Crypto World

What about the American consumer?

Welcome to our institutional newsletter, Crypto Long & Short. This week:

- Alex Tapscott on the stalling of the CLARITY Act and how it’s impacting the average American consumer.

- Aisha Hunt writes that crypto will grow by upgrading Wall Street’s trusted products rather than replacing them.

- Top headlines institutions should pay attention to by Helene Braun

- “RWA Perp Volume by Category: Equities Overtake Commodities” in Chart of the Week

Expert Insights

What about the American consumer?

By Alex Tapscott, CEO, CMCC Global Capital Markets

The little guy is getting lost in the political horse-trading around the CLARITY Act.

The U.S. Senate Banking Committee recently advanced the Digital Asset Market CLARITY Act, legislation that, if enacted, could finally establish clear rules for digital assets in the United States. The bill has survived months of bipartisan negotiations and horse trading between banking interests and upstart fintech companies.

A bipartisan compromise brokered by Senators Thom Tillis (R-NC) and Angela Alsobrooks (D-MD) broke a log-jam that had slowed down the bill’s progress. In the end, the banks got most of what they wanted in this “deal”: the legislation explicitly prevents fintech platforms from treating stablecoins, digital assets backed by dollars, as interest bearing accounts, while still permitting them to pay rewards and bonuses, as banks and credit card issuers do.

That should have ended the debate. Yet banking lobby groups are demanding tighter restrictions to eliminate many forms of consumer rewards altogether. Clearly, they seek to squash this already compromised bill before a full Senate vote, so that it never reaches the Resolute Desk.

Lost amid the political wrangling of crypto and banking interests is the average American consumer.

According to the Consumer Financial Protection Bureau (CFPB), Americans paid roughly $5.8 billion in overdraft fees in 2023, even after years of industry efforts to reduce so-called “junk fees.” Overdraft charges disproportionately hit financially vulnerable households, with nearly 80% of fees concentrated among 9% of accounts. And then there are account minimums, wire charges and payment delays, which add friction. Meanwhile, the average savings rate is only 0.38%.

Consumers want financial services to move faster, cost less and earn them more.

Stablecoins are gaining popularity because they herald a world where digital dollars move across the internet as cheaply and seamlessly as a WhatsApp message. They can lower remittance costs, improve access to digital commerce, expedite real-time payments and create new ways for consumers to save, spend and transact online.

And Americans are asking for CLARITY because many already use these tools. According to the Crypto Council for Innovation, one in five American adults now owns cryptocurrency. That’s roughly 68.5 million people. Stablecoins are among the fastest-growing categories of digital assets, particularly among younger consumers, immigrants, freelancers and underserved communities seeking faster and cheaper financial tools. Four in five merchants believe accepting crypto could help attract new customers, while 73% of small business owners expect crypto payments to grow.

That’s what makes this debate so politically mystifying. For years, progressives argued that concentrated financial power harmed consumers and Main Street. They criticized large banks for extracting rents while lobbying against regulations that diluted bank influence. Those critiques were often correct. Today some of those progressives, like Elizabeth Warren, who championed the Consumer Financial Protection Bureau, are now defending banking profits against a technology that could inject real competition into financial services and empower consumers and small businesses.

Congress should pass CLARITY in its current form to benefit American consumers and preserve American competitiveness and leadership in the next era of financial technology. This lead is by no means assured: today, 88% of global crypto trading volume occurs on non-U.S.-based exchanges, while foreign-issued stablecoins account for 75% of stablecoin volume. Over the past decade, the U.S. share of global crypto developers has fallen from 38% to just 19%.

Do American politicians want their country to continue leading, or do they prefer watching such financial transformation from the sidelines?

In the 1990s, the Clinton administration helped usher in the commercial internet through the Telecommunications Act of 1996, a bipartisan effort expanding innovation and competition. Now, Congress has an opportunity to unleash the new internet of value by passing CLARITY.

Under GENIUS and CLARITY, stablecoin issuers must meet strong reserve requirements, transparency obligations, anti-money laundering standards, cybersecurity rules and consumer protections. Sensible public policy will unleash investment and innovation, as it did in the internet era.

This story need not end in conflict between banks and blockchains. Incumbents can just as easily embrace blockchain and its various benefits, from real-time global settlement and tokenized assets, to new forms of on-chain lending, payments, savings and commerce.

The question is whether lawmakers will vote to lead this next technological revolution and advance the interests of American consumers or cede the future to entrenched interests.

Principled Perspectives

Why Crypto May Need ETFs More Than ETFs Need Crypto

By Aisha Hunt, founder of Kelley Hunt, PLLC

Crypto spent its first decade trying to replace Wall Street. Its next trillion dollars may come from partnering with it. The first wave of tokenization focused on creating new assets, new venues and new systems outside traditional finance. Some of that innovation mattered. Much of it struggled with the same problem: markets do not scale on technology alone. They scale on trust, liquidity and distribution. That reality favors ETFs.

The ETF wrapper became one of the most successful financial products of the modern era because it solved practical investor problems at scale: low-cost access, transparency, intraday liquidity, operational simplicity and broad distribution across brokerage platforms and advisory channels.

Those advantages took decades to build. Tokenization does not erase them. In fact, it may amplify them. If blockchain rails can be integrated into ETFs, investors may not have to choose between innovation and protection. They could gain exposure to familiar products with the potential benefits of faster settlement, programmable ownership, collateral mobility and broader digital interoperability, all inside a structure already trusted by institutions, advisors and retail investors.

That is a far bigger commercial opportunity than asking trillions of dollars to migrate into unfamiliar vehicles. This is why one underappreciated development matters. On January 21, 2026, F/m Investments LLC and The RBB Fund, Inc. filed what is believed to be the first exemptive application by an ETF issuer seeking to tokenize shares of an exchange-traded fund, TBIL, the U.S. Treasury 3 Month Bill ETF. The proposal would record ownership on a permissioned blockchain ledger while preserving the same fund, same economics, same exchange listing and same regulatory framework. The application remains pending before the SEC, and there can be no assurance relief will be granted. That may sound like a niche legal filing. It is not. It is a test of whether capital markets modernization happens inside the regulatory perimeter or outside it.

That distinction matters to investors because the next major on-chain growth category may not be speculative tokens. It may be trusted yield, usable collateral and regulated exposure. Stablecoins already demonstrated the demand for digitally native dollars. The next logical step is digitally native instruments backed by real portfolios, real governance and real investor protections.

That is where tokenized ETFs could become powerful.

Imagine Treasury exposure that can plug into next-generation collateral networks. Imagine ETF shares that remain within familiar regulatory guardrails while operating on more modern rails. Imagine advisors and institutions accessing blockchain efficiency without having to underwrite experimental structures.

The first tokenization narrative was “replace incumbents.” The stronger narrative may be “upgrade incumbents.” That does not diminish crypto; it commercializes it.

For regulators, tokenized ETFs may offer a pragmatic path forward: enable innovation where investor protections remain intact, rather than pushing demand into parallel channels with greater uncertainty. For exchanges, custodians, brokers and market makers, it could create a new infrastructure layer around products investors already understand.

For issuers, it may become a race. The firms that combine trusted wrappers, credible assets and functional on-chain rails could capture disproportionate flows. And for allocators, the signal may be simple: blockchain technology is becoming less about novelty and more about plumbing.That is usually when real adoption begins.

The broader lesson is that distribution often beats disruption:

Who already has trusted wrappers?

Who already has liquidity?

Who already has access to advisors, retirement assets and institutions?

Who can bridge old rails and new rails fastest?

Those questions point toward ETFs.

The next trillion dollars of tokenized assets may not come from inventing something entirely new; they may come from upgrading what already works. Crypto’s first era was about building outside the system. Its next era may be about powering the system.

Headlines of the week

By Helene Braun

A few of crypto’s biggest debates converged this past week as Michael Saylor’s Strategy (MSTR) sold bitcoin to fund preferred stock dividends, JPMorgan CEO Jamie Dimon escalated his fight against yield-bearing stablecoins during the CLARITY Act debate, and Citi projected tokenized securities could grow into a $5.5 trillion market by 2030, driven by rising demand for onchain Treasuries and tokenized stocks.

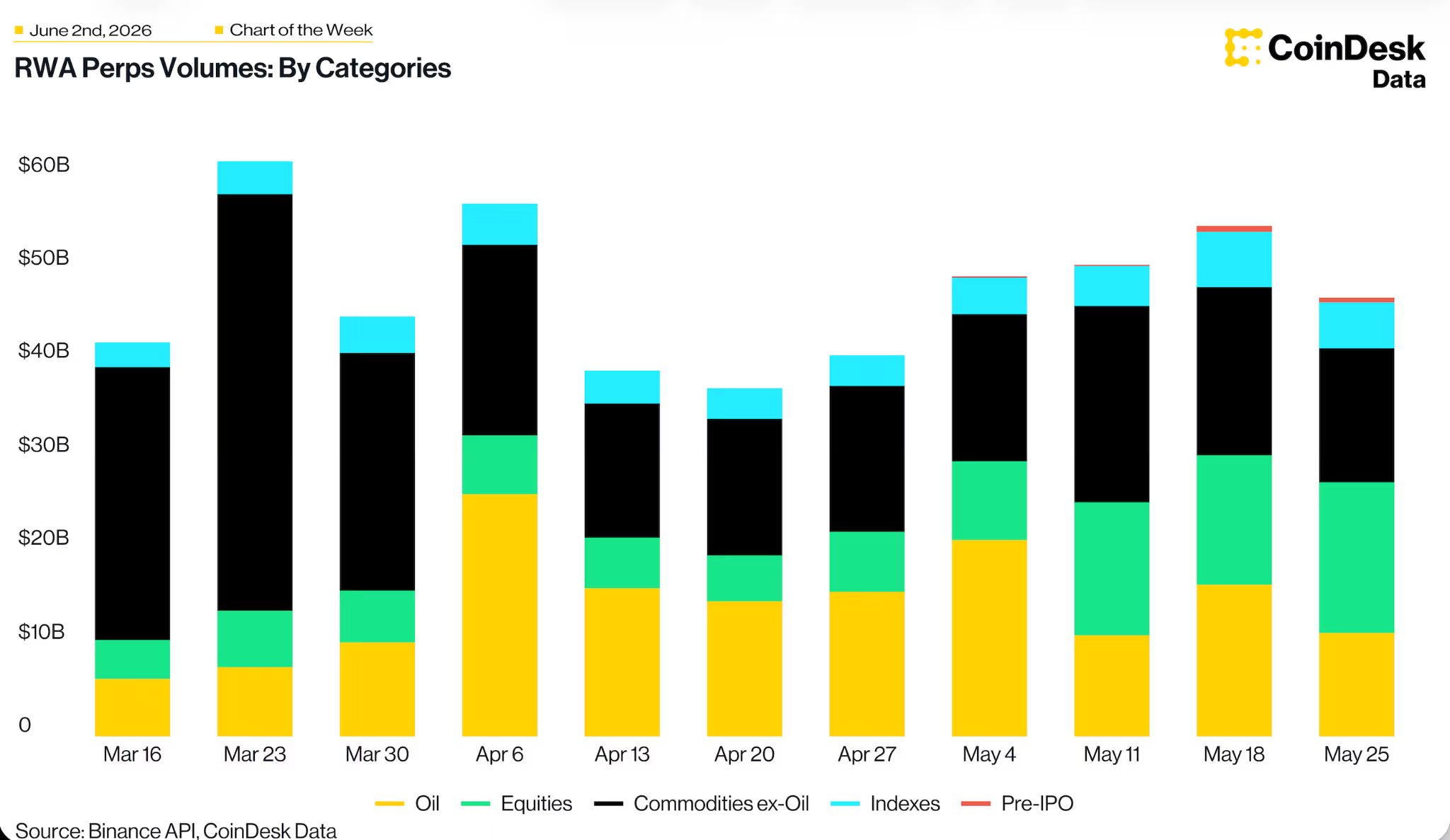

Chart of the Week

RWA Perp Volume by Category: Equities Overtake Commodities (excluding oil)

RWA perps run ~$45–60 billion/week, and flow is rotating out of commodities into equities. Equities roughly tripled to ~$18 billion and just overtook the commodities (excluding oil) block, while oil faded after its April macro spike. This implies that crypto-venue derivatives are increasingly used for 24/7 equity exposure, with commodities now the episodic, event-driven slice.

Listen. Read. Watch. Engage.

Looking for more? Receive the latest crypto news from coindesk.com and market updates from coindesk.com/institutions.

Note: The views expressed in this column are those of the author and do not necessarily reflect those of CoinDesk, Inc., CoinDesk Indices or its owners and affiliates.

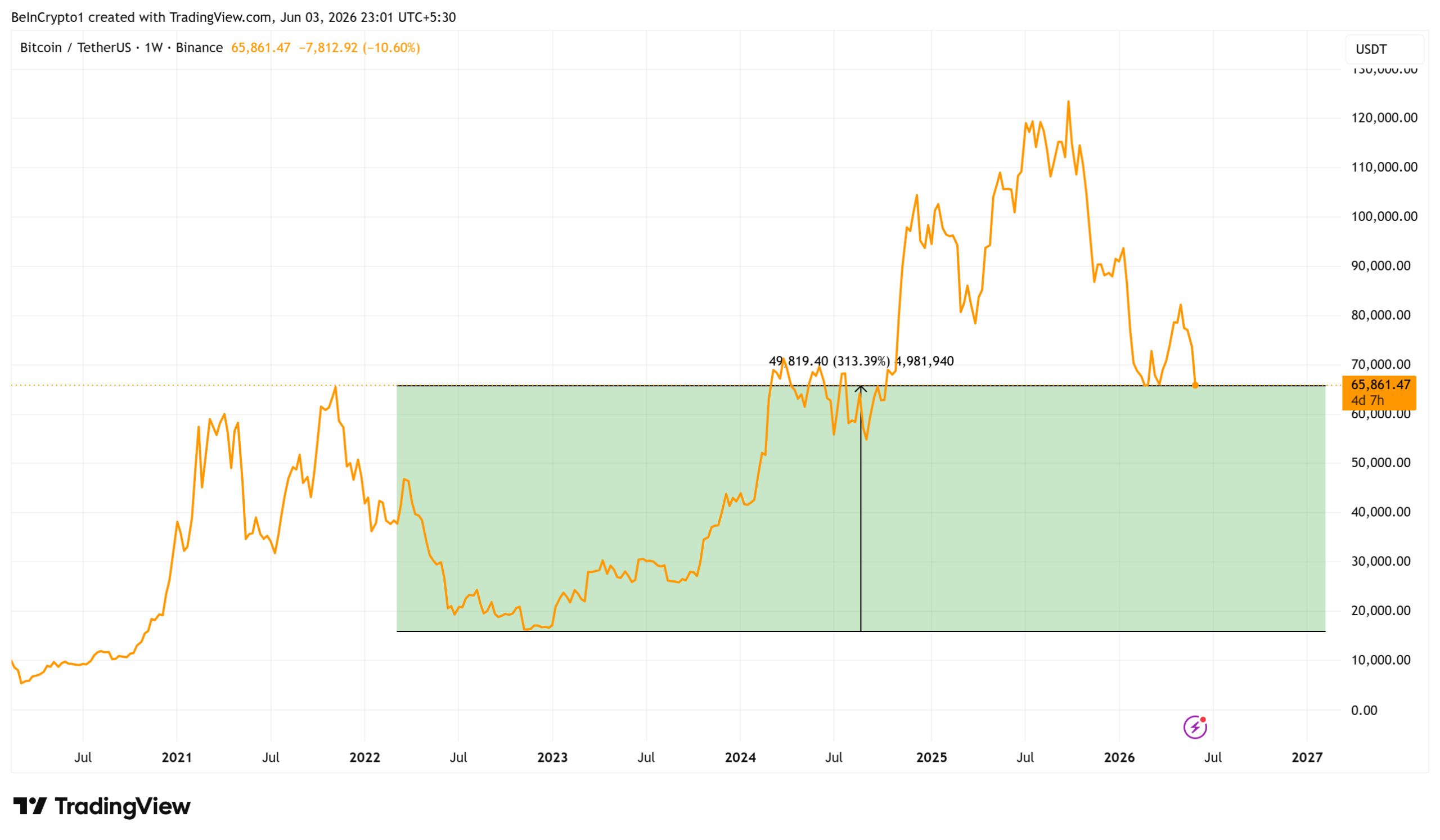

Raoul Pal, who ran European hedge-fund sales at Goldman Sachs before founding Real Vision, has rejected claims that money is fleeing crypto for technology stocks. He says the data tell a different story.

His pushback came as US equities slipped at Wednesday’s open, pressured by fears of a hawkish Federal Reserve and stalled Iran-US talks.

Why Raoul Pal Is Pushing Back on the Crypto Doom Narrative

Pal challenges the crypto is finished narrative, rejecting the sentiment that capital now favors AI and chip makers.

To back the claims, he measures returns from the 2022 liquidity-cycle low, when the FTX collapse drove Bitcoin near $15,700 in November.

From that trough, Bitcoin has gained about 318%, trading near $65,800. The Nasdaq 100 has risen roughly 187% over the same span, to near 30,660.

That gap is the heart of his case. Bitcoin has outpaced the tech benchmark by a wide margin, even after a steep recent pullback.

Pal argues that liquidity cycles, not market narratives, drive prices. He has made that case since launching Global Macro Investor in 2005, and frames the current weakness as a mid-cycle correction.

“The ‘Crypto is dead, its all going to tech stocks’ narrative is alluring but overall this is the actual results from the liquidity cycle low in 2022…” Pal wrote.

Other analysts also expect crypto to outperform tech stocks.

Follow us on X to get the latest news as it happens

Bitcoin Trades Below Its Record as Stocks Wobble

Despite the cumulative gains, Bitcoin has cooled lately. The token traded near $65,800 on Wednesday, down about 2.7% over 24 hours. That sits far below its record high of $126,080, though its market value still tops $1.3 trillion.

Stocks, meanwhile, opened weak. Over $500 billion was wiped from US equities within 20 minutes of the open, analyst Bull Theory said.

“US equity indices pulled back from records amid risks of a hawkish Federal Reserve and the lack of progress between Iran and the US. The S&P 500, Nasdaq 100 edged lower and the Dow lost 0.5%. Data from the ADP showed the private sector added a net 122,000 jobs in May, above expectations, to add leeway for the Fed to raise rates and fight inflation.,” wrote analysts at Trading Economics.

Pal’s framework has both supporters and critics. Backers say the data confirms that global liquidity expansion rewards high-beta assets like Bitcoin.

Skeptics argue he picked the exact low. Others say AI has changed how capital now flows into equities.

Pal also contends Bitcoin trades at a discount to liquidity conditions. His models point toward a higher liquidity target once financial conditions ease again.

The token’s link to the Nasdaq has tightened over the past year. That connection cuts both ways, since Bitcoin tends to fall harder when stocks drop.

The post Raoul Pal Shuts Down ‘Crypto Is Dead’ Narrative With One Chart appeared first on BeInCrypto.

Another crypto-focused political action committee, the Defend Developers PAC, has joined the field of campaign-funding operations that have in recent years put the industry on the political map.

The new entrant won’t rival the sector’s leading super PAC, Fairshake, nor is it expected to jump to the scale of the mid-level committees that include the Fellowship PAC linked to Tether and the Digital Freedom Fund tied to Tyler and Cameron Winklevoss at Gemini. But it’s approaching the political field differently than others, by backing incumbent lawmakers who’ve already proven to be allies to its cause: the legal protection of crypto developers and creators of decentralized finance (DeFi) projects.

“We plan to raise and contribute more than six figures across dozens of key races in the midterms, because crypto technologists deserve champions in Congress who will go to bat for them,” said Gavin Zavatone, the PAC’s founder, in a Wednesday statement announcing the effort. Zavatone is also the policy lead at the DeFi Education Fund, a trade association that lobbies for DeFi-friendly policymaking.

Defend Developers — federally registered last month — is what’s known as a hybrid PAC, meaning it can make direct contributions to candidates that follow the Federal Election Commission limits as well as channeling unlimited corporate contributions into independent ads. The bulk of the crypto sector’s high-profile political intervention has been through super PACs that have no monetary limits, though another new PAC, the Blockchain Leadership Fund established by Anchorage Digital and Chainlink, is also a hybrid.

“As a hybrid PAC, we’re building the political infrastructure to ensure the United States remains the best place in the world to build blockchain technology freely — and we’re doing it the right way, powered by individual contributions raised directly from the founders, builders, and CEOs who have the most at stake,” Zavatone said. The board of directors behind him include members from Uniswap Labs, DEF and the Solana Policy Institute, though no dollar amounts have yet been disclosed about its initial funding.

Without the tens of millions deployed by Fairshake and its affiliates, a new crypto PAC isn’t likely to make major waves. Fairshake is coming away with its latest primary election wins this week, having backed nine Democratic U.S. House of Representatives candidates in California, one in New Jersey and Republican U.S. Senate Mike Rounds in South Dakota. All of them won their primaries on Tuesday, maintaining a high win record for crypto-supporting politicians that Fairshake bought independent ads for, though the PAC didn’t expend more than $476,000 (for U.S. Representative George Whitsides) on this week’s races.

Fairshake had expended $6.5 million in its successful effort to make sure veteran House lawmaker and crypto critic Al Green lost out to Christian Menefee in their Texas primary last week. However, the super PAC — one of the largest in U.S. politics — has also seen a few misfires, such as in Illinois.

The general election in November brings extremely high stakes, with the potential to shift the party majority to Democrats in at least one chamber of Congress.

Read More: The crypto industry’s massive political war chest is starting to lean Republican ahead of midterms

Bitcoin (BTC) hovered near two-month lows on Wednesday as 2022 bear-market comparisons returned.

Key points:

- Bitcoin traders bring back the 2022 bear market to assess where BTC price action might go next.

- History shows a new lower high followed by a breakdown of a key 50-month trend line.

- That trend line has held throughout 2026 so far.

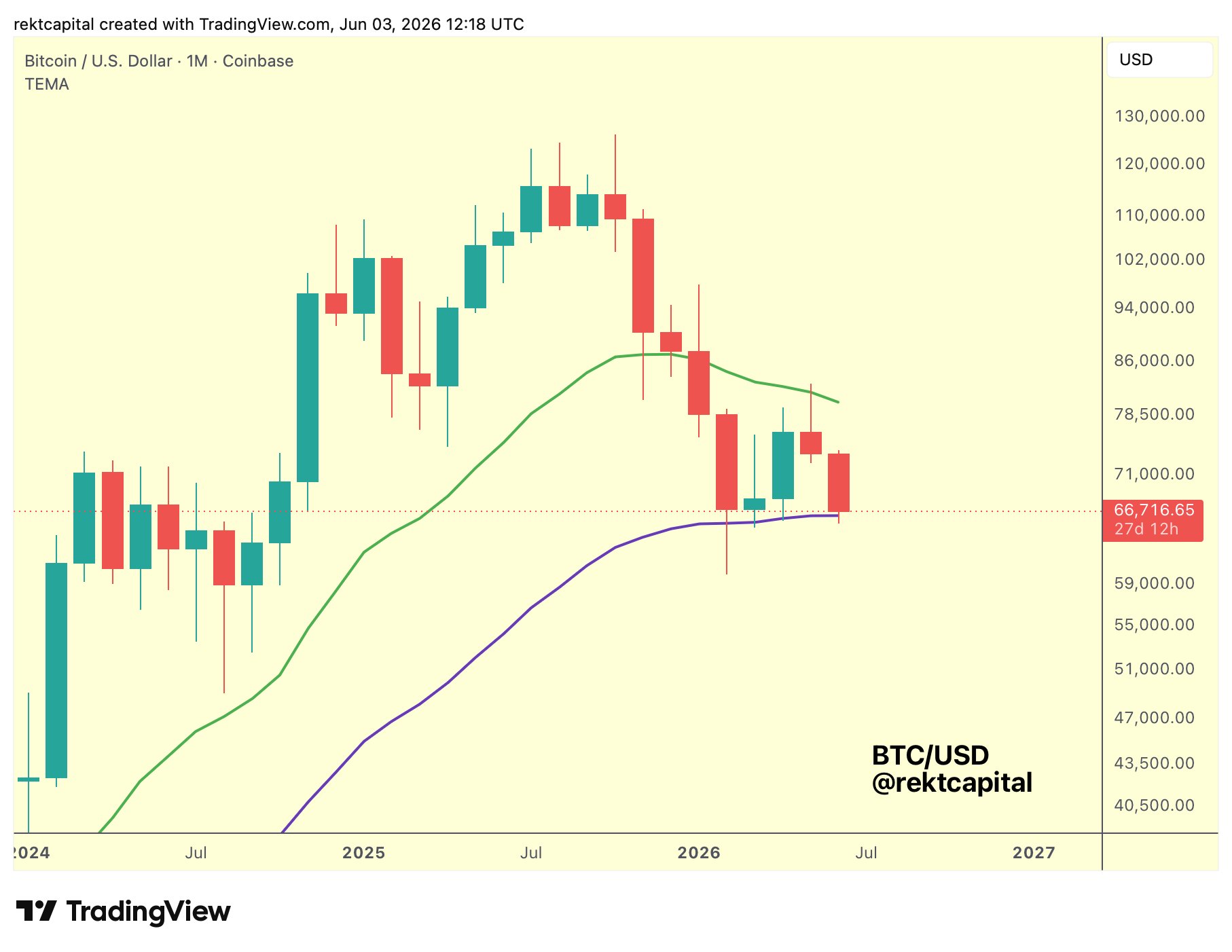

Analysis: Bitcoin 50-month trend line break down “likely”

Data from TradingView showed cooling BTC price volatility after a trip to $65,362 on Bitstamp — a level last seen in early April.

BTC/USD one-hour chart. Source: Cointelegraph/TradingView

After billions of dollars in liquidations, BTC/USD fielded new warnings that the worst of the bear market may still be ahead.

Trader and analyst Rekt Capital focused on the 50-month exponential moving average (EMA) trend line at $66,628.

“Over time, Bitcoin is likely to breakdown from this EMA and continue macro downside in this Bear Market,” he warned in one of several posts on X.

Rekt Capital said that if history were to repeat from the 2022 bear market, price should now see a relief bounce to form a lower high before returning to the 50-month EMA, which would in turn fail as support.

“Historically, Bitcoin tends to rebound initially from the 50-Month EMA but then loses it as support as the Bear Cycle progresses,” he added.

BTC/USD one-month chart with 21, 50EMA. Source: Rekt Capital/X

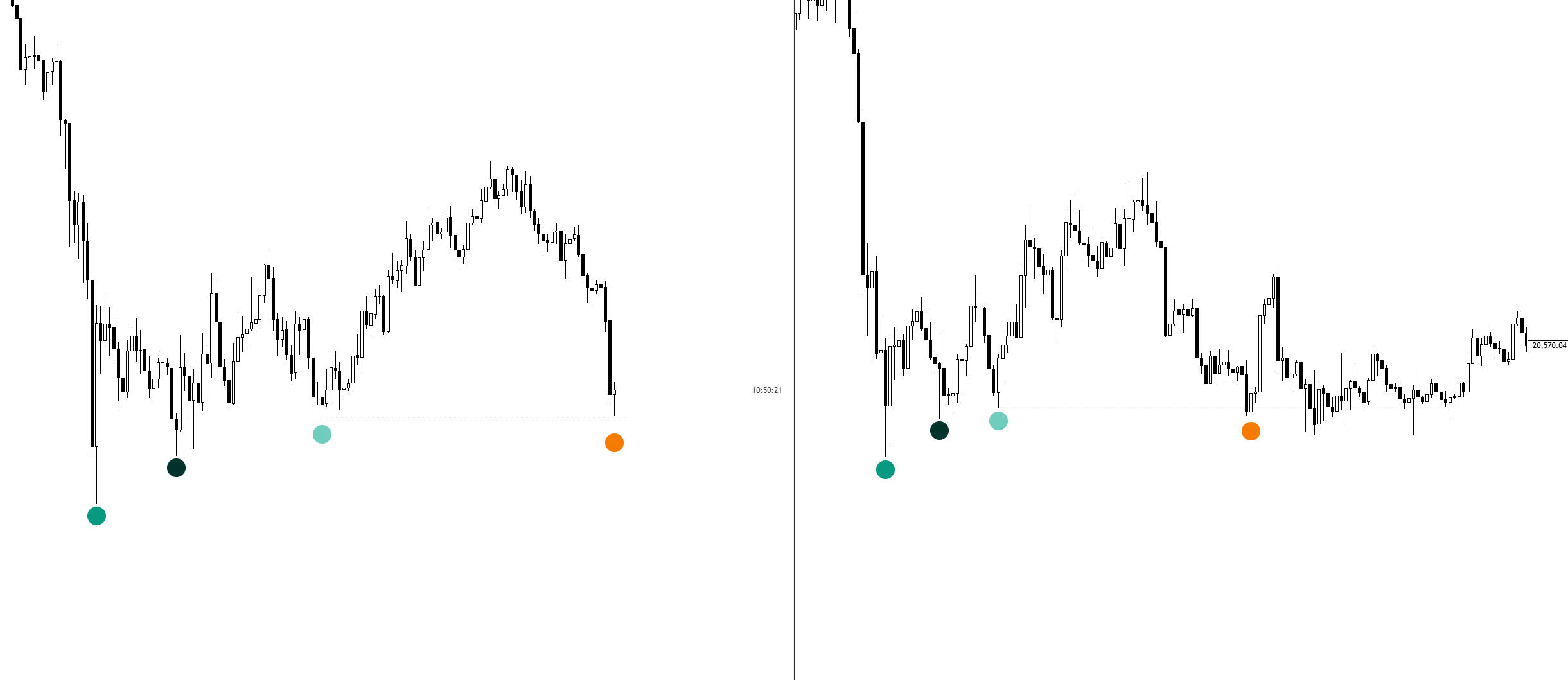

Continuing, trader Leviathan argued that the 2026 bear market was copying its predecessor “almost perfectly.”

“Every stage printing in the same order,” an X post reported, calling $60,000 the “line that matters.”

“Hold it – liquidity flush complete, recovery begins. Lose it – deeper correction, no support below. One level, two completely different outcomes. Market makes the call soon.”

BTC/USD two-week chart comparison. Source: Leviathan/X

Another trader, Killa, leveraged 2022 price action to suggest “weeks” of consolidatory movement between $63,000 and $65,000 next.

BTC price chart comparison. Source: Killa/X

BTC price support reclaim could offer 700%+ returns

A silver lining on the day came from historical reactions to the 50-month EMA.

Related: Bitcoin has hit ‘max fear’ below $67K as analysis sees BTC price rebound

Analytics account Paradox noted the extent of potential gains that could come from Bitcoin’s eventual reclaim of the trend line after losing it.

“$BTC lost the monthly 50MA in 2022. It reclaimed it 5 months later, delivering a 715% return over the next 2 years,” it told X followers.

In February, BTC/USD saw several daily closes below the trend line, ultimately avoiding a full breakdown. In March and April, meanwhile, it functioned successfully as support.

BTC/USD one-day chart with 50-month EMA (blue line). Source: Cointelegraph/TradingView

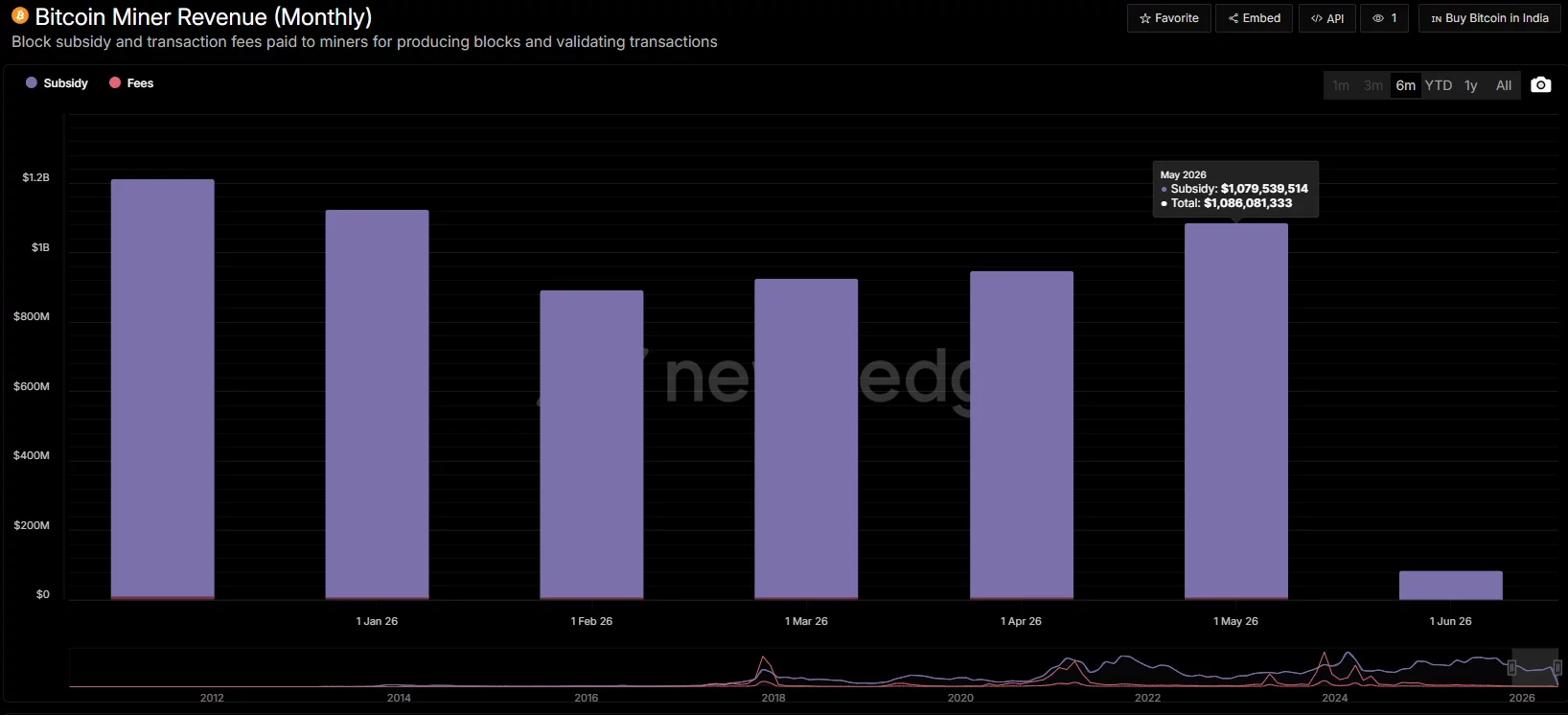

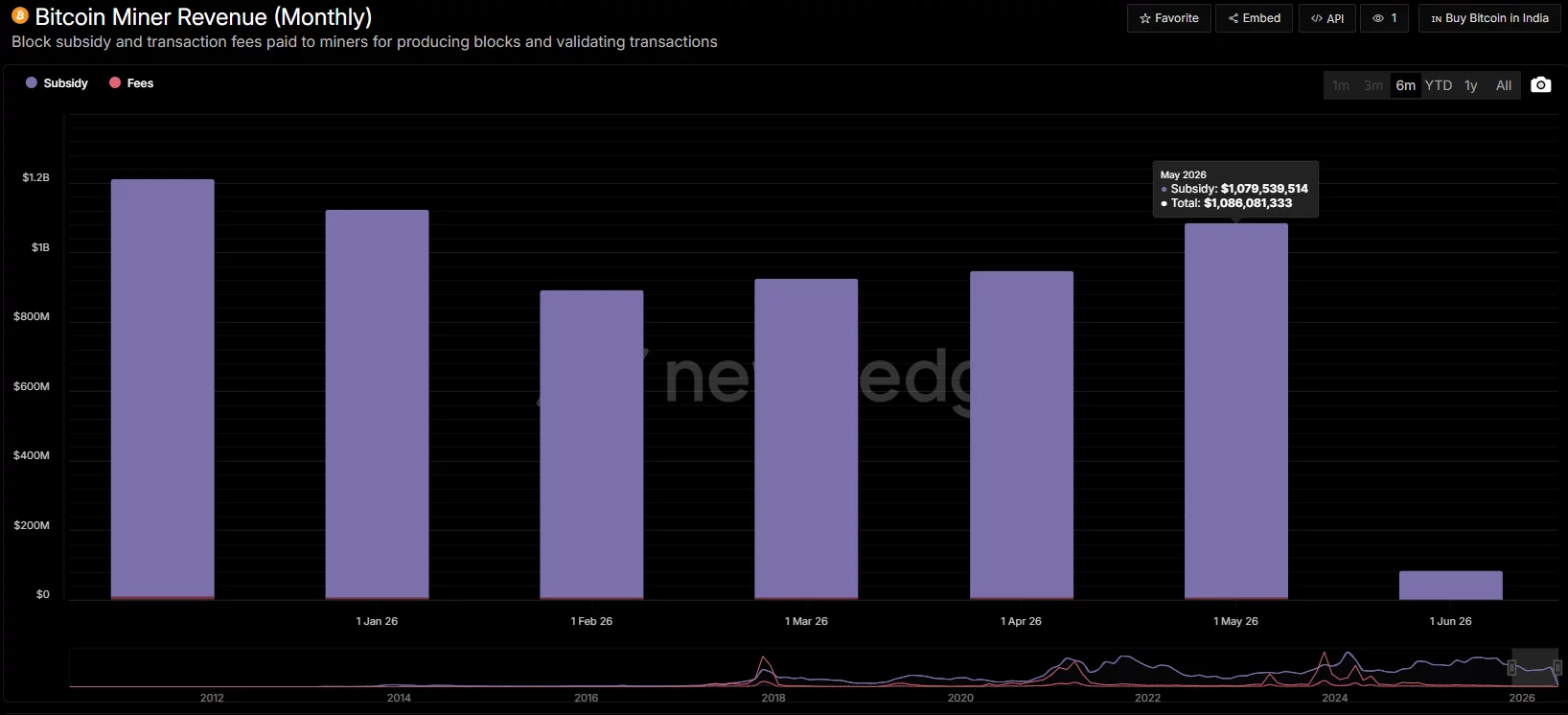

Bitcoin miners have entered June with revenue above $1 billion for the first time in four months, but falling Bitcoin prices are already putting renewed pressure on mining economics.

Summary

- Bitcoin miner revenue topped $1.08 billion in May, the highest level since January.

- Hashprice fell nearly 18% in a month as Bitcoin hovered near the $65,000 support zone.

- A projected 9% difficulty cut may ease pressure on miners if current conditions persist.

According to data from Newhedge, miners generated $1.086 billion in revenue during May, the highest monthly total since January. Most of that income came from the 3.125 BTC block subsidy, which contributed roughly $1.079 billion, while transaction fees accounted for only a small portion of earnings.

Even as miners posted a stronger month, conditions have weakened since the start of June. According to data from crypto.news, Bitcoin (BTC) price dropped as much as 4.5% on June 3, touching an intraday low of $65,700. The leading crypto asset was trading a little higher at $65,800 at press time.

Bitcoin’s recent decline followed heightened geopolitical tensions after Iran launched retaliatory strikes against U.S. targets, prompting a broader risk-off move across financial markets.

Meanwhile, analysts at Citigroup recently argued that sustained spot Bitcoin ETF outflows have also been a more important driver of Bitcoin’s weakness than Strategy’s sale of 32 BTC. In a research note, the bank pointed to nearly $4 billion in ETF withdrawals and described ETF flows as one of the strongest indicators of demand for the asset.

Falling Bitcoin prices are reducing miner profitability

As Bitcoin price trades close to the important $65,000 support area, mining profitability has continued to deteriorate.

Data from Hashrate Index shows the daily value generated by one petahash per second of mining power has fallen to approximately $30.77, down from $37.44 a month ago. The decline represents a drop of nearly 18% over the past 30 days and has pushed hashprice to levels last seen in early April.

Mining companies are already responding to the weaker economics. Network hashrate has fallen from around 1,000 exahashes per second to below 975 EH/s as some operators reduce activity or disconnect less efficient machines.

Meanwhile, slower mining activity has affected block production times. Hashrate Index data showed blocks were being produced every 10 minutes and 59 seconds on average, well above Bitcoin’s 10-minute target. If current conditions persist until the next adjustment period around June 13, estimates suggest mining difficulty could decline by roughly 9%.

A lower difficulty level would reduce competition among miners and allow remaining participants to earn slightly more Bitcoin for the same amount of computing power.

Technical and network signals point to a critical period ahead

While the expected difficulty reduction could provide temporary relief, Bitcoin’s price remains the biggest factor affecting miner revenue.

According to a previous analysis report by crypto.news, Bitcoin is approaching completion of a rounding top formation on the daily chart. Such a pattern is generally considered a bearish reversal formation, and a decisive break below $65,000 could expose the next major demand zone near $60,000.

On the other hand, the same analysis stated that a recovery above $68,700 could weaken the bearish setup and create conditions for a move back toward $72,000.

Transaction fees have offered limited support. After remaining below 0.6% of total block rewards for an extended period, fee income has recently improved. Recent network data shows fees accounted for roughly 1.16% of total block rewards over the past 24 hours.

For now, miners are balancing the benefits of a likely difficulty cut against a market that remains under pressure from ETF outflows and geopolitical uncertainty. Whether May’s strong revenue performance can continue through June may depend largely on Bitcoin’s ability to hold above key support levels.

Bitcoin’s recent struggles to rise in tandem with U.S. stocks has sparked a wave of explanations, from concerns about Michael Saylor’s Strategy (MSTR) selling bitcoin to questions about whether institutional demand is beginning to fade.

Charles Schwab analyst Jim Ferraioli sees a simpler explanation: Bitcoin is losing the momentum trade.

“Bitcoin has been in a bear market since October,” Ferraioli said in an interview. “Not to say it’s as simple as that, but it’s kind of simple as that.”

The comments stand in contrast to a market narrative that has remained largely focused on positive developments. Over the past year, crypto has secured spot ETF approvals, attracted billions of dollars in institutional capital and moved closer to regulatory clarity in Washington. Yet despite those developments, bitcoin has struggled to sustain the type of explosive rally many investors expected.

Instead, capital has been flowing elsewhere.

“We found a bottom in early February, and since then another large Wall Street firm had a successful ETF launch, and so you saw this kind of return to the institutional adoption narrative,” Ferraioli said.

That rebound helped bitcoin recover from its February lows. But unlike previous crypto cycles, the recovery stalled before developing into a broad speculative frenzy.

That’s because crypto investors are not fundamentally driven, but chase momentum, he said. In his view, bitcoin’s problem isn’t a lack of bullish news. It’s competition.

Historically, crypto has benefited when it becomes the market’s most compelling speculative opportunity. When prices rise, traders pile in. When another asset class begins attracting attention, capital often follows.

“Crypto investors historically just go wherever the momentum is,” Ferraioli said. “And momentum is out of crypto at the moment.”

The destinations for that capital have changed over the past year.

Some investors have gravitated toward precious metals. Gold has attracted significant inflows as investors seek alternatives to both equities and crypto. Others have become increasingly focused on artificial intelligence, which has emerged as the dominant growth narrative across financial markets.

The AI boom has created a new class of speculative opportunities that didn’t exist in previous crypto cycles. Public companies tied to AI infrastructure, data centers and advanced computing have generated strong returns, while anticipated IPOs from firms such as OpenAI and Anthropic have become focal points for investors looking for the next growth story.

According to Ferraioli, crypto investors are participating in that shift as well.

“I think people that are excited about momentum are getting excited about IPOs,” he said. “Then some of these you can actually access the private shares on these decentralized exchanges on Hyperliquid.”

That trend is significant because it highlights how crypto-native trading infrastructure is increasingly allowing investors to speculate on assets beyond cryptocurrencies themselves.

Platforms such as Hyperliquid (HYPE) have introduced perpetual contracts tied to private companies, commodities and other non-crypto assets, giving traders new places to deploy capital.

For bitcoin, that means it is no longer competing solely against other cryptocurrencies.

It is competing against every major speculative narrative in the market.

Ferraioli also downplayed concerns surrounding Strategy’s recent sale of 32 bitcoin, a transaction that sparked debate among investors because of Saylor’s long-standing reputation as one of bitcoin’s most committed advocates.

“The narrative has been that they’ll never sell,” Ferraioli said. Yet he believes the market impact of the transaction itself has been overstated. “But I don’t think [the sale] is what’s really driving it,” he said.

Instead, he views the sale as a convenient narrative attached to a broader trend that was already underway.

Part of that trend may be tied to investor cost bases and many ETF investors are still recovering from sharp swings over the past year and see the current price point as an opportunity to exit positions rather than increase them.

“I think you get to those levels and you get people that are saying, ‘Hey, I made my money back, maybe I’ll revisit it later,’” Ferraioli said.

That dynamic has contributed to a market that feels very different from the euphoric phases of previous cycles.

Ferraioli argues that institutional adoption, while real, remains smaller than many market participants assume. Bitcoin ETFs have expanded access to crypto, but much of the asset class remains dominated by retail investors and momentum-driven traders.

“Again, this is primarily a retail asset,” he said.

The distinction matters because retail investors often react differently than traditional institutional allocators. Rather than building positions based on discounted cash flow models or long-term valuation frameworks, they tend to chase trends.

That behavior helps explain why bitcoin has struggled to capitalize on positive regulatory developments.

The crypto industry is awaiting potential passage of the Clarity Act, a bill that many industry participants believe could provide a clearer framework for digital assets in the U.S. Over the longer term, Ferraioli believes such developments could support adoption.

In the short term, however, regulation alone may not be enough to reverse the current trend.

“There is still more demand for downside protection,” he noted elsewhere in Schwab’s market outlook, though that pressure has begun to ease in recent weeks.

Seasonality may also be contributing to the slowdown. Summer has historically been one of bitcoin’s weaker periods, as trading activity declines and investors shift attention elsewhere.

“People know that for bitcoin seasonally summer is the weakest time,” Ferraioli said.

That leaves the market in an awkward position.

Institutional adoption is improving. Regulatory clarity is advancing. Major financial firms continue building crypto products. Yet none of those developments guarantee higher prices if investor attention is focused elsewhere.

“There’s a lack of a reason to be buying here when there’s other things you can choose,” Ferraioli said.

For now, he argues, the biggest challenge facing bitcoin isn’t Saylor, regulation or even macroeconomics.

It’s that investors have found something else to chase.

Crypto World

Old DxSale Lockers Drained for $7.3M Across 1,400 BNB Chain Pools as Owner-Privilege Exploits Pile Up

An attacker drained roughly $7.3 million from more than 1,400 legacy liquidity-provider positions sitting in old DxSale locker contracts on BNB Chain, security firms PeckShield and Coinsult flagged on May 29, a drain made possible not by a smart-contract bug but by a silent ownership transfer… Read the full story at The Defiant

[PRESS RELEASE – Mahe, Seychelles, June 3rd, 2026]

Whale.io is excited to announce the official launch of The Whale Printer, an on-platform staking system for the native $WHALE token. The feature enables eligible token holders to lock $WHALE for fixed periods in exchange for predetermined token rewards.

The staking system is structured around three lock-up periods, each associated with a fixed multiplier and corresponding annual percentage yield (APY):

$WHALE Staking Yields

Whale Printer offers three straightforward lock periods with impressive returns:

- 90 days (1.2x multiplier) — 107.8% APY

- 180 days (1.5x multiplier) — 129% APY

- 365 days (3x multiplier) — 200% APY

Multipliers are fixed at the time a staking position is created, providing predefined reward terms throughout the selected lock period.

Whale Printer Reward Pool

All rewards are paid from a dedicated pool of 20 billion $WHALE, representing 20% of the total token supply. The pool does not replenish. When it is exhausted, The Whale Printer closes permanently and no new staking positions can be opened. This creates strong incentives for early participants while ensuring long-term sustainability and real value accrual for $WHALE stakers.

How to Stake $WHALE on Whale.io

To participate, $WHALE tokens must be available within a Whale.io account balance. Staking positions can be created through the token page by selecting a token amount and preferred lock period.

The system supports up to 10 concurrent staking positions per account, each operating independently with its own allocation, lock period, and completion timer. The minimum staking requirement is determined by platform parameters. Early withdrawal is not available for active staking positions.

Why Stake $WHALE

$WHALE serves as the native utility token of the Whale.io ecosystem. According to the project, token distribution has occurred through platform gameplay, missions, and user activity, without allocations to private sales, presales, or venture capital participants.

Whale Printer expands the token’s functionality by introducing a staking mechanism that distributes rewards in $WHALE based on selected lock periods and predefined reward structures.

Whale Printer is now available through whale.io/token

About Whale.io

Whale.io is a leading online crypto casino and sportsbook. The platform features exclusive Whale Originals games, blockchain-integrated rewards, massive cashback, and a strong emphasis on transparency, community ownership, and on-chain verifiability. With $WHALE as its native utility token, Whale.io continues to build one of the most rewarding ecosystems in crypto gaming.

To discover the future of Whale.io Casino and $WHALE token users can:

Read more on whale.io/token

Visit Whale socials: https://linktr.ee/whalesocials_tg

The post Whale.io Launches Whale Printer: $WHALE Token Staking appeared first on CryptoPotato.

A monthly research report from Bitwise’s European arm published this week pegs bitcoin’s theoretical “fair value” at roughly $224,000 if the asset were widely adopted as portfolio insurance against G20 sovereign debt defaults.

The research team described the figure as a “model-implied illustrative figure, not a price target or forecast,” however.

The figure stems from a theoretical framework first proposed by analyst Greg Foss in 2021, which treats bitcoin as a credit default swap on sovereign bonds.

Because the bitcoin network has no central issuer and operates without a sovereign backstop, the Foss model frames it as a non-correlated hedge against the possibility of major sovereign defaults.

The implied $224,000 fair value depends on the weighted default probability across group of 20 (G20) sovereigns and the market capitalization of the bonds being notionally insured.

It built the case around stress in sovereign bond markets. Japanese 30-year government bond yields have hit record highs while 10-year JGB yields sit at multi-decade peaks.

The International Monetary Fund and OECD have warned that governments and companies are set to borrow $29 trillion from bond markets this year, 17% higher than 2024, with the IMF describing markets as becoming less forgiving and investors as increasingly questioning the limits of sovereign borrowing capacity.

Bitwise singled out Japan’s JGB market as particularly vulnerable, citing its roughly $7.5 trillion size as the world’s second-largest sovereign bond market, Japanese investors’ approximately $1.2 trillion in U.S. Treasury holdings, and Japan’s roughly 230% debt-to-GDP ratio.

It noted that 10-year swap spreads, which measure sovereign risk premia, are at their highest levels since the 2011-2012 European debt crisis across major sovereign bonds.

But the report flagged some near-term headwinds for bitcoin as well.

Higher global bond yields have made Strategy’s (MSTR) STRC perpetual preferred equity dividends less attractive to investors, and STRC has recently traded below par.

Strategy buys have accounted for roughly two-thirds of institutional bitcoin demand via global treasury companies and bitcoin ETPs through 2026 to date, per Bitwise’s count, meaning a stall in Strategy’s STRC-funded accumulation could materially dent the flow.

The upside scenarios Bitwise outlines hinge on monetary policy and sovereign stress.

A Fed pause under newly confirmed chair Kevin Warsh against rising inflation could push real yields lower, which the report cited as a historical tailwind for bitcoin. A sovereign bond capitulation that forces central bank intervention to safeguard financial stability could validate bitcoin’s role as a decentralized hedge against sovereign counterparty risk.

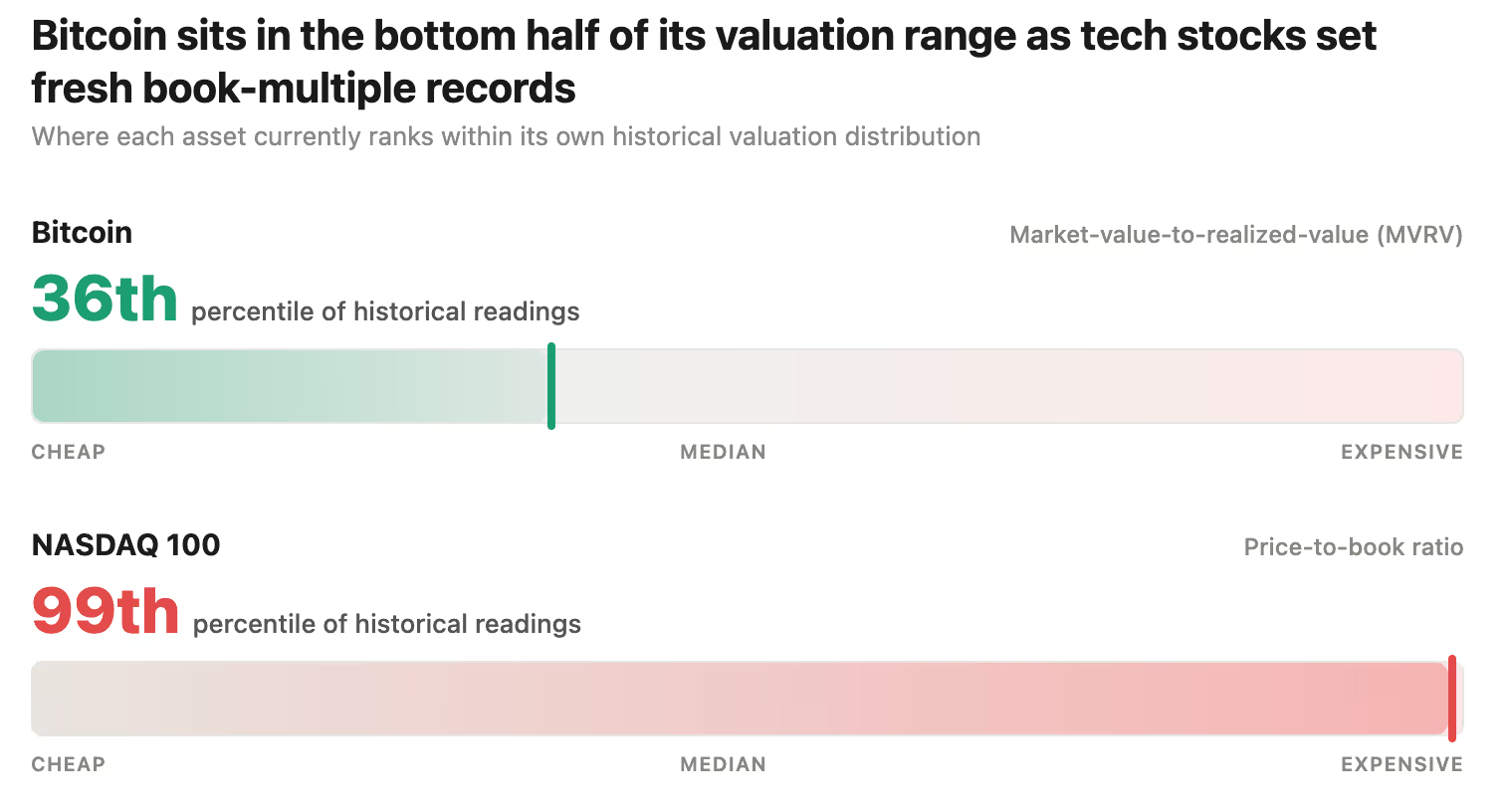

On valuation, the report flagged one of the most extreme divergences between bitcoin and U.S. large-cap tech it has observed. Bitcoin’s market-value-to-realized-value ratio sits in the lower half of its historical distribution, with only 36% of historical readings below the current level.

The NASDAQ 100’s price-to-book ratio, by contrast, is at its highest level on record, with 99% of historical readings below the current level.

Bitcoin was trading near $66,300 on Wednesday after sliding from above $71,000 earlier this week.

The European Union’s Markets in Crypto Assets Regulation (MiCA) reaches a pivotal juncture on July 1, when the transitional regime concludes and crypto asset service providers operating under national regimes must hold a MiCA licence or discontinue EU operations. According to ESMA, non-authorized entities will not be permitted to operate within the bloc from that date and should implement wind-down plans and client migrations rather than rely on an open-ended transitional status while awaiting a decision.

The deadline raises the prospect that some firms will suspend EU activities while their MiCA applications are under review, potentially disrupting access for millions of EU-based users who continue to engage with platforms not yet authorized under MiCA.

Key takeaways

- Effective July 1, any crypto asset service provider without a MiCA licence, operating under national exemptions, must cease EU operations or risk enforcement actions.

- Regulators have explicit enforcement tools to halt services, force client offboarding, publish firm names, and impose administrative fines for unauthorized activity under MiCA.

- France has authorised 19 CASPs so far, with about 25 additional applications under review, while unauthorized providers face criminal penalties (up to two years in prison and a 30,000 euro fine).

- Germany requires that providers previously operating under exemptions obtain licence by June 30, with enforcement measures possible where appropriate.

- Austria did not extend grandfathering under its pre-MiCA regime; no exchanges are operating without a licence in the country, with nine CASPs licensed by the FMA and a significant volume of MiCA applications still in process.

- Industry estimates suggest a sizable share of European users may still interact with non-MiCA-authorized platforms; OKX Europe’s analysis indicates that a substantial portion of active users may be on non-authorized exchanges.

- Major exchanges remain in the licensing process, including Bitget (Austria) and Binance (Greece); neither is currently listed among MiCA-authorized providers in the EU, with statuses evolving as regulators review applications.

National enforcement landscapes and licensing progress

France’s Autorité des marchés financiers (AMF) has authorised 19 crypto asset service providers to operate under MiCA, with roughly 25 applications still under review. The AMF emphasizes that from July 1, providers not licensed under MiCA must cease their activities within the French market. The regulator has also signaled that it can blacklist firms, issue public warnings, and seek court orders to block access to sites targeting French users. Unauthorized activity is treated as a criminal offence with potential penalties including prison time and fines.

Germany has adopted a national implementation approach that includes a licensing requirement for providers previously operating under exemptions. BaFin, its national regulator, indicated that a licensing window closes by June 30, and enforcement may be applied where appropriate as regulators review ongoing applications. The German stance aligns with MiCA’s directive for national authorities to grant immediate enforcement powers against unauthorised services.

Austria presents a stricter posture by choosing not to extend any grandfathering for virtual asset service providers under its pre-MiCA regime. The post-transition environment is designed so that no exchanges operate without a licence. The Finanzmarktaufsicht (FMA) has licensed nine CASPs to date, and it notes that MiCA-related applications are significant, though it does not disclose pending figures.

Legal risk, enforcement tools, and what the end of transitional periods means for providers

Industry legal counsel stress that simply having a MiCA application in progress does not shield a CASP from the July 1 deadline. Firms continuing to serve EU clients without an authorised MiCA framework will be operating unlawfully and cannot expect business-as-usual treatment once transitional protections lapse. MiCA itself equips member states with clear authorities to order an immediate halt to services, mandate client offboarding, publicly name non-compliant firms, and impose administrative fines for unauthorized activity. This creates a path for rapid, targeted action by regulators against non-compliant platforms.

These enforcement provisions bear significantly on the operational dynamics across the EU, potentially triggering abrupt wind-downs, forced migrations of clients to compliant platforms, and heightened scrutiny of cross-border service provision. The end of transitional periods also intersects with broader regulatory expectations around AML/KYC compliance, consumer protection, and ongoing supervisory oversight of licensing practices across member states.

Impact on users and market structure

The potential disruption extends beyond the regulated landscape into user access and liquidity across the European market. Analysis shared with Cointelegraph by OKX Europe suggests a sizable portion of European crypto users may still be active on platforms that are not MiCA-authenticated. OKX Europe quantified a period from May 2025 to May 2026 during which 18.5 million crypto app downloads occurred in Europe; approximately 7.6 million of those downloads, or 41%, were for exchanges not appearing on the independent MiCA-authorized provider register maintained from ESMA and national datapoints. OKX cautions that app-install data undercounts user activity due to browsers or earlier-app usage, and thus estimates may not capture all active users. OKX Europe CEO Erald Ghoos described this as a meaningful exposure, noting that many users may still rely on non-authorized platforms through multiple access channels.

The European Securities and Markets Authority (ESMA) has not provided a public estimate of how many EU users remain on unauthorised platforms, citing the absence of non-public information. The regulatory framing underscores a transition in market structure: as MiCA entrants consolidate, a period of adjustment is expected where users migrate to licensed venues or where enforcement narrows the field of available services. This shift has potential implications for cross-border banking relationships, stablecoin integration within regulated rails, and the standardization of licensing and supervisory practices across jurisdictions.

Active applicants and ongoing licensing momentum

Not all major exchanges have achieved MiCA licensure. Bitget has applied for a MiCA licence in Austria in 2025 and indicated it expects regulatory approval in the second quarter of 2026; it has stated it will refrain from offering EEA services until authorization is granted. Binance has pursued a MiCA licence in Greece via the Hellenic Capital Market Commission and is not listed among MiCA-authorized providers in the EU as of now. Binance did not respond to requests for comment on its application status. The ongoing review processes for these and other providers will shape the pace at which non-localized regional operations convert to fully MiCA-compliant activity.

These licensing trajectories illustrate how enforcement timelines, national regulatory interpretations, and the resources available to review applications will influence the competitive landscape. For exchanges of scale, the MiCA licensing process functions not merely as a compliance hurdle but as a potential market access gate that can determine cross-border growth and consumer reach within the EU’s single market framework.

Closing perspective

As the July 1 deadline approaches, the EU’s MiCA framework moves from principle to practice, pushing providers toward formal licensing, wind-down planning, or exit from the EU market. The evolution will test regulatory coordination among member states, map user exposure across compliant and non-compliant platforms, and redefine the structural dynamics of crypto service provision in Europe. Forward-looking vigilance will be essential for institutions tracking licensing trajectories, enforcement actions, and the practical implications for compliance, risk management, and customer continuity in a transitioning market.

On-chain data confirmed that the Zcash network is down, it has been producing no blocks for over 4 hours, a catastrophic deviation from the protocol’s 2.5-minute block target that left thousands of transactions stranded in the mempool with zero confirmations.

— Coin Bureau (@coinbureau) June 3, 2026

JUST IN: Zcash reportedly down after failing to produce any block in the past 4 hours, per InfinityHedge. pic.twitter.com/KdijaSlbCQ

JUST IN: Zcash reportedly down after failing to produce any block in the past 4 hours, per InfinityHedge. pic.twitter.com/KdijaSlbCQ

ZEC dropped 2% in the hour following the four-hour mark of the halt, with exchange deposit services on Binance and Kraken effectively frozen as no block confirmations cleared. This could be a consensus bug, a mining coordination failure, or something uglier has not been confirmed.

Discover: The Best Crypto to Diversify Your Portfolio

Zcash Down: Blockchain Halt

Block explorers monitoring the Zcash chain confirm the halt is real and sustained. Under normal operation, the network targets a new block every 2.5 minutes via its Equihash proof-of-work consensus, and these four hours of silence have likely brought 96 missed blocks.

Community developers active on the Zcash Foundation and Electric Coin Co. (ECC) forums have circulated two primary theories: a consensus bug triggered by a recent minor node update, or an unforeseen interaction with the network’s difficulty adjustment algorithm.

As of now, a standard 51% attack has been largely ruled out as the signature here is total cessation of block production, and not chain reorganization.

INTEL: Zcash coordinated a network upgrade due to an Orchard pool soundness vulnerability.

Multiple block explorers, including the official explorer, still appear to be catching up after the upgrade, while block production is reportedly continuing, as seen on ZecMiningPool.

We… https://t.co/743lwfwqJ7 pic.twitter.com/eW3tJNz6Tf— Solid Intel

(@solidintel_x) June 3, 2026

What the data does NOT yet confirm is the precise block height at which production stopped, if the halt is affecting both Zcashd and ECC’s Zebra client simultaneously, or if a hotfix is imminent.

This is not the first time Zcash’s dual-client architecture has created consensus-layer stress, in early June 2026, an emergency Zebra consensus patch was required to prevent a network split, and a separate Emergency Orchard Upgrade temporarily paused shielded private transactions to address a pool vulnerability.

The pattern of rapid-response emergency patches is becoming a feature rather than an anomaly. Until ECC or the Zcash Foundation issues an official post-mortem, the cause sits in an uncomfortable grey zone. Miners are clearly not producing. The reason why remains unconfirmed.

ZEC Price Slides as Network Outage Triggers Confidence Selloff

ZEC was trading in the range of around 2% lower from an hour ago, with selling pressure accelerating precisely as the four-hour mark of the blockchain halt became apparent to broader market participants. The move mirrors the pattern seen across other network disruption events, slow initial reaction, then a sharp leg down once the duration makes denial impossible.

ZEC had staged an extraordinary recovery from its July 2024 lows under a dollar, surging over 16x to the $250 range by April 2026, with a 16% single-day spike to $372 recorded on April 9, 2026, and another sharp 30% move in May that put the coin at above $600.

The structural read is bearish until block production resumes and an official explanation confirms the halt is contained.

Discover: The Best Token Presales

The post Zcash Down: No Blocks Produced in 4 Hours appeared first on Cryptonews.

Baggaley, Bance and Kafaji set to leave Brighton Women

Apple agrees to hand India the financials it spent months trying to withhold

Adoptive dad in Preston Davey trial says he ‘misplaced’ trust in partner

-

Tech6 days ago

Tech6 days agoWaymo dominates autonomous vehicle registrations as Tesla trails behind

-

News Videos5 days ago

News Videos5 days agoThis is BROKEN! INSANE 5x MONEY CAR WASH WEEK! The NEW GTA Online UPDATE Today! (GTA5 New Update)

-

Tech4 days ago

Tech4 days agoSpaceX just won a second Golden Dome contract. This one is $4.16 billion.

-

News Videos5 days ago

News Videos5 days agoSHE IS KILLING XRP!!! WATCH URGENT AND ACT FAST

-

Business2 days ago

Business2 days agoJade Biosciences, Inc. (JBIO) Discusses Positive Interim Results From JADE101 Phase I Healthy Volunteer Study and Development Plans Transcript

-

NewsBeat5 days ago

NewsBeat5 days agoFIRST NIGHT REVIEW: Take That bring the Circus back to life in spectacular sun-soaked style

-

Crypto World5 days ago

Crypto World5 days agoCFTC Has Approved the First Regulated Bitcoin Perpetual Contract in the U.S.

-

Business4 days ago

Business4 days agoIs the Spurs Phenom Already Better Than Prime Diesel?

-

NewsBeat5 days ago

NewsBeat5 days agoNovak Djokovic v Joao Fonseca LIVE: French Open latest scores and results after Jannik Sinner’s shocking collapse

-

Crypto World5 days ago

Crypto World5 days agoSnowflake (SNOW) Stock Rallies on Strong Q1 Results and AI Product Growth

-

Entertainment5 days ago

Entertainment5 days agoWeak ‘Supergirl’ Box Office Tracking Amid Milly Alcock Backlash

-

Business4 days ago

Business4 days agoDemand Conditions Improve In Chemicals Sector In April 2026

-

Crypto World5 days ago

Crypto World5 days agoMicroStrategy Moves $30 Million in BTC to Coinbase Prime: Is the Bitcoin Sell-Off Already Here?

-

Politics4 days ago

Politics4 days agoThe House | Inside Andy Burnham’s Makerfield Campaign: “Nobody Thinks This Is In The Bag”

-

Tech5 days ago

Tech5 days agoThis Week In Security: Ubiquiti Fixes, And FreeBSD Joins The Club You Don’t Want To Join

-

Entertainment4 days ago

Entertainment4 days agoOne of the Greatest Sitcoms of All Time Shoots Up Apple TV’s Charts 11 Years Later

-

Entertainment5 days ago

Entertainment5 days agoMaddox Jolie-Pitt Legally Requests to Drop Brad’s Surname

-

Crypto World1 day ago

Crypto World1 day agoSeagate (STX) Stock Surges to Record High on AI Boom and Legal Settlement

-

Entertainment4 days ago

Entertainment4 days agoBritney Spears Shares Troubling Update After Hard Year

-

Entertainment5 days ago

Entertainment5 days agoBruce Willis’ Generosity Resurfaces Amid His Dementia

You must be logged in to post a comment Login