Editor’s note: This article is intended to provide a general overview of the ETF for educational purposes only and, unlike other articles on Seeking Alpha, does not offer an investment opinion about the ETF.

Business

TopBuild Stock Soars 16% on $17 Billion Takeover Deal by QXO in Building Products Mega-Merger

NEW YORK — TopBuild Corp. shares skyrocketed more than 16% in early Monday trading on April 20, 2026, surging $67.80 to $478.11 after the leading insulation and building products installer agreed to be acquired by QXO Inc. in a $17 billion cash-and-stock transaction that values the company at a substantial premium.

The deal, announced late Sunday, marks a major consolidation move in the fragmented building products distribution and installation sector. QXO will pay $505 per share for TopBuild, representing a 23.1% premium to Friday’s closing price of $410.31 and a 19.8% premium to the 60-day volume-weighted average price. The transaction is expected to close in the third quarter of 2026, subject to shareholder and regulatory approvals.

Under the terms, TopBuild shareholders can elect to receive $505 in cash or approximately 20.2 shares of QXO common stock for each TopBuild share, subject to proration to maintain an overall mix of roughly 45% cash and 55% stock. The structure gives investors a choice between immediate liquidity and participation in the combined company’s future growth.

TopBuild (NYSE: BLD), headquartered in Daytona Beach, Fla., is a dominant player in the installation of insulation and commercial roofing, as well as a specialty distributor of related building materials. The company operates across the United States and Canada with a network of more than 14,000 employees and hundreds of branches. It has grown aggressively through acquisitions, completing seven deals in 2025 alone that added about $1.2 billion in annual revenue, including the Progressive Roofing and Specialty Products and Insulation transactions.

The acquisition creates a powerhouse with combined annual revenue exceeding $18 billion and adjusted EBITDA above $2 billion. QXO, which has been rapidly expanding its building products platform, described the deal as immediately and substantially accretive to earnings while targeting $300 million in synergies by 2030 through operational efficiencies, procurement savings and cross-selling opportunities.

“TopBuild is an exceptional business with market-leading positions, strong free cash flow generation and a proven track record of growth through both organic execution and strategic acquisitions,” QXO executives said in a joint statement. “This combination accelerates our vision of building a scaled, diversified leader across the building products value chain.”

Analysts and investors reacted positively to the premium and strategic fit. The surge in TopBuild shares reflected the market’s quick pricing in of the deal value near $505, though some early profit-taking and uncertainty around the proration mechanics kept the stock below that level in morning trading. Volume was significantly elevated as traders rushed to position themselves.

The deal comes as TopBuild has delivered consistent strong performance. For the full year 2025, the company reported sales of approximately $5.4 billion and adjusted EBITDA exceeding $1 billion. In its February 2026 outlook, TopBuild projected 2026 sales between $5.925 billion and $6.225 billion with adjusted EBITDA in the range of $1.005 billion to $1.155 billion, driven by continued acquisition integration and healthy underlying demand in residential and commercial construction.

Recent operational highlights include the promotion of John Achille to president and chief operating officer in early April, signaling internal confidence in execution capabilities. The company is scheduled to report first-quarter 2026 results on May 5, with a conference call at 9 a.m. ET, though the takeover agreement now shifts focus to deal-related matters.

For QXO, the move significantly broadens its footprint in insulation, roofing and mechanical insulation distribution. The combined entity is expected to benefit from TopBuild’s specialized installation expertise and nationwide branch network, complementing QXO’s existing distribution operations.

Wall Street had generally viewed TopBuild favorably before the announcement, with a consensus “Moderate Buy” rating from 16 analysts and an average price target around $440. The takeover offer represents a clear step-up from those targets, potentially capping near-term upside unless the deal faces complications or a superior bid emerges.

Regulatory hurdles include Hart-Scott-Rodino antitrust clearance, though both companies expressed confidence in obtaining approvals given limited direct overlap in certain markets. The agreement includes a $600 million termination fee payable by TopBuild if it accepts a superior proposal under specified circumstances, along with customary “no-shop” provisions and matching rights for QXO.

Some shareholder advisory firms and law firms quickly signaled scrutiny. Ademi LLP announced an investigation into whether TopBuild’s board obtained a fair price and adequately considered alternatives, a common step in large M&A deals that often leads to additional disclosures but rarely derails transactions.

TopBuild has returned substantial capital to shareholders in recent years, repurchasing more than $434 million of its stock in 2025 and over $2 billion over the past decade. The company’s disciplined approach to capital allocation, combining tuck-in acquisitions with buybacks, has supported strong compound annual growth since its 2015 spin-off from Masco Corp. — nearly 13% in sales and more than 25% in adjusted EBITDA.

The building products sector has seen increased M&A activity amid favorable long-term demographics, including housing shortages and aging infrastructure needs. Insulation demand benefits from energy efficiency trends and stricter building codes, while commercial roofing and mechanical insulation provide diversification.

Industry observers noted that the premium reflects TopBuild’s high-quality assets, including its skilled installer workforce and relationships with major homebuilders and general contractors. The deal also comes against a backdrop of steady U.S. construction spending, even as interest rates and material costs have created periodic headwinds.

For TopBuild employees and customers, the companies pledged a smooth transition with no immediate changes expected to day-to-day operations. QXO plans to add one TopBuild nominee to its board upon closing.

The transaction values TopBuild at an enterprise value that underscores the strategic premium for scale in a consolidating industry. With QXO assuming the role of acquirer, the combined platform could pursue further bolt-on deals while realizing cost synergies from overlapping functions.

As trading continued Monday morning, TopBuild shares held most of their gains but traded with volatility typical of deal stocks. Some investors locked in profits near the $478 level while others bet on potential upside if the market fully prices in the $505 valuation or if QXO shares perform well.

QXO’s own stock reacted positively in premarket and early sessions, reflecting investor approval of the accretive nature of the deal and the expanded scale. The merger is structured as a two-step transaction, providing a clear path to completion once approvals are secured.

Looking ahead, both companies will focus on obtaining shareholder votes, regulatory clearances and preparation of a registration statement for the QXO shares to be issued. The expected Q3 2026 closing timeline gives time for integration planning while minimizing disruption to ongoing operations.

TopBuild’s transformation from a spin-off to a market leader highlights the value created through disciplined execution and opportunistic acquisitions. The pending sale to QXO caps a strong run for shareholders while positioning the business within a larger platform poised for continued growth in the North American building products market.

The announcement injects fresh momentum into an otherwise quiet start to the week for many construction-related stocks. With housing demand supported by demographic trends and commercial activity showing resilience, the combined QXO-TopBuild entity could emerge as a more formidable player capable of weathering cyclical fluctuations.

As details continue to emerge and the market digests the implications, TopBuild’s dramatic 16%+ jump on April 20 served as a vivid illustration of how transformative M&A can rapidly reshape shareholder value in the industrials sector. Investors will now monitor developments around approvals, any competing offers and the companies’ ability to articulate a compelling vision for the combined future.

Continue Reading

Food Business News webinar highlighted five startups innovating within segments they see as dated.

Starfighters Space: Bootstrap Approach To Space Industry But Scaling Challenges

A view shows a second-generation R1S at electric auto maker Rivian’s manufacturing facility in Normal, Illinois, on June 21, 2024.

Joel Angel Juarez | Reuters

A tornado damaged part of Rivian Automotive‘s factory in central Illinois over the weekend, according to a message sent to employees Sunday night by CEO RJ Scaringe that was viewed by CNBC.

The tornado touched down on the plant, Scarigne said. That area was being used for parts storage and logistics for Rivian’s upcoming R2, which is a crucial product for the company that’s expected to be on sale this spring.

Scaringe said operations in the damaged area are expected to resume this week, while other major portions of the plant, such as its assembly lines, are operating as planned. No injuries have been reported as a result of the incident, according to a company spokeswoman.

“While Building 2 has sustained damage and is closed for the time being as we complete our assessments, I am incredibly relieved to share that there were no injuries at our plant,” Scaringe said in his message to employees.

Scaringe said the company would “share more information as it becomes available, but for now, our priority is ensuring our Normal [Illinois] team is safe and supported.”

Apparent photos posted online of the aftermath, which was first reported by TechCrunch, showed damage to the roof and at least one wall of the recently constructed building.

The National Weather Service reports the factory was hit amid a “significant tornado outbreak” that occurred Friday across the upper Midwest. Confirmed tornadoes near the factory Friday night were classified as EF1, with estimated peak winds of 100 mph, according to NWS.

FXC: Understanding The Benefits And Risks Of Adding Currency Exposure To Your Portfolio

Credo Technology: Hypergrowth Leader Solving The AI Connectivity Bottleneck

American Petroleum Institute CEO Mike Sommers joins ‘Varney & Co.’ to warn that a global oil shortfall and disruptions in the Strait of Hormuz could drive gas prices higher just as peak summer demand begins.

President Donald Trump pushed back Monday on his own energy secretary’s claim that a return to $3-a-gallon gas will not come through the end of the year.

“No, I think he’s wrong on that, totally wrong,” Trump told The Hill on Monday, when asked about Energy Secretary’s Christopher Wright’s interview with CNN’s “State of the Union” on Sunday.

Trump remains steadfast in his conviction that gas prices in America are going to drop precipitously “as soon as this ends,” referring to the oil blockade in the Strait of Hormuz, echoing oft-repeated vows for those concerned that oil prices in America might actually return all the way up to Biden administration levels.

“The blockade is very powerful, very strong,” Trump added to The Hill, pointing at Iran’s obstruction effort. “They lose $500 million a day with the blockade up. We control it. They don’t control it.”

BESSENT WARNS GAS STATIONS THAT TREASURY DEPT WILL KEEP THEM ‘HONEST’ AFTER SPIKE IN PRICES

The AAA Fuel Prices state by state show the highest prices in the coastal states and the lowest prices in the midwest states. (Gasprices.aaa.com)

Wright’s comments were not all that unaligned with Trump’s position, but Wright was a bit less convicted on prices on when gas might drop below $3 again.

“I don’t know, that could happen later this year, that might not happen until next year, but prices have likely peaked and they will start going down,” Wright told CNN’s Jake Tapper, who asked further that gas “might not be under $3 a gallon until 2027?”

“Certainly, with a resolution of this conflict, you will see prices go down,” Wright added. “Prices across the board on energy prices will go down.”

OIL PRODUCERS ORG SHREDS CALIFORNIA DEM FOR BLAMING IRAN WAR FOR HIS DISTRICT’S GAS PRICES

Gas prices in the U.S. are higher amid the Iranian Strait of Hormuz obstruction, but they are still well below the Biden-era prices due to inflation caused by restrictive fossil fuel energy policy. (Sean Gallup/Getty Images)

“Under $3 a gallon is pretty tremendous — in inflation-adjusted terms,” Wright added to Tapper. “We had that in the Trump administration, but we hadn’t seen that in inflation-adjusted terms for quite a long time. We will get back there, for sure.”

Fuel prices in America on Monday are at an average of $4.04, according to AAA.

The highest average prices come in the coastal states, the only places where gas is over $4, while the midwest states have the lowest averages in the low-to-mid 3s.

| Ticker | Security | Last | Change | Change % |

|---|---|---|---|---|

| CHEV | CHARGING ROBOTICS INC | 3.3 | +0.80 | +32.00% |

| SUN | SUNOCO | 63.05 | -1.49 | -2.31% |

| XOM | EXXON MOBIL CORP. | 146.44 | -5.54 | -3.65% |

| CVX | CHEVRON CORP. | 183.99 | -4.16 | -2.21% |

| SHEL | SHELL PLC | 87.81 | -3.69 | -4.03% |

| DINO | HF SINCLAIR | 57.15 | -2.96 | -4.92% |

BESSENT RULES OUT GOVERNMENT INTERVENTION IN OIL FUTURES MARKET DURING IRAN WAR

Trump had long warned that the rise in American gas prices at the pump was a transitory inflation issue on the expectation that global oil supply was strained due to Iran’s retaliatory choking off of oil flowing through the Strait of Hormuz.

Trump and Treasury Secretary Scott Bessent have also noted for weeks that the U.S. is a net exporter of oil, has plenty of supply, with only a fraction of oil from the Middle East. So when local gas stations raised prices under the fear of future supply shortages elsewhere around the globe — potential “bad actors,” according to Bessent — they were not only guessing, but expecting something that would never come, they argued.

“We’ll be looking at Treasury to try to keep the retail gas stations honest — that you did this on the way up, better be doing this on the way down,” Bessent told the CNBC Invest in America Forum last week. “And I am sure the president will call out anyone who’s a bad actor.”

Former U.S. Energy Secretary Dan Brouillette joins ‘Varney & Co.’ to break down the global oil supply shock driving gas prices higher, weigh in on when relief could come at the pump and slam Democratic energy policies.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

What went up, must now come down, Bessent told the CNBC forum host Wednesday when asked if the above was a warning.

“I’m sure that,” Bessent said with a calculated pause, “everyone will be a good actor.”

Businesses can apply online through a portal for refunds expected to total $160bn.

Nicolae Popescu/iStock via Getty Images

The iShares MSCI Global Metals & Mining Producers ETF (PICK) is a passively managed exchange-traded fund designed to track companies that participate in mining, extraction, or the production of industrial and base metals, excluding precious metals exposure. The strategy is regionally diversified and provides exposure across a number of different metals, including copper, iron & steel, and aluminum, amongst other materials. The strategy can be utilized by investors seeking diversified exposure to commodity producers and their respective cash flows in relation to the price of the commodities produced.

About iShares MSCI Global Metals & Mining Producers ETF

PICK was launched by iShares on January 31, 2012 on the Cboe BZX Exchange. PICK has a net expense ratio of 39bps, a relatively low cost strategy when compared to most peer ETFs.

Seeking Alpha

PICK exhibits substantial depth, though thin liquidity with $1.9b in net assets and a 30-day average trading volume of 538k shares. As a result of the lower liquidity, PICK exhibits a relatively wide 30-day median bid/ask spread of 0.18%, potentially adding additional fees when actively traded.

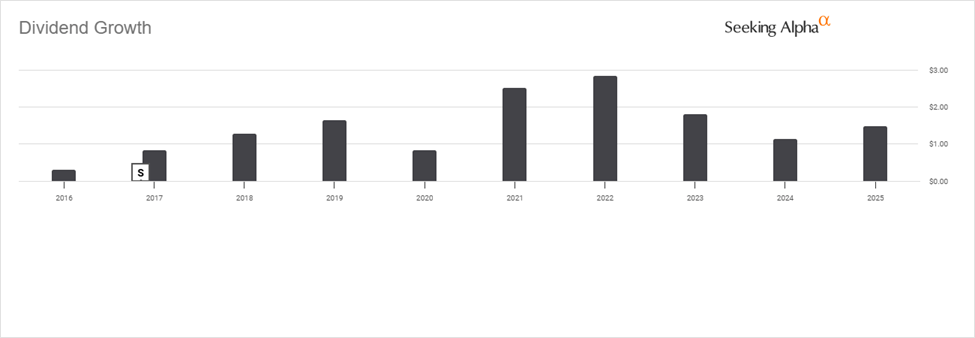

PICK pays out a semiannual distribution at an annualized rate of $1.28/share over the last twelve months, yielding 2.04%. Distributions can vary widely from period to period, making this strategy most appropriate for capital appreciation rather than income.

Seeking Alpha

PICK was designed to track the MSCI ACWI Select Metals & Mining ex Gold ex Silver Investable Market Index, which tracks the performance of companies that participate in industrial and the rare earth metals market. The Index consists of 234 constituents with exposure to small- through large-cap producers; the Index has a median constituent market capitalization of $1.21b with the largest constituent having a market capitalization of $175b. The Index is reviewed on a quarterly basis.

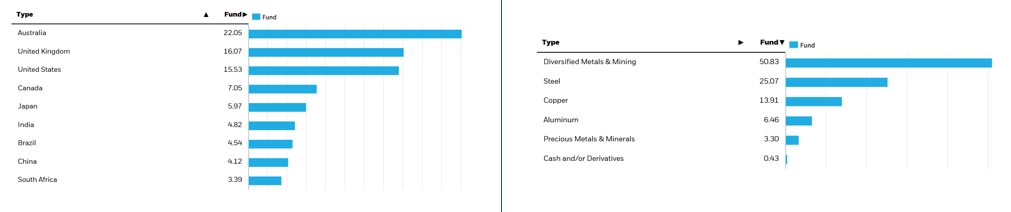

PICK currently invests across 244 holdings, which consist of equities as well as some exposure using futures derivatives. The ETF primarily invests in diversified metals & mining companies, making up 51% of the total portfolio weight, followed by steel at 25%, and copper at 14%. The strategy is regionally diversified with Australia accounting for 22% of regional exposure. Other regions include the UK at 16%, the US at 15.53%, and Canada at 7%.

Corporate Filings

The top 10 holdings within PICK account for 46% of the total portfolio’s assets. In contrast, the bottom 10 holdings account for roughly 0.12%. Top holdings within the ETF include BHP Group (BHP) at 12.30%, Rio Tinto PLC (RIO) at 6.80%, Freeport-McMoran (FCX) at 5.93%, and Glencore PLC (GLEN) at 4.55%.

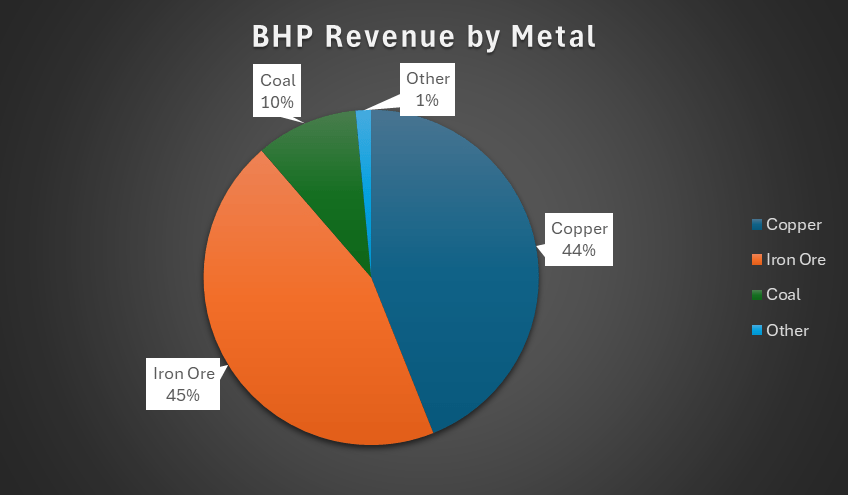

BHP is an Australia-based diversified mining enterprise, primarily producing copper and iron ore at the global scale.

Corporate Filings

Freeport-McMoran is a US-based copper producer, operating globally in mining and refining.

Thematically, the metals & mining sector can be viewed through a variety of lenses. For copper, a major theme to consider is the increasing investments in power infrastructure and data centers, each requiring vast amounts of copper to operate. Iron exhibits broadly diversified themes, including automobile production, industrial manufacturing, power, and construction, amongst others. Sector demand can vary by region; the US may exhibit a larger focus in the automotive industry whereas China may exhibit more steel utilization in construction. Being mindful of macroeconomic trends like annual vehicle production, trucking, and construction starts may be useful indicators for assessing this component of the portfolio.

Some other factors investors may consider when investing in the strategy include international trade. For example, China has historically been a major counterparty to BHP’s iron ore mining operations. For example, Chinese imports accounted for roughly 63% of BHP’s sales in FY25. Trade disputes between the two countries could significantly impact operations and must be taken into consideration when evaluating PICK as an investment, particularly given the portfolio concentration in BHP.

Another factor to consider is trade tariffs. For example, Alcoa’s (AA) business has been impacted in the last year resulting from the 50% duty on imported aluminum and steel. Alcoa has historically imported aluminum into the US through Canada, resulting in mismatched economics throughout FY25 before the Midwest Spread created a marketable opportunity. Alcoa holds a much lower weight in the strategy at 1.10% of net assets, though I believe the theme can apply to all constituents if import duties were to persist.

Overall, PICK can be considered as both a microeconomic and macroeconomic investment strategy given the ETF’s global footprint and general demand across regions and industries. At the microeconomic level, more efficient mining practices and ESG policies can influence the cost of production, or the all-in cash cost.

Investor Suitability

PICK can be utilized by investors seeking a diversified equity strategy tied to the global metals & mining industry. PICK may be best utilized as a buy-and-hold ETF given its relatively light trading volumes. PICK may also be utilized as part of an industry rotation or a macroeconomic strategy given the diverse portfolio of commodity producers. In terms of growth expectations in the fund, a benefit of owning the commodity producers over the commodities outright is that commodity producers gain exposure to stronger commodity prices, cost management, and cash flow generation; owning a portfolio of commodities is limited to the aggregate increase in commodity prices with no additional economic upside potential.

Risks Related to PICK

PICK may expose investors to a variety of risks that should be considered prior to making an investment decision, particularly when considering its global exposure. International trade, geopolitical risk, war, ESG policies, inflation rates, commodity prices, fuel costs, transportation costs, and interest rates can all influence the performance of the underlying companies within the portfolio.

Final Thoughts

PICK can be utilized as a diversified metals & mining investment strategy for investors seeking to participate in the cash flows earned by companies with direct exposure to industrial and base metals. I believe PICK offers investors greater value over investing in a commodity-based portfolio given that the producers provide more economic upside beyond the commodity price. Given the international footprint of the portfolio, investors must consider international trade risk when evaluating whether a broad strategy is appropriate for their investment needs.

This article answers three main questions about PICK:

- What type of investor is PICK most suitable for?

- Does PICK offer diversification to foreign companies?

- Is PICK considered an income ETF or is it focused more on capital appreciation?

Form 6K YY Group Holding Ltd For: 20 April

Check out what’s clicking on FoxBusiness.com.

Macy’s is recalling thousands of Arch Studio tea kettles after federal safety officials warned of a potential burn hazard tied to the product.

The recall, announced April 16 by the Consumer Product Safety Commission (CPSC), affects approximately 4,600 units, according to the agency.

Officials said the tea kettle’s handle can detach during use when heated, posing a risk of serious injury due to burns. The company has received three reports of the handle detaching, though no injuries have been reported.

POPULAR BABY FOOD BRAND HIT BY ‘CRIMINAL ACT’ AS RAT POISON FOUND IN SEIZED JAR

“Arch Studio” and “HJ10525” are etched on the underside of the recalled kettles. (CPSC)

The recall applies to Arch Studio-branded stainless-steel tea kettles with a black handle and a 1.9-quart capacity. The kettles measure about 10.7 inches long, 7.59 inches wide and 8.62 inches high, with “Arch Studio” and model number “HJ10525” etched on the underside.

CPSC says the tea kettle’s handle can detach during use when heated. (CPSC)

The products were sold at Macy’s stores nationwide and online at macys.com from August 2025 through February 2026 for about $50, according to the CPSC. The kettles were imported by Macy’s Merchandising Group Inc. of New York and manufactured in China.

| Ticker | Security | Last | Change | Change % |

|---|---|---|---|---|

| M | MACY’S INC. | 19.54 | +0.46 | +2.41% |

Consumers are urged to stop using the recalled kettles immediately and contact Macy’s for a full refund. The company is offering refunds by check, and customers will be provided with a prepaid shipping label to return the product. No purchase receipt is required.

CLICK HERE TO GET FOX BUSINESS ON THE GO

Macy’s did not immediately respond to FOX Business’ request for comment.

Politics38 seconds ago

Mandelson process ‘beggars belief’: Keir Starmer’s statement to parliament in full

Sports2 minutes ago

Snooker needs new faces and personalities – teenager Moody

Tech3 minutes ago

When it comes to leadership, do companies know what they are doing?

-

Crypto World7 days ago

Crypto World7 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

NewsBeat6 days ago

NewsBeat6 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Theodora Dress

-

Crypto World7 days ago

Crypto World7 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

News Videos5 days ago

News Videos5 days agoSecure crypto trading starts with an FIU-registered

-

Sports3 days ago

Sports3 days agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Crypto World6 days ago

Crypto World6 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

Business1 day ago

Business1 day agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Crypto World3 days ago

Crypto World3 days agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Politics3 days ago

Politics3 days agoPalestine barred from entering Canada for FIFA Congress

-

Business4 days ago

Business4 days agoCreo Medical agree sale of its manufacturing operation

-

Politics1 day ago

Politics1 day agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Entertainment7 days ago

Entertainment7 days agoBrand New Day’ Footage Reveals the Devastating Impact of ‘Now Way Home’

-

Crypto World3 days ago

Crypto World3 days agoRussia Introduces Bill To Criminalize Unregistered Crypto Services

-

Tech6 days ago

Tech6 days agoMicrosoft adds Windows protections for malicious Remote Desktop files

-

Entertainment7 days ago

Entertainment7 days agoKarol G’s ‘Ultra Raunchy’ Coachella Set Gave ‘Satanic Vibes’

-

Entertainment7 days ago

Entertainment7 days agoHow Babylon 5 Turned Brief Side Story Into Emotional Masterpiece

-

Crypto World7 days ago

Crypto World7 days agoSenate Bill Faces Delay Over Stablecoin Yield Debate

-

Tech7 days ago

Tech7 days agoWhat was the first ransomware attack to demand payment in Bitcoin?

-

Tech5 days ago

Tech5 days ago‘Avatar: Aang, The Last Airbender’ Leaked Online. Some Fans Say Paramount Deserves the Fallout

You must be logged in to post a comment Login