Business

Chemed Stock Jumps 11% on Q1 Beat, VITAS Hospice Strength and Raised 2026 Outlook

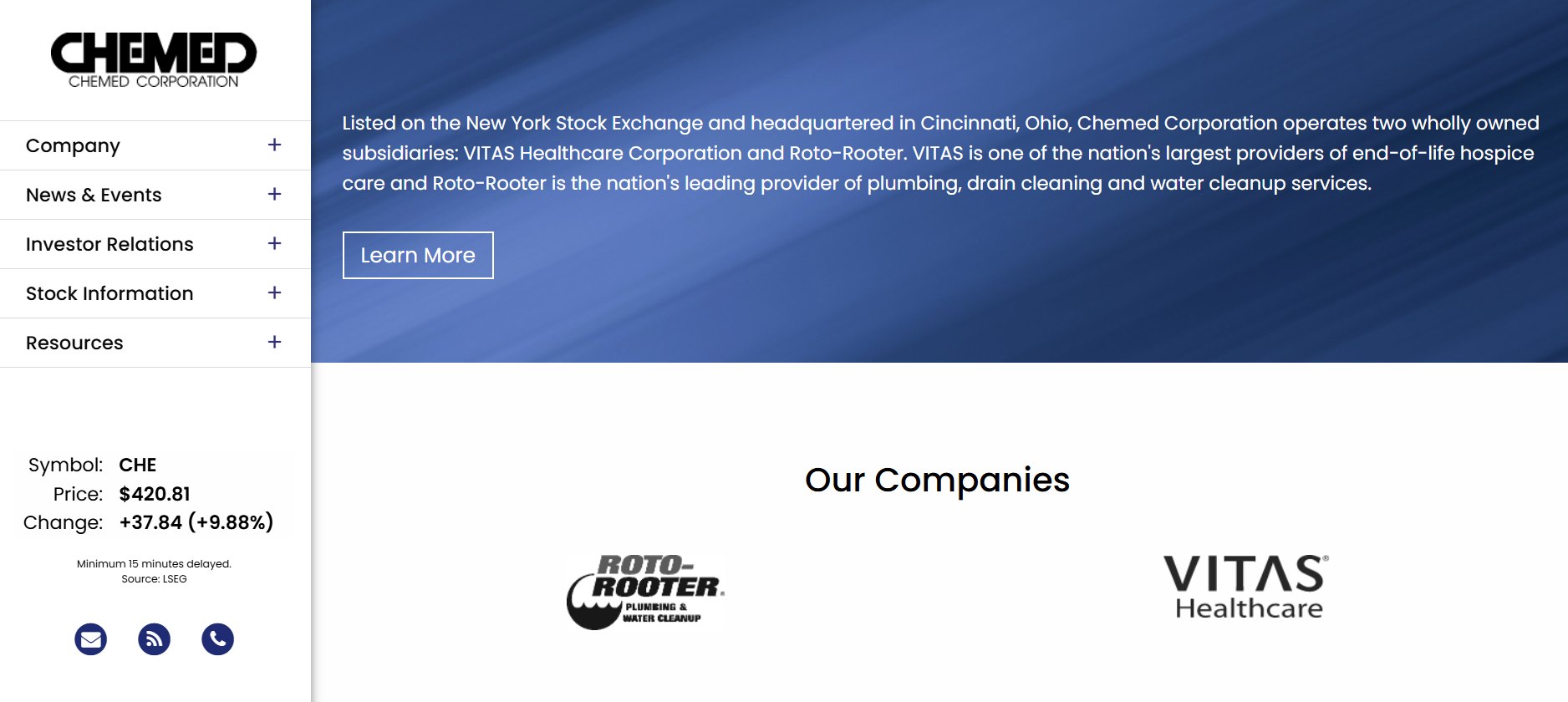

CINCINNATI — Chemed Corp. shares soared more than 10% in midday trading Friday, climbing to around $424 after the healthcare services company delivered a solid first-quarter 2026 earnings beat, highlighted by strong performance at its VITAS hospice business and an upgraded full-year outlook that exceeded Wall Street expectations.

The stock (NYSE: CHE) opened sharply higher and sustained robust gains on April 24, with trading volume well above average. The move reflects investor relief and enthusiasm following Chemed’s report late Thursday, which showed resilience in its core end-of-life care operations amid a challenging environment for Medicare-funded services.

Chemed reported first-quarter revenue of $657.5 million, up 1.6% year-over-year and slightly ahead of analyst estimates around $649.8 million to $656.3 million. Adjusted diluted earnings per share reached $5.65, beating consensus forecasts of approximately $5.30 to $5.36. GAAP net income stood at $66.3 million, or $4.84 per share.

VITAS Healthcare, the nation’s largest provider of hospice services, drove much of the positive momentum. Net patient revenue rose 3.1% to $420 million, supported by an average daily census of 22,723 patients. Management noted improving admission trends and effective cost management despite ongoing Medicare rate pressures.

Roto-Rooter, Chemed’s plumbing and drain cleaning segment, delivered steady results with margins holding up well despite higher marketing investments. The dual-business model — combining stable healthcare cash flows with cyclical but high-margin service operations — continues to provide resilience.

Chemed raised its full-year 2026 adjusted EPS guidance to $24.00–$24.75 from the previous range of $23.25–$24.25. The midpoint represents roughly 13% growth over 2025 levels, signaling management’s confidence in sustained VITAS recovery and operational efficiencies.

CEO Kevin McNamara emphasized disciplined capital allocation during the earnings call. The company repurchased 500,000 shares for $197.7 million in the quarter at an average price of $395.36, demonstrating confidence in its valuation. Approximately $229.6 million remains under the current repurchase authorization.

Wall Street reacted positively to the beat-and-raise. Several analysts noted the stronger-than-expected VITAS trends as a key positive, helping alleviate concerns from prior quarters. Price targets have edged higher, though the stock’s valuation remains premium given its defensive healthcare exposure and consistent cash generation.

Chemed operates two distinct but complementary businesses. VITAS provides end-of-life care across 17 states and the District of Columbia, serving patients through interdisciplinary teams focused on comfort and quality of life. Roto-Rooter offers essential plumbing, drain, and excavation services through company-owned and franchise locations nationwide.

The company has long maintained a reputation for conservative management and shareholder-friendly policies, including regular share repurchases and a modest dividend. Its balance sheet remains solid with low leverage, providing flexibility for both organic growth and potential acquisitions.

Analysts view Chemed as a defensive play with growth potential. Demographic tailwinds in an aging U.S. population support long-term hospice demand, while Roto-Rooter benefits from consistent home maintenance needs. However, Medicare reimbursement rates and regulatory changes in healthcare remain ongoing watch items.

Friday’s surge marks a notable rebound and pushes shares toward recent highs. Year-to-date performance had been relatively muted before the earnings catalyst, making the double-digit move particularly eye-catching in a mixed broader market session.

For investors, Chemed offers exposure to stable, recession-resistant businesses with strong free cash flow characteristics. The company’s ability to generate consistent earnings and return capital through buybacks has historically appealed to value-oriented and income-focused portfolios.

Challenges include labor costs in healthcare, inflationary pressures on Roto-Rooter operations, and potential policy shifts affecting Medicare Advantage and hospice margins. Management has demonstrated skill in navigating these dynamics through pricing discipline and operational improvements.

As trading continued Friday afternoon, CHE shares consolidated some gains but remained firmly positive with elevated volume. The reaction underscores the market’s appreciation for companies that deliver reliable results and raise guidance in an uncertain economic environment.

Looking ahead, Chemed will focus on executing its expanded guidance while continuing share repurchases and investing in capacity where appropriate. The second half of 2026 will test whether recent VITAS momentum sustains amid any broader healthcare funding pressures.

The impressive intraday surge highlights Chemed’s appeal as a steady compounder with defensive qualities. With a strong balance sheet, improving operational trends and shareholder-friendly capital allocation, the company continues to navigate its dual-business model effectively in 2026.

SAN ANTONIO — Victor Wembanyama remains in the NBA’s concussion protocol and is listed as questionable for Friday’s Game 3 against the Portland Trail Blazers, though the Spurs phenom traveled with the team to Portland as he continues progressing through league-mandated steps following a scary head injury in Game 2.

The 22-year-old Defensive Player of the Year suffered the concussion in Tuesday’s 106-103 loss when he was fouled by Jrue Holiday, tripped while driving to the basket and fell hard, hitting his jaw and face on the court. He appeared dazed, left the game early in the second quarter and did not return as the series evened at 1-1. Spurs coach Mitch Johnson confirmed the diagnosis immediately after the game.

Wembanyama reported to the Spurs’ practice facility Wednesday for light cardio work without worsening symptoms and returned Thursday for further evaluation. He was cleared to travel with the team for Games 3 and 4 this weekend in Portland, a positive development that signals stabilization. However, he cannot engage in unrestricted basketball activity until he completes multiple cognitive, neurological and exertion tests under medical supervision.

NBA concussion protocol requires a minimum 48-hour period before full participation can be considered, along with a graduated return-to-play process monitored by team doctors and league specialists. The median absence for concussions in the NBA is approximately seven to nine days, though some players recover faster and others take longer to ensure full safety.

Coach Mitch Johnson described Wembanyama as “progressing” on Thursday but stopped short of confirming availability for Game 3. “We’ll see how he feels and continue to follow the protocol,” Johnson said. The team is preparing as if he may not play, leaning on its young core including De’Aaron Fox, Keldon Johnson and Stephon Castle to compete on the road.

Wembanyama’s absence was noticeable in Game 2. He had dominated Game 1 with a franchise playoff debut record of 35 points, showcasing the length, shot-blocking and perimeter skills that make him a generational talent. Without him, Portland exploited interior gaps and rallied late behind Scoot Henderson’s strong performance.

Medical experts emphasize caution with young stars. A second concussion in quick succession carries amplified risks, and studies show elevated chance of musculoskeletal injuries in the 90 days following a head injury. The Spurs, known for conservative player management, are prioritizing long-term health over short-term playoff urgency.

Game 3 tips off Friday night at Moda Center in Portland. Even if Wembanyama is cleared, many insiders view participation as unlikely given the timeline and the organization’s approach. A return for Game 4 on Sunday or Game 5 back in San Antonio appears more realistic if symptoms continue to improve.

The series backdrop adds pressure. The Spurs earned the No. 2 seed in the West and returned to the playoffs for the first time since 2019 largely thanks to Wembanyama’s meteoric rise. His playoff debut already created franchise lore, but the injury tests San Antonio’s depth and resilience in what many viewed as a winnable first-round matchup.

Portland senses an opening. With home-court energy and experience, the Trail Blazers will look to capitalize on the Spurs’ temporary vulnerability. A win in Game 3 could shift momentum dramatically toward an upset.

Fan reaction has been overwhelmingly supportive, with calls for caution dominating social media. Supporters emphasize protecting the franchise cornerstone over rushing him back. The organization has echoed that sentiment, stressing that Wembanyama’s long-term health remains the priority.

Wembanyama has shown eagerness throughout the process, reporting to the facility daily and pushing to travel. His competitive drive is well-documented, but medical staff hold final say. Further evaluations in Portland will determine the next steps in his recovery.

Broader NBA concussion management has evolved with greater emphasis on safety. The league’s protocol includes baseline testing, independent neurological oversight and a step-by-step return process. Teams increasingly err on the side of caution with young stars, understanding the risks of repeated head trauma.

For the Spurs, navigating the series without their best player tests coaching ingenuity and depth. Home-court advantage from the regular season provides a cushion, but extending the series without Wembanyama would strain resources ahead of a potential second-round matchup.

As Game 3 approaches, pregame updates will provide the latest clarity. Whether Wembanyama suits up or watches from the sideline, his presence looms large over the series. The basketball world watches closely as the Spurs push forward in what promises to be a memorable postseason.

Wembanyama’s rapid ascent since being drafted No. 1 overall in 2023 has captivated fans globally. This early playoff injury tests both his resilience and the Spurs’ ability to compete at the highest level without their transcendent talent. For now, cautious optimism prevails as the organization balances competitiveness with care for its cornerstone.

Pinnacle Financial Partners: Post-Merger Goals Are On Track

TORONTO — POET Technologies Inc. shares surged more than 30% in midday trading Friday, climbing to around $15.33 as investors piled into the photonics innovator amid accelerating AI-driven demand for its optical interconnect technology and positive updates on financing and strategic positioning.

The stock (NASDAQ: POET) opened sharply higher and sustained strong gains on April 24, with trading volume exploding well above average. The dramatic move extends a powerful rally that has seen shares more than double in recent weeks, driven by growing excitement around POET’s role in solving critical data transfer challenges in next-generation AI systems.

POET Technologies develops photonic integrated circuits and optical engines designed to move data at dramatically higher speeds and lower power consumption than traditional copper-based solutions. Its technology is particularly relevant for AI infrastructure, where hyperscale data centers require ultra-fast, energy-efficient optical connections between chips and servers.

Recent catalysts have fueled the surge. The company has secured significant orders linked to major players, including connections through Marvell Technology following its acquisition of Celestial AI. POET’s chief financial officer Thomas Mika confirmed progress on these fronts in recent interviews, noting strong customer validation and production ramps.

POET also raised substantial capital recently — more than $225 million in Q4 2025 plus an additional $150 million in early 2026 — building a robust war chest of approximately $430 million. This financial strength positions the company to scale manufacturing and pursue commercial opportunities aggressively.

The company is advancing plans to redomicile its headquarters to the United States, a move intended to simplify tax structures for American investors and mitigate Passive Foreign Investment Company (PFIC) concerns raised in a recent short-seller report. POET’s management responded forcefully to the report, providing clarity on QEF elections and calling many allegations a “nothing burger.”

Analysts and retail investors have embraced the AI optics narrative. POET’s hybrid integrated photonics platform aims to address the “laser problem” in AI hardware by enabling more efficient light-based data transmission. As AI models grow larger and data center power demands escalate, optical solutions like POET’s are gaining traction as a potential differentiator.

The stock’s momentum has been amplified by heavy options activity, with call volumes far outpacing puts in recent sessions. This speculative fervor echoes earlier meme-like runs but is increasingly underpinned by tangible business progress, including design wins and partnerships in the optical communications space.

POET reported its Q4 2025 results in early April, showing a narrower net loss and progress on commercialization. While revenue remains modest as the company transitions from development to execution, management expressed confidence in scaling production and securing additional hyperscaler customers.

Challenges persist. POET is still pre-revenue at meaningful scale, faces execution risks in ramping manufacturing, and operates in a highly competitive sector dominated by larger players. Short-seller scrutiny highlighted governance and tax issues, though the company’s proactive responses appear to have reassured many investors.

Wall Street coverage remains limited but generally constructive on the long-term opportunity. Price targets vary widely, reflecting the speculative nature of the stock, but recent momentum has pushed sentiment higher. The company’s market capitalization has grown rapidly but remains modest relative to the potential addressable market in AI infrastructure.

For investors, POET represents a high-risk, high-reward bet on the optical revolution in AI. Supporters point to the technology’s differentiation, strong balance sheet and timing with massive data center buildouts. Skeptics caution about dilution risks, execution hurdles and the company’s history of volatility.

As trading continued Friday afternoon, POET shares held most of their gains amid elevated volume. The surge stands out even in a broader semiconductor rally, highlighting investor appetite for pure-play AI infrastructure stories.

Looking ahead, key milestones include production ramps, additional customer announcements and progress on the U.S. redomicile. The company’s next earnings report in May will be closely watched for updates on commercialization timelines and cash utilization.

POET Technologies’ rapid rise underscores the market’s fascination with innovative solutions to AI’s physical constraints. Whether the company can translate technological promise into sustained commercial success remains the central question, but Friday’s move shows investors are increasingly willing to bet on that potential.

US-Kuwaiti journalist leaves Kuwait after release from detention, US official says

Bertina Engelbrecht

CEO & Executive Director

Good afternoon. Thank you for joining the webcast of our Interim Results for the 6 months ended 28th February 2026. I’m Bertina Engelbrecht, Chief Executive Officer of the Clicks Group. I am joined by Gordon Traill, our Chief Financial Officer, who is in a completely different time zone. Gordon and I will take you through the presentation of our interim results, and we’ll respond to any questions you may have after the conclusion of our presentation.

This slide sets out the outline of our presentation. I will, as usual, kick off with a review of our performance of the past 6 months. Gordon will then present an overview of the financial results. I will walk you through the trading performances of our operating business units, starting with Clicks, followed by UPD. And I will then close with the outlook for the group.

Please feel free to submit any questions you may have via the webcast platform during or after the conclusion of our presentation. Sue Hemp will read out your questions to which Gordon and I will respond.

I will now take you through the review of the period. It has been a tough 6 months. Despite some interest rate relief and signs of a slow recovery in the economic environment, trading conditions remain constrained, especially for middle-income households. Competition intensified as new players entered the market. Traditional players extended into health and beauty categories, giving rise to heightened levels of promotions aimed at capturing a greater share of the consumer’s wallet.

CUPERTINO, Calif. — Apple is closing in on its long-awaited entry into the foldable smartphone market, with the latest rumors pointing to a September 2026 launch for the iPhone Fold alongside the iPhone 18 Pro models and a revolutionary crease-free design that could set a new standard for the category.

After years of speculation and multiple delays, credible reports now suggest Apple’s first foldable device is firmly on track for a fall 2026 debut. Trial production has reportedly begun at Foxconn, with mass production potentially starting as early as July, putting the device on a timeline similar to previous Pro models. While some earlier concerns about manufacturing snags had raised questions about a possible slip into 2027, recent updates from Bloomberg’s Mark Gurman and Chinese leakers indicate the project remains on schedule.

The device, widely referred to in leaks as the iPhone Fold (though Apple is unlikely to use that exact name), is expected to feature a book-style folding mechanism rather than a clamshell flip design. When closed, it will sport a compact approximately 5.5-inch outer display, making it one of Apple’s smallest modern iPhones. When unfolded, it opens into a tablet-like 7.8-inch inner screen with a wider 4:3 aspect ratio reminiscent of the iPad mini.

One of the most exciting rumored features is Apple’s aggressive approach to the infamous foldable crease. Multiple sources claim the iPhone Fold will feature a nearly invisible or dramatically reduced crease — potentially as shallow as 0.15mm — thanks to advanced hinge technology using liquid metal alloys and specialized display layers. This would represent a significant leap over current competitors like Samsung’s Galaxy Z Fold series.

Design leaks and alleged dummy models shared by reliable sources in recent weeks show a sleek, premium build with a titanium frame for durability and strength at thin dimensions. The device is expected to measure roughly 9.5mm thick when folded and an ultra-slim 4.5mm when opened. Apple is reportedly prioritizing a premium feel, with potential color options in black and white and a focus on minimal bezels.

Camera expectations are more conservative than current iPhone Pro models. Rumors point to a dual 48-megapixel rear setup and dual front cameras (one for each display orientation), with some reports suggesting an under-display selfie camera on the inner screen. Face ID may be replaced by a side-mounted Touch ID button to help maintain the slim profile.

Power and performance details remain sparse but promising. The iPhone Fold is tipped to feature Apple’s A20 Pro chip built on a 2nm process, paired with up to 12GB of RAM. Battery capacity rumors range from 5,088mAh to as high as 5,800mAh — potentially the largest ever in an iPhone — to support the dual displays and power-hungry multitasking features expected in a future iOS version optimized for foldables.

Pricing speculation centers around a premium positioning. Analysts expect the iPhone Fold to start at $2,000 or higher, significantly above even the iPhone 18 Pro Max. This ultra-premium tag could limit initial volumes but would boost Apple’s average selling price and help justify the heavy investment in foldable technology.

The software experience will be critical. iOS 27 is expected to bring enhanced multitasking, split-screen capabilities, and app continuity features tailored for the larger inner display. Developers are already preparing for the new form factor, though full optimization may take time after launch.

Supply chain reports indicate Samsung Display is providing the foldable panels, with trial production underway. Any last-minute issues could still push shipments into October or December, following a September announcement alongside the standard iPhone 18 lineup. Apple has used staggered release strategies before, such as with the original iPhone X.

The foldable iPhone represents a major evolution for Apple after more than a decade dominating the traditional slab smartphone market. It would directly challenge Samsung’s dominance in foldables while opening new use cases for productivity, media consumption and creative work on iOS. Success could expand Apple’s addressable market significantly, though high pricing and the learning curve for foldable usage remain potential hurdles.

Industry observers are watching closely as Apple’s entry could validate and accelerate the entire foldable category. Competitors are already ramping up their own efforts in anticipation. For consumers, the iPhone Fold could finally deliver the seamless blend of phone and mini-tablet that many have been waiting for.

As development continues through the summer, more concrete details and potentially official teaser imagery could emerge. For now, the latest rumors paint an exciting picture of Apple’s most ambitious iPhone yet — one that could redefine the company’s flagship lineup for years to come. Whether the crease-free promise holds up in real-world use will be one of the biggest questions when the device finally arrives.

Netlist director Jun Cho sells $41,600 in company stock

Texas finds Camp Mystic’s flood emergency plan deficient for reopening

Justin Law has a Ph.D in Chemistry from Rice University and has earned the CFA Institute Investment Foundations certificate. He applies his knowledge to deep value and dividend paying stocks.Justin is a contributor to the investing group The Dividend Kings where he curates the Dividend Champions list, a monthly publication of companies with a history of consistently increasing their dividends. The Dividend Kings is a group of analysts teaching individuals how to invest more wisely in dividend stocks. Learn More.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of O, BMY, GIS, VZ either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Tom de Swaan

Ladies and gentlemen, dear shareholders and depository receipt holders, I’m pleased to open this meeting. Welcome to this General Meeting of Shareholders. As usual, I’ll tell you everybody who is present on behalf of the bank. And on behalf of the Supervisory Board, the entire Supervisory Board is present. I’m the Chairman. To my left is Michiel Lap is Vice Chair of the Supervisory Board and Chair of the Risk and Capital Committee. This is Laetitia Griffith, Daniel Hartert, Mariken Tannemaat; Sarah Russell, who chairs the Audit Committee; Femke de Vries as Chair of the Supervisory Sustainability Committee; and myself, I’m the Chair of the Supervisory Board and also of the Selection and Nominations Committee.

On behalf of the Executive Board, the following Board members are present. Some are facing you on the stage, others are elsewhere in the room. To my right is Marguerite Berard, CEO; Ferdinand Vaandrager, CFO; Serena Fioravanti, Chief Risk Officer. In the — elsewhere in the room, Carsten Bittner, CI&TO; Dan Dorner, the Head of our Corporate Banking; Choy van der Hooft-Cheong, Head of Wealth Management; and of course, Annerie Vreugdenhil, Head of Personal and Business Banking.

The Secretary to this meeting is, as usual, Hanneke Dorsman to my left, General Counsel and ABN AMRO Company Secretary. On behalf of E&Y, our auditor, Hanneke Overbeek who is present. And on behalf of the Employee Council, Arlene Bosman. Welcome, Arlene.

We have civil law notary Bart Jan Kuck from Zuidbroek present to supervise the correct conduct

Star in Concussion Protocol After Hard Fall

Microsoft-backed Space and Time targets no-code Web3 apps

Oscar De La Hoya admits he would consider comeback under one condition

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business5 days ago

Business5 days agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Politics6 days ago

Politics6 days agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Entertainment5 days ago

NBA Analyst Charles Barkley Chimes in on Ice Spice McDonald’s Fiasco

-

Tech6 days ago

Tech6 days agoAuto Enthusiast Scores Running Tesla Model 3 for Two Grand and Turns It Into Bare-Bones Go-Kart

-

Politics4 days ago

Politics4 days agoGary Stevenson delivers timely reminder to register to vote as deadline TODAY

-

Politics2 days ago

Politics2 days agoMaking troops accountable for war crimes threatens US alliance, ex-SAS colonel warns

-

Politics2 days ago

Politics2 days agoDisabled people challenge government SEND proposals over segregation concerns

-

Fashion8 hours ago

Fashion8 hours agoWeekend Open Thread – Corporette.com

-

Business3 days ago

Business3 days agoRolls-Royce Voted UK’s Most Iconic Trade Mark as IPO Register Hits 150

-

Politics2 days ago

Politics2 days agoZack Polanski responds to home secretary’s taser threat

-

Politics2 days ago

Wings Over Scotland | How To Get Away With Crimes

-

Politics2 days ago

Politics2 days agoStarmer handler McSweeney to be dragged from shadows by Foreign Affairs Committee

-

Crypto World6 days ago

Crypto World6 days agoKelp DAO rsETH Bridge Hack Drains $292M as DeFi Losses Top $600M in Two Weeks

-

Politics2 days ago

Politics2 days ago‘Iran is still a nuclear threat’

-

Crypto World3 days ago

Crypto World3 days agoNew York sues Coinbase, Gemini over prediction market offerings

-

Business3 days ago

Business3 days agoThe Job Benefits Most Men Don’t Know to Negotiate

-

Crypto World16 hours ago

Crypto World16 hours agoMichael Saylor says BTC winter is over. Market analyst disagrees, says bitcoin was in a pullback

-

Politics5 days ago

Politics5 days agoReform investigating candidate who ‘hates’ the NHS

-

Crypto World5 days ago

Crypto World5 days agoBitcoin, ether, solana slide, oil jumps on renewed U.S.-Iran war risks

-

Crypto World6 days ago

Nasdaq Rally Extends to 13 Days as Call Options Volume Nears Record High Levels

You must be logged in to post a comment Login