Whether you’re interested in background music for your next party or you’re looking to upgrade a stereo system, there’s a speaker set ready for you. Speakers tend to be designed with a specific purpose in mind. For example, you might need speakers for your TV, computer speakers or a set for a specific room. Or perhaps you need portable Bluetooth speakers to take on a trip. There’s a speaker for every situation.

BLUETOOTH SPEAKER DEALS OF THE WEEK

Deals are selected by the CNET Group commerce team, and may be unrelated to this article.

Advertisement

Not all speakers are created equal

I’ve highlighted the best wired and wireless speakers I’ve tested costing between $50 and $1,000. While most of the included systems are powered speakers, you’ll also find passive bookshelf speakers, such as the Elac Debut 2.0 B6.2, which just need to be paired with a great AV receiver.

From smart speakers to outdoor speakers to immersive home theater systems, every model I’ve chosen boasts great sound quality and is the best speaker in its particular category. I’ll update this list periodically as we review new products, so you can take your audio setup to the next level.

With great sound, a compact size and the Alexa voice assistant built-in, the Sonos Era 100 packs a lot of punch, making it the best smart speaker for the money.

Advertisement

Elac has been belting out classic, affordable designs ever since its, er, debut in 2015. The Debut 2.0 exemplifies the brand’s appeal to both the budget-conscious and audiophiles. It offers a lively, insightful sound and attractive looks for around $400.

Pros

Advertisement

Big, generously proportioned speakers

Excellent sound quality perfect for long binge sessions

Nothing holds a candle to it for the money

Cons

Could be smoother, especially with its lower register

Dustcaps didn’t quite line up

Want the biggest sound? You’ll need big speakers. The fit and finish of the large Fluance XL8 towers is unmatched by other speakers at its price. The sound of the XL8F is open and thrilling, but never shrill, and when fed a movie soundtrack these speakers simply zing. They’re no slouch with music either. If you truly want the maximum speaker for your money, the huge Fluance XL8F has no equal.

Pros

Advertisement

Very compact (pocket-friendly)

More bass and volume than most speakers this small

Waterproof and dustproof (IP67)

Integrated strap

Can be linked to another StormBox Micro for stereo mode

USB-C charging

8 hours of battery life

Cons

Not as durable as Bose SoundLink Micro

Distorts slightly at higher volumes with certain tracks

Budget Bluetooth speakers are seemingly a dime a dozen, but among the countless options there do lie some gems. The $50 Tribit Stormbox Micro is a compact, portable speaker that offers both waterproofing and excellent bass for its size.

Pros

Advertisement

Compact, easy to set up and affordable

Excellent dialogue reproduction

Tried and true Roku experience

Cons

Lacks bass in movies and music

The $130 Roku Streambar is a hybrid soundbar-4K video streamer and the most welcome surprise is that it’s able to perform both tasks well. Pair it with a bedroom TV and the optional Onn Wireless Sub for a killer home theater setup.

If there was ever a bargain in home theater it was this — for around the same price as the Elac speakers above you can get a full Dolby Atmos setup. With a sub! Sound quality is excellent and the Klipsch kit includes all of the cables you need in the box.

Advertisement

The Edifier R1280DB offers almost everything you could want in a PC speaker — excellent sound, a range of connections including Bluetooth and a compact footprint — and all for a reasonable $150. It doesn’t offer USB, though, so connect the headphone/line out of your PC to it instead.

Advertisement

Pros

Excellent sound in a compact size

Amazon Alexa onboard

DTS Virtual:X

Articulate subwoofer

The Yamaha YAS-209 is one of the most fully featured soundbars the company has ever offered — especially at the price. With Alexa, HDMI connectivity and a wireless subwoofer, this soundbar doesn’t want for anything. The sound quality is great, too.

Advertisement

Pros

Motorized speakers work well.

Excellent sound for movies and music.

Plenty of connections

Includes rears and wireless sub.

Cons

Not as easy to use as Sonos Arc

No Apple AirPlay support

Somewhat short surround cables

The Vizio Elevate may have one big gimmick at the core of it, that revolving height speaker, but it also offers sound quality to back up the gee-whizzery. This is a 5.1.4 Dolby Atmos soundbar, with a hefty subwoofer, and its performance is equally thrilling in both movies and music. Add in a bunch of streaming features and you have the best surround system under a grand.

There’s a great debate these days about what the current crop of AI chatbots should and shouldn’t do for you. We aren’t wise enough to know the answer, but we were interested in hearing what is, apparently, Microsoft’s take on it. Looking at their terms of service for Copilot, we read in the original bold:

Copilot is for entertainment purposes only. It can make mistakes, and it may not work as intended. Don’t rely on Copilot for important advice. Use Copilot at your own risk.

While that’s good advice, we are pretty sure we’ve seen people use LLMs, including Copilot, for decidedly non-entertaining tasks. But, at least for now, if you are using Copilot for non-entertainment purposes, you are violating the terms of service.

Legal

While we know how it is when lawyers get involved in anything, we can’t help but think this is simply a hedge so that when Copilot gives you the wrong directions or a recipe for cake that uses bleach, they can say, “We told you not to use this for anything.”

It reminds us of the Prohibition-era product called a grape block. It featured a stern warning on the label that said: “Warning. Do not place product in one quart of water in a cool, dark place for more than two weeks, or else an illegal alcoholic beverage will result.” That doesn’t fool anyone.

Advertisement

We get it. They are just covering their… bases. When you do something stupid based on output from Copilot, they can say, “Oh, yeah, that was just for entertainment.” But they know what you are doing, and they even encourage it. Heck, they’re doing it themselves. Would it stand up in court? We don’t know.

Others

Now it is true that probably everyone will give you a similar warning. OpenAI, for example, has this to say:

Output may not always be accurate. You should not rely on Output from our Services as a sole source of truth or factual information, or as a substitute for professional advice.

You must evaluate Output for accuracy and appropriateness for your use case, including using human review as appropriate, before using or sharing Output from the Services.

You must not use any Output relating to a person for any purpose that could have a legal or material impact on that person, such as making credit, educational, employment, housing, insurance, legal, medical, or other important decisions about them.

Our Services may provide incomplete, incorrect, or offensive Output that does not represent OpenAI’s views. If Output references any third party products or services, it doesn’t mean the third party endorses or is affiliated with OpenAI.

Notice that it doesn’t pretend you are only using it for a chuckle. Anthropic has even more wording, but still stops short of pretending to be a party game. Copilot, on the other hand, is for fun.

Your Turn

How about you? Do you use any of the LLMs for anything other than “entertainment?” If you do, how do you validate the responses you get?

When things do go wrong, who should be liable? There have been court cases where LLM companies have been sued for everything, ranging from users committing suicide to defaming people. Are the companies behind these tools responsible? Should they be?

Anthropic is using copyright takedown notices to try to contain an accidental leak of the underlying instructions for its Claude Code AI agent. According to the Wall Street Journal, “Anthropic representatives had used a copyright takedown request to force the removal of more than 8,000 copies and adaptations of the raw Claude Code instructions … that developers had shared on programming platform GitHub.” From the report: Programmers combing through the source code so far have marveled on social media at some of Anthropic’s tricks for getting its Claude AI models to operate as Claude Code. One feature asks the models to go back periodically through tasks and consolidate their memories — a process it calls dreaming. Another appears to instruct Claude Code in some cases to go “undercover” and not reveal that it is an AI when publishing code to platforms like GitHub. Others found tags in the code that appeared pointed at future product releases. The code even included a Tamagotchi-style pet called “Buddy” that users could interact with.

After Anthropic requested that GitHub remove copies of its proprietary code, another programmer used other AI tools to rewrite the Claude Code functionality in other programming languages. Writing on GitHub, the programmer said the effort was aimed at keeping the information available without risking a takedown. That new version has itself become popular on the programming platform.

Right wing broadcasters are having a very good time under Brendan Carr, who has looked to destroy all remaining media consolidation limits to let them merge. Such companies, like Sinclair, Nexstar, and Tegna, don’t do journalism so much as they do soggy, right wing propaganda and infotainment, usually with endless fear mongering about drugs, homelessness, and crime rates.

They’re just one part of the right wing’s effort to remake the entirety of media into a massive safe space for dim autocrats.

Carr’s latest effort: he rubber stamped Nexstar Media Group’s $6.2 billion purchase of Tegna behind closed doors. Carr let the merged companies ignore our remaining media consolidation limits, which prevent one company from being the primary broadcast news voice for more than 39 percent of households (the new combined company reaches 54.5 percent).

Nexstar (a very Republican friendly company that also owns The Hill), not that long ago fired a journalist whose reporting angered Trump. Combined with Tegna, the two companies will own 221 Big Four broadcast stations, or more than half of the U.S. stations affiliated with FOX, NBC, ABC, or CBS.

Advertisement

Carr’s been on a campaign to ensure these right-wing loyal companies have more power in their dealings with their national counterparts (remember how they helped Carr censor Jimmy Kimmel?). The efforts come as local Americans increasingly live in “local news deserts” where quality local journalism simply no longer exists.

Anna Gomez, the lone Democrat left at the FCC (Republicans refuse to fill the other seat), didn’t have nice things to say about Carr’s decision to ignore the public interest protections without a transparent, public vote (indicating Carr very clearly knew this would be very unpopular):

As always, Carr’s order approving the merger leverages all manner of pseudo-legalistic sounding bullshit to justify ignoring Congress and the law. And he parrots a bunch of completely empty promises by Nexstar that they’ll ramp up the production of more “local news”:

“We note that Nexstar has made significant commitments in the agency’s record as well, further ensuring that this transaction promotes the public interest. To further serve its local communities, Nexstar commits to expanding its investment in local news and programming, including increasing the amount of local news it provides in acquired markets.”

Except again, by “news” we mean right wing propaganda. And Brendan Carr never meaningfully holds corporate power accountable for anything, unless it involves a comedian making fun of the president or companies not being suitably racist enough for the president’s liking.

Eight states have already filed a lawsuit challenging the legality of the decision. The lawsuits understandably focus heavily on the competition impacts, and the likely higher cable TV prices that will result for most of you:

Advertisement

“By consolidating with a major competitor, Nexstar would likely acquire the power to charge MVPDs higher retransmission consent fees for Big 4 station content. In turn, those MVPDs would likely pass on the increased retransmission consent fees, in large measure, to their subscribers in the form of substantially higher cable and satellite bills.”

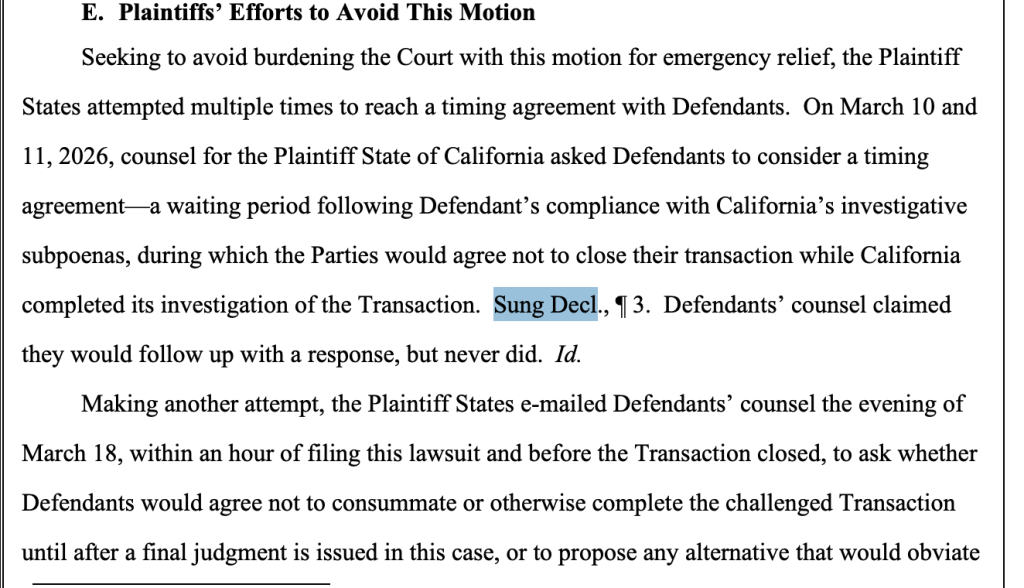

California regulators attempted to slow the process down by proposing a standard timing agreement with Nexstar, where the company would suspend its acquisition of Tegna until the state completed its investigation.

But something of particular note: on pages 16-17 of the states’ amended complaint, it becomes clear that Nexstar completely ignored the State AGs for 8 days, then ignored their lawsuit for another 18 hours, and then told the state AGs “The relief sought in your Complaint is no longer available.”

In other words, what passes for some of the only real antitrust enforcement we have (a scattered coalition of states) have to fight both consolidated corporate power and the authoritarian, corrupt government simultaneously to make any inroads in the public interest.

“This is completely unprecedented,” Free Press (the consumer group, not the Bari Weiss troll farm) Research Director S. Derek Turner told me via email. “Nexstar and the Trump DOJ and FCC seem to have acted in concert to deprive the citizens of of these 8 states their rights to have our AG enforce the antitrust laws on our behalf.”

If Carr succeeds here, I suspect it won’t be long before you see Sinclair and this new combined company merge. Carr is also fielding requests by the big four national broadcasters to eliminate restrictions preventing them from merging as well (one of many reasons they’ve been so feckless). After that, you’ll likely see more consolidation across telecom, tech, and media.

Advertisement

It is, just in case we’ve forgotten, the complete opposite of the “antitrust reform populism” Trump, and a long line of useful idiots, promised last election season.

While this is certainly an act of some desperation (less than 20% of all U.S. TV viewing is now broadcast), claiming this doesn’t matter because this is “just local broadcasting” and the “future is the internet” (something I see often) is a violent misread of the dire stakes of the situation. This aggressive, Trump-loyal consolidation hasn’t, and isn’t, just being confined to broadcast television (see: Twitter, TikTok).

This is, to be clear, a coordinated and illegal authoritarian/corporatist effort to ignore the public interest and the law to expand right wing propaganda’s power over an already clearly befuddled and broadly misinformed electorate. Right wingers will continue to engage in this quest to dominate the entirety of U.S. media (following in the steps of Victor Orban in Hungary) until they run into something other than the political and policy equivalent of soft pudding.

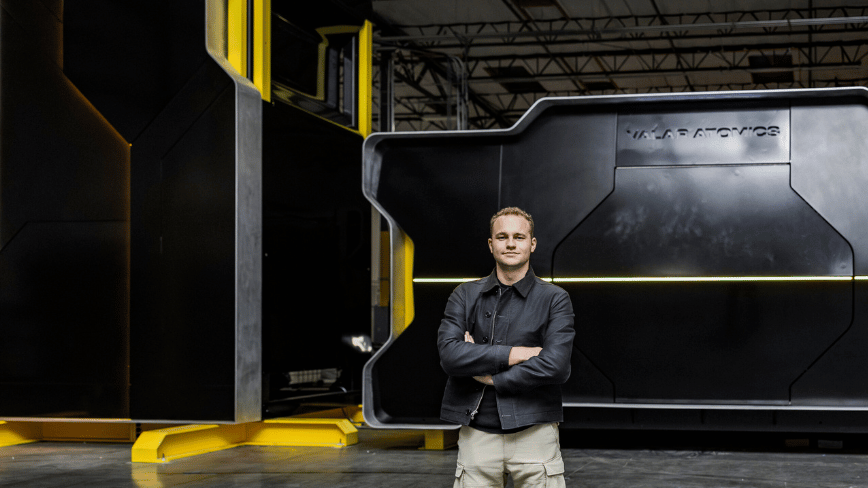

Isaiah Taylor was sixteen when he decided the nuclear industry had a size problem. Not that reactors were too dangerous or too expensive, though they are both, but that they were simply too big. The multi-gigawatt monuments to Cold War-era engineering that still dot the American landscape were designed for a grid that moved power in one direction: from a distant plant to a distant city. They were never meant to sit behind a hyperscaler’s fence line, feeding a cluster of GPU racks whose appetite doubles every eighteen months.

Taylor, now 27, founded Valar Atomics in 2023 to build something different. On Tuesday, the El Segundo, California-based startup announced it has raised $450 million at a $2 billion valuation, according to Bloomberg. The round comprises $340 million in equity and $110 million in debt, and it lands barely five months after a $130 million Series A that valued the company at a fraction of its current price.

The backers read like a roster of the Americandefence-tech establishment that has lately been writing enormous cheques. Palmer Luckey, the Anduril Industries founder whose company was recently reported to be pursuing a $4 billion raise at a $60 billion valuation, is an investor. So is Shyam Sankar, the chief technology officer of Palantir Technologies. The earlier Series A was led by Snowpoint Ventures, the firm co-founded by Doug Philippone, Palantir’s former head of global defence, alongside Day One Ventures and Dream Ventures. Lockheed Martin board member and former AT&T chief executive John Donovan also participated.

Valar’s pitch is built around what it calls “gigasites”, sprawling industrial campuses that would host hundreds or even thousands of small, high-temperature gas-cooled reactors operating in concert. Each unit uses helium as a coolant and TRISO fuel encased in graphite, a combination that allows the reactors to run at significantly higher temperatures than conventional light-water designs. The company says these clusters can deliver dense, steady, carbon-free power tailored to the load profiles of AI data centres, industrial manufacturers, and grid-constrained regions.

It is anaudacious answer to an increasingly urgent question: where will the electricity come from? The International Energy Agency projects that data-centre power consumption will double by 2026. Goldman Sachs estimates that 85 to 90 gigawatts of new nuclear capacity will eventually be needed to help fill the gap. Microsoft, Amazon, and Google have all signed nuclear power agreements in recent months, but the reactors those deals depend on do not yet exist at commercial scale.

Advertisement

Valar claims a meaningful head start. In November 2025, the company announced that its NOVA Core achieved zero-power criticality at Los Alamos National Laboratory’s National Criticality Experiments Research Centre, making it what the Breakthrough Institute described as the first company to reach that milestone under the US Department of Energy’s Nuclear Reactor Pilot Programme. Zero-power criticality — a self-sustaining chain reaction of uranium-235 without reaching full operating temperatures — is a necessary validation step, not a working power plant, but it is further than most of Valar’s competitors have publicly demonstrated.

The company is now preparing its Ward250 reactor, a 100-kilowatt thermal high-temperature gas-cooled unit, for power operations at the Utah San Rafael Energy Research Centre. In February 2026, the reactor was airlifted from California to Utah aboard three C-17 Globemaster military cargo aircraft in a joint operation between the Departments of Defence and Energy — a logistical stunt that doubled as a proof of concept for rapid reactor deployment. Valar is targeting operational status before 4 July 2026, the deadline the DOE set for three reactors in its pilot programme to achieve criticality.

Taylor’s trajectory has beenunconventional even by deep-tech standards. A self-taught coder who launched his first venture as a teenager, he comes from a family with nuclear roots: his great-grandfather, Ward Schaap, was a physicist on the Manhattan Project. The Ward250 reactor carries Schaap’s name. Taylor has assembled a leadership team that includes Mark Mitchell, the former president of Ultra Safe Nuclear Corporation, and Muhammad Shahzad, the former president and chief financial officer of Relativity Space.

The competitive field is crowded and well-funded. TerraPower, backed by Bill Gates, broke ground on a sodium-cooled reactor in Wyoming last year. Kairos Power is building a molten-salt demonstration plant in Tennessee. X-energy has a partnership with Dow Chemical for an industrial HTGR. Oklo, which went public via a SPAC in 2024, is developing a fast-neutron microreactor. None has yet delivered commercial power from an advanced design.

Advertisement

Valar has also taken a combative approach to regulation thatfew young companies would risk. In April 2025, the startup sued the Nuclear Regulatory Commission, arguing that the agency’s licensing framework unlawfully restricts small-scale reactor innovation by requiring the same approval process for low-power test reactors as for full-scale commercial plants. The lawsuit, filed alongside the states of Texas, Utah, Louisiana, Florida, and Arizona, as well as fellow reactor startups Last Energy and Deep Fission, seeks to shift regulatory authority for small reactors to individual states. The case has since been paused amid the Trump administration’s broader executive order to overhaul the NRC.

The $2 billion valuation places Valar among the most richly valued nuclear startups in the United States, a distinction that would have seemed absurd five years ago. Whether the premium reflectsgenuine confidence in the technology or the gravitational pull of AI-adjacent capitalis a question the next eighteen months should begin to answer. If the Ward250 reaches power operations in Utah this summer, Valar will have done something no advanced-reactor startup has managed: moved from incorporation to criticality to grid-connected electricity in roughly three years. If it does not, $2 billion will buy a very expensive physics experiment in the desert.

A delivery of medical supplies by Project C.U.R.E. (Project C.U.R.E. Photo)

[Editor’s Note: Agents of Transformation is an independent GeekWire series, underwritten by Accenture, exploring the adoption and impact of AI and agents. See coverage of our related event.]

Project C.U.R.E. had the answers. Decades of repair manuals for X-ray machines, anesthesia equipment and other medical devices — plus inventory data for the 250 semi-truck containers of supplies it ships to clinics worldwide every year. The problem was access: the archives had grown too large for any one person to navigate.

Now the nonprofit is turning to AI to start unlocking those resources, using the technology to predict future supply needs and search its manuals database for specific fixes.

“We’ve got almost 40 years of manuals,” said Doug Jackson, CEO of Project C.U.R.E., a Denver nonprofit providing medical aid. “There’s no way that any one person can sit down in a room and read through all those manuals. But AI can.”

Project C.U.R.E. was among 1,500 organizations in Bellevue, Wash., last week for Microsoft’s Global Nonprofit Leadership Summit, which centered on a high-stakes paradox for the social sector. The event’s focus was accelerated AI adoption and agentic tools, but the move toward automation keeps running into the gap between the technology’s potential and the real costs, skills and time required to deploy it.

Advertisement

Children International, a Kansas City-based organization serving impoverished youth, found a way to bridge that divide. Its employees are using AI agents for tasks including bulk translation of the letters sent from donors to children receiving their support.

“We had to do something different,” said Tim Batcha, vice president of Global Information Technology at Children International, speaking at the summit. He explained that too much effort was going toward day-to-day operations instead of advancing the nonprofit’s core mission.

To help others eager to deploy AI, the tech giant last Wednesday unveiled Microsoft Elevate for Changemakers, which expands the company’s Elevate program launched last July.

The initiative has three components:

Advertisement

“AI for Nonprofits” credential: The professional certificate created with LinkedIn and NetHope develops skills applicable for this specific sector.

AI skills training: Live and on-demand instruction modules are focused on nonprofit needs and target areas such as Microsoft Copilot’s agentic tools, change management and responsible AI governance.

Changemaker Fellowship: The program creates a global cohort supporting fellows deploying AI in their operations and is funded by Microsoft, EY, Caribou and others.

Inclusion and anxiety

Justin Spelhaug, president of Microsoft Elevate, left, and Tim Batcha, vice president of Global Information Technology at Children International, speaking at a Microsoft summit on March 25. (GeekWire Photo / Lisa Stiffler)

Changemakers aims to address challenges Microsoft own leaders’ repeatedly acknowledged at the summit — that while AI is likely to be one of the most influential technologies of this era, it’s also creating widespread concerns around job loss and other community impacts and threatens to further widen tech inequities worldwide.

“This defining moment of our time can either be more inclusive or it can be less inclusive based on the decisions that we make in rooms like this all around the world,” said Justin Spelhaug, director of Microsoft Elevate, addressing attendees.

Microsoft President Brad Smith said that one of the best ways to overcome fears and build support for AI is to get people using the technology at home and in their work.

“Anxiety, especially in the United States, has reached people before AI has,” Smith said.

Advertisement

The company has committed to providing more than $5 billion in support for nonprofits over the next year alone through discounts and donations of its technology, as well as grants.

In an interview with GeekWire, Spelhaug pointed to two key operations where AI is likely to have the greatest impact for nonprofits:

Answering calls from the people served by the organizations to answer basic questions and address straightforward needs, replacing automated phone systems with a “press 1, press 2” menu.

Improving fundraising by tracking donor information, providing personalized communications and supporting lead follow ups.

“There’s no shortage of problems in the world to solve,” Spelhaug said. “Let’s get people solving those problems and AI taking care of the work that it can take care of.”

AI ambitions and experiments

Seattle-based Evergreen Goodwill is testing AI as a tool for managing the millions of pounds of donated apparel and household goods every year that it sells or tries to recycle.

The century-old nonprofit was selected last year as an AI for Good Lab grant recipient and is using the funds to pilot the use of AI in pricing some of the roughly 26 million items it processes annually. It’s testing computer vision tech at one site that scans items and suggests prices — currently requiring staff to display individual items, but eventually aimed at an automated system.

Advertisement

Manually sorting and pricing “is very high stress,” said Brent Deim, Goodwill’s vice president of technology. The tech should help employees work faster, build AI skills, and its language capabilities can open up roles for people with limited English.

The AI-enabled tech should also result in more consistent pricing, prevent undervaluing of items, and ultimately increase proceeds that fund its free education and job training programs.

Evergreen Goodwill needs to price 26 million donated items each year to sell in its stores. (Evergreen Goodwill Photo)

And those initiatives are another opportunity for integrating AI, said Huan Do, Goodwill’s VP of mission advancement. Do is eager to apply the Changemakers’ AI credential to the programs to “enable our students to be the best employees available for a 21st century workforce.”

Rapid pace of change

Jackson of Project C.U.R.E. has his own ambitious ideas for AI. One is to create videos with avatars that guide healthcare workers in remote communities in repairing broken medical devices themselves — avatars that reflect the people being assisted, speaking their language and dialect.

But he also recognizes the hurdles to making AI initiatives a reality. For his 35-person team — even with 35,000 volunteer supporters — budget and staffing constraints loom large.

Advertisement

So do the challenges of digitizing historic paper records, persuading clinics to enter current operational data, and navigating privacy and data-use concerns. Keeping pace with rapidly evolving technologies, and ensuring those technologies can talk to one another, add further pressure.

“I’m just sitting here thinking, ‘Oh man, we are so far behind already,’” Jackson said after a tech demo at the summit. “We’ll try to get there.”

The Harbor Freight tool ecosystem includes plenty of quality gear. The retailer prioritizes great prices on equipment that’s no less valuable in actual use than more expensive types. Harbor Freight sells a range of in-house brands under a variety of toolmaker badges, focusing on automotive equipment, power and hand tools, and even accessories like safes, workbenches and other storage solutions. But there are some tools sold by the outlet that demand a bit of experience and knowledge to use safely or correctly.

DIYers are often eager to get their hands on a new piece of gear. This can give them the motivation they need to set off on a journey of discovery as they tackle the next exciting project on their to-do list. Yet some tools are far more difficult to use than others, introducing issues or safety concerns for those with limited experience or who don’t know how they operate. There’s also a wide range of tools that may feature simple operation, but are only utilized in support of extremely demanding tasks that beginners may not be ready to handle. These 12 tools epitomize this slate of issues. Yet, in many cases bringing their output within your wheelhouse is all about brushing up on your knowledge base; home improvement YouTube channels, online forums, and work within smaller, similar project areas can prepare you a bit better to enlist the help of these pieces of equipment.

Advertisement

Bauer 20V 4-1/2-Inch Slide Switch Angle Grinder

The Bauer 20V 4-1/2-Inch Slide Switch Angle Grinder is an obvious inclusion on a list of tools the beginners might want to rethink. This type of equipment is supremely versatile power, as it can be deployed for cutting, shaping, and even surface preparation tasks like sanding. But this is a tool that feels bound by a blood feud against its owner every time the disc spins up. Angle grinders produce incredible rotational force, and so you’ll want to be extra careful about keeping a firm grasp as you use one. This Bauer model also features a slide switch, which can be a little more dangerous than a paddle-operated solution because it’s unlikely you’ll be holding it at the switch while in use, prompting routine use of the lock-on position. The paddle switch on a tool like an alternative Hercules model features better trigger placement, allowing you to cut the power with much greater ease.

Advertisement

A beginner might still be enticed by the Bauer model, particularly because of its $40 price tag. It does possess a tool-free blade guard and a dual-position side handle. Opting for this tool isn’t necessarily a mistake, but understanding that the unit produces up to 10,500 RPM with a lock-on functionality that you’ll use virtually every time you reach for the grinder (speaking from experience) will keep you safer.

Advertisement

Pittsburgh Needle File Set (12-Piece)

Harbor Freight’s range of accessory tools is robust; plenty of options in this part of its catalog are certainly impressive. The Pittsburgh Needle File Set offers extensive coverage across a range of file geometries that can help support innumerable tasks ranging from touching up a shovel’s edge to keeping your lawn mower’s blades in good working order. The set it is listed at Harbor Freight for just $4, adding an element of cost effectiveness that is truly rare for such a hard hitting option with tremendous versatility. There’s absolutely nothing wrong with this set of files and 601 Harbor Freight buyers have given it a 4.6 star average rating with a 98% recommendation rate.

Where this tool set falls short for beginners is at the back end of each file; none of the tools come with a handle. This is just fine for users who understand how to add them, or perhaps prefer to tackle detail work without one attached for greater control. But this demands a different level of dexterity and command that beginners may not have mastered yet. Pittsburgh also offers a 10-piece needle file set as well as a 12-piece precision set that each feature handles attached to the tools alongside price tags that remain below $10.

Advertisement

Pittsburgh 8-Pound Hickory Sledgehammer

Most tasks featuring a hammer won’t require truly excessive pounding force, but demolition can sometimes demand a sledgehammer. There’s nothing quite like knocking down wall elements with a heavy sledge. Sometimes it’s impractical, and a different demo tool like a reciprocating saw might do a better job, but it’s undeniable how much fun you’ll have smashing apart components bound for the trash heap. However, beginners might not realize until they swing their sledgehammer for the first time that varying handle materials can play a significant role in the experience. The hammer that gets the nod on this list is the outlet’s Pittsburgh 8-Pound Hickory Sledgehammer.

The potential trouble here is that while a wooden handle offers a traditional feel and better responsiveness to the user, it also translates vibration significantly more freely into the hands. For the same reason that youth players don’t swing wooden bats while the pros exclusively carry lumber to the plate, a wooden handle on your striking tool can ultimately send painfully uncomfortable shockwaves running through your forearms. Pittsburgh also offers an 8-pound fiberglass-handled option for $27, just two bucks more than the hickory selection.

Advertisement

Bauer 15 Amp 14-Inch Portable Concrete Pull Saw

The consaw is a critically important tool for anyone working with brick, block, or concrete. It’s something of a demolition tool, but it can also be used to cut material to length during installation tasks. This is a tool that delivers immense power to support some of the hardest cutting requirements you’ll encounter. I’ve rented a consaw on a few occasions, and they’ve always been gasoline-powered models laid out in the traditional format for a classic power output and surprisingly buttery smooth cutting performance. I don’t have personal experience with the Bauer 15 Amp 14-Inch Portable Concrete Pull Saw, but two important features underpinning its use give me pause as someone who’s used tools in this arena before.

It’s worth noting that the tool is listed at Harbor Freight for $300, which is significantly cheaper than the typical consaw that can easily cost thousands of dollars. It also features a 4.2 star average rating from 235 buyers. However, the corded power source means that your mobility may ultimately be severely restricted. It’s also designed to cut on a pull stroke, specifically. This can limit your ability to make clean cuts in vertical walls and other elements, but is likely to enhance accuracy when cutting stock in a horizontal motion.

Advertisement

Windsor Design No. 33 Bench Plane

Harbor Freight offers a small selection of hand planes. The Windsor Design No. 33 Bench Plane appears to be a beautifully crafted woodworking tool, featuring a 23-degree blade angle, hardwood handles with brass fittings, and a high carbon steel cutting blade measuring 2-¾ inches wide for quality cutting and a pleasant experience all around. The tool is listed for $13, making it a cost-effective option that’s likely even more approachable than vintage gear you’d find at a garage sale. However, this is a tool that frequently gets middling to poor user ratings: It features a 3.7 star average from 779 buyers.

Advertisement

Numerous users report that the blade is not razor sharp out of the package and that additional elements of setup work are required to get the plane to take a smooth shaving. It’s simply not ready to use out of the box. To be fair, a $13 precision woodworking tool really shouldn’t be compared directly to much more expensive alternatives that might be capable of transitioning straight from packaging to workbench. Expectation and knowledge about plane maintenance can really trip up a beginner woodworker with this unit. If you aren’t aware of the tasks involved in preparing a hand plane for service, you may ultimately find more frustration with this tool than enjoyment.

Advertisement

Fasten-Pro Tacking Gun

The Fasten-Pro Tacking Gun looks to be the same kind of tool as any other staple gun you might consider. Because of this visual similarity it’s easy to mix up heavy duty tacking guns and staplers designed for lighter service. This unit from Harbor Freight gets quality reviews, with a 4.2 star average rating from 436 buyers, but it’s not the right tool for handling light fastening tasks. Instead, this fires heavy gauge T-50 style staples suitable for use in hardwoods and even soft metal components.

The tacking gun is a quality option for handling heavier fastening formats, but it’s actually not the best solution for this kind of work in many instances. If you’re driving lots of heavy duty staples into workpieces, the Fasten-Pro hammer tacker is often the better solution because it’s much faster and also limits the amount of force placed on your hands and forearms.

If lighter duty jobs or on the docket, the same brand is still a go-to option, with a three-way tacker and staple gun that delivers standard brad fasteners or U-shaped staples. This tool offers a lighter touch when a heavy dollop of force that would come from a tool like the tacking gun might damage your work surface. Finally, Fasten-Pro’s 2-in-1 stapler/brad nailer offers the same nuanced touch with an electric-powered actuation rather than your grip strength.

Advertisement

Pittsburgh 28-Inch Cable Cutters

The Pittsburgh 28-Inch Cable Cutters is yet another tool that makes this list, but not because it’s a bad implement or fails to achieve a similar standard to alternative solutions. Instead, it exists within a niche subsection of the DIY world in which users will be buying the tool to support a specific, often highly demanding task. Heavy-duty cable cutters like this are not pulled out of the toolbox to shear through small wires designed to carry minimal current. This tool features 28-inch handles to deliver the extreme leverage required to bite into armored cables and other dense power supply lines. Anytime you’re working with electricity, it’s crucial to ensure that you’ve taken the time to prepare the environment and double check your safety protocols. There are a range of mistakes that DIYers frequently make during electrical tasks; many of them come from a lack of experience and can result in shocks or injuries.

By all accounts this is a high quality tool, with 432 customers giving it a 4.1 star average rating. They like its $25 price point and note routinely that it can cut with ease through even thick cable and wire rope. But users will need to be abundantly careful when pulling out these cutters to ensure they aren’t preparing to snip through a live wire carrying a dangerous amperage level. Fortunately, electrical safety is exceedingly simple as long as you’re diligent about your checks and workflow.

Advertisement

Chicago Electric Power Tools 7 Amp 4-Inch Handheld Dry-Cut Tile Saw

Cutting tile isn’t a job for the faint of heart. Even with quality tools at your disposal, this is a nerve-wracking task that requires precision and patience. Maintaining deliberate action throughout a cut and moving at the right speed to limit chipping or breakage is essential. For this reason, many users across all levels of knowledge and skill tend to gravitate toward bulkier, stationary cutting implements, frequently involving moving the workpiece rather than the blade. A tool like the Chicago Electric Power Tools 7 Amp 4-Inch Handheld Dry-Cut Tile Saw runs counter to this preference.

Advertisement

The tool retails for just $40, making it an affordable power tool. It also sports a 4.4 star average rating from 475 customer reviews, indicating that so can be useful in the right hands. Personally, I have limited experience cutting tile but I did try once with an angle grinder, failing miserably to keep the edges clean. However, I’ll add that anytime you leave a chipped edge, there’s a high probability of creating a razor-sharp side while throwing equally dangerous chips around your workspace. Therefore, any tile job you encounter requires care and attention. The tool itself delivers 12,000 RPM blade speeds with the ability to cut material up to 1-⅛-inch thick.

Advertisement

Central Machinery 7 Horsepower Plate Compactor

A plate compactor is a heavy-duty power tool, frequently running on a gasoline engine. The Central Machinery 7 Horsepower Plate Compactor is exactly this kind of device, and offers plenty of pounding force to flatten hard landscaping material. The tool gets great reviews from buyers, with a 4.7 star average rating across 250 reviews and a 97% recommendation rate. It’s listed for $700, which is a pretty good bargain when considering the high cost alternatives out there in the market. Where a beginner may falter with a tool like this is in their project scope.

Even a small landscaping job requiring a plate compactor tends to leverage a huge volume of heavy material. Last year, when installing a paver driveway, I rented one of these tools; the task of compacting my subbase material was straightforward and enjoyable. What was far more time-consuming was the actual task of laying gravel and sand. A one-car installation required substantial excavation alongside 8 tons of replacement material in addition to the paver bricks themselves, which are no picnic to move either. If you aren’t fully prepared for the physicality of the tasks that come before a plate compactor makes its entrance in your project workflow, you’ll likely be rethinking your decision about handling the job yourself.

Advertisement

Pittsburgh 7-Inch Poly Hand Riveter Kit

Rivets form an important addition to any renovator’s fastening capabilities. You’ll often lean on nails and screws, but rivets are just as valuable when securing fabrics and other materials to wood or even in handling repairs to clothing. Riveters are a key tool when using these fasteners. Among Harbor Freight’s options is the Pittsburgh 7-Inch Poly Hand Riveter Kit. It’s a one-handed tool that promises to set rivets of varying sizes “perfectly in a single stroke.” For those with experience handling a riveter, this may be the case, but operating this type of tool with one hand can be challenging for beginners. The force required to collapse a rivet and set the back end for a secure hold is fairly substantial. Doing it without two hands on the tool can ultimately be more effort than many are ready to deliver.

A classic riveter that offers more leverage is the Fasten-Pro 11-inch model. It features a 360-degree swivel head and comes with four nosepieces for great coverage across a range of needs. Another selection that can make for an enhanced experience is the Doyle 10-inch professional model. It’s a little more expensive, but features a “100% lifetime guarantee” and offers even greater leverage with an ergonomic grip design and a range of color-coded nosepieces.

The Hercules 15 Amp 66-Pound 1-⅛-Inch Hex Breaker Hammer is a heavy-duty tool that serves one hyper-specific purpose. It’s not like a rotary hammer that can function as a drilling tool or a concrete chipping option, as it just performs the singular demolition task. Instead, this tool exclusively delivers up to 58 joules of impact energy, making it capable of immense power output in support of large scale demolition. It’s exceptionally capable, but the job it’s designed to handle isn’t one that many beginner tool users will want to take on by themselves.

Breaking up large concrete segments is a multi-stage job. First you’ll need to destroy the element using a tool like the breaker hammer. This option offers 1,000 beats per minute while also utilizing a built in Maximum Vibration Control to keep user fatigue to a minimum. But that’s only part of the task. Removing the heavy concrete remnants is an entirely new and demanding subtask that can’t be ignored once the initial demolition is completed. As a result, this is easily a job that can make you feel like you’re in over your head.

Advertisement

Bauer 4 Cubic Foot Cement Mixer

The Bauer 4 Cubic Foot Cement Mixer is a tool with 190 ratings from customers, accumulating a 4.8 star average with a 98% recommendation rate. Customers frequently note that it’s easy to use while delivering high quality at a low price. The tool can support mixing tasks featuring up to two 80-pound bags of concrete, mortar, stucco, or other needs. This makes it quality option in support of medium to semi-large concrete tasks or finish work like plastering or rendering walls. Even on smaller projects, having a dedicated mixer available can take a lot of the hassle out doing this job yourself. The tool is available for $380, which is by all accounts a very reasonable price point.

Advertisement

Anyone in the market for a concrete mixing solution will certainly want take a look at this tool. However, it usually takes a special kind of project to demand a mixer like this. You’re often going to seek out mixing solutions for larger pours or substantial plastering tasks rather than small touchup work. As a result, all the other elements of the project are frequently intensely demanding. This may not always be feasible for a home improver, and getting halfway through before realizing you’re way past your comfort zone can sometimes be worse than starting from scratch with professional help.

Advertisement

Methodology

Each of the tools on this list presents unique challenges of one type or another. Frequently, there’s a different option from Harbor Freight that may be better suited to a beginner’s needs. However, some jobs that these tools are specifically designed to fulfill may be better left to professionals. Potentially dangerous tools can increase the risk of injury in the hands of a less experienced operator, while others are purpose-built for heavy duty work that can quickly become overbearing on a beginner who may not have fully prepared for the amount of work ahead.

Although the jogging stroller is a fixture of suburban life, allowing parents the opportunity to get some exercise while letting their young children a chance for some fresh air, it would seem like the designers of these strollers have never actually gone for a jog. Requiring a runner to hold their hands at fixed positions can be incredibly uncomfortable and disrupts most people’s strides and cadence — so [John] attempted to solve the problem after finding one of these strollers on the secondhand market.

While there are some purpose-built strollers that attempt to address these issues, they can be pricey. Rather than shell out for a top-dollar model, [John] got to work with his 3D printer and created a prototype device that allows him to attach the stroller at his waist while leaving his hands free. There were a few problems to overcome here, the first of which would cause the device to buckle under certain loading situations. This was solved with some small pieces of rope which act as flexible bump stops, keeping the hinge mechanism from binding up. Another needed to be solved with practice, which was that it took some time to be able to steer the stroller without using one’s hands.

As an added bonus, [John] also included a system that tracks the distance the stroller has traveled. Using a hall effect sensor and a magnet attached to the wheel, a small microcontroller is able to quickly calculate distance and display it on a tiny screen mounted near the handlebars. Although smartphones are handy, their GPS systems can be surprisingly inaccurate, so a system like this can be a better indicator since it’s being directly measured. All in all, not a bad few upgrades to a secondhand stroller.

As generative AI matures from a novelty into a workplace staple, a new friction point has emerged: the “shadow AI” or “Bring Your Own AI (BYOAI)” crisis. Much like the unsanctioned use of personal devices in years past, developers and knowledge workers are increasingly deploying autonomous agents on personal infrastructure to manage their professional workflows.

“Our journey with Kilo Claw has been to make it easier and easier and more accessible to folks,” says Kilo co-founder Scott Breitenother. Today, the company dedicated to providing a portable, multi-model, cloud-based AI coding environment is moving to formalize this “shadow AI” layer: it’s launching KiloClaw for Organizations and KiloClaw Chat, a suite of tools designed to provide enterprise-grade governance over personal AI agents.

The shadow AI crisis: Addressing the BYOAI problem

The impetus for KiloClaw for Organizations stems from a growing visibility gap within large enterprises. In a recent interview with VentureBeat, Kilo leadership detailed conversations with high-level AI directors at government contractors who found their developers running OpenClaw agents on random VPS instances to manage calendars and monitor repositories.

“What we’re announcing on Tuesday is Kilo Claw for organizations, where a company can buy an organization-level package of Kilo Claws and give every team member access,” explained Kilo co-founder and head of product and engineering Emilie Schario during the interview.

“We can’t see any of it,” the head of AI at one such firm reportedly told Kilo. “No audit logs. No credential management. No idea what data is touching what API”.

This lack of oversight has led some organizations to issue blanket bans on autonomous agents before a clear strategy on deployment could be formed.

Advertisement

Anand Kashyap, CEO and founder of data security firm Fortanix, told VentureBeat without seeing Kilo’s announcement that while “Openclaw has taken the technology world by storm… the enterprise usage is minimal due to the security concerns of the open source version.”

Kashyap expanded on this trend:

“In recent times, NVIDIA (with NemoClaw), Cisco (DefenseClaw), Palo Alto Networks, and Crowdstrike have all announced offerings to create an enterprise-ready version of OpenClaw with guardrails and governance for agent security. However, enterprise adoption continues to be low.

Enterprises like centralized IT control, predictable behavior, and data security which keeps them compliant. An autonomous agentic platform like OpenClaw stretches the envelope on all these parameters, and while security majors have announced their traditional perimeter security measures, they don’t address the fundamental problems of having a reduced attack surface. Over time, we will see an agentic platform emerge where agents are pre-built and packaged, and deployed responsibly with centralized controls, and data access controls built into the agentic platform as well as the LLMs they call upon to get instructions on how to perform the next task. Technologies like Confidential Computing provide compartmentalization of data and processing, and are tremendously helpful in reducing the attack surface.”

Advertisement

KiloClaw for Organizations is positioned as the way for the security team to say “yes,” providing the visibility and control required to bring these agents in-house.

It transitions agents from developer-managed infrastructure into a managed environment characterized by scoped access and organizational-level controls.

Technology: Universal persistence and the “Swiss cheese” method

A core technical hurdle in the current agent landscape is the fragmentation of chat sessions.

During the VentureBeat interview, Schario noted that even advanced tools often struggle with canonical sessions, frequently dropping messages or failing to sync across devices.

Advertisement

Schario emphasized the security layer that supports this new structure: “You get all the same benefits of the Kilo gateway and the Kilo platform: you can limit what models people can use, get usage visibility, cost controls, and all the advantages of leveraging Kilo with managed, hosted, controlled Kilo Claw”.

To address the inherent unreliability of autonomous agents—such as missed cron jobs or failed executions—Kilo employs what Schario calls the “Swiss cheese method” of reliability. By layering additional protections and deterministic guardrails on top of the base OpenClaw architecture, Kilo aims to ensure that tasks, such as a daily 6:00 PM summary, are completed even if the underlying agent logic falters.

This is critical because, as Schario noted, “The real risk for any company is data leakage, and that can come from a bot commenting on a GitHub issue or accidentally emailing the person who’s going to get fired before they get fired”.

Product: KiloClaw Chat and organizational guardrails

While managed infrastructure solves the backend problem, KiloClaw Chat addresses the user experience. Schario noted that “Hosted, managed OpenClaw is easier to get started with, but it’s not enough, and it still requires you to be at the edge of technology to understand how to set it up”. Kilo is looking to lower that barrier for the average worker, asking: “How do we give people who have never heard the phrase OpenClaw or Claudebot an always-on AI assistant?”.

Advertisement

Traditionally, interacting with an OpenClaw agent required connecting to third-party messaging services like Telegram or Discord—a process that involves navigating “BotFather” tokens and technical configurations that alienate non-engineers.

“One of the number one hurdles we see, both anecdotally and in the data, is that you get your bot running and then you have to connect a channel to it. If you don’t know what’s going on, it’s overwhelming,” Schario observed.

“We solved that problem. You don’t need to set up a channel. You can chat with Kilo in the web UI and, with the Kilo Claw app on your phone, interact with Kilo without setting an external channel,” she continued.

This native approach is essential for corporate compliance because, as she further explained, “When we were talking to early enterprise opportunities, they don’t want you using your personal Telegram account to chat with your work bot”. As Schario put it, there is a reason enterprise communication doesn’t flow through personal DMs; when a company shuts off access, they must be able to shut off access to the bot.

Advertisement

Looking ahead, the company plans to integrate these environments further. “What we’re going to do is make Kilo Chat the waypoint between Telegram, Discord, and OpenClaw, so you get all the convenience of Kilo Chat but can use it in the other channels,” Breitenother added.

The enterprise package includes several critical governance features:

Identity Management: SSO/OIDC integration and SCIM provisioning for automated user lifecycles.

Centralized Billing: Full visibility into compute and inference usage across the entire organization.

Admin Controls: Org-wide policies regarding which models can be used, specific permissions, and session durations.

Secrets Configuration: Integration with 1Password ensures that agents never handle credentials in plain text, preventing accidental leaks.

Licensing and governance: The “bot account” model

Other security experts note that handling bot and AI agentic permissions are among the most pressing problems enterprises are facing today

As Ev Kontsevoy, CEO and co-founder of AI infrastructure and identity management company Teleport told VentureBeat without seeing the Kilo news: “The potential impact of OpenClaw as a non-deterministic actor demonstrates why identity can’t be an afterthought. You have an autonomous agent with shell access, browser control, and API credentials — running on a persistent loop, across dozens of messaging platforms, with the ability to write its own skills. That’s not a chatbot. That’s a non-deterministic actor with broad infrastructure access and no cryptographic identity, no short-lived credentials, and no real-time audit trail tying actions to a verifiable actor.”

Advertisement

Kilo is proposing to solve it with a major change in organizational structure: the adoption of employee “bot accounts”.

In Kilo’s vision, every employee eventually carries two identities—their standard human account and a corresponding bot account, such as scott.bot@kiloco.ai.

These bot identities operate with strictly limited, read-only permissions. For example, a bot might be granted read-only access to company logs or a GitHub account with contributor-only rights. This “scoped” approach allows the agent to maintain full visibility of the data it needs to be helpful while ensuring it cannot accidentally share sensitive information with others.

Addressing concerns over data privacy and “black box” algorithms, Kilo emphasizes that its code is source available.

Advertisement

“Anyone can go look at our code. It’s not a black box. When you’re buying Kilo Claw, you’re not giving us your data, and we’re not training on any of your data because we’re not building our own model,” Schario clarified.

This licensing choice allows organizations to audit the resiliency and security of the platform without fearing their proprietary data will be used to improve third-party models.

Pricing and availability

KiloClaw for Organizations follows a usage-based pricing model where companies pay only for the compute and inference consumed. Organizations can utilize a “Bring Your Own Key” (BYOK) approach or use Kilo Gateway credits for inference.

The service is available starting today, Wednesday, April 1. KiloClaw Chat is currently in beta, with support for web, desktop, and iOS sessions. New users can evaluate the platform via a free tier that includes seven days of compute.

Advertisement

As Breitenother summarized to VentureBeat, the goal is to shift from “one-off” deployments to a scalable model for the entire workforce: “I think of Kilo for orgs as buying Kilo Claw by the bushel instead of by the one-off. And we’re hoping to sell a lot of bushels of of kilo claw”.

That’s a massive $1250 saving on a machine packed with serious hardware. At the center of the Nimo N159 is an 8-core AMD Ryzen 7 7735HS processor paired with Radeon 680M graphics which delivers nippy performance across demanding tasks, creative workflows, and heavy multitasking.

Backing that up is 32GB of DDR5 RAM, giving the system plenty of headroom for running multiple applications.

Advertisement

Today’s top creative laptop deal

A large 1TB NVMe SSD provides fast boot times, quick app launches, and enough space for projects, media libraries, and everyday files.

The 15.6-inch Full HD IPS display promises clear visuals with wide viewing angles, making it comfortable to use for long sessions. A nearly 180-degree hinge adds flexibility when sharing content or adjusting the screen to suit different working positions.

While the integrated graphics card is going to limit use for video editing, the high-performance Ryzen 7 processor coupled with 32GB DDR5 RAM is an essential for photo editing, particularly if you’re creating images for online. I can’t see color gamut listed here or on the official website, so I can’t recommend it for print-ready content creation.

Advertisement

A built-in fingerprint reader allows quick sign-ins, and a physical webcam privacy switch gives direct control over camera access when you’re not using it.

It’s powered by a 54Wh battery paired with 100W USB-C fast charging support. The laptop includes HDMI and five USB ports, as well as Wi-Fi and Bluetooth support.

At just $859, the Nimo N159 with 32GB of RAM and a 1TB SSD is a solid deal you won’t want to miss out on.

We spend hours testing every product or service we review, so you can be sure you’re buying the best. Find out more about how we test.

JBL Live 780NC: Two-minute review

I was not expecting to be as impressed by the JBL Live 780NC as I ended up being. Even out of the box, it looked like another good but not great $200-range pair of headphones that excel in certain areas but end up making compromises elsewhere. But really the only compromises are the lack of a charging cable and the fact you can’t remove the ear pads.

But dig a little deeper and the JBL Live 780NC start to shine. The feature set rivals that of the best wireless headphones out there like the Sony WH-1000XM6. Sure, most wireless headphones now come with active noise cancellation and an ambient mode, but many don’t come with Auracast, as powerful of an EQ (and personalized EQ), or Dolby Atmos and Hi-Res support. At least, not at this price.

Advertisement

I’ll throw in the obligatory these-aren’t-perfect counterpoints — and there are a few. The bass can sometimes get a little out of control to the point where I usually had the bass cut through the EQ when listening. And the Dolby Atmos feature is a bit underwhelming for music, not to mention that only a handful of streaming services provide Dolby Atmos content. Still, the JBL Live 780NC get high marks from me. And if you give them a chance, you’ll probably feel the same.

(Image credit: Future / James Holland)

JBL Live 780NC: Price and release date

Priced $249.95 (about £190 / AU$360, but currently launched in US only)

Launch date March 12, 2026

With a March 2026 launch date in the US, the JBL Live 780NC are the newest addition to JBL’s lineup of over-ear headphones, having landed alongside their 680NC on-ear counterparts. And despite being among the more expensive of JBL’s offerings (only out priced by the JBL Tour One M3 Smart Tx and the JBL Quantum One), they’re firmly in the mid-tier price range for over-ear wireless cans in general, coming in at $249.95 (about £190 / AU$360). They’re also available in five colors: black, green, blue, white, and champagne.

Unfortunately, at the time of writing, the JBL Live 780NC are only available in the US. However, considering their predecessor, the 2023-issue JBL Live 770NC, can be purchased in the UK and Australia, my guess is that it’s only a matter of time before these headphones will become available in those regions as well.

Advertisement

JBL Live 780NC: Specs

Swipe to scroll horizontally

Drivers

40mm drivers

Active noise cancellation

Advertisement

Adaptive

Battery life

Up to 50 hours with ANC On, 80 without

Weight

Advertisement

260g

Connectivity

Bluetooth 6.0

Frequency range

Advertisement

10Hz – 40kHz

Waterproofing

N/A

Other features

Advertisement

Multipoint connectivity, App Support, Adaptive Active Noise Cancellation and Transparency Mode, Hi-Res, Spatial Audio, Fast Charging, Auracast, Voice Assistant

JBL Live 780NC: Features

Image 1 of 4

(Image credit: Future / James Holland)

(Image credit: Future / James Holland)

(Image credit: Future / James Holland)

(Image credit: Future / James Holland)

Multipoint and Auracast available

Personalizable EQ according to what you can hear

Deep EQ manipulation

The JBL Live 780NC may be as feature-filled as any other pair of headphones on the market. Not only do they come with multipoint connectivity, but allow for use with Auracast where you can connect multiple headphones to one source, as well as Bluetooth with LE Audio (something Apple doesn’t currently support). They even do that thing where they stop playing when you take them off your head.

The active noise cancellation and Ambient (sometimes referred to as transparency) mode are fairly deep. You can set levels of both using a slider, as well as turn on an adaptive mode for the ANC. TalkThru, basically an ambient mode hyperaware of human voices, is also an option here. And they work pretty well too.

Advertisement

Sign up for breaking news, reviews, opinion, top tech deals, and more.

The ANC was able to completely block out ambient noise with music playing at 50%, while the ambient mode was able to still allow me to fully understand a conversation on TV while listening to music at 60%.

Of course, while you can cycle through the types of “Ambient Sound Control” as JBL calls it with a press of a button on the headphones, the real fine tuning happens in the JBL headphone app. The app has a number of additional features and ways of customizing your experience.

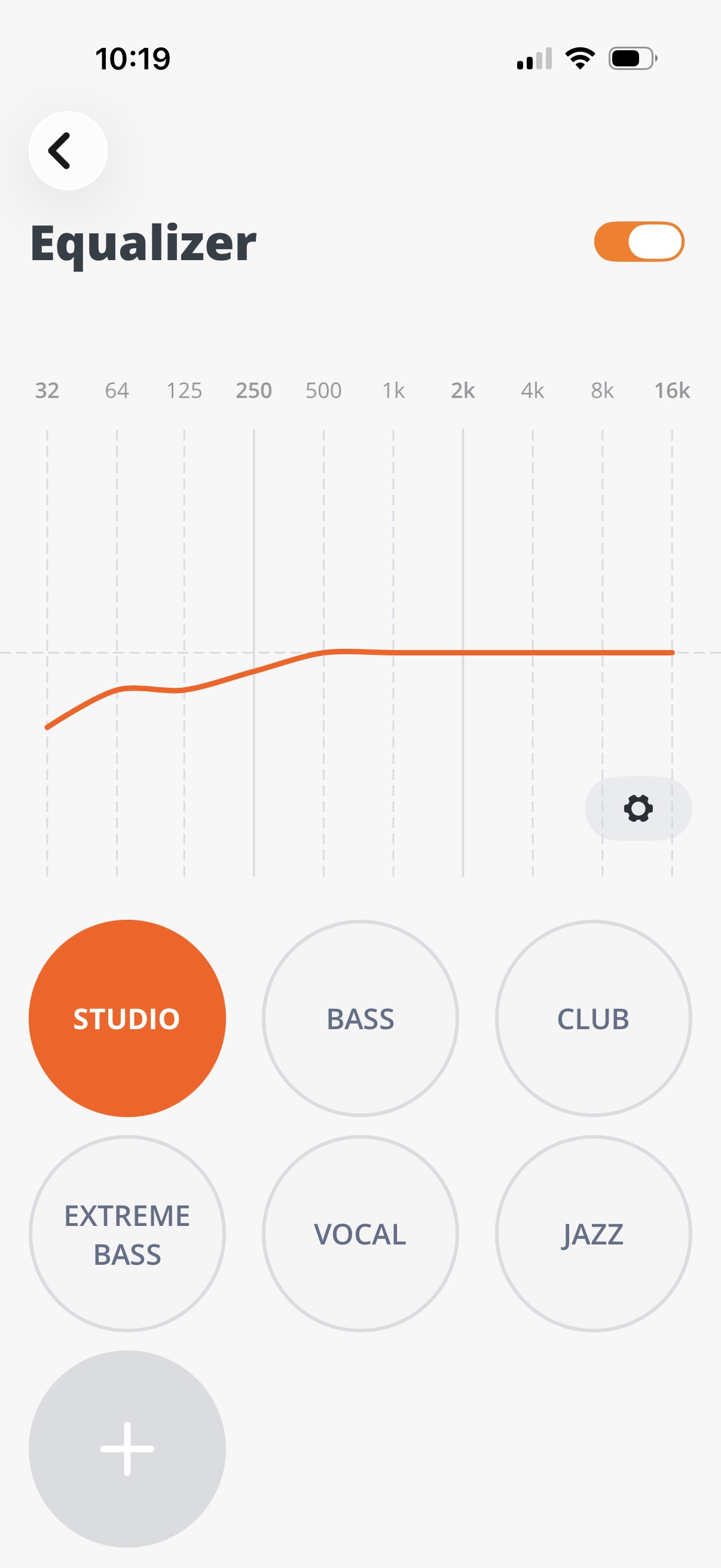

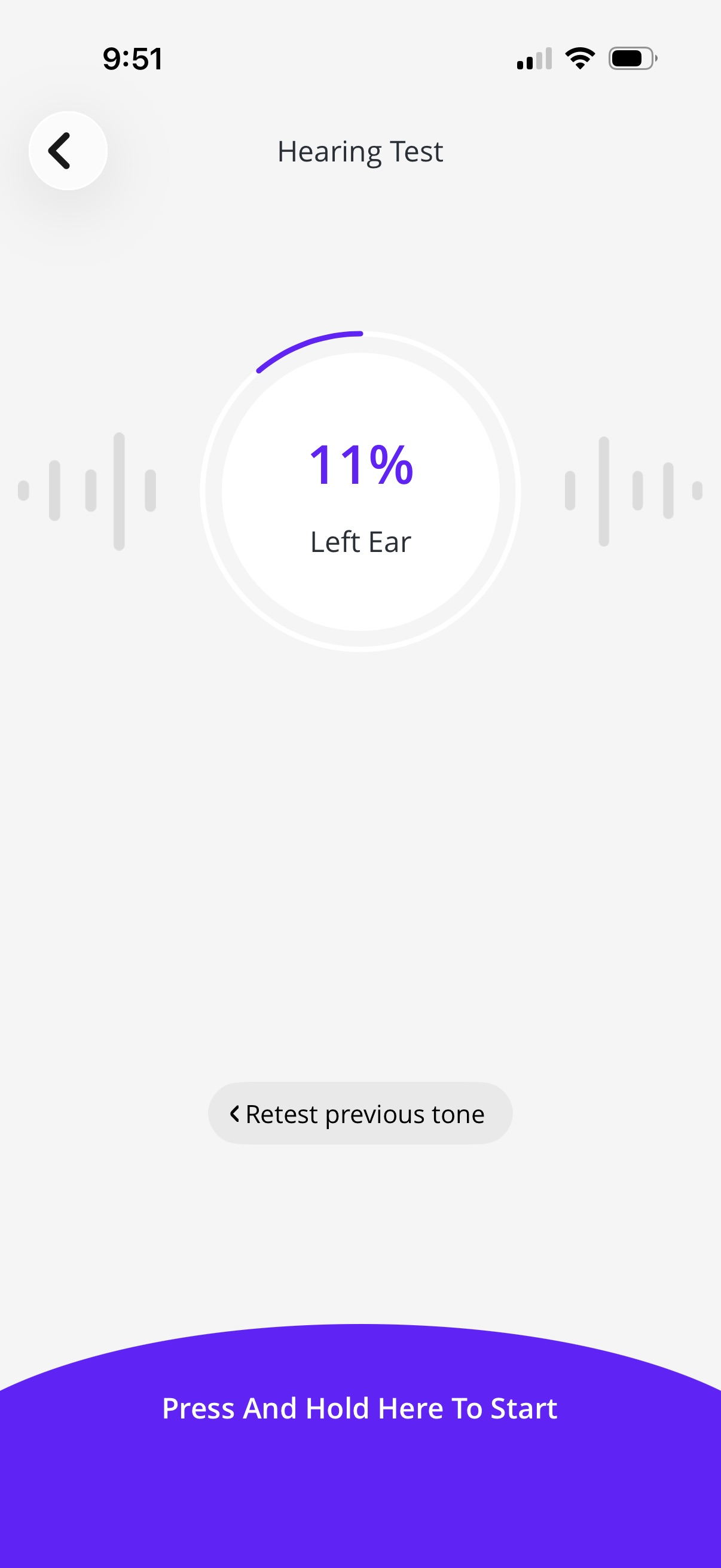

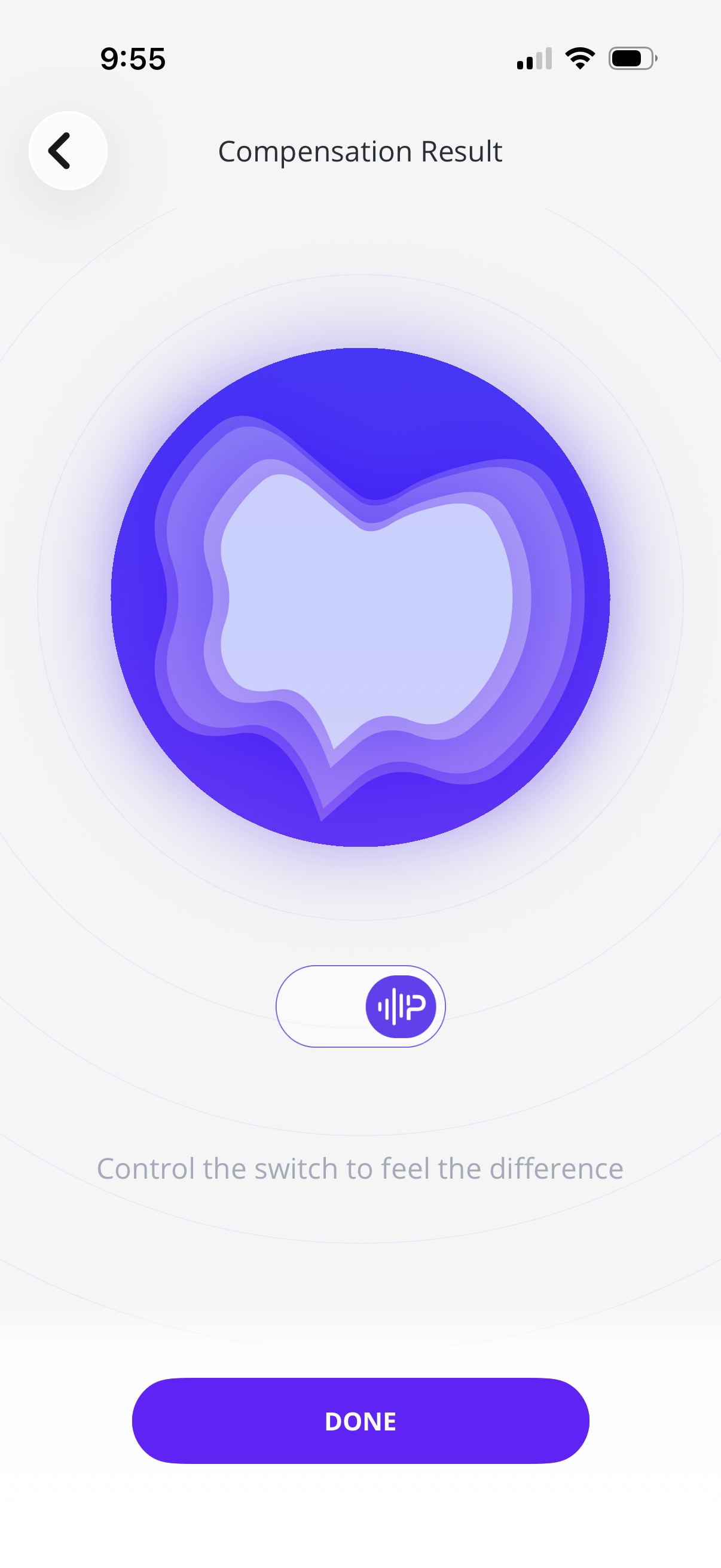

For instance, Personi-fi 3.0 is a cool feature that tests how well you can hear a series of frequencies on both ears and then adjusts the EQ to offset any hearing loss you have. I also appreciated that I could toggle it on and off after going through the process.

Advertisement

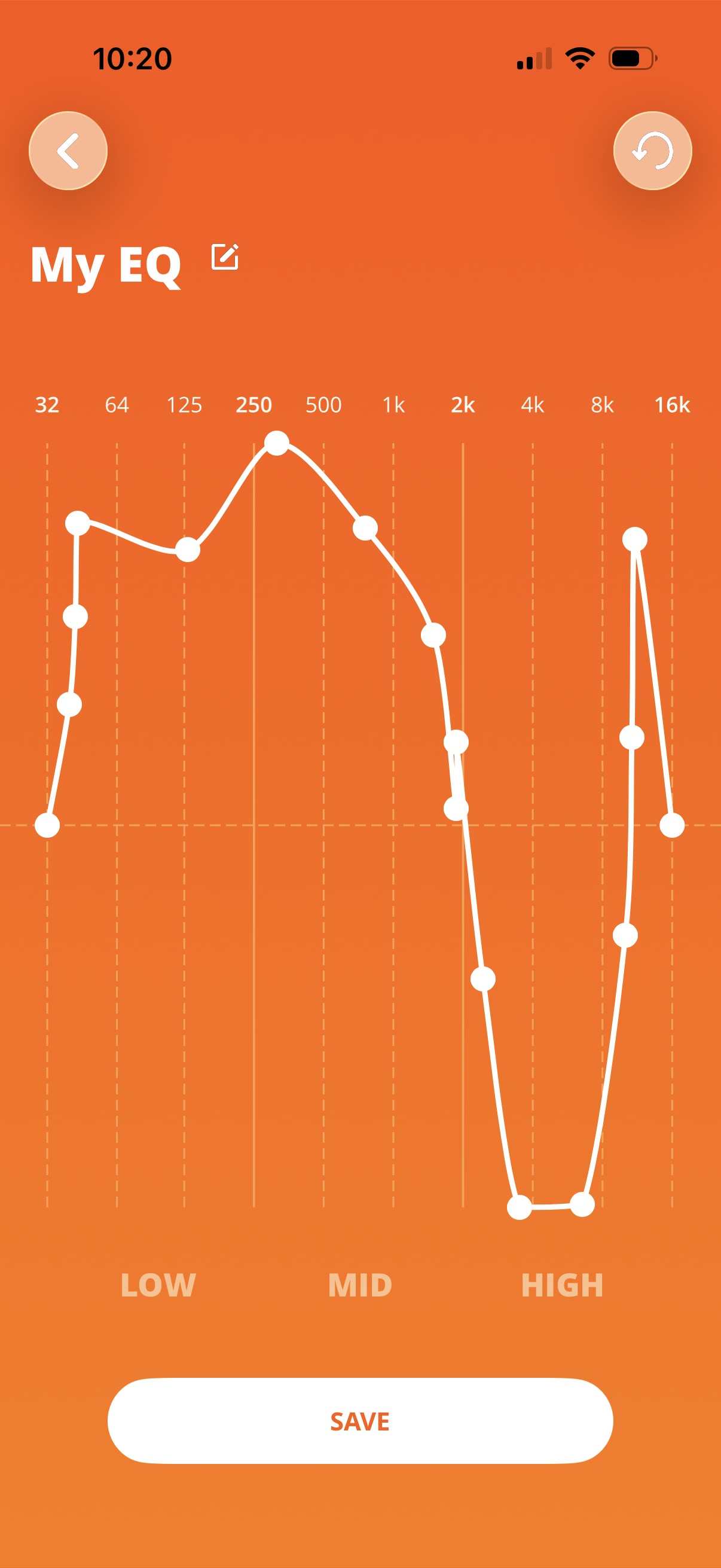

Speaking of EQ, there are six presets available through the included Equalizer function with the ability to add more. More importantly, however, is the fact that I can create a completely custom EQ with a seemingly infinite amount of points (I stopped at 17) where you can boost or cut up to 6 dB.

Spatial sound gets its own set of three presets – Movie, Music, and Game – though there isn’t any more control other than selecting between them. There’s also a left / right balance, and a Low Volume Dynamic EQ setting so that audio still sounds present even when turned down.

I also appreciate the number of settings for better sounding calls, even allowing you to hear your own voice if you want.

Lastly, it also comes with a relax mode that allows you to play any combination of up to five relaxing sounds from one to sixty minutes (selectable along a slider). It’s a nice if slightly gimmicky feature.

Advertisement

JBL Live 780NC: Design

No charging cable included

Comfortable, (if slightly tight) fit

Plenty of on-unit controls

When unboxing the JBL Live 780NC, a couple things popped out to me. I was a little disheartened to see that JBL didn’t include a charging cable, though not too much, since it uses USB-C and anyone with a modern smartphone can use the same cable to charge these headphones. More appreciated was the inclusion of a carrying pouch, albeit a fairly thin one, as well as the USB-C to aux cable for more analog listening.

Mostly though, I liked the fact that the JBL Live 780NC, while not reinventing the wheel, don’t look like every other pair of over-ear wireless headphones out there. Not only do they come in the five different colors mentioned above (my test unit is black), but the earcups have a rounded almost-retro-but-not-quite shape to them that with oversize earpads give it an accessible yet slightly elevated look.

(Image credit: Future / James Holland)

The earpads might not be removable but they are plush as is the headband, while the rest of the Live 780NC are a combination of durable plastic and sturdy metal – most notably the hinge. JBL doesn’t give an exact measurements, but each earcup looks to have an adjustment range of about an inch and a half giving these headphones the flexibility to fit on just about any head. Plus, the earcups can swivel flat as well as fold, which make them easier to carry.

The headphones sit tight on the head without too much pressure for a secure and comfortable fit. And if you try these on and find them too tight, adjusting the ear cups will alleviate the pressure. At 260 grams, they’re not light. But I didn’t find them fatiguing to wear for long listening sessions. Though they’re not really meant for active wear, I even tried them on while going for a run and found them comfortable the entire time.

Advertisement

I also like the fact that cloth covering the 40mm drivers has a sizable “L” and “R” etched into them to indicate sides. I’ve experienced more than one pair of headphones that hide the left and right indicators in some forgotten crevice, making me spend a few extra seconds figuring out the proper headphone orientation (first world problems).

Typically, many wireless headphones have all the controls on one side. That’s not the case with the JBL Live 780NC. The right side does have more on it, containing the power / bluetooth slider and ANC / AmbientAware button along with the USB-C port. You can also tap the outside of the ear cup for various additional controls like play / pause, mic mute, call answer, and voice assistant cycling. The left side is a little more minimal but does have the all important volume controls.

(Image credit: Future / James Holland)

JBL Live 780NC: Sound

Really impressive sound, except for overly pronounced bass

Spatial audio is a treat, if a bit underwhelming

Ridiculously long battery life

Having spent quite some time testing the JBL Live 780NC, listening to all sorts of genres through Apple Music with Dolby Atmos and lossless on (and therefore able to listen to music in Hi-Res and with spatial audio on), I’ve come away quite impressed.

The sound quality here is better than I was expecting it to be considering the more mid-range price tag. Regardless of what I listened to, the mids and high end came through very clearly.

Advertisement

The mids have a good amount of body so rock and more mid-forward music retains its edge, while the high end has the kind of clarity to keep sounds like cymbals coming through with a crispness they deserve.

The one place that the audio quality lines up more closely with my experience of headphones in this price range is the bass. For instance, I’ve never listened to U2 and thought there was too much bass.

(Image credit: Future / James Holland)

That is until I tested these headphones and put on Until The End of the World in an effort to find some kind of rock in Dolby Atmos. I also tested with some hip hop, like Duckwrth and J. Cole, where that big bass worked better, but as soon as I turned on the bass boost EQ preset, it completely overwhelmed the rest of the audio. If you’re a bass head and welcome hearing damage, you might like that.

I did appreciate the ability to play Dolby Atmos through these headphones, though the availability of this content is limited to only a handful of streaming services. Yet, the spatial audio effect is more limited than it is with a physical atmos system. On the bright side, it is more impactful when watching shows or movies (or gaming), giving content a more three dimensional experience.

Advertisement

Still, everything does have more clarity to it with more separation between aural elements like instruments and backing vocals. Part of that is listening in Hi-Res lossless audio but some of it is also the Dolby Atmos since it allows for a bigger sense of space in the soundstage. It is a virtual approximation since these headphones rock just one 40mm driver per side. That said, this is still incredible audio for $250.

Using the headphones for calls is almost as impressive. As the wearer, I was able to hear calls clearly. And due to the dual beamforming mics — there are four mics total — coupled with an AI-trained algorithm, the caller on the other end could hear me just as clearly, stating that they wouldn’t have even known I was speaking through the 780NC if I hadn’t told them.

What probably blows me away the most — at least in terms of how far headphones have come in a few years — is the ridiculously long battery life. A five minute fast charge garners four hours use. And though it takes two hours to fully charge from empty, once charged, the JBL Live 780NC can last up to 80 hours, 50 if you’re always using ANC. I’ve charged these headphones once since I got them and that’s only because they arrived with a 50% battery life out of the box.

(Image credit: Future / James Holland)

Advertisement

JBL Live 780NC: Value

JBL Live 780NC sound better than their price

Similar features in other headphones cost more

Only a few headphones come with better battery life

Aesthetically and design-wise, the JBL Live 780NC look like the mid-tier headphones that they are. But, the amount of features on hand as well as the superb sound quality (as long as you’re okay with a big low end) and impressive battery life feel like they belong in a more expensive pair.

If we look at other wireless headphones out there, the Sony WH-1000XM6 are one of the first ones to pop up on any best of list. While their ANC is probably the best out there (along with Bose’s top options), they also go for a much heftier $449 / £399 / AU$699. They also have a more limited battery life, lasting 30 hours with ANC on. And they’re a bit more limited when it comes to other features. They would get a little bit of a pass regarding the limited features since they’ve been out since 2024, but the prices haven’t really come down much since their release. You might find them at around $400, but not really any less than that outside of a sales event.

You can find some headphones with better battery life like the Cambridge Audio Melomania P100, which provide up to 100 hours of battery life. But those are more expensive, at $299 / £249 (AU$510 approx.), and don’t offer spatial audio support. On top of that, the ANC is not as good on the Cambridge as it is on the JBL.

Should I buy the JBL Live 780NC?

Swipe to scroll horizontally

Beyerdynamic Aventho 300 scorecard

Attributes

Advertisement

Notes

Rating

Features

Just about every feature from ANC to personalized EQ and spatial audio are on hand here.

Advertisement

5/5

Design

The JBL Live 780NC have a comfortable fit and are available in a number of colors. I do wish they came with a charging cable.

4.5/5

Advertisement

Performance

The spatial audio might be too subtle and the bass too big, but make no mistake – these headphones sound very good. Plus, the battery life is amazing.

4.5/5

Value

Advertisement

These headphones punch above their weight when it comes to features, battery life, and sound quality.

4.5/5

Buy them if…

Advertisement

Don’t buy them if…

JBL Live 780NC: Also consider

(Image credit: Future / James Holland)

How I tested the JBL Live 780NC

Tested over a two-week period

Tested with different music as well as video streaming and gaming

Tested the various features

I spent two weeks using the JBL Live 780NC as my daily headphones. While using them, I listened to all sorts of genres from electronic and hip hop to rock and acoustic music to compare the frequency range and soundstage. I also tested them with streaming video, video games, and used the various settings such as ANC, transparency mode, EQ, and multipoint.

I’ve spent the last few years reviewing audio equipment and have spent even longer using my critical ear as a listener and musician to understand what does and doesn’t sound good.

You must be logged in to post a comment Login