any products constructed this exchange, and it does all this without requiring the reader to understand what is happening at the code level.

Here is what the entry looks like in numbers. Analysts project 100x from the current entry at $0.000000186, and 191% APY staking adds to every position inside while the listing window closes. The best crypto presale is the entry where verified security meets presale pricing, and once the Binance listing opens this number is gone permanently.

Cardano (ADA)

ADA trades at $0.25 per CoinMarketCap, testing multi month support as the correction drags layer 1 tokens lower.

A recovery to $0.35 delivers 40% over months, meaningful for patient holders, while the presale entry targets 100x from one listing event and the wallets entering are positioned for the returns this cycle produces.

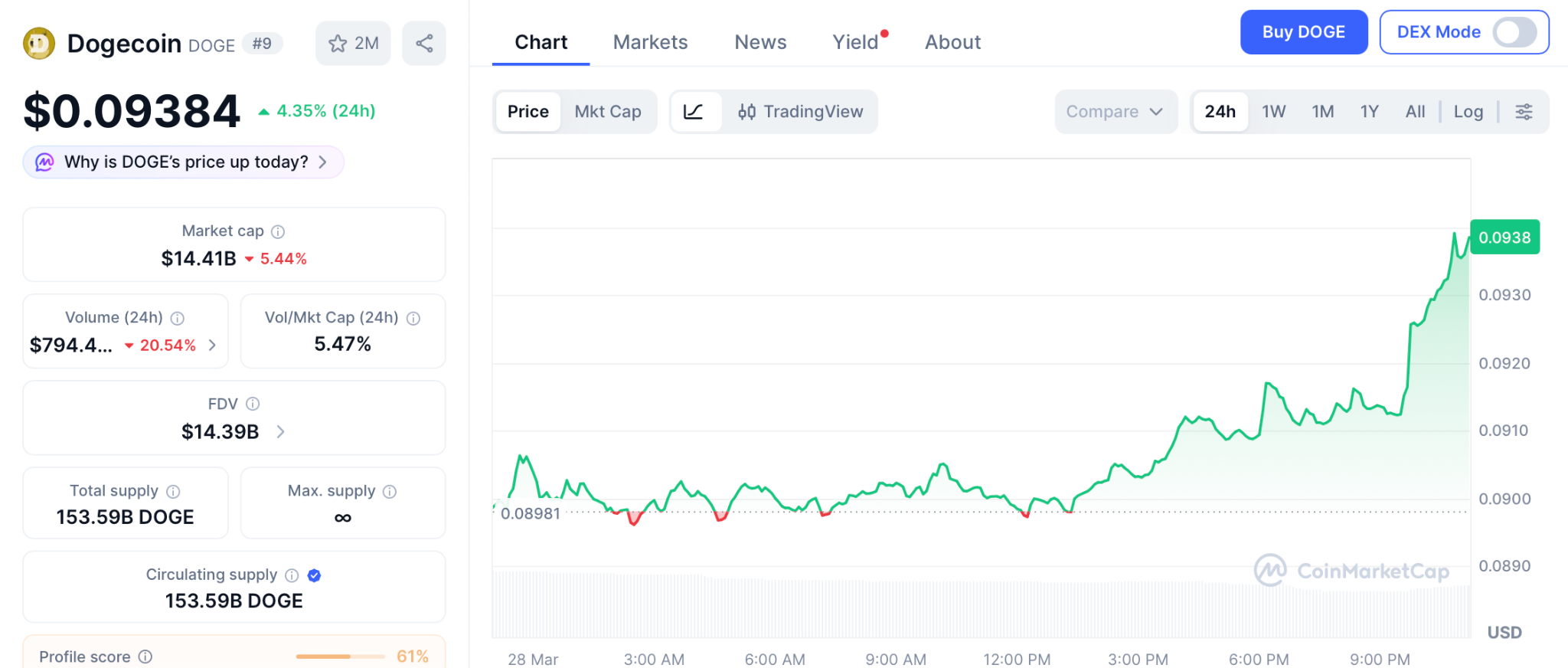

Dogecoin (DOGE)

DOGE trades at $0.093 per CoinMarketCap, holding above key support as the meme sector waits for the next catalyst.

A recovery to $0.12 delivers 32% over months, respectable for meme believers, while presale entries are where the cycle defining returns are built and Pepeto offers that exact math before the Binance listing opens.

The Best Crypto Presale Is Where the Next Dogecoin Forms and the Wallets Inside See the Pattern

The Claude Mythos leak crashed BTC to $66,000, and every previous cycle proved the same thing: once Bitcoin confirms direction, the viral projects with real utility capture the overflow faster than anything else. The addresses filling the best crypto presale are not guessing.

They see the next Dogecoin forming inside Pepeto because no project in 2026 has matched this level of viral energy and no meme coin has ever carried real exchange tools into a listing. The Pepeto official website is where those wallets are entering with size, and once the listing arrives this entry disappears permanently.

Click To Visit Pepeto Website To Enter The Presale

FAQs

Why is Pepeto the best crypto presale as the Claude Mythos leak crashes BTC?

Pepeto is the best crypto presale with a verified exchange that scans every contract before capital enters, more than $8 million raised, and analysts projecting 100x.

What drives demand for the best crypto presale right now?

Real exchange utility combined with limited presale supply creates the conditions for 100x, and the Pepeto official website is where the entry is still open.

How does the best crypto presale protect capital in this market?

Pepeto’s exchange scans every contract before funds move, confirmed by a SolidProof audit, and the Binance listing targets 100x for every wallet entering now.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

TLDR:

- Bitcoin failed to hold above key resistance after a retest, signaling a classic rejection pattern for BTC.

- Analyst Dami-Defi warns that rallies below the yellow line are relief bounces with the $63K zone as next target.

- Coinbase continues selling into every bounce while spot inflows from institutions remain notably absent.

- A weekly close below $68K could confirm deeper downside, with analysts eyeing the $55K to $60K range.

Bitcoin’s price action is drawing serious attention after a failed retest at a key resistance level. The rejection has shifted market sentiment toward the downside.

Analysts are now pointing to the $63,000 demand zone as the next probable target. With no confirmed breakout and weak institutional inflows, the path of least resistance appears to trend lower in the near term.

Failed Retest at Key Resistance Puts $63K in Focus

Bitcoin broke above a critical resistance level but could not sustain the move. The price returned to retest that level and was firmly rejected.

Analyst Dami-Defi flagged this as a textbook breakout attempt followed by retest and rejection. That sequence historically points toward a return into the previous trading range.

Dami-Defi described the behavior as anything but confirmed breakout price action. A legitimate breakout holds above the broken level after the retest occurs.

The failure to do so hands control back to the bears. He maintained a straightforward stance: bearish until the chart proves otherwise on closes.

With BTC trading below the yellow resistance line, rallies carry little conviction. Dami-Defi characterized any upward moves as relief bounces rather than trend reversals.

The $63,000 base, marked as a gray demand zone, now serves as the next key magnet. That area represents where buyers previously stepped in with enough force to matter.

Should that $63,000 zone fail to hold on real closes, the analyst warned of further downside. A clean break below it would shift the chart toward a deeper correction scenario.

Traders are encouraged to focus on closing prices rather than short-term wicks. The rejection at resistance remains the clearest signal guiding this outlook.

Institutional Selling and Macro Weakness Reinforce Downside Risks

Higher timeframe analysis from analyst Junar adds another layer to the bearish case. He pointed out that Bitcoin lost the critical 72,500 level on the higher timeframe chart.

That loss carries weight because it reflects a structural shift in bullish momentum. A reclaim above that level would be needed to revive any serious push toward $79,000.

Until then, Junar noted that Coinbase continues selling into every bounce. Spot inflows from institutional players remain absent at current price levels.

That dynamic limits buying pressure and keeps the market vulnerable to further slippage. Choppy price action is expected to persist over the coming weeks as a result.

A weekly close below $68,000 would serve as the next major warning for traders. Junar identified that level as separating a consolidation phase from a genuine breakdown.

Losing it on closes puts $60,000 squarely in view as the following target. He advised traders to consider building positions gradually in the $55,000 to $60,000 range.

Junar also urged market participants to tune out overly optimistic narratives currently circulating online. Swing trades carry elevated risk under these conditions, making scalping the more practical approach. Until a clear directional shift emerges, patience remains the most disciplined strategy available.

BBC’s ‘best’ true crime doc returns with harrowing 999 call

Answer, Hints and Full Solution for March 29, 2026

Something Very Bad Is Going To Happen Cast: Where You’ve Seen The Netflix Stars Before

-

NewsBeat4 days ago

NewsBeat4 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

News Videos3 days ago

News Videos3 days agoParliament publishes latest register of MPs’ financial interests

-

Sports6 days ago

Sports6 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

Sports6 days ago

Sports6 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Business7 days ago

Business7 days agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Tech6 days ago

Tech6 days agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Tech6 days ago

Tech6 days agoAI enters the chat: New Seattle dating app relies on tech to facilitate meaningful human connections

-

Business2 days ago

Business2 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

News Videos6 days ago

News Videos6 days agoCh 9 Financial Management Part 1 | Detailed One Shot | Class 12 Business Studies Boards 2026

-

NewsBeat1 day ago

NewsBeat1 day agoThe Story hosts event on Durham’s historic registers

-

NewsBeat4 days ago

NewsBeat4 days agoTesco is selling new Cadbury Dairy Milk bar and people can’t wait to try it

-

Business7 days ago

Business7 days agoWill Duke Basketball Win It All? Duke Basketball Enters Second Round as Third Favorite to Claim NCAA Title

-

Sports6 days ago

Sports6 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who hit 12 Derby-Oaks Doubles enters picks

-

Tech5 days ago

Tech5 days agoSamsung will soon let you control smart home devices from your car’s dashboard

-

Entertainment8 hours ago

Entertainment8 hours agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

NewsBeat7 days ago

NewsBeat7 days agoUpdate on Wisbech river crash as search for teenage boy enters fifth day

-

Entertainment6 days ago

Entertainment6 days agoCynthia Bailey Dishes on ‘RHOA’ Season 17, Discusses Kandi

-

NewsBeat6 days ago

NewsBeat6 days agoColombian military plane with 110 soldiers onboard crashes following takeoff

-

Fashion5 days ago

Fashion5 days agoDoes It Matter What You Wear When You’re Laid Off and Looking?

-

Business5 days ago

Business5 days agoMore women enter wealth management, but few in advisory roles: study

You must be logged in to post a comment Login