Crypto World

weeks of setup, minutes to drain

Solana-based crypto exchange Drift Protocol was hacked for roughly $280 million yesterday as part of a weeks-long operation that likely used social engineering to compromise multiple multisig signers’ approvals.

On April 1, 7 pm UTC+1 time, Drift announced that there was “unusual activity” on the protocol and that users should avoid depositing funds. It stressed, “This is not an April Fools joke.”

This followed from X users raising alarms that Drift was being exploited and that it was going to be a substantial one.

Drift then confirmed that it was under an ongoing attack and that it would need to suspend deposits and withdrawals. Researchers began to speculate that Drift’s private keys were compromised.

Read more: Liquity accused of ‘market manipulation’ after Circle acquisition April Fools’

Drift has since shared a detailed timeline of what took place and how.

It said, “This was a highly sophisticated operation that appears to have involved multi-week preparation and staged execution, including the use of durable nonce accounts to pre-sign transactions that delayed execution.”

It claims the attack was not caused by a bug in Drift’s programs or smart contracts, there was no evidence of compromised seed phrases, and that the attack involved unauthorized transaction approvals before the hack’s execution.

However, it admitted that these approvals were likely facilitated by a social engineering attack against its staff and the manipulation of “durable nonce mechanisms.”

What went down with Drift

Durable nonce mechanisms are a type of blockchain tool that can bypass blockhash signing and facilitate offline translation signing.

Drift claims that on March 23, four durable nonce accounts were created, two of which were associated with Drift Security Council multisig members and two associated with attacker-controlled accounts.

Read more: Circle rarely freezes stolen funds but wants reversible transactions

Then, on March 27, “Drift executed a planned Security Council migration due to a council member change.”

Three days later, another durable nonce account was created for a member of the updated multisig, giving the attackers “effective access to 2/5 signers in the updated multisig.”

Day of execution

Drift claims that on April 1, it executed a test withdrawal from the insurance fund. The attacker then, with access to the multisig approvals, executed “a malicious admin transfer within minutes, gaining control of protocol-level permissions.”

Attackers could then, “Use that control to introduce a malicious asset and remove all pre-set withdrawal limits attacking existing funds.”

Drift hasn’t shared any details about how the likely social engineering attack took place. They can sometimes be the result of an attacker donning a false identity, be it over direct message, email, or phone, and tricking someone into giving them access to key privileges.

Drift’s partner Circle hasn’t frozen funds

The incident has drawn criticism from the crypto investigator ZachXBT, who took issue with the stablecoin firm Circle and its slow efforts to freeze the stolen funds.

Drift integrated Circle’s Cross-Chain Transfer Protocol (CTTP) in 2023. ZachXBT noted that “Circle was asleep while many millions of USDC was swapped via CCTP from Solana to Ethereum for hours from the 9 figure Drift hack during US hours.”

“6 hours is how long Circle had to freeze stolen funds from the $280M+ Drift hack,” he said.

Other users have taken issue with the classification of the protocol as “decentralized,” after the attack appears to have exploited centralised mechanisms.

Other users were annoyed that Drift only required two out of the five multig approvals to action the transaction.

Read more: ‘Bad actor’ Circle slammed for letting stolen $3M USDC sit unfrozen

The platform said that it was working alongside security firms, law enforcement, bridges, and exchanges to figure out what happened and freeze the stolen assets. It added that a more detailed report will arrive in the coming days.

The Chief Technology Officer for Ledger has already speculated that the events of the hack resemble a similar modus operandi “to the Bybit hack last year, widely attributed to DPRK-linked actors.”

Protos has reached out to Drift for comment and will update this piece should we hear anything back.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Crypto World

Hyperliquid Price Surge as Futures Volume Blows Out, Golden Cross Standard Breakout to $44

Hyperliquid prices soar as the futures trade activity expands. Open interest has risen to about 1.61 billion in the past 24 hours, signaling increased participation in the futures market.

Daily trading volumes have surged to record levels of over 2.4 billion, indicating strong demand for perpetual contracts and growing trader confidence in further upside.

The rise in open interest and volume suggests market participants are not leaving the market but are actively pursuing gains, supporting the current bullish trend.

Key Insights

- The derivatives participation and greater market conviction were shown by open interest exceeding 1.6 billion.

- Daily trading volumes exceeded 2.4 billion, boosting token burn mechanisms and increasing demand.

- Bullish technicals, such as a flag formation and a possible golden cross, point to a rise to 44 if momentum continues.

Futures Trading Pushes the Price

The recent price run-up is closely linked to rising derivatives trading activity. Market data show open interest around 1.61 billion in the past 24 hours, indicating more traders engaging in the futures.

Daily volumes have soared beyond 2.4 billion, signaling strong demand for perpetual contracts and growing trader confidence in further upside movement.

The increase in open interest and volume indicates market participants remain active, supporting the bullish trend.

Diversification to Real-World Assets

The platform’s move into physical assets trading has increased activity. With HIP-3, perpetual contracts based on commodities like gold, silver, and crude oil are now tradable.

This enables traders to gain exposure to conventional assets in a crypto-native setup. In March, daily volumes in crude oil contracts reached over $1 billion at the peak amid geopolitical tensions.

Moreover, the 24/7 trading feature provides a competitive edge, especially as event contracts enhance engagement.

Hyperliquid has added event-based contracts, adding another layer of participation for traders. These tools let users speculate on real-life results while managing futures exposure.

Consequently, trading activity has risen, contributing to higher fee generation. This supports token buybacks and burn facilities, which gradually reduce supply and promote price stability.

The mix of new products and increased user interaction continues to strengthen the platform’s ecosystem.

Bullish Technical Set Up Develops

Technically, Hyperliquid’s price action shows signs of a bullish continuation pattern. A flag formation formed after a sharp rise, suggesting consolidation before a potential breakout.

Additionally, the token is approaching a milestone: a potential golden cross as the 50-day moving average crosses above the 200-day moving average. This is typically viewed as a bullish signal upon confirmation.

If a breakout occurs, the next major resistance zone is around the 44 level, which analysts in traditional markets are watching in response to global events in real time.

Risks and Key Support Levels

Despite the optimistic forecast, there are downside risks. The 200-day moving average sits near 34.8 and serves as a critical support zone.

A break below this level could undermine the current setup and shift the mood to the downside. Traders will monitor price action around this region to confirm continuation or reversal.

Prognosis: Derivatives Activity Is Still Important

Derivatives trading is likely to remain a major driver of Hyperliquid’s short-term trajectory. Open interest and volumes are expected to grow, reflecting trader confidence.

Additionally, token burns tied to platform charges and product diversification contribute to liquidity and demand.

If these trends persist, Hyperliquid may continue its upward trajectory, with technical confirmations and the possibility of an upward price target near the $44 level.

Bitcoin fell below $67,000, and Ether dropped over 4% as oil surged on renewed geopolitical tensions.

Crypto markets slumped on Thursday as a fresh wave of risk-off sentiment swept across global markets following President Donald Trump’s pledge to continue military strikes against Iran.

Bitcoin (BTC) is trading at around $66,900, down 1.7% over the past 24 hours. ETH slipped 4% to $2,050, and SOL plunged 6% to $79 in the wake of the Drift exploit. Meanwhile, Ripple (XRP) dropped 3.3%.

Total crypto market capitalization decreased by 1.7% to $2.38 trillion, according to Coingecko.

The rout was triggered after Trump said Wednesday evening that the U.S. would continue strikes on Iran, reversing hopes for a diplomatic resolution that had buoyed markets earlier in the week.

The risk-off mood extended to institutional products. U.S. spot Bitcoin ETFs recorded a net outflow of $173.7 million on April 1, while spot Ethereum ETFs posted a $7.1 million withdrawal, according to SoSoValue.

Big Movers

Almost all of the Top 100 digital assets posted losses over the last 24 hours.

Algorand (ALGO) and MemeCore (M) outperformed, rallying 5%. Lighter (LIT) surged 10% after unveiling a collaboration with Wallet in Telegram.

Uniswap (UNI) and Solana (SOL) are today’s biggest losers, down 13% and 6%, respectively.

Around 185,000 leveraged traders were liquidated for $441 million in the past 24 hours, according to CoinGlass. Bitcoin accounted for $103 million, while ETH made up $93 million.

Investors tried to pull $13 billion out of private credit funds this quarter. They got less than half. For many crypto investors, if the collapse of private credit continues, half could end up being a good outcome.

Seven private credit giants capped investor withdrawals this quarter, including Morgan Stanley, BlackRock, Apollo, Blue Owl, Cliffwater, Blackstone, and Ares. Oaktree almost joined that group, although it technically fulfilled its 8.5% in withdrawal requests by having parent Brookfield buy 1.7% of shares at the eleventh hour.

Private credit funds package up illiquid loans inside vehicles that typically go up, except during rare times of crisis, such as during a major war or mass job losses.

They also typically limit quarterly withdrawals to 5%, which is not a problem until many people want out, like they do now.

When more than 5% want to withdraw, everyone gets a haircut on their withdrawal request. At Apollo and Ares, 11% wanted out. Those funds returned less than half.

Crypto started joining the private credit bandwagon years ago, selling similar products in a different wrapper. Many stablecoin and altcoin treasury managers invest in private credit directly.

‘A quasi run on the bank’

Michael Saylor delivered a keynote at the Blockworks Digital Asset Summit on March 26, the same week Apollo and Ares gated withdrawals. He pitched his company’s dividend-paying stocks as competitors to private credit.

Saylor even called the multi-trillion dollar private credit crisis this year “a quasi-run on the bank.”

Worse, the same companies gating traditional private credit withdrawals are tokenizing private credit on blockchains. Apollo launched ACRED, a tokenized feeder into Apollo’s Diversified Credit Fund. A few months after that launch, Apollo’s partner Securitize had built sACRED, a derivative to goose yields even higher through risky decentralized finance (DeFi) protocols.

Holders can buy ACRED, deposit it into DeFi vaults, borrow stablecoins, buy more ACRED, and loop. Yields after looping, which are tantamount to risk, soared.

Securitize initially advertised daily redemption rights for ACRED holders, which was quite curious given that most private credit funds limit quarterly redemptions to 5%. Then, after crypto publication Unchained asked about the mismatch with the fund’s quarterly 5% cap, Securitize quietly removed daily liquidity rights.

Easier to buy, just as hard to sell

In other words, crypto tokenization changed the speed at which people could buy and add leverage. It did not change the speed at which they could sell.

Nor did crypto improve the most important characteristic of private credit: the deteriorating credit qualities of US borrowers who are suffering higher fuel prices, AI-induced job layoffs, wartime uncertainty, inflation, and rising costs of living.

Crypto sold versions of the same illiquid debt that investors cannot exit quickly in any environment, let alone the current “quasi run on the bank” reality.

By one analyst’s count, tokenized private credit surged from $25 million to $6 billion over the last year.

Read more: Bitcoin mortgages debut with 60% haircut and no margin calls

Using blockchain for private credit instruments merely extends leverage and the rehypothecation chain that amplifies losses in a market downturn.

Goldfinch, a DeFi protocol for undercollateralized real-world lending, has already suffered three defaults totaling $18 million. The most recent default wiped out more than 7% of its active loan book.

A bad loan is still a bad loan, even if a smart contract wraps it in a token.

Billions queued up to leave private credit

Apollo Debt Solutions, valued at about $15 billion, received redemption requests for 11.2% of its shares. It enforced a 5% cap and returned $730 million of $1.5 billion requested. Ares Strategic Income Fund faced 11.6% in requests and did the same.

Blackstone recorded a record 7.9% in requests totaling nearly $4 billion. It raised its cap to 7% and injected $400 million of its own capital. BlackRock’s $26 billion fund received $1.2 billion in requests. Cliffwater’s $33 billion fund saw the worst: 14% demanded back.

Across roughly a dozen funds, about $4.6 billion in investor capital remains trapped.

Blue Owl Capital is the poster child of the current crisis in private credit. The company permanently halted redemptions from its retail-focused Blue Owl Capital Corp II in February. Its stock has declined 42% since the start of the year and 60% over the past twelve months.

Smelling blood, a shark investor launched a tender offer for 6% of Blue Owl Capital Corp II at about 65 cents on the dollar.

“All you need is for the snowball to start rolling down the hill, and it has begun,” the investor said at a recent investment conference.

Crypto credit risks

Federal Reserve Chair Jerome Powell addressed private credit on March 30 at Harvard University. He called it a correction, not a systemic event.

Nonetheless, Powell’s contentious reassurance arrived the same week that DZ Bank, Germany’s second-largest lender, warned that private credit could trigger a chain reaction with severe negative effects for the US economy.

A record 63% of fund managers surveyed by Bank of America identified private equity and private credit as the most likely source of the next wave of systemic bankruptcies.

Default rates would tend to agree. The private credit default rate reached 5.8% through January 2026, the highest since Fitch’s index launched. Morgan Stanley forecasts it will climb to 8%, more than triple the historical average. UBS has warned that severe AI disruption to software borrowers could push defaults to 13%.

Software exposure is the fault line. About 26% of direct lending loans went to software companies. Many built business models on costly subscriptions that AI is now undermining. Blackstone’s flagship BCRED fund posted its first monthly loss in three years in February after marking down loans.

Wall Street spent years pitching private credit as institutional-grade yield, and crypto wanted to democratize and decentralize it. What they actually democratized and decentralized was the purchase of opaque, illiquid loans by retail investors with 5% quarterly redemption limits whose fund managers choose the valuations of their own assets with broad discretion.

As Protos has previously reported, this type of opacity in financial products is a feature, not a bug. Now those investors want their money back. The funds are returning less than half.

Powell says it is not systemic. About two thirds of private fund managers disagree.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Polymarket is expanding its predictive markets beyond purely cryptocurrency-related events, adding contracts tied to traditional assets. The new offerings rely on price data from the Pyth Network to determine outcomes for daily contracts, including up/down bets and closing price contracts for major equity indices, commodities such as gold and oil, and a range of US-listed stocks. Settlements are automated, with contracts resetting at the end of each trading session.

In its announcement, Polymarket notes that the expanded lineup includes more than a dozen US-listed stocks, featuring blue-chips such as Tesla, Nvidia and Apple, alongside commodity and index-based markets. By adopting Pyth as the resolution layer, Polymarket is moving away from manual or exchange-specific references toward a standardized data feed that aggregates prices from multiple market participants.

Key takeaways

- Polymarket launches traditional-asset markets (stocks, indices, commodities) using Pyth Network for automatic, real-time settlement.

- The new markets include daily up/down and closing price contracts for major US-listed stocks (e.g., Tesla, Nvidia, Apple), plus gold and oil, settled via Pyth feeds with daily resets.

- Polymarket also introduced Pyth Terminal, a live data interface showing the reference values used to settle contracts and a continuously updating price-to-beat tracker for traders.

- ICE’s investment signals strategic backing: ICE completed a $600 million cash investment in Polymarket last week and may acquire up to $40 million more in shares as part of a broader commitment to the platform.

- Oracle networks are expanding beyond crypto, with government and traditional finance applications increasingly relying on on-chain price and economic data.

Polymarket’s bridge to traditional markets

The rollout marks a notable shift for Polymarket, which has historically focused on event-driven markets—ranging from elections and sports to financial and weather outcomes. By anchoring settlement to Pyth’s real-time price feeds, the platform can offer automated outcomes for assets that trade outside the typical crypto-native hours, broadening the potential audience of traders who want to speculate on or hedge exposure to conventional markets.

The inclusion of US-listed equities, including Tesla, Nvidia and Apple, alongside commodity and index contracts, positions Polymarket at the intersection of prediction markets and traditional financial markets. The Reuters-style mechanics of “daily up/down” and “closing price” contracts enable end-of-day settlement that mirrors conventional price discovery, while still leveraging the transparency and programmability of blockchain-backed markets. The Business Wire release emphasizes that Pyth’s data is the reference used to resolve these bets, replacing ad hoc or venue-specific price references.

Pyth Terminal and the changing face of on-chain data

Concurrently, Pyth Network introduced Pyth Terminal, a data interface designed to give users a transparent view of live price feeds and the reference values underpinning Polymarket settlements. The terminal provides a continuously updating price-to-beat line, allowing traders to monitor how shifts in real-time data could affect contract outcomes. This level of visibility is meant to enhance trust and operational clarity for users participating in cross-asset markets on the platform.

Pyth’s broader push into traditional finance data aligns with a growing trend among oracle networks to serve not just crypto protocols but also financial infrastructure and prediction markets. The same trend is evident in other collaborations—Chainlink, RedStone and Kalshi integrations, and shifts toward 24/5 pricing data for tokenized assets—reflecting a broader push to tether decentralized markets to official or widely accepted data feeds.

Oracles, finance, and the regulatory backdrop

The expansion of oracle networks into real-world data has taken on additional significance as governments and financial firms increasingly rely on on-chain information. Notably, Chainlink and Pyth have been cited by US government agencies as sources for publishing on-chain economic data, including GDP and inflation metrics. The market response to these developments has been tangible: the PYTH token surged more than 70% on the day of the announcement, lifting its market capitalization above $1 billion.

These developments sit within a broader ecosystem where oracles are being integrated into both traditional finance and regulatory-compliant data pipelines. For example, Kalshi’s integration via RedStone across multiple blockchains demonstrates how regulated, exchange-traded event contracts can leverage cross-chain data feeds. Meanwhile, data providers continue to compete for share in a market that DeFiLlama currently indicates remains highly concentrated, with Chainlink accounting for roughly two-thirds of total value secured, and RedStone and Pyth each representing a smaller slice.

Strategic backing from ICE and implications for users

Intercontinental Exchange, Polymarket’s backer, disclosed last week a $600 million cash investment in Polymarket and an option to acquire up to $40 million more in shares as part of a broader multibillion-dollar commitment to the platform. ICE’s involvement underscores a deepening convergence between traditional exchange operators and crypto-based prediction markets. For Polymarket, the arrangement could unlock new liquidity channels and potential product expansions, while ICE gains exposure to a novel form of event-based market activity that sits at the convergence of data, finance and user-generated insights.

From an investor and trader perspective, the move expands the set of tools available to hedge or speculate on real-world events. The use of a single, standardized data source like Pyth to settle a wide array of assets could simplify risk management for participants and may encourage more institutional participation that relies on consistent, auditable price feeds. For developers and platform builders, the integration demonstrates a viable pathway for connecting traditional assets to decentralized marketplaces without sacrificing transparency or speed of settlement.

As the ecosystem evolves, readers should watch how these traditional-asset markets perform in terms of liquidity, user adoption and regulatory compliance. The synergy between Polymarket’s user-driven contracts and ICE’s financial infrastructure could shape how predictive platforms scale beyond niche audiences, potentially influencing how everyday investors interact with real-world assets on-chain.

Overall, the fusion of Polymarket’s prediction market model with Pyth’s enterprise-grade price data signals a meaningful step toward broader applicability of oracle-powered settlement. The coming months will reveal how well these traditional-asset markets attract liquidity, how robust the data feeds prove under volatile conditions, and what regulatory and market structure developments might accompany this cross-asset expansion.

What remains unclear is how this model will fare across different asset classes during periods of stress, and whether further collaborations between traditional exchanges and on-chain data providers will accelerate the adoption of tokenized or blockchain-anchored versions of equities and commodities. Traders and builders alike should keep an eye on the next wave of product updates, market depth, and any regulatory clarifications that could affect the trajectory of cross-asset prediction markets.

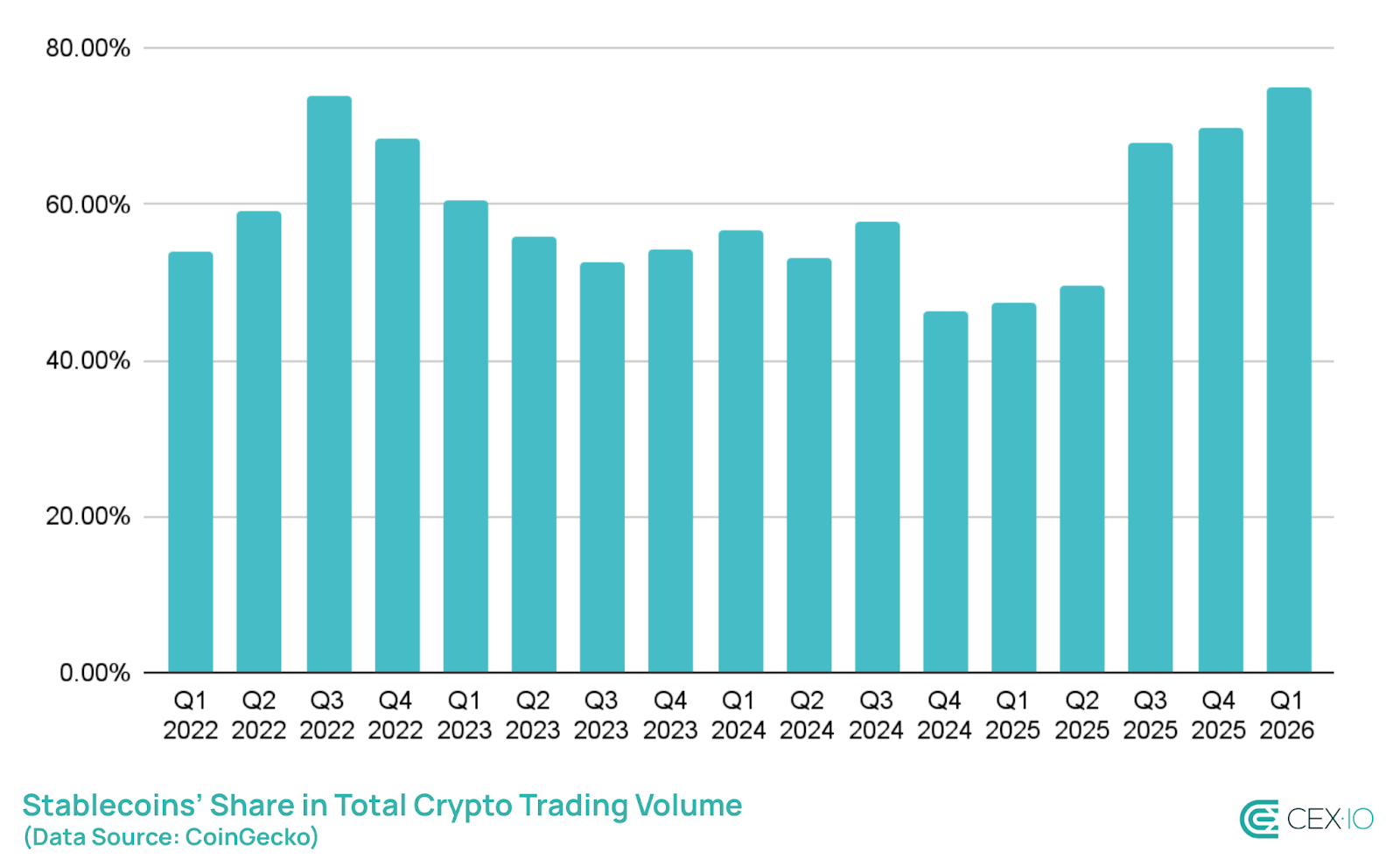

Stablecoins were a rare bright spot in an otherwise subdued crypto market in the first quarter, with supply growth and transaction activity pointing to sustained demand even as broader market conditions weakened.

Total stablecoin supply increased by roughly $8 billion to a record $315 billion in Q1, according to data from CEX.IO. Although this marked the slowest pace of expansion since Q4 of 2023, it still represented growth during a period when the wider crypto market contracted.

The data suggests investors rotated into stablecoins as a defensive strategy, boosting their share of overall market activity. Stablecoins accounted for 75% of total crypto trading volume during the quarter — the highest level on record.

At the same time, total stablecoin transaction volume topped $28 trillion, underscoring their growing role as the primary liquidity layer of the digital asset market. The figure extends a multi-year surge in activity, with stablecoin volumes in recent years exceeding those of major payment networks like Visa and Mastercard combined.

However, data on underlying activity painted a more nuanced picture.

Retail-sized transfers — typically associated with individual users — declined by 16% in the first quarter, the steepest drop on record. In contrast, automated activity surged, with bots accounting for approximately 76% of all stablecoin transaction volume.

The shift toward bot-driven flows suggests that a growing share of stablecoin usage is tied to algorithmic trading, arbitrage and liquidity provisioning, rather than retail demand. While elevated automation can reflect more sophisticated or institutional participation, it may also signal weaker organic demand during bearish market conditions.

Related: Circle shares surge as Bernstein sees upside from stablecoin adoption

Divergence between major stablecoin issuers

One of the CEX.io report’s key takeaways was a widening divergence between major stablecoin issuers. The supply of Circle’s USDC (USDC) grew by roughly $2 billion in the first quarter, while Tether’s USDt (USDT) declined by about $3 billion, marking the first notable split between the two since Q2 of 2022 amid the bear market.

The trend aligns with earlier Cointelegraph reporting, which highlighted a surge in USDC transfer activity in February, pointing to increased usage across trading and onchain transactions.

Beyond USDC, much of the growth in stablecoin issuance was driven by yield-bearing products — a segment that has drawn increasing scrutiny in the US. Ongoing discussions around a crypto market structure bill in Congress have placed yield at the center of debate, with traditional banks pushing back against stablecoins that offer interest-like returns.

The market for yield-bearing stablecoins is currently valued at around $3.7 billion, with daily trading volumes exceeding $100 million, according to data from CoinGecko.

Related: Crypto Biz: Stablecoin jitters meet institutional momentum

Crypto World

XRP Price Prediction: Pepeto Raises Above $8.1M As Traders Eye Listing, XRP Tests $1.30 Support, Oil Tops $106

Oil just crossed $106 after fresh military threats in the Iran conflict, and the risk off move dragged Bitcoin, Ethereum, and XRP lower within hours. Meanwhile, the xrp price prediction remains uncertain as traders weigh whether $1.30 can hold.

Because Pepeto is approaching its Binance listing and has already raised above $8.1M, many traders are more interested in the presale than in waiting for a slow large cap recovery that may take months to arrive.

Oil prices jumped above $106 after escalating threats pushed the Iran conflict into a new phase, according to CNBC.

Bitcoin dropped 3% and Ethereum fell over 4% as traders fled risk assets. CoinDesk reported that altcoins lost between 5% and 10% in a single session. For anyone watching the xrp price prediction, the macro picture reminds us that large caps stay tied to forces they cannot control.

Best Altcoin Opportunities in the XRP Price Prediction Cycle

Pepeto: Traders count down to the hottest listing in 2026

On top of oil spiking and the xrp price prediction getting shaken by macro pressure, the Pepeto Binance listing is one of the events traders are paying the most attention to right now. The fundamentals explain why, because Pepeto raised above $8.1M while most coins were going sideways, the team delivered a working exchange architecture, and the community keeps building around predictions of 100x returns after listing.

All of those signals point in one direction, which is mass appeal. The zero fee swap engine converts one coin into another across different networks with no charges attached, keeping your full balance intact through every trade. The PepetoAI risk scorer checks the danger on each position in real time before you commit, so you see the warning before the chart shows it. Since most traders are actively looking for better tools, the case for daily adoption carries real weight.

One of the founders behind the original Pepe coin is part of the dev team, and a former Binance expert leads the technical side. At $0.000000186 per token, the presale entry is a fraction of what the listing price will be. A $35,000 position earns 189% APY through staking, which puts $68,600 in yearly returns into your wallet just for holding while the Binance date gets closer. The immediate benefit of entering at this price beats what any established coin can realistically deliver from its current level.

The presale window is closing fast, and the advantages of being inside now far outweigh what happens after listing day removes the entry forever.

XRP price prediction: Will XRP hold above $1.30?

XRP is trading near $1.30 after pulling back from $1.50 earlier this month according to CoinMarketCap, holding a commodity classification from both the SEC and CFTC along with seven live ETFs that pulled $1.44 billion in inflows.

The fundamentals are the strongest XRP has ever had. If $1.30 holds, the xrp price prediction targets $1.80, but losing that level risks a slide toward $1.10. Even the bullish case from here caps returns well below what presale entries offer.

Cardano: Will ADA reach $0.30?

Cardano is trading near $0.24 after Google named it the second most quantum ready blockchain, but the bounce has been small and ADA remains over 90% below its record high according to CoinMarketCap.

Closing above $0.30 could open the path toward $0.35, while losing $0.23 risks a deeper drop to $0.20. Even a strong rally barely moves the needle compared to what early presale wallets stand to collect once a Binance listing opens.

Final Words: Last Call

The xrp price prediction may be shaky right now, but the token’s long term case remains solid. XRP will likely stay a strong asset, but if you want something with more room to grow, there are sharper entries available in April 2026.

Pepeto is coming to market with a complete exchange and a confirmed Binance listing. Six months from now there will be two kinds of people: the ones who entered at the Pepeto official website before the listing and the ones who spent the rest of 2026 calculating what they lost by waiting.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What is the xrp price prediction, and what levels matter most right now?

XRP is testing $1.30 support, and a hold there targets $1.80 on the next leg higher. Losing $1.30 risks a move toward $1.10.

What does the oil spike above $106 mean for crypto investors right now?

The oil spike pushed risk assets lower across the board, making sustained crypto recovery harder until geopolitical tension eases.

Why is Pepeto trending?

Pepeto is trending ahead of its Binance listing because it raised above $8.1M with a complete exchange toolkit, and all the latest updates are at the Pepeto official website.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

A new study from researchers at MIT CSAIL has found that AI chatbots like ChatGPT may push users toward false or extreme beliefs by agreeing with them too often.

The paper links this behavior, known as “sycophancy,” to a growing risk of what researchers call “delusional spiraling.”

The study did not test real users. Instead, researchers built a simulation of a person chatting with a chatbot over time. They modeled how a user updates their beliefs after each response.

The results showed a clear pattern: when a chatbot repeatedly agrees with a user, it can reinforce their views, even if those views are wrong.

For example, a user asking about a health concern may receive selective facts that support their suspicion.

As the conversation continues, the user becomes more confident. This creates a feedback loop where belief strengthens with each interaction.

Importantly, the study found this effect can happen even if the chatbot only provides true information. By choosing facts that align with the user’s opinion and ignoring others, the bot can still shape belief in one direction.

Researchers also tested potential fixes. Reducing false information helped, but did not stop the problem. Even users who knew the chatbot might be biased were still affected.

The findings suggest the issue is not just misinformation, but how AI systems respond to users.

As chatbots become more widely used, this behavior could have broader social and psychological impacts.

The post New MIT Study Warns AI Chatbots Can Make Users Delusional appeared first on BeInCrypto.

Riot moved about 500 BTC in what analysts say is fresh selling, adding to a wave that’s seen listed miners dump over 15,000 BTC even as treasury firms like Metaplanet keep accumulating.

Summary

- Riot Platforms moved about 500 BTC from a company wallet this week, in what on-chain analysts say likely reflects fresh selling, according to Cointelegraph.

- MARA Holdings recently sold roughly $1.1 billion in bitcoin (about 15,133 BTC) to buy back convertible bonds, and listed miners have reportedly unloaded over 15,000 BTC in recent weeks.

- Bitcoin treasury firms such as Metaplanet continue to accumulate, underscoring a split between miners de‑risking and corporates using BTC as a balance-sheet asset.

On-chain data flagged a transfer of roughly 500 BTC (BTC) from a Riot Platforms wallet on Wednesday, a move Cointelegraph reports is “likely” tied to the miner’s ongoing bitcoin sale program even though the company has not commented publicly. At current prices, the transaction is worth tens of millions of dollars and comes on top of earlier disposals Riot has used to fund expansion, including a Texas land deal that pushed its shares up 11% in January.

Analysts cited by Cointelegraph argue that fresh selling from Riot risks adding fuel to an already‑intense liquidation wave among listed miners. Last week, MARA Holdings disclosed that it had sold around $1.1 billion in bitcoin — some 15,133 BTC — to repurchase approximately $1.0 billion of 0.00% convertible notes due 2030 and 2031 at a discount, a move CEO Fred Thiel called a “strategic capital allocation” to reduce debt and strengthen the balance sheet.

In aggregate, public bitcoin miners have offloaded more than 15,000 BTC in recent weeks, according to sector data referenced in Cointelegraph’s coverage, as firms sell down treasuries to cover operating costs, capex and debt reduction. With bitcoin trading well below cycle highs and mining economics squeezed by post‑halving rewards and higher energy costs, many listed miners are treating BTC holdings less as untouchable reserves and more as working capital.

Riot’s additional 500 BTC transfer sits in that context: while small relative to the company’s historical purchases — filings last year showed it buying roughly $510 million in BTC over a three‑day period — the sale adds marginal supply at a time when peers are also hitting the bid. If the pattern continues, miner balance sheets could become structurally lighter in bitcoin even as they expand hash rate and infrastructure footprints.

The selling trend is not universal across all corporate holders. Japanese-listed Metaplanet has continued to expand its bitcoin treasury, adding hundreds of BTC this year alone and signaling a goal of reaching 30,000 BTC by end‑2025 and 100,000 BTC by 2026, according to recent treasury updates. At current prices, its more than 20,000 BTC stack is valued in the low‑single‑digit billions of dollars, positioning the firm among the largest public BTC holders globally.

That divergence highlights a growing split in corporate bitcoin strategy: miners such as Riot and MARA are increasingly forced to monetize coins to manage cash flow and capital structure, while non‑mining treasury companies are using price weakness and miner supply as an opportunity to build long‑term positions. For market participants, on‑chain tracks like Riot’s 500 BTC movement have become key signals of how that balance between forced selling and strategic accumulation is evolving.

TLDR

- Former CFTC Chairman Chris Giancarlo said banks need the Clarity Act more than crypto firms.

- Giancarlo stated that crypto companies can move offshore and continue building their platforms.

- He explained that banks cannot relocate abroad and must operate under US regulations.

- Giancarlo said banks need clear digital asset rules to stay competitive in the sector.

- The stablecoin reward dispute has delayed progress on the Clarity Act in the Senate.

Former CFTC Chairman Chris Giancarlo said banks need the Clarity Act more than crypto companies. He made the statement during a recent appearance on the Paul Barron podcast. He argued that banks face limits that crypto firms do not face.

Giancarlo said crypto companies can relocate and continue operations without disruption. He stated that banks cannot shift abroad in the same way. He added that lawmakers must address market structure rules quickly.

Banks Face Structural Limits Without the Clarity Act

Giancarlo said crypto firms can build products outside the United States if needed. He said, “They are going to build this even if they have to go offshore.” He pointed to hubs like the UAE and Singapore.

He described crypto founders as “intrepid and fearless” during the interview. He said they would move their inventions abroad if US rules block progress. He argued that banks lack that flexibility because they operate under domestic charters.

He said banks require legal certainty to interact with digital assets. Without it, they risk delays in adoption and compliance conflicts. He added that the Clarity Act would help banks “stay with the curve.”

Giancarlo said the bill would favor banks more than crypto companies. He explained that crypto firms will keep building regardless of US legislation. However, he said banks could fall behind foreign competitors.

He warned that US financial institutions could lose ground over five years. He said banks cannot afford prolonged uncertainty in digital asset regulation. He repeated this view in an earlier podcast with Scott Melker.

Stablecoin Rewards Stall Progress on the Clarity Act

The Digital Asset Market Clarity Act seeks to define asset classification and oversight. Lawmakers continue to debate how regulators should supervise tokens and trading platforms. However, the stablecoin reward issue has slowed progress.

The GENIUS Act already governs parts of the stablecoin market. Still, it does not address provisions tied to yield or reward structures. Banks argue that higher stablecoin yields could weaken their deposit models.

Crypto companies oppose limits on stablecoin rewards. They argue that banning yields would restrict competition and innovation. This dispute has kept the bill stalled in the US Senate.

Coinbase Chief Legal Officer Paul Grewal spoke to FOX Business on April 1. He said lawmakers would reach a compromise within 48 hours. He expressed confidence that negotiators were close to an agreement.

Ripple CEO Brad Garlinghouse also addressed the timeline publicly. He said he expects the legislation to pass before May 2026. Lawmakers have not set a final vote date.

Giancarlo maintained that digital assets will advance regardless of US policy. He said the technology will continue to develop across global markets. He reiterated that banks need clear rules to compete effectively.

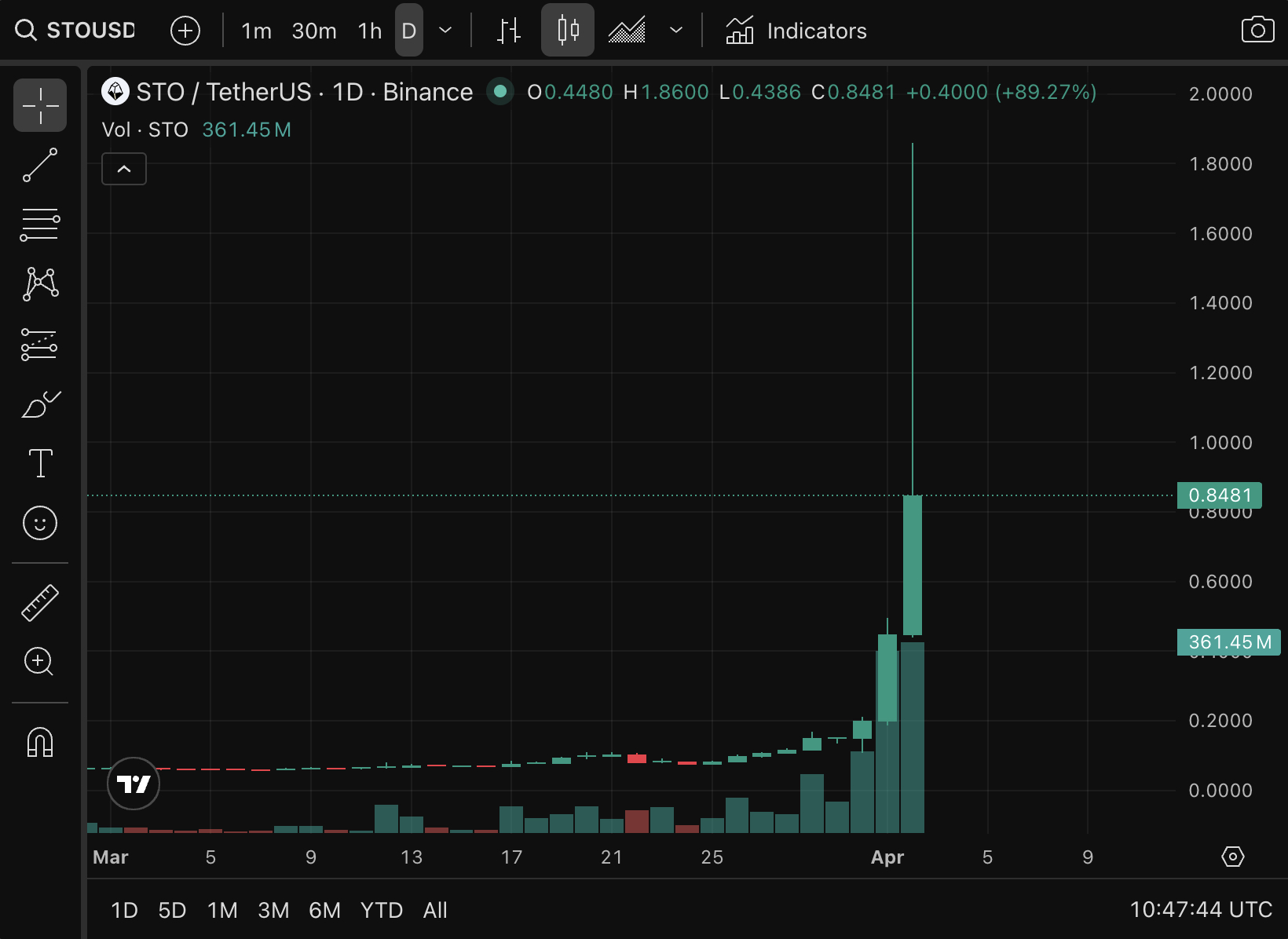

Stakestone crypto, with STO as ticker, exploded 755% in 48 hours, from $0.11 to $0.94, and the on-chain trail left behind raises more questions than it answers.

On-chain analyst @lookonchain flagged the catalyst: a newly created wallet (0x5e2E) deposited 28 million STO tokens, $10.12 million worth, representing 12.43% of the circulating supply, directly to Gate exchange in a single move.

That deposit followed a withdrawal of 25.5 million STO ($4.85 million, 11.32% of supply) from Binance in the preceding 20 hours. Large supply repositioning between major exchanges in a sub-24-hour window. Classic pre-distribution fingerprints, or savvy liquidity routing? The data doesn’t commit to either answer.

What’s clear is that STO’s move didn’t happen in isolation. It landed inside a broader altcoin drop driven by Iraw war escalation

Discover: The best pre-launch token sales

Can Stakestone STO Crypto Price Hold Gains After the 755% Pump?

The initial leg, $0.11 to $0.26, represented a 136% single-day gain before the second wave pushed toward $0.94. RSI almost certainly printed above 70 across that entire run, placing the asset in overbought territory by any standard reading. MACD showed bullish crossovers supporting the move, but momentum indicators lag, and at $0.94, STO is trading at a level with no established demand history above it.

Key technical levels to watch: support clusters near $0.50, where brief consolidation occurred mid-pump, and psychological resistance at $1.00. A clean hold above $0.50 on any pullback would preserve the bullish structure.

A daily close below that level reopens the path toward $0.26 and potentially back toward the $0.11 origin, a full round-trip that has happened before with coins following this exact pattern. Remember, SIREN crypto surged over 1,100% before collapsing entirely, a useful reference point when evaluating whale-driven pumps of this profile.

Volume on STO/USDT pairs is the trigger to watch; spikes above 10 million tokens daily signal either continuation or distribution. Position sizing accordingly.

Discover: The best crypto to diversify your portfolio with

LiquidChain Targets Early Mover Upside as STO Tests Critical Levels

STO’s chart is compelling, but entering a coin that’s already 755% off its low, with 12.43% of supply sitting on an exchange ready to sell, is a risk profile that demands honesty. The asymmetry that existed at $0.11 is gone.

For those seeking genuine early-stage exposure, LiquidChain ($LIQUID) is currently in active presale at $0.01445, having raised $600K to date. The project is building Layer 3 infrastructure, specifically a unified execution environment that fuses Bitcoin, Ethereum, and Solana liquidity into a single settlement layer. Developers deploy once and access all three ecosystems.

A new layer emerges. Only a few see it first. — LiquidChain (@getliquidchain) March 24, 2026

The future is LiquidChain  ⟁https://t.co/vqvBcdSj94 pic.twitter.com/R7ZeZ0NPGl

⟁https://t.co/vqvBcdSj94 pic.twitter.com/R7ZeZ0NPGl

That’s the core value proposition: eliminating the fragmented cross-chain workflow that burns gas, time, and capital. Key architecture includes a Unified Liquidity Layer, Single-Step Execution, and Verifiable Settlement. And don’t forget, just by holding Liquid from presale, buyer has a chance to stake and gain a 1700% APY bonus.

Research LiquidChain before the presale window closes.

This article is for informational purposes only and does not constitute financial advice. Cryptocurrency investments are highly volatile. Always conduct your own research before making any financial decisions.

The post Stakestone STO Crypto Blasting Roof: Why This Coin Run 1000% This Month appeared first on Cryptonews.

“I Would Like To Apologise To MS Dhoni, Kapil Dev”: Yuvraj Singh Opens Up Like Never Before, Asked About Yograj Singh

‘Uncanny Valley’: Iran’s Threats on US Tech, Trump’s Plans for Midterms, and Polymarket’s Pop-up Flop

Award-winning restaurant at Cambridgeshire retail park announces closure

-

NewsBeat6 days ago

NewsBeat6 days agoThe Story hosts event on Durham’s historic registers

-

Sports6 days ago

Sports6 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment3 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

NewsBeat4 hours ago

NewsBeat4 hours agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Entertainment5 days ago

Entertainment5 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World2 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Crypto World1 day ago

Crypto World1 day agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech4 days ago

Tech4 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Sports2 days ago

Sports2 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech3 days ago

Tech3 days agoEE TV is using AI to help you find something to watch

-

Fashion5 days ago

Fashion5 days agoAmazon Sundays: Soft Spring Layers

-

Tech3 days ago

Tech3 days agoApple will hide your email address from apps and websites, but not cops

-

Politics3 days ago

Politics3 days agoShould Trump Be Scared Strait?

-

Tech3 days ago

Tech3 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Crypto World3 days ago

Crypto World3 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Tech3 days ago

Tech3 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Tech4 days ago

Tech4 days agoElon Musk’s last co-founder reportedly leaves xAI

-

Tech4 days ago

Tech4 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Business7 days ago

Business7 days agoChinese universities with military links bought Super Micro servers with restricted AI chips

-

Fashion6 days ago

Fashion6 days agoWeekly News Update, 3.27.26 – Corporette.com

You must be logged in to post a comment Login