Crypto World

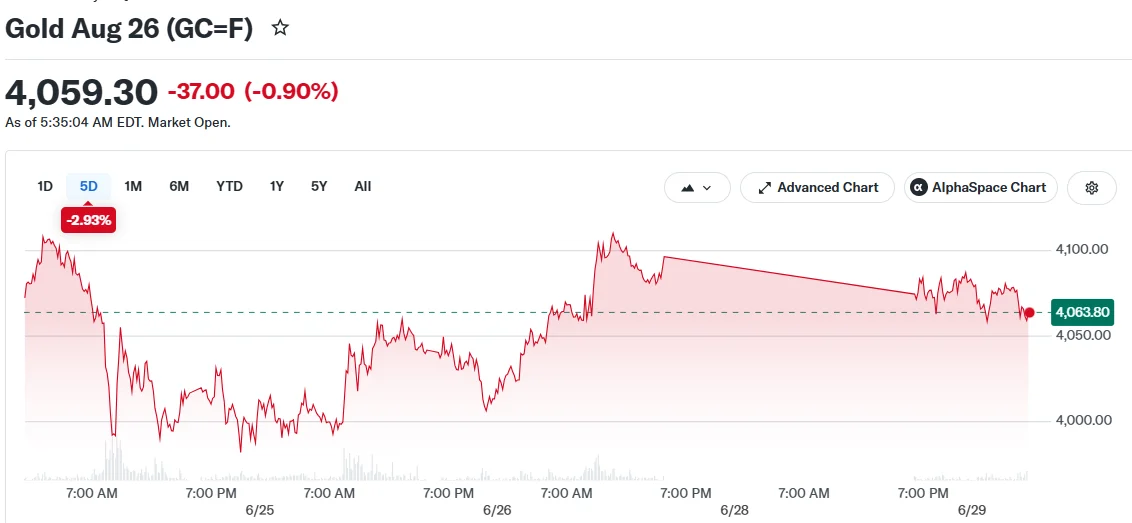

Gold Tumbles Below $4,050 as Mideast Tensions Spark Rate Hike Concerns

Key Takeaways

- Precious metal declined more than 1% on Monday, approaching $4,000 per ounce following renewed military exchanges between the US and Iran

- Washington and Tehran have committed to suspending hostilities and will convene for diplomatic discussions in Doha this Tuesday

- The yellow metal has surrendered approximately 23% of its value since joint US-Israeli military operations against Iran commenced in late February

- Derivative markets indicate over 30% probability of Federal Reserve rate increases before 2026 concludes

- Critical employment statistics scheduled for release this week may shape the central bank’s policy direction

Renewed military confrontations between Washington and Tehran during the weekend drove precious metal valuations downward on Monday, bringing the commodity close to the $4,000 threshold as inflationary pressures re-emerged in financial markets.

Spot bullion decreased 1.1% to $4,043.62 per ounce during early Asian trading sessions. Futures contracts for gold retreated 1% to $4,056.77.

The United States and Iran engaged in military operations across the Persian Gulf throughout the weekend, undermining a temporary cessation of hostilities that had previously stabilized energy commodity markets. A vessel transporting Qatari petroleum was damaged during these confrontations, interfering with maritime traffic through the Strait of Hormuz.

Notwithstanding the escalating tensions, both nations have committed to cease military operations. Diplomatic representatives are scheduled to convene in Doha on Tuesday, as reported by Axios through confidential government sources.

Bullion Weakens Under Rate Expectations and Dollar Strength

Gold has experienced sustained downward momentum for several months. The precious metal has depreciated roughly 23% since coordinated US-Israeli strikes against Iranian targets began in late February.

Elevated energy commodity valuations stemming from the regional conflict have accelerated inflationary trends, prompting market participants to anticipate prolonged restrictive monetary policies from central banking institutions. This dynamic has particularly disadvantaged gold, which generates no income for holders.

Derivative market pricing currently reflects greater than 30% likelihood of Federal Reserve rate increases materializing before the conclusion of 2026, based on CME Fedwatch analytics.

A robust American currency combined with elevated Treasury bond yields have compounded downward pressure. The Federal Reserve’s June policy meeting conveyed a restrictive stance, while recent inflation measurements registered elevated levels, though consistent with analyst projections.

The central bank’s preferred inflation metric, the personal consumption expenditures price index, advanced 0.4% during May. Government bond yields experienced modest declines following that data release.

Additional precious metals similarly declined on Monday. Silver retreated 1.8% to $58.11 per ounce. Platinum decreased 0.4% to $1,612.20.

Employment Report Poised to Dominate Market Attention This Week

Market participants are monitoring numerous economic indicators scheduled for release this week to assess future monetary policy trajectories.

Japanese manufacturing output figures, Chinese purchasing managers surveys, and European inflation measurements are all anticipated.

However, the primary focus remains the United States nonfarm payrolls report covering June. Resilient labor market conditions would provide the Federal Reserve additional justification for implementing rate increases.

Any indication that employment growth maintains momentum could accelerate gold’s decline, as elevated borrowing costs amplify the opportunity cost of maintaining non-income-producing assets such as bullion.

The diplomatic negotiations scheduled in Doha on Tuesday will also command significant attention. A sustainable peace agreement could alleviate energy price pressures and diminish inflationary expectations, fundamentally altering the trajectory for gold.

Currently, the metal remains confined near multi-month lows, suspended between geopolitical instability and the probability of ascending interest rates.

Wife of former FTX executive seeks to preclude her husband’s guilty plea

In a Friday filing with the US District Court for the Southern District of New York (SDNY) over campaign finance charges, Michelle Bond’s legal team asked the court to consider precluding evidence related to former FTX Digital Markets co-CEO Ryan Salame, her husband who is currently serving a 90-month sentence after he pleaded guilty in 2023.

Bond faces campaign finance charges alleging that her unsuccessful 2022 congressional run in New York was partially funded by contributions from FTX facilitated by Salame. As part of the filings this week, Bond asked the court to exclude evidence of her husband’s guilty plea and “related plea materials,” in which the former executive admitted to making “political contributions in [his] name that were funded by transfers from the bank accounts” of an entity tied to FTX.

“The Court should preclude the government from introducing or referring to Mr. Salame’s guilty plea or any related plea materials, because their minimal probative value is substantially outweighed by the risk of unfair prejudice to Ms. Bond,” said the filing.

Bond’s lawyers added:

“[…] Mr. Salame’s plea materials lack any probative value as to Ms. Bond’s guilt, knowledge, or intent. Mr. Salame’s plea is an admission of his own guilt, not evidence of Ms. Bond’s state of mind or participation in any charged offense.”

The motion also requested the court include information related to Bond’s “contemporaneous divorce and custody proceedings,” arguing that though she and Salame were not married at the time of the alleged crime, the former FTX executive was not an “ordinary ‘individual’ donor” contributing to her campaign.

Related: US Senate unanimously adopts resolution opposing clemency for SBF

The criminal case is one of the latest involving individuals tied to the defunct crypto exchange following its 2022 collapse. Salame, former FTX CEO Sam Bankman-Fried and former Alameda Research CEO Caroline Ellison were all sentenced to prison for their role in the misuse of customer funds and related charges.

Former congressman ordered to pay $35,000 over Kalshi bet

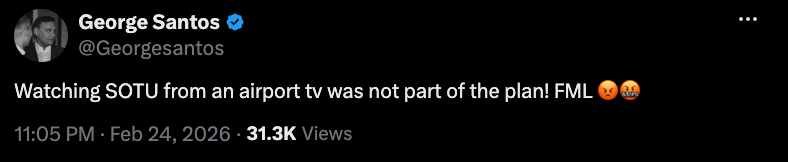

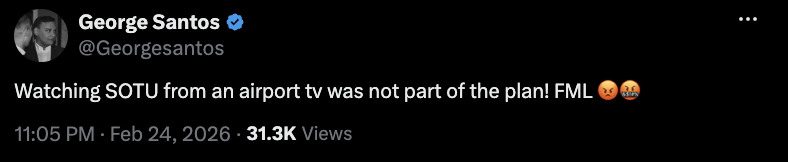

George Santos, a former New York House representative who was expelled from Congress in 2023, was ordered to pay a $17,500 civil monetary penalty and $17,570 in disgorgement from profits earned over bets placed on prediction markets platform Kalshi. The order from the US Commodity Futures Trading Commission (CFTC) stemmed from Santos trading on event contracts betting on his appearance at the 2026 State of the Union address in Washington, DC.

“While buying and selling positions in this market, Santos posted on social media about his plans to attend or not attend the SOTU,” said the CFTC. “In his social media posts, Santos made a series of material misrepresentations and omissions about whether he would attend the SOTU. After these posts, the SOTU contract prices moved in a direction that was favorable to Santos’ positions which allowed him to make over $17,500.”

February X post about his State of the Union attendance. Source: George Santos

Santos is barred from trading on prediction market platforms for three years as part of the order. He was also previously sentenced to 87 months in prison for wire fraud and aggravated identity theft in 2025, but served only three months before his sentence was commuted by US President Donald Trump.

US solider accused of making $400,000 Polymarket bet seeks to dismiss charges

Gannon Ken Van Dyke is a US soldier who faces charges for allegedly making more than $400,000 on Polymarket event contracts using nonpublic information tied to a military operation involving the removal of Venezuelan President Nicolás Maduro in January. He was involved in the operation removing Maduro, according to the US Justice Department, and allegedly used insider information to bet whether the Venezuelan president would be removed from power, leading to criminal charges in April.

In a Friday SDNY filing, Van Dyke’s legal team filed a 51-page memo in support of a motion to dismiss the indictment based on different legal theories, including that the Commodity Exchange Act (CEA) at the center of three of the charges was “ambiguous” in treating event contracts as “swaps.”

Although the CFTC under Chair Michael Selig has claimed that the agency has “exclusive jurisdiction” over prediction markets on the basis that event contracts are treated as “swaps,” Van Dyke’s lawyers said the lack of clarity was sufficient to dismiss some of the charges.

“If Congress, executive branch agencies, and courts all find the ‘swap’ definition ambiguous, how can ordinary citizens have fair notice that prediction market wagers are covered by the CEA?” said the filing. “They cannot.”

The case is expected to have significant implications for lawmakers and government officials using prediction markets. Trump’s teleprompter operator reportedly made more than $100,000 using Kalshi event contracts related to the president’s speeches.

Based on a schedule filed in June, Van Dyke is potentially looking at a trial beginning in late 2026 or early 2027. He has pleaded not guilty to all charges.

Magazine: Here’s why the CLARITY Act’s ethics deal may be so hard to reach

The attacker working through Coldcard-generated keys is now emptying wallets worth a few thousand dollars each.

Galaxy Research flagged a third wave of sweeps early Sunday, roughly 208 bitcoin drained from 1,912 addresses between Friday midday and Saturday morning UTC.

That is just over a tenth of a bitcoin per victim. The July 30 opening wave averaged close to a full coin, 1,083 bitcoin from 1,196 addresses in 41 minutes.

Observed losses across all three waves now total 1,367 bitcoin, nearly $89 million, from 4,585 addresses.

Wave three sends each victim’s coins to its own destination rather than the handful of shared collector addresses that made the first two easy to map, and parks them in pay-to-witness-script-hash outputs, a format that can carry multisignature or timelock conditions, instead of the plain single-key outputs used before.

It batched an average of six victims into each sweep where wave one took exactly one at a time, and it scanned only the default derivation path, the standard branch of the key tree a wallet checks first, instead of testing several branches per seed.

Perhaps due to the quickly re-escalating tension in the Middle East, the cryptocurrency market has posted fresh losses over the past few hours, with BTC dropping to $62,000 after failing to reclaim the $63,000 support during the day.

XRP was not spared, as it just slipped below $1.05. The asset was rejected at $1.20 during the mid-July rally after the favorable US inflation data for June, and eventually lost the coveted $1.10 support. Now, it fights for the last line of defense before the bulls would have to defend the $1.00 zone.

Popular analyst EGRAG CRYPTO outlined the significance of the $1.05 level, calling it the ‘battlefield’ region. Although he noted earlier today that the cross-border token had managed to maintain that level, he acknowledged the predominantly bearish structure of lower highs on the 4-hour chart.

The short-term path of recovery would be a successful defense of $1.05 before XRP can bounce above $1.083 and eventually reclaim the $1.10 level, which now acts as resistance.

EGRAG laid out an even more promising road ahead for the asset if it manages to continue its recovery, with the “major price target” set at $1.30.

However, a decisive breakdown below $1.05 would essentially mean that XRP will head toward the notable liquidity zone at around $1.00, he warned.

Mikybull Crypto also believes XRP has the strength to stage a surprising comeback. The analyst claimed that the asset’s bullish reversal run is currently loading despite the negative outlook.

His long-term chart compares the current market structure with the one from two years ago when XRP was highly compressed at around $0.60. Once it broke out the upper boundary, though, it rocketed to a fresh all-time high within less than a year.

“Before the last run, I screamed for you to buy at a crazy discount. The opportunity is presenting again,” he said now.

History is not on XRP’s side at the moment, though, as August has been quite a painful month for the asset. As reported earlier today, the cross-border token was deep in the red in all four previous editions.

The post XRP Price Dips to ‘Battlefield’ Zone, but Analysts See Major Reversal Opportunity appeared first on CryptoPotato.

Pi Coin (PI) rose 8% on Saturday to $0.0870. The move pushed the token onto CoinGecko’s trending list, days before a hard deadline for Pi Network.

Nodes are the computers that check Pi transactions. The people who run them have until August 11 to install an update. Nodes that miss it get cut off.

Why Pi Coin Is Trending Again

CoinGecko ranked PI second on its trending board on Saturday. Most other coins on that list were falling. Pi Coin was one of the few going up.

The bigger picture is less kind. While PI has gained 7% over the past week, it is still down 25% over the past month. The token is worth about $957 million in total, making it the 67th largest coin.

Trading stayed thin. Pi Network market data shows roughly $8.6 million changed hands in 24 hours.

What the August 11 Deadline Means

Protocol v26 is the latest step in a long chain of updates that started at version 19. Pi says it makes smart contracts safer. It also improves how the network stores data and talks to other blockchains.

“Protocol 26 is a major milestone ahead of the final planned upgrade, Protocol 27. With 8 successful upgrades completed over the past few months, these final two upgrades will bring the network up to date with the latest protocol features, improvements, and functionality,” the team noted.

Follow us on X to get the latest news as it happens

Only node operators need to act. People who mine Pi on their phones do not. Pi lists every step on its node page.

Pi nodes agree on transactions in small trusted groups, a design borrowed from Stellar. The July 22 Protocol v25 rollout added the cryptography that privacy apps need.

Why Pi Coin Rallies Keep Fading

Traders have seen this before. PI jumped 24% ahead of the July 22 update. It handed the gain back once the day arrived. The Protocol 24 mainnet upgrade in June ended the same way.

Zoom out and it looks worse. PI hit a record low of $0.0710 on July 14. It now sits 79% below where it traded a year ago.

New supply is the main drag. PiScan data cited last month showed about 1.71 billion PI unlocking over the next year. That is a heavy load for a market trading under $10 million a day.

Protocol v27 is the last planned update. Whether August 11 shifts the PI price forecast outlook comes down to one thing. Buyers have to show up faster than the new coins do.

The post Pi Coin Defies Market Trend Before Key Deadline: Will the 10% Bounce Hold? appeared first on BeInCrypto.

Who are possible challengers to FIFA President Gianni Infantino?

Infantino was originally expected to easily retain his position at the helm of FIFA in March 2027.

Now, with public calls for review into his leadership, potential rivals may feel emboldened.

“FIFA is full of sharks, and there’s no question that many of them can smell blood. Infantino’s election in 2027, which seemed like a sure bet only a few days ago, is now an open question,” Boykoff says.

Challengers for his role must submit their candidacies by Nov. 18, and there has already been some speculation as to who might make a bid.

Sheikh Salman bin Ebrahim Al Khalifa, president of the Asian Football Confederation (AFC), was defeated by Infantino in 2016, the current administrator’s first term, but he could return a decade later as a frontrunner. He called Infantino’s investment proposal and his failure to consult AFC on it “totally unacceptable,” putting the two publicly at odds.

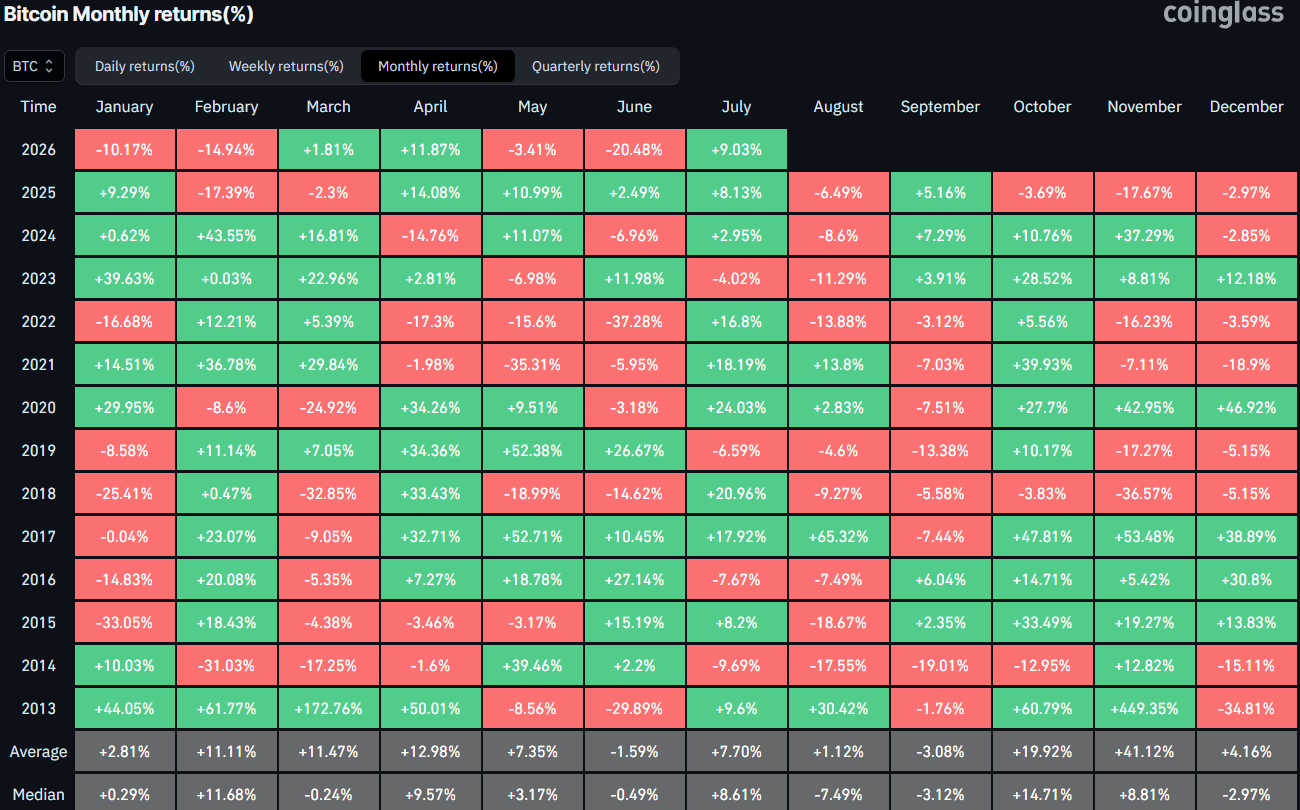

We will begin with the mandatory disclaimer, as we are well aware that historical performance does not guarantee similar moves in the future. However, history does tend to rhyme, and that’s what happened in July for BTC.

The question is: will August follow suit, as the month has not been kind to the largest cryptocurrency, especially the last four editions.

July Brought Some Gains

Before we explore what happened in July, here’s a brief outlook of the painful June, which set the stage for a rebound during the seventh month of the year. The 2026 edition of June became the most violent in terms of price moves for the cryptocurrency in precisely four years. It tumbled by 20.48% in 2026 compared to 37.28% in June 2022.

As such, it was almost expected that July would be a better month. History was also on BTC’s side as 9 out of the last 11 were in the green. However, the start was actually quite surprising as bitcoin dipped below $58,000 on July 1 for the first time in nearly two years.

The bears quickly lost control, though, and the asset reclaimed the coveted $60,000 level within a day or two. It wasn’t the most volatile of months, but BTC still managed to post some gains and peaked on July 21 at $67,000. This became its highest price tag in two months.

However, it was rejected there despite the softer-than-expected inflation data for June and the fact that the Fed refused to hike interest rates last week. Thus, bitcoin ended the month at under $64,000, which was still a 9% monthly increase.

Your Move, August

As popular analyst Ali Martinez put it yesterday: August hasn’t been kind to bitcoin. In fact, the last four have all been in the red, posting losses of 13.88%, 11.29%, 8.6%, and 6.49%, respectively. The silver lining is that the declines become less violent over time.

The broader August perspective is still deeply negative, though. Only three out of the last 12 editions have been in the green, with 2017 standing out as the most bullish one on record. At the time, BTC rocketed by over 65%, but it was a different time and a vastly different market phase.

For now, BTC enters August 2026 with lots of uncertainty not only within the industry itself, where interest has dwindled lately, but on a macro perspective as well. The war in the Middle East continues, and the one between Ukraine and Russia too, while inflation remains an issue, and Trump’s controversial actions tend to halt each breakout attempt in its tracks.

The post Bitcoin Rebounded in July, but Bears Target an August Pullback appeared first on CryptoPotato.

Cointelegraph is committed to providing independent, high-quality journalism across the crypto, blockchain, AI, and fintech industries.

All news, reviews, and analyses are produced with full journalistic independence and integrity. For more details on our standards and processes, please read our Editorial Policy.

A crypto-industry-backed political action committee affiliate has intensified its advertising push ahead of next week’s Michigan Republican primary, according to the latest Federal Election Commission (FEC) filings. Protect Progress PAC, which the filings indicate is funded largely by contributions from cryptocurrency companies Ripple Labs and Coinbase, has spent more than $2 million on media to influence the contest in Michigan’s 13th Congressional District.

The most recent updates, filed as of Thursday, show the committee ramping up spending in support of U.S. Representative Shri Thanedar while also funding opposition to his Democratic challenger, Donavan McKinney. The renewed disclosures come shortly after earlier reporting showed the PAC had already ramped up its buy—effectively doubling its reported ad spending from the prior week.

Key takeaways

- FEC filings show Protect Progress PAC has spent over $2 million on media for Michigan’s 13th district primary race.

- New disclosures add $884,240 to advertisements supporting Shri Thanedar and more than $150,000 to ads opposing Donavan McKinney.

- The PAC’s funding is described in the filings as being largely backed by cryptocurrency companies Ripple Labs and Coinbase.

- Thanedar’s legislative record includes support for crypto-related bills such as the GENIUS Act and the CLARITY Act.

- Protect Progress is an affiliate of Fairshake, a major outside spender in U.S. elections tied to crypto industry policy goals.

Michigan’s 13th district: Protect Progress increases ad buys

According to FEC disclosures accessed via the commission’s docquery system, Protect Progress PAC reported spending more than a combined $2 million on media in connection with Michigan Representative Shri Thanedar and his Democratic primary contest against Donavan McKinney.

As of Thursday, the filings reflect a further escalation: compared with what the PAC had already reported spending a week earlier, the committee’s latest report effectively doubled its media spending. The additional outlay includes $884,240 dedicated to ads supporting Thanedar and more than $150,000 aimed at opposing McKinney.

The Michigan primary is scheduled for Tuesday, but the filings underscore that the committee and its network have been willing to deploy substantial resources well before Election Day. Similar patterns have been visible across multiple congressional races during the 2026 cycle, according to the article’s referenced coverage and FEC-based reporting.

Why the race is drawing crypto-linked political money

Thanedar’s congressional record is at the center of the narrative around why outside groups see his candidacy as important for crypto policy. During his time in the House, he voted in favor of the stablecoin-focused GENIUS Act and supported the legislative push for clearer digital asset market structure—the Digital Asset Market Clarity (CLARITY) Act, which has been discussed in the Senate.

He also cosponsored the Promoting Innovation in Blockchain Development Act, an effort aimed at protecting developers. Supporters of crypto policy reform often point to such measures as steps toward a more predictable regulatory environment, while critics argue the industry has too much influence over the political process.

For voters watching the contest, the spending escalation suggests the primary is being treated as more than a local political test—it is being framed by donors and advocacy networks as part of a broader strategy to influence which lawmakers back specific digital asset legislation.

McKinney’s response and the broader allegations over crypto influence

McKinney has publicly characterized the ad push as a payoff for political favors. In a July 21 statement related to the PAC spending, he said “the crypto lobby is paying my opponent back for helping Trump make over $1 billion since taking office,” according to a video shared on his campaign’s Facebook page.

That comment appears to reference the U.S. President’s disclosures about crypto-related earnings, including a figure cited in earlier reporting referenced by the article—more than $1.4 billion from crypto investments in 2025—along with concerns raised by Democrats that Trump could be using his role to profit through policies such as GENIUS.

While those claims are rooted in political argument rather than direct proof of intent tied to the specific Michigan ads, they highlight a recurring tension in U.S. crypto politics: outside spending may be framed by industry-aligned PACs as policy support, while opponents often describe it as evidence of undue influence.

Cointelegraph reports that it reached out to both Thanedar’s and McKinney’s campaigns for comment on the PAC expenditures but did not receive an immediate response.

Fairshake’s affiliates: national momentum in multiple primaries

Protect Progress PAC is an affiliate of Fairshake, a political network that has become one of the most prominent outside spenders linked to crypto industry policy goals. Fairshake was responsible for spending more than $170 million across the 2024 election cycle through media buys supporting candidates it viewed as aligned with crypto-friendly regulation, as summarized in the article.

The article also notes that affiliates have already deployed millions of dollars in 2026 races beyond Michigan, pointing to activity in states including Texas and Illinois. In addition, it cites Public Citizen reporting from June that Fairshake and its affiliates accounted for more than $82 million out of roughly $189 million deployed by crypto companies during the 2026 election cycle.

Fairshake itself reportedly listed holding a $193 million “war chest” as of January, according to figures referenced in the piece. Taken together with the Michigan disclosures, the pattern suggests a sustained approach: deploy substantial resources early enough to shape narrative and voter attention around specific legislative priorities.

The article further describes similar affiliate activity in other congressional primaries. It says Defend American Jobs PAC spent more than $65,000 on media in Washington’s 4th congressional district to support a Republican candidate, with Washington holding primaries on the same day as Michigan.

In Alabama, scheduled primaries on Aug. 11 are also described as a focus for Fairshake-linked spending. FEC filings cited in the article indicate Defend American Jobs PAC spent more than $511,000 on media supporting Jerry Carl Jr., a Republican who represented Alabama’s 1st congressional district from 2021 to 2025.

For readers tracking the cycle, these parallel contests illustrate how crypto-aligned PAC affiliates appear to treat primary elections as strategic targets—places where candidate positioning on digital asset policy could be determined before general election dynamics begin.

What to watch as Michigan’s primary approaches

With Michigan’s 13th district primary scheduled for Tuesday, the key question is whether Protect Progress’s latest ad surge will further alter voter perceptions or turnout in the remaining days. More broadly, the filings reinforce that crypto-linked political spending is not limited to high-profile general election races—affiliates are actively contesting primaries with resources intended to influence policy direction well after election season announcements fade.

Binance founder Changpeng Zhao (CZ) says this bear market has no shortage of money. Plenty of it is hunting for somewhere to go.

Elsewhere, Social Capital founder Chamath Palihapitiya said where he thinks it should land. Not in artificial intelligence (AI) chips.

The Bear Market Has Money. It Is Not Buying Crypto

CZ did not say where the money should go, but acknowledged that there was a lot of liquidity floating despite the bear market.

The numbers show why it is not going into crypto. Bitcoin (BTC) trades near $63,037. It is down 45% in a year. That is almost exactly half its October 6 record.

Chamath Is Buying Land, Not Chips

Meanwhile, the Social Capital founder Chamath Palihapitiya, a venture capitalist, entrepreneur, and investor, buys three things at once. Land, a power connection, and an empty building to hold the computers.

“LPS (Land Power Shell) is still the most obvious and fastest path to cash on cash returns,” Palihapitiya wrote.

Palihapitiya is a former senior executive at Facebook (now Meta), a renowned SPAC sponsor, and former minority owner of the Golden State Warriors.

His reason is simple. Towns keep blocking data centers. Every site that already has power gets rarer.

The numbers back him. Data Center Watch counted at least 75 US projects blocked or delayed in early 2026, worth about $130 billion.It was the worst quarter on record. Opposition groups doubled and now operate in 49 states.

Politicians joined in. More than 300 state data center bills were filed in six weeks. Maine missed becoming the first state to ban them outright by one House vote.

Why He Quit the Chip Business

He says he helped start Groq in 2016. Nvidia licensed Groq’s technology last December. The deal was not exclusive. Groq founder Jonathan Ross moved to Nvidia.

Neither company gave a price, but Palihapitiya says $20 billion. Still, he would not do it again as chips have to run too fast, factories have to be too exact, and a startup cannot get enough memory.

How Much Power He Has Bought

Palihapitiya says he and his partner Anita Vlallian have acquired almost six gigawatts (GW). It arrives in stages through 2029.

One deal shows the going rate. Nasdaq-listed TeraWulf used to mine Bitcoin. In July it leased a 401-megawatt site in Hawesville, Kentucky, to Anthropic. The lease runs 20 years and should bring in about $19 billion.

Here is the part that proves his point. That site is not built yet. Power starts flowing in late 2027 and reaches full load in early 2028.

The money is committed anyway. Palihapitiya holds roughly 15 times that much capacity. His is not leased out yet, so the figure shows the size of his bet, not its value.

However, miners got there first, and already own cheap power, land with grid hookups, and empty sheds. Coinbase chief executive Brian Armstrong disputed the mining warning in July.

What Could Go Wrong

Jordi Visser of 22V Research says easy money is over in AI. He expects about 30% a year now.

The land bet also needs the protests to keep coming. If towns start approving data centers again, the scarcity goes away.

TeraWulf’s $19 billion is a forecast too. Its own filing calls it expected revenue.

CZ is right. The money is out there. The question is whether it buys power lines or comes back to Bitcoin and crypto markets.

The post CZ Says Bear Market Money is Hunting, Social Capital Founder Says Skip AI Chips appeared first on BeInCrypto.

Darline Graham makes her political debut in South Carolina

US Justice Department subpoenas New York Times freelancer over North Korea story, paper says

2026 AIG Women’s Open Sunday tee times: Round 4 pairings

-

Sports6 days ago

Sports6 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business3 days ago

Business3 days agoWhy Trees Belong on the Risk Register

-

Fashion1 day ago

Fashion1 day agoWeekend Open Thread: Wit & Wisdom

-

Tech6 days ago

Tech6 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Politics1 day ago

Politics1 day agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Politics5 days ago

Politics5 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Crypto World7 hours ago

Crypto World7 hours agoMicroStrategy Post-Earnings CLARITY Act Push Could Add New Catalyst for Its Stock

-

Politics5 days ago

Politics5 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

News Videos6 days ago

News Videos6 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Entertainment4 days ago

Entertainment4 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Business4 days ago

Business4 days agoMajor shareholder moves on Canyon

-

Crypto World7 days ago

Crypto World7 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Politics6 days ago

Politics6 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

News Videos2 days ago

News Videos2 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World15 hours ago

XRP Ledger v3.3.0 brings five institutional features

-

Entertainment7 days ago

Entertainment7 days agoSara Gilson Killed By Husband After Viral “Pedophile” TikTok Video

-

Crypto World4 days ago

Crypto World4 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech5 days ago

Tech5 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

News Videos4 days ago

News Videos4 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Politics2 days ago

Politics2 days agoLuke Littler’s dominance sparks GOAT debate

You must be logged in to post a comment Login