Business

The Broyhill Q1 2026 Letter

Getty Images

When we look back. . . the nature of the forces currently in train will have presumably become clearer. We may conceivably conclude from that vantage point that. . . the American economy was experiencing a once-in-a-century acceleration of innovation, which propelled forward productivity, output, corporate profits, and stock prices at a pace not seen in generations, if ever. ¹

The Broyhill Equity Composite declined 6.0% in the first quarter, net of all fees and expenses, lagging global equity markets as the MSCI All Country World Index declined 3.1%. ² Individual performance may vary depending on individual account allocations, legacy positions, and capital flows. Detailed quarterly reports, including account and benchmark performance, portfolio holdings, and transaction history, have been posted to our investor portal.

After a strong start to the year for the portfolio, global stocks fell sharply following the strikes on Iran. Despite our defensive positioning, with nearly half the portfolio invested in noncyclical sectors, our stocks did not provide the protection we expected or that we’ve historically provided. While we don’t invest on a one-month horizon, nor do we place undue emphasis on short-term results, we do remain relentless in our work to protect your capital from significant market losses. So, I want to explain what drove the gap versus our expectations, because the context matters – and because we believe the setup from here is unusually compelling.

Three structural portfolio tilts moved against us simultaneously.

• We own no energy – the only sector with positive returns in March.

• Nearly half the portfolio is invested in businesses outside the U. S. , and European markets declined sharply given their higher sensitivity to energy prices (while this is broadly true of continental Europe, our companies have minimal exposure to the Middle East or the rising price of oil).

• Our large non-cyclical exposure – consumer staples and healthcare – underperformed in a down market, which is not supposed to happen and historically has not lasted.

What didn’t happen is as important as what did. Across the portfolio, businesses are performing well and meeting or exceeding our expectations. Consensus estimates continued rising even as our stock prices declined in March. That disconnect – improving fundamentals and falling prices – suggests this move was a positioning-driven sell-off, not a fundamental one. It’s also why we believe our stocks are poised to catch back up to fundamentals.

Performance Review

It’s hard not to be uber bullish when stocks are enjoying a once-in-a-century acceleration in innovation, resulting in a surge in productivity and corporate profits. But as it turns out, we are actually witnessing a twice-in-a-century acceleration in innovation, as the opening quote of this letter was first delivered by Former Fed Chairman Alan Greenspan in January 2000. As they say, history doesn’t repeat, but. . .

Top Contributors

Valvoline (VVV) was our largest contributor in the quarter. While the market spent its days hallucinating about the terminal value of artificial intelligence, Valvoline went on quietly changing oil, opening new stores, while moving more cars through its bays than any other competitor in the industry. Since we’ve owned it, shares have exhibited significantly more volatility than the business itself, but what matters is that the underlying unit economics are intact, while unit growth, service mix, and price continue moving in the same direction.

Honeywell (HON) was our second-largest contributor in the quarter. Management accelerated the aerospace spin-off, moving the separation up to the end of June and leaving behind a pure-play automation business. We continue to believe the pieces, including the recently announced Quantinum IPO, are worth meaningfully more than the whole. Upcoming Investor Days are the next chance for the market to do the math.

Ball Corporation (BALL) rounded out our top three contributors during the quarter. When we initially acquired the position, our thesis centered around the company’s post-aerospace-divestiture status, which left it a pure-play packaging company well positioned to return significant capital to investors. As the thesis played out, we sold into the re-rating and redeployed proceeds into more attractive opportunities.

Top Detractors

IQVIA (IQV) was our largest detractor despite fundamentals being far better than price action suggested. The stock has sold off because investors have convinced themselves that AI will compress economics faster than it drives demand. At the current price, we are more than willing to take the other side of that trade. Large pharma is structurally reliant on IQVIA’s clinical trial architecture and proprietary data assets, and we think it is highly unlikely that Claude can automate away the FDA approval process. While the burden of proof remains on the company, we believe we are being paid well to wait at the stock’s current valuation.

Louis Vuitton (LVMUY) was our second-largest detractor, posting its worst quarterly performance on record, driven by the Middle East conflict and fears of a broader slowdown in luxury demand. Beneath the headlines, Wines & Spirits delivered its biggest beat in years as the Hennessy destocking cycle ends, Watches & Jewelry beat as Tiffany continues to gain share, and Fashion & Leather continues its slow sequential improvement. The stock now trades at the bottom of its valuation range, which we find compelling for a business of this quality.

Avantor (AVTR) made our list of detractors for the last time in the first quarter. The destocking cycle has run far longer than we initially modeled, but the bigger issue was self-inflicted. Successive management teams failed to defend the share against Thermo Fisher (TMO). After swapping half of our position for Thermo last year, we took our

remaining lumps and redeployed the capital into Sotera Health (SHC), where litigation fears have created an opportunity to own a mission-critical sterilization duopoly at a meaningful discount to intrinsic value.

Key Transactions

We run a concentrated portfolio and aim to invest over a three- to five-year horizon. With roughly 20 positions, that translates into a handful of new ideas in a normal year. But like our returns, our ideas come in lumps, as volatility creates opportunity.

The extreme dispersion we saw in the first quarter handed us an opportunity to populate the book with at least a year’s worth of new ideas. Running towards controversy after big dislocations is our bread and butter. I suspect that’s a gene inherited from my father, who still fills his car to the ceiling with random items he doesn’t need from close-outs (most recently, Livingston Mall in NJ) or even relics of the past left on the roadside. In markets, such a strategy rarely guarantees short-term success, but over the long term, it has consistently been our most reliable generator of alpha.

During the quarter, we booked a portion of our gains on Phillip Morris (PM) and fully liquidated several positions. In addition to Ball, noted previously, we liquidated profitable investments in Kenedy Wilson (KW) and Fresenius Medical Care (FMS), as the former agreed to a higher bid from CEO Bill McMorrow and Fairfax Financial (FRFHF), and proceeds from the latter were redeployed into more attractive opportunities. We also fully liquidated two positions – Evolution (EVVTY) and Avantor – after reducing exposure to each, to reinvest in higher conviction ideas.

We initiated several new positions during the quarter. We bought Microsoft (MSFT) as the stock’s valuation declined to levels in line with the broader market. We initiated a new position in Smurfit WestRock (SW) with proceeds from Ball, as we suspect continued capacity tightening and additional pricing will drive mid-term results well above guidance and current consensus. We bought Sotera Health, a sterilization-franchise medical device business whose customers cannot easily replace it, where an ongoing tort overhang has created a price we believe materially underestimates the underlying business. And we established two new positions in the depressed housing industry – Masco (MAS) and Floor and Décor (FND), as we believe the normalized earnings power of both companies has increased significantly through market share gains and expense efficiencies captured during this extended downturn. We also began accumulating shares of Leggett & Platt (LEG), anticipating a higher bid from Somnigroup International (SGI), and fully exited when that bid emerged.

A Few Words on Healthcare

While investors have focused on the trillions of dollars in market capitalization that have evaporated from the software sector in recent months, the Medical Device and Life Sciences & Tools industries have not been far behind in terms of creative destruction. In the wake of this latest leg down, we significantly increased our investments in the sectors, bringing both IQVIA and Sotera Health into our top holdings.

Clinical research is one of the most regulated industries on the planet – and for good reasons. It’s literally a matter of life and death. And while Claude has dramatically increased our own productivity, we surmise that government agencies, including the FDA, will be somewhat slower to embrace these magical tools. When you consider that

AI adoption within at least one large, highly regulated US bank consists of mandates from management that employees use Copilot at least x times each week, the thought of the FDA entertaining a material shift in trial paradigms over the next several years seems exceedingly unlikely. To put the agency’s pace of change in perspective, regulators began accepting digital data submissions in PDF format less than a decade ago.

CROs, or Clinical Research Organizations like IQVIA, sit squarely in the crosshairs of investors’ concerns, given AI’s potential to completely reimagine how research is conducted. In fact, we’d even suggest that drug discovery may represent the single most significant benefit of AI as the quantity of new molecules tested and drugs coming to market accelerates at a pace beyond even the wildest imaginations of Watson and Crick. But despite our impressive leaps in understanding the human genome since its initial discovery, our understanding of human biology remains incomplete at best. And where we lack a deep understanding, we will still need experiments to test hypotheses and to observe how these drugs actually work amid the mystery of human biology, regardless of what AI models might promise.

While it may take time for the market to separate the wheat from the chaff, we expect that the Life Sciences Tools and broader research ecosystem will ultimately benefit from accelerating AI-driven demand for the data that fuels these models. And as AI compresses drug pipelines and increases the likelihood of clinical success, the growing number of drugs reaching the market will require more research, development, and tools. A recent analysis found that AI-designed molecules clear Phase I at 80-90%, compared with a historical average of 40-50% for conventional discoveries. ³ None of these candidates have been commercialized yet, but dozens have entered human trials, and several are now in Phase II. As Big Pharma’s return on investment improves, the rational response is to spend more on R&D, not less. Some functions will inevitably move back in-house, but we do not see the longer-term outsourcing trend reversing, as pharma simply doesn’t have the infrastructure or the data outside its own narrow indications. Bottom line: we think the data and scaled infrastructure that IQVIA provides will become meaningfully more effective, and a great deal safer, than a workflow vibe-coded by a pharmacist. We also think this makes the company more valuable, not less.

Recent channel checks support this view, framing AI more often as an opportunity than a threat. RFP flow and awards are improving as funding loosens and risk appetite returns; decision-making timelines are shortening, and pricing is firming. The bear case is that the majority of AI efficiencies gained by CROs will be captured by sponsors. But this ignores the fact that CROs have always been under pressure from Big Pharma to pass along savings. AI-generated efficiencies will certainly create additional opportunities to do so. This isn’t new. These companies have thrived for decades by finding ways to execute trials more efficiently, leveraging cost reductions into operating leverage to offset pricing pressures. That playbook hasn’t changed. But the price has shifted materially, with shares of IQVIA, for example, trading at half the broader market’s multiple, down from the 40% premium reached before COVID.

Bottom Line

We are keenly aware that our current positioning has weighed heavily on our relative performance of late. And we recognize that this has likely tested the patience of even our longest-duration investors. Simply owning a collection of good businesses does little to change that when their shares fail to deliver meaningful gains, while broader indices march steadily higher, and everyone around you is boasting about their biggest winners. While others are doing better at the moment, we think many are taking risks far greater than they appreciate. That is why we have stayed in our lane, rather than underwriting risks we don’t believe are properly priced.

Our job is to protect your capital while taking calculated risks to grow it over time. Periods like this test conviction. They also plant the seeds of future outperformance. This view may continue to cost us in the near term if momentum remains dominant over fundamentals. But with oil sitting in triple digits, geopolitics still in flux, and recorded crowding in US benchmarks trading at record valuations, we are willing to accept the risk of short-term underperformance because the reward for being correctly positioned when the market does turn has rarely looked more asymmetric than it does today.

While we cannot predict when that will arrive, what it will look like, or how quickly it will unfold, what we can tell you is that the portfolio is meaningfully cheaper today than it was at the start of the year. Importantly, our view of the underlying businesses we own has not changed: we believe they are worth considerably more than the market is giving them credit for. Rising tensions in the Middle East, regardless of how they unfold, would not change that assessment.

We have been here before. Our relative results have always been cyclical. But a decade of data tells a consistent story. We have seen the pattern clearly: periods where relative performance compresses (as we saw during the speculative rally immediately following COVID) have consistently been followed by sharp recoveries (many of which included short-term drawdowns as we experienced in March). The current dip looks a lot like previous ones, which have historically been followed by our best relative performance.

One More Thing

There is nothing to writing. All you do is sit down at a typewriter and bleed. – Ernest Hemingway

A few years after joining Broyhill in 2005, a friend suggested that I start a blog to share our insights, which had, until then, been distributed only internally. That site, The View from the Blue Ridge, was eventually folded into the firm’s website. Writing has always been a valuable tool for me, both personally and professionally. It has never been a particularly easy or enjoyable process, but the result usually justifies the effort. Through writing, I am able to flesh out my thinking, find holes in my logic, and distinguish highly confident ideas from those held more loosely. But as the business has grown, I’ve had less time to share our work publicly beyond these letters. Coming into this year, I decided it was time to change that.

We are excited to announce the launch of Vitruvian Value, where I will share our thinking, our ideas, our frameworks, and the lessons from running a concentrated portfolio through decades of market cycles, along with the occasional commentary on markets and human behavior.

We are grateful for your continued trust and partnership. We come into the office each day striving to earn it, and we realize just how fortunate we are to have such a wonderful group of like-minded, long-term investors who place their confidence in us. You enrich our network, strengthen our competitive advantage, and just make our work all the more enjoyable. As always, please feel free to reach out anytime with questions. We enjoy hearing from you.

Sincerely,

Christopher R. Pavese, CFA

References

- Remarks by Chairman Alan Greenspan Before the Economic Club of New York, January 2000

- For standardized performance data, including 1-year, 3-year, and since-inception net returns with benchmark comparisons, please refer to the Broyhill Equity Fact Sheet. Past performance is not indicative of future results.

- How Successful Are AI-Discovered Drugs in Clinical Trials, Drug Discovery Today (2024).

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Vodafone appoints Olaf Koch as non-executive director

“Trump has never had alcohol in his life. China gave him a beverage to toast, and Trump drank it. This is a very subtle, but STRONG statement on who’s really in charge,” claimed one viral social media post.

According to the Asian Business Daily, “During the proceedings, President Trump was seen raising his glass containing the toasting wine and bringing it to his lips, appearing to take a sip. He then handed the glass to a staff member, and cameras caught him seemingly holding the wine in his mouth for a moment before swallowing.”

Trump has repeatedly said he has never consumed alcohol — a rare claim among modern US presidents.

“I’ve never had a drink,” Trump told Fox News after his election victory in 2017.

According to the BBC, Trump’s decision to avoid alcohol stems from the death of his older brother, Freddie Trump, who died at the age of 42 from complications related to alcoholism.

Trump has also reportedly advised his children to stay away from drugs, alcohol and cigarettes.

However, Bruce LeVell, a former Trump adviser and former White House small business advocate, dismissed the viral speculation in a post on X, saying, “It’s not alcohol, and I speak for the President.”

In another post, he added, “President Trump does not drink or do drugs. You want a president like that.”

Trump was on an official visit to China on an invitation from Chinese president Xi Jinping. It was the first visit to China by a US president in nine years.

What happened during Trump’s China visit

Trump departed China on Friday while highlighting several business agreements reached during the trip, even as Beijing warned Washington against mishandling the sensitive Taiwan issue and criticised the Iran war.

“We’ve settled a lot of different problems that other people wouldn’t have been able to solve,” Trump said after meeting Chinese President Xi Jinping in Beijing on the second day of talks.

The discussions reportedly covered the Iran conflict, Taiwan, trade ties and other major geopolitical issues. While Xi did not publicly comment on his talks with Trump regarding Iran, China’s foreign ministry later issued a strong statement expressing frustration over the conflict.

I’ve been researching companies in-depth for over a decade, from commodities like oil, natural gas, gold and copper to tech like Google or Nokia and many emerging market stocks, which I believe could help me provide useful content for readers. After writing my own blog for about 3 years, I decided to switch to a value investing-focused YouTube channel, where I researched hundreds of different companies so far. I would say my favorite type of company to cover are metals and mining stocks, but I am comfortable with several other industries, such as consumer discretionary/staples, REITs and utilities.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

SEOUL — Investors weighing Samsung Electronics against SK Hynix for 2026 portfolios face a classic choice between diversified stability and pure-play AI growth as the global memory-chip supercycle intensifies. SK Hynix has surged ahead in high-bandwidth memory leadership and profitability, while Samsung leverages its vast resources to close the gap and offers broader exposure across semiconductors, smartphones and consumer electronics.

Both South Korean giants posted record first-quarter 2026 results driven by explosive demand for AI servers, but analysts give SK Hynix a slight edge for investors seeking maximum upside from the HBM boom. SK Hynix commands roughly 54 percent of the global HBM market and secured about 70 percent of NVIDIA’s HBM4 orders for the Vera Rubin platform, with its entire 2026 chip supply already sold out in key categories. Samsung, traditionally the larger player in conventional DRAM and NAND, is pouring more than $73 billion into chip expansion this year to regain ground.

The memory supercycle shows no signs of slowing. Surging AI infrastructure spending has pushed DRAM and NAND prices higher, with some server memory categories up more than 60 percent since late 2025. SK Hynix reported operating margins near 72 percent in Q1, while Samsung’s memory division approached similar levels despite broader business losses in foundry and system LSI.

SK Hynix: Pure AI Play with Explosive Momentum

SK Hynix stands out as the clearer beneficiary of the AI tailwind. Its focus on high-margin HBM products, critical for training and running large language models, has translated into record profits. The company’s operating profit in recent quarters has outpaced Samsung’s memory segment, with analysts forecasting continued dominance through 2027 as HBM4 shipments ramp.

Investors benefit from SK Hynix’s tight alignment with NVIDIA and other hyperscalers. The firm’s technological edge in stacking and thermal management gives it pricing power and near-term market share gains. Shares have responded with strong year-to-date gains, though valuations reflect the premium for leadership.

Risks remain. SK Hynix’s heavy concentration in memory leaves it more exposed to any slowdown in AI spending. Geopolitical tensions around its China facilities and potential U.S. export restrictions on advanced chips could also weigh on operations.

Samsung: Diversified Giant with Catch-Up Potential

Samsung offers a more balanced risk-reward profile. While lagging in HBM, the company is accelerating investments and has already raised prices on key chips by up to 60 percent. Its foundry, mobile and consumer electronics businesses provide natural hedges against memory cyclicality.

The conglomerate’s scale allows it to fund aggressive R&D and capacity expansion without the same financing constraints faced by pure-play competitors. Samsung’s upcoming HBM4 products and planned early deliveries could narrow the gap with SK Hynix by late 2026. Analysts highlight its long-term ability to leverage synergies across the value chain.

However, near-term challenges persist. Labor union tensions at Samsung’s key Pyeongtaek campus — which produces half of global DRAM and vital HBM — threaten production if strikes materialize in May and June. The company also carries higher exposure to cyclical consumer markets compared with SK Hynix.

Analyst Consensus and Valuation Comparison

Wall Street remains bullish on both. Samsung carries a Strong Buy consensus from 37 analysts with an average 12-month price target around KRW 274,000. SK Hynix earns similar enthusiasm, with many firms citing its HBM leadership as justification for a premium multiple.

Valuations reflect differing stories: SK Hynix trades at a higher forward price-to-earnings multiple justified by faster growth, while Samsung appears relatively cheaper on a diversified basis. Both offer attractive dividends relative to global tech peers, though SK Hynix’s payout is more modest given reinvestment needs.

Currency movements also matter. The Korean won’s fluctuations against the dollar can amplify or mute returns for international investors. South Korea’s export-driven economy ties both stocks closely to global trade and tech spending.

Broader Market and Economic Context

The AI memory boom forms part of a larger semiconductor upcycle. Data-center buildouts by hyperscalers continue at record pace, with HBM demand outstripping supply through at least 2027. Traditional DRAM and NAND markets benefit indirectly as customers stockpile ahead of shortages.

South Korea’s semiconductor sector, which both companies dominate, accounts for a massive portion of the KOSPI index. The iShares MSCI South Korea ETF provides convenient bundled exposure, with the pair comprising more than 25 percent of the fund.

Global risks include U.S.-China trade tensions, potential AI spending pauses and commodity price swings. On the positive side, any resolution in Middle East conflicts could ease energy costs and support broader economic growth.

Investment Recommendation for 2026

For growth-oriented investors chasing the purest AI memory exposure, SK Hynix edges out as the stronger 2026 pick. Its technological lead, sold-out capacity and sky-high margins position it to capture disproportionate upside from continued HBM demand.

Conservative or diversified investors may prefer Samsung for its scale, multiple business lines and potential to close the HBM gap. The stock offers a margin of safety through non-memory revenue streams and remains undervalued relative to growth prospects.

A balanced approach — owning both or using the MSCI South Korea ETF — mitigates single-company risk while capturing the sector tailwind. Dollar-cost averaging and monitoring quarterly results, especially HBM shipment updates and Samsung’s labor situation, will be key.

Neither stock is without volatility. Memory cycles have historically been dramatic, and AI hype could moderate if economic conditions shift. Yet current fundamentals — tight supply, strong pricing and multi-year demand visibility — support an upbeat outlook for both through 2026 and into 2027.

As the AI infrastructure buildout accelerates, the Samsung-SK Hynix duel will remain one of the most watched battles in global tech. Investors who correctly time entry into the memory supercycle could see substantial returns, but thorough research and risk management remain essential in this fast-moving sector.

BofA reiterates Buy on Alphabet stock ahead of developer event

Morgan Stanley downgrades Aardvark Therapeutics stock rating on FDA hold

Earnings call transcript: Recruit Holdings Q4 2025 beats expectations with record results

Getty Images

By Ivan Castano

The Iran war has sent aluminum prices higher this year, unnerving a slew of global industries that rely on the base metal to manufacture cars, canned goods and aircraft.

Before the conflict began in late February, prices were hovering at $3,200 per metric ton (tonne) but rose to a four-year high of $3,500 per tonne a fortnight later as fears of supply shocks hit the market.

Wood Mackenzie had already predicted a 200,000-tonne deficit for this year, possibly rising to 800,000 tonnes by 2028. This was sharply higher than the roughly 50,000-tonne shortage expected as of late 2025, when electric vehicles (EVs), renewable energy (mainly solar panels) and AI data centers were taking demand to new heights.

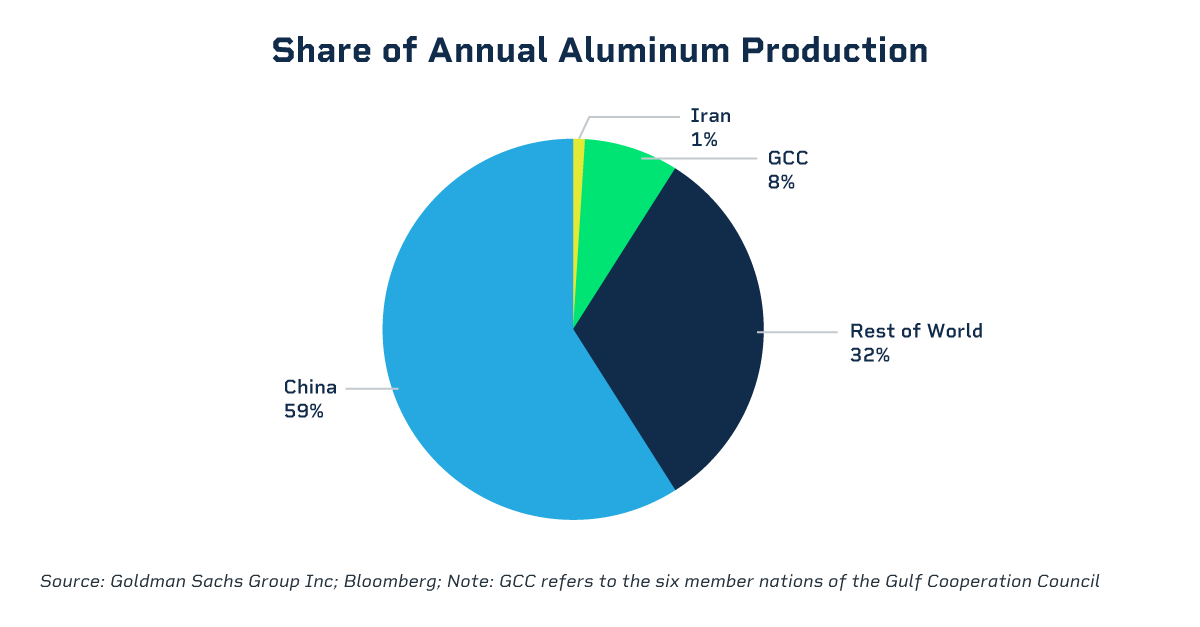

Crucially, the war triggered the closure of the Strait of Hormuz, a vital waterway through which Middle East output – which accounts for 9% of the world’s total – reaches ports in Europe and the United States. Simultaneously, Aluminium Bahrain (Alba), which operates the globe’s largest smelter, announced it would cut output by 19% due to the maritime disruption.

“The closure of ports and plants is likely to cause significant turbulence in the aluminum market,” according to a Wood Mackenzie report, which also noted that the loss of the Gulf States’ outflows “would significantly tighten the balance over the next 6-12 months.” There are no viable ways of offsetting the loss from interrupted shipping or prolonged shutdowns.

Some carmakers, particularly EV manufacturers who use around 25% more aluminum than combustion models, have also announced they will cut production until there is greater clarity about the supply chain’s future.

Regional Disparities in Aluminum Pricing

While the rising flat price of aluminum is in focus, current events are further widening regional price differentials.

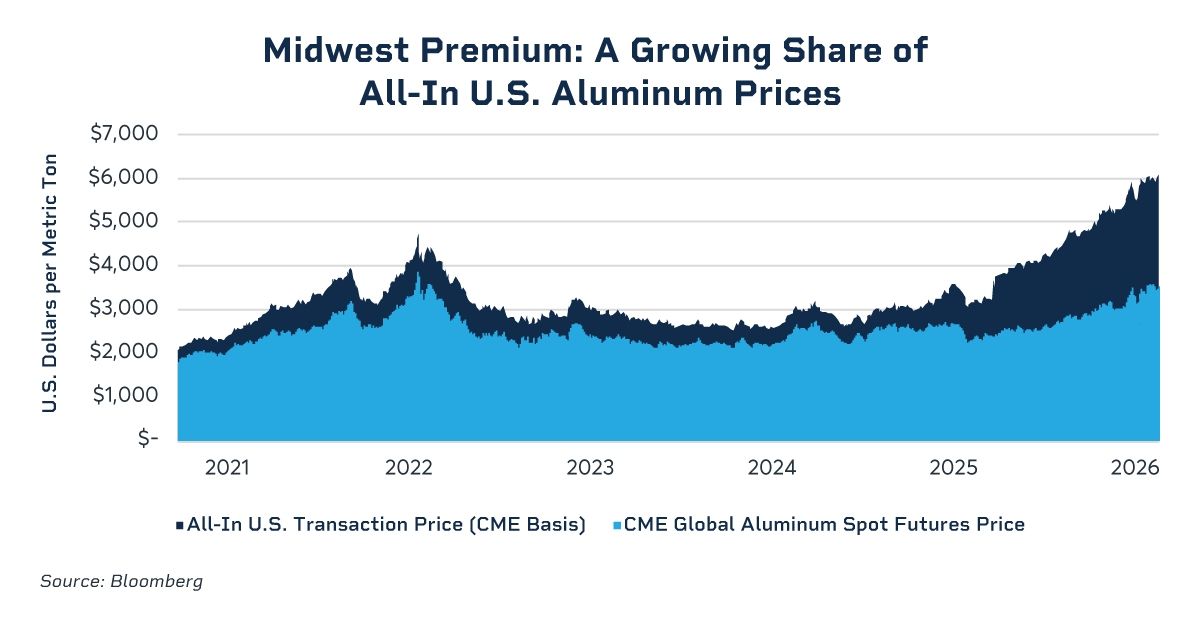

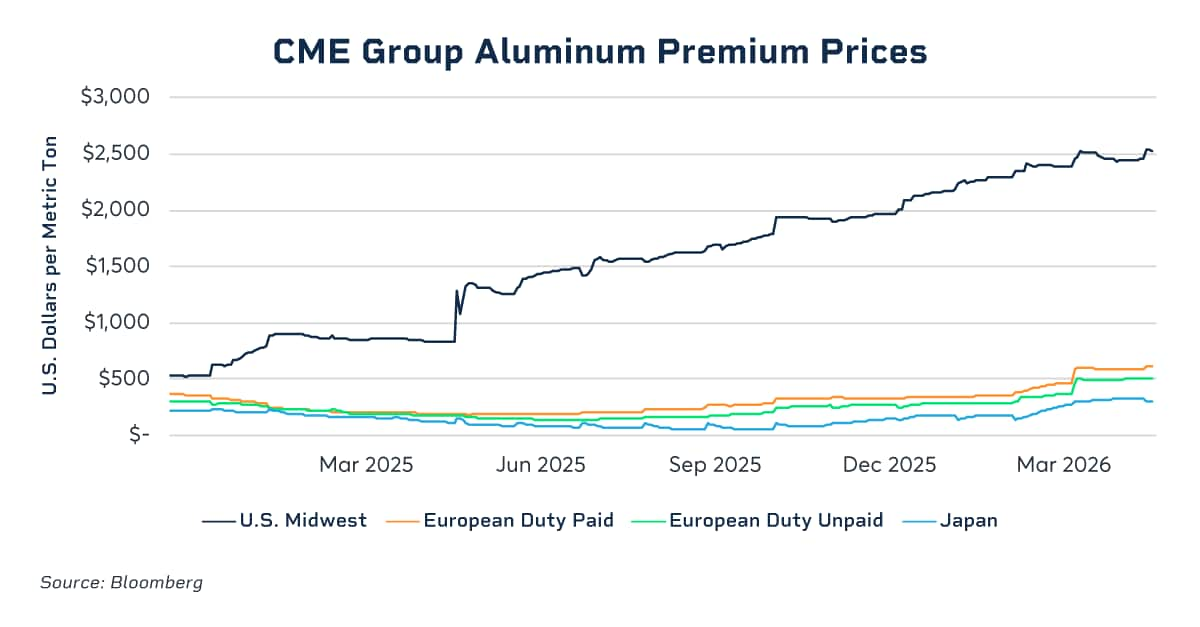

So-called physical premiums (a markup to the global price that reflects the regional fundamentals, cost of shipping and tariffs) are sharply above their pre-war baselines. The spreads – commonly called the Midwest Premium for the U.S.; the Rotterdam Duty-Paid, or European Premium Duty-Unpaid, for Europe; and the Japanese Premium for Asia – were trading around $2,529, $612, $507 and $302, respectively, as of early May. To help investors manage related price risks, CME Group offers futures on these regional premiums, in addition to futures on aluminum itself. Traders can either trade the regional premium as a standalone or the all-in price, covering the global price plus the premium.

With a historically high Midwest Premium, U.S.-bound aluminum is fetching over $6,000 per tonne, squeezing manufacturers in a country that imports the vast majority of supplies. Roughly 12% of these imports come from the Middle East, where American buyers have increasingly turned to with tariffs and sanctions significantly limiting the import and producer origins to choose from.

“Our contracts provide a key risk management tool for U.S. aluminum consumers and have become a critical piece to mitigate price risk and help protect margins,” said Ian Caton, Senior Director of Metals Products at CME Group.

The conflict in Iran expedited the expansion of an already-growing regional premium, he added. The introduction of Section 232 tariffs in 2018 first kicked off this increase for U.S. consumers, a trend further exaggerated as tariff policies broadened over the past year.

In contrast, European and Japanese markets face considerably smaller regional spreads, as they lack comparable tariff structures, though they have also jumped in the wake of the war.

Europe’s premium is now roughly at $612 per tonne, while Japan’s is at $302 per tonne, both up around 70% from their pre-war levels.

Interestingly, however, Europe’s Rotterdam premium surged over 50% in 2025 as a shutdown at Iceland’s key supplier, Aluminum Iceland, a carbon tax for non-EU importers and an output slump in Mozambique strangled supply.

In Japan, opposite forces were at play. The Asian country faced an aluminum oversupply as the automotive industry slashed production and stocks were already abundant. This brought prices lower, hitting a $58 per tonne bottom late last year. Then, as demand began to pick up and the trade blockade started, prices surged to $181 a tonne in February before settling even higher as of late April.

“The impact depends on the region,” Caton noted. “The global price plays a role, but regional considerations have become an increasing proportion of the notional value of the all-in cost of aluminum. The U.S. Midwest premium, for example, now accounts for over 40% of the all-in transaction price for aluminum in the U.S.”

Recycling to the Fore

Amid supply headwinds, U.S. buyers are bolstering their recycling capacity to ensure they have sufficient aluminum stocks.

Subodh Das, CEO and founder of industry consultancy Phinix, said the United States has invested $10 billion in the process and has the capacity to increase repurposed output to 4 million tonnes this year, up from 3 million tonnes in 2025.

Beyond ramping up old facilities or installing new ones, there must be a bigger effort to leverage landfilled capacity, according to Das.

“One and a half million tons of scrap are landfilled every year, while 1.5 million are exported,” he said. “We need to stop landfilling, and we need to export less.”

The U.S. could also benefit from raising production, Das added, an effort that recently got a boost after Emirates Global Aluminium and Century Aluminum struck a joint venture to make 750,000 tonnes of the metal in Oklahoma, nearly doubling current capacity from a plant it claimed will be the nation’s largest.

Despite the war’s uncertainty, Das said the U.S. has a 120-million ton aluminum reserve in landfills, largely derived from used beverage cans, that could be put to work if the conflict further impacts global stocks.

Alan Taub, an engineering professor at the University of Michigan’s Electric Vehicle Center, agreed more must be done to buoy recycling, especially as automobile prices continue to skyrocket.

“The aluminum price impact is the most concerning coming from the war,” he said. “We are having an automotive affordability problem with average sales prices north of $50,000. While the industry tends to know how to cope by adding extra capacity, or using materials in different ways, after adding value [like turning the metal into an automotive casting], component prices have risen dramatically.”

By adding secondary or ‘scrap’ aluminum into the manufacturing mix, industries can reap huge cost savings from lower energy usage while cutting emissions, said Taub.

But this isn’t always easy.

“One of the challenges in shredding [a car dismantling process] is that you get secondary aluminum that can be contaminated with iron (from steel bolts or brackets),” which can undermine the structural integrity of the resulting material, Taub said. Consequently, the industry is developing more iron-tolerant variants such as aluminum alloys blended with manganese and/or magnesium.

Annie Creasy’s AIM Mining has failed in another crack at Wiluna Mining despite lawyer going hard at directors.

Even Trump, an enthusiastic supporter of both the World Cup and Fifa president Gianni Infantino, has said he “wouldn’t pay it either” when asked about the prices. Tickets for sale for the final at New Jersey’s MetLife Stadium were officially offered at up to $32,970 (£24,540), while resale tickets have been listed for more than $2m.

Arne Slot has an uphill battle to get the fans back on side

5 Altcoins Ready To Pump (Crypto Bill WINNERS LIST)

Hartlepool memorial tournament to honour Syed Taalay Ahmed

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

![Why Bitcoin Won’t Stop! [Even With 3.8% CPI Shock]](https://wordupnews.com/wp-content/uploads/2026/05/1778835689_maxresdefault-80x80.jpg)

-

Crypto World7 days ago

Crypto World7 days agoHarrisX Poll Found 52% of Registered Voters Support the CLARITY Act

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Marianne Dress

-

Fashion4 days ago

Fashion4 days agoCoffee Break: Travel Steam Iron

-

Fashion4 days ago

Fashion4 days agoWhat to Know Before Buying a Curling Wand or Curling Iron

-

Tech5 days ago

Tech5 days agoAuto Enthusiast Carves Functional Two-Stroke Engine from Solid Metal

-

Politics3 days ago

Politics3 days agoWhat to expect when you’re expecting a budget

-

Business6 days ago

Business6 days agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Politics6 days ago

Politics6 days agoPolitics Home Article | Starmer Enters The Danger Zone

-

Tech4 days ago

Tech4 days agoGM Agrees To Pay $12.75 Million To Settle California Lawsuit Over Misuse Of Customers’ Driving Data

-

Crypto World6 days ago

Crypto World6 days agoPROS explodes 48% as Upbit and Bithumb listings ignite demand

-

Crypto World5 days ago

Crypto World5 days agoCZ says US crypto rivals tried to block Trump pardon

-

Tech3 days ago

Tech3 days agoGM agrees to $12.75M California settlement over sale of drivers’ data

-

Entertainment7 days ago

Entertainment7 days agoYNW Melly Denied Bond Again Ahead Of Double Murder Retrial

-

Crypto World6 days ago

Crypto World6 days agoKraken Parent Seeks OCC Charter, Signaling Regulated Banking Access

-

Crypto World7 days ago

The Hantavirus Danger: Can a Potential Outbreak Spark a New Meme Coin Frenzy?

-

Sports7 days ago

Sports7 days agoAfter Waka Waka, Shakira now drops first teaser for FIFA WC 2026 song | FIFA World Cup 2022

-

Crypto World6 days ago

Crypto World6 days agoSolana UFO Meme Coins Surge After Pentagon Reveals Alien Files

-

Entertainment6 days ago

Entertainment6 days agoBethenny Frankel Says She Loves ‘Torturing’ Men

-

Sports7 days ago

Sports7 days agoWhy Nathan Mackinnon Remains the Hart Trophy Favourite over Connor McDavid and Nikita Kucherov | NHL

-

Crypto World2 days ago

Bitcoin Suisse expands with Digital Asset License and Investment Business Act Registration Approval in Bermuda

You must be logged in to post a comment Login