Crypto World

Banks use the XRP Ledger. They don’t buy XRP

This is the uncomfortable truth at the center of the XRP investment case in 2026.

Summary

- XRP Ledger adoption is real, but ledger usage does not automatically create XRP token demand.

- XRP value capture depends on fee burn, reserves, and bridge-currency demand, but each channel has limits.

- RLUSD helps Ripple serve banks, yet it may also let institutions use Ripple infrastructure without buying XRP.

- The real test is whether XRP lending, RWA trading pairs, and ODL volume scale enough to require the token.

The XRP Ledger is winning. Banks and payment firms are adopting it, tokenized funds are settling on it, stablecoins are moving across it, and Ripple has built an end-to-end institutional infrastructure that traditional finance can plug into without changing how it operates. By almost every measure of adoption, the thesis XRP holders have believed for years is finally coming true.

And yet the XRP token has spent 2026 stuck in a narrow band around $1.30, far below where its believers expected adoption to take it. The reason is a problem most bullish coverage glosses over: a thriving XRP Ledger does not automatically create demand for the XRP token. Banks can use the rails without ever buying the asset.

This piece works through exactly how XRP is supposed to capture value, why those mechanisms are not firing the way holders hoped, what would have to change for the disconnect to close, and how to tell the difference between a transitory lag and a structural flaw. It is the honest version of the XRP story.

The disconnect, stated plainly

Start with the two facts that do not fit together, because holding them side by side is the whole point.

Fact one: the XRP Ledger is being adopted by serious institutions. Ripple Payments and On-Demand Liquidity are live across more than 40 corridors with named partners processing real cross-border flows. UnionBank in the Philippines, the first fully licensed virtual asset bank there, uses ODL for remittances. Travelex Bank Brazil, Yes Bank and Axis Bank in India, and dozens of other institutions have moved past pilots into production. Cumulative Ripple Payments volume crossed $95 billion as of January 2026. Tokenized funds sit on the ledger, stablecoins move across it, and Ripple has assembled a full stack, prime brokerage through Ripple Prime, treasury services through Ripple Treasury, and a bundled product combining stablecoin issuance, custody, and digital identity. This is real institutional adoption, not vaporware.

Fact two: the XRP token has gone nowhere. It trades around $1.30, pinned below its moving averages, locked in a range that has held since early in the year. The adoption keeps growing and the price keeps not responding. After reaching above $3.50 in the prior summer, XRP entered a long decline of lower highs and lower lows that the adoption news has not reversed.

The gap between these two facts is the most important thing to understand about XRP right now, and it has a name worth using: value capture. A blockchain can be wildly successful as infrastructure while its native token captures almost none of that success in price. That is not a contradiction or a market error. It is a question of plumbing, specifically whether the token is mechanically required, in meaningful quantities, by the activity flowing across the network. For XRP, the honest answer in 2026 is: not as much as you would think.

How XRP is supposed to capture value

XRP has three plausible channels through which network usage could translate into token demand. Walking through each one shows why the disconnect exists, because each channel turns out to be weaker than the bull case assumes.

The first channel is fee burn. Every transaction on the XRP Ledger destroys a tiny amount of XRP as a fee, which is mildly deflationary and, in theory, links usage to scarcity. The problem is scale. The amount of XRP burned daily has collapsed 95 percent since December 2024, from around 15,000 XRP per day to a current range of roughly 163 to 750 XRP per day. Over the entire history of the ledger, only about 14 million XRP have ever been burned, equal to 0.014 percent of the total supply. To put that in perspective, even if tokenized-asset activity drove a burn rate one hundred times higher than today, it would still take decades to create meaningful scarcity. And there is a catch that makes fee burn self-defeating as a value driver: fees only climb materially when the network is congested, and congestion is the opposite of what a payment network wants. So XRP is consumed every time the ledger is used, but fee burn alone cannot move the valuation in any macro-relevant way.

The second channel is the reserve mechanism, and it is the most direct and measurable of the three. The XRP Ledger requires users to lock up small amounts of XRP to open an account and to own certain ledger objects. Current mainnet requirements are 1 XRP per account plus 0.2 XRP per owned item, and the items that consume reserves include trust lines, which are needed to hold most issued assets such as stablecoins and tokenized instruments. This means that as more accounts and more tokenized assets live on the ledger, more XRP gets locked into reserves, creating genuine structural demand. This is the strongest part of the bull case. But notice its limit: the demand is tied to the number of accounts and objects, not to the dollar value being settled. A bank moving a billion dollars across the ledger locks up the same trivial reserve as a bank moving a thousand. The reserve mechanism scales with the count of things, not the value of flows, which caps how much demand it can generate even under heavy institutional use.

The third channel is the bridge-currency function, the original thesis, and the one in the most trouble. In Ripple’s On-Demand Liquidity model, a payment firm converts local currency into XRP, sends it across the ledger in seconds, and converts it to the destination currency on arrival, eliminating the need to park cash in foreign accounts. Every such transaction does generate real buy demand for XRP, because the token is actually purchased as the bridge. This is the mechanism that directly ties usage to token demand. The problem is twofold: ODL volume, while real, is not large enough to move the price on its own, and Ripple has introduced something that may cannibalize it.

The RLUSD problem the bulls underplay

The thing most likely to weaken XRP’s strongest value-capture channel is a Ripple product: its own stablecoin, RLUSD.

RLUSD launched as a dollar-backed stablecoin and crossed a $1.26 billion market cap in under a year. Ripple now runs a hybrid model where RLUSD operates alongside XRP in Ripple Payments. The official framing is elegant: RLUSD provides price stability for banks that do not want crypto volatility, while XRP acts as the bridge that swaps between different currencies. In this telling, the two are complementary, with XRP as the settlement layer moving value between stablecoin systems.

But look at it from a bank’s perspective and the tension becomes obvious. Many financial institutions prefer stablecoin settlement precisely because it avoids holding a volatile asset like XRP, even for the few seconds of a bridge transaction. If a bank can settle a corridor using RLUSD end to end, it has no need to touch XRP at all. By offering RLUSD, Ripple meets banks where they are, which is good for Ripple the company, but it also hands those banks a way to use Ripple’s infrastructure without generating XRP demand. The hybrid model that bulls cite as proof of XRP’s central role may, in practice, route around the token in exactly the corridors where stablecoins work well.

This connects to a broader competitive reality. In dollar-denominated corridors, stablecoins like USDC and USDT are genuine competitors to XRP, settling cross-border payments almost as fast while holding their value in transit. XRP’s structural advantage is real but specific: it shines in fiat-to-fiat corridors where neither party wants dollar exposure, particularly emerging-market routes where a direct local-currency-to-local-currency bridge beats routing through a dollar stablecoin. That is a meaningful niche, but it is a niche, and the rise of regulated stablecoins under frameworks like the GENIUS Act puts a ceiling on XRP’s addressable market even where it does not eliminate the use case.

The starkest illustration came when Société Générale tokenized its euro stablecoin on a ledger: the operation could be carried out without any party needing to hold XRP beyond the fraction of a cent required to pay the transaction fee. That is the disconnect in a single example. The ledger gets the business. The token gets a fraction of a cent.

Why this isn’t necessarily fatal

Having made the bear case honestly, it is worth giving the bull case its strongest form, because the disconnect is not proof that XRP is doomed. It is proof that XRP’s value capture depends on specific things happening that have not happened yet.

The reserve mechanism genuinely does scale with adoption, and if the XRP Ledger becomes the settlement layer for a large fraction of tokenized real-world assets, the cumulative reserve demand from millions of accounts and tens of millions of ledger objects could become substantial. The bull case is not that any single mechanism is huge, but that account growth, trust-line proliferation, and tokenized-asset issuance compound over time into structural demand that the current depressed price does not reflect.

There is also genuine optionality in the roadmap. The XRP Ledger is adding lending protocols and a native decentralized exchange, and if those achieve real adoption, they create new contexts in which XRP could be required as a base trading pair or collateral. Garlinghouse has made aggressive predictions, including that the XRP Ledger could eventually capture 14 percent of the volume currently running through SWIFT, which if even partially realized would represent a transformation in ODL scale that does move the token. The regulatory unlock matters too: the CLARITY Act writing XRP’s commodity status into law would green-light US banks for ODL adoption and open the door to spot ETFs, both of which create demand channels that regulatory uncertainty has kept closed.

The honest framing is that the bull case is conditional, not broken. XRP captures value if specific conditions are met: if the new protocols achieve real adoption, if tokenized-asset issuers choose to use XRP as a medium of exchange rather than operating purely in stablecoins, and if ODL volume scales into truly transformative territory rather than growing incrementally. Those are real possibilities. They are just not guarantees, and the current price reflects a market that has stopped paying for the promise and started waiting for the proof.

How to tell a lag from a flaw

The most useful thing an XRP holder or analyst can do is define, in advance, what evidence would distinguish a temporary disconnect from a permanent structural feature. Vague faith that “adoption will eventually flow to the token” is not analysis. Specific, falsifiable thresholds are.

One sharp framework, laid out by analysts watching the value-capture question, proposes three concrete tests over a six-month horizon. First, lending volumes denominated in XRP exceeding $500 million, which would show the new DeFi protocols creating real token demand. Second, at least three major real-world-asset issuers incorporating XRP as a trading pair in their products, which would show tokenized-asset activity actually requiring the token rather than routing around it in stablecoins. Third, ODL volume consistently exceeding $500 million per day, which would show the bridge-currency function scaling to a level that generates sustained buy pressure. If those three things happen, the current disconnect is a transitory phase and the bull case is vindicated. If they do not, the disconnect is structural, and XRP is an infrastructure token whose infrastructure simply does not need much of it.

The remittance math gives a sense of the distance involved. The global remittance market is roughly $685 billion annually. XRP processed around $15 billion through ODL in 2024, about 2.2 percent penetration. That is meaningful progress, but it is also a reminder of how far the network is from the dominance its more ambitious price targets imply. For XRP to reach the $5-plus targets that bulls cite, ODL adoption would need to scale into transformative territory, doubling and redoubling rather than growing 30 to 50 percent a year.

So the practical guidance is to ignore the adoption headlines that do not specify token demand and watch the three thresholds instead. “Bank X is using the XRP Ledger” tells you nothing about whether bank X is buying XRP. “ODL volume hit $500 million a day” tells you everything. The disconnect closes when the metrics that actually require the token start moving, and not before.

The bottom line on the disconnect

XRP in 2026 is the cleanest example in crypto of a successful network whose token has not yet been invited to the party. The XRP Ledger has achieved something rare: it has become financial infrastructure that institutions adopt because it is efficient, compliant, and cheap. That is a genuine accomplishment, and the adoption is not fake. But the three mechanisms that are supposed to turn that adoption into XRP demand, fee burn, reserves, and the bridge-currency function, are each weaker than the bull narrative assumes. Fee burn is negligible and self-defeating. Reserves scale with object count, not settled value. And the bridge function, the strongest channel, is being partially routed around by Ripple’s own RLUSD stablecoin and squeezed by the broader rise of regulated dollar stablecoins.

None of this means XRP cannot appreciate. It means XRP’s appreciation depends on conditions that are identifiable and not yet met: real adoption of the ledger’s new lending and DEX protocols, tokenized-asset issuers actively choosing XRP as a medium of exchange, and ODL volume scaling past the levels where it generates real buy pressure. The CLARITY Act and a wave of post-legislation bank partnerships could accelerate all of this, which is why the regulatory calendar matters so much to XRP specifically.

For holders, the discipline is to stop treating ledger adoption and token demand as the same thing, because they are not. The ledger is thriving and the token is waiting, and the gap between them will close only when the specific value-capture mechanisms start firing at scale. Watch the lending volumes, the RWA trading pairs, and the daily ODL figures. Those numbers, not the partnership press releases, will tell you whether the banks using the XRP Ledger ever actually start buying XRP. Until they do, the most accurate description of XRP is the one the bulls least like to hear: great infrastructure, waiting for its token to matter.

This article is for informational purposes and does not constitute financial or investment advice. Cryptocurrency markets are highly volatile. The figures and analysis described reflect data available as of June 5, 2026. Always do your own research and consult with qualified financial professionals before making investment decisions.

In such times of distress where all crypto assets head south, including the largest altcoin, the retail public generally turns to more experienced and prominent names to look for support.

In an interesting development, though, one of the key crypto figures with a long connection to Ethereum, ConsenSys co-founder Joseph Lubin, has made a large ETH transfer after years of inactivity, which stirred the pot rather than calming the public.

Is Lubin Dumping ETH?

Lookonchain shared data showing that the transfer occurred just hours ago, in which Lubin sent out 80,001 ETH (valued at over $121 million). This wallet linked to him has been inactive for over three years, and the timing now is what raised so many questions.

Some asked why he didn’t sell at the very top last year when the asset neared $5,000 for the first time ever. Others believed retail investors might follow the example in what appears to be a capitulation event.

However, there were those who noted that Lubin simply needs to cover his leveraged trades on other platforms, such as MakerDAO. When an asset dumps as hard as ETH did in the past few days, the risk for forced closures (liquidations) skyrockets unless the trader provides more liquidity or collateral.

Is #Ethereum co-founder Joseph Lubin(@ethereumJoseph) preparing to dump $ETH?

A wallet linked to Joseph Lubin, which holds 243,300 $ETH($370M), transferred out 80,001 $ETH($121.6M) after more than 3 years of inactivity.https://t.co/s6lzxlNpRy pic.twitter.com/f0hyWvQBAm

— Lookonchain (@lookonchain) June 6, 2026

Lubin’s intentions remain unclear at the moment, but the general consensus (no pun intended) in the comments below Lookonchain’s post is that the transfer increased the overall FUD. However, there’s no confirmation that he indeed sold or plans to do so.

Will ETH Dump Toward $1K?

Speaking on the asset’s disastrous price action over the past week or so, Ali Martinez noted that ETH has hit its first bearish target at $1,560. It went even below that, and the popular analyst outlined his second, significantly more painful one, situated at just over $1,000, which would be another 50% drop from the current levels.

Rekt Capital, another popular analyst with over 550,000 followers on X, supported Martinez’s target. They noted that ETH has broken below the multi-year uptrend line and there’s a solid chance it slumps toward $1,000 in the not-so-distant future. It’s worth noting that the world’s largest altcoin hasn’t traded at such low levels since the 2022 bear market.

Ethereum has finally broken down from the multi-year uptrend line

The multi-year technical uptrend is over

Price has revisited the orange area for the first time since early 2025

If price Monthly Closes beneath orange and turns it into new resistance, there’s a good… https://t.co/0OCG5J6xGd pic.twitter.com/ek8SrG7qzk

— Rekt Capital (@rektcapital) June 5, 2026

The post Is Joseph Lubin Abandoning Ethereum as Analysts Warn of a $1K Crash? appeared first on CryptoPotato.

Bitcoin has fallen nearly 25% over the past month, yet Coinbase CEO Brian Armstrong has argued that key parts of the crypto industry continue to grow despite the downturn.

Summary

- Brian Armstrong says Bitcoin’s decline does not reflect the performance of the entire crypto industry.

- Coinbase CEO points to growth in stablecoins, derivatives, and prediction markets despite the ongoing market downturn.

- Armstrong argues U.S. crypto policy is tied to economic competition with China and global financial leadership.

According to a June 6 X post, Armstrong said many investors continue to treat Bitcoin’s performance as a proxy for the broader crypto market. He noted that perception no longer matches how the industry operates today, noting that crypto activity now extends into multiple areas of finance beyond the largest cryptocurrency.

“People still think (or feel) because Bitcoin is down crypto is down…Crypto touches every area of finance, and is much broader than Bitcoin now. It will take some time for this to sink in.”

At the time of writing, data from crypto.news showed Bitcoin (BTC) trading near $60,100 after losing roughly 17% over the previous week. The asset’s market capitalization stood around $1.22 trillion, while 24-hour trading volume climbed over 30%, indicating heightened trading activity during the selloff.

Armstrong told followers that crypto now touches many segments of financial markets and suggested that the industry has developed far beyond a single asset class. While reaffirming his support for Bitcoin, he described the cryptocurrency as one important part of a much larger ecosystem rather than the sole indicator of sector health.

“And yes – Bitcoin is going to do great and is as important as ever – one of many cycles we’ve all been through.”

Growth remains visible outside Bitcoin

Pointing to areas that continue attracting activity, Armstrong highlighted crypto derivatives, perpetual futures markets, stablecoins, and prediction platforms. According to his remarks, expansion across those segments shows that digital asset markets are becoming less dependent on Bitcoin’s price movements than in earlier years.

Recent comments from Armstrong also place crypto development within a broader economic and geopolitical context.

In a separate post reported by crypto.news, the Coinbase chief argued that competition with China could push the United States to strengthen its position in digital finance.

Describing international competition as a force that encourages innovation, Armstrong said U.S. policymakers should view crypto legislation as part of the country’s economic rivalry with Beijing. He argued that years of market leadership had contributed to complacency and suggested that renewed competition could improve American performance.

Stablecoin policy remains a key battleground

Alongside his comments on market growth, Armstrong has continued to warn that restrictive digital asset regulations could push innovation outside the United States. Over the past year, he has repeatedly argued that poorly designed rules may encourage companies and capital to move offshore.

Particular attention has been placed on stablecoin legislation currently under discussion in Washington.

According to Armstrong’s previous statements, restrictions on interest-bearing stablecoins would not eliminate investor demand for yield-producing products. Instead, he has argued that such policies could benefit foreign stablecoin issuers and central bank digital currency initiatives operating beyond U.S. regulatory oversight.

Debate over those proposals has also intensified friction between crypto companies and traditional financial institutions.

As reported by crypto.news, JPMorgan CEO Jamie Dimon recently criticized Armstrong in unusually direct terms during the ongoing dispute over crypto regulation and market structure legislation.

Responding to criticism from the banking sector, Armstrong has accused large financial institutions of seeking regulatory advantages rather than competing through better products. His position has remained consistent as lawmakers consider frameworks that could define how digital assets, stablecoins, and related financial services operate within the United States.

While Bitcoin’s recent decline has drawn most investor attention, Armstrong’s latest comments suggest he believes the industry’s long-term trajectory will be shaped just as much by adoption of stablecoins, derivatives, and other crypto-based financial services as by the price of BTC itself.

Illinois lawmakers advanced a $56 billion state budget that embeds a Digital Asset Privilege Tax Act amendment, setting up a 0.2% tax on crypto transactions conducted by a “digital asset broker” within the state. The provision, tucked into Senate Bill 3019 as part of the FY 2027 revenue package, would require digital asset brokers operating in Illinois to register and comply with new reporting obligations. The measure passed along party lines and now awaits Governor JB Pritzker’s signature to take effect.

The proposal comes with a serious enforcement mechanism: brokers failing to register or adhere to the new rules could face charges that qualify as a Class 3 felony, with potential prison terms of two to five years and fines up to $25,000. State officials project the tax would generate about $60 million for the next fiscal year, providing a new revenue stream for the budget package.

As of Friday morning, Pritzker had signaled his intention to sign the bill but had not yet affixed his signature. A public statement from the governor’s office indicated plans to support the measure, but the law has not become binding while awaiting the formal signing process.

Industry advocates quickly pushed back, arguing the tax and its broad registration requirements would be economically harmful and badly timed. The Digital Chamber and the Illinois Blockchain Association issued statements highlighting concerns about stakeholder engagement and noting that no other state has imposed a similar levy. They warned that the proposal could create uncertainty for businesses and investors operating in Illinois without giving adequate notice or guidance.

The policy arrives amid a broader set of regulatory actions in Illinois, including a separate move by the governor related to prediction markets. Earlier this year, Pritzker signed an executive order barring state employees from betting on event contracts on platforms such as Kalshi and Polymarket, citing conflicts of interest and access to nonpublic information as grounds for concern.

Key takeaways

- The FY 2027 budget package includes a Digital Asset Privilege Tax Act amendment that imposes a 0.2% tax on crypto transactions conducted by a “digital asset broker” in Illinois.

- Registration and reporting requirements would apply to entities operating as digital asset brokers in the state; violations could be treated as a Class 3 felony with prison terms of 2–5 years and fines up to $25,000.

- The measure is projected to raise about $60 million for Illinois’ next fiscal year, according to state estimates.

- Industry groups argue the tax is economically destructive, lacks stakeholder engagement, and would set a negative precedent since no other state has enacted a similar levy.

- The proposal follows governor-level actions on prediction-market platforms, signaling a broader trend toward tighter crypto regulation in the state.

A sweeping budget move pins a new crypto tax to the FY 2027 package

The Digital Asset Privilege Tax Act amendment is embedded in Senate Bill 3019, a lengthy revenue and tax package designed to fund Illinois’ 2027 budget. The provision specifies a 0.2% tax on transactions executed by a “digital asset broker making or effectuating the sale of the digital asset business activity.” The language suggests a broad reach, with registration and compliance requirements set to apply to entities operating in the state’s crypto market. The bill, a 1,624-page document, was approved by the General Assembly on Monday and now hinges on the governor’s signature to become law.

Crucially, the measure would not be a mere licensing fee. It would attach serious penalties to noncompliance, including making it a Class 3 felony for brokers who fail to register or follow the rules from January 1 of the fiscal year. The potential repercussions—two to five years in prison and fines up to $25,000—underscore the administration’s intent to treat digital asset activity with substantial regulatory gravity.

In the fiscal context presented by lawmakers, the tax is pitched as a revenue tool to support Illinois’ 2027 budget. The administration projects the levy could bring in roughly $60 million, a figure that would contribute to balancing the state’s finances in a year when the crypto sector remains a political touchpoint for both sides of the aisle.

The bill’s appearance in a broad budget package has sparked debate about process and timing. Advocates for the measure argue that the state needs a clearer framework for digital asset activity and that the tax aligns Illinois with other forms of capital markets regulation. Critics, however, contend that the approach is heavy-handed, lacks stakeholder input, and could chill crypto innovation within the state’s borders.

For readers tracking regulatory clarity, the bill’s text and formal references are accessible through the Illinois General Assembly’s SB3019 documents and associated summaries. The proposed framework would weave into a broader tax and revenue strategy that Illinois officials hope will create a more predictable regulatory environment for crypto operators within the state.

Industry response and policy design

The reactions from industry groups emphasize concerns over process and impact. The Digital Chamber and the Illinois Blockchain Association argued that the Digital Asset Privilege Tax Act would introduce an economically destructive regime without sufficient stakeholder engagement. They warned that the lack of precedent—no other state has adopted a similar tax—could expose Illinois to unintended consequences, including decreased innovation, compliance burdens for startups, and potential shifts in activity to more crypto-friendly states.

Beyond the tax’s existence, observers note that the policy would compel crypto firms to register and adhere to reporting conventions, potentially creating a regulatory moat around Illinois-based activity. While supporters describe the move as a necessary step toward oversight and consumer protection, opponents warn that the implementation details will determine whether the measure stifles legitimate activity or enhances market integrity.

The debate touches on broader questions about state-level crypto regulation in the United States: how to balance consumer safeguards with fostering a thriving digital asset ecosystem, and how to design taxes that are enforceable yet not punitive toward legitimate business models. As with many such proposals, the devil is in the details—especially regarding how “digital asset brokers” would be defined, how registration would work in practice, and what constitutes “business activity” under the statute.

Prediction markets and the regulatory backdrop

The Illinois tax proposal arrives alongside a programming shift from the governor on another crypto-related front. In April, Pritzker signed an executive order restricting state employees from participating in prediction-market platforms such as Kalshi and Polymarket, citing concerns about potential conflicts of interest and the risk of making bets based on nonpublic information. The administrative move reflects ongoing state-level caution around platforms that enable probabilistic markets tied to real-world events.

Taken together, these actions illustrate a multi-pronged approach to crypto governance in Illinois: a budgeting mechanism that could formalize a new tax framework for digital assets, and executive actions aimed at preventing perceived conflicts of interest within state employment. The combination signals policymakers are pursuing a stricter regulatory stance while seeking to ensure fiscal resources for the state’s budgetary needs.

What investors and operators should watch next

For market participants, the most immediate question is whether Governor Pritzker will sign the bill into law. If signed, Illinois would establish a formal, state-level tax regime and registration framework for digital asset brokers, complete with felony-level penalties for noncompliance. The enacting details—how “digital asset broker” is defined in practice, what registration entails, and how enforcement would unfold—will shape the policy’s economic impact on exchanges, brokerages, and other asset-service providers operating in Illinois.

From a strategic perspective, the proposal spotlights a broader pattern: states experimenting with crypto taxation and oversight as a means to raise revenue and establish governance standards. Investors and builders should monitor how enforcement would be phased in, whether the measure faces legal challenges, and how this risk interacts with broader regulatory trends nationwide. If enacted, Illinois could become a reference point for similar state-level approaches, influencing both market access and compliance costs for domestic crypto activity.

As the bill moves through the final sign-off stage, observers should also keep an eye on any legislative clarifications or amendments that might alter the scope of the tax or its penalties. While the stated aim is to fund the state budget, the policy’s real-world effect will hinge on how clearly regulators define terms, how burdens are allocated, and how flexible the regime remains in the face of evolving technologies and market structures.

In sum, Illinois is testing a new blueprint for crypto oversight within a state budget framework. The coming weeks will reveal whether the plan gains formal enactment, how it is calibrated for business practicality, and what impact it may have on the broader regulatory conversation across the United States.

Bitcoin reclaimed the $61,000 level in Asian morning hours Saturday after briefly dipping below $60,000 overnight, steadying after a strong U.S. jobs report on Friday triggered a sharp selloff across stocks, bonds and crypto.

The token fell as low as $59,227 before buyers stepped back in, and was trading around $61,000, down about 1.3% on the day.

The bounce came off a level traders had been watching closely. Bitcoin had been sliding toward $60,000 all week as a record run of ETF outflows and Strategy’s first bitcoin sale since 2022 removed buyers that had supported the price. The break below the round number overnight did not turn into a deeper breakdown, with the token recovering more than $1,500 off the low.

The selloff that drove the dip started outside crypto. Friday’s nonfarm payrolls report came in solid, and rather than cheering the strength, markets repriced the Federal Reserve outlook hard. Swaps now fully price a rate increase by the end of 2026, a reversal from the cuts expected under newly confirmed chair Kevin Warsh. Two-year Treasury yields jumped 12 basis points to 4.16%, the dollar rose, and risk assets fell.

The damage was worst in the AI trade. The Nasdaq 100 sank about 5%, its steepest drop since April 2025, and a gauge of chipmakers tumbled 10%. The S&P 500 fell 2.6% and failed to complete a tenth straight weekly gain.

Other tokens remain deep in the red on the week. Ether is down 21.6% over seven days to around $1,575, solana down 23.7% to $63, and XRP, dogecoin and BNB all between 13% and 20% lower. Hyperliquid’s HYPE, which outperformed through most of the recent bleed, is down 9.9% over the same stretch.

The leverage washout was heavy. Around $1.60 billion in positions were liquidated over 24 hours across roughly 308,000 traders, according to CoinGlass, with longs accounting for $1.21 billion. Bitcoin saw $534 million in liquidations and ether $423 million, while Zcash, in the middle of its own 44% collapse tied to a disclosed bug in its Orchard privacy pool, logged another $115 million.

With $60,000 pierced overnight but quickly reclaimed, the question is whether bitcoin can build on the bounce or whether the level gives way on a retest. A clean break below it would put the token back into territory it last traded during the February drawdown.

Bitcoin’s recent crash began with a violent rejection at $82,000 that drove it south to $59,000 on Friday, which became its lowest price tag since before the US presidential elections in November 2024.

Following such a painful decline, the asset has dropped into a critical zone where long-term indicators and historical patterns begin to converge. Perhaps that’s why many analysts have started to debate whether the bottom is just around the corner or another leg down could be in the making.

The Rainbow Chart

Popular analyst Crypto Rover noted recently that BTC had declined below the ‘rainbow chart’ (seen in the embedded video below), which was just the second such occurrence in its recent history. The reason for this long-term valuation model’s rarity is that it comes during extreme market conditions.

The last time it happened, BTC dumped toward $15,000 during the 2022 bear market. For many long-term bitcoin holders, it signals that the cryptocurrency is entering deeply undervalued territory; hence, it could be close to the bottom. For now, though, the asset remains firmly below it even after managing to rebound from the $59,000 low.

$BTC just fell below the rainbow chart.

Historically, this has happened 2 times.

• 2022: $15,500

• 2026: $63,000Most Bitcoin OG’s remember this. pic.twitter.com/SkOQrIDXBT

— Crypto Rover (@cryptorover) June 5, 2026

Another key level now in focus is the 200-week exponential moving average (EMA), which was brought up by fellow analyst CRYPTOWZRD. They noted that it has historically served as a reliable support during bear markets, and in most previous cycles BTC has bottomed either at or very close to it.

Bitcoin is currently testing it, and if it manages to hold above it and reclaim momentum, it could strengthen the case for a bottom forming in the low-$60,000 range. A clean breakdown, though, would likely open the door for deeper losses and extend the correction phase.

Maybe Not Complete?

Rekt Capital compared the current bear phase to the 2022 landscape and concluded that there’s a major discrepancy in the divergences from the previous all-time highs. In 2022, BTC deviated 22% below its 2017 all-time high, while it has not gone just 12% under the 2021 all-time high.

“Bitcoin is getting close to a bottom but it’s not there quite yet and there’s still time left,” the analyst concluded.

For now, the main signals remain mixed as long-term valuation models and key technical levels suggest BTC is getting close to a bottom, but it’s not necessarily there yet. As volatility remains elevated, the market seems to be entering a ‘make-or-break’ phase that could define the next major trend.

The post Bitcoin Nearing a Bottom? Key Indicators Flash Mixed Signals After $59K Drop appeared first on CryptoPotato.

Greece has prepared plans for a 15% cryptocurrency capital gains tax as officials move to bring digital assets into the country’s tax system.

Summary

- Greece is preparing legislation to impose a 15% capital gains tax on cryptocurrency profits, with the first €500 in gains exempt.

- Officials revealed the proposal would formally bring crypto assets into Greece’s tax code, with a bill expected to reach parliament in the coming months.

- The move comes as other jurisdictions, including Israel and Illinois, pursue different strategies to increase crypto tax compliance and revenue collection.

According to a report, Greece’s Finance Ministry is drafting legislation that would impose a 15% tax on profits from cryptocurrency investments, filling a gap in a tax framework that currently lacks dedicated rules for digital assets.

Two government officials familiar with the matter disclosed that the proposal is expected to reach parliament in the coming months. One senior official said the legislation would formally incorporate cryptocurrencies into Greece’s tax code, creating a clearer set of rules for investors and tax authorities.

Under the proposal, the first €500 ($580) in crypto gains would be exempt from taxation. A second official said that the measure would apply to capital gains from cryptocurrency investments but would not cover individuals mining digital assets.

Mining activities conducted through registered companies, however, would remain subject to taxation.

The move places Greece among a growing number of jurisdictions seeking to capture revenue from digital asset activity. Crypto taxation across Europe varies significantly, ranging from about 8% in Cyprus to as much as 30% in France, with most countries taxing capital gains rather than individual transactions.

Governments are expanding crypto tax oversight

Alongside Greece’s proposal, authorities in several countries have recently intensified efforts to improve crypto tax compliance.

Earlier this week, crypto.news reported that the Israel Tax Authority received far fewer disclosures than expected under a voluntary crypto tax reporting program launched in August 2025. As per the report, the authority had hoped to recover up to $1 billion in tax revenue from undeclared cryptocurrency profits but has so far received disclosures covering only about $50 million in crypto assets.

58 taxpayers had used the program, which allows eligible crypto holders to avoid criminal prosecution if they correct past filings and pay outstanding taxes. Taxpayers must complete disclosures and settle liabilities before Aug. 31, 2026, while eligibility is limited to investors whose crypto holdings did not exceed roughly $522,000 as of December 2024.

Back in Greece, officials said that estimating the size of the domestic crypto market remains difficult because many investors use trading platforms located outside the country. As a result, authorities have not yet produced revenue forecasts tied to the proposed tax.

Transaction taxes are also gaining attention

Elsewhere, lawmakers in Illinois have advanced a different approach to taxing digital assets.

According to a fiscal year 2027 budget bill approved by the Illinois General Assembly, the state plans to introduce a 0.2% tax on cryptocurrency transactions facilitated by digital asset brokers. State budget documents estimate the measure could generate approximately $60 million in revenue annually.

Crypto.news previously reported that the proposal, known as the Digital Asset Privilege Tax Act, would require digital asset brokers to register with the state before conducting covered transactions.

The legislation also includes criminal penalties for non-compliance, with unregistered operations potentially facing Class 3 felony charges after Jan. 1.

Industry opposition has already emerged. In a joint letter, the Digital Chamber and the Illinois Blockchain Association argued that the proposal could damage the state’s digital asset sector and noted that no other U.S. state currently imposes a comparable crypto transaction tax.

Against that backdrop, Greece’s proposal adds another example of governments seeking formal mechanisms to tax cryptocurrency activity, even as officials continue to grapple with the challenges of tracking profits generated across global trading platforms.

The Cardano (ADA) price has fallen about 35% in under a month, and founder Charles Hoskinson now admits he is powerless to stop the ecosystem’s decline.

That confession, made after another major project announced its shutdown, has revived a blunt question. Is Cardano dead for good, or is this just a brutal cycle low in the making?

A Shrinking Ecosystem Behind Hoskinson’s Warning

The bear case starts with Hoskinson himself. Reacting to the shutdown of analytics platform Tap Tools, he warned of a wave of failures and said he is tired of “managing a decline.”

The data backs the warning. Cardano TVL, the total value locked in its DeFi apps, has collapsed from about $905 million in late 2024 to just $139.77 million. That’s an 85% dip.

Trading has drained too. Weekly Cardano DEX volume has fallen from a peak near 19 million ADA in late 2025 to about 1.9 million, close to the year’s lowest week.

Network use is fading in step. Daily active addresses have slipped from a late-2025 peak near 17,600 to about 14,900, while token (ADA) trading volume has nose-dived.

This reveals low network usage and also low reception for ADA, in a crypto market where trading (riding the volatility) has been a trend lately.

Hoskinson even floated a nuclear option, launching a new Cardano with a proof-of-burn to leave hostile holders behind. He insists the technology is sound, with the Leios upgrade due at year’s end, and blames economics and governance instead.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

The question is whether any Cardano project is still growing against the tide.

Top Protocols Bleed, With One Exception

Most of Cardano’s biggest apps are sliding with the chain. Minswap, its largest decentralized exchange, lost about 11% of its locked value over the month. That is evident in the Dune data from earlier, which suggests a dip in DEX trading volume.

Indigo, a protocol for minting synthetic assets, fell roughly 19%. Djed, Cardano’s stablecoin, dropped about 21%.

Even SoSoValue, the multi-chain data and ETF-tracking platform, saw its Cardano footprint shrink about 19%. The weakness reaches beyond native projects.

One name bucks the trend. Surf Lending, a lending protocol, grew its locked value by about 98% over the month and 14% in a week. That is the lone green entry in the top 10 and the closest thing to hope on the fundamental side. Yet Surf Lending holds only about $4.62 million.

A single small protocol cannot reverse an ecosystem that has shed hundreds of millions. The bigger tell sits with the traders who move the most money.

Smart Money and Whales Have Stopped Believing

The positioning data is bleak. Cardano’s smart money index, which tracks how informed money trades against the crowd, has fallen to its lowest level of 2026. This happened as the price corrected by over 35% since May 10 with rising sell volume.

Leverage interest has drained too. ADA futures open interest, the total value of outstanding futures contracts, has collapsed from about $1.6 billion in September 2025 to roughly $324 million.

This aligns with the earlier drop in token trading volume data and highlights a lack of discernible sentiment for the token, either bullish or bearish.

Whales are stuck rather than confident. On Hyperliquid, nearly all large long positions sit underwater, with entries between $0.20 and $0.37, and most hold through the losses.

Even smart money, as revealed by Nansen AI, is offside. Its only profitable trade is a single short, while its long bets keep bleeding.

If the people who move the most money see no rebound yet, the chart has to make the case instead. The only silver lining is that the underwater long trades have not yet closed their positions.

It is optimism or denial, depending on how the ADA price chart shapes up.

The Cardano Price Level That Settles the Question

The chart is brief but blunt. The ADA price has traded inside a falling channel since early January. Its May 10 breakout attempt failed before the slide resumed.

ADA has dropped about 35% from that May peak near $0.29 and now sits close to $0.19. The next key support is $0.17. A break under $0.178 would expose $0.141 and even $0.094, and would hand the dead-chain narrative real weight. That level is only about 9% away.

The on-chain side offers one counter. ADA spot exchange outflows have grown to about $2.26 million, a hint that some holders are continuing to buy despite the fear.

For the bulls, a reclaim of $0.26 would push the death talk to the back seat. That case strengthens if protocols like Surf Lending grow and outflows hold.

For now, $0.17 separates a slide toward $0.09 from a recovery that silences the obituaries.

The post Is Cardano Dead After Hoskinson’s Shocking Confession? appeared first on BeInCrypto.

This article was updated with comments from Bitget CEO Gracy Chen.

Bitget has expanded the use of 15 tokenized stocks and ETFs by enabling them as margin collateral for USDT-M futures trading through its Unified Trading Account and Multi-Asset Mode.

Summary

- Bitget has enabled 15 tokenized stocks and ETFs as margin collateral for USDT M futures trading through its Unified Trading Account.

- Assets including rAAPL, rTSLA, rNVDA, rMSFT, rSPY, and rQQQ can now be used to meet margin requirements while maintaining futures positions.

- The update extends Bitget’s tokenization strategy, following the launch of its Reality platform and a growing lineup of tokenized equities, ETFs, and pre IPO trading products.

According to a press release shared with crypto.news, the update took effect on June 4 and allows traders to use selected tokenized equities and exchange-traded funds to meet margin requirements while maintaining futures positions. Newly eligible assets include rAAPL, rAMZN, rMETA, rMU, rTSLA, rGOOGL, rNVDA, rINTC, rMSFT, rASML, rAVGO, rTSM, rQQQ, rSPY, and rSNDK.

Under Bitget’s Unified Trading Account structure, users can manage spot holdings, derivatives positions, and margin obligations within a single account. The exchange said Multi-Asset Mode for USDT-M futures now allows these tokenized instruments to contribute toward collateral requirements, reducing the need to convert assets into a single settlement currency before entering futures trades.

Speaking about the rollout, Bitget CEO Gracy Chen said users increasingly want more ways to put tokenized assets to work across different trading activities as adoption of tokenized financial products grows.

“As tokenized assets continue to gain traction across global markets, users are looking for more ways to utilize their holdings across different trading activities. Adding tokenized stocks and ETFs as margin assets increases flexibility within the Unified Trading Account and supports a more seamless experience across crypto and traditional market products.”

Tokenized products gain a larger role inside Bitget’s ecosystem

The latest addition builds on Bitget’s recent push into tokenized financial products. In May, the exchange introduced Reality, a regulated tokenization platform that issues blockchain-based rTokens backed 1:1 by publicly traded U.S. stocks and ETFs held through regulated broker-dealers.

According to Bitget’s May announcement, Reality was designed to provide on-chain access to traditional financial assets while addressing issues that have historically limited tokenized markets, including liquidity constraints and the handling of dividends and corporate actions. The company said rTokens are supported by infrastructure connected to major U.S. exchanges and backed by reserve attestations conducted through accounting firm The Network Firm.

Several of the assets added as margin collateral this week originate from the Reality product suite. Rather than limiting those tokens to spot market exposure, Bitget is now allowing traders to deploy them within its derivatives framework.

During the same month, Bitget also launched SPCXUSDT, a SpaceX-linked pre-IPO perpetual contract that lets traders speculate on market expectations surrounding a potential public listing without owning SpaceX shares. The exchange also introduced IPO-linked products and expanded access to tokenized equities through multiple offerings tied to public and private markets.

Competition grows in tokenized asset markets

Beyond its exchange platform, Bitget Wallet integrated xStocks infrastructure in May, bringing access to more than 130 tokenized stocks and ETFs through a self-custodial wallet. Bitget Wallet said the move increased its tokenized real-world asset offering to more than 300 products, including equities, commodities, precious metals, and index-linked assets.

According to Bitget, its tokenized equity products have processed more than $30 billion in trading volume since 2025. The company has also stated that users can access more than 100 tokenized stocks, ETFs, commodities, foreign exchange products, and precious metals through its trading ecosystem.

Bitcoin price traded near $61,925 on June 5 as selling pressure kept BTC close to the $60,000 support zone, with ETF flows, whale deposits, and weak sentiment driving the next market test.

Summary

- Bitcoin price slipped near $61,925 as traders focused on $60,000 support after sharp weekly selling.

- ETF outflows and Strategy’s rare sale weakened confidence while AI-linked capital rotation added market pressure.

- Whale Binance deposits doubled in June, adding short-term selling risk as sentiment turned bearish fast.

Bitcoin price nears $60,000 support

Bitcoin price data from crypto.news showed BTC at $61,925, down 3.44% over 24 hours and 15.82% over seven days. The asset traded between $61,394 and $64,353 during the day, while 24-hour volume stood at $56.21 billion.

The latest move placed Bitcoin just above the $60,000 level. That round number has become the main support zone after BTC lost the $65,000 area and failed to hold earlier ranges near $70,000.

Bitcoin has now dropped sharply from last week’s levels above $74,000. The pullback also took BTC far below its October 2025 all-time high of $126,080, with crypto.news data showing a drawdown of more than 50%.

A break below $60,000 would move Bitcoin back into the zone seen during the February drawdown. If sellers keep control below that level, traders may turn to the $55,000 area as the next major support.

ETF outflows and Strategy sale weigh on sentiment

Bitcoin’s latest fall comes as ETF demand weakens. U.S. spot Bitcoin ETFs recently posted heavy outflows.

Fresh ETF data also showed a small $3.05 million daily net inflow on June 4, per SoSoValue. However, that single inflow came after 13 consecutive days of net outflows and did not erase the broader pressure. Total net assets still stood near $80.40 billion, while cumulative net inflows remained strong at $54.27 billion.

Strategy also drew market attention after disclosing its first Bitcoin sale since 2022. The company sold 32 BTC at an average price of $77,135 between May 26 and May 31, raising about $2.5 million for preferred stock distributions.

The sale was small compared with Strategy’s overall holdings. Still, traders watched it closely because Strategy had long acted as a steady corporate buyer during previous market stress.

Michael Saylor framed the weakness as part of a wider capital rotation. He said spot Bitcoin ETFs had seen about $4 billion in outflows since May 14 while capital markets funded AI infrastructure at scale. He called it “a capital rotation, not a Bitcoin impairment.”

Whales move BTC back to Binance

CryptoQuant analyst Darkfost said whale BTC deposits on Binance have accelerated during the June selloff. The analyst defined whales as entities moving more than 100 BTC, equal to over $6 million at current prices.

According to the update, Binance saw whale inflow peaks of about 8,200 BTC on June 2 and more than 6,400 BTC on June 4. The monthly average has also risen from about 1,200 BTC since mid-April to more than 2,800 BTC.

That change shows large holders are moving more coins onto exchanges. Such transfers can signal plans to sell, hedge, or manage risk during a fast market decline.

Darkfost said this behavior looked more like emotional risk management than a planned long-term move. The last time Binance whale inflows reached similar levels was during Bitcoin’s fall below $60,000 in early February.

This adds short-term selling pressure while price trades near a key level. If whale inflows stay elevated, BTC may struggle to reclaim lost support without stronger spot demand.

Sentiment flips as traders watch $55,000

Santiment data showed Bitcoin sentiment turned sharply lower after price fell from the late-May high. The firm said BTC moved from near $78,000 to about $63,800, with most of the decline happening in three days.

Social sentiment was strongly positive near the highs, then turned bearish as price broke down. Santiment said the crowd was most bullish near the top and most bearish near the lower range.

The firm also noted that sentiment is not a timing tool. Still, it said peak fear can sometimes appear near a “potential local bottom.” That wording remains cautious because price has not confirmed a reversal.

Crypto Patel also pointed to lower long-term accumulation zones. He wrote that 2026 to 2027 could become a “potential accumulation period,” with $50,000 to $40,000 acting as a possible spot buying zone if reached.

For now, Bitcoin price analysis remains tied to three levels. Bulls need to defend $60,000 and reclaim $65,000 to ease near-term pressure. Bears need a clean break below $60,000 to open the path toward $55,000 and possibly lower supports.

The next sessions may show whether the current fall is a panic-driven flush or the start of a deeper reset. ETF flows, whale exchange deposits, and Bitcoin’s reaction near $60,000 will likely guide the next move.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

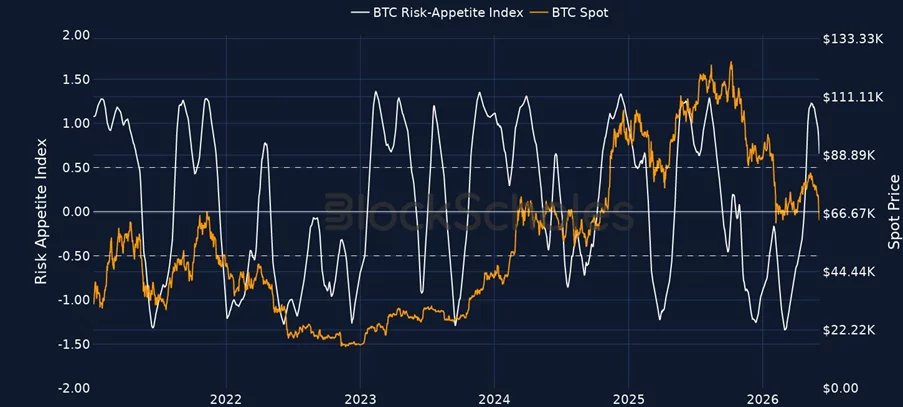

Bitcoin and Ethereum trading activity has fallen to multi-quarter lows on Hyperliquid, while volume in equity-linked and pre-IPO perpetual contracts has climbed sharply.

Summary

- Bitcoin and Ethereum perpetual futures volumes on Hyperliquid have fallen to multi-quarter lows as traders increasingly turn to equity and commodity-linked contracts, according to Block Scholes.

- Pre IPO perpetual trading volume has climbed above $50 million per day from less than $5 million, with SpaceX-linked contracts leading activity.

- Block Scholes analyst Thahbib Rahman said speculative interest remains strong in markets such as stock index perps, commodities, and HYPE despite weaker sentiment around Bitcoin and Ethereum.

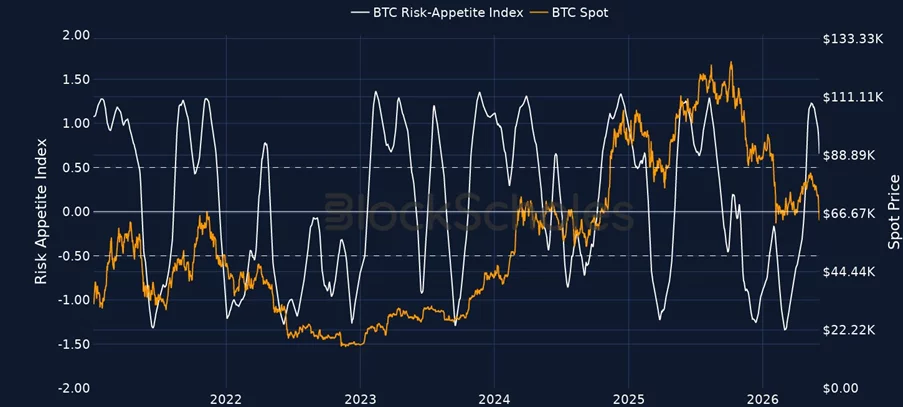

According to a June 5 report from Block Scholes shared with crypto.news, risk sentiment around the two largest cryptocurrencies has continued to weaken, even as speculative demand remains active in other parts of the market.

The research firm pointed to its in-house Bitcoin and Ethereum Risk Appetite Indexes, which have moved lower over the past week alongside declines in both assets.

Recent weakness in crypto majors has coincided with several market developments. Block Scholes noted that Strategy sold $2.5 million worth of Bitcoin from its holdings, a move that came after years of public commitment from Executive Chairman Michael Saylor to continue accumulating the asset.

The report also highlighted the longest streak of outflows from U.S. spot Bitcoin ETFs since their launch.

Rather than viewing Bitcoin’s drop toward the low $60,000 region as a sign of fading interest across the entire digital asset market, Block Scholes argued that trading activity has become concentrated in a different set of instruments.

Traders turn to stock and commodity-linked perpetuals

Data from Hyperliquid shows that daily Bitcoin perpetual futures volume has remained near $2 billion, while Ethereum volumes have stayed around $600 million to $700 million, levels Block Scholes described as multi-quarter lows.

At the same time, activity tied to equity and commodity markets has expanded rapidly on the platform. According to Block Scholes, the three most actively traded non-crypto perpetual contracts on Hyperliquid are XYZ100, which tracks the Nasdaq-100, SP500, an S&P 500-linked product, and CL, a contract tied to WTI crude oil.

Combined daily volume across those three markets has reached approximately $1.3 billion, generating $27.1 billion in notional trading volume over the past month. Block Scholes said that total equals about 112% of Ethereum perpetual volume and roughly 38% of Bitcoin perpetual volume on the exchange during the same period.

The report said the development does not necessarily represent a dollar-for-dollar migration of capital from Bitcoin and Ethereum. Instead, the report argued that trader attention and speculative activity that previously supported crypto majors are increasingly being directed toward alternative markets available through the same trading venue.

Pre-IPO contracts draw growing interest

Beyond stock index and commodity products, Block Scholes identified pre-IPO perpetual contracts as another area attracting crypto-native traders.

According to the report, the ratio of pre-IPO perpetual volume relative to Ethereum perpetual volume increased from roughly 0.1% to a peak near 3.0% in recent weeks. Daily trading volume in the segment has climbed from less than $5 million to more than $50 million, with contracts linked to SpaceX accounting for much of the increase.

Block Scholes said the rise has been abrupt and concentrated, with activity accelerating into late May and early June while Bitcoin and Ethereum volumes remained subdued.

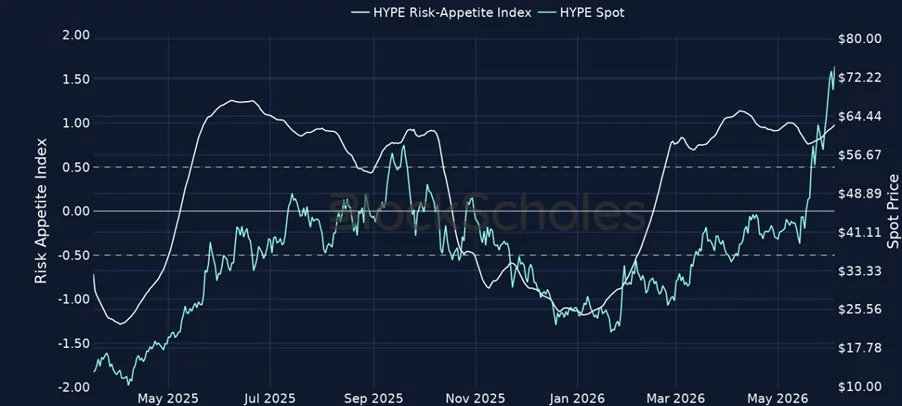

The firm’s risk appetite data also showed a divergence among digital assets. While sentiment tied to Bitcoin and Ethereum has weakened, Block Scholes reported that Hyperliquid’s HYPE token is one of the few major crypto assets where its risk appetite indicator continues to move higher.

HYPE risk appetite index. Source: block Scholes.

As previously reported by crypto.news, Binance Research recently published a report noting that capital has been flowing toward a concentrated group of U.S. equity sectors, including artificial intelligence infrastructure, semiconductor companies, defense contractors, energy firms, and commodities.

According to the report, strong performance in those sectors has historically reduced liquidity available to Bitcoin and other alternative assets.

Using the CBOE Dispersion Index as a measure of market concentration, Binance Research noted that the indicator recently reached 42, its third-highest reading on record. The firm argued that periods of concentrated equity leadership have often coincided with weakness in Bitcoin as investors direct funds toward a smaller group of high-performing themes.

I Have Taken A GLP-1. I Want To Talk About Skinny Celebrities.

Lady Phyll: ‘Pride can’t just be a party when we’re still fighting to survive’

Ariana Grande Pop-Up Merch Shop Draws Crowds in San Francisco Ahead of Bay Area Tour Kickoff

-

Business4 days ago

Business4 days agoJade Biosciences, Inc. (JBIO) Discusses Positive Interim Results From JADE101 Phase I Healthy Volunteer Study and Development Plans Transcript

-

Tech7 days ago

Tech7 days agoSpaceX just won a second Golden Dome contract. This one is $4.16 billion.

-

Sports3 days ago

Sports3 days agoFrench Open 2026 results: Alexander Zverev beats Rafael Jodar and will play Jakub Mensik in semi-finals

-

Business7 days ago

Business7 days agoIs the Spurs Phenom Already Better Than Prime Diesel?

-

Tech4 days ago

Tech4 days agoCryZENx Releases Fresh Playable Content Deep Inside Jabu-Jabu for His Ocarina of Time Remake

-

Fashion14 hours ago

Fashion14 hours agoWeekend Open Thread: Evereve – Corporette.com

-

Crypto World18 hours ago

Crypto World18 hours agoJensen Huang Approves Samsung, SK Hynix, and Micron for NVIDIA (NVDA) HBM4 Memory Supply

-

Business3 days ago

Business3 days agoTrump Taps Housing Chief Bill Pulte as Acting Intelligence Director After Gabbard Exit

-

Politics7 days ago

Politics7 days agoThe House | Inside Andy Burnham’s Makerfield Campaign: “Nobody Thinks This Is In The Bag”

-

Crypto World22 hours ago

LBank Surpasses 25 Million Users Worldwide as AFA Partnership Continues to Drive Global Growth

-

Entertainment7 days ago

Entertainment7 days agoOne of the Greatest Sitcoms of All Time Shoots Up Apple TV’s Charts 11 Years Later

-

Business7 days ago

Business7 days agoDemand Conditions Improve In Chemicals Sector In April 2026

-

NewsBeat7 days ago

NewsBeat7 days agoEverything you need to know as Cambridge’s Strawberry Fair returns after cancelled year

-

Crypto World4 days ago

Crypto World4 days agoSeagate (STX) Stock Surges to Record High on AI Boom and Legal Settlement

-

NewsBeat3 days ago

NewsBeat3 days agoRepublicans balk at Trump’s attempt to appoint a MAGA enforcer to lead National Intelligence

-

Entertainment7 days ago

Entertainment7 days agoBritney Spears Shares Troubling Update After Hard Year

-

Crypto World3 days ago

Crypto World3 days agoEU AI Data Center Project Faces Delays as Funding Gaps Grow

-

Tech7 days ago

Tech7 days agoAcer’s Swift Air 14 is a peppy MacBook Neo rival with some cool upgrades and a $699 ask

-

Business3 days ago

Business3 days agoAehr Test Systems Stock Soars 17% Amid Surging AI Demand and Conference Spotlight

-

Entertainment3 days ago

Entertainment3 days agoDid The Mandalorian And Grogu Already Ruin The Next Star Wars Movie?

You must be logged in to post a comment Login