Business

Bringing institutional-grade research to bonds is a game changer for retail investors: Saurav Ghosh of Jiraaf

Addressing this, Saurav Ghosh, Co-Founder of Jiraaf, believes that bringing institutional-grade research to the debt market could be a game changer for individual investors.

In an interaction with Kshitij Anand, he explains how traditional reliance on credit ratings often falls short, why issuance-level analysis is critical, and how structured research reports can help investors better understand risk, pricing, and liquidity.

Corporate bond funds are gaining traction for fixed-income investors seeking steady returns amid rising inflation risks and a potential pause in interest rate cuts. With yields at elevated levels, shorter-duration accrual strategies are favored over those betting on rate movements, offering attractive spreads over government securities and bank fixed deposits.

As bond investing becomes more mainstream, such tools could play a pivotal role in making retail investors more informed, confident, and efficient in building their portfolios. Edited Excerpts –

Kshitij Anand: To begin with, if you can help us understand what research reports are and why they are important for investors, which Jiraaf launched recently.

Saurav Ghosh: So, the job of any research report is to essentially simplify complex underlying investment opportunities. I would say most Indian investors are very familiar with the equity segment. There are multiple brokerage houses that release reports on particular companies and stocks. So, you will have, let us say, Motilal Oswal Financial Services giving a buy rating on Reliance Industries Ltd shares—so that is a research report.

Essentially, a research report covers business analysis, the underlying sector and industry that the companies are operating in, and what cash flows are expected. These are complex analyses, and finally, they provide a simplified summary at the end, with the objective of telling the reader what a possible decision could be after having read and consumed all the information in a very structured and simplified manner. So, that is the job of a research report.

Till now, it has mostly been relevant on the equity side of the Indian ecosystem. What we are trying to do is bring that same institutional-grade research to the debt market.

Kshitij Anand: Equity research reports have played a big role in making stock market investing much easier, so how have they helped retail investors?

Saurav Ghosh: Prior to these research reports being available, an Indian investor was not very confident about their own understanding of the subject matter or the underlying investment opportunity. Today, of course, everyone in India does their own kind of research as well because there are so many tools and avenues that are accessible. But while the data is available, how you consume it, summarise it, and come to a final conclusion differs from person to person.

Everyone is looking to build confidence in their own research, and having institutions do that research for you—or having these research reports available—gives every investor confidence in what they are actually investing in. So, as I said, if I am buying a Reliance Industries Ltd stock, I may feel I understand its business, but sometimes it is far more complex than my understanding.

When an institution breaks it down and presents it in a well-documented report, I feel that I understand the business better. I know the numbers better. And when, for example, Motilal Oswal Financial Services gives a buy rating or a target price, it also gives me confidence that this is a good-quality stock to invest in. That is the kind of confidence we are trying to build.

On the flip side, sometimes we also identify pitfalls. If someone gives a sell rating, it may be because they have considered certain factors that we have not. This can help us avoid a bad decision as well. So, that is the aim of research reports.

On the equity side, investors today are far more evolved, financially aware, and actively making investment decisions because research reports have essentially hand-held Indian investors over the last one or two decades. That is also why the understanding of the equity market has evolved to where it is today.

Kshitij Anand: And in fact, if you look at the equity markets, investors have access to research reports, but the Indian bond market did not really have something equivalent to what equity investors used to have. So, why did that gap persist?

Saurav Ghosh: Bond markets are evolving, and traditionally, the bond market has largely been the playground for very large institutions in India. Since it has primarily been an institutional space, these participants have been doing their own in-house research and have not relied on external sources. They have large research and analytics teams, so they do not need to depend on external advice or information to make decisions. Because of this historical participation structure, there was no real need for research reports.

However, over the last three to four years, we have seen retail investors in India increasingly take an interest in bond markets. People are now actively seeking to invest in bonds and include them in their financial portfolios. With the growing participation of individual investors, there is now a need for institutional-grade research—similar to what exists in the equity market—to be made available in bond markets as well. This will help investors access high-quality insights, understand investments better, and ultimately evolve into more informed bond market participants.

Kshitij Anand: In the absence of quality issuance-level bond research, investors often relied mainly on credit ratings, as we discussed earlier in the podcast. What was the problem with that?

Saurav Ghosh: Credit ratings have largely been used as a proxy to assess risk in bond markets, not just by individual investors but also by institutions. However, they have several limitations when it comes to making investment decisions. Typically, a credit rating assesses the overall quality of a company, mostly from a long-term perspective. Ratings are broadly categorised into short-term (less than one year) and long-term ratings, such as AAA, AA, and so on. These primarily evaluate the business and the financial health of the company over a long horizon.

This approach has its limitations. For example, a company may be rated BBB because its five- or ten-year outlook is weaker than that of an AA- or A-rated company. However, that does not necessarily mean it is unsuitable for a one-year investment. A BBB-rated company could perform well in the near term due to favourable sectoral tailwinds, improving company fundamentals, strong collateral, or attractive pricing that enhances the risk-reward equation. Credit rating reports do not address these aspects.

They also do not evaluate whether pricing is competitive, what liquidity is available in the secondary market, or whether an investor can easily exit by finding a buyer. Additionally, they do not provide peer comparisons—how similarly rated issuers or companies in the same industry are priced and traded. These are critical factors for investors when making decisions, such as whether they are getting the best opportunity or the most attractive pricing.

Another key limitation is the lack of issuance-level analysis. In bond markets, investors participate in specific issuances, and each issuance can differ in terms of security, collateral, and covenants. While these are technical aspects, they essentially determine how well a particular issuance is structured from a risk perspective. Credit ratings assess the company as a whole but do not evaluate individual issuances. As a result, one issuance from a company may be highly secure and well-collateralised, while another may be unsecured and carry higher risk.

Since credit ratings often miss these nuances, it becomes important to cover them through institutional-grade research. This is why we have been among the first to introduce research reports for bond markets in India.

Kshitij Anand: I am sure you highlighted many aspects about issuances. So, did this over-reliance on ratings influence investor behaviour in the bond market? Do you see that trend as well?

Saurav Ghosh: One major influence of credit ratings has been on the underlying perception of risk among investors. People tend to believe that AAA- or AA-rated instruments are safe, while anything below that carries a high degree of risk. What individual investors are often unable to do today is quantify risk at each rating level.

While AAA-rated instruments are indeed among the safest in the bond market, it does not mean that a BBB-rated issuer is bad—it simply means it carries relatively higher risk than a AAA-rated issuer. The key question is: can I quantify that degree of risk? If I can, then I can also determine how much additional return I should expect for taking that extra risk, and whether the risk-reward equation is favourable.

This is an important aspect of investing in the bond and debt markets, which many investors struggle with due to the over-reliance on credit ratings as the sole measure of risk. Another important point is that, historically, for bonds with a tenor of less than two to three years, a BBB-rated issuer carries a default risk of less than 2%, while a AAA-rated issuer has a default risk of less than 0.3%. This means the probability of default increases by roughly 1.7% from AAA to BBB, with intermediate ratings falling proportionately in between.

At the same time, AAA-rated companies currently offer yields of around 7.5% in the Indian market, while BBB-rated companies may offer yields closer to 13%. This implies that investors are earning an additional yield of about 5.5% for taking an incremental default risk of around 1.5–1.7%. This is the perspective investors should consider when making decisions.

However, this kind of analysis is often missing due to the over-reliance on credit ratings as the only benchmark. That is why we aim to provide investors with better access to information and a more nuanced, issuance-level perspective, enabling them to make more informed decisions.

Kshitij Anand: Also, could you highlight that while a listed company has one listed equity, it can have multiple listed bonds? Why is that distinction important for investors to understand?

Saurav Ghosh: Yes, this is very important. A company raises debt multiple times during its lifecycle, and each time it does so through a separate issuance in the capital market. In contrast, in the equity market, when a company raises equity capital, all investors are treated equally. Each shareholder owns the same class of shares, and there is typically one share price.

In debt markets, however, each issuance can have different characteristics. For instance, every bond issuance has its own structure of security. It is important to understand whether a particular issuance is secured or unsecured, and if secured, what the underlying collateral is. Additionally, each issuance may come with different covenants. For example, if the company faces a rating downgrade, does the investor receive additional yield? Or do they have the option to exit through early redemption? These are important considerations.

Even for the same issuer, these features can vary from one issuance to another. This means that one issuance may carry a higher degree of risk than another, even though the issuer remains the same. Investors often assume that if a company is rated A, then all its issuances carry the same level of risk, but that is not necessarily true. At the issuance level, risk can vary based on factors such as security, covenants, and structure.

This is why it is crucial to analyse investment opportunities in the bond market at the issuance level. Our research reports aim to address this gap by focusing not just on issuer-level analysis but also on issuance-level details, rather than relying solely on credit ratings.

Kshitij Anand: Now that you have talked so much about research reports, could you also highlight what exactly an issuance-level bond research report is?

Saurav Ghosh: An issuance-level bond research report effectively covers five key aspects. First, we cover the business and the management. These are also partly covered in rating reports. This includes the history of the management, their credentials in running the business, and their background prior to this venture, among other details. It provides a comprehensive view of both the business and the management. On the business side, the report covers the market in which the company operates, the margins in the business, its customer base, and so on.

The second aspect is the financial analysis of the business. While this is also covered in credit rating reports, we go much deeper. The analysis includes profitability at the business level—not just current performance, but also the future outlook—as well as the inherent financial strength of the business, including leverage and other key metrics.

Beyond these two, the remaining aspects are not typically covered in credit rating reports. The third aspect is issuance assessment. Here, we analyse the security package, collateral, and repayment structure—whether payments are monthly or quarterly—as these factors can influence risk. We also compare the issuance with other issuances by the same company to determine whether it is the best available opportunity or if better options exist.

The fourth aspect is pricing. We evaluate how the issuance is priced relative to past issuances, peers within the same sector or rating category, and its pricing in the secondary market where institutional participants are active. This provides a complete perspective on valuation and also indicates the expected liquidity of the issuance.

The fifth aspect is the economic and sector outlook. If you are investing with a one- to two-year horizon, it is important to understand how the underlying sector is expected to perform over that period. A favourable macro or external environment reduces the likelihood of stress on the company.

Overall, the report is built around these five pillars, with the objective of arriving at a comprehensive scorecard that helps investors determine whether a particular issuance is worth participating in.

Kshitij Anand: From a broader perspective, why is issuance-level research especially important in the Indian bond market today?

Saurav Ghosh: I have already spoken about the importance of issuance-level details, but to summarise, there are two additional risks beyond credit risk that investors need to consider: liquidity risk and interest rate risk. These research reports help quantify those risks as well. While credit ratings provide insight into credit risk, issuance-level reports help investors understand liquidity—whether they can exit the investment easily—and whether the issuance is fairly priced.

If an investor enters at the right pricing, their interest rate risk is lower, and even if liquidity tightens, the impact on the bond’s capital value will be limited. This helps investors safeguard their investments and make better decisions.

Lastly, it is important to recognise that while the issuer remains the same, the quality of issuances can differ. A company may offer strong collateral and security to institutional investors but weaker terms in public issuances. Investors should not be at a disadvantage in such cases.

Overall, these reports empower investors with the right set of information to make more informed and confident investment decisions.

Kshitij Anand: And also, can issuance-level research change how investors build bond portfolios now?

Saurav Ghosh: Absolutely, because a lot of times, as I said, with the availability of issuance-level reports, investors will think differently. Let us say a particular BBB-rated company has a balance tenor of one year. Now, you are not just thinking of it as a BBB-rated company; you are thinking, while it is a BBB-rated company, can I take this risk for one year? I am not investing my money for five or ten years—I am just investing for the next one year. So, can I take that risk over this time frame?

With that understanding, people will construct their portfolios very differently because they will view risk differently. And once you look at risk differently, the way you construct your portfolio and think about generating yields and returns from it will completely change. So, with the availability of issuance-level reports, people will become smarter at constructing their financial portfolios than before.

Kshitij Anand: How does Jiraaf RA’s launch address this market gap now?

Saurav Ghosh: I think it is a big game changer. At Jiraaf, we have always been at the forefront of helping our investors gain maximum access to information so that they can make the right decisions. About three months ago, we launched our bond analyser, which is the first bond analytics platform in the ecosystem. It provided access to information, but investors still had to summarise and interpret that information themselves.

We have now taken this a step further with the launch of bond research. This means that investors not only have access to information, but also to structured and summarised insights derived from that data, presented in a simple and easy-to-understand manner. So, people do not need to do all the analysis themselves—they can read the research report and gain a strong understanding of the issuer and the issuance. This helps them make well-informed decisions about whether they want to include a particular bond in their portfolio.

As a result, decision-making becomes quicker, simpler, and more efficient. At Jiraaf, our intent is to provide investors with maximum clarity and complete transparency so that they can confidently make their investment decisions. This initiative goes a long way in enabling that.

Kshitij Anand: Could bond research reports do for bond investors what equity research reports did for stock investors? Can they match expectations? I am sure investors would want to know more about that.

Saurav Ghosh: Yes, 100%. Once you start trusting the research, you start trusting the institution. Over time, research reports can become an everyday tool, just like they have in the equity market. Investors can quickly go through a report—in 30 seconds to a minute—focus on the key data points, and arrive at an investment decision.

It becomes almost like being on autopilot—you see a report, review a few key metrics, and your decision is largely formed. I believe we will reach that stage in the bond market as well. In fact, institutional-grade research could have an even greater impact in the bond market than it has had in equities, because bonds are relatively more complex instruments that require deeper understanding. That is exactly what this initiative aims to provide.

(Disclaimer: Recommendations, suggestions, views, and opinions given by experts are their own. These do not represent the views of the Economic Times)

Australia’s share market has fallen for four of the past five weeks, following a storm of profit warnings, earnings disappointments, interest rate hikes and fuel security woes.

Claire Tyrrell speaks to Ella Loneragan about the state of major projects in South Perth, as development times ramp up.

“Overall, UK politics is a mess, there are already signs that foreign buyers are ditching the gilt market. If there is a major rout in the pound and/or gilts in the coming days, prospective candidates may need to assess whether now was a wise time to make a move against the PM,” she said.

Intuitive Machines Set To Launch In The Space Race

Hargreave Hale AIM VCT allots 105,364 shares at 33.55p

Zelenskiy condemns Russia after strike on Kyiv apartment block kills 24

Vodafone appoints Olaf Koch as non-executive director

“Trump has never had alcohol in his life. China gave him a beverage to toast, and Trump drank it. This is a very subtle, but STRONG statement on who’s really in charge,” claimed one viral social media post.

According to the Asian Business Daily, “During the proceedings, President Trump was seen raising his glass containing the toasting wine and bringing it to his lips, appearing to take a sip. He then handed the glass to a staff member, and cameras caught him seemingly holding the wine in his mouth for a moment before swallowing.”

Trump has repeatedly said he has never consumed alcohol — a rare claim among modern US presidents.

“I’ve never had a drink,” Trump told Fox News after his election victory in 2017.

According to the BBC, Trump’s decision to avoid alcohol stems from the death of his older brother, Freddie Trump, who died at the age of 42 from complications related to alcoholism.

Trump has also reportedly advised his children to stay away from drugs, alcohol and cigarettes.

However, Bruce LeVell, a former Trump adviser and former White House small business advocate, dismissed the viral speculation in a post on X, saying, “It’s not alcohol, and I speak for the President.”

In another post, he added, “President Trump does not drink or do drugs. You want a president like that.”

Trump was on an official visit to China on an invitation from Chinese president Xi Jinping. It was the first visit to China by a US president in nine years.

What happened during Trump’s China visit

Trump departed China on Friday while highlighting several business agreements reached during the trip, even as Beijing warned Washington against mishandling the sensitive Taiwan issue and criticised the Iran war.

“We’ve settled a lot of different problems that other people wouldn’t have been able to solve,” Trump said after meeting Chinese President Xi Jinping in Beijing on the second day of talks.

The discussions reportedly covered the Iran conflict, Taiwan, trade ties and other major geopolitical issues. While Xi did not publicly comment on his talks with Trump regarding Iran, China’s foreign ministry later issued a strong statement expressing frustration over the conflict.

I’ve been researching companies in-depth for over a decade, from commodities like oil, natural gas, gold and copper to tech like Google or Nokia and many emerging market stocks, which I believe could help me provide useful content for readers. After writing my own blog for about 3 years, I decided to switch to a value investing-focused YouTube channel, where I researched hundreds of different companies so far. I would say my favorite type of company to cover are metals and mining stocks, but I am comfortable with several other industries, such as consumer discretionary/staples, REITs and utilities.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

SEOUL — Investors weighing Samsung Electronics against SK Hynix for 2026 portfolios face a classic choice between diversified stability and pure-play AI growth as the global memory-chip supercycle intensifies. SK Hynix has surged ahead in high-bandwidth memory leadership and profitability, while Samsung leverages its vast resources to close the gap and offers broader exposure across semiconductors, smartphones and consumer electronics.

Both South Korean giants posted record first-quarter 2026 results driven by explosive demand for AI servers, but analysts give SK Hynix a slight edge for investors seeking maximum upside from the HBM boom. SK Hynix commands roughly 54 percent of the global HBM market and secured about 70 percent of NVIDIA’s HBM4 orders for the Vera Rubin platform, with its entire 2026 chip supply already sold out in key categories. Samsung, traditionally the larger player in conventional DRAM and NAND, is pouring more than $73 billion into chip expansion this year to regain ground.

The memory supercycle shows no signs of slowing. Surging AI infrastructure spending has pushed DRAM and NAND prices higher, with some server memory categories up more than 60 percent since late 2025. SK Hynix reported operating margins near 72 percent in Q1, while Samsung’s memory division approached similar levels despite broader business losses in foundry and system LSI.

SK Hynix: Pure AI Play with Explosive Momentum

SK Hynix stands out as the clearer beneficiary of the AI tailwind. Its focus on high-margin HBM products, critical for training and running large language models, has translated into record profits. The company’s operating profit in recent quarters has outpaced Samsung’s memory segment, with analysts forecasting continued dominance through 2027 as HBM4 shipments ramp.

Investors benefit from SK Hynix’s tight alignment with NVIDIA and other hyperscalers. The firm’s technological edge in stacking and thermal management gives it pricing power and near-term market share gains. Shares have responded with strong year-to-date gains, though valuations reflect the premium for leadership.

Risks remain. SK Hynix’s heavy concentration in memory leaves it more exposed to any slowdown in AI spending. Geopolitical tensions around its China facilities and potential U.S. export restrictions on advanced chips could also weigh on operations.

Samsung: Diversified Giant with Catch-Up Potential

Samsung offers a more balanced risk-reward profile. While lagging in HBM, the company is accelerating investments and has already raised prices on key chips by up to 60 percent. Its foundry, mobile and consumer electronics businesses provide natural hedges against memory cyclicality.

The conglomerate’s scale allows it to fund aggressive R&D and capacity expansion without the same financing constraints faced by pure-play competitors. Samsung’s upcoming HBM4 products and planned early deliveries could narrow the gap with SK Hynix by late 2026. Analysts highlight its long-term ability to leverage synergies across the value chain.

However, near-term challenges persist. Labor union tensions at Samsung’s key Pyeongtaek campus — which produces half of global DRAM and vital HBM — threaten production if strikes materialize in May and June. The company also carries higher exposure to cyclical consumer markets compared with SK Hynix.

Analyst Consensus and Valuation Comparison

Wall Street remains bullish on both. Samsung carries a Strong Buy consensus from 37 analysts with an average 12-month price target around KRW 274,000. SK Hynix earns similar enthusiasm, with many firms citing its HBM leadership as justification for a premium multiple.

Valuations reflect differing stories: SK Hynix trades at a higher forward price-to-earnings multiple justified by faster growth, while Samsung appears relatively cheaper on a diversified basis. Both offer attractive dividends relative to global tech peers, though SK Hynix’s payout is more modest given reinvestment needs.

Currency movements also matter. The Korean won’s fluctuations against the dollar can amplify or mute returns for international investors. South Korea’s export-driven economy ties both stocks closely to global trade and tech spending.

Broader Market and Economic Context

The AI memory boom forms part of a larger semiconductor upcycle. Data-center buildouts by hyperscalers continue at record pace, with HBM demand outstripping supply through at least 2027. Traditional DRAM and NAND markets benefit indirectly as customers stockpile ahead of shortages.

South Korea’s semiconductor sector, which both companies dominate, accounts for a massive portion of the KOSPI index. The iShares MSCI South Korea ETF provides convenient bundled exposure, with the pair comprising more than 25 percent of the fund.

Global risks include U.S.-China trade tensions, potential AI spending pauses and commodity price swings. On the positive side, any resolution in Middle East conflicts could ease energy costs and support broader economic growth.

Investment Recommendation for 2026

For growth-oriented investors chasing the purest AI memory exposure, SK Hynix edges out as the stronger 2026 pick. Its technological lead, sold-out capacity and sky-high margins position it to capture disproportionate upside from continued HBM demand.

Conservative or diversified investors may prefer Samsung for its scale, multiple business lines and potential to close the HBM gap. The stock offers a margin of safety through non-memory revenue streams and remains undervalued relative to growth prospects.

A balanced approach — owning both or using the MSCI South Korea ETF — mitigates single-company risk while capturing the sector tailwind. Dollar-cost averaging and monitoring quarterly results, especially HBM shipment updates and Samsung’s labor situation, will be key.

Neither stock is without volatility. Memory cycles have historically been dramatic, and AI hype could moderate if economic conditions shift. Yet current fundamentals — tight supply, strong pricing and multi-year demand visibility — support an upbeat outlook for both through 2026 and into 2027.

As the AI infrastructure buildout accelerates, the Samsung-SK Hynix duel will remain one of the most watched battles in global tech. Investors who correctly time entry into the memory supercycle could see substantial returns, but thorough research and risk management remain essential in this fast-moving sector.

Pharmaceutical Takeda to layoff 4,500 people from global workforce

My XRP Prediction For 2026 Will SHOCK YOU!! Raoul Pal

Democrats back independents in some red state races

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Marianne Dress

-

Fashion4 days ago

Fashion4 days agoCoffee Break: Travel Steam Iron

-

Fashion4 days ago

Fashion4 days agoWhat to Know Before Buying a Curling Wand or Curling Iron

-

Tech5 days ago

Tech5 days agoAuto Enthusiast Carves Functional Two-Stroke Engine from Solid Metal

-

Politics3 days ago

Politics3 days agoWhat to expect when you’re expecting a budget

-

Business6 days ago

Business6 days agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Politics6 days ago

Politics6 days agoPolitics Home Article | Starmer Enters The Danger Zone

-

Tech4 days ago

Tech4 days agoGM Agrees To Pay $12.75 Million To Settle California Lawsuit Over Misuse Of Customers’ Driving Data

-

Crypto World6 days ago

Crypto World6 days agoPROS explodes 48% as Upbit and Bithumb listings ignite demand

-

Crypto World5 days ago

Crypto World5 days agoCZ says US crypto rivals tried to block Trump pardon

-

Tech3 days ago

Tech3 days agoGM agrees to $12.75M California settlement over sale of drivers’ data

-

Entertainment7 days ago

Entertainment7 days agoYNW Melly Denied Bond Again Ahead Of Double Murder Retrial

-

Crypto World6 days ago

Crypto World6 days agoKraken Parent Seeks OCC Charter, Signaling Regulated Banking Access

-

Crypto World7 days ago

The Hantavirus Danger: Can a Potential Outbreak Spark a New Meme Coin Frenzy?

-

Sports7 days ago

Sports7 days agoAfter Waka Waka, Shakira now drops first teaser for FIFA WC 2026 song | FIFA World Cup 2022

-

Crypto World6 days ago

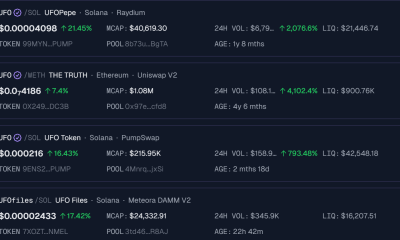

Crypto World6 days agoSolana UFO Meme Coins Surge After Pentagon Reveals Alien Files

-

Entertainment6 days ago

Entertainment6 days agoBethenny Frankel Says She Loves ‘Torturing’ Men

-

Tech7 days ago

Tech7 days agoThe Xperia 1 VIII leak finally gives Sony some swagger

-

Sports7 days ago

Sports7 days agoWhy Nathan Mackinnon Remains the Hart Trophy Favourite over Connor McDavid and Nikita Kucherov | NHL

-

Crypto World2 days ago

Bitcoin Suisse expands with Digital Asset License and Investment Business Act Registration Approval in Bermuda

You must be logged in to post a comment Login