Crypto World

Saylor’s Bitcoin Flywheel Is Now Spinning in Reverse

Strategy turned a software company into the largest corporate Bitcoin holder on earth by exploiting a simple loop: trade above your Bitcoin’s value, issue stock, buy more Bitcoin, repeat. In June 2026, Bitcoin broke below $60,000, the stock fell under its own Bitcoin value, and the loop began running the other way. Here is how the machine works, why it reverses, and whether Saylor is actually trapped.

Summary

- Strategy’s mNAV fell to roughly 0.80, meaning its stock trades below the value of the Bitcoin it holds, which disables the premium-funded loop the company used to grow.

- The same reflexive flywheel that compounded gains on the way up now compounds pressure on the way down: at a discount, issuing equity destroys Bitcoin per share, and issuing preferred stock turns expensive, choking both funding taps at once.

- Annual dividend obligations across its preferred stack quadrupled to about $1.2 billion while cash reserves fell roughly 38%, collapsing dividend coverage from more than seven years to around 14 months.

- STRC, the key funding instrument, trades near $82 against a $100 par value, and a tiny 32-Bitcoin sale to fund a dividend broke Strategy’s long-standing never-sell narrative.

- Analysts are split between a “trap” thesis and a “strained but not broken” view, and the outcome hinges almost entirely on Bitcoin’s price, with a roughly $1 billion debt maturity in 2027 as the key deadline.

For five years, Michael Saylor ran one of the most effective financial machines in modern markets, a self-reinforcing loop that converted a mid-sized software company into the largest corporate holder of Bitcoin on earth, with more than 847,000 coins on its balance sheet.

The machine had a simple engine at its center: as long as Strategy’s stock traded at a premium to the value of the Bitcoin it held, the company could issue new shares or preferred stock above that value, use the cash to buy more Bitcoin, and increase the amount of Bitcoin backing each existing share, which justified the premium and let the loop run again. It was elegant, it was relentless, and for a long time, it worked spectacularly, turning Strategy into a Bitcoin proxy that often rose faster than Bitcoin itself.

In late June 2026, that engine threw itself into reverse. Bitcoin crashed below $60,000, Strategy’s stock fell beneath the value of its own Bitcoin, and the loop that had compounded gains on the way up began compounding pressure on the way down.

This piece explains how the flywheel works, why a falling price flips it into a doom loop, and whether Saylor is genuinely trapped or merely strained.

The reason this matters far beyond one company is that Strategy is the template. Hundreds of imitators built Bitcoin and crypto treasury companies on the same premium-driven logic, and the entire category has never faced a real test of what happens when the premium evaporates, and the price of the underlying asset sits below cost.

Strategy is now running that experiment in public, with its stock at a multi-year low, a stack of preferred shares trading below their face value, a dividend bill that has quadrupled in six months, and analysts openly debating whether the company can keep funding itself without selling the Bitcoin on which its entire identity is built, never selling.

The mechanics are intricate, but the core story is one of reflexivity, a feedback loop that amplifies whatever direction the market is already moving, and the lesson it is teaching is that a flywheel is only a flywheel while the premium holds.

The machine that made Strategy the biggest Bitcoin holder on earth

To understand why Strategy is in trouble, you first have to understand why it worked so well, because the same mechanism does both. The key number is something analysts call mNAV, shorthand for the ratio between the company’s market value and the net asset value of the Bitcoin it holds.

When mNAV is above one, the stock trades at a premium: investors are paying more for a share of Strategy than the Bitcoin behind that share is worth. That premium is the fuel for the entire engine. When the stock trades above the value of its Bitcoin, Strategy can issue new shares into the market, raise cash at that elevated price, spend the cash on more Bitcoin, and end up with more Bitcoin per share than it started with, even after the new shares dilute the count. Existing shareholders come out ahead, the higher Bitcoin-per-share figure justifies the premium, and the company can do it all again.

This is the flywheel, and for years it spun in Strategy’s favor with remarkable force. Every time Bitcoin rose, the premium tended to widen, which let Strategy raise more capital on better terms, which bought more Bitcoin, which lifted Bitcoin-per-share and the stock alongside it.

The company layered on a second source of fuel, a series of preferred stock instruments that let it raise money without diluting common shareholders directly, expanding the machine’s capacity. By accumulating relentlessly through this loop, Strategy built a position of more than 847,000 Bitcoin, acquired at an average price of roughly $76,000 per coin, and turned itself into the way many investors chose to hold leveraged exposure to Bitcoin through a regular brokerage account.

Saylor made perpetual accumulation the company’s whole identity, and the premium-funded flywheel was the mechanism that made the accumulation possible. The crucial thing to notice, the thing that explains everything that followed, is that the entire machine depends on that premium. Take away the premium, and the engine does not just slow down. It runs backward.

The week the premium died

That is precisely what happened in the final week of June 2026, and the speed of it caught even seasoned observers off guard. Bitcoin, which had been grinding lower for weeks beneath all of its major moving averages, broke hard, falling to around $59,000 in its worst single-day drop in months, a decline of roughly 5% that triggered a cascade of forced liquidations across crypto derivatives markets, with about $1.1 billion of leveraged positions wiped out in a single day. Strategy fell with it, as it almost always does, but it fell further.

The stock dropped more than 10% to around $92, then slid the next session again, breaking below $100 for the first time since early 2024 and hitting a two-and-a-half-year low. From its peak, the stock had lost roughly 81% of its value, erasing on the order of $150 billion in market capitalization.

The number that mattered most, though, was not the stock price or even the Bitcoin price. It was the mNAV, which fell to approximately 0.8. Strategy was now trading at a discount to its own Bitcoin: the market valued the company at less than the coins on its balance sheet were worth.

For a company whose entire model rests on trading at a premium, crossing below 1 is not a cosmetic change but a structural one, because it disables the engine. And it disabled both halves of that engine at once. With the common stock below the value of its Bitcoin, issuing new shares would destroy Bitcoin-per-share rather than build it.

With the preferred shares trading well below their face value, raising money through new preferred issuance had become punishingly expensive. Both capital taps, the two ways Strategy funds itself, were constrained at the same moment, and the company found itself holding more than 847,000 Bitcoin bought at an average price far above the current one, sitting on an estimated $10.6 billion in unrealized losses, with every coin it purchased in 2024, 2025, and 2026 underwater. The premium that powered the flywheel was gone, and without it, the machine had nothing to run on.

Why a discount breaks the flywheel

It is worth being precise about why crossing below an mNAV of one is so damaging, because the reversal is not merely the absence of the previous tailwind; it is an active headwind. Run the flywheel logic backward, and the problem becomes clear.

At a premium, issuing stock to buy Bitcoin increases Bitcoin-per-share, which helps shareholders. At a discount, the same action does the opposite: if the company issues shares below the value of its Bitcoin and uses the proceeds to buy more, each existing share ends up backed by less Bitcoin than before, not more, because the new shares were sold for less than the Bitcoin they represent.

The accretive loop becomes a dilutive one. The single most important tool Strategy used to grow now actively harms the shareholders it is meant to serve, which means the company effectively cannot use it. The equity engine does not just idle at a discount; it goes into reverse if switched on.

The preferred-stock engine suffers a parallel breakdown. Strategy’s preferred instruments were designed to raise money efficiently, but that efficiency depended on those instruments trading at or above their face value. When they slip well below face value, the company can only issue new ones by effectively promising a much higher yield, which makes the funding expensive and, past a point, impractical. So the second tap tightens just as the first one closes.

The result is a company that, at the very moment its Bitcoin is underwater, and its cash needs are rising, has lost the two mechanisms it relied on to raise money. This is the essence of reflexivity, the property that makes the model so powerful in both directions.

On the way up, a rising price widens the premium, which eases funding, which buys more Bitcoin, which lifts the price further. On the way down, a falling price kills the premium, which chokes funding, which raises the specter of selling Bitcoin to cover obligations, which threatens to push the price down further still. The machine is built to amplify, and amplification is wonderful until the direction changes.

STRC: the funding engine that stalled

Nowhere is the stall more visible than in the preferred instrument Strategy nicknamed Stretch, which trades under the ticker STRC and has become the clearest barometer of the company’s stress.

STRC is a perpetual preferred stock, meaning it has no maturity date, with a variable dividend rate that the company resets monthly with the explicit goal of keeping the security trading near its $100 face value.

Strategy launched it in mid-2025 through an offering that raised roughly $2.5 billion, marketing it to income-seeking investors as something close to a high-yield savings account, a stable instrument paying a generous dividend, recently around 11.5%, distributed in cash twice a month.

As a fundraising engine, STRC was meant to let Strategy raise money to buy Bitcoin without diluting common shareholders, and it worked beautifully while it traded at or above face value.

In June 2026, STRC broke down. It fell to record lows near the low 80s, roughly 17% below its face value, and that gap is what signals the engine has stalled. The loop only works above par: when STRC trades above $100, Strategy can issue new shares and funnel the proceeds into Bitcoin cheaply. Below par, that mechanism breaks, because issuing new preferred stock at a discount means accepting a far higher effective cost of capital.

The decline also drew a pointed accusation from longtime Bitcoin critic Peter Schiff, who argued that Saylor had marketed STRC to risk-averse retirees by assuring them the volatility had been stripped out, and that with the instrument now well below what many paid for it, erasing close to two years of dividends in price terms, the company had made material misrepresentations. Strategy’s defenders counter that the dividend rate resets precisely to pull the price back toward par over time, and that the decline reflects the market demanding a higher yield in a stressed environment rather than a fundamental break.

Either way, the practical reality is the same: the instrument designed to be Strategy’s smooth, reliable funding engine is sputtering, and a sputtering STRC means the company has lost its least dilutive way to raise cash at the worst possible time.

The dividend bill nobody is talking about enough

While the headlines fixate on the Bitcoin price and the stock, the more immediate pressure on Strategy is something quieter and arguably more dangerous: a cash squeeze created by its own dividend obligations. As Strategy issued more and more preferred stock to fund its Bitcoin buying, it accumulated a growing stack of instruments, STRC alongside others trading under tickers like STRK, STRF, STRD, and STRE, each carrying a dividend that must be paid in cash.

The combined annual obligation across all of them has ballooned from roughly $300 million at the start of 2026 to approximately $1.2 billion by June, a near fourfold increase in under six months. That is $1.2 billion a year the company must pay out, regardless of what Bitcoin does, regardless of whether its stock trades at a premium or a discount.

Against that rising bill, the company’s cash cushion has shrunk. Strategy’s dollar reserves fell by about 38% over the first half of 2026, partly because it spent roughly $1.5 billion in May buying back convertible notes, draining the very buffer that supports the dividends. The result is a metric that has deteriorated alarmingly: dividend coverage, a measure of how long the cash reserve could keep funding the payouts, collapsed from more than seven years to around 14 months.

One prominent analytics firm calculated that Strategy would need to rebuild its reserves to roughly $2.8 billion to restore a comfortable two years of coverage, and urged the company to halt Bitcoin purchases entirely until it does.

The squeeze is structural and self-inflicted: the more preferred stock Strategy issued to buy Bitcoin, the larger its perpetual cash obligations grew, and those obligations do not pause when Bitcoin falls. Crucially, the dividends are cumulative, meaning any payment Strategy skips still has to be made up later, so the company cannot simply switch them off to conserve cash without damaging its standing with the investors it depends on.

This is the real near-term pressure point. It is not that Bitcoin is down; it is that the bills come due in dollars, the dollar reserve is shrinking, and the usual ways of refilling it have stopped working.

The 32-Bitcoin sale that said everything

The moment that crystallized the market’s anxiety was almost comically small in scale. In late May and early June 2026, Strategy sold 32 Bitcoin, worth around $2.5 million, to help fund a distribution on its preferred stock.

Against a holding of more than 847,000 coins, 32 Bitcoin is a rounding error, a fraction of a fraction of the stack. And yet the disclosure sent a shock through the market, with Strategy’s shares falling more than 9% in a single session and Bitcoin itself sliding on the news. The reaction was wildly out of proportion to the size of the sale, which is exactly what made it significant.

The reason a negligible sale moved the market so much is that it broke a narrative. For years, Saylor’s defining promise was that Strategy buys Bitcoin and never sells it, that the company is a one-way accumulation vehicle whose conviction is absolute. The 32-coin sale, however tiny, was the first time in roughly 4 years that Strategy had sold any Bitcoin at all, and it was sold not opportunistically but to cover a cash obligation.

The company framed it as a demonstration of strength, proof that it could meet its dividend commitments through asset sales if needed. The market read it the opposite way: as the first visible crack in the never-sell promise, and as confirmation that the dividend machine had grown large enough to force sales of the asset it was built to accumulate.

A treasury company that has to sell its treasury to pay its bills has crossed a psychological line, and the size of the sale is almost beside the point. What investors saw was the principle giving way, and the principle was the whole story. Once the market accepts that Strategy will sell Bitcoin to meet obligations, the only remaining question is how much and how often, and that question hangs over everything.

Is Saylor actually trapped?

This brings us to the word that has attached itself to Saylor’s situation: trapped.

The trap thesis, laid out by several analysts, runs like this. Strategy cannot effectively buy, because at a discount, raising money to purchase Bitcoin destroys shareholder value rather than creating it. It cannot easily sell, because dumping Bitcoin would crystallize billions in losses and, given Strategy’s size, would likely push the Bitcoin price down further, deepening the very problem it is trying to solve and harming the asset that underpins the entire structure. And it cannot comfortably stand still, because the dividend obligations keep coming due in cash, the reserve keeps shrinking, and the preferred shares keep signaling stress.

One veteran portfolio manager assigned rough odds to the outcomes, putting his base case at a 70% chance that Strategy keeps selling small amounts of stock at unfavorable, non-accretive levels, slowly grinding the mNAV down toward an even steeper discount, with a smaller chance that Saylor sells several billion dollars of Bitcoin outright to buy time. In this reading, every available move makes some part of the structure worse, which is what a trap means.

The case against the trap framing deserves equal weight, because the situation, while genuinely strained, is not the same as imminent collapse, and several analysts argue exactly that. Forced selling is not actually required right now. Strategy is not contractually obligated to sell Bitcoin to defend its preferred shares; it can raise the dividend rate, issue shares even at unattractive levels, or use other tools to signal it can keep paying, and it has been doing so. It still holds an enormous, unencumbered Bitcoin position and retains real flexibility.

One prominent equity analyst reiterated a buy rating with a price target far above the current level, describing the preferred-stock decline as a market-driven reset of the yield investors require instead of a structural breakdown, a sign of a model strained but not broken.

Saylor himself points out that, despite the brutal drawdown, the stock remains a multiple of where it traded when he began buying Bitcoin in 2020, and that the company’s long-term objective is to maximize Bitcoin per share over the years, not to defend any particular monthly price. And the entire predicament reverses if Bitcoin simply recovers: a rising price would restore the premium, reopen the funding taps, and turn the flywheel forward again.

The honest assessment is that Strategy is under real, compounding pressure with a narrowing set of good options, which is a serious condition, but it is not yet insolvency, and conflating strain with doom is its own kind of error.

The 2027 wall and the price that has to hold

If you want to know what the market is really watching for, look past the daily price swings to a specific date and a specific number. Strategy carries debt, and one analyst has flagged roughly $1 billion of it maturing in September 2027.

To repay that obligation without selling Bitcoin, the reasoning goes, Strategy’s stock would need to trade above roughly $183, a level that corresponds to a Bitcoin price somewhere around $91,500 at an mNAV of one.

With the stock near or below $100 and Bitcoin around $60,000, the company sits far below that threshold, which is why the 2027 maturity has become a focal point. It is not an immediate crisis, since the date is more than a year out and Strategy has tools and time, but it functions as a deadline against which all the other pressures are measured. The runway is real, but it is not unlimited.

This frames the two scenarios cleanly. In the recovery scenario, Bitcoin climbs back over the months ahead, Strategy’s stock returns to a premium, the funding engine reopens, the preferred shares drift back toward par, and the dividend coverage rebuilds, at which point the trap dissolves, and the flywheel resumes spinning forward, exactly as it has after previous Bitcoin downturns.

Saylor’s entire bet is that this is what happens, that Bitcoin’s long-term trajectory rescues the structure as it always has before, and that conviction through the drawdown is the price of the eventual recovery.

In the adverse scenario, Bitcoin stays low or falls further, the discount persists, STRC remains below par, the cash reserve keeps shrinking against the $1.2 billion dividend bill, and Strategy is forced into steady, value-destroying sales of stock or, eventually, Bitcoin, grinding the structure down toward the 2027 wall in a weakened state.

The truth is that no one knows which path unfolds, because it depends overwhelmingly on the one variable Saylor cannot control, the price of Bitcoin. What can be said is that the model has lost its margin for error. For years, the flywheel gave Strategy the luxury of never having to be right about timing. Now, for the first time, timing matters, and the company is waiting on a price recovery it can only hope for.

What it means beyond Strategy

Step back from the single company and the larger significance comes into focus, because Strategy is not an isolated case but the original of a type. Its success spawned a wave of imitators, more than 200 Bitcoin and crypto treasury companies built on the identical premium-driven logic, each raising capital against a market premium to its holdings and buying more of the underlying asset, each implicitly assuming the premium would persist.

None of these companies had truly been tested by a sustained environment in which the underlying asset trades below their cost and the premium turns into a discount, because that environment had not arrived at scale.

Now it has, and Strategy, as the largest and most leveraged example, is the stress test the entire category is watching. What breaks or holds at Strategy tells every imitator something about the durability of the model they copied.

The deeper lesson is about the nature of reflexivity itself, and it is a lesson that applies to far more than Bitcoin treasuries. A reflexive machine, one whose inputs feed its outputs feed its inputs, is a wealth-compounding marvel while the cycle runs in your favor and a value-destroying trap when it runs against you, and the same features that make it powerful in one direction make it dangerous in the other.

Strategy’s flywheel did not change; the direction did, and that was enough to convert the most admired financial engine in crypto into a structure that analysts now describe with words like pickle and trap. Whether Saylor escapes depends on Bitcoin, and Bitcoin has rescued him before, which is why writing the company off would be as foolish as assuming it is invincible.

The honest watch list is short and specific: whether the mNAV climbs back above one, whether STRC reclaims its par value, whether the dividend coverage stabilizes, whether the company sells more Bitcoin, and above all, whether Bitcoin’s price recovers in time. Until those questions resolve, the machine that built the largest corporate Bitcoin position on earth is spinning in reverse, and everyone who copied it is watching to see how far backward it goes.

Frequently Asked Questions

What is mNAV and why does it matter for Strategy?

mNAV is the ratio between Strategy’s market value and the net asset value of the Bitcoin it holds. Above 1, the stock trades at a premium to its Bitcoin, which lets the company issue shares above that value, buy more Bitcoin, and increase Bitcoin per share, the loop that powered its growth. In June 2026, mNAV fell to about 0.8, meaning the stock trades at a discount to its own Bitcoin. That breaks the engine, because issuing shares at a discount destroys Bitcoin per share instead of building it, disabling Strategy’s main way of funding itself.

Why is Strategy’s flywheel now working against it?

Because the model is reflexive, amplifying whatever direction the market is moving. At a premium, a rising Bitcoin price widens the premium, eases funding, and buys more Bitcoin, lifting the stock further. At a discount, a falling price kills the premium, chokes funding, and raises the prospect of selling Bitcoin to cover obligations, which can push the price down further. The same mechanism that compounded gains on the way up now compounds pressure on the way down. Both of Strategy’s funding taps, common equity and preferred stock, are constrained at once because the stock trades below its Bitcoin value.

What is STRC and why is its price important?

STRC, nicknamed Stretch, is Strategy’s perpetual preferred stock, with a variable dividend reset monthly to keep it trading near its one-hundred-dollar face value. It was a key fundraising engine: when it trades above face value, Strategy can issue more and buy Bitcoin cheaply without diluting common shareholders. In June 2026, it fell to record lows near the low eighties, well below par, which breaks that mechanism, because issuing new preferred at a discount means a much higher cost of capital. Its slide is the clearest market signal that Strategy’s smoothest funding source has stalled.

Is Michael Saylor being forced to sell Bitcoin?

Not in a forced, contractual sense, at least not yet. Strategy did sell thirty-two Bitcoin in mid-2026 to fund a dividend, its first sale in about four years, which alarmed the market as a symbolic break from its never-sell stance. But the company is not required to sell to defend its preferred shares; it can raise the dividend rate, issue shares, or use other tools, and it retains a large, unencumbered Bitcoin position. The risk is that persistent stress leads to steady, value-destroying sales over time. Analysts consider a near-term forced liquidation unlikely, while disagreeing on how much pressure builds from here.

Why did selling just 32 Bitcoin matter so much?

Because it broke a narrative instead of a balance sheet. 32 Bitcoin is a rounding error against Strategy’s 847,000-coin stack, but it was the first sale in roughly four years and was made to cover a cash obligation, not to take profit. Saylor’s defining promise was that Strategy buys and never sells, so any sale, however small, signaled that the dividend machine had grown large enough to force sales of the asset it exists to accumulate. Once the market saw the never-sell principle give way, the only remaining questions were how much and how often, which is why a tiny sale moved the stock sharply.

Could Strategy recover, or is the model broken?

It could recover, and the outcome depends overwhelmingly on Bitcoin’s price, which Saylor cannot control. If Bitcoin climbs back, the premium returns, the funding taps reopen, the preferred shares drift toward par, and the flywheel resumes spinning forward, as it has after past downturns. If Bitcoin stays low, the discount persists, the cash squeeze from a $1.2 billion dividend bill worsens, and the company faces steady, value-destroying sales heading toward a roughly $1 billion debt maturity in 2027. Some analysts call the model strained but not broken; others see a trap. The honest answer is that the margin for error is gone, and timing now matters.

This article is information, not investment advice. It describes a fast-moving and contested situation, and prices, holdings, dividend obligations, and analyst views change quickly. Figures reflect reporting available as of June 25, 2026. Cryptocurrency and equities are volatile, and nothing here is a recommendation to buy or sell any asset. Verify current data from primary sources and consider your own circumstances before making any decision.

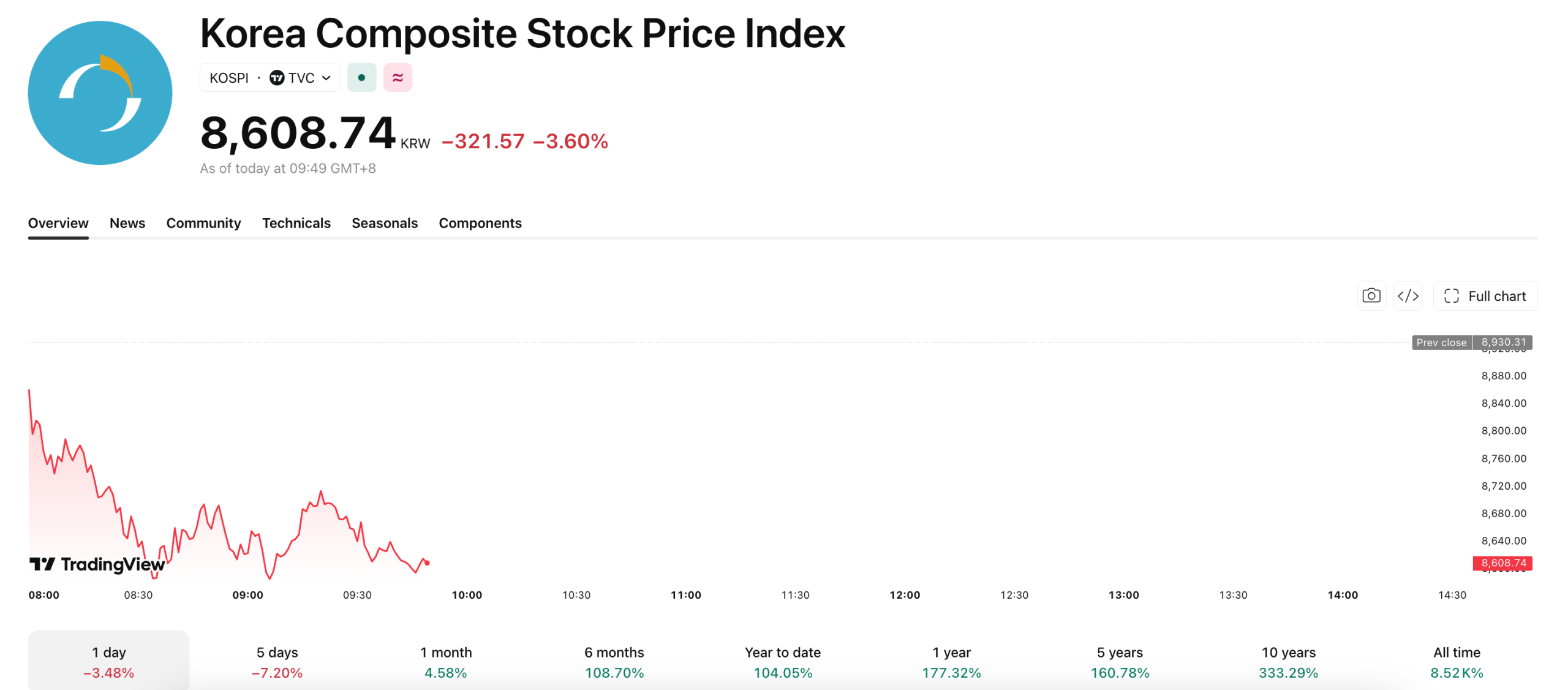

At the same time, SoftBank Group dropped more than 12%, fueling a broad Asian selloff after Apple and Microsoft raised product prices, confirming that soaring AI chip costs have begun forcing Big Tech’s hand.

South Korea’s KOSPI showed the damage of a Western market in flux. June 25th’s close was 8,930.31, but it quickly dropped in early trading on Friday to around 8,600.

AI Chip Crisis Reaches the Consumer

Apple raised prices on MacBooks and iPads by up to $300 on June 25, citing an “unprecedented” surge in memory and storage chip costs driven by AI data center demand. Its shares closed more than 6% lower.

Microsoft followed hours later, announcing Xbox console price increases of $100 to $150 per model, effective August 1. Microsoft stock fell 3.5%. The back-to-back announcements from two of the world’s most valuable technology companies confirmed what investors had feared: the AI chip shortage is no longer an industry-level problem. It now hits consumer prices directly.

Asia Bears the Brunt

That confirmation rattled Asian markets on Friday. South Korea’s SK Hynix and Samsung fell more than 4%. SK Square, a technology holding company with heavy semiconductor exposure, declined around 7%. Japan’s chip equipment maker Advantest dropped more than 6%, while Tokyo Electron fell over 2%.

SoftBank faces additional headwinds beyond the regional selloff. Its chip design subsidiary Arm Holdings fell 3.2% overnight, underperforming even as broader AI stocks recovered.

Analysts at Ortus Advisors noted investor enthusiasm for SoftBank may also be capped by reports that OpenAI could push back its IPO to 2027, as the company struggles to attract demand at a $1 trillion valuation. SoftBank ranks among OpenAI’s most prominent backers.

Matt Maley, strategist at Miller Tabak, put the broader concern plainly.

“A few cracks have developed in the tech sector recently. Therefore, we believe it will be extremely important to watch how these hyperscalers trade going forward because if they continue to decline, it’s going to make it very tough for the rest of the market to advance.”

— Matt Maley, Miller Tabak

Micron’s stronger-than-expected earnings and Qualcomm’s AI data center chip deal with Meta offered partial relief. But SoftBank’s aggressive AI infrastructure bets leave it particularly exposed to any sustained repricing of the trade.

The post Asia’s Tech Stocks Take the Hit as Apple and Microsoft Push Chip Costs to Consumers appeared first on BeInCrypto.

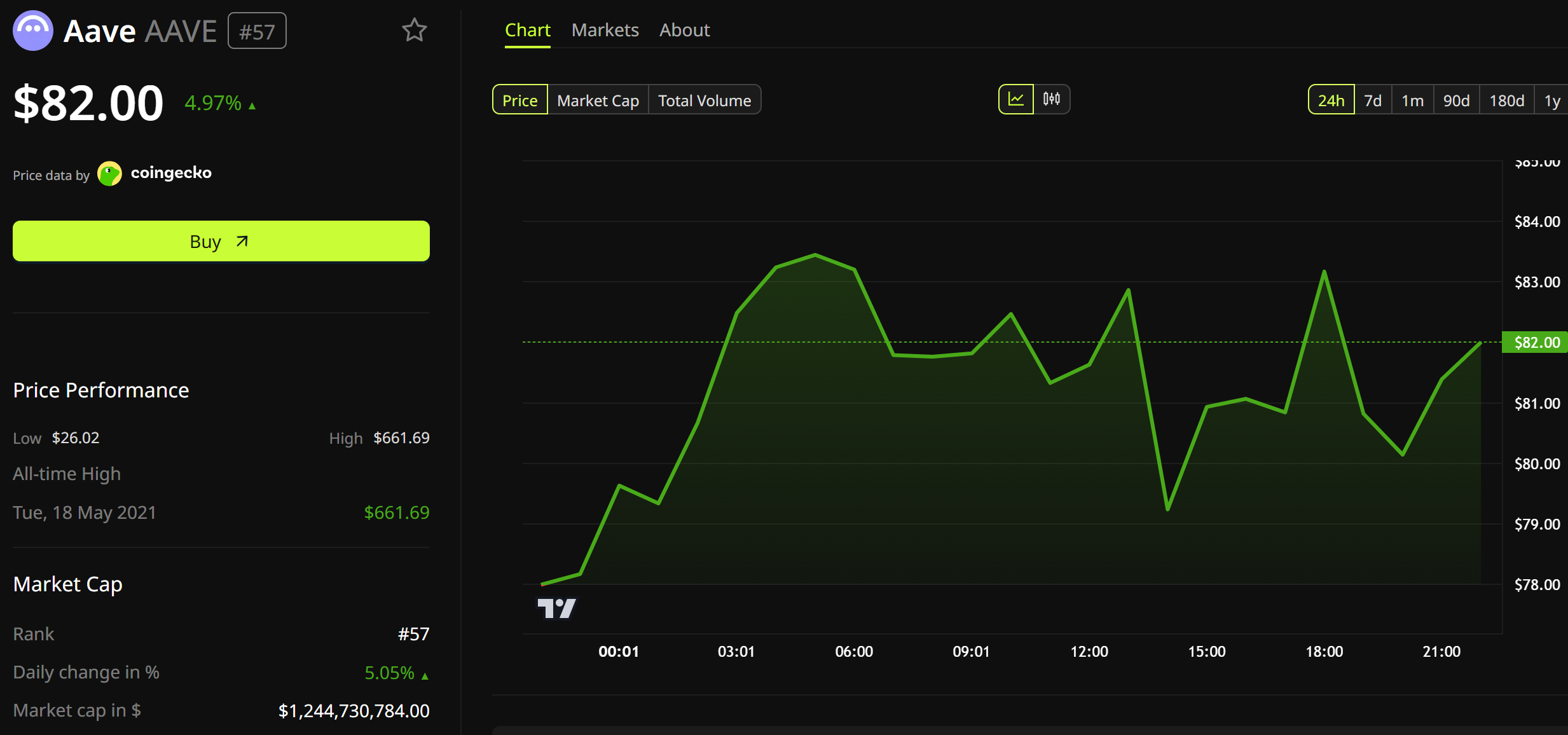

Aave founder Stani Kulechov denied claims that the protocol would sell AAVE tokens at a 70% discount, responding to a report that crypto exchange Kraken is in talks to buy a stake in the lender.

The report described a roughly 15% stake at a $385 million valuation, though neither company has confirmed those terms. AAVE traded near $82, up almost 5% over 24 hours, as the debate spread.

Why the Kraken Aave Stake Report Drew Pushback

The figures behind the report trace to anonymous sources, and Kulechov called the framing inaccurate. He confirmed only that outside parties had discussed buying an AAVE allocation held by Aave Labs.

Any deal would build on an existing tie. In 2025, the Aave DAO voted 99.8% to license its code to Kraken’s Ink network, which now runs a white-label lending market that shares revenue back to Aave.

The talks also surface as Aave rebuilds from April’s KelpDAO exploit, which left up to $230 million in bad debt after attackers borrowed against unbacked tokens.

Although Aave’s smart contracts were never breached, the fallout erased more than a third of its deposits, which sit near $12 billion today.

Kulechov Points to Revenue and Planned AAVE Buybacks

Kulechov rejected the idea that Aave would offload tokens cheaply.

“there is NO WAY we’d sell AAVE at a 70% discount lol,” he articulated.

Follow us on X to get the latest news as it happens

He said Aave Labs only serves the DAO as a service provider and takes none of the protocol’s revenue. That revenue instead routes to token holders under the Aave Will Win framework.

“100% of Aave Protocol and GHO revenue goes to the $AAVE token.”

He also teased Aavenomics 3.0, which would make AAVE buybacks automatic. That extends a discretionary program already cleared to buy up to $50 million of AAVE a year.

The token traded higher after the post.

What Comes Next for Aave and Kraken

A stake would fit Kraken’s acquisition run ahead of its planned public listing. The exchange agreed this year to buy derivatives venue Bitnomial for up to $550 million, securing rare US derivatives licenses.

Some analysts still see sharp upside for the token despite the April setback.

Aave plans a quarterly community call within weeks. Whether the Kraken talks firm up, and how automated buybacks reshape AAVE, should become clearer then.

The post Aave Founder Stani Kulechov Denies Kraken Stake Sale Report, Confirms AAVE Buybacks appeared first on BeInCrypto.

Computer memory chipmaker Micron Technology (MU) delivered blowout Q3 earnings on Wednesday, lifting the entire AI memory sector, AI-related stocks and even giving crypto a slight boost.

Bitcoin climbed back above $60,000 after markets closed, but bullish AI sentiment will ultimately pull more liquidity away from crypto.

Micron shares surged 16% in premarket trading on Thursday after the memory chipmaker’s third quarter guidance exceeded Wall Street expectations. Third-quarter revenue came in at $41.5 billion versus estimates of $35.7 billion, while earnings per share (EPS) reached $25.11 compared with expectations of $20.49.

Memory chips have become the backbone of AI infrastructure, particularly high-bandwidth memory (HBM), which is essential for training and running large AI models. CEO Sanjay Mehrotra told analysts there was “no line of sight” to when supply would catch up with demand, with the shortage expected to persist well beyond 2027.

The company also issued strong fourth quarter guidance, forecasting revenue of approximately $50 billion, well ahead of Wall Street expectations of $43.2 billion.

The AI boom has weighed heavily on the crypto market this year, with bitcoin now more than 50% below its October all-time high, trading at the $60,000 level.

Broadcom (AVGO) and OpenAI have unveiled Jalapeño, OpenAI’s first custom AI chip, and the launch gives the Broadcom-OpenAI partnership a central seat in the AI infrastructure race.

Yet positioning data tells a more cautious story, because money flow and relative strength show large investors quietly favoring rivals like Micron and AMD, even as the headlines belong to Broadcom.

Jalapeño Validates Broadcom’s Whole AI Strategy

OpenAI designed Jalapeño from scratch for large-language-model inference, and Broadcom built it. The chip went from design to manufacturing tape-out in just nine months, which the companies call the fastest such cycle ever in advanced semiconductors. OpenAI’s own models helped speed up the design.

That speed matters because it proves the bet Broadcom has made in its AI business. Broadcom does not sell ready-made AI chips like Nvidia (NVDA). Instead, it co-designs custom chips, known as ASICs, for a single customer and earns design and manufacturing fees.

Jalapeño shows that the model can deliver a frontier chip fast. Every major AI lab now has a reason to design its own chip with Broadcom rather than only buy Nvidia GPUs.

Broadcom CEO Hock Tan said that the launch “validates very well the business model” that every “model maker” and “frontier model developer” will eventually design and build their own silicon, simply because “they can do it much better.”

The numbers behind it are large. Early testing shows performance per watt “substantially better” than the current state of the art, and the platform is set for gigawatt-scale deployment with Microsoft and other partners starting late 2026.

So the catalyst is real, and the Broadcom stock narrative is strong. The flow data, however, does not fully agree.

Money Flow Favors Micron and AMD, Not Broadcom

Despite the headline, AVGO is lagging its own sector. Its relative strength, measured against the chip benchmark SOXX at 100, is 53.6, so the stock is underperforming the group even on its big news day.

The reason sits in the flow data. Chaikin Money Flow (CMF), a proxy for institutional buying and selling pressure, reads -0.006 for AVGO. A negative number signals distribution, meaning more money is leaving the stock than entering it.

The contrast with peers is the real tell. CMF reads +0.169 for AMD and +0.076 for Micron (MU), both firmly in accumulation. The Micron stock might be getting all the post-earnings beat attention.

Big money is rotating into the chipmakers tied to the memory and GPU build-out, not into Broadcom.

This happens because the Jalapeño win is a long-dated story. Deployment starts in late 2026, so traders chasing nearer-term momentum are parking cash elsewhere.

That said, not every corner of the market is selling Broadcom.

Perp Traders and Analysts Stay Bullish on Broadcom Stock

On Nansen, smart-money perpetual traders are net long AVGO by roughly $165,000, with longs outweighing shorts by more than 5-to-1.

The position is small, spread across just two wallets, so the conviction is thin. The same desks are heavily net short Nvidia (NVDA) by about $14 million, which suggests they may see Broadcom as the better near-term bet within the group.

Wall Street is firmer. Every recent analyst action on the stock is a Buy. JPMorgan’s Harlan Sur lifted his broadcom stock price target to $580 from $500, while Oppenheimer sits at $535 and UBS at $485. The stock trades near $390 and is up roughly 10% this year.

The split is clean. The Jalapeño chip and unanimous Buy ratings point up, while AVGO’s negative Chaikin Money Flow of -0.006 and its 53.6 relative strength against SOXX flash the warning. A flip in institutional money flow back above zero is what tips Broadcom back to bullish.

The post Broadcom Built OpenAI’s First Chip in Record Time, but the Money Went Elsewhere appeared first on BeInCrypto.

As AI floods the internet with convincing fake humans, proving that a user is a real, unique person is becoming one of crypto’s hardest and most valuable problems. This guide explains what proof of personhood is, how the leading approaches work, and why the cure raises concerns of its own.

Summary

- Proof of personhood aims to verify that each real person can obtain only one identity while protecting their privacy.

- The technology has gained urgency as AI makes it easier to create convincing fake identities that can exploit voting, airdrops, and online platforms.

- Biometric systems, social trust networks, and zero knowledge identity methods offer different ways to verify unique humans, each with its own tradeoffs between privacy, security, and scalability.

Proof of personhood is a cryptographic mechanism that lets someone prove they are a real, unique human being, one person counted exactly once, without revealing who they actually are. That combination is what makes it both powerful and difficult: it must guarantee uniqueness, so that a single person cannot register as a thousand, while preserving anonymity, so that proving you are human does not force you to expose your identity. The problem it solves is old, but it has become urgent for a new reason. For most of the internet’s history, telling humans from machines was a minor nuisance handled by simple puzzles.

Now, with artificial intelligence able to generate text, images, voices, and entire online personas indistinguishable from a real person’s, the open internet faces a verification crisis: bots can flood platforms, manipulate votes, drain airdrops, and impersonate humans at a scale and quality never seen before. This guide explains what proof of personhood is, the attack it defends against, the main approaches to building it, the leading real-world example and its controversies, and why a technology meant to protect humanity raises hard questions of its own.

The reason this topic has moved to the center of crypto and beyond is that “one real human, counted once,” turns out to be a foundational requirement for a surprising range of things. Fair token airdrops depend on it, or a handful of people with thousands of fake accounts will scoop up everything meant for a community. Democratic voting and decentralized governance depend on it, or whoever can spin up the most identities wins.

Any system that distributes scarce resources to people, from community rewards to the long-discussed idea of a universal basic income, depends on being able to tell one person from a thousand sock puppets. And increasingly, the world of artificial intelligence depends on it, both to keep bots out of human spaces and, in a twist, to let trustworthy AI agents act on behalf of verified humans.

Proof of personhood sits at the intersection of cryptography, identity, and the defining technological anxiety of the moment, which is why it has become one of the most watched and most contested ideas in the field.

The sybil attack: the problem at the root

To understand proof of personhood, you first have to understand the attack it exists to stop, which is called a sybil attack. The name comes from a famous case study of a person with many personalities, and in computing it describes a single actor creating many fake identities to gain influence they should not have. On a network where one identity equals one vote, one share, or one claim, a sybil attacker who controls a thousand identities controls a thousand times the influence of an honest participant who has just one. Almost every open online system that tries to be fair, every vote, every giveaway, every reputation score, every “one person, one share” distribution, is vulnerable to someone who can cheaply manufacture identities.

Historically, sybil attacks were limited by the friction of creating convincing fake accounts at scale, and by crude defenses like puzzles meant to slow bots down. Artificial intelligence demolishes both limits. Modern systems can generate unlimited unique-looking personas, complete with plausible writing, profile photos, and behavior, and can solve the puzzles that once filtered them out.

The very technology that makes AI useful, its ability to produce human-like content, is what makes it the ultimate sybil weapon, capable of populating the internet with armies of fake humans cheaply and convincingly. This is the deeper reason proof of personhood has surged in importance: the old, informal defenses against sybil attacks have broken down precisely when the cost of mounting one has collapsed. If you cannot tell a real, unique human from a generated one, then every system that assumed it could is suddenly exposed, and rebuilding a reliable way to prove humanness becomes foundational infrastructure rather than a nice-to-have.

What a good proof-of-personhood system must achieve

Before looking at how anyone builds proof of personhood, it helps to define what success even requires, because the requirements pull against each other, and that tension shapes every design. A strong system needs to satisfy several properties at once. It must guarantee uniqueness, ensuring each real person can obtain exactly one verified identity and cannot register many. It must preserve privacy, so that proving you are a unique human does not force you to reveal your name, your face, or a linkable record of everything you do. It must resist attack, holding up against sophisticated adversaries, increasingly AI-powered, trying to fake or duplicate humanness. And ideally it must scale to billions of people across every country, language, and level of access, without excluding those who lack documents or technology.

The difficulty is that these goals are in tension. The strongest way to guarantee uniqueness is usually to collect something deeply personal and hard to fake, like a biometric, but collecting biometrics is exactly what threatens privacy and raises ethical alarms. The most privacy-preserving approaches, which avoid collecting sensitive data, often struggle to guarantee uniqueness or to resist a determined attacker.

Scaling to everyone on earth conflicts with the careful, high-assurance verification that strong uniqueness demands. Every proof-of-personhood design is, in effect, a particular set of compromises among uniqueness, privacy, security, and inclusivity, and there is no design that maximizes all four at once. Understanding a given system, therefore, means asking which of these properties it prioritizes and which it sacrifices, because that choice, more than any technical detail, determines what the system is good for and what it puts at risk.

The main approaches to proving humanness

There are several broad families of proof-of-personhood design, each making a different bet about how to balance those competing goals. The first and most discussed is biometric verification, which uses a physical trait of the human body, an iris, a face, that is hard to fake and naturally unique, to guarantee one person equals one identity. The bet here is that specialized hardware reading a unique biological signal is the only approach robust enough to resist an adversarial, AI-saturated environment, because you cannot generate a real human iris with a language model. The strength is powerful uniqueness; the cost is the privacy and ethical weight of collecting biometric data and the need for physical hardware and in-person enrollment.

A second family is the social-graph approach, which builds humanness through webs of trust: real people vouch for other real people, and the network of mutual verification makes it hard for a lone attacker to fake many identities, because each fake one would need real humans willing to vouch for it. This avoids collecting biometrics and leans on human relationships instead, but it can struggle to scale and to resist a well-resourced attacker who infiltrates the graph. A third family relies on credentials and accumulated signals, combining evidence like existing verified accounts, on-chain history, or government documents into a score or a passport that suggests a unique human without a single biometric gatekeeper.

This is flexible and privacy-conscious but generally offers softer guarantees of uniqueness than a biometric. A fourth, emerging family uses zero-knowledge identity techniques, proving facts about yourself, that you are an adult, that you are a unique holder of some credential, without revealing the underlying data, and increasingly leans on device-based passkeys and similar tools. Each family is a different answer to the same question, and the field has not settled on a winner, because each answer sacrifices something the others preserve.

The leading example: World and the Orb

The most prominent attempt to build proof of personhood at global scale is the project now called World, formerly Worldcoin, created by a company co-founded by the chief executive of a leading artificial intelligence lab alongside other founders, and launched in 2023. World made the boldest possible bet on the biometric approach, and examining it concretely shows both the promise and the problems of the whole field. Its centerpiece is a custom hardware device called the Orb, a polished sphere that scans a person’s iris.

The reasoning is that the iris is highly unique and extremely hard to forge, so an in-person iris scan is a strong way to guarantee that each verified human is counted exactly once, even against AI adversaries that can fake almost anything made of pixels but cannot fake a living eye on demand.

The privacy design is central to World’s pitch, because iris scanning sounds alarming and the project knows it. According to the project, when the Orb scans your iris it generates a unique cryptographic code, deletes the actual image after processing, and distributes only anonymized fragments of the code across a network to confirm you have not enrolled before.

The result is meant to be a credential, called a World ID, that proves you are a unique human without revealing your identity or storing your biometric image, with zero-knowledge techniques letting you later prove “I am a verified unique human” to an app without exposing anything else. The project reports a scale no other proof-of-personhood effort has reached, on the order of millions of people verified through Orbs and a widely used identity app, which is a meaningful achievement for a category that has historically struggled to grow. World is, in short, the clearest real-world test of whether the biometric approach can become global infrastructure, and its trajectory, successes and backlash alike, is where the abstract debate over proof of personhood becomes concrete.

The AI age and the pivot to verifying agents

What has thrust proof of personhood from a niche idea into a mainstream conversation is the arrival of capable artificial intelligence, and the relationship between the two is closer than it first appears. The same advances that make AI able to flood the internet with fake humans also make a reliable proof of humanness more valuable, because humanness is becoming the scarce, trustworthy thing in a sea of synthetic content. This is why a figure deeply associated with frontier AI is also behind the leading proof-of-personhood project: one venture helps create the problem of indistinguishable machine-generated humans, and the other proposes the verification layer to manage it. As AI-generated text, images, video, and behavior become impossible to tell from the real thing, a system that can certify “a unique human is behind this” turns into foundational infrastructure for trust online.

There is a striking twist in how the field is now evolving. Proof of personhood started as a way to keep bots out of human spaces, but it is increasingly being repurposed to let AI agents operate responsibly within human systems. As autonomous AI agents begin acting on people’s behalf, making purchases, sending messages, executing tasks, a new question arises: which human is this agent acting for, and is that human real and accountable? Proof-of-personhood projects have begun building tools that tie an AI agent to a verified human principal, so that an agent can prove it represents a genuine, unique person rather than running wild as an anonymous bot.

The leading project has also pivoted toward enterprise use, selling proof-of-humanity verification to companies, video platforms, and identity providers that want high assurance a user is real, while keeping the service free for the individuals being verified. The through-line is that AI did not just create demand for proving humans are human; it is reshaping proof of personhood into a layer that governs both humans and the machines acting for them.

Where proof of personhood actually gets used

It is easy to treat proof of personhood as an abstraction, so it helps to ground it in the concrete situations where a reliable proof of unique humanness changes what is possible. The most immediate is fair distribution. Crypto projects frequently give away tokens to early users through airdrops, and the entire premise, rewarding a broad community, collapses if a handful of people can each register thousands of identities and vacuum up the supply meant for many.

A proof-of-personhood gate, requiring each claimant to prove they are a unique human, restores the fairness the airdrop was supposed to deliver, and the same logic extends to any system handing scarce resources to people: community rewards, grants, promotional credits, or the long-discussed vision of a basic income distributed to verified individuals rather than to whoever runs the most bots.

A second arena is governance and voting. Decentralized organizations and online communities increasingly make decisions by vote, and a vote is only meaningful if each person counts once. Without proof of personhood, governance defaults to systems where influence is bought, whoever holds the most tokens or controls the most accounts decides, which concentrates power and invites manipulation.

A reliable proof of unique humanness opens the door to genuine one-person-one-vote systems online, a building block for fairer collective decision-making that has been technically out of reach. A third arena is the everyday integrity of online spaces: social platforms drowning in AI-generated accounts, review systems gamed by fake humans, and communities overrun by bots all need a way to certify that a participant is a real, unique person, and proof of personhood offers exactly that certification without forcing users to surrender their identities.

The newest and fastest-growing arena is the one created by autonomous AI. As software agents begin acting on people’s behalf, the question of which human stands behind a given agent becomes urgent, both to assign accountability and to keep anonymous bots from masquerading as authorized representatives.

Proof-of-personhood tools that bind an agent to a verified human principal let an agent prove it acts for a genuine, unique, accountable person, which is becoming a prerequisite for trusting agents with real tasks and real money. Enterprises are also adopting proof-of-humanity checks to defend high-value interactions, from video calls to account access, against deepfakes and impersonation.

Across all these cases, the common thread is the same: wherever a system needs to know that a participant is a real, unique human, and increasingly wherever it needs to know which human is behind a machine, proof of personhood is the missing layer that makes the guarantee possible. That breadth of application, spanning fairness, governance, online integrity, and the entire emerging world of AI agents, is why the idea has drawn so much attention despite its unresolved controversies.

The serious objections

A guide that only described the promise of proof of personhood would be misleading, because the field, and especially its biometric flagship, has drawn intense and substantive criticism that any honest reader should weigh. The first objection is the biometric honeypot problem. Building a system that scans the irises or faces of millions of people creates, by its nature, one of the largest collections of biometric data in the world, and even with deletion and anonymization, critics argue that such a database is an irresistible target and that the consequences of biometric data being compromised are uniquely severe, because you cannot change your eyes the way you change a password. The risk of normalizing mass biometric collection, and of who ultimately controls it, sits at the heart of the unease.

The second objection is centralization. A system built on specialized hardware that the project manufactures and controls creates a chokepoint: a single company decides who can verify, where the devices go, and how the system runs, which sits awkwardly with crypto’s ideals of decentralization and raises the prospect of a private entity becoming a gatekeeper of human identity online. The third objection is regulatory and ethical: the leading project has faced pushback, suspensions, and investigations from data-protection authorities in numerous countries worried about consent, privacy, and whether scanning eyes in exchange for tokens, sometimes in lower-income regions, is exploitative.

A fourth, more technical critique questions whether a crypto token needs to be attached to identity verification at all, suggesting the financial layer may be unnecessary to the core function. And a fifth points out that large platforms or governments could build competing verification systems with less controversy, or that softer software-only methods might prove good enough, leaving the biometric approach burdened by risks its rivals avoid. None of these objections proves the technology is bad, but together they explain why proof of personhood, despite solving a real and growing problem, remains genuinely contested.

Why it matters and where it goes

Stepping back, proof of personhood is one of those rare ideas whose importance is rising in lockstep with the technology that makes it necessary, and that is the clearest way to understand its trajectory. The case for it is straightforward and getting stronger: as AI erases the line between human and machine online, almost every system that assumed it could tell the difference, fair distribution, honest voting, bot-free communities, accountable AI agents, needs a new foundation, and a reliable way to prove unique humanness is that foundation. The demand is real, it is growing, and it is not going away, which is why serious people and serious money keep flowing toward the problem even after years of difficulty and controversy.

The open question is not whether proof of personhood matters but which approach, if any, will earn enough trust to become a genuine standard. The biometric path offers the strongest uniqueness guarantees and the most scale so far, but carries the heaviest privacy, centralization, and regulatory baggage. The social-graph, credential, and zero-knowledge paths avoid some of that baggage but offer softer guarantees or struggle to scale. It is entirely possible that no single system wins, and that the future is a patchwork of methods suited to different contexts, a biometric proof for the highest-assurance needs, lighter software proofs for everyday ones.

It is also possible that the privacy concerns prove decisive and the world rejects mass biometric identity altogether, pushing the field toward less invasive designs. What seems certain is that the underlying need, proving a real, unique human in a world full of convincing fakes, is now permanent, and that how society chooses to meet it, and who it trusts to run the infrastructure, will be one of the defining questions where crypto, artificial intelligence, and identity collide. Proof of personhood is the attempt to answer it, and the answer is still being written.

Frequently Asked Questions

What is proof of personhood in simple terms?

Proof of personhood is a way to prove you are a real, unique human, counted exactly once, without revealing who you are. It has to do two things at the same time: guarantee uniqueness, so one person cannot create many identities, and preserve privacy, so proving you are human does not expose your name or identity. It matters because, as AI makes fake humans cheap and convincing, many online systems, fair giveaways, honest voting, bot-free communities, can only work if they can reliably tell one real person from a thousand fakes.

What is a sybil attack?

A sybil attack is when a single actor creates many fake identities to gain influence they should not have. On a system where one identity equals one vote or one share, someone controlling a thousand fake identities has a thousand times the honest influence. Almost every open online system that tries to be fair is vulnerable to it. Sybil attacks used to be limited by the friction of making convincing fake accounts, but AI removes that limit by generating unlimited realistic personas, which is why defending against sybil attacks now requires proving real, unique humanness.

How does the iris-scanning approach work?

The leading biometric project uses a device called the Orb to scan a person’s iris, because the iris is highly unique and very hard to fake, even by AI. According to the project, the Orb generates a unique cryptographic code from the scan, deletes the actual image after processing, and distributes only anonymized fragments to confirm the person has not enrolled before. The result is a credential proving you are a unique human without revealing your identity, and zero-knowledge techniques let you later prove “I am a verified unique human” to an app without exposing anything else about yourself.

What are the alternatives to biometric verification?

Several. Social-graph systems build humanness through webs of trust, where real people vouch for other real people, avoiding biometrics but struggling to scale. Credential-based systems combine signals like verified accounts, on-chain history, or documents into a score suggesting a unique human, offering flexibility but softer uniqueness guarantees. Zero-knowledge identity methods prove facts about you, such as being a unique credential holder, without revealing the data, and increasingly use device-based passkeys. Each approach makes a different trade-off among uniqueness, privacy, security, and scale, and the field has not settled on a single winner.

Why is proof of personhood controversial?

Mainly because the strongest approach, biometrics, raises serious concerns. Collecting iris or face data from millions creates a large biometric database that critics see as a honeypot, made worse because you cannot change your biometrics like a password. Building it on hardware one company controls creates centralization and gatekeeping worries that clash with crypto’s ideals. The leading project has faced regulatory pushback and suspensions in many countries over privacy and consent, and some argue that verifying people in lower-income regions for tokens is exploitative. Others question whether a token is needed at all, or whether less invasive methods would suffice.

How does proof of personhood relate to AI?

Closely, in two directions. First, AI created the urgency: as it makes fake humans cheap and convincing, proving real humanness becomes valuable precisely because humanity is becoming the scarce, trustworthy thing online. Second, the field is evolving from keeping bots out to governing the AI agents now acting on people’s behalf. New tools tie an AI agent to a verified human principal, so an agent can prove it represents a genuine, accountable person instead of running as an anonymous bot. So proof of personhood is becoming a layer that verifies both humans and the machines acting for them.

This article is educational information, not investment or identity-security advice. Proof-of-personhood projects, their scale, and their regulatory status change quickly, and details reflect reporting available as of June 25, 2026. Consider the privacy and security implications carefully, and verify current information from primary sources before enrolling in or relying on any identity system.

Asset manager 21shares has revised down several of its bullish expectations for the crypto industry in 2026, arguing that while key market infrastructure is improving, weaker price action and slower retail and enterprise participation have dampened momentum.

In its midyear outlook, the firm said sectors ranging from exchange-traded products (ETPs) and stablecoin regulation to tokenization and prediction markets are continuing to mature. Still, it expects that major DeFi security incidents and enterprise adoption that is “slower-than-expected” will make a number of previously planned 2026 targets harder to reach.

Key takeaways

- 21shares says crypto infrastructure is advancing faster than market prices, leaving parts of the industry on track while broader growth is constrained.

- Despite more institutional involvement, 21shares maintains that Bitcoin’s four-year cycle remains intact.

- Prediction markets are highlighted as a standout growth area, with 21shares projecting annual trading volume could exceed $100 billion.

- Crypto ETPs are described as resilient in the long run, even as US spot Bitcoin ETFs have seen about $3 billion in net outflows this year.

- Regulatory clarity in the US is cited as helping convert ETF application backlogs into new launches beyond Bitcoin and Ether.

Bitcoin’s cycle still matters, even with institutions reshaping markets

One of 21shares’ clearest messages is that Bitcoin’s four-year market rhythm continues to play a central role. The firm pointed to Bitcoin’s post-halving behavior and argued that increased institutional involvement has changed how the asset trades during downturns without changing the cycle itself.

21shares said Bitcoin peaked at roughly $126,000 in October 2025 before pulling back sharply, and it has continued to trade in a manner consistent with past post-halving patterns. In its view, institutional ownership has helped limit how violently markets draw down, but the fundamental cyclical behavior has not been disrupted.

The firm’s stance also echoes commentary from former 21shares co-founder Ophelia Snyder, who left the company after its acquisition by FalconX in 2025. In a recent Substack post, Snyder argued that institutionalization makes crypto more entangled with broader financial and macroeconomic drivers. She wrote that the investor base is larger, more institutional, and more connected to the traditional financial system—meaning geopolitical developments and macro shifts can influence crypto pricing more than they once did.

Prediction markets and regulation-driven momentum

While 21shares trimmed some of its broader growth projections, it elevated specific segments where adoption dynamics appear stronger. The firm singled out prediction markets as one of the industry’s best-performing areas, forecasting that annual trading volume could surpass $100 billion this year.

The outlook also ties market development to regulation, particularly in the US. 21shares argued that improving regulatory clarity has helped transform a backlog of crypto ETF submissions into a more continuous stream of new product launches—expanding offerings beyond the initial wave of Bitcoin and Ether-focused vehicles.

In that context, 21shares referenced the Securities and Exchange Commission’s generic listing standards as a mechanism behind the pace of ETF conversions. It also highlighted a single case: Hyperliquid, which the firm described as standing out among newer US spot ETF tracking structures. According to 21shares, US spot ETFs tracking the asset pulled in over $150 million in net inflows in under a month, which it framed as evidence that traditional capital continues to find its way into digital-asset products.

ETPs show durability despite weaker spot inflows

21shares also addressed crypto ETP performance, arguing that short-term flows do not fully reflect investor behavior during weaker market conditions. The firm noted that while US spot Bitcoin ETFs have recorded roughly $3 billion in net outflows this year, the total holdings are still just above 1.25 million BTC—close to an all-time high for Bitcoin holdings inside the category.

That balance matters because it suggests many investors are not rushing to exit after periods of volatility. 21shares said holdings remain supported by investors who either hold through downturns or accumulate strategically even when Bitcoin trades well below earlier highs.

Beyond Bitcoin-only flows, the report’s theme is that the institutional pipeline has not shut off; it has simply become more selective and less reflexive during drawdowns. For market participants, this distinction can be important: outflows can pressure near-term sentiment, but the level of cumulative holdings can point to longer-term positioning rather than capitulation.

Consolidation accelerates across treasuries and scaling ecosystems

Another major thread in 21shares’ midyear outlook is consolidation. The firm said public companies holding crypto on their balance sheets are increasingly diverging, with some smaller treasury players trading below the value of their digital assets. In 21shares’ framing, this gap can intensify pressure on weaker players and make mergers or strategic combinations more likely.

A similar dynamic, the report suggests, is playing out in Ethereum’s layer-2 ecosystem. 21shares said a handful of dominant rollups continue to take market share while many smaller networks struggle to attract meaningful user activity and liquidity. For builders and users, the implication is that network effects and capital efficiency are becoming more decisive differentiators—particularly in a market where growth is harder to come by.

What to watch next

As 21shares moves several 2026 targets out of reach, investors should watch whether regulatory catalysts (especially ETF-related) and segment-specific strength (like prediction markets) can offset the drag from weaker price conditions, security setbacks in DeFi, and slower enterprise adoption.

Crypto World

Circle and Nomura join forces to target a $440 billion daily foreign exchange market in Japan

Boston-based stablecoin issuer Circle Internet Financial announced a partnership on Thursday with Japanese financial conglomerate Nomura Holdings to launch a digital asset settlement business. The firms plan to deploy a corporate payment service in Japan as early as 2027.

The agreement will let Japanese businesses exchange yen for USDC, Circle’s U.S. dollar-backed stablecoin, according to the announcement first reported by Nikkei. USDC is the world’s second-largest dollar-pegged stablecoin, boasting a market cap of $73.8 billion as of this writing.

The Circle stablecoin token can be used for cross-border supplier payments, transfers between overseas affiliates, and foreign exchange settlements.

The business aims at Japan’s import, export, and corporate currency markets. Bank for International Settlements data shows that Japan’s foreign exchange market handled $440 billion in daily transactions as of 2025. Standard bank wires take two to three business days to clear funds between yen and foreign currencies. This blockchain setup can drastically reduce that transfer time.

Bitcoin (BTC) hit new 21-month lows at Thursday’s Wall Street open as high US inflation unsettled stock markets.

Key points:

- Bitcoin returns to its lowest level since September 2024, dropping to $58,000.

- US PCE inflation rocks equities, with the Nasdaq 100 shedding 2% in just 30 minutes.

- BTC’s correction mirrors the price action seen throughout the 2022 bear market.

Crypto liquidations pass $600 million in an hour as BTC price drops

Data from TradingView showed BTC/USD dropping to $58,035 on Bitstamp — a level it last traded at in September 2024.

BTC/USD one-hour chart. Source: Cointelegraph/TradingView

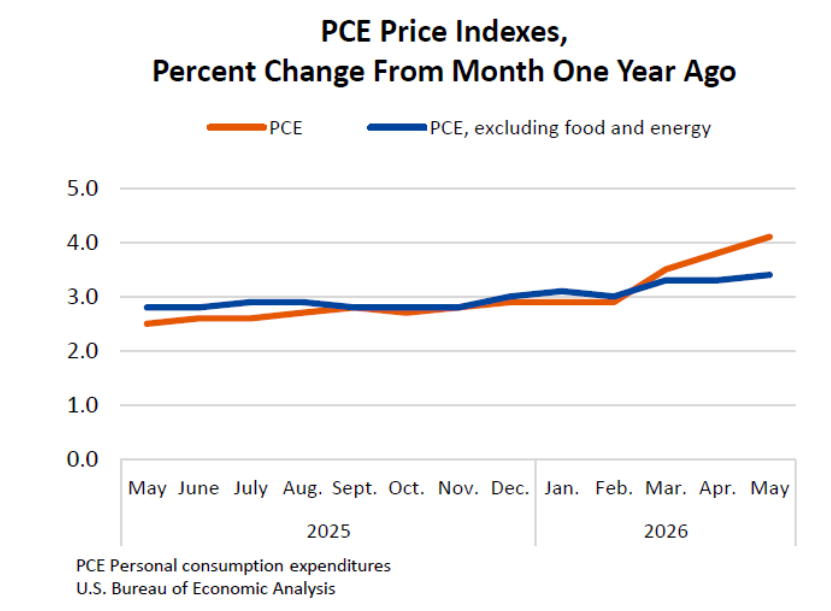

The May print of the US Personal Consumption Expenditures (PCE) index came in at 4.1%, setting a new three-year record.

“From the preceding month, the PCE price index for May increased 0.4 percent. Excluding food and energy, the PCE price index increased 0.3 percent,” a data release from the Bureau of Economic Analysis (BEA) stated.

“From the same month one year ago, the PCE price index for May increased 4.1 percent. Excluding food and energy, the PCE price index increased 3.4 percent from one year ago.”

US PCE one-month % change (screenshot). Source: BEA

Stocks reacted with volatility, with the Nasdaq Composite Index down 0.5% at the time of writing, while the S&P 500 managed to eke out a gain.

The Nasdaq 100, meanwhile, saw a larger snap decline of 2% in just 30 minutes at the open.

“What a chart,” trading resource The Kobeissi Letter responded on X.

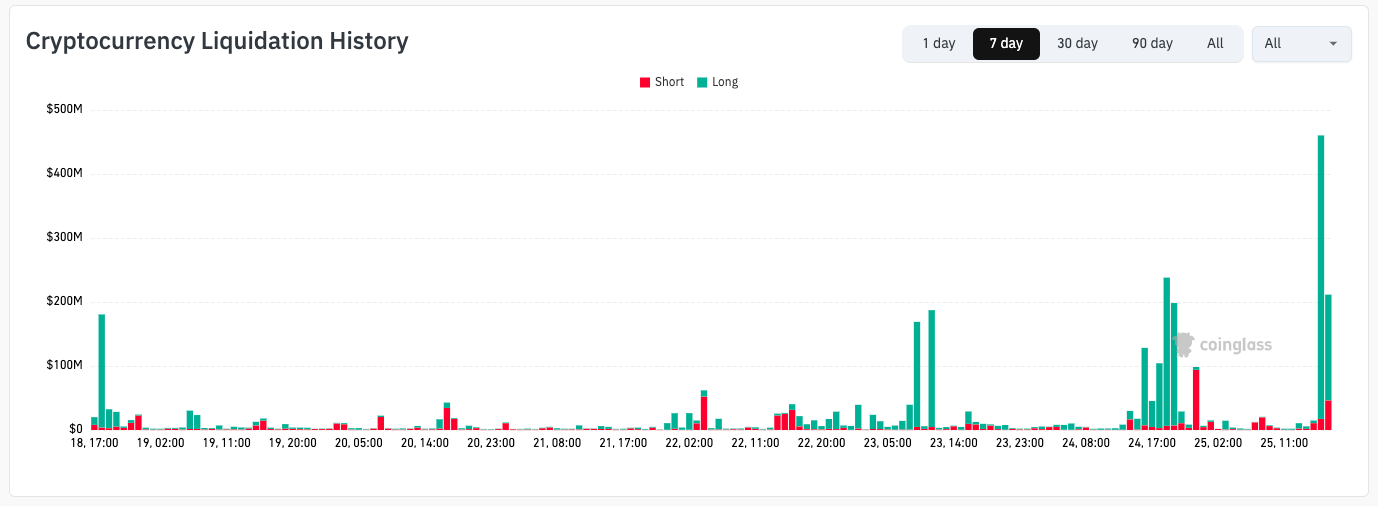

Bitcoin itself sparked considerable long position liquidations, with CoinGlass putting the cross-crypto liquidation total at $600 million over a single hour.

Crypto liquidation history (screenshot). Source: CoinGlass

Commenting, market participants suggested that price moves were being artificially managed to squeeze positions.

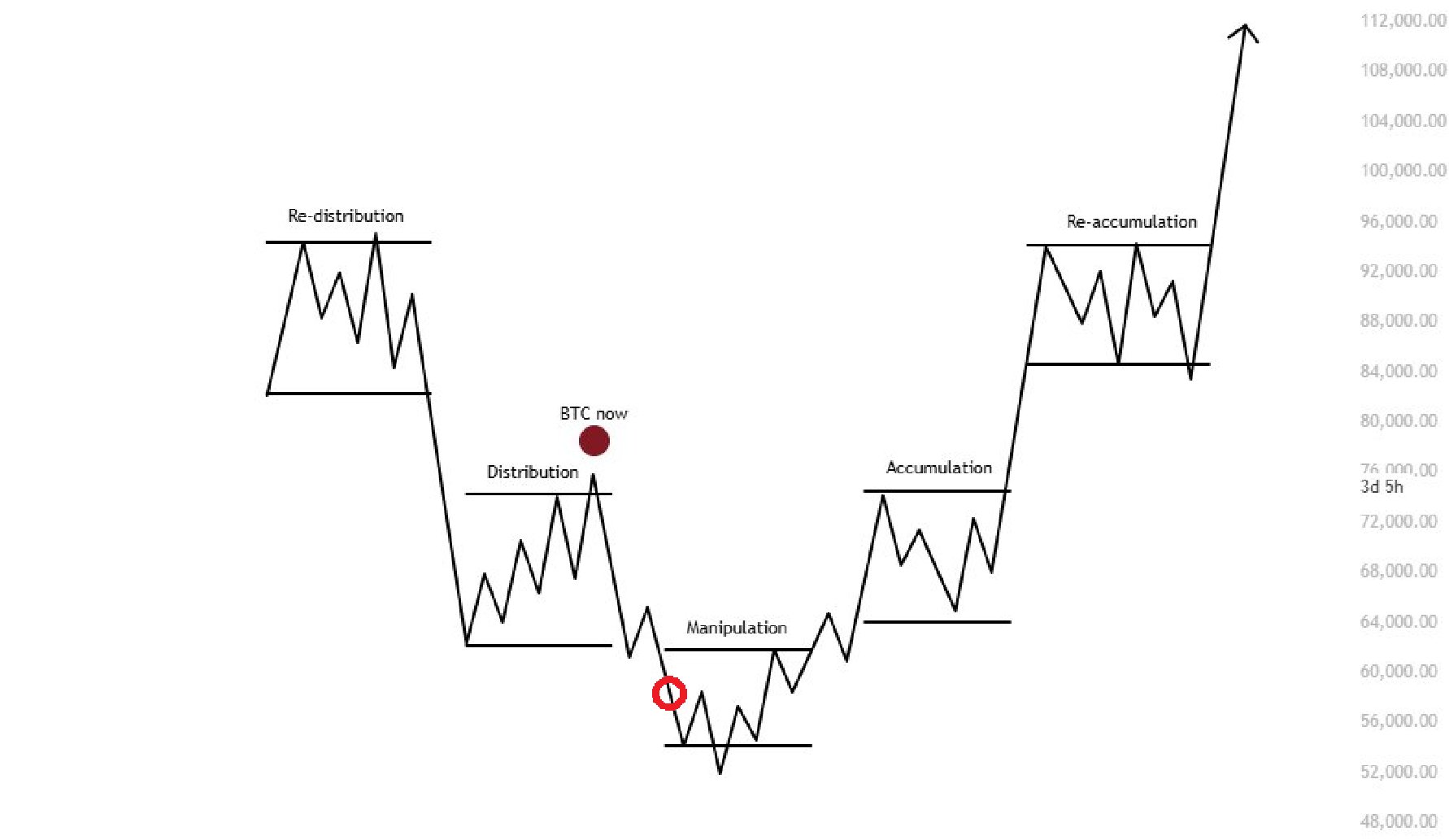

“$BTC is in the manipulation phase,” pseudonymous trader Killa told X followers.

“Every time $BTC trades sub-$60K, that is our manipulation beneath the significant $60K swing low on the weekly and quarterly. Precisely the reason why the orderbook is stacked below us.”

Source: Killa/X

Niels Klaver, cofounder of crypto platform STABL Agency, suggested that BTC/USD “seems to be going for its final leg down of this bear market.”

“$55K remains the target,” he added, referring to an increasingly popular short-term price goal.

BTC/USDT one-week chart. Source: Niels Klaver/X

Bitcoin analysis sees new resistance near $65,000

As BTC price action attempted a modest rebound, trader and analyst Rekt Capital had already described $60,000 support as “clearly weakening.”

Related: BTC price four-year trend calls for $76K as analysis says Bitcoin ‘not broken’

“Once June Monthly Closes, we’ll know from which price July will be able to potentially spring into a post-breakdown relief rally,” an X post read.

BTC/USD one-month chart. Source: Rekt Capital/X

Rekt Capital maintained that the market was acting similarly to 2022, with the 50-month exponential moving average (EMA) tipped to become new resistance next.

BTC/USD one-month chart. with 50EMA. Source: Cointelegraph/TradingView

South Korean cryptocurrency exchange Bithumb was order to pay a $136,000 fine after it was found to have breached personal information protections rules when it sent user data overseas.

In a Thursday notice, the country’s Personal Information Protection Commission (PIPC) said that its investigation into Bithumb found that the exchange had “transferred personal information overseas without the separate consent of the data subjects during the process of order book sharing and virtual asset transfer with overseas virtual asset exchanges.”

The incident was connected to Bithumb sharing its Tether (USDT) order books between September and November 2025 with BingX, despite obtaining consent to share the data with Stellar, as well as sharing user information with 13 overseas exchanges.

“The Personal Information Protection Commission determined that there is a necessity to provide personal information for anti-money laundering purposes when transferring virtual assets to other exchanges, but regarding the overseas transfer of personal information and the data subject’s right to self-determination, it was determined that, as this is a closely related matter, it is necessary to strictly comply with the requirements and procedures stipulated in the Protection Act,” the notice said, in translation.

Source: PIPC

One of the largest crypto exchanges in South Korea, Bithumb has been subject to intense scrutiny from authorities.

The country’s financial watchdog imposed a six-month suspension of the exchange’s activities in March over alleged violations of South Korea’s Financial Information Act, but a court reversed the decision in April. Earlier this month, police reportedly raided Bithumb’s offices as part of an investigation into alleged nepotism involving South Korean lawmaker Kim Byung-gi.

Related: SBI to acquire Bitbank in $289M deal creating Japan’s biggest crypto exchange

South Korean crypto tax set to take effect in 2027

South Korea’s Finance Ministry confirmed in May that a 22% tax on cryptocurrency gains would be imposed beginning in January 2027. The tax has faced several delays in implementation after initially expected to go into effect in 2025, but will likely affect many South Koreans who hold crypto.

According to the Yonhap news agency, about 16 million South Koreans were invested in digital assets as of March 2025.

Earlier this month, Chainalysis said that it signed a memorandum of understanding with the Korean National Police Agency (KNPA), aimed at building investigative capability within South Korea’s law enforcement.

One of the driving factors behind the pact is to better combat North Korea-linked crypto attacks, with South Korea’s police “at the forefront” of tackling these threats.

Magazine: Japanese pension fund tips 1% in crypto, G7 urges action on NK hackers: Asia Express

Crypto World

Aave Co-Founder Kulechov Dismisses AAVE Discount Sale Reports, Teases Aavenomics 3.0 Buyback Plan

TLDR:

- Kulechov firmly denied reports of selling AAVE at a 70% discount, calling the media framing inaccurate.

- All Aave Protocol, GHO, and product revenue flows entirely to the AAVE token under the Aave Will Win proposal.

- Aave Labs is designing Aavenomics 3.0, featuring a new automated and non-discretionary AAVE buyback mechanism.

- Aave targets the entire financial asset market, including real-world assets, beyond the crypto-native TAM.

Aave co-founder Stani Kulechov has moved to address circulating discussions about AAVE token sales and the protocol’s revenue model.

In a post on X, Kulechov pushed back on what he called inaccurate media framing surrounding Aave Labs and its token allocation.

He confirmed that all protocol and GHO revenue flows to the AAVE token while teasing a new automated buyback mechanism. The protocol currently generates $134 million in annualized revenue.

Kulechov Rejects Discount Sale Reports, Outlines Revenue Framework

Kulechov was direct in dismissing reports suggesting AAVE tokens could be sold at a steep discount. Addressing the claim head-on, he wrote, “There is NO WAY we’d sell AAVE at a 70% discount lol.”

He then moved to clarify the structure governing all revenue flows within the Aave ecosystem. The Aave Will Win (AWW) proposal, already passed by the DAO, forms the backbone of that structure.

Under AWW, 100% of Aave Protocol and GHO revenue is directed to the AAVE token. Kulechov confirmed the framework also covers all product revenue streams. “AWW also applies to all product revenue, including the Aave App, Aave Pro, and Swaps,” he stated. None of that revenue flows to Aave Labs, which operates solely as a service provider to the DAO.

He also addressed Aave Labs’ own AAVE token allocation separately. Kulechov noted that “multiple market participants have discussed purchasing, directly or indirectly, through deeper long-term partnerships.”

That allocation is distinct from the DAO’s revenue framework and does not alter how protocol earnings are distributed to token holders.

On intellectual property, Kulechov was equally clear. He confirmed that “all intellectual property, including the Aave brand and any software built for Aave, belongs to AAVE.” Token holders, not Aave Labs, hold rights over these core assets under the current governance structure.

Aavenomics 3.0 and Aave’s Broader Financial Ambition

Beyond correcting the revenue narrative, Kulechov pointed to a coming upgrade. He revealed that “the Aave team is designing Aavenomics 3.0, which includes a new automated and non-discretionary buyback mechanism.” He noted that further details would follow in a later announcement, keeping the specifics close for now.

The planned buyback builds on a strong revenue foundation. Aave is generating $134 million in annualized revenue, all of which flows to the Aave DAO.