Business

Netflix Stock Dips Slightly on April 1 as Investors Await Q1 Earnings Amid Recent Price Hikes

Netflix Inc. shares edged lower Wednesday, trading around $95.66 midday after closing at $96.15 the previous session, as Wall Street positioned for the streaming giant’s first-quarter 2026 earnings report scheduled for April 16.

The stock opened near $93 before climbing intraday, reflecting a volatile but relatively contained session. Volume remained active following a strong 3.42% gain on Tuesday, when shares closed at $96.15 on higher-than-average turnover of more than 54 million shares. Year to date, Netflix has posted modest gains of roughly 2.5%, though it remains well below its 52-week high of $134.12 reached in mid-2025.

Analysts and investors are closely watching how recent subscription price increases and advertising-tier momentum will shape the upcoming results. On March 25, Netflix quietly raised prices across all plans without a formal announcement. The standard ad-free tier jumped to $19.99 monthly from $17.99, the premium plan rose to $26.99, and the ad-supported option increased by $1 to $8.99. It marked the company’s fifth price hike in six years, underscoring its pricing power in a competitive streaming landscape.

“Netflix continues to demonstrate strong monetization capabilities,” one market observer noted, pointing to the company’s ability to pass on costs while maintaining subscriber loyalty. The moves come as Netflix eyes further growth in advertising revenue, which more than doubled in 2025 to over $1.5 billion and is projected to roughly double again in 2026.

Recent Performance and Market Context

Netflix shares have shown resilience in recent weeks despite broader market fluctuations. Tuesday’s advance followed positive reactions to the price adjustments, with some sessions seeing gains of more than 1%. However, the stock has traded in a wide range over the past year, dipping as low as $75.01 amid concerns over content spending, competition and earlier uncertainty surrounding a potential Warner Bros. Discovery acquisition that Netflix ultimately walked away from.

As of early April 1 trading, the stock was down about 0.48% at $95.66, with a market capitalization hovering near $406 billion. The price-to-earnings ratio stood around 46, reflecting expectations of continued profitability growth even as the company invests heavily in content.

Wall Street maintains a generally optimistic stance. Consensus analyst ratings lean toward “moderate buy,” with an average price target suggesting potential upside of around 19-20% from current levels. Optimism stems from Netflix’s massive global subscriber base — which surpassed 325 million paid members by the end of 2025 — and steady expansion into live sports, gaming and international markets.

Q1 Earnings on the Horizon

Netflix is set to release its first-quarter 2026 financial results after the market close on April 16, followed by a live video interview with co-CEOs Ted Sarandos and Greg Peters, along with Chief Financial Officer Spence Neumann. Investors will scrutinize several key metrics:

- Subscriber growth and retention: How the recent price hikes affect churn rates.

- Advertising revenue: Progress toward doubling ad income in 2026.

- Content spending: The company has signaled heavier investment this year, which could pressure margins in the short term.

- Free cash flow and profitability: Guidance for the full year will be closely parsed.

For the first quarter, analysts expect revenue around $12 billion or higher, building on the fourth-quarter 2025 results that showed 18% year-over-year growth to more than $12 billion and earnings per share of 56 cents, narrowly beating estimates.

Full-year 2026 revenue guidance issued earlier pointed to a range of $50.7 billion to $51.7 billion, driven by membership gains, pricing and advertising. Operating margins are targeted to improve, though increased content outlays — potentially reaching $20 billion annually — remain a focus for cost-conscious investors.

Strategic Shifts and Competitive Landscape

Netflix has pivoted aggressively in recent years. The introduction and expansion of its ad-supported tier has opened new revenue streams, appealing to price-sensitive viewers while allowing the company to maintain premium offerings for others. Live programming, including sports events and unscripted specials, has helped differentiate the platform from rivals like Disney+, Amazon Prime Video and emerging competitors.

The company also collected a significant $2.8 billion breakup fee after stepping away from a bid for Warner Bros. Discovery assets, providing a cash cushion as it prioritizes organic growth and share repurchases in the longer term.

Challenges persist. Heavier 2026 content spending could weigh on margins, and competition for viewer attention remains fierce. Some analysts have flagged risks of slowing subscriber additions in mature markets, though international expansion continues to offer tailwinds.

Bay Area-based Netflix, with its headquarters in Los Gatos, continues to be a bellwether for the technology and entertainment sectors. Its performance influences broader sentiment toward streaming stocks and ad-supported digital media.

What Investors Are Watching

Market participants are weighing several factors heading into earnings season:

- Impact of price increases: Will higher bills lead to cancellations, or will loyal subscribers absorb the changes as they have in past rounds?

- Ad tier traction: Growth in this segment is critical for long-term revenue diversification.

- Content pipeline: Upcoming releases and original programming slate for the remainder of 2026.

- Macro environment: How inflation, consumer spending and global economic conditions affect discretionary entertainment budgets.

Some voices on Wall Street have expressed caution, noting that Netflix shares have lagged the broader market over certain periods despite strong fundamentals. Others argue the current valuation offers an attractive entry point for a company with proven scalability and a massive addressable audience.

Social media and trading forums buzzed Wednesday with mixed commentary. Some users highlighted the stock’s recent stability as a positive sign, while others pointed to the upcoming earnings as a potential volatility catalyst.

Broader Industry Implications

Netflix’s trajectory carries weight beyond its own balance sheet. As the pioneer of streaming, its success or struggles often set the tone for peers. Recent price adjustments across the industry suggest many platforms are testing similar monetization strategies.

Meanwhile, the entertainment landscape evolves rapidly with technological advances in artificial intelligence for content creation, personalized recommendations and competitive bidding for sports rights.

For retail investors, particularly those in tech-heavy regions like the San Francisco Bay Area, Netflix remains a core holding or watchlist staple. Its ability to adapt — from DVD rentals to global streaming dominance — has long captivated shareholders.

Outlook and Advice for Investors

With Q1 results less than two weeks away, analysts recommend reviewing individual risk tolerance before making moves. Long-term bulls point to Netflix’s track record of innovation and subscriber monetization as reasons for confidence. Bears cite elevated content costs and valuation multiples as areas of concern.

Diversification remains key. While Netflix has delivered extraordinary returns over two decades — turning early investments into life-changing gains for many — past performance does not guarantee future results.

Investors can track real-time quotes on platforms like Yahoo Finance, Nasdaq.com or their brokerage accounts. Official updates will come via Netflix’s investor relations site ahead of the April 16 release.

As midday trading continued on April 1, the slight dip appeared contained, with many viewing it as routine profit-taking after Tuesday’s advance rather than a shift in sentiment. Attention now turns squarely to the earnings report, which could set the narrative for Netflix’s stock through the spring and beyond.

Whether the streaming leader sustains its momentum or faces renewed pressure will depend on execution in a crowded digital entertainment arena. For now, the market awaits fresh data with cautious optimism.

How I Would Invest $1 Million Today

Small details can sink large tax deductions for charitable donations.

A case in point: Two recent Tax Court decisions involving first cousins who donated 13.3 acres of land to Highland City, Utah, in 2018. The judge ruled that Stephen Martin and Clint Martin, who were close growing up and later did business together, can’t deduct $665,000 for the land donation. A limited liability company owned by the cousins acquired the land for $22,000 at a delinquent-tax auction in 2014.

Copyright ©2026 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

Middle East conflict and rising oil prices could weaken the Thai baht to 33 per dollar. Thailand’s reliance on oil imports makes it vulnerable to increased costs, potentially impacting its trade balance and currency value.

Key Points

- The Thai baht could weaken beyond 33 per US dollar due to rising Middle East war-driven oil prices.

- Thailand’s status as a net oil importer means higher import costs, potentially shifting its trade surplus into a deficit and increasing baht volatility.

- In a prolonged conflict, oil prices exceeding $100 per barrel would likely push the baht to near 33 against the dollar.

Escalating Middle East Conflict’s Impact on the Baht

The ongoing escalation of conflict in the Middle East poses a significant threat to the Thai baht, with K-Research predicting a potential weakening to 33 baht per US dollar. This projection is primarily driven by the anticipated surge in global oil prices. As a net oil importer, Thailand faces a substantial increase in its import bill, which directly impacts its trade balance. The baht has already experienced a decline, reaching a three-month low, reflecting capital flight towards the US dollar as a safe-haven asset. This trend is further bolstered by expectations that the US Federal Reserve may adopt a more cautious approach to interest rate cuts due to rising inflation.

Economic Ramifications of Sustained High Oil Prices

Should the conflict in the Middle East persist, leading to a prolonged period of high oil prices, the economic consequences for Thailand could be severe. K-Research estimates that if oil prices consistently exceed $100 per barrel, the baht is highly likely to depreciate towards the 33 mark. This scenario would drastically erode Thailand’s trade surplus, potentially pushing it into a deficit. The country’s significant reliance on oil imports, accounting for approximately 5-6% of its GDP, makes it particularly vulnerable compared to neighboring Southeast Asian nations. This heightened economic vulnerability contributes to increased volatility in the baht.

Increased Baht Volatility and Market Outlook

Beyond the direct impact on oil prices, the geopolitical tensions are contributing to increased volatility in the baht. Year-to-date, baht volatility has risen to 7.7%, surpassing the median for regional currencies. This elevated volatility, coupled with other domestic economic pressures, creates an uncertain trading environment. In the near term, SCB Financial Markets anticipates the baht to trade within a range of 31.6 to 31.9 against the US dollar. This outlook is influenced by the strengthening of the dollar index, driven by the intensifying fighting in the Middle East and the consequent demand for the greenback as a secure investment.

Source : Bangkok Post – Baht faces pressure from oil upswing

Other People are Reading

I Wouldn't Want To Retire Without These 3 Investments

For the full financial year 2025-26, revenue from operations rose 11.9% to Rs 7,620.9 crore from Rs 6,807.9 crore in FY25. Net profit for the year increased 12.8% to Rs 268.7 crore, compared with Rs 238.3 crore in the previous financial year.

The company said its results include the financial impact of the amalgamation of Sir Shadi Lal Enterprises Ltd, effective April 1, 2025. The figures have been restated to reflect the acquisition date of June 20, 2024.

Triveni Engineering said the National Company Law Tribunal-approved Composite Scheme of Arrangement became effective on May 19, 2026, completing the merger and demerger process. Under the scheme, Sir Shadi Lal Enterprises has been amalgamated with Triveni, while the Power Transmission Business will be demerged into Triveni Power Transmission Ltd with effect from April 1, 2026.

The accounting impact of the demerger will be reflected in FY27. FY26 will be the last year in which the Power Transmission Business forms part of Triveni Engineering’s consolidated results. The business, which operates in the gears and defence segments, will be pursued independently under Triveni Power Transmission Ltd from FY27.

NEW YORK — Seagate Technology Holdings plc (NASDAQ: STX), a leading provider of data storage solutions, has seen its shares climb sharply in 2026 amid surging demand for high-capacity hard disk drives fueled by artificial intelligence infrastructure needs. Trading near $880 in late May, the stock carries a consensus Moderate Buy to Strong Buy rating from analysts, though elevated valuations prompt questions about whether to buy or sell ahead of further AI-driven growth.

The Fremont, California-based company reported strong fiscal third-quarter 2026 results in late April, with revenue reaching $3.11 billion, up 44% year-over-year and beating estimates. Non-GAAP earnings per share hit $4.10, exceeding forecasts, while gross margins expanded to record levels around 47%. CEO Dave Mosley highlighted robust cloud customer demand for the tenth consecutive quarter.

For the fiscal fourth quarter, Seagate guided revenue to $3.45 billion, plus or minus $100 million, and non-GAAP EPS of $5.00, plus or minus $0.20, signaling continued momentum. Management raised its long-term annual revenue growth target to a minimum of 20% over the next several years, citing structural shifts from AI.

Analyst coverage remains predominantly bullish. Across 20-25 firms, the consensus stands at Moderate Buy or Strong Buy, with roughly 20 Buy ratings, a handful of Holds and minimal Sells. Average 12-month price targets range from approximately $746 to $834, implying potential downside from current levels for some models, though high targets reach $1,140 and optimistic calls hit $1,000 or more.

Recent adjustments include Barclays raising its target to $1,000, BofA to $900, and Evercore ISI to $1,000, reflecting confidence in sustained hyperscaler spending. Rosenblatt set a $1,000 target post-earnings, while others maintain Buy ratings citing margin expansion and product leadership.

Seagate’s positioning benefits from the AI data explosion. Hard disk drives remain critical for cost-effective mass storage in data centers, where AI training and inference generate unprecedented volumes of data. The company’s Mozaic platform with Heat-Assisted Magnetic Recording (HAMR) technology enables higher capacities, such as 40TB+ drives, supporting cloud providers’ needs.

Exabyte shipments reached 199 in the March quarter, up 39% year-over-year. Management noted strong visibility from customer agreements and expects sequential growth and margin gains into fiscal 2027.

For investors leaning buy, the thesis centers on a multi-year AI storage supercycle. Seagate’s near-monopoly in high-capacity HDDs for enterprise, combined with improving margins and free cash flow nearing $1 billion per quarter, supports potential re-rating. Some models project fiscal 2026 revenue around $10-11 billion with continued EPS growth.

Valuation has expanded significantly from prior years, with shares up over 600% from 2025 lows. Forward multiples sit above historical averages, raising concerns for bears about execution risks or potential slowdown in AI capex. Competition from solid-state drives could pressure the HDD market longer-term, though cost advantages favor disks for bulk storage.

Financial health appears solid. The company has generated strong cash flow, enabling debt management and returns to shareholders. Recent note exchanges adjusted capital structure without major dilution concerns. However, cyclical exposure to tech spending remains inherent.

Broader industry trends reinforce the opportunity. Hyperscalers continue building out AI clusters, requiring vast storage layers. Seagate’s innovations in energy-assisted recording position it to capture share as capacities scale. CEO Mosley emphasized that agentic AI will further accelerate data creation and retention needs.

Risks include supply chain constraints for advanced components, potential moderation in AI investment if economic conditions shift, and high customer concentration. Insider selling has occurred at elevated prices, though often tied to compensation plans.

Portfolio considerations suggest Seagate fits growth-oriented technology or thematic AI allocations. Position sizing should reflect volatility, as the stock has experienced sharp swings despite the uptrend. Near-term catalysts include fiscal fourth-quarter results in late July and updates on Mozaic 4+ ramp.

Longer-term projections vary. Optimistic scenarios tied to 20%+ annual growth and margin targets see substantial upside if AI adoption accelerates. Conservative views factor in potential saturation or technology transitions, tempering expectations. Discounted cash flow models have at times suggested undervaluation relative to growth.

In the current environment, Seagate exemplifies how legacy hardware players can thrive in the AI era by addressing foundational infrastructure needs. While not immune to broader market corrections or sector-specific headwinds, its execution on financial metrics and roadmap has sustained analyst enthusiasm.

Investors evaluating a position should weigh their horizon and risk appetite. Those convinced of prolonged AI data center buildouts may see current levels as reasonable entry despite the run-up, particularly on pullbacks. Others may monitor for clearer signals on margin sustainability or competitive dynamics before committing.

As with technology hardware stocks, thorough analysis of quarterly trends and industry developments is advised. Seagate’s performance will depend on maintaining leadership in high-capacity storage amid rapid evolution in data center architectures. The ongoing AI investment cycle is expected to provide further clarity on the company’s ability to deliver sustained shareholder value through 2026 and beyond.

LONDON — British royal officials are considering plans to reverse extensive renovations made to Frogmore Cottage, the former Windsor home of Prince Harry and Meghan Markle, three years after the couple vacated the property at the request of King Charles III. The potential changes could restore elements of the Grade II-listed building to its pre-Sussex configuration, including possibly subdividing it back into separate units.

The property, gifted to the couple by Queen Elizabeth II in 2018, underwent a reported £2.4 million ($3 million) refurbishment before they moved in. The work included structural updates, new utilities and personalized features such as a yoga studio. Harry and Meghan later repaid the costs from their own funds after stepping back as working royals in 2020.

According to reports, the cottage has stood largely empty since the couple’s eviction in 2023. Assessments are now underway to determine future uses, with one option being to undo some of the couple’s modifications to make the residence more suitable for other royal staff or to return it closer to its original layout as two semi-detached homes. No construction work has begun, and Buckingham Palace has declined to comment.

The news, first reported by The Sun on May 27, has renewed public interest in the property’s role within the royal estate. Frogmore Cottage sits on the grounds of Windsor Castle, part of the Crown Estate. Any future renovation costs would likely fall under the Sovereign Grant, funded by taxpayers.

The original renovation drew significant scrutiny at the time due to its expense. Updates reportedly encompassed new heating, wiring, plumbing and interior customizations to transform the historic structure into a family home for the then-newlywed couple and their son Archie. The couple moved in shortly before Archie’s birth in 2019.

Since departing the U.K. for California, Harry and Meghan have maintained a strained relationship with senior royals. The 2023 request for them to vacate Frogmore came amid ongoing tensions, including the publication of Harry’s memoir “Spare.” The property has remained unoccupied, prompting discussions about its efficient use within the royal portfolio.

Royal property management often balances historic preservation with practical needs for staff housing. Sources familiar with the planning process indicated that experts are evaluating the feasibility and cost of reverting modifications. Subdividing the cottage could allow it to accommodate multiple households, potentially increasing its utility on the estate.

The Grade II listing imposes restrictions on alterations to protect the building’s architectural heritage. Any reversal would require careful planning to comply with preservation standards while addressing modern functionality. Insiders described the process as complex and potentially expensive, though exact figures for new work remain undisclosed.

Public reaction has been mixed. Some view the potential changes as a pragmatic step to repurpose a vacant royal asset, closing a chapter associated with the Sussexes’ time as working royals. Others criticize it as wasteful spending on already-renovated property, especially given broader cost-of-living pressures. The story has fueled ongoing tabloid coverage of royal family dynamics.

Harry and Meghan have built new lives in Montecito, California, where they reside with their two children. Their Archewell Foundation continues philanthropic efforts, and the couple has pursued media projects, including Netflix documentaries and Harry’s published writings. They have made occasional visits to the U.K. but maintain a reduced official role.

The Frogmore situation reflects broader adjustments within the royal household under King Charles. The monarch has sought to streamline operations and address multiple vacant or underutilized properties across estates. Similar discussions have involved other residences, including those linked to Prince Andrew.

Property experts note that royal homes often undergo cycles of renovation as occupants change. Frogmore Cottage’s history dates back over two centuries, originally serving as a retreat associated with Queen Charlotte. Its evolution from staff housing to a consolidated family home and potentially back illustrates shifting royal needs.

Buckingham Palace’s longstanding policy of not commenting on private family matters or internal property decisions leaves many details unconfirmed. The Crown Estate manages such assets separately but coordinates with royal needs. Any public expenditure on reversals could face questions in future Sovereign Grant reports.

For now, the cottage stands as a symbol of a transitional period in royal history. The couple’s brief occupancy marked a modern chapter that ended amid high-profile departures and public debates over royal funding and relevance. Whether full reversal proceeds depends on ongoing assessments balancing cost, heritage and utility.

Observers suggest the move, if implemented, would represent another step in reconfiguring royal living arrangements. With no immediate occupants identified, officials appear focused on long-term practicality. The saga continues to captivate audiences interested in the intersection of monarchy, property and family relations.

As evaluations continue, the future of Frogmore Cottage remains fluid. It joins a list of royal properties whose roles adapt with each generation. The potential undoing of the Sussex-era changes underscores how even personal homes within the institution can reflect larger institutional priorities.

The developments arrive as the royal family navigates public scrutiny and operational efficiency. King Charles has emphasized sustainability and modernization in estate management. Any decision on Frogmore will likely prioritize functionality for current royal needs over past associations.

In the meantime, the story serves as a reminder of the complexities surrounding royal residences. From initial taxpayer-funded upgrades to repayment and now potential reversal, Frogmore Cottage’s journey highlights the financial and symbolic weight attached to such properties. Further updates may emerge as assessments conclude.

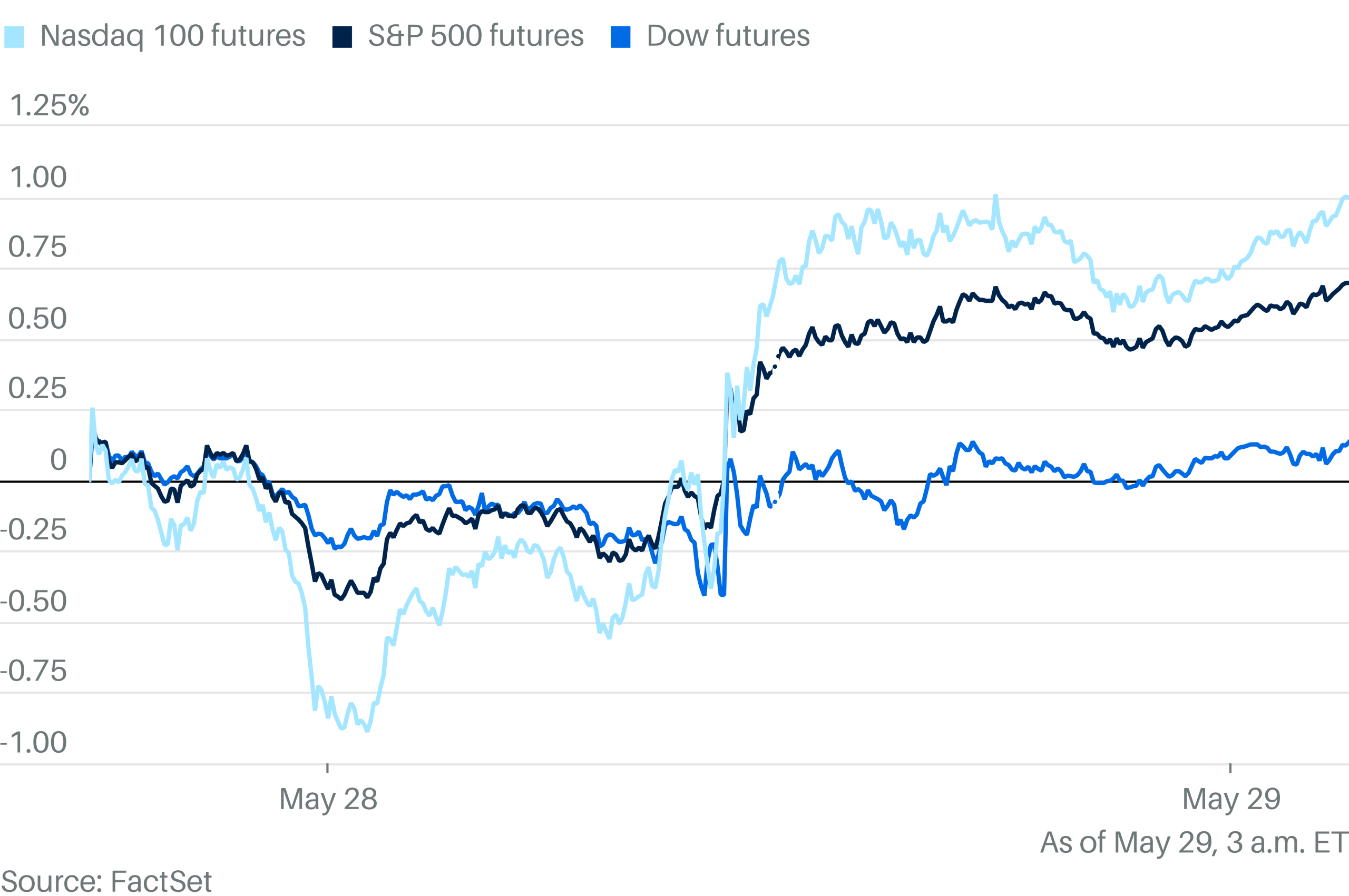

Stocks looked set to rise on the last trading day of May, putting the S&P 500 on course for a ninth straight week of gains.

Futures tracking the S&P 500 climbed 0.1% on Friday. Contracts tied to the tech-heavy Nasdaq 100 also rose 0.1%. Dow Jones Industrial Average futures were up 74 points, or 0.2%. The three major indexes eked out record closing highs on Thursday thanks to a rally in software stocks.

The market has been on a tear since late March, with the Nasdaq about to notch its best two-month stretch since November 2002, according to Dow Jones Market Data. The S&P 500 is headed for its best two-month spell since May 2020.

With the 2026 FIFA World Cup just weeks away, the world’s top national teams are finalizing preparations for the largest tournament in history. Hosted across the United States, Canada and Mexico from June 11 to July 19, the 48-team event promises high drama as favorites like Spain and France lead a competitive field chasing the ultimate prize.

Betting markets and expert analyses consistently place Spain as narrow favorites, followed closely by France, with a cluster of European and South American powerhouses rounding out the top contenders. The expanded format adds unpredictability, but pedigree, form and squad depth point to a familiar group of elites.

Here is an analysis of the top 10 teams most likely to contend for the title, based on current FIFA rankings, recent performances, betting odds and projections as of late May 2026.

1. Spain (+450 to +475)

Spain enters as the team to beat after winning Euro 2024 in commanding fashion. Luis de la Fuente’s side boasts a dynamic young core led by Lamine Yamal, Pedri and Rodri. Their possession-based style, combined with tactical flexibility, makes them formidable.

Yamal, despite a recent hamstring injury that could sideline him for Spain’s opener, remains a key threat and is expected to feature. Spain’s midfield control and depth give them an edge in a grueling schedule. Projections show them with the highest expected goals and tournament win probability around 20-26%.

2. France (+480 to +500)

The reigning FIFA No. 1 side features unmatched attacking talent with Kylian Mbappe leading the line. France’s squad depth across all positions remains elite, even after a Euro 2024 semifinal exit. Their blend of speed, power and technical quality positions them as perennial contenders.

Experts note France may possess the most raw talent in the tournament. Coach Didier Deschamps has experience guiding them to a final in 2022, and they are seen as the biggest threat to Spain.

3. England (+600 to +650)

England’s “Golden Generation” continues to mature, with Jude Bellingham, Phil Foden and Harry Kane forming a potent core. Reaching the Euro 2024 final showed progress, though finishing remains a question mark. Their physicality and set-piece prowess suit knockout football.

Gareth Southgate or his successor will rely on squad harmony in what could be a breakthrough year for the Three Lions.

4. Argentina (+800 to +900)

The defending champions arrive with Lionel Messi, now 38, seeking a record sixth World Cup appearance and a potential back-to-back title — a feat not achieved since Brazil in 1962. Messi was included in the squad announced this week.

Argentina topped CONMEBOL qualifying comfortably. While age catches up to some veterans, their experience and winning mentality under Lionel Scaloni make them dangerous. No team has successfully defended the title in the modern era, adding pressure.

5. Brazil (+750 to +800)

Despite a dip in recent form, Brazil’s historical pedigree and young talent pool keep them in the conversation. The five-time champions feature emerging stars alongside established names. Their athleticism and flair remain hallmarks.

Critics point to this as potentially the least talented Brazil squad in decades, yet their ceiling in a single-elimination setting is high.

6. Portugal (+900 to +950)

Cristiano Ronaldo’s pursuit of a first World Cup title drives Portugal. At 41, Ronaldo’s role may be more limited, but a supporting cast including Bruno Fernandes provides creativity. Portugal reached the Euro 2024 quarterfinals and possesses strong depth.

7. Germany (+1,000 to +1,300)

Hosts of Euro 2024 showed signs of revival. Julian Nagelsmann’s side blends youth and experience, with strong home support potentially boosting them if they advance deep. Defensive improvements have been noted.

8. Netherlands (+1,400 to +1,700)

The Dutch bring tactical discipline and individual quality, led by players like Virgil van Dijk. Consistent quarterfinal appearances in recent majors underscore their reliability as contenders.

9. Belgium (+2,200 to +2,500)

Kevin De Bruyne remains the heartbeat of a transitioning Belgian side. While the “golden generation” has aged, Belgium retains enough quality to cause upsets and reach the latter stages.

10. Morocco (+7,500 to +10,000)

The 2022 semifinalists represent Africa’s best hope. Their organized defense and counterattacking threat, combined with passion, make them a dangerous outsider in the expanded field.

Other notable mentions include the United States as co-hosts (+6,000 to +6,500), seeking a deep run on home soil, Colombia, Uruguay and emerging sides like Norway.

The tournament’s structure, with more teams advancing from groups, favors depth and recovery from early setbacks. Injuries remain a factor, particularly for star players like Yamal.

Coaches emphasize preparation amid a packed calendar. “We need to give him the time he needs,” Spain’s de la Fuente said regarding Yamal’s recovery.

FIFA rankings as of April 2026 place France first, followed by Spain, Argentina and England, aligning closely with betting odds and projections.

The group stage draw has created several intriguing matchups, though specific groups add layers of complexity for favorites. Home advantage for the U.S., Mexico and Canada could play a role, but European sides have dominated recent odds.

Ultimately, the 2026 World Cup represents a clash of styles and generations. Spain’s current momentum as European champions gives them a slight edge, but France’s talent pool and Argentina’s champion pedigree ensure nothing is certain.

As the tournament approaches, focus intensifies on squad fitness, tactical innovations and the ability to perform under pressure in North America’s diverse venues. One thing is guaranteed: global audiences will witness football at its highest level.

NEW YORK — Lumentum Holdings Inc. (NASDAQ: LITE), a key supplier of optical components powering artificial intelligence data centers, has captured investor attention in 2026 as its stock trades near $855 following strong quarterly results driven by hyperscale demand. With analysts maintaining a consensus Moderate Buy to Buy rating and significant price target upside, the question of whether to buy or sell the shares centers on continued AI infrastructure spending versus valuation risks in a competitive photonics market.

The San Jose, California-based company reported robust fiscal third quarter 2026 results on May 5, with net revenue reaching $808.4 million, up substantially from the prior year. GAAP net income stood at $144.2 million, or $1.50 per diluted share, while non-GAAP net income hit $225.7 million, or $2.37 per share. Gross margins improved to 44.2% on a GAAP basis and 47.9% on a non-GAAP basis.

This performance reflects Lumentum’s strong positioning in optical transceivers, lasers and switching solutions essential for AI training clusters. Revenue has accelerated for multiple consecutive quarters, fueled by 200G and higher-speed products for next-generation data centers.

Analyst sentiment remains largely positive. Across roughly 20 Wall Street firms, the consensus is Moderate Buy, with 13-14 Buy or Strong Buy ratings and a handful of Holds. Average 12-month price targets range from approximately $1,012 to $1,127, implying 18-32% upside from recent trading levels around $855. High targets reach $1,400, while lows sit near $600 to $900.

Recent updates include Barclays raising its target to $1,000 while maintaining Equal Weight, JPMorgan lifting to $1,130 with an Overweight rating, and Rosenblatt holding a Buy at $1,300. Stifel and others have also expressed confidence in the AI-driven growth story.

Lumentum has benefited from the AI supercycle. Its products, including 1.6T DR4 OSFP transceiver prototypes and 1060nm VCSEL platforms for optical interconnects, address bandwidth, power and scaling challenges in AI infrastructure. Demonstrations at OFC 2026 highlighted advancements in scale-up, scale-out and scale-across architectures.

The company is expanding manufacturing capacity, including a new U.S. facility for advanced lasers targeted at the world’s largest AI data centers. This move aims to meet surging demand from hyperscalers and reduce potential supply constraints.

Management has expressed optimism. In earnings commentary, executives noted record revenues and leverage in the business model, with expectations for continued growth into fiscal 2027. Optical Circuit Switch (OCS) business exceeded targets ahead of schedule.

For bulls, the case rests on Lumentum’s technological leadership in high-speed optics. The shift to AI workloads has created a multi-year tailwind, with analysts projecting sustained revenue expansion as data center buildouts continue. Diversification beyond traditional telecom into industrial lasers and 3D sensing provides additional stability.

Valuation remains a key consideration. Shares have risen dramatically over the past year, reflecting AI enthusiasm, but forward multiples are elevated compared to historical norms. Some models suggest the stock trades at a discount to intrinsic value based on projected cash flows from AI optics growth.

Bear cases highlight execution risks, customer concentration among a few large hyperscalers, and potential cyclicality if AI spending moderates. Competition in the photonics space from peers could pressure margins. Short-term technical signals have shown mixed readings, with some near-term caution flagged by moving averages.

Financially, Lumentum has demonstrated improving profitability and cash generation. Sequential revenue growth from fiscal Q1 through Q3 2026 underscores momentum, with non-GAAP operating margins expanding significantly. The balance sheet supports ongoing investments in R&D and capacity.

Broader industry trends support a constructive outlook. Hyperscalers’ push toward higher-bandwidth interconnects for AI training and inference favors suppliers like Lumentum with proven high-volume manufacturing expertise. Inclusion in major indices has also attracted passive inflows.

Portfolio managers note that LITE fits within growth-oriented technology allocations, particularly those focused on AI infrastructure. Position sizing should account for volatility typical in semiconductor-adjacent names. Near-term catalysts include fiscal fourth quarter results and updates on new product ramps.

Risks include macroeconomic slowdowns affecting tech capex, supply chain disruptions for critical materials like indium phosphide, and geopolitical factors influencing global trade. Regulatory scrutiny on AI energy consumption could indirectly impact deployment timelines.

Longer-term forecasts vary by source. Optimistic projections see continued compounding from AI tailwinds, potentially driving revenues toward multi-billion-dollar annual run rates. More conservative views temper expectations around market saturation or technology shifts.

In the current environment, Lumentum exemplifies the intersection of photonics innovation and artificial intelligence demand. While not without risks inherent to high-growth tech stocks, the company’s execution on financial targets and product roadmap has bolstered confidence among most covering analysts.

Investors considering a position should evaluate their time horizon and risk tolerance. Those bullish on sustained AI infrastructure investment may view current levels as an opportunity, particularly following any pullbacks. Others may opt to wait for clearer signals on margin sustainability or broader market conditions.

As with any equity, particularly in the dynamic semiconductor and optics sector, thorough due diligence is essential. Lumentum’s trajectory will likely hinge on its ability to maintain leadership in next-generation optical solutions amid intense competition and rapid technological evolution. The coming quarters of data center deployment cycles will provide further clarity on whether the AI optics boom translates into lasting shareholder value.

How I Would Invest $1 Million Today

Why Manchester United’s £3.3million signing did not make his debut this season

SpaceX just won a second Golden Dome contract. This one is $4.16 billion.

-

Business6 days ago

Business6 days agoNYT Strands Answers May 24 2026 Revealed for Puzzle No. 812 Theme Summer Essentials

-

NewsBeat3 days ago

NewsBeat3 days agoIsrael says it has killed new Hamas military leader in Gaza City airstrikes

-

Politics5 days ago

Politics5 days agoBridgerton Season 5: Cast, Release Date And Everything We Know So Far

-

Business3 days ago

Business3 days agoSelena Gomez Reportedly Upset Over Benny Blanco’s Comments on Her ‘Terrible’ Diet

-

Crypto World4 days ago

Crypto World4 days agoMicron Crosses $1 Trillion Market Cap as AI Demand Reshapes Memory Sector

-

Tech5 days ago

Tech5 days agoMicrosoft’s quiet Claude Code retreat and the real cost of enterprise AI

-

Business5 days ago

Business5 days agoBTS Sells Out Four Las Vegas Shows at Allegiant Stadium for ARIRANG World Tour

-

Tech4 days ago

Tech4 days agoChina assigns ID codes to 28,000+ humanoid robots

-

News Videos3 days ago

News Videos3 days agoXRP *JUST* SUCCEEDED!!!! CLARITY ACT EXPOSED!!! (SHE EXPOSED IT)

-

Tech1 day ago

Tech1 day agoWaymo dominates autonomous vehicle registrations as Tesla trails behind

-

Tech3 days ago

The Samsung pay deal is the moment Korean unions changed register

-

Tech5 days ago

Tech5 days agoWestone Audio and Etymotic Acquired by Fidelity Collective in Major IEM Market Move

-

Tech3 days ago

Tech3 days agoMillions of AI agents imperiled by critical vulnerability in open source package

-

Crypto World6 days ago

Brian Armstrong Outlines Crypto Vision for the Future Financial System

-

Entertainment4 days ago

Entertainment4 days ago‘Breaking Bad’ Star’s Easy-to-Binge 6-Part Crime Series Spin-Off Is Finally Heading to Free Streaming

-

Crypto World3 days ago

SpaceX’s $2 Trillion IPO: Why Tech Giants Nvidia (NVDA), Apple (AAPL), and Microsoft (MSFT) May Face Pressure

-

Crypto World5 days ago

Crypto World5 days agoNvidia (NVDA) CEO Calls on Super Micro to Strengthen Export Controls Amid Smuggling Probe

-

Tech3 days ago

Tech3 days agoNASA taps Blue Origin to deliver lunar rovers for Moon Base initiative

-

NewsBeat5 days ago

NewsBeat5 days agoHottest May day ever as London hits 34.8C in 2C leap from previous records

-

Crypto World18 hours ago

Crypto World18 hours agoSnowflake (SNOW) Stock Rallies on Strong Q1 Results and AI Product Growth

You must be logged in to post a comment Login