Business

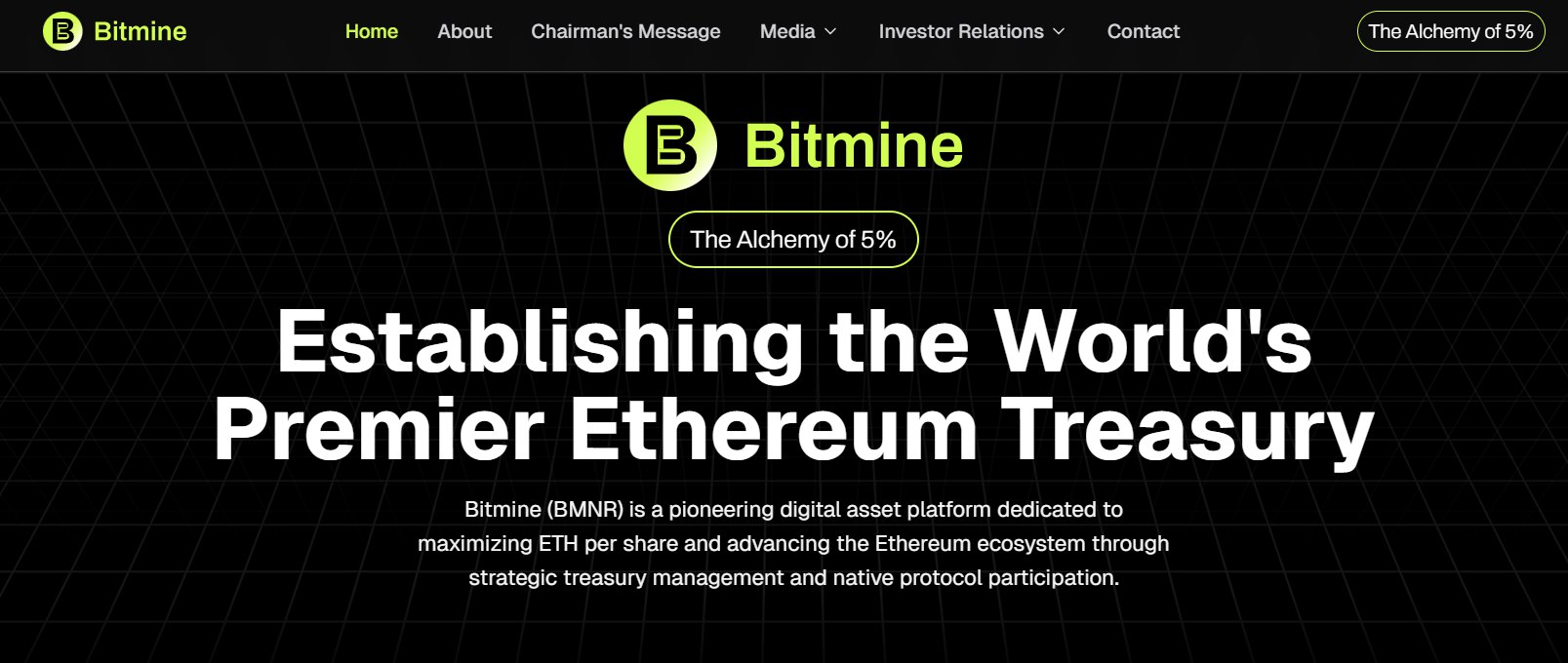

Bitmine Immersion Technologies Stock Climbs to $21.57 on NYSE Debut and Massive $11.8B Ethereum Treasury

NEW YORK — Shares of Bitmine Immersion Technologies Inc. rose Monday to $21.57, up 28 cents or 1.32%, as the Ethereum-heavy treasury company continued to draw investor attention following its recent uplisting to the New York Stock Exchange and aggressive accumulation of digital assets.

The Las Vegas-based firm, which operates under the ticker BMNR, has transformed from a Bitcoin mining operation using advanced immersion cooling technology into what it calls the world’s leading Ethereum treasury company. As of its latest disclosure on April 13, Bitmine reported total crypto, cash and “moonshot” holdings of $11.8 billion, including 4.875 million ETH tokens — roughly 4% of Ethereum’s total supply.

The company’s stock has experienced extreme volatility in recent weeks, swinging on news of its massive ETH purchases, the NYSE move and an expanded $4 billion share repurchase program. Shares climbed as much as 13% on April 9 following the uplisting announcement but have pulled back from earlier 2026 highs near $161 amid broader crypto market fluctuations and concerns over valuation.

Bitmine’s strategy centers on what it terms “the alchemy of 5%,” an ambitious goal of accumulating up to 5% of Ethereum’s circulating supply as its primary treasury reserve asset. Executive Chairman Tom Lee, a prominent crypto commentator, has been vocal in defending the approach, framing market dips as buying opportunities and predicting strong long-term recovery for ETH.

The company has repeatedly updated investors on its growing ETH stack. Recent filings showed holdings climbing from 4.474 million tokens in early March to the current 4.875 million, acquired through disciplined purchases funded in part by its Bitcoin mining and hosting operations. At current Ethereum prices around $2,100-$2,300 per token, the treasury alone represents a multi-billion-dollar position that dwarfs many traditional corporate balance sheets.

On April 9, Bitmine officially uplisted from the NYSE American to the main New York Stock Exchange board, retaining the BMNR ticker. The move was accompanied by an expansion of its share repurchase authorization from $1 billion to $4 billion, one of the largest buyback programs announced by a crypto-related public company this year. Management signaled it would use the authority opportunistically if shares trade below intrinsic value tied to its ETH holdings.

Analysts have taken notice. B. Riley raised its price target to $33 from $30, while the consensus target hovers around $34.50, implying more than 60% upside from current levels. Some observers describe Bitmine as trading at a discount to its net asset value when factoring in the Ethereum treasury, cash reserves exceeding $700 million and smaller positions in Bitcoin and “moonshot” investments such as stakes in Beast Industries and Eightco Holdings.

Bitmine’s origins lie in immersion-cooled Bitcoin mining. The company deploys specialized hardware submerged in non-conductive dielectric fluid to improve energy efficiency, reduce heat and extend equipment life compared with traditional air-cooled setups. While it is winding down proprietary self-mining exposure and deferring new site builds, it continues to offer hosting, equipment sales and advisory services in the Bitcoin ecosystem.

A key growth initiative is the launch of MAVAN — the Made-in-America Validator Network — its proprietary Ethereum staking solution. The company has already staked more than 3 million ETH and aims to generate additional yield through native protocol participation and decentralized finance mechanisms. MAVAN is expected to contribute to operating revenue once fully operational, though accounting treatment of staking rewards remains a point of investor focus ahead of upcoming quarterly reports.

Financial results reflect the company’s pivot. For fiscal year 2025 ending August 31, Bitmine reported revenue of approximately $6.1 million, largely from mining and related services, with net income influenced heavily by unrealized gains or losses on its digital asset holdings. Recent quarters have shown significant swings in earnings per share due to crypto price volatility. The company maintains no net debt and emphasizes a fortress balance sheet to support its treasury strategy.

Investor sentiment has been mixed. Some praise the transparent, frequent disclosures on holdings as a model for public crypto companies, while critics point to potential overvaluation risks, dilution from past capital raises and the concentrated bet on Ethereum. A short-term pullback earlier in April followed questions about whether the $11.4 billion treasury figure adequately accounted for cost basis and market conditions.

Bitmine’s leadership, including CEO Chi Tsang and CFO/COO Young Kim, has highlighted institutional backing and the appeal to investors seeking indirect exposure to Ethereum without directly holding the volatile asset. The strategy positions the company as a hybrid play: infrastructure roots in efficient mining combined with a bold digital asset treasury.

Broader market context has played a role in the stock’s movement. Ethereum prices have faced pressure from macroeconomic factors, including interest rate expectations and regulatory developments, yet Bitmine has continued accumulating during dips. The company reported its largest single Ethereum purchase in months in early April, adding tens of thousands of tokens.

As a newly minted NYSE-listed name, Bitmine gains increased visibility, potential for higher trading volumes and eligibility for inclusion in broader indices over time. The uplisting also enhances credibility with traditional investors exploring crypto exposure through public equities.

Risks remain substantial. The value of Bitmine’s treasury is directly tied to Ethereum’s price, which can experience sharp swings. Regulatory changes affecting staking, custody or digital asset classification could impact operations. Competition in both mining and treasury strategies is intense, with larger players in the space also building crypto reserves.

Looking ahead, investors will watch for the next quarterly update and any further details on MAVAN’s revenue contribution. Full-year fiscal 2026 guidance has not been detailed extensively, but management continues to prioritize ETH accumulation per share and ecosystem participation.

Bitmine’s immersion cooling technology, originally developed for mining efficiency, has drawn parallel interest for potential applications in high-performance computing and AI data centers, where heat management is critical. While not yet a core revenue driver, the expertise could provide diversification opportunities.

The company’s frequent press releases on holdings have created a cadence of news flow that keeps it in the spotlight among retail and institutional crypto watchers. With roughly 455 million shares outstanding and a market capitalization near $9.7 billion, Bitmine trades as a mid-cap name with outsized crypto leverage.

As of mid-April 2026, the stock’s 52-week range spans from lows near $3.20 to highs above $160, underscoring the speculative nature of the name. Volume has spiked on announcement days, reflecting heightened trader interest.

Bitmine positions itself as more than a miner or a holding company — it aims to be an active participant in the Ethereum network through staking and infrastructure. Whether this “Ethereum treasury” model delivers sustainable shareholder value will depend on crypto market cycles, execution on MAVAN and prudent capital allocation via the buyback.

For now, with shares hovering around $21.57 and a massive treasury backing the story, Bitmine Immersion Technologies remains one of the most closely watched names at the intersection of traditional mining infrastructure and next-generation digital asset strategies.

Qualcomm EVP Palkhiwala sells $325k in shares

Alignment healthcare CEO Kao sells $6.16 million in stock

Mizuho lowers HF Sinclair stock price target on earnings outlook

MSc in Finance. Long-term horizon investor mostly with 2-5 year horizon. I like to keep investing simple. I believe a portfolio should consist of a mix of growth, value, and dividend-paying stocks but usually end up looking for value more than anything. I also sell options from time to time.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

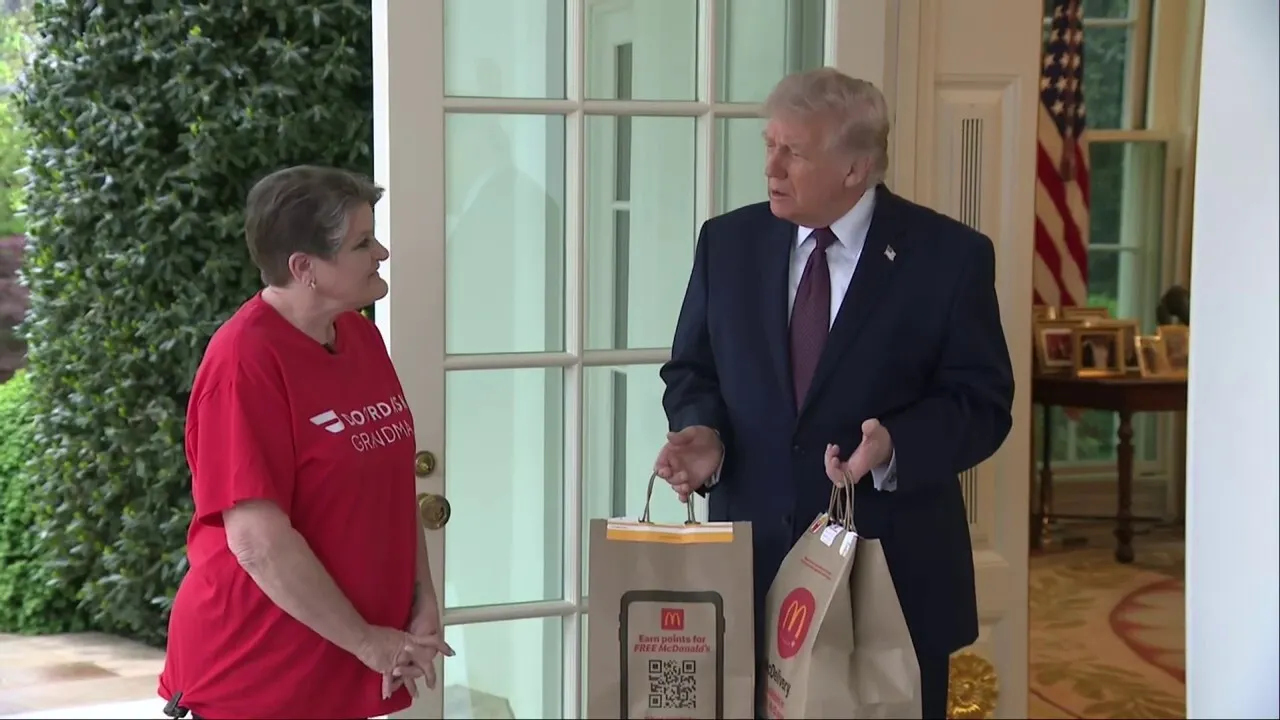

Gig worker shares story of surprise $11,000 savings during White House delivery as President Donald Trump promotes sweeping tax cuts before Tax Day.

A DoorDash delivery driver praised President Donald Trump at the White House, saying his “no tax on tips” policy helped her family “immensely” and delivered more than $11,000 in savings ahead of Tax Day.

The driver, Sharon Simmons, met Trump during a delivery to the White House, where she thanked him directly, telling him it had made a significant difference for her household.

“It has helped my family out immensely and I definitely appreciate it,” Simmons said, referring to the administration’s push to eliminate taxes on tips.

Simmons, who has worked as a full-time DoorDash driver since 2021, said tips make up a major portion of her income. She told the president she saved more than $11,000 under the policy, calling the amount “very surprising” when asked if the total exceeded her expectations.

IRS GUIDANCE FOR TRUMP’S NO TAX ON TIPS’ AND OVERTIME DEDUCTIONS: WHAT TO KNOW

A DoorDash driver told Trump his “no tax on tips” policy saved her over $11,000, helping her family manage expenses during her husband’s cancer treatment. (Fox News / Fox News)

The savings came at a critical time for her family. According to information shared during the event, Simmons’ husband reduced his work hours while undergoing cancer treatment, leaving her income – and the tips she earned – as a key source of financial support. The additional money has helped cover medical-related expenses, offset lost income and pay for travel to visit family.

Trump used the moment to highlight his broader tax agenda, pointing to Simmons’ experience as an example of what he described as widespread relief for working Americans.

“So the reason for this is the fact that I heard you picked up an extra $11,000 because the tax bill was so big – the refund was the biggest you’ve ever had,” Trump said, crediting the “Great Big Beautiful Bill.” He also referenced similar anecdotes from other taxpayers who, he said, received larger-than-expected refunds under his policies.

IRS REVEALS 2026 TAX ADJUSTMENTS WITH CHANGES FROM ‘BIG, BEAUTIFUL BILL’

Sharon Simmons, or “DoorDash Grandma”, delivered McDonald’s to President Donald Trump in the Oval Office. (Fox News / Fox News)

The “no tax on tips” initiative is part of a broader tax package the administration says is aimed at boosting take-home pay for service industry workers and others who rely on variable income.

According to the White House, millions of Americans have already benefited from the provision, with average deductions reaching into the thousands of dollars.

During the exchange, Trump also emphasized that the reported savings did not include potential additional benefits tied to overtime provisions, another component of his tax plan.

SOCIAL SECURITY COMMISSIONER FRANK BISIGNANO NAMED IRS CEO

President Trump pulled cash out of his pocket to give “DoorDash Grandma” a tip. (Fox News / Fox News)

The interaction carried a lighter moment as well, when a reporter asked whether the White House was known for tipping delivery workers. Trump paused before handing Simmons a tip and replied, “Yes, very.”

At one point, Trump gestured to the scene and joked, “This doesn’t look staged, does it?” as he continued to promote the policy and its impact.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

For Simmons, the focus remained on the tangible difference the tax change made in her daily life – and the stability it provided during a difficult year for her family as she balanced work and caregiving responsibilities.

The coverage comes at a time when Paytm shares have corrected 20% from its 52-week peak of Rs 1,381 on the NSE. This year, the stock has plunged 15% as domestic and global markets remain hit with Iran-Israel/US war that has now completed 44 days and the issues remain unresolved.

Notwithstanding the recent correction, the stock is trading 31% higher on a one-year basis, witnessing a sharp rebound of 16% in April.

One 97 shares are currently trading above their 50-day simple moving average (SMA) of Rs 1,096 while slipping below their 200-day SMA of Rs 1,173.

4 things that work for Paytm:

1) Leading fintech with strong monetization

Paytm is 3rd largest player in UPI (P2P+ P2M) value share of 6.9% (February 2026) transaction processed. Paytm’s ecosystem evolved from customer to merchant centric with improving monetization capability as indicated by steady rise in revenue per MTU to Rs 1,155 (annually for December 2025 quarter.

“Rise in monetization capability is driven by strong distribution network, diversified product portfolio and strong brand recall. Its vast

active merchant base (48 million December 2025), leadership position within faster growing UPI-P2M and moat in merchant lending should continue drive strong revenue growth of 25% CAGR over FY26-28e,” Haitong note said.Payments contributes 60% of total revenue and should continue dominate revenue mix as per Haitong’s estimates.

2) Strong moat in merchant lending (ML) distribution

Paytm’s financial services distribution has rebounded strongly, with revenue rising 59% YoY in 9MFY26 and its share increasing to 30%, driven largely by merchant lending. Its tech-led collection model and wide sales network create a strong moat, attracting lending partners. With only ~7% of merchants currently using lending services (target: 20%), there remains significant growth potential.

3) Levers for margin momentum

Paytm’s net payments revenue is expected to grow at a 38% CAGR over FY26–28, outpacing GMV growth of 25%, driving margins to 10 bps+ by FY28. The expansion will be led by a higher share of MDR-yielding instruments, rising EMI transactions, growth in Paytm Postpaid, and regulatory approval as a Payment Aggregator. While near-term EBITDA may see some impact from PIDF adjustments, management remains confident of offsetting this over the long term.

Also read | BSE loses ‘cheap’ tag post 80% rally in one year. Can Q4 performance, NSE IPO drive rerating?

4) Operating leverage

Paytm turned core EBITDA (ex-other income) positive in June 2025 quarter and reported core-EBITDA margin of 6% driven by benefits from operating leverage and reported profit before tax (PBT) of Rs 590 crore in 9MFY26.

“Paytm should continue on its journey to optimize its cost and we expect core EBITDA/PAT to grow by 49%/ 44% CAGR over FY26-28e. We expect Paytm to deliver core-EBITDA (%) of 17% core EBITDA (%) by FY28 broadly in-line with management guidance,” Haitong note said.

5) Peer comparison

Within the payments space, Paytm has built a strong business model at merchants’ end and it has strong moat around distribution of lending products vis-a-vis PB Fintech, PhonePe, Pine Labs, Groww and Moneyview, this brokerage said.

Paytm and PhonePe reported similar revenues, but Paytm stands out with positive core EBITDA (5.3%) versus PhonePe’s losses, while PineLabs remains smaller but profitable. Paytm has also improved efficiency, sharply reducing employee costs and maintaining relatively lower marketing spends. However, it continues to invest more in technology compared to most peers.

(Disclaimer: The recommendations, suggestions, views, and opinions given by the experts are their own. These do not represent the views of The Economic Times.)

So the Iranians wouldn’t give up their uranium enrichment or dismantle their enrichment facilities. Or hand over their already enriched uranium. So President Trump turned the tables, applied some Trumpian Jiu-Jitsu, and put a United States naval blockade on the Strait of Hormuz that will be enforced in the Gulf of Oman.

I’m not sure anybody yet knows how this is all going to go down, but at least beginning today, here’s what America’s Central Command said: “Any vessel entering or departing the blockaded area without authorization is subject to interception, diversion, and capture. The blockade will not impede neutral transit passage through the Strait of Hormuz to or from non-Iranian destinations.”

To my way of thinking, what that means is that anybody that does business with Iran is going to have their ships blockaded. And if the Iranian motorboats take pot shots at our Navy, we will obliterate them just the way we did with all those Venezuelan drug boats. To a large extent, Mr. Trump has adopted the Venezuela model. Iran sells no oil, makes no money, therefore can’t disperse any money they don’t have, and America takes de facto control of the whole Persian Gulf area.

The president had to say about all of this: “It’s called all in, and all out.” He added: “We think that numerous countries are going to be helping us with this also, but we’re putting on a complete blockade. We’re not going to let Iran make money on selling oil to people that they like, and not people that they don’t like or whatever it is. It’s going to be all or none,” and “I predict they come back and give us everything we want.”

Former U.S. special envoy for Ukraine Gen. Keith Kellogg discusses how the U.S.-Iran conflict is impacting China and Russia as a U.S. naval blockade of the Strait of Hormuz takes effect on ‘Kudlow.’

I say good. Then there’s the question of when will Iran go completely bankrupt? Some quick numbers from several sources, including TIPP Insights and Foundation for Defense of Democracies more than 90 percent of Iran’s nearly 110 billion in annual trade transits the Persian Gulf, crude oil alone was earning $139 million per day before the war started. Petrochemicals earn another $54 million per day.

So at $435 million a day in lost revenues, that comes to $159 billion over a year. That $159 billion loss of revenues is roughly 50 percent more than the entire Iranian budget which comes to roughly $100 billion. At what point does bankruptcy come into play? I honestly don’t know yet.

According to sources, on-shore oil storage in Iran begins to top out in about 13 days. So that means the infrastructure shutting will cause permanent damage. Whether this economic obliteration will bring Iran back to the negotiating table remains to be seen.

There’s a couple of Iranian Islamic Revolutionary Guard Corps crazies that seem to be leaders right now, Mojtaba Vehedi, and Mohammad-Bagher Ghalibaf. So I wouldn’t be so sure about any benevolent regime change. The big question is how long will it take to starve them out?

Business

Intuitive Machines Stock Climbs 2.4% as $180M NASA Lunar Contract and $900M Revenue Outlook Fuel Momentum

HOUSTON — Intuitive Machines Inc. shares rose more than 2% in early trading Monday to $24.14 as the lunar exploration company continued to draw investor interest following its recent $180.4 million NASA contract win and ambitious full-year 2026 revenue guidance of $900 million to $1 billion, nearly five times 2025 levels.

The modest gain came amid ongoing enthusiasm for commercial space plays, with Intuitive Machines benefiting from renewed focus on NASA’s Artemis program and the company’s expanding role in delivering payloads and infrastructure to the lunar surface. The stock has shown significant volatility in recent weeks, surging as much as 37% in early April after the major NASA award before experiencing some pullback.

Intuitive Machines announced the $180.4 million Commercial Lunar Payload Services (CLPS) task order from NASA on March 24. The contract calls for the company to deliver seven science and technology payloads — including an Australian Space Agency lunar rover and technologies from Blue Origin’s Honeybee Robotics — to the lunar South Pole region using its larger Nova-D class lander. This marks the company’s fifth CLPS task order and the first requiring the heavier cargo-class lander, expanding its operational capabilities on the Moon.

The award adds substantial visibility to Intuitive Machines’ backlog, which stood at approximately $943 million as of late February after incorporating the Lanteris Space Systems acquisition and other program wins. About 60-65% of the backlog is expected to convert to revenue in 2026, providing a strong foundation for growth.

In its fourth-quarter and full-year 2025 earnings released March 19, Intuitive Machines projected 2026 revenue between $900 million and $1 billion, with positive adjusted EBITDA for the year. The outlook reflects contributions from lunar missions, national security contracts such as the Space Development Agency’s Tranche 3 Tracking Layer, and diversified services following strategic acquisitions.

The company has successfully completed two lunar missions — IM-1 and IM-2 — demonstrating its Nova-C lander’s ability to achieve soft landings and conduct operations on the lunar surface, including the southernmost operations to date. IM-3 remains on track for a 2026 launch, with IM-4 and the newly awarded IM-5 missions following in subsequent years.

Intuitive Machines has also broadened its portfolio beyond pure lunar landers. The acquisition of Lanteris Space Systems (formerly Maxar Space Systems) for roughly $800 million in early 2026 added satellite manufacturing capabilities, while the purchase of KinetX Aerospace strengthened its space navigation and flight dynamics expertise. These moves have diversified revenue streams into national security and commercial satellite programs.

A $175 million strategic equity investment announced earlier in 2026 provided additional capital to support growth initiatives, including expansion of its Space Data Network for persistent lunar connectivity. The company launched EchoStar XXV and continues to pursue opportunities in in-space data processing and communications.

Despite the strong top-line momentum, challenges remain. Fourth-quarter 2025 revenue came in at $44.8 million, missing some estimates, and the company continues to manage cash burn as it scales operations. Free cash flow use improved year-over-year to $56 million in 2025, but profitability remains a focus as higher-margin service revenue grows.

Analysts have responded positively to the NASA contract and guidance. Several firms raised price targets following the March announcements, with consensus leaning bullish on the long-term runway in lunar infrastructure. The stock hit all-time highs near $24.30 in early April amid the contract news and broader excitement around NASA’s Artemis II crewed lunar flyby mission.

Intuitive Machines’ technology emphasizes scalable lunar landers, autonomous surface operations and communications networks designed to support sustained human and robotic presence on the Moon. Its Space Data Network aims to provide reliable connectivity across the lunar surface and cislunar space, a critical enabler for future Artemis missions and potential commercial activities such as resource utilization.

The company’s Houston headquarters positions it at the heart of NASA’s lunar ambitions, with strong ties to the agency’s Commercial Lunar Payload Services initiative. Success on IM-1 and IM-2 has built credibility, helping secure larger and more complex task orders.

Broader sector tailwinds have supported the stock. Renewed U.S. commitment to returning astronauts to the Moon, combined with commercial interest in lunar economy opportunities, has lifted valuations across space infrastructure names. Intuitive Machines stands out for its proven landing track record and expanding payload delivery capabilities.

Risks include execution on complex missions, potential delays in launch schedules, competition from other CLPS providers and the capital-intensive nature of space hardware development. The stock remains highly volatile, typical for small-cap space companies with binary mission outcomes and heavy reliance on government contracts.

As of Monday, trading volume appeared moderate, with the 2.44% gain reflecting continued optimism rather than fresh catalysts. Investors will watch for updates on IM-3 preparations and any additional contract awards in the coming months. First-quarter 2026 results are expected in early May.

Intuitive Machines has evolved rapidly from a startup focused on lunar landings to a broader space infrastructure and services provider. Its backlog growth, successful missions and strategic acquisitions have transformed its profile, attracting both retail momentum traders and institutional interest in the commercial space sector.

For long-term believers, the company’s path hinges on converting its substantial backlog into revenue while maintaining operational excellence on upcoming lunar flights. Positive execution could validate the aggressive 2026 guidance and support further re-rating of the stock.

Monday’s modest advance kept the shares trading near recent highs, underscoring sustained investor appetite for companies playing key roles in humanity’s return to the Moon. With multiple missions on the horizon and a diversified business base, Intuitive Machines appears well-positioned to benefit from the next phase of lunar exploration and commercialization.

TBG: Consistent Dividend Growth But Underwhelming Total Returns

Ian Bezek is a former hedge fund analyst at Kerrisdale Capital. He has spent the decade living in Latin America, doing the boots-on-the ground research for investors interested in markets such as Mexico, Colombia, and Chile. He also specializes in high-quality compounders and growth stocks at reasonable prices in the US and other developed markets. Ian leads the investing group Ian’s Insider Corner. Features of the group include: the Weekend Digest which covers everything from new ideas to updates on current holdings and macro analysis, trade alerts, an active chat room, and direct access to Ian. Learn More.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

ClearBank says it’s first Dutch bank with MiCA approval, rolls out EURC, USDC

I’m A Celebrity viewers say ‘what’s the point’ as they fume over ‘annoying’ twist

Qualcomm EVP Palkhiwala sells $325k in shares

-

Politics3 days ago

Politics3 days agoUS brings back mandatory military draft registration

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Veronica Beard

-

Sports3 days ago

Sports3 days agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Tech6 days ago

Tech6 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Politics1 day ago

Politics1 day agoWorld Cup exit makes Italy enter crisis mode

-

Crypto World4 days ago

Crypto World4 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Business3 days ago

Business3 days agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Politics4 days ago

Politics4 days agoMalcolm In The Middle OG Turned Down ‘Buckets Of Money’ To Appear In Reboot

-

Fashion6 days ago

Fashion6 days agoLet’s Discuss: DEI in 2026

-

Crypto World5 days ago

Crypto World5 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

NewsBeat1 day ago

NewsBeat1 day agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Business3 days ago

Business3 days agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Business2 days ago

Business2 days agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

Crypto World4 hours ago

Crypto World4 hours agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

Politics4 days ago

Politics4 days agoLBC Presenter Mocks Trump Over Iran War Failures

-

Crypto World3 days ago

Crypto World3 days agoFederal judge blocks Arizona from bringing criminal charges against Kalshi

-

Tech4 days ago

Tech4 days agoA version of Windows 10 released a decade ago is now eligible for additional security patches

-

NewsBeat2 days ago

NewsBeat2 days agoJD Vance announces ‘no agreement’ with Iran over nuclear weapons fear

-

Business3 days ago

Business3 days agoIMF retains floor for precautionary balances at SDR 20 billion

-

Entertainment4 days ago

Entertainment4 days agoA ‘Bridgerton’ Star’s New Survival Thriller Is a Must-Watch on Netflix This Weekend

You must be logged in to post a comment Login