Crypto World

Explore how the Condorcet paradox exposes the limits of perfect fairness in blockchain consensus.

Consensus guarantees today, focus on two properties: Consistency and Liveness. Consistency requires that all nodes eventually agree on the same set and sequence of transactions, while liveness ensures the system continues to process new transactions. What they do not address is whether the agreed-upon transaction order totally reflects fairness.

In public blockchains, transaction ordering has direct economic consequences. The order in which transactions execute determines who captures value and who pays the cost, particularly as validators, block builders, or sequencers can exploit their privileged role in block construction for financial gain. This practice is known as maximal extractable value (MEV) and includes the profitable frontrunning, backrunning, and sandwiching of transactions. Prima facie, there is no obvious way to prevent MEV extracting practices because block proposers hold unilateral power over transaction ordering, and no protocol rule inherently constrains how they exercise that power.

To address this, transaction order-fairness has been proposed as a third essential consensus property. A protocol is transaction order-fair if no participant can systematically bias transaction ordering beyond what objective network conditions and protocol rules imply. By limiting how much power a block proposer has to reorder transactions, fair-ordering protocols move blockchains closer to being transparent, predictable, and MEV-resistant.

However, even this intuitive idea of fairness encounters a structural limit. In an asynchronous distributed system, there is no globally defined reception order because each node observes messages at different times, and no shared clock exists. Therefore, no protocol can guarantee execution strictly according to a single universal arrival sequence. This limitation follows from the basic constraints of distributed consensus under asynchronous communication, not from any particular design choice.

The Condorcet Paradox and the Impossibility of Perfect Fairness

The most intuitive and strongest notion of fairness is called Receive-Order-Fairness (ROF). It simply means “first-come, first-served.” ROF dictates that if most nodes receive transaction A before transaction B, then A should be processed before B.

That sounds simple and fair. However, the problem is that nodes do not all see transactions at the exact same time. Messages travel at different speeds. Some computers might receive A first. Others might receive B first. Because of this, it is impossible to guarantee perfect “first-come, first-served” fairness unless every node can communicate instantly with no delays. In real networks, that never happens.

There is also a deeper problem called the Condorcet paradox. This idea comes from voting theory. It shows that even when each person (or node in this case) has a clear and consistent order in their own mind, the group as a whole can end up with a loop that makes no sense.

For example:

- Most nodes see A before B

- Most nodes see B before C

- Most nodes see C before A

This produces a majority preference cycle (A→B→C→A), meaning no single ordering satisfies the majority view across all pairs. The network cannot construct one sequence that matches what most nodes observed first.

Because perfect ROF is unachievable under these conditions, practical systems adopt some weaker fairness guarantees as outlined in the sections below.

Hashgraph’s Fairness Model: Graph of Hashes, Median Timestamps, and aBFT Consensus

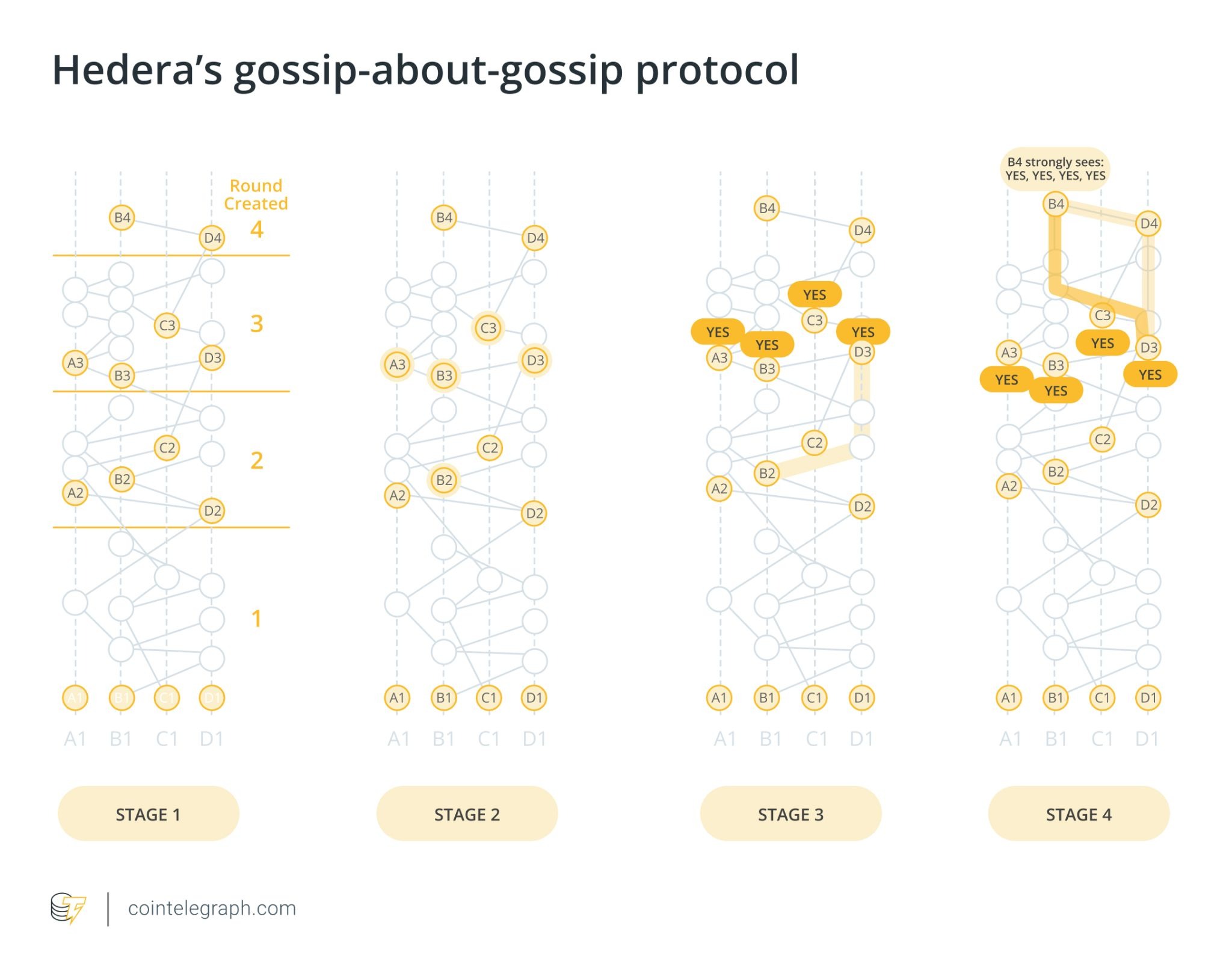

Hedera, which employs the hashgraph algorithm, approaches the fairness problem through a directed acyclic graph (DAG) of cryptographically linked events. It is a leaderless consensus algorithm that operates in a fully asynchronous setting and achieves Asynchronous Byzantine Fault Tolerant (aBFT). Under this model, honest nodes eventually reach agreement on the same transaction log even under unbounded message delays. Consensus ordering emerges from network-wide observation through a virtual voting process: the order is calculated collectively by nodes rather than assigned by a designated block producer.

When a node receives a transaction, it packages it into a message called an event and gossips it to peers. When another node creates a subsequent event, it records the hash of the events it has already seen and digitally signs the new event. This provides cryptographic proof that the node had seen prior events before signing the new one. The hashgraph, therefore, enforces causal order: once a node publishes an event, the ancestry embedded in that event proves which transactions preceded it.

This linkage can be represented as an edge in the DAG. If one event is a direct or indirect ancestor of another, a downward path exists between them in the graph, and the protocol provides a cryptographic guarantee that the ancestor event was created first. Transactions connected by such paths are ordered according to their causal relationships in the graph. When two events have no ancestor relationship, they are concurrent, and the protocol resolves their relative order through the round-received mechanism. Each event is assigned a round based on when a supermajority of nodes, defined as more than two-thirds, can be shown to have strongly seen it through the DAG structure. Events assigned to earlier rounds are ordered first.

For events that share the same round-received, the protocol uses median timestamps to determine ordering. Each node records a local timestamp when it first receives an event. The consensus timestamp assigned to an event is the median of the timestamps reported across the node set. This timestamp is not derived from arbitrary local clocks in isolation. It is constrained by the gossip ancestry preserved in the hashgraph: a node cannot claim to have received an event before its causal predecessors without producing a detectable inconsistency in the DAG.

Under the standard aBFT assumption that fewer than one-third of nodes are Byzantine, the median falls on an honest timestamp or between two honest timestamps, which prevents adversarial nodes from shifting the median beyond a bounded range.

The Condorcet paradox can still apply to concurrent events, specifically those with no ancestor relationship in the DAG, where different nodes may observe them in different orders. The DAG structure eliminates this ambiguity for causally linked events: no contradictory causal paths can exist because each event’s ancestry is cryptographically fixed at creation. Because gossip propagation typically causes new events to become descendants of prior events within fractions of a second, most transactions fall into clear causal chains. The remaining concurrent events are resolved through round-received assignment and median timestamps as described above.

However, the hashgraph’s fairness guarantees have a bounded adversarial surface. A node still determines when to gossip an event, which events to relay first, and how long to delay relaying. These choices reshape the first-seen patterns that feed into median timestamp computation. The DAG cannot misrepresent the causal order it records, but it can be strategically shaped by gossip behavior before that order is recorded.

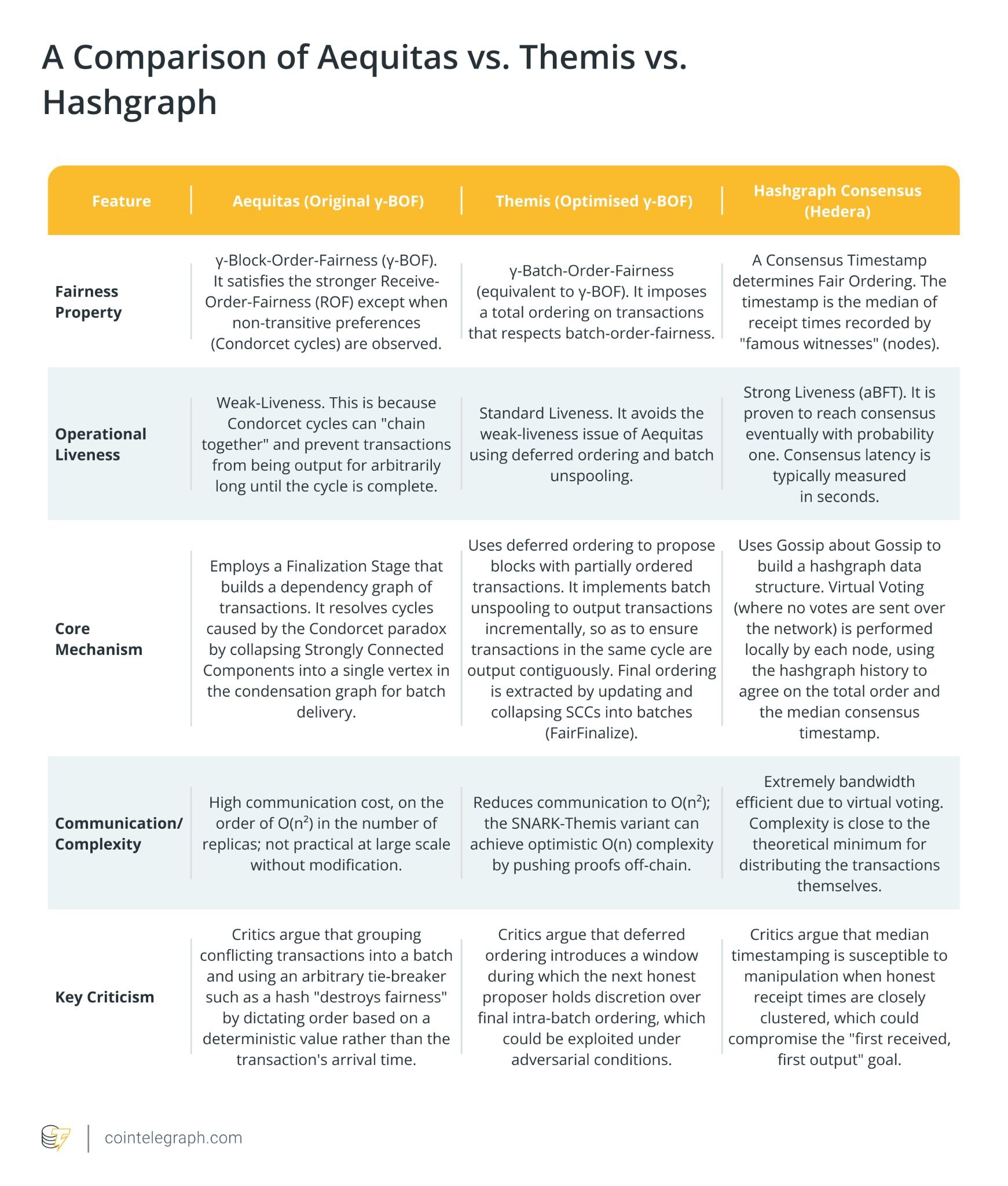

BOF Protocols: Fairness Through Batch Aggregation

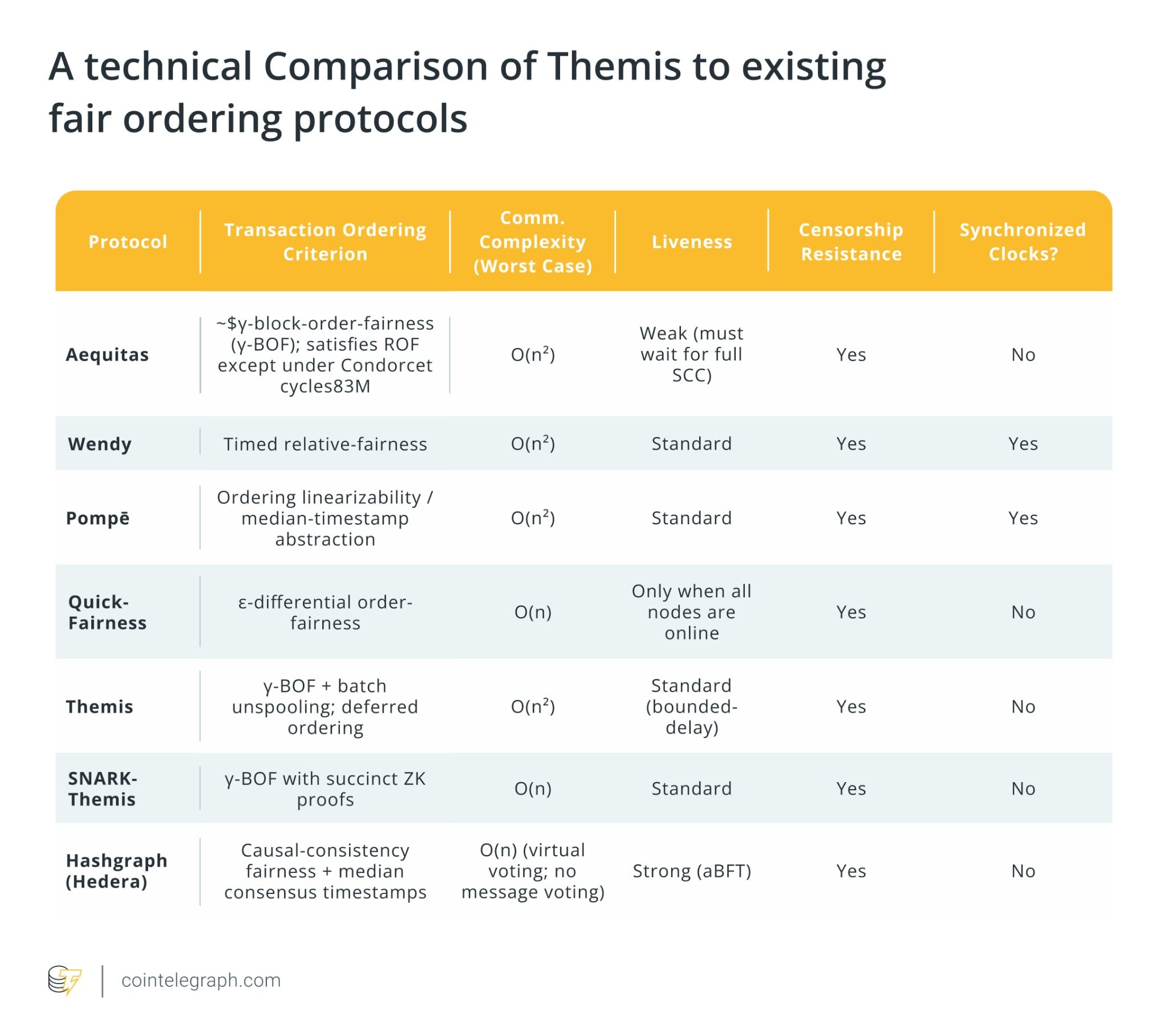

BOF protocols define a “block” as the set of transactions forming a single Condorcet cycle, and then order these blocks fairly while ignoring the ordering inside the block. The BOF criterion was first introduced by Mahimna Kelkar et al. (2020) in “Order-Fairness for Byzantine Consensus,” which formalized the Aequitas family of protocols. In Aequitas, BOF requires that if a γ-fraction of nodes observe block (b) before block (b′), then no honest node may output (b) after (b′). The γ-fraction is the proportion of nodes that must agree on a block ordering for that ordering to be considered “fair” and enforced by the consensus protocol.

For BOF, if the fairness predicate indicates that a transaction tx should precede tx′, then tx cannot appear in a later block than tx′. When the fairness relation becomes cyclic, the protocol collapses the entire strongly connected component into a single block, because BOF treats that block, not the individual transaction, as the atomic fairness unit. Under γ-BOF, the only forbidden outcome is placing tx′ in a strictly earlier block than tx when a directed constraint tx→tx′ exists. The protocol permits both transactions to appear in the same block and places no restrictions on their ordering inside that block.

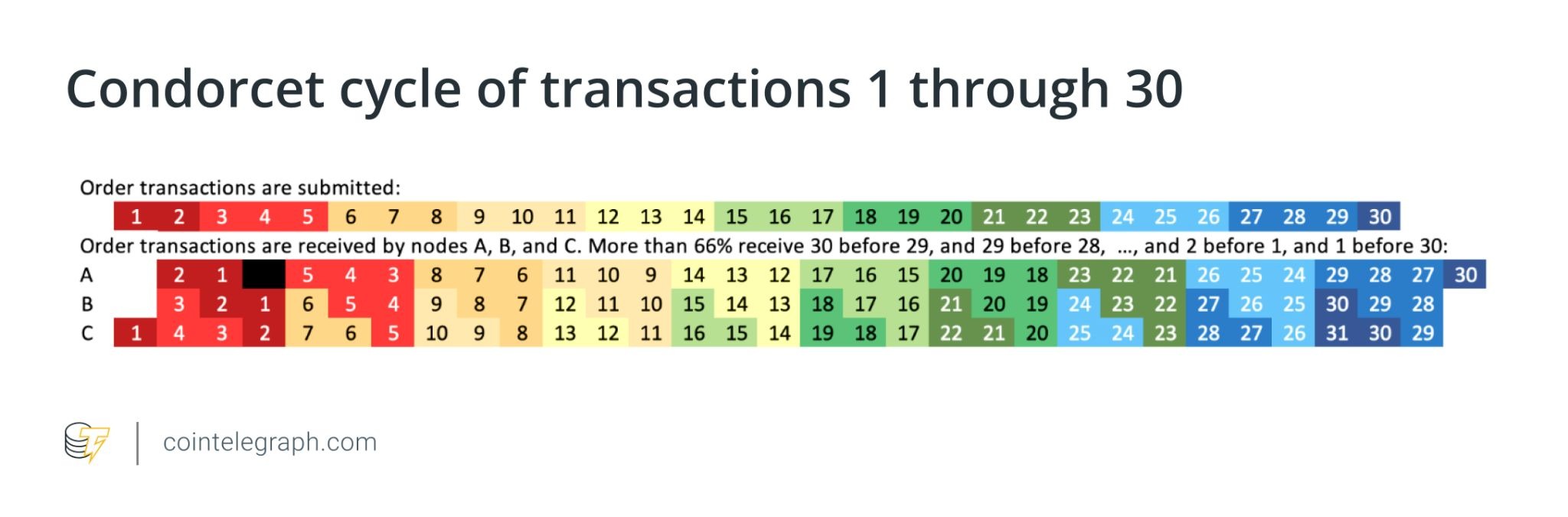

For example, Figure 2 below, is a Condorcet cycle of 30 transactions, so they would be in a single block. Sorting by hash might place 30 before 1 in the final ordering. However, a γ-fraction of nodes observed transaction 1 before transaction 30, yet placing 30 before 1 is still considered “fair” under γ-BOF. Because 1 and 30 are in the same block, and this notion of fairness only considers the order of the blocks, not the order of the transactions within a block.

When no cycles exist, BOF coincides with the strong form of ROF. When Condorcet cycles emerge, all transactions participating in the cycle are placed into a single block, and a deterministic method, such as a hash-based rule, orders events within that batch.

The protocol proceeds through three coordinated stages to ensure consistent transaction ordering across the network: the Gossip stage, the Agreement stage, and the Finalization stage.

In the gossip stage, nodes use FIFO broadcast to disseminate transactions in the order they were locally received per sender, preserving per-sender sequence so that each peer maintains a comparable transaction view. Once gossiping stabilizes, the agreement stage begins, where nodes execute a Set Byzantine Agreement (Set-BA) protocol to reach consensus on a unified set of local orderings that will serve as the foundation for the global order. In the finalization stage, nodes construct a dependency graph that captures transaction ordering relationships. Any transactions forming a cycle within this graph are grouped into the same strongly connected component and finalized together within a block.

However, Aequitas suffers from weak liveness, as its high communication cost and strict fairness constraints require the protocol to wait for the entire Condorcet cycle before finalizing the collapsed SCC. Because Condorcet cycles can chain indefinitely, this waiting period can grow without bound. Thus, transaction delivery can be delayed for an arbitrarily long time, and creates the “freeze” risk that defines Aequitas’ weak-liveness guarantee.

Themis was introduced to solve this. It preserves the same γ-BOF property while resolving these liveness and communication issues. Like Aequitas, Themis also constructs a dependency graph and collapses SCCs during its “FairFinalize” stage. The SCCs represent the same non-transitive Condorcet cycles underlying the γ-BOF relaxation, and Themis uses the condensation graph to derive the batch structure of the final output. The key difference is that Themis does not wait for a full cycle to complete. Instead, it uses deferred ordering and batch unspooling to output SCCs incrementally while allowing new transactions to continue flowing. This preserves γ-BOF but upgrades Aequitas’ weak liveness to standard liveness, and guarantees delivery within a delay bound.

In its standard form, Themis requires each participant to exchange messages with most other nodes in the network. As the number of participants increases, the amount of communication grows rapidly, roughly proportional to the square of the network size. However, in its optimized version, SNARK-Themis, nodes use succinct cryptographic proofs to verify fairness without needing to communicate directly with every other participant. This reduces the communication load so that it grows only in direct proportion to the number of nodes, thus allowing Themis to scale efficiently even in large networks.

If a malicious proposer attempts to exploit the situation by proposing an empty block, Themis employs deferred ordering, where the partially ordered batch (B₁) is still accepted, and the final, precise order of its transactions is determined later by the next honest proposer. That proposer finalizes the order based on verifiable transaction relationships, not personal discretion. This design ensures finalization depends only on bounded network delay, not on the arbitrary behavior of the current proposer, thus closing a key liveness gap that Aequitas could not guarantee.

This structure guarantees that every transaction is both included and executed deterministically, even in the presence of conflicting arrival orders. Because Themis leverages the internal dependency graph and SCC condensation to extract a final ordering, it is resilient to adversarial manipulation. Attackers cannot simply reorder or front-run other users’ transactions once they are included in the batch. Any attempt to alter dependencies would break the verified graph consistency.

In an empirical analysis by Mahimna Kelkar et al., γ-BOF resists adversarial reordering more strongly than timestamp-based approaches in geo-distributed networks. However, it requires significantly more computational and protocol complexity, which can also be seen as a downside.

Conclusion:

Perfect fairness in transaction ordering is structurally unattainable in distributed systems that lack synchronized clocks and instantaneous communication. The Condorcet paradox ensures that majority preferences can conflict in ways no single linear order can satisfy. The real question is how to find the most realistic and useful trade-offs.

Hashgraph and BOF represent two coherent answers. Neither approach is inherently superior. Both embed fairness directly into the consensus mechanism rather than relying on trust or authority. Both approaches demonstrate that fairness is not a binary property but a spectrum of trade-offs defined by formal impossibility results. Where synchrony is unavailable, and clocks are untrusted, the choice between median-timestamp aggregation and batch-order collapsing reflects different but equally principled responses to the same underlying constraint.

Key Takeaways

- ASML shares tumbled 7.82% to close at $1,778.46, significantly lagging broader market indices

- Allegations surfaced regarding possible violations of U.S. export control regulations related to Chinese sales

- Proposed bipartisan legislation threatens to halt all deep-ultraviolet lithography (DUV) equipment exports to China

- Chinese market represents approximately 20% of ASML’s anticipated 2026 revenues

- Despite volatility, Wells Fargo upgraded price target to $2,200 with consensus rating at Moderate Buy

Shares of ASML (ASML) experienced a sharp decline on Tuesday, closing at $1,778.46—a 7.82% drop that significantly outpaced the broader market’s losses. While the S&P 500 shed 1.44% and the Nasdaq fell 2.22% during the same trading session, ASML’s pullback was notably steeper.

The semiconductor equipment manufacturer’s slide followed reports that U.S. officials have raised concerns about possible export control violations involving the company’s business with China. Compounding investor anxiety, a bipartisan legislative proposal now threatens to completely prohibit deep-ultraviolet (DUV) lithography equipment shipments to the Chinese market.

The stakes are substantial: China is projected to contribute approximately 20% of ASML’s total revenue stream in 2026, making this exposure a critical focal point for market participants.

ASML issued a formal denial of the allegations, clarifying that no extreme ultraviolet (EUV) systems were shipped to China in breach of existing controls. While this statement may mitigate some reputational risk, regulatory scrutiny appears likely to intensify.

Beyond the immediate allegations, market participants are increasingly concerned about potential restrictions on software updates, spare parts, and maintenance services for equipment already deployed in China. This ongoing service revenue has represented a significant, albeit understated, contributor to ASML’s financial performance.

Competitive dynamics add another layer of complexity. Nikon has been expanding its presence in mature-node immersion lithography systems, while Chinese domestic manufacturers continue advancing their indigenous capabilities—developments that could exert downward pressure on both pricing and profit margins in ASML’s lower-tier product segments.

Upcoming Earnings Release

Despite Tuesday’s selloff, ASML’s fundamental performance metrics remain robust. The company is scheduled to report quarterly results on July 15, 2026. Wall Street analysts project earnings per share of $7.98, representing a substantial 75.38% year-over-year increase.

Second-quarter revenue estimates stand at $10.28 billion, reflecting 17.83% growth compared to the prior-year period. Full-year consensus forecasts call for EPS of $36.69 and revenues of $45.35 billion—representing increases of 31.27% and 22.67%, respectively.

In the most recent quarter, ASML delivered EPS of $8.28 on $10.15 billion in revenue, achieving a return on equity of 48.69% and maintaining a net profit margin of 27.65%.

The stock currently trades at a forward price-to-earnings multiple of 52.58, above the industry average of 47.43. Its price-to-earnings-growth (PEG) ratio of 1.55 also exceeds the sector norm of 1.48.

Wall Street Maintains Cautious Optimism

Despite the recent volatility, analyst sentiment remains generally supportive. Wells Fargo elevated its price objective from $1,750 to $2,200 while maintaining an overweight rating. Bank of America similarly increased its target price and retained a Buy recommendation.

Morgan Stanley and Barclays have both reaffirmed overweight ratings in recent research updates.

The Street consensus stands at Moderate Buy, comprising four Strong Buy ratings, 20 Buy recommendations, five Hold ratings, and three Sell calls. The average price target of $1,772.62 closely aligns with Tuesday’s closing price.

However, not all institutional investors are holding steady. Riverbridge Partners LLC reduced its ASML position by 40.3% during the first quarter, divesting 1,201 shares. Following this reduction, the firm maintained 1,781 shares valued at approximately $2.35 million.

From a technical perspective, ASML’s 50-day moving average sits at $1,610.59, while the 200-day moving average stands at $1,411.79, suggesting the stock retains a cushion before testing long-term support levels. The 52-week trading range spans from $683.48 to $1,959.04.

ASML currently carries a Zacks Rank of #3 (Hold), with earnings per share estimates revised downward by 1.11% over the past month.

Kalshi has filed a federal lawsuit challenging a new Illinois law that would require prediction market platforms offering sports event contracts to obtain state licenses before operating.

Summary

- Kalshi has sued Illinois, arguing the state’s sports prediction market law violates federal authority.

- The company says complying with the law would conflict with CFTC rules and create unrecoverable costs.

- The lawsuit comes as Kalshi pursues a reported $40 billion valuation and expands its crypto product lineup.

According to a filing submitted Tuesday in the U.S. District Court for the Northern District of Illinois, Kalshi sued Illinois Governor JB Pritzker, Attorney General Kwame Raoul, members of the Illinois Gaming Board, and other state officials, arguing that the state has overstepped federal authority over regulated prediction markets.

The complaint targets Illinois Senate Bill 3019, which was signed into law last week as part of the state’s fiscal year 2027 budget package. Kalshi argued that the legislation unlawfully interferes with the Commodity Exchange Act by treating sports event contracts offered on federally regulated prediction markets as sports wagers subject to state licensing requirements. The company said the law is scheduled to take effect on July 1.

Kalshi says federal rules override Illinois licensing requirements

According to the complaint, Kalshi believes the Commodity Futures Trading Commission has exclusive authority over its event contracts because they are regulated under the Commodity Exchange Act. The company alleged that Illinois cannot impose an additional licensing system on products already overseen by the federal regulator.

Kalshi argued that stopping sports event contracts in Illinois would leave the company in conflict with the CFTC’s requirement to operate a uniform national market. The filing also claimed that restricting Illinois users would force Kalshi to build costly technology systems to block access in the state, expenses it said could not be recovered even if it later won the case.

At the same time, the complaint argued that complying with Illinois’s licensing framework would expose the company to another set of costly regulatory obligations. According to Kalshi, ignoring the new law is also not a practical option because state enforcement could include criminal penalties.

The disputed legislation also introduced a 0.2% tax on cryptocurrency transactions, a measure that has already drawn criticism from several participants in the digital asset industry.

In addition, the law expanded the state’s definition of an “exchange wager” to include agreements, contracts, transactions, or swaps traded on prediction markets when tied to sporting contests, placing those products under the same rules as traditional sports betting operators.

Legal dispute grows as Kalshi expands business

The Illinois case adds to a series of legal disputes over whether states or the federal government has primary authority over sports-related prediction markets.

The CFTC, now led by Commissioner Michael Selig, has maintained that prediction market event contracts fall under its jurisdiction because they qualify as swaps under federal law. Federal regulators have already challenged similar state actions, including recent litigation involving restrictions imposed in Kentucky.

Legal analysts have suggested that the conflicting positions taken by state gaming regulators and federal authorities could eventually require resolution by the U.S. Supreme Court if lower courts continue reaching different conclusions.

Meanwhile, the lawsuit comes as Kalshi continues expanding its business. The company has reportedly entered discussions to raise fresh funding at a valuation of about $40 billion, up from the $22 billion valuation it secured less than two months ago.

Sports-related contracts account for roughly 65% of trading volume, according to company data, while multi-outcome combination contracts introduced last year have become one of its fastest-growing products.

Recent product launches have also extended Kalshi’s regulated offerings. As reported by crypto.news, on June 24, the company added perpetual crypto futures tied to Zcash, Near Protocol, and Shiba Inu, increasing its CFTC-regulated lineup to 13 digital assets operating under contracts without expiration dates.

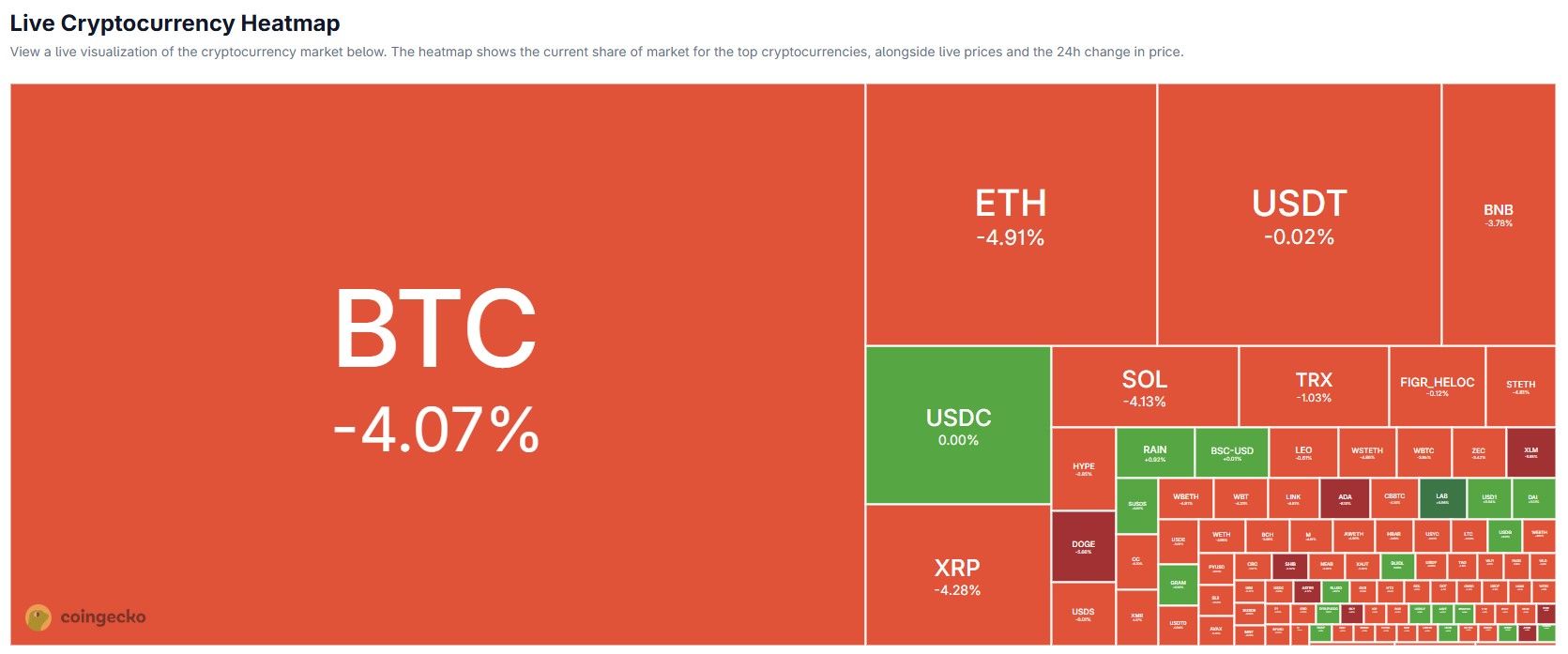

Crypto markets sold off hard on June 24, wiping out more than $600 million in leveraged long positions within hours. Bitcoin and Ethereum absorbed the heaviest of the crypto liquidations.

The drop was broad rather than isolated. Nearly every major token turned red, and the forced selling concentrated on the largest exchanges. Binance led every venue.

Red Floods the Market

A live cryptocurrency heatmap captured the scale of the rout. Bitcoin (BTC) showed a 4.07% daily loss on the snapshot, while Ethereum (ETH) fell 4.91%.

Large caps followed in lockstep. XRP dropped 4.28%, Solana (SOL) lost 4.13%, and BNB slid 3.78%. Dogecoin (DOGE) ranked as the worst major performer at 5.86%.

The uniform selling pointed to risk-off pressure rather than a single token story. By press time the 24-hour declines had eased, with Bitcoin near $60,585 and Ethereum around $1,606 after a modest intraday bounce.

Longs Bear the Brunt of the Flush

The selloff was a leverage event. A 12-hour liquidation heatmap showed traders betting on higher prices getting wiped out across the board.

Bitcoin led with $336.47 million in liquidated longs. Ethereum followed at $188.82 million. Solana added $39.09 million, while a broad Others group totaled $70.80 million.

Centralized venues took the largest hits. Binance recorded $350.58 million in liquidations, far ahead of the field.

Hyperliquid placed second at $147.24 million, a notable showing for a decentralized exchange. Bybit followed with $120.08 million, then Gate at $55.89 million and OKX near $47.84 million.

Crypto Liquidations: Bitcoin Hinges on $63,000 Wall

The Binance BTC/USDT liquidation leverage heatmap explains why any Ethereum and Bitcoin bounce may struggle. Bitcoin traded flat near $63,000 for most of June 23 before breaking down.

Price stair-stepped lower through June 24, sliding toward $59,700 before steadying around $60,000. The descent cut straight through dense liquidation clusters.

Those bright clusters now sit overhead between $61,500 and $63,000. They mark heavy leverage that could act as resistance on any rebound.

A reclaim of $63,000 would invalidate the bearish setup. A loss of the $59,700 support could expose lower levels and trigger another cascade.

Bitcoin now sits between a wall of overhead liquidations and a thin floor below. The next move depends on which level breaks first.

The post $600M Wiped Out in Hours: Crypto’s Leverage Bloodbath Just Hit BTC and ETH Hardest appeared first on BeInCrypto.

Crypto World

Wall Street AI Watch: Micron (MU) Results, SK Hynix $29B Listing, and Chip Stock Recovery

Quick Summary

- Micron’s quarterly report served as a critical barometer for ongoing AI infrastructure investment

- Chip stocks like Nvidia and Broadcom rebounded strongly following this week’s earlier downturn

- SK Hynix unveiled plans for a U.S. stock market debut potentially worth $29 billion

- The Nasdaq regained ground after multiple days of technology-led losses

- Cerebras delivered earnings results, offering insight into specialized AI chip demand

Artificial intelligence remained front and center across financial markets today. Between quarterly earnings announcements and a blockbuster listing reveal, semiconductor companies commanded attention from traders and investors alike.

Micron’s Report Becomes AI Demand Litmus Test

[[LINK_START_0]]Micron’s quarterly earnings release[[LINK_END_0]] stood as the session’s most anticipated event.

Market participants track Micron carefully since its memory products power AI servers and data center infrastructure. Robust performance in these segments indicates continued aggressive spending by hyperscalers on artificial intelligence capabilities.

Anticipation ran high ahead of the announcement. Micron shares had delivered solid returns throughout 2026, leaving Wall Street eager for validation that high-bandwidth memory sales momentum persisted.

The implications extended well beyond a single company’s performance. Positive figures would reinforce optimism about semiconductor industry health. Disappointing numbers might trigger concerns about the actual pace of AI capital expenditure growth.

Few quarterly reports this season attracted comparable investor scrutiny.

Chip Sector Mounts Strong Recovery

Following recent pressure, semiconductor equities rallied meaningfully.

Nvidia, [[LINK_START_1]]Broadcom[[LINK_END_1]], and Intel all posted gains as capital flowed back into AI-linked stocks. The price action indicated many market participants viewed the recent selloff as an entry point rather than a fundamental warning.

AI-related capital spending continues representing one of the market’s most powerful tailwinds.

Hyperscale cloud providers maintain multi-billion-dollar commitments to data center expansion, advanced processors, and networking infrastructure. Today’s recovery demonstrated that underlying conviction in the sector remains intact.

Volatility has increased noticeably, yet demand emerged swiftly at lower price levels.

SK Hynix Announces Plans for $29 Billion U.S. Market Debut

The session’s most significant corporate development originated from SK Hynix.

The South Korean memory manufacturer disclosed intentions to pursue a United States listing in a transaction potentially generating approximately $29 billion. Upon completion, this would represent one of the largest public offerings on record.

[[LINK_START_2]]SK Hynix[[LINK_END_2]] specializes in high-bandwidth memory production, a critical component enabling contemporary AI system performance.

A U.S. market presence would provide investors with direct exposure to one of the most sought-after segments within the semiconductor value chain. The announcement underscores extraordinary investor appetite for AI-connected equity opportunities.

Nasdaq Composite Regains Momentum

The [[LINK_START_3]]Nasdaq[[LINK_END_3]] index posted positive returns following multiple consecutive down sessions.

Technology shares paced the advance as market participants grew increasingly comfortable with current valuations after the recent correction. While inflation and monetary policy concerns persist, buying interest nonetheless materialized.

The rebound indicates investors remain prepared to add exposure when high-quality technology companies experience pullbacks.

Semiconductors, AI infrastructure providers, and cloud computing firms continue leading broader market performance over the trailing twelve months.

Cerebras Provides Additional AI Sector Perspective

[[LINK_START_4]]Cerebras[[LINK_END_4]] published quarterly results as well, capturing attention from investors seeking exposure beyond dominant chip manufacturers.

The firm produces processors engineered exclusively for artificial intelligence computing tasks. Its financial performance offered visibility into demand patterns for specialized hardware operating outside Nvidia’s ecosystem.

The report contributed additional data points suggesting AI hardware investment remains broadly distributed rather than concentrated among just a handful of suppliers.

Investors continue monitoring emerging players like Cerebras to gauge the true breadth of AI infrastructure deployment.

The quarterly figures reinforced that artificial intelligence maintains its position as the defining investment theme propelling technology sector allocation as 2026 progresses.

The old saying – sell in May and go away – proved to be right once again for the cryptocurrency markets. It was just six weeks ago when bitcoin had evidently reclaimed the $80,000 level and even surged to a multi-month peak at almost $83,000. The sentiment was gradually improving and there were even calls for $100,000 by the summer.

However, the tides turned viciously and the asset was rejected vigorously. Its decline since then has been nothing short of painful, dumping below $60,000 earlier today for the second time in June.

Is This Why?

Popular analyst Ali Martinez brought out the Coinbase Premium metric earlier today as the markets were crashing to fresh low. CryptoPotato reported when BTC dumped below $60,000 but managed to maintain above the $59,000 level and has now reclaimed the former.

According to Martinez, though, the metric that stands out the most for the past six weeks or so is the one that tracks how much BTC costs on Coinbase compared to Binance. In general, if the Premium is in the green, it means US investors (typically institutions) are accumulating bitcoin en masse on Coinbase, pushing its price there above the levels on international exchanges.

However, the last 46 days have not seen such green days. Or, as Martinez put it:

“A negative premium means BTC is trading cheaper on Coinbase, suggesting that US institutional buying pressure has dried up.”

He believes this slowdown mimics the massive investor exodus from the US-based spot Bitcoin ETFs. The funds have bled approximately $5 billion in essentially the same timeframe because “American smart money appears to be sitting on the sidelines, waiting for macroeconomic clarity before re-entering the accumulation phase.”

Other Plausible Reasons

As we recently noted, the ETFs are indeed among the many possible reasons behind BTC’s latest leg down. Others include the uncertainty around the war against Iran, strengthening dollar, or even some OG investors selling off. However, another biggie that stands out is the FUD around Strategy and its Stretch shares.

STRC has dumped below its par price of $100, currently trading at a hefty discount at $80. This essentially increases the pressure that the BTC-buying machine is under as the ‘flywheel’ effect is disrupted and the company now has to pay higher yield. According to some analysts, this could result in massive BTC sales from Strategy.

The post Is This the Hidden Reason Behind Bitcoin’s $23K Collapse in Just 6 Weeks? appeared first on CryptoPotato.

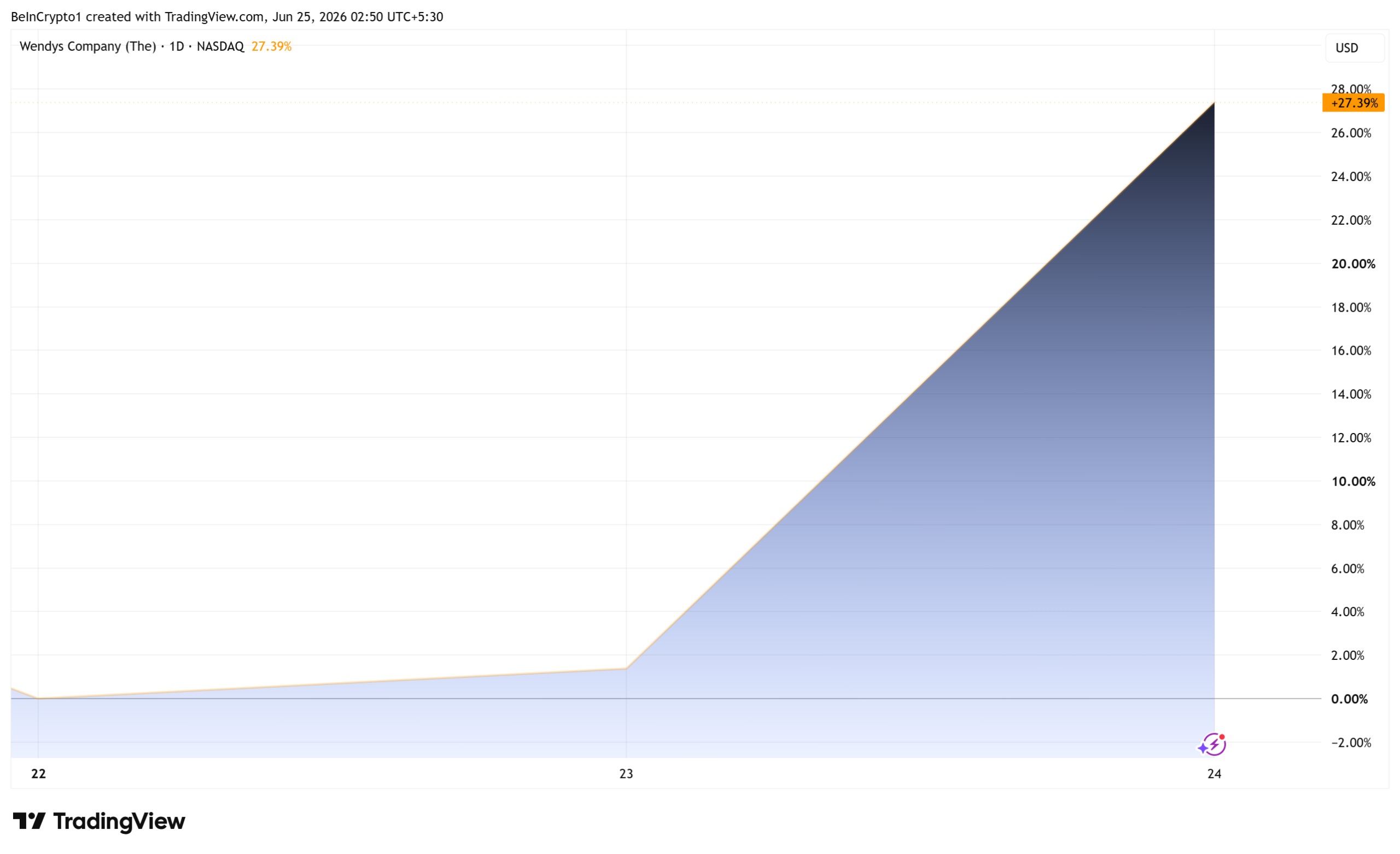

Wendy’s stock climbed almost 30% on Wednesday after traders on Reddit’s WallStreetBets forum rallied behind the struggling burger chain, reviving the meme-stock playbook that powered GameStop in 2021.

The rally lifted Wendy’s shares (WEN) to an intraday high near $8.89 and triggered at least one volatility halt, even as sales keep sliding.

Why Wendy’s Stock Drew a Short Squeeze

The move started with a since-deleted WallStreetBets post that urged members to rescue the chain before it collapsed. Copycat posts showing share and options purchases quickly followed.

“Save Wendy’s before it’s too late,” the post read.

Follow us on X to get the latest news as it happens

Volume confirmed the frenzy. More than 202 million shares changed hands, over 15 times the recent average.

The stock logged its biggest single-day gain since March 2020, CNBC reported. Wendy’s had ended the prior session near $6.26, not far from a multiyear low.

The squeeze setup is real but far smaller than 2021. About 23% of Wendy’s float was sold short before the rally, according to S3 Partners. The same firm put GameStop’s short interest above 140% of its float ahead of the 2021 squeeze.

Rising prices can still force shorts to buy back stock, which pushes prices higher. That pattern drove the AMC and GameStop squeeze, and it resurfaced this year during the GameStop meme stock frenzy.

A CFO Hire Gives Bulls a Story

Sentiment had a fundamental hook too. Wendy’s named Steve Cirulis chief financial officer on June 23, succeeding Ken Cook, according to a regulatory filing.

Cirulis ran finance at Potbelly alongside Bob Wright, now Wendy’s CEO. The company credits the pair with a more than 500% gain in Potbelly’s share price during their tenure.

That record gave retail buyers a turnaround story to chase, a familiar driver of meme driven market moves. The hire builds on a recovery plan the company calls Project Fresh.

Fundamentals Still Point Down

The business behind the rally remains weak. US same-restaurant sales fell 7.8% in the first quarter, and net income slid to $22.7 million.

Quarterly earnings still beat reduced forecasts, yet the rally rests on sentiment rather than results.

Wendy’s has been here before. A June 2021 Reddit post hailed Wendy’s as the perfect WallStreetBets stock and briefly drove shares up 26%. That rally faded within weeks because almost none of the stock was sold short.

This time a crowded short base gives the move real fuel. Still, most names lifted by Reddit traders and markets eventually gave back their gains.

Wendy’s gains holding may depend on how long the crowd stays interested.

The post Wendy’s Stock Climbs 30% as WallStreetBets Targets a GameStop Repeat appeared first on BeInCrypto.

![]()

Kalshi is seeking to raise fresh capital at a valuation of about $40 billion, nearly doubling the $22 billion valuation it targeted in its previous funding round, according to a Financial Times report citing people familiar with the matter.

The prediction markets platform could close the fundraising as soon as the third quarter of this year, FT said.

If completed, the deal would widen Kalshi’s valuation lead over rival Polymarket, which was last reported to be seeking funding at $15 billion. The two platforms have emerged as the dominant names in the prediction markets sector, while many other entrants have increased the industry’s competitive landscape.

Kalshi’s previous funding round, which valued the company at $22 billion, attracted a roster of high-profile investors including Philippe Laffont’s Coatue Management, Sequoia Capital, Andreessen Horowitz and Morgan Stanley.

Competition in the sector has intensified as firms race to capture users and expand product offerings.

Kalshi operates as a federally regulated exchange in the United States, a distinction that has helped it attract mainstream investors and institutional backing. Meanwhile, Polymarket, which uses blockchain infrastructure and cryptocurrency-based settlement, has gained popularity among crypto traders and has become widely followed during recent election cycles.

Michelle Bond, the wife of Ryan Salame—former co-CEO of FTX Digital Markets—has been scheduled for trial in November following delays tied to motions connected to Salame’s plea agreement. The proceeding comes as prosecutors pursue remaining criminal accountability related to the 2022 collapse of FTX, an episode that has since reshaped regulatory scrutiny of crypto-linked political activity and financial crime controls.

On Wednesday, U.S. District Judge George Daniels of the Southern District of New York set Bond’s trial to begin on Nov. 9. Bond faces four charges alleging violations of U.S. campaign finance law, stemming from prosecutors’ claims that FTX-related money was used to improperly support a 2022 congressional bid.

Key takeaways

- Judge George Daniels ordered Michelle Bond’s criminal trial to start on Nov. 9 in the Southern District of New York.

- Bond is charged with four offenses related to alleged campaign finance violations connected to the 2022 U.S. House race in New York’s 1st district.

- Prosecutors alleged that Ryan Salame used FTX funds in a “sham” payment arrangement, which they said violated campaign finance rules.

- The case is part of the final criminal track arising from FTX’s 2022 bankruptcy, following convictions and prison sentences for other key figures.

Bond’s trial date set amid motion-related delays

Bond’s schedule reflects procedural disputes that have continued since the charges were brought. A week earlier, Judge Daniels denied a motion by Bond seeking dismissal of the indictment. According to reporting by Cointelegraph, the defense argued that prosecutors had promised Salame he would not be charged if he pleaded guilty—an issue that, if accepted, could have materially affected Bond’s exposure.

With the dismissal attempt rejected, the court moved forward to establish a firm trial start date. For compliance and legal teams, the decision is significant because it underscores how plea negotiations and alleged assurances can become contested topics in later proceedings involving related defendants, even when one defendant has already resolved the matter through a plea agreement.

Alleged campaign finance conduct tied to the FTX collapse

Bond’s case is anchored in an August 2024 indictment. Prosecutors alleged that Bond and Salame “illegally funded” Salame’s political activity by using FTX resources to support a 2022 campaign for the U.S. House of Representatives.

The government’s allegations include that Salame used $400,000 of FTX funds as part of a “sham” payment intended to comply on paper while violating campaign finance laws in substance. Bond reportedly ran as a Republican in New York’s 1st congressional district, though she lost in the primary to Nicholas LaLota.

From an institutional perspective, the case illustrates a recurring enforcement theme: where crypto-related business failures intersect with political contributions, prosecutors may pursue campaign finance statutes in addition to financial fraud and related offenses. That creates additional compliance expectations for crypto firms and their leadership regarding the provenance of funds, controls around payments, and documentation that can withstand scrutiny across regulatory regimes.

How the plea deal with Salame shaped the remaining proceedings

Ryan Salame pleaded guilty and ultimately received a 7.5-year prison sentence, concluding his own criminal case. Authorities alleged that, as part of a conspiracy to make unlawful political contributions, Salame and others used money linked to FTX to support political activity. Salame later attempted to vacate his plea, arguing that prosecutors had misled him regarding whether Bond would face charges. Ultimately, he reported to prison in October 2024, leaving the dispute to continue within his wife’s case.

Bond’s trial therefore sits at the end of a broader U.S. prosecution landscape stemming from FTX’s collapse and its aftermath. The government’s pursuit of multiple individuals tied to FTX has included defendants who received prison time, as well as cooperation outcomes that reduced sentences for some witnesses.

In addition to Bond’s expected trial, the FTX criminal docket has largely reached resolution for several other participants. Sam “SBF” Bankman-Fried and Caroline Ellison—former Alameda Research CEO—were convicted or sentenced in separate proceedings. Two other former executives, Nishad Singh and Gary Wang, were given time served after testifying against Bankman-Fried at trial, reflecting the structure of cooperation-driven outcomes.

Parallel litigation: Bankman-Fried’s appeal and pardon bid

While Bond’s matter moves toward trial, Sam Bankman-Fried remains at a different procedural stage. Authorities convicted him on seven felony charges and sentenced him to 25 years in prison in 2024. Although Bankman-Fried sought to appeal his conviction and sentence, the Second Circuit recently rejected his appeal, leaving limited avenues for relief.

Separately, Bankman-Fried has pursued clemency routes, including applying for a presidential pardon from Donald Trump. However, as the appellate process has narrowed, the practical pathway to freedom is now tied either to further legal escalation to the U.S. Supreme Court or to executive action via pardon—an uncertainty that continues to shape the political and legal discourse around the case.

For institutional observers, this matters less because it affects crypto markets directly and more because it highlights how high-profile crypto fraud enforcement can diverge into distinct tracks: courtroom adjudication, sentencing appeals, and executive clemency. These overlapping tracks can influence how defense strategies and prosecutorial positions are evaluated in future cases with similar fact patterns involving financial wrongdoing and political or public-facing conduct.

Closing perspective

Bond’s Nov. 9 trial date sets a clear procedural next step, but unresolved questions around the indictment’s dismissal arguments—and how courts treat alleged assurances connected to plea deals—could still be consequential if litigated through motions and pretrial rulings. As the remaining FTX-related prosecutions narrow toward final outcomes, compliance professionals should watch how courts evaluate links between crypto-linked funding flows and regulated activity outside the financial sector, including campaign finance rules.

Crypto World

Ethereum Holds Near $1,600 as Whale Activity and Stablecoin Data Hint at a Potential Trend Reversal

TLDR:

- Ethereum is trading near $1,600, approximately 21% below its 30-day peak amid sustained market weakness.

- Two whale wallets withdrew $58.83M in ETH from Kraken and Bitgo, matching prior Bitmine purchase patterns.

- Binance stablecoin reserves and netflows have shifted to neutral, signaling a pause in aggressive capital flight.

- The bullish regime shift probability has climbed to 45%, but confirmation signals are still needed before acting.

Ethereum is trading around $1,600, roughly 21% below its 30-day peak, as on-chain data and whale activity draw renewed attention.

A quantitative regime model currently enforces a highly defensive stance, limiting market exposure to just 15%. Yet underlying metrics are shifting, with the probability of a bullish regime transition climbing to 45%.

Analysts and market observers are watching closely for confirmation signals before adjusting their positioning.

Defensive Model Meets Stabilizing Liquidity

Ethereum’s current price decline reflects a broader period of caution across crypto markets. The systematic regime model relies on multiple data layers, not price action alone.

It factors in Bitcoin’s structural cycles, derivative flows, and stablecoin dynamics on major exchanges like Binance.

Trend filters remain weak, with a moving average death cross showing a spread of -18.8%. That reading keeps the model in a highly defensive mode, reducing exposure significantly. However, momentum indicators tell a different story at the margin.

MACD histograms are contracting positively, suggesting that selling pressure may be running out of steam. This divergence between long-term trend weakness and short-term momentum stabilization is a key feature of the current setup.

Crucially, stablecoin data on Binance adds another layer of nuance. Stablecoin reserves registered a z-score of -0.32σ, while netflows came in at +0.20σ, both now in neutral territory.

This suggests the aggressive capital flight seen during deep corrections has paused, and exchange liquidity is no longer actively draining.

Whale Withdrawals Add a Bullish Variable

On-chain intelligence firm Arkham flagged notable activity from two fresh whale addresses this week. The wallets withdrew a combined $58.83 million worth of Ethereum from Kraken and Bitgo within hours.

Arkham noted that the purchase patterns matched prior observed activity linked to Bitmine, raising speculation about institutional accumulation.

Arkham posted on X: “Is Tom Lee stacking ETH this week?” referencing Bitmine chairman Tom Lee, known for public bullish stances on digital assets. The withdrawal pattern drew attention because it occurred against a backdrop of broader price weakness.

Ethereum recorded a 2.94% decline over the past 24 hours and a 7.43% drop over the past seven days, with 24-hour trading volume reaching $13.08 billion. Despite that, large-wallet behavior suggests some participants are positioning ahead of a potential reversal.

A decisive shift in Binance stablecoin netflows toward positive territory could serve as an early signal of returning risk appetite.

Until that confirmation arrives, the data supports patience rather than conviction in either direction. Ethereum’s next move may depend on whether these liquidity and behavioral signals continue to align.

Crypto World

Ethlabs Will Overlap with the Ethereum Foundation and Draw Its 'Densest Talent,' Funders Say

Ethlabs, a new Ethereum research lab backed by the network's two largest corporate holders, launched this week with a pitch to complement the Ethereum Foundation. Its own funders concede it will also compete as Ethlabs is “playing to win.” "I think they will be complementary," Joseph Chalom, chief… Read the full story at The Defiant

Lucky note in phone, Gurindervir Singh targets sub-10 mark | More sports News

Mistral launches OCR 4, turning document extraction into a full enterprise AI play

Money! – Kaytoven (money money green green) (Slowed + Reverb)

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment4 days ago

Entertainment4 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Tech2 days ago

Tech2 days agoMicrosoft accidentally kills epic Outlook email threads

-

Sports1 day ago

Sports1 day agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Business4 days ago

Business4 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics6 days ago

Politics6 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Crypto World20 hours ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World17 hours ago

Crypto World17 hours agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Politics5 days ago

Politics5 days agoAndy Burnham and the meaning of Makerfield

-

Business22 hours ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Business5 days ago

Business5 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

NewsBeat5 days ago

NewsBeat5 days agoKeir Starmer Allies Question His Chances For No 10

-

Tech6 days ago

Tech6 days agoAWS enters the context layer race with a graph that learns from agents, not manual curation

-

Crypto World5 days ago

Crypto World5 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Crypto World5 days ago

Crypto World5 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World5 days ago

Crypto World5 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Tech3 days ago

Tech3 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Entertainment5 days ago

Entertainment5 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Tech2 days ago

Tech2 days agoNearly 7,000 fake Amazon domains registered ahead of Prime Day 2026, researchers warn

-

Business6 days ago

Business6 days agoBrexit cost 6% of UK economy, Bank of England company data suggests

You must be logged in to post a comment Login