Crypto World

Bitcoin Believers Who Lasted 16 Months Just Sold Every Coin to Survive

Genius Group (GNS) sold its entire Bitcoin (BTC) treasury of 84.15 BTC on April 1, 2026, fully repaying $8.5 million in debt and leaving the company with zero BTC on its balance sheet.

The Singapore-based AI-powered education company adopted its Bitcoin-first strategy on November 12, 2024, just days after the US presidential election, committing to hold 90% or more of its reserves in BTC.

Genius Group Moves From 440 BTC to Zero

The exit marks the end of a 16-month run as one of the earliest post-election corporate BTC treasury adopters.

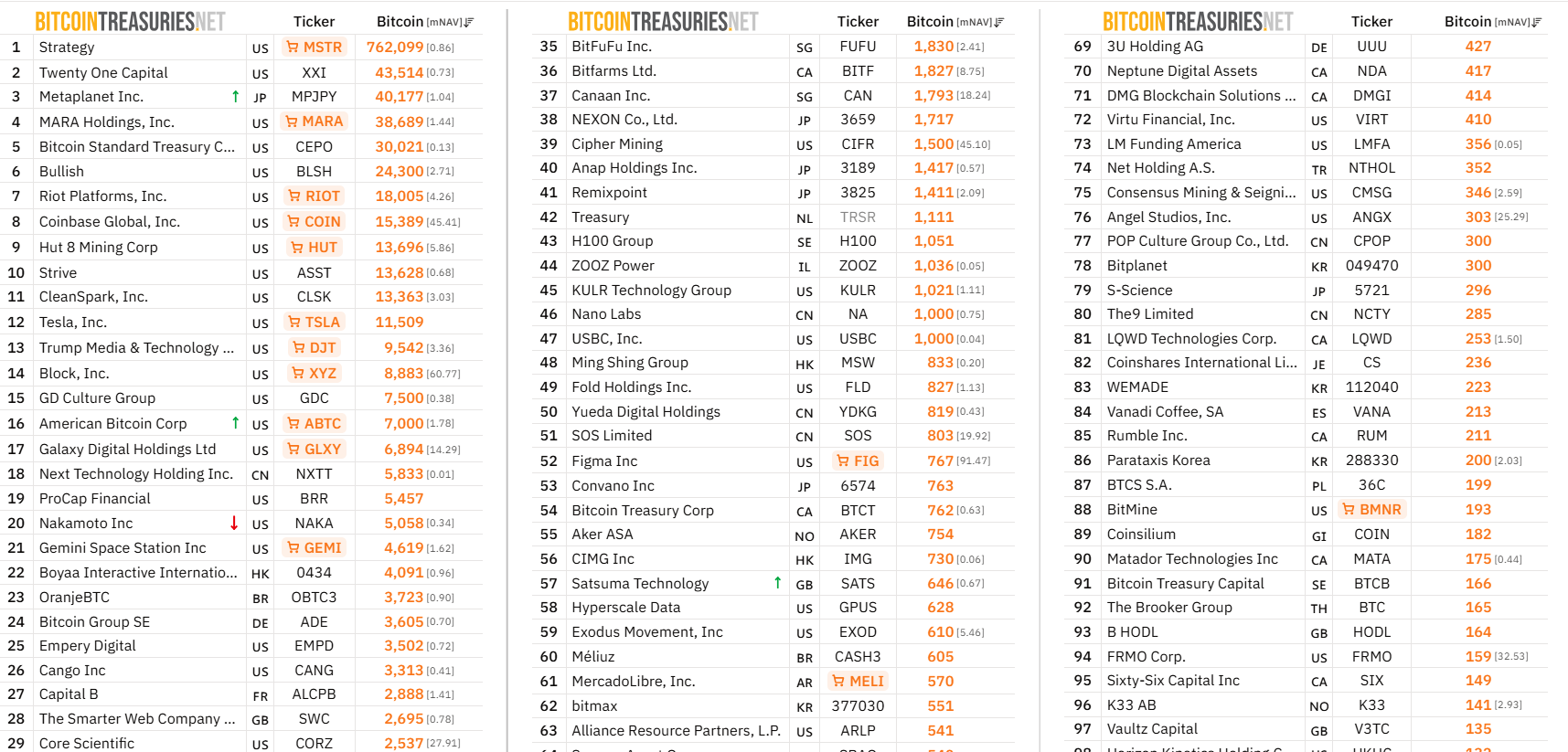

Genius Group’s BTC accumulation peaked at approximately 440 BTC by early 2025. Based on current rankings, this would place the firm among the top 70 public companies holding BTC.

The company tied its treasury strategy directly to its identity as an AI-powered education group. They framed BTC as its primary reserve asset alongside workforce training and experiential learning programs.

The unraveling began when a US court order blocked the company from raising capital or issuing new shares.

That legal constraint removed the company’s ability to fund operations without tapping its BTC holdings. Sales proceeded in stages rather than in a single transaction.

By February 6, 2026, Genius Group held exactly 84.15 BTC after selling approximately 96 BTC between late December 2025 and early February 2026.

The partial sales reduced a BTC-backed loan from roughly $8.5 million to around $3.3 million before the final liquidation cleared the balance entirely.

Debt Pressure Forces the Exit

The final BTC sale occurred during Q1 2026 and was completed before March 31. The company announced zero holdings on April 1 alongside its Q1 results, confirming the full debt repayment.

The exit came at a loss. Genius Group’s average BTC cost basis sat near $102,000 per coin from earlier accumulation. Meanwhile, prices during the Q1 sale period ran softer, around $66,500.

Despite the treasury wipeout, the company’s core operations showed growth. Q1 2026 operational revenue reached $3.3 million, up 171% from $1.2 million in Q1 2025.

Gross profit grew 228% to $2.0 million, and gross margin improved to 62% from 52% a year earlier. Adjusted EBITDA from operations turned positive at $600,000, compared to negative $400,000 in Q1 2025.

CEO Roger Hamilton attributed the operational improvement to a strategic focus on higher-margin education programs across Genius School, Genius Academy, and Genius Resorts.

“Our first quarter marks a significant milestone for Genius Group. It shows that our focus on three revenue drivers – Genius School, Genius Academy, and Genius Resorts – is paying off, with our operational revenue getting close to tripling year-on-year,” read an excerpt in the announcement, citing founder and CEO Roger

A Pause, Not an Exit

Genius Group framed the BTC liquidation as a temporary measure rather than a permanent reversal of strategy.

The company stated it will recommence building its Bitcoin treasury when it believes market conditions are more favorable.

Hamilton has accumulated 5.5 million company shares since 2024, a signal management cited as a sign of confidence in the company’s longer-term direction.

The company also pointed to continued expansion of its Genius City project in Bali, a combined education and residential hub, as part of its broader Southeast Asia growth plan.

Whether the company can rebuild a BTC treasury position without the fundraising constraints that forced the selldown will depend on the resolution of its ongoing legal proceedings and BTC price conditions at the time of any renewed accumulation.

The post Bitcoin Believers Who Lasted 16 Months Just Sold Every Coin to Survive appeared first on BeInCrypto.

Opinion by: João Garcia, DevReal lead at Cartesi.

Decentralized finance presents itself as a transparent alternative to Wall Street. Yet, what it has largely reconstructed is a simplified version of finance, engineered less around market resilience than around the constraints of gas fees. That trade-off, once treated as a technical footnote, is increasingly shaping the limits of what DeFi can become.

So long as computational minimalism remains the overriding priority, financial robustness will remain secondary, and periods of market stress will continue to expose that imbalance.

When markets move faster than the virtual machine

DeFi has rebuilt the familiar architecture of finance, including exchanges, lending markets, derivatives and stablecoins. However, the way these systems function reveals how tightly they are bound by their execution environments.

Risk parameters tend to remain static, and although collateral thresholds can adjust, they typically do so slowly, through governance processes rather than automatic recalibration. Liquidation engines currently rely on fixed formulas rather than adaptive portfolio models that account for shifting volatility or correlations. What appears as a design preference is often a concession to computational limits.

On Ethereum and similar chains, floating-point arithmetic is absent or emulated, iterative simulations are expensive, and continuously recomputing cross-asset exposure can quickly become impractical. The outcome is that financial logic is compressed into forms that are deterministic and affordable to execute, even if that compression strips away nuance.

This architecture performs adequately in stable conditions, but volatility has a way of testing its edges. During MakerDAO’s “Black Thursday” event in March 2020, vaults were liquidated at effectively zero bids, as auction mechanics struggled under collapsing prices and network congestion.

In later downturns, protocols such as Aave and Compound leaned on mass liquidations triggered by fixed collateral ratios, rather than dynamic portfolio recalculations. When Curve’s pools were destabilized in 2023 following a smart contract exploit, the stress radiated outward into lending protocols that treated LP tokens as static collateral, compounding systemic risk.

In each instance, decentralization itself was not the breaking point. Rather, rigid financial logic operated inside an execution layer that could not continuously recompute risk as conditions deteriorated.

Traditional markets evolved in the opposite direction. Banks and clearinghouses simulate thousands of stress scenarios, recalculating exposure as correlations shift and volatility regimes change. Margin requirements respond dynamically to market conditions, and the response is led by substantial computational infrastructure and mature numerical tooling. Public blockchains, by contrast, were not designed with that degree of iterative financial processing in mind.

The illusion of simplicity

Constraining computational complexity reduces certain attack surfaces. Simplicity at the protocol layer, however, does not dissolve complexity in the financial system. It merely pushes it elsewhere.

When risk cannot be modeled and recomputed transparently on-chain, it migrates off-chain into dashboards, analytics teams, discretionary parameter adjustments and emergency governance coordination. The blockchain may remain the settlement layer, but the adaptive intelligence that stabilizes the system increasingly operates outside it. During volatility spikes, protocols often depend on rapid human coordination to adjust parameters, while oracles and large token holders acquire disproportionate influence over outcomes.

The system retains its decentralized base, yet its capacity to respond flexibly depends on actors operating beyond deterministic execution. What appears structurally simple at the smart contract level can conceal a more complex and less transparent operational reality.

DeFi did not converge on simplified finance because static ratios and deterministic curves were proven superior. It converged there because richer computational models were prohibitively expensive to run. As markets deepen, leverage increases, and instruments grow more interdependent, that compromise becomes harder to ignore. Fixed thresholds and blunt liquidation engines, initially safeguards, can begin to function as amplifiers of stress.

Computation as a missing primitive

The deeper constraint, more than decentralization, is execution design.

If verifiable execution environments begin to approximate general-purpose computing systems, the financial design space expands. Native floating-point assistance, iterative algorithms and access to established numerical libraries would allow models to be expressed directly rather than translated into simplified approximations.

Related: Wall Street will eventually submit to the rules of DeFi

This change would allow lending protocols to incorporate scenario-based stress testing instead of relying primarily on fixed collateral ratios. Margin requirements may also adjust in response to observed volatility rather than governance cadence. It could also see credit systems recompute multivariable risk scores transparently, replacing binary heuristics with more granular assessments.

The aim is not to introduce complexity for its own sake. It is to keep financial intelligence inside the protocol, where it remains visible and enforceable, rather than externalizing it into operational layers that users cannot easily audit. This underscores the broader point that the limitations confronting DeFi are largely architectural choices, not inevitabilities of decentralization.

A credibility ceiling

DeFi now stands at a structural crossroads. One direction preserves gas-optimized minimalism, keeping base-layer execution clean while allowing increasingly sophisticated financial logic to migrate off-chain. That path may maintain clarity at the smart contract level, but it constrains how far decentralized finance can responsibly scale.

The alternative is to treat computation itself as a first-class primitive and to accept more capable execution environments in exchange for systems that can adapt, recompute and stress-test transparently. If complex risk logic cannot live on-chain, DeFi will continue to project simplicity in code while relying on discretion in practice.

Markets will not moderate their complexity to accommodate virtual machine constraints. If decentralized finance intends to operate at a meaningful scale, its computational foundations will have to evolve alongside the financial ambitions built on top of them.

Opinion by: João Garcia, DevReal lead at Cartesi.

This opinion article presents the author’s expert view, and it may not reflect the views of Cointelegraph.com. This content has undergone editorial review to ensure clarity and relevance. Cointelegraph remains committed to transparent reporting and upholding the highest standards of journalism. Readers are encouraged to conduct their own research before taking any actions related to the company.

Crypto World

Here is how Drift attackers drained more than $270 million using a Solana feature designed for convenience

The attack on Drift Protocol was not a hack in the traditional sense.

Nobody found a bug or cracked a private key. There wasn’t a flash loan exploit or manipulated oracle either.

Instead, an attacker used a legitimate Solana feature, ‘durable nonces,’ to trick Drift’s security council into pre-approving transactions that would be executed weeks later, at a time and in a context the signers never intended.

The result was a drain of at least $270 million that took less than a minute to execute but more than a week to set up.

What durable nonces are and why they exist

On Solana, every transaction includes a ‘recent blockhash,’ essentially a timestamp that proves the transaction was created recently. That blockhash expires after about 60 to 90 seconds. If the transaction is not submitted to the network within that window, it becomes invalid. This is a safety feature and helps prevent old, stale transactions from being replayed later.

Durable nonces override that safety feature. They replace the expiring blockhash with a fixed ‘nonce,’ a one-time code stored in a special onchain account, that keeps the transaction valid indefinitely until someone chooses to submit it.

The feature exists for legitimate reasons. Hardware wallets, offline signing setups, and institutional custody solutions all need the ability to prepare and approve transactions without being forced to submit them within 90 seconds.

But indefinitely valid transactions create a problem. If one can get someone to sign a transaction today, it can be executed next week or next month, per the system’s hardcoded rules. The signer has no way to revoke their approval once it is given, unless the nonce account is manually advanced, which most users do not monitor.

How the attacker used them

Drift’s protocol was governed by a ‘Security Council multisig,’ a system in which multiple people (in this case, five) share control, and any action requires at least two of them to approve. Multisigs are a standard security practice in DeFi, where the idea is that compromising a single person is not enough to steal funds.

But the attacker did not need to compromise anyone’s keys. All they needed were two signatures, and they appear to have obtained them through what Drift describes as “unauthorized or misrepresented transaction approvals,” meaning the signers likely thought they were approving a routine transaction.

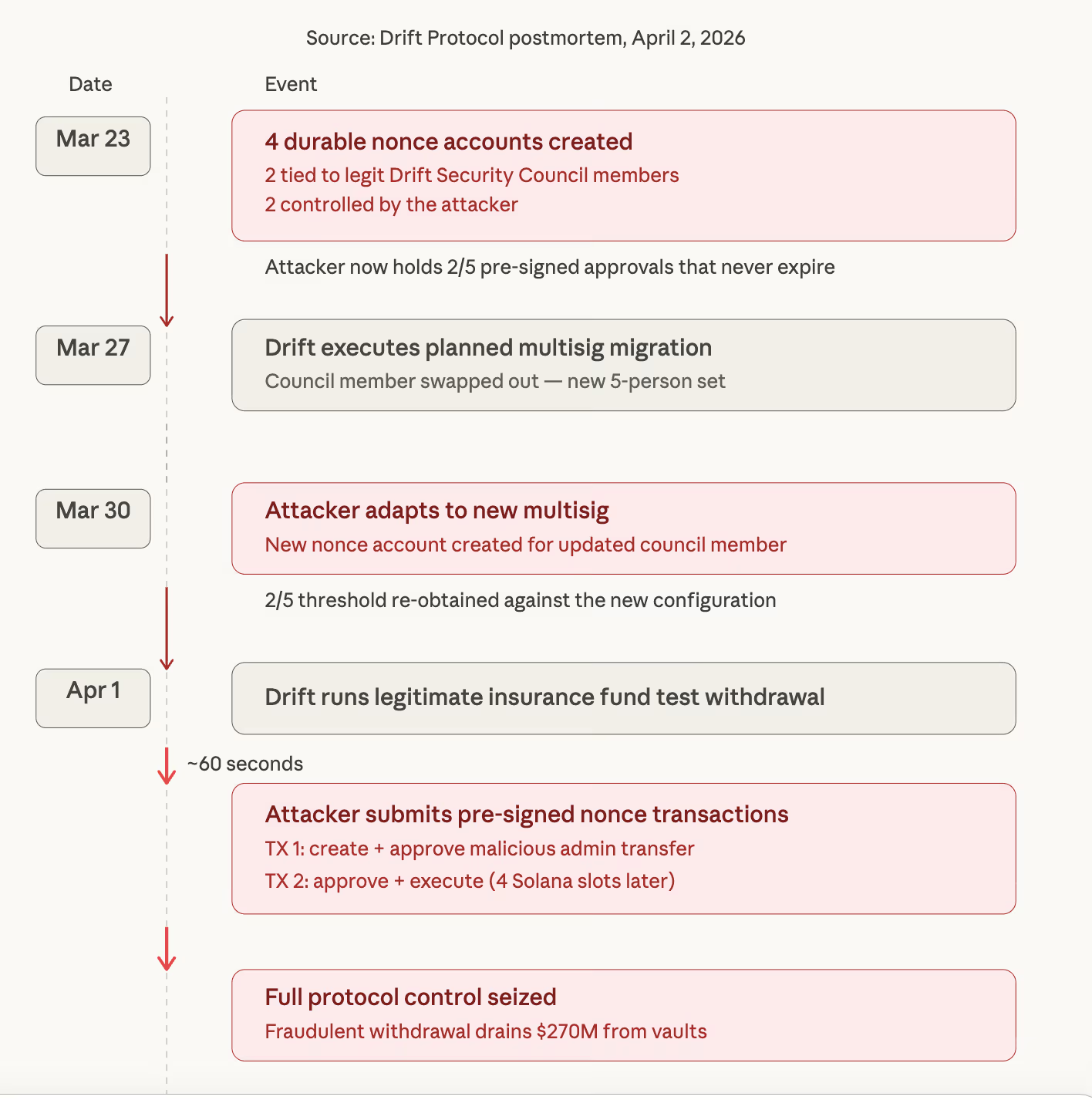

Here is the timeline Drift published in a Thursday X post.

On March 23, four durable nonce accounts were created. Two were associated with legitimate Drift Security Council members. Two were controlled by the attacker. This means the attacker had already obtained valid signatures from two of the five council members, locked into durable nonce transactions that would not expire.

On March 27, Drift executed a planned Security Council migration to swap out a council member. The attacker adapted. By March 30, a new durable nonce account appeared, tied to a member of the updated multisig, indicating the attacker had re-obtained the required two-of-five approval threshold under the new configuration.

On April 1, the attacker executed.

First, Drift ran a legitimate test withdrawal from its insurance fund. Approximately one minute later, the attacker submitted the pre-signed durable nonce transactions. Two transactions, four slots apart on the Solana blockchain, were enough to create and approve a malicious admin transfer, then approve and execute it.

Within minutes, the attacker had full control of Drift’s protocol-level permissions. They used that control to introduce a fraudulent withdrawal mechanism and drain the vaults.

What was taken and where it went

Onchain researchers tracked the fund flows in real time. The breakdown of stolen assets, compiled by security researcher Vladimir S., totaled roughly $270 million across dozens of tokens.

The largest single category was $155.6 million in JPL tokens, followed by $60.4 million in USDC, $11.3 million in CBBTC (Coinbase wrapped bitcoin), $5.65 million in USDT, $4.7 million in wrapped ether, $4.5 million in DSOL, $4.4 million in WBTC, $4.1 million in FARTCOIN, and smaller amounts across JUP, JITOSOL, MSOL, BSOL, EURC, and others.

The primary drainer wallet was funded eight days before the attack via NEAR Protocol intents but remained inactive until execution day. Stolen funds were transferred to intermediary wallets that were funded just the day before via Backpack, a decentralized crypto exchange that requires identity verification, potentially giving investigators a lead.

From there, funds moved to Ethereum addresses via Wormhole, a cross-chain bridge. Those Ethereum addresses had been pre-funded using Tornado Cash, the sanctioned privacy mixer.

ZachXBT, a prominent onchain investigator, noted that over $230 million in USDC was bridged from Solana to Ethereum via Circle’s CCTP (Cross-Chain Transfer Protocol) across more than 100 transactions.

He criticized Circle, the centralized issuer of USDC, for not freezing the stolen funds during a six-hour window after the attack began around noon Eastern time.

The attack was also reminiscent of recent social engineering attempts, using tactics similar to those seen before, according to a social media post by a user who goes by ‘Temmy.’ “we’ve seen this before. we’ve seen this so many times,” the user said.

“bybit. $1.4 billion. the attacker compromised the signing infrastructure and tricked signers into authorizing malicious transactions. same concept. social engineering. not code. ronin bridge. $625 million. compromised validator keys. same story. cetus protocol. $223 million. different method but same result. hundreds of millions gone.” the post said.

What was not compromised

What failed was the human layer around the multisig. Durable nonces allowed the attacker to separate the moment of approval from the moment of execution by more than a week, creating a gap in which the context of the signed document no longer matched the context in which it was used.

All deposits into Drift’s borrow-and-lend products, vault deposits, and trading funds are affected. DSOL tokens not deposited in Drift, including assets staked to the Drift validator, are unaffected. Insurance fund assets are being withdrawn and safeguarded. The protocol has been frozen, and the compromised wallet has been removed from the multisig.

As such, this is the third major exploit in recent months that did not involve a code vulnerability. Social engineering and operational security failures, rather than smart contract bugs, are increasingly how money leaves DeFi protocols.

The durable nonce vector is particularly dangerous because it exploits a feature that exists for good reason and is difficult to defend against without fundamentally changing how multisig approvals work on Solana.

The open question, which Drift’s forthcoming detailed postmortem will need to answer, is how two separate multisig members approved transactions they did not understand, and whether any tooling or interface changes could have flagged durable nonce transactions as requiring additional scrutiny.

Read more: North Koreans hackers likely behind $286 million Drift Protocol exploit

The US dollar has been firm, but the drivers behind the move may be more complex than they first appear.

While geopolitical tension and shifts in risk sentiment play a role, current price behaviour seems increasingly influenced by inflation expectations and yields. As oil prices move higher, markets reassess the outlook for inflation and interest rates, which continues to support the dollar.

This video explores the underlying macro dynamics and why the current environment may be more conditional than it seems.

Watch it now and stay updated with FXOpen.

💬 Don’t forget to like, comment, and subscribe for more professional market insights every week.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Social media platform X is preparing a new security measure aimed at shutting down a widespread form of crypto phishing that leverages hijacked accounts to promote scam tokens.

The company will soon auto-lock any account that mentions cryptocurrency for the first time in its history, according to the company’s Head of Product Nikita Bier. Users will need to go through additional verification before being allowed to post again.

Bier said the feature targets the core incentive behind these attacks. “This should kill 99% of the incentive,” he wrote, referring to the current wave of phishing that tricks users into giving up their credentials, then uses their accounts to push crypto scams.

The change was unveiled in response to a detailed firsthand account from an X user who lost control of their account after falling for a phishing email disguised as a copyright violation notice.

The attacker, the user said, used a pixel-perfect fake login page to harvest two-factor codes, then locked the user out and began promoting fraudulent crypto projects from their account.

Crypto scams on X

These types of attacks have been extremely common on X, an inheritance from before it was acquired by Elon Musk and was still called Twitter.

One of the most common tactics is the “double your money” scam, in which users are told to send cryptocurrency in exchange for a promise of more. Others push fake memecoins or fraudulent airdrops, often using hijacked accounts to lend credibility.

Impersonation is one of the most powerful tools. Spoofed accounts impersonating major personalities have repeatedly tricked followers into clicking malicious links that mimic legitimate crypto platforms.

Cryptocurrency transactions are irreversible, so once a user falls for such an attack, their funds are gone.

The most infamous example came in 2020, when hackers accessed Twitter’s internal systems and took control of major accounts, including those of Apple, Barack Obama, and Elon Musk.

They used those accounts to promote a fake bitcoin giveaway, netting over $100,000 before the posts were removed. That breach, carried out through social engineering against Twitter employees, resulted in the hacker receiving a 5-year sentence.

X has made several attempts to bolster security. These have included bot purges, API restrictions, and behavioral detection. The latest move to auto-lock accounts that post about crypto for the first time builds on those efforts, aiming to cut off the tactic at its root: by making hijacked accounts useless for scams.

Bier also called out Google for failing to stop phishing emails at the email level, pointing the finger at the tech giant’s share of the responsibility for failing to protect its users from phishing attacks.

Wallet in Telegram launched native perpetual futures trading on April 2, 2026, powered exclusively by Lighter, bringing leveraged access to 50+ markets inside the chat app.

The feature went live without requiring users to download any external app or connect a third-party wallet, with positions opening directly inside Telegram.

Perpetual Volumes Set the Stage

The timing of the integration follows a period of sharp growth in on-chain derivatives. Perpetual trading volumes surged over 300% in 2025, with monthly activity consistently exceeding $1 trillion.

Lighter (LIT) processed $65.47 billion in volume in March 2026, ranking fourth among perpetual decentralized exchanges (DEXs) by monthly volume.

The platform runs on a custom zero-knowledge (ZK) rollup on Ethereum, where every order match and liquidation is verifiably proven on-chain.

Lighter’s 24-hour trading volume reached $2.08 billion on the day of the announcement, with open interest sitting at $663 million, per CoinGecko data.

What the Integration Offers

Users accessing the new Perpetuals tab inside Wallet in Telegram can trade over 50 markets spanning crypto, metals, stocks, and oil. Leverage goes up to 50x, and positions can be opened from as little as $1.

Wallet in Telegram confirmed the launch via its official X (Twitter) account, stating the feature allows users to go long or short in seconds.

Lighter confirmed the partnership was open to outside builders as well.

“…the Partner Attribution program is open to anyone ready to build,” they wrote.

The Partner Attribution program now lets any developer integrate Lighter’s perpetuals and spot infrastructure into their own apps, with credit flowing back to the referring builder.

No further details on revenue-sharing terms were disclosed at launch.

LIT Price Reacts and Competitive Context

The Lighter (LIT) token rose 5% on the announcement. However, Lighter still trails the category leader by a significant margin.

Hyperliquid processed $178.23 billion in volume during March 2026, more than double the combined volume of the next three competitors.

The Telegram distribution could narrow that gap. Wallet in Telegram reaches over 150 million users, a retail audience that neither Hyperliquid nor other DEX competitors currently have direct access to through a native chat-app integration.

Whether the Telegram user base converts into sustained trading volume will determine how much the partnership moves Lighter’s competitive position in the months ahead.

The post Wallet in Telegram Adds Perpetuals via Lighter DEX, Fuels 5% LIT Price Surge appeared first on BeInCrypto.

Solana-based crypto exchange Drift Protocol was hacked for roughly $280 million yesterday as part of a weeks-long operation that likely used social engineering to compromise multiple multisig signers’ approvals.

On April 1, 7 pm UTC+1 time, Drift announced that there was “unusual activity” on the protocol and that users should avoid depositing funds. It stressed, “This is not an April Fools joke.”

This followed from X users raising alarms that Drift was being exploited and that it was going to be a substantial one.

Drift then confirmed that it was under an ongoing attack and that it would need to suspend deposits and withdrawals. Researchers began to speculate that Drift’s private keys were compromised.

Read more: Liquity accused of ‘market manipulation’ after Circle acquisition April Fools’

Drift has since shared a detailed timeline of what took place and how.

It said, “This was a highly sophisticated operation that appears to have involved multi-week preparation and staged execution, including the use of durable nonce accounts to pre-sign transactions that delayed execution.”

It claims the attack was not caused by a bug in Drift’s programs or smart contracts, there was no evidence of compromised seed phrases, and that the attack involved unauthorized transaction approvals before the hack’s execution.

However, it admitted that these approvals were likely facilitated by a social engineering attack against its staff and the manipulation of “durable nonce mechanisms.”

What went down with Drift

Durable nonce mechanisms are a type of blockchain tool that can bypass blockhash signing and facilitate offline translation signing.

Drift claims that on March 23, four durable nonce accounts were created, two of which were associated with Drift Security Council multisig members and two associated with attacker-controlled accounts.

Read more: Circle rarely freezes stolen funds but wants reversible transactions

Then, on March 27, “Drift executed a planned Security Council migration due to a council member change.”

Three days later, another durable nonce account was created for a member of the updated multisig, giving the attackers “effective access to 2/5 signers in the updated multisig.”

Day of execution

Drift claims that on April 1, it executed a test withdrawal from the insurance fund. The attacker then, with access to the multisig approvals, executed “a malicious admin transfer within minutes, gaining control of protocol-level permissions.”

Attackers could then, “Use that control to introduce a malicious asset and remove all pre-set withdrawal limits attacking existing funds.”

Drift hasn’t shared any details about how the likely social engineering attack took place. They can sometimes be the result of an attacker donning a false identity, be it over direct message, email, or phone, and tricking someone into giving them access to key privileges.

Drift’s partner Circle hasn’t frozen funds

The incident has drawn criticism from the crypto investigator ZachXBT, who took issue with the stablecoin firm Circle and its slow efforts to freeze the stolen funds.

Drift integrated Circle’s Cross-Chain Transfer Protocol (CTTP) in 2023. ZachXBT noted that “Circle was asleep while many millions of USDC was swapped via CCTP from Solana to Ethereum for hours from the 9 figure Drift hack during US hours.”

“6 hours is how long Circle had to freeze stolen funds from the $280M+ Drift hack,” he said.

Other users have taken issue with the classification of the protocol as “decentralized,” after the attack appears to have exploited centralised mechanisms.

Other users were annoyed that Drift only required two out of the five multig approvals to action the transaction.

Read more: ‘Bad actor’ Circle slammed for letting stolen $3M USDC sit unfrozen

The platform said that it was working alongside security firms, law enforcement, bridges, and exchanges to figure out what happened and freeze the stolen assets. It added that a more detailed report will arrive in the coming days.

The Chief Technology Officer for Ledger has already speculated that the events of the hack resemble a similar modus operandi “to the Bybit hack last year, widely attributed to DPRK-linked actors.”

Protos has reached out to Drift for comment and will update this piece should we hear anything back.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Russia has moved to shut down crypto mining operations across 13 regions, targeting an estimated 50,000 miners in what amounts to the most sweeping enforcement action since the country legalized the activity in August 2024.

The bans, extending through 2031 during peak autumn-winter seasons, signal that Moscow’s tolerance for grid-straining mining has hit a structural limit, not just a seasonal one.

The immediate pressure is energy: affected Siberian regions are reporting shortfalls of nearly 3,000 MW on the Unified Energy System grid, driven largely by miners exploiting cheap, heavily subsidized local electricity. That’s not a rounding error – it’s a grid crisis, and Russian officials are treating it as one.

Key Takeaways:

- Ban Scope: Mining restrictions now cover 10 active regions – including Irkutsk Oblast, parts of Buryatia and Zabaikalsky Krai, six North Caucasus republics, and Russian-occupied Ukrainian territories – with seasonal bans running through 2031.

- Affected Miners: An estimated 50,000 operators face enforcement, with major firm BitRiver among the hardest hit due to its reliance on Irkutsk’s low-cost power infrastructure.

- Energy Context: Power shortfalls in Siberian regions have reached nearly 3,000 MW, with miners blamed for exploiting subsidized electricity at grid-destabilizing scale.

- Escalation Path: Year-round bans in southern Buryatia and Zabaikalsky Krai take effect January 1, 2026, moving beyond seasonal restrictions into permanent operational prohibition.

- What to Watch: A government commission on the electric power sector is expected to convene soon to finalize expanded year-round bans; potential amnesty programs in the North Caucasus could redirect illegal miners toward licensed operations.

Discover: Top Crypto Presales to Watch Before They Launch

What the Russia Crypto Mining Ban Actually Does – and Why the Regional Selection Matters

The mechanics are straightforward: registered and unregistered miners in covered regions are prohibited from operating during designated periods, with enforcement escalating to include FSB agents, drones, and surveillance technology in areas like Kabardino-Balkaria, where illegal operations hidden in abandoned buildings caused over 1 billion rubles ($13 million) in utility damages in 2025 alone.

The regional selection isn’t arbitrary. Irkutsk Oblast faces a full-year ban – its southern areas were already restricted earlier in 2025, freeing up 320 MW – because it anchors the cheap-power arbitrage that made Siberia a global mining hub in the first place.

The North Caucasus republics (Dagestan, North Ossetia-Alania, Ingushetia, Chechnya, Kabardino-Balkaria, and Karachay-Cherkessia) are included because illegal mining there has metastasized beyond regulatory reach.

The inclusion of occupied Ukrainian territories – Donetsk, Luhansk, Zaporizhzhia, and Kherson – reflects Moscow’s intent to consolidate energy control in those regions rather than tolerate gray-market extraction.

Power officials in Buryatia welcomed the year-round bans, with TASS and Kommersant reporting officials cited relief from “serious” shortages. The Industrial Mining Association took the opposite view, stating the restrictions “reduce [Southern Siberia’s] attractiveness to investors” and leave miners “vulnerable.” Both reactions are accurate – which is precisely what makes this ban structurally significant rather than cosmetic.

50,000 Miners Offline – What That Means for Global Hash Rate

Russia currently accounts for roughly 5% of global Bitcoin hash rate, according to Cambridge Centre for Alternative Finance data – a share built almost entirely on the cheap, subsidized electricity now being clawed back.

Displacing 50,000 operators from that base doesn’t evaporate hash rate; it redistributes it, and the redistribution logic points toward the United States, Kazakhstan, and parts of Central Asia as the most likely beneficiaries.

That matters because hash rate geography isn’t just a mining industry statistic – it shapes where block rewards flow, which jurisdictions capture mining revenue, and how resilient the network is to coordinated regulatory pressure.

A meaningful contraction in Russian hash rate tightens the global difficulty adjustment modestly in the short term, briefly improving margins for miners elsewhere before difficulty recalibrates. Bitcoin’s broader market performance adds another variable: compressed miner margins in a sideways or declining price environment accelerate the exit of marginal operators, potentially amplifying the hash rate shift beyond what the Russian ban alone would produce.

BitRiver – the largest industrial mining operator in Russia, anchored to Irkutsk’s power infrastructure – faces the most acute operational exposure. Its model was built on energy-cost arbitrage that the Russian state is now explicitly dismantling.

Explore: Best Crypto Projects With High Growth Potential in 2026

The post Russia Targets 50,000 Miners as Crypto Mining Banned in 13 Regions appeared first on Cryptonews.

Summary

- French tokenized exchange Lise plans to list aerospace parts maker ST Group in what is expected to be Europe’s first fully on-chain IPO.

- Lise operates under the EU’s DLT Pilot Regime and is backed by institutions including BNP Paribas, CACEIS and Bpifrance.

- ST Group forecasts about $68 million in potential project revenues over the next decade, targeting aerospace, defense and space programs.

French stock exchange Lise is preparing to list aerospace components supplier ST Group in what is expected to be Europe’s first fully on-chain initial public offering, according to a report from CoinDesk. The listing on the Paris-based venue would mark a milestone for tokenized primary markets in the EU, moving an IPO’s trading and settlement entirely onto distributed ledger infrastructure.finance.

Lise, short for Lightning Stock Exchange, was authorized last year under the EU’s Distributed Ledger Technology Pilot Regime, becoming the first institution in Europe approved to operate a fully tokenized equity exchange that fuses trading and settlement on-chain. Headquartered in Paris, Lise counts French financial heavyweights BNP Paribas, CACEIS — a subsidiary of Crédit Agricole — and public investment bank Bpifrance among its backers, underscoring that this is not a fringe experiment but a regulated market infrastructure project.

ST Group produces composite material components for aerospace, defense and space projects, positioning it squarely in Europe’s strategic industrial base. CoinDesk reported that potential project revenues linked to the company’s pipeline are estimated at around €59 million, roughly $68 million at current rates, over the next ten years, giving investors a sense of the growth opportunity Lise aims to channel into its tokenized venue.

By opting for an on-chain IPO rather than a listing on a traditional exchange, ST Group is effectively stress‑testing whether tokenization can offer small and mid-sized issuers a cheaper and more flexible way to tap public equity markets. Lise’s stated mission is to provide a lower-cost, more efficient listing path for SMEs and mid-caps, replacing the lengthy, document-heavy IPO process with a digital workflow where ownership is recorded, transferred and settled on a single ledger.

Under the DLT Pilot Regime, Lise is allowed to combine the functions of a multilateral trading facility and a central securities depository on one blockchain system, enabling near‑instant, atomic settlement and continuous 24/7 trading. Advocates argue that such architectures cut post‑trade risk and administrative overhead by collapsing what is now a multi‑day, multi‑intermediary chain into a single synchronized platform.

The French initiative lands as other venues experiment with tokenized securities. In one crypto.news story, tokenization specialist Securitize secured EU‑wide approval to run a regulated trading and settlement system on Avalanche under the same DLT Pilot framework, while another story covered 21X’s plans for an EU‑regulated tokenized securities market using Chainlink for cross‑chain data and interoperability. A separate crypto.news story detailed how JPMorgan executed a tokenized treasuries transaction using Ondo Finance and Chainlink, illustrating how major banks are testing on-chain rails for traditional assets.

If Lise successfully floats ST Group fully on-chain, it will provide a live case study for whether tokenized exchanges can genuinely lower issuance costs and broaden investor access, or whether regulatory and operational frictions still blunt the promise of blockchain in public equity markets.

Blue Owl is experiencing elevated redemption requests for two of its private credit funds, according to letters to shareholders issued Thursday.

The firm’s flagship OCIC fund, with about $36 billion in assets under management, received redemption requests of about 21.9% of shares outstanding during the first quarter, the firm said. Blue Owl’s smaller, tech-oriented fund, OTIC, received redemption requests of 40.7% during the same period, it said.

In both of the funds, Blue Owl opted to cap requests at 5%. Blue Owl attributed the higher-than-usual requests to “heightened market concerns around AI-related disruption to software companies.”

“We continue to observe a meaningful disconnect between the public dialogue on private credit and the underlying trends in our portfolio,” Blue Owl said in the shareholder letters.

Shares of Blue Owl were down 1% in mid-morning trading Thursday after paring earlier losses.

The private credit industry has been roiled in recent months by concerns that it is overexposed to the software industry – an area that’s been under pressure over fears of disintermediation from artificial intelligence.

Software represents about 20% of portfolio exposure among business development companies, known as BDCs (a publicly traded proxy for private credit), according to Jefferies. Headline fears about default risk in the sector have driven a small but wealthy group of institutional investors to seek the exits from many of these funds.

“As public market dislocations and AI-related uncertainty reshape sentiment, dispersion is increasing across the sector, creating opportunities for experienced lenders to deploy capital selectively at improved terms,” the technology-focused letter reads.

Blue Owl, which is unique in having two of these nontraded private credit funds, is also among the last to report redemptions. The firm’s percentage of redemptions is multiples higher than its peers.

Most firms have opted to use the 5% cap, but some, including Cliffwater and Blackstone allowed slightly more redemptions.

Blue Owl’s OTIC technology fund saw redemption requests of 17% in the fourth quarter, which it fulfilled. OCIC’s requests were 5% in the fourth quarter.

The two funds previously drew interest from hedge funds Saba and Cox, which extended tender offers to locked-up holders at a steep discount.

Blue Owl said in the most recent quarter, its tech fund’s redemption requests were amplified by a more concentrated shareholder base, particularly within certain wealth channels and regions. For its flagship fund, the firm said the activity was driven by a “small minority of the investor base,” with 90% of shareholders electing not to tender.

Both funds saw gross inflows, which combined with the 5% gates resulted in modest net outflows.

Crypto markets are stuck in a holding pattern as geopolitical tensions in the Middle East cloud an otherwise improving macro backdrop, according to crypto asset manager Grayscale.

“The war in Iran overshadowed virtually all other market developments in March,” the Grayscale research team said in a Wednesday report.

Before the conflict escalated, global growth appeared to be strengthening and central banks were leaning toward rate cuts. That outlook has been disrupted by a sharp rise in oil prices, which has fueled inflation concerns and pushed interest rate expectations higher, weighing on risk assets and keeping investors on the sidelines, the report said.

Since the outbreak of the Middle East conflict, crypto markets have been volatile but broadly rangebound, with sharp headline-driven swings tied to oil prices and shifting risk sentiment. Bitcoin initially dropped into the mid-$60,000s on the first escalation, then rebounded toward the low-$70,000s before slipping back again as the conflict dragged on and macro conditions tightened.

More recently, renewed escalation has pushed bitcoin down roughly 10% from March highs, alongside declines in ether (ETH) and other tokens, as investors pulled back from risk assets. Despite the turbulence, performance has held up better than some traditional markets, with bitcoin roughly flat since the start of the war and even outperforming equities at times, underscoring both its sensitivity to macro shocks and its relative resilience.

For now, Grayscale expects many market participants to wait for greater clarity. If the conflict eases and energy prices retreat, markets could quickly reprice toward a more supportive macro environment. If not, persistently high oil prices may continue to pressure growth and delay a broader recovery.

Even so, crypto has shown notable resilience. Prices have held relatively steady through the volatility, suggesting a more durable bottom may be forming. The research team also pointed to continued inflows into spot crypto investment products and a pickup in futures positioning as signs that risk appetite is stabilizing beneath the surface.

Looking ahead, the report argued that the key catalyst for a sustained rebound will be a reduction in macro uncertainty. But it maintains that the long-term drivers of the asset class, including growing adoption of stablecoins and tokenized assets, remain intact.

The stablecoin market has expanded rapidly in recent years, with total supply rising from about $20 billion in 2020 to more than $300 billion by 2025, and sitting around $315 billion, according to industry data.

The sector added roughly $100 billion in 2025 alone, reflecting renewed growth after a brief contraction, as demand for dollar-pegged digital assets surged across trading, payments and onchain finance.

Periods of heightened uncertainty like the current one have historically presented attractive opportunities for long-term investors positioning for the next phase of growth, the report added.

Read more: Bitcoin holds ground as gold, silver slide on ETF outflows and liquidity strains: JPMorgan

XRP $5 $10 Potential

Beautiful tributes to Westhoughton musician Sam Lewis Eccles

As April 2026 Progresses, Family and Investigators Persist in Their Efforts

-

Business7 days ago

Business7 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

NewsBeat6 days ago

NewsBeat6 days agoThe Story hosts event on Durham’s historic registers

-

Tech7 days ago

Tech7 days agoIntercom’s new post-trained Fin Apex 1.0 beats GPT-5.4 and Claude Sonnet 4.6 at customer service resolutions

-

Sports6 days ago

Sports6 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment3 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment5 days ago

Entertainment5 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World2 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Crypto World19 hours ago

Crypto World19 hours agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech4 days ago

Tech4 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Sports2 days ago

Sports2 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech2 days ago

Tech2 days agoEE TV is using AI to help you find something to watch

-

Fashion4 days ago

Fashion4 days agoAmazon Sundays: Soft Spring Layers

-

Tech3 days ago

Tech3 days agoApple will hide your email address from apps and websites, but not cops

-

Tech3 days ago

Tech3 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Tech2 days ago

Tech2 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Politics3 days ago

Politics3 days agoShould Trump Be Scared Strait?

-

Crypto World3 days ago

Crypto World3 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Fashion7 days ago

Fashion7 days agoWhat Are Your Favorite T-Shirts for the Weekend?

-

Business6 days ago

Business6 days agoChinese universities with military links bought Super Micro servers with restricted AI chips

-

Fashion6 days ago

Fashion6 days agoWeekly News Update, 3.27.26 – Corporette.com

You must be logged in to post a comment Login