Crypto World

What is a crypto trust bank? Charters, custody, and the Fed Master Account

A wave of crypto firms, from Ripple to Circle, have won national trust bank charters, and several are chasing a Federal Reserve master account. This guide explains what a crypto trust bank actually is, what a charter does and does not grant, and why the real prize sits at the central bank.

Summary

- A crypto trust bank is a chartered trust institution that custodies digital assets and manages stablecoin reserves, bringing crypto custody inside the regulated banking system without being a full retail bank.

- A national trust charter lets a crypto firm custody its own assets and reserves and obviate the patchwork of state money-transmitter licenses, but it cannot take ordinary deposits or carry federal deposit insurance.

- In 2025 and 2026, a wave of crypto firms, including Ripple, Circle, Paxos, Fidelity Digital Assets, and others, won conditional national trust charters.

- The bigger prize is a Federal Reserve master account, which would give direct access to the central bank’s payment rails and let a firm hold reserves at the Fed itself, something no crypto-native firm has yet achieved.

- Charters and master accounts primarily benefit stablecoins and custody businesses by deepening their regulatory standing, marking crypto’s convergence with traditional banking.

A crypto trust bank is a chartered financial institution, supervised like a bank, whose purpose is to custody assets and provide fiduciary services rather than to take deposits and make loans, and which a crypto firm uses to hold digital assets and manage stablecoin reserves inside the regulated banking system. That definition contains the key to understanding the whole subject: a trust bank is a real, regulated bank, but a specialized kind, built around safekeeping and trust services rather than the deposit-taking and lending that define ordinary retail banks.

In 2025 and 2026, a remarkable wave of crypto firms obtained or pursued these charters, transforming companies once seen as outside the financial system into federally supervised institutions, a shift that marks one of the clearest signs yet of crypto converging with traditional banking. This guide explains what a trust bank is, what a national trust charter actually grants a crypto firm and what it pointedly does not, why so many crypto companies suddenly wanted one, the even larger prize of a Federal Reserve master account, and what the whole development means for stablecoins, for the industry, and for users.

The reason this matters is that the relationship between crypto and the banking system has been one of the defining tensions of the industry’s history. For years, crypto firms depended on traditional banks to hold their customers’ money and connect them to the financial system, a dependence that became a serious vulnerability during periods of regulatory pressure and bank failures, when crypto companies found their accounts closed or their banking partners collapsing.

The move to obtain trust charters is, in large part, an effort to end that dependence by bringing crypto firms inside the regulated banking system on their own terms. This guide covers what a trust bank is, the powers and limits of a charter, the 2025-2026 wave of approvals, a worked example of how a charter changes a stablecoin issuer’s position, the central-bank master account that is the ultimate goal, what it all means for stablecoins, and the genuine limits and risks that the headlines often gloss over.

What a trust bank is

Start with the institution itself, because the word “bank” carries assumptions that a trust bank does not always meet. In traditional finance, a trust bank is a bank that specializes in custody and fiduciary services rather than in the deposit-taking and lending that most people associate with banking. Its core business is holding assets on behalf of clients, safeguarding them, and managing them in a fiduciary capacity, meaning with a legal duty to act in the client’s interest.

Trust banks have long existed to custody securities, manage estates and trusts, and provide safekeeping for institutions, and they are regulated as banks, but their activities are narrower and, in important ways, less risky than those of a full-service commercial bank, because they are not lending out customer money or running the maturity mismatches that make ordinary banking risky.

This specialization is exactly what makes the trust bank model attractive to crypto firms. A crypto company’s central regulated need is custody: safely holding digital assets and, for stablecoin issuers, holding and managing the reserve assets that back their tokens. A trust bank charter is purpose-built for precisely this kind of safekeeping and fiduciary activity, which is why crypto firms gravitated to it instead of to a full commercial banking charter that would saddle them with powers and obligations they neither need nor want.

By becoming a trust bank, a crypto firm gains the regulated standing and supervisory oversight of a banking institution while staying within the narrower scope of custody and trust services that match its actual business.

Understanding that a trust bank is a custody-and-fiduciary institution, not a deposit-and-lending one, is the foundation for understanding everything a crypto trust charter does and does not provide.

What a national trust charter grants, and what it does not

A national trust charter, granted in the United States by the federal regulator that oversees national banks, gives a crypto firm a specific and valuable set of capabilities, and it is important to be precise about both what it includes and what it excludes. On the positive side, the charter allows the firm to operate as a federally supervised trust bank, custodying digital assets and, under expanded rules, managing stablecoin reserves and providing certain payment-related services.

Crucially, it lets the firm custody its own assets and reserves directly, instead of depending on a third-party bank, and it can obviate the need for the patchwork of separate state money-transmitter licenses that crypto firms have historically had to collect state by state, replacing a fragmented compliance burden with a single federal charter. It also confers the legitimacy and oversight of a banking institution, which matters enormously to the institutional clients a crypto firm wants to serve.

The exclusions are just as important, and they are where headlines often mislead. A national trust charter does not make a crypto firm a full bank in the everyday sense. It does not permit the firm to take ordinary deposits, the way a retail bank accepts checking and savings accounts. It does not come with federal deposit insurance, the government protection that backs ordinary bank deposits up to a limit, because trust banks generally do not hold the kind of deposits that insurance covers.

And it does not authorize the firm to lend, to run the credit business at the heart of commercial banking. So when a crypto firm “becomes a bank” via a trust charter, it gains custody, reserve management, and regulated standing, but it does not gain the ability to take insured deposits or make loans. This distinction is not a quibble; it is central to understanding what these charters actually mean, because a customer who assumes a chartered crypto trust bank offers the same protections as an insured retail bank would be mistaken, and that misunderstanding could matter a great deal in a crisis.

Why crypto firms suddenly want them

The sudden rush of crypto firms toward trust charters in 2025 and 2026 was not coincidental, and understanding the motivations explains the strategic logic. The first and most fundamental driver is independence from third-party banks. For most of crypto’s history, firms relied on partner banks to hold customer funds, custody reserves, and connect to the financial system, and that dependence proved dangerous: during periods of regulatory pressure and amid a series of bank failures, crypto companies found their banking relationships severed or their partner banks collapsing, threatening their operations through no fault of their own. A trust charter lets a firm custody its own assets and reserves directly, removing that single point of failure and the strategic vulnerability it created.

The second driver is regulatory tailwind. A shift in the political and regulatory environment toward a more accommodating posture on crypto opened a path for these charters that had been effectively closed before, and the federal regulator approved a cluster of crypto firms in a coordinated wave, signaling a broader acceptance of crypto-native institutions in the banking system.

The third driver is the rise of stablecoin regulation: as comprehensive rules for stablecoins took shape, holding a trust charter aligned a firm with the likely requirements, particularly around the custody and management of reserves, positioning compliant issuers ahead of the curve. The fourth is simple competitive and reputational advantage: a federally chartered trust bank carries a legitimacy that a lightly regulated startup cannot match, and for firms courting banks, asset managers, and corporations as clients, that regulated standing is a powerful selling point.

Together, these drivers, independence, regulatory opening, stablecoin alignment, and legitimacy, explain why a long list of major crypto firms pursued charters at once, turning what had been a fringe idea into an industry-wide movement.

A worked example: a stablecoin issuer with and without a charter

To see why a charter matters in practice, compare a stablecoin issuer’s position before and after obtaining one, because the contrast makes the abstract benefits concrete.

Without a charter, a stablecoin issuer must rely on third-party banks to hold the reserve assets that back its tokens, the cash and short-term government securities that give the stablecoin its value. This dependence creates several vulnerabilities. The issuer is exposed to the health of its partner banks, so if one of them fails or freezes the account, the reserves and the stablecoin itself are jeopardized, a danger that became vividly real when a stablecoin temporarily lost its peg after a bank holding part of its reserves collapsed. The issuer must also navigate a patchwork of state-by-state money-transmitter licenses, a costly and fragmented compliance burden, and it lacks the regulated standing that would reassure cautious institutional users.

With a national trust charter, the same issuer’s position is transformed. It can custody its own reserve assets directly through its chartered trust bank, under federal supervision, removing the dependence on potentially fragile third-party banks. In some cases the firm gains oversight at both the federal and state level, a dual-supervision structure that few stablecoin issuers can match and that serves as a strong signal of credibility to institutions evaluating whether to trust the stablecoin.

The single federal charter can replace much of the state-by-state licensing burden, simplifying compliance. And the regulated standing of a trust bank reassures the banks, asset managers, and corporations the issuer wants as customers, lowering the barrier to adoption. The worked comparison shows the charter’s real value clearly: it converts a stablecoin issuer from a firm dependent on outside banks and a fragmented license patchwork into a federally supervised institution that controls its own reserves and carries banking-grade legitimacy. That transformation is precisely why stablecoin issuers were among the most eager pursuers of these charters.

The real prize: a Federal Reserve master account

As valuable as a trust charter is, it is a stepping stone to something larger, and the ultimate goal for the most ambitious crypto firms is a Federal Reserve master account. A master account is the account a financial institution holds directly with the central bank, and it represents the deepest possible integration into the financial system. It grants direct access to the central bank’s payment rails, the core networks through which money moves between institutions, and access to base money held at the central bank itself, instead of balances held at a commercial bank. For most of the financial system, this kind of direct central-bank access is reserved for traditional banks, and obtaining it is the difference between operating at the edge of the system and operating at its core.

For a crypto firm, particularly a stablecoin issuer, the appeal of a master account is profound. It would allow the firm to hold the reserves backing its stablecoin directly at the central bank, the safest possible place to keep them, eliminating the counterparty risk of relying on commercial banks and giving institutions unparalleled confidence in the stablecoin’s solvency and the safety of its redemptions. It would also allow direct settlement through the central bank’s payment systems, a powerful capability for a payments-focused firm.

The obstacle is that the bar is extraordinarily high, and no crypto-native firm has yet been granted a master account. The central bank has historically been cautious about extending this access to non-traditional institutions, uninsured trust banks face the most stringent review, and previous attempts by crypto-adjacent firms to win access have been denied. Several chartered crypto firms have applied and are waiting, with no guaranteed outcome and no clear timeline. The master account is the real prize precisely because it is so hard to win and so transformative if won, marking the moment a crypto-native firm would plug directly into the heart of the financial system.

What it means for stablecoins and the industry

Stepping back, the trust-charter wave is, more than anything, a stablecoin story, and seeing why clarifies the whole development. The firms most eager for charters were heavily those with stablecoin businesses, because the charter speaks directly to a stablecoin issuer’s central regulated needs: custodying and managing the reserve assets that back the token, doing so under credible supervision, and removing the dependence on third-party banks that has repeatedly threatened stablecoins in the past.

As comprehensive stablecoin regulation took shape, a trust charter became close to a prerequisite for operating a serious, institutionally trusted stablecoin in the United States, and the firms that obtained charters positioned their stablecoins as the most credible and best-supervised in the market. The dual oversight some of them gained, federal and state, became a competitive selling point, a way to signal to institutions that the stablecoin’s reserves are held to banking-grade standards.

The broader significance is the convergence of crypto and traditional banking. The trust-charter wave marks the moment when crypto firms stopped operating outside the regulated banking system and began entering it as supervised institutions, accepting the obligations of banking regulation in exchange for its legitimacy and stability. This is a profound shift from crypto’s early ethos of operating apart from, and often in opposition to, the traditional financial system. It signals a maturing industry in which the leading firms seek the same regulated standing as banks, and in which the line between a crypto company and a financial institution blurs. For the industry, this convergence brings legitimacy, stability, and access, the ability to custody assets safely, serve institutional clients, and integrate with the financial system.

It also brings the constraints of regulation, the compliance burdens, capital requirements, and supervision that come with a banking charter. The trust-charter wave is, in essence, crypto’s leading firms choosing to join the financial system instead of replacing it, which is one of the most consequential shifts in the industry’s trajectory.

Risks and limits to understand

For all the significance of the trust-charter movement, several risks and limits deserve clear attention, because the headlines tend to overstate what these charters mean. The most important point for any user is the one already emphasized: a crypto trust bank is not a full, insured retail bank. It does not carry federal deposit insurance, so assets held with a chartered crypto trust bank do not enjoy the government protection that backs ordinary bank deposits up to a limit.

A customer who assumes a “crypto bank” offers the same safety net as an insured retail bank is mistaken, and in a failure scenario, that misunderstanding could be costly. The charter brings supervision and legitimacy, which are real, but it does not transform custody into an insured deposit, and that distinction must not be lost.

Other limits and risks are substantial. The Federal Reserve master account that many firms seek remains unattained by any crypto-native firm and is far from assured, so the deepest integration into the financial system, and the reserve-safety benefits that come with it, are still aspirational instead of achieved. The charters themselves are often conditional, meaning the firms must still satisfy capital, governance, and risk-management standards before operating fully, and conditional approval is not the same as a fully operational bank.

Traditional banking groups have opposed extending charters and central-bank access to crypto firms, citing systemic-risk concerns, and that opposition could shape how far the privileges extend. There is also regulatory and political risk: the accommodating posture that opened the path to these charters could shift, and supervisory expectations could tighten. And the convergence itself carries a subtler risk, that bringing crypto firms inside the banking system concentrates new kinds of risk within the regulated perimeter in ways regulators are still learning to assess.

None of this negates the genuine progress the charters represent, but anyone evaluating a chartered crypto trust bank, whether as a user, an investor, or an observer, should hold a clear view of what the charter does and does not provide, treat the master account as a hope instead of a fact, and never mistake banking-grade supervision for deposit insurance.

Frequently Asked Questions

What is a crypto trust bank in simple terms?

A crypto trust bank is a chartered, bank-supervised institution built around custody and fiduciary services instead of deposits and lending, which a crypto firm uses to hold digital assets and manage stablecoin reserves inside the regulated banking system. It is a real, regulated bank, but a specialized kind: its job is safekeeping and trust services, not taking checking accounts or making loans. Crypto firms pursue this model because their central regulated need is custody, and a trust charter is purpose-built for exactly that, giving them banking-grade standing without the powers and obligations of a full commercial bank.

What does a national trust charter let a crypto firm do?

It lets the firm operate as a federally supervised trust bank, custodying digital assets and, under expanded rules, managing stablecoin reserves and providing certain payment-related services. Crucially, it lets the firm custody its own assets and reserves directly instead of depending on third-party banks, and it can replace the patchwork of state money-transmitter licenses with a single federal charter. It also confers the legitimacy and oversight of a banking institution. What it does not grant is the ability to take ordinary insured deposits or to make loans, so it is not a full retail bank.

Does a crypto trust bank have deposit insurance?

No, and this is one of the most important things to understand. National trust charters generally do not come with federal deposit insurance, the government protection that backs ordinary bank deposits up to a limit, because trust banks do not hold the kind of deposits that insurance covers. So assets held with a chartered crypto trust bank do not enjoy the safety net that an insured retail bank provides. A customer who assumes a “crypto bank” offers the same protection as an insured bank is mistaken, and that distinction could matter greatly in a failure. The charter brings supervision and legitimacy, not deposit insurance.

Why did so many crypto firms get charters in 2025 and 2026?

Several reasons converged. The biggest was independence from third-party banks, since crypto firms had repeatedly been hurt when partner banks closed their accounts or failed, and a charter lets a firm custody its own assets directly. A more accommodating regulatory environment opened a path that had been effectively closed, and the regulator approved a cluster of firms together. The rise of comprehensive stablecoin regulation made a charter close to a prerequisite for a serious stablecoin. And the legitimacy of a federal charter is a powerful selling point to institutional clients. Together these drove an industry-wide rush.

What is a Federal Reserve master account and why does it matter?

A master account is an account held directly with the central bank, granting direct access to its payment rails and to base money held at the central bank itself, instead of balances at a commercial bank. For a stablecoin issuer, it would allow holding reserves directly at the central bank, the safest possible place, eliminating commercial-bank counterparty risk and giving institutions strong confidence in the stablecoin’s safety. It is the real prize because it represents the deepest integration into the financial system, but the bar is extremely high, no crypto-native firm has yet been granted one, and applications remain pending with uncertain outcomes.

What does the trust-charter wave mean for the crypto industry?

It marks the convergence of crypto and traditional banking. The leading crypto firms are choosing to enter the regulated banking system as supervised institutions, accepting banking regulation in exchange for its legitimacy, stability, and access, a profound shift from crypto’s early ethos of operating apart from the traditional system. It is largely a stablecoin story, since charters speak directly to issuers’ need to custody reserves credibly. The convergence brings legitimacy and integration but also the constraints of regulation, and it signals a maturing industry whose leading firms increasingly resemble, and seek to operate alongside, traditional financial institutions.

This article is educational information, not legal, financial, or investment advice. Charter approvals, master account decisions, and regulations are evolving, and details reflect reporting available as of June 26, 2026, which can change quickly. Crucially, a chartered crypto trust bank is generally not covered by federal deposit insurance. Verify current information from primary sources before relying on anything described here.

A survey arranged by digital asset services provider CoinShares found that more than half of UK-based financial advisers reported the bulk of their clients’ crypto holdings were outside their oversight.

According to the results of a CoinShares survey released on Thursday, 52% of UK advisers in a group of 261 European wealth management professionals said that the majority of their clients’ digital assets exposure was essentially “invisible” to them. Among all the EU countries surveyed, including France, Germany, Italy and Switzerland, the number was 25%, with 61% of advisers saying that they worked in companies that explicitly restricted digital assets or provided no clear internal guidance.

“The capital has already been allocated,” said CoinShares co-founder and CEO Jean-Marie Mognetti. “The people entrusted with managing it simply cannot see it, and in most cases not because clients are unwilling to engage, but because firm policy prevents them from doing so. This is not a knowledge problem. It is not a demand problem. It is a firm-policy problem becoming a wrong-way risk.”

He added:

“[…] Visibility comes before advice. You cannot allocate, manage risk or earn trust over assets you cannot see.”

Source: CoinShares

The UK’s Financial Conduct Authority (FCA), the watchdog overseeing digital asset regulation, reported in December that about 8% of the country’s adults were invested in crypto. The group recently proposed allowing authorized investment funds to hold up to a 10% allocation of cryptocurrency exchange-traded notes.

Related: Bank of England eases stablecoin rules, introduces 40B pound issuance cap

Potential new leadership to shake up UK crypto policy?

UK Prime Minister Keir Starmer resigned as Labour leader on Monday amid pressure from many in his own party, opening the door to a recently elected member of parliament to take the reins.

In a recent by-election, former Mayor of Greater Manchester Andy Burnham won a seat as a member of parliament representing Makerfield, positioning him to be heavily favored by many in Labour to replace Starmer. While it’s unclear how Burnham may handle crypto policy on a national stage, as mayor, he supported the blockchain industry as a driver for economic development.

Magazine: AI is banking the unbanked in Africa… faster than crypto

The European Parliament’s economic affairs committee has urged the European Commission to assess whether crypto lending and borrowing, staking, non-fungible tokens (NFTs) and decentralized finance (DeFi) should be regulated.

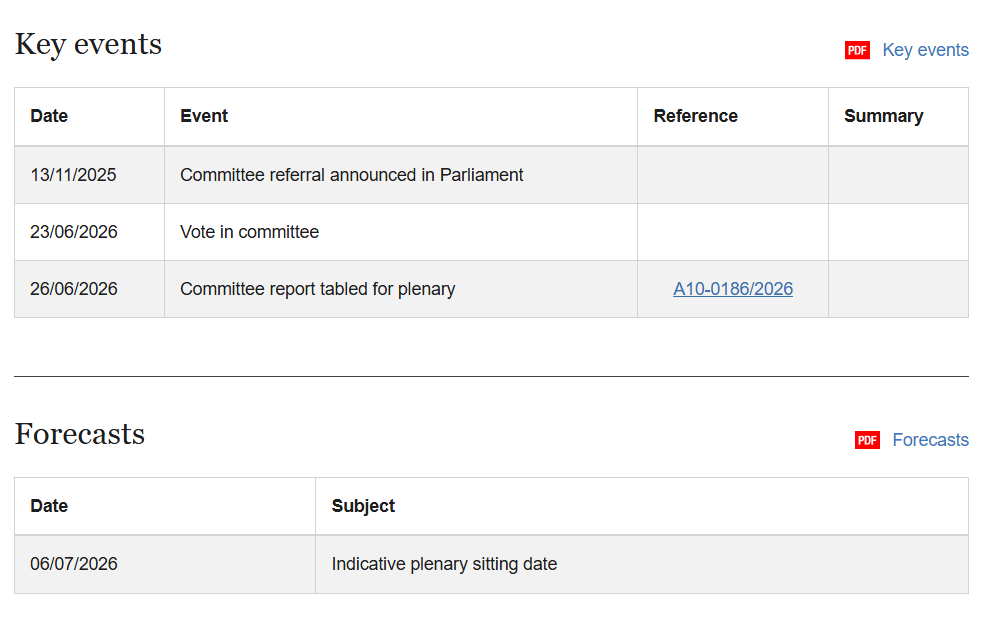

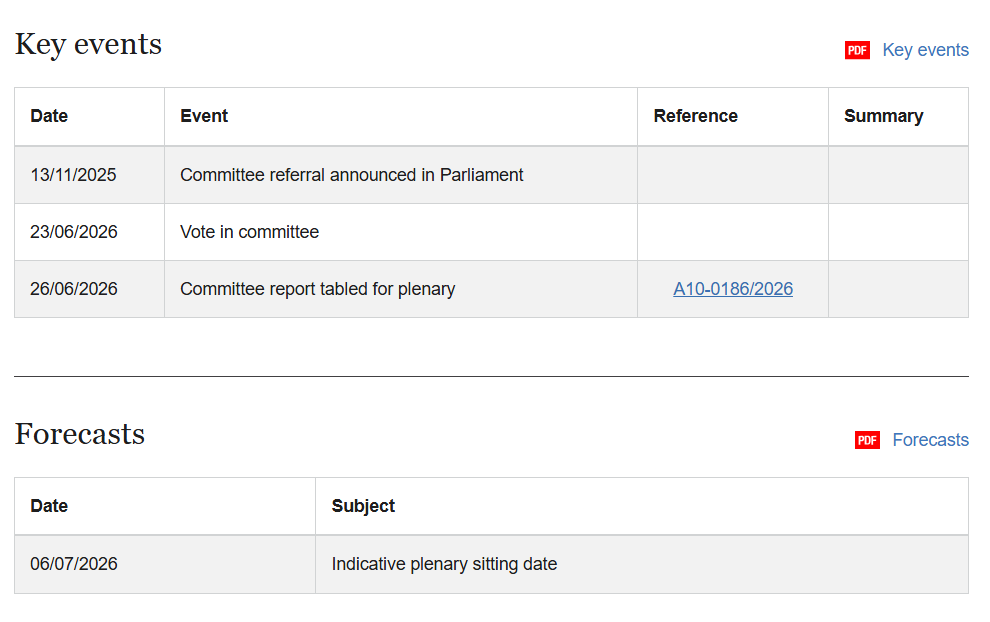

The recommendations were part of a report tabled Friday for plenary vote. It also called for promoting tokenization across financial services, encouraging euro-denominated stablecoins and assessing whether additional crypto activities should be regulated under the European Union’s Markets in Crypto-Assets Regulation (MiCA).

Drafted by Belgian Member of the European Parliament Johan Van Overtveldt, the report is an own-initiative resolution by the Committee on Economic and Monetary Affairs (ECON) that outlines recommendations for the Commission on digital asset regulation.

It will next go before the European Parliament for a vote, expected July 7. If adopted, the resolution would become Parliament’s official position on digital assets policy but would not amend MiCA or create new legal obligations.

The legislative timeline shows the committee’s approval of the report and its referral for a plenary vote. Source: European Parliament

Related: European Parliament throws support behind digital euro

EU warms up to regulated stablecoins

The recommendations also reflect an evolving view of stablecoins among policymakers. Days after former Bank for International Settlements general manager and longtime crypto critic Agustín Carstens softened his stance on stablecoins, the report welcomed euro-denominated stablecoins under MiCA and encouraged their development to support the bloc’s payment sector.

In 2023, Van Overtveldt called for tighter restrictions on cryptocurrencies following the banking turmoil surrounding Silicon Valley Bank, Signature Bank and Silvergate Bank. The crisis was also closely tied to stablecoins, as USDC issuer Circle held roughly $3.3 billion of its reserves at Silicon Valley Bank when it collapsed, briefly causing USDC to lose its dollar peg.

Van Overtveldt likened cryptocurrencies to drugs during the 2023 banking crisis. Source:Johan Van Overtveldt

The report argued that euro-denominated stablecoins could complement tokenized commercial bank deposits and wholesale central bank digital currencies while enabling faster and cheaper cross-border payments. It also said broader adoption could strengthen the competitiveness of EU financial markets and the international role of the euro.

The stance also aligns with ECON’s broader vision for Europe’s digital money ecosystem. On Tuesday, the committee backed legislation for a digital euro, with lawmakers arguing that public and private forms of digital money should coexist rather than compete.

Related: Poland president vetoes MiCA bill again as crypto companies look to license abroad

Lawmakers look beyond MiCA’s current scope

Van Overtveldt first presented a draft of the report in February before months of negotiations and amendments by ECON members. The earlier version largely focused on MiCA’s existing framework, including stablecoin classifications and legal certainty for multi-issued stablecoins.

The committee-approved report urged consistent application of MiCA across the EU to preserve a level playing field for crypto firms. It also warned member states against introducing national requirements beyond MiCA that could fragment the bloc’s digital asset industry.

The Commission is already reviewing MiCA. In May, the Commission launched a public consultation seeking feedback on whether the framework should be expanded to cover areas including DeFi, staking, lending, NFTs and tokenized financial assets, while also reopening debate over the regulation’s ban on interest-bearing stablecoins.

Meanwhile, MiCA’s transitional period ends July 1, after which crypto asset service providers generally must hold authorization under the regulation to continue operating across the EU.

Magazine: AI is banking the unbanked in Africa… faster than crypto

Polymarket says a third-party vendor compromise discovered on Thursday enabled attackers to inject malicious code into its website interface, leading to a phishing campaign that targeted multiple users. According to blockchain analyst Specter, the injected script was used to drain an estimated $2.94 million from at least 11 Polymarket wallets.

Polymarket stated that the incident has been contained and that the compromised dependency has been removed. The platform also said affected users will receive full refunds. Cointelegraph contacted Polymarket for comment but did not receive a response before publication.

Key takeaways

- Polymarket reported a third-party vendor compromise that allowed attackers to inject a malicious script into its frontend.

- Analyst Specter linked the malicious code to phishing activity, estimating losses of about $2.94 million across at least 11 user wallets.

- Polymarket said the issue has been contained, a dependency has been removed, and users will be fully refunded.

- Blockchain security reporting data indicates the incident fits within a high volume of crypto breaches in the quarter.

- Separately, DefiLlama data shows private key compromise remains the dominant cause of reported exploit losses over the last 30 days.

Frontend compromise and phishing-driven wallet losses

The Polymarket incident centers on a supply-chain style failure rather than a direct smart contract exploit. Specter said the malicious script appeared to enable a phishing attack that redirected or induced users into compromising credentials or authorizations, culminating in unauthorized asset movement from user wallets.

In practice, this type of front-end compromise can be especially damaging for institutions and compliance teams because it shifts the risk profile away from on-chain mechanics alone. Even where contracts are unchanged, malicious web-layer code can manipulate user behavior, compromise session-related security assumptions, or trick users into signing harmful transactions. For regulated entities that integrate with or route user access to crypto services, incidents like this highlight the need for tighter vendor governance and continuous integrity controls over externally served dependencies.

Polymarket’s response suggests the affected component was identified and removed after discovery. Its commitment to fully refund users also raises operational and policy considerations: while refunds may mitigate user harm, they do not automatically address whether the underlying controls—such as third-party software update processes, dependency monitoring, and incident response playbooks—were sufficient to prevent reoccurrence.

DefiLlama breach reporting underscores a pattern of recurring exploit methods

The Polymarket case arrives as crypto security incident reporting remains elevated. DefiLlama data places the event within a broader timeline: the third quarter’s second quarter-to-date statistics indicate the quarter had its most-hacked period by incident count, according to Cointelegraph’s reference to DefiLlama and its reporting on Q2.

DefiLlama also reports that June saw reported crypto exploit losses of $74.9 million across 29 incidents, exceeding May’s $60.5 million total but remaining well below April’s $644 million peak.

Among the largest June incidents were a $36 million Humanity Protocol exploit, a $4.7 million Secret Network bridge exploit, two separate Aztec exploits valued at $2.1 million each, and a $1.7 million bridge exploit tied to Taiko. While each exploit involves different technical pathways, they collectively reinforce a key compliance reality: incident frequency and magnitude continue to stress operational risk management across exchanges, wallets, and service providers with protocol-level exposure.

DefiLlama’s breakdown of losses over the past 30 days points to private key compromise as the most common leading vector, accounting for 43% of reported exploit losses. Fake proof exploits made up 10%, and reverse MEV honeypots accounted for 8%. For risk teams, these categories matter because they indicate whether controls should prioritize key management, signature/authorization integrity, or transaction routing safeguards for automated systems and integrators.

Private key history at Polymarket highlights multiple threat surfaces

About a month before the reported Polymarket frontend incident, the prediction market disclosed an additional exploit traced to a six-year-old private key used for internal top-up operations. Cointelegraph previously reported that Polymarket said contracts and user funds remained safe in that earlier case and that all permissions associated with the compromised key were revoked.

Taken together, the two events underscore that Polymarket—or any crypto service with on-chain and off-chain touchpoints—can face multiple, distinct threat surfaces: backend key management for operational processes, and web-delivered dependencies for user-facing interactions. For institutional stakeholders, the combination can complicate assurance: even when one control area is remediated (for example, permissions revoked after a key issue), a separate control plane—like third-party dependency integrity—can still introduce new risk.

Polymarket’s scale also implies higher stakes for incident governance. DefiLlama reports that the platform holds more than $450 million in total value locked, up from $112 million a year ago.

Regulatory and compliance implications for crypto firms and integrators

Although Polymarket operates in a market with evolving regulation, incidents of this nature feed directly into compliance expectations for crypto businesses. Under frameworks such as the EU’s Markets in Crypto-Assets regulation (MiCA), firms are expected to meet governance and operational resilience obligations, while AML/CFT requirements under applicable regimes typically extend to “know your customer” processes and the protection of user funds. Supply-chain compromise and phishing-driven theft also raise questions for regulated counterparties about how customer asset protection claims are substantiated in practice.

For exchanges, wallet providers, payment processors, and institutional service providers, vendor-linked incidents may trigger additional internal review under third-party risk management policies. Common areas include: the lifecycle management of dependencies, auditability of frontend build and deployment pipelines, incident detection and containment procedures, and the adequacy of refund or restitution policies. Even if the theft originates outside on-chain code, user harms can still translate into regulatory scrutiny about consumer protection, disclosures, and operational risk controls.

Cross-border differences in enforcement priorities can further complicate response. In the United States, where crypto enforcement actions have frequently addressed security, consumer protection, and alleged failures in compliance controls, and where federal agencies coordinate through legal processes and subpoenas, a frontend-driven phishing incident can still be framed as a failure to maintain reasonable safeguards. Separately, AML/KYC obligations do not prevent phishing, but they can affect how stolen funds are identified, how affected users are supported, and how suspicious activity is triaged.

For institutional compliance monitoring, the most actionable element is the incident pattern itself: third-party compromise leading to user deception, alongside persistent exploit vectors such as key compromise. These themes suggest that governance should cover both technical controls (key management, permissioning, transaction integrity) and administrative controls (vendor oversight, software supply-chain assurance, and documented response measures).

Closing perspective

Polymarket says the compromised dependency has been removed and that affected users will be refunded. The next phase will likely involve detailed post-incident validation of the compromised supply chain, verification of residual exposure across its frontend delivery stack, and continued alignment of technical controls with the compliance expectations institutions apply to customer protection and operational resilience. Security incident reporting will remain a key reference point for assessing whether this case reflects a broader systemic risk pattern or an isolated vendor failure.

Binance’s competitive advantages are facing a hard new test. Europe’s sweeping new crypto rulebook reopens an old question: how much of its dominance is due to scale, and how much to a regulatory gap.

The pressure is immediate. The European Union (EU) is forcing Binance out of the bloc under new Markets in Crypto-Assets (MiCA) rules. Days earlier, OKX chief executive Star Xu split its success into four parts, arguing each leans on those gaps.

Binance Has Four Competitive Advantages

Analysts and rivals credit Binance’s dominance to four pillars, a breakdown Xu recently detailed. Each is a real strength. Each also now faces a harder test.

Regulatory Arbitrage

Binance scaled quickly by operating across many markets, often ahead of local licensing requirements. That kept costs low. US prosecutors later found that it had never filed a suspicious activity report and let US users trade more than $898 million with sanctioned Iran.

It settled for $4.3 billion in 2023, the year founder Changpeng Zhao pleaded guilty and resigned.

Since then, it has chased licenses and, when pushed, left markets instead, exiting Canada, the Netherlands, and an earlier German application.

A Market-Leading Listings Engine

Binance turns attention into volume better than any rival. It took 39.2% of the top exchanges’ spot trading in 2025, almost five times the share of its nearest competitor, according to CoinGecko.

By its own count, it processed $34 trillion in total product volume across the year. Its Launchpad and constant listings keep traders chasing the next token, though critics warn the sharpest hype cycles leave retail holding the losses.

Unmatched Distribution

Binance counted more than 300 million registered users by the end of 2025, the company reported. A network of affiliates, volunteer Angels, and media partners stretches that reach further.

Supporters call it strong community building. Critics call it narrative management when bad news lands.

Heavy Compliance Investment

Binance’s compliance spending has topped $200 million a year, up from $158 million two years earlier, chief executive Richard Teng told Bloomberg. It fielded about 63,000 law enforcement requests in 2024, up from 58,000.

Yet US prosecutors still imposed a three-year independent monitor in 2023, and critics, Xu among them, say the controls long trailed the marketing.

“Let’s see how Binance plays the regulatory arbitrage game again…Regulators are ultimately evaluating outcomes, not organizational charts,” Xu said, with his own exchange competing directly with Binance.

Follow us on X to get the latest news as it happens

Why the Moat May Still Hold

Binance’s scale is hard to dispute. It pushed $7.3 trillion in spot trades in 2025, far ahead of the field. It also held the top rank through the upheaval that followed CZ’s exit and Teng’s arrival.

Binance says its proof-of-reserves system now backs about $163 billion in user assets.

That base reaches across Asia, the Middle East, and Latin America, well beyond Europe.

Even so, the EU squeeze is real. Binance is winding down EU services next week, and it withdrew its Greek bid days ago.

“Binance is not leaving Europe,” Gillian Lynch, its Head of Europe and UK, told Reuters.

Rivals are circling. Kraken cleared Ireland and Coinbase chose Luxembourg, ready to absorb users Binance sheds.

Analyst Paul Barron is less alarmed, calling the deadline a priced-in consolidation that mostly clears dormant platforms.

The open question is how much of Binance’s lead is scale and how much is a regulatory gap. Cleaner rules should start to answer it.

The post How MiCA is Testing Binance’s Four Competitive Advantages appeared first on BeInCrypto.

Dogecoin and Hyperliquid’s HYPE led the week’s losses across crypto, falling near 10%, as money kept flowing toward stocks tied to the artificial-intelligence boom and away from major tokens.

Dogecoin slid 9.6% over seven days to about $0.076 and HYPE lost 9.9%, the steepest falls among the majors. Ether dropped 8.4% to about $1,581 and XRP fell 7.8% to $1.06, while solana and tron held up better, roughly flat on the week at $72 and $0.32.

Bitcoin was the steadier major, down 5.3% to around $60,345 on Saturday after dipping to about $58,800 on Friday and recovering, per CoinDesk data.

“Bitcoin approached $58K at its lows late Thursday and early Friday, but in both cases, aggressive buying quickly pushed it back into the $60K range,” Alex Kuptsikevich, FxPro chief market analyst, told CoinDesk. “This pattern resembles margin position liquidations during downtrend spikes, followed by strong buying on pending orders during the recovery.”

“Given deteriorating sentiment among institutional investors and their ability to quickly divest from cryptocurrencies to stabilise their balance sheets, it is worth preparing for continued pressure and periodic sell-off spikes by leveraged traders,” he added.

Ripple CEO Brad Garlinghouse said he remains bullish on bitcoin but that Michael Saylor’s approach to funding bitcoin purchases has damaged the broader crypto market, in a CNBC interview on Friday, as the preferred stock at the center of Strategy’s model fell to a record low.

“Financial engineering does not drive long-term value,” Garlinghouse said, arguing that the lasting value of any digital asset comes from its usefulness. “Team Michael Saylor wasn’t focused on the right stuff and that has hurt the overall market.”

He separated that from his view on the asset itself, saying he is still bullish on bitcoin.

Garlinghouse’s target was the machine Strategy has used to accumulate bitcoin. For about a year, the company has issued preferred shares, a class of stock that pays a fixed dividend, to raise cash for more bitcoin.

Its STRC share carries an 11.5% annual dividend and is engineered to trade near $100. Garlinghouse pointed to STRC trading about 25% below that level as a “damning indictment” of the strategy.

Bitcoin’s price volatility around and just under $60,000 continued at the end of the business week, but the asset has managed to climb above this level as of Saturday morning.

Most larger-cap alts are slightly in the green, with XRP trading above $1.05 and ETH standing close to $1,600. SOL has risen the most from this cohort.

BTC Fights for $60K

The business week began on the right foot for the primary cryptocurrency as the asset rebounded from the weekend slump to $62,500 and tapped $65,500 on Monday. However, that was a short-lived attempt for a more profound recovery as the bears were quick to intervene and halt all the progress.

In the following hours, the asset fell to $62,000. It bounced to $63,000, but the next leg down was even more painful. Bitcoin broke below $60,000 for the second time this month and tapped $59,000. After another dead-cat bounce to almost $62,000, the asset plunged even harder on Thursday, dumping to $58,000 for the first time since late 2024.

The latest leg down was strongly related to the adverse price moves observed from Strategy’s MSTR, which also marked a multi-year low of under $80. Nevertheless, BTC has managed to recover some ground from the aforementioned low and now stands at just over $60,000 despite the new attacks in the Middle East.

Its market capitalization has risen to $1.210 trillion on CG, while its dominance over the alts remains under 56%.

SOL, AAVE Pump

Ethereum continues to climb gradually after the recent low of $1,510 and now trades close to $1,600 following a minor daily increase. XRP has reclaimed the $1.05 support after a 2% jump since yesterday. Solana’s SOL has gained the most from the larger-cap alts today and sits above $72.

Even more impressive gains come from AAVE, AVAX, and MORPHO. Aave’s token has risen by double digits and sits above $95, while AVAX is north of $6.6. MORPHO has neared $1.80 following a 7% jump.

In contrast, MemeCore continues to drop, losing another 20% of value and struggling below $0.70 as of now.

The total crypto market cap has recovered over $80 billion since the Thursday low and is up to $2.170 trillion.

The post Solana (SOL) Rebounds Above $70, Bitcoin (BTC) Fights for $60K: Weekend Watch appeared first on CryptoPotato.

Prediction-market operator Kalshi is in talks to raise fresh capital at a valuation of roughly $40 billion, according to the Financial Times, nearly double the price tag from a round that closed just seven weeks ago. The Financial Times first reported the talks, citing people familiar with the… Read the full story at The Defiant

Securitize has secured commitments expected to deliver about $400 million ahead of its planned New York Stock Exchange debut through a merger with Cantor Equity Partners II.

Summary

- Securitize expects to raise about $400 million ahead of its planned NYSE listing through a merger with Cantor Equity Partners II.

- Backed by BlackRock, Morgan Stanley, Coinbase, and Circle, the firm continues expanding its tokenization business with new institutional products.

- The market debut comes as Securitize grows its on-chain asset platform while defending itself in a patent dispute with tZERO.

According to Securitize, fewer than 30% of shareholders in Cantor Equity Partners II, the special purpose acquisition company taking the firm public, chose to redeem their shares following the final redemption results.

The company said it now expects to receive approximately $400 million in gross proceeds from the transaction, including related private investment in public equity (PIPE) financing, before transaction-related expenses.

The proposed listing comes as tokenization companies continue attracting institutional attention, with firms seeking to bring traditional financial assets onto blockchain networks. Securitize counts BlackRock, Morgan Stanley, Coinbase, and Circle among its backers and has become one of the largest providers of tokenization infrastructure for financial institutions.

The merger is expected to complete next week

Market reaction has been positive ahead of the vote. Shares of Cantor Equity Partners II closed 7% higher at $10.86 on Friday before extending gains in after-hours trading to $11.

According to Securitize, shareholders are scheduled to vote on the merger on Monday. If approved and all remaining closing conditions are satisfied, the transaction is expected to close on July 1. The combined company is then expected to begin trading on the New York Stock Exchange under the ticker SECZ on July 2.

Commenting on the listing, Securitize co-founder and CEO Carlos Domingo said reaching the public markets represents an important step for the company after more than eight years of building tokenization infrastructure.

“Reaching the public markets is a significant milestone for Securitize and a reflection of the growing momentum behind tokenization.”

Domingo added that tokenized securities, once considered largely theoretical by major financial institutions, are now moving into mainstream finance as institutional adoption continues to grow.

The public debut also follows several months of expansion for the company. As previously reported by crypto.news, Securitize recently extended its Tokenized AAA CLO Fund (STAC) to the Solana blockchain. The company said Ethena Labs plans to allocate $250 million to the fund, which invests in U.S. dollar-denominated AAA-rated collateralized loan obligation tranches.

According to Securitize, the product is developed with BNY serving as custodian of the underlying assets and sub-adviser through BNY Investments.

Institutional tokenization business continues to expand

Alongside new investment products, Securitize has continued growing its role in tokenized capital markets. Earlier this year, the company partnered with the New York Stock Exchange to support the exchange’s planned tokenized securities platform.

Crypto.news previously reported that Securitize provides tokenization infrastructure for more than 650 funds and oversees more than $4 billion in tokenized assets. BlackRock has also deepened its relationship with the firm.

In May, crypto.news reported that the asset manager filed a second Securitize-powered tokenized fund with the U.S. Securities and Exchange Commission after its BUIDL fund expanded to roughly $2.3 billion in assets.

At the same time, Securitize is dealing with a legal dispute ahead of its market debut. As reported by crypto.news, the company recently asked the U.S. District Court for the District of Delaware to declare that its products do not infringe patents owned by tZERO after receiving a cease-and-desist letter. Securitize called the allegations “without merit,” while tZERO said its claims involve patents covering compliance systems, investor registry checks, and tokenized market infrastructure.

Separate industry forecasts also point to continued growth in tokenized finance. Earlier this month, Standard Chartered projected that tokenized assets used in decentralized finance could reach $2.7 trillion by the end of 2030, up from current levels.

Base, Coinbase’s Ethereum layer-2 network, has resumed normal operation after a consensus-related issue temporarily halted block production for nearly two hours on Thursday. The incident triggered “unhealthy” block building, leaving new blocks unable to be created until the network isolated and corrected the underlying problem.

Base said blocks were later being produced normally and that the broader ecosystem infrastructure had recovered and synced. The outage was unusual for a chain that has become a go-to venue for activity on Ethereum’s scaling roadmap, highlighting how sensitive rollup operations can be when consensus and sequencing logic fail.

Key takeaways

- Base went offline briefly due to a consensus problem that resulted in an invalid block being sequenced and prevented new block creation.

- Base reported recovery of “healthy blockbuilding” and confirmed ecosystem-wide infrastructure synchronization.

- The outage occurred around an on-chain upgrade window, with a Base upgrade (“Beryl”) scheduled for 6 pm UTC.

- Network creators emphasized that user funds remained safe, while reiterating that a block-production halt is not acceptable.

- Thursday’s incident joins a small set of notable recent outages affecting major L2 ecosystems.

How the outage unfolded

Base’s status page said it began investigating “unhealthy” block production at 4:03 pm UTC on Thursday. In a subsequent update at 5:21 pm UTC, the Base team explained that it had “isolated a consensus problem” which caused an invalid block to be sequenced.

According to the status updates, that invalid sequencing stopped progress at the protocol level: “This prevented new blocks from being created.” In other words, the issue was not presented as a simple infrastructure hiccup; it was tied to the chain’s ability to agree on what should be built next.

Recovery confirmed, post-mortem expected

Base later posted an operational recovery update just before 6 pm UTC. It said the network had “recovered healthy blockbuilding,” and that ecosystem-wide infrastructure was able to sync again. Base also indicated that it had identified the issue and would continue investigating the root cause, promising a full post-mortem.

Separately, Base’s creator Jesse Pollack used X to reassure users that funds on the network are safe. Pollack also framed the halt as a solvable operational setback, saying it would be used to “level up” Base as a platform aimed at supporting continuous, global finance.

An uncommon downtime event for a leading L2

The episode stands out as a rare downtime event for Base. The report notes that Base is widely considered among the most-used Ethereum layer-2 networks, and it cites the chain’s previous major outage in August 2025, when Base reportedly went down for 33 minutes. That earlier incident is referenced via Base’s status page.

Such disruptions matter for users and developers because L2 block production is the backbone for transaction inclusion, sequencing, and timely settlement flows. Even if funds remain safe, a halt can translate into delays for withdrawals, reduced reliability for dApps, and friction for systems that assume steady block cadence.

Upgrade timing raises questions for reliability planning

Base downtime appeared to occur separately and shortly ahead of a scheduled network upgrade dubbed “Beryl,” planned for 6 pm UTC. The described goal of the Beryl upgrade was to reduce delays on withdrawals and introduce a new token standard intended for real-world assets and stablecoins.

That timing is important for operators and integrators: when an outage overlaps with a planned change, teams typically have to ensure that the network can recover cleanly and continue the upgrade without compounding issues. Base did not state that the outage directly affected the Beryl rollout, but the proximity means builders watching Base would likely want to see post-recovery monitoring closely through the upgrade window.

The incident also comes amid broader reminders across the L2 landscape. The report points to Sui experiencing two periods of downtime on back-to-back days in May, each involving temporary stops in block production. In that case, Sui later attributed the downtime to a network update it said it knew had a low probability of causing a halt—an example of how even planned changes can create operational risk.

What to watch next

Base has said it will share a detailed post-mortem and identified the consensus problem responsible for blocking new block creation. Investors, traders, and developers should watch for that report, plus confirmation that the Beryl upgrade proceeds smoothly with stable block production and no renewed consensus symptoms around the new token standard changes.

Jeffrey Donaldson exposes the limits of political self-righteousness

Catching A Falling Calf: A Contrarian Case For America's Beef Packers

52% of UK wealth advisers can’t see clients’ crypto

-

Entertainment6 days ago

Entertainment6 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports4 days ago

Sports4 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech5 days ago

Tech5 days agoMicrosoft accidentally kills epic Outlook email threads

-

Fashion15 hours ago

Fashion15 hours agoWeekend Open Thread: Staud – Corporette.com

-

Business6 days ago

Business6 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics1 day ago

Politics1 day agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics1 day ago

Politics1 day agoPotential 2028er World Cup attendee leaderboard

-

Business1 day ago

Business1 day agoAsia stock markets slide as tech shares slump

-

Tech2 days ago

Tech2 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World3 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World3 days ago

Crypto World3 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World2 days ago

Crypto World2 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Business3 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World7 days ago

Crypto World7 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Sports12 hours ago

Sports12 hours agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World4 hours ago

Crypto World4 hours agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Crypto World16 hours ago

Crypto World16 hours agoRTX holders must register wallets before token distribution begins

-

Crypto World19 hours ago

Crypto World19 hours agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World7 days ago

Crypto World7 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Sports2 days ago

Sports2 days agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

You must be logged in to post a comment Login