Crypto World

What is atomic settlement? Payment-versus-Payment and the and of settlement risk

Atomic settlement means both sides of a deal are complete at the same instant or neither does, removing the centuries-old danger that one party pays and the other fails to deliver. This guide explains payment-versus-payment, why blockchains make it natural, and how banks are now testing it for cross-border trades.

Summary

- Atomic settlement means both sides of a transaction complete at the exact same moment or neither does, removing the risk that one party pays and the other fails to deliver.

- It targets settlement risk, the danger that has haunted finance for decades, most famously when a bank’s collapse left counterparties paid on one leg but not the other.

- Payment-versus-payment (PvP) applies this to currency trades and delivery-versus-payment (DvP) to securities, ensuring the two legs are linked and simultaneous.

- Blockchains and smart contracts make atomic settlement natural, because a single transaction can be programmed to either execute both legs together or fail entirely.

- The shift promises to compress settlement from days toward instant, and bank-backed projects are now testing it for cross-border foreign exchange.

Atomic settlement is a way of completing a transaction so that both sides happen at the same instant or neither happens at all, with no possibility that one party fulfills its obligation while the other fails to fulfill theirs. The word “atomic” captures the essential property: the transaction is indivisible, an all-or-nothing event that cannot be split into a completed half and an uncompleted half. This may sound like an obscure technicality, but it addresses one of the oldest and most dangerous problems in finance, the risk that arises in the gap between agreeing to a trade and actually settling it, during which one party can pay or deliver while the other defaults, leaving the first party out of pocket.

Atomic settlement closes that gap entirely by binding the two sides of a transaction together so they succeed or fail as a single unit. Blockchains, as it happens, are unusually well suited to delivering this property, which is why atomic settlement has become a central promise of tokenized finance.

This guide explains what atomic settlement is, the settlement risk it eliminates, how it applies to payments and securities, why blockchains make it natural, and how banks are now testing it in the real world.

The reason this matters is that settlement risk, though invisible to most people, is a genuine systemic danger that has caused real crises, and the financial industry has spent decades and enormous resources trying to manage it. Atomic settlement offers something the traditional system has never quite achieved: the complete elimination of that risk, not its mitigation but its removal, by making it structurally impossible for one leg of a trade to settle without the other.

Combined with the ability to compress settlement times from days to near-instant, the implications for capital efficiency and financial stability are significant. This guide covers the meaning of atomicity, the nature of settlement risk and the famous failure that named it, the payment-versus-payment and delivery-versus-payment models, a concrete worked example, why blockchains make atomic settlement natural, the move from multi-day to instant settlement, the real-world bank projects now testing it, and the genuine hurdles that remain.

What atomic settlement means

Begin with the core property, because everything else follows from it. A transaction is atomic when it is indivisible: it either completes in full, with both sides fulfilling their obligations simultaneously, or it does not happen at all, with neither side committed. There is no in-between state in which one party has paid and the other has not.

The term is borrowed from computing, where an atomic operation is one that cannot be interrupted partway through, and it carries the same meaning in finance: an atomic settlement cannot be left half-done. If anything would prevent both legs from completing together, the entire transaction reverts, returning both parties to where they started as if nothing had happened.

This all-or-nothing quality is what makes atomic settlement powerful. In an ordinary transaction split across time, there is always a window during which one party has performed and is waiting for the other to perform, and in that window the first party is exposed to the risk that the second fails.

Atomic settlement abolishes that window by making the two performances a single, simultaneous, inseparable event. Neither party can find itself having given value without receiving it, because the giving and receiving are bound together and happen at once or not at all.

The significance is that a risk which traditional finance has always had to manage, monitor, and price, the risk lurking in the gap between the legs of a trade, simply ceases to exist under atomic settlement, because the gap itself is gone. Understanding that the entire benefit flows from this one structural property, indivisibility, is the key to understanding why atomic settlement matters.

The problem it solves: settlement risk

To appreciate atomic settlement, you have to understand the danger it removes, which is called settlement risk, and there is no better illustration than the event that gave one form of it its name. In 1974, a German bank named Herstatt was shut down by regulators in the middle of a business day. Earlier that day, counterparties had paid the bank in German marks as their side of foreign-exchange trades, expecting to receive United States dollars in return once the New York business day began. But the bank was closed before it made those dollar payments, so the counterparties had handed over their marks and received nothing back. They had performed their leg of the trade and were left exposed when the bank failed to perform its leg. This specific danger, where one party pays and the other fails before reciprocating, became known as Herstatt risk, a permanent reminder of what settlement risk can do.

Settlement risk, in general, is the risk that arises in any transaction where the two sides do not settle simultaneously. Whenever there is a gap between when one party performs and when the other does, the party that goes first is exposed to the possibility that the counterparty defaults, becomes insolvent, or simply fails to deliver in that interval. This is sometimes called principal risk, because the party can lose the entire principal amount it advanced, not merely the profit on the trade.

Across the global financial system, where trillions of dollars in currencies, securities, and other assets change hands daily, settlement risk is a pervasive and serious concern, and managing it requires extensive infrastructure, collateral, monitoring, and trust. Atomic settlement is so significant precisely because it does not merely reduce this risk through better management; it eliminates it structurally, by ensuring the two legs settle together so that neither party is ever exposed to the other’s potential failure. The problem that closed Herstatt and has haunted finance ever since simply cannot occur when settlement is atomic.

Payment-versus-Payment and Delivery-versus-Payment

The principle of atomic settlement shows up in finance under two main labels, depending on what is being exchanged, and knowing the difference clarifies the concept. When the exchange is one currency for another, as in a foreign-exchange trade, the atomic version is called payment-versus-payment, often abbreviated PvP.

Under PvP, the payment in one currency and the payment in the other currency are linked so that both happen simultaneously or neither does, ensuring that no party can pay in one currency without receiving the other. This is the direct answer to Herstatt risk: under true PvP, the situation that destroyed Herstatt’s counterparties, paying marks and not receiving dollars, becomes impossible, because the two payments are bound together.

When the exchange is an asset for a payment, as when securities are bought or sold, the atomic version is called delivery-versus-payment, abbreviated DvP. Under DvP, the delivery of the security and the payment for it are linked so that the asset changes hands at the same instant as the money, ensuring that no party delivers a security without receiving payment, and no party pays without receiving the security.

Both PvP and DvP are expressions of the same atomic principle applied to different kinds of trades, and both aim to eliminate the settlement risk that lives in the gap between the legs. The traditional financial system has built elaborate infrastructure to approximate these protections, such as specialized settlement institutions that hold both legs and release them together, but these systems are complex, do not cover every currency or market, and still leave gaps. Atomic settlement on a blockchain offers a way to achieve PvP and DvP more directly and more universally, which is a large part of why the technology has drawn such intense institutional interest.

A worked example: an FX trade with and without atomicity

To make settlement risk and its atomic solution concrete, walk through a single foreign-exchange trade both ways. Suppose a bank in Europe agrees to sell ten million euros to a bank in Asia in exchange for the equivalent in dollars. Under the traditional, non-atomic process, the two payments may not happen at the same moment, because the banks operate in different time zones and through different payment systems.

The European bank might send its euros during its business day, expecting the dollars to arrive later when the other party’s systems process the payment. In the interval between sending the euros and receiving the dollars, the European bank is exposed: if the Asian bank fails, defaults, or is shut down in that window, the European bank has paid ten million euros and may receive nothing, losing the entire principal. This is exactly the Herstatt scenario, and it is a real risk that institutions must monitor and manage on every such trade.

Now run the same trade with atomic settlement. The euro payment and the dollar payment are bound together into a single, indivisible transaction, structured so that both transfers execute at the same instant or neither executes at all. If for any reason the dollar leg cannot complete, the euro leg does not complete either, and both banks remain exactly where they started, with no exposure and no loss.

The European bank can never find itself having sent euros without receiving dollars, because the protocol makes that outcome structurally impossible. The risk window that existed in the traditional version is gone, not managed or reduced but eliminated, because the two legs are no longer separated in time. That is the difference atomicity makes: it converts a trade with an unavoidable risk window into a trade with no risk window at all, which is why the financial industry regards atomic settlement as a genuine advance rather than an incremental improvement.

Why blockchains make atomic settlement natural

Atomic settlement is not new as a concept, but blockchains make it dramatically easier to achieve, and understanding why reveals the deep fit between the technology and the problem. A blockchain transaction is, by its nature, atomic at the level of the ledger: it either executes completely and is recorded, or it fails and changes nothing. Smart contracts, the programmable agreements that run on many blockchains, extend this property to complex, multi-step transactions.

A smart contract can be written so that it performs two transfers, say, moving one asset from party A to party B and another asset from party B to party A, as a single operation that either completes both transfers together or reverts entirely, leaving both parties untouched. This is atomic settlement expressed directly in code, with the all-or-nothing guarantee enforced by the blockchain itself rather than by an external institution.

This is a profound fit, because the property that finance has always struggled to guarantee, that two legs of a trade settle together or not at all, is something a blockchain provides almost for free, as a basic feature of how it works. The earliest crypto version of this idea was the atomic swap, a way for two parties to exchange different cryptocurrencies such that the swap either completes for both or fails for both, with no possibility of one party absconding with the other’s coins.

The same principle now underpins the tokenization of traditional assets: if currencies and securities are represented as tokens on a blockchain, then trades between them can be settled atomically by smart contracts, achieving true PvP and DvP without the elaborate intermediary infrastructure the traditional system requires. The blockchain becomes the neutral venue where both legs settle simultaneously and trustlessly. This is why atomic settlement is so central to the institutional interest in tokenization: the technology delivers, as a native capability, the settlement guarantee that traditional finance has spent decades and fortunes trying to approximate.

From multi-day to instant settlement

Closely tied to atomic settlement is the compression of settlement time, and the two together explain much of the institutional excitement. In traditional markets, settlement often does not happen immediately after a trade is agreed; instead, it occurs after a delay, commonly a couple of business days for many securities, a convention referred to by labels like T plus two, meaning trade date plus two days.

This delay exists for historical and operational reasons, because the traditional system needs time to coordinate the many parties, records, and transfers involved in settling a trade. But the delay is costly: during the gap between trade and settlement, capital is tied up, positions carry risk, and the settlement exposure discussed above persists for longer. Shortening the cycle has been a long-running goal of market reform, with markets gradually moving from longer cycles to shorter ones over the years.

Atomic settlement on a blockchain points toward the logical endpoint of this trend: instant settlement, sometimes called T plus zero, where the trade settles the moment it is executed. Because a smart contract can bind and complete both legs simultaneously, there is no operational reason for a multi-day delay; the settlement can happen at the instant of the trade.

This collapses the settlement window from days to seconds, which has large benefits. Capital is freed immediately rather than tied up for days, settlement risk persists for moments instead of days, and the entire system becomes more efficient and less exposed. The combination of atomicity, which removes the risk in the gap between legs, and instant settlement, which removes the gap in time, is what makes blockchain-based settlement so attractive to institutions.

Together, they promise a financial system where trades settle instantly and with no settlement risk, a meaningful improvement over a status quo built around multi-day cycles and the risks they carry.

The real-world push: bank projects and tokenization

This is not merely theoretical, because banks and market infrastructures are actively testing atomic settlement, which signals that the technology is moving from concept toward production. A notable recent example is a bank-backed initiative bringing together a large group of international banks to study faster cross-border foreign-exchange settlement using atomic, payment-versus-payment swaps of compliant stablecoins, aiming to replace the multi-day settlement that currency trades often still require with simultaneous, same-instant settlement.

The design deliberately works with existing bank standards and messaging infrastructure instead of asking banks to abandon their systems, layering atomic settlement onto the rails they already use. The scale of such efforts, involving banks representing trillions of dollars in assets, shows that the institutional world takes atomic settlement seriously as a practical goal, not just a research curiosity.

The broader context is the tokenization of real-world assets, which is the larger movement that atomic settlement enables. As currencies, government bonds, equities, and funds are increasingly represented as tokens on blockchains, the trades between them can be settled atomically, achieving the simultaneous, risk-free settlement that has long been the ideal.

Major financial institutions and market infrastructures have been running pilots and building platforms for tokenized assets precisely because the settlement properties are so attractive, and the tokenized-asset sector has grown substantially as a result. The convergence of tokenized assets and atomic settlement is, in many ways, the heart of the institutional crypto thesis: not speculative tokens, but the use of blockchain technology to settle real financial transactions instantly and without settlement risk.

The bank projects testing it today are the early, concrete steps toward that future, and their progress is a useful signal of how quickly atomic settlement is moving from promise to practice.

Risks and open questions

For all its promise, atomic settlement carries real hurdles and risks that an informed reader should weigh instead of accepting the idealized vision. The first is a liquidity requirement: atomic settlement demands that both legs of a trade be available to settle at the same instant, which means the necessary assets or funds must actually be present on the settlement venue simultaneously. In a world where value is fragmented across many blockchains and traditional systems, ensuring that both legs are present and ready at the same moment is a genuine operational challenge, and a trade cannot settle atomically if one side’s liquidity is not there when needed.

Other open questions are significant. Legal finality is one: for atomic settlement to be trusted by institutions, the law must recognize a blockchain settlement as final and irreversible in the same way it recognizes traditional settlement, and the legal frameworks for this are still developing in many jurisdictions.

Fragmentation is another, because if assets are tokenized across many incompatible blockchains, achieving atomic settlement between them requires interoperability that does not always exist, and bridging between chains can reintroduce the very risks atomic settlement was meant to remove.

There are also operational demands, since instant, around-the-clock settlement requires institutions to manage liquidity continuously instead of within business-day cycles, a real change to how treasury operations work. And the technology itself must be secure, because a flaw in a settlement smart contract could undermine the guarantees the whole system relies on.

None of these hurdles is necessarily fatal, and the active bank projects suggest they are being worked through, but they are real, and atomic settlement should be understood as a powerful approach still maturing instead of a finished solution. As with any emerging financial technology, the gap between a successful pilot and universal adoption can be wide, and the risks in that gap are worth respecting.

Frequently Asked Questions

What is atomic settlement in simple terms?

Atomic settlement is a way of completing a transaction so that both sides happen at the same instant or neither happens at all. The word “atomic” means indivisible: the transaction cannot be left half-done, with one party having paid and the other not. If anything would stop both legs from completing together, the whole transaction reverts and both parties end up where they started. This removes the risk that one party performs while the other fails, which is the core danger in any trade where the two sides do not settle simultaneously.

What is settlement risk?

Settlement risk is the danger that arises in the gap between agreeing to a trade and actually settling it, during which one party can pay or deliver while the other defaults, leaving the first party exposed. It is sometimes called principal risk, because the exposed party can lose the entire amount it advanced. The classic example is Herstatt risk, named after a German bank shut down in 1974 after its counterparties had paid it in marks but before it paid them dollars, leaving them with nothing. Atomic settlement eliminates this risk by binding the two legs together.

What is the difference between PvP and DvP?

Both are forms of atomic settlement applied to different trades.

Payment-versus-payment, or PvP, applies to currency exchanges, linking the payment in one currency to the payment in the other so both happen together or neither does, which directly prevents Herstatt-style losses.

Delivery-versus-payment, or DvP, applies to securities, linking the delivery of the asset to the payment for it so the security and the money change hands at the same instant. Both express the same atomic principle, ensuring no party gives value without simultaneously receiving what they were promised.

Why are blockchains good at atomic settlement?

Because a blockchain transaction is naturally atomic: it either executes completely or fails and changes nothing. Smart contracts extend this to complex trades, allowing two transfers to be bound into a single operation that either completes both together or reverts entirely. This gives, as a native feature, the all-or-nothing settlement guarantee that traditional finance has spent decades trying to approximate with elaborate intermediary infrastructure. When currencies and securities are tokenized on a blockchain, trades between them can settle atomically through smart contracts, achieving true PvP and DvP directly.

What is the difference between T+2 and T+0 settlement?

T plus two means a trade settles two business days after it is agreed, a common convention in traditional markets that exists because the legacy system needs time to coordinate the many parties and records involved. During that delay, capital is tied up and settlement risk persists. T plus zero, or instant settlement, means the trade settles the moment it is executed, which atomic settlement on a blockchain makes possible because a smart contract can complete both legs simultaneously. Moving from T plus two to T plus zero frees capital immediately and shrinks the risk window from days to seconds.

Is atomic settlement actually being used?

It is being actively tested and piloted instead of universally deployed. Bank-backed initiatives have brought together large groups of international banks to study faster cross-border foreign-exchange settlement using atomic, payment-versus-payment swaps, working with existing bank standards instead of replacing them. The broader tokenization of real-world assets, which has grown substantially, relies on atomic settlement as a core benefit, and major institutions have run pilots and built platforms around it. So atomic settlement is moving from concept toward practice, though real hurdles around liquidity, legal finality, interoperability, and operations remain to be worked through.

This article is educational information, not financial or investment advice. The technology and the projects described are still developing, and details reflect reporting available as of June 26, 2026, which can change quickly. Verify current information from primary sources before relying on anything described here.

Prediction-market operator Kalshi is in talks to raise fresh capital at a valuation of roughly $40 billion, according to the Financial Times, nearly double the price tag from a round that closed just seven weeks ago. The Financial Times first reported the talks, citing people familiar with the… Read the full story at The Defiant

Securitize has secured commitments expected to deliver about $400 million ahead of its planned New York Stock Exchange debut through a merger with Cantor Equity Partners II.

Summary

- Securitize expects to raise about $400 million ahead of its planned NYSE listing through a merger with Cantor Equity Partners II.

- Backed by BlackRock, Morgan Stanley, Coinbase, and Circle, the firm continues expanding its tokenization business with new institutional products.

- The market debut comes as Securitize grows its on-chain asset platform while defending itself in a patent dispute with tZERO.

According to Securitize, fewer than 30% of shareholders in Cantor Equity Partners II, the special purpose acquisition company taking the firm public, chose to redeem their shares following the final redemption results.

The company said it now expects to receive approximately $400 million in gross proceeds from the transaction, including related private investment in public equity (PIPE) financing, before transaction-related expenses.

The proposed listing comes as tokenization companies continue attracting institutional attention, with firms seeking to bring traditional financial assets onto blockchain networks. Securitize counts BlackRock, Morgan Stanley, Coinbase, and Circle among its backers and has become one of the largest providers of tokenization infrastructure for financial institutions.

The merger is expected to complete next week

Market reaction has been positive ahead of the vote. Shares of Cantor Equity Partners II closed 7% higher at $10.86 on Friday before extending gains in after-hours trading to $11.

According to Securitize, shareholders are scheduled to vote on the merger on Monday. If approved and all remaining closing conditions are satisfied, the transaction is expected to close on July 1. The combined company is then expected to begin trading on the New York Stock Exchange under the ticker SECZ on July 2.

Commenting on the listing, Securitize co-founder and CEO Carlos Domingo said reaching the public markets represents an important step for the company after more than eight years of building tokenization infrastructure.

“Reaching the public markets is a significant milestone for Securitize and a reflection of the growing momentum behind tokenization.”

Domingo added that tokenized securities, once considered largely theoretical by major financial institutions, are now moving into mainstream finance as institutional adoption continues to grow.

The public debut also follows several months of expansion for the company. As previously reported by crypto.news, Securitize recently extended its Tokenized AAA CLO Fund (STAC) to the Solana blockchain. The company said Ethena Labs plans to allocate $250 million to the fund, which invests in U.S. dollar-denominated AAA-rated collateralized loan obligation tranches.

According to Securitize, the product is developed with BNY serving as custodian of the underlying assets and sub-adviser through BNY Investments.

Institutional tokenization business continues to expand

Alongside new investment products, Securitize has continued growing its role in tokenized capital markets. Earlier this year, the company partnered with the New York Stock Exchange to support the exchange’s planned tokenized securities platform.

Crypto.news previously reported that Securitize provides tokenization infrastructure for more than 650 funds and oversees more than $4 billion in tokenized assets. BlackRock has also deepened its relationship with the firm.

In May, crypto.news reported that the asset manager filed a second Securitize-powered tokenized fund with the U.S. Securities and Exchange Commission after its BUIDL fund expanded to roughly $2.3 billion in assets.

At the same time, Securitize is dealing with a legal dispute ahead of its market debut. As reported by crypto.news, the company recently asked the U.S. District Court for the District of Delaware to declare that its products do not infringe patents owned by tZERO after receiving a cease-and-desist letter. Securitize called the allegations “without merit,” while tZERO said its claims involve patents covering compliance systems, investor registry checks, and tokenized market infrastructure.

Separate industry forecasts also point to continued growth in tokenized finance. Earlier this month, Standard Chartered projected that tokenized assets used in decentralized finance could reach $2.7 trillion by the end of 2030, up from current levels.

Base, Coinbase’s Ethereum layer-2 network, has resumed normal operation after a consensus-related issue temporarily halted block production for nearly two hours on Thursday. The incident triggered “unhealthy” block building, leaving new blocks unable to be created until the network isolated and corrected the underlying problem.

Base said blocks were later being produced normally and that the broader ecosystem infrastructure had recovered and synced. The outage was unusual for a chain that has become a go-to venue for activity on Ethereum’s scaling roadmap, highlighting how sensitive rollup operations can be when consensus and sequencing logic fail.

Key takeaways

- Base went offline briefly due to a consensus problem that resulted in an invalid block being sequenced and prevented new block creation.

- Base reported recovery of “healthy blockbuilding” and confirmed ecosystem-wide infrastructure synchronization.

- The outage occurred around an on-chain upgrade window, with a Base upgrade (“Beryl”) scheduled for 6 pm UTC.

- Network creators emphasized that user funds remained safe, while reiterating that a block-production halt is not acceptable.

- Thursday’s incident joins a small set of notable recent outages affecting major L2 ecosystems.

How the outage unfolded

Base’s status page said it began investigating “unhealthy” block production at 4:03 pm UTC on Thursday. In a subsequent update at 5:21 pm UTC, the Base team explained that it had “isolated a consensus problem” which caused an invalid block to be sequenced.

According to the status updates, that invalid sequencing stopped progress at the protocol level: “This prevented new blocks from being created.” In other words, the issue was not presented as a simple infrastructure hiccup; it was tied to the chain’s ability to agree on what should be built next.

Recovery confirmed, post-mortem expected

Base later posted an operational recovery update just before 6 pm UTC. It said the network had “recovered healthy blockbuilding,” and that ecosystem-wide infrastructure was able to sync again. Base also indicated that it had identified the issue and would continue investigating the root cause, promising a full post-mortem.

Separately, Base’s creator Jesse Pollack used X to reassure users that funds on the network are safe. Pollack also framed the halt as a solvable operational setback, saying it would be used to “level up” Base as a platform aimed at supporting continuous, global finance.

An uncommon downtime event for a leading L2

The episode stands out as a rare downtime event for Base. The report notes that Base is widely considered among the most-used Ethereum layer-2 networks, and it cites the chain’s previous major outage in August 2025, when Base reportedly went down for 33 minutes. That earlier incident is referenced via Base’s status page.

Such disruptions matter for users and developers because L2 block production is the backbone for transaction inclusion, sequencing, and timely settlement flows. Even if funds remain safe, a halt can translate into delays for withdrawals, reduced reliability for dApps, and friction for systems that assume steady block cadence.

Upgrade timing raises questions for reliability planning

Base downtime appeared to occur separately and shortly ahead of a scheduled network upgrade dubbed “Beryl,” planned for 6 pm UTC. The described goal of the Beryl upgrade was to reduce delays on withdrawals and introduce a new token standard intended for real-world assets and stablecoins.

That timing is important for operators and integrators: when an outage overlaps with a planned change, teams typically have to ensure that the network can recover cleanly and continue the upgrade without compounding issues. Base did not state that the outage directly affected the Beryl rollout, but the proximity means builders watching Base would likely want to see post-recovery monitoring closely through the upgrade window.

The incident also comes amid broader reminders across the L2 landscape. The report points to Sui experiencing two periods of downtime on back-to-back days in May, each involving temporary stops in block production. In that case, Sui later attributed the downtime to a network update it said it knew had a low probability of causing a halt—an example of how even planned changes can create operational risk.

What to watch next

Base has said it will share a detailed post-mortem and identified the consensus problem responsible for blocking new block creation. Investors, traders, and developers should watch for that report, plus confirmation that the Beryl upgrade proceeds smoothly with stable block production and no renewed consensus symptoms around the new token standard changes.

Tokenization platform Securitize is set to make its long-awaited leap into the public markets after reporting final redemption results for its merger partner, Cantor Equity Partners II (CEPT). According to Securitize’s filing, fewer than 30% of CEPT shareholders chose to redeem their shares—an outcome that improves the odds that the deal can move forward as scheduled.

The company said the transaction is expected to generate approximately $400 million in gross proceeds, including private investment in public equity (PIPE) financings. The merger is expected to close on Wednesday, July 1, followed by trading on the New York Stock Exchange under the ticker SECZ on Thursday, July 2, subject to shareholder approval on Monday and other closing conditions.

Key takeaways

- Securitize said final redemption results show less than 30% of CEPT shareholders redeemed, a lower-than-feared level that supports deal momentum.

- The merger is expected to bring in about $400 million in gross proceeds, including PIPE financing, excluding transaction-related expenses.

- The company plans to begin NYSE trading under ticker SECZ on July 2, after the July 1 expected closing.

- The move reflects accelerating institutional interest in tokenized securities amid heightened attention from US regulators.

Redemption results reduce uncertainty for the merger

The immediate catalyst for CEPT’s post-announcement trading was Securitize’s update on final redemption outcomes. In a statement to investors reported by PR Newswire, Securitize said that its final redemption results indicated that fewer than 30% of CEPT shareholders elected to redeem.

Redemption thresholds matter for SPAC-style transactions because they directly affect the cash proceeds available at closing. While Securitize did not characterize the numbers as “unexpected” in its release, the company’s disclosure effectively signals that the funding structure underpinning the merger is likely to remain intact, clearing one of the more common obstacles for deals tied to shareholder opt-outs.

On Friday, CEPT shares rose, closing up 7% to $10.86 and continuing higher after hours to $11, according to market data cited alongside the announcement.

Expected proceeds and what they mean for tokenization ambitions

Beyond the redemption update, Securitize outlined the expected funding to be raised through the combination. The company said it expects to receive approximately $400 million in gross proceeds from the merger, including related PIPE financings, while excluding transaction-related expenses.

For investors watching tokenization, the scale of the proceeds is not just about corporate finance—it also points to how seriously major market participants are preparing for tokenized securities infrastructure. Tokenization remains a complex intersection of technology, market structure, and regulatory compliance. Capital raised in public markets can help cover product expansion, business development, and operational scaling as tokenized offerings move from pilots toward broader rollouts.

Securitize positions the listing as a “significant milestone” and, in remarks shared in the company’s release, CEO Carlos Domingo framed the step as evidence that tokenization is shifting from a niche concept to a mainstream institutional priority.

Why this public listing matters to the tokenization market

Securitize’s debut arrives at a moment when Wall Street increasingly views tokenization as a route to improved settlement efficiency and asset accessibility, while regulators continue to refine expectations for how tokenized securities should be offered and traded.

The company is backed by major institutions, including BlackRock and Morgan Stanley, and also counts crypto-native firms such as Coinbase and Circle among its supporters, according to the information provided in the announcement. That blend matters because it suggests tokenization is being pursued simultaneously through traditional capital markets channels and crypto rails—an alignment that can influence how liquidity, custody, and compliance tooling evolves.

In addition, Securitize has been actively working with established market infrastructure. Earlier this year, the company partnered with the New York Stock Exchange in March to support tokenized assets for the exchange’s upcoming tokenized securities platform—an effort reported by Cointelegraph. While that project is distinct from Securitize’s SPAC path, it reinforces the company’s goal of becoming a bridge between regulated markets and tokenized issuance.

Elsewhere in the broader ecosystem, Standard Chartered earlier this month projected that tokenized assets active in decentralized finance could expand 37-fold to $2.7 trillion by the end of 2030. That kind of forecast underscores why investors are paying attention to tokenization platforms that can operate across different settlement and trading environments.

Regulatory backdrop: SEC decisions still shape the pace

Even as interest grows, US regulatory uncertainty continues to influence how quickly tokenized products can be adopted in mainstream trading venues. In mid-May, Cointelegraph reported that the US Securities and Exchange Commission was reportedly ready to allow trading of tokenized stocks under an innovation-related framework. However, the plan was later delayed after stock exchange officials raised concerns about implementation details, according to that earlier coverage.

This matters for Securitize and peers because the path from “tokenization is possible” to “tokenization is broadly tradable” depends heavily on regulatory clarity—especially around operational readiness, market oversight, and the mechanics of secondary trading for tokenized instruments. A public-market listing can bring visibility and liquidity, but compliance and market structure decisions still determine how fast product adoption accelerates.

What to watch next

With a planned July 1 closing and July 2 NYSE start under ticker SECZ, the next key signal will be whether shareholder approval and remaining closing conditions clear without further complications. Investors should also watch how regulatory developments around tokenized stock trading evolve, since they will likely influence the pace at which tokenization platforms convert momentum into large-scale liquidity and recurring issuance.

US-listed spot Bitcoin exchange-traded funds (ETFs) posted their largest June daily net outflows on Thursday, following renewed weakness in Bitcoin that pushed the asset below the $60,000 level. The withdrawals underscore a cooling in demand that many US-listed ETF investors previously relied on as a stabilizing institutional inflow channel.

SoSoValue data shows the outflows amounted to $696.3 million on the day, exceeding the prior monthly peak of $519.2 million recorded on June 2. As a result, total net outflows for June rose to $3.61 billion, lifting year-to-date net outflows to $4.6 billion, according to the same dataset.

Key takeaways

- US spot Bitcoin ETFs saw a $696.3 million net outflow on Thursday, the largest daily outflow in June.

- June net outflows reached $3.61 billion, bringing year-to-date net outflows to $4.6 billion (SoSoValue).

- Total net assets in US spot Bitcoin ETFs fell below $73 billion for the first time since late 2024, down roughly 57% from a reported October 2025 peak.

- Separate tracking data indicates ETF BTC holdings declined by about 63,500 BTC over the past 30 days.

- Strategy’s reported June buying pace slowed materially, prompting renewed scrutiny of institutional accumulation risk management and liquidity planning.

Spot Bitcoin ETF outflows accelerate in June

The Thursday withdrawals represent a material step-down in net inflows that had been supporting ETF balance sheets earlier in the year. According to SoSoValue, the $696.3 million net outflow surpassed the previous June high daily outflow recorded on June 2, signaling that the pullback is not confined to isolated days.

From a compliance and institutional risk perspective, sustained outflows can affect how ETF issuers and their service providers manage operational readiness and liquidity across custody, brokerage settlement, and fund administration. While ETFs remain structurally distinct from crypto spot custody models used by direct holders, the flow-through effect on the underlying Bitcoin exposure can become relevant to internal risk controls, including contingency planning for valuation, margining arrangements (where applicable), and concentration monitoring.

ETF net assets and holdings retrace from late-2025 highs

In addition to daily flows, broader balance-sheet data points to a sustained contraction in the ETF complex. SoSoValue reports that total net assets in US-listed spot Bitcoin ETFs have fallen below $73 billion for the first time since late 2024. The same source previously cited a record net assets level of $169.5 billion in October 2025; the latest figure is about $72.6 billion, representing a decline of roughly 57%.

WalletPilot data provides a view into the underlying Bitcoin holdings. It indicates that the funds held a combined 1.24 million BTC as of Tuesday, with approximately 63,500 BTC leaving the products over the prior 30 days. For institutions, the shift from flow-based indicators to holdings-based indicators is often critical: daily net flows can reverse quickly, but reductions in the total BTC held can influence longer-horizon risk assessments related to custody balances, redemption dynamics, and exposure to market-wide volatility.

Strategy’s slower accumulation draws renewed attention

ETF outflows are occurring alongside signs that other large sources of institutional Bitcoin demand are easing. Strategy, described as the world’s largest corporate Bitcoin holder, reportedly reduced its pace of Bitcoin accumulation during June.

Company filings indicate Strategy has bought roughly 3,600 Bitcoin so far in June, down from about 25,000 BTC in May and more than 50,000 BTC in April. The filings also show a net sale of 32 BTC earlier in the month—one of the few instances in which the company has sold Bitcoin during its accumulation period.

The change in behavior has prompted renewed debate about corporate treasury strategy, particularly whether liquidity preservation becomes a priority during market downturns. Critics have argued that Strategy should pause additional purchases and instead rebuild cash reserves, pointing to the importance of downside risk management for firms that rely on balance-sheet leverage and equity-linked financing structures.

In June’s context, institutional scrutiny is not limited to “buy or sell” decisions. It also extends to how capital is raised, how discount rates and equity market conditions influence treasury financing, and what liquidity buffers are maintained to support continued operations. These issues can indirectly affect how regulated counterparties—such as lenders, underwriters, and custodians—assess operational continuity.

Financing-market pressure and the preferred stock debate

Strategy’s perpetual preferred stock (STRC) has reportedly come under pressure. The stock has traded below its intended $100 benchmark level, with Thursday’s close reported at $75.69, down 6.37%.

The price movement has fueled discussion around whether the company’s preferred share financing approach is aligned with its long-term accumulation plan under stressed market conditions. CryptoQuant analysts raised concerns about timing and risk management, while Bitcoin advocate Samson Mow argued that STRC has a “self-repairing mechanism” that activates when the stock trades below its $100 benchmark. He also noted that Strategy pauses new share issuance through its ATM program at that level, limiting new supply.

For institutional stakeholders, this debate matters because financing mechanics can influence the predictability of future purchasing behavior. Where issuance programs and preferred-stock terms include triggers or constraints, equity-market volatility can propagate into accumulation schedules—creating uncertainty for counterparties that model corporate Bitcoin demand. It also raises questions for governance and disclosure oversight, particularly for firms subject to securities regulation and investor reporting obligations.

More broadly, policy compliance teams monitoring the crypto market may find it useful to connect these developments to regulatory context. US-listed spot Bitcoin ETFs operate under a mature set of investor protection expectations, including custody arrangements and securities-law compliance frameworks. At the same time, corporate treasuries and their financing instruments intersect with conventional financial regulation, making transparency and risk disclosures a recurring theme for oversight bodies.

What to watch next

Whether ETF outflows continue or reverse will likely remain the near-term indicator that shapes institutional exposure to Bitcoin via regulated wrappers. Separately, Strategy’s future acquisition cadence and any further changes in financing-market conditions could affect expectations for corporate demand, reinforcing the need for monitoring of disclosures, treasury liquidity posture, and the operational implications of sustained reductions in net asset growth.

Rosen Law Firm opened a securities investigation into Strategy Inc., examining whether the Bitcoin treasury company issued materially misleading disclosures to investors across its entire capital stack, including common shares and all four series of preferred stock. The investigation notice,… Read the full story at The Defiant

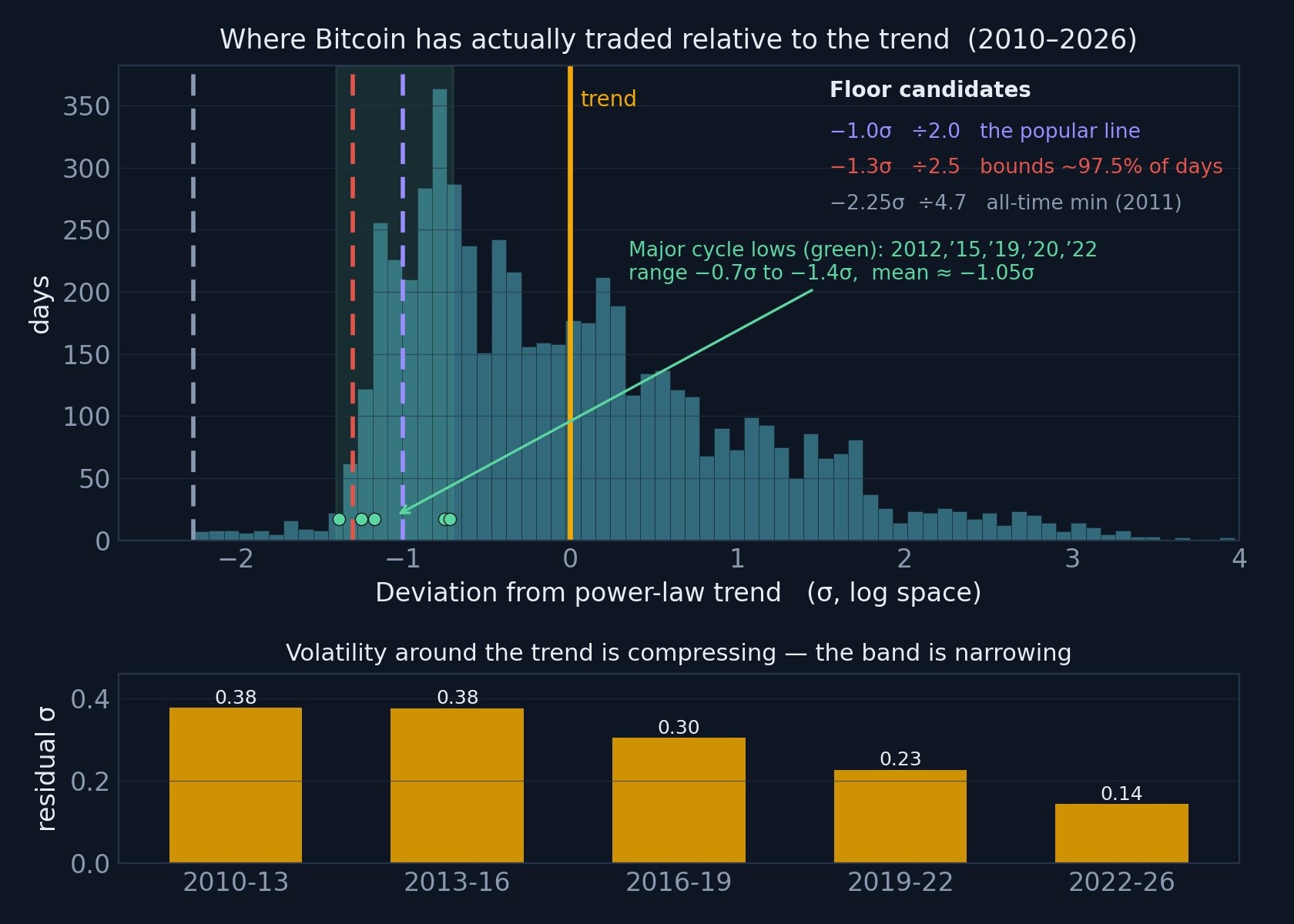

Bitcoin’s (BTC) drop to $58,000 has pushed the price into a zone that long-term power-law models have historically associated with cycle bottoms. The data does not confirm a bottom range, though it shows BTC trading in a price range that has repeatedly marked major lows since 2014.

Derivatives data and liquidation levels highlight $55,000 as the next key support level and the $65,000-$68,000 range as the next major upside area of interest.

Bitcoin power-law puts $58,000 in historical range

Giovanni’s Bitcoin power-law model places the network’s long-term trend price near $135,000, making the recent drop to $58,000 roughly 54% below the all-time high and 1.22 standard deviations beneath that trend.

According to the analyst, the key takeaway is straightforward: the previous cycle lows in 2012, 2015, 2019, 2020, and 2022 all fell within a similar statistical range. By that measure, the latest decline falls within a territory that has historically marked the deep bear-market lows rather than a break in Bitcoin’s long-term growth path.

Bitcoin price deviation based on the power-law trend. Source: X

The model estimates the commonly referenced “-1σ” support near $68,000, while the stronger historical floor sits closer to $55,000. Giovanni also noted that Bitcoin would need to trade below roughly $17,000 for more than a year before the power-law itself could be considered invalid.

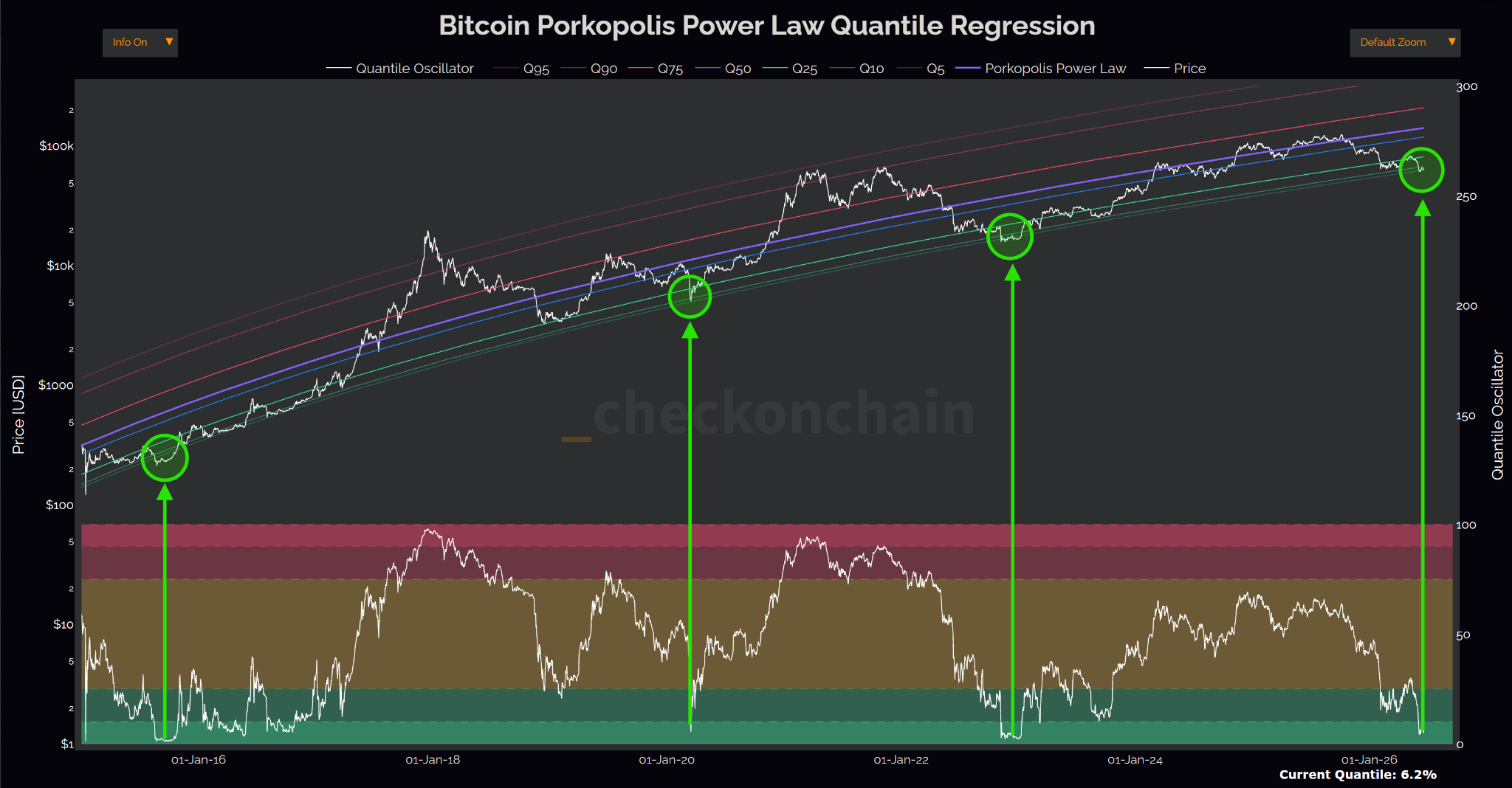

A second metric points in the same direction. Bitcoin’s power-law quantile has fallen to 6.2%, indicating the asset is cheaper than roughly 94% of its historical observations when measured against the power-law model. The chart highlights similar readings during the 2015, 2020, and 2023 cycle lows, with the current market now revisiting that historically rare valuation zone.

Bitcoin power-law quantile regression chart. Source: Checkonchain

Related: Bitcoin drops to $58K on high US PCE inflation as trader sees ‘manipulation’

Key BTC price levels to watch

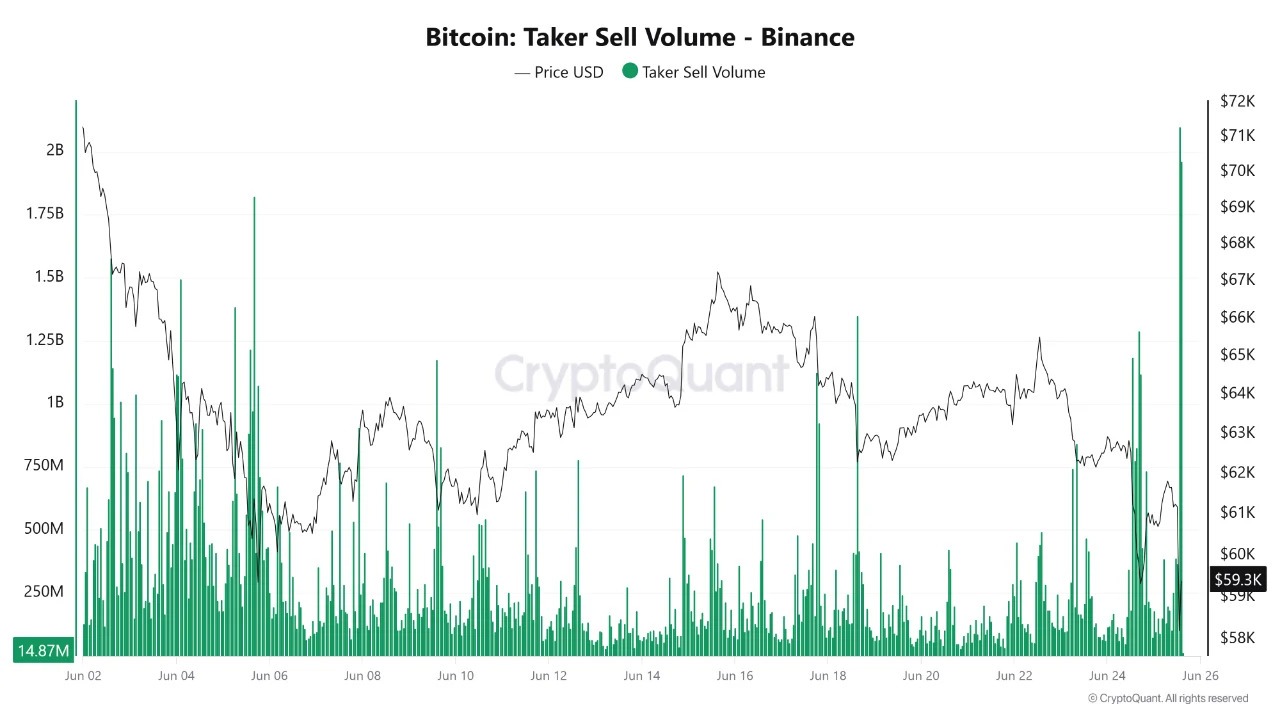

Bitcoin fell to a new yearly low of $58,000 after aggressive selling swept through Binance. The hourly taker sell volume reached $2.1 billion, followed by another $1.9 billion in the next hour after the New York market open, marking the exchange’s largest hourly sell pressure since May 4.

Bitcoin taker sell volume on Binance. Source: CryptoQuant

The flush liquidated more than $300 million in long BTC positions before the price rebounded toward $60,000. That level now carries added significance. A daily close back above $60,000 preserves the developing relative-strength index (RSI) bullish divergence across the one-hour, four-hour, and daily time frames which signals that selling momentum is fading even as the price prints lower lows.

BTC/USDT, one-day chart. Source: Cointelegraph/TradingView

Futures trader Byzantine General shared a similar outlook, saying the move to $58,000 cleared out leveraged longs while drawing in fresh short sellers. In his view, a daily close above $60,000 would strengthen the case that Bitcoin has printed a local bottom for now.

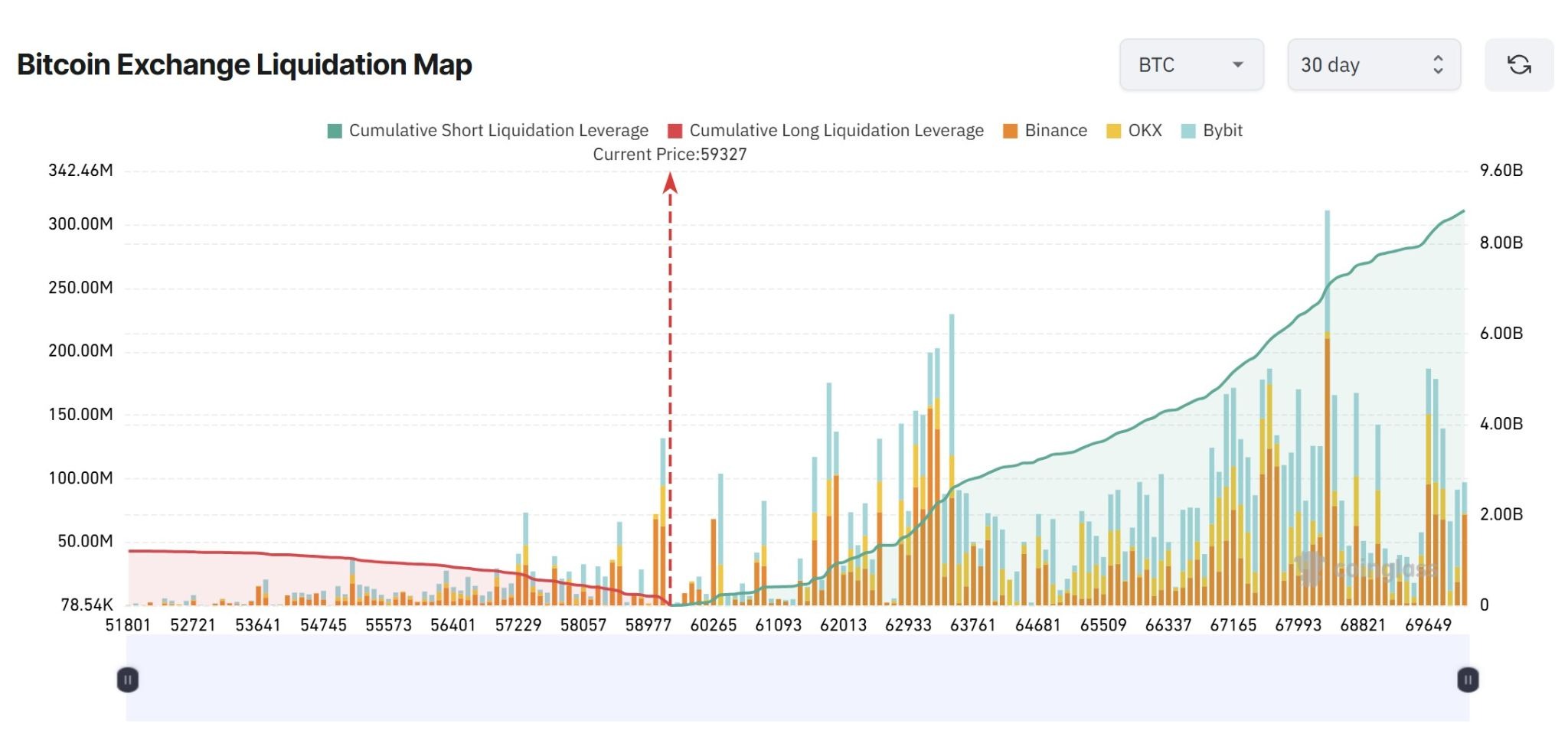

That would also shift attention toward a large pocket of upside liquidity. More than $4 billion in short liquidations cluster near $65,000, compared with about $1 billion below $55,000, creating a four-to-one imbalance. A relief rally could then target internal liquidity near $68,000, where a daily fair-value gap adds another area of interest for traders.

BTC liquidation map. Source: CoinGlass

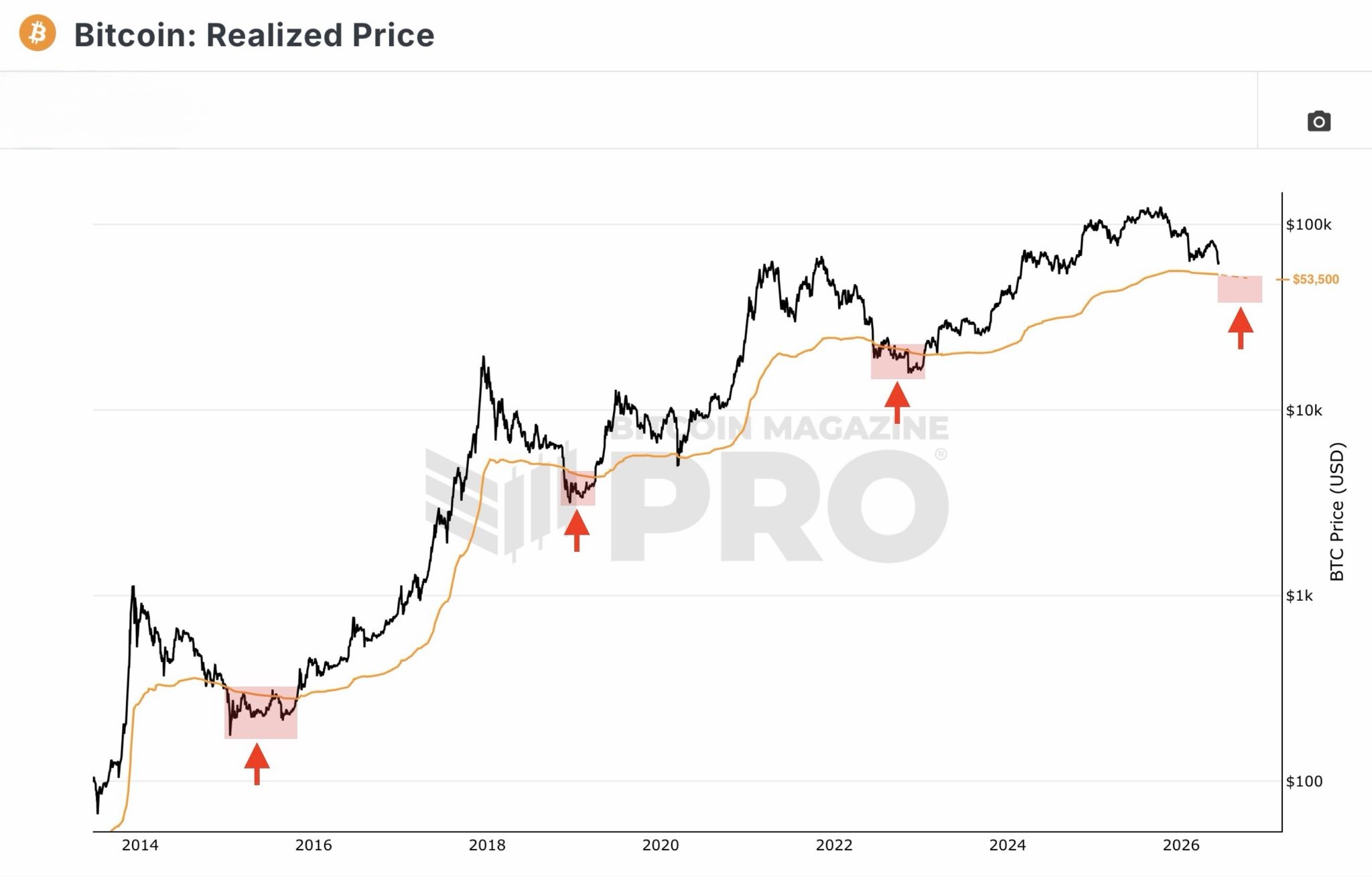

Meanwhile, a daily close below $60,000 reinforces the bearish bias on both the short-term and long-term charts. The next area of interest then shifts to $55,000, where Bitcoin’s September 2024 weekly range low converges with its realized price near $54,000.

The realized price, which tracks the average cost basis of all onchain coins, has historically provided support at every major Bitcoin bear-market bottom since 2014. That trend makes the $54,000-$55,000 region a key level for traders to watch if selling pressure continues.

Bitcoin’s realized price. Source: X

Related: Bitcoin drop to $58K brings out bears: Is BTC’s next stop below $50K?

Tether's USDT has drawn level with ether, narrowing the gap for the second-largest cryptocurrency by market capitalization to a fraction of a percent. The stablecoin briefly overtook ether earlier this month, the first time a dollar-pegged token has done so. USDT carried a market cap of about… Read the full story at The Defiant

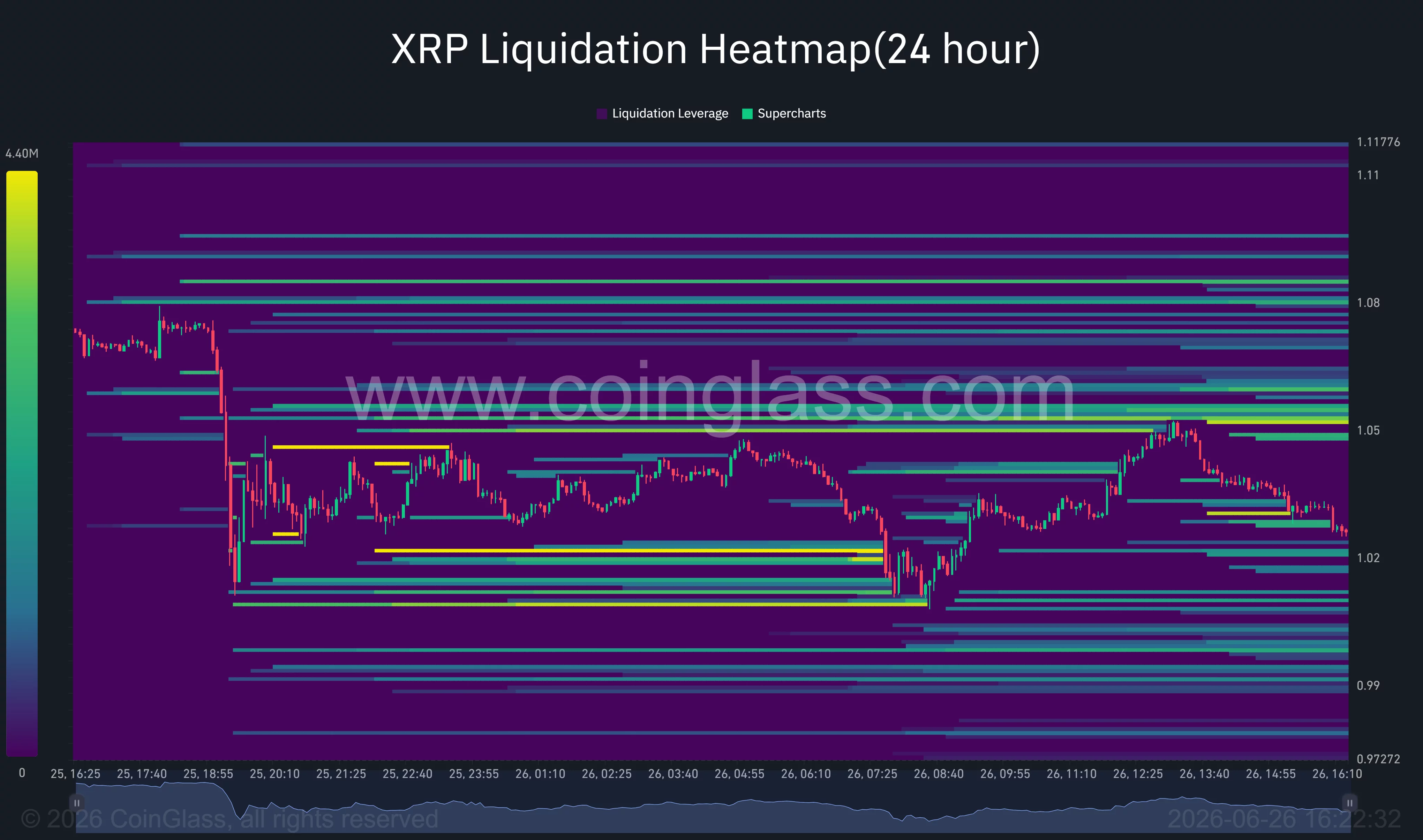

XRP has fallen to its lowest level in months after a sharp selloff driven by a major derivatives flush and fresh pressure across the crypto market, while technical charts now show the token testing the lower boundary of a long-term falling wedge.

Summary

- XRP has fallen toward the key $1 support after a $10.8 billion crypto options expiry triggered heavy market-wide selling.

- A multi-month falling wedge and oversold momentum indicators suggest the token is nearing a critical technical inflection point.

- Analysts warn a break below $1 could expose lower support zones, while reclaiming $1.10 would improve the bullish outlook.

According to data from crypto.news price, XRP (XRP) price dropped from around $1.07 on June 25 to $1.01 on June 26, extending its year-to-date decline to more than 40%. The decline accelerated as a $10.8 billion crypto options expiry triggered heavy volatility across digital assets and forced a wave of long liquidations.

At the same time, sentiment surrounding the XRP ecosystem weakened after decentralized finance protocol Strobe Finance abruptly announced it would shut down operations.

The selling pressure arrived as investors also reduced exposure to risk assets following stronger expectations that the U.S. Federal Reserve could keep interest rates higher for longer. Bitcoin’s slide below the $60,000 level removed another layer of support for altcoins, leaving XRP among the weaker large-cap tokens during Thursday’s session.

XRP approaches long-term support as liquidation clusters build overhead

The daily chart shows XRP trading at the lower edge of a falling wedge that has contained price action for almost a year. The pattern has compressed between descending resistance and gradually declining support, with the token now sitting close to the wedge’s lower boundary near $1.00.

Momentum indicators remain weak. The MACD has stayed below its signal line with histogram bars still in negative territory, while the Aroon indicator continues to favor sellers after Aroon Down climbed back toward 100 and Aroon Up remained subdued. Together, the indicators suggest bears still control the short-term trend even as XRP price approaches a historically important support zone.

The four-hour chart presents another important technical level. XRP has retraced almost the entire advance measured by the displayed Fibonacci range and now trades just above the 100% retracement near $1.01. Price also remains below the Supertrend resistance around $1.10, while the RSI has slipped to nearly 31, placing momentum close to oversold territory but without confirming a bullish reversal.

Derivatives positioning also highlights where volatility could increase next. CoinGlass liquidation heatmap data show large concentrations of leveraged positions clustered between roughly $1.05 and $1.08, while another sizable liquidity pocket sits around the $1.02 area. Those zones could attract price in either direction as traders compete for liquidity, increasing the likelihood of sharp short-term swings.

On-chain positioning has also drawn attention to nearby support. According to well-followed analyst Ali Martinez, UTXO Realized Price Distribution data identify $1.06 as a major accumulation level where more than 830 million XRP previously changed hands.

“XRP is testing a major volume block at $1.06…If the market drops below this level, the next core support targets are $0.80, $0.62 and $0.51.”

Bears retain control while lower demand zones come into focus

Several downside risks could still invalidate any recovery attempt. A sustained move below the wedge support around $1.00 would break one of XRP’s longest-running chart structures and could expose lower historical demand zones identified by both technical and on-chain data.

Commenting on the latest structure, crypto analyst ChartNerd noted that XRP has entered an area of interest after weeks of decline but warned that losing the current support would shift attention toward the $0.90-$0.70 range, where previous buying activity was concentrated.

$XRP has continued to decline into our area of interest since our last update two weeks ago. The deeper price retraces, the stronger the risk-reward setup becomes. If the new local $1.00 low is swept, the next major demand zone sits in the $0.90/$0.70 region. https://t.co/IzZZOIksTy pic.twitter.com/5K0KwKmTpr

— 🇬🇧 ChartNerd 📊 (@ChartNerdTA) June 26, 2026

Any recovery will also depend on conditions outside the XRP market. Additional institutional outflows from crypto investment products, another round of heavy derivatives liquidations, or stronger-than-expected U.S. economic data that reinforce expectations for restrictive Federal Reserve policy could extend pressure across digital assets.

Conversely, reclaiming the $1.10 region and breaking above the falling wedge resistance would be the first technical signal that buyers are regaining control.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

At least three Strategy officials published coordinated investor reassurances Friday morning, as bitcoin traded around $59,600 and the company's STRC preferred shares languished near record lows of $73-75. Executive Chairman Michael Saylor, bitcoin executive Chaitanya Jain and President and CEO… Read the full story at The Defiant

LA Thieves, FaZe, G2, OpTic advance to upper semis at CDL Major 4

Trump Administration Allows Anthropic to Release Mythos to Select US Organizations

Mahmood announces new refugee sponsorship route into UK

-

Entertainment6 days ago

Entertainment6 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports4 days ago

Sports4 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech5 days ago

Tech5 days agoMicrosoft accidentally kills epic Outlook email threads

-

Fashion14 hours ago

Fashion14 hours agoWeekend Open Thread: Staud – Corporette.com

-

Business6 days ago

Business6 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics1 day ago

Politics1 day agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics7 days ago

Politics7 days agoAndy Burnham and the meaning of Makerfield

-

Politics1 day ago

Politics1 day agoPotential 2028er World Cup attendee leaderboard

-

Business1 day ago

Business1 day agoAsia stock markets slide as tech shares slump

-

Tech2 days ago

Tech2 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World3 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World3 days ago

Crypto World3 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World2 days ago

Crypto World2 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Business3 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World7 days ago

Crypto World7 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Sports11 hours ago

Sports11 hours agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World3 hours ago

Crypto World3 hours agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Crypto World15 hours ago

Crypto World15 hours agoRTX holders must register wallets before token distribution begins

-

Crypto World18 hours ago

Crypto World18 hours agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World7 days ago

Crypto World7 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

You must be logged in to post a comment Login