Crypto World

SoFi’s crypto relaunch brought in $121.6 million in Q1. Almost all of it went to costs

Nationally chartered U.S. bank SoFi’s relaunched crypto business generated $121.6 million in crypto transaction revenue in the first quarter, its first granular disclosure of the unit’s economics since the bank returned to the cryptocurrency space late last year.

That revenue was almost entirely offset by $120.7 million in related transaction costs, leaving just $852,000 in net crypto transaction revenue, according to the company’s latest quarterly filing.

The company reported earnings of $0.12 per share on a GAAP basis, or about $0.13 on an adjusted basis, up from $0.06 a year earlier.

SoFi said it records crypto transactions on a gross basis because it acts as principal, buying crypto from or selling it to third-party liquidity providers before transferring it to or from customer accounts. The structure appears similar to a brokerage model, where the platform intermediates trades rather than taking directional risk.

The company reported “239,509 crypto accounts” as of March 31, a metric that captures the total number of accounts opened through its platform, rather than active traders.

The figures give the first public read on SoFi’s crypto business since its in-app trading launch in November.

SoFi had outlined its return to crypto in June, with plans for crypto investing and blockchain-based remittances..

SoFi said that the GENIUS Act would require it to migrate SoFiUSD to a “separately licensed or regulated entity.” SoFi launched SoFiUSD in December as a stablecoin for enterprise payments.

The company said in the filing that it began minting SoFiUSD in the first quarter and entered a partnership with Mastercard to support future settlement capabilities across the card network.

SoFi said its own crypto holdings remain immaterial and are held as incidental inventory for operations, not as long-term investments.

TLDR

- Shopify Inc stock rose 3.55% on May 7 and outperformed the Software and IT Services sector, which gained 2.16%.

- The company exceeded analyst expectations for revenue and earnings per share in the first quarter of 2026.

- Gross Merchandise Volume remained above $100 billion for the second consecutive quarter.

- The stock initially declined after Shopify issued softer second-quarter revenue guidance.

- Market sentiment improved as investors reassessed the company’s overall financial strength and long-term strategy.

Shopify Inc (SHOP) stock rose 3.55% on May 7, outpacing the Software & IT Services sector, which gained 2.16%. The rally followed renewed focus on the company’s first-quarter 2026 earnings and strategic updates. Trading activity also highlighted strong turnover in Microsoft Corp, Palantir Technologies Inc, and Meta Platforms Inc.

Shopify Inc Stock Rebounds After Earnings Reassessment

Shopify released its Q1 2026 results on May 5 and exceeded analyst estimates for revenue and earnings per share. The company reported Gross Merchandise Volume above $100 billion for the second consecutive quarter. It also maintained healthy free cash flow margins and reported growth in Merchant Solutions revenue.

However, the stock declined on May 5 and May 6 after management issued softer second-quarter revenue guidance. Executives projected slower growth compared with the first quarter, which prompted short-term selling pressure. Despite that reaction, the May 7 rebound indicated that traders reassessed the guidance in context with overall performance.

Shopify highlighted higher AI-driven order volumes during the quarter, reflecting expanded product capabilities. The company also continued to grow its fintech offerings and international operations. Management emphasized disciplined cost control and sustained margin performance during its earnings call.

Sector Performance and Market Activity Support Gains

The broader Software & IT Services sector advanced 2.16% during the same session. Microsoft Corp climbed 2.76%, while Palantir Technologies Inc gained 4.58%. Meta Platforms Inc added 1.66%, placing them among the top three stocks by turnover in the sector.

Analysts responded to the earnings report by adjusting certain price targets while maintaining favorable ratings. Several firms reiterated “Buy” or “Outperform” recommendations following the results. Consensus estimates still point to implied upside from current trading levels.

Institutional activity also drew attention during the week. Cathie Wood’s ARK ETFs purchased Shopify shares on May 5 and May 6. The company also has an authorized share buyback program, which signals management’s confidence in its capital position.

Shopify confirmed that Merchant Solutions revenue expanded year over year in Q1 2026. The company also reiterated its focus on scaling AI tools across merchant services. It reported that GMV exceeded $100 billion again, closing the quarter with steady operational metrics.

Crypto World

Ripple’s XRPL Linked to Interbank System in Major Pilot With JPMorgan, Mastercard, Ondo

Blockchain settlement rails are increasingly becoming intertwined with the global financial system. A group of firms recently achieved a feat that could introduce 24/7 settlements for traditional financial markets.

According to a tweet, the tokenization platform Ondo Finance, card services provider Mastercard, and JP Morgan’s blockchain platform, Kinexys, are involved in achieving the latest milestone. The companies successfully completed a pilot transaction that connected Ripple’s XRP Ledger (XRPL) with interbank settlement rails.

XRPL Linked to Interbank Settlement Rails

The pilot linked XRPL to global banking infrastructure, enabling institutions to execute cross-border transactions in a single, integrated flow. The assets used for the project were tokenized U.S. Treasury bills. The feat marked the first time tokenized Treasuries were settled across borders in near real time, outside traditional banking hours.

The process entailed Ondo processing Ripple’s redemption of the Ondo Short-Term U.S. Government Treasuries (OUSG) first. Mastercard routed instructions to Kinexys through its multi-token network, while JP Morgan delivered USD to Ripple’s Singapore bank account.

Completed in under five seconds, rather than the usual one to three business days, the pilot transaction highlighted a hybrid model in which XRPL handled the asset token movement while traditional banking rails facilitated fiat settlement.

“Tokenized assets are no longer separate from the global financial system. For the first time, a public blockchain and global banking infrastructure settled a cross-border transaction of a tokenized fund together in real time. Together, we’re laying the groundwork for 24/7 global markets that never close,” Ondo Finance stated.

The Rise of Tokenization on Wall Street

With Treasuries moving like crypto on settlement rails that do not have closing hours, the $30 trillion U.S. Treasury market could be opened to a new wave of investors. Multiple financial institutions, including Wall Street’s biggest firms, are already scrambling to get on this bandwagon.

Besides Treasuries, these institutions are also attempting to tokenize bonds and deposits. A few days ago, the Depository Trust & Clearing Corporation (DTCC) announced plans to launch a new tokenization service for bonds and Treasuries in October.

Meanwhile, the tokenized stocks sector has witnessed massive growth over the past year. In fact, the market cap of the tokenized real-world assets (RWAs) sector as a whole more than tripled from $5.42 billion to $19.32 billion in the last 15 months ending March 2026. The sector grew so well that it outperformed stablecoins.

The post Ripple’s XRPL Linked to Interbank System in Major Pilot With JPMorgan, Mastercard, Ondo appeared first on CryptoPotato.

Jack Dorsey’s payments firm Block rose 7.9% in after-hours trading as its Q1 earnings surpassed analyst estimates, despite posting its first loss in three years.

Block’s Q1 earnings came in at 85 cents per share, beating the Zacks consensus estimate of 68 cents per share. Investors responded positively, driving Block shares to $75.70 after hours, Google Finance data shows.

“This quarterly report represents an earnings surprise of +25.68%,” said Zacks Equity Research on Thursday. “Over the last four quarters, the company has surpassed consensus EPS estimates two times.”

Expanding Bitcoin’s use into the payments space has been a key area of focus for Dorsey, who previously argued that widespread payment adoption is needed to fulfill Satoshi Nakamoto’s original vision of Bitcoin as a peer-to-peer electronic cash system. In late April, Block noted that over 800,000 US-based merchants have enabled Bitcoin transactions for everyday purchases.

Block reports first quarterly loss in three years

The earnings beat came despite Block reporting its first quarterly loss since 2023, driven by a 23.8% drop in the price of Bitcoin over the three-month period.

Q1 net loss was $309 million, which included a $172.8 million bitcoin remeasurement loss on the 8,883 Bitcoin it held as of March 31.

Bitcoin revenue from Cash App and other Block products fell to $1.8 billion from $2.33 billion a year ago.

Block attributed the fall to “Bitcoin trading dynamics” and a “strategic decision to reduce the fee” charged on certain Bitcoin transactions on Cash App.

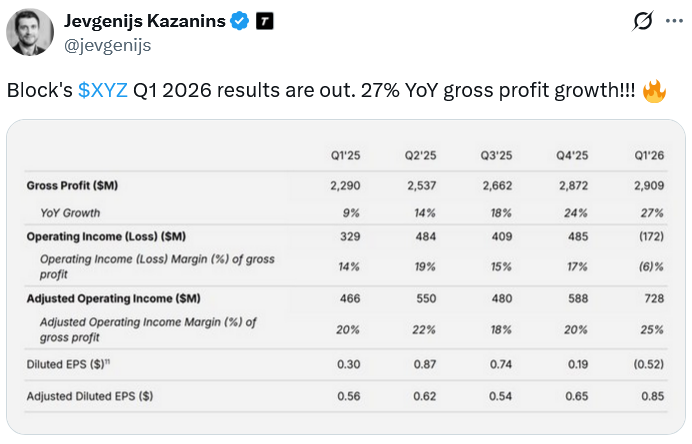

Block’s gross profit rises 27% in Q1

Block’s Q1 gross profit — net sales minus cost of goods sold — reached $2.9 billion, up 27% from a year earlier.

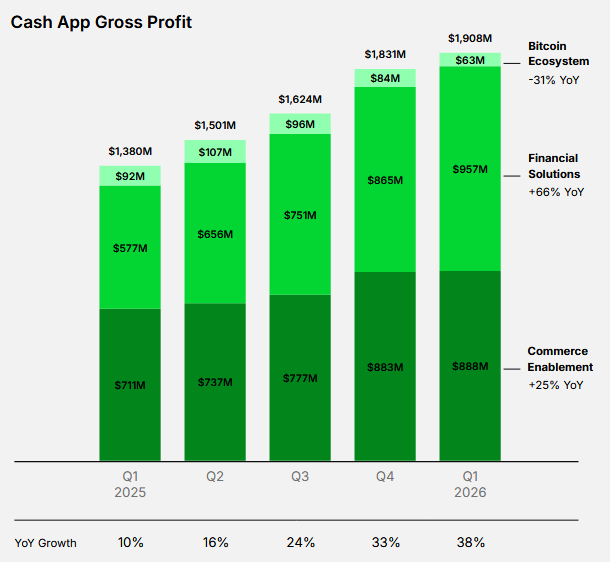

Bitcoin payments in Cash App contributed $63 million to Block’s gross profit, while Square had no meaningful impact on Block’s Bitcoin business.

Avory & Co. founder and chief investment officer Sean Emory said “Block had a strong quarter,” having “beat and raised” its guidance.

Source: Jevgenijs Kazanins

The quarter also included a restructuring overhaul in late February, when Dorsey announced about 4,000 staff cuts, representing roughly 40% of the company’s workforce, as part of a plan to rely more on AI in search of greater operational efficiency. Block’s operational expenses rose 57.2% year-on-year to $3.08 billion in Q1.

Cash App’s quarter-over-quarter change in gross profit. Source: Block

Block expands Bitcoin offerings

In late April, Block launched a proof-of-reserves for its corporate Bitcoin treasury and for users to confirm Bitcoin balances on Cash App and Square as part of a push to increase transparency with its customer base.

Related: Bitcoin exchange reserves fall to two-year low after $8B exodus

In the same announcement, Block unveiled a Bitkey hardware wallet with a touchscreen to verify transactions and a new feature on Cash App allowing certain users to automatically convert payments into Bitcoin.

It also started offering 5% Bitcoin cash back rewards for Square merchants and raised customer withdrawal limits fivefold to $10,000 per day and $25,000 per week, extending Dorsey’s push to broaden Bitcoin’s role in everyday payments.

Magazine: Guide to the top and emerging global crypto hubs — Mid-2026

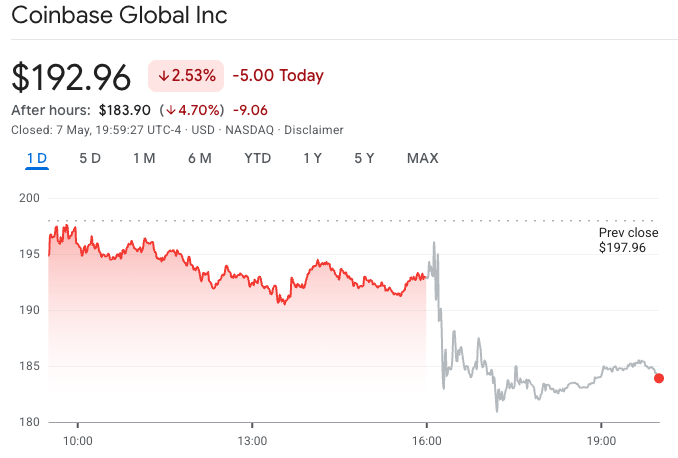

Coinbase Global Inc. entered 2026 with a sobering first-quarter performance, delivering a net loss and revenue figures that underscored the headwinds facing the crypto industry. The exchange posted a $394.1 million net loss for Q1, marking a second consecutive quarterly loss after a $667 million shortfall in Q4 2025, and a meaningful drift away from profitability despite revenue coming in below expectations.

The company reported revenue of $1.41 billion for the quarter, trailing consensus estimates of around $1.5 billion. Earnings per share stood at a loss of $1.49, compared with analysts’ expectations for a positive 36-cent print. The quarterly results arrive as macro conditions remained challenging for crypto trading and related services, weighing on Coinbase’s topline and margins alike.

On the call accompanying the release, Coinbase CFO Alesia Haas stressed the broader market backdrop, noting that “macro conditions were genuinely tough” and that the total crypto market capitalization and overall trading volume declined by more than 20% quarter over quarter. The numbers reflect a wider crypto winter in early 2026, even as the company has sought to diversify beyond pure spot trading into other asset classes and services.

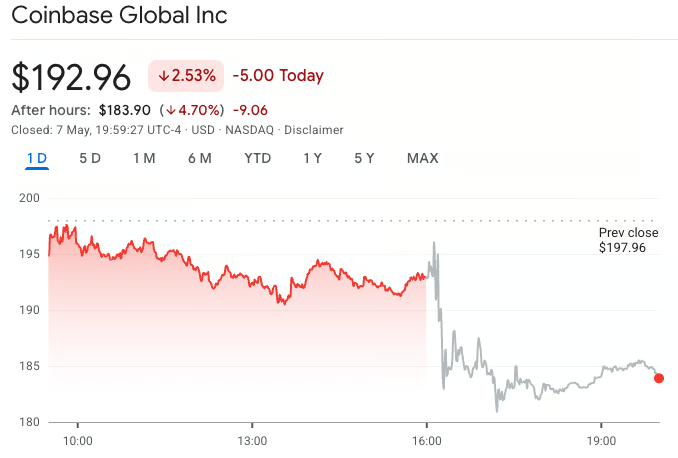

Following the report, Coinbase’s stock traded lower in regular hours and slid further in after-hours trading, dipping under $184. The retreat comes as investors weigh not only quarterly performance but the company’s longer-term plan to navigate a market where trading activity has cooled and competition for revenue sources has intensified.

Coinbase’s quarterly challenges come as peers in the crypto ecosystem also grapple with slower revenue and tighter spreads, forcing many to reconfigure operations and human resources. The stock has fallen more than 14% this year, prompting a series of strategic adjustments designed to conserve cash and explore new growth avenues.

Looking ahead, Coinbase is pursuing a broader strategy to diversify beyond a single focus on spot crypto. Chief executive officer Brian Armstrong told investors that the world economy is moving on-chain, and Coinbase was built to capitalize on that transition. He framed the current period as an interim phase in which some asset classes outperformed while spot crypto assets lagged, with the expectation that diversification would eventually yield a more balanced trajectory over time.

That pivot toward a multi-asset platform aligns with a broader industry conversation about tokenized finance and adjacent revenue streams. In recent quarters, Coinbase has signaled interest in markets that extend beyond traditional spot trading, including prediction markets and other services that could complement trading activity. The company has also taken steps to constrain costs as part of a broader effort to return to a more sustainable earnings trajectory.

The market backdrop outside Coinbase has been mixed. Rival Robinhood Markets also reported softer-than-expected first-quarter results, with crypto revenue and trading volumes shrinking versus a year earlier. Industry analysts have suggested that the decline in crypto stocks presents a potential entry point for investors seeking exposure to the tokenization narrative, a view that Bernstein conveyed in March. The research firm argued that the downturn in crypto equities could be an opportunity to gain exposure to a broader shift toward tokenized finance — including stablecoins and prediction markets — that could gain traction in the coming years.

From a regulatory and adoption standpoint, Coinbase’s push to broaden product lines could help mitigate volatility tied to crypto price swings by generating revenue from non-trading services. The company also faces ongoing scrutiny around exchange operations, user protection, and the regulatory clarity required to support a more expansive suite of financial products tied to digital assets. Investors will be watching closely how new business lines perform and whether they can scale in a market where trading activity remains uneven and capital costs have risen.

In a quarterly filing that accompanied the earnings, Coinbase reaffirmed the numbers and provided the formal context for these results. The company’s Q1 2026 10-Q lays out the period’s performance and offers a window into the balance sheet, cash burn, and the company’s ongoing cost-control initiatives. For those seeking to review the official documentation, the filing is available here: Coinbase Q1 2026 10-Q.

As Coinbase navigates these headwinds, investors will be looking for concrete signs that the company can translate its strategic ambitions into tangible revenue streams. The first-quarter miss highlights the gap between the pace of strategic diversification and the immediate earnings trajectory that investors have grown accustomed to in a year of crypto market volatility. The company’s leadership will need to demonstrate that the contemplated shift toward a multi-asset platform can begin to offset declines in core trading activity, particularly if market conditions remain challenging in the near term.

Analysts’ take on the quarter remained mixed, with some noting the difficulty of beating revenue expectations in a slowing market. The Q1 2026 results also come after a period during which Coinbase announced cost-reduction measures, including workforce reductions, to align its cost structure with a slower revenue environment. The company disclosed that it laid off approximately 14% of its workforce, roughly 700 employees, as part of an ongoing effort to protect margin during a period of slower top-line growth.

For now, the path forward hinges not only on market conditions but on execution across new product lines and services. Armstrong’s message to investors — that the on-chain economy will continue to expand and that Coinbase was built to participate in that expansion — remains the north star for the company. The question for investors is whether the diversified approach will translate into a sustainable uplift in revenue and profitability as the broader crypto cycle evolves.

Looking ahead, readers should monitor Coinbase’s progress on cost discipline, the performance of new business initiatives, and how the company hedges against ongoing volatility in crypto markets. As the sector recalibrates, Coinbase’s ability to monetize non-trading activities and scale new products could determine whether the stock can weather the current downturn and participate in a future upswing as tokenization and on-chain finance gain broader traction.

Key takeaways

- Q1 2026 results show a $394.1 million net loss for Coinbase, extending a loss streak from Q4 2025, with revenue of $1.41 billion versus roughly $1.50 billion expected.

- Analysts anticipated earnings per share of 36 cents, but Coinbase reported a loss of $1.49 per share, contributing to a subdued reaction in after-hours trading and a stock price below $184.

- Macro headwinds were cited as a major factor, with total crypto market capitalization and trading volume down more than 20% quarter over quarter.

- Cost-cutting and strategic diversification are central to Coinbase’s plan, including layoffs of about 700 employees (roughly 14% of the workforce) and pivoting toward multi-asset offerings and services beyond spot trading.

- Industry context suggests mixed signals: peers like Robinhood also reported softer results, while analysts at Bernstein argued the downturn may create opportunities to tap into tokenization themes and a broader on-chain economy.

Q1 results and the market backdrop

Coinbase’s first-quarter performance arrived amid a crypto market backdrop that has yet to regain its footing. The company’s CFO underscored the macro challenges during the earnings call, reiterating that a meaningful portion of the revenue softness stemmed from a broad decline in crypto activity. The revenue miss was not just a function of weaker trading volumes but also a softer contribution from non-trading lines, illustrating the difficulty of maintaining profit margins when core activity contracts.

Despite the disappointing quarter, Coinbase’s leadership emphasized a strategic shift toward a broader asset-classes approach. Armstrong framed the current period as a phase where the ecosystem is evolving, with spot crypto assets lagging while other assets may contribute more meaningfully to the platform’s revenue mix over time. This multi-asset strategy, if executed effectively, could reduce sensitivity to price swings in the underlying crypto market and create a more resilient business model.

Moving beyond spot: diversification as a growth lever

The push to diversify aligns Coinbase with a broader industry thesis that tokenized finance and on-chain services will become a core driver of value creation. In the near term, the company is testing and expanding into new product areas that could complement trading activity and broaden the addressable market. Such a transition is not guaranteed to bear fruit quickly, but it represents an important strategic hedge against persistent volatility in spot markets.

At the same time, cost discipline remains a practical necessity. The decision to trim the workforce is a blunt acknowledgment that growth in an uncertain macro environment requires tighter expense management. Investors will want to see if these reductions translate into improved unit economics and whether the company can fund its expansion into new lines without compromising risk controls or user experience.

What to watch next

As Coinbase charts its path through 2026, investors should monitor several key developments: the performance of non-trading revenue streams, the pace and impact of ongoing cost initiatives, regulatory developments that could unlock or constrain on-chain products, and the degree to which the broader market recovers and supports trading volumes. The company’s quarterly progress on its multi-asset strategy will be particularly telling, as this plan represents both an opportunity to stabilize revenue and a test of management’s ability to execute beyond the traditional exchange model.

In case readers want to review the formal quarterly documentation, Coinbase’s Q1 2026 filing is accessible here: Q1 2026 10-Q.

Further context on the quarter’s expectations and peer performance can be found in market coverage surrounding Robinhood’s comparable results and Bernstein’s commentary on crypto equities and tokenization themes. These perspectives underscore a sector-wide pivot toward new revenue engines even as traditional trading volumes remain volatile.

Overall, Coinbase’s Q1 2026 results crystallize a transitional moment for the company and the crypto ecosystem: a time of deliberate restructuring and strategic experimentation, set against a backdrop of ongoing market headwinds and regulatory evolution. How quickly the new growth pillars can scale will shape the trajectory of Coinbase’s earnings power in the quarters ahead.

What remains uncertain is how smoothly the new initiatives will integrate with the existing platform and whether investors will see a clear path to profitability as macro conditions evolve. For now, the market will watch closely for signals that the diversification strategy is gaining traction and that cost controls are translating into measurable improvements in margins.

Coinbase shares slid Thursday after the US crypto exchange reported a steep first-quarter loss while revenue missed Wall Street expectations.

Coinbase reported a net loss of $394.1 million in Q1, its second consecutive quarterly loss after reporting a $667 million loss in Q4 2025. It swung from a $65.6 million profit a year earlier.

“Macro conditions were genuinely tough,” Coinbase chief financial officer Alesia Haas told investors on an earnings call. “Total crypto market cap and total crypto trading volume were both down more than 20% quarter-over-quarter.”

Coinbase’s earnings come as other crypto companies have also struggled to turn a profit in the first months of 2026 as a crypto market slump pushed some traders to other investments.

Meanwhile, Coinbase’s Q1 revenue was $1.41 billion, missing analyst estimates of $1.5 billion. Transaction revenue slumped 40%, while subscription and services revenue — representing its business outside trading — fell 13.5% from a year earlier.

Its earnings per share were a $1.49 loss, compared to analysts’ expectations of 36 cents per share, which saw Coinbase dropping by 4.7% after hours on Thursday to under $184.

Coinbase shares fell in regular and after-hours trading on Thursday amid the company’s first-quarter earnings. Source: Google Finance

Coinbase’s stock has fallen more than 14.5% this year, prompting the exchange to pursue new business lines such as prediction markets and cost-cutting measures, including laying off 14% of its workforce, or about 700 employees, on Monday.

Despite the company’s earnings, CEO Brian Armstrong struck an optimistic tone on the earnings call, telling investors that “the world economy is moving on-chain, and Coinbase was built to capitalize on this transition.”

He added that over the past year, Coinbase has aimed to transition from “a primarily spot-focused crypto platform into a place where you can now trade any asset class.”

“We’re in kind of this interim period where spot crypto assets were down a bit, other asset classes were up. As we diversify, these things will get balanced out, where we’ll just be in a more upward channel over time,” Armstrong added.

Related: Block Inc rises 8% as Q1 gives ‘earnings surprise’ despite Bitcoin dip

Coinbase rival Robinhood Markets also missed estimates for the first quarter last month as its crypto revenue and trading volumes nearly halved from a year earlier.

Bernstein said in March that the decline in crypto stocks presented a more attractive entry point for investors seeking exposure to the current hot theme of tokenization and maintained a bullish rating on Coinbase and Robinhood.

It argued that the companies offered investors exposure to a broader shift toward tokenized finance, including stablecoins and prediction markets, which it expected to gain traction in the coming years.

Magazine: Guide to the top and emerging global crypto hubs — Mid-2026

American Bitcoin posted an $81.8 million net loss in Q1 2026, even as the Trump-backed miner set a new quarterly production record of 817 BTC and cut its mining cost by 23%.

Summary

- American Bitcoin reported an $81.8 million net loss in Q1, up from a $59.5 million loss in Q4 2025.

- Bitcoin fell 22% during the quarter, triggering a $117.2 million non-cash impairment charge on the company’s holdings.

- The company mined a record 817 BTC and reduced its cost per coin to $36,200, a 23% improvement from $46,900 in Q4 2025.

American Bitcoin reported a net loss of $81.8 million in Q1 2026, driven by a 22% bitcoin price decline that triggered a $117.2 million non-cash impairment on its digital asset holdings. Revenue from mining fell to $62.1 million from $78.3 million in the prior quarter.

Despite the headline loss, CEO Mike Ho pushed back. “Strip out the non-cash mark-to-market adjustment on our Bitcoin required by FASB,” he said, “and the underlying business was profitable and we did not sell a single coin.”

Gross mining margins held above 50% and the cost per coin fell to $36,200, a 23% improvement from $46,900 in Q4 2025.

Record production, widening paper losses

American Bitcoin mined 817 BTC in Q1, its highest quarterly output to date, and purchased an additional 803 BTC for its treasury. Total holdings reached 7,021 BTC as of March 31. Co-founder Eric Trump told Consensus Miami on Wednesday:

“In just over eight months as a public company, we have become the 16th largest bitcoin holder globally and scaled to more than 28 exahash of capacity.”

The company completed the deployment of 11,298 new Bitmain miners in early March, bringing its total fleet to 89,242 machines and 28.1 EH/s of capacity. Operating expenses for the quarter totalled $150.7 million.

ABTC shares fell roughly 7% in pre-market trading after the results missed analyst estimates by 17%. As crypto.news reported, ABTC debuted on Nasdaq through a reverse merger in September 2025, briefly pushing Eric Trump’s paper stake into billionaire territory before a sustained selloff.

Core Scientific (CORZ) reported a $347.2 million first-quarter net loss as its Bitcoin self-mining revenue fell sharply and high-density colocation became its largest revenue source.

In its earnings report published Wednesday, the company reported a net loss of $1.06 per diluted share for the quarter. A year earlier, Core Scientific reported diluted earnings of $1.24 per share.

Core Scientific said the loss included $266.5 million in non-cash impairment charges and a $30.8 million non-cash loss from changes in the fair value of warrants and contingent value rights.

Revenue rose to $115.2 million from $79.5 million a year earlier, but fell short of analyst expectations. Zacks Equity Research said analysts expected $120.2 million in revenue, with Core Scientific’s results coming in about 4.1% below expectations.

The results show Core Scientific’s transition from a Bitcoin miner into an AI infrastructure company, with high-density colocation now generating most of its revenue. The shift gives the company a larger business, but it also highlights how its legacy mining operations have weakened.

Bitcoin mining revenue falls

Core Scientific’s digital asset self-mining revenue fell to $30.1 million from $67.2 million a year earlier, with the company mining 279 Bitcoin (BTC) during the quarter, down 45% from the same period in 2025. According to its 10-Q filing, Core Scientific sold 2,385 Bitcoin during the quarter for $208.3 million to fund planned capital expenditures and other cash needs.

Core Scientific’s six-month price chart. Source: Yahoo Finance

Despite the weaker mining results, Core Scientific’s shares have gained over the past six months. Yahoo Finance data shows CORZ closed at $24.63 on Wednesday, up about 19.6% over six months, before falling 7.43% to $22.80 in pre-market trading at the time of writing.

In a separate announcement, Core Scientific said it plans to scale its Muskogee, Oklahoma, campus to about 1.5 gigawatts of gross power, or about 1.0 gigawatt of leasable power, partly through the planned acquisition of Polaris DS. The company has also started construction on a second, unleased 82.5-megawatt building at the campus.

Related: Trump-linked American Bitcoin reports $82M Q1 loss, revenue miss

Core Scientific expands AI-linked colocation business

Core Scientific’s first-quarter growth came from high-density colocation rather than Bitcoin production, with the company’s mining revenue and Bitcoin output falling while its AI-linked hosting business generated most of its revenue.

The company said its colocation revenue rose to $77.5 million in the first quarter from $8.6 million a year earlier, driven by additional billable customer power capacity delivered during the quarter.

The company said it was billing for 243 megawatts of capacity as of March 31, representing about $350 million in average annualized colocation revenue.

The revenue shift follows a series of hosting agreements with CoreWeave. In June 2024, Core Scientific said it signed 12-year contracts to deliver about 200 megawatts of infrastructure to host CoreWeave’s high-performance computing operations.

The companies later expanded the relationship. In an SEC filing in February 2025, the companies said CoreWeave’s total contracted high-performance computing infrastructure with Core Scientific had increased to about 590 megawatts across six sites.

Magazine: Guide to the top and emerging global crypto hubs: Mid-2026

Blockstream CEO Adam Back told Consensus Miami 2026 that bitcoin is winning a security war against DeFi, and that pension funds and sovereign entities are the next buyers.

Summary

- Adam Back argued at Consensus Miami that Bitcoin’s simpler architecture is pulling institutional capital away from DeFi platforms hit by repeated smart contract exploits.

- He outlined Bitcoin adoption in three waves: retail ownership, spot ETF access, and now institutional allocation through managed portfolios and sovereign entities.

- Back estimated roughly 200 bitcoin treasury companies exist globally and said BlackRock model portfolio allocations have not yet fully taken effect.

Blockstream CEO Adam Back argued at Consensus Miami 2026 that Bitcoin’s comparatively simple network architecture is separating it from more experimental blockchain ecosystems that have suffered repeated smart contract failures.

Back described the dynamic as Bitcoin winning “the DeFi security war,” as institutional investors grow more sophisticated in understanding where security risk actually sits. “Bitcoin infrastructure is much more simple, robust, security first,” he said.

Back said institutions are no longer trying to reshape Bitcoin into traditional finance infrastructure. Instead, he argued, they are adapting themselves to Bitcoin’s incentive structure and conservative security model.

That dynamic, he said, opens the door for Bitcoin-native tokenization and DeFi systems that prioritize safety over rapid experimentation, using layer-2 solutions such as Blockstream’s Liquid Network.

The three waves of bitcoin adoption

Back outlined Bitcoin adoption as occurring in three sequential waves: direct retail ownership, spot ETF access through brokerages and advisers, and now institutional allocation through managed portfolios, pension funds, and sovereign entities.

“The model portfolios that BlackRock and others are putting out,” he said, “those allocations haven’t taken effect yet,” suggesting the largest wave of institutional capital has not yet arrived.

Back also estimated roughly 200 bitcoin treasury companies now exist globally, including BSTR, the firm he leads as CEO.

He described BSTR as a more actively managed approach to bitcoin exposure, intended to generate returns through both holdings and fund management strategies rather than passive accumulation. The comments came as bitcoin traded above $81,000 at the time of the Consensus session.

TLDR

- American Bitcoin increased its Bitcoin holdings to more than 7,300 BTC valued at about $592 million.

- The company produced 817 Bitcoin in Q1 2026, marking its strongest quarterly output to date.

- American Bitcoin also purchased around 803 Bitcoin during the quarter to expand reserves.

- Total Bitcoin reserves grew by roughly 1,600 BTC in a single quarter.

- Satoshis per share rose to about 663, reflecting a 20% increase.

American Bitcoin Corp. expanded its Bitcoin reserves beyond 7,300 BTC after a record production quarter. The Nasdaq-listed miner valued its holdings at about $592 million. Co-founder Eric Trump confirmed the figures and said the company maintained its accumulation strategy.

American Bitcoin Expands Holdings and Production

American Bitcoin began building its Bitcoin position in mid-2025 and accelerated purchases in early 2026. The company now ranks as the 16th largest corporate Bitcoin holder. Eric Trump said, “Our Bitcoin accumulation strategy remained intact despite a challenging market environment.”

During Q1 2026, the company produced about 817 Bitcoin, its strongest quarterly output. It also acquired around 803 Bitcoin through targeted purchases. Total reserves grew by roughly 1,600 Bitcoin during the quarter.

The company reported that Bitcoin price declined about 22% quarter over quarter. Despite weaker prices, American Bitcoin continued expanding its balance sheet. It confirmed that satoshis per share rose to about 663, up nearly 20%.

Management linked the increase in satoshis per share to faster Bitcoin growth than share count expansion. The company said this metric reflects shareholder exposure to Bitcoin reserves. It maintained that production and purchases supported reserve growth.

Operational Gains Lift Efficiency and Capacity

American Bitcoin reduced its mining cost per Bitcoin to about $36,000 in Q1 2026. The figure marked a 23% decline from the previous quarter. The company attributed the drop to improved fleet efficiency and cost control.

Mining gross margins held near 52% despite lower Bitcoin prices. Revenue reached about $62 million compared with $78 million in Q4 2025. The company reported a net loss of roughly $82 million for the quarter.

American Bitcoin expanded its owned fleet to about 89,242 miners. Total capacity reached around 28.1 EH/s, up nearly 12% from the prior quarter. The company energized new capacity at its Drumheller site.

The Drumheller expansion added about 3.05 EH/s from next-generation miners. Following deployment, operational hashrate reached roughly 25.0 EH/s. The company confirmed that this level reflects continued scaling of its mining platform.

American Bitcoin stated that it will continue operating its expanded fleet. It also confirmed that reserve totals exceeded 7,300 BTC at quarter’s end. Eric Trump reiterated that the company remains focused on disciplined growth.

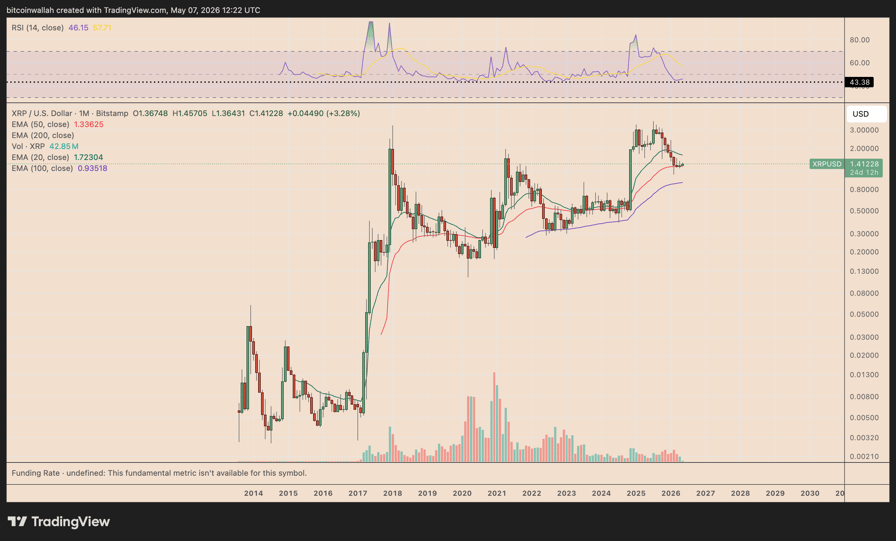

XRP (XRP) is testing a key long-term support level that has historically preceded major rebounds, according to a monthly chart shared by analyst MikybullCrypto.

Key takeaways:

- XRP has jumped by roughly 30% from its February lows.

- Multiple fractals suggest the price is bottoming out, supported by strong XRP ETF inflows.

XRP chart hints at rebound toward $12

Milkybull’s chart shows XRP trading inside a rising channel that has guided price action since 2014. XRP is now near the channel’s lower trendline around $1.30–$1.40, a zone that previously acted as a launchpad for large upside moves.

XRP/USD monthly chart. Source: TradingView/MilkybullCrypto

The analyst says XRP is “probably going to $12,” a level that roughly aligns with the channel’s midpoint.

Momentum indicators support the rebound thesis. XRP’s monthly relative strength index (RSI) has cooled toward a historical support area near 40–45, similar to levels that appeared before past rallies.

In a Thursday post, analyst JD pointed to the same RSI support zone as a potential “cycle bottom” signal for XRP.

His two-week chart shows XRP breaking out of a multi-year symmetrical triangle, then pulling back toward the breakout area.

XRP/USD two-week chart. Source: TradingView/JD

The chart’s projected green target zone aligns with the $8–$14 range, implying strong upside if XRP holds the retest zone.

The bullish outlooks follow XRP’s sharp rebound in recent weeks, up by about 30% from its February lows at around $1.11.

Related: XRP price copies 2025 chart fractal that last time sparked 66% gains

In the period, XRP has largely benefited from renewed risk sentiment led by the US–Iran ceasefire, as well as market-specific fundamentals.

These include Rakuten Wallet’s XRP integration, which expanded the token’s reach in Japan, and $81.6 million in April inflows into US spot XRP ETFs, their strongest monthly total of 2026.

In the first week of May, XRP ETFs have attracted $28.17 million in inflows already.

US XRP ETF net flows. Source: SoSoValue

XRP still risks 2022-style bear market repeat

However, the bullish XRP setup is not guaranteed. The bears will try to pull the price down below the channel support. This would invalidate the bullish structure and put XRP at risk of deeper losses.

XRP/USD monthly chart. Source: TradingView

The support overlaps closely with XRP’s 50-month exponential moving average (50-month EMA, the red line) near $1.33.

Losing this support cluster shifts focus toward the 100-month EMA (the purple line) near $0.93, implying a roughly 30% drop from current levels. A similar plunge occurred during the 2022 bear market.

Shopify Inc Stock Climbs 3.55% on Renewed Earnings Focus

8 Forgotten Sitcoms From the 2000s That Have Aged Like Fine Wine

Falcon Mill Bolton open to the public this weekend for art exhibition

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

![BITCOIN: CRAZY!!!! THIS IS CRAZY!!!! [trades]](https://wordupnews.com/wp-content/uploads/2026/05/1778214197_maxresdefault-80x80.jpg)

-

NewsBeat4 days ago

NewsBeat4 days agoChannel 5 – All Creatures Great and Small series 7 new post

-

Crypto World20 hours ago

Crypto World20 hours agoUpbit adds B3 Korean won pair as Base token gains Korea access

-

Tech6 days ago

Tech6 days agoTrump’s 25% EU auto tariff breaches Turnberry Agreement that also covers semiconductors and digital trade

-

NewsBeat21 hours ago

NewsBeat21 hours agoNCP car park operator enters administration putting 340 UK sites at risk of closure

-

Sports6 days ago

Sports6 days agoPaul Scholes issues Marcus Rashford reality check as agreement emerges over Man United star

-

Entertainment6 days ago

Entertainment6 days agoMet Gala 2026 Rumored Guest List Is Turning Heads

-

Business7 days ago

Business7 days agoStrait of Hormuz Blockade Persists Amid US-Iran Standoff, Sending Oil Prices Soaring

-

Entertainment6 days ago

Entertainment6 days agoKylie Jenner Hit With Second Lawsuit From Ex-Housekeeper

-

Entertainment6 days ago

New on Prime Video in May 2026 — Full List of Movies and Shows

-

Tech7 days ago

Tech7 days agoMeta ends Sama contract after Kenyan workers report seeing intimate footage from Ray-Ban smart glasses users

-

Sports6 days ago

Sports6 days agoCavaliers vs. Raptors Game 6 live score, updates, highlights from 2026 NBA playoffs first-round series

-

Sports6 days ago

Sports6 days agoDavid Benavidez responds to team Canelo saying the fight will never happen

-

Entertainment5 days ago

New Netflix Movies in May 2026 — My Top 3 Picks to Stream

-

Entertainment5 days ago

Entertainment5 days agoMelissa Joan Hart and More Stars Attend 2026 Kentucky Derby

-

Sports6 days ago

Sports6 days agoIPL 2026: ‘Love you darling’- Hardik Pandya’s reaction to MS Dhoni steals the show |Watch | Cricket News

-

Entertainment6 days ago

Entertainment6 days agoYoung and the Restless Next Week: Cane Arrested & Matt’s Deadly New Scheme!

-

Business5 days ago

Business5 days agoLuka Doncic Injury Update: Doncic’s Hamstring Recovery Slows Lakers’ Hopes Against Thunder: Can He Run Yet?

-

Sports7 days ago

Sports7 days agoBayern won’t hand bottom side Heidenheim ‘gifts’ despite PSG game

-

Crypto World5 days ago

Pi Network Mandates Protocol 23 Upgrade for All Mainnet Nodes Before May 15 Deadline

-

Sports7 days ago

Sports7 days agoWhat Preity Zinta Said After Punjab Kings’ First Defeat Of IPL 2026

You must be logged in to post a comment Login