Crypto World

‘Bitcoin to zero’ searches just hit a record. Could it happen?

Something revealing is happening on Google.

Summary

- U.S. searches for “Bitcoin to zero” reached a record as fear intensified during the market decline.

- Bitcoin reaching zero would require a fatal technical failure, total abandonment, or an effective worldwide ban.

- Its distributed ownership, mining infrastructure, ETFs, corporate holdings, and liquidity make complete abandonment highly improbable.

- Record fear searches are a sentiment signal and have historically appeared closer to bottoms than market tops.

Searches for the phrase “Bitcoin to zero” have surged to the highest level ever recorded in the United States, hitting a peak score of 100 on Google Trends, stronger than the panic spikes of the 2022 collapse and the 2025 drawdowns.

The query is a window into the crypto market’s collective psychology in mid-2026: with Bitcoin down sharply from its highs, the Fear and Greed Index buried in extreme fear, and the longest Bitcoin ETF outflow streak on record, a growing number of people are typing the most existential question a holder can ask into a search bar.

Could Bitcoin actually go to zero?

It is a fair question, and it deserves a serious answer instead of either reflexive dismissal or doom-mongering.

The honest response requires separating what would truly have to happen for Bitcoin to reach zero from the panic that drives people to search for it, and understanding why the record-breaking fear in the search data is, historically, more likely a contrarian signal than a prophecy.

This piece takes the question seriously, walks through the actual scenarios that could send Bitcoin to zero and why each is improbable, and explains what the search surge really tells us.

What the search data is actually showing

Start with the signal itself, because the “Bitcoin to zero” search spike is remarkable and worth understanding before judging what it means.

According to Google Trends data, U.S. searches for “Bitcoin to zero” climbed to a peak score of 100, the maximum on Google’s relative scale, marking the highest level on record.

This is not a modest uptick.

The phrase has spiked during previous market drawdowns, including the 2022 bear market and briefly in 2025, but the current surge is stronger than those previous peaks.

That means more people are searching for Bitcoin’s potential demise now than at any point in its history, including during the FTX collapse.

For most of 2023 and early 2024, interest in the phrase remained muted, reflecting calmer markets.

The sudden record-breaking rise reflects acute retail anxiety as Bitcoin consolidates after a sharp decline.

The context explains the fear.

Bitcoin has fallen substantially from its cycle high, the Fear and Greed Index has registered readings deep in extreme fear, U.S. spot Bitcoin ETFs bled through a record 13-day outflow streak draining billions, and the broader market shed hundreds of billions in a matter of days.

For a retail investor watching their portfolio collapse amid a relentlessly negative news cycle, “Is this going to zero?” is the natural question, and the search data captures millions of people asking it simultaneously.

The spike is a direct readout of peak retail fear, the moment when the emotional bottom feels closest.

Here is the first and most important thing to understand about that signal: peak-fear searches have historically clustered near market bottoms, not before further collapses.

The same behavioral pattern that drives the Fear and Greed Index applies to search behavior.

People search “Bitcoin to zero” when they are most afraid, and they are most afraid after prices have already fallen hard, which is precisely when much of the selling has already occurred.

The record-breaking nature of the current search spike, stronger than 2022 or 2025, is therefore as easily read as a sign of capitulation-level fear as a warning of imminent doom.

The intensity of the “Bitcoin to zero” searches is, paradoxically, one of the better contrarian arguments that Bitcoin is not going to zero.

But to make that case properly, the scenarios must be examined.

What would have to happen for Bitcoin to reach zero

To answer the question seriously, it is necessary to ask what “Bitcoin to zero” would actually require, because zero is a specific and extreme outcome, not just a big further decline.

For Bitcoin to reach zero, it would need to become genuinely worthless, held by no one, used by no one, and valued by no one.

Walking through the scenarios that could produce that outcome reveals how high the bar is.

The first scenario is a fatal technical failure.

Bitcoin could, in theory, go to zero if its underlying technology catastrophically and irreparably broke: a flaw that allowed the supply to be counterfeited at will, a break in its cryptography, or a failure of its consensus mechanism so severe that the ledger could no longer be trusted.

This is the scenario that the Zcash Orchard bug recently made vivid for a privacy coin.

But for Bitcoin specifically, it is extraordinarily unlikely.

Bitcoin’s core cryptography and consensus have operated without a successful protocol-level breach for more than 15 years, securing trillions of dollars in value through relentless adversarial testing.

The cryptography securing it—SHA-256 hashing and elliptic-curve signatures—is the same battle-tested cryptography underpinning much of the global financial and security infrastructure.

Even the quantum-computing threat, the most discussed long-term technical risk, is years away and is being actively addressed through proposals like BIP-360.

A sudden fatal technical break is the clearest path to zero and also among the least probable.

The second scenario is total network abandonment.

Bitcoin could go to zero if everyone simply stopped using it—if miners stopped securing it, developers stopped maintaining it, exchanges stopped listing it, and holders stopped holding it—all at once.

But this contradicts everything observable about Bitcoin’s current state.

The network is secured by an enormous, globally distributed mining industry with billions of dollars invested in hardware and energy infrastructure.

It is held by tens of millions of individuals, public companies with Bitcoin on their balance sheets, spot ETFs holding tens of billions in assets, institutions, and governments exploring strategic reserves.

For Bitcoin to reach zero through abandonment, all these committed, heavily invested participants would have to abandon it simultaneously.

That is not how a deeply entrenched, widely held asset behaves.

The infrastructure and ownership are far too distributed and committed for coordinated total abandonment.

The third scenario is a global regulatory ban so complete that it extinguishes all use.

A coordinated worldwide prohibition, with every major government banning ownership, trading, and mining simultaneously and enforcing it effectively, could theoretically strangle Bitcoin.

But this scenario has only grown less plausible over time, not more.

The trend in 2026 is the opposite of a global ban: the United States is exploring a strategic Bitcoin reserve, spot ETFs have been approved across major markets, regulatory frameworks such as the CLARITY Act are advancing to legitimize rather than prohibit crypto, and Bitcoin is being woven into mainstream finance through mortgage recognition and institutional products.

A coordinated global ban would require the world’s governments, many of which now hold Bitcoin through seizures or are developing favorable regulatory systems, to reverse course in perfect unison.

That is geopolitically implausible.

Even authoritarian bans have historically pushed Bitcoin activity underground rather than extinguishing it.

Why each path to zero is improbable

Having laid out the scenarios, it is worth being explicit about why, in combination, they make zero a genuine tail risk rather than a realistic forecast.

The reasoning matters more than the conclusion.

The deepest reason is that Bitcoin has crossed a threshold of entrenchment that makes total worthlessness extraordinarily difficult to achieve.

An asset goes to zero when it has no holders, users, infrastructure, or believers—the state of a failed startup token or collapsed scheme.

Bitcoin is the opposite.

It has the deepest liquidity in crypto, distributed ownership, the largest and most committed mining base, regulated financial products built on top of it, corporate and potentially sovereign treasuries holding it, and a track record spanning more than 15 years.

Each of these is a structural anchor against zero, and they reinforce one another.

The ETFs need the asset to exist. Miners are financially committed to securing it. Corporate holders have staked their balance sheets on it. Governments holding seized coins have an interest in its value.

Zero would require all these anchors to fail together.

They are held by different parties with different incentives in different jurisdictions, making coordinated total failure close to impossible.

The historical record reinforces the point.

Bitcoin has been declared dead hundreds of times throughout its history and has survived the 2018 bear market that took it down roughly 84%, the 2022 collapse that took it down 77% amid the Terra and FTX failures, and numerous smaller crashes.

Each decline generated its own “Bitcoin to zero” fears.

In every case, the asset recovered and later reached new highs, not because recovery is guaranteed, but because the structural anchors held and capitulation eventually exhausted itself.

The current drawdown, severe as it feels, is so far shallower than the 2018 and 2022 declines that preceded recoveries.

A holder searching “Bitcoin to zero” today is doing what holders did at every previous bottom, and at every previous bottom the asset did not go to zero.

None of this means zero is impossible, and intellectual honesty requires acknowledging that.

An authentically catastrophic, unprecedented technical break or an unforeseeable coordinated global collapse cannot be ruled out with absolute certainty.

Anyone claiming Bitcoin can never, under any circumstances, go to zero is overstating the case.

But “cannot be ruled out with absolute certainty” is a very different claim from “is a realistic outcome to plan around.”

Zero is a genuine tail risk—the kind of low-probability, high-impact scenario that belongs in a serious risk assessment—not the base case the record-breaking search spike might suggest.

The honest framing is that Bitcoin going to zero is improbable to the point that it should inform position sizing and risk management more than panic selling.

That is the opposite of what the search surge suggests people are doing.

What actually does go to zero

A useful way to calibrate the Bitcoin-to-zero question is to examine the kinds of crypto assets that have actually gone to zero.

Plenty have, and the contrast with Bitcoin is instructive.

Crypto is littered with assets that went to zero or close to it, and they share characteristics Bitcoin conspicuously lacks.

Failed algorithmic stablecoins such as TerraUSD collapsed to near-zero when their mechanism broke because their value depended entirely on a confidence loop that, once shattered, had nothing underneath it.

Thousands of ICO tokens from the 2017 boom went effectively to zero when their projects failed to deliver because they were claims on promises that never materialized, with no users, revenue, or staying power.

Exchange tokens such as FTX’s FTT collapsed when the exchange behind them failed because their value was tied to a single company that turned out to be fraudulent.

Countless meme coins have gone to zero after their fleeting attention faded because attention was the only thing supporting them.

The common thread among assets that actually went to zero is that each depended on a single point of failure: a mechanism, company, promise, or wave of attention that, once removed, left nothing behind.

TerraUSD depended on its algorithm. FTT depended on FTX. ICO tokens depended on teams delivering. Meme coins depended on hype.

When the single supporting pillar collapsed, the asset had no other foundation.

It went to zero because there was nothing else holding it up.

This is what going to zero actually looks like: the removal of the one thing an asset depended on.

Bitcoin is structurally the opposite, which is why the contrast matters.

It does not depend on a single mechanism that can break, one company that can fail, one team that can fail to deliver, or one wave of attention that can fade.

It is supported by a distributed mining industry, ownership across tens of millions of holders, regulated financial products, corporate and potentially sovereign treasuries, a track record spanning more than 15 years, and the deepest liquidity in crypto.

Each is an independent pillar held by different parties with different incentives.

For Bitcoin to go to zero, all these independent pillars would have to fail together, whereas the assets that actually went to zero each had only one pillar to lose.

The things that go to zero are single-point-of-failure assets.

Bitcoin is the most multiply redundant asset in crypto, which is precisely why the historical examples of crypto going to zero do not map onto it.

Understanding what does go to zero clarifies why Bitcoin almost certainly will not.

What the search surge really tells us

Step back from the scenarios, and the more useful question is what the record “Bitcoin to zero” search spike actually signals about the market.

The answer points in a more constructive direction than the query implies.

The search surge is, first and foremost, a sentiment indicator, and an extreme one.

It belongs in the same family as the Fear and Greed Index reading deep in extreme fear: a measure of how frightened the market is, not a measure of what is actually likely to happen.

The fact that “Bitcoin to zero” searches hit a record, stronger than in 2022 or 2025, shows that retail fear has reached an extreme rarely seen.

That is information about psychology, not Bitcoin’s fundamental prospects.

As with all extreme sentiment readings, the contrarian interpretation has historical weight.

Peak fear has tended to cluster near bottoms because, by the time the maximum number of people are searching whether their investment is going to zero, the maximum amount of capitulation selling has typically already happened.

The behavioral pattern is consistent and worth internalizing.

Search interest in Bitcoin, including fearful queries, spikes during sharp price declines, not during calm uptrends.

That means these searches are a lagging reaction to price rather than a leading predictor of it.

People do not search “Bitcoin to zero” when Bitcoin is at all-time highs.

They search it after it has already fallen hard, which is structurally close to the point of maximum pessimism.

This is why analysts read surging search interest during a sell-off as a potential sign that retail is re-engaging and capitulation may be peaking, in the same way they read extreme-fear measurements.

The record search spike is the crowd at its most afraid, and the crowd at its most afraid has historically been wrong about the direction more often than right.

There is a second, subtler signal in the surge: it indicates retail attention is returning to Bitcoin after a period of disengagement.

For much of the period when institutions and ETFs dominated the market, retail search interest faded.

The resurgence of searches, even fearful ones, suggests everyday investors are paying attention again.

Whether that attention converts into buying or selling is uncertain, but renewed retail engagement is itself a precondition for the broad participation that has historically accompanied recoveries.

The honest synthesis is that the record “Bitcoin to zero” search spike is best understood not as evidence that Bitcoin is going to zero, which the scenarios show is improbable, but as evidence that fear has reached an extreme and retail attention has returned.

That combination has historically appeared near bottoms instead of before further collapses.

The people searching the question are, in aggregate and historically, asking it close to the worst possible moment to act on the fear behind it.

How to actually think about the question

For anyone worried enough to search “Bitcoin to zero,” the constructive path is to translate fear into disciplined thinking rather than letting it drive action.

A few principles help.

The first is to right-size the risk.

Bitcoin going to zero is a real tail risk, which means it should inform how much of a portfolio is placed into Bitcoin in the first place, not whether someone panic-sells after a decline.

A risk that cannot be ruled out with certainty is a reason for prudent position sizing and holding an amount that could be lost entirely.

It is not automatically a reason to capitulate at the bottom of a drawdown.

If the possibility of zero is frightening, the lesson is about allocation discipline before the fact, not panic after it.

Selling into extreme fear because of a sudden awareness of a tail risk that existed all along is reacting to emotion, not new information.

The second principle is to recognize that the question itself is a contrarian signal.

Anyone searching “Bitcoin to zero” is, by definition, experiencing the emotional state that has historically marked bottoms rather than tops.

That does not guarantee a bottom is in.

But it should prompt reflection that the urge to sell is strongest at exactly the moments that have historically rewarded buying or holding.

The discipline is to notice that the fear is shared by a record number of people, that record-shared fear has preceded recoveries before, and that acting on it places the investor alongside the crowd that has historically been wrong at the extremes.

The clearest answer to the bottom-feared question is that Bitcoin going to zero is improbable to the point of being a tail risk rather than a forecast.

The asset has crossed a threshold of entrenchment, distributed ownership, institutional integration, and proven resilience that makes total worthlessness extraordinarily difficult to achieve.

The scenarios that could cause it—fatal technical failure, total abandonment, or a coordinated global ban—are each individually unlikely and collectively close to implausible.

The record-breaking search spike is not a prophecy of that outcome but a thermometer of extreme fear, and extreme fear has historically clustered near bottoms.

None of this is a promise that Bitcoin will recover, cannot fall further, or that zero is literally impossible.

Each of those claims would overstate the case.

The more measured truth is that the question millions are now searching reflects a moment of maximum fear, that the answer to the literal question is “almost certainly not,” and that the people asking it are, historically, asking close to the wrong time to act on that fear.

The search data is real. The fear is real.

The most likely meaning of both is not that Bitcoin is dying, but that the market is frightened, which is a very different and far more survivable condition.

This article is for informational purposes and does not constitute financial or investment advice. Cryptocurrency markets are highly volatile. The figures and analysis described reflect data available as of June 2026. Always do your own research and consult with qualified financial professionals before making investment decisions.

Crypto World

WTI Analysis: Gap Breaks Short-Term Trend as Price Remains Trapped Between the POC and Profile Boundary

WTI crude oil plunged by more than 7% on 27 July 2026 after the US suspended a series of strikes against Iran over the weekend, raising hopes of a diplomatic solution and the reopening of shipping through the Strait of Hormuz, according to CNBC. Brent crude also fell below $90 per barrel. Meanwhile, Bloomberg reported that Yemen’s Houthi movement had claimed attacks on Saudi Aramco facilities in Jizan and Yanbu, suggesting that the conflict remains far from resolved.

WTI Technical Analysis

Since the beginning of July, XTIUSD had been developing a short-term uptrend. A rebound from the $68 area on 2 July evolved into a sustained rally, supported by an ascending trendline. This trendline held until the market peaked near $94.2, but it was broken on 27 July following a sharp gap lower. Since then, the price has been attempting to move through two key levels within the current market profile: the POC at $84.7 and the lower profile boundary at $82.7. If this area fails to hold and the decline continues, the green support level at $80.5 could become increasingly important. Notably, the gap occurred on relatively modest trading volume considering the scale of the price move.

Above current levels lies the upper boundary of the market profile at $90.3, which could become the next upside target if the market reverses. Beyond that, traders will be watching the red resistance level at $94.2. The RSI + MAs indicator currently reads 36, 55 and 60, suggesting that the market remains unbalanced and is still searching for equilibrium.

Summary

The relatively low trading volume accompanying the gap suggests that the sell-off may have been driven largely by emotion, leaving room for buyers to return if the geopolitical risk premium begins to rebuild. For now, oil prices remain confined to a narrow range between the POC and the lower boundary of the market profile, where momentum for the next significant move may be building.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Pseudonymous crypto analyst NoName says that despite its recent recovery, Bitcoin (BTC) could still be weeks away from its bear market low.

According to them, an unfilled fair value gap (FVG) above the current price may be completed before a final drop toward the $39,000 to $49,000 range.

Analyst Expects Rally First, Then Final Drop

In a July 28 post on X, NoName said many traders have stopped expecting lower prices because BTC has started to recover, comparing today’s market mood with the periods leading up to the final declines in 2018.

“I saw the same thing in 2018,” the analyst wrote. “People believed in the rally right before the final drop. Sentiment was identical to what I’m seeing right now.”

According to the market watcher, Bitcoin is climbing because there’s an unfilled fair gap value above the market. An FVG is a price zone that gets skipped over during a fast move, which price often comes back to fill before continuing in the same direction.

Many traders see the current move up as the beginning of a bullish reversal, but NoName believes the rally is only part of a larger setup. The analyst expects Bitcoin to first enter and fill the gap before falling immediately, or within one to three days, into what they described as a multi-week search for a bottom between $39,000 and $49,000. Only after those conditions are met will the trader consider turning bullish.

The latest comments follow an earlier post in which the analyst noted that they sold BTC near its 2025 all-time high around $117,000 before the bear market that followed. According to them, market sentiment has changed from “pure euphoria” at the peak to “pure despair” today, and they maintain that the bear market still has “weeks left” before reaching a zone they’d prefer to buy Bitcoin in.

Price Swings Keep Traders Divided

Kalshi has currently assigned a 55% probability that the OG cryptocurrency reaches $50,000 before returning to $100,000, reflecting the continuing uncertainty about the next major move.

However, some traders like KillaXBT have argued that many investors are becoming overly focused on waiting for Bitcoin to revisit $50,000 or even $40,000, comparing today’s sentiment with 2022, when traders waited for a move to $10,000 that never came. He suggested that accumulating earlier, instead of chasing the exact bottom, has been the better strategy historically.

Bitcoin’s latest price action has done little to settle the debate, with the asset reversing and dropping to around $63,000 ahead of the US Federal Reserve’s interest rate decision just after it had reclaimed $65,000 following a lull in hostilities between the US and Iran. It is down about 3% in the last seven days per CoinGecko data, although over 30 days it has gained more than 5%, while sitting almost 50% below its all-time high of over $126,000 recorded in October 2025.

The post Bitcoin Could Drop to $39K Before Bottom, Analyst Warns appeared first on CryptoPotato.

Binance co-founder Changpeng “CZ” Zhao has endorsed the concept of “license passporting” across ASEAN, arguing that crypto and stablecoin providers that are already regulated in one country should not have to restart the licensing process when expanding into neighboring markets.

Speaking Tuesday at the “One ASEAN, One Digital Economy” fireside chat during the ASEAN Tech Summit Manila 2026, Zhao backed an approach originally raised by FinTech Alliance PH founding chair Lito Villanueva: a simplified approval pathway—or license portability—so regulators can still conduct due diligence, but without forcing applicants to complete a wholly new application from scratch in each jurisdiction.

Key takeaways

- Zhao supports regulatory passporting across ASEAN to reduce the “apply from zero” burden for already-licensed crypto and stablecoin firms.

- He framed cross-border coordination as largely a political issue, while suggesting the underlying technology and compliance architecture are manageable.

- A streamlined regional licensing model could lower compliance costs and encourage competition across fragmented ASEAN rules.

- ASEAN has precedent for simplified cross-border authorization in other parts of finance, though crypto-specific passporting does not yet exist.

- The EU’s MiCA framework provides a clearer passporting example, highlighting the contrast between region-wide rules and ASEAN’s country-by-country regulatory environment.

Why “passporting” matters for crypto in ASEAN

ASEAN countries currently regulate digital assets through separate national frameworks, which can translate into multiple licensing processes for firms trying to operate regionally. Zhao’s argument is that this patchwork discourages cross-border expansion and increases overhead—both of which can slow access to new services and leave costs higher for users.

At the same time, Zhao did not suggest regulators would be sidelined. His core position was that regulators should retain the ability to review and assess applicants, but that the administrative burden should be lighter when a firm already holds a license in another participating market.

In practical terms, that distinction could matter most for compliance-heavy business models—such as custody, exchange operations, and certain stablecoin-related activities—where duplication of documentation, legal reviews, and internal controls can become expensive and time-consuming with each new country entry.

ASEAN already uses simplified approvals in other sectors

While ASEAN does not currently have a bloc-wide “passport” specifically for crypto companies, regulators have used streamlined cross-border mechanisms in capital markets to deepen integration. One example is the ASEAN Capital Markets Forum (ACMF) framework for Collective Investment Schemes (CIS).

According to the ACMF, its Collective Investment Schemes Framework “allows” a fund authorized in its home jurisdiction to be offered in participating host jurisdictions through a streamlined authorization process. The initiative began operating in Malaysia, Singapore, and Thailand in 2014, and later expanded when the Philippines joined in 2021. The ACMF describes the Philippines’ entry as an enhancement to ASEAN capital markets connectivity. (See: ACMF CIS cross-border framework and ACMF news release on Philippines entry.)

Separately, the ACMF has also introduced the “ACMF Pass” under its Professional Mobility Framework. This arrangement enables eligible investment advisers licensed in one participating jurisdiction to receive fast-track registration to provide advisory services in another jurisdiction without obtaining another full license. The ACMF details the Professional Mobility initiative and related arrangements on its website. (See: ACMF Professional Mobility and ACMF announcement.)

Zhao’s crypto “passporting” idea is broader than these finance-specific programs, but the examples underscore a key point for investors and operators: ASEAN regulators have, in practice, found ways to use mutual recognition and simplified approvals in areas where rules differ across member states.

Europe’s MiCA shows how passporting can work in practice

A closer analogue outside ASEAN is the European Union’s Markets in Crypto-Assets Regulation (MiCA) regime, which includes passporting rights for authorized crypto-asset service providers. Under the approach described in earlier reporting, an authorized provider can offer services across EU member states after notifying its home regulator about the countries and services involved. (See: Cointelegraph’s coverage of MiCA passporting.)

Zhao’s comments suggest he sees alignment across ASEAN as more difficult than building common technical rails, partly because policy and regulatory approaches vary between countries. Still, his central claim remains: the pathway for a firm already licensed in one ASEAN market should be meaningfully easier when it enters another—provided regulators can still evaluate the application on its substance.

What changes—and what remains uncertain

If ASEAN regulators adopted a passporting or license portability model for crypto, the biggest immediate change would likely be operational: firms could focus compliance resources on meeting baseline requirements, rather than rebuilding licensing dossiers for each country. That could also affect market dynamics by making it easier for licensed operators to expand service offerings, potentially improving competition and reducing consumer-facing costs over time—an outcome Zhao explicitly tied to broader regional participation.

However, a major uncertainty remains how “lighter” the process could realistically be under current political and regulatory structures. Even within systems that use simplified approvals, host jurisdictions often still apply their own rules or requirements. In other words, passporting can reduce duplication without eliminating local oversight.

For readers watching ASEAN’s crypto landscape, the next signal to track would be whether regional bodies or individual regulators begin converging on shared standards for licensing and ongoing supervision—especially for businesses tied to stablecoins and custody/exchange services, where risk controls are central.

Zhao’s endorsement highlights that the technology for cross-border licensing mechanics is not the main barrier; coordination among regulators is. The practical question now is whether ASEAN moves from principles like mutual recognition and streamlined approvals in capital markets toward comparable frameworks for crypto—without compromising local regulatory objectives.

Psalion announced its third and largest venture fund on July 27, introducing a $50 million Singapore vehicle for pre-seed and seed-stage blockchain companies.

Summary

- Psalion launched a $50 million Fund III targeting seed-stage blockchain infrastructure, stablecoins, RWA and DeFi.

- MAS records list Fund III as restricted, limiting Singapore offers to accredited and institutional investors.

- Fund III led Beezie’s $4 million round, its first disclosed investment after the launch announcement.

The firm said Fund III will target infrastructure, middleware, trade finance, real-world assets, stablecoins, decentralised finance and selected consumer applications.

The announcement was followed one hour later by Fund III’s first publicly disclosed deal. Psalion said it led a $4 million funding round for Beezie, a commerce platform that links physical collectibles with on-chain digital twins.

Psalion Fund III targets six blockchain sectors

Psalion said the fund will back founders connecting established businesses with blockchain rails. Managing Partner Tim Enneking described the strategy as investing where web2 businesses operate on web3 infrastructure. The firm did not publish target cheque sizes, its planned number of investments or a deployment deadline.

The release called the vehicle a $50 million fund, but it did not identify limited partners, committed capital or a first-close amount. Its headline said Psalion had “closed” the fund, while the body described the event as a launch. The available documents therefore support describing $50 million as the announced fund size, rather than independently confirmed capital already deployed.

Psalion’s website says its existing venture portfolio includes projects such as Solana, Aave, Sushi, Polkadot, Arkis, Hinkal and stablecoin protocol Usual. The firm also operates digital-asset yield and lending strategies for professional investors.

Singapore records limit the fund to eligible investors

Fund III uses Singapore’s Variable Capital Company structure and is managed by Conduit Asset Management. The Monetary Authority of Singapore’s directory confirms that Conduit holds a Capital Markets Services licence for fund management.

MAS’s CISNet database lists Psalion VC Fund III VCC as a restricted scheme. That listing means MAS has been informed of an intended offer to accredited and other eligible investors. It does not authorise the fund for non-accredited retail investors and does not represent an MAS endorsement.

Singapore’s Accounting and Corporate Regulatory Authority describes a VCC as a corporate structure created for investment funds. A VCC can issue and redeem shares without shareholder approval and can operate as one fund or as an umbrella containing separate sub-funds.

Psalion said Fund III led Beezie’s $4 million round. Beezie allows users to obtain physical collectibles through a gamified system, then keep an item or sell it back under the platform’s terms. Each physical asset receives an on-chain digital twin, according to the company.

Moreover, Beezie reported more than $170 million in gross merchandise value, over $85 million in year-to-date revenue and more than 30,000 active users since January 2026. The press release presented those figures as company data and did not include audited financial statements.

The capital is intended to support inventory purchases, geographic growth and expansion across collectibles, luxury and entertainment. Psalion did not disclose its individual contribution, valuation terms or ownership stake in Beezie.

The investment fits Psalion’s stated focus on consumer products where blockchain infrastructure operates behind the interface. It also gives Fund III a disclosed portfolio company immediately after its launch.

Crypto venture capital remains selective

The fund arrives during a weaker venture environment. As previously reported, Coinbase Ventures completed 30 investments during the first half of 2026, while broader fundraising slowed and capital became concentrated among fewer investors and projects.

Psalion’s target sectors continue to attract large rounds. Pharos Network raised $44 million for institutional RWA infrastructure. Citi Ventures also invested in stablecoin payments company BVNK, although the investment amount was not disclosed.

The next updates will be further portfolio announcements, details about investor subscriptions and any revised disclosures concerning the $50 million size. Fund III must also remain within Singapore’s restricted-scheme framework while being offered there.

No public token or listed security was announced in connection with the fund. There was therefore no verified market-price reaction directly tied to the launch.

The Hong Kong Monetary Authority (HKMA) published a white paper on quantum preparedness on July 27, rating its banking sector 2.3 out of 10 and targeting full readiness by 2030.

Bitcoin (BTC) faces the same quantum threat but has no regulator to set a deadline. Its transition depends entirely on community consensus, which remains divided.

Regulators Can Mandate. Bitcoin Must Agree

The HKMA’s first Quantum Preparedness Index found the sector at an early stage. Around half of the surveyed banks have no formal post-quantum cryptography (PQC) plan. Another 32% have not started their transition at all.

Even so, the regulator can force the pace. It announced a PQC toolkit developed with the Hong Kong University of Science and Technology, along with industry workshops. The target is a full score of 10 by 2030.

“The HKMA will continue to support the banking sector’s PQC transition, with the aim of achieving full sectoral readiness (a QPI score of 10) by 2030 through practical guidance, training, and industry engagement,” the regulator noted.

Bitcoin has no equivalent mechanism. Speaking on the BeInCrypto Experts Council, Oxford quantum computing lecturer Stefano Gogioso contrasted this with Ethereum (ETH), where a foundation at least shapes a post-quantum roadmap.

“Bitcoin has a completely different governance structure in that it doesn’t have one,” he said.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The Quantum Fix Exists, but Consensus Doesn’t

Proposals do exist. Developers merged BIP-360 into Bitcoin’s proposal repository in February. BIP-360 proposes introducing a new Pay-to-Merkle-Root (P2MR) output type through a soft fork. It functions similarly to Pay-to-Taproot (P2TR) but removes the key path spend.

“For clarity, this proposal specifically mitigates the risk of long exposure attacks on outputs that support tapscript and script trees. While some other Bitcoin output types, such as P2SH, are safe against long exposure attacks, taproot is not and taproot is the only currently activated output type that supports tapscript and script trees,” the proposal reads.

Follow us on X to get the latest news as it happens

A draft proposal, BIP-361, co-authored by Casa co-founder Jameson Lopp, would phase out Bitcoin’s legacy ECDSA and Schnorr signatures and, eventually, make coins that fail to migrate difficult to access.

This raises concerns about 1.7 million BTC in early pay-to-public-key addresses, the majority of which are attributed to Satoshi Nakamoto. Still, a greater obstacle remains. Everyone has to agree on what to do next.

CryptoQuant CEO Ki Young Ju previously warned that consensus, not code, is the real bottleneck. He noted that Bitcoiners rarely unite behind changes that seem to touch the network’s founding principles.

Thus, the HKMA will measure its banks against a deadline. Bitcoin’s readiness has no scorecard, and no one is empowered to create one.

The post Hong Kong Gave Banks a 2030 Quantum Deadline: Who Gives Bitcoin One? appeared first on BeInCrypto.

Binance co-founder Changpeng “CZ” Zhao backed crypto license passporting across ASEAN on July 28 during a fireside discussion at the ASEAN Tech Summit Manila 2026.

Summary

- CZ backed simplified ASEAN crypto licensing, allowing regulated firms to avoid full repeat applications regionally.

- ASEAN currently has no bloc-wide crypto passport, leaving approvals and supervision with national regulators separately.

- Four jurisdictions already use streamlined ASEAN fund authorisations, offering a limited model for future coordination.

The session covered digital assets, stablecoins and the future of regional finance.Zhao supported a proposal raised by FinTech Alliance PH founding chair Lito Villanueva. Under the idea, a crypto company licensed in one ASEAN jurisdiction could seek simplified approval elsewhere instead of submitting another complete application.

The proposal would still allow host regulators to assess applicants and impose local conditions. It would not automatically permit a company to operate across every ASEAN market.

ASEAN crypto license passport could reduce repeat filings

Crypto companies operating across Southeast Asia currently face separate licensing processes, compliance checks and supervisory requirements. Zhao argued that recognising some work completed by another regulator could reduce duplicated filings and lower market-entry costs.

A common process could also make regional expansion easier for exchanges, custodians and stablecoin payment providers. However, Zhao’s support does not amount to an ASEAN policy decision. No regulator or ASEAN body has announced a formal crypto passporting proposal, consultation or target date.

Binance has direct experience with fragmented licensing. The exchange is seeking more approvals across Asia while working through separate national requirements. Reuters reported in July that Binance planned to expand its regional licensing footprint but had not identified all the markets involved.

ASEAN regulators have already adopted cross-border recognition arrangements for parts of traditional finance. The ASEAN Collective Investment Schemes Framework allows qualifying funds authorised in one participating jurisdiction to seek streamlined approval in another.

Malaysia, Singapore and Thailand launched the framework in 2014. The Philippines later joined through a supplemental memorandum signed by the four national securities regulators.

The ASEAN Capital Markets Forum also operates the ACMF Pass. It allows eligible investment professionals to obtain fast-track registration for advisory work in participating jurisdictions without securing another full license.

Those programmes provide a procedural model, but they do not cover crypto exchanges or stablecoin issuers. They also preserve the power of host regulators to review applicants and enforce domestic rules.

National crypto rules remain the main obstacle

ASEAN members regulate digital assets through different laws, agencies and product classifications. Requirements can involve local incorporation, capital reserves, cybersecurity, custody, disclosures and anti-money-laundering controls.

The Philippines shows how several approvals can apply to one service. Binance and BlockShoals lacked the central bank license required for certain payment and transaction activities, despite participating in a Securities and Exchange Commission sandbox.

The Philippine SEC later allowed BlockShoals to begin sandbox testing using Binance infrastructure. However, the approval did not replace separate Bangko Sentral ng Pilipinas requirements. In related coverage, the testing programme included a 90-day integration period before user onboarding could begin.

A regional passport would therefore require regulators to agree which authority acts as the home supervisor and which responsibilities remain with each host country.

Europe provides a broader crypto comparison

The European Union’s Markets in Crypto-Assets Regulation provides the clearest direct comparison. MiCA allows an authorised crypto-asset service provider to offer services across EU member states after completing the required notification process.

That system relies on a shared legal rulebook, common authorisation standards and cooperation between national regulators. ASEAN does not currently have an equivalent regional crypto law.

Notably, Binance missed the full MiCA licensing deadline and restricted some European services. The case shows that passporting reduces repeated national applications but does not remove scrutiny during the original approval process.

ASEAN’s Digital Economy Framework Agreement may create another venue for regional cooperation. Negotiations have concluded, and the agreement is undergoing legal review before an expected November 2026 signing. Official descriptions cover digital payments, data governance and cybersecurity, but no published document confirms that crypto license passporting forms part of the agreement.

Any crypto passport would still require negotiations among national regulators, common minimum standards and an information-sharing system. For now, Zhao’s proposal remains a recommendation for future regional policy rather than an approved licensing route.

Elon Musk says he plans to give away nearly his entire fortune. The pledge answers a public challenge from Nobel Prize-winning economist Daron Acemoglu.

The challenge cited a claim Musk made in a video interview. He said robots and artificial intelligence (AI) will soon make goods so abundant that money loses its meaning. Acemoglu, however, asked Musk to back that claim with real money, not just words.

Musk’s Trillion-Dollar Challenge and Shrinking Fortune

Daron Acemoglu, a Massachusetts Institute of Technology (MIT) economist who shared the 2024 Nobel Prize in Economic Sciences, posted the challenge on X on July 27. He proposed that Musk donate his roughly $1 trillion fortune to charity no later than 2036.

Acemoglu argued the pledge would demonstrate genuine confidence in Musk’s own AI predictions. It would also, he wrote, ease public worry over the political influence of billionaires and trillionaires. He further asked for an impartial body to pick the charities, all effective and non-ideological.

The post quickly drew attention. Commentator Gad Saad amplified it on X, noting Acemoglu’s Nobel credentials. Musk answered within hours.

He offered no further detail on a timeline, dollar figure, or charitable vehicle. Therefore, the scope of his pledge remains unclear.

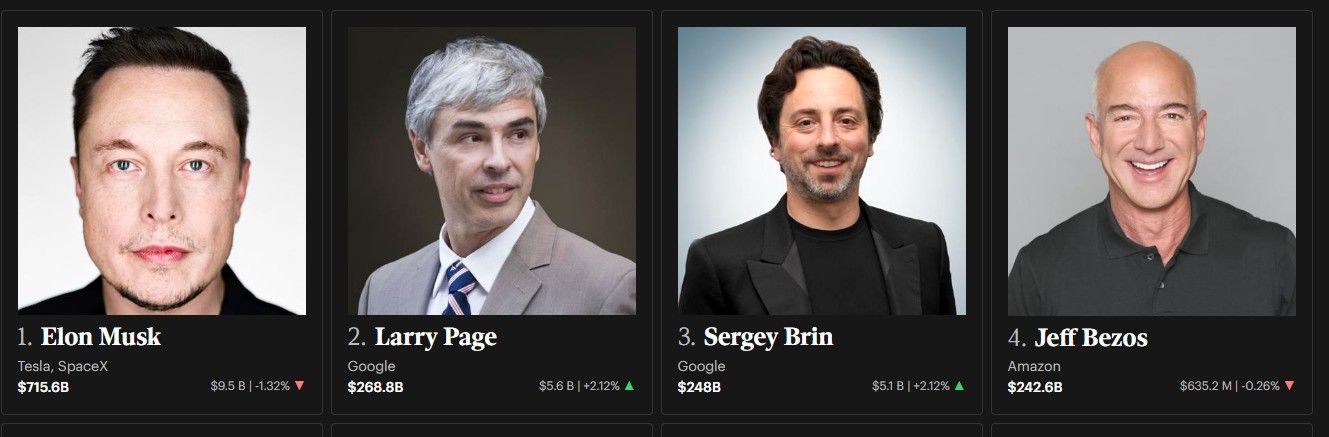

The challenge landed as Musk’s wealth kept falling. His net worth dropped to $695.7 billion on July 27, according to Forbes, after SpaceX shares slid another 4.8% to around $109.50. The stock has now fallen roughly 50% since its June 16 peak, even after a successful Starship test launch. Musk’s stake includes 4.8 billion SpaceX shares plus 350 million stock options, so each price swing moves his fortune sharply.

Forbes’ real-time billionaires tracker put his fortune at $715.6 billion on Tuesday, down 1.32%, or $9.5 billion, on the day. Google co-founders Larry Page and Sergey Brin followed at $268.8 billion and $248 billion, both up 2.12%. Amazon founder Jeff Bezos trailed at $242.6 billion, down 0.26%. All three remain well behind Musk despite his recent losses.

Musk recently called himself a former trillionaire after a SpaceX slide pushed his net worth below trillion status last month. He first crossed that threshold following SpaceX’s record Nasdaq debut in June, a milestone that fueled fresh debate over America’s widening wealth gap. Despite the recent drop, Musk still holds a commanding lead over the world’s next-richest people.

What Investors Will Watch Next

Acemoglu’s challenge adds fresh scrutiny to Musk’s AI forecasts, which he expanded on in a recent AI risk interview. Meanwhile, SpaceX shares face an August share lockup that could pressure the stock further. Some analysts still see room for a rebound, while others warn a slide below $100 would signal little investor confidence in the company’s AI ambitions.

Whether Musk formalizes his pledge remains an open question. His fortune’s next moves, and SpaceX’s, may ultimately decide the answer.

The post Elon Musk Accepts Nobel Economist’s Trillion-Dollar Charity Bet: Will He Deliver? appeared first on BeInCrypto.

Bitmine chairman Tom Lee said on CNBC on Monday that crypto is recovering because it is being embraced outside the United States. Europe, Japan, and Russia are passing CLARITY Act-like bills to regulate the industry, which has spurred market momentum, he said.

Lee believes when this happens in the US, it will supercharge the market, which will become the programmable software layer of money.

“Because crypto is turning money into software, a lot of things can turn into money,” he said. Once that happens, things like loyalty points and reputation could start behaving a lot like money – especially in the hands of AI agents, one of crypto’s killer use cases.

This is why CLARITY Act matters more than many realize https://t.co/sckumOwJxa

— Thomas (Tom) Lee (not drummer) FundstratDirect.com (@fundstrat) July 27, 2026

Key Crypto Bill Still In Limbo

BlackRock Senior Managing Director and Global Head of Market Development Samara Cohen echoed the sentiment, stating that the measure is an “important step toward establishing a regulatory framework for digital assets that puts investors first.”

She added that the bill would “help the United States shape the next era of market structure — supporting innovation while preserving the transparency, resilience and investor protections that keep the US the global leader in capital markets.”

The CLARITY Act passed the House in July 2025 with strong bipartisan support and advanced out of the Senate Banking Committee on May 14, 2026.

However, recent negotiations have centered on an ethics and conflict-of-interest section barring the president and members of Congress from issuing or sponsoring digital assets. A merged Senate text was released on July 22, incorporating ethics provisions.

Senate Majority Leader John Thune said on July 23 that he doesn’t expect the bill to reach a vote before the summer recess, with ethics remaining the main sticking point.

No floor vote is currently scheduled, so the practical deadline for 2026 passage is before the Senate’s August recess, around August 7. Missing it would likely push action into the post-midterm “lame-duck” period or into 2027.

“The procedural steps … make finishing before recess extremely difficult,” said policy relations consultant Anne Kelley.

“I know many people are disappointed it won’t clear by early August. That does not mean CLARITY is done for the year.”

Opposition Wants More Concessions

“It does sound like a lot of concessions were given, but those who oppose the bill still want to extract something else,” said Lee, who remained hopeful that “anything could happen.”

In a separate post, Lee listed some of the major financial institutions supporting the CLARITY Act, which included Goldman Sachs, BlackRock, Fidelity, Franklin Templeton, and Charles Schwab. “Congress needs to act and pass this bill,” he said.

The post BlackRock Backs CLARITY Act as Tom Lee Predicts Programmable Money Revolution appeared first on CryptoPotato.

Binance co-founder Changpeng “CZ” Zhao backed crypto license passporting across ASEAN, arguing that firms regulated in one market should be able to enter others through a simplified approval process rather than applying from scratch.

Speaking Tuesday during the “One ASEAN, One Digital Economy” fireside chat at the ASEAN Tech Summit Manila 2026, Zhao backed an idea raised by FinTech Alliance PH founding chair Lito Villanueva for regulatory passporting or license portability. Zhao said regulators could still review applicants but should not require them to complete another full licensing application from scratch.

A regional licensing framework could reduce compliance costs, encourage competition and make it easier for crypto and stablecoin services to operate across ASEAN’s fragmented regulatory markets. Member states regulate digital assets separately, creating multiple approval processes for companies seeking a regional presence.

“I think that’s mostly a political problem,” Zhao said of cross-border coordination, adding that the technology was simple. He said allowing more licensed platforms to compete could improve services and lower costs for consumers.

Binance co-founder Changpeng Zhao (left) with FinTech Alliance PH founding chair Lito Villanueva (right) at the ASEAN Summit in Manila. Source: Aubrey Paller

ASEAN has precedents for regional passporting

ASEAN does not currently have a bloc-wide passport for crypto companies, but regional regulators have created streamlined cross-border arrangements elsewhere in finance.

The ASEAN Capital Markets Forum’s (ACMF) operates the Collective Investment Schemes Framework, which allows a fund authorized in its home jurisdiction to be offered in participating host jurisdictions through a streamlined authorization process. The framework was first operationalized in Malaysia, Singapore and Thailand in 2014, while the Philippines joined in 2021, according to the ACMF.

The forum also introduced the ACMF Pass under its Professional Mobility Framework. The arrangement lets eligible investment advisers licensed in one participating jurisdiction receive fast-track registration to provide advisory services in another without obtaining another license.

Related: Philippine bank BPI plans stablecoin payments pilot

These programs are narrower than the passporting idea Villanueva raised and Zhao supported, and remain subject to host-market requirements, but they show that ASEAN regulators have previously used mutual recognition and simplified approvals to deepen integration.

A direct crypto comparison exists in the European Union. Under the Markets in Crypto-Assets Regulation, an authorized crypto-asset service provider can use passporting rights to provide services across EU member states after notifying its home regulator of the countries and services involved.

Zhao said differences in national policies and regulatory approaches make alignment harder than building common technical rails. Still, he argued that firms already licensed in one market should face a lighter application process when entering another ASEAN jurisdiction.

Magazine: Inside the ‘fake police raid’ that forced a $1M Bitcoin transfer

A US exchange can list a new prediction market by filing a form saying the contract complies with the law, and start trading the next day. No approval required.

Summary

- Prediction market prices are well calibrated overall: studies of thousands of settled markets find outcomes occurring at close to their implied frequencies, with accuracy that beats individual experts and polls.

- The best-documented distortion is the favorite-longshot bias: cheap contracts win less often than their prices imply and expensive contracts win slightly more, so buyers of long shots earn systematically negative returns.

- Capital lock-up is the least discussed distortion: a contract paying $1 in six months is worth less than its probability today because the money is committed and earning nothing, which pushes long-dated prices below fair value.

- Calibration varies by domain and horizon, with political markets showing compression toward 50% at long horizons, attributed to opposing partisan bets cancelling instead of informing.

- Fees, spreads, and the maker-taker split move realized returns meaningfully on instruments priced in cents, and resolution risk sits underneath everything as the possibility that a correct forecast still fails to pay.

Behind that speed sits a trapdoor written into Dodd-Frank, three undefined words, and a rulemaking the CFTC opened this June to finally settle what they mean.

The most useful sentence ever written about prediction markets is that a contract trading at 70 cents implies a 70% probability, and the most useful next sentence is that this is an approximation with known, measurable errors. Both halves matter. The first is why journalists, analysts, and increasingly institutional data buyers treat these prices as forecasts: the mapping is real, and the empirical record supporting it is better than most critics assume. The second is why traders who read the price as literal truth lose money in patterned, predictable ways. Research covering hundreds of thousands of settled contracts across the largest venues now supports a precise account of where the mapping holds and where it bends, and the answer is not that markets are wrong but that a price is a market-clearing number produced by capital under constraints, not a probability produced by an oracle. This guide walks the evidence: the calibration record, then the five distortions, then how to read a price properly.

The mapping, and why it mostly works

Start with the good news, because it is stronger than the skeptical framing usually allows.

Calibration studies plot implied probabilities against realized frequencies: take every contract that traded at roughly 30 cents, check how often those events actually happened, and see whether the answer is close to 30%. Across large samples of settled markets, the resulting curve tracks the ideal diagonal closely. One analysis of thousands of markets on the largest regulated venue found overall accuracy above 90% across probability ranges, with the curve hugging the diagonal and no evidence of gross systematic error. Academic work examining more than 300,000 contracts reached a compatible conclusion: prices are informative, and they improve as markets approach settlement, which is exactly what an efficient information aggregator should do as uncertainty resolves.

Comparisons to alternatives are the second part of the case. Aggregated market prices have generally outperformed individual expert forecasts, single polls, and simple statistical models, because the mechanism rewards being right with money and punishes confident error, which is a stronger incentive structure than reputation. Market efficiency has also been improving as the sector grows: spreads on the leading venue compressed sharply as volume expanded, which mechanically improves price quality. For context, crypto.news has explained where the liquid markets live and why the venue structure matters for market quality.

So the base case is that these prices deserve to be taken seriously as probability estimates. The rest of this guide is about the five ways they deviate, each of which is measurable and each of which points the same direction: the deviations mostly hurt the participant who reads the price naively.

Distortion one: the favorite-longshot bias

The best-documented bias in the literature, imported from a century of horse-race betting research, is that markets overprice unlikely outcomes and underprice likely ones.

The evidence in prediction markets is now substantial. Studies of large Kalshi samples find that low-priced contracts win far less often than needed to break even, while high-priced contracts win slightly more often and deliver small positive returns. One analysis found that events priced above 80% occurred about 84% of the time, several points below what their prices implied, meaning even the favorites side of the bias produces a modest shortfall against expectations at that end of the range. The pattern shows up across politics, entertainment, and economic data releases, and across trade sizes and volumes, which argues against it being an artifact of one market type.

The explanations are behavioral and structural in combination: people systematically overestimate small probabilities, a finding that predates prediction markets by decades; cheap contracts offer lottery-like payoff profiles that attract optimistic buyers; and limited arbitrage capital means the mispricing is not fully competed away. For a participant, the practical implication is uncomfortable and simple: buying long shots at five or ten cents is, on the historical record, a systematically losing strategy, and the sellers of those contracts have been the ones collecting.

Distortion two: capital lock-up

The most underappreciated distortion has nothing to do with psychology. It is arithmetic about time.

Buying a contract at 70 cents commits 70 cents until settlement, earning nothing in the meantime. If settlement is a week away, the cost of that commitment is negligible. If settlement is a year away, the buyer has forgone a year of risk-free return on the capital, which at prevailing rates is a meaningful percentage of the stake. Rational participants therefore pay less than the true probability for long-dated contracts, and recent work formalizes this as settlement discounting: in collateralized markets where capital sits locked until resolution, the price-as-probability mapping is incomplete, because these venues are information aggregators embedded in capital markets, not frictionless probability oracles.

The practical consequences run in two directions. For a reader treating the price as a forecast, long-dated contracts systematically understate the true probability, and the effect compounds with the horizon. For a trader, the discount is not an anomaly to exploit but the market correctly pricing the cost of committed capital, which means an apparent edge on a distant contract may be entirely consumed by the opportunity cost of getting there. Any comparison between a prediction market price and a poll or model output should account for this, and almost none do.

Distortion three: liquidity and domain

Calibration is not uniform across markets, and the variation is systematic enough to have been decomposed.

Volume concentrates heavily: political and macroeconomic contracts have accounted for a majority of trading on the largest venues, which means those markets have the tight spreads, the professional participation, and the price quality that the calibration studies mostly measure. Thin markets on obscure questions inherit none of that, and a 40-cent price in a book with a fifteen-cent spread carries far less information than the same number on a Fed decision.

Domain matters beyond liquidity. Research examining calibration across knowledge domains, horizons, and trade sizes found that a handful of components accounted for the large majority of variation, with political markets showing pronounced underconfidence: prices compressed toward 50%, understating the probability of favored outcomes, at nearly every horizon and most strongly among the largest traders. The proposed mechanism is bilateral cancellation, in which opposing partisan bets pull prices toward the middle without adding information, and the same pattern replicated on a structurally different venue, which strengthens the finding.

There is also a category where calibration is close to meaningless: questions with no historical base rate. A market on whether an unprecedented technological milestone occurs by a distant date has nothing to anchor to, and its price reflects sentiment among a small self-selected group. Those markets are entertainment dressed as forecasting, and they should be read accordingly.

Distortion four: fees, spreads, and who you trade as

On instruments priced in cents, transaction costs are not a rounding error, and the research shows they fall unevenly.

Analyses of the maker and taker split find that participants providing liquidity earn better returns than those taking it, for two compounding reasons: makers obtain better prices by definition, and takers generally pay the fees. Layer the favorite-longshot bias on top and the worst realized outcomes concentrate among takers buying cheap contracts, which is also the most intuitive behaviour for a new participant. The gap is measurable in the return data across price deciles.

The spread deserves separate attention because it is the cost most often ignored. A two-cent spread on a 65-cent contract consumes roughly 3% of the position immediately on a round trip, which against an expected edge of a few percentage points can erase the trade’s entire rationale. Spread quality has improved substantially with volume, but it varies enormously by market, and checking it before sizing is the single highest-return habit available.

Distortion five: resolution risk

The last distortion is the one that turns a correct forecast into a loss, and it is structural, not statistical.

A contract pays according to its stated resolution criteria as adjudicated by its named source or process, and that adjudication can diverge from what an ordinary observer concludes happened. On regulated venues the source is typically a designated authority, which makes disputes rare but not impossible where wording is ambiguous. On blockchain-based venues, settlement runs through decentralized oracle processes with proposal, challenge, and token-holder voting stages that this publication examines in detail, and there the divergence risk is materially higher and has produced real disputed payouts. That is the risk underneath every price.

The correct way to hold this is as a haircut on every price. A contract at 90 cents is not a 90% chance of being paid; it is a roughly 90% chance the event occurs multiplied by the probability that the resolution process pays it as expected. In liquid markets with objective single-source criteria, that second factor is close to one. In ambiguously worded or contentious markets, it is meaningfully lower, and it is entirely absent from the headline number.

What the calibration research cannot tell you

Before assembling the method, one honest caveat about the evidence base, because the studies cited above have limits that their headline numbers conceal.

The samples are historical and venue-specific. The largest datasets cover a regulated exchange over a period running from 2021 through 2025, an era in which prediction markets were smaller, more concentrated among sophisticated participants, and dominated by categories with clean resolution sources. Calibration measured on that population may not describe a market that has since added tens of millions of retail accounts through brokerage distribution, expanded aggressively into sports, and grown volumes by an order of magnitude. More retail participation could improve calibration by adding diverse information or worsen it by adding correlated sentiment, and the honest answer is that nobody yet knows which dominates at current scale.

Selection also shapes what gets measured. Calibration studies necessarily examine markets that resolved, which excludes contracts delisted, withdrawn, or voided, and those are disproportionately the ambiguous or contested ones where the price-to-probability mapping would have performed worst. The measured record is therefore a record of the well-behaved subset, and the true error rate including resolution failures is worse than the curves show.

Regime change is the third limit. Calibration is a property of a market’s participant mix, incentive structure, and information environment, all of which are shifting fast: new venues, new distribution, institutional data buyers, leveraged product variants, and a legislative environment that could remove entire categories. Findings proven on one configuration do not automatically survive into the next, which is why the coming election cycle is the most informative calibration test the sector has faced, and why any confident claim about accuracy should be dated.

None of this undermines the base case. It sharpens it: prediction market prices have a good measured record on a specific historical population under specific conditions, and the correct posture is to use that record as evidence while treating the current, much larger, much more retail market as an ongoing experiment whose results are not yet in.

How to read a price properly

Assemble the five and a usable method falls out.

Treat the price as a strong prior, never a fact. Adjust upward for long-dated contracts to account for the capital lock-up discount. Discount extreme prices toward the middle, since long shots are overpriced and heavy favourites are slightly overpriced too. Weight the reading by liquidity, taking prices from deep, professionally traded markets seriously and thin ones as sentiment. Read the resolution criteria and apply a haircut where the wording admits argument. And when trading rather than reading, account for fees, the spread, and whether you are making or taking, because those costs land before any edge does.

None of this argues against the instruments. The calibration record is genuinely good, better than most alternatives, and improving with volume. It argues for reading them the way a professional reads any market-implied number, an inflation breakeven or an options-implied volatility: as information produced by capital under constraints, containing real signal and predictable distortions, and worth more to the person who knows which is which.

One last practical note, aimed at the readers who consume these prices without ever trading them, which is now most of the audience. Prediction market numbers increasingly appear in political commentary, market research, and media dashboards as substitutes for polls, and the substitution is usually presented without any of the qualifications above. A responsible citation of a market price does three things: it names the venue, since calibration differs by market structure and resolution architecture; it names the date and horizon, since the same question priced a year out and a week out carries different distortions; and it treats the number as one estimate among several, never the answer, because the research showing markets beat individual experts does not show them beating the combination of markets, models, and polls read together. Crypto.news has also covered who is buying these numbers as exchanges, sportsbooks, and data buyers fight over the value of market-implied probabilities.

The strongest version of the case for these instruments is that they add a real, financially disciplined signal to a forecaster’s toolkit. The weakest version, and unfortunately the most common in circulation, is that a number from a screen settles a question. The distance between those two readings is what this guide has been about, and it is entirely made of the five distortions above.

Frequently asked questions

Does a 70-cent contract mean a 70% probability?

Approximately. Calibration studies across thousands of settled markets find implied probabilities track realized frequencies closely, with overall accuracy above 90% across price ranges. The mapping is a good first approximation with documented deviations at the extremes, over long horizons, in thin markets, and after fees.

What is the favorite-longshot bias?

The tendency for cheap contracts to win less often than their prices imply and expensive ones to win slightly more. Research on large samples finds low-priced contracts deliver systematically negative returns while high-priced contracts yield small positive ones, with one analysis showing events priced above 80% occurring about 84% of the time. Buying long shots is, on the record, a losing strategy.

Why do long-dated contracts trade below their true probability?

Because capital is locked until settlement and earns nothing meanwhile. Committing money for a year to a contract paying $1 has a real opportunity cost, so rational buyers pay less than the fair probability, an effect recent research formalizes as settlement discounting. Any comparison of a long-dated market price to a poll or model should adjust for it.

Are prediction markets more accurate than polls or experts?

Generally yes, in the aggregate. Market prices have outperformed individual expert forecasts, single polls, and simple statistical models across many studies, because participants are financially rewarded for accuracy and penalized for confident error. The advantage is largest in liquid markets and smallest in thin ones with no historical base rate to anchor prices.

Which markets should be trusted least?

Thin ones, distant ones, and unprecedented ones. Wide spreads mean low information content; long horizons introduce the lock-up discount and, in political markets, documented compression toward 50%; and questions with no historical base rate, such as unprecedented technological milestones, have nothing anchoring their prices beyond the sentiment of a small self-selected group.

How much do fees and spreads matter?

Considerably, on contracts priced in cents. A two-cent spread on a 65-cent contract costs roughly 3% on a round trip, which can exceed a realistic edge. Research also finds liquidity providers earn better returns than takers, who both pay fees and receive worse prices, with the gap widest among buyers of cheap contracts.

What is resolution risk?

The possibility that a contract fails to pay as expected because of how it resolves rather than what happens in the world. Contracts settle against named sources and pre-written criteria, so ambiguity can produce outcomes that surprise participants, and on blockchain venues using decentralized oracle voting the risk is materially higher. Every price should be read with a haircut for it.

How should a careful reader use these prices?

As a strong prior rather than a fact: adjust long-dated prices upward for capital lock-up, discount extreme prices toward the middle, weight by liquidity, read the resolution criteria, and subtract transaction costs before assuming an edge. Treated that way, prediction market prices are among the most useful public forecasts available. This is educational information, not investment advice.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. Research findings cited reflect published studies of historical data and do not predict future accuracy, and trading event contracts carries risk of total loss of amounts invested. Always do your own research. Information is accurate as of July 27, 2026.

Safran SA 2026 Q2 – Results – Earnings Call Presentation (OTCMKTS:SAFRY) 2026-07-28

WTI Analysis: Gap Breaks Short-Term Trend as Price Remains Trapped Between the POC and Profile Boundary

Demi Lovato Slams TikTok Video Claiming She’s Been Cloned

![Bitcoin Is Getting Ready For A Sizeable Move! [Time To Pay Attention]](https://wordupnews.com/wp-content/uploads/2026/07/1785221163_maxresdefault-80x80.jpg)

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Brooks Brothers

-

Crypto World7 days ago

Crypto World7 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

NewsBeat7 days ago

NewsBeat7 days agoHow a former Blue Peter presenter stunned America’s Got Talent judges

-

Tech1 day ago

Tech1 day agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Business6 days ago

Business6 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Entertainment7 days ago

Entertainment7 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Crypto World5 days ago

Crypto World5 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

Politics20 hours ago

Politics20 hours agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Sports1 day ago

Sports1 day agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Sports4 days ago

Sports4 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Fashion4 days ago

Fashion4 days ago16 Dresses for the High Summer Event

-

News Videos5 days ago

News Videos5 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Politics2 days ago

Politics2 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

Entertainment4 days ago

Entertainment4 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

News Videos1 day ago

News Videos1 day agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Crypto World2 days ago

Crypto World2 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Crypto World5 days ago

Crypto World5 days agoUniswap (UNI) pushes deeper into tokenized RWAs with permissioned trading pools

-

Crypto World6 days ago

Crypto World6 days agoSablier Labs Enters Maintenance Mode, Halts Development

-

Tech3 days ago

Tech3 days agoAnthropic launches Claude Opus 5, a cheaper AI model for coding, agents and enterprise workflows

-

Entertainment2 days ago

Entertainment2 days agoSara Gilson Killed By Husband After Viral “Pedophile” TikTok Video

You must be logged in to post a comment Login