Crypto World

Bitcoin triggers $1.48B liquidation wave after PCE inflation fuels rate fears

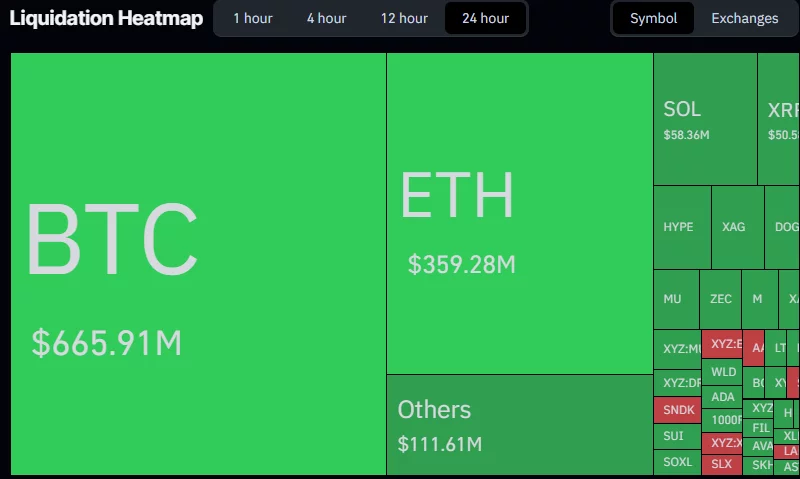

Bitcoin’s drop below $60,000 has triggered nearly $1.48 billion in crypto liquidations after fresh U.S. inflation data reinforced expectations that interest rates could remain higher for longer.

Summary

- Bitcoin’s drop below $60,000 triggered $1.48 billion in crypto liquidations, with long traders suffering the biggest losses.

- A $9.33 billion Bitcoin options expiry and rising inflation concerns have added to volatility across crypto markets.

- Stronger U.S. inflation, ETF outflows, and Strategy’s stock decline have reinforced expectations of higher interest rates.

According to data from crypto.news, Bitcoin (BTC) fell 3.3% to an intraday low of $58,188 on June 25 before recovering to around $59,200 at press time. Ethereum (ETH) declined 4.7% to $1,567, while XRP dropped 3.7% to $1.03. The total cryptocurrency market capitalization also fell 2.2% to $2.13 trillion.

According to CoinGlass, more than 217,700 traders were liquidated over the past 24 hours, with total losses reaching approximately $1.48 billion. Long positions accounted for $1.21 billion of those liquidations, while short traders lost about $270 million. Bitcoin led the selloff with roughly $665 million in liquidations, followed by Ethereum at $359 million and XRP at $50.5 million.

Derivatives positioning keeps volatility elevated

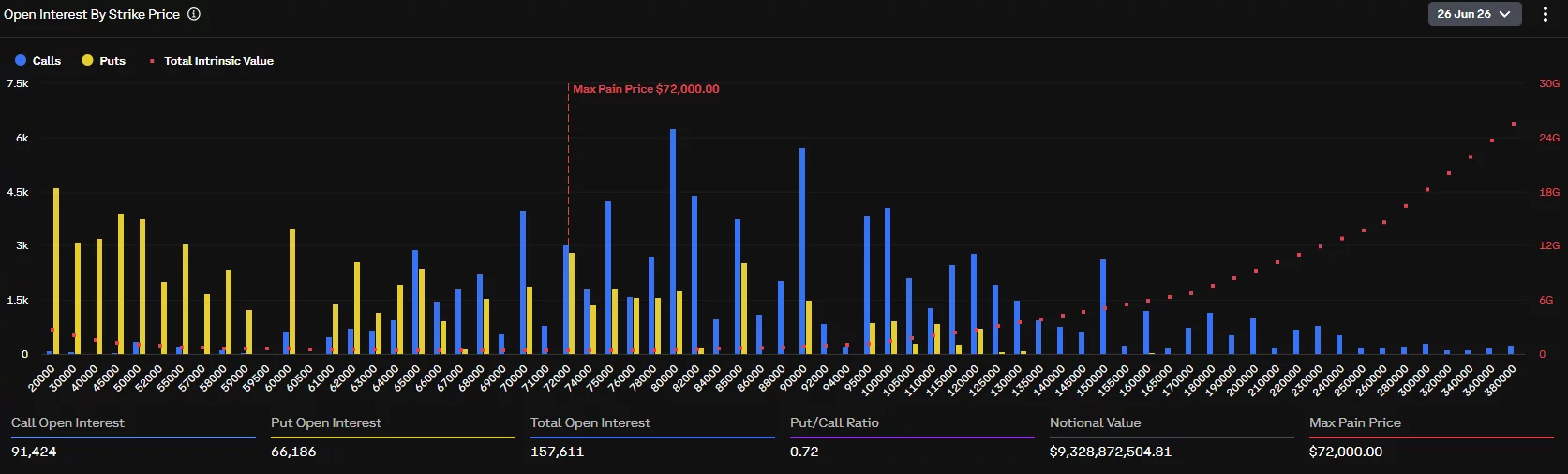

Alongside the spot market decline, traders are preparing for one of the largest Bitcoin options expiries of the year. Data from Deribit shows roughly $9.33 billion in Bitcoin options, representing 157,611 open contracts, are scheduled to expire on Friday.

Call open interest is concentrated between the $75,000 and $90,000 strike prices, while put positioning is clustered across the $20,000 to $70,000 range. Deribit’s max pain price stands at $72,000, well above Bitcoin’s current market price. With Bitcoin trading far below the largest call positions, options traders could continue adjusting hedges into expiry, increasing short-term price swings.

Meanwhile, XRP derivatives remain tilted toward bullish positioning despite the broader selloff. CoinGlass data shows Binance XRP traders maintained a 2.53 long-to-short ratio, while OKX traders posted a 2.68 ratio, suggesting many participants are still positioned for a rebound. However, such crowded long positioning can increase liquidation risk if selling pressure persists.

Offering a longer-term perspective, analyst Daan Crypto Trades said he sees the green support zone on his chart as an area to gradually accumulate Bitcoin rather than trying to identify the exact market bottom.

He added that the weekly 200-week moving average has historically provided attractive value and said he remains comfortable accumulating in the $60,000 region, even though he believes lower prices remain possible during 2026.

Meanwhile, fellow analyst Lennaert Snyder said he had already taken profits on most of his Bitcoin short position following the latest breakdown.

“If we’re printing new lows I’m eyeing 55K for a reaction, but even the 40s are fine with me.”

Inflation data reinforces higher-for-longer outlook

According to the U.S. Bureau of Economic Analysis, the Personal Consumption Expenditures (PCE) price index increased 4.1% year over year in May, up from 3.8% in April, while headline PCE rose 0.4% on a monthly basis.

Although both readings came in slightly below economists’ expectations of 4.2% annually and 0.5% monthly, inflation remained more than double the Federal Reserve’s 2% target.

The report also showed core PCE increased 0.3% during the month and 3.4% from a year earlier. At the same time, the BEA reported that personal income rose 0.7%, while real consumer spending increased 0.3%, suggesting the U.S. economy remains resilient despite elevated borrowing costs. First-quarter GDP growth was also revised upward to 2.1%.

The inflation data arrived as institutional demand for Bitcoin continued to soften. U.S. spot Bitcoin exchange-traded funds have recorded roughly $6.4 billion in net outflows over the past 30 days, the largest monthly redemption period since the products launched. Pressure has also spread to equities, with Strategy shares falling more than 12% below $100, coinciding with Bitcoin’s break under $60,000.

Prediction markets have also turned increasingly cautious. According to Polymarket, traders are assigning a 66% probability that Bitcoin falls below $50,000, while the odds of a decline below $45,000 have risen to 46%.

Adding to those concerns, Bank of America recently revised its outlook and now expects three Federal Reserve rate hikes this year, replacing its earlier expectation that policymakers would keep rates unchanged.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

More than half of UK wealth advisors say most of their clients’ crypto holdings sit outside their oversight. A new CoinShares survey blames firm policy, not investor appetite or advisor knowledge.

The poll of 261 wealth professionals across France, Germany, Italy, Switzerland and the UK found 52% of British advisors report a management gap above 50%. Across Europe, one in four faces the same blind spot.

Firm Policy Drives the Crypto Blind Spot

The survey defines the management gap as the share of a client’s digital asset exposure that an advisor cannot see. Holdings on personal exchanges or self-custody wallets fall outside the advisory relationship.

The report ties the gap to one factor. Some 61% of advisors work at firms that restrict digital assets or give no internal guidance. In those firms, active recommendation drops to 1%, against 48% at firms with clear support.

The gap moves the other way, from 4% at supportive firms to 34% at restrictive ones. CoinShares put the unmanaged exposure 8.5 times wider in blocked firms, the basis for its wrong-way risk warning.

The knowledge gap tracks the same line. More than three-quarters of advisors who call themselves under-informed work at blocked firms. That suggests training follows firm policy rather than the reverse.

The pattern is sharpest in the UK, which posts the widest gap even as domestic crypto regulation reforms advance.

“This is not a knowledge problem. It is not a demand problem. It is a firm-policy problem becoming a wrong-way risk,” Jean-Marie Mognetti, CoinShares co-founder and CEO said in the report.

Follow us on X to get the latest news as it happens

Advisors Want Access, Not Training

Asked what would raise their confidence, advisors pointed to structural change. Regulatory recognition of digital assets as a mainstream asset class ranked first at 45%. Access to exchange-traded products (ETPs) followed at 43%.

CoinShares commissioned the survey through Citywire. The firm is itself a Nasdaq-listed issuer of crypto ETPs, the access advisors ranked second.

Client-facing educational tools ranked last at 9%. The split suggests the barrier is institutional, since neither recognition nor product access is something an advisor can deliver alone. A broader EU crypto rules review is now testing how the framework performs.

Regulation Could Close the Gap

Britain’s stance has shifted fast. The Financial Conduct Authority banned retail sales of crypto exchange-traded notes in January 2021. It reopened retail crypto ETN access in October 2025. The regulator has since proposed letting authorized funds hold up to 10% in those products.

On the continent, the Markets in Crypto-Assets (MiCA) transition ends on July 1. The shift creates a single European crypto market for regulated products. France’s financial regulator, the AMF, has opened a review of which assets qualify for UCITS funds. Digital assets still make up a sliver of Europe’s roughly €15 trillion regulated retail fund market.

Italy offers a counterpoint. Its advisor-led retail model records the lowest gap in the survey at 12%. With the MiCA July deadline approaching, engagement is converting demand into managed exposure there.

For wealth firms, the cost of waiting is rising. An estimated £1 trillion ($1.3 trillion) will pass to the UK’s next generation within a decade. Advisors who cannot see a client’s crypto risk losing the account as it changes hands.

Up to 8% already report rising client interest alongside an unmanaged majority, a sign clients are not waiting. The coming year of rule changes may decide who keeps that wealth in view.

The post About 50% of UK Wealth Advisors Cannot See Most of Their Clients’ Crypto Holdings appeared first on BeInCrypto.

Bitcoin DeFi is struggling to move beyond the promise stage, and the shutdown of Botanix earlier this month has become a new stress test for the idea of “programmable Bitcoin.” The closure—after nearly four years of work and about a year of mainnet uptime—raises a hard question for builders: if a well-funded, technically ambitious Bitcoin scaling project with live applications and competitive yields can’t sustain usage, is decentralized finance actually in Bitcoin’s roadmap in the way advocates expected?

Data from DefiLlama suggests the scale remains small. Total value locked (TVL) across Bitcoin DeFi protocols is about $4.12 billion, a figure that’s tiny relative to Bitcoin’s roughly $1.2 trillion market capitalization and far smaller than the value managed through spot Bitcoin exchange-traded funds, corporate treasuries, and custodial accounts. As Bitwise’s Andre Dragosch put it in comments to Cointelegraph, Bitcoin’s strength as “pristine collateral” has outpaced the plausibility of Bitcoin as a standalone DeFi execution layer.

Key takeaways

- Botanix shut down citing insufficient demand for the network’s yield and activity to cover ongoing infrastructure costs.

- Bitcoin DeFi TVL remains comparatively small, with DefiLlama placing it at about $4.12 billion across protocols.

- Wrapped BTC on large, liquid Ethereum-compatible venues continues to outcompete Bitcoin-aligned execution chains on practical convenience and liquidity.

- Some builders argue the issue is structural—Bitcoin’s user base behaves more like reserve-asset holders than active DeFi traders.

- Other teams say the opportunity is real but depends on trust, institutional-grade risk frameworks, and Bitcoin-anchored designs rather than direct EVM cloning.

Botanix’s shutdown spotlights a demand problem

Botanix announced it was winding down without pointing to a hack or regulatory shock. Instead, the project attributed the decision to demand. According to the shutdown description, the chain “worked” technically: around 25 million transactions, roughly 200,000 wallets, and tens of millions of dollars in bridged funds. Yet those metrics did not translate into the fee volume needed to sustain the business.

The project’s co-founders pointed to a pattern familiar across parts of BTCFi: users often come for yield and treat BTC primarily as store-of-value collateral, then adopt passive strategies. When borrowing, trading, and frequent fund movements don’t happen at a scale large enough to generate consistent protocol fees, even solid technical execution can fail to reach economic viability.

As Botanix’s design reflects broader BTCFi infrastructure, users had to bridge Bitcoin into a tokenized representation on an Ethereum Virtual Machine (EVM)-based environment before accessing DeFi functionality. That additional bridge step—and the smart contract assumptions that come with it—remains a recurring friction point for Bitcoiners, even when a team argues its security model is more Bitcoin-aligned than typical wrapped BTC approaches.

Botanix co-founder Willem Schroé told Cointelegraph that he would not have changed the core architecture. In his view, the “best rates” the project offered were not enough to defeat the default utility of wrapped BTC on Ethereum. He attributed this outcome to Ethereum’s extensive infrastructure, entrenched liquidity, and longer-established “Lindy effect,” along with practical differences in user experience and regulatory comfort.

Why “native” Bitcoin DeFi hasn’t become mainstream

More broadly, Botanix’s experience reinforced a conclusion echoed by researchers: Bitcoin is still primarily treated as a reserve asset rather than a platform for programmable financial products. For many existing DeFi patterns—lending, leveraged exposure, and yield—wrapped BTC on established EVM ecosystems is described as “genuinely sufficient” for user needs.

That sufficiency matters because BTCFi alternatives frequently ask users to accept additional complexity: bridge risk, custody assumptions during tokenization, and the unfamiliarity of a smaller application ecosystem. When the liquidity, integrations, and trading venues are already available through wrapped BTC on major networks, users have less incentive to migrate to a dedicated Bitcoin-aligned execution layer.

The broader BTCFi landscape also appears to concentrate around venues that have “own the user relationship,” leaving independent infrastructure to row upstream against convenience and branding. In the same vein, activity consolidation on liquid venues can make it harder for smaller Bitcoin-specific projects to bootstrap the kind of fee-generating usage they need.

Quantitatively, the gap between hype and usage remains stark. A May 2026 analysis cited by Cointelegraph, based on a GoMining survey of 730 Bitcoin holders, reported that 77% had never used a BTCFi platform and only 3% had integrated BTCFi into their overall Bitcoin strategy. Even with the caveat that the sample consisted of engaged Bitcoin holders who opted into the survey, the results suggest BTCFi is still closer to a niche behavior than a mass-market routine.

Justin d’Anethan of Arctic Digital added that liquidity and yields on EVM or Solana Virtual Machine (SVM) native solutions often remain better than those offered by Bitcoin-specific approaches. He also described the real-world alternatives many clients use when they want to “put their Bitcoin to work,” including centralized desks and exchanges lending out BTC, basis-style structures, and institutional credit pools.

Are “standalone” Bitcoin DeFi layers the wrong target?

Andre Dragosch argued to Cointelegraph that Botanix’s failure points to a structural mismatch between where Bitcoiners allocate capital and what standalone Bitcoin DeFi execution layers require. In his framing, capital seeking yield has largely shifted toward wrapped BTC products on mature, liquid venues rather than bridging into bespoke federations.

For Dragosch, the key isn’t just that people haven’t “discovered” Bitcoin-native DeFi, but that the base-layer culture and design incentives of Bitcoin—slow, conservative, and aligned with store-of-value narratives—don’t naturally produce the kind of user demand that bespoke execution layers depend on.

That view implies a central tension: Bitcoin’s “reserve collateral” role may be driving the next wave of institutional adoption, while “onchain execution” is a separate goal requiring a different user base and different economic incentives. The next phase of adoption, Dragosch suggested, may run through institutions and balance sheets more than through new Bitcoin DeFi execution stacks.

Builders still see room—trust and Bitcoin-anchored design matter

Not everyone agrees that the problem is a lack of demand for Bitcoin-backed lending and yield, but there is a shared theme around trust and infrastructure readiness.

Diego Gutierrez Zaldivar, CEO of RootstockLabs—an EVM-compatible, Bitcoin-secured sidechain—disputed the idea that there is no demand for Bitcoin-linked DeFi services. He told Cointelegraph that the constraint is trust: institutions require operational, legal, and risk management frameworks that go beyond simply deploying smart contracts.

Zaldivar also claimed that more than 40% of Bitcoin DeFi activity runs through Rootstock, pointing to use cases such as real-world asset settlements and institutional vaults. He further said that flows involving hundreds or even thousands of BTC deposits have started to appear—something he said was rare only two or three years ago.

Meanwhile, Chainway Labs co-founder Orkun Mahir Kılıç, associated with Citrea, criticized the premise of cloning EVM DeFi primitives onto Bitcoin as a dead end. He argued Botanix’s outcome reflects a verdict on that approach rather than on Bitcoin DeFi itself. In his view, while “more secure” doesn’t automatically change user behavior, the security guarantee can be decisive for institutions and large holders who need trust-minimized transactions without a custodian to fail.

For other users, he suggested, the differentiator is not abstract security—it’s the presence of applications that genuinely aren’t available elsewhere.

As Bitcoin DeFi continues to test whether its economic model can survive outside Ethereum’s deepest liquidity, the key things to watch next are whether Bitcoin-anchored projects can sustain fee-generating usage without relying on passive collateral behavior, and whether institutional flows grow in ways that reduce the dependency on bridging and trusted intermediaries.

Kraken and Maple have teamed up to launch an onchain “warehouse financing” facility designed to support crypto-backed loans with a structure borrowed from traditional credit markets. The partnership aims to help Kraken expand its institutional lending operation while limiting the amount of balance-sheet capital it needs to deploy for each loan issuance.

In a Thursday announcement, the firms said the facility will fund Kraken’s OTC lending business using a bankruptcy-remote special purpose vehicle (SPV) and USDC-denominated financing. Maple is providing senior financing, while Kraken retains a stake in the transactions.

Key takeaways

- Kraken and Maple are applying a traditional warehouse/credit structure to crypto-backed lending, using a bankruptcy-remote SPV.

- Maple will supply senior financing for the loans, while Kraken will keep exposure through a retained stake.

- The facility is intended to allow collateral and loan performance tracking onchain, including Bitcoin and Ether-backed loans.

- Kraken affiliates are expected to originate, sell, and service loans, with third-party SPV administration by Zaria.

- The partners did not disclose the facility’s size or financing terms.

How the “onchain warehouse” structure works

Warehouse financing is a familiar concept in traditional markets: lenders provide capital that can support a stream of loans, while loan assets are packaged and managed in ways that can isolate risk. In this case, Kraken’s OTC lending is planned to be financed via an SPV intended to be “bankruptcy-remote,” meaning the loan collateral is structured so the borrower cannot simply file for bankruptcy to disrupt repayments and asset separation.

According to the announcement, Maple’s senior financing will be routed through the SPV, while Kraken will retain a stake. The SPV is also designed to support onchain transparency—Maple said the setup gives institutional lenders senior, overcollateralized exposure backed by Bitcoin and Ether, with collateral and loan performance tracked onchain.

That distinction matters for institutional participants who need predictable legal and operational processes in addition to technical visibility. Compared with many earlier crypto lending designs—often based on more direct counterparty structures—this approach borrows from established credit securitization mechanics to separate roles: originators, holders of collateral, financiers, and administrators.

Roles of Kraken Financial, Zaria, and Maple

The facility’s operational flow is split among several entities. Kraken affiliates will originate, sell, and service the loans while retaining a position in the transaction, according to the announcement.

Kraken Financial, described as a Wyoming-chartered Special Purpose Depository Institution, will hold the underlying collateral. Independent SPV administrator Zaria will oversee administration of the facility, while Maple provides senior financing through the SPV structure.

Kraken and Maple did not disclose the facility’s total size or any financial terms, leaving investors without key details such as leverage, pricing, or the expected scope of loan volumes. Those missing datapoints will likely be important for market participants assessing how “warehouse” capacity translates into real lending throughput.

Tokenized credit keeps pulling in institutional capital

The launch arrives as tokenized credit continues to broaden beyond early experiments. According to RWA.xyz data cited in the announcement, tokenized credit has grown to more than $6.2 billion in distributed value—up from roughly $1.87 billion a year ago. The same source is used to frame Maple as the largest platform in the sector, with approximately $1.4 billion in tokenized credit assets.

This matters because scaling tokenized lending depends on two linked developments: more institutional comfort with credit risk (including seniority and collateralization) and more infrastructure for tracking and managing loan performance. By tying credit exposure to onchain accounting while keeping the legal architecture anchored in an SPV, the partnership is positioning institutional lenders to evaluate risk with more real-time transparency than in purely offchain structures.

The firms’ move also fits into a broader post-2022 pattern in crypto finance, where lending businesses rebuilt after high-profile collapses. Failures involving Celsius and BlockFi, among others, accelerated scrutiny across counterparties, collateral practices, and liquidity management—pressuring the market to adopt more conservative structures and clearer risk segregation.

Broader lending momentum—and why it still isn’t uniform

Interest in tokenized credit has also been reinforced by mainstream finance research. Earlier coverage noted that in May, analysts at Bernstein suggested tokenized credit could be a large expansion vector for blockchain-based lending, estimating a potential addressable market of up to $4 trillion as tokenized credit expands beyond niche use cases into areas such as mortgages, auto loans, and small-business lending.

At the same time, not all lending is progressing evenly. While institutional-grade, collateralized products are gaining traction, parts of decentralized finance have faced setbacks. Earlier this month, lending protocol Radiant Capital said it would wind down after failing to recover from a $50 million exploit in 2024, citing an inability to replace lost funds or secure new capital. That contrast underlines a key tension in the sector: onchain lending is advancing where it can align incentives and reduce fragility, but many DeFi lending models still struggle when they encounter capital replacement and risk-control challenges.

In May, Kraken and Maple’s ecosystem context also included other moves toward tokenized lending capacity—such as Ripple securing a $200 million credit facility from Neuberger Berman to expand its institutional prime brokerage lending business. That financing was described as intended to support margin lending and other credit products for hedge funds, trading firms, and institutional clients. Together with the Kraken-Maple facility, these developments point to a recurring theme: regulated institutions and established asset managers are exploring credit lines and onchain settlement where they can better manage risk.

Going forward, the most important things to watch are whether the partnership reports concrete deployment figures—such as loan volume, onboarding pace, default or liquidation behavior, and how efficiently onchain tracking maps to real-world servicing—and whether other lenders adopt similar SPV-style architectures for crypto-backed credit. With the facility’s size and terms not yet disclosed, market participants will likely look for early operational signals to judge how quickly “onchain warehouse financing” can move from structure to sustained lending scale.

Ether treasury company Sharplink has bought Ether for the first time in eight months as the token sank to its lowest price this year on Thursday.

On-chain data from Arkham shows a wallet associated with Sharplink received 5,000 Ether (ETH), worth $7.85 million, from crypto prime brokerage FalconX on Thursday. The last time it received Ether from FalconX was on Oct. 26, when it bought $78.3 million worth of ETH.

The purchase comes as Ether hit $1,537 on Thursday, its lowest price in 2026. The latest purchase could suggest a revival of the company’s active Ether accumulation strategy.

“I’m seeing genuine corporate accumulation conviction holding strong amid subdued price action,” Andri Fauzan Adziima, the research lead at Bitrue Research Institute, told Cointelegraph.

Sharplink CEO Joseph Chalom told Cointelegraph in May that he saw three catalysts that could spur growth in the price of Ether.

The first was the passage of the CLARITY Act in the US, while the second was a return to market risk appetite, which will depend on an easing in geopolitical tension and cooling of the artificial intelligence investment thesis. Chalom’s third catalyst was the continued growth of real-world asset tokenization.

The Senate is yet to vote on its version of the CLARITY Act, and the House Financial Services Committee said it would hold a hearing on the bill on July 17. The US and Iran are working toward a final peace agreement to end months of conflict and tokenized real-world assets have now reached a distributed asset value of $31.55 billion, close to its highest level this year.

Sharplink now holds 876,285 ETH

Sharplink was founded in 2019 as an affiliate marketing service provider to the sports betting and gambling industries, but pivoted to become an Ethereum treasury company in June 2025, with Consensys co-founder and CEO Joe Lubin named as chairman.

It became the largest publicly traded corporate holder of ETH, but lost the title to Bitmine in August, just two months after Bitmine launched its own Ether buying strategy.

Related: Bitmine, Sharplink and Joe Lubin back Ethereum R&D nonprofit

The company now holds 876,285 ETH and ETH equivalents, which it has accumulated over time through active ETH purchases and staking rewards. Its competitor, Bitmine, holds 5.67 million ETH after acquiring another 52,203 ETH last week.

Source: Sharplink

“We continue to maintain a steady pace of accumulation throughout 2026. We believe we are in the early stages of crypto spring,” Bitmine chairman Tom Lee said.

Sharplink added to the Russell indexes

The purchase also comes just days before Sharplink is expected to join the Russell 2000 and Russell 3000 indexes on Monday.

Inclusion in the indexes is widely viewed as positive because many active and passive funds, including exchange-traded funds, typically buy stocks from them.

Chalom in May said that joining the Russell indexes would broaden the company’s shareholder base and strengthen its access to capital markets.

Magazine: Guide to the top and emerging global crypto hubs: Mid-2026

Story Protocol, a layer-1 blockchain built around intellectual property licensing, is pivoting to artificial intelligence as it rebrands as the DATA Foundation.

The company said Thursday that it will focus on building “essential infrastructure for training AI,” which it called “the most valuable and least solved category of IP.”

“Frontier AI labs have hit a multi-billion-dollar data bottleneck, where the internet has been effectively exhausted for scraping,” the company said. “The remaining supply is either expensive and bespoke or legally undocumented, leaving labs without a way to source data at scale, prove its provenance, or guarantee its quality.”

Story is the latest crypto project to turn to AI as funding and hype for the technology accelerate. Multiple crypto miners have also shifted to running the high-performance computers needed for AI, giving a major boost to their revenue in a crypto bear market.

The company said it is also launching an on-chain registry for AI training data provenance and licensing, called Trace, and is integrating with Kled, a company that provides licensable data sets for AI training.

Story president and product chief Andrea Muttoni will become CEO of the DATA Foundation, and Kled founder Avi Patel will join as chief data officer and adviser.

Andrea Muttoni speaking at a conference in Italy in 2024. Source: YouTube

Muttoni said that a year ago, Story had “set out to build the IP layer for the internet,” but the companies behind the “most valuable music, games, and brands guard their most valuable IPs jealously, and the open nature of permissionless licensing clashed with the very control the companies want to keep.”

He added that Story found an AI data-processing project it incubated, called Poseidon, had shown “immediate traction” with major AI firms and raised a $15 million seed round in July 2025.

Muttoni said that as AI companies “effectively run out of internet to scrape,” those that can supply them with “clean, verified, licensed data at scale are going to become some of the most valuable businesses ever built.”

He added that Poseidon will be “the processing layer of the protocol,” while Trace, the on-chain registry, will allow AI companies to verify entire data sets and allow contributors to enforce their terms.

Muttoni said that Kled, which pays people for tasks such as taking videos of their surroundings or capturing ambient audio to train AI, will also become the “flagship app” on DATA.

Related: Crypto Biz: Is AI the exit strategy for miners?

“The most important IP of this era is the data you can’t scrape: how a surgeon’s hands move, how a robot grips, how people speak, drive, and work in the real world,” said Story founder Seung-yoon Lee, who will serve as an adviser to DATA.

“DATA is where that conviction goes next: an end-to-end network that proves real-world data’s origin, licenses it, and pays the people who made it,” he added.

Story’s pivot comes as other major crypto platforms are retooling for AI.

Forbes reported Monday that Web3 gaming powerhouse Immutable is pivoting from gaming to launch an AI marketing platform aimed at game publishers.

Crypto exchange Coinbase announced earlier this month that it is launching a tool that will allow consumer AI models to connect with a user’s exchange account and make trades or execute strategies as it seeks to expand beyond being a platform to buy and sell crypto.

Magazine: AI is banking the unbanked in Africa… faster than crypto

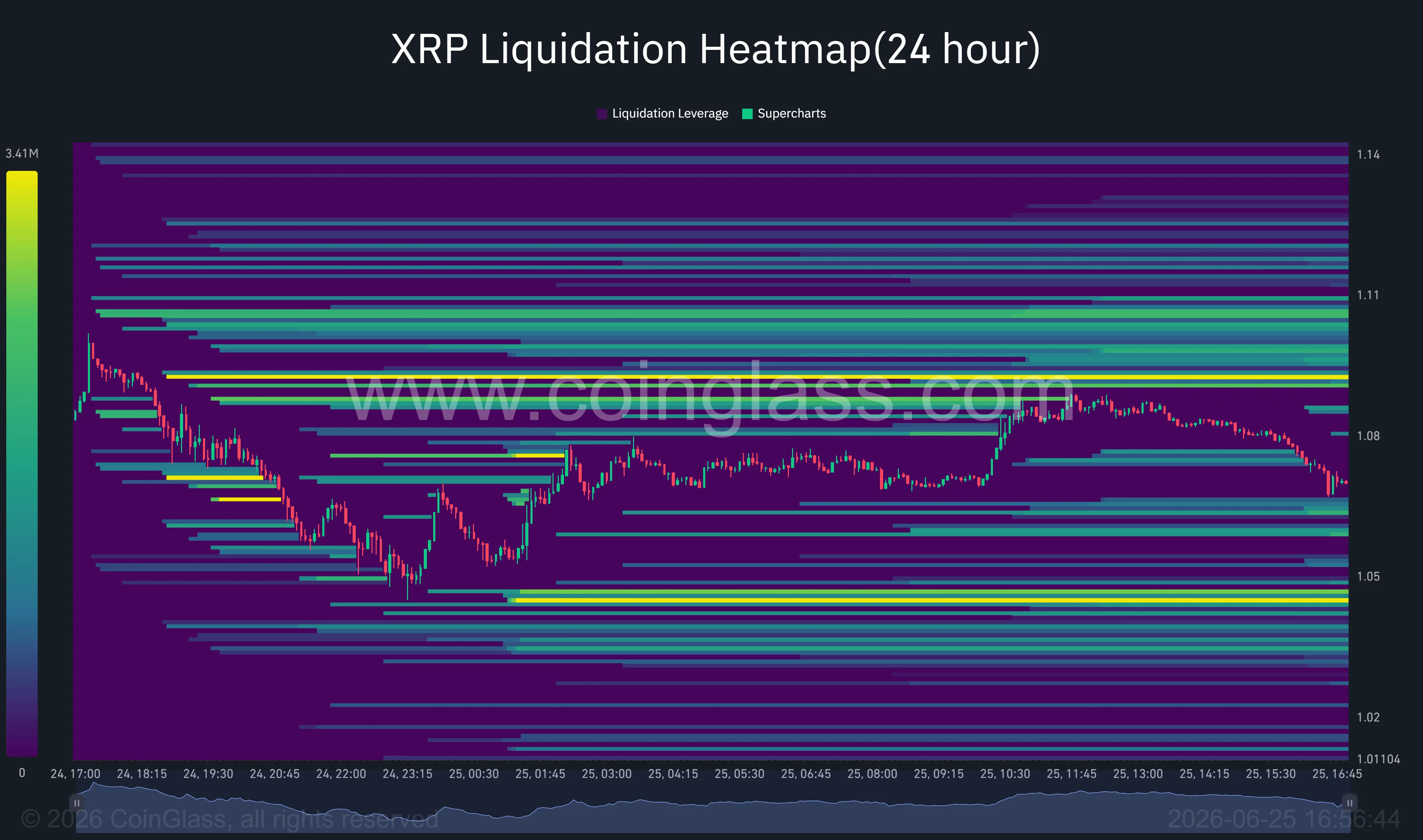

XRP has dropped through the $1.07 support area as traders brace for another leg lower amid mounting bearish pressure.

Summary

- XRP has fallen below the key $1.07 support level, increasing the risk of a deeper correction.

- Bearish chart patterns, liquidation clusters, and weak momentum continue to favor sellers.

- Regulatory uncertainty and macroeconomic headwinds have added pressure to the token’s near-term outlook.

According to data from crypto.news, XRP (XRP) price has fallen about 8% over the past week, extending losses after breaking below the $1.085 support area that had contained the price for several sessions.

The breakdown has left the token trading near $1.07 and shifted short-term sentiment firmly in favor of sellers as traders contend with regulatory uncertainty, weak on-chain activity, and a cautious macro backdrop.

Technical breakdown exposes lower support levels

The daily chart shows XRP slipping beneath the Murrey Math 3/8 support level at $1.0742, a zone that had acted as the lower boundary of its recent trading range. Price is now approaching the next major Murrey support near $0.9766, while the 14-day RSI sits around 33, leaving momentum close to oversold territory but without any confirmed bullish divergence.

On the four-hour chart, XRP continues to trade inside a descending channel after rejecting the upper trendline during its latest recovery attempt. Supertrend remains bearish with resistance near $1.115, while the Aroon indicator favors sellers, with Aroon Down above 70 and Aroon Up at zero, suggesting the prevailing downtrend remains intact.

Unless buyers reclaim the $1.11-$1.12 region, rallies may continue to attract selling pressure.

CoinGlass liquidation data shows the largest concentration of leveraged short liquidations around $1.09, while another significant liquidity cluster sits near $1.045 below the current price. Those zones could become near-term magnets as leveraged traders are forced out of positions.

Meanwhile, the absence of equally large liquidation pockets immediately above current levels suggests buyers have limited fuel for a sustained squeeze unless fresh demand enters the market.

Commenting on the market structure, well-followed analyst Altcoin Sherpa argued that XRP continues to weaken across multiple timeframes.

“Honestly doesn’t look great on the lower time frames (or any time frame) and I think this probably keeps grinding lower. Wouldn’t be surprised to see this go to like $0.75.”

Sherpa’s view aligns with the high-volume profile shown on his chart, where the next major demand zone sits well below current prices.

Macro risks and regulatory uncertainty continue to weigh on sentiment

Beyond the charts, traders are also watching an approaching July 1 regulatory deadline under California’s Digital Asset Financial Assets Law. Ripple has not yet appeared on the state’s public registry of confirmed applicants, prompting concerns that administrative delays could affect regional operations involving its RLUSD stablecoin and payment services. Although the issue is limited to California, uncertainty has added another layer of caution to XRP trading.

On-chain activity has offered little encouragement. Exchange inflows increased as large holders moved tokens onto trading platforms, suggesting some whales preferred reducing exposure rather than accumulating in weakness.

At the same time, XRP Ledger activity has remained subdued following the conclusion of Ripple’s long-running SEC case, leaving the market without a fresh catalyst to attract meaningful retail participation.

Global macro conditions have added further pressure. Rising geopolitical tensions in the Middle East have pushed energy prices higher and revived concerns that inflation could remain elevated. These developments have reduced expectations for Federal Reserve rate cuts and encouraged investors to rotate away from higher-risk assets, including cryptocurrencies.

As Bitcoin has struggled to regain momentum under those conditions, XRP and other large-cap altcoins have experienced sharper percentage declines as leverage unwinds across the market.

The bearish outlook would begin to weaken if XRP reclaims the $1.085-$1.11 resistance band and breaks above the descending channel, potentially forcing short sellers to cover positions clustered near $1.09.

Failure to defend the $1.045 liquidity zone, however, could expose the psychologically important $1.00 level, while a decisive break below that support would strengthen the case for a deeper decline toward the $0.97 Murrey support and potentially the $0.75 area highlighted by Altcoin Sherpa.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Blockchain technology has transformed the way digital assets are created, transferred, and managed. While early blockchain networks operated largely in isolation, the industry’s rapid growth has created a new challenge: enabling seamless communication between multiple blockchain ecosystems. As decentralized technologies continue to mature, the next stage of blockchain evolution is no longer about building individual networks—it’s about connecting them.

Blockchain connectivity is becoming the foundation for a more unified digital economy where assets, data, applications, and users can move freely across different chains without friction. This shift is opening new possibilities for scalability, efficiency, and innovation that were previously impossible.

Why Connectivity Matters

The blockchain ecosystem has expanded into hundreds of independent networks, each designed with different priorities. Some prioritize speed, others emphasize security, privacy, decentralization, or specialized applications. While this diversity fuels innovation, it also fragments liquidity, users, and applications.

Without reliable connectivity, users often face:

- Complicated asset transfers

- Multiple wallet management

- Fragmented liquidity

- Duplicate infrastructure

- Poor user experience

The next generation of blockchain infrastructure aims to eliminate these barriers by making different networks work together as a cohesive ecosystem.

Beyond Simple Asset Transfers

Early interoperability solutions focused primarily on transferring tokens between blockchains. While valuable, future connectivity extends far beyond moving digital assets.

Modern blockchain communication enables:

- Cross-chain smart contract execution

- Shared liquidity across ecosystems

- Unified decentralized applications

- Secure messaging between blockchains

- Cross-network governance

- Identity portability

- Data synchronization

Instead of isolated chains competing for users, networks can now collaborate while maintaining their own unique strengths.

The Rise of Cross-Chain Applications

The next wave of decentralized applications is increasingly becoming chain-agnostic.

Rather than forcing users to choose a single blockchain, future applications can leverage the advantages of multiple networks simultaneously.

For example, an application could:

- Execute transactions on one chain for lower costs

- Store important data on another device for greater security

- Access liquidity from several ecosystems

- Verify identities across multiple networks

- Utilize specialized services from different blockchain infrastructures

This flexibility allows developers to optimize performance without compromising user experience.

Smarter Infrastructure

Artificial intelligence, automation, and programmable infrastructure are beginning to complement blockchain connectivity.

Smart routing systems can automatically determine:

- The fastest network

- The lowest transaction costs

- The most secure execution path

- Optimal liquidity sources

- Efficient settlement routes

Rather than requiring users to manually select networks, future infrastructure can make these decisions automatically in the background.

Security Remains the Priority

Greater connectivity also increases responsibility.

Every connection between blockchains creates additional security considerations. As a result, the industry continues investing heavily in:

- Cryptographic verification

- Decentralized validation

- Multi-layer security models

- Formal smart contract verification

- Continuous monitoring systems

- Trust-minimized communication protocols

Strong security practices ensure that greater interoperability does not come at the expense of decentralization or user protection.

Improved User Experience

One of the biggest transformations may be invisible to users.

Future blockchain applications are expected to hide much of the underlying complexity.

Instead of asking users to:

- Switch networks

- Bridge assets manually

- Understand multiple token standards

- Manage numerous wallets

Applications can perform these processes automatically.

Users simply interact with services while the underlying infrastructure coordinates activity across multiple blockchains behind the scenes.

Supporting Global Digital Economies

As digital finance, tokenized assets, gaming, supply chains, and digital identity continue expanding, seamless blockchain connectivity becomes increasingly essential.

Connected blockchain infrastructure can support:

- Global payments

- Tokenized real-world assets

- Cross-border commerce

- Enterprise data sharing

- Digital identity systems

- Autonomous machine-to-machine transactions

- Decentralized financial infrastructure

The ability to securely exchange information across networks creates opportunities for entirely new digital business models.

The Road Ahead

The future of blockchain is unlikely to be dominated by a single network. Instead, it is shaping up to become an interconnected ecosystem where specialized blockchains collaborate rather than compete.

Connectivity enables developers to build more capable applications, businesses to operate more efficiently, and users to enjoy smoother digital experiences. As interoperability technologies continue advancing, blockchain infrastructure will increasingly resemble the internet itself—a network of networks working together to deliver seamless global access.

Conclusion

The next stage of blockchain connectivity represents a major milestone in the industry’s evolution. Rather than existing as isolated ecosystems, blockchains are becoming interconnected platforms capable of securely exchanging assets, data, and functionality across diverse networks.

As this infrastructure matures, users may no longer need to think about which blockchain they are using. Instead, they will simply access decentralized services that work seamlessly across an increasingly connected digital landscape. This evolution has the potential to unlock greater innovation, broader adoption, and a more efficient decentralized future for everyone.

REQUEST AN ARTICLE

Take-Two Interactive (TTWO) shares fell nearly 3% this week after Rockstar Games officially opened Grand Theft Auto (GTA) VI pre-orders, triggering a classic sell-the-news reaction from short-term traders.

The stock surged 13% last week amid growing anticipation. When the moment arrived, profit-taking erased a substantial portion of those gains.

Standard Price Falls Short of Investor Expectations

Rockstar confirmed GTA 6 launches November 19, 2026, with a standard edition priced at $79.99 for PlayStation 5 and Xbox Series X|S.

That figure, however, disappointed bulls who had speculated the title could command between $90 and $100. Grand Theft Auto has sold over 470 million units worldwide, which some investors cited as justification for a premium price point.

The $79.99 figure does not tell the full pricing story. Rockstar also confirmed an Ultimate Edition for $99.99, which bundles exclusive vehicles and apparel. Still, analysts had largely expected the base price to push past $80.

No Discs Inside Physical Retail Editions

Physical collectors received a further setback. Retail boxed editions will not contain a disc. Each box holds only a digital download code, with pre-loading beginning November 12 for both physical and digital pre-orders.

Meanwhile, the GTA meme coin surge across crypto markets on the same day confirmed how far the franchise’s cultural reach extends beyond traditional gaming.

GTA VI Launch Confirmed as Single-Player Experience

The pre-order announcement confirmed GTA 6 will launch exclusively as a single-player title. Sony’s official PlayStation FAQ states GTA 6 is “a single-player experience,” with no online mode listed. Rockstar has not announced a launch date for GTA VI Online or clarified how the existing GTA Online service relates to the new title.

For investors, this detail carries weight. Analysts widely project GTA Online as Take-Two’s most durable long-term revenue source. A delayed online rollout pushes that monetization deeper into 2027 or beyond.

The pattern mirrors GTA 5’s 2013 launch, where the online component arrived weeks after the main title. However, investor expectations in 2026 are far more closely tied to recurring digital revenue than they were 13 years ago.

Analysts Stay Bullish

Thursday’s slide follows a sell-the-news pattern common across financial markets. Traders position ahead of anticipated catalysts, then exit once the catalyst is confirmed.

Similarly, this year’s Wendy’s meme stock surge showed how quickly enthusiasm can flip into profit-taking before buyers return at lower prices.

Despite the single-day drop, Wall Street’s long-term outlook for TTWO remains firmly positive. Bank of America analyst Omar Dessouky maintained a Buy rating with a price target of $368. Morningstar projects GTA 6 unit sales of 60-70 million in fiscal year 2027. That would represent record digital distribution for the publisher.

Take-Two Raises Full-Year Bookings Forecast Ahead of GTA 6 Launch

Take-Two also raised its full-year bookings forecast to between $6.65 billion and $6.7 billion. The broader gaming token sector has already demonstrated renewed investor appetite in 2026, suggesting sustained interest in gaming assets across both traditional and digital markets.

The five-month runway to the November 19 launch gives the US stock market and TTWO investors time to reassess. How quickly Rockstar activates GTA VI Online may ultimately prove more consequential to Take-Two’s long-term trajectory than first-day pre-order numbers.

The post GTA 6 Pre-Orders Send Take-Two Stock Down as Price and Launch Details Disappoint appeared first on BeInCrypto.

For years, a blockchain was one chain doing everything. The modular thesis breaks that apart into specialized layers for execution, settlement, consensus, and data availability. This guide explains the new stack, why rollups need a data layer, and what the design buys and costs.

Summary

- Modular blockchains split execution, settlement, consensus, and data availability across specialized layers to improve scalability.

- Rollups process transactions off the main chain while relying on shared settlement and data availability layers for security.

- The modular approach increases flexibility and throughput, but also introduces added complexity, fragmentation, and layered trust assumptions.

A modular blockchain is a blockchain that splits the core jobs a network must perform across separate, specialized layers, instead of having a single chain do all of them at once. To see why that is a meaningful idea, you have to know the four jobs every blockchain has to handle: execution, which means running transactions and smart contracts; settlement, which means finalizing results and resolving disputes; consensus, which means agreeing on the order of transactions; and data availability, which means making sure the transaction data is actually published so anyone can check it.

A traditional blockchain, now called monolithic, does all four itself, on one chain, which is simple and tightly integrated but runs into a hard ceiling on how much it can scale, because one chain doing everything can only go so fast before it becomes congested or expensive. The modular approach unbundles those jobs, letting different layers each specialize in one of them, and that unbundling has become the dominant way ambitious blockchains now scale. This guide explains the four functions, the difference between monolithic and modular designs, how rollups and data availability layers fit together, the leading examples, and the real trade-offs the modular path involves.

The reason this matters is that scaling has been blockchain’s defining challenge for a decade, captured in the so-called trilemma, the observation that a single chain struggles to be simultaneously scalable, secure, and decentralized, and usually has to sacrifice one. Monolithic chains tend to push hard on scale at some cost to decentralization, or preserve decentralization at the cost of speed.

The modular thesis offers a different escape from the trilemma: if no single chain has to do everything, then each layer can optimize for its own job, and the system as a whole can reach a scale no monolithic chain easily matches while preserving strong security and decentralization where it counts.

By 2026 this thesis moved from theory to the dominant architecture, with specialized data availability networks serving dozens of execution chains and a whole stack of modular components in production. Understanding the modular design is therefore close to understanding where blockchain infrastructure as a whole is heading.

The four jobs of a blockchain

Everything about modularity follows from understanding the four functions a blockchain performs, so it is worth taking each in turn. Execution is the actual computation: when you swap tokens or run a smart contract, execution is the process of taking your transaction, applying it, and updating the network’s state to reflect the new balances. It is the layer users interact with most directly, and it is computationally heavy, because every transaction has to be processed. Settlement is the layer that provides finality and a home for dispute resolution: it is where the results of execution are anchored and made authoritative, the bedrock that other layers can treat as the final word on what happened, and where, in some designs, proofs are verified or fraudulent claims are challenged.

Consensus is the mechanism by which the network’s participants agree on a single, ordered history of transactions, so that everyone shares the same view of what happened and in what sequence, which is what stops double spending and keeps the ledger consistent. Data availability is the one most people have never heard of and the one that turns out to be central to modular design. It is the guarantee that the data behind every transaction is actually published and obtainable, so that anyone can download it, check that the rules were followed, and reconstruct the state if needed. If transaction data is not available, no one can verify whether the network cheated, which means data availability is a quiet but essential foundation of trust. In a monolithic chain, all four of these jobs happen together in one tightly bound system. The modular insight is that they do not have to, and that pulling them apart lets each be done far better.

Monolithic versus modular

The cleanest way to grasp modularity is to contrast it directly with the monolithic model it departs from. A monolithic blockchain bundles all four functions into a single integrated chain. Every full node executes every transaction, participates in consensus, stores all the data, and treats the chain itself as the settlement layer. The great virtue of this design is simplicity and tight integration: everything lives in one place, applications can interact seamlessly, and there are no seams between layers to manage.

A well known high performance chain that prizes raw speed exemplifies the monolithic approach, pushing a single integrated chain to process enormous throughput by demanding powerful hardware from its nodes. The cost of the monolithic design is the ceiling it imposes: because every node must do everything, the chain can only scale so far before either fees rise, congestion sets in, or the hardware requirements grow so heavy that fewer participants can run a node, which erodes decentralization.

A modular blockchain breaks the bundle apart so that different layers handle different jobs. A typical modern arrangement separates execution from the rest: specialized execution layers run the transactions and smart contracts, while a different layer or layers handle settlement, consensus, and data availability. The flagship example is the rollup-centric design, where lightweight execution chains called rollups process transactions off to the side and then lean on a robust base layer for settlement and data availability.

The benefit is specialization: an execution layer can be tuned purely for fast, cheap transaction processing without also bearing the full weight of securing the entire system, because it borrows security from the base layer beneath it. The system as a whole can then scale by adding many execution layers on top of a shared foundation, multiplying capacity in a way a single monolithic chain cannot. Monolithic favors integration and simplicity; modular favors specialization and scale, and that is the core of the design choice.

Rollups: the execution layer of the modular world

The most important modular component to understand is the rollup, because rollups are how the modular vision actually gets used today. A rollup is a separate chain that handles execution, processing transactions quickly and cheaply off the main chain, and then posts a compressed record of what it did back down to a base layer for security. The name comes from the way it rolls up many transactions into a single batch and submits that batch to the base chain, so the base chain does not have to process each transaction individually but can still serve as the ultimate source of truth. This is the mechanism that lets a modular system scale: thousands of transactions happen cheaply on the rollup, and only a condensed summary touches the expensive, highly secure base layer.

There are two main families of rollup, distinguished by how they convince the base layer that their batched transactions are valid. Optimistic rollups assume the transactions are honest by default and allow a window during which anyone can challenge a fraudulent batch by submitting a fraud proof, with the base layer settling the dispute. Zero knowledge rollups instead generate a cryptographic validity proof for each batch, mathematically showing the transactions were processed correctly, which the base layer verifies without re running them.

Both achieve the same goal of inheriting the base layer’s security while doing execution elsewhere, and both depend critically on one thing: the data behind their transactions must be available, so that anyone can verify the rollup’s claims or reconstruct its state. A rollup that posted only a summary without making the underlying data available would be asking the world to trust it blindly, which defeats the purpose. This is exactly why data availability, the obscure fourth function, becomes the linchpin of the entire modular architecture.

Data availability: the linchpin

Data availability deserves its own section because it is the function that modular design elevated from an afterthought to a centerpiece. When a rollup posts its batch of transactions, the crucial requirement is that the full transaction data be published somewhere accessible, so that anyone can check the rollup did its job honestly, challenge it if not, and rebuild the state if the rollup operator disappears.

Where that data gets published, and how cheaply, turns out to be one of the biggest factors in how well a modular system performs, because publishing data is a major part of what a rollup pays for. If the base layer makes data publication expensive, rollups are expensive; if a layer makes it cheap, rollups become dramatically cheaper.

This created demand for a new kind of specialized chain whose entire job is data availability: a data availability layer. Rather than executing transactions or settling disputes, such a chain exists purely to order data and keep it available cheaply and reliably for the rollups that depend on it. The pioneering example is a network built specifically as a modular data availability layer, which uses an elegant technique called data availability sampling to scale. Instead of requiring every node to download an entire block to confirm the data is there, lightweight nodes each randomly sample a small number of pieces of the block.

With enough independent samples, the network can be confident, to very high probability, that all the data is genuinely available, without anyone having to download all of it. Combined with techniques that let each application fetch only its own slice of data, this lets a data availability layer serve many rollups at once, cheaply and at scale. By 2026, such a layer was providing data availability for dozens of rollups, a concrete sign that the modular separation of data availability into its own specialized network had become real, working infrastructure.

The leading modular stacks

It helps to see how these pieces assemble into real systems, because the modular world is not one design but a few competing and complementary stacks. The most influential is the rollup-centric roadmap of the leading smart contract platform, which deliberately reoriented itself around modularity. Rather than trying to scale by making its own base layer process everything faster, it chose to become primarily a settlement and data availability foundation, with the heavy execution pushed out to a thriving ecosystem of rollups built on top.

A pivotal upgrade introduced a dedicated, cheaper space for rollups to post their data, often called blob space, which slashed the cost of data availability and, with it, the fees rollups charge users, bringing many transactions down to a fraction of a cent. Further upgrades aim to expand that data capacity dramatically over time. The result is a layered system: a secure base layer for settlement and data, and many execution focused rollups handling the day-to-day activity cheaply above it.

Alongside this sits the specialized data availability layer approach, where rollups choose to post their data to a purpose built data availability network instead of, or in addition to, the base settlement layer, often to get even lower costs. There is also a connection to another modular idea covered elsewhere: shared security through restaking, where a pool of staked capital can be used to secure new services, including data availability layers, letting them inherit strong economic security on day one rather than bootstrapping their own.

Together, these pieces form a menu of modular components, settlement layers, data availability layers, execution rollups, and shared security providers that teams can mix and match to assemble a custom chain. A project can launch its own rollup tuned for gaming or social applications, point it at whichever data availability layer is cheapest, and settle to whichever base layer it trusts, without building a validator set or a full monolithic chain from scratch. That composability of infrastructure, the ability to assemble a chain from specialized parts, is the practical payoff of the modular thesis and a large part of why it spread so quickly.

An analogy: the restaurant and the food court

Because the modular stack has so many pieces, an analogy can anchor the whole idea before the trade offs pile up. Think of a monolithic blockchain as a single restaurant that does everything under one roof: it grows its own ingredients, cooks every dish, seats the diners, and washes the dishes, all with the same staff in the same building. The advantage is seamless coordination, since everything happens in one place and nothing has to be handed off. The limitation is capacity: that one kitchen can only cook so many meals at once, and if you want to serve far more people, you either build an enormous, expensive kitchen that few can staff, or you accept long waits and high prices when demand surges. A single integrated chain faces the same ceiling, because every node has to do every job.

Now picture a food court instead. The building provides the shared foundation, the tables, the security, the guarantee that the space stays open and orderly, while many specialized vendors handle the cooking, each focused on one cuisine and tuned to serve its customers quickly and cheaply. In this picture the shared building is the base layer providing settlement and data availability, and the individual vendors are the rollups handling execution.

No single vendor has to provide its own security or build its own premises; they all inherit that from the building, so they can concentrate purely on serving food fast. The food court can serve vastly more people than the single restaurant, because capacity grows by adding vendors instead of straining one kitchen, which is exactly how a modular system scales by adding execution layers on a shared foundation.

The analogy also captures the costs honestly. A food court is more complex than a single restaurant: there are more independent operators, more things that can go wrong with any one vendor, and more coordination required to keep the shared space working. If you want a dish that combines ingredients from three different vendors, you have to carry your tray between them, which is clumsier than ordering everything from one kitchen, just as moving assets or composing an application across separate rollups is more awkward than operating within one integrated chain. And every vendor depends on the building: if the shared foundation fails to keep the lights on or the doors open, every vendor suffers, just as a rollup inherits the weaknesses of the data availability and settlement layers beneath it.

The food court trades the seamless simplicity of the single restaurant for far greater capacity and specialization, accepting more complexity and more handoffs in return. That is precisely the bargain the modular blockchain makes, and seeing it as a food court instead of a single restaurant makes both the appeal and the cost intuitive.

What modularity buys you

Having laid out the architecture, it is worth being precise about the genuine advantages the modular approach delivers, because they explain why it became dominant. The headline benefit is scalability. By separating execution from the base layer and letting many rollups run in parallel on top of a shared foundation, a modular system can process vastly more total activity than a single monolithic chain, because capacity is added by stacking execution layers instead of straining one chain. The cheap data availability layers compound this by driving down the dominant cost of running a rollup, which is why transaction fees on modern rollups have fallen to fractions of a cent for simple transfers.

The second benefit is specialization and flexibility. Because each layer focuses on one job, each can be optimized far beyond what a generalist chain could achieve: a data availability layer can be ruthlessly efficient at keeping data available, an execution rollup can be tuned for a specific use case, and a settlement layer can prioritize security and finality. This also gives builders flexibility and sovereignty: a team can launch a chain tailored to its needs, choosing its own execution environment and rules, while still inheriting security and data availability from established layers instead of recreating them.

The third benefit is improved decentralization at the verification level. Techniques like data availability sampling let lightweight nodes verify that a network is behaving honestly without running expensive hardware, which means more ordinary participants can help keep the system honest, countering the tendency of high performance monolithic chains to concentrate power among those who can afford powerful machines. Scalability, specialization, and verifiable decentralization are the real prizes the modular design competes for, and it pursues them by refusing to make any single chain carry the whole load.

The trade-offs and criticisms

No architecture is free, and an honest account of modularity has to weigh its real costs against the monolithic simplicity it replaces. The first cost is complexity. A modular system has many moving parts, execution on one layer, data on another, settlement on a third, bridges and proofs connecting them, and that complexity creates more surface area for bugs, misconfigurations, and failures than a single integrated chain. More layers mean more things that can go wrong and more seams that must be secured. The second cost is fragmentation. When activity spreads across many separate rollups, liquidity and users fragment too, and moving assets or composing applications across different execution layers can become awkward, slow, or risky, sacrificing some of the seamless composability that a single monolithic chain offers, where every application can interact with every other instantly.

The third cost is a subtler security consideration. A rollup’s safety depends on the layers beneath it, so if the data availability layer it relies on fails to keep data available, or the settlement layer it trusts is compromised, the rollup inherits that weakness. Modular systems must therefore reason carefully about the trust assumptions of every layer they depend on, and a chain that uses a less secure data availability layer to save money is making a real trade off in safety, even if it is not always obvious to users.

Defenders of the monolithic approach argue that tight integration delivers a simpler, more composable, more uniformly secure system, and that the high performance monolithic chains have shown a single chain can scale further than the modular camp once assumed. The honest conclusion is that monolithic and modular are not strictly better or worse but represent different bets: monolithic wagers that integration and raw single chain performance win, while modular wagers that specialization and stacking win. By 2026 the modular bet had clearly become the dominant architecture for ambitious new infrastructure, but the trade offs it carries, complexity, fragmentation, and layered trust, are real, and the debate over which approach ultimately prevails is far from settled.

Frequently Asked Questions

What is a modular blockchain in simple terms?

A modular blockchain splits the core jobs a network must do across separate, specialized layers, instead of one chain doing everything. The four jobs are execution (running transactions and smart contracts), settlement (finalizing results and resolving disputes), consensus (agreeing on transaction order), and data availability (making sure transaction data is published so anyone can check it). A traditional, monolithic chain does all four itself, which limits how far it can scale. A modular design lets each layer specialize in one job, so the system as a whole can scale much further while preserving security.

What is the difference between monolithic and modular blockchains?

A monolithic blockchain handles execution, settlement, consensus, and data availability all on one integrated chain, where every node does everything. It is simple and tightly integrated but hits a ceiling on scale, because one chain doing everything can only go so fast before fees rise or hardware demands shrink the node set. A modular blockchain separates those jobs across layers, typically pushing execution onto rollups while a base layer handles settlement and data availability. This trades some simplicity and composability for much greater scalability and specialization.

What is a rollup and how does it fit in?

A rollup is a separate execution chain that processes transactions cheaply off the main chain, then posts a compressed batch back to a secure base layer for settlement and data availability. It rolls up many transactions into one batch so the base layer does not process each individually but still serves as the source of truth. Optimistic rollups assume validity and allow fraud challenges; zero knowledge rollups submit cryptographic validity proofs. Rollups are how the modular vision scales in practice, and they depend on their transaction data being made available so anyone can verify them.

Why is data availability so important?

Because verifying a rollup, or any chain, requires that the data behind its transactions actually be published and obtainable. If the data is not available, no one can check whether the rules were followed, challenge fraud, or reconstruct the state if an operator vanishes. Where and how cheaply that data is published is one of the biggest factors in a modular system’s cost, since publishing data is much of what a rollup pays for. This created specialized data availability layers whose entire job is to keep data available cheaply, using techniques like sampling so light nodes can confirm availability without downloading everything.

What is Celestia and what does a data availability layer do?

A data availability layer is a specialized chain whose only job is to order transaction data and keep it available cheaply and reliably for the rollups that rely on it, instead of executing transactions or settling disputes. The pioneering example was built specifically for this purpose and uses data availability sampling, where lightweight nodes each randomly check small pieces of a block so the network can be confident, to high probability, that all the data is present without anyone downloading the whole block. By 2026 such a layer was providing data availability for dozens of rollups.

What are the downsides of modular blockchains?

Three main ones. Complexity: many moving parts across layers, plus the bridges and proofs connecting them, create more surface area for bugs and failures than a single integrated chain. Fragmentation: spreading activity across many rollups splits liquidity and users and can make moving assets or composing applications across layers awkward, sacrificing some of a monolithic chain’s seamless composability. And layered trust: a rollup’s safety depends on the layers beneath it, so relying on a weaker data availability or settlement layer to save money introduces real security trade offs. Monolithic defenders argue tight integration is simpler and more uniformly secure.

This article is educational information, not investment advice. Blockchain architectures, projects, and technical details evolve quickly, and the descriptions here reflect the state of the field as of June 25, 2026. Verify current information from primary sources before relying on anything described here.

Aave has rebounded sharply from this week’s sell-off and is now testing a key long-term resistance level after renewed buying, short-covering activity, and fresh optimism around the DeFi lending protocol lifted market sentiment.

Summary

- AAVE has rebounded 17% from its recent low and is testing a nine-month descending trendline near key breakout resistance.

- Bulls must secure a daily close above the $85-$88 zone to target $102 next, while $72-$75 remains critical support.

- Rising stablecoin inflows, improving derivatives positioning, and stronger momentum indicators have fueled the latest recovery.

According to data from crypto.news, Aave (AAVE) climbed as much as 17% from its Wednesday low near $72 to trade around $82 on June 25, recovering nearly all of the previous session’s losses. The rally followed heavy buying around a long-standing support zone, where sellers lost control after failing to extend the breakdown.

The recovery also coincided with renewed interest across decentralized finance tokens as traders rotated back into higher-beta assets following a wave of liquidations that swept through the crypto market earlier this week.

Rebound has pushed AAVE into a decisive technical resistance zone

The daily chart shows AAVE rebounding directly from the $72-$75 demand area before reaching the upper boundary of a descending trendline that has capped every rally since late 2025. Price now sits just below trendline resistance near $85, a level that traders are closely watching for confirmation of a larger trend reversal.

Commenting on the setup, crypto analyst Master of Crypto wrote in a June 24 X post:

“$AAVE is testing the top of a 9-month descending channel. A daily close above $85-88 could confirm the breakout, with $102 as the first target and $132 next. If the breakout fails, $72-75 remains the key support zone.”

The four-hour chart reinforces that view. AAVE has broken above a multi-day consolidation range near $77.7 while reclaiming its 20, 50, 100, and 200 simple moving averages, which now cluster between roughly $71 and $76.

Holding above those averages would strengthen the bullish case, while rejection near the descending trendline could trigger another retest of the recent breakout area.

Momentum indicators have also improved. Daily RSI has climbed above 60 after rebounding from oversold territory earlier this month, while the MACD has completed a bullish crossover and continues to expand above the zero line.

On the four-hour timeframe, RSI has advanced toward the upper-60s, showing buyers remain in control without yet reaching extreme overbought conditions.

Derivatives positioning and DeFi flows have strengthened the recovery

The recovery follows an aggressive unwind of bearish positioning after AAVE found support at its long-term demand zone. As spot buyers stepped in, short sellers were forced to cover positions, accelerating the advance through successive resistance levels.

The move gained additional momentum once price reclaimed its short-term moving averages, encouraging systematic traders to add fresh long exposure.

On-chain activity has also improved. Fresh USDT deposits into Aave’s lending markets have increased available liquidity across the protocol, supporting borrowing activity and reinforcing investor confidence in one of DeFi’s largest lending platforms. Stronger stablecoin inflows often accompany periods of renewed capital deployment into decentralized finance, particularly after sharp market-wide corrections.

Derivatives positioning has added another layer of support. Rising open interest alongside positive funding rates suggests traders have continued building long exposure instead of simply closing shorts. That combination points to fresh capital entering the market rather than a temporary relief rally driven solely by liquidations.

Macro conditions remain mixed. The Federal Reserve’s higher-for-longer interest-rate stance continues to weigh on speculative assets, while a firm U.S. dollar has limited risk appetite across crypto markets.

Even so, established DeFi protocols such as Aave have continued attracting capital from investors seeking on-chain yield opportunities, allowing the token to outperform many large-cap altcoins during the latest rebound.

The next several sessions will likely determine whether buyers can convert the current recovery into a confirmed breakout. A daily close above the $85-$88 resistance zone would expose the next upside targets around $102 and $132, while failure to clear the descending trendline could send AAVE back toward support between $72 and $75.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Pepe Double Sends Ivory Coast Into First-Ever World Cup Knockout Stage

Judge halts Trump’s order to create federal voter list

About 50% of UK Wealth Advisors Cannot See Most of Their Clients’ Crypto Holdings

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment5 days ago

Entertainment5 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports2 days ago

Sports2 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech4 days ago

Tech4 days agoMicrosoft accidentally kills epic Outlook email threads

-

Business5 days ago

Business5 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics6 days ago

Politics6 days agoAndy Burnham and the meaning of Makerfield

-

NewsBeat7 days ago

NewsBeat7 days agoKeir Starmer Allies Question His Chances For No 10

-

Tech9 hours ago

Tech9 hours agoA Look At A Gaggle Of Transputer Boards

-

Crypto World2 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World2 days ago

Crypto World2 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Business2 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Business6 days ago

Business6 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Crypto World6 days ago

Crypto World6 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Crypto World6 days ago

Crypto World6 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World6 days ago

Crypto World6 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Entertainment6 days ago

Entertainment6 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Tech5 days ago

Tech5 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Sports15 hours ago

Sports15 hours agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

-

Tech3 days ago

Tech3 days agoNearly 7,000 fake Amazon domains registered ahead of Prime Day 2026, researchers warn

-

Business5 days ago

Business5 days agoMHP SE 2026 Q1 – Results – Earnings Call Presentation (OTCMKTS:MHPSY) 2026-06-20

You must be logged in to post a comment Login