Crypto World

BlockDAG’s $0.00025 Entry is the 2026 Opportunity DOGE and SHIB Can No Longer Offer

Crypto markets continue to shift as investors balance caution with the search for fresh opportunities. Established meme coins are offering mixed signals, with Dogecoin price today hovering near key levels after light gains, while volume remains soft. At the same time, the shiba inu price is moving sideways following recent volatility, keeping traders focused on whether consolidation will turn into a breakout or further decline.

Against this backdrop, BlockDAG is drawing stronger attention by offering access before public trading begins. Its final private round is live at a fixed price of $0.00025, with no vesting and full token delivery at launch. Early buyers also receive limited early trading access, a structure rarely available to retail participants. For investors tracking potential top crypto gainers, BlockDAG (BDAG) presents a clearer, earlier entry point than most market options today.

Dogecoin Price Today Shows Mixed Signals Near $0.11 Level

Dogecoin is showing mixed signals as the crypto market remains uncertain. Fear is still present, but selling pressure has slowed for now. The meme coin sector rose 3% in the last day, reaching a market value of $38.10 billion. Dogecoin gained about 2%, trading between $0.1058 and $0.11. Dogecoin price today sits near $0.1079, while daily trading volume fell sharply by over 43% to $1.26 billion. Recent data also shows $2.40 million in liquidations.

If weakness continues, Dogecoin price today could slip toward the $0.1068 support level, and deeper losses may push it below $0.1057. On the upside, a recovery could lift Dogecoin price today toward $0.1090 and possibly above $0.1102 if buying strength improves.

Shiba Inu Price Trades Sideways Amid Market Uncertainty

Shiba Inu starts February 2026 in a consolidation phase as traders closely watch price trends, on-chain data, and overall market sentiment. After strong volatility in recent months, price action has slowed, raising questions about whether a breakout or sideways movement will follow. Shiba Inu price is currently trading near $0.000006521, reflecting a 5.91% daily decline. The token holds a market cap of about $3.85 billion, while trading volume stands near $144.75 million.

Technical charts show downward pressure, with resistance around $0.00000702. Strong buying could push prices toward this level. However, if selling increases, support lies near $0.00000661, with further downside toward $0.00000600. Indicators show mixed signals, keeping the Shiba Inu price in focus for the coming weeks.

BlockDAG Final Private Round Goes Live at $0.00025

Most traders chase top crypto gainers after the move has already happened. The BlockDAG private sale flips that script by letting participants step in before price discovery even begins.

This final private round is live at $0.00025, locking in a launch valuation that public buyers won’t see again. With a projected launch price of $0.05, BDAG is positioned for a 200× upside, but only for those who secure allocation now. Once this round closes, the opportunity window shuts with it.

What makes this setup different is execution. There’s no vesting, no delayed claims, and no waiting periods. On launch day, your full allocation is delivered straight to your wallet. Clean. Simple. Immediate.

Then comes the edge most people never get: nine hours of early trading access before public markets open. That window exists for one reason: to let private sale participants position ahead of the initial volatility wave. While others rush in blind, you’re already active.

This isn’t a rolling sale or an evergreen offer. The final allocation is finite. When it fills, BDAG becomes fully distributed, forever. From that point on, exposure is limited to open-market buys at whatever price demand sets.

For anyone scanning the market for the top crypto gainers of the next cycle, this private sale isn’t about hype. It’s about timing, structure, and access, three things public markets never offer equally. The dashboard is open. Supply is moving. The clock isn’t slowing down.

BlockDAG Makes Its Case as a Future Top Crypto Gainer

As markets pause, the contrast between hesitation and opportunity is becoming clearer. Dogecoin price today and Shiba Inu price continue to reflect uncertainty, with both assets locked in tight ranges and waiting on a broader market push. For investors chasing momentum, patience is being tested.

BlockDAG, however, is operating on a different timeline. Its final private round at $0.00025 offers fixed pricing, instant ownership, and early trading access before the public rush begins. Once this window closes, entry shifts to open markets at unknown prices. For those scanning the horizon for the next wave of top crypto gainers, the choice is simple. Act early, or watch from the sidelines as demand takes over.

Private Sale: https://purchase.blockdag.network

Website: https://blockdag.network

Telegram: https://t.me/blockDAGnetworkOfficial

Discord: https://discord.gg/Q7BxghMVyu

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

TLDR

- Genius Group sold its entire Bitcoin holdings to fully repay $8.5 million in debt.

- The company said it plans to rebuild its Bitcoin treasury when market conditions improve.

- Genius Group previously held 440 Bitcoin as part of its Bitcoin-first strategy.

- A US court order restricted the company from raising funds or issuing shares.

- Nakamoto disclosed a $20 million Bitcoin sale earlier this week.

Genius Group has liquidated its remaining Bitcoin holdings to fully repay $8.5 million in debt, the company confirmed today. The NYSE-listed firm said it cleared the balance after selling all digital asset reserves. It also stated that it plans to rebuild its Bitcoin treasury when market conditions improve.

Genius Group and Bitcoin Strategy Shift

Genius Group adopted a Bitcoin-first treasury policy in late 2024 after Donald Trump won the US presidential election. The company committed to allocating at least 90% of its reserves to Bitcoin. By February 2025, it held 440 BTC as part of that strategy.

However, a US court order later blocked the company from raising funds or issuing shares. As a result, Genius Group began selling portions of its Bitcoin holdings. Last month, it sold about 86 BTC and retained around 84 BTC.

The company confirmed that it has now liquidated the remaining coins. It used the proceeds to fully repay its outstanding $8.5 million debt. Genius Group stated that it intends to rebuild its Bitcoin treasury when markets become favorable.

Corporate Bitcoin Sales Expand as Nakamoto and MARA Adjust Holdings

Genius Group was not alone in reducing its Bitcoin exposure. Nakamoto, led by Bitcoin advocate David Bailey, disclosed the sale of $20 million in Bitcoin earlier this week. The company did not provide further details about the transaction.

Meanwhile, MARA Holdings reported the sale of 15,133 Bitcoin valued at roughly $1.1 billion. The company said it used the proceeds to finance the buyback of its 2030 and 2031 convertible notes. These moves followed a broader pullback in corporate digital asset holdings.

Revenue Growth and Gross Profit Drive Operational Turnaround

Genius Group reported Q1 2026 operational revenue of $3.3 million. The figure marked a 171% year-over-year increase. Gross profit rose 228% to $2.0 million during the same period.

Net profit from operations reached $2.7 million, reversing a loss recorded in the prior year. The company attributed the turnaround to higher-margin educational programs and experiential learning initiatives. Adjusted EBITDA improved to $600,000.

The company also highlighted several recent initiatives. It launched Genius School as a model future school and expanded Genius City in Bali. It also introduced AI-powered Space Capsule learning pods and reported continued CEO investment in company shares.

Federal Reserve Governor Michelle Barr said on Tuesday that clearer U.S. stablecoin rules could accelerate the sector’s growth, but she warned that regulators must address money-laundering risks, bank-run concerns and consumer protection as they implement the GENIUS Act.

Speaking at a Federalist Society event on stablecoin regulation, Barr emphasized that the law would provide “needed clarity” for issuers. Yet she stressed that the ultimate impact will hinge on how federal and state agencies translate the statute into concrete rules.

Stablecoins are still primarily used for crypto trading and as a dollar-denominated store of value in certain foreign markets. Barr noted their potential to reduce remittance costs, speed up trade-finance processes and help firms manage treasury operations. She also highlighted risks, including bad actors acquiring stablecoins in secondary markets without identity checks, and the temptation for issuers to pursue yield in reserve assets in ways that could erode confidence during periods of stress.

Her remarks come as U.S. agencies shift from drafting legislation to writing rules. The Treasury Department opened a second round of public comment on implementing the GENIUS Act in September 2025, signaling the administration’s intent to craft a regulatory framework that fosters innovation while addressing illicit finance, consumer protections and financial stability concerns.

Key takeaways

- The GENIUS Act provides a federal framework and clarity for stablecoin issuers, but real impact depends on the specifics of forthcoming rulemaking by federal and state authorities.

- Regulators are prioritizing guardrails around reserve assets, anti-money-laundering checks, consumer protections and capital/liquidity requirements for issuers.

- The Treasury’s ongoing public consultation underscores a balance-driven approach: enabling innovation while mitigating systemic and illicit-finance risks.

- Past discussions of stability and trust in privately issued digital money inform the current stance, as officials warn against overreach that could undermine confidence in redemption at par during stress.

GENIUS Act’s framework under scrutiny

The GENIUS Act, signed into law on July 18, 2025, established a federal pathway for U.S. payment stablecoins, mandating one-to-one backing with reserve assets such as U.S. dollars and Treasury securities. The statute anticipated a phased rollout, taking effect 18 months after signing or 120 days after final agency rules are published, whichever comes later. The rulemaking process now centers on translating that framework into practical requirements for issuers, custodians, and the networks that support on-chain dollars.

Barr’s remarks reflect a broader tension in the policy agenda: while the law aims to reduce regulatory uncertainty and spur legitimate adoption, it also raises questions about how to supervise reserve management, ensure robust AML controls and prevent consumer harm if redemption experiences stress. In her view, clear guardrails are essential to prevent a repeat of past fragilities seen during financial upheavals when private money markets faced losses or liquidity strains.

The governance question is not purely theoretical. The act explicitly contemplates reserve-asset backing and the prudential requirements that might accompany it, including capital and liquidity standards. Barr cited the potential for regulatory arbitrage between federal and state authorities as a practical risk if rules are unevenly applied across jurisdictions, potentially fragmenting the market and complicating compliance for issuers operating nationwide.

Beyond issuance, the scope of control – such as whether regulators oversight beyond the mere act of minting stablecoins to include the management of reserves, settlement rails and treasury operations – remains a focal point for policy negotiators. Barr’s framing suggests that a comprehensive approach will be essential to maintain market integrity and reassure users that stablecoins remain a reliable, on-demand dollar proxy even under stress.

Safeguards, compliance frictions and market dynamics

One recurring theme in Barr’s remarks is the risk of illicit finance and the need for rigorous identity checks in secondary markets. The possibility that bad actors could circumvent oversight by acquiring stablecoins off-exchange underscores the demand for robust Know Your Customer and AML controls throughout the ecosystem. Regulators are weighing how to enforce identity verification without stifling legitimate financial activity or driving participants to opaque, cross-border channels.

Another area of focus is the management of reserve assets. The GENIUS Act envisions reserves that can include U.S. dollars and U.S. Treasuries, but the regulatory calculus around what constitutes acceptable collateral, how reserve liquidity is maintained and how stress scenarios are modeled remains unsettled. Barr pointed to the risk that issuers might pursue yields that look attractive in normal times but prove destabilizing when conditions tighten. These considerations are central to preserving confidence that stablecoins can be redeemed on demand at stable value.

The policy conversation is also being shaped by concurrent statements from other U.S. regulators. Fed Vice Chair for Supervision Michelle Bowman has indicated that capital and liquidity rules for stablecoin issuers are already in development, while the Federal Deposit Insurance Corporation chair has said the agency does not expect deposit insurance for stablecoins under the GENIUS framework. Taken together, the signals suggest a cautious but forward-moving rulemaking process designed to keep stablecoins within a managed risk envelope while supporting legitimate innovation.

From an investors’ perspective, the rulemaking trajectory matters for how quickly stablecoins can scale as a trusted payment instrument, and how exposure to reserve risk or issuer missteps is priced into the market. For users and builders—wallet providers, exchanges and on-chain infrastructure—the clarity around compliance expectations and reserve governance will influence product design, KYC workflows and treasury-management features. The line between activity that is permissible under the law and what would trigger supervisory action remains a critical area to watch as agencies publish draft rules and conduct public consultations.

What to watch next for the stablecoin voyage

With the GENIUS Act as the anchor, the regulatory timetable is shifting toward concrete rules that will define how stablecoins operate in the United States. The ongoing public-comment process signals a willingness to refine the framework to accommodate financial innovation while strengthening protections against financial crime and systemic risk. Key milestones to monitor include the issuance of final agency rules, the precise calibration of reserve-asset standards, and the delineation of permissible activities beyond straightforward issuance—such as on-chain settlement mechanics and intermediation functions by custodians.

Market participants should also gauge how other major economies approach stablecoins, as global operators weigh whether U.S. rules will remain the gold standard or push activity toward more permissive or restrictive jurisdictions. In the near term, investors may see a bifurcation: issuers that align quickly with evolving standards could gain faster access to U.S. markets, while those that lag might encounter higher compliance costs or restricted access to U.S. rails. For users, the prospect of stronger consumer protections and clearer redemption guarantees offers a more predictable environment, though it could come with increased onboarding checks and slower transactions in some cases.

Ultimately, Barr’s speech reinforces a central fact: the GENIUS Act is a landmark attempt to reconcile private, on-chain money with public safeguards. The outcome will hinge on the rigor of rulemaking and the resilience of the safeguards regulators implement. As the process unfolds, the industry will be watching not only how reserve assets are treated, but how the rules address specialized risks such as cross-border use, illicit financing channels and the potential for runs during shocks.

Readers should stay attentive to the pace of rule publication and the specifics agencies publish about capital, liquidity and AML standards, as those details will shape the feasibility and cost of compliant stablecoin programs in the United States.

The evolving regulatory backdrop underscores a broader theme for the crypto space: legitimate-scale adoption depends on credible assurances that stablecoins can deliver on the promise of speed, reliability and safety, without compromising financial stability or enabling misuse.

As policymakers refine the balance between innovation and protection, the market will likely respond with a mix of pragmatic partnerships, new compliance tooling and product innovations designed to navigate a tighter but clearer regulatory horizon.

What remains uncertain is how quickly final rules will land and how issuers, custody providers and exchanges will adapt to a potentially stricter regime. Still, Barr’s remarks emphasize a deliberate, risk-conscious path forward—one that could ultimately help stablecoins mature from niche tools into mainstream financial rails.

The $1.7 trillion asset manager will absorb the 250 Digital team and all liquid crypto strategies previously managed by CoinFund, targeting pensions and sovereign wealth funds.

TLDR

- Jamie Dimon said JPMorgan may enter the prediction markets sector in the future.

- He ruled out offering contracts tied to sports or political events.

- Goldman Sachs confirmed it is actively reviewing prediction market opportunities.

- Polymarket and Kalshi remain leading platforms as competition expands.

- Coinbase and Robinhood have added prediction trading to their services.

JPMorgan CEO Jamie Dimon said the bank may enter prediction markets as large institutions assess the fast-growing sector. He shared the update during a CBS interview on Tuesday. His remarks place JPMorgan alongside Goldman Sachs in reviewing potential offerings.

JPMorgan Reviews Prediction Markets Strategy

Dimon confirmed JPMorgan is studying the space but set clear limits. “It’s possible one day we’ll do something like that,” Dimon said. However, he ruled out markets tied to sports or politics.

He stressed that the bank would follow strict internal standards. “There’s a bunch of stuff we won’t do,” Dimon said. He added, “We have strict rules around insider information.”

Goldman Sachs has also advanced its review of prediction markets. CEO David Solomon addressed the topic during the bank’s January earnings call. He said the firm has engaged directly with industry leaders.

“I personally met with the two big prediction companies,” Solomon said. He said he spent hours learning about their models and leadership. He added that a team continues to evaluate the sector.

Neither bank has disclosed launch timelines. They have also not detailed technology choices or regulatory structures. However, their statements confirm active internal discussions.

Polymarket, Kalshi, and Rising Crypto Platforms

Prediction markets were once centered on two main platforms. Polymarket and Kalshi dominated the sector for years. Now, competition has expanded quickly across crypto and traditional firms.

Coinbase and Robinhood have integrated prediction market trading. These companies offer retail access through existing platforms. Their entry has increased user participation and market volume.

Polymarket operates on blockchain infrastructure using Polygon. Users deposit stablecoins and place outcome-based trades. Smart contracts record transactions and settle payouts automatically.

Kalshi uses a regulated exchange model without blockchain systems. It offers event contracts under centralized order matching. The platform handles settlement through traditional mechanisms.

Polymarket has secured partnerships and investment backing. It maintains ties with Intercontinental Exchange, which owns the New York Stock Exchange. The company holds an estimated $20 billion valuation.

Kalshi recently closed a funding round led by Coatue Management. The round valued the platform at about $22 billion. These figures reflect growing capital flows into prediction markets.

Regulation in the United States continues to evolve. Authorities assess how event contracts should be classified. Banks have indicated they will monitor policy developments closely.

Earlier this month, the Commodity Futures Trading Commission advanced oversight efforts. The agency outlined steps to build a regulatory framework. These actions mark the latest formal move shaping prediction markets in the U.S.

A crypto governance critique argues that token voting has not fulfilled its decentralized promise, and markets may offer a better coordination mechanism. In a perspective piece, Francesco Mosterts, co-founder of Umia, outlines why the early dream of “on-chain democracy” via token-weighted votes faces fundamental flaws—and how a market-based approach could reshape how on-chain organizations decide what to build and fund.

Mosterts emphasizes that crypto’s strength lies in markets: prices, incentives, and capital flows already coordinate almost every facet of the ecosystem, from token valuations to lending rates and blockspace demand. Yet when governance arrives, the system often abandons markets. He points to ongoing governance frictions across major protocols and a troubling pattern of participation and influence in DAOs. A recent study covering 50 DAOs found a persistent engagement gap: token holders vote inconsistently, and a single large voter can sway about 35% of outcomes, while four voters or fewer can influence two-thirds of decisions. In practice, this means governance power remains highly concentrated even as a decentralization narrative remains loud.

Key takeaways

- Token voting suffers from chronic underparticipation: most token holders abstain, leaving decisions to a small, active minority.

- Whales wield outsized influence, undermining the egalitarian premise of decentralized governance and risking outcomes dominated by a few large holders.

- There is no price signal attached to governance votes, creating misalignment between information, conviction, and action.

- Markets-based governance—where outcomes are priced and funded—could transform governance from expression of opinion into a mechanism of measurable conviction.

The promise and limits of token governance

The original vision of DAOs began with a simple idea: token holders would govern by voting on proposals, thereby aligning ownership with decision rights. The first wave of experiments—DAOs launched in 2016 and beyond—sought to replace centralized management with code-driven governance. Tokens, in theory, would symbolize both ownership and influence, enabling any participant to steer a protocol’s direction by casting a vote.

In practice, however, token voting has struggled to live up to that promise. Three core challenges repeatedly surface: participation, the dominance of whales, and incentive misalignment. Participation remains uneven, as many governance decisions require significant time and effort to review and analyze. The result is governance fatigue, with the majority of token holders remaining passive while a narrow cadre of participants makes the call on key proposals.

Whales compound the problem. Large holders can and do tilt outcomes, demoralizing ordinary voters who feel their input matters less than those with bigger balance sheets. This dynamic starkly contrasts with the ideal of a broad, democratic process where every tokenholder has a meaningful voice.

Then there’s the incentive issue. Governance voting lacks a direct economic signal—votes carry equal weight regardless of a voter’s information, due diligence, or risk tolerance. There is little price for being right or penalty for being wrong, which can encourage speculative or uninformed participation rather than careful, conviction-driven decision-making.

Why pricing decisions could fix governance

The argument pivots on a simple observation: crypto already uses markets to allocate capital, price risk, and signal conviction across a spectrum of activities. If governance can be integrated with pricing mechanisms, it could convert opinions into measurable expectations and align participation with real economic incentives. In other words, decision markets could monetize governance outcomes by letting participants buy and sell bets on proposed directions or policies, thereby revealing collective conviction through market activity.

Advocates of this approach point to several possible benefits. First, decision markets would incentivize participants to research proposals more thoroughly, because their capital at stake would fluctuate with the perceived success of a given outcome. Second, pricing governance outcomes would help surface true preferences and risk assessments, reducing the influence of uninformed voting and opportunistic behavior. Finally, markets could extend beyond mere protocol decisions to broader capital allocation—funding the most promising initiatives with transparent, incentive-aligned mechanisms from inception.

There is a growing sense in the ecosystem that the governance bottleneck—characterized by protracted debates, treasury disputes, and stalled proposals—is a symptom of the misalignment between how decisions are made and how value is created. If crypto wants governance to be a true coordination engine, it may need to borrow from markets more aggressively. Predictions markets, futures-like payoffs on governance outcomes, and futarchy-inspired mechanisms are increasingly revisited as potential pathways to price governance bets and coordinate action around credible forecasts.

What changes when governance is priced, not just voted on

Framing governance as a pricing problem could shift the dynamic from passive endorsement to active, informed risk assessment. By attaching economic signals to decisions, participants would be exposed to the consequences of their bets in real-time, incentivizing careful evaluation of proposals and potential trade-offs. The broader implication is a move from “vote for my preferred outcome” to “trade for the outcome you expect to materialize.”

Beyond improving participation and alignment, decision markets could influence how on-chain organizations allocate resources from day one. Startups and protocols might raise capital with built-in incentive structures for governance that reflect the true costs and benefits of proposed initiatives. In this view, token voting remains valuable for signaling preferences, but it becomes part of a wider system where markets determine which directions receive support and funding, and within what conditions.

As the ecosystem debates these ideas, it’s worth noting that some observers have already flagged governance tensions at prominent protocols. For example, coverage from Cointelegraph highlighted governance disputes around Aave’s exit from a DAO governance framework, underscoring the fragility of current models when high-stakes decisions collide with real-world incentives. The ongoing tug-of-war between governance control and treasury strategy illustrates how far the current approach is from a scalable, market-informed model.

What to watch next as markets reshape on-chain governance

The broader market is watching for experiments that meaningfully integrate pricing into governance. If decision markets can demonstrate durable improvements in decision quality and coordination speed without compromising decentralization, they could become a central feature of the next generation of on-chain organizations. The revival of discussions around futarchy, prediction markets, and other market-based coordination tools points to a phase of crypto where governance becomes less about voting rituals and more about economically rational decision-making under uncertainty.

Still, several questions remain unresolved. How would such markets be designed to prevent manipulation or collusion? What safeguards would ensure that price signals reflect diverse risk tolerances and long-term value creation rather than short-term speculation? And how would regulators treat on-chain decision markets that directly influence capital allocation and product strategy?

What’s clear is that token voting, while historically significant as crypto’s first big governance experiment, is unlikely to be the final answer to decentralized coordination. The next era could see governance complemented, or even superseded, by markets that price outcomes, align incentives, and actively guide what gets built with transparent, market-driven signals.

In the meantime, readers should monitor ongoing debates about how to harmonize decentralization with effective governance, particularly where treasury management, proposal execution, and cross-chain coordination are concerned. The direction crypto takes next—whether sticking with traditional voting or embracing a pricing-based framework—will shape how communities decide and fund the protocols they rely on every day.

Ripple XRP moved closer to full national trust bank status on April 1 as the OCC’s final rule – detailed in Bulletin 2026-4 – took effect, formalizing a regulatory framework that directly enables Ripple’s conditionally approved national trust bank charter to progress toward operational status.

The rule revises chartering regulation to allow national trust banks to conduct non-fiduciary activities alongside fiduciary ones, expanding the scope of what Ripple National Trust Bank can legally offer once pre-opening conditions are satisfied.

XRP traded at $1.3364 on April 1, with technical indicators shifting bullish for the first time in two weeks as the regulatory milestone landed.

The OCC issued this rule after conditionally approving charters for Ripple National Trust Bank, First National Digital Currency Bank, BitGo, Fidelity, and Paxos – a cluster of approvals that signals the agency’s deliberate move to integrate crypto-native and crypto-adjacent institutions into the federally regulated banking system.

That this rule arrives under a Trump-era OCC that has explicitly positioned itself as pro-crypto makes the timing more than procedural: it is structural.

- Rule Scope: OCC Bulletin 2026-4 takes effect April 1, expanding national trust bank authority to include non-fiduciary activities – custody and safekeeping of digital assets now explicitly in scope.

- Ripple’s Position: Ripple National Trust Bank holds conditional OCC approval from December 2025, pending satisfaction of AML, KYC, capital adequacy, and risk control conditions before full operations begin.

- Regulatory Background: XRP was classified as a digital commodity by the SEC and CFTC on March 17, 2026, clearing the legal ambiguity that had shadowed Ripple’s institutional adoption narrative for years.

- XRP Market Impact: XRP price sat at $1.3364 on April 1, with bullish technicals emerging for the first time in two weeks; exchange outflows signal accumulation among holders amid the regulatory catalyst.

- What to Watch: Ripple’s Federal Reserve master account application is the next gating variable – Kraken’s approval sets a precedent, and Ripple’s clearance would give it direct access to Fed payment rails.

Discover: Top Crypto Presales to Watch Before They Launch

What the OCC Final Rule Actually Does – and Why the Terminology Change Matters

The core mechanism of OCC Bulletin 2026-4 is a terminological revision that carries operational weight: the agency replaced the phrase “fiduciary activities” with “operations of a trust company and activities related thereto” in its chartering regulation.

That distinction matters. Under the prior framework, national trust bank charters were more narrowly scoped around fiduciary functions – managing assets on behalf of clients in a representative capacity. The revised language explicitly opens the door to non-fiduciary activities, which includes custody and safekeeping services where the institution holds assets but does not exercise discretionary management over them.

For digital asset firms, that difference is the entire product. Custody – holding client crypto assets under federal oversight without necessarily exercising fiduciary discretion – is the foundational service that institutional clients require before allocating capital through a regulated entity.

The OCC has been explicit that this rule neither expands nor contracts its chartering authority; it clarifies what charter-holders can operationally do. That framing matters because it neutralizes the argument that the OCC is overstepping – the agency is not creating new powers, it is specifying existing ones with enough precision for digital asset custody to fit cleanly within them.

The rule’s April 1 effective date follows a sequence: conditional approvals for Ripple, BitGo, Fidelity, and Paxos came first, and the final rule now establishes the operational framework those approved entities will operate under once their pre-opening conditions are cleared. Ripple’s path to full charter runs through this framework directly.

Ripple XRP Specific Position – From SEC Defendant to Federal Bank Applicant

The speed of Ripple’s regulatory repositioning over the past 18 months is the context that makes April 1 significant: a company that spent years fighting the SEC over whether XRP was an unregistered security received a digital commodity classification on March 17, 2026, and now holds a conditional OCC national trust bank charter – a trajectory that would have been unthinkable in 2023, and that now positions Ripple as one of the most institutionally credible crypto-native entities in the U.S. banking framework.

Ripple National Trust Bank’s conditional approval enables the company to operate as a federally regulated fiduciary, custody client assets under federal oversight, and integrate RLUSD – its stablecoin – and XRP-denominated products within U.S. banking infrastructure.

The remaining conditions – robust risk controls, compliance systems, AML and KYC procedures, and capital adequacy thresholds – must be satisfied before full operations begin. Commentator Xaif noted the rule’s potential to enable federal-level digital asset custody services for Ripple once those restrictions lift, framing it as infrastructure rather than just licensing.

"The digital marketplace is important to the future, and Ripple is the right partner to take us there." — Eddie Gonzalez, President, i-payout — Ripple (@Ripple) March 16, 2026

Ripple Payments helps i-payout deliver real-time payouts into the U.S. & Canada, from days to seconds.

See how →… pic.twitter.com/WWNmJc9utQ

Ripple has also applied for a Fed master account, which would give it direct access to Federal Reserve payment rails – the same access Kraken recently received approval for.

Analysts tracking XRP’s institutional adoption narrative have flagged the Fed master account as the variable that converts national trust bank status into full-stack banking capability. The Bank Policy Institute, representing JPMorgan, Goldman Sachs, and Citigroup, is reportedly weighing a lawsuit against the OCC over crypto firm charters – a sign that incumbent banks view these approvals as competitive threats, not bureaucratic formalities.

Explore: Best Crypto Projects With High Growth Potential in 2026

The post Ripple XRP Nears National Bank Status as OCC Rule Takes Effect April 1 appeared first on Cryptonews.

TLDR

- Gnosis, Zisk, and the Ethereum Foundation launched the Ethereum Economic Zone at EthCC 2026 in Cannes.

- The framework aims to connect more than 20 Ethereum layer two networks under a unified structure.

- The Ethereum Economic Zone enables synchronous smart contract calls across rollups and the mainnet.

- The system uses ETH as the default gas token and removes separate bridge requirements.

- Early partners include Aave, Centrifuge, and a Swiss-based EEZ Alliance.

The Ethereum Economic Zone launched on March 29 at EthCC in Cannes to address layer-2 fragmentation. Gnosis, Zisk, and the Ethereum Foundation introduced the rollup framework at the Palais des Festivals. The initiative aims to unify liquidity and restore synchronous composability across the Ethereum mainnet and participating rollups.

Ethereum Economic Zone framework targets L2 fragmentation

Gnosis, Zisk, and the Ethereum Foundation presented the Ethereum Economic Zone during EthCC 2026 in Cannes. They introduced a rollup framework that connects multiple layer-2 networks under a shared structure. The project seeks to reduce fragmentation across more than 20 operational Ethereum L2s.

Those networks currently secure about $40 billion in assets but operate as isolated systems. Each L2 maintains separate liquidity pools, deployments, and bridge infrastructure. As a result, users and developers navigate disconnected environments.

Gnosis co-founder Friederike Ernst addressed this issue during the conference. She said, “Ethereum doesn’t have a scaling problem. It has a fragmentation problem.” She added that each new L2 creates another isolated liquidity pool and bridge.

The Ethereum Economic Zone enables smart contracts to perform synchronous calls across rollups and the mainnet. It allows atomic transactions that execute across networks within a single process. The framework also uses ETH as the default gas token.

Developers can remove separate bridge protocols under this structure. The system keeps security anchored to Ethereum’s base chain. Project backers said the design restores composability between rollups.

Zisk developer Jordi Baylina joined Ernst during the presentation. They described the framework as aligned with Ethereum’s scaling roadmap. The collaboration receives co-funding from the Ethereum Foundation.

Zisk CEO Maria Roberts spoke during the event. She said, “The zone will facilitate a new era of blockchain innovation.” She added that developers can integrate existing applications into the framework “pretty easily.”

Conference highlights institutional focus and market data

Early partners include Aave, Centrifuge, and a Swiss-based EEZ Alliance. Organizers confirmed these groups joined at launch. Coverage from The Block and CoinDesk reported their participation.

Ethereum’s shift toward cheaper L2 networks has reduced mainnet fee revenue. ETH trades near $2,000 according to recent market data. The network secures about $53 billion in DeFi total value locked.

Stablecoins on Ethereum account for about $163 billion in value. Market data cited by Phemex outlined these figures. Organizers positioned EEZ as a structural upgrade for capital flow efficiency.

EthCC organizers described 2026 as “the year of professionalisation of Ethereum and the wider crypto ecosystem.”

The conference relocated to Cannes for this edition. The event featured institution-focused forums.

Kaiko launched its Agora forum during the conference. Organizers said the forum targets professional market participants. They highlighted infrastructure and market structure discussions.

Separate reporting referenced Kaiko’s findings on market structure gaps. One report stated that an Alameda trading gap still exists. The conference sessions addressed transparency and liquidity topics.

The Ethereum Economic Zone framework officially went live during EthCC. Project representatives confirmed that onboarding discussions continue with other L2 teams. The launch took place on March 29 at the Palais des Festivals in Cannes.

By Omkar Godbole (All times ET unless indicated otherwise)

As the new quarter gets underway, the crypto market is sending a subtle but important signal: traders seem a bit more cautious about bitcoin than ether (ETH).

You can see this in the options market, where more experienced traders and institutions go to hedge risk or generate extra returns. Think of options as a kind of insurance. Traders can buy protection against price drops (puts) or bet on price increases (calls), depending on their outlook.

Right now, one key metric, called a risk reversal, is negative for both bitcoin and ether across different time frames. In simple terms, that means puts, or downside protection, is more expensive than bullish bets. When traders are willing to pay more for put options, it usually signals lingering fears of a price drop. That’s perfectly normal, considering the brutal downtrend in bitcoin and ether since October.

But here’s where it gets interesting: that caution is stronger for bitcoin. Put options on bitcoin are more expensive than those on ether across all time frames, suggesting traders are more worried about BTC’s downside risk.

The difference becomes even clearer when zooming further out. Longer-dated ether options, such as those expiring next March, are only slightly bearish, while bitcoin’s equivalent options carry a much steeper premium for downside protection.

In short, the market is betting that ether will be relatively resilient. That would signal a bullish trend change in the ether-to-bitcoin ratio, which has been in a downtrend since August (see the technical analysis section).

Ether has risen 5% over the past 24 hours, outpacing bitcoin , XRP (XRP), solana (SOL), and the CoinDesk 20 Index. Several smaller tokens associated with quantum-computing-resistant technology have rallied by 20% or more.

Analysts said a firm breakout in BTC above its 50-day moving average of $68,680 will likely strengthen the bullish momentum.

In traditional markets, the 10-year U.S. Treasury yield fell for the fourth straight day while futures tied to the Nasdaq and S&P 500 rose nearly 0.5%. Together, these things point to risk-on sentiment ahead. Stay alert

Read more: For analysis of today’s activity in altcoins and derivatives, see Crypto Markets Today

What to Watch

For a more comprehensive list of events this week, see CoinDesk’s “Crypto Week Ahead“.

- Crypto

- Macro

- April 1, 8:15 a.m.: U.S. ADP Employment Change for March (Prev. 63K)

- April 1, 10:00 a.m.: U.S. ISM Manufacturing PMI for March (Prev. 52.4)

- Earnings (Estimates based on FactSet data)

Token Events

For a more comprehensive list of events this week, see CoinDesk’s “Crypto Week Ahead“.

- Governance votes & calls

- Unlocks

- Token Launches

- April 1: Orexn (OXN) enters a phased exchange listing period after the token generation event.

Conferences

For a more comprehensive list of events this week, see CoinDesk’s “Crypto Week Ahead“.

Market Movements

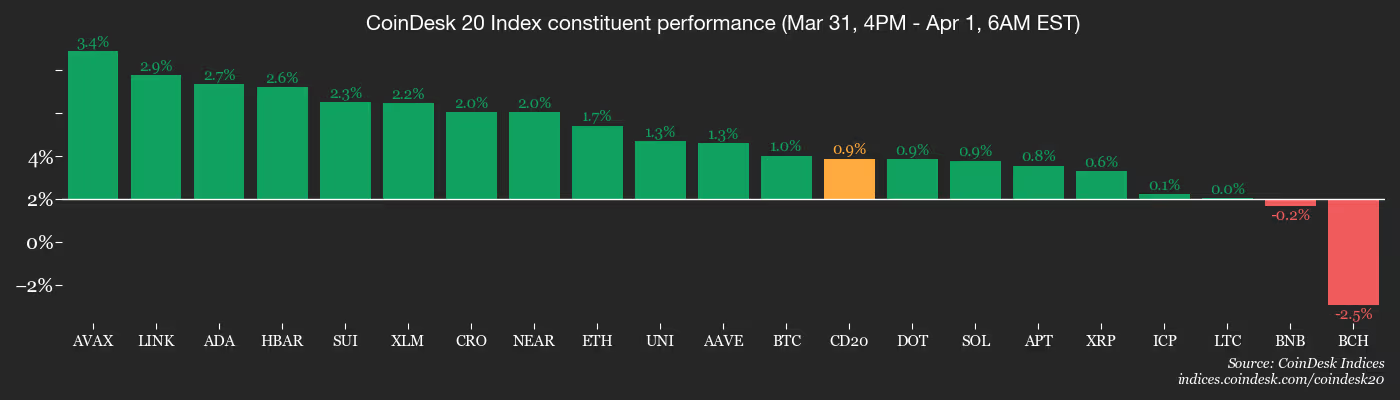

- BTC is up 0.61% from 4 p.m. ET Wednesday at $68,622.64 (24hrs: +3.34%)

- ETH is up 1.47% at $2,136.90(24hrs: +5.27%)

- CoinDesk 20 is up 0.62% at 1,968.28 (24hrs: +3.62%)

- Ether CESR Composite Staking Rate is unchanged at 2.76%

- BTC funding rate is at 0.0033% (3.5193% annualized) on Binance

- DXY is down 0.37% at 99.59

- Gold futures are up 1.5% at $4,748.80

- Silver futures are down 0.69% at $74.40

- Nikkei 225 closed up 5.24% at 53,739.68

- Hang Seng closed up 2.04% at 25,294.03

- FTSE is up 1.63% at 10,342.45

- Euro Stoxx 50 is up 1.75% at 5,667.09

- DJIA closed on Tuesday up 2.49% at 46,341.51

- S&P 500 closed up 2.91% at 6,528.52

- Nasdaq Composite closed up 3.83% at 21,590.63

- S&P/TSX Composite closed up 2.61% at 32,768.04

- S&P 40 Latin America closed up 4.26% at 3,623.86

- U.S. 10-Year Treasury rate is down 3.2 bps at 4.279%

- E-mini S&P 500 futures are up 0.33% at 6,592.25

- E-mini Nasdaq-100 futures are up 0.48% at 24,030.25

- E-mini Dow Jones Industrial Average Index futures are up 0.36% at 46,750.00

Bitcoin Stats

- BTC Dominance: 58.72% (-0.04%)

- Ether-bitcoin ratio: 0.03111 (0.89%)

- Hashrate (seven-day moving average): 1,004 EH/s

- Hashprice (spot): $32.37

- Total fees: 2.47 BTC / $166,441

- CME Futures Open Interest: 104,900 BTC

- BTC priced in gold: 14.5 oz.

- BTC vs gold market cap: 4.58%

Technical Analysis

- The chart shows daily swings in the ether-bitcoin ratio in the candlestick format.

- The ratio has been trending lower since August, showcasing ether underperformance relative to bitcoin. This downtrend is represented by the yellow line that connects the steady decline over seven months.

- The outlook would flip bullish if the ratio rises past this trendline. Such a move would confirm renewed investor preference for ether, as suggested by the options market.

Crypto Equities

- Coinbase Global (COIN): closed on Tuesday at $174.61 (+8.60%), +1.80% at $177.75 in pre-market

- Circle Internet (CRCL): closed at $95.41 (+6.12%), +2.69% at $97.98

- Galaxy Digital (GLXY): closed at $18.45 (+7.58%), +1.94% at $18.81

- Bullish (BLSH): closed at $35.73 (+7.39%), +0.95% at $36.07

- MARA Holdings (MARA): closed at $8.16 (+4.62%), +1.35% at $8.27

- Riot Platforms (RIOT): closed at $12.36 (+4.48%), +2.35% at $12.65

- Core Scientific (CORZ): closed at $14.96 (+7.55%), -0.40% at $14.90

- CleanSpark (CLSK): closed at $8.51 (+4.03%), +2.12% at $8.69

- CoinShares Valkyrie Bitcoin Miners ETF (WGMI): closed at $34.82 (+7.70%), +1.81% at $35.45

- Exodus Movement (EXOD): closed at $6.50 (+4.84%), -0.92% at $6.44

Crypto Treasury Companies

- Strategy (MSTR): closed at $124.80 (+2.77%), +1.48% at $126.65

- Strive (ASST): closed at $10.02 (+6.94%), +1.90% at $10.21

- SharpLink Gaming (SBET): closed at $6.45 (+7.32%), +2.02% at $6.58

- Upexi (UPXI): closed at $0.99 (+3.90%), +6.49% at $1.05

- Lite Strategy (LITS): closed at $1.16 (+11.54%)

ETF Flows

Spot BTC ETFs

- Daily net flow: $117.5 million

- Cumulative net flows: $56.09 billion

- Total BTC holdings ~ 1.29 million

Spot ETH ETFs

- Daily net flow: $31.2 million

- Cumulative net flows: $11.59 billion

- Total ETH holdings ~ 5.70 million

Source: Farside Investors

While You Were Sleeping

Trump says Iran war could end in ‘two weeks’, with or without deal (euronews): Trump, who will address the nation Wednesday night, said the war in Iran could end in two to three weeks. However, Israeli Prime Minister Benjamin Netanyahu said its war on Tehran will continue.

Iran fires missiles across Middle East as Trump signals exit (Bloomberg): Iran fired missiles across the Middle East while Israel and the U.S. kept up their bombardment of the Islamic Republic, even as Trump fueled market optimism by signaling he’s preparing to end the war.

UAE wants to force Hormuz open and is willing to join the fight (The Wall Street Journal): The UAE is preparing to help the U.S. and other allies open the Strait of Hormuz by force, Arab officials said, a move that would make it the first Persian Gulf country to join the war.

Crypto asset manager CoinShares to list on Nasdaq after $1.2 billion SPAC deal (CoinDesk): CoinShares, a leading European digital asset manager with over $6 billion under management, is set to begin trading on the Nasdaq Stock Market under the ticker symbol CSHR.

Summary

- EthCC 2026 in Cannes has introduced a dedicated institutional forum, The Agora by Kaiko, drawing more than 60 speakers and around 600 participants from traditional finance and Web3.

- For the first time, firms like Bloomberg, S&P Global, BNP Paribas, Euroclear, Amundi, SG Forge and Tradeweb are on the official EthCC agenda to debate Ethereum’s market structure under Europe’s MiCA regime.

- With MiCA and new EU tax rules nearing full implementation, panellists argued that Ethereum’s future liquidity and depth will increasingly depend on institutional rails rather than purely on retail-driven DeFi.

EthCC 2026 has shifted decisively from a builders’ retreat to an institutional showcase, as this year’s edition in Cannes hosts the inaugural “Agora” forum curated by market data provider Kaiko for more than 60 expert speakers and roughly 600 TradFi and crypto-market professionals.

Held on March 31 at the JW Marriott and branded as a neutral stage “where the foundations of digital market structure will be examined,” the event is explicitly designed for executives from banks, asset managers, trading venues and blockchain projects to interrogate how far crypto and digital assets can underpin the next generation of financial infrastructure.

If previous EthCC editions were best known for governance wars and protocol roadmaps, Cannes has brought bankers directly into the developers’ line of sight. Reporting from French outlet CrypCool notes that “Jean‑Marc Stenger, PDG de SG Forge,” alongside Aave founder Stani Kulechov and representatives from Euroclear, Bloomberg, BNP Paribas, S&P Global, Amundi, Google and Tradeweb, are now part of the official program, with Euroclear’s Isabelle Delorme cited as evidence that “l’institution est désormais dans la salle.” A separate analysis from TechFlow captures the mood shift more bluntly: “What was new was the formal participation of traditional financial institutions… on EthCC’s official agenda for the first time,” the publication writes, arguing that developers and market-structure professionals are finally sharing the same stage rather than operating in parallel tracks.

The core of the Agora’s agenda is not token launches but plumbing. According to Kaiko’s event materials, discussion tracks span tokenization of financial instruments, perpetual futures and ETPs, collateral mobility, and the convergence between centralized and decentralized venues. As one invitation post from Kaiko’s Hadrien Comte on LinkedIn put it, the goal is “a day of conversation focusing on tokenization, market infrastructure transformation, capital efficiency in institutional crypto, and next-generation digital asset investment strategies” rather than marketing pitches.

Underpinning those debates is Europe’s maturing regulatory environment. Commentaries from TechFlow, ODaily and Moomoo all highlight a “regulatory puzzle” coalescing around the EU’s Markets in Crypto‑Assets Regulation (MiCA), which is expected to be fully implemented by mid‑2026 and will cover trading platforms, stablecoin issuers and institutional participants. Combined with new EU‑wide and national tax-reporting frameworks for digital assets, that clarity offers the legal scaffolding banks and asset managers say they need before committing more balance sheet to Ethereum-based products.

For Ethereum (ETH) itself, the message from Cannes is that future liquidity may rely as much on regulated rails as on organic DeFi flows. CrypCool argues that the involvement of SG Forge, Euroclear and Tradeweb in Ethereum debates “valide une thèse: la convergence TradFi/DeFi est un chantier opérationnel,” adding that for ETH holders “la profondeur institutionnelle du marché se construit en partie ici.” That view is echoed in a Phemex dispatch, which describes EthCC 2026 as marking “un changement significatif dans l’écosystème Ethereum, avec la participation… d’institutions financières traditionnelles” and the launch of The Agora as a forum dedicated to aligning digital assets with traditional capital markets.

In short, EthCC’s centre of gravity has moved. The same conference that once incubated “governance meme” experiments now features Bloomberg terminals, Euroclear settlement specialists and bank capital-markets teams arguing over how Ethereum’s blockspace, rollups and collateral models fit into their risk frameworks. Whether that ultimately leads to deeper, more stable liquidity for ETH or dilutes the ecosystem’s grassroots ethos is a debate that will likely continue long after the lights go down in Cannes.

Key takeaways

-

Meta plans to introduce dollar-linked stablecoin payments across its platforms in late 2026. Unlike its earlier Libra attempt, the company will not issue its own cryptocurrency but instead integrate existing stablecoins.

-

Regulatory opposition to the Libra/Diem project made it clear that governments were uncomfortable with Big Tech issuing private global currencies. Meta’s new strategy reflects those lessons by avoiding direct control over the currency itself.

-

Instead of managing stablecoin reserves or issuance, Meta intends to work with external partners that handle infrastructure, compliance and settlement, while Meta itself focuses on user experience and payment distribution.

-

With billions of users across Facebook, Instagram and WhatsApp, Meta can embed stablecoin payments into everyday social and commercial interactions, potentially creating one of the largest digital payment ecosystems.

Meta is re-entering the stablecoin market with a revised strategy. Following the regulatory challenges that ended its previous Libra project, the company plans to introduce dollar-linked digital payments across its social media platforms in late 2026.

Rather than developing its own cryptocurrency, Meta is now opting to facilitate third-party stablecoins on its apps. This approach indicates a shift in focus. Instead of managing the currency itself, the company aims to leverage its massive user base to control how and where these transactions occur.

This article explores why Meta’s 2026 stablecoin strategy relies on partnerships rather than issuing its own currency. It examines how regulatory lessons from Libra, new stablecoin rules and Meta’s vast platform distribution are shaping a model focused on payment integration rather than monetary control.

The enduring lesson of Libra

To understand why Meta is being cautious with digital payments today, you need to look at its earlier attempt.

In June 2019, Meta, then Facebook, announced Libra, an ambitious plan to create a global digital currency linked to a basket of traditional currencies. The idea was to enable fast, low-cost payments across Facebook, WhatsApp and Instagram and to build a new cross-border payment system used by billions of people.

However, regulators quickly pushed back.

Governments in the US, Europe and other regions raised several concerns. They worried that a prominent private company launching a currency could weaken national monetary control and create risks to financial stability. There were also concerns about inadequate safeguards against money laundering and illicit finance. Meta’s past controversies over data privacy, including the Cambridge Analytica scandal, further deepened distrust.

The idea that a social media company with billions of users could launch something resembling a private global currency alarmed policymakers. Under strong political pressure, several partners left the project. Libra was later renamed Diem, but the project eventually shut down in 2022.

The episode made it clear that regulators would not accept Big Tech issuing its own currency. Meta’s current strategy reflects that lesson. Instead of creating a new coin, it now plans to integrate existing regulated stablecoins from partners and act mainly as a payments platform.

An alternative stablecoin approach for 2026

Meta is renewing its efforts in stablecoins, this time by integrating stablecoin payments directly into its platforms without issuing its own coin.

The company has issued requests for proposals (RFPs) to external partners capable of handling the back-end stablecoin infrastructure. Meta’s role would center on crafting a seamless user payment experience within its apps rather than managing the currency itself.

This could involve introducing a built-in digital wallet feature, allowing users to send and receive stablecoin payments throughout Meta’s ecosystem, which includes Facebook, Instagram and WhatsApp.

The planned rollout targets the second half of 2026.

This strategy marks a significant shift from the earlier Libra/Diem model. Instead of attempting to launch a new global monetary system, Meta is now positioning itself as a major distribution and user interface layer for established, regulated stablecoins like USDC (USDC) or USDt (USDT), potentially through partners such as Stripe.

Did you know? The term “stablecoin” was first widely used around 2014 and 2015, as crypto developers experimented with tokens designed to maintain stable value against fiat currencies, long before large tech platforms began exploring their payment potential.

Why partners may matter more than owning the power

At first glance, Meta’s decision to outsource stablecoin infrastructure could seem like a step back from control. It may actually amplify the company’s strengths.

Meta holds a wide distribution reach. With billions of active users across Facebook, Instagram and WhatsApp, it operates one of the planet’s largest communication and social networks. Seamlessly embedding stablecoin payments into these everyday apps could rapidly establish one of the world’s biggest digital payment ecosystems. It enables Meta to reach its objective without the need to issue a coin itself.

In this setup, real value shifts away from minting the currency and toward directing how and where it moves. Stablecoin issuers handle reserves, backing and regulatory compliance, while infrastructure providers manage settlement and back-end rails. What Meta brings to the table is the intuitive user interface, the social context and the daily transaction flow.

The Stripe angle

Stripe has become a front-runner for partnership in Meta’s revived stablecoin push. It has aggressively built its stablecoin capabilities, taking steps such as its acquisition of Bridge, a specialized crypto infrastructure firm that powers custody, transfers and blockchain-based payments at scale.

The ties between Meta and Stripe run deep. Stripe co-founder and CEO Patrick Collison joined Meta’s board of directors in April 2025, fueling speculation about closer strategic alignment between the two companies.

If Stripe, through Bridge, becomes the primary back-end partner, Meta gains instant access to a mature, regulated payments stack. This would help Meta bypass the heavy lift of building compliant infrastructure from the ground up. Stripe would own the complex financial pipeline, including settlement, compliance and reserves. Meta, on the other hand, would focus on delivering a frictionless, engaging user experience across its massive social ecosystem.

Regulatory changes have reshaped the industry

The evolution of the regulatory environment is a key reason Meta is choosing partners over power in its 2026 stablecoin push.

In 2025, the US passed the GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act). This law created a clear federal framework for payment stablecoins. It established strict requirements for 1:1 reserves with high-quality liquid assets. Other compliance requirements include issuer licensing and oversight, risk management, transparency through monthly reserve disclosures and consumer protections.

While the GENIUS Act brings much-needed clarity and promotes innovation in regulated stablecoins, it also imposes certain restrictions. Only permitted issuers, typically regulated banks, their subsidiaries or qualified nonbank entities, can legally issue payment stablecoins in the US.

This environment favors established, heavily regulated financial institutions and infrastructure providers over large consumer tech companies. By choosing to partner with compliant stablecoin issuers and infrastructure providers instead of issuing its own coin, Meta sidesteps regulatory burdens, compliance costs and intense scrutiny.

Did you know? The original Facebook payments system launched in 2009, allowing users to purchase virtual goods in games. It was one of Meta’s earliest experiments in building a payments ecosystem inside social platforms.

Stablecoins as the foundation for AI-driven commerce

Meta’s renewed focus on stablecoins also ties into a larger shift in technology. The company is making major investments in artificial intelligence (AI), with projections for 2026 indicating a capital expenditure (CapEx) range of $115 billion to $135 billion. A significant portion of this spending supports the development of autonomous digital agents. These are AI systems that can independently handle tasks such as shopping, booking services and executing payments on behalf of users.

In this scenario, stablecoins could serve as an ideal global settlement layer. These digital dollars offer instant, programmable, borderless transactions that machines can execute reliably and efficiently.

For Meta, embedding stablecoin payments could unlock several practical use cases, including:

-

Fast, low-cost cross-border payouts to creators worldwide

-

Seamless transactions in international marketplaces

-

Automated purchases and payments initiated by AI agents

-

Easier financial access and payments in emerging markets where traditional banking remains limited

In this context, stablecoins move beyond speculative crypto tools. They become essential infrastructure for machine-to-machine and AI-powered commerce.

Did you know? Stablecoins are widely used for international remittances and cross-border payments, particularly in regions where traditional bank transfers are slow or expensive.

The wider competition among platforms

Meta is not the only company exploring stablecoin payments.

Across the technology industry, major platforms are actively looking for ways to bring digital currencies into their ecosystems. The main goal is no longer to create and issue new coins. Instead, the focus is on controlling the payment systems built on top of existing stablecoins.

Shopify, for instance, facilitates payments in USDC on Base at checkout through partnerships with Coinbase and Stripe. PayPal’s PYUSD is designed for payments on PayPal and for transfers between PayPal, Venmo and external wallets or exchanges.

The reasoning is straightforward. When a platform enables and processes transactions, it gains valuable insight into users’ economic behavior. This information allows the company to develop new products and services tied to payments.

Stablecoins provide a practical solution. They enable programmable, instant and borderless payments without depending completely on traditional banks. For companies with hundreds of millions or billions of users worldwide, this represents a very large opportunity.

Risks remain significant

Even with a partnership-based approach, Meta’s stablecoin plan still faces certain risks.

-

Regulatory constraints: Regulatory attention on large technology companies continues to be strong, particularly when they enter financial services. Governments could introduce new rules or limits on how platforms offer or integrate digital payments.

-

Operational challenges: These include the risk of fraud, the need for strong wallet security, the high costs of regulatory compliance and the complexity of handling customer disputes at a very large scale.

-

User reluctance: Finally, the entire effort depends on whether users actually choose to use it. If the sign-up process feels too difficult, or if rules add too much extra friction, many people may simply stick with familiar payment methods such as cards or bank transfers.

Meta’s task will be to meet all regulatory requirements while keeping the experience simple and easy for users.

Cointelegraph maintains full editorial independence. Guides are produced without influence from advertisers, partners or commercial relationships. Content published in Guides does not constitute financial, legal or investment advice. Readers should conduct their own research and consult qualified professionals where appropriate.

The single step of going to a Slimming World class changed Anna’s life

AGPU Stock Doubles on April 1 as Axe Compute Lands $12M GPU Deals Fueling AI Infrastructure Push

Genius Group Clears $8.5M Debt After Bitcoin Sale

-

News Videos7 days ago

News Videos7 days agoParliament publishes latest register of MPs’ financial interests

-

Business6 days ago

Business6 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

Tech6 days ago

Tech6 days agoIntercom’s new post-trained Fin Apex 1.0 beats GPT-5.4 and Claude Sonnet 4.6 at customer service resolutions

-

NewsBeat5 days ago

NewsBeat5 days agoThe Story hosts event on Durham’s historic registers

-

Sports5 days ago

Sports5 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment2 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment4 days ago

Entertainment4 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World1 day ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Sports1 day ago

Sports1 day agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech3 days ago

Tech3 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Entertainment7 days ago

Entertainment7 days agoHBO’s Harry Potter Series Will Definitely Fail For One Big Reason, And It’s Not J.K. Rowling Or Snape

-

Crypto World2 days ago

Crypto World2 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Tech1 day ago

Tech1 day agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Fashion6 days ago

Fashion6 days agoEn Vogue in Brown Leather and Tailored Neutrals by Atelier Savoir, Styled by J Bolin

-

Politics2 days ago

Politics2 days agoShould Trump Be Scared Strait?

-

Tech1 day ago

Tech1 day agoEE TV is using AI to help you find something to watch

-

Fashion6 days ago

Fashion6 days agoWhat Are Your Favorite T-Shirts for the Weekend?

-

Fashion5 days ago

Fashion5 days agoWeekly News Update, 3.27.26 – Corporette.com

-

Tech2 days ago

Tech2 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Fashion4 days ago

Fashion4 days agoAmazon Sundays: Soft Spring Layers

You must be logged in to post a comment Login