Crypto World

The case for bringing Wall Street’s darkest corners to crypto

The largest traders have a problem: how to keep their activity quiet enough to not influence market prices or reveal any long-term strategies.

In traditional markets like equities, they’ve had that ability for decades through so-called dark pools and off-exchange venues. Even as far back as January 2025, more than half of all U.S. equities trading took place off public exchanges, according to Bloomberg data.

Crypto has never had an equivalent, and the absence is increasingly difficult to ignore. Every trade on Hyperliquid, every order on a decentralized exchange, is visible to anyone paying attention, and companies like DeFiLlama and Arkham exist to collect and present that data in a digestible way.

The crypto market, which prides itself on disrupting traditional finance, has replicated one of TradFi’s most persistent structural problems: If you’re big enough to move markets, everyone can see you coming. As a result, firms providing liquidity on public decentralized exchanges say their strategies get reverse-engineered quickly

“On Hyperliquid, one of the top market makers told us they have to rotate their trading strategies every three weeks because they get copied,” Denis Dariotis, co-founder of GoQuant, a crypto trading infrastructure firm backed by GSR, said in an interview. “That’s the alpha problem.”

There are other consequences, too. Market makers — the firms providing the liquidity that keeps crypto markets functioning — operate in full public view, and the industry has developed a habit of making them the villain whenever something goes wrong. Recent scrutiny of Jane Street‘s involvement in the Terra/Luna collapse is only the latest example. A large firm’s onchain activity gets traced, a narrative forms and the company spends weeks managing a PR crisis over trades that, on a traditional venue, would have been entirely unremarkable.

GoQuant’s answer is GoDark, a decentralized exchange (DEX) set to start up on Solana in May. That platform uses zero-knowledge proofs to conceal trade details not just from other market participants, but also from the node operators running the order book. The ambition is radical: a matching engine where nobody in the system can see what they’re matching.

The immediate question is whether that’s technically achievable at any useful speed. Zero-knowledge proofs are computationally expensive, and the architecture adds latency that privacy-agnostic systems don’t have to absorb. Internal testing puts order matching at 25 to 50 milliseconds — Dariotis frames this as fast relative to most decentralized exchanges, where execution often runs into the hundreds of milliseconds, and he’s right. But it’s also an order of magnitude slower than what’s available to firms co-located with a centralized exchange. For retail traders that gap probably doesn’t matter. For the market makers GoDark is banking on to provide liquidity, it might.

Which brings up the harder problem. A private exchange with no volume is just a dark room. GoDark’s plan to seed liquidity mirrors what Hyperliquid did with its HLP vault — users deposit funds, the funds get deployed as market-making liquidity, participants take a cut of fees and first access to liquidations.

It worked for Hyperliquid. But it has not worked for most of the DEXes that have tried to replicate the model since, which have generally seen volume collapse once the incentive period ends.

Then there is the regulatory question, which the team has so far avoided having to answer directly. Traditional dark pools are private in the narrow sense that they conceal pre-trade order information, but they operate under post-trade reporting requirements and regulatory oversight.

GoDark’s privacy is more absolute by design, it’s structurally incapable of producing a full audit trail. The inclusion of automated OFAC screening is a gesture toward compliance, but it is unlikely to satisfy regulators who have spent the past three years pushing crypto toward more transparency, not less. How that tension resolves — and whether it limits institutional participation to jurisdictions with lighter oversight — remains to be seen.

GoDark is separate from GoQuant’s existing institutional product of the same name, a spot DEX built with Copper and GSR that enters production next month and targets a different, narrower client base. The May launch is the retail-facing version.

Key Highlights

- On April 10, 2026, Principal Financial Officer Snizhana P. Quan exercised options and sold 20,000 shares of Lightwave Logic, netting approximately $207,000 at $10.36 per share.

- The transaction reduced her direct stake by 26.3%, though she maintains ownership of 51,125 shares plus 55,000 unexercised options.

- Shares of LWLG have skyrocketed 939% in the trailing twelve months, propelling market capitalization to $1.58 billion.

- Annual revenue from licensing reached only $106,855 in 2025, while the company recorded a net loss exceeding $20.3 million.

- Recent strategic milestones include a collaboration agreement with Tower Semiconductor and integration into the GDSFactory design platform.

Over the past year, Lightwave Logic (LWLG) has emerged as one of the market’s most explosive performers, with shares rocketing upward by 939%. Against this backdrop, a key financial executive has monetized a portion of her equity stake.

Snizhana P. Quan, serving as the company’s Principal Financial Officer, completed a same-day exercise-and-sale transaction on April 10, 2026, involving 20,000 employee stock options. The shares were sold at a weighted average of $10.36 each, producing proceeds of approximately $207,000.

LWLG shares settled at $10.60 when the market closed that day.

This form of transaction—exercising options and immediately selling the underlying stock—is common among corporate officers. It generally serves liquidity needs or addresses tax obligations associated with equity compensation, rather than signaling pessimism about future prospects.

Quan transitioned from her previous position as corporate controller to the PFO role in January 2026. After completing this sale, she continues to own 51,125 shares outright, along with 4,800 shares held indirectly via a domestic partner.

Additionally, she holds 55,000 vested stock options that remain unexercised, preserving substantial economic exposure to the company’s performance.

SEC disclosures reveal that Director Craig Ciesla executed similar option exercises and share sales during the same period. Both insiders acted following a secondary offering and the stock’s extraordinary price appreciation.

The Financial Reality Behind the Valuation

While the stock price has soared, Lightwave Logic’s actual revenue generation remains extremely limited. For the full year 2025, the company recognized merely $106,855 from licensing and royalty streams. Net losses for the period totaled $20.3 million.

A year ago, the company’s market capitalization hovered below $150 million. Today, it commands a valuation of $1.58 billion.

The disparity between market value and revenue generation is substantial. The firm ended 2025 holding $69 million in cash reserves, providing a multi-year financial cushion based on current operating expenditures. However, meaningful product-based income has yet to materialize.

Strategic Foundry Collaborations Provide Development Momentum

From a technology standpoint, Lightwave Logic has executed two significant initiatives drawing investor attention. The company successfully embedded its electro-optic polymer solution into the GDSFactory process design kit and established a formal development partnership with Tower Semiconductor (TSEM).

These advances carry weight because they streamline the path for prospective clients to incorporate LWLG’s polymer technology within established foundry manufacturing flows.

The firm is positioning itself to serve data center and artificial intelligence interconnect applications, where appetite for enhanced optical component performance continues expanding. Embedding its materials within standard foundry processes represents a critical milestone toward achieving commercial-scale adoption.

Valuation estimates from the Simply Wall St community span a remarkably broad range—from approximately $0.02 to $14.50 per share—underscoring the polarized views among market participants.

At market close on April 10, 2026, LWLG was changing hands at $10.60 per share.

A hacker exploited the Polkadot-based cross-chain interoperability protocol Hyperbridge, netting about $237,000 and raising renewed security concerns about blockchain bridge infrastructure.

An attacker minted 1 billion bridged Polkadot (DOT) tokens in a single transaction on Hyperbridge, according to blockchain data shared by cybersecurity platform CertiK. The exploit only affected DOT on Ethereum that was bridged through Hyperbridge, while native DOT tokens and the wider Polkadot ecosystem remain unaffected, Polkadot noted in a Monday X post.

CertiK said the hacker managed to mint the tokens after he “slipped through a forged message to change the admin of Polkadot token contract on Ethereum.” Limited liquidity in the bridged DOT pool capped the proceeds at 108.2 Ether (ETH), worth around $237,000.

Hyperbridge pauses operations after exploit

Hyperbridge paused operations after the attack while the team worked on an upgrade, with contributor Web3 Philosopher saying the initial diagnosis pointed to a malicious proof that fooled the protocol’s Merkle tree verifier.

The exploit is notable because Hyperbridge has marketed itself as a proof-based interoperability layer built to deliver “full node security” for crosschain bridges. The incident also follows Aethir’s disclosure last week that it had contained a separate bridge exploit and kept user losses below $90,000.

Cybersecurity research company Blocksec Falcon said the likely root cause of the exploit was a Merkle Mountain Range (MMR) proof replay vulnerability caused by missing proof-to-request binding, though the final root cause has not yet been confirmed by the protocol.

The native DOT token briefly dipped to a daily low of $1.16 on Monday, before recovering to trade above $1.19 at the time of writing, according to CoinGecko.

Hackers exploit SubQuery network for $130,000

Security incidents continue to hit crypto protocols despite a sharp year-over-year drop in DeFi exploit losses.

Related: New AI cybercrime tool targets crypto, bank KYC systems via deepfakes

On Sunday, the data indexing protocol SubQuery Network was also exploited for around $130,000 due to missing access control data that exposed the code written over two years ago.

The vulnerability enabled the attacker to set his own contract as the withdrawal target for staking rewards, blockchain security auditor Pashov said in a Sunday X post.

Hackers stole over $168 million from 34 decentralized finance (DeFi) protocols in the first quarter of 2026, marking a significant decline from the $1.58 billion stolen in the first quarter of 2025, when the record $1.4 billion Bybit hack occurred.

Cointelegraph has contacted Hyperbridge for comment on the root cause of the exploit.

Magazine: Meet the onchain crypto detectives fighting crime better than the cops

Blockchain sleuth ZachXBT said Garrett Dutton’s 5.9 Bitcoin has already been sent to deposit addresses associated with KuCoin.

Garrett Dutton, an American musician better known as “G. Love,” said he lost $420,000 worth of Bitcoin after installing a malicious app impersonating the self-custody crypto app Ledger Live from Apple’s App Store and entering his seed phrase.

“I had a really tough day,” Dutton told his 67,500 followers in a post on X on Saturday, adding that he lost his 5.9 Bitcoin (BTC) stash “in an instant” after spending about 10 years accumulating the coins to secure his retirement.

In a follow-up post, crypto sleuth ZachXBT said that Dutton’s Bitcoin has been sent to deposit addresses linked to the crypto exchange KuCoin across nine transactions. KuCoin replied to the post with a statement typically addressed to customers.

The incident highlights a continued problem that bad actors have posed in the crypto industry. On Tuesday, the US Federal Bureau of Investigation reported that Americans lost over $11 billion from crypto-related incidents in 2025, up from the $9 billion recorded the previous year.

Related: Hong Kong retiree loses $840K in triple ‘crypto expert’ scam

Dutton said he was tricked into sharing his seed phrase after downloading the malicious software on his new Apple MacBook Neo but didn’t share which link he used.

“I been in the crypto circus since 2017. Today they caught me off guard. It was my own damn fault for not being more diligent. But let it serve as a warning. There’s so many scams,” he added.

Cointelegraph was unable to find the fake Ledger app on Apple’s App Store at the time of writing. Cointelegraph reached out to Apple for comment but did not receive an immediate response.

Fake Ledger apps have appeared on Microsoft’s store

Scammers have been adopting this fake Ledger app strategy since at least 2023.

That year, almost $600,000 worth of Bitcoin was stolen from several users who downloaded a fake Ledger Live application from Microsoft’s app store.

Microsoft admitted that the malicious app had bypassed its review process and took it down shortly after.

Magazine: Asia Express: Phantom Bitcoin checks, China tracks tax on blockchain

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Quantum AI trading bots gain traction in 2026 as investors seek advanced automation for passive income.

Summary

- Quantum AI trading bots gain traction in 2026, offering faster, data-driven automated trading

- BitsStrategy combines quantum computing and AI to enhance trade accuracy across crypto and stocks

- Investors adopt quantum AI tools for hands-free trading and optimized passive income strategies

In 2026, quantum AI trading bots are emerging as a game-changer for anyone looking to earn passive income from trading. These bots leverage the power of quantum computing and artificial intelligence to execute trades more efficiently and accurately than ever before.

They can analyze massive datasets, recognize complex patterns, and make trading decisions in real time, all while operating 24/7. Whether someone is a beginner or an experienced trader, quantum AI bots can help them automate their trading strategies and optimize their profits.

In this article, we will explore the 6 best quantum AI trading bots for 2026 that can help anyone start earning passive income with minimal effort.

1. BitsStrategy: Leading quantum AI bot for automated trading

Overview:

BitsStrategy is one of the top-rated quantum AI trading platforms for 2026. It combines quantum computing with artificial intelligence to enhance the decision-making process and deliver better results. BitsStrategy analyzes market data in real-time, enabling traders to take advantage of opportunities quickly, ensuring higher accuracy in their trades.

Why Choose BitsStrategy?

- Advanced Quantum AI for faster data processing and improved trade execution.

- Fully automated trading with minimal setup.

- Compatible with both cryptocurrency and stock markets.

- Offers customizable risk management features to optimize profits.

Best For:

- Traders looking for an easy-to-use, hands-off trading experience.

- Those interested in both crypto and stock market trading.

Click to register and receive a free $10 real reward!

2. CryptoHopper: Quantum AI for smarter trading decisions

Overview:

CryptoHopper is an AI-powered trading bot that integrates quantum computing for enhanced precision. This platform provides traders with real-time market analysis and quick decision-making, optimizing trading strategies for both novice and expert users. CryptoHopper is especially favored by crypto traders due to its easy-to-use interface and powerful AI.

Why Choose CryptoHopper?

- Quantum AI-enhanced predictions for more informed trade decisions.

- Customizable trading strategies based on individual goals.

- Integrates with popular exchanges like Binance and Kraken.

- Provides a free trial to test the platform’s features.

Best For:

- Crypto traders looking for a precise and customizable trading experience.

- Beginners who want to explore automated trading with minimal setup.

3. 3Commas: Quantum AI with risk management tools

Overview:

3Commas is a popular trading platform that integrates quantum AI to improve trading accuracy and reduce risks. It offers powerful automation tools, including smart trading terminals, portfolio management, and customizable risk management features. 3Commas allows users to backtest trading strategies, ensuring they are optimized for real market conditions.

Why Choose 3Commas?

- Quantum AI-driven strategies for faster and smarter trading decisions.

- Customizable risk management tools to minimize losses.

- Multi-exchange support, enabling traders to trade across different platforms.

- Offers a free plan with access to basic features.

Best For:

- Traders who want both automation and control over their strategies.

- Those seeking risk management features for better protection of their capital.

4. Pionex: Free quantum AI bots for arbitrage and grid trading

Overview:

Pionex is an all-in-one trading platform that offers 16 free bots, including grid trading and arbitrage strategies, powered by quantum AI. These bots analyze market trends and execute trades efficiently, allowing traders to benefit from various trading opportunities without constantly monitoring the market.

Why Choose Pionex?

- 16 free bots with quantum AI for automated arbitrage and grid trading.

- High liquidity and quick trade execution.

- Built-in risk management features to protect investments.

- Easy-to-use interface, ideal for beginners.

Best For:

- Beginner traders looking for simple and automated trading bots.

- Those interested in leveraging grid trading and arbitrage strategies.

5. Coinrule: AI-based quantum trading for custom strategies

Overview:

Coinrule is a no-code trading bot that allows users to create their own trading rules using quantum AI technology. Whether someone is new to trading or a professional, Coinrule offers a customizable platform that lets them set up automated strategies based on their personal trading goals.

Why Choose Coinrule?

- Quantum AI-powered rule-based trading with no coding required.

- Integrates with major exchanges like Binance and Coinbase.

- Free tier with basic features to help beginners get started.

- Ability to backtest custom strategies for optimal performance.

Best For:

- Beginners who want to create personalized trading strategies without coding.

- Intermediate traders who want to customize their automated trading experience.

6. Trality: Algorithmic trading with quantum AI power

Overview:

Trality is an algorithmic trading platform that uses quantum AI to help traders design, backtest, and deploy their strategies. Trality stands out due to its emphasis on both ease of use and advanced functionality, making it suitable for both newcomers and experienced traders.

Why Choose Trality?

- Quantum AI-powered trading algorithms for smarter market decisions.

- Ability to backtest strategies before going live, reducing risk.

- Python-based programming for experienced traders to create custom algorithms.

- Free plan with basic tools for new users.

Best For:

- Advanced traders who want to create custom algorithms with Python.

- Those who value strategy backtesting and data-driven decisions.

How Quantum AI trading bots can help anyone earn passive income

Using quantum AI trading bots to generate passive income is becoming increasingly popular in 2026. These bots work 24/7, automatically executing trades, optimizing strategies, and reducing the need for constant monitoring. Quantum AI trading bots analyze market data at incredible speeds, helping traders make faster and more accurate decisions.

For those looking to earn passive income, these bots offer a hands-off trading experience. By setting the bot up with a desired strategy and risk tolerance, anyone can let it run while the AI takes care of the rest. However, it’s important to note that while these bots can optimize trades, the inherent risks of the financial markets still apply. Using proper risk management tools, such as stop-loss orders, is essential for minimizing potential losses.

Conclusion: Start earning passive income with quantum AI trading bots

The future of trading is here, and quantum AI trading bots are at the forefront of this revolution. By leveraging quantum computing and AI, these bots provide faster decision-making, better trade optimization, and more accurate market predictions. Whether someone is a seasoned investor or just starting out, these 6 best quantum AI trading bots in 2026 can help them automate their trading and earn passive income with minimal effort.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Crypto World

International Business Machines (IBM) Stock Tumbles 22% as Citi Analyst Sets $285 Price Target

Key Takeaways

- International Business Machines shares have plummeted nearly 22% in 2026, marking the company’s steepest year-opening decline since 2002.

- Citi Research’s Fatima Boolani launched coverage with a Buy recommendation and set a $285 price objective.

- The company reached a $17 million settlement agreement with the Department of Justice regarding diversity program allegations.

- This DOJ resolution represents the inaugural case from its “Civil Rights Fraud Initiative,” established in the prior year.

- The tech giant’s quantum computing strategy targets delivery of its most advanced system in 2029.

Shares of International Business Machines have experienced a brutal 2026, plunging nearly 22% since January 1st. This performance represents the company’s most challenging year opening since 2002, when the stock tumbled 26% during the identical timeframe. The decline reflects a widespread software sector selloff that has pressured technology stocks universally.

International Business Machines Corporation, IBM

Yet the downturn hasn’t deterred Citi Research’s Fatima Boolani from taking a contrarian stance. This past Friday, she launched coverage on the tech veteran with a Buy recommendation and established a $285 price objective — suggesting approximately 23% appreciation potential from present valuations. Shares were changing hands at $231.25 during that session, declining 2.5% intraday.

Boolani’s investment thesis revolves around IBM’s demonstrated capacity for enduring — and transforming through — transformative technology cycles. From tabulating machines through desktop computing to information technology consulting, the corporation has completely restructured its business model multiple times. This legacy, she contends, demonstrates an “uncanny ability” to maintain market relevance throughout successive technological disruptions.

Enterprise Loyalty and Artificial Intelligence Strategy

This resilience manifests clearly in the company’s client retention patterns. Evercore ISI’s Amit Daryanani highlighted a comparable observation during the previous month, emphasizing that IBM’s enterprise customers have maintained their relationships despite numerous opportunities to transition away from legacy mainframe platforms. This retention characteristic proves difficult to quantify — yet carries substantial weight.

Currently, the company’s product ecosystem encompasses database platforms, development frameworks, and hybrid computing architectures. Boolani views this positioning as an optimal substrate for artificial intelligence implementation, maintaining that enterprise-grade AI solutions will necessarily integrate with established IT infrastructure — precisely IBM’s operational territory.

She additionally dismissed concerns that AI-first startups could displace established enterprise software providers like International Business Machines. The corporation’s extensive consulting partnerships with Fortune 500 organizations provide “competitive insulation,” according to her analysis. Furthermore, those emerging AI vendors might leverage IBM as a gateway for enterprise market penetration.

The company’s capital expenditure requirements remain below cloud hyperscale competitors, which Boolani argues warrants a more favorable free cash flow valuation multiple. She characterized the stock’s underperformance relative to the broader megacap technology cohort as “punitive,” particularly considering the margin expansion she anticipates.

$17 Million Diversity Program Resolution

As Wall Street analysts constructed their bullish arguments, the company simultaneously concluded a regulatory matter with federal authorities. International Business Machines agreed to remit $17 million to resolve a Department of Justice investigation examining its diversity, equity and inclusion initiatives.

This resolution marks the inaugural settlement stemming from the DOJ’s “Civil Rights Fraud Initiative,” a division created last year to scrutinize DEI programs through civil anti-fraud legislation. Federal prosecutors claimed the company employed a “diversity modifier” that connected executive compensation to achieving demographic benchmarks.

The tech company rejected any wrongdoing allegations. The settlement document explicitly clarifies that it constitutes “neither an admission of liability by IBM nor a concession by the United States that its claims are not well-founded.”

Company representatives confirmed they have already discontinued or restructured the programs under examination.

Regarding longer-term strategic initiatives, the corporation’s quantum computing development roadmap continues generating investor interest. Management remains committed to launching its most sophisticated quantum platform in 2029. Boolani characterized this capability as an “important call option” for growth-oriented investors, observing that the company’s established government sector relationships provide a robust foundation in this emerging technology domain.

The crypto market cap fell below the $2.5 trillion mark on Monday after the U.S. officially moved to impose a maritime blockade on Iranian traffic through the strategic Strait of Hormuz.

Summary

- Crypto market cap dropped below $2.5 trillion after the U.S. imposed a maritime blockade on Iranian traffic through the Strait of Hormuz, escalating geopolitical tensions.

- Oil prices surged above $100 while global markets, including equities and even traditional safe havens, faced pressure as investors moved to cash amid rising uncertainty.

- Ongoing tensions and upcoming U.S. PPI data could drive further downside in crypto if inflation remains elevated and keeps Fed policy tighter for longer.

According to recent reports, the U.S. Central Command confirmed through a Navy official that it had begun a blockade of all maritime traffic entering and exiting Iranian ports starting at 10 a.m. ET today.

As noted by the U.S. President in a recent Truth Social post, the U.S. Navy would seek and interdict any vessel in international waters that has paid a transit toll to Iran in the Strait of Hormuz. According to the administration, such payments are characterized as world extortion.

Along with the blockade, the U.S. Navy has deployed destroyers to the Strait to begin clearing naval mines allegedly laid by Iran to ensure a safe pathway for non-Iranian commercial traffic.

It should be noted that, unlike a total closure, the U.S. stated it would still permit freedom of navigation for vessels traveling strictly between non-Iranian ports. Hence, the move is an effective attempt to isolate Iran economically while keeping global energy lanes open for allies.

This escalation follows after diplomatic efforts to resolve ongoing tensions failed in Islamabad last week. These talks collapsed specifically over the Iranian government’s persistence in sticking to its long-term nuclear program.

Shortly following the recent report, oil prices spiked back above $100 on fears that rising energy costs and renewed inflation could hurt the global economy. West Texas Intermediate crude oil rose over 8% to $104.6, while Brent crude climbed back to $102.7.

The downturn was not confined to the crypto market alone. Notably, even traditional safe-haven assets such as gold and silver fell slightly on the day as investors scrambled for liquidity, while Asian indices such as Japan’s Nikkei 225 and the Hang Seng closed significantly lower at the end of their sessions.

The crypto market will likely continue to struggle from escalating tensions between the U.S. and Iran, especially as the situation in the Strait of Hormuz remains volatile.

With a shaky so-called ceasefire between the two nations further strained by Iran’s defiance, risk on assets such as cryptocurrencies could continue to lose their appeal to investors as they pivot towards safer alternatives such as U.S. bonds and gold as a defensive hedge.

Against this backdrop, the U.S. PPI is set to be released tomorrow, Tuesday, at 8:30 a.m. ET. The market estimates the headline producer price index to rise by 1.2% on a monthly basis.

A stronger-than-expected PPI reading can embolden the Fed to maintain high interest rates for longer and hence place further downward pressure on crypto prices, while any sign of cooling could provide some much-needed relief to the struggling crypto sector.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Three altcoins are flashing critical technical setups heading into the third week of April 2026. RaveDAO (RAVE), Polkadot (DOT), and Official Trump (TRUMP) each face pivotal price levels that could define short-term direction.

RAVE continues its parabolic rally with a 185% daily surge. Meanwhile, DOT struggles after a bridge exploit sent the token near all-time lows. TRUMP tests double bottom support ahead of a key holder event.

RAVE Fibonacci Extensions Point Toward $9.00 Target

RaveDAO has been one of the most explosive movers in crypto this month. The token is currently trading at $7.47, reflecting a 185% gain in the past 24 hours alone. This rally extends a larger parabolic move that has delivered gains of over 3,500% from recent lows.

The structure of the advance suggests ordered, Fib-aware positioning rather than random price action. Key Fibonacci extension levels have acted as a staircase throughout the move. The 2.272 extension at $5.45 held as intraday support.

The next major target sits at the 2.618 Fibonacci extension near $8.99. That level aligns closely with the psychological $9.00 zone. With the current price at $7.47, the gap to that target is roughly 18%.

Breakout candles carried significantly elevated volume. The current daily candle shows no signs of exhaustion wicks or upper shadow rejections. The candle body remains full, closing near its high.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

However, manipulation concerns have emerged alongside the rally. Certain wallets reportedly deposited 18.58 million RAVE tokens onto Bitget roughly 10 hours before the pump began. The token’s low circulating supply of approximately 239 million out of a 1 billion maximum amplifies concentrated buying pressure.

On the downside, a daily close below $5.45 would crack the parabolic structure. A break below $3.68 would fully invalidate the bullish case and open the door toward $2.12.

A correction is likely due, as the RSI remains extremely overheated at 99.

DOT Falls Near All-Time Lows After Bridge Exploit

Polkadot is trading at $1.18, down 8% from Sunday’s highs. The decline follows a Hyperbridge gateway exploit that allowed an attacker to mint 1 billion bridged DOT tokens on Ethereum.

The attacker used a forged cross-chain message to change the admin of Polkadot’s token contract on Ethereum. They then minted the full supply and dumped it in a single transaction. The operation netted approximately 108.2 ETH, worth roughly $237,000.

Limited liquidity for the bridged asset capped the attacker’s profit. The exploit did not compromise Polkadot’s native relay chain or the DOT token on its own network. It targeted only the wrapped DOT representation on Ethereum.

Despite this distinction, major South Korean exchanges Upbit and Bithumb suspended DOT deposits and withdrawals as a precaution. The move added further selling pressure to an already weakened token.

DOT now trades dangerously close to its all-time low of $1.10. The token needs to reclaim the $1.22 level to stabilize. A positive development around the exploit response or network security could help restore confidence.

If DOT establishes above $1.22, it could then challenge the resistance at $1.33.

A failure to hold current levels would likely push the price toward $1.10. It could potentially fall even further below that floor.

TRUMP Price Tests Double Bottom at $2.78

Official Trump is trading at $2.81, roughly flat over the past 24 hours. The token sits near a critical support level that may form the base of a double bottom pattern.

The upcoming Mar-a-Lago crypto and business conference scheduled for April 25 has drawn attention to the token. The event offers the top 297 holders a seat at the gathering. The 29 largest whales receive VIP access to the president directly. A qualification snapshot was taken on April 10.

TRUMP needs to hold $2.78 to maintain the double bottom structure. If buyers defend that level, a breakout above the neckline at $3.08 could trigger a rally toward $3.34. That target aligns with the 0.618 Fibonacci retracement level and would represent a 19% gain from the current price.

The bearish scenario emerges if the $2.78 support fails. A breakdown there would send TRUMP toward its all-time low. New lows near $2.44, the 1.272 Fibonacci extension level, could follow. The token remains roughly 96% below its all-time high of $73.43 set in January 2025.

The April 25 holder event can no longer generate significant demand, since the snapshot has already been taken. However, any positive catalyst from the event remains the key variable for TRUMP’s price action.

The post 3 Altcoins to Watch for the 3rd Week of April 2026 appeared first on BeInCrypto.

Bitcoin and artificial intelligence appear to be moving in opposite directions regarding how their power is distributed.

Summary

- Bitcoin mining is increasingly shifting toward industrial-scale operations while AI development begins to move toward smaller and more personal device applications.

- The edge AI market is projected to reach 119 billion dollars by 2033 as localized data processing and privacy needs drive a 300 percent growth rate.

- High energy costs in the United States are pushing Bitcoin hash rates toward the Global South, with Ethiopia and Paraguay emerging as major hubs for hydroelectric mining.

Galaxy Research head Alex Thorn pointed out on Sunday that Bitcoin mining, which started on simple home computers, now mostly happens in massive industrial warehouses using specialized gear. AI, however, may take the reverse route.

While AI currently lives in giant, restricted data centers, Thorn believes open-source progress is closing the gap as major models hit limits in memory and data.

“If local models keep getting smaller, cheaper, and more efficient, AI may become increasingly personal and on-device,” he noted.

Localized computing on the rise

Grand View Research estimates the global market for “Edge AI”—technology that runs locally on gadgets rather than through a central cloud—will reach $119 billion by 2033.

This represents a jump from roughly $25 billion expected in 2025. The growth stems from the explosion of connected devices and a need for instant data processing that does not rely on a distant server.

Market analysts at GVR attributed this momentum to the expansion of the Internet of Things (IoT). Industry trends show a “rising focus on data privacy and localized intelligence at the network edge,” which allows companies to automate tasks without sending sensitive information to a central hub.

Mining moves to the Global South

A separate report from the crypto exchange KuCoin on Friday showed that while Bitcoin hardware is harder for individuals to own, the locations of these machines are spreading out globally.

High electricity prices in the United States have made mining unprofitable in certain regions, with costs to produce a single coin sometimes exceeding $100,000.

Operators are now seeking cheaper energy in places like Ethiopia and Paraguay, where hydroelectric power is plentiful. Such a move helps protect the network by ensuring it isn’t tied to the politics or power grids of just one or two nations.

According to KuCoin, “this decentralization of mining power across different continents enhances the security of the network by making it less vulnerable to any single country’s political or environmental shocks.”

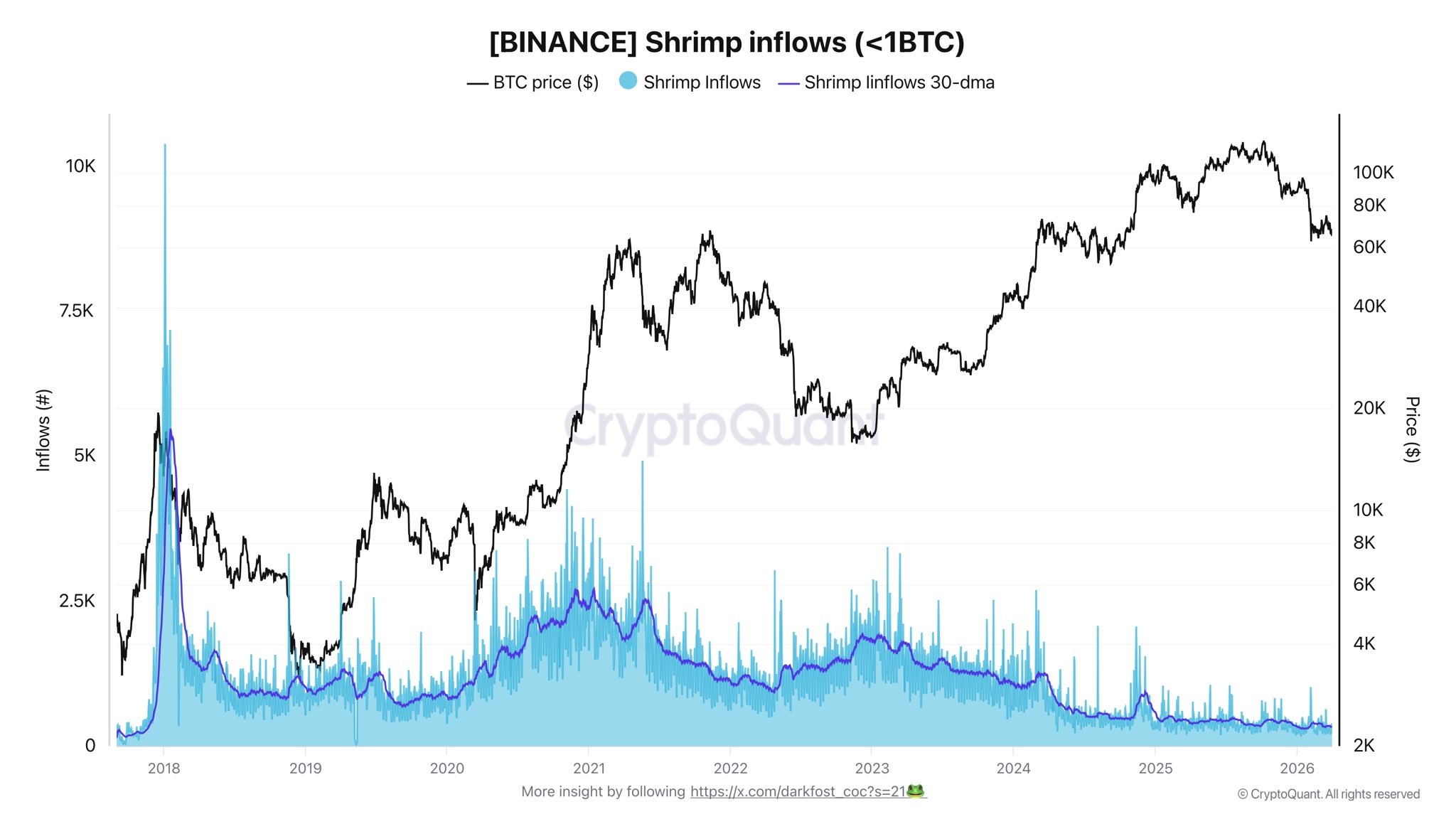

Financial institutions have “accelerated” their participation in crypto markets this year, while retail investors have pulled out, said Exodus CEO JP Richardson on Sunday.

“This might be the first cycle in crypto history where institutions are in a bull market, and retail doesn’t even know it,” the crypto executive said.

Richardson cited a few examples, such as the stablecoin market capitalization all-time high this year, Morgan Stanley’s Bitcoin (BTC) ETF launch, Schwab starting a waitlist for spot Bitcoin trading, Franklin Templeton announcing a crypto division and Fannie Mae accepting Bitcoin-backed mortgages.

“In 2018 and 2022, institutions pulled out with retail. This time, they accelerated,” he said.

This shift could signal that crypto has evolved from volatile, retail-driven hype cycles to a more mature, institution-led market with steadier accumulation, deeper liquidity and reduced reliance on emotional spikes or panic selling.

Cost of living crisis keeping retail away

MN Fund founder and crypto YouTuber Michaël van de Poppe echoed the sentiment in an X post on Sunday, stating, “It’s super clear that retail isn’t interested in crypto.”

“Almost everyone has a hard time paying their bills on a monthly basis,” he added, referring to the escalating cost-of-living crisis and inflationary pressures.

“That’s why this cycle won’t be the retail cycle. It’s the institutional cycle and will take longer.”

Related: Bitcoin price falls under $71K as US-Iran war tensions spark sell-off

CryptoQuant analyst “Darkfost” noted that retail activity hit a nine-year low earlier this month, reporting that inflows from small accounts with less than 1 BTC reached a record low on Binance.

“Retail investors are clearly absent from the market,” he said.

The analyst added that some retail investors may have recently left the crypto market to move into equities and commodities, which have also delivered strong performances.

Near-term sentiment remains fragile

CoinEx exchange chief analyst Jeff Ko told Cointelegraph on Monday that near-term sentiment “remains fragile and heavily macro-driven, especially by oil, the dollar, and inflation expectations.”

“At this stage, the move still looks more like a macro risk premium overwhelming the near-term bid than a genuine deterioration in crypto appetite.”

He said he was more confident over the medium term, adding, “I do not expect oil prices to remain elevated given the underlying supply-demand fundamentals.”

Magazine: Bitcoin quantum-safe without upgrade? CZ’s 2031 crypto vision: Hodler’s Digest

Key Takeaways

- Q1 2026 earnings release scheduled for April 14, pre-market hours

- Options market anticipates approximately 3.87% price movement — exceeding the 2.71% historical average

- Consensus estimates point to $5.45 EPS (+7% YoY) and $49.13B revenue (-8% YoY)

- Goldman Sachs upgraded target to $365 (Buy rating); Morgan Stanley lowered to $334 (Equal Weight)

- Shares gained 8.3% in the past month despite a 3% year-to-date decline

JPMorgan Chase unveils its first-quarter 2026 financial results this Tuesday, April 14, ahead of the market open. As the banking sector’s lead-off reporter, the company’s performance will provide critical insights into industry-wide trends.

The options market is signaling potential volatility, with implied movement around 3.87% following the earnings announcement. This exceeds JPM’s typical post-earnings fluctuation of 2.71% across the previous four quarters, suggesting investors are bracing for significant revelations.

Shares have slipped approximately 3% since the year began. Investor sentiment has been dampened by concerns surrounding artificial intelligence infrastructure spending and geopolitical instability related to tensions with Iran.

However, recent momentum has shifted favorably. JPMorgan’s stock has climbed 8.3% during the last 30 days, tracking closely with the banking sector’s 8.5% advance over the identical timeframe.

Consensus Forecasts and Expectations

Analysts project first-quarter earnings per share of $5.45, representing 7% year-over-year expansion. Revenue projections stand at $49.13 billion, reflecting an approximately 8% contraction compared to the prior-year period.

The anticipated revenue downturn deserves attention. During the previous quarter, JPMorgan reported $46.77 billion in revenue — a 6.9% annual increase — yet fell short of earnings expectations.

Estimate revisions have remained relatively stable throughout the past month, indicating analysts aren’t anticipating major deviations. The banking giant has historically demonstrated an ability to surpass Street predictions.

Wall Street Price Targets Show Divergence

Analyst perspectives vary considerably approaching the earnings event.

Goldman Sachs analyst Richard Ramsden elevated his valuation target to $365 from $352 while maintaining a Buy recommendation. Goldman’s thesis centers on improved banking sector valuations following this year’s roughly 7% decline, which has brought multiples closer to historical benchmarks.

Goldman highlighted several focal points for investors: net interest income projections, capital markets revenue impact from market turbulence, and potential credit quality deterioration or loan loss reserve changes stemming from elevated energy costs.

Conversely, Morgan Stanley adopted a more cautious stance. Analyst Manan Gosalia reduced his price objective to $334 from $365 while retaining an Equal Weight designation. The firm implemented sector-wide target reductions averaging 9%, citing inflationary pressures, Middle Eastern geopolitical risks, and private credit market vulnerabilities.

These contrasting targets frame the current Street consensus. Among 12 Buy recommendations and 8 Hold ratings, the average analyst price target stands at $337.00 — suggesting potential upside of approximately 8.76% from present levels. The aggregate rating qualifies as a Moderate Buy.

Serving as the inaugural major banking institution to report this earnings cycle, JPMorgan’s financial disclosure will establish the narrative framework for peer institutions. Trading commences at 9:30 AM ET on April 14.

Pete Davidson Reveals ‘Brutal’ Mom Moment That Got Him Sober

Israel whine about effigy of butcher Benjamin Netanyahu

Trent vs DMart: Which retailer’s shares should you buy now?

-

Politics3 days ago

Politics3 days agoUS brings back mandatory military draft registration

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Veronica Beard

-

Sports3 days ago

Sports3 days agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Tech6 days ago

Tech6 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Politics19 hours ago

Politics19 hours agoWorld Cup exit makes Italy enter crisis mode

-

Crypto World4 days ago

Crypto World4 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Fashion7 days ago

Fashion7 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Business3 days ago

Business3 days agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Politics3 days ago

Politics3 days agoMalcolm In The Middle OG Turned Down ‘Buckets Of Money’ To Appear In Reboot

-

Fashion6 days ago

Fashion6 days agoLet’s Discuss: DEI in 2026

-

Crypto World5 days ago

Crypto World5 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

NewsBeat11 hours ago

NewsBeat11 hours agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Business3 days ago

Business3 days agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Business2 days ago

Business2 days agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

Politics3 days ago

Politics3 days agoLBC Presenter Mocks Trump Over Iran War Failures

-

Crypto World2 days ago

Crypto World2 days agoFederal judge blocks Arizona from bringing criminal charges against Kalshi

-

Tech7 days ago

Tech7 days agoSuper Meat Boy 3D, coin-pushing chaos and other new indie games worth checking out

-

Tech3 days ago

Tech3 days agoA version of Windows 10 released a decade ago is now eligible for additional security patches

-

Tech7 days ago

Tech7 days agoWhat is the release date for The Boys season 5 episodes 1 to 2 on Prime Video?

-

NewsBeat1 day ago

NewsBeat1 day agoJD Vance announces ‘no agreement’ with Iran over nuclear weapons fear

You must be logged in to post a comment Login