Crypto World

Ukraine transfers $8.3 million in seized crypto amid potential plans for strategic reserve

“This is the first time that seized crypto assets have actually been handed over to state management,” the statement reads. The funds came from wallets controlled by a member of an alleged international hacker group, the office said.

However, fund management involves custody of the digital assets, not ownership. The USDT sits in a wallet ARMA controls but has not been formally confiscated, a step that requires a conviction. ARMA already manages seized homes and cars, yet has no record of taking crypto onto its books.

Investigators accused the group of attacking people and companies in Europe and the U.S., stealing private data, demanding ransoms and laundering proceeds in Ukraine through real estate, cars and other high-value property.

Four suspects, including the alleged organizer, have been detained and remain in custody, the statement adds, and have not yet been convicted. Investigators estimate the damage from the group’s activities at more than $100 million.

Authorities have so far seized assets worth over $11.1 million, including homes, apartments, cars, $1 million in cash and virtual assets equal to more than $8.3 million.

Crypto World

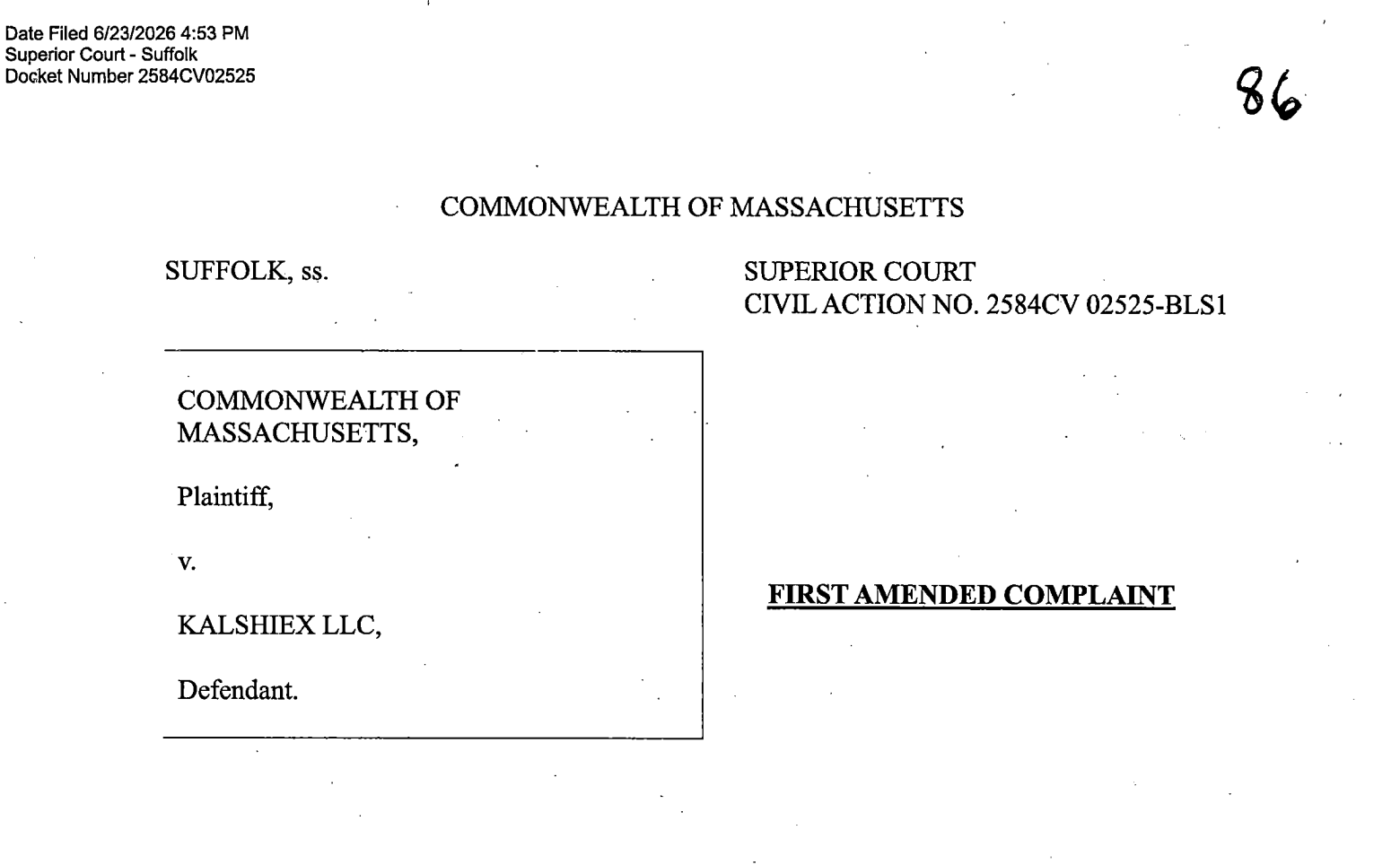

Massachusetts AG Files Amended Lawsuit Against Kalshi over Sports Betting after Court Ruling

Prediction markets platform Kalshi’s legal battle against Massachusetts will continue after a judge ruled that state authorities could add allegations against the company over sports betting.

In a Tuesday filing in Suffolk County Superior Court, associate justice Peter Krupp allowed state authorities to file a 71-page amended complaint, building on a filing alleging that Kalshi engaged in sports wagering in violation of state laws.

The amended complaint included allegations that Kalshi “targets those under 21 years of age and does little to stop them from using its platform,” citing the company’s marketing to university campuses and presenting images in ads of people who “appear to be younger than 21 years old.”

“Kalshi allows anyone who is at least 18 years old to create an account and wager on sports events by purchasing event contracts,” alleged Massachusetts authorities.

Source: Massachusetts Superior Court

Massachusetts Attorney General Andrea Joy Campbell announced the lawsuit against Kalshi in September 2025, alleging that the company needed to be licensed by the Massachusetts Gaming Commission to comply with state laws on online sports wagers. In January, a judge granted a preliminary injunction barring Kalshi from offering sports event contracts as the case was under review.

Related: US senators push to end CFTC ‘assault’ on state oversight of prediction markets

The Massachusetts case is just one of many involving state-level authorities and prediction markets companies like Kalshi and Polymarket, who offer users the ability to trade using event contracts on a variety of outcomes related to sports, politics and current events.

While Kalshi has been blocked from offering sports bets in some jurisdictions, it also has support from the US Commodity Futures Trading Commission (CFTC), which in April filed a brief in Massachusetts arguing the agency had “exclusive jurisdiction” over prediction markets. The CFTC, under Chair Michael Selig, has claimed that event contracts on the platforms amount to “swaps” covered by the Commodity Exchange Act and were not subject to state regulation.

“Congress has entrusted the CFTC with the sole authority to regulate commodity derivatives markets, including prediction markets,” said Selig. “To any state that seeks to nullify federal law and seize authority over these markets, I say again: we will see you in court.”

Cointelegraph reached out to Kalshi for comment but did not receive an immediate response. Following the initial complaint in September, a spokesperson said that the company was “ready to defend” itself in court.

Gaming organizations look to CLARITY Act for clarity on prediction markets

While one of the cases between a prediction markets platform and US state authority could ultimately reach the US Supreme Court given the arguments over federal and state laws, some groups are looking to Congress for solutions.

Earlier this month, national gaming and tribal organizations and labor groups called on US senators to add language “that explicitly prohibits event contracts tied to sports and casino-style gaming” to the Digital Asset Market Clarity (CLARITY) Act. The bill, under consideration in the Senate, is expected to give the CFTC more regulatory authority over digital assets.

Magazine: Does ‘Paper Bitcoin’ mean there’s an unlimited supply of BTC?

Nearly 1,700 UK investors have sued Binance and founder Changpeng Zhao (CZ) in London’s High Court, seeking at least £150 million ($200 million) over crypto derivatives they say were sold unlawfully.

The claimants argue the exchange marketed risky leveraged products to retail traders from late 2019 without proper authorization. Some say they lost tens of thousands of pounds when those bets turned against them.

The Binance UK Lawsuit Tests Who Pays

The case reaches beyond one exchange. It revives a question crypto has long avoided. When an unlicensed platform sells high-risk products, who absorbs the losses, the platform or the trader? It is a gap UK crypto oversight has not closed.

Britain’s Financial Conduct Authority (FCA) banned retail crypto derivatives in January 2021. It cited extreme volatility and a high risk of sudden losses. The regulator estimated the ban would save retail consumers around £53 million ($70 million).

The claimants say Binance pushed such products around that ban, breaching the Financial Services and Markets Act.

That statute may matter more than any risk warning. Under it, deals arranged by an unauthorized firm can be ruled unenforceable, letting clients reclaim their money and losses.

The real question is whether buyer beware can survive when the seller broke the rules. Britain already forced Binance to restructure under UK financial promotion rules in 2023.

Defenders of open trading say adults chose leverage with full warnings. Critics counter that an unauthorized seller cannot hide behind the risks its customers accepted.

Binance Digs In for a Long Fight

Binance has vowed to defend the claim. A spokesperson told Reuters the exchange honors its legal duties.

“Binance remains committed to its obligations to users and to operating in accordance with applicable law.”

Follow us on X to get the latest news as it happens

The allegations echo earlier ones. In 2023, the US Commodity Futures Trading Commission charged Binance and CZ with running an illegal derivatives exchange.

Regulators said it courted American users it had claimed to block. Months later, both pleaded guilty in a $4.3 billion settlement, the largest the crypto sector had seen.

The London claim names Cayman-registered Binance Holdings, UAE-based Nest Exchange, and unnamed operators.

CZ, pardoned in the US last year, is named personally. Even so, that structure could make any UK judgment hard to enforce.

The timing is awkward. The claim lands just as Binance exits Europe after its EU license bid failed, leaving its main authorization in the UAE.

Should the court void these deals, buyer beware may no longer protect exchanges that sold unauthorized products. The precedent would reach past Britain.

For an industry built on caveat emptor, that is the real verdict, even if compensation takes years.

The post UK Investors Sue Binance for $200 Million in Losses They Chased With Leverage appeared first on BeInCrypto.

With Bitcoin plunging below $60,000 and Strategy’s share price down by more than 70% from the high, some crypto investors are questioning if Strategy could become this cycle’s Terra/LUNA — a highly leveraged bet on crypto market structure that explodes under stress.

The company’s response? A new capital framework released on Monday aimed at addressing investors’ fears.

The package includes up to $1 billion in buybacks for MSTR, up to $1 billion in buybacks for STRC and related securities, an increase in STRC’s dividend to roughly 12%, and a cash buffer expansion to $2.55 billion.

Of particular note for a company famed for its maximalist approach to Bitcoin, Strategy also said it may sell up to $1.25 billion in BTC holdings if required to meet dividend or debt obligations.

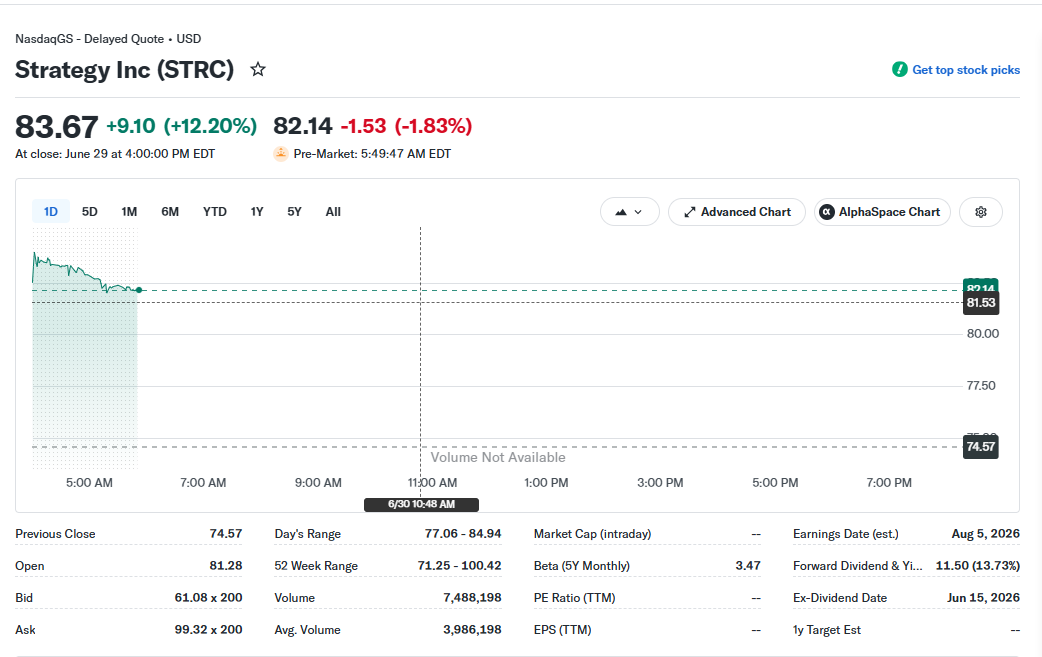

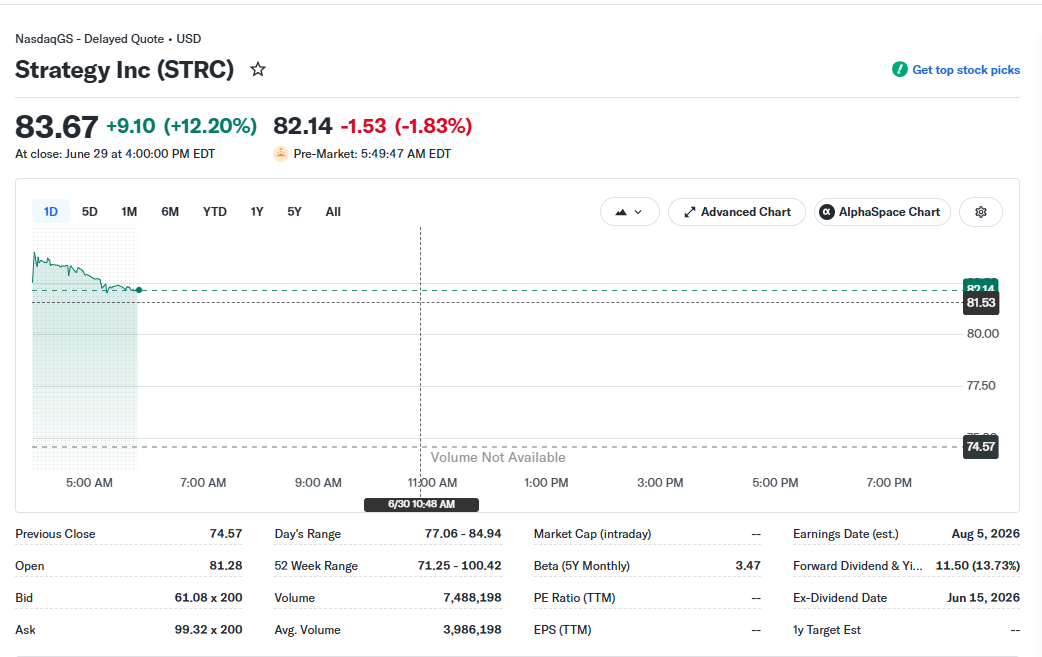

Markets responded positively to the news, with both STRC and MSTR shares rallying more than 12% in after-hours trading. STRC is currently trading at $84.86, a significant improvement on the $72.06 it was trading at on June 26.

STRC share price rallied by over 12% in after-hours trading. Source: Yahoo Finance.

But is the plan enough to assuage fears that STRC’s structure — famously cooked up by CEO Michael Saylor with the help of an LLM — could expose Strategy to a “death spiral” of reflexive funding risks during periods of market stress?

What is STRC and why is it controversial?

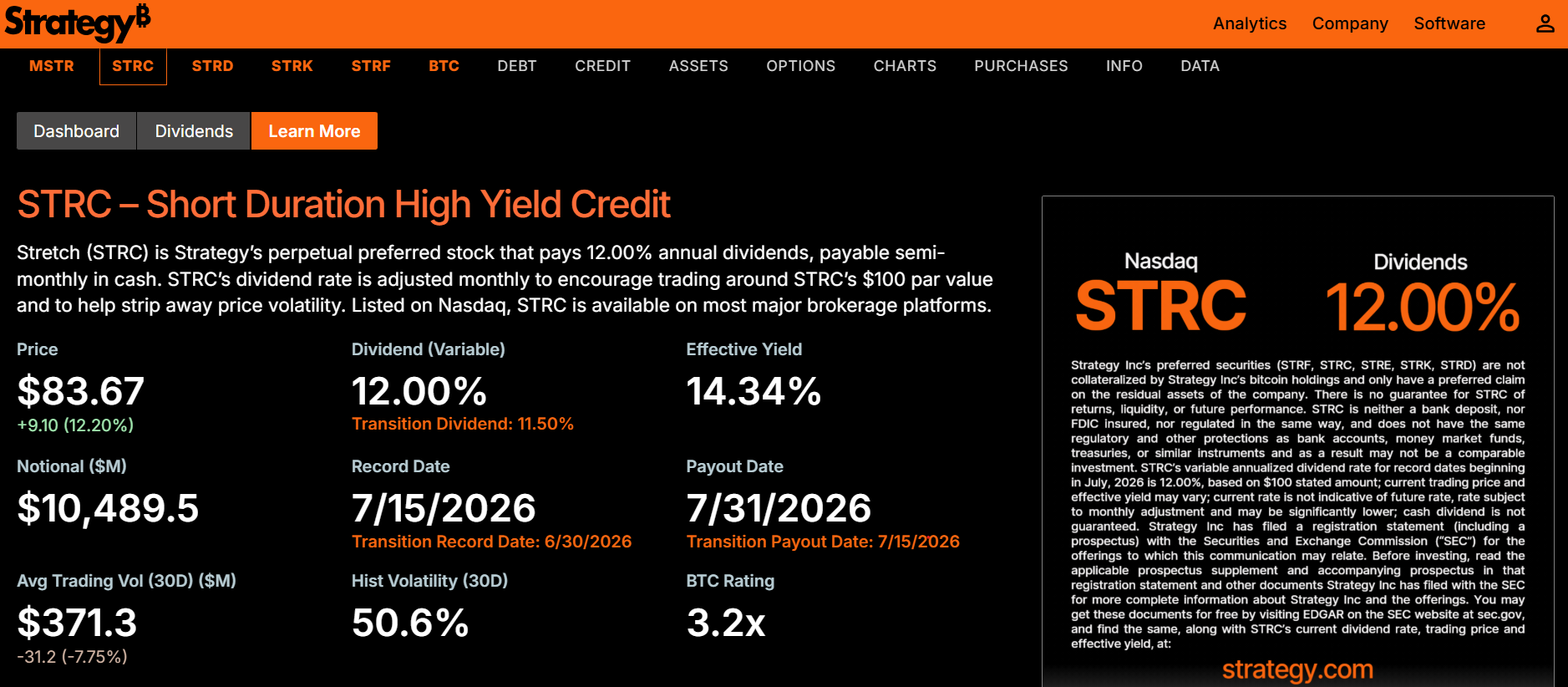

STRC is part of Strategy’s capital structure linked to its broader Bitcoin treasury strategy. It sits between traditional equity and debt-like instruments, offering investors yield while maintaining exposure to the company’s Bitcoin holdings.

Related: Strategy’s MSTR may plunge 80% if it repeats this dot-com-era fractal

Strategy describes STRC as a perpetual preferred stock paying a 12% annual dividend on a $100 par value, funded from its cash reserve and Bitcoin-linked capital framework.

While the structure is designed to provide financing flexibility without issuing traditional debt, analysts have questioned whether its stability depends on continued investor demand in secondary markets, particularly during periods of Bitcoin volatility or tighter liquidity conditions.

By contrast, Strategy’s common stock is called MSTR and it represents an equity ownership stake in Strategy along with voting rights. The fate of the two securities is closely aligned, but they are different. Similarly, Strategy’s position as the largest buyer of Bitcoin (and perhaps in future as a seller) means its fate is closely intertwined with the price of Bitcoin at present.

Perpetual goldbug and Bitcoin critic Peter Schiff has repeatedly called out Strategy’s model, pointing out that it “can’t sell Bitcoin without crashing the price of Bitcoin. Even if Strategy merely stops buying Bitcoin, that change alone would crush the market.”

Strategy describes STRC as a short-duration, high-yield credit. Source: Strategy

Yet Taran Dhillon, head of digital assets at Kula, told Cointelegraph that “Bitcoin volatility alone is unlikely to break a structure like Strategy’s.”

He said that a more meaningful test is “whether Bitcoin remains under pressure while access to capital becomes progressively more expensive or difficult.”

The Bear case: feedback loops and liquidity dependency

Some argue that Strategy’s entire fundraising and equity model is inherently reflexive, compounding both upside and downside cycles. The same flywheel that amplifies gains in bull markets can accelerate losses during the bear, when falling Bitcoin and share prices collide with weaker demand.

Ripple CEO Brad Garlinghouse made that exact point on CNBC this week. “Financial engineering does not drive long term value,” he said.

Kyle Rodda, senior analyst at Capital.com, told Cointelegraph that Strategy effectively operates as a momentum-driven Bitcoin accumulation vehicle, in which capital raises funds for Bitcoin purchases that, in turn, support the company’s valuation. However, he warned that the dynamic can reverse under stress.

“Strategy’s business definitely compounds momentum in both directions,” Rodda said, adding that in weaker conditions, rising funding costs and declining investor appetite can reinforce downward pressure.

Related: Grayscale’s Pandl says Strategy should sell $3B Bitcoin to restore confidence

He also argued that secondary market liquidity is a structural dependency, meaning large-scale selling or refinancing pressures could have wider spillovers into Bitcoin markets themselves.

Among Bitcoiners, Charles Edwards, the founder of Capriole Investments, is one of Strategy’s most hawkish commentators of late.

He compared stressed conditions in digital asset treasury companies to broader crypto deleveraging events, warning that feedback loops can accelerate losses when leverage and sentiment deteriorate.

“Anyone else getting LUNA 2022 vibes on MicroStrategy?” he posted on June 26.

Comparing Strategy to Terra/LUNA. Source: Charles Edwards

The neutral view: the real risk is funding markets, not Bitcoin

While the bearish sentiment around Strategy piles up on X, Dhillon told Cointelegraph that stress would likely first appear in funding conditions, pointing to widening discounts, higher yields, and reduced issuance capacity as early warning signals.

In his view, Strategy’s Bitcoin holdings are less relevant than whether the company can continue refinancing or rolling capital efficiently during periods of market stress.

And while failure of STRC to maintain its “peg” of $100 has caused much consternation, STRC isn’t pegged to $100 in the way a stablecoin is pegged to the value of $1. The yield simply gets more attractive the further the price falls under $100, which in theory, should see buyers push the price back to $100 at some point.

A Bitfire Research report shared with Cointelegraph said that STRC’s recent price dislocations should not be interpreted as structural failure.

The firm argued that de-pegging events are largely driven by sentiment and liquidity conditions rather than changes to Strategy’s underlying fundamentals or solvency profile.

“Strategy (formerly MicroStrategy) faces no near-term insolvency risk,” the firm wrote.

Bull case: stress is not insolvency

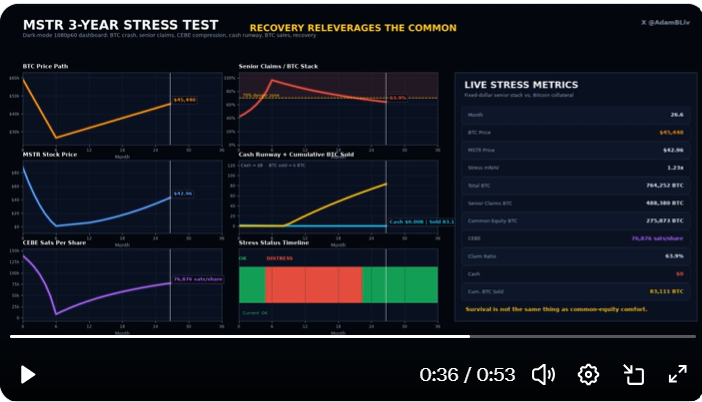

Strategy supporter Adam Livingston, a Bitcoin advocate and author, ran what he described as a “three-year MSTR stress test” under extreme conditions, including a 55% Bitcoin drawdown, closed capital markets, and sustained cash burn requiring large Bitcoin sales to meet obligations.

Related: CryptoQuant warns on Strategy’s dividend coverage as cash reserve falls 38%

In his model, Strategy’s senior claims expand sharply in Bitcoin terms, while the company’s “common equity Bitcoin exposure” (CEBE) compresses significantly. He described this as “CEBE getting annihilated”, falling from 138,161 sats per share to 7,884 sats per share at the trough of the simulation.

Death spiral? This model says no. Source: Adam Livingston

The model assumes no new Bitcoin purchases or equity issuance during the downturn, with approximately 115,727 BTC sold over the three years to service obligations before stabilization conditions return.

Despite the severity of the drawdown, Livingston’s model ultimately shows Strategy surviving the cycle, ending with over 700,000 BTC remaining on its balance sheet and a recovering net asset structure once market conditions normalize.

What Strategy actually changed

The new framework represents the most explicit attempt yet by Strategy to address concerns around liquidity and reflexivity risk.

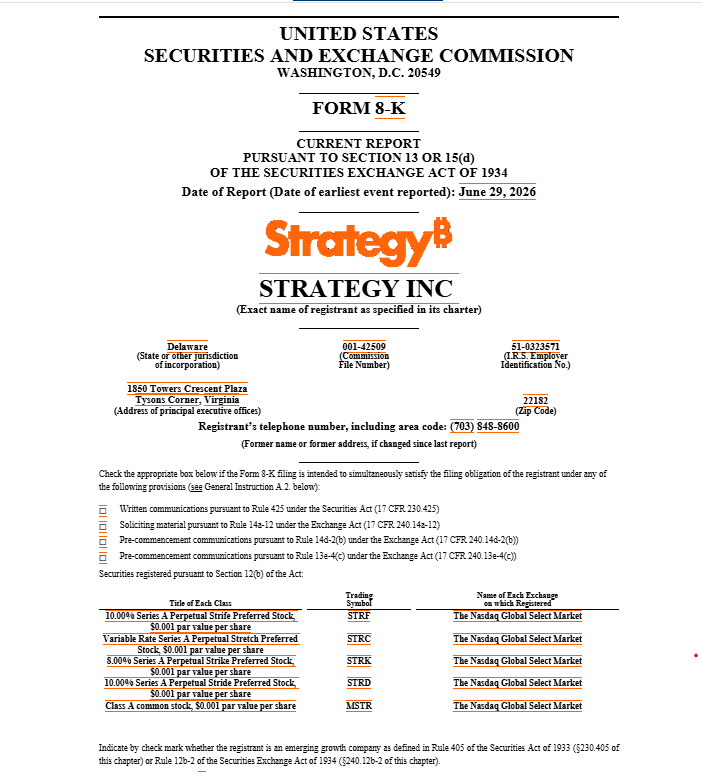

Key components of Strategy’s June 29 8-K filing that aim to restore confidence in the company, include buybacks for MSTR shares and STRC and a big focus on expanding cash reserves to pay dividends. The nuclear option of selling up to $1.25 billion in Bitcoin holdings to pay dividends is included partly as a way to assure markets Bitcoin maximalist Michael Saylor will reluctantly sell assets if he’s forced to.

Related: Bitcoin price is down over 40% since STRC launched: Is Strategy ‘fine’?

Strategy’s 8-K filing, June 29. Source: US Securities and Exchange Commission

Dhillon said the framework “meaningfully improves” transparency around how Strategy would respond under stress, with the expanded $2.55 billion reserve and clearer Bitcoin monetization plan helping strengthen investor confidence.

But Schiff pointed out that the current market cap of MSTR is $30 billion, while the current value of its Bitcoin is $50 billion. “Until MSTR’s market cap rises above the value of its Bitcoin, any Bitcoin bought by issuing MSTR shares creates a negative Bitcoin yield,” he said.

A stronger toolkit, same core bet

While the framework strengthens Strategy’s ability to manage short-term stress, it does not eliminate its reliance on capital markets to sustain its broader Bitcoin accumulation strategy.

As Dhillon told Cointelegraph, the key test will be whether funding conditions remain accessible during periods of market stress, rather than Bitcoin price action alone.

He added that the update clarifies Strategy’s capital allocation playbook, and gives management a more defined order of operations, which makes its overall strategy more credible.

For critics like Rodda, the underlying concern persists. Strategy’s structure remains exposed to feedback loops if liquidity tightens across both equity and credit markets.

While Strategy’s move introduces clearer liquidity buffers, buybacks, and contingency options, including potential Bitcoin sales, the debate over structural reflexivity has not yet been fully resolved.

The question now is not whether STRC is inherently fragile in theory, but whether Strategy’s expanded toolkit can withstand a prolonged period of capital market stress, and whether investors still want exposure to a vehicle that amplifies Bitcoin’s cycles and adds risk, rather than simply tracking them.

Magazine: Bitcoin will not hit $1M by 2030, says veteran trader Peter Brandt

The U.S. Commerce Department would have more authority to shield domestic artificial intelligence technology from the supply chains of foreign adversaries in a bill introduced Tuesday by two Republican senators who’ve been at the center of crypto legislation in this congressional session: Tim Scott and Bill Hagerty.

The new bill would give Commerce the ability to block “transactions involving technology designed, developed, manufactured, or supplied by persons owned, controlled, or directed by foreign adversary countries.” But it’s being pushed by the two Republicans as this session of Congress is winding toward the summer break and midterm elections, leaving it little opportunity to advance unless it’s later latched onto a must-move bill.

“Americans should not have to worry that China or Russia can use the technology in our cars, phones, or networks against us,” said Scott, the chairman of the Senate Banking Committee, who worked with Hagerty to pass last year’s Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act.

Strategy’s recently updated capital framework—allowing the company to raise funds through potential Bitcoin sales—has drawn support from parts of Wall Street even as prominent industry figures questioned whether the change truly strengthens Strategy’s long-term Bitcoin thesis.

On Monday, Benchmark Equity Research reiterated a Buy rating on Strategy’s Class A shares (MSTR) and kept a $570 12-month price target, according to a report reviewed by Cointelegraph. Strategy’s MSTR stock rose about 12.6% to roughly $92.70, while its STRC preferred shares climbed around 12.2% to about $83.70, based on figures cited by TradingView and Yahoo Finance. In Tuesday’s premarket trading, however, both names slipped as skepticism persisted about the durability and implications of the new framework.

Key takeaways

- Benchmark reaffirmed a Buy rating for Strategy’s MSTR and maintained a $570 12-month price target after the company disclosed a revised capital framework.

- Under the update, Strategy authorized potential Bitcoin sales of up to $1.25 billion to raise capital rather than relying solely on equity or debt.

- The approved sale capacity is estimated at about 21,082 BTC, roughly 2.5% of Strategy’s stated 847,363 BTC holdings, according to CoinGecko-linked figures in the reporting.

- Supporters view the shift as a move toward active balance-sheet management; critics argue it may not resolve a perceived market “overhang” and could undermine long-term credibility.

- Strategy has sold Bitcoin before, including a small 2026 sale and a larger 2022 sale tied to a tax-related transaction strategy that was later followed by repurchases.

How Strategy’s capital framework shifted

The core change is the authorization of potential Bitcoin (BTC) sales of up to $1.25 billion. Rather than depending exclusively on issuing additional stock or taking on debt, Strategy can use sales as one capital-raising lever, according to the company’s update referenced by Cointelegraph in earlier coverage: Strategy capital framework preserves Bitcoin exposure.

CoinGecko-linked calculations cited in the reporting place the $1.25 billion ceiling at approximately 21,082 BTC at current prices. That amount is described as about 2.5% of Strategy’s total holdings of 847,363 BTC, based on figures referenced alongside Cointelegraph’s earlier reporting: Strategy’s reserve and BTC accumulation coverage.

Support: more flexibility, less “one-way” exposure

Benchmark’s assessment emphasized that the update addresses concerns investors had raised during a period of heightened volatility. In the firm’s view, the changes provide more flexibility in how Strategy manages its capital structure.

Benchmark’s analysts characterized the shift as transforming Strategy from a “one-way” accumulation vehicle into an active manager that can adjust both sides of its balance sheet—something they called a meaningful positive for shareholders. Benchmark’s report, reviewed by Cointelegraph, argues that the framework gives investors a clearer view of how the company can respond as market conditions evolve.

That interpretation resonated with at least some individual market participants. Investor Simon Dedic suggested the move could represent a local bottom in sentiment around Strategy, implying that earlier fears about the company’s structure may have been overstated. Dedic also proposed that some selling pressure may have been linked to expectations that Strategy was preparing liquidity ahead of the framework update.

What skeptics fear: credibility and market “overhang”

Not all reactions were positive. Trader and investor Scott Melker said the framework appears aligned with what investors have pushed for—such as building a larger cash reserve and adopting a more flexible capital plan—but he cautioned that only time will tell whether the changes genuinely restore confidence.

Melker’s point reflects a key tension in the Strategy debate: even if flexibility reduces the risk of abrupt financial constraints, investors may still worry about whether flexibility translates into sustained belief that Strategy remains primarily a long-term Bitcoin accumulator. The concern is particularly sharp because Strategy has been one of the market’s major Bitcoin buyers.

Arca chief investment officer Jeff Dorman framed the issue differently, arguing that Strategy may need to sell roughly $2 billion to $3 billion worth of Bitcoin to remove a “constant overhang” he associates with the company’s market presence. In other words, the authorization threshold may not be enough—if investors perceive that selling must be large and sustained enough to meaningfully change market dynamics.

Ripple CEO Brad Garlinghouse added another layer to the criticism, saying that “financial engineering doesn’t drive long-term value.” In remarks shared in his public commentary and on CNBC’s “Squawk on the Street,” Garlinghouse argued that Michael Saylor’s team was not focused on what he considers the “right stuff” and that the strategy had hurt the broader market.

Strategy has sold Bitcoin before—so what’s actually new?

The debate is complicated by the fact that Strategy is not new to Bitcoin sales. The reporting points to a small sale in May 2026—selling 32 BTC for $2.5 million—and to an earlier transaction in 2022 in which the company sold 704 BTC as part of a tax-related transaction strategy before later repurchasing a similar amount of Bitcoin, according to an SEC filing cited in the original text: SEC archive.

What appears new in this latest framework is not the fact of potential sales, but the explicit scale and authorization of BTC sales up to $1.25 billion as a capital tool. That distinction matters for traders and long-term holders because the size and repeatability of potential sales affect expectations—whether Strategy is merely managing isolated liquidity needs or signaling a more systematic willingness to monetize Bitcoin under certain circumstances.

Where investors should look next

What will determine whether the framework strengthens Strategy’s case is how the company actually uses (or avoids using) the authorized sale capacity, and whether market participants update their expectations for how much Bitcoin supply could reach the market if conditions deteriorate. Until there’s clearer evidence from subsequent capital actions, skepticism and support are likely to remain split along the same fault line: flexibility versus the durability of a “long-term buyer” narrative.

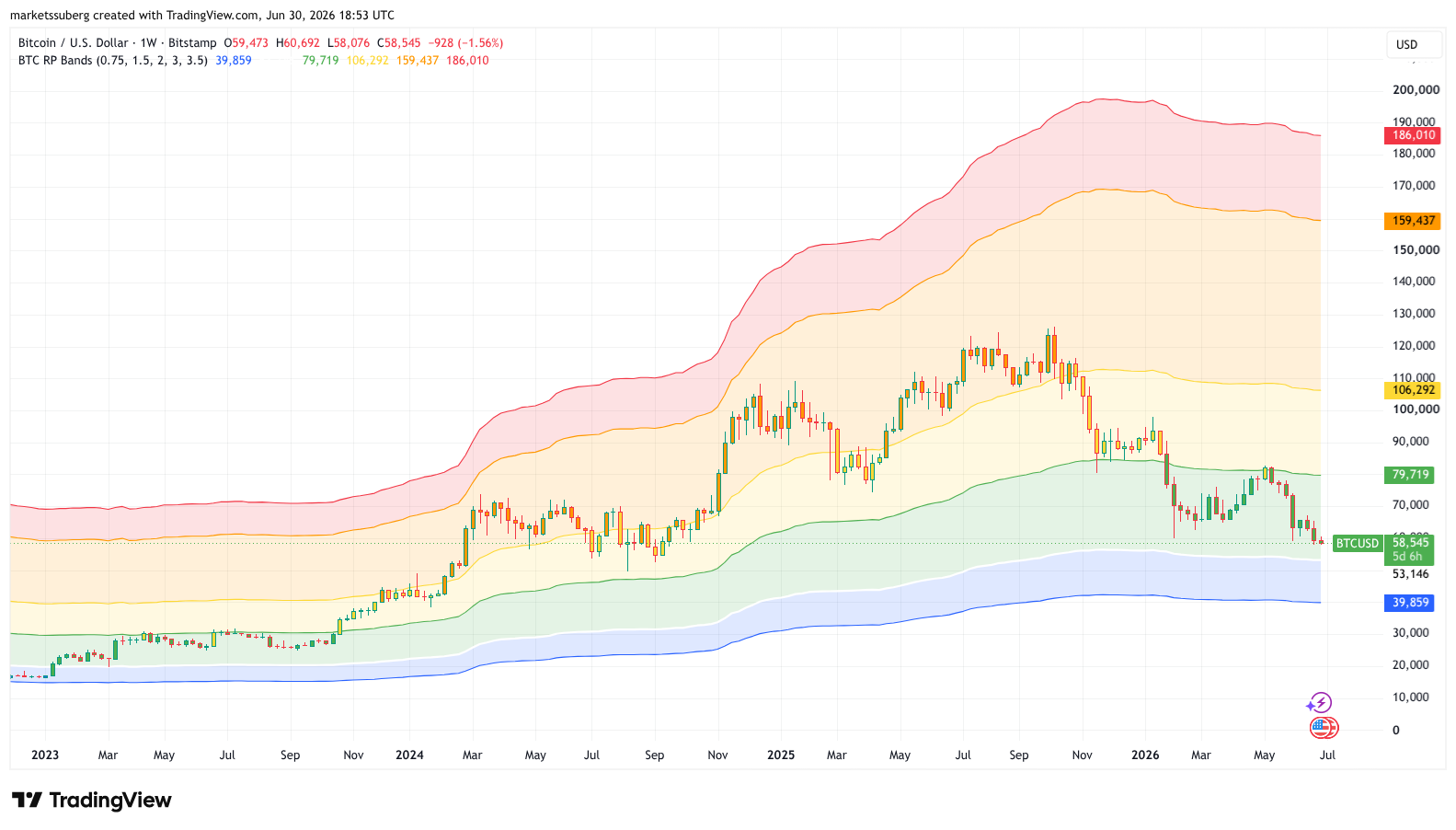

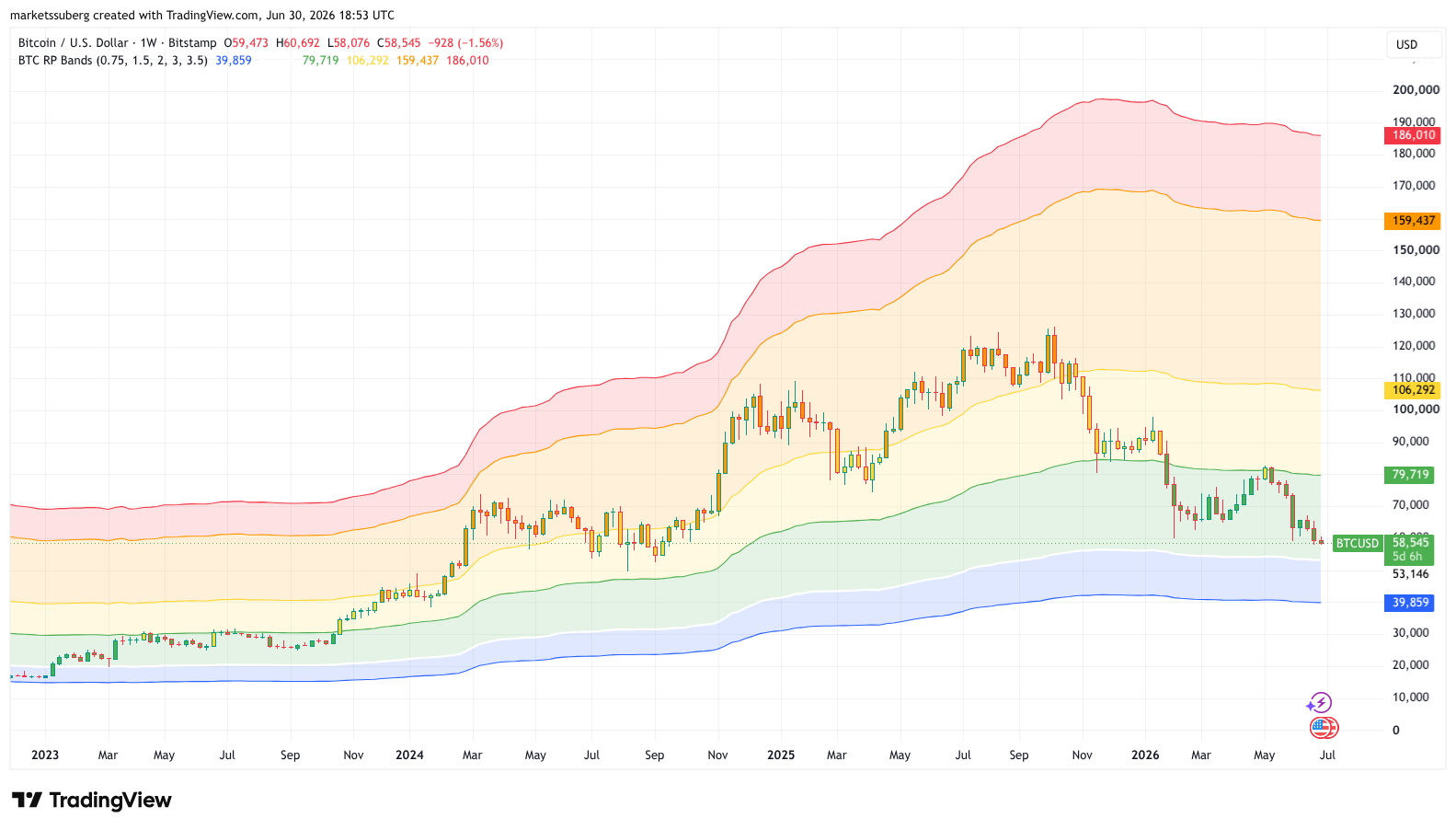

Bitcoin (BTC) is fast approaching a buying level that analysts describe as a top “investment opportunity.”

Key points:

- Bitcoin only needs to dip another $5,000 to hit a buy-in level that has always marked the bear-market bottom zone.

- This “best” area to invest is now on the radar of traders and analysts alike.

- PlanB describes a return below the level as “likely” during the 2026 bear market.

BTC price nears a classic bear-market buy-in zone

Data from onchain analytics platform CryptoQuant shows that BTC/USD is less than 10% away from its aggregate realized price.

Realized price is the average price at which the BTC supply last moved onchain, and currently sits at around $53,300. BTC/USD has not traded below it since the end of its last bear market in 2022, according to data from TradingView.

“Looking back, every recurring bear market has brought a bleak period when Bitcoin fell below its realized price, and that has been the best Bitcoin investment opportunity,” CryptoQuant contributor Crypto Sunmoon commented.

BTC/USD one-week chart with realized price data. Source: Cointelegraph/TradingView

Realized price comes in various iterations, reflecting the aggregate cost basis of various Bitcoin investor cohorts.

Market participants, however, are eagerly awaiting the return of the broader cost basis, given its role as a potential bear-market bottom marker.

“If that moment comes again, where price falls below the realized price, invest for the new cycle,” CryptoQuant suggested.

Bitcoin will “likely” fall under realized price

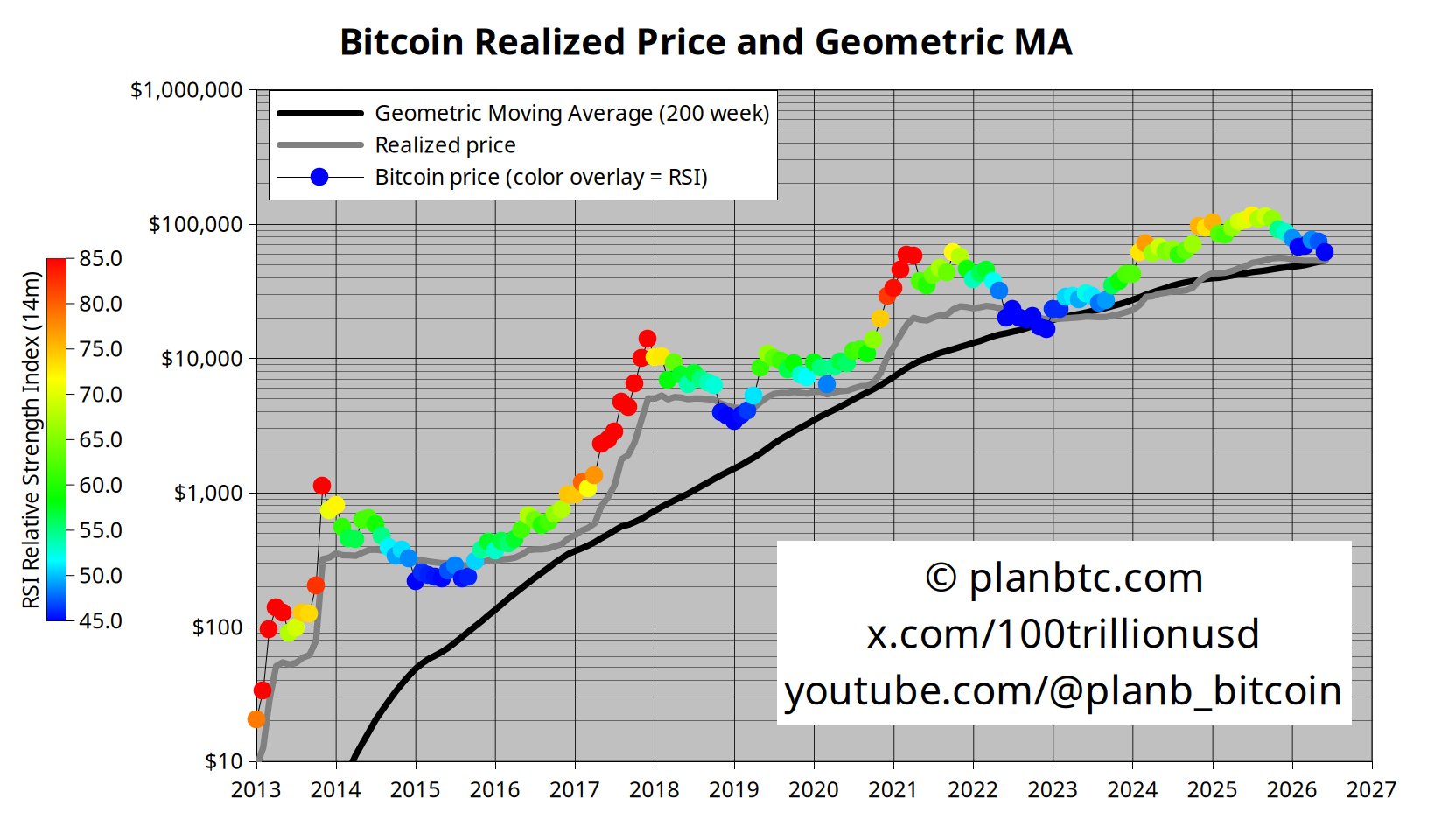

In recent months, PlanB, the pseudonymous creator of the Stock-to-Flow BTC price models, has listed a drop below the realized price as one of two key conditions that must be met to secure a trend reversal.

Related: Bitcoin price risks drop below $58K as US dollar hits 40-year high against yen

The other, closing candles below the 200-week moving average (WMA), began several weeks ago.

“Market is 50/50 on if February $60k was the bottom, or the bear will continue,” he wrote in an X post at the start of June.

“IMO data is telling us that we have not seen bottom formation yet, and that there is a >50% probablility that we go lower (below 200wma $61k or realized price $53k).”

Bitcoin realized price data. Source: PlanB/X

In a later post, PlanB added that Bitcoin would “likely bottom below” the realized price.

Continuing on realized price, commentator Aaron Bennett said that a drop to the key level was still possible despite the presence of institutional holders who were absent from previous bear markets.

“I’d be surprised if we don’t touch this, or go below it for a few weeks,” he told X followers last week.

Bittensor cut its emissions in half in December, and roughly 70% of the supply is locked in staking. The supply side looks tight, but a halving only moves price if demand shows up to meet it.

Summary

- Bittensor (TAO) ran its first halving on Dec. 12, 2025, cutting daily emissions from 7,200 to 3,600 TAO against a fixed 21 million cap, the same hard-cap design Bitcoin uses.

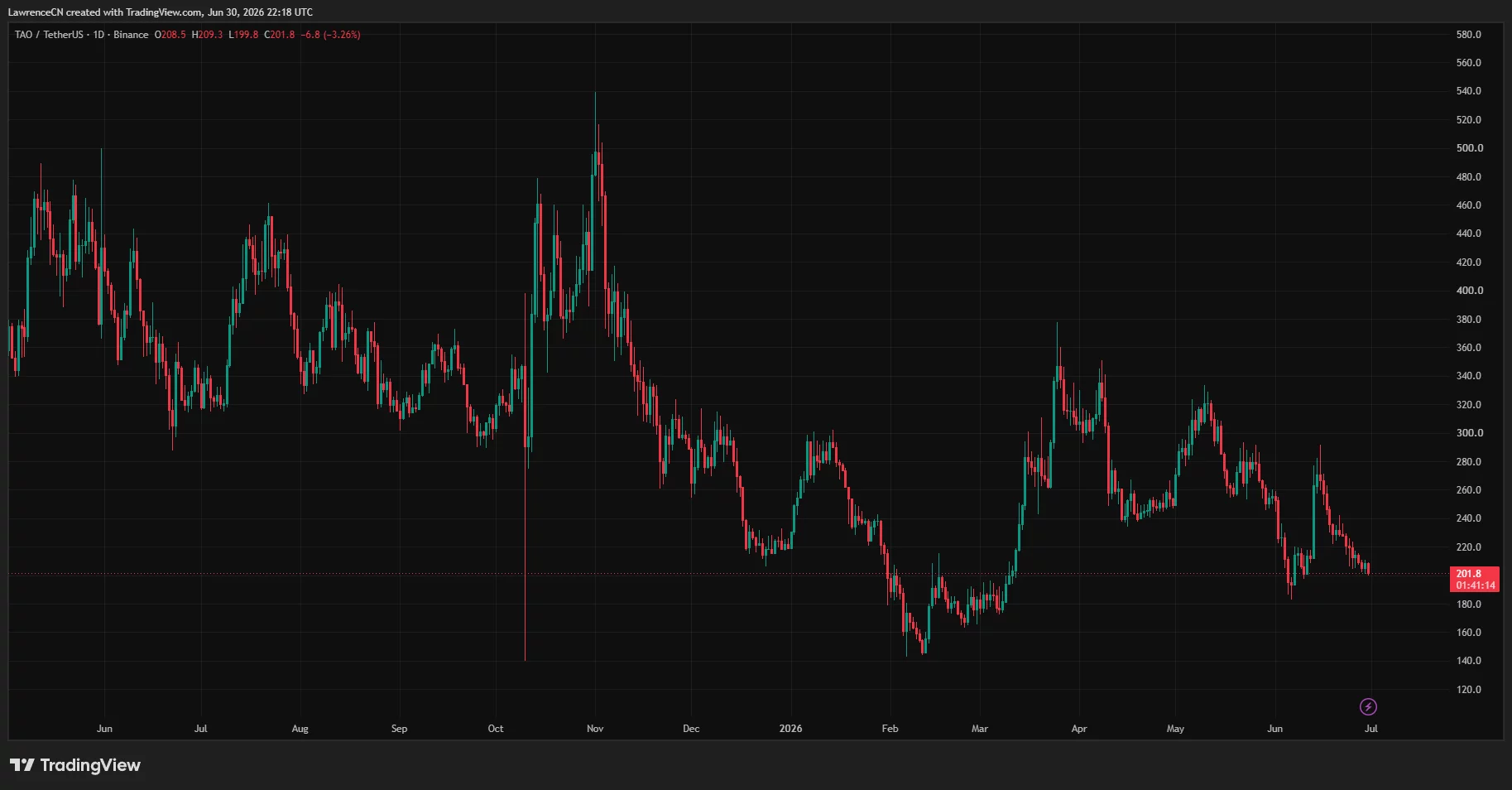

- TAO trades near $250 as of late June 2026, roughly 65% below its early-2024 record near $757, ranked around #27 to #37 with a market cap close to $3 billion and only about 11 million tokens in circulation.

- The bull case rests on a tightening float: with around 70% of supply staked for roughly 10% yield, the halved emissions slowly thin out sell-side pressure, which can lift price if demand holds or grows.

- The bear case is that a halving is a supply event the market already knew about, and TAO’s real problem is proving its subnets capture lasting value instead of riding AI-narrative momentum that fades.

- Analyst forecasts for 2026 run wide, from Gate near a $236 average to Coinpedia eyeing a $500 reclaim, with the outcome hinging on subnet revenue, ETF flows, and the broader AI trade more than on the halving alone.

Bittensor’s first halving is already in the past. It happened on Dec. 12, 2025, and the daily issuance of TAO dropped from 7,200 tokens to 3,600 overnight. So the live question for 2026 is not whether the halving will happen. It is what a halving actually does to a token whose price sits 65% below its record, whose technical picture is bearish, and whose deeper story is still unproven. The supply math is real. Whether it matters depends on demand, and that is the harder part of the forecast.

This piece walks through how the Bittensor halving works, why a supply cut takes months to filter into the market, the demand-side question the halving does not answer, what the charts say at current levels, the institutional wildcard around a possible spot ETF, and where analysts think TAO could trade in 2026. It closes with bull, base, and bear scenarios and a short FAQ.

How the Bittensor halving actually works

Bittensor is an open marketplace for machine intelligence. Models, compute, and data compete inside specialized markets called subnets, and the network scores their output through a mechanism known as Yuma Consensus.

TAO is the settlement token that pays for useful work and secures the network through staking. The protocol was started in 2019 by AI researchers Ala Shaabana and Jacob Steeves, and its token design borrows directly from Bitcoin: a fixed cap of 21 million coins and a halving schedule that cuts new issuance over time.

The December 2025 halving was the first of these events. Daily emissions fell from 7,200 TAO to 3,600. In plain terms, the network now mints half as much new TAO each day as it did before. Miners and validators who earn TAO for their contributions receive a smaller flow of new tokens, which over time means less fresh supply hitting the market. The mechanism is the same logic that underpins Bitcoin halvings, where reduced issuance has historically preceded periods of price strength, though the cause and effect is never as clean as the charts make it look in hindsight.

The key difference between a halving in theory and a halving in practice is timing. Issuance dropped instantly on the halving date, but the effect on circulating supply is gradual. The tokens already in circulation do not disappear, and the slower drip of new supply only changes the balance of buyers and sellers over weeks and months, not in a single candle. That is why the halving is better understood as a structural shift in the background rather than a switch that flips price higher on the day.

Why the supply cut takes months to bite

The most important number for the supply thesis is not the emission rate. It is how much TAO is locked away and cannot be sold. Roughly 70% of the circulating supply is staked by validators and delegators, who earn an annual yield in the region of 10% for securing the network. Staked tokens are not idle, but they are also not sitting on exchange order books waiting to be dumped. That combination, halved emissions plus a high staking ratio, is what makes the Bittensor float look unusually thin compared with most tokens of similar size.

Here is the chain of logic the bulls lean on. New supply has been cut in half. A large majority of existing supply is staked and earning yield, so holders are paid to keep it locked. If demand for TAO stays flat or rises while the liquid, sellable float shrinks, the price pressure shifts upward over time. This is the classic supply-shock argument, and on paper it is coherent. With only about 11 million of the 21 million cap in circulation and most of that staked, the genuinely tradable supply is a fraction of the headline number.

The honest caveat is that supply shocks are slow and conditional. The phrase doing the heavy lifting is “if demand stays flat or rises.” Reduced emissions cannot lift a price by themselves if buyers walk away faster than sellers do. Through the first half of 2026, that is roughly what happened: TAO slid toward $200 in early June before rebounding, even though the halving was months in the rearview mirror. The supply setup was already in place, and it did not stop the drawdown. The lesson is that the halving loads the spring, but something on the demand side has to pull the trigger.

The demand side the halving does not solve

This is the part of the forecast that actually decides where TAO goes, and it has nothing to do with the halving. Bittensor’s value depends on whether its subnets capture real, durable economic demand for machine intelligence, or whether TAO is mostly a high-beta proxy for AI enthusiasm that rises and falls with the narrative.

There is a real case to make. The subnet ecosystem has expanded past 120 active markets, each handling a specialized task such as inference, compute, data, or prediction. The network reported around $43 million in Q1 2026 revenue from AI services, which is a concrete sign that money is moving through the system instead of just speculation.

The Dynamic TAO, or dTAO, upgrade lets subnets allocate emissions based on real demand instead of fixed rewards, which is meant to price intelligence by the market and push Bittensor from a research project toward actual economic activity. The ambition is large: to be the settlement layer for intelligence itself, the place where models, compute, data, and incentives meet in one market.

The bear reading is that this is still unproven, and the network has shown it can break. In April 2026, a high-profile subnet exit triggered a roughly 25% price drop, exposing how much concentration and governance fragility sit underneath the optimistic story. The market punished the weak decentralization signal fast.

The deeper worry is value capture: even if subnets generate revenue, it is not yet clear how much of that value flows back to the TAO token itself rather than to the subnet operators or token holders downstream. An AI token can have busy subnets and still struggle to translate that activity into sustained token demand.

When AI excitement runs hot across the market, TAO tends to jump, and when attention rotates elsewhere, it tends to fade. That correlation is the bear case in one sentence: if TAO is mostly AI-hype beta, the halving will not save it.

What the charts say right now

At current levels near $250, TAO sits in a bearish-to-neutral technical posture. Through June, it traded below the cluster of 50-day, 100-day, and 200-day exponential moving averages sitting roughly between $256 and $270, which means the medium-term trend has been pointing down and that band overhead acts as resistance. Momentum readings have hovered in weak-to-neutral territory, with relative strength index values in the mid-30s to mid-50s depending on the day, not oversold enough to scream reversal and not strong enough to confirm one.

The levels traders watch are clear. On the downside, the $200 area has acted as a line in the sand through June, and a decisive break below it opens the door toward the February low near $163. On the upside, the first hurdle is reclaiming that $256 to $270 moving-average band, and above it the structure points toward $352 and then $396, the levels several analysts flag as the gateway to a larger move.

The longer-term chart frames the whole range: an accumulation floor around $160 to $200 and a distant ceiling near the $720 to $760 zone that produced the record in early 2024. TAO has cycled inside that channel before, finding demand at the lows and heavy profit-taking at the highs.

The takeaway from the charts is that TAO is not in a breakdown, but it is not in an uptrend either. It needs to reclaim its moving averages before the supply thesis gets any technical confirmation, and until it does, the halving narrative is a fundamental tailwind fighting a bearish trend.

The institutional wildcard

The most underpriced catalyst in the TAO forecast may be the one that has nothing to do with the chart. Grayscale filed an S-1 for a Bittensor trust on Dec. 30, 2025, and its Grayscale Bittensor Trust is already live over the counter, giving accredited investors a regulated wrapper for TAO exposure. Bitwise has also filed for a spot TAO product, with a U.S. regulatory decision expected around August 2026. The exact timing is not guaranteed, and approval is not certain, but the direction of travel matters.

The reason this is a wildcard rather than a sure thing is the corridor it opens. Once an asset is treated as ETF-eligible, it stops being dismissed as a pure speculation and starts being treated as infrastructure exposure that funds can hold without touching spot crypto directly. Bitcoin went through this in its earlier institutional phase, and Ethereum followed.

TAO is now entering the same corridor as the leading decentralized-AI asset. Anticipation alone can move price, because spot buyers tend to position early when future access looks credible.

There is a broader narrative tailwind too. When confidence in centralized AI wobbles, capital has flowed toward decentralized alternatives, and one such episode pushed an estimated $2.87 billion into AI crypto tokens inside a single week. TAO is the default beneficiary of that rotation given its position as the category leader by market cap. The flip side is that this same dependence on the AI narrative is exactly the fragility the bears point to: flows that arrive on a narrative can leave on one too.

What analysts forecast for TAO in 2026

Forecasts for TAO in 2026 span an enormous range, which is itself the honest signal: the outcome depends on variables no model can pin down. The figures below are third-party projections, presented as a spread of views, not as targets this publication endorses.

On the cautious end, Gate’s model centers 2026 around an average near $236, with a projected low close to $130 and a high around $318, essentially expecting TAO to hold near current levels with wide swings. Coindataflow’s experimental forecast sits in a similar low band, with a 2026 high near $281. In the middle and higher, Changelly’s analysis points to a 2026 range of roughly $388 to $472 with an average near $402, while Cryptopolitan’s technical read frames a $134 to $570 band with an average around $475.

Coinpedia takes a more constructive technical view, arguing that if TAO clears resistance at $352 and $396 in the 1st half of the year, the path opens toward a $500 reclaim. Looking further out, long-term projections from several of these firms cluster in a $900 to $3,000 range for 2030, premised on decentralized AI demand expanding and TAO holding its category lead.

The width of that spread, from a low near $130 to highs above $570 in the same year, is not a failure of analysis. It is an accurate reflection of how much hinges on whether subnet demand compounds, whether an ETF arrives, and whether the AI trade stays in favor. The halving sets the supply backdrop. These other forces decide the magnitude.

How the Bittensor halving compares with Bitcoin’s

The halving thesis borrows its emotional weight from Bitcoin, where four-year supply cuts have lined up with major bull runs. The comparison is useful, but it breaks down in ways that matter for the forecast. Bitcoin’s halving reduces the new supply paid to miners who secure a settlement network whose demand driver is, broadly, monetary: people want to hold Bitcoin as a store of value.

Bittensor’s halving reduces the new supply paid to miners and validators who produce and verify machine intelligence, and TAO’s demand driver is supposed to be usage of that intelligence through subnets. Those are different engines.

The practical consequence is that a Bittensor halving cannot lean on the same reflexive narrative. Bitcoin’s halvings work partly because a huge population of holders believes they work, which makes the belief partly self-fulfilling. TAO does not yet have that scale of conviction, and its price has shown it: the token fell after the December halving instead of rallying on it, because the AI-token market cared more about subnet performance and the broader risk environment than about a supply chart. The halving is real and structurally helpful, but anyone modeling TAO on a clean Bitcoin-style post-halving curve is importing an assumption the data has not yet earned.

There is also a proportionality difference. Bitcoin’s reduced issuance is a small fraction of its already-large circulating supply, so the supply effect is gradual while the narrative effect is immediate.

For TAO, the emission cut is proportionally larger against a much smaller circulating base, which should make the mechanical supply effect more potent over time, yet the narrative effect is weaker because fewer participants treat the halving as gospel. The net is a token where the fundamentals of the halving may matter more than they do for Bitcoin, while the storytelling matters less.

The deeper design point sits underneath all of this. Bittensor was built by Ala Shaabana and Jacob Steeves in 2019 around Yuma Consensus, the mechanism that scores and rewards useful machine-intelligence work. That design is what lets the network claim it pays for output instead of raw hardware uptime, and it is the foundation of the value-capture argument. The halving sharpens the supply side of that design, but it does not resolve whether the scoring turns into durable token demand, which remains the open question the price keeps asking.

What to watch through the rest of 2026

For readers tracking TAO instead of chasing headlines, a short list of signals will reveal which scenario is unfolding well before the price confirms it. The first is subnet revenue: the roughly $43 million reported for the first quarter is the number to watch for growth, because rising real revenue is the strongest evidence that the value-capture story is working instead of stalling. The Second is the moving-average band between $256 and $270; reclaiming and holding above it would be the first technical sign the bearish trend has turned.

The third is the ETF timeline, with a U.S. decision expected around August 2026. An approval, or even rising odds of one, would open the institutional corridor the bull case needs, while a denial or a delay removes a catalyst the market has started to anticipate.

The fourth is governance stability: after the April subnet exit that triggered a 25% drop, any repeat of concentration or governance trouble would confirm the fragility the bears emphasize and could undo months of recovery in days. The fifth is the health of the broader AI trade, since TAO has behaved as a high-beta proxy for AI sentiment, and a rotation out of AI tokens would pressure it regardless of its own progress.

Watched together, these five tell a more reliable story than any single price target. If subnet revenue climbs, the moving averages flip, and the ETF path advances, the supply setup from the halving finally has demand to work with, and the bull case gains real footing. If revenue stalls, governance wobbles, and the AI trade cools, the thin float will amplify the downside instead of cushioning it. The halving set the stage in December. These signals decide whether anyone shows up to use it.

Bull, base, and bear scenarios for TAO

The scenarios below combine the supply setup with the demand and institutional variables that actually drive the outcome. They are illustrative ranges built from the third-party forecasts above and current market structure, not guarantees.

Bull case

In the bull scenario, the halving thesis works as designed and demand shows up to meet the tightening float. Subnet revenue keeps climbing from the $43 million Q1 pace, dTAO routes emissions toward markets with real usage, and the value-capture question starts to resolve in TAO’s favor. A spot ETF decision lands favorably or looks likely, pulling regulated capital into a thin float where roughly 70% of supply is staked and out of reach. TAO reclaims the $256 to $270 moving-average band, breaks $352 and $396, and runs toward the $500 area that Coinpedia and others flag, with the more aggressive long-term models pointing higher into 2027 if the AI trade stays hot. This case depends on the AI narrative staying strong and the network avoiding another governance shock.

Base case

In the base scenario, the halving slowly does its quiet work but no single catalyst fires hard. Subnet activity grows unevenly, the ETF path advances but without a clean approval inside 2026, and the AI trade runs warm instead of euphoric. TAO spends the year chopping inside its broad trading channel, roughly between the $200 floor and the low-$400s, with the average landing near the $236 to $402 zone that the Gate and Changelly models bracket. The thin float keeps downside contained on dips, but the unproven value-capture story caps rallies. This is the “constructive but unconfirmed” outcome where the supply setup helps at the margin without overpowering a cautious market.

Bear case

In the bear scenario, the halving is revealed as a supply event the market already priced, and TAO behaves as AI-hype beta. The value-capture question stays unanswered, another subnet exit or governance dispute dents confidence the way April’s did, and the broader AI trade rotates out. TAO loses the $200 floor and slides toward the February low near $163 or lower, with the bearish low-end forecasts near $130 coming into view. In this case, the staking lockup offers little protection, because holders unwind positions when yield no longer offsets falling token value, and the thin float that amplifies rallies amplifies declines just as efficiently.

Frequently Asked Questions

When was the Bittensor halving and what changed?

The first Bittensor halving took place on Dec. 12, 2025. Daily TAO emissions were cut in half, from 7,200 tokens to 3,600. The network follows a Bitcoin-style design with a fixed 21 million supply cap, so issuance steps down over time. The supply effect is gradual, filtering into circulating supply over months instead of moving price on the halving date itself.

Does a halving guarantee TAO goes up?

No. A halving reduces the rate of new supply, which can support price if demand holds or grows, but it cannot lift a token on its own. TAO slid toward $200 in the months after the December halving before rebounding, which shows that reduced emissions do not override weak demand or a bearish trend. The halving loads the supply side, but demand has to do the rest.

Why is roughly 70% of TAO staked, and why does it matter?

Holders stake TAO to help secure the network through validators and delegators, and they earn an annual yield around 10% for doing so. Staked tokens are locked and not readily available to sell, which thins the liquid float. Combined with halved emissions, the high staking ratio is the core of the supply-shock argument, since it shrinks the genuinely sellable supply.

What is the biggest risk to the TAO forecast?

The biggest risk is that TAO is valued mostly on AI-narrative momentum instead of durable demand for its subnets. The subnet ecosystem generates revenue, but how much value flows back to the TAO token is unproven, and a high-profile subnet exit in April 2026 triggered a roughly 25% drop. If the AI trade cools or governance fragility resurfaces, the supply setup will not protect the price.

Could a spot TAO ETF change the picture?

Possibly. Grayscale’s Bittensor Trust is already live over the counter, Grayscale filed an S-1, and Bitwise has filed for a spot product, with a U.S. decision expected around August 2026. A favorable outcome would open a regulated channel for institutional capital into a thin float, which the bull case leans on. Approval and timing are not guaranteed, so it remains a catalyst to watch instead of a certainty.

Where do analysts think TAO could trade in 2026?

Third-party forecasts span a wide range. Cautious models such as Gate center near a $236 average with a low around $130, while higher views from Changelly and Cryptopolitan point to averages around $400 to $475 and Coinpedia flags a possible $500 reclaim if key resistance breaks. Long-term 2030 projections from several firms cluster between $900 and $3,000. The spread reflects genuine uncertainty about subnet demand, ETF flows, and the AI trade.

Disclaimer: This article is for information purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency prices are highly volatile, and price predictions are speculative estimates that may not occur. Nothing here is a recommendation to buy or sell any asset. Always do your own research and consider consulting a licensed professional before making financial decisions. Figures are accurate as of June 30, 2026, and will change.

Crypto World

Banks Won’t Open Accounts For AI Agents So 100 Billion Bots Will Live On Crypto Instead

Everyone’s debating whether humans will adopt crypto. Nobody’s talking about the actual adoption wave already happening: machines.

The Adoption Story Everyone’s Got Wrong

For fifteen years, the crypto industry has obsessed over one question: when will humans adopt crypto en masse?

Wrong question.

Animoca co-founder Yat Siu just pointed out something far more consequential: banks won’t open accounts for AI agents. So somewhere between 50 and 100 billion bots will operate on crypto wallets and stablecoins instead.

Not humans. Machines.

This isn’t a future prediction. This is already happening. And it changes the entire premise of what “crypto adoption” actually means.

Why Banks Can’t Serve AI Agents

Think about what opening a bank account requires: identity verification, legal personhood, a Social Security number or equivalent, a physical address, a human signature, regulatory compliance frameworks built around individual humans or registered legal entities.

An AI agent has none of this. It’s not a person. It’s not (yet) a recognized legal entity in most jurisdictions. It doesn’t have a passport. It doesn’t have a fixed address. It might exist as code running across distributed servers with no single point of identity.

Traditional banking infrastructure simply wasn’t built for this. KYC (Know Your Customer) protocols assume a customer who is, definitionally, a human or a registered company. An autonomous AI agent breaks that assumption completely.

So when AI agents need to transact, pay for compute, pay other agents for services, settle accounts, manage budgets, they literally cannot use a bank account. The infrastructure doesn’t exist. The regulatory framework doesn’t exist. The bank wouldn’t even know who to call if something went wrong.

Why Crypto Solves This By Accident

Crypto wallets don’t require identity verification at the protocol level. A wallet is just a cryptographic key pair. No bank manager has to approve it. No KYC process has to validate a human behind it.

This was originally designed for human privacy and censorship resistance. Nobody built crypto wallets specifically for AI agents.

But the architecture happens to solve exactly the problem AI agents have: it allows any entity, human or machine, to hold and transfer value without needing institutional approval of its identity.

Stablecoins compound this. They’re programmable, instantly transferable, and don’t require the agent to navigate currency conversion or cross-border banking friction. An AI agent in any jurisdiction can hold USDC and transact with another AI agent anywhere else, instantly, without a bank in the loop.

This wasn’t crypto’s intended use case. It’s becoming crypto’s accidental killer app.

What “100 Billion Bots” Actually Means

Let’s sit with that number for a second.

100 billion is roughly 12x the world’s human population. If even a fraction of projected AI agent deployment happens, agents handling customer service, executing trades, managing supply chains, negotiating contracts, paying for API calls, settling micro-transactions between other agents, the volume of machine-to-machine value transfer could dwarf human transaction volume entirely.

Every agent that needs to pay another agent for a service, every agent that needs to pay for compute resources, every agent that needs to settle a transaction on behalf of the human or company it serves, all of that needs rails. And those rails can’t run through traditional banking because traditional banking wasn’t built to onboard a machine as a customer.

So the rails being built right now are crypto rails: wallets, stablecoins, on-chain settlement, smart contracts that execute agent-to-agent agreements without human intervention.

The Real Story Nobody’s Telling

The crypto industry spent a decade trying to convince retail users that Bitcoin would replace cash. It didn’t work the way they hoped. Volatility scared people off. Complexity scared people off. Most humans still prefer their bank app.

But while everyone was trying to convert grandma into a crypto user, an entirely different category of user emerged that doesn’t care about volatility, doesn’t get confused by seed phrases, doesn’t need a friendly UI, and doesn’t have the emotional hangups humans have about money.

AI agents don’t panic-sell. They don’t get scared by red candles. They don’t need education about “not your keys, not your coins.” They just need programmatic access to value transfer that doesn’t require a bank’s permission.

Crypto, it turns out, might be a far better fit for machine commerce than human commerce.

Who’s Already Building For This

This isn’t speculative anymore. The infrastructure race is underway.

Coinbase’s “Coinbase for Agents” platform lets AI agents execute crypto trades and payments autonomously. Whatever the risks (and there are real ones, as I wrote about previously), the demand signal is clear: someone built this because agents need it.

A new venture called t54, founded by an ex-Ripple engineer and backed by Ripple and Franklin Templeton, is building a trust layer specifically to verify and insure AI agents that spend money autonomously. That’s not a hypothetical product. That’s $5 million in funding chasing a problem that exists today: how do you trust an autonomous agent with financial authority?

Stablecoin infrastructure is being explicitly redesigned around agent-to-agent payments, not just human remittances or trading.

This is an arms race nobody’s covering with the seriousness it deserves, because it’s not as exciting as a token price chart.

The Implications Are Bigger Than Crypto

If AI agents become primary economic actors, negotiating, paying, settling, transacting at machine speed and machine scale, the implications go well beyond whether Bitcoin hits a new all-time high.

Regulatory frameworks built for humans will need to expand to cover non-human economic actors. Who’s liable when an AI agent commits fraud, makes an error, or gets hacked mid-transaction? Existing law doesn’t have clean answers, because existing law assumes a human or a registered company is on the other side of every transaction.

Trust and verification become the actual product, not the transaction itself. When humans transact, identity and reputation are partially handled by institutions (banks, governments, credit bureaus). When agents transact, that entire trust layer has to be rebuilt from scratch on-chain.

Economic activity could scale beyond what any human institution monitors in real-time. If 100 billion agents are transacting, the volume and speed of that activity will exceed what any regulator, bank compliance team, or auditor can review using current methods.

This is the actual frontier. Not “will retail adopt Bitcoin.” It’s “what happens when the majority of economic transactions on a blockchain aren’t initiated by a human at all.”

Why This Should Worry You (A Little)

Every wave of financial infrastructure built without adequate oversight eventually creates a crisis. The 2008 financial crisis happened partly because complex financial instruments outpaced regulatory understanding. Algorithmic trading caused multiple flash crashes because automated systems moved faster than human circuit breakers could respond.

Now we’re building financial rails specifically because traditional, regulated banking infrastructure refuses to onboard the new class of economic actor. That refusal isn’t banks being lazy. It’s banks correctly identifying that they don’t have a framework for verifying, insuring, or holding accountable a non-human customer.

So the activity moves to an environment with even less oversight: crypto rails, where verification is optional, accountability is unclear, and the volume could eventually dwarf anything traditional finance has dealt with.

That’s not necessarily catastrophic. But it’s not nothing either.

The Question Nobody’s Answering

If 100 billion AI agents are transacting on crypto rails, processing value at a scale that exceeds human economic activity, who exactly is responsible when something goes wrong at that scale?

Not “which agent made the bad trade.” The systemic question: who governs an economy where the majority of participants aren’t human, aren’t legally accountable in any traditional sense, and exist as code that can be duplicated, modified, or shut down without the due process we’ve built around human economic actors?

Nobody has a good answer yet. Because until recently, nobody thought this was the actual adoption story.

What This Means For Crypto’s Future

Crypto spent years trying to be money for people. It might end up being money for machines instead.

That’s a stranger, less romantic story than “the people’s currency” or “the future of finance for everyone.” But it might be the more accurate one.

The next decade of crypto’s relevance may not be determined by whether your aunt buys Bitcoin. It may be determined by how many AI agents need a wallet, how fast they transact, and whether anyone builds the accountability infrastructure before the volume becomes unmanageable.

100 billion bots are coming. The rails are already being built. And almost nobody is asking the right questions about what happens next.

If AI agents become the majority of economic activity on crypto rails, should they have the same legal accountability as humans? Or do we need an entirely new framework? Drop your take.

Bitcoin is drawing fresh attention from onchain analysts as it edges toward a frequently cited “buy-in” threshold near realized price—an area that has historically aligned with bear-market bottoming windows. According to onchain data referenced by CryptoQuant, BTC/USD is now less than 10% away from its aggregate realized price, currently around $53,300.

While realized price is not a guarantee of timing or outcomes, the current proximity is prompting traders to watch for a move below that cost-basis marker. Pseudonymous modeler PlanB has also argued that a break under realized price remains a plausible route to completing a bottom process, alongside another widely tracked trend condition.

Key takeaways

- CryptoQuant data indicates BTC/USD is within roughly 10% of realized price (about $53,300), a level that has previously marked a recurring bear-market opportunity.

- Realized price has not been breached by BTC/USD since the end of the 2022 bear market, based on TradingView data cited in the analysis.

- PlanB has highlighted two conditions for trend reversal—one involving candles closing below the 200-week moving average, and another involving a move below realized price.

- PlanB suggested in early June that the market is still “50/50” on whether February’s $60K was the bottom, with a later post describing a “likely” bottom below realized price.

Why realized price is back in focus

Realized price is used by onchain observers as a proxy for the aggregate cost basis of Bitcoin holdings. It reflects the average price at which the existing BTC supply last moved on-chain, making it a reference point for where investors’ entry costs cluster.

In a piece of analysis referenced by CryptoQuant, contributor Crypto Sunmoon noted that “every recurring bear market” has been followed by a period in which Bitcoin fell below its realized price, and that this has historically represented the “best” investment opportunity. The same analysis points out that BTC/USD has not traded below realized price since the end of the prior bear market in 2022, using TradingView data as the reference point.

At around $53,300 for realized price, BTC would need to dip roughly another $5,000 to reach that level, based on the “less than 10%” distance described in the source material. Market participants are watching this area because, if realized price is breached again, it could signal a broader shift in market positioning—particularly as the market attempts to move from long drawdowns toward stabilization.

PlanB’s two-condition framework for a reversal

Beyond onchain cost-basis levels, PlanB—creator of Stock-to-Flow-based BTC price modeling—has framed the path to reversal around two key conditions. In recent months, PlanB has listed a drop below realized price as one of those conditions that would need to occur for a more confident bottoming process.

The other condition involves the 200-week moving average (WMA). Earlier in the year, PlanB stated that the 200-week WMA requirement had already begun to play out, referencing a trend line that was associated with the 2022 bear-market structure.

PlanB also addressed timing uncertainty directly. In an X post at the start of June, he described the market as “50/50” on whether the February $60K area marked the bottom or whether the bear market would continue. In that context, PlanB’s later messaging broadened the odds for further downside, pointing followers toward the likelihood of an additional leg lower.

“IMO data is telling us that we have not seen bottom formation yet, and that there is a >50% probablility that we go lower (below 200wma $61k or realized price $53k).”

In a subsequent post referenced in the article, PlanB added that Bitcoin would “likely bottom below” the realized price level. The implication for traders is straightforward: if realized price is treated as part of a bottom-completion checklist, waiting for it to break becomes a way to align positioning with the model’s scenario, rather than relying only on shorter-term price action.

What changes this time—and what doesn’t

One of the subtler themes in the discussion is whether this bear-market cycle behaves like prior ones, especially given differences in who holds Bitcoin and how market structure has evolved. The source material highlights an argument from commentator Aaron Bennett, who suggested that the realized price area can still be tested even with institutional holders present—an element he notes as absent from previous bear markets.

That said, the presence of new categories of buyers does not automatically remove downside risk. In the same referenced exchange on X, Bennett said he would be “surprised” if Bitcoin did not at least “touch” the realized price level or dip below it for “a few weeks.”

This is where realized price as a metric becomes particularly useful to investors: it’s not solely about who is buying today, but about where Bitcoin’s cost basis sits in aggregate. Even if institutions help change demand dynamics near certain price points, a prolonged trend lower can still carry the market into regions where many holders are underwater—creating conditions that have historically coincided with bear-market bottoming phases.

How investors might use this information

Realized price is best understood as a behavioral reference level rather than a precise timing tool. The fact that BTC/USD has not traded below realized price since the end of the 2022 bear market raises the stakes for the current approach: a break would represent a new interaction between spot price and the prevailing onchain cost basis.

For traders, the immediate question is whether the market can force a close below realized price, which the CryptoQuant analysis describes as a recurring bear-market marker. For longer-term investors, the takeaway is less about predicting exact dates and more about understanding how historically significant thresholds can reappear in late-cycle conditions.

With PlanB framing realized price as likely part of the bottom process—and emphasizing that the 200-week WMA condition is tied into the same reversal narrative—watching both levels may help market participants assess whether the market is moving closer to a full-cycle reset or stalling before completing the “checklist” suggested by these models.

Bitcoin’s next move around the realized price region is likely to remain a focal point because it sits at the intersection of onchain cost-basis logic and a broader set of trend-reversal conditions being tracked by well-known modelers and commentators. The key uncertainty is whether any dip under realized price leads to sustained stabilization—or whether the market overshoots it before a durable bottom forms.

Phantom, the largest Solana wallet by market share, said the team behind Ventuals is joining the company this week, weeks after the Hyperliquid-based perpetuals venue shut down. The hires are Ventuals co-founders Alvin Hsia and Emily Hsia, along with engineer Aris Samad, Phantom said in an… Read the full story at The Defiant

Drugs, shootouts and trips to M&S: Forget the Costa del Sol – how the NETHERLANDS became the new playground for British gangsters

Organic Valley debuts cheese snacks

Massachusetts AG Files Amended Lawsuit Against Kalshi over Sports Betting after Court Ruling

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics5 days ago

Politics5 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World21 hours ago

Crypto World21 hours agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics5 days ago

Politics5 days agoPotential 2028er World Cup attendee leaderboard

-

Business5 days ago

Business5 days agoAsia stock markets slide as tech shares slump

-

News Videos2 days ago

News Videos2 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech5 days ago

Tech5 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World7 days ago

Crypto World7 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World7 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World5 days ago

Crypto World5 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World3 days ago

Crypto World3 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business7 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World4 days ago

Crypto World4 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Business20 hours ago

Business20 hours agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Sports4 days ago

Sports4 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech3 days ago

Tech3 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech3 days ago

Tech3 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World4 days ago

Crypto World4 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World6 days ago

Crypto World6 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

You must be logged in to post a comment Login