Crypto World

Caesars, DraftKings, and the ZunaBet Surge

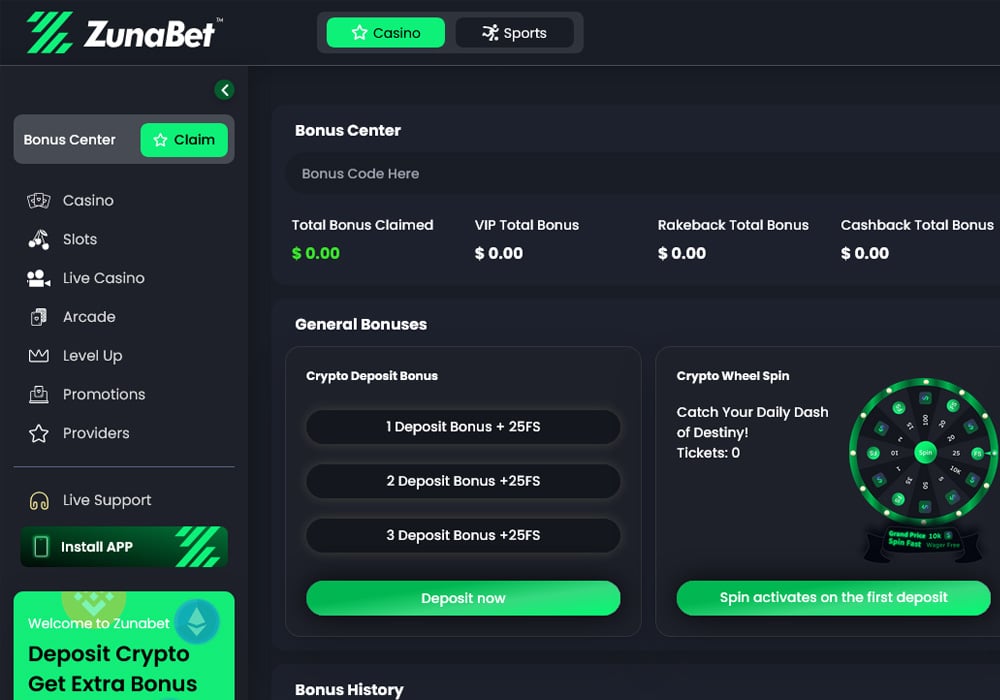

Caesars and DraftKings are two names that show up in nearly every US online betting conversation. Both have spent years building strong recognition through major league deals, polished apps, and nonstop ad spend. But the industry is moving, and a fresh group of crypto-first casinos is starting to win over players who want a quicker, more modern experience. ZunaBet, launched in 2026, is one of the names becoming part of that shift.

Here is how Caesars and DraftKings compare today, and where ZunaBet is starting to make its mark as a different kind of platform.

The Two Big Names in US Betting

Caesars has been part of gambling for decades. The brand built its reputation in physical casinos before moving online through Caesars Palace Online Casino and the Caesars Sportsbook. Everything runs on fiat money, with deposits through cards, bank transfers, and PayPal. The Caesars Rewards program ties online play to perks at Caesars resorts, including hotel stays and dining credits.

DraftKings reached the top another way. It started as a daily fantasy sports site before growing into a full sportsbook and online casino. It is now one of the most familiar names in US sports betting, with sharp mobile apps and partnerships across the major leagues. Like Caesars, it works only in dollars and runs under state-by-state licensing.

Both are reliable picks for players who want a regulated US betting experience. But both also carry the same limits. They only operate in certain states, withdrawals are slower than what crypto sites manage, and their game libraries are smaller compared to global platforms. Their loyalty programs still follow the same tier and points layout that has been around for years.

ZunaBet Joins the Story

ZunaBet is a newer name climbing in player conversations since its 2026 launch. It is owned by Strathvale Group Ltd and operates under an Anjouan gaming license. The biggest gap between ZunaBet and the older brands sits at the foundation. ZunaBet was built around crypto from day one rather than adapted later from a fiat-based system.

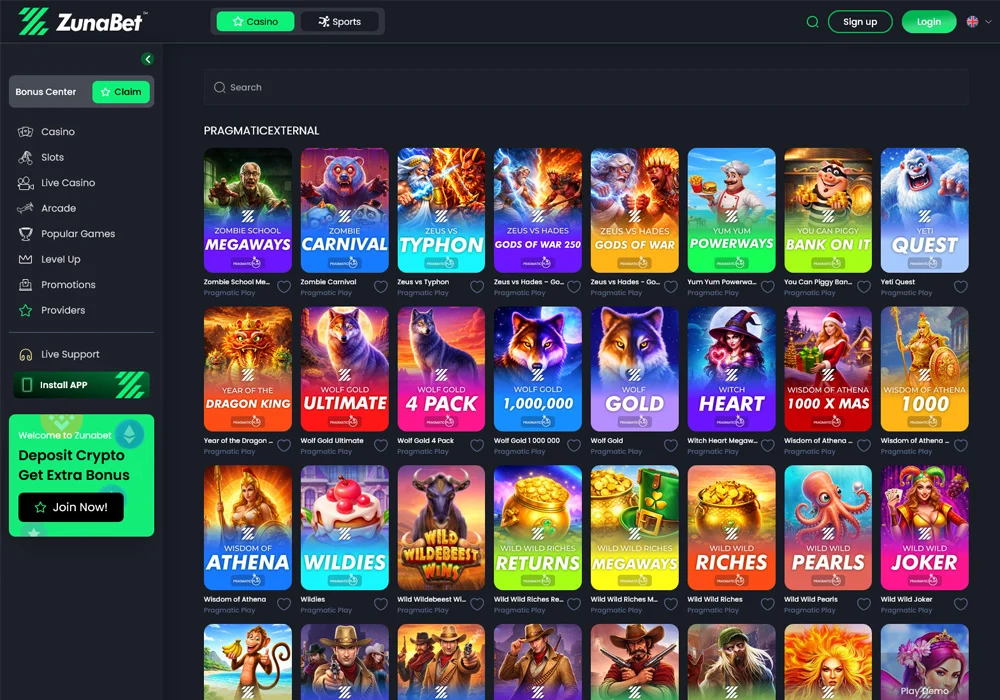

The casino offers more than 11,000 games from over 60 providers, including big studios like Pragmatic Play, Hacksaw Gaming, Yggdrasil, BGaming, and Evolution. That library easily outpaces what most US-licensed casinos can carry. Slots, table games, and live dealer rooms all sit under one account.

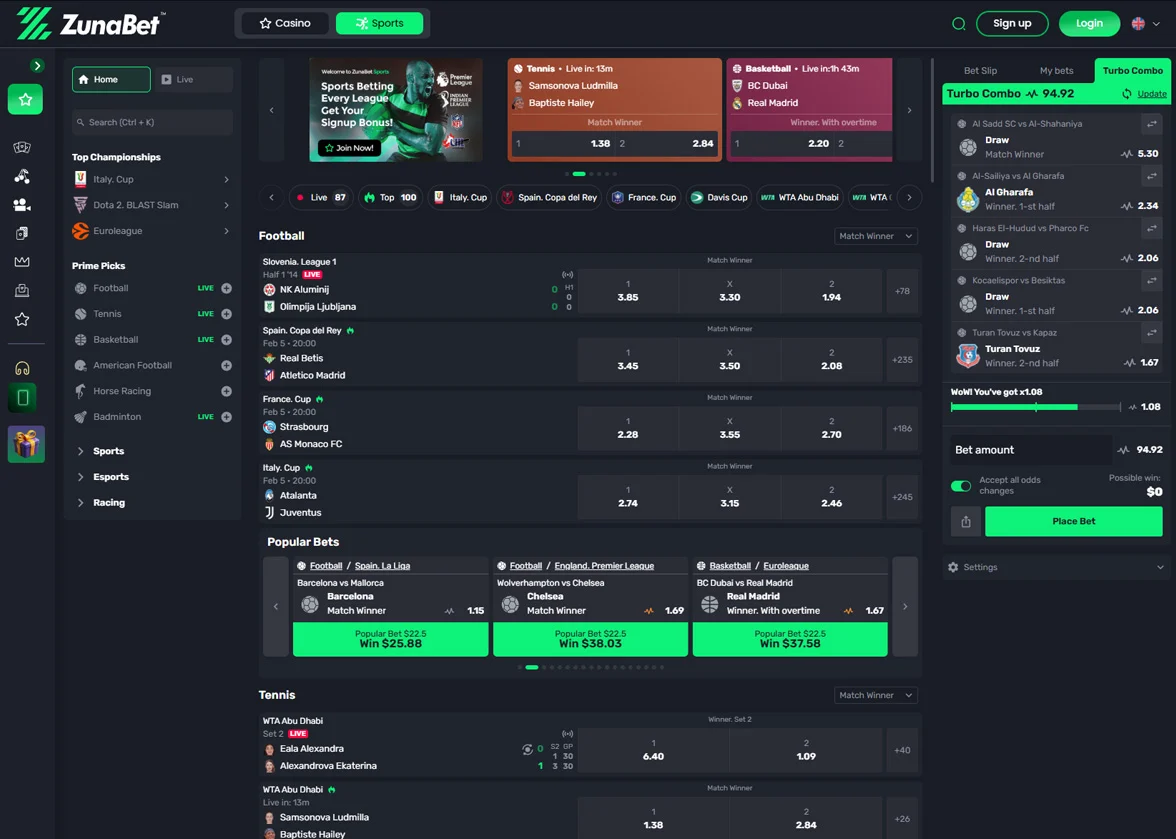

A full sportsbook is part of the package too. It covers football, basketball, tennis, NHL, and the other major sports, alongside esports like CS2, Dota 2, League of Legends, and Valorant. Virtual sports and combat sports finish out the menu. That puts ZunaBet in the same hybrid space as DraftKings, but with broader coverage rolled into one platform.

Crypto vs Traditional Models

This is where ZunaBet really separates from the older brands. Caesars and DraftKings only handle dollars. That means bank processing, possible holds, and slower payouts.

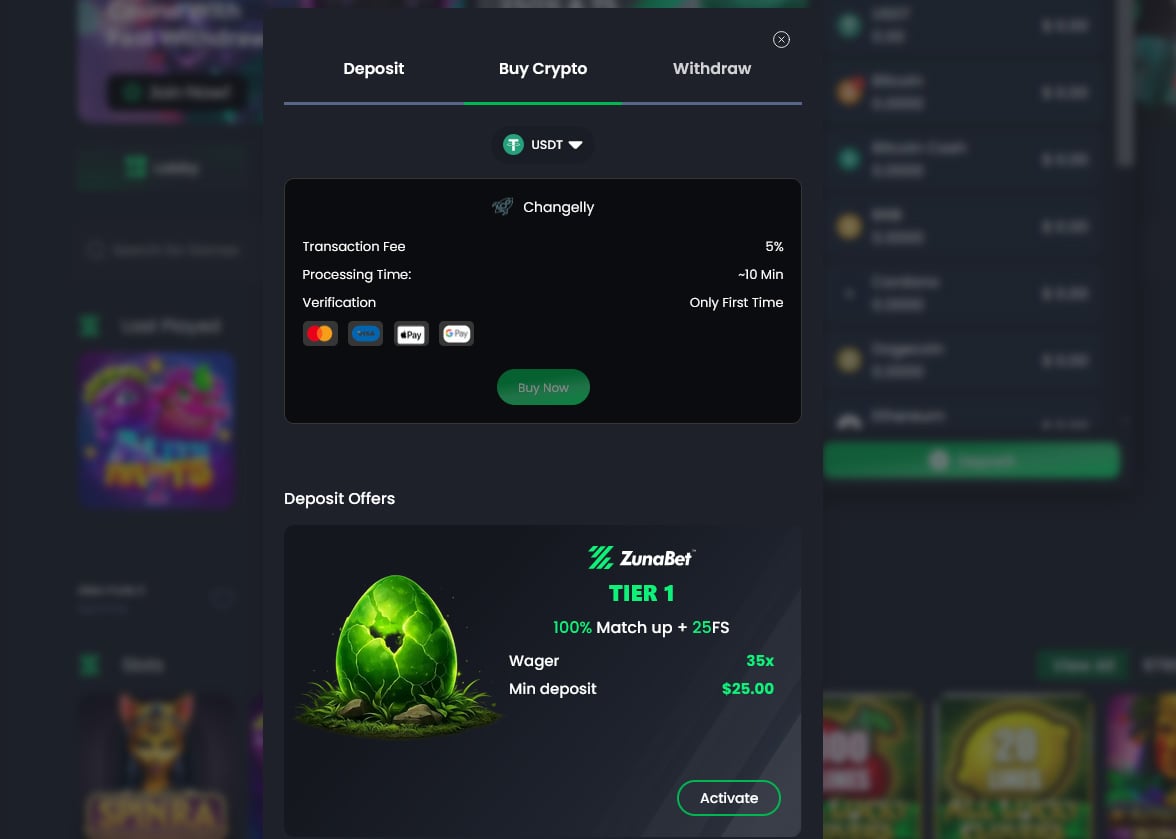

ZunaBet supports more than 20 cryptocurrencies, including Bitcoin, Ethereum, USDT across multiple chains, Solana, Dogecoin, Cardano, and XRP. There are no platform fees on transactions, and withdrawals move quickly. For players who already use crypto or just want quicker and cheaper transfers, the upgrade is clear.

Crypto platforms also tend to operate globally instead of being limited to specific states. Players in many regions can use the full casino and sportsbook without the patchwork rules that come with US brands. For a generation that already spends much of its time in digital, crypto-friendly spaces, that fits how they expect any modern platform to work.

Welcome Offers Side by Side

Caesars and DraftKings both run welcome offers, usually built around a deposit match or a risk-free first bet. The exact terms shift by state, and wagering rules can be strict.

ZunaBet offers a welcome package worth up to $5,000 plus 75 free spins, spread across three deposits. The first deposit gets a 100% match up to $2,000 plus 25 spins. The second adds a 50% match up to $1,500 plus 25 spins. The third gives another 100% match up to $1,500 plus 25 spins. Marketed as a 250% bonus over three deposits, it gives new players more chances to explore the platform than a one-shot offer would.

Loyalty Programs Compared

Caesars Rewards is one of the most established loyalty programs in gambling. The link to physical resort perks is a strong draw for players who visit Vegas or Atlantic City. DraftKings Dynasty Rewards lets players earn points to swap for bonuses, free bets, and event access.

Both work, but both follow the same loyalty card formula the industry has used for decades. ZunaBet takes a different approach. Its program runs on a dragon evolution theme with a mascot called Zuno. There are six tiers: Squire at 1% rakeback, Warden at 2%, Champion at 4%, Divine at 5%, Knight at 10%, and Ultimate at 20% rakeback at the top.

Players also pick up tier-based free spins up to 1,000 spins, VIP club access, and double wheel spins as they climb. The whole setup feels closer to leveling up in a game than swiping a points card. For players who enjoy that kind of system, it lands harder than a standard VIP program.

Why ZunaBet Is Worth a Closer Look

Caesars and DraftKings still make sense for players who want a familiar, regulated US betting experience. Both brands are strong, and neither is going to lose its place. But what players want from these sites is changing fast. Quick payouts, deeper libraries, and more engaging rewards are turning into baseline expectations rather than nice extras.

ZunaBet is built around that baseline. The crypto-first foundation means fast payments and low fees. The game library outpaces what most established brands carry. The sportsbook covers traditional sports and esports together. The dragon loyalty program turns regular play into a journey with clear rewards at every step.

For players who want speed, variety, and a more modern feel, ZunaBet is one of the most exciting options on the market right now. It is still an emerging platform, but the direction is clear. A new generation of players expects crypto support, gamified rewards, and global access as standard features, not extras layered on top.

Caesars and DraftKings shaped what online betting looks like today. ZunaBet is one of the platforms shaping what comes next.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

A Japanese corporate pension fund that serves roughly 1,200 small and mid-sized businesses plans to earmark about 1% of its assets to cryptocurrency for fiscal year 2026, according to Nikkei.

The Nationwide Business Corporate Pension Fund, based in Okayama, reportedly intends to gain crypto exposure through a passive investment vehicle managed by a major hedge fund that holds multiple crypto assets. The pension fund manages about 21.3 billion yen (approximately $130 million), per the report.

Key takeaways

- The Nationwide Business Corporate Pension Fund plans an allocation of roughly 1% of assets to cryptocurrency for fiscal year 2026.

- Exposure would reportedly be obtained via a passive fund managed by a large hedge fund holding multiple digital assets.

- CoinPost reports the fund’s broader currency mix is 80% yen, 15% US dollars, and 5% other currencies.

- The pension allocation aligns with Japan’s broader push to bring crypto under a regulatory framework closer to traditional financial products.

Japan’s pension sector begins testing crypto exposure

According to CoinPost, the pension fund’s move is part of an effort to diversify its portfolio risk, with crypto added as one potential asset class alongside fiat currencies. While the planned allocation is relatively small, it is notable given the conservative profile typically associated with corporate retirement vehicles—especially in a market where most crypto access has historically been concentrated among retail investors and speculative trading venues.

The proposed approach also matters for how pension funds manage risk. Rather than selecting individual tokens or running active strategies internally, the plan points to a passive fund wrapper—something that could make governance, rebalancing, and operational oversight easier for institutions that are not structured around crypto trading.

Regulatory changes could make allocations easier to justify

The pension development arrives as Japan advances legislation intended to align crypto with mainstream securities rules. On June 11, Japan’s House of Representatives passed a bill that would bring crypto assets under the Financial Instruments and Exchange Act, subjecting them to a regulatory regime more similar to that applied to conventional financial products.

The legislation is expected to move forward to the House of Councilors. If adopted as anticipated, the path would likely clarify the compliance landscape for exchanges and intermediaries—an issue that becomes critical for institutions considering custodial arrangements, fund structures, and investor protections.

The bill has also been discussed in the context of tax reforms. The reporting notes the potential for a shift toward a 20% flat tax on digital-asset gains from the current maximum of 55%. Any change in the tax burden can alter the incentive structure for long-term participation and may make institutional and wealth-manager participation more predictable.

Broader institutional momentum: from banks to listed crypto players

Crypto’s institutional footprint in Japan is expanding on multiple fronts, suggesting the pension allocation is part of a wider trend rather than an isolated decision.

Earlier, SBI Shinsei Bank reportedly began testing a deposit-linked rewards program that issues vouchers redeemable for Bitcoin, Ether, or XRP, ahead of a planned permanent launch this autumn. While vouchers are not the same as a direct pension allocation, the mechanism reflects growing comfort among regulated financial institutions with distributing crypto-linked value to customers.

In parallel, Metaplanet—described as Japan’s largest publicly listed Bitcoin holder—agreed to acquire Siiibo Securities for 2.1 billion yen on June 12. The company said the acquisition is intended to support the development and distribution of Bitcoin-linked yield products through a newly formed securities arm. The move underscores how public crypto holdings are pushing into regulated product pipelines rather than remaining purely as treasury investments.

What investors should watch next

For markets, the key question is whether Japan’s legislative and product-building momentum translates into broader institutional allocations beyond pilots and small percentages. The pension plan is small relative to the fund’s total holdings, but it could be influential if other conservative retirement investors observe the framework and decide the operational and regulatory risks are manageable. Readers should watch the House of Councilors process for the crypto bill and any further detail on the pension fund’s crypto passive vehicle—particularly how it will handle custodial controls, valuation, and rebalancing once fiscal year 2026 approaches.

Polymarket paid mostly college-age creators to stage fake winning bets on copycat versions of its website. A Wall Street Journal investigation found none of the roughly $1.9 million in bets shown across 1,105 videos were real.

The findings run counter to the company’s core pitch. Polymarket settles every real trade on a public blockchain that anyone can audit. Its growth campaign relied on the opposite, staged trades on fake sites that no ledger could verify.

How Polymarket’s Alleged Fake Bets Worked

Real Polymarket trades run on the Polygon blockchain and settle in USDC. Markets resolve through UMA’s permissionless oracle, where anyone can propose or dispute an outcome by posting a $750 bond. Every position is public.

The marketing operation lived entirely off that ledger. The Journal reportedly reviewed 1,105 videos from 10 promoted creators between December and mid-May. Around 70% showed a bet, and none were genuine.

One video showed a creator winning $100,000 after Trump appeared to say the word McDonald’s in January. Trump never said it publicly that month, and the clip was older.

On the real market, public data shows more than 50 accounts made that bet, and all lost.

Many clips were filmed on dummy sites such as poiymarket.com, built to mirror the real platform. Across 118 videos, creators celebrated roughly $900,000 in fabricated wins. The same bets would have lost more than $166,000.

Creators earned about $2,000 to $3,000 a month and were told not to disclose the payments. A hired marketing firm then pushed the clips past 140 million views. The pattern echoes an earlier market resolution dispute that dented user trust.

Scandal Hits During Polymarket’s US Comeback

The timing is awkward. US regulators fined Polymarket $1.4 million in 2022 for running an unregistered market and ordered the winding down of non-compliant trades.

The company later reincorporated in Panama, with its headquarters reportedly a shared law office that also worked with FTX.

Polymarket has since won a regulated US market entry and now wants to bring its exchange onshore.

The fake campaign specifically targeted American users, who can still reach the offshore site through a VPN.

Trust questions are not new. A separate Journal analysis found most users lose money, even as the videos sold easy profit.

Now competing with regulated rival Kalshi, Polymarket said it will audit its promotional content.

That review, which is changing how regulators view its onshore push, may shape the next phase of the prediction market race.

The post Polymarket Accused of Using Fake Winning Bets to Fuel Viral Growth appeared first on BeInCrypto.

Key Takeaways

- Data center operations now represent AMD’s primary revenue catalyst, powered by EPYC server chips and Instinct AI accelerators

- Market share gains don’t require overtaking Nvidia — capturing a significant portion of explosive AI chip demand is sufficient

- Conservative 2031 projection points to approximately $704, while optimistic scenarios exceed $1,500

- Analyst sentiment remains constructive: 30 Buy recommendations, 12 Hold, 1 Sell — overall Moderate Buy rating

- Current trading levels exceed consensus price targets, suggesting near-term valuation concerns following recent gains

Advanced Micro Devices has emerged as a critical player in the artificial intelligence infrastructure expansion.

The firm’s first-quarter 2026 financial report illustrated this strategic shift unmistakably. Revenues climbed substantially, fueled by robust appetite for EPYC data center processors and Instinct GPU accelerators. The data center segment has displaced gaming and consumer processors as the company’s dominant growth driver.

Shares currently change hands near $537. This valuation reflects significant optimism already embedded in the market price.

Advanced Micro Devices, Inc., AMD

The optimistic investment thesis hinges on three critical factors. Cloud hyperscalers increasingly prioritize vendor diversification for AI silicon. AMD has established substantial positioning in server processors following years of systematically capturing territory from Intel. The company’s AI accelerator development timeline positions it as a viable alternative computing platform.

Nvidia maintains commanding leadership in AI acceleration hardware. However, AMD’s success doesn’t require outright victory in this competition. Even a substantial minority position in an explosively expanding market translates to dramatically increased business scale.

Three Potential Trajectories Through 2031

Financial analysts have constructed three distinct scenarios for AMD’s evolution over the next seven years.

Under pessimistic assumptions, AMD expands but struggles to secure adequate AI accelerator adoption. Revenues might approach $70 billion, yet margin compression limits profitability. Applying a 25x earnings multiple yields a stock price near $200.

The middle-ground projection presents more favorable conditions. AMD sustains data center penetration, expands Instinct GPU deployment, and achieves margin improvement. Revenue could reach $120 billion with earnings per share around $22. A 32x valuation multiple supports a price target of approximately $704.

The optimistic scenario envisions transformational success. Should AMD establish itself as the definitive second AI chip platform while simultaneously expanding CPU and enterprise computing presence, revenues might hit $180 billion. With EPS at $40 and a premium valuation, shares could trade beyond $1,500.

Weighting these scenarios by probability generates a blended target near $807 — representing roughly 50% appreciation from current levels, or approximately 8.5% annualized returns.

Current Wall Street Perspective

The analyst community maintains generally favorable views, albeit with important caveats.

AMD presently carries 1 Strong Buy, 30 Buy ratings, 12 Holds, and 1 Sell, per MarketBeat data. The aggregate rating stands at Moderate Buy.

The complication: average analyst price targets fall below AMD’s current market price. This gap suggests analysts appreciate the business fundamentals while believing the stock has outpaced near-term justification following its recent advance.

The Road Ahead for AMD

AMD’s EPYC processor family has systematically captured CPU market share from Intel over consecutive quarters. This provides the company with established data center relationships independent of Instinct GPU revenue contributions.

Executive guidance has previously outlined expectations for sustained multi-year expansion, anchored by data center growth. These projections form the foundation for 2031 valuation models.

For AMD to generate meaningful market outperformance from current levels, execution closer to the bullish scenario appears necessary. The base-case trajectory delivers returns roughly aligned with broader equity market expectations — respectable, but below the outsized gains growth-oriented investors typically seek.

First-quarter 2026 data center revenue established a new company record for quarterly performance.

XRP price traded near $1.14 on June 21, with the token still locked in a narrow range after failing to clear $1.20.

Summary

- XRP price traded near $1.14 as buyers defended the key $1.10 support zone after weak volume.

- Ripple adoption keeps growing through RLUSD, MXNB, Mastercard settlement links and AI payment tools.

- ETF inflows and low exchange reserves support the rebound case, but whale selling remains under pressure.

According to crypto.news data, XRP showed a 24-hour move of -0.34%, with price action between $1.13 and $1.15.

The token stayed almost flat over seven days but remained down more than 16% over 30 days. Trading volume stood near $872 million, while market value held around $70.97 billion, keeping XRP in sixth place among crypto assets.

The setup remains simple. Bulls need to protect $1.10, while a close above $1.20 would give the market a reason to revisit $1.25 and $1.30.

XRP price stays locked inside a tight range

Last week’s range view has held. XRP buyers pushed toward $1.20, but they did not secure a breakout with strong volume. Sellers also failed to break the $1.10 floor, keeping the token inside the same band.

That makes $1.10 the first level to watch. A clean move below that area could expose $1.05 and then the $1.00 zone.

The upside path also remains clear. XRP needs volume above $1.20 before bulls can target $1.25 and $1.30. Without that confirmation, the move looks more like consolidation than a new trend.

This range still matters. Long periods of flat trading often build pressure, but direction still depends on who wins the range. A breakout without volume would carry less weight than a close backed by stronger spot demand.

Ripple adoption supports the long-term case

Ripple’s ecosystem news gave bulls a stronger utility argument even as price stayed weak. The company has pushed RLUSD into more payment channels and recently backed Flutterwave’s Series E round to support stablecoin adoption in African payments.

Ripple also worked with Bitso on MXNB, a Mexican peso stablecoin on the XRP Ledger. Ripple is expanding RLUSD through Mastercard’s stablecoin settlement network and MXNB-powered cross-border payment infrastructure.

The XRP Ledger also moved deeper into automated payments. Crypto.news reported that Ripple launched the XRPL AI Starter Kit, allowing AI agents to use XRP and RLUSD for payments through the x402 protocol.

This does not guarantee higher prices. It does show that XRP’s utility story is moving beyond retail trading and into payments, stablecoins, settlement and machine-to-machine transfers.

CLARITY Act and reserves shape the catalyst

Regulation remains a key part of the XRP price analysis. As crypto.news reported, the CLARITY Act has cleared committee and now needs Senate votes, with the 60-vote threshold still ahead.

The bill matters for XRP because it could give institutions clearer rules for digital commodities and tokenized settlement. XRP is already being used in tokenized Treasury settlement pilots, but larger adoption still depends on legal certainty.

Supply data adds another layer. Crypto.news reported that XRP exchange reserves fell to a seven-year low near 1.6 billion tokens, down about 50% from October 2025. Low exchange supply can make price more sensitive when demand arrives.

Fund flows are another support point. According to SoSoValue data, XRP-linked products recorded about $10.66 million in weekly net inflows for the week ending June 18, close to $10.68 million in the prior week. Cumulative net inflows rose to about $1.45 billion, while total net assets moved closer to $1 billion.

Still, whale activity keeps risk on the table. As previously reported, whales had distributed more than 30 million XRP in five days, while network activity weakened.

Analysts watch $1.10 and $1.20

Technical analysts remain split. EGRAG CRYPTO described the two-month XRP chart as “E is the battlefield,” pointing to a structure that could support a future breakout if buyers defend the current zone.

The analyst listed much higher cycle targets, including $9.50 to $17.23, with $13 as a main focus. Those targets remain speculative while XRP trades near $1.14 and below the $1.20 breakout area.

For now, the market does not need targets to define the next move. XRP needs to hold $1.10, reclaim $1.20 and then show stronger volume. A failure at $1.10 would keep sellers in control.

ETF flows, lower exchange reserves and Ripple adoption support the rebound case. Whale selling, weak activity and a stalled breakout support the cautious case. XRP is still waiting for a clean trigger.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

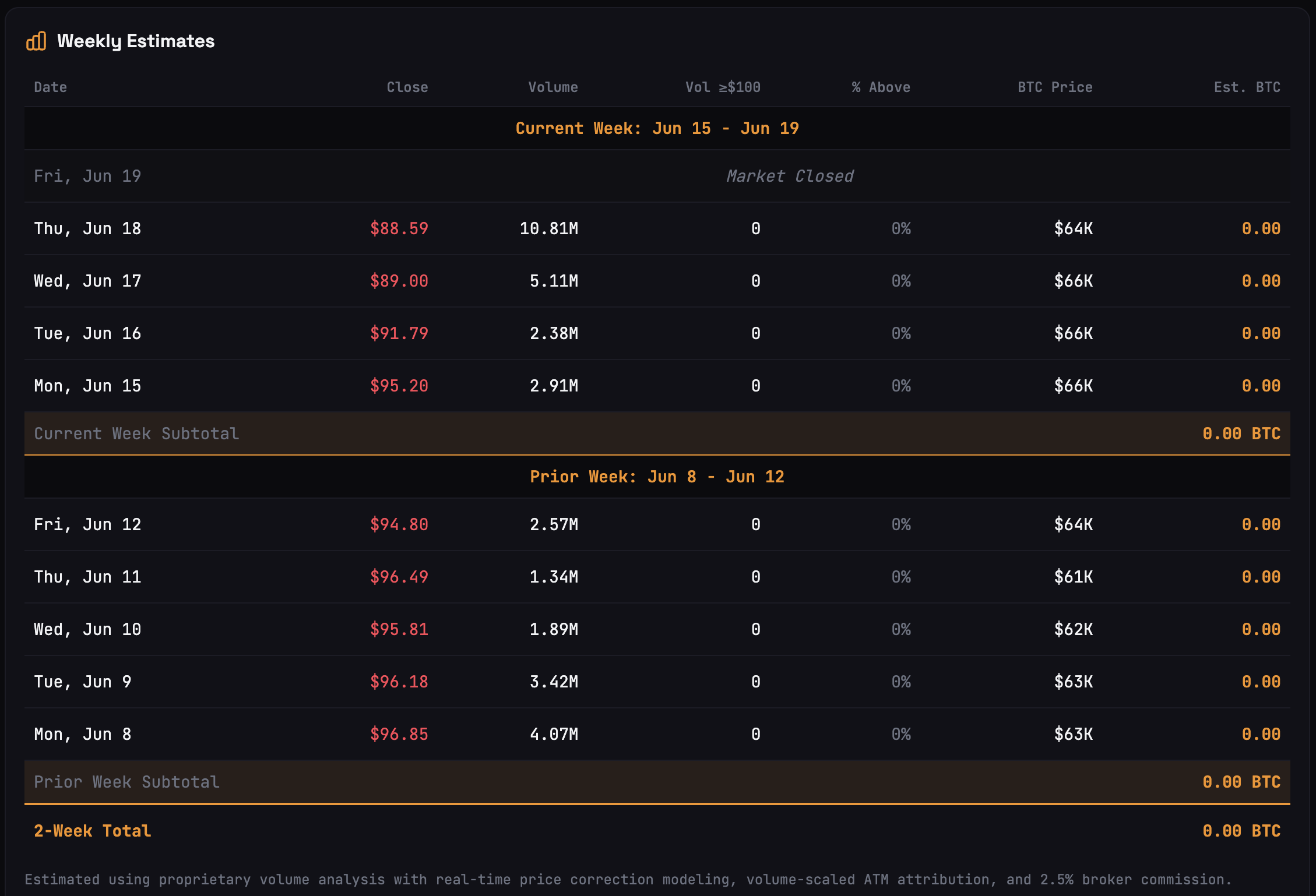

Bitcoin (BTC) has fallen roughly 50% since Michael Saylor’s Strategy launched Stretch (STRC), its flagship Bitcoin-funding vehicle, in late July 2025.

BTC/USD monthly chart. Source: TradingView

Key takeaways:

- STRC is acting like a classic Ponzi scheme, argue Peter Schiff and other critics.

- Other analysts disagree, noting that STRC’s drop below the $100 par is due to a leverage wipeout.

Critics say STRC looks like a “classic centralized Ponzi”

STRC was designed to trade near its $100 par value, enabling Strategy to raise capital to buy more Bitcoin. The instrument is now trading at a deep discount, suggesting that the BTC buying channel is under pressure.

On Thursday, STRC fell to a record low of $82.53 before closing at $88.59, still below the $100 par value.

STRC daily chart. Source: TradingView

Launched in July 2025, STRC was designed to trade near par through adjustable dividends, currently 11.5% annualized, with proceeds used primarily to acquire Bitcoin.

The widening discount has pushed STRC’s effective yield above 12.9% and contributed to a pause in at-the-market share issuance. That risks slowing down the capital-raising flywheel behind Strategy’s Bitcoin treasury, which now holds more than 846,000 BTC.

In finance, a “flywheel” is a self-reinforcing business model where growth in one metric directly helps grow another, compounding momentum.

But trading 13% below par has revived criticism of Strategy’s funding model.

Bitcoin critic Peter Schiff has repeatedly described STRC as “a classic centralized Ponzi,” arguing that it depends on Strategy’s ability to raise fresh capital through new share sales or sell Bitcoin to meet obligations.

Source: X/Peter Schiff

Crypto trader DonAlt also questioned STRC’s recent price action, asking why the instrument was “trading like a Ponzi” after its sharp move below par.

Strategy has not directly addressed this in recent statements, instead continuing to present STRC as preferred equity supported by its Bitcoin-focused treasury strategy.

However, the company has moved STRC to a semi-monthly dividend schedule, with payouts now designed to occur twice a month rather than monthly.

Strategy’s Bitcoin buying pace slows as STRC slumps

The pace of Strategy’s Bitcoin accumulation has slowed sharply as STRC trades below par value.

The company added 1,550 BTC for $101 million in the week ending June 8 and another 1,587 BTC for $100 million in the week ending June 15, lifting total holdings to 846,842 BTC.

Those were meaningful purchases, but they were far smaller than Strategy’s weekly buys earlier in 2026.

For instance, in April, Strategy bought 34,164 BTC for $2.54 billion in a single week. In May, it added another 24,869 BTC for roughly $2.01 billion. By contrast, June’s weekly additions have been closer to $100 million each.

The slowdown also coincided with a small but notable 32 BTC sale earlier in June, worth about $2.5 million, to help cover dividend obligations.

Related: Bitcoin price sets $64.5K week-to-date low as Strategy selling worries return

The sale was tiny compared with Strategy’s overall Bitcoin treasury, but it showed that cash obligations can still force limited BTC sales when STRC-led funding becomes less efficient.

STRC-led weekly BTC buying estimates. Source: STRC.LIVE

Analyst says STRC drop is a leverage wipeout

The STRC sell-off looked more like a leverage wipeout than a deterioration in Strategy’s fundamentals, according to Jesse Myers, head of Bitcoin strategy at The Smarter Web Company.

“Strategy is fine,” he said in a Thursday post, adding that the company could pay STRC dividends for 32 years if conditions remain unchanged, and indefinitely if Bitcoin appreciates at roughly 2% annually.

STRC’s long stretch near $99–$100 encouraged investors to use heavy leverage, with some assuming the instrument would stay above $95. Once the price slipped, margin calls and forced selling accelerated the decline.

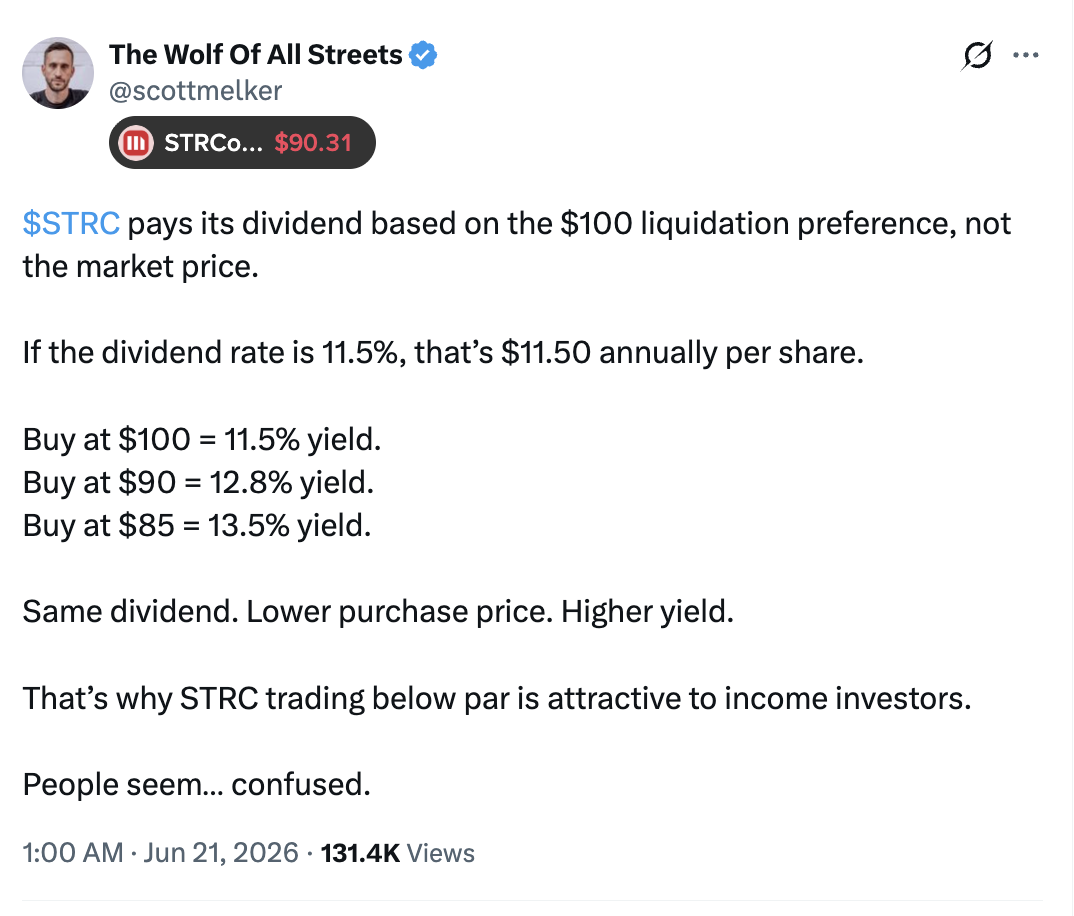

The discount may also attract income buyers, according to analyst Scott Melker.

In a Sunday post, he noted that STRC’s dividends are based on the $100 liquidation preference, not the market price. At an 11.5% dividend rate, buyers at $90 earn about 12.8%, while buyers at $85 earn roughly 13.5%.

Source: X/Scott Melker

At current prices, STRC offers an effective yield of about 13%. Strategy may announce its next dividend rate on June 30, while retaining other options, including MSTR share issuance and cash reserves, to fund its Bitcoin purchases.

Bitcoin can survive another price crash as it has done so many times in the past, reassured the CEO of CryptoQuant, Ki Young Ju.

However, he envisions another major threat for the asset – boredom, and he linked it to Strategy’s STRC shares, which have raised some eyebrows in the past few weeks.

Boredom, Not a Crash

If you have followed the cryptocurrency industry for a few (or more) years, you are probably aware of its intense volatility at times. Bitcoin has been the object of some mind-blowing fluctuations, up or down. Of course, the skyrocketing liquidations on the way down are usually the ones people read about, and don’t get me wrong, there have been plenty of instances in which the asset has tumbled by double digits daily. However, it has also risen in the opposite direction violently before.

Naturally, the current market state and the past several months, starting with the early October massacre, the February calamity, and the June crash, are examples of bear-dominated trends. Nevertheless, BTC has managed to withstand all of those and has (for now) returned stronger than before.

Consequently, CryptoQuant’s chief exec didn’t seem too bothered about the potential of another crash. However, he believes boredom could pose a more profound threat, especially if Strategy’s controversial Stretch (STRC) fails to operate as intended.

“Strategy’s STRC structure becomes truly dangerous not when Bitcoin simply crashes, but when Bitcoin spends years moving sideways, and the bear market drags on.”

He added that “long stagnation kills the story,” as BTC can survive another crash if the market still believes in the next leg up. However, weak demand due to stagnation leads to compressed MSTR premium and makes “Saylor’s capital-raising machine much harder to sustain.”

A Reason to Believe

Young Ju further explained that the real challenge for Saylor and his company is not just to keep buying bitcoin, but to give the market “a new reason to believe.”

“After nearly a decade in this industry, I’ve realized Bitcoin’s core has not really changed. What changes every cycle is the story around why BTC price should keep going up. But, most of those stories now feel exhausted.”

He warned that BTC failed to serve as digital gold when it was needed, as it traded like a tech stock. It was supposed to be freedom money built by cypherpunks, but many OGs are now shilling other coins. It also faces the rising threat of advanced quantum computing.

Although he remains a firm believer that “the pool of capital that could flow into Bitcoin is massive,” he noted that the “sense of an inevitable catalyst feels much weaker” now compared to 10 years ago.

“It makes me a little sad to see the ideas that originally pulled me in gradually get consumed and diluted: freedom money, energy money, and institutional adoption.”

The post Bitcoin’s Biggest Risk Is Boredom, Not Another Price Crash: CryptoQuant CEO appeared first on CryptoPotato.

TLDR

- The XRP Ledger’s core server software xrpld v3.2.0 launched June 15, targeting 30–40% memory optimization

- Node operators and developers identified several technical issues via GitHub shortly after deployment

- A node operator experienced complete sync failure post-upgrade despite previous version stability

- Reported issues encompass configuration parsing problems, transaction relay defects, and validator data distribution gaps

- Adoption remains at 26% network-wide; no critical network failures documented

Following the June 15 deployment of xrpld version 3.2.0, the XRP Ledger development community has documented numerous technical issues with the network’s updated core server infrastructure.

The software update promised notable enhancements including performance optimization and a projected 30% to 40% decrease in memory consumption. The release also transitioned the server nomenclature from “rippled” to “xrpld” while incorporating enhanced security protocols.

Yet, shortly following the launch, node administrators and software engineers started documenting problems through the official GitHub issue tracker.

Synchronization Problems and Configuration Glitches

A node administrator documented that their infrastructure running v3.2.0 completely failed to retrieve ledger information following the update. The system maintained connection status but synchronization ceased entirely. Notably, identical hardware performed flawlessly under version 3.1.3. This issue, submitted June 18, awaits resolution.

Another documented problem reveals that configuration files containing inline comments trigger server crashes during initialization. The legacy parsing system fails to properly handle comments in specific parameters, generating a “BadLexicalCast” exception.

Project maintainers have validated multiple reports as legitimate defects requiring technical assessment.

Relay and Validator Network Concerns

Engineers identified a defect affecting transaction propagation mechanisms to network peers. A computational error restricts the number of peers receiving transaction broadcasts, potentially causing insufficient network distribution.

The resource fee tracking mechanism also drew scrutiny. The current implementation only preserves the maximum fee value while discarding previous entries, behavior developers classify as erroneous.

Validator list propagation presented another challenge. Currently, validator metadata transmits exclusively to inbound peer connections while excluding outbound links. This asymmetry affects validator information distribution throughout the network infrastructure.

Developers identified potential unsigned integer overflow vulnerabilities during ledger sequence validation processes. Additional reports highlighted inconsistent transaction routing parameters and compromised node identification when utilizing ephemeral cryptographic keys.

A further report outlined a logical deficiency in ledger state tracking that can strand nodes in undefined states without established recovery procedures.

Current Status Assessment

Presently, none of the documented defects have triggered network-wide service disruptions. The XRP Ledger Foundation alongside open-source development contributors continue examining all submitted reports via the project’s GitHub platform.

Network adoption of version 3.2.0 currently stands at 26%. The substantial majority of nodes continue operating on previous software releases.

The XRP Ledger Foundation has not released official communications or remediation patches at publication time. All identified issues remain under ongoing technical evaluation.

Key Takeaways

- Scaramucci anticipates Bitcoin will begin its upward momentum in Q4 2026 through early 2027

- He dismisses concerns about Michael Saylor and Strategy, calling them financially secure

- Strategy maintains approximately $52 billion in Bitcoin holdings plus $1 billion cash reserves

- Declining retail interest and reduced Google search activity represent bullish indicators in his view

- ETF capital flows and institutional accumulation have created a less volatile cycle compared to previous periods

Anthony Scaramucci, founder of SkyBridge Capital, told CNBC that Bitcoin remains aligned with its traditional four-year market cycle. He anticipates an upward price movement commencing in late 2026 and extending into the first quarter of 2027.

According to Scaramucci, the current market cycle has exhibited less volatility than previous iterations. Bitcoin experienced approximately 50% retracement from peak levels, significantly less than the 60–70% corrections observed in earlier cycles. He attributes this moderation to sustained ETF capital inflows and growing institutional participation.

“I think Bitcoin starts to rally late in the fourth quarter of 2026 into early 2027,” he said.

Scaramucci identified diminishing market attention as an encouraging development. Search volume for Bitcoin on Google has declined substantially, and retail investor enthusiasm has waned. He characterized this apathy as a pattern that typically emerges near cycle lows rather than market peaks.

He emphasized that Bitcoin’s market remains comparatively modest in size. Consequently, even limited fresh capital entering the market can generate substantial price appreciation. Scaramucci disclosed that he maintains significant personal Bitcoin exposure.

“I still like it. I own a lot of it,” he said.

Strategy’s Position Draws Support From Scaramucci

Scaramucci dismissed criticisms surrounding Strategy’s substantial Bitcoin position. He highlighted Michael Saylor’s access to robust capital markets and a solid financial foundation.

“You have to really understand the mechanisms of the balance sheet to understand that Bitcoin can go a lot lower, and he’s virtually not in trouble,” he said.

Strategy’s Bitcoin treasury stands at approximately $52 billion in current value. This reserve provides coverage for 31 months of dividend payments and interest commitments. The firm additionally maintains $1 billion in liquid cash reserves.

No significant debt obligations come due before 2028. Saylor has stated publicly that Strategy can continue servicing its preferred stock dividends and enhancing shareholder returns as long as Bitcoin appreciates by a minimum of 1.25% annually.

Scaramucci observed that Strategy’s equity continues trading at a premium relative to its underlying Bitcoin reserves. He suggested this premium provides investors with “necessary arbitrage” opportunities that justify the investment thesis.

“I like him. I think he’s going to be right,” Scaramucci said of Saylor.

He further mentioned that recent geopolitical developments and declining energy costs could suppress inflationary pressures. Should this scenario materialize, the Federal Reserve might implement interest rate reductions, potentially benefiting Bitcoin and broader risk assets.

Drawing on nearly four decades of investment experience, Scaramucci characterized the present market conditions as a late-cycle deceleration rather than the conclusion of Bitcoin’s long-term appreciation trajectory.

Quick Summary

- Total net revenue for 2025 reached $4.5B at Robinhood, representing a 52% annual increase

- First quarter 2026 brought $1.07B in revenue (up 15%), while Gold membership reached 4.3 million users

- Wall Street’s consensus 12-month target averages approximately $112, marginally exceeding today’s ~$108 trading level

- Projections for 2031 suggest a baseline target near $148, with optimistic scenarios approaching ~$293

- Probability-weighted analysis indicates a 2031 price around $156, representing potential gains of ~44% from present values

Robinhood (HOOD) stock currently hovers around the $108 mark, prompting investors to question its trajectory over the coming half-decade.

The trading platform delivered $4.5 billion in consolidated net revenue throughout 2025, marking a substantial 52% year-over-year expansion. Profitability metrics showed strength as well, with net income totaling $1.9 billion while adjusted EBITDA surged 76% to reach $2.5 billion.

Momentum carried into the first quarter of 2026. Robinhood generated $1.07 billion in quarterly revenue, reflecting 15% growth compared to the same period a year earlier. Earnings per share on a diluted basis landed at $0.38, representing a 3% improvement. The premium Gold subscription service expanded its user base by 36%, hitting an all-time high of 4.3 million subscribers.

Operational metrics from May painted an even stronger picture. The platform’s funded customer count climbed to 27.7 million, while aggregate platform assets swelled to $377 billion—a 48% year-over-year jump. During Q1 alone, net deposits totaled $17.7 billion.

The company has evolved significantly beyond its original retail equity trading roots. Today, Robinhood encompasses options trading, cryptocurrency transactions, retirement planning tools, banking services, credit card offerings, prediction market participation, and access to private market opportunities.

Exploring Three Distinct Price Scenarios

Three potential pathways illustrate where HOOD shares might trade by 2031.

Under a bearish scenario, annual revenue reaches approximately $6.5 billion, but compressed margins and subdued trading activity constrain profitability. Applying a 22x price-to-earnings ratio yields a potential stock price around $35.

The baseline projection estimates annual revenue of roughly $10 billion by 2031. Assuming net profit margins stabilize around 35% and earnings per share hit $3.90, a 38x valuation multiple suggests a price target near $148.

An optimistic scenario envisions Robinhood successfully constructing a comprehensive financial ecosystem. Should revenue climb to $14 billion with EPS reaching $6.50, a 45x earnings multiple would support a stock price approaching $293.

Balancing these scenarios through probability weighting produces a 2031 target price around $156—translating to approximately 44% appreciation from current levels, or roughly 7.5% compound annual growth.

Wall Street’s Current Perspective

Analyst sentiment toward Robinhood remains constructive, though enthusiasm appears measured.

MarketBeat data reveals HOOD holds 18 Buy recommendations, 5 Hold ratings, and no Sell opinions. The overall consensus stands at Moderate Buy. However, the mean 12-month price objective sits around $112—only marginally higher than current trading levels.

This modest near-term target despite positive ratings suggests analysts recognize the long-term opportunity while acknowledging limited immediate upside following the stock’s recent appreciation.

Several headwinds warrant consideration. Current valuation multiples appear elevated. Transaction-based revenue streams face cyclical pressures. Cryptocurrency markets exhibit high volatility. The regulatory environment remains uncertain. Established financial institutions pose formidable competitive challenges.

Conversely, Robinhood possesses meaningful competitive strengths—including a substantial, demographically young customer base, expanding subscription-driven revenue from Gold memberships, growing assets under administration, and continuous product portfolio diversification.

Realistic modeling places the 2031 price range between $150 and $160. Achieving the $293 bull case target would require Robinhood to successfully transform into a comprehensive financial super app serving next-generation consumers.

Blockstream CEO Adam Back said concerns over Strategy’s small Bitcoin sale are overblown, framing the move as normal treasury management rather than a warning sign for the company’s Bitcoin plan.

Summary

- Adam Back said Strategy’s small Bitcoin sale showed balance sheet flexibility, not bearish treasury change.

- Strategy sold 32 BTC for about $2.5 million to fund preferred stock dividend payments due.

- Crypto.news later reported Strategy bought 1,550 BTC, keeping its accumulation story active for now again.

Speaking in a Bloomberg interview shared on YouTube, Back addressed questions about Strategy selling 32 BTC to help pay preferred stock dividends. He said the sale showed the firm could meet obligations while keeping Bitcoin at the center of its balance sheet.

Back frames sale as balance sheet use

Back argued that the market should not treat the 32 BTC sale as a bearish signal. In his view, Strategy used a small part of its Bitcoin position to support investor payments and reduce pressure on the capital structure.

He also said the move showed how Bitcoin can function inside a corporate treasury. Rather than showing weak conviction, it showed that a company can hold Bitcoin, raise capital against it and use a limited amount when cash needs arise.

Back’s argument also places the sale inside a larger shift in corporate Bitcoin finance, where companies use BTC alongside preferred shares, debt, common equity, and market tools today.

Strategy’s first sale drew attention

As previously reported by crypto.news, Strategy disclosed on June 1 that it sold 32 Bitcoin between May 26 and May 31 at an average price of $77,135. The sale raised about $2.5 million.

The filing said proceeds were expected to fund distributions on the company’s preferred stock. The sale represented about 0.0038% of Strategy’s Bitcoin holdings at the time, but it drew attention because Michael Saylor had long promoted a “never sell” message around Bitcoin.

Crypto.news later reported that Saylor separated personal investor advice from corporate treasury actions. “I said to YOU never sell your bitcoin,” Saylor said at BTC Prague.

Preferred dividends remain in focus

The debate centers on Strategy’s preferred stock model. Preferred shares can give investors yield, but they also create recurring cash needs that the company must meet through cash reserves, equity issuance or limited Bitcoin sales.

Strategy’s STRC preferred stock has faced pressure after falling below its $100 par value. As crypto.news reported, Saylor defended the company’s Bitcoin-backed strategy and said its Bitcoin and cash reserves still exceeded outstanding debt by about $48 billion.

Some critics argue that dividend obligations could become harder to manage if market conditions weaken. Supporters say the 32 BTC sale showed Strategy has several funding tools and does not need to abandon its long-term accumulation plan.

Strategy remains a net accumulator

The sale did not stop Strategy from buying more Bitcoin. Crypto.news reported that the company later bought 1,550 BTC for $101.3 million, lifting its holdings to 845,256 BTC after the sale disclosure.

That purchase was nearly 50 times larger than the 32 BTC sale. It helped support Back’s view that the transaction was not a broad retreat from Bitcoin.

Saylor has also argued that Bitcoin does not need staking or protocol-based yield. In a separate post covered by crypto.news, he framed Bitcoin as the base layer for credit, money, yield and equity products.

For now, the issue is not whether Strategy still wants Bitcoin. The question is how it funds preferred dividends while keeping investor trust and managing balance sheet risk.

Taiwan to stage five days of combat readiness drills

Japan Pension Fund Considers 1% Allocation to Crypto

Meet Curaçao’s Record-Breaking Goalkeeper Eloy Room

-

Business7 days ago

Business7 days agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Miami – Corporette.com

-

Crypto World6 days ago

Zimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Business1 day ago

Business1 day agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Entertainment7 days ago

Entertainment7 days agoMatt Damon’s Viral Sci-Fi Thriller Has Taken Over HBO Max

-

Tech7 days ago

Tech7 days agoAs AI companies race to go public, who else is along for the ride?

-

Business7 days ago

Business7 days agoAnthropic staff to meet White House officials next week, Axios reports

-

Crypto World1 day ago

Crypto World1 day agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World7 days ago

Crypto World7 days agoBitcoin could crash to $48,000, if this historical pattern is triggered

-

NewsBeat7 days ago

NewsBeat7 days agowhat doctors are seeing in ebike crashes

-

NewsBeat7 days ago

NewsBeat7 days agoWarning of disruption as Cardiff Crossrail works to start

-

NewsBeat7 days ago

NewsBeat7 days agoTributes to former deputy head teacher at Cambridge school among death and funeral notices

-

Entertainment7 days ago

Entertainment7 days agoKate Middleton Glare Goes Viral After Kids Booed At Royal Event

-

Politics7 days ago

Politics7 days ago“Israel’s” ban on ICRC visits ruled illegal, but Knesset moves to stop them permanently

-

News Videos7 days ago

News Videos7 days agoFinancial Accounting | Last Day Revision Strategy and Booster | CMA Inter – June 2026

-

Crypto World7 days ago

Crypto World7 days agoXRP ETFs Outperform As Bitcoin And Ethereum Funds Extend Outflow Trend

-

Tech6 days ago

Tech6 days agoOver 400 Arch Linux packages compromised to push rootkit, infostealer

-

Business7 days ago

Business7 days agoInvesco Quality Income Fund Q1 2026 Commentary

-

NewsBeat7 days ago

NewsBeat7 days agoSinger Oliver Tree dies aged 32 in helicopter crash in Brazil

-

Crypto World7 days ago

Crypto World7 days agoMarket Preview: SpaceX (SPCX) IPO Record, Federal Reserve Meeting, and Iran Nuclear Agreement

You must be logged in to post a comment Login