I am a 35-year stock market investor, MBA, and retired reporter and editor for the San Francisco Chronicle. My primary style is a mix of growth and income, with attention to special situations.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of ATUUF either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

The Wind Academy’s director Geoff Briggs called it a “significant step forward” for his business

Olly Hassan (left) and Geoff Briggs of The Wind Academy.(Image: The Wind Academy)

A Blyth training provider to the growing offshore energy sector its plotting its own expansion after securing funding.

The Wind Academy, which specialises in vocational courses for renewables industry, is set to extend its facilities at the Port of Blyth following the injection of more than £42,000 from the Business Growth Fund. It will support training infrastructure for wind turbine technicians working on offshore and onshore developments.

The Academy’s growth ambition is led by director Geoff Briggs and business development manager, Olly Hassan, who are broadening its training capacity and industry partnerships.

Mr Briggs said: “This funding is a significant step forward for the Wind Academy. It allows us to invest directly in our training facilities and ensure we are delivering high-quality, industry-ready training for the offshore and onshore wind sectors.

Advertisement

“As demand for renewable energy skills continues to rise, this support helps us grow sustainably and create real opportunities for people in the region.”

The Business Growth Fund support was delivered through Business Northumberland. Coun Richard Wearmouth, cabinet member for regeneration at Northumberland County Council, said: “The Wind Academy is playing an important role in developing the skills needed for the future of renewable energy. This funding will help the business grow, invest in its facilities and continue supporting the region’s low-carbon economy.”

Jon Paul Heron, business advisor at UMi, who helped guide the process, added: “It’s been a pleasure supporting the Wind Academy on its growth journey. This investment will help strengthen its position as a key training provider for the wind sector and support long-term economic growth in Northumberland.”

The Wind Academy is based out of the Energy Central learning hub at the Port of Blyth, which has recently announced its own major expansion programme in a bid to capture more work in offshore wind. Bosses this week set out a £100m vision which includes reclaiming up to three hectares of land from the River Blyth estuary at the port’s Battleship Wharf terminal.

Advertisement

The additional space and facilities will be marketed at wind farm developers and operators amid an expected influx of North Sea energy projects. The North East is well placed to benefit from the Government’s next offshore lease auction that could take place in 2027 and could feature predominantly sites off the region’s coast.

That round could bring another 6GW of wind energy to the UK though it is unlikely that turbines will be in place and turning before the 2030s.

The U.S. economy added 115,000 jobs in April, the Labor Department said, far exceeding expectations. The unemployment rate stayed unchanged at 4.3%. The jobs report puts the Federal Reserve’s focus squarely on inflation data when it comes to determining its next move on interest rates. Four months ago, a big question for the Fed was whether it needed to keep cutting rates to support what looked like a shaky labor market. But that question is now gone.

Intel shares rose 14% after The Wall Street Journal reported that the chip maker struck a preliminary deal to supply chips to Apple. It’s still unclear which Apple products Intel would make chips for. Intel reached a stock-market value of $628 billion, and its shares are up almost 500% in the past year. The news lifted other semiconductor stocks, including Micron, which gained 15%. The PHLX Semiconductor Index rose 5.5%. Apple’s stock climbed 2%.

Good afternoon to everyone here in Perth, and good morning to all of those joining us from London, and welcome also if you are tuning in virtually. As Chair of Rio Tinto, I have the privilege of welcoming you to our 2026 Annual General Meetings. This year, in keeping with our focus of embedding stronger, sharper and simpler ways of working across the business, we are holding the Rio Tinto plc and the Rio Tinto Limited AGMs contemporaneously.

Our meetings are linked audiovisually, so all shareholders can participate in a joint discussion as provided for under Rio Tinto plc’s Articles of Association and Rio Tinto Limited’s constitution. As you know, AGMs are an opportunity for open conversations and for deepening understanding. They allow us as a Board to hear from you and to respond to the topics you are interested in.

And next year, our directors will be present in person at the plc AGM in London with a limited AGM held contemporaneously in Australia. And we plan to continue this arrangement for future AGMs with our directors alternating their physical attendance annually. This naturally builds on our regular engagement with investors throughout the year. In fact, over the last 2 months, I’ve met personally with shareholders representing more than 1/4 of Rio Tinto plc’s issued capital and 1/3 of Rio Tinto Limited’s issued capital.

Prior to November 2022, artificial intelligence (AI) was something most people associated with futuristic movies. Then OpenAI released ChatGPT, and everything changed. AI was no longer an invisible algorithm quietly powering the world’s most sophisticated companies. Suddenly, the average person could use it to write code, compose poems, edit articles and much more.

The adoption was staggering. ChatGPT reached 100 million users in just two months, making it the fastest-growing consumer application in history at the time, and it has never looked back. Over the next three years, AI became the single most dominant investment theme on Wall Street, working its way into business models across every sector of the economy.

Advertisement

But is it a good thing? That seems to depend on who you ask.

The general consensus is that powerful emerging technology ultimately benefits society and raises our standard of living. The transition, however, can be rocky. There is a growing perception that AI may already be stifling traditional job growth, as companies slow hiring in anticipation of reducing their need for employees. While that has far-reaching implications across the economy, I want to focus on one area: lending rates and mortgages in particular.

A Housing Market Already Under Stress

The housing market has been a serious concern and a source of heated debate for the past five years. In 2021, the Federal Reserve began raising interest rates to combat sky-high inflation. In roughly one year, the 30-year fixed rate mortgage went from under 3% to well over 7%.

Raising rates to fight inflation is designed to address the problem from the demand side. The theory in housing seems fairly straightforward: if money is more expensive to borrow, buyers will be less aggressive in pursuing new homes.

Advertisement

But that is not quite what happened. Most housing analysts now conclude that raising mortgage rates so dramatically, after such a prolonged period of historic lows, effectively froze the supply of homes that would normally come to market. If someone is sitting on a 3% mortgage, there is little incentive to trade it in for a 7% one. Combined with a decrease in new builds, housing inventory dried up and prices rose even higher.

So Where Do Mortgage Rates Come From?

Before exploring how AI might affect mortgage rates, it helps to understand what drives them in the first place.

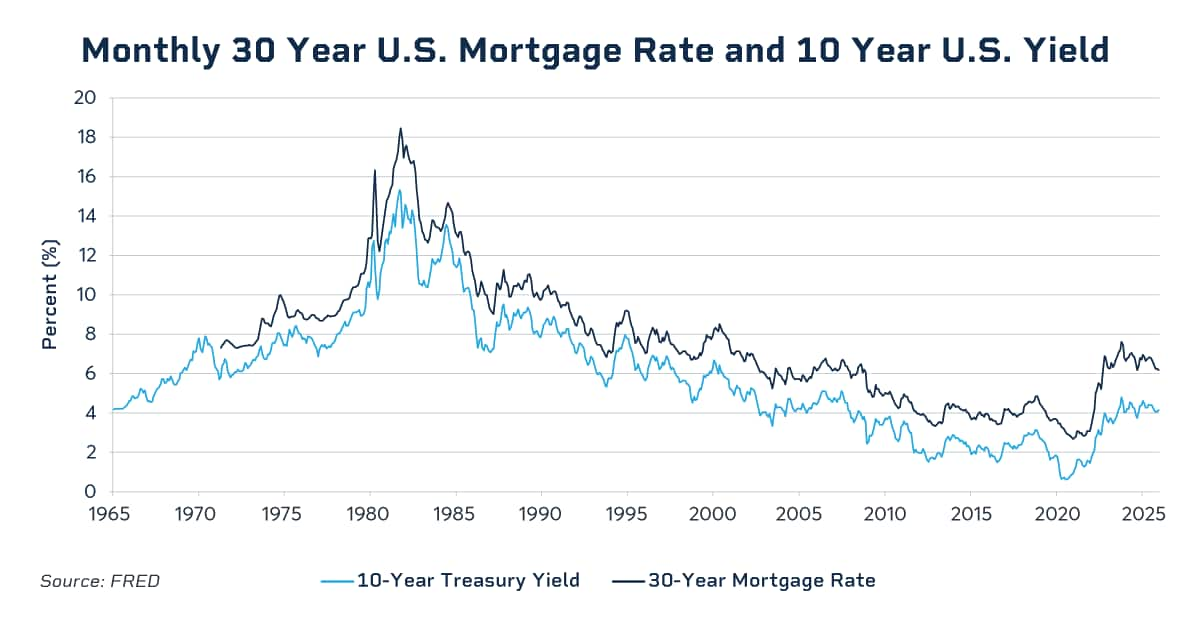

The average 30-year fixed mortgage is actually held for about 12 years. Because of that, mortgage rates closely track the U.S. 10-year Treasury yield, which is the nearest matching maturity. Historically, the spread between the 10-year yield and the 30-year fixed mortgage rate averages around 180 basis points. In plain terms, if the 10-year Treasury yield is sitting at 4%, one would expect the 30-year fixed rate to be somewhere around 5.8%.

That spread exists for two reasons. First, a mortgage carries default risk that a U.S. Treasury bond simply does not. Second, there are real servicing and administrative costs baked into every mortgage. AI could potentially affect both the Treasury yield side of the equation and the factors that create the spread. Here are a few potential ways those scenarios might play out.

Advertisement

Scenario 1: AI Sparks Deflation, Rates Fall

If the biggest economic impact of AI turns out to be massive productivity gains spread across most sectors of the economy, the effect could be deflationary. We saw something similar play out in the 1990s with the internet. Many economists give Federal Reserve Chairman Paul Volcker full credit for reducing inflation in the early 1980s, but a compelling case can be made that the maturation of the internet was a significant deflationary force in its own right.

It is also worth noting that slower job growth, one of the more visible side effects of AI adoption, would likely further dampen consumer spending and add another layer of downward pressure on prices. Disinflation (where prices rise, but slowly) or outright deflation (where prices decline) makes owning long-duration bonds more attractive, which pushes yields lower. History also tells us that the Fed tends to cut short-term rates when disinflation becomes a concern, pulling yields lower across the entire curve. The end result of this scenario would likely be meaningfully lower mortgage rates.

Scenario 2: AI Fuels a Boom, Rates Rise

Alternatively, the AI revolution could ignite a massive domestic economic expansion. In that environment, investment money might flow out of the relative safety of U.S. Treasuries and into higher-returning opportunities in the market. That rotation could push bond prices down and yields up. If the economic boom also generates demand-driven inflation, it would only accelerate the selling pressure on bonds. In this scenario, mortgage rates could move higher.

Scenario 3: AI Compresses the Spread

This scenario gets less attention but may be the most interesting. Even if Treasury yields stay right where they are, AI could narrow the spread between the 10-year yield and the 30-year fixed mortgage rate.

Advertisement

It is possible that AI will improve risk assessment while simultaneously reducing the servicing and administrative costs embedded in the mortgage process. If one assumes that 30% to 50% of that 180 basis point spread is administrative in nature, cutting those costs in half with AI would not be a trivial result. Borrowers could see meaningfully lower rates even in a flat-rate environment, simply because the cost of originating and managing a mortgage comes down.

Where the Evidence Points

No one can say with certainty which of these scenarios will dominate, and it is entirely possible that elements of all three play out simultaneously. However, many analysts seem to believe the weight of evidence points toward lower rates.

For market participants looking to manage this uncertainty, Mortgage Rate futures offer a way to hedge mortgage servicing rights and pipeline risk that can be associated with a changing rate environment. The contract is based on the Optimal Blue Mortgage Market Index, which tracks real-time rate lock data from over one-third of U.S. residential mortgage originations.

The combination of AI-driven productivity gains, the deflationary pressure of a slower labor market and the prospect of leaner mortgage operations creates a compelling case that mortgage rates are more likely to fall than rise over the coming years. For prospective homebuyers who have been sitting on the sidelines waiting for relief, that may finally be the light at the end of a very long tunnel.

The S&P 500 capped the week off with another record high, flirting with the 7,400 milestone. With a 2.3% weekly gain, the index has now climbed for six consecutive weeks, matching its longest winning streak since October

Good morning, ladies and gentlemen, and welcome to Grupo Cibest Bancolombia First Quarter 2026 Earnings Conference Call. My name is Paul, and I will be your operator for today’s call. [Operator Instructions] Please note that this conference is being recorded.

Please note that this conference call will include forward-looking statements, including statements related to our future performance, capital position, credit-related expenses and credit losses. All forward-looking statements whether made in this conference call and future filings and press releases or verbally, address matters that involve risks and uncertainties. Consequently, there are factors that could cause actual results to differ materially from those indicated in such statements, including changes in general economic and business conditions, changes in currency exchange rates and interest rates. Introduction of competing products by other companies, lack of acceptance of new products or services by our targeted clients, changes in business strategy and various other factors that we describe in our reports filed with the SEC.

With us today is Mr. Juan Carlos Mora, Chief Executive Officer; Mr. Mauricio Botero Wolff, Chief Strategy and Financial Officer; Mr. Rodrigo Prieto, Chief Risk Officer; Mrs. Catalina Tobon, Investor Relations and Capital Markets Director; and Mrs. Laura Clavijo, Chief Economist.

Advertisement

I will now turn the call over to Mr. Juan Carlos Mora, Chief

You must be logged in to post a comment Login