Crypto World

Schwartz proposes XRPL fix as front-running fears return

David “JoelKatz” Schwartz has proposed a transaction reservation plan for the XRP Ledger after fresh claims that users may still face front-running and sandwich attacks on payments, offer crossing, DEX trades and AMM swaps.

Summary

- Schwartz proposed reserved XRPL transaction slots to place protected trades before later disclosed transactions first.

- XRPresso claimed queue visibility may expose payments, offers, DEX trades and AMM swaps to targeting.

- XRPL’s growing DeFi roadmap makes transaction ordering fairness a larger concern for users and builders.

The debate started after XRPresso said some actors may be able to view pending transactions before a ledger closes and use that information to target trades.

“A serious front-running issue continues on the XRPL that disadvantages regular users.” XRPresso said validators and well-connected nodes can view transactions in the pre-validation queue, then submit their own transactions to seek a better position in the final ledger order.

XRPresso said the issue matters most for users trading through wallets and dApps. According to the post, the final order inside each ledger follows a known deterministic process, and repeated submissions may raise the chance of landing near a target trade. That could worsen slippage for the original trader when a sandwich strategy succeeds.

Schwartz lays out a reservation scheme

“For the reasons I’ve explained, I’m not that concerned about this issue.” Schwartz wrote that the concern still deserved a practical answer. He then proposed a transaction reservation scheme that could make a disclosed transaction execute before any transaction formed after it became visible.

The plan would add a new ledger object called ReservedTxns. That object would hold a ledger sequence number and an array of transaction IDs. A new TxnReserve transaction would let a user reserve a slot for a transaction in a future ledger, as long as the request meets fee, timing and execution rules.

Schwartz said a reservation should cost at least twice the normal transaction fee. The target ledger would need to be greater than the current ledger and no more than 16 ledgers ahead. Each reserved object would hold fewer than 32 transaction IDs, unless the design later expands the cap.

Reserved transactions would run first

Under the proposal, a reserved transaction would be broadcast close to the point when the prior ledger’s proposals are known. Schwartz said XRPL software could add a feature to hold such transactions and release them only when that condition is met. The transaction should also set its last valid ledger to the ledger where it is expected to run.

When that ledger executes, the network would first check whether a ReservedTxns object exists for the ledger sequence number. If it exists, the network would execute listed transactions that are in the consensus set before other transactions. It would then remove them from the set to stop repeat execution and delete the reservation object.

XRPL documentation says canonical ordering is built to be deterministic, efficient and hard to game. Its DEX documentation also says transaction order is designed to discourage front-running because trades execute when a new ledger closes. However, XRPL’s algorithmic trading documentation says front-running is difficult, but not impossible.

DeFi upgrades raise the stakes

The timing comes as XRPL developers continue to expand the network’s DeFi stack. The XRPL Foundation recently proposed AMM Swappable Curves, a draft upgrade that would add StableSwap and concentrated liquidity options to the native automated market maker. XRPL is also preparing native lending and programmable escrow tools.

Those upgrades could bring more on-chain trading, credit and settlement activity to XRPL. Recent coverage also showed institutional use cases, including a tokenized Treasury settlement involving Ripple and JPMorgan. As activity grows, transaction ordering and pending trade visibility may draw more attention from builders, traders and validators.

Schwartz also addressed possible denial-of-service risks. He said an attacker could try to fill reservation slots across many ledgers, but rising fees could make that costly. Under one example, fees would rise once 16 slots are filled and could reach several times the base reserve near 30 slots. The proposal is not yet a formal amendment, but it gives the XRPL community a clear technical path to review.

Instead of a resurgence and a breath of fresh air for the bulls, the primary cryptocurrency’s condition has only worsened, with a 6% price drop over the past week.

The bearish environment has prompted several analysts to issue pessimistic forecasts, with some envisioning declines to around $50K.

How Much Lower?

Last week, BTC briefly plummeted to around $58,000, thus reaching its lowest level since September 2024. In the following days, the bulls reclaimed some lost ground, and the cryptocurrency is currently hovering around $60,000.

According to X user Chiefy, another short-term pullback might be on the horizon. The analyst claimed that BTC has historically bottomed out about 427 days after each cycle’s all-time high, suggesting a plunge to $51,000 may follow next.

AlΞx Wacy also weighed in, basing their thesis on the asset’s past performance. That said, the X user argued that the cryptocurrency will either start a two-year bull run or bleed for an additional six months.

Some prominent figures, including the American businessman and media personality Dave Portnoy, recently floated the idea that BTC may collapse to zero. His post drew heavy criticism from many Bitcoin proponents, who opined that such a scenario is impossible, while others suggested that comments like this often appear when the market is nearing a cycle bottom.

BTC’s halving, which occurs roughly every four years, is another key reference point analysts use to estimate market tops and floors. Looking at previous cycles, the asset has shown remarkably consistent timing between major lows and highs, and if history repeats itself, the bottom may arrive sometime between October 4 and October 17, 2026.

Of course, this is not guaranteed and would depend on numerous factors, including ETF flows. Lately, outflows from these investment vehicles have far exceeded inflows, reflecting waning investor enthusiasm and setting the stage for a further correction in the near future.

The Bullish Scenario

Despite pessimistic views from numerous analysts and the crypto market’s depressed state, BTC may still be on the verge of a short-term resurgence.

First, we’ll take a look at the popular Fear & Greed index, which has been in “extreme fear” territory for quite some time. This reflects the prevailing panic among investors and, at first glance, sounds like bad news for the cryptocurrency. However, such conditions have historically mapped the cycle bottoms and have often been followed by major rebounds.

Next on the list is BTC’s Relative Strength Index (RSI), which has been hovering around 30 for the last few days. Such ratios suggest that the asset is oversold and due for a potential rally, while levels above 70 are seen as a warning of an incoming pullback.

Last but not least, one should keep in mind that July has historically been a strong month for BTC, with the price finishing in red territory only 4 out of 13 times.

The post Bitcoin (BTC) Price Warning: Why Another Drop Could Be Coming This Week appeared first on CryptoPotato.

Everyone is watching the CLARITY Act for what it does to crypto market structure. Buried inside it is a provision with a different target entirely: a ban on a US central bank digital currency. It is literally one of the bill’s three names. Here is what the anti-CBDC provision does, why it is there, and why it may matter more for stablecoins than for anything else.

Summary

- The CLARITY Act carries an anti-CBDC provision so central that it is one of the bill’s three official short titles, alongside the market-structure language that gets all the attention.

- The provision amends the Federal Reserve Act to bar the Fed from issuing a retail central bank digital currency directly or indirectly, and from using one to conduct monetary policy, without explicit approval from Congress.

- A central bank digital currency would be a direct liability of the Fed recorded on a government-controlled ledger, which supporters argue would hand the government real-time visibility into individual transactions.

- The biggest practical effect would be to remove the only potential government-backed competitor to private stablecoins, handing issuers of tokens like USDC, USDT, and Ripple’s RLUSD a durable structural advantage.

- The same CBDC ban is advancing on several tracks at once, including a four-year ban that already passed both chambers inside a housing bill, so the CLARITY provision is part of a broader, redundant Republican push.

Almost everyone watching the CLARITY Act is watching it for one reason: it would settle the long fight over whether crypto tokens are securities or commodities, reshaping how the entire digital-asset market is regulated. That is the headline, and it is a big one. But folded inside the same bill is a provision aimed at something completely different, a ban on a United States central bank digital currency, and it is not a minor footnote.

The anti-CBDC language is so integral to the legislation that it is one of the bill’s three official short titles: the same act is named the Digital Asset Market Clarity Act, the CLARITY Act, and the Anti-CBDC Surveillance State Act. In other words, stopping a government digital dollar is not a rider quietly attached to the bill; it is one of the bill’s stated purposes, written into its very name. Yet because the market-structure debate consumes nearly all the attention, the CBDC ban has traveled largely under the radar, which is exactly why it is worth examining on its own.

The reason this matters extends well beyond a technical change to the Federal Reserve Act. A ban on a US central bank digital currency touches some of the most charged questions in money today: financial privacy, government surveillance, the future of the dollar, and, most concretely for crypto, the competitive fate of private stablecoins. Removing the possibility of a government-issued digital dollar does not just settle a privacy debate; it clears the field of the one competitor that could have challenged the private stablecoins now becoming central to crypto and payments.

This piece explains what the anti-CBDC provision actually does, what a central bank digital currency is and why it generates such fierce opposition, the political case behind the ban, the bigger prize of a protected lane for private stablecoins, the several parallel tracks on which the ban is moving, the serious arguments against it, and what it all means for crypto holders. The market-structure fight may decide how crypto is regulated, but the CBDC provision could quietly shape who wins the payments future, which makes it one of the most consequential parts of the bill almost nobody is discussing.

What the provision actually does

Start with the mechanics, because the provision is specific. The anti-CBDC language amends the Federal Reserve Act to impose several related prohibitions on the central bank. It bars the Federal Reserve banks from offering certain products or services directly to individuals, which is the structural feature a retail digital dollar would require, since a true retail CBDC would mean ordinary people holding accounts or balances directly with the Fed.

It prohibits the Fed from issuing a central bank digital currency, or any digital asset substantially similar to one, directly to individuals or indirectly through financial institutions or other intermediaries. It prohibits the use of a central bank digital currency to conduct monetary policy. And in its fuller forms, the anti-CBDC framework also bars the Fed from even testing or developing a CBDC without explicit authorization from Congress.

The throughline of all these provisions is a single principle: the Federal Reserve should not be able to create a digital dollar for the general public on its own authority. Under the ban, any move toward a retail CBDC would require Congress to pass a law specifically authorizing it, rather than the Fed proceeding through its own rulemaking. This converts the question of a digital dollar from a decision the central bank could make into one that only elected legislators could make, which supporters see as a crucial check and critics see as an unnecessary handcuff.

Notably, the bans are generally written to protect private, dollar-denominated digital currencies that are open and preserve the privacy features of physical cash, meaning they target a government-issued CBDC specifically while leaving private stablecoins untouched. That carve-out is not incidental; as the later sections show, protecting private stablecoins while blocking a government one is arguably the whole point.

What a CBDC is, and why it draws such fire

To understand the intensity of the opposition, you have to understand what a central bank digital currency actually is, because it is easy to confuse with the digital money people already use. The dollars in an ordinary bank account are already digital, but they are a liability of a commercial bank, not the Federal Reserve, and they pass through the banking system with its existing layers of intermediation.

A retail central bank digital currency would be fundamentally different: it would be a direct liability of the Federal Reserve itself, a form of digital money issued and backed by the central bank, held by the public, and recorded on a ledger the government controls. In its retail form, it would be used by ordinary people for everyday transactions, the digital equivalent of cash but issued directly by the state, as distinct from a wholesale CBDC, which financial institutions would use to settle large transactions among themselves.

The objection that animates the ban is captured in the bill’s own framing as an anti-surveillance measure. Critics of CBDCs, including the lawmakers behind the provision, argue that because a retail CBDC would be recorded on a centralized, government-controlled ledger, it would give the issuing authority complete, real-time visibility into individual transactions, and potentially the power to control or restrict how people spend their own money.

To this way of thinking, a government digital currency is the antithesis of the privacy that cash and, in a different way, cryptocurrency provide, and it edges toward a system of financial surveillance incompatible with a free society. Supporters of the ban frame it as protecting Americans from government overreach into their financial lives.

This is why the provision carries the loaded name Anti-CBDC Surveillance State Act, and why the issue has become a rallying point: for its proponents, blocking a CBDC is about preventing a tool of state surveillance before it can be built, which is a far more emotive cause than the technical market-structure questions that surround it in the same bill.

The political case behind the ban

The anti-CBDC provision did not arrive by accident; it reflects a deliberate and long-standing political push, and understanding that context clarifies why it sits inside the CLARITY Act. Opposition to a US central bank digital currency has been a priority for many Republican lawmakers and for the current administration, framed around privacy and limited government.

The legislator most associated with the standalone anti-CBDC effort has described its purpose as codifying the President’s stated effort to prevent the development of a central bank digital currency and to keep the country’s digital-currency policy in the hands of the American people rather than what he called the administrative state.

The President signed an executive order opposing a CBDC early in the administration, and the Treasury Secretary has publicly stated that a digital dollar is off the table, with the government instead focusing its energy on passing crypto legislation like the CLARITY Act.

This alignment between the administration and congressional Republicans is why the anti-CBDC language has been pursued through multiple vehicles and why it found a home inside the CLARITY Act. For its proponents, the goal is not merely to stop a CBDC that might be built someday, but to write the prohibition into durable law so that no future administration could pursue a digital dollar without going back to Congress.

It is worth being precise that this is a contested, partisan framing rather than a neutral consensus: supporters present the ban as a vital privacy protection, while opponents, as a later section details, see it as solving a problem that does not exist and forfeiting a tool other countries are embracing.

But on the proponents’ side, the case is coherent and deeply felt: a retail CBDC represents, in their view, an unacceptable expansion of government power over individuals’ money, and banning it preemptively is a way to foreclose that risk for good. That conviction is what put an anti-surveillance measure into a crypto market-structure bill and made it one of the bill’s defining names.

The bigger prize: a moat for private stablecoins

Beyond the privacy argument, the anti-CBDC provision carries a commercial consequence that may matter more for crypto than the surveillance debate, and it concerns the booming market for private stablecoins. Stablecoins are privately issued digital tokens pegged to the dollar, and they have become central to crypto trading and increasingly to real-world payments, with the largest, such as Circle’s USDC and Tether’s USDT, accounting for the overwhelming majority of stablecoin volume, and newer entrants like Ripple’s RLUSD growing quickly.

A retail central bank digital currency would be the one thing capable of seriously challenging these private stablecoins, because a government-issued digital dollar would offer the public a sovereign, risk-free digital alternative to a privately issued token. If people could hold digital dollars directly from the Federal Reserve, the appeal of holding a private stablecoin would diminish for many uses.

By banning a US CBDC, the provision removes that competitor before it can exist, and this is where the privacy framing and the commercial reality converge. The ban forecloses the only credible government-backed rival to private stablecoins, effectively handing issuers a structural advantage that no amount of regulation or marketing could buy them: the absence of a sovereign competitor, guaranteed by law.

This is why the CLARITY Act and the stablecoin framework already signed into law are best understood as sequential pieces of the same strategy. The earlier law set up the licensing framework for private stablecoins, and the CLARITY Act, by blocking a CBDC, helps clear the competitive field on which those stablecoins will operate. The result is a deliberate tilt of the payments future toward private issuers and away from a government digital dollar.

For crypto, and for the stablecoin issuers in particular, this is arguably the most important practical effect of the anti-CBDC provision: not the abstract privacy principle, but the concrete removal of the one competitor that could have constrained the private stablecoin market just as it is becoming central to the industry. Holders of stablecoin-linked assets, including those in the XRP ecosystem given Ripple’s RLUSD, sit on the favorable side of that tilt.

The ban is moving on several tracks at once

An important nuance, often lost in coverage, is that the CLARITY Act is not the only vehicle carrying the CBDC ban, and appreciating the full picture prevents overstating the role of any single bill. The same anti-CBDC objective has been advancing through at least three parallel paths. First, the language lives inside the CLARITY Act itself as one of its named components.

Second, a standalone Anti-CBDC Surveillance State Act passed the House of Representatives as its own bill and went to the Senate separately, giving the prohibition an independent path. Third, and most strikingly, a four-year ban on a Federal Reserve CBDC, running through the end of 2030, was attached to an unrelated housing bill that passed the Senate by an overwhelming margin and cleared the House, putting it on the verge of becoming law.

That housing-bill ban illustrates both the momentum behind the anti-CBDC push and the political turbulence around it. The provision sailed through Congress with broad support, banning the Fed from issuing a CBDC directly or indirectly through intermediaries while explicitly protecting private stablecoins that are open and preserve cash-like privacy. But the bill’s signing was delayed when the President held it up over an unrelated demand on separate legislation, a reminder that even broadly supported measures can get caught in larger political standoffs, and that the delay consumed legislative time the CLARITY Act itself could ill afford.

The takeaway is that the CBDC ban is overdetermined: it is being pursued through redundant channels, so even if the CLARITY Act stalls, the prohibition may well become law through one of the other paths. For anyone trying to gauge the future of a US digital dollar, the honest assessment is that the political system has moved decisively against one, through multiple overlapping efforts, of which the CLARITY Act provision is one prominent part instead of the sole determinant.

The serious case against the ban

Evenhandedness requires taking the arguments against the CBDC ban seriously, because they are substantive and come from credible quarters, not just from would-be government surveillers. The most striking criticism is that the ban would make the United States a global outlier. A great many countries are actively developing or piloting central bank digital currencies, with China’s digital yuan among the most advanced and well over a hundred countries exploring the technology in some form.

Banning a CBDC outright would make the United States the only major economy to foreclose the option entirely, which critics argue cedes ground in the evolution of money and could, over time, weaken the dollar’s competitive position in a world moving toward digital sovereign currencies. The concern is not that a digital dollar is necessarily desirable, but that permanently banning even the ability to build one is a drastic and possibly shortsighted response.

A related criticism is that the ban could hamper legitimate central-bank work on the future of payments. The Federal Reserve participates in international efforts to modernize cross-border payments using tokenized central-bank money, and a sweeping prohibition could undercut that research and the United States’ role in shaping global standards. Critics also note a certain irony: the Federal Reserve was not actually building a retail CBDC, so the ban forecloses a project that did not exist, which they argue makes it more a symbolic and ideological act than a response to a real and present threat.

From this angle, the provision solves a hypothetical problem at the cost of real flexibility, while the privacy concerns it cites could in principle be addressed through design choices instead of an outright ban. Supporters answer that a preemptive, permanent ban is exactly the point, because it removes the temptation and the risk for good, and that the surveillance dangers are too serious to leave to future design promises. Both sides have a coherent case, and reasonable people land in different places, but the debate is real and should not be flattened into a simple privacy-versus-surveillance morality tale. The ban has genuine costs as well as the benefits its supporters emphasize.

What it means for crypto and XRP holders

For crypto holders trying to translate all this into something actionable, the anti-CBDC provision points in a fairly clear direction, even if its effects are more structural than immediate. The most direct consequence is favorable for private stablecoins and, by extension, for the parts of the crypto ecosystem built around them.

By removing the prospect of a government-issued digital dollar, the ban protects the competitive position of private stablecoins at exactly the moment they are becoming central to crypto payments and settlement. Issuers like Circle and Tether benefit from the absence of a sovereign rival, and so does Ripple’s RLUSD, which means holders in the XRP ecosystem have a stake in this outcome even though it sits in the regulatory weeds instead of the price charts. The broader thesis that private, on-chain dollars will carry an increasing share of payments gets a meaningful boost when the public-sector alternative is taken off the table by law.

The effects on the wider crypto market are more diffuse but still real. The anti-CBDC stance is part of the same policy posture that favors private digital assets and lighter-touch regulation, and its advance signals an environment broadly supportive of the industry. At the same time, holders should keep the provision in proportion. Because no US retail CBDC was actually being built, the ban changes the hypothetical future more than the present reality, and its largest effects are competitive and long-term instead of an immediate catalyst for any token’s price.

It is also worth remembering that the ban is moving through several vehicles, so its fate is not bound to the CLARITY Act alone, and that the privacy debate it embodies is genuinely contested, with credible arguments on both sides about whether foreclosing a CBDC serves or harms the country’s long-term interests. The clear-eyed reading for a holder is that the anti-CBDC provision is a quiet but meaningful tailwind for private stablecoins and the broader private-digital-money thesis, embedded in a bill whose market-structure provisions will likely matter more for prices in the near term, but whose CBDC language may shape the deeper question of who owns the future of digital payments.

Frequently Asked Questions

Does the CLARITY Act really ban a US CBDC?

Yes, the anti-CBDC provision is one of the bill’s three official short titles, alongside the Digital Asset Market Clarity Act and the CLARITY Act, the third being the Anti-CBDC Surveillance State Act. The language amends the Federal Reserve Act to bar the Fed from issuing a retail central bank digital currency directly to individuals or indirectly through intermediaries, from using a CBDC for monetary policy, and, in its fuller forms, from even testing one without explicit authorization from Congress. So blocking a government digital dollar is not a minor rider but one of the bill’s stated purposes, even though the market-structure provisions receive nearly all the public attention.

What is a central bank digital currency?

A central bank digital currency, or CBDC, is digital money issued and backed directly by a country’s central bank. A retail CBDC, the kind the ban targets, would be held by ordinary people and used for everyday transactions, making it a direct liability of the Federal Reserve recorded on a government-controlled ledger. This differs from the digital dollars already in bank accounts, which are liabilities of commercial banks, not the Fed. It also differs from a wholesale CBDC, which financial institutions would use to settle large transactions among themselves. The retail version is what generates the privacy concerns, because it would route everyday payments through a ledger the government controls.

Why do supporters want to ban a CBDC?

Supporters frame it as a privacy and anti-surveillance measure. Their core argument is that a retail CBDC, recorded on a centralized government ledger, would give the state real-time visibility into individuals’ transactions and potentially the power to control how people spend their money, which they see as incompatible with financial freedom. The provision’s name, the Anti-CBDC Surveillance State Act, captures this framing. Proponents, including the administration and many Republican lawmakers, want to write the ban into durable law so no future administration could build a digital dollar without explicit congressional approval, foreclosing what they view as a serious surveillance risk before it can materialize.

How does banning a CBDC affect stablecoins?

It helps private stablecoins significantly. A government-issued digital dollar would be the one thing capable of seriously challenging private stablecoins like USDC, USDT, and Ripple’s RLUSD, because it would offer the public a sovereign, risk-free digital alternative. By banning a US CBDC, the provision removes that competitor before it can exist, handing private stablecoin issuers a structural advantage guaranteed by law. The bans are also typically written to protect private stablecoins explicitly while blocking the government one. This is arguably the most important practical effect of the provision, tilting the future of digital payments toward private issuers and away from a public digital dollar.

Is the CLARITY Act the only bill banning a CBDC?

No, and this is an important nuance. The same anti-CBDC objective is advancing through several parallel tracks. It exists inside the CLARITY Act as one of its named components, a standalone Anti-CBDC Surveillance State Act passed the House separately and went to the Senate, and a four-year CBDC ban running through 2030 was attached to an unrelated housing bill that passed both chambers and is near becoming law. So the prohibition is being pursued redundantly, which means it may become law through one of these paths even if the CLARITY Act stalls. The CLARITY provision is one prominent part of a broader push instead of the sole vehicle.

What are the arguments against banning a CBDC?

Critics make several serious points. A ban would make the United States the only major economy to foreclose a CBDC entirely, while many countries, including China with its digital yuan, are actively developing them, which critics argue cedes ground in the evolution of money and could weaken the dollar’s long-term position. They note the Fed was not actually building a retail CBDC, so the ban forecloses a project that did not exist, making it more symbolic than responsive to a real threat. They also warn it could hamper legitimate central-bank work on modernizing cross-border payments. Supporters counter that a permanent, preemptive ban is precisely the point, removing the risk for good. Both sides have coherent arguments

This article is information, not legal, financial, or investment advice. The status and contents of the CLARITY Act, the standalone anti-CBDC legislation, and related bills reflect reporting available as of June 27, 2026, and can change. The CBDC debate is politically contested, and this article presents the arguments of multiple sides instead of endorsing any. Nothing here is a recommendation regarding any token or security. Verify current details from primary sources and consider your own circumstances before making any decision.

Bitcoin is heading toward the end of June with traders focused on a potential make-or-break area near $60,000—an important level that bulls have struggled to defend as bearish momentum has carried into the second quarter. At the same time, several widely watched momentum and onchain signals are flashing early “stabilization” clues that could complicate the bearish narrative.

Technical traders point to bullish divergences in RSI across multiple time frames, while onchain analytics from CryptoQuant highlights a “first bottoming flag” tied to how broadly Bitcoin’s unspent outputs remain in profit versus loss. Separately, macro traders are preparing for a tight window of economic releases—especially the U.S. manufacturing PMI—and the market’s sensitivity to U.S. labor data and geopolitical developments.

Key takeaways

- RSI divergences are appearing across several time frames in Bitcoin’s charts, an indication that selling pressure may be losing traction.

- June’s performance has been weak—CoinGlass data cited in the report shows nearly a 19% loss for BTC/USD in June, its worst since the 2022 bear market.

- Traders are comparing the current $60,000 test to prior bear-market behavior, arguing that support often breaks only after repeated attempts.

- CryptoQuant says a UTXO profitability indicator is at its lowest level since 2022, suggesting an early stage of internal “market clean-up.”

- Seasonality research cited by traders suggests July has historically been a better month than June in many years, though outcomes can vary.

RSI divergences revive recovery odds as June nears its close

As June approaches its end, analysts and traders are watching whether Bitcoin can hold a key structural level. According to TradingView data cited in earlier coverage, RSI signals across multiple time frames are showing bullish divergences—instances where price behavior and momentum diverge in a way that historically can precede reversals or at least a pause in decline.

Cointelegraph previously reported that RSI cues across time frames are aligning into bullish divergences with price as June ends. The article also referenced a comment from Bitcoin whale “Gerla” (CryptoGerla) on X, saying the four-hour chart is showing a bullish RSI divergence while a potential double bottom forms.

Other traders have emphasized that such divergence signals have not consistently appeared in prior dips during 2026. Pseudonymous commentator “Heisenberg” noted on X that recent oversold RSI divergences had not shown up in the same way during earlier drops—until the current setup—suggesting the present decline may be maturing rather than simply accelerating.

Still, the presence of divergences is not the same as confirmation. The same coverage points out that $60,000 has increasingly acted as resistance, with bulls unable to push through decisively—an issue that keeps traders wary of a breakdown scenario heading into month-end.

Why $60,000 matters: the “mid-2022” support test comparison

One reason traders treat the $60,000 level as more than just a psychological number is historical patterning. In the source reporting, commentators compared the current situation to 2022, when Bitcoin repeatedly interacted with the $30,000 area before it finally failed and later produced a bear-market low.

CoinGlass data cited in the article places Bitcoin’s June drawdown at nearly 19% for BTC/USD—described as the worst since the 2022 bear market and the sharpest performance so far this year. That framing matters because it puts current price weakness into context: the market is not just drifting lower, it is experiencing a month that resembles the intensity of prior major risk-off phases.

On X, commentator “Exitpump” argued that significant support and resistance levels rarely break on the first attempt, often requiring repeated tests before momentum flips decisively. The same post likened the current $60,000 dynamics to the way $30,000 behaved earlier in the 2022 cycle. Importantly, the argument here is conditional: even if June is fragile, it may not be a single-day event that determines the next trend leg.

Macro pressure points: PMI, labor data, and geopolitical risk

Even with technical setups improving, Bitcoin’s short-term direction often depends on what happens in U.S. economic data. The source highlights a “short but busy” four-day trading week ending Q2, with the manufacturing PMI as a potential swing factor.

According to the report, the Institute for Supply Management (ISM) is set to publish the manufacturing Purchasing Managers Index (PMI) on Wednesday. The source notes that the PMI has been breaking out from a multiyear downtrend and that estimates call for a score around the mid-50s, with a possible mild decrease versus the prior month. In prior coverage, Cointelegraph had described PMI strength as a potential tailwind for crypto markets.

Thursday’s June nonfarm payrolls report is another key focus. As trading resource The Kobeissi Letter summarized in a thread on X, the market is also set to react to geopolitical developments as the U.S. and Iran agree to discuss their fragile peace agreement. The same note tied the week’s schedule to the end of Q2, with earnings season on the horizon—factors that can amplify cross-asset volatility.

The report also stresses that Bitcoin’s correlation with equities has been inconsistent in recent months, and it includes an example of trader Daan Crypto Trades pointing to BTC versus the S&P 500 returning to a level seen during earlier risk-stress periods. That matters for investors because it implies the market may not be moving in a straight line with stock indices—meaning both crypto-specific and macro drivers can compete.

Seasonality and “first bottoming flag” signals: early stabilization vs. full reversal

Two separate narratives are being used to explain why July could look different from June. The first is historical seasonality. The source cites research shared by Rekt Capital on X, arguing that in previous years July has often offset June’s weakness—sometimes followed by August weakness that cancels July’s upside. CoinGlass data referenced in the article supports this pattern by showing only a few exceptions since 2013, while 2025 is noted as a case where both months finished green.

The second narrative is onchain. The report highlights a CryptoQuant QuickTake post by contributor I. Moreno, who described an “early clear sign” of deeper market clean-up. Moreno focuses on the UTXO Block P/L Count Ratio Model, an indicator that compares how blocks of unspent outputs are distributed between profit and loss across the network.

In Moreno’s explanation as quoted in the source, a high ratio can indicate many UTXO blocks still sit in profit—often associated with higher distribution risk. When the ratio falls toward lower ranges, profitability compresses, losses spread more widely, and the market enters a more advanced reset phase.

The report states that the ratio is currently 5.9, described as the lowest since 2022 and one of the lowest readings on record, which Moreno called Bitcoin’s “first bottoming flag” of the current bear market. However, the same source cautions that this may only indicate the start of internal reset rather than the completion of a full bottom—history suggests additional stress absorption may still be required.

What this combination of signals implies is not certainty, but a shift in balance: momentum indicators are improving at the same time an onchain metric suggests distribution pressure may be moving into an earlier phase of exhaustion. The unresolved question is whether $60,000 holds long enough for those signs to translate into a sustained reversal.

Going forward, traders and investors should watch month-end price acceptance around $60,000, the immediate reaction to U.S. PMI and labor data, and whether the RSI divergences persist as July starts—alongside onchain follow-through on the “bottoming flag” theme highlighted by CryptoQuant.

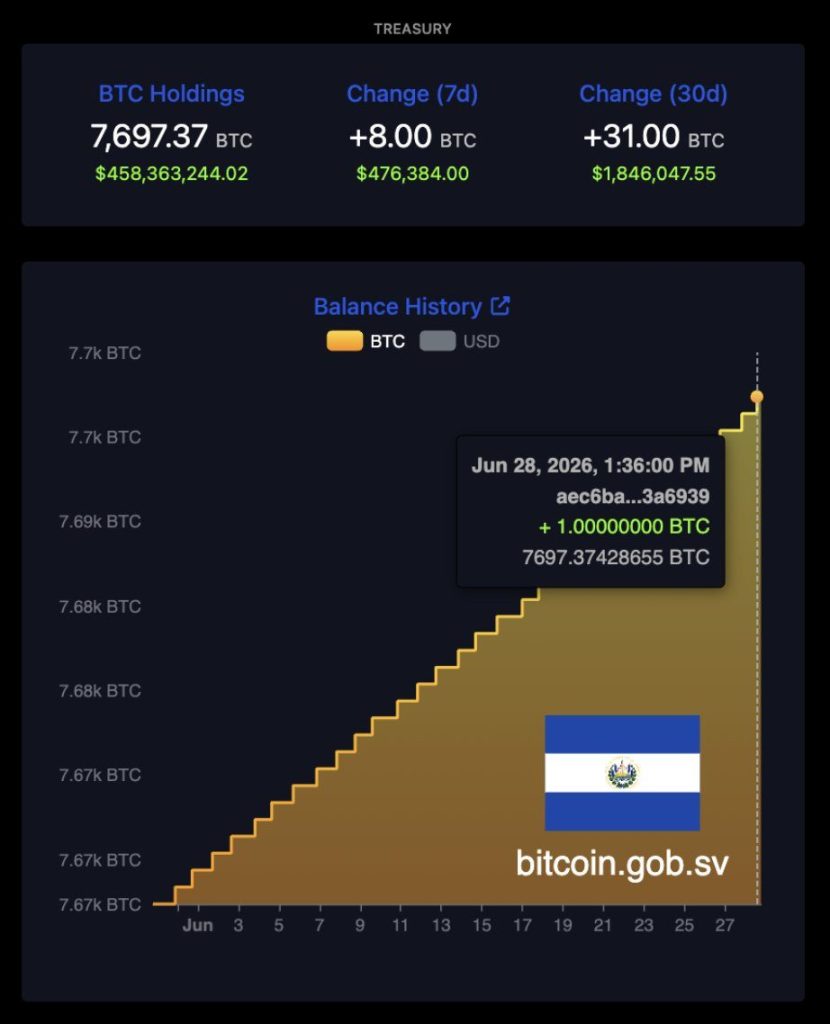

Bitcoin News: El Salvador’s Bitcoin reserve stands at 7,696 BTC, worth approximately $460M as of June 28, but the number is doing more political work than the accounting behind it can cleanly support.

President Nayib Bukele’s government continues to publicly promote a one-BTC-per-day BTC accumulation strategy, even as the country operates under a $1.4Bn Extended Fund Facility with the IMF that imposes a hard zero ceiling on voluntary public-sector Bitcoin purchases.

That gap between public messaging and loan conditionality is the central tension the next IMF review will force into the open.

Bitcoin was trading in the $59,000 to $60,000 range at the time of publication, down roughly 19% over 30 days. That drawdown matters here because it compounds the fiscal optics: at the reserve’s peak valuation near $800M in early 2026, the strategy looked like a winning sovereign bet.

At current prices, the same 7,696 BTC position represents a significant unrealized loss and a balance-sheet line item that the IMF is watching closely.

The country occupies a unique position in the history of sovereign Bitcoin. It made BTC legal tender in September 2021, built the state-run Chivo wallet infrastructure to support public adoption, and turned BTC purchases into a national brand. That era is now constrained by the terms of the IMF deal, which it needed to stabilize public finances.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Bitcoin News: The IMF Ceiling Is Precise. The Reserve Growth Is Not.

The IMF’s Extended Fund Facility, approved by the Fund’s Executive Board in early 2025, includes a continuous quantitative performance criterion with a zero ceiling on voluntary BTC accumulation by the public sector.

A parallel ceiling covers public-sector BTC-denominated or BTC-indexed debt and tokenized instruments. These are not aspirational targets; they are performance criteria tied to disbursement. Missing them has consequences.

The complication is that El Salvador’s reported holdings have risen since the program began. Official data showed 5,968 BTC at the program’s December 2024 start; BitcoinTreasuries now lists 7,696 BTC as of late June 2026. On its face, that trajectory contradicts a no-accumulation pledge.

The IMF’s explanation, confirmed by spokesperson Julie Kozack, is that increases in the Strategic Bitcoin Reserve Fund reflect consolidation of BTC across various government-owned wallets, notably from a BANDESAL cold-storage address, rather than net new market purchases by the public sector. The total BTC controlled across all government wallets, the IMF says, has remained unchanged.

That distinction is technically defensible under international public-sector accounting standards, which treat all government-controlled wallets as a consolidated position.

But it is not self-evident from the public-facing reserve tracker, and it leaves El Salvador’s one-BTC-a-day narrative in a structurally ambiguous place: the claim may describe internal wallet movements rather than fresh sovereign accumulation, or it may not.

Discover: The Best Token Presales

Bukele’s Bitcoin Brand Versus the Loan’s Hard Conditions

The political logic of Bukele’s sovereign Bitcoin strategy was always layered. BTC purchases were simultaneously a hedge against dollar dependency, a brand-building exercise for international Bitcoin audiences, and a domestic political signal.

The one-BTC-a-day narrative still travels effectively on social media and still positions El Salvador as the flagship experiment in crypto regulation by adoption rather than restriction. None of that political value disappears under IMF oversight.

What changes is the accountability structure. The IMF program required El Salvador to report all public-sector hot and cold wallet addresses and corresponding BTC balances, with deadlines at the end of March 2025, the end of June 2025, and the end of December 2025.

It also required the government to exit its public involvement in the Chivo wallet by July 2025, to liquidate the Fidebitcoin trust, and to publish audited financial reports for all Bitcoin-linked public entities. The Fund’s stated position is that “efforts will continue” to ensure El Salvador does not accumulate additional BTC, phrasing that signals ongoing scrutiny rather than a settled compliance verdict.

A government reserve cannot be redeemed the way ETF shares can. US spot Bitcoin ETFs absorbed roughly $5.94 billion in outflows over six consecutive weeks during the same period El Salvador’s reserve was under pressure, illustrating exactly how quickly institutional Bitcoin demand can reverse.

El Salvador has no equivalent exit mechanism. Its reserve must coexist with budget targets, IMF disbursement conditions, and public accounting requirements simultaneously. That is a different kind of constraint than a corporate treasury or an ETF sponsor faces.

Discover: The Best Crypto to Diversify Your Portfolio

The post El Salvador Claims It’s Buying Bitcoin Daily, But the IMF Disagrees appeared first on Cryptonews.

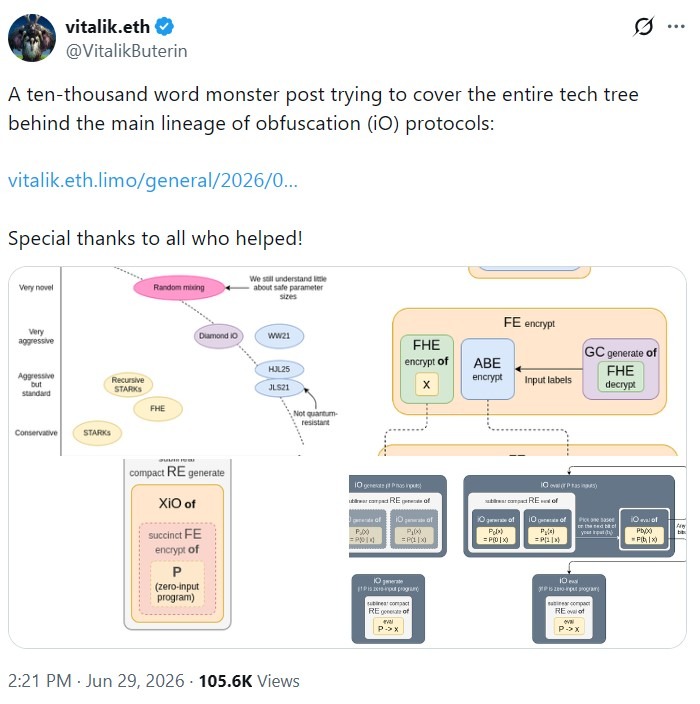

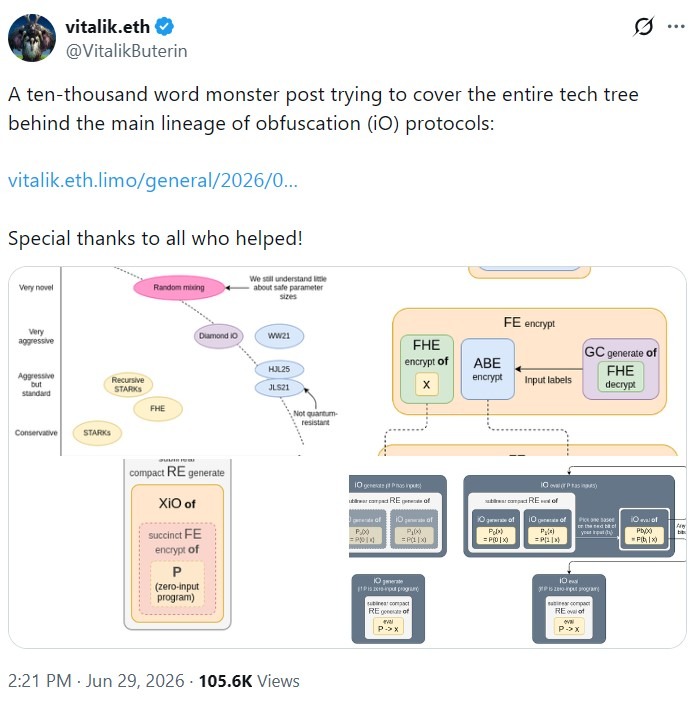

Ethereum co-founder Vitalik Buterin published a technical essay outlining how cryptography could one day enable people to vote privately onchain without relying on a trusted group to manage ballots or reveal the result.

In a blog post on Monday, Buterin said a cryptographic approach called indistinguishability obfuscation (iO), combined with blockchain infrastructure, could support private and collusion-resistant voting with “almost no trust assumption.” The approach would replace threshold committees, which jointly decrypt voting data, with protected programs designed only to reveal the outcome.

Private onchain voting remains dependent on groups of operators safeguarding information and behaving honestly. Removing that dependency could make decentralized governance harder to manipulate, reduce the risk of insider interference and allow voters to participate without exposing how they voted, according to Buterin.

However, Buterin said the technology remains impractical. He said the most conservative constructions require what he described as “galactic” amounts of computation. He said faster approaches rely on less-tested security assumptions, which means that the idea presents a more long-term research direction rather than a deployment-ready system.

Source: Vitalik Buterin

How indistinguishability obfuscation could protect onchain votes

According to Buterin, iO is a form of cryptography that turns software into a protected program. People can run the program and receive the intended output, but they cannot inspect its internal code or extract the data stored inside it. Buterin described the concept as hiding the code rather than the information being processed.

For onchain voting, Buterin said an obfuscated program could contain the logic needed to process encrypted ballots and reveal the final tally without exposing individual votes, essentially removing the need for a threshold committee whose members collectively hold the keys required to decrypt the result.

Buterin said blockchains would still play a key role because an obfuscated program cannot prevent itself from being copied or independently maintain changing information.

Related: Ethereum whale who shorted October 2025 crash opens $19.7M ETH short position

Buterin’s broader privacy push

Buterin previously connected iO with private voting in his Ethereum roadmap published in October 2024. He said the approach could provide stronger privacy and resistance to coercion. His latest essay expands on that earlier proposal by examining how the underlying cryptography could be constructed, the security assumptions it requires and the technical barriers preventing it from becoming practical.

In April 2025, Buterin proposed a more immediate privacy roadmap for Ethereum, calling for privacy tools to be integrated into existing wallets. The proposal also advocated for stronger protections against data collection by infrastructure providers that wallets use to access Ethereum.

Buterin also drew funding from his personal holdings to fund privacy-preserving technologies. On Jan. 30, he earmarked 16,384 Ether (ETH), worth about $45 million at the time, to fund initiatives focused on privacy, open infrastructure and self-sovereign tools.

Magazine: Japanese pension fund tips 1% in crypto, G7 urges action on NK hackers: Asia Express

Key Highlights

-

Verizon shares gained following announcement of strategic BT partnership worth $4B.

-

Equal ownership structure establishes balanced control between both telecom leaders.

-

Combined platform will deliver services to 3,000 enterprise customers in over 180 nations.

-

Agreement includes $625M equalization payment from Verizon to BT.

-

Industry veteran Martijn Blanken selected to helm the new enterprise entity.

Shares of Verizon Communications (VZ) experienced upward movement following the revelation of a strategic international partnership with BT Group. The telecommunications giants unveiled plans for an equally controlled enterprise joint venture that merges their worldwide corporate operations. The initiative focuses on delivering services to multinational corporations operating in more than 180 nations. Verizon’s stock finished trading at $46.54, representing a 1.02% increase, though pre-market activity showed a modest 0.30% decline to $46.37.

Verizon Communications Inc., VZ

Telecommunications Powerhouses Forge International Enterprise Alliance

BT Group and Verizon have agreed to merge their worldwide corporate operations into a single jointly managed entity. The arrangement establishes equal governance rights for both telecommunications providers. As part of the financial terms, Verizon will transfer an equalization sum of $625 million to BT.

The newly formed organization will cater to over 3,000 corporate clients spanning international territories. Combined yearly revenues are projected to reach approximately $4 billion. This strategic alliance provides both corporations with an expanded infrastructure for delivering enterprise connectivity solutions.

According to company statements, the framework will enable multinational corporations to access protected communication and networking capabilities. The partnership merges BT International with Verizon’s overseas enterprise wireline division. Consequently, the operation will emphasize international connectivity, cloud-based networks, and regulatory compliance services.

Partnership Delivers Enhanced Scale for Corporate Network Services

The collaborative enterprise focuses on corporations requiring protected worldwide networks spanning diverse geographic areas. It will address data management, operational demands, and compliance standards for large-scale organizations. Furthermore, both companies anticipate that the unified network infrastructure will generate operational efficiencies following completion.

The entity will be legally established in the Bailiwick of Jersey. Nevertheless, primary operations and tax residency will be maintained in the United Kingdom. The venture will also establish commercial arrangements with both founding organizations after finalization.

BT and Verizon will maintain direct service to their respective home markets while backing the new corporate platform. BT will concentrate on its United Kingdom initiatives, while Verizon will continue direct customer service within United States territories. This organizational approach enables both corporations to streamline overseas operations while preserving dominance in core markets.

Industry Veteran Martijn Blanken Tapped as Future Leader

BT and Verizon have designated Martijn Blanken as the prospective chief executive officer of the collaborative venture. His official appointment is contingent upon successful completion of the agreement. Blanken is scheduled to join BT on September 1, 2026, ahead of the anticipated launch date.

Blanken brings extensive experience from senior positions throughout telecommunications, technology, and digital infrastructure sectors. His professional background encompasses executive leadership at Telstra, Openwave Systems, EXA Infrastructure, and KPN. The partners chose an executive with substantial expertise managing international network operations.

Clive Selley will maintain his position as chief executive of BT International throughout the transition period. Verizon’s management framework will continue without modification. Both international divisions will function autonomously until regulatory authorities approve the transaction.

Agreement Awaits Regulatory Clearance Process

The partnership remains subject to regulatory approvals and mandatory employee consultations in applicable jurisdictions. During this interim period, BT and Verizon will maintain separate operations for their international businesses. Both organizations have committed to upholding service obligations to existing customers throughout the approval process.

Goldman Sachs served as primary financial advisor to BT throughout the transaction. Deloitte provided transaction services advisory support, while Freshfields LLP delivered legal representation. Morgan Stanley advised Verizon, with Kirkland & Ellis LLP serving as its legal counsel.

The arrangement provides Verizon with enhanced positioning in worldwide enterprise connectivity markets. It simultaneously enables BT to restructure its international operations under a more concentrated framework. The transaction must successfully navigate the requisite approval procedures before the venture commences active operations.

South Korea’s DAT (Digital Asset Treasuries) crypto firms face fresh delisting risk under revised KOSDAQ regulations taking effect on July 1. Several companies that profited from Bitcoin holdings now sit directly in the crosshairs of the new retention rules.

The reform reshapes how Korean markets treat publicly listed crypto treasury players going forward.

What the New Korean Regulations Mean for DAT Crypto Firms

A Digital Asset Treasury, or DAT, is a publicly listed company that stockpiles cryptocurrencies as a core strategic asset on its balance sheet. The model mirrors what Strategy (formerly MicroStrategy) pioneered in the United States, and what Metaplanet has rolled out across Japanese capital markets.

In this way, South Korea has accelerated the implementation of stricter KOSDAQ listing regulations, effective July 1, 2026. The market capitalization threshold rises to 200 billion KRW (~$145 million) by the end of 2026 and 300 billion KRW (~$217 million) from January 2027.

Firms failing to meet the minimum for 30 consecutive trading days face managed stock status and risk automatic delisting within 90 days unless they recover the required level for 45 consecutive days.

Follow us on X to get the latest news as it happens.

The trigger for DAT crypto firms is specific. Several of these companies recorded major paper profits through their crypto holdings as Bitcoin rallied across the past year. However, those gains may now fall within the scope of the new retention threshold, exposing the firms to immediate delisting review.

The reform signals a broader regulatory stance. Korean authorities continue tightening every layer of the digital asset ecosystem, from exchange ownership caps to stablecoin frameworks. Moreover, the KOSDAQ revisions now extend that pressure directly to publicly listed firms holding crypto on their corporate balance sheets.

How DAT Crypto Firms Like Bitplanet Are Now Positioned

Bitplanet is the most visible example of South Korea’s emerging DAT crypto sector. The company was created in July 2025 when a consortium led by Asia Strategy and Sora Ventures acquired KOSDAQ-listed SGA. Furthermore, Bitplanet now holds 300 BTC and aims to accumulate 10,000 BTC over the long term.

The firm’s playbook draws directly from international precedents. CEO Lee Seong-hoon has publicly cited Strategy and Metaplanet as the inspiration behind Bitplanet’s model. As a result, the company has positioned itself as Korea’s first true treasury-focused listed crypto vehicle.

Bitplanet is also expanding into operational businesses. The firm recently signed an MOU with Nasdaq-listed Antalpha to deploy Bitcoin mining equipment valued at approximately 15 billion won (~$10.8 million) across sites in Oman and Paraguay. Moreover, AI data center plans add a second revenue stream alongside the core treasury accumulation business.

The broader question is structural. South Korea remains one of the largest retail crypto markets in the world. However, the path for listed DAT crypto firms now depends on how strictly regulators apply the July 1 threshold and whether transparency can outweigh formal compliance gaps under the new framework.

The post South Korea’s New Rules Put Crypto Treasury Firms at Risk of Major Delisting appeared first on BeInCrypto.

As the chart shows, AUD/USD has entered a distinctly bearish phase in recent weeks, reflecting the broader consolidation — and in some cases outright weakness — that the US dollar has begun imposing across most major currency pairs.

Fundamental Analysis

The Reserve Bank of Australia concluded its June meeting by holding the cash rate steady at 4.35%, opting to monitor the effects of the three consecutive hikes already delivered since the start of the year. The board acknowledged that financial conditions have tightened and that the economy is showing early signs of slowing, while maintaining a vigilant stance on inflation, which remains above target.

In theory, a pause after a tightening sequence — with a cash rate at 4.35%, the highest in the G10 — is a structurally supportive signal for the Australian dollar, as elevated rate differentials tend to attract flows toward AUD-denominated assets. However, markets had already fully priced in this outcome, stripping the decision of any surprise. AUD/USD has consequently failed to post any meaningful bullish impulse, sliding toward almost three-month lows near 0.6890, weighed down by renewed US dollar strength on growing Federal Reserve rate hike expectations. Adding further complexity to the outlook, the ongoing Middle East conflict continues to weigh on global risk sentiment, acting as an additional headwind for a currency that markets have long treated as a barometer of global risk appetite.

Technical Analysis

The most representative benchmark for the Australian dollar’s momentum, AUD/USD seems to have already shifted his path. Following a prolonged period of broad greenback strength, the pair has gradually developed a bearish structure over recent weeks.

→ Bullish scenario: a key support zone sits in the 0.6880–0.6850 area. Should this level hold, it could restore some of the strength lost in recent weeks and bring the pair back to test the resistance between 0.6980 and 0.7000 — a threshold that will be decisive for the next directional move. A sustained recovery would also require a more relaxed geopolitical backdrop, as risk sentiment continues to cap AUD’s upside potential.

→ Bearish scenario: should support fail to hold — or should the pair test the descending trendline in play and reject it, confirming the prevailing downtrend — AUD/USD could revisit levels last seen at the start of the year, with the 0.6700–0.6600 zone as the next significant area of interest.

With a more relaxed geopolitical environment and a hawkish central bank behind it, will the Australian dollar manage to reclaim its strength on the forex stage?

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Key Takeaways

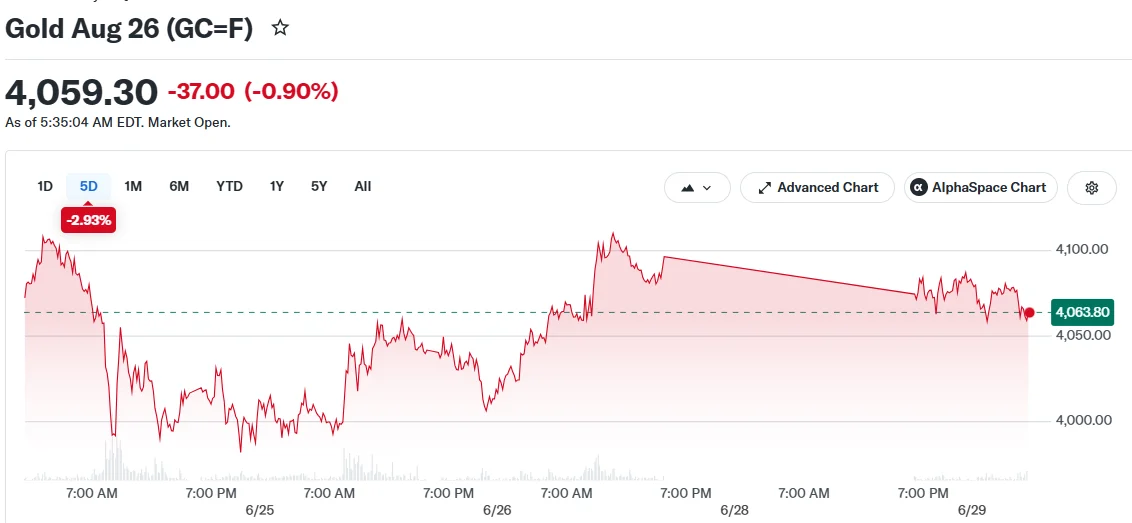

- Precious metal declined more than 1% on Monday, approaching $4,000 per ounce following renewed military exchanges between the US and Iran

- Washington and Tehran have committed to suspending hostilities and will convene for diplomatic discussions in Doha this Tuesday

- The yellow metal has surrendered approximately 23% of its value since joint US-Israeli military operations against Iran commenced in late February

- Derivative markets indicate over 30% probability of Federal Reserve rate increases before 2026 concludes

- Critical employment statistics scheduled for release this week may shape the central bank’s policy direction

Renewed military confrontations between Washington and Tehran during the weekend drove precious metal valuations downward on Monday, bringing the commodity close to the $4,000 threshold as inflationary pressures re-emerged in financial markets.

Spot bullion decreased 1.1% to $4,043.62 per ounce during early Asian trading sessions. Futures contracts for gold retreated 1% to $4,056.77.

The United States and Iran engaged in military operations across the Persian Gulf throughout the weekend, undermining a temporary cessation of hostilities that had previously stabilized energy commodity markets. A vessel transporting Qatari petroleum was damaged during these confrontations, interfering with maritime traffic through the Strait of Hormuz.

Notwithstanding the escalating tensions, both nations have committed to cease military operations. Diplomatic representatives are scheduled to convene in Doha on Tuesday, as reported by Axios through confidential government sources.

Bullion Weakens Under Rate Expectations and Dollar Strength

Gold has experienced sustained downward momentum for several months. The precious metal has depreciated roughly 23% since coordinated US-Israeli strikes against Iranian targets began in late February.

Elevated energy commodity valuations stemming from the regional conflict have accelerated inflationary trends, prompting market participants to anticipate prolonged restrictive monetary policies from central banking institutions. This dynamic has particularly disadvantaged gold, which generates no income for holders.

Derivative market pricing currently reflects greater than 30% likelihood of Federal Reserve rate increases materializing before the conclusion of 2026, based on CME Fedwatch analytics.

A robust American currency combined with elevated Treasury bond yields have compounded downward pressure. The Federal Reserve’s June policy meeting conveyed a restrictive stance, while recent inflation measurements registered elevated levels, though consistent with analyst projections.

The central bank’s preferred inflation metric, the personal consumption expenditures price index, advanced 0.4% during May. Government bond yields experienced modest declines following that data release.

Additional precious metals similarly declined on Monday. Silver retreated 1.8% to $58.11 per ounce. Platinum decreased 0.4% to $1,612.20.

Employment Report Poised to Dominate Market Attention This Week

Market participants are monitoring numerous economic indicators scheduled for release this week to assess future monetary policy trajectories.

Japanese manufacturing output figures, Chinese purchasing managers surveys, and European inflation measurements are all anticipated.

However, the primary focus remains the United States nonfarm payrolls report covering June. Resilient labor market conditions would provide the Federal Reserve additional justification for implementing rate increases.

Any indication that employment growth maintains momentum could accelerate gold’s decline, as elevated borrowing costs amplify the opportunity cost of maintaining non-income-producing assets such as bullion.

The diplomatic negotiations scheduled in Doha on Tuesday will also command significant attention. A sustainable peace agreement could alleviate energy price pressures and diminish inflationary expectations, fundamentally altering the trajectory for gold.

Currently, the metal remains confined near multi-month lows, suspended between geopolitical instability and the probability of ascending interest rates.

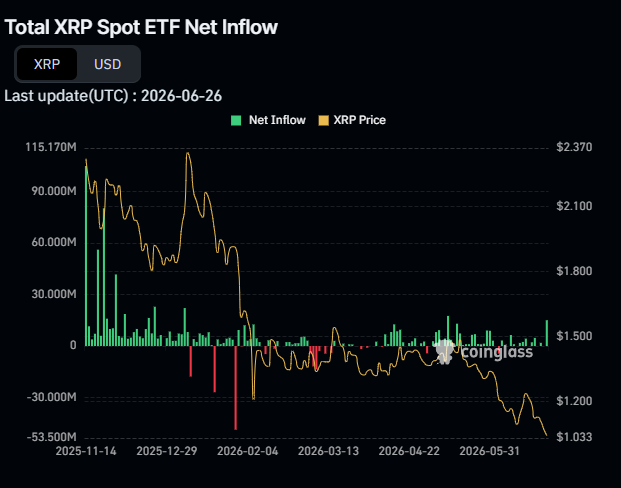

XRP (XRP) spot exchange-traded funds extended their inflow streak to eight consecutive weeks through June 26, pulling in $22.99 million. Bitcoin (BTC) ETFs shed hundreds of millions over the same period as BTC slid to its lowest price since late 2024.

The gap between the two assets widened sharply last week. Bitcoin ETFs recorded $444.50 million in net outflows in a single session, per CoinGlass data. XRP ETFs posted zero outflow days across the week.

XRP Holds Steady While Bitcoin Bleeds

Last week’s $22.99 million XRP ETF print was the largest single-week figure in June. Bitwise’s XRP ETF led flows, contributing $11.18 million on June 26. Franklin Templeton’s XRPZ added $3.80 million the same day.

Canary Capital and Grayscale recorded minimal movement across most sessions. The seven active funds hold combined assets under management approaching $1 billion.

Bitcoin ETFs have now posted seven consecutive weeks of net outflows. Total net assets across the BTC ETF complex fell to $81.85 billion from roughly $107.8 billion in mid-May.

BTC Falls Below $60,000 as Macro Pressures Mount

Bitcoin fell to below $60,000 on June 25, its lowest level since October 2024. Several factors hit at once. A selloff in semiconductor and AI stocks pushed investors away from risk assets. Reports of a potential CLARITY Act delay added regulatory uncertainty. ETF redemptions created additional mechanical selling as issuers sold underlying BTC to meet withdrawals.

BTC now sits roughly 31% lower year-to-date and more than 50% below its October 2025 all-time high of $126,272.

XRP has also dropped from its January 2026 peak of $2.40. However, the XRP price has held up better than BTC on a relative basis. The eight-week ETF inflow streak signals that institutions view XRP’s regulatory clarity as a separate factor from the broader market selloff.

Whether that bid holds into July will depend on CLARITY Act progress and macro conditions in the weeks ahead.

The post XRP ETF Inflows Hit 8-Week Streak: Will Bitcoin ETF Outflows Continue? appeared first on BeInCrypto.

Haberman: Trump “threw accelerant” on post-Iraq, post-financial crisis political turmoil

Wimbledon dress code rules now after female stars were ordered to ditch bras

Rocket Lab to Buy Iridium for $8 Billion in ‘Transformative’ Space Deal

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Renter of Home in Anne Heche Crash Denies Settlement With Son

Blockchain.com files with SEC for U.S. IPO

Haberman: Trump “threw accelerant” on post-Iraq, post-financial crisis political turmoil

Martin Lewis: Why broadband and mobile bills should stay fixed #gmb #money #consumer

SECRET XRP ANNOUNCEMENT NO ONE IS TALKING ABOUT #xrp #crypto #trump

-

Sports6 days ago

Sports6 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech7 days ago

Tech7 days agoMicrosoft accidentally kills epic Outlook email threads

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics3 days ago

Politics3 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics3 days ago

Politics3 days agoPotential 2028er World Cup attendee leaderboard

-

Business3 days ago

Business3 days agoAsia stock markets slide as tech shares slump

-

Tech4 days ago

Tech4 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World5 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World4 days ago

Crypto World4 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World5 days ago

Crypto World5 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

News Videos17 hours ago

News Videos17 hours agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Business5 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World2 days ago

Crypto World2 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Crypto World2 days ago

Crypto World2 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Sports3 days ago

Sports3 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World3 days ago

Crypto World3 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World3 days ago

Crypto World3 days agoRTX holders must register wallets before token distribution begins

-

Tech1 day ago

Tech1 day agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech2 days ago

Tech2 days agoRussian hackers now target Signal backup recovery keys

-

Sports4 days ago

Sports4 days agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

You must be logged in to post a comment Login