Crypto World

Crypto Long & Short: Asia’s digital asset crackdown: accountability gets personal

Welcome to our institutional newsletter, Crypto Long & Short. This week:

- Bob Williams on how stricter crypto regulations in Asia are putting more personal responsibility on senior leaders, making strong governance and D&O insurance essential.

- The FBI’s Haidy Grigsby on how crypto scams are increasingly targeting experienced investors by building trust and tricking them into making larger deposits until their money is gone.

- Top headlines institutions should pay attention to by Francisco Rodrigues.

- Hyperliquid’s TradFi bet is now 40% of its own volume in Chart of the Week.

Expert Insights

Asia’s digital asset crackdown: accountability gets personal

By Bob Williams, FinTech, digital assets, & blockchain advisory leader (Asia/Pacific), Lockton Companies

A new wave of digital asset regulations across Asia is increasing pressure on trading platforms and asset managers to strengthen governance — and to reassess their Directors’ and Officers’ (D&O) liability insurance arrangements.

In recent months, three leading digital asset hubs — Hong Kong, Singapore and South Korea — have announced plans to refine their respective regulatory frameworks. As regulatory expectations rise and senior management’s personal accountability becomes clearer, platform operators must stay informed of these developments and evaluate whether their existing risk transfer strategies remain fit for purpose.

Hong Kong: expanding accountability beyond governance

In August 2025, Hong Kong’s Securities and Futures Commission (SFC) issued a circular to licensed virtual asset trading platform operators clarifying senior management’s responsibilities regarding the custody of clients’ virtual assets. The circular reinforces expectations around governance, internal controls and effective oversight, signaling a continual shift toward personal accountability for directors and senior management.

An emerging consideration from the SFC’s consultation process is whether virtual asset management service providers should be permitted to rely on non‑SFC‑regulated or offshore custodians. From an insurance perspective, the availability of coverage for virtual asset risks is closely tied to the robustness of custody arrangements, including security controls, operational resilience and asset protection standards. To date, insurance capacity has largely been supported by the prescriptive requirements imposed on SFC‑regulated custodians and platforms.

If alternative custody models are permitted, ensuring that non‑regulated or offshore custodians are held to equivalent standards, including appropriate insurance coverage will be critical. Without alignment, firms that have invested heavily to meet Hong Kong’s regulatory and insurance expectations may face a competitive disadvantage, while the objective of enhancing investor protection and market integrity could be undermined.

Singapore: reinforcing senior management competency

In 2025, Singapore introduced licensing requirements for digital token service providers serving only overseas customers, bringing a broader range of firms within the Monetary Authority of Singapore’s regulatory perimeter.

Under the licensing guidelines, the competency and fitness of key individuals are core admission criteria. Senior management is expected to demonstrate a clear understanding of the regulatory framework and to exercise effective oversight and control over business activities and staff.

As regulatory expectations rise, so too does the personal exposure of directors and officers. In this context, D&O insurance remains a critical component of a firm’s overall risk management framework, helping to protect personal assets in the event of claims or regulatory actions arising from alleged governance or oversight failures.

South Korea: gearing up for Digital Asset Basic Act

South Korea is pursuing a more expansive regulatory overhaul through the proposed Digital Asset Basic Act, introduced to the National Assembly in June 2025. The bill seeks to formalize the digital asset market by regulating issuance, trading practices and distributions, while introducing new governance structures around asset listing and delisting decisions.

These imminent changes would significantly increase compliance obligations for trading platforms and related service providers. In this environment, D&O insurance plays an important role in protecting directors and officers from the financial consequences of legal actions, investigations or claims arising from alleged regulatory breaches.

Navigating regulatory complexity with D&O insurance

Across Hong Kong, Singapore and South Korea, regulators are refining already sophisticated frameworks to address the evolving risks of digital assets. These developments reflect a broader global trend toward intensified regulatory scrutiny and heightened expectations of senior management accountability.

For firms operating in the region, this means proactively reviewing governance structures, custody arrangements and insurance programs to ensure leadership is appropriately protected against emerging liabilities. D&O insurance is no longer a secondary consideration — it is a core element of responsible risk management in an increasingly regulated digital asset landscape.

Informed Perspectives

Crypto scams are not just targeting the uninformed

By Haidy Grigsby, special agent, cybercrime and digital evidence unit, Tennessee Bureau of Investigation

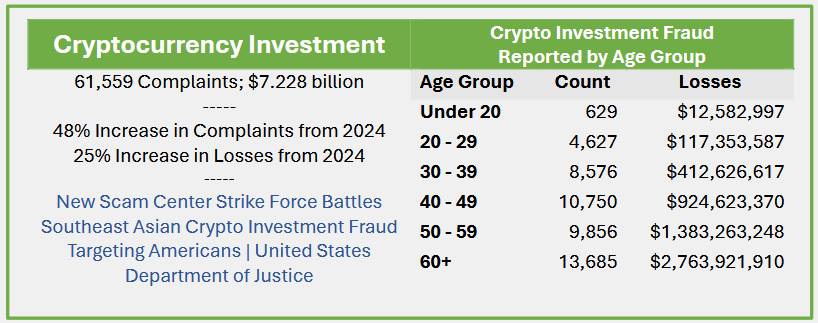

A common assumption is that crypto scams prey on the uninformed. While this is often true in financial fraud, crypto-related frauds are increasingly catching experienced investors, retired professionals and former market participants off guard with increasing frequency.

In my work at the FBI, I recently met with a retired trader who fit that profile exactly. He met a young woman online who claimed to know someone involved in crypto trading. He was told he had been selected as a consultant because of his experience. His case illustrates a strategy that we now see often.

Initial contact often begins with a wrong-number text, LinkedIn message or social media outreach. What starts as professional often turns personal or romantic, a tactic known as “pig butchering.” Scammers flatter expertise, create exclusivity and get the target to move the conversation to encrypted apps. In this case, “she” said WhatsApp was easier for her.

Exploiting familiarity with legitimate infrastructure, victims are instructed to open accounts on real exchanges, then use self-custody wallets to access external sites through built-in Web3 browsers. Because they click within a trusted app, they often don’t realize that they have left it.

These fraudulent markets mimic real ones with a twist: unlike real markets, these platforms allow one daily trade at a set time, ostensibly to capture optimal volatility. Victims choose long or short, allocate funds and confirm a brief trade lasting seconds or minutes. The scammer will often claim to contribute their own funds, reinforcing trust and the illusion of shared risk.

Balances grow and profits appear real. In truth, no trading occurs — the website is controlled by the operation, and the returns aresimply numbers entered by the scammer on their end.

To build credibility, victims are encouraged to withdraw a small amount after a “winning” trade. The withdrawal appears processed successfully, but is funded with cryptocurrency stolen from other victims and is meant to encourage larger future deposits. “I took profits. It had to be real,” the retired trader told me in frustration.

The websites change domains and branding frequently, with victims being told the company is merging, upgrading or rebranding. In reality these changes occur because of law enforcement takedowns, and victims are simply redirected to “new trading platforms.”

When victims attempt larger withdrawals, the narrative shifts: regulatory holds, tax prepayments, liquidity verification thresholds or tier upgrades. Each explanation is paired with urgent demands for more funds.

Convincing victims of the truth remains one of the greatest challenges. When I spoke with the retired trader, it was difficult to convince him I was law enforcement and that he had been dealing with a criminal organization, not one individual. No one wants to believe the person they built trust with and gave substantial sums of money to never existed. This retired trader was left to face his family, admit he had been defrauded and ask for help with basic living expenses. By the time he accepted reality, his retirement savings were already gone: assets had been transferred overseas, laundered and liquidated.

Source: FBI Internet Crime Complaint Center (IC3), 2025 Internet Crime Report, p. 53, https://www.ic3.gov/AnnualReport/Reports/2025_IC3Report.pdf

The FBI’s 2024 data show losses rising with age, likely reflecting the fact that older individuals have more accumulated wealth than those in their 20s.

Victims gather evidence: phone numbers, accounts, photos and websites — most of it turns out to be stolen, fake or AI-generated. Despite the difficulties in apprehending the perpetrators of these sophisticated schemes, law enforcement continues to pursue these cases. Anyone affected should cease all communication and report the incident to local law enforcement, IC3.gov and Chainabuse.com.

Headlines of the Week

– By Francisco Rodrigues

This week’s headlines show institutional adoption has kept on growing in the cryptocurrency space, yet old dangers remain. Protocol exploits, state-sponsored attacks, and technology disruption remain active threats.

Chart of the Week

Hyperliquid’s TradFi bet is now 40% of its own volume

Hyperliquid’s HIP-3 has scaled from ~$115 million in its first week (Oct 2025) to a peak of $17.8 billion/week, now consistently representing 35–40% of total protocol volume. Despite launching as a crypto-adjacent product, HIP-3 is overwhelmingly a TradFi venue, with Commodities alone driving ~60% of volume and pure crypto categories accounting for just ~12%. The aggregate (core + HIP 3) volume continues to decline since the early March 2026 peak with the HYPE price now following the same trend.

Listen. Read. Watch. Engage.

- Listen: Jennifer Sanasie is joined by Bloomberg Intelligence Senior Analyst James Seyffart to break down what Morgan Stanley’s bitcoin ETF could mean for institutional flows, fee competition, and the next phase of crypto adoption.

- Read: In Crypto for Advisors, Paul Frost-Smith, CEO of Komainu, covers how institutional crypto is converging with traditional finance, but speed can introduce risk if legal and compliance layers aren’t aligned. Then, in “Ask an Expert,” Sam Boboev from the “Fintech Wrap Up,” details the key coordination risks institutions must solve for.

- Watch: Jennifer Sanasie hosts Public Keys from the NYSE. Christopher Perkins discusses the recent acquisition by Franklin Templeton and the new “Franklin Crypto,” Superstate CEO Robert Leshner and Invesco’s Kathleen Wrynn break down their partnership, and NYSE Senior Market Strategist Michael Reinking, CFA unpacks the macro environment.

- Engage: Have you bought tickets to Consensus Miami yet? More speakers have been added to the agenda! Surrounding Consensus is an institutional summit, an advisor-focused “Wealth Management Day,” 100+ ancillary events and much, much more.

Looking for more? Receive the latest crypto news from coindesk.com and market updates from coindesk.com/institutions.

Note: The views expressed in this column are those of the author and do not necessarily reflect those of CoinDesk, Inc., CoinDesk Indices or its owners and affiliates.

Payment stablecoin issuers in the United States will be required to implement a regime targeting illicit finance under the proposed framework for the GENIUS Act.

In a Wednesday notice, the US Treasury Department said its Financial Crimes Enforcement Network and Office of Foreign Assets Control (OFAC) had issued a joint proposed rule to implement provisions of the GENIUS Act, signed into law in July 2025.

The proposal would direct payment stablecoin issuers to establish and maintain an anti-money laundering (AML) and countering the financing of terrorism (CFT) program, maintain a sanctions compliance program, and have the ability to “block, freeze and reject” certain stablecoin transactions. Issuers would be treated as financial institutions for purposes of the Bank Secrecy Act (BSA).

“Bringing stablecoin issuers into full BSA/OFAC compliance effectively turns them into bank-like gatekeepers,” Snir Levi, CEO of blockchain intelligence firm Nominis, told Cointelegraph. “That means significantly more wallet freezes, transaction blocking and asset seizures at scale,” he said.

Treasury’s notice was part of the implementation of the GENIUS Act, the stablecoin payments bill signed into law by US President Donald Trump last year. The legislation provides a framework for stablecoin issuers and is expected to be a boon for crypto markets. It will be effective 18 months after it was signed in July or 120 days after federal authorities issue related regulations.

Related: NYT revives Adam Back theory in latest bid to identify Bitcoin creator

On Tuesday, the US Federal Deposit Insurance Corporation (FDIC) issued its own proposed rule as part of the agency’s GENIUS Act implementation. The FDIC said stablecoin holders would not be insured under the bill, though reserve deposits for issuers would receive protection.

Stablecoin yield fight rages between US lawmakers and banking and crypto industries

While federal agencies work on implementation of the GENIUS Act, Congress has effectively been stalled on progress for a bill to establish a digital asset market framework, called the CLARITY Act when it passed the House of Representatives last year.

With the Senate Banking Committee yet to schedule a markup on the bill — a necessary step before a full floor vote in the chamber — crypto and banking representatives have been meeting with White House officials to discuss issues related to stablecoin yield, tokenized equities and ethics.

The White House’s Council of Economic Advisers said on Wednesday that a ban on stablecoin yield in the bill “would do very little to protect bank lending,” claiming that it would impose costs on users.

As of Wednesday, the banking committee had not rescheduled a markup on the CLARITY Act.

David Woodcock steps into the role as US senators await answers to questions on the agency’s dropping lawsuits against Justin Sun and several crypto companies.

The US Securities and Exchange Commission (SEC) has appointed David Woodcock as director of its division of enforcement as lawmakers press for answers on his predecessor’s departure.

In a Wednesday notice, the SEC said Woodcock would be taking over as the agency’s top enforcer starting on May 4. Sam Waldon will continue to serve as acting director of the division until then.

Woodcock, a partner at the law firm Gibson, Dunn and Crutcher, chairs that firm’s Securities Enforcement Practice Group. He previously worked as the director of the commission’s Fort Worth office from 2011 to 2015.

According to SEC Chair Paul Atkins, the appointment comes as the agency is “restoring Congressional intent by prioritizing cases that provide meaningful investor protection and strengthen market integrity.” Woodcock said that he planned to “execute the Chairman’s vision” in his role at the agency.

He replaces Margaret Ryan, who resigned in March. Her departure prompted several US lawmakers to question whether she left due to the SEC’s decision to drop several crypto-related enforcement cases.

Related: US Treasury moves forward with GENIUS Act, focusing on illicit finance

Two senators have called for Atkins to answer questions as to whether Ryan “faced resistance” from SEC leadership over enforcement cases tied to US President Donald Trump. These included a February 2025 decision — one month after the president took office — to drop a fraud case against Tron founder Justin Sun, tied to the Trump family-backed World Liberty Financial crypto platform.

“[The SEC] may have exercised preferential treatment for financial partners of President Trump against the advice and warnings of senior staff when the agency declined to litigate credible fraud cases,” wrote Senator Richard Blumenthal in a March 30 letter to Atkins.

“No investor benefit or protection” from past actions

On Tuesday, the SEC released a report on its enforcement results for the 2025 fiscal year. The agency reported seven enforcement cases of crypto companies that were registration-related and six related to the definition of a broker-dealer.

According to the SEC, it “identified no direct investor harm” and claimed that the cases “produced no investor benefit or protection,” calling them “a misinterpretation of the federal securities laws.” The narrative was the latest example of the SEC’s shift in enforcement of crypto-related cases following Trump’s inauguration.

TLDR

- The XFUNDS ETF, named Nicholas Bitcoin and Treasuries AfterDark ETF (NGHT), toggles between bitcoin and U.S. Treasuries throughout the day.

- The fund focuses on bitcoin’s overnight performance, capitalizing on the largest share of returns that occur after U.S. market hours.

- XFUNDS CEO David Nicholas emphasized that the strategy targets bitcoin’s global trading behavior, especially outside U.S. market hours.

- The NGHT ETF reduces exposure to bitcoin during the day and increases its position in U.S. Treasuries.

- The launch of the XFUNDS ETF coincides with heightened competition in the bitcoin ETF market, with Morgan Stanley debuting its own spot bitcoin ETF.

The newly launched XFUNDS ETF, named Nicholas Bitcoin and Treasuries AfterDark ETF (NGHT), offers investors a unique strategy. This fund toggles between bitcoin exposure and short-term U.S. Treasuries, adjusting throughout the day. It aims to capitalize on bitcoin’s performance during global market hours while minimizing exposure during U.S. trading hours.

XFUNDS ETF Shifts Between Bitcoin and Treasuries

The XFUNDS ETF targets Bitcoin’s movements outside of U.S. market hours. The fund’s strategy focuses on bitcoin’s overnight performance, which historically provides the most substantial returns. David Nicholas, CEO of XFUNDS, explained the fund’s approach, stating, “Bitcoin trades 24/7, and its behavior is increasingly driven by global activity outside U.S. market hours.”

To execute this strategy, the NGHT fund adjusts its holdings at the close of U.S. markets. It reduces exposure to Bitcoin and moves into U.S. Treasuries during the daytime. The ETF then shifts back to bitcoin after market hours, aiming to capture bitcoin’s “overnight alpha.” This strategy provides a targeted approach to trading the cryptocurrency market while minimizing risk during the day.

Rising Competition Among Bitcoin ETFs

The launch of the XFUNDS ETF comes at a time of increased competition in the bitcoin ETF market. On the same day, Morgan Stanley introduced its own spot bitcoin ETF, MSBT, with a 0.14% fee. This new product puts pressure on established players like BlackRock and Grayscale.

Financial experts believe that the MSBT could become a major player, with projections of $5 billion in assets under management within its first year. On the other hand, inflows into spot bitcoin ETFs are also gaining momentum. Recent data showed a surge of $471 million in net inflows, marking the largest single-day inflow in six weeks. This uptick signals growing investor interest in Bitcoin-focused ETFs.

Nasdaq filed a rule change on April 7 to expand its Exchange-Traded Product (ETP) definition to include Class ETF Shares, a hybrid product that blends mutual fund and ETF structures.

The amendment to Equity 1, Section 1(a)(15) would let issuers of these products use the exchange’s optional Initial ETP Open process on their first day of trading.

What the Rule Change Means for ETF Issuers

Class ETF Shares are exchange-traded shares issued by open-end funds that also offer traditional mutual fund share classes.

The SEC approved Nasdaq’s generic listing standards for these products in November 2025 under Rule 5703.

Separately, the SEC approved Nasdaq’s Initial ETP Open in May 2025. That process gives ETP issuers the option to delay a security’s opening from Pre-Market Hours at 4:00 a.m. ET until regular Market Hours at 9:30 a.m. ET.

The delay allows the Nasdaq Halt Cross to set an opening price, supporting more orderly price discovery.

Until now, only ETPs listed under existing Nasdaq rules could access that functionality. The new filing adds Rule 5703 to the list, extending the same option to Class ETF Shares.

A Growing Pipeline of Dual-Class Funds

The filing arrives as asset managers race to bring dual-class funds to market. The SEC has approved roughly 48 firms for multi-class ETF exemptive relief out of approximately 100 applications filed as of March 2026.

Major names including BlackRock, Fidelity, JPMorgan, and Morgan Stanley have all submitted applications.

However, operational infrastructure still lags behind regulatory progress. The DTCC’s automated solution for processing mutual fund-to-ETF share exchanges is not expected to go live until May 18, 2026.

Full custodian and market maker buildouts may not follow until late 2026 or 2027.

Nasdaq’s rule took immediate effect under Section 19(b)(3)(A)(iii) of the Securities Exchange Act.

The exchange has also asked the SEC to waive the standard 30-day operative delay, arguing the change is a non-controversial, definitional amendment that does not alter existing listing standards or the mechanics of the Initial ETP Open.

The SEC retains the authority to temporarily suspend the rule within 60 days if it determines the change raises investor protection concerns.

The post Nasdaq Wants to Give New ETFs a Smoother Launch Day appeared first on BeInCrypto.

Blockstream CEO Adam Back, downplayed the immediacy of quantum computing as a threat to the Bitcoin network, but emphasized the need for the industry to prepare.

A foundational figure in Bitcoin history for his cryptography work, dating back to the 1990s, Back laid out his central argument, saying that while quantum risk is real in theory, it is not yet practical, in an interview with Bloomberg on Tuesday.

Back noted that “the current hardware…generally doesn’t have any error correction.” That aligns with two recent papers highlighted in a thread on X, one a sober engineering analysis, the other a deadpan satire, which make that case from opposite directions. Together, they frame quantum computing as a long-term rather than near-term risk to cryptographic systems.

However, Back said the “lede” is not about dismissing the threat but about timing the response correctly. “We don’t have to agree about the timeline for quantum computers to become powerful enough to be a threat, because the prudent thing to do is to prepare Bitcoin and give people the option to migrate their keys to a quantum ready format, and to have, let’s say, a decade in which to do that.”

That timeline echoes reporting that post-quantum cryptography (PQC) is already moving from theory to implementation, particularly after NIST finalized standards in late 2024.

Back also stressed that preparation work is already active across the ecosystem, pointing to ongoing research and deployment. “There’s a 20-person research team that’s been working on this. Publishing papers and implementing things, putting them live.” He cited Blockstream’s Liquid network as an early proving ground.

The industry’s challenge is less about reacting to a breakthrough and more about coordinating a slow, orderly migration, before the risk becomes urgent.

UPDATE (April 8, 113:25 UTC): Adds link to Bloomberg interview.

Morgan Stanley’s spot bitcoin exchange-traded fund (ETF) began trading Wednesday with solid early activity, logging more than 1.6 million shares traded and roughly $34 million in inflows, the bank said.

The fund, listed under the ticker MSBT, tracks the CoinDesk Bitcoin Benchmark 4 PM New York Settlement Rate and charges a 0.14% expense ratio. It is the cheapest fund in the category, offering a clear, if narrow, pricing advantage to competitors.

MSBT entered the market with a different strength than others: distribution. Morgan Stanley’s wealth management arm oversees trillions of dollars in client assets and operates one of the largest financial advisor networks in the industry. That reach could help the fund gain traction as more investors access bitcoin through advisors rather than direct trading platforms.

Some experts anticipate the fund to draw capital from existing products, especially BlackRock’s iShares Bitcoin Trust (IBIT), the largest spot bitcoin ETF currently on the market. MSBT has a lot of catching up to do. IBIT, which launched among nine other ETFs in January 2024, has amassed over $53 billion in assets, quickly becoming the asset manager’s most successful ETF.

Wednesday’s trading offers an early signal of demand, though it remains to be seen whether MSBT can sustain momentum in a market dominated by a handful of large players.

UPDATE (April 8, 2026, 20:00 UTC): Adds additional detail.

Crypto World

Panda Bonds Surge as Global Borrowers Ditch Dollar Debt for Cheaper Yuan Financing in 2026

TLDR:

-

- Foreign panda bond issuance tripled year on year in March 2026, reaching 27.8 billion yuan in one month alone.

- China’s 10-year bond yield of 1.82% makes yuan borrowing roughly 60% cheaper than equivalent U.S. dollar debt.

- The U.S. dollar’s share of global reserves dropped to 56.32% in 2025, its lowest recorded level since 1995.

- Iran now requires oil tanker transit fees through the Strait of Hormuz to be paid in yuan or Bitcoin only.

- Foreign panda bond issuance tripled year on year in March 2026, reaching 27.8 billion yuan in one month alone.

Panda bonds recorded a dramatic rise in foreign issuance in March 2026, tripling year on year to 27.8 billion yuan. That equals roughly $4 billion in a single month.

Total yuan-denominated financing by foreign borrowers reached a record 218 billion yuan in the opening weeks of 2026.

The full year of 2025 produced only $167 billion through yuan notes and loans combined. The shift spans sovereign governments, global banks, and multilateral development institutions.

Record Deals Signal a Structural Turn in Yuan Borrowing

Deutsche Bank issued the largest single panda bond ever placed by a foreign bank, totaling 5.5 billion yuan. The three-year tranche was oversubscribed 1.55 times and the five-year 1.63 times.

Indonesia sold 9.25 billion yuan at roughly one percentage point below its euro-denominated debt issued the same week.

The Asian Infrastructure Investment Bank placed 3 billion yuan, with 58% allocated to overseas investors. Morgan Stanley, Barclays, and Hungary also joined as new or repeat yuan issuers in 2026. The Asian Development Bank had already raised a record 8.3 billion yuan in March 2025.

The cost advantage is a key factor. China’s 10-year bond yield sits at 1.82%, against 4.46% for the U.S. Treasury equivalent. That spread of 260 basis points is the widest recorded since August 2025.

As @BullTheoryio noted on X, “Borrowing in yuan is approximately 60% cheaper than borrowing in dollars right now.” For governments with heavy trade exposure to China, that arithmetic is difficult to overlook. The yuan now accounts for 34.5% of China’s cross-border goods trade settlements, up from 10% in 2017.

China is the dominant trading partner for more than 120 countries. When trade with the largest partner settles in yuan, holding that currency as a working reserve follows naturally. The offshore dim sum bond market hit a record 870 billion yuan in 2025, its eighth straight year of growth.

Dollar Weakness and Treasury Market Signals Add Further Pressure

The U.S. dollar index fell 9.6% in full year 2025, its worst annual result since 2017. In the first half of 2025 alone, it dropped 10.7%, the worst first-half performance in over 50 years. The dollar’s share of global reserves fell to 56.32%, the lowest since 1995.

China’s U.S. Treasury holdings fell to $682.6 billion in November 2025, down from $1.32 trillion in 2013. China has been selling U.S. Treasuries for nine consecutive months as of late 2025. That steady reduction reflects a deliberate portfolio rebalancing by the world’s second-largest economy.

Research from the National Bureau of Economic Research shows that Treasuries’ convenience yield turned negative, sitting at -0.25% for 10-year maturities.

That premium once saved the U.S. government hundreds of billions in annual borrowing costs. State Street confirmed that since April 2025, rising Treasury yields now reflect fiscal risk rather than economic strength.

During a global bond sell-off in March 2026, U.S. Treasury yields spiked to 4.4055%, a near eight-month high. China’s 10-year yield moved only from 1.80% to 1.84% across the same period. The contrast in stability was widely noted across international fixed income markets.

Iran now charges oil tankers transiting the Strait of Hormuz $1 per barrel of cargo. Payments are accepted only in Bitcoin or Chinese yuan.

A very large crude carrier with 2 million barrels owes up to $2 million per transit. Iran’s National Security Committee passed legislation codifying this fee structure, and at least two vessels paid in yuan before the ceasefire was announced.

TLDR

- Ripple has launched a Treasury Management System with native digital asset capabilities, allowing businesses to manage both fiat and digital assets.

- The new system integrates Digital Asset Accounts and Unified Treasury, making it the first TMS to directly support on-chain digital asset management.

- CFOs and treasury teams can now manage traditional cash balances alongside digital assets like XRP and RLUSD in a single system.

- Ripple’s Treasury platform addresses the growing demand for seamless digital asset solutions among fintech platforms and financial leaders.

- The new solution provides regulated Ripple-native accounts, simplifying asset management and ensuring compliance with industry standards.

Ripple, the San Francisco-based blockchain firm, has announced the launch of its Treasury Management System (TMS) with native digital asset capabilities. This new development is designed to support businesses in managing both fiat and digital assets efficiently. Ripple’s new offering aims to enhance enterprise blockchain solutions, simplifying the process of integrating digital assets into corporate treasuries.

Ripple’s Treasury Management System to Revolutionize Corporate Finance

Ripple’s new Treasury Management System is set to change how CFOs and treasury teams manage digital assets. The platform integrates on-chain digital asset capabilities, allowing businesses to handle both traditional fiat currencies and digital assets in a single system. Ripple’s solution eliminates the need for separate custody platforms and reconciliation processes, streamlining treasury operations.

The addition of Digital Asset Accounts and Unified Treasury within Ripple Treasury makes it the first TMS to directly integrate digital asset management. CFOs can now manage their assets more seamlessly, avoiding the complexities of using separate systems for digital currencies like XRP and RLUSD. This innovative move allows companies to focus on financial strategy rather than on the technicalities of asset management.

According to Ripple, this system addresses the growing demand from fintech platforms and financial leaders who are seeking smoother gateways for digital asset integration. Reece Merrick, Ripple’s top executive, highlighted that 72% of finance leaders believe offering a digital asset solution is critical to staying competitive in the market. As companies face uncertainty about implementing these solutions, Ripple aims to fill this gap with its new product.

Digital Asset Accounts Offer New Opportunities for Businesses

Ripple’s new Treasury platform provides businesses with the ability to create Ripple-native Digital Asset Accounts. These accounts allow companies to hold and manage digital assets like XRP and RLUSD in a regulated environment. By integrating digital assets into the corporate treasury, Ripple simplifies how businesses manage their cash and crypto balances in one unified system.

The introduction of these accounts comes at a time when companies are seeking to diversify their asset portfolios. The platform’s seamless integration of digital assets alongside traditional fiat currencies offers a more straightforward way for businesses to engage with the growing digital economy. Ripple’s new system ensures that businesses are equipped to stay ahead in a rapidly changing financial landscape.

Bitcoin extended its recovery after a 7% surge above $72,000 this week, reclaiming key technical levels and setting up a potential move toward the $90,000 zone as macro sentiment improves. Traders pointed to a constructive setup, with the cryptocurrency nudging past a symmetrical triangle pattern and stabilizing above critical supports, including the $68,000 area where major moving averages converge. Analysts highlighted that maintaining momentum above $70,000 would be essential to unlock the next leg higher, targeting roughly 25% gains to the $90,000 mark if the breakout holds.

Meanwhile, on-chain and derivatives activity signaled shifting market dynamics as traders expressed renewed buying conviction. A notable spike in taker buy volume on Binance, the largest crypto exchange by volume, followed a favorable macro development, further reinforcing a bullish tilt among market participants.

Key takeaways

-

Bitcoin forms a bullish setup after reclaiming the $72,000 region, with a symmetrical-triangle breakout implying a target near $90,000.

-

Binance taker buy volume surged by about $2.7 billion within two hours after the US-Iran ceasefire announcement, illustrating aggressive buying by futures traders.

-

Binance net taker volume rose to about $1.02 billion—the highest since March 17—suggesting a broad return of aggressive buying activity on the platform.

-

The Coinbase premium index turned positive, signaling renewed demand from U.S. participants after a prolonged period of negative readings.

-

RSI has climbed to roughly 56, moving away from oversold conditions and adding to the case for continued upside pressure, provided Bitcoin can hold above key supports.

Technical setup reinforces bullish outlook

Bitcoin’s latest move sits atop a chart pattern that traders watch for directional cues. After breaking above the upper boundary of a symmetric triangle last week, the price began to stabilize above the $70,000 level, a threshold that previously served as a ceiling during the recent pullback. A daily close above this pivot would formally confirm the breakout, analysts say, with the next major resistance around the $76,000 area before buyers contend with the $80,000 zone. From there, a measured move could place Bitcoin on a path toward the $90,000 target, representing roughly a 25% advance from current levels.

A broader look at momentum shows the daily RSI firming to the mid-50s, up from oversold conditions in February. That shift in momentum, combined with the price trading above significant averages, lends a degree of confidence to bulls that the recovery could extend beyond the short term, provided demand remains steady and macro risk appetite improves.

“Bitcoin breaks through the crucial $71K level and builds a bullish structure,” noted Michael van de Poppe, founder of MN Capital, in a recent post. He emphasized that sustaining a hold above the breakout level would be critical for extending the rally toward higher highs and higher lows, a pattern that could reinforce upward momentum.

Analysts caution that the road to $90,000 includes intermediate hurdles, with the 76,000 and 80,000 ranges acting as tests before buyers are able to press toward the higher target. Still, the immediate setup—reclaiming key support, improving RSI, and a confirmed breakout—adds a pragmatic layer of confidence for buyers who have been cautious since the last correction.

Liquidity signals point to renewed buying appetite

Beyond the technicals, a surge in derivatives activity on Binance captured attention as a gauge of sentiment shifts. CryptoQuant researchers reported that taker buy volume—representing aggressive market-buy orders on Binance futures—jumped by about $2.7 billion within two hours following the US-Iran ceasefire announcement. The breakdown showed roughly $1.2 billion and $1.5 billion appearing in sequence, underscoring how macro headlines can quickly reallocate risk appetite toward Bitcoin.

“This sudden improvement in visibility allows investors to reposition in the short term, and sends a constructive signal for Bitcoin,” CryptoQuant analyst DarkFost commented on the rapid liquidity inflows.

The same data set indicated that Binance’s cumulative net taker volume climbed to about $1.02 billion—the strongest reading since March 17—highlighting a broader return of aggressive buying pressure from traders on the platform. Amr Taha of CryptoQuant noted that the flow suggested traders were buying with a view to improving macro sentiment, not merely reacting to a crypto-specific headline.

On-chain demand returns to the fore

In addition to derivatives activity, on-chain indicators echoed a renewed interest from U.S. participants. The Coinbase premium index, a barometer of demand relative to spot prices on Coinbase, flipped back into positive territory after a stretch of negative readings. The shift implies stronger willingness among U.S.-based buyers to acquire BTC at prevailing prices, aligning with the broader bid tone seen on exchanges and in market commentary.

Observers frame this combination of technical breakout, liquidity influx, and positive premium signals as a sign that Bitcoin may be reestablishing a foothold above key levels after weeks of consolidation. If macro catalysts continue to tilt favorably and risk appetite remains buoyant, the path toward higher targets could become more plausible for the remainder of the quarter.

What to watch next

Looking ahead, traders will be watching whether Bitcoin can defend the $70,000 to $72,000 zone on any pullbacks, paving the way for the next test of $76,000 and the critical hurdle at $80,000. A sustained close above $80,000 would add conviction to a longer-term upside narrative toward $90,000 and beyond, while a failure to hold could invite a retracement to lower support levels.

Beyond price action, the story remains sensitive to macro developments, including geopolitical headlines and broader risk sentiment. As traders recalibrate positions in response to evolving news, the question remains whether the recent surge in taker buying on Binance is a durable indicator of institutional-style participation or a temporary reaction to headlines.

Readers should monitor how the market responds to incoming data and policy signals in the days ahead, particularly any developments that influence U.S. risk appetite and the pace of global liquidity movement. The next few sessions could reveal whether Bitcoin sustains its momentum or enters a new phase of consolidation as traders reassess risk exposure.

The stablecoin news out of Washington this week goes beyond reserves and redemptions — FinCEN, the Treasury’s financial crimes unit, has proposed rules that would fundamentally reform how stablecoin issuers and all US financial institutions handle anti-money laundering compliance, shifting from box-checking paperwork toward risk-based self-policing of illicit transactions.

Summary

- FinCEN published a proposed rule on April 7 that would “fundamentally reform” BSA compliance programs for all financial institutions — including stablecoin issuers, who are classified as financial institutions under the GENIUS Act — requiring them to build risk-based AML frameworks focused on actual illicit finance threats rather than prescriptive documentation

- Treasury Secretary Scott Bessent framed the proposal explicitly as a reduction in compliance burden: the goal is to redirect resources away from lower-risk activities toward higher-risk ones, with enforcement actions reserved only for “significant or systemic failures”

- Under the new framework, stablecoin issuers must build programs around four core pillars: internal policies and controls including risk assessments, a designated BSA compliance officer located in the US, employee training tailored to the firm’s risk profile, and independent testing of the program’s effectiveness

The stablecoin news most relevant to compliance teams this week is not from the FDIC or OCC. It comes from FinCEN. The Financial Crimes Enforcement Network proposed rules on April 7 that would reshape how all US financial institutions — including stablecoin issuers — manage their anti-money laundering programs. The core shift: from measuring compliance by the volume of filings and paperwork to measuring it by demonstrated effectiveness at identifying and stopping illicit finance.

Treasury Secretary Scott Bessent described the intent directly: “Our proposal restores common sense with a focus on keeping bad actors out of the financial system, not burying America’s banks in more red tape.” FDIC Chair Travis Hill, whose agency is a co-proposing regulator, called it “perhaps the most important of the reforms Congress envisioned in the AML Act.”

The GENIUS Act, signed into law in July 2025, classified all permitted payment stablecoin issuers as “financial institutions” under the Bank Secrecy Act. That classification means the FinCEN proposal applies to them with the same force it applies to banks. Stablecoin firms that previously operated under lighter compliance regimes — relying on state money transmitter licenses and minimal internal monitoring — must now build programs that meet bank-level AML standards.

This is not a future requirement. The GENIUS Act’s implementing regulations must be finalized by July 18, 2026. Any stablecoin issuer operating after that date without a compliant program faces potential enforcement actions covering civil penalties, criminal prosecution, and license revocation.

The Four Pillars FinCEN Now Requires

Under the proposed framework, every covered financial institution — including stablecoin issuers — must build their AML program around four core components. First: internal policies, procedures, and controls, including a documented risk assessment process that identifies the specific illicit finance threats the issuer faces based on its customers, products, and geography. Second: a BSA compliance officer physically located in the United States with supervisory authority over the program. Third: ongoing employee training tailored to the institution’s actual risk profile. Fourth: independent testing by an outside party that evaluates whether the program has been effectively implemented — with explicit language prohibiting auditors from substituting their own judgment for the institution’s risk-based determinations.

The proposal also limits when enforcement is appropriate. FinCEN stated it would generally not initiate significant supervisory action unless an institution had “a significant or systemic failure” to maintain its program — a standard intended to protect well-run programs from technical violations that pose no real illicit finance risk.

As crypto.news reported, the FDIC simultaneously proposed its own 191-page stablecoin rule covering reserves and redemption standards. As crypto.news noted, the GENIUS Act’s enforcement framework spans the Treasury, Federal Reserve, OCC, and FDIC — with FinCEN and OFAC playing central roles in sanctions and AML oversight. The FinCEN proposal fills the compliance design gap the statute left open.

Comments on the proposed rule are due 60 days after Federal Register publication, before the July 18 regulatory deadline.

Xiaomi: Smartphone Cost Pressures Persist, But Robotics And Agentic AI Could Drive Long-Term Upside

US Treasury Moves Forward with GENIUS Act, Focusing on Illicit Finance

10 Nearly Perfect Fantasy Movies, Ranked

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Alan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

How to Use a BA II Plus Calculator For Financial Mathematics | Exam FM | JK Math

MAJOR XRP LEAK AT LIVE EVENT! ($33 TRILLION XRP 2026 PLAN!!!)

![Efektif gak sih? [Adira Finance berizin dan diawasi oleh Otoritas Jasa Keuangan] #CobaMoservice](https://wordupnews.com/wp-content/uploads/2026/04/1775683573_maxresdefault-80x80.jpg)

Efektif gak sih? [Adira Finance berizin dan diawasi oleh Otoritas Jasa Keuangan] #CobaMoservice

-

NewsBeat6 days ago

NewsBeat6 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business6 days ago

Business6 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Spanx – Corporette.com

-

Business5 days ago

Business5 days agoExpert Picks for Every Need

-

Business3 days ago

Business3 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports4 days ago

Sports4 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business7 days ago

Business7 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech1 day ago

Tech1 day agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business3 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Tech6 days ago

Tech6 days agoCommonwealth Fusion Systems leans on magnets for near-term revenue

-

Fashion2 days ago

Fashion2 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Fashion1 day ago

Fashion1 day agoLet’s Discuss: DEI in 2026

-

Politics5 days ago

Wings Over Scotland | The quality of mercy

-

Business4 days ago

Business4 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Tech7 days ago

Tech7 days agoFollowing Artemis II’s Journey Around The Moon

-

Fashion6 days ago

Fashion6 days agoStatement Sunglasses: The Accessory Shaping Modern Fashion

-

Business7 days ago

Business7 days agoInvestor reactions to Trump’s speech on Iran war

-

Tech7 days ago

Tech7 days agoDaily Deal: The Modern No-Code Development Bundle

-

Politics7 days ago

Politics7 days agoTrans kids protest the Department of Education

-

Sports6 days ago

Justin Jefferson’s Situation Remains Unchanged after JSN’s Deal

You must be logged in to post a comment Login