Crypto World

Ionic Digital, Celsius-Linked Bitcoin Miner, Targets Nasdaq Direct Listing Amid AI Shift

Ionic Digital, the company formed out of the Celsius Mining restructuring, has filed with the U.S. Securities and Exchange Commission to list on the Nasdaq via a direct listing. The move is designed to create a public trading venue for existing shareholders rather than to generate fresh funding for the business.

In a registration statement submitted on Monday, Ionic said registered stockholders may sell up to 10.8 million shares of Class A stock under the proposed ticker “IOND,” according to the SEC filing: https://www.sec.gov/Archives/edgar/data/2007691/000118518526002704/ionicdigis1061026.htm.

Key takeaways

- Ionic Digital has filed for a Nasdaq direct listing that would allow existing shareholders to sell Class A shares, not to raise new capital.

- The company plans to trade under the proposed ticker “IOND,” with up to 10.8 million Class A shares available for sale by registered stockholders.

- Ionic’s strategy is shifting from Bitcoin mining toward AI and high-performance computing infrastructure.

- A major part of that plan centers on a 234-megawatt Texas power site that the company leased for AI workloads under a long-term contract.

- Recent financial results show leasing revenue rising while Bitcoin mining revenue has declined year over year.

Why the direct listing matters for Celsius creditors

For many participants in the Celsius bankruptcy process, the practical challenge has been converting received restructuring shares into liquid, market-priced assets. Ionic’s filing indicates that the proposed Nasdaq direct listing is meant to address that: the listing “will not raise new capital” and instead establishes a public market for existing shares.

That includes former Celsius creditors who received Ionic shares through the lender’s restructuring plan, the company said in its SEC submission. In other words, the immediate purpose is liquidity and price discovery—important for holders who may otherwise be waiting for private market exits or secondary trading limitations.

From mining operator to AI infrastructure provider

Ionic was formed in 2024 to acquire Celsius Mining’s assets as part of the bankruptcy restructuring. In its filing, the company described a strategic pivot that began in 2025: it is repositioning itself from a Bitcoin-mining-focused business into a digital infrastructure company that serves AI and high-performance computing workloads.

A key element of that pivot is the company’s Ward County property in Texas. The site—originally developed to support Bitcoin mining—has been repurposed for AI infrastructure demand. According to the company, Ionic’s AI strategy is anchored by a long-term lease that turns a mining power base into contracted computing capacity.

The Ward County lease underpins the new revenue model

The SEC filing ties the AI transition to a contract Ionic executed in October 2025. Ionic said it leased the Ward County facility to AI infrastructure provider Nscale under a 126-month agreement. Ionic characterized the deal as nearly $2 billion in contracted revenue.

Importantly, the company noted the contract may be expandable. The agreement could include an additional 89 MW if Ionic secures the necessary capacity and approvals. If that additional capacity is brought into the arrangement, Ionic said the contracted revenue could rise to approximately $2.6 billion, as stated in the filing.

The company also pointed to evidence that its pivot is beginning to reflect in financial reporting. In the first quarter of 2026, Ionic reported $44 million in digital infrastructure leasing revenue. At the same time, it said Bitcoin mining revenue declined 82% year over year to $7.4 million, alongside a reduced number of active miners and the ongoing repurposing of the Ward County site.

Share sale logistics and what comes next

Under the SEC registration statement, registered stockholders may sell up to 10.8 million shares of Ionic’s Class A stock in connection with the proposed direct listing. Because a direct listing does not necessarily involve a traditional underwriting process designed around raising capital, the structure typically emphasizes secondary liquidity—consistent with Ionic’s stated goal that the Nasdaq move is not intended to fund new operations.

The filing also lands after Ionic completed a $400 million equity private placement on Friday, according to company communications referenced in the original coverage. Ionic said the proceeds are intended for general corporate purposes, and its CEO, Andy Stewart, indicated the funding supports continued development of its digital infrastructure assets.

For investors and Celsius creditors watching this transition, several details will likely determine how quickly the market starts pricing Ionic’s AI thesis. These include how much additional capacity (if any) is secured beyond the initial contract footprint, and whether leasing revenue keeps growing fast enough to offset the decline in mining-related income.

Near-term, the key question is whether Ionic’s contractual roadmap for AI and high-performance computing continues to translate into steadily increasing reported revenue as Bitcoin operations are further wound down and capacity is redeployed.

Traders work at the New York Stock Exchange on June 26, 2026.

NYSE

Small-cap U.S. stocks are capping off one of their strongest first halves in decades. But this is not your ordinary small-cap boom led by traditional businesses linked to the economic cycle.

This run, like the one going on with their larger-cap peers, has been driven by the rapid buildout of AI infrastructure, as spending spreads beyond the largest technology companies to a broader network of suppliers.

Investors believe the small-stock rally can broaden out beyond tech and continue, as long as interest rates stay in check.

The Russell 2000 Index has surged more than 21% this year, putting the benchmark on track for its best first-half performance since 1991. The advance marks a sharp turnaround after years of underperformance versus large-cap peers.

“It’s both a valuation catch-up story and a fundamental story,” said Amy Zhang, portfolio manager at Alger. “The valuation gap was so wide that a truck can drive through it. At the same time, fundamentals are improving in small caps and I think that’s why it’s causing the broadening trade.”

Semiconductor and semiconductor-equipment companies have been the biggest winners, underscoring how the AI investment boom is rippling through the broader market. Chip-related companies account for 16 of the Russell 2000’s 50 best-performing stocks this year, including Aehr Test Systems, Ichor Holdings and MaxLinear, which have all rallied more than 400%.

Rather than competing directly with industry leaders like Nvidia, many of these smaller companies are benefiting from rising demand across the AI supply chain. As chipmakers and cloud providers ramp up spending on AI infrastructure, suppliers of semiconductor equipment, components and connectivity solutions are seeing the gains trickle down, amplifying revenue and earnings growth for companies with much smaller market capitalizations.

“I think a significant part of the small cap story is tied to AI,” Zhang said. “The impact of AI investment trickles down from large-cap leaders to small-cap companies. The effect will be more amplified for small-cap companies, in terms of revenue and probability growth.”

More Than Just AI

While AI has been a key driver of the rally, strategists say the small-cap rebound has been supported by a broader set of fundamental tailwinds and can continue.

“Small-cap leadership has been notable amid the mega-cap-driven bull market, although small caps have meaningful exposure to semiconductors and technology hardware,” said Adam Turnquist, chief technical strategist at LPL Financial. “Building fundamental strength has also helped offset headwinds from higher rates.”

Consensus forecasts for Russell 2000 companies’ 2026 earnings growth have climbed to 38% from about 23% at the start of the year, according to LPL, reflecting growing optimism that profit growth is broadening beyond the largest technology companies.

Russell 2000 year to date

Turnquist also pointed to several other catalysts that could continue to support the asset class, including small caps’ greater exposure to the U.S. economy, expectations for increased merger-and-acquisition activity — particularly in the pharmaceutical and biotechnology industries — and tax incentives designed to encourage capital investment.

Higher rates a threat?

The biggest threat to the small-cap rally may be the same force that held the group back for years: higher interest rates.

The Federal Reserve next meets July 28-29, with traders pricing in about a 30% chance of a rate increase, according to CME Group’s FedWatch tool. By September, markets see more than a 60% probability of at least one quarter-point hike.

Higher borrowing costs pose a particular challenge for smaller companies, which generally carry more floating-rate debt and face greater refinancing needs than their large-cap peers. Bank of America estimates that every additional 25-basis-point hike would reduce Russell 2000 operating earnings by about 2%.

“This could challenge the expected 4Q profits acceleration (and sentiment) in small caps, which have the most refi risk,” Bank of America strategists said in a note.

Even so, many investors believe the worst of the tightening cycle is over. The Fed raised interest rates by a cumulative 500 basis points between March 2022 and mid-2023, one of the most aggressive hiking campaigns in decades.

“We’re probably close to peak inflation and peak rates,” Zhang said. “We had significant headwind the last five years, and I think the headwind is going to abate and turning into a tailwind.”

—With reporting by Deena Zaidi

Crypto World

A Look Inside Saylor’s Bitcoin Monetization Program: Strategy Files to Sell $1.25B in BTC

Bitcoin News: Michael Saylor’s Strategy (Nasdaq: MSTR) filed on June 29 to sell up to $1.25 billion worth of Bitcoin, framing the potential liquidation as a “Bitcoin Monetization Program” designed to bolster its cash reserve, cover preferred stock dividends, and service interest obligations.

The filing marks the most explicit structural retreat yet from the accumulate-at-all-costs playbook Saylor spent years selling to institutional and retail investors alike.

The proximate trigger was June 27, when Strategy’s mNAV, the ratio of its enterprise value to its Bitcoin holdings, fell below 1 for the first time.

That number is not just an optics problem. The entire capital model depended on trading at a premium to net Bitcoin value, which let the company issue equity and preferred stock to buy more BTC at accretive prices. With mNAV at 0.99, that flywheel has stalled.

Strategy’s cash reserve currently stands at approximately $2.55 billion. The company said any Bitcoin sales would be executed “from time to time” depending on market conditions and capital needs, language that keeps the door open without committing to a specific timeline or tranche size.

It also authorized two separate share repurchase programs of up to $1 billion each: one for its Class A common stock and one for its Digital Credit Securities, which cover the preferred stock series including STRK, STRF, and STRD.

The preferred stack is where the pressure concentrates. STRK carries an 8% annual dividend on roughly $584 million raised. STRF pays 10%, compounding to 18% if payments are missed, on $711 million raised. STRD, the most recent series, generated approximately $979.7 million in net proceeds at a 10% non-cumulative rate.

Combined, the annual preferred dividend burden exceeds $700 million. When Bitcoin was trading near its late-2025 highs around $125,000 and mNAV was firmly above 1, issuing new equity to cover those costs was trivially easy. At $60,000 Bitcoin with a sub-1 mNAV, it is not.

This is also not the first time Strategy has touched its Bitcoin treasury. On June 1 the company sold 32 BTC for approximately $2.5 million, a small transaction explicitly tied to funding preferred stock distributions. The June 29 filing raises the potential scale by several orders of magnitude.

Bitcoin price action heading into the filing had already done significant damage. BTC retested $58,000 last week alongside a $3 billion market outflow and a concurrent crash in MSTR shares, compressing Strategy’s NAV coverage at exactly the moment it needed room.

Bitcoin has since recovered modestly to approximately $60,175, but remains well off levels where Strategy’s model operated without friction. Options market structure around the $60,000 range has kept price action choppy, with no clean technical resolution yet.

Peter Schiff, gold advocate and longtime Bitcoin critic, did not miss the moment. In a June 29 post, Schiff said Strategy was “now a Bitcoin seller”, a pointed description given Saylor’s years of public messaging that Bitcoin should never be sold. Following the June 1 transaction, Schiff had written, “What Saylor giveth, Saylor taketh away,” arguing that the company’s aggressive accumulation had helped push Bitcoin price higher before this year’s reversal. His framing is polemical, but the underlying structural point, that Strategy’s buying was itself a price support mechanism that runs in reverse when the model flips, is not wrong.

Strategy has pushed back on the capitulation narrative, maintaining publicly that Bitcoin remains its “primary treasury reserve asset” and that liquidity management does not represent a change in long-term conviction.

The board also adopted a policy requiring at least 12 months of reserve coverage for preferred dividends and interest obligations. That is a meaningful governance shift toward balance-sheet discipline, and an implicit acknowledgment that market access can no longer be assumed.

MSTR shares traded at $82.31 at time of writing, down 3.5% on the day, continuing a sharp decline from the stock’s highs when Bitcoin was approaching $125,000. The contrast between those two data points tells the whole story: MSTR was not just a Bitcoin proxy, it was a leveraged bet on mNAV staying above 1. That condition no longer holds.

Discover: The Best Token Presales

Bitcoin News: MSTR, Does the $90 Level Hold, or Is the Model Still Repricing?

At $92, MSTR is holding just above what has emerged as near-term psychological support around $90. A breach of that level on volume would likely accelerate selling from holders who bought into the company as a premium Bitcoin vehicle, because the premium is now gone, and the equity offers neither the purity of direct BTC exposure nor the safety of a company generating operating cash flow to backstop the position.

The two $1 billion repurchase programs give management a tool to defend both the common stock and the preferred series, which is not nothing. Buybacks at these levels could provide a technical floor if deployed aggressively.

But repurchase authorization and actual deployment are different things, and the company’s first obligation is covering those preferred dividend payments before it can return capital to common holders.

The most likely near-term outcome is continued range-bound choppiness in MSTR between $80 and $89, with direction determined almost entirely by whether Bitcoin can reclaim $63,000 and hold it.

A recovery through that level would push mNAV back above 1 and reopen the equity issuance window. A continuation lower toward $55,000 would force a materially larger Bitcoin sale than the $1.25 billion ceiling currently authorized, and that scenario would likely reprice the entire preferred stack.

El Salvador, by contrast, has continued accumulating Bitcoin under IMF scrutiny, underscoring that not every institutional BTC holder faces the same structural constraints Strategy does. The next signal worth tracking is whether Strategy executes any material BTC sale in the coming two weeks and how the preferred series trades in response.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The post A Look Inside Saylor’s Bitcoin Monetization Program: Strategy Files to Sell $1.25B in BTC appeared first on Cryptonews.

Kaspa price has surged about 15% over the past day as investors have positioned ahead of the network’s long-awaited Toccata hard fork despite continued weakness across the crypto market.

Summary

- Kaspa surged 15% as traders positioned ahead of the scheduled Toccata hard fork.

- Investors expect the upgrade to add smart contracts, KRC-20 tokens, and DeFi functionality.

- Technical buying and short covering helped KAS outperform a weak crypto market.

According to the Kaspa network, the Toccata hard fork is scheduled to activate on the mainnet at approximately 16:15 UTC on June 30. Exchanges including HTX temporarily suspended deposits and withdrawals ahead of the upgrade to support the transition.

The upgrade introduces native smart contract functionality through the SilverScript programming language, while also adding support for KRC-20 tokens, decentralized finance applications, and zero-knowledge privacy features.

Together, these additions remove one of the network’s biggest limitations by expanding Kaspa beyond its original role as a high-speed proof-of-work payment blockchain.

Toccata upgrade has changed Kaspa’s utility

With the hard fork approaching, trading activity has accelerated as investors position for higher on-chain activity. According to the Kaspa network, the upgrade is expected to enable developers to build decentralized applications directly on Kaspa by introducing native smart contract functionality, expanding the network beyond its traditional payment use case.

On-chain activity has also supported the bullish narrative. The network is approaching a cumulative milestone of roughly 2.35 billion transactions, demonstrating continued usage of its BlockDAG architecture even as new features are introduced. Supporters of the network have long argued that BlockDAG enables higher parallel transaction throughput than conventional blockchain designs, reducing congestion during periods of elevated demand.

The technical setup amplified the move. Before the hard fork, Kaspa had spent several months trading inside a prolonged consolidation range, with buyers repeatedly defending the $0.025-$0.030 area. The upgrade arrived while many derivatives traders remained positioned for further downside, creating conditions for a short squeeze as spot demand increased.

Forced liquidations of bearish positions added momentum to the rally once price broke above its recent trading range.

The daily chart also shows the recovery pushing KAS back above its 20-day simple moving average near $0.030 while testing resistance around the 50-day moving average near $0.0317. At the same time, the MACD has produced a bullish crossover with the histogram turning positive, indicating improving momentum.

Still, the token trades below its declining 100-day and 200-day moving averages, suggesting that a sustained trend reversal would require additional buying pressure.

Technical buying has outweighed macro headwinds

Kaspa’s rally has unfolded while much of the cryptocurrency market continues to struggle under an unfavorable macro backdrop. A stronger-than-expected 4.1% U.S. Core PCE inflation reading and the Federal Reserve’s hawkish policy stance under Chair Kevin Warsh have pressured risk assets in recent days, contributing to an estimated $1.79 billion in cumulative outflows from U.S. spot Bitcoin exchange-traded funds.

Unlike many proof-of-stake networks, however, Kaspa operates on a proof-of-work model with approximately 95.4% of its maximum supply already in circulation. With new token issuance steadily declining over time, the introduction of smart contracts and execution fees through the Toccata upgrade has strengthened the network’s utility without materially increasing supply.

Those supply dynamics, combined with renewed developer opportunities and short-covering activity, have helped Kaspa outperform most major cryptocurrencies even as capital has continued flowing out of other digital assets.

Whether the rally extends from here may depend on whether buyers can reclaim resistance around the 50-day and 100-day moving averages before challenging the longer-term 200-day average near $0.0353.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Crypto World

Institutional demand for BTC is below supply as ETF outflows, new coins flood market: Crypto Daily

Though BTC has recently stabilized around $60,000, the prospects for a meaningful recovery remain bleak because institutional demand is falling significantly short of soaking up supply.

The latest chart by Glassnode shows that bitcoin exchange-traded funds (ETFs) have sold off 71,600 BTC, worth over $4 billion, this month, the largest redemption on record. Meanwhile, corporate treasuries, or digital asset treasury firms, have snapped up just 7,500 BTC. Add to that the fresh coins mined each day, and the net figure comes to around -77,000 BTC ($4.4 billion).

In other words, more supply is hitting the market than the biggest players are absorbing, creating what analysts call a “supply overhang.” Big-money vehicles are actually adding to the selling pressure.

Against this backdrop, Strategy (MSTR), the largest bitcoin digital asset company, announced a BTC monetization plan on Monday, authorizing up to $1.25 billion in potential bitcoin sales, mainly to build a $2.55 billion U.S. dollar reserve to cover preferred dividends and interest expenses.

These developments suggest that any price bounce is likely to be short-lived, unless those flows flip positive and institutional demand returns. It’s a key signal for traders watching whether the recovery has real fuel or is just temporary.

Australia’s crypto travel rule comes into force on July 1, adding new data checks for users who send or receive digital assets through regulated exchanges.

Summary

- Australia’s crypto travel rule starts July 1, adding new data checks for exchange transfers.

- Exchanges must collect sender, receiver and wallet details before processing covered virtual asset transfers.

- Self-custody remains allowed, but transfers touching regulated platforms will face more user checks.

AUSTRAC’s transitional rules say some obligations for new virtual asset services were deferred until July 1, including travel rule obligations for virtual asset transfers.

The change affects virtual asset service providers with a link to Australia. AUSTRAC says covered services include crypto-to-fiat exchange, crypto-to-crypto exchange, safekeeping services, transfer services and certain services linked to token offers.

Exchanges must collect transfer details

Under AUSTRAC’s travel rule guidance, businesses that transfer money, virtual assets or property for customers must collect, verify and pass on key information about the transfer. AUSTRAC says the rule helps create transparency across the transfer chain and gives regulators and law enforcement access to needed data.

For virtual asset transfers, AUSTRAC says ordering institutions must check whether the receiving wallet is custodial or self-hosted. They must also carry out due diligence and pass on required information when the other institution is properly licensed or not required to be licensed.

Self-custody transfers face extra checks

Transfers to self-hosted wallets receive different treatment. AUSTRAC says a business does not need to send information to another business in the transfer chain when the transfer goes to a self-hosted wallet. However, the ordering institution must still collect and verify payer information and collect payee and tracing information.

This is the point drawing user concern online. Trader Greeny wrote on X that “crypto in Australia changes forever” and said small transfers would face the same data checks as larger transfers. Separate compliance summaries also state that Australia has no transaction threshold for the crypto travel rule, meaning the rule applies regardless of transfer size.

Users debate privacy and compliance

Reddit posts show mixed reactions from Australian crypto users. One user wrote, “you can forget about sending crypto anonymously,” while another said “the regulated platforms were never anonymous.” The comments reflect a split between users focused on privacy and others who view exchange reporting as expected under financial crime rules.

AUSTRAC has also updated broader reporting systems. The agency said it received more than 2 million threshold transaction reports and over 450,000 suspicious matter reports last year, and those figures may rise as more businesses fall under the framework from July 1.

Broader crypto rules are tightening

Australia’s travel rule arrives as the country moves toward broader crypto licensing. As reported by crypto.news, ASIC recently extended temporary licensing relief for crypto firms until Sept. 30, giving companies more time to apply for financial services licenses.

As previously reported by crypto.news, Australia’s Senate committee also backed a bill that would bring crypto exchanges and tokenized custody platforms under the country’s financial services licensing regime. That framework targets platforms that hold customer assets and requires governance, disclosure and custody standards.

The July 1 rule does not ban self-custody or crypto transfers. It changes how regulated platforms handle transfers when user assets enter or leave those platforms. For Australian users, the near-term change is practical: exchanges may ask for more details before processing deposits or withdrawals.

TL;DR

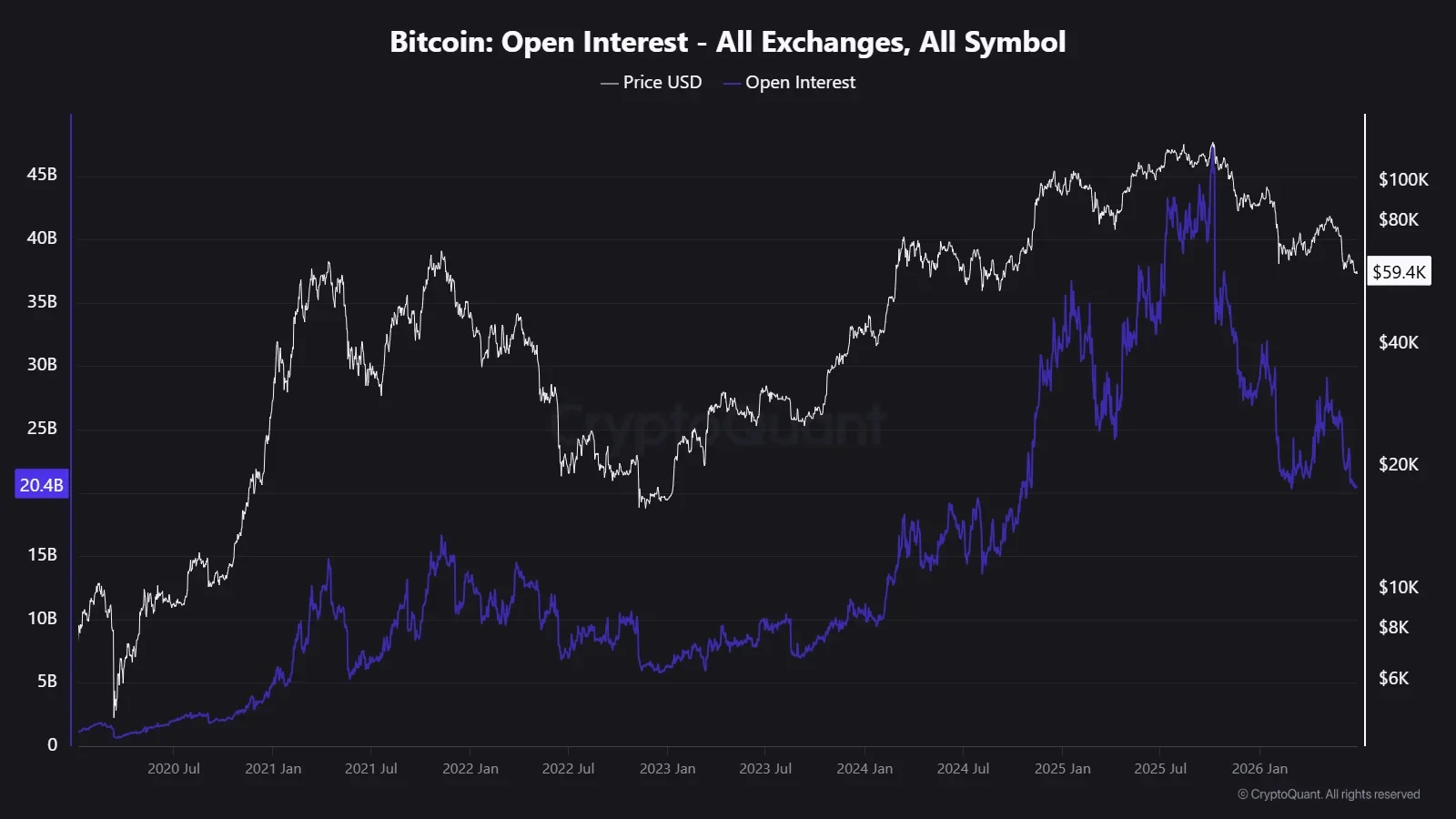

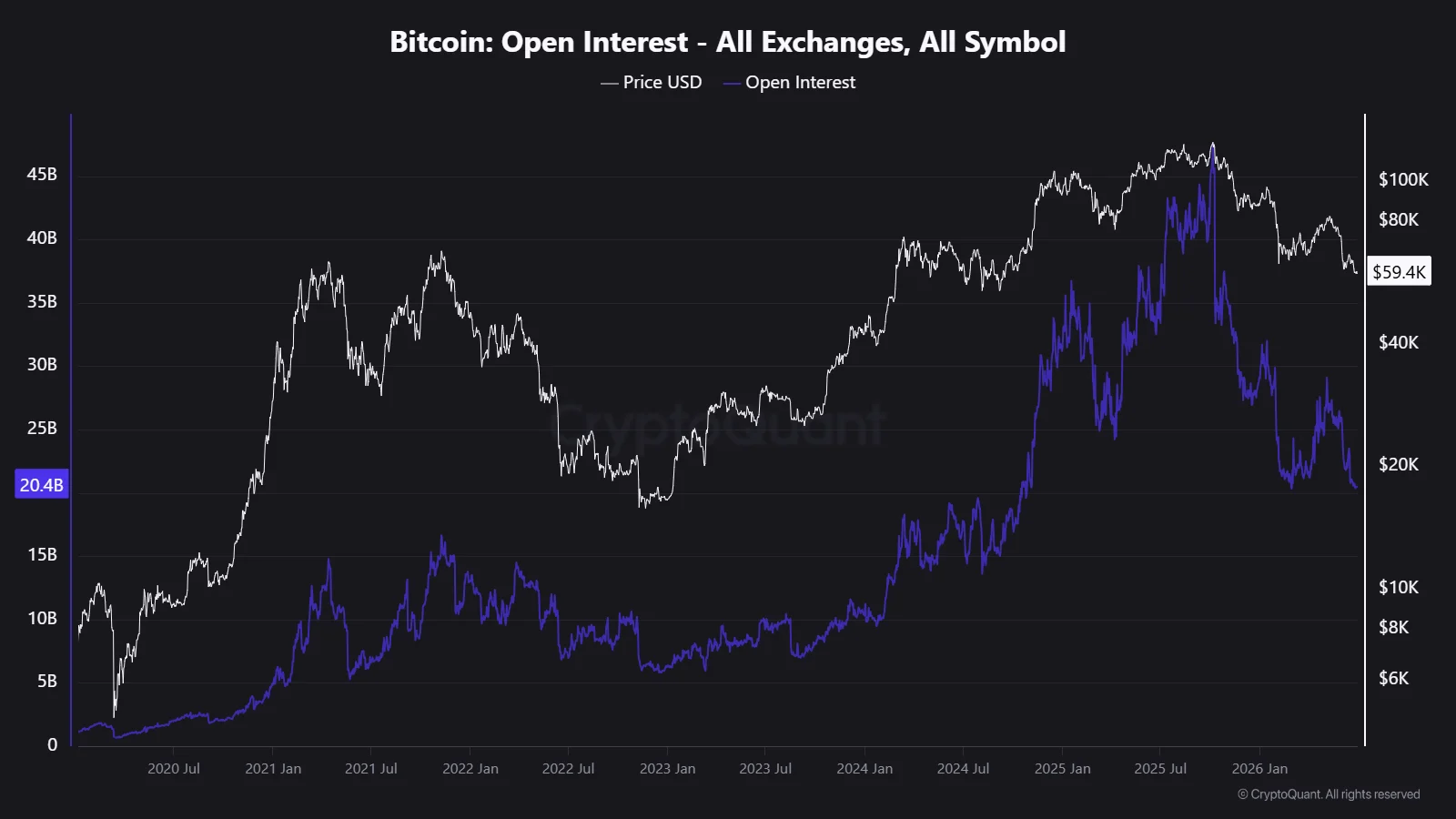

- Bitcoin open interest has dropped from nearly $45 billion to $20.4 billion, reflecting a major reduction in market leverage.

- The decline followed several liquidation events that gradually unwound leveraged futures positions.

- Bitcoin’s price and open interest have fallen at a similar pace, pointing to an orderly deleveraging process.

- Despite the sharp reduction in leverage, the data does not confirm that Bitcoin has reached a market bottom.

The Bitcoin (BTC) futures market has undergone a significant reduction in leverage, with open interest declining from a peak of nearly $45 billion in July 2025 to approximately $20.4 billion, according to CryptoQuant data. The decline reflects a broad unwinding of leveraged positions rather than a sudden market collapse, as both Bitcoin’s price and open interest have fallen at a comparable pace.

Open interest represents the total notional value of outstanding futures contracts. A decline in this metric indicates that positions are being closed, either through liquidations or traders voluntarily reducing exposure. The latest data shows that more than 45% of peak leverage has been removed from the market.

Open Interest Decline Mirrors Bitcoin’s Price Correction

CryptoQuant’s data shows that the reduction in open interest coincided with several notable liquidation events over the past year. The largest occurred on October 10, when Bitcoin fell from an all-time high near $122,574 to roughly $105,000 following record single-day liquidations.

The deleveraging continued into early February, when open interest declined by more than 20% within days as Bitcoin dropped to around $61,000. Additional liquidations through June further reduced outstanding futures positions, bringing total open interest down to approximately $20.4 billion.

According to the data, leverage and Bitcoin’s price have declined at a similar rate throughout the period. This pattern suggests that excess leverage has been gradually removed from the market instead of triggering a disorderly selloff where prices fall much faster than positions are unwound.

Data Shows Deleveraging Has Continued, but Does Not Confirm a Market Bottom

Despite the sharp decline in leverage, the available data does not indicate that Bitcoin has reached a market bottom. Historical observations note that falling open interest has previously been followed by extended periods of sideways trading or additional price declines before a sustained recovery emerged.

Current open interest also remains well above the levels recorded during 2023, when it fell to roughly $10 billion, indicating that further deleveraging remains possible based on historical comparisons.

Meanwhile, the weekly Bitcoin price chart shows the asset trading below $60,000, just below the $68,000–$70,000 range, an area that served as a previous support and resistance zone.

Bitcoin was changing hands at approximately $59,227 as of press time as prices continued to struggle, while volume delta remained negative, reflecting continued selling pressure during the period shown.

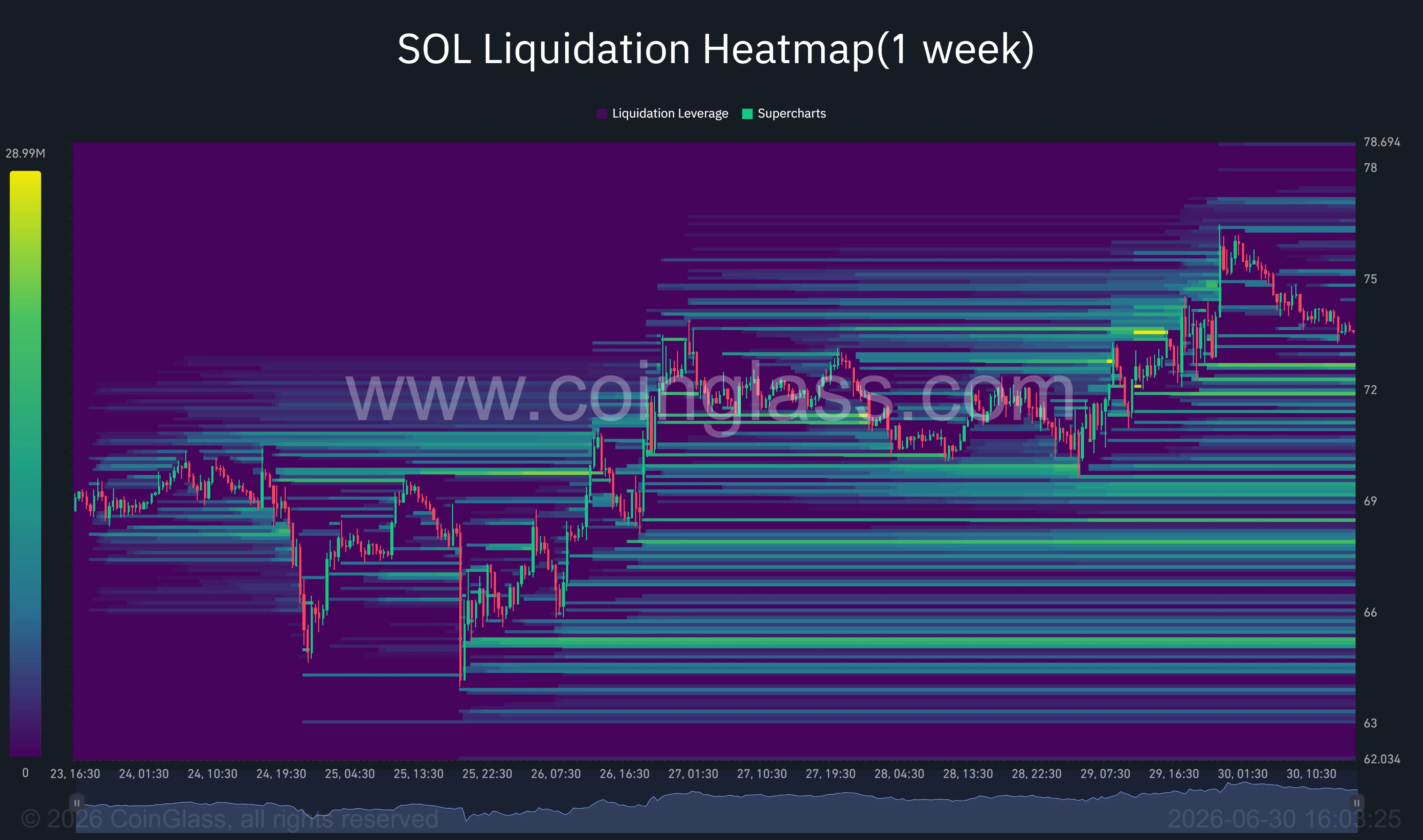

Solana price has extended its recovery to nearly 18% over the past week as record tokenized stock activity and growing institutional adoption helped the token outperform a crypto market still weighed down by macroeconomic uncertainty.

Summary

- Solana price has rallied nearly 18% as record tokenized stock trading boosted network activity and investor demand.

- Technical indicators show bulls testing key resistance between $76 and $80, with liquidation clusters adding volatility.

- Analysts see room for further gains, though macroeconomic uncertainty and weaker support levels remain key risks.

According to data from crypto.news, Solana (SOL) climbed from a local low near $64 on June 25 to an intraday high of $75.8 on June 30 before easing back toward the $73 region. Its rebound came while Bitcoin remained below $60,000 following another failed breakout attempt, allowing SOL to stand out as one of the few large-cap cryptocurrencies to post a strong weekly gain.

One catalyst behind the move came from Solana’s tokenized asset ecosystem. The network processed a record $1.36 billion in weekly tokenized equity volume, accounting for roughly 96% of all on-chain stock trading during the period. The surge in real-world asset activity increased on-chain transactions and demand for SOL as the network’s native gas token, adding a source of organic spot buying beyond speculative trading.

Institutional adoption also continued to build. Spot Solana exchange-traded funds managed by firms including Bitwise and Fidelity surpassed $1.06 billion in combined assets under management. Unlike spot Bitcoin ETFs, several Solana products distribute staking rewards to shareholders, giving investors an additional yield component alongside price exposure.

Additionally, MoneyGram joined the network as a validator while Toss Bank expanded its use of Solana infrastructure for cross-border stablecoin remittances, adding another layer of long-term network participation.

Real-world asset growth has boosted demand for Solana

The 1-day chart shows Solana rebounding sharply after defending support near $64 earlier this week. Price has reclaimed the 20-day simple moving average around $70.9 and is trading above it, while the Chaikin Money Flow has climbed back into positive territory at 0.17, suggesting capital has returned after weeks of persistent selling pressure.

Yet, SOL remains below the 50-day, 100-day and 200-day moving averages near $76.4, $81.0 and $94.6 respectively, leaving a heavy resistance band overhead.

The 4-hour chart paints a constructive short-term picture despite Tuesday’s pullback. Solana completed a strong recovery from the June 25 low and briefly pushed above the 0.786 Fibonacci retracement level at $73.85 before reaching $76.49.

Momentum has eased since then, with the MACD histogram beginning to contract while the RSI has slipped to around 55 after briefly approaching overbought territory. Holding above the 0.618 Fibonacci level near $71.8 would keep the current recovery intact, while a sustained move above $76.5 could expose the next psychological resistance near $80.

Derivatives positioning suggests volatility may not be over. CoinGlass liquidation data shows dense short liquidation clusters between $74 and $76, helping explain the sharp squeeze that carried SOL to its weekly high. Another sizeable concentration of leveraged positions sits around the $72 area, while heavier long liquidation pockets extend toward $69 and $66.

A clean break above $76 could trigger another wave of short liquidations, whereas losing $72 may accelerate downside as leveraged longs begin to unwind.

Commenting on the market structure, well-followed analyst Michaël van de Poppe wrote:

“The flip is an easy buy opportunity for me, but overall, I think that the markets are looking to get more upside momentum and I would expect $120-130 as a potential target area in Q3/Q4 of this year.”

Another optimistic assessment came from fellow analyst Ardi, who argued Solana could be repeating Ethereum’s 2022 recovery pattern. He noted that reclaiming the 21-week exponential moving average near $85 would strengthen the case that SOL has already established its cycle low.

Support at $72 remains crucial for the bullish outlook

Despite Solana’s relative strength, macro conditions continue to present meaningful risks. Markets remain under pressure after the latest U.S. Core PCE inflation reading came in above expectations, reinforcing the possibility that the Federal Reserve could keep interest rates elevated for longer. Rising Treasury yields and continued demand for defensive assets have already weighed on cryptocurrencies, with Bitcoin struggling to regain the $60,000 level.

From a technical standpoint, failure to hold above the $71.8-$72 support region would weaken the current recovery and shift attention back toward $69 and the recent swing low near $64.

On the upside, reclaiming the cluster of moving averages between $76 and $81 would provide the first convincing signal that Solana’s recent rally is developing into a broader trend reversal rather than another relief bounce within its longer-term downtrend.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

A Michigan judge has temporarily blocked Kalshi from allowing residents to place bets on sporting events while the state pursues claims that the platform is violating gambling laws. The decision, issued by Ingham County Circuit Court Judge Rosemarie Aquilina, is set to last 14 days and expires on July 13.

According to a court filing provided through a Thomson Reuters Law360 document, the court said Kalshi could be fined $120,000 for each day it fails to meet the order’s geolocation requirements. Aquilina also argued that Michigan residents risk “irreparable harm” by being “exploited by Kalshi’s sports betting operation masquerading as an investment opportunity.”

Key takeaways

- Michigan’s temporary restraining order halts Kalshi’s sports event betting for now and emphasizes compliance with geolocation requirements.

- Kalshi faces financial exposure under the order, with a cited $120,000-per-day penalty for noncompliance.

- The move follows similar court-ordered pressure in Nevada and ongoing litigation involving multiple prediction market platforms.

- Prediction market sports activity has surged during the FIFA World Cup, with record trading volumes reported by Dune.

- Regulatory scrutiny is intensifying as states and the CFTC challenge the legal classification of event contracts.

Michigan’s temporary block targets geolocation compliance

Ingham County Circuit Court Judge Rosemarie Aquilina granted a temporary restraining order against Kalshi, restricting the company’s sports betting-related offerings to Michigan residents. The court order is tied to geolocation rules, meaning the platform must ensure users are properly excluded or restricted based on location before the order runs its course.

Per the filing, failure to comply can trigger substantial daily penalties. The order’s short duration—14 days—signals an escalation rather than a final resolution, but it also adds immediate operational risk for prediction market operators that rely on broad national access.

Michigan’s action also fits into a wider pattern: regulators and courts across the US have been testing where prediction markets fall within gambling law frameworks, even when operators frame their products as market-like event contracts.

Kalshi joins a growing list of prediction market legal setbacks

This latest Michigan development adds to the pressure Kalshi has faced in other jurisdictions. The article’s referenced reporting notes that Nevada issued a temporary ban on Kalshi earlier in March, making Michigan the second state to impose a court-ordered restriction on Kalshi’s sports event contracts.

Beyond Kalshi, the broader prediction market sector is also under legal scrutiny. On June 17, Kentucky sued five prediction market platforms—including Kalshi and Polymarket—accusing them of operating unlicensed sports betting. According to the same coverage, more than a dozen other states have also taken prediction market operators to court.

Federal regulators are involved as well. The US Commodity Futures Trading Commission (CFTC) has sued several states, arguing that event contracts already subject to federal oversight fall under the CFTC’s exclusive authority.

For users and traders, the practical effect is uncertainty about where and how these markets can legally operate. For operators, it raises compliance burdens and can force changes to access controls, product design, or both—especially when courts act quickly through temporary restraining orders.

World Cup momentum lifts prediction market volumes

While court cases continue to unfold, trading activity in prediction markets has remained active during major sporting events. The article points to sports betting activity rising in prediction markets since the start of the FIFA World Cup.

According to Dune data cited in the report, daily taker volume—a measure of contracts bought or sold by traders filling existing orders—reached a record $713 million on June 20. That high point came more than a week after the tournament started on June 11.

On a broader time basis, the report also cites Defirate data showing sports as the leading category on two of the largest prediction markets. Monthly sports betting volume rose 40% to $9.5 billion on Kalshi and increased 175% to $5.3 billion on Polymarket.

Separately, a referenced Bernstein report predicted that the 2026 FIFA World Cup would generate more than $3 billion in incremental sports betting handle and add between $5 billion and $10 billion in consumer prediction market volume. While that forecast focuses on a future tournament, the World Cup’s current trading lift provides evidence that such demand forecasts may be based on repeatable patterns rather than one-off hype.

From betting to crypto onboarding: new users find the chain

The surge in World Cup-linked trading is also tied, in at least one dataset, to crypto user discovery. The report states that Polymarket has acted as an onboarding layer for new cryptocurrency users, with about 60% of World Cup bettors interacting with the blockchain for the first time during their prediction market entry.

That figure comes from a Bitget Wallet study of 857,000 users, shared with Cointelegraph. The report adds that the “World Cup winner” contract alone generated over $3.5 billion in trading volume on Polymarket, based on platform data for the event.

These points matter because they underscore a key tension in the regulatory debate: prediction markets are often marketed as a trading experience, yet the mechanics frequently route users through blockchain-based infrastructure. Even when users treat the activity as entertainment or wagering, it can still create measurable crypto engagement—potentially increasing the visibility of these markets to regulators.

What to watch next

With Michigan’s restraining order set to expire on July 13 and new enforcement dynamics playing out across states, the next critical question is whether courts move from short-term blocks to longer remedies, and how prediction market platforms adjust geolocation and access controls under mounting legal pressure.

Key Takeaways

- Uber has terminated its autonomous vehicle collaboration with Alphabet’s Waymo in Phoenix, Arizona.

- The rideshare company is currently arranging a replacement autonomous vehicle partnership in Phoenix with an undisclosed provider.

- Waymo robotaxis continue operating through Uber’s platform in Austin and Atlanta markets.

- The partnership dissolution comes after Waymo issued a recall affecting approximately 3,900 self-driving vehicles due to software defects.

- Analysts maintain a Strong Buy rating on UBER stock with projected upside of 43.2%, though shares are down 8% in 2026.

Uber Technologies (UBER) shares declined 0.92% following confirmation that the rideshare giant has discontinued its autonomous vehicle collaboration with Alphabet’s (GOOGL) Waymo subsidiary in the Phoenix, Arizona market. Meanwhile, GOOGL shares rose 4.82%, though this movement doesn’t appear connected to the partnership termination.

The dissolution of the Phoenix arrangement concludes a collaboration initially established in 2023. That original agreement integrated Waymo’s self-driving vehicles into Uber’s ride-hailing ecosystem and food delivery operations.

According to a Waymo representative, the autonomous vehicles previously deployed in the Phoenix pilot program have been reintegrated into Waymo’s proprietary fleet. Phoenix residents can continue accessing these robotaxis exclusively through Waymo’s dedicated application rather than Uber’s platform.

Phoenix’s Role as First Test Market

The Phoenix market served as the inaugural testing ground for the Uber-Waymo collaboration. An Uber representative characterized the deployment as “an intentionally limited deployment,” involving approximately a dozen vehicles specifically allocated to this pilot program.

This relatively modest fleet size reflects the experimental nature of the Phoenix operation compared to Uber’s broader self-driving vehicle strategy. Despite terminating the Waymo arrangement, Uber maintains its commitment to autonomous vehicle services in Phoenix. The company is currently finalizing arrangements with an alternative AV provider, though the partner’s identity remains undisclosed.

Waymo’s robotaxis haven’t been completely removed from Uber’s service offerings. Customers in Austin and Atlanta can still access Waymo’s autonomous vehicles through the Uber application.

The partnership termination timing carries significance. This development follows Waymo’s recent recall of nearly 3,900 self-driving vehicles nationwide.

The recall targeted a software malfunction that potentially allowed vehicles to enter closed freeway construction areas and continue operating. Reuters identified the recall as contextual background for the Phoenix partnership dissolution, though neither organization has explicitly connected these events.

Uber’s Comprehensive Autonomous Vehicle Approach

Uber has been aggressively expanding its autonomous vehicle partnership portfolio beyond Waymo. Current collaborators include Rivian, Amazon’s Zoox division, China-based Pony.AI, and Croatian startup Verne.

Notably absent from Uber’s AV partner roster is Tesla. The rideshare platform has not established any robotaxi arrangements with Elon Musk’s electric vehicle manufacturer.

During the first quarter 2026 earnings conference call, CEO Dara Khosrowshahi provided growth metrics to investors. He reported that autonomous vehicle mobility trips facilitated through Uber’s platform surged more than 1,000% compared to the previous year.

Uber currently operates autonomous ride services across eight metropolitan areas. Management has outlined expansion objectives to reach up to 15 cities before year-end.

Wall Street analysts remain optimistic about Uber’s prospects despite the stock’s challenging 2026 performance. The Strong Buy consensus recommendation reflects 28 Buy ratings alongside only two Hold ratings.

The average analyst price target stands at $108.12, suggesting potential upside of 43.2% from present trading levels.

UBER shares have declined 8% year-to-date, contrasting with the favorable analyst outlook. The company has not provided a timeline for revealing its new Phoenix autonomous vehicle partnership.

A routine filing crowned Goldman Sachs the largest institutional holder of XRP ETFs, and the market read it as Wall Street validating XRP. The next filing showed Goldman had quietly exited the entire position and rotated into crypto stocks instead. Here is what the round trip actually reveals about XRP, Ripple, and how Wall Street is really playing crypto.

Summary

- Goldman Sachs was crowned Wall Street’s biggest XRP whale after a December 31 filing showed a $153.8 million position across four XRP ETFs, roughly 73% of the top 30 institutions’ combined exposure.

- The market read it as a powerful institutional endorsement of XRP, arriving while retail sentiment was mired in extreme fear, the classic “smart money accumulating” narrative.

- A 13F filing is a rear-view mirror, and the catch was timing: the snapshot predated a roughly 40% drop in XRP, leaving open whether Goldman held through the decline.

- The next filing answered it: Goldman had completely exited its XRP and Solana ETF positions and rotated into crypto equities such as Circle, Galaxy Digital, and Coinbase, boosting some stakes by as much as 249%.

- The episode is a lesson in reading delayed filings and a window into how Wall Street is really playing crypto, often preferring the companies and infrastructure over the tokens, which echoes the core question hanging over XRP.

In March 2026, a routine regulatory filing handed XRP holders the kind of headline they had waited years for: Goldman Sachs, the most prestigious investment bank on Wall Street, had been revealed as the single largest institutional holder of XRP exchange-traded funds in the U.S., with a position worth $153.8 million spread across four separate funds. For a token whose entire bull thesis rests on institutional adoption finally arriving, this looked like the proof. The largest bank in the world had quietly loaded up on XRP while ordinary investors were selling in fear, the very picture of smart money moving ahead of the crowd. The crypto community celebrated, analysts framed it as validation that XRP had cleared Wall Street’s due-diligence bar, and the story spread as evidence that the institutional era for XRP had begun.

It was, for a moment, exactly the catalyst the narrative needed. Then the next filing arrived, and it told the opposite story. When Goldman disclosed its following quarter, the $153.8 million XRP position had vanished entirely. The bank had exited its XRP ETF holdings completely, exited its Solana ETF holdings completely, trimmed its Bitcoin and Ethereum exposure, and redirected capital into crypto-related equities instead, increasing stakes in companies like Circle, Galaxy Digital, and Coinbase by as much as 249%.

The biggest XRP whale on Wall Street had, by the time the market crowned it, already swum away. This article tells the full story of that round trip and, more importantly, what it reveals. It covers the filing that created the whale, why the market loved it, why filings are a rear-view mirror, the exit that followed, where Goldman actually moved its money, the retail reality behind the XRP ETF, and what the whole episode means for Ripple and XRP. The analysis is information, not advice, and the lesson is both practical and structural: delayed filings can mislead, and Wall Street may prefer crypto infrastructure over the tokens themselves.

The filing that crowned a whale

Start with what was actually disclosed, because the precision of it is part of why the market took it so seriously. In a quarterly 13F filing, the mandatory disclosure large institutions must make of their equity holdings, Goldman Sachs reported a position of $153.8 million spread across four spot XRP ETFs as of December 31, 2025. The breakdown, first surfaced by the journalist Eleanor Terrett and analyzed by Bloomberg Intelligence analyst James Seyffart, showed roughly $40 million in Bitwise’s XRP ETF, $38.5 million in the Franklin XRP Trust, $38 million in Grayscale’s XRP fund, and $36 million in the 21Shares product. That made Goldman the single largest disclosed institutional holder of XRP ETF shares in the country.

To put its dominance in context, Seyffart’s analysis found that the top 30 institutional holders collectively controlled just over $211 million in XRP ETF exposure, and Goldman alone accounted for roughly 73% of that total. It was not a marginal position; it dwarfed the rest of the institutional field. Two details made the disclosure especially compelling to observers. First, it was Goldman’s first disclosed crypto allocation beyond Bitcoin and Ethereum, which meant the bank was extending its digital-asset exposure into an altcoin for the first time, a meaningful step for an institution of its stature.

Second, the position was deliberately constructed rather than concentrated: Goldman spread its bet across four different issuers in roughly equal slices, the kind of diversified allocation that signals a considered, risk-managed decision rather than an opportunistic punt. When the largest investment bank in the world shows up in the filings of four separate XRP funds with a carefully distributed nine-figure position, it suggests the trade was intentional and institutional, not incidental. The regulatory clarity that followed the conclusion of Ripple’s legal battle, combined with the ETF approvals it enabled, had given an institution like Goldman a familiar, regulated wrapper through which to hold XRP exposure, and Goldman appeared to have used it decisively. On its face, this was the institutional validation the XRP thesis had always promised.

Why the market loved the story

It is worth dwelling on why this filing landed so powerfully, because the appeal reveals what the XRP community has been hungry for. The core of the XRP bull case has long been that the token’s real catalyst is institutional adoption: that once banks, asset managers, and other large players begin holding and using XRP, demand will arrive at a scale that retail speculation never could, and the price will follow. For years, that adoption was promised but rarely visible in a form retail holders could point to. A 13F filing showing the world’s most prestigious investment bank as the single largest institutional holder of XRP ETF shares was exactly the visible, concrete proof the narrative had been missing.

It was not a vague partnership announcement or a settlement that proved the plumbing worked; it was Goldman Sachs, by name, in the filings, with a nine-figure position. The timing amplified the effect. The disclosure landed during a period when retail sentiment across crypto was mired in extreme fear, with the broad market stuck in a pessimistic stretch lasting weeks. Against that backdrop, the revelation fit one of the most seductive patterns in investing: the contrarian “smart money accumulating while the crowd panics” story.

The interpretation almost wrote itself. While ordinary investors were selling XRP in fear, Wall Street’s most powerful bank was quietly buying, which implied that the people with the best information and the deepest resources saw value precisely where retail saw only losses. That framing is emotionally powerful because it offers reassurance to holders sitting on losses, recasting their pain as the entry point that institutions were exploiting. Commentators leaned into it, describing a wave of institutional “super fans” piling into XRP ETFs and treating Goldman’s position as the leading edge of a broader Wall Street embrace. The story was compelling, well-sourced, and emotionally satisfying; its only flaw was that it was already out of date.

The catch nobody priced in

Here is the structural problem that the celebration overlooked, and it is fundamental to how 13F filings work. A 13F is a rear-view mirror. It discloses what an institution held as of the end of a calendar quarter, but it is filed weeks later, which means that by the time the public sees the position, it reflects where the institution stood at the snapshot date, not where it stands when the filing becomes news. Goldman’s $153.8 million XRP position was a snapshot as of December 31, 2025.

The filing that revealed it became public in February and drove headlines into March, but the holding it described was already two to three months stale by the time the market reacted to it. Goldman could have trimmed, added to, or exited the position entirely in the intervening period, and the filing would say nothing about it. The market was celebrating a photograph of the past as if it were a live feed. That gap mattered enormously in this case because of what happened to XRP in the interim.

The snapshot captured Goldman’s position at the end of a quarter when XRP was trading materially higher; the token had peaked near $2.40 in early January 2026. Over the following weeks, XRP fell hard, declining more than 40% through the first quarter as the broader market weakened, the same drawdown that prompted Standard Chartered to cut its year-end XRP target from $8 to $2.80 in mid-February. So the celebrated Goldman position was struck before a major decline, and the obvious question, which the more careful analysts raised at the time, was whether Goldman had held through that drawdown or exited as XRP fell. The bullish crowd treated the position as current conviction; the careful reading treated it as an open question.

The next filing settled the matter, and it did not settle it in the bulls’ favor. That is why stale filing data needs to be read differently from live flow data. A 13F can prove that an institution held something at a point in time, but it cannot prove present conviction. In crypto, where a token can move 40% before the filing becomes public, that difference is not academic.

Then Goldman sold everything

When Goldman’s first-quarter 2026 13F filing arrived in May, it revealed that the bank had completely exited its XRP ETF position. The $153.8 million spread across four funds, the holding that had crowned Goldman the biggest XRP whale on Wall Street, was simply gone. And it was not only XRP: Goldman had also exited its Solana ETF holdings entirely, erasing positions it had previously held across multiple Solana products. The bank trimmed its Bitcoin and Ethereum ETF exposure as well, reducing those holdings rather than eliminating them.

In other words, the institution that the XRP community had celebrated as a marquee believer had, by the next available snapshot, removed XRP from its portfolio completely, alongside a broader pullback from altcoin ETF exposure. The whale had not merely trimmed; it had fully unwound the position that made the headlines. The implication reframes the entire earlier narrative. The story that spread in February and March, of Wall Street’s biggest bank accumulating XRP while retail panicked, was describing a position that Goldman was in the process of exiting, or had already decided to exit, even as the public celebrated it.

The “smart money accumulating” interpretation was, in hindsight, exactly backward: the smart money was on its way out, and the delayed nature of the filing meant retail was cheering an entry at almost the moment of the exit. This does not prove that Goldman timed anything perfectly or that its move was a verdict on XRP’s long-term prospects; a single bank’s quarterly allocation decisions reflect many factors, including risk management, mandate changes, and portfolio rebalancing, not necessarily a strong directional view. But it does demolish the specific bullish read that had been built on the earlier filing. The institutional validation that the XRP thesis leaned on turned out, in this instance, to be an institution heading for the door.

For a holder who had taken comfort in the Goldman headline, the follow-up filing was a cold lesson in how stale the comfort had been. The better takeaway is not that every institutional filing is meaningless, but that timing and persistence matter. A real institutional adoption story has to survive more than one delayed snapshot. It has to show up quarter after quarter, across more than one institution, and through drawdowns.

Where the money actually went

The most revealing part of the episode is not that Goldman sold XRP, but what it bought instead, because the rotation tells a story about how Wall Street is really approaching crypto. In the same first-quarter filing that showed Goldman exiting XRP and Solana ETFs, the bank substantially increased its equity stakes in crypto-related companies, boosting positions in firms such as Circle, the stablecoin issuer, Galaxy Digital, the digital-asset financial-services firm, and Coinbase, the exchange, by as much as 249%. So Goldman did not exit crypto. It rotated within crypto, moving out of direct token exposure through altcoin ETFs and into the equities of the companies that operate the crypto economy’s infrastructure.

This is a meaningful signal about institutional strategy, and arguably a more durable insight than the original whale headline. Buying the companies instead of the tokens reflects a particular thesis: that the reliable way to profit from crypto’s growth is to own the businesses that monetize the activity, the picks-and-shovels of the industry, instead of betting on the price of any individual asset. A stablecoin issuer earns on reserves and transaction volume, an exchange earns on trading fees, and a digital-asset financial-services firm earns across market conditions, whereas an altcoin ETF simply tracks a volatile token price. For a risk-managed institution, the equities can look like a steadier way to gain crypto exposure than a single token.

The rotation suggests that, at least for this quarter and this bank, Wall Street’s conviction was stronger in the crypto economy’s infrastructure than in the XRP token itself. That distinction, between the businesses that run on crypto and the tokens crypto runs on, is precisely the distinction that has haunted XRP, and it is why this episode matters far beyond a single bank’s trade. Goldman’s money went to the companies, not the coin. For XRP holders, that distinction is the uncomfortable heart of the story.

The retail reality behind the XRP ETF

The Goldman round trip also punctures a broader assumption about XRP’s ETFs, and the data here is clarifying. Despite the institutional framing that the Goldman headline encouraged, the XRP ETF complex is, in fact, overwhelmingly retail-driven. According to Ripple’s own data, around 84% of U.S. XRP ETF assets are held by retail investors, a striking figure that stands in sharp contrast to Solana ETF products, where institutional participation runs closer to half. So even at the moment Goldman was being celebrated as the face of institutional XRP adoption, the reality was that the ETFs were funded mostly by ordinary investors, with institutions like Goldman representing a smaller, and as it turned out, transient slice.

The institutional adoption story was at a far earlier and thinner stage than the marquee headline suggested. The flow data fills in the picture. XRP ETFs launched in late 2025 and accumulated assets quickly, crossing $1 billion in cumulative inflows by mid-December and surpassing $1.5 billion by early March 2026, a pace Ripple described as among the fastest institutional adoption curves in regulated ETF history. But that momentum did not hold.

By the middle of 2026, total XRP ETF assets under management had fallen back to roughly $1 billion, well below the peak, as inflows slowed dramatically and the token’s price decline eroded the value of the holdings. The retail base has shown genuine conviction, sustaining inflow streaks even through falling prices, which is a real and somewhat encouraging signal of grassroots demand. But conviction from retail is a different foundation than sustained institutional accumulation, and the Goldman episode laid bare how much of the institutional story was projection. The ETFs proved that regulated XRP access works and that demand exists, but the demand is mostly retail, the institutional participation is early and uneven, and the single biggest institutional holder turned out to be a seller.

That is a more sober picture than the one the original headline painted, and a more accurate one. It also makes the broader ETF flow picture more important than any single famous holder. ETF demand can matter for XRP, but it matters most when flows are persistent, diversified, and not merely the result of retail conviction in a falling market. Until institutional ownership broadens and holds through volatility, the ETF story remains real but incomplete.

What it means for Ripple and XRP

So what does the whole episode actually mean for Ripple and the token? The sobering read is that it exposes how thin the institutional-validation narrative was, and it reinforces the deepest concern about XRP. The pattern that has defined XRP through this period is that Ripple keeps winning, genuinely, in the institutional arena, while the token struggles to capture the value, because the market distinguishes between adoption of Ripple’s infrastructure and demand for XRP itself. Goldman’s rotation maps onto that distinction with uncomfortable precision: the bank moved out of the XRP token and into the equities of crypto companies, choosing the businesses over the coin.

If sophisticated institutions, when they want crypto exposure, increasingly prefer to own Circle, Coinbase, and Galaxy over holding XRP, that is the value-accrual problem expressed through a portfolio: Wall Street betting on the crypto economy without betting on the token. For a holder, the lesson is to treat institutional-adoption headlines with the same skepticism the Goldman story now demands, and to ask not whether institutions are touching the ecosystem but whether they are holding the asset. That is the value-accrual question in depth, and it keeps resurfacing across Ripple’s story. Ripple can win business while XRP still has to prove that those wins create direct token demand.

The fairer, more balanced read does not let the bears claim too much, though. One bank’s quarterly decision is not a referendum on XRP, and there are real counterpoints. Goldman exited Solana too, so the move looks more like a broad altcoin-ETF pullback amid a risk-off market than a targeted verdict on XRP specifically. The bank could re-enter; 13F filings capture a moment, and the next one could show a different posture.

The retail demand underpinning the XRP ETFs has been persistent, holding through the drawdown, which suggests a genuine base of conviction that does not depend on any single institution. And the structural supports for XRP remain in place: regulated ETF access exists, the legal status is clearer than for almost any major token, and the CLARITY Act, if it passes, could codify XRP’s commodity status into federal law and unlock the larger, more durable institutional buyers, pensions and asset managers, that cannot allocate to an asset until its status is settled in statute. That is the catalyst that could unlock real institutions, and it remains the most important distinction between today’s retail-heavy ETF demand and the institutional allocation XRP bulls still expect. In that reading, Goldman was simply early and tactical, not a leading indicator, and the real institutional money is still waiting on a catalyst that has not yet arrived.

Both readings are legitimate. What the episode settles is only that the institutional era for XRP had not, in fact, begun when the headline said it had. The Goldman headline was a sign of interest, not proof of durable adoption. The sellout was a warning about overreading a single filing, not proof that XRP has no institutional future.

What to watch from here

The productive way to carry this lesson forward is to track the signals that would actually indicate institutional conviction in XRP, instead of reacting to stale snapshots. The first is the sequence of upcoming 13F filings, watched not for a single marquee name but for whether institutional XRP ETF holdings broaden and persist across multiple players and multiple quarters, which is what real adoption would look like, as opposed to one bank’s transient position. A durable institutional base would show up as sustained, distributed holdings that survive drawdowns, not a one-quarter cameo. Whether Goldman itself re-enters in a later filing is worth noting too, though it should be read as one data point instead of a verdict.

The second signal is the trajectory of XRP ETF flows and assets: whether the retail-driven inflows that have sustained the funds continue, and whether institutional participation rises from its currently thin share toward the higher levels seen in some other products. The third, and most consequential, is the CLARITY Act, because the structural argument is that the largest institutions are not absent by choice but constrained by the lack of statutory clarity, and that legislation codifying XRP’s status is the catalyst that would unlock them. If that money arrives, it would be visible in exactly the filings this episode taught us to read carefully. And the fourth is whether Wall Street’s apparent preference for crypto equities over tokens, the Circle-and-Coinbase rotation Goldman exemplified, becomes a durable pattern.

If institutions keep choosing the companies over the coins, that is the value-accrual question answering itself in real time. The Goldman round trip was a single episode, but it handed XRP holders a durable framework: celebrate adoption when it is current, distributed, and sustained, not when it is a stale snapshot of a position already being unwound. Read that way, the whale that swam away taught a more useful lesson than the whale that was never quite there. For price-focused readers, where the token stands now is the next practical question, because ETF flows, regulation, and institutional ownership only matter if they eventually show up in the chart.

Frequently asked questions

Was Goldman Sachs really the biggest XRP holder?

It was the largest disclosed institutional holder of XRP ETF shares, based on its 13F filing for the quarter ending December 31, 2025, which showed a $153.8 million position spread across four spot XRP ETFs, roughly 73% of the top 30 institutions’ combined exposure. That made it the single biggest institutional name in the XRP ETF field at that snapshot. Importantly, this was a position in XRP ETFs, not direct token holdings, and it described where Goldman stood at year-end 2025, not necessarily where it stood when the filing became public news in early 2026. The next filing revealed Goldman had since exited the position entirely.

Did Goldman Sachs sell its XRP?

Yes. Goldman’s subsequent 13F filing, covering the first quarter of 2026 and disclosed in May, showed that the bank had completely exited its XRP ETF position; the entire $153.8 million holding was gone. It also exited its Solana ETF holdings entirely and trimmed its Bitcoin and Ethereum ETF exposure. So by the time the market was celebrating Goldman as the biggest XRP whale, based on the earlier year-end snapshot, the bank had already unwound the position. This is a direct consequence of how 13F filings work: they disclose holdings weeks after the snapshot date, so a celebrated position can already be sold by the time it makes headlines.

Why did Goldman exit XRP?

The filing does not state reasons, and a bank’s quarterly allocation decisions reflect many factors, including risk management, mandate changes, and rebalancing, not necessarily a directional verdict on XRP. Two contextual points stand out. First, Goldman exited Solana ETFs too and trimmed Bitcoin and Ethereum, suggesting a broad pullback from altcoin and crypto-ETF exposure during a risk-off, falling market instead of a targeted call against XRP. Second, and more tellingly, Goldman rotated into crypto-related equities instead, increasing stakes in companies like Circle, Galaxy Digital, and Coinbase by as much as 249%, which suggests a strategic preference for owning the businesses of the crypto economy over holding volatile tokens directly.

What did Goldman buy instead of XRP?

Goldman rotated into the equities of crypto-related companies. In the same filing that showed it exiting XRP and Solana ETFs, the bank substantially increased its stakes in firms such as Circle, the stablecoin issuer, Galaxy Digital, a digital-asset financial-services firm, and Coinbase, the exchange, raising some positions by as much as 249%. The logic this implies is a picks-and-shovels thesis: profiting from crypto’s growth by owning the businesses that earn revenue from the activity, issuers, exchanges, and financial-services firms, instead of betting on the price of any single token. It is a more risk-managed way to gain crypto exposure, and it reflects a preference for the infrastructure of crypto over the assets themselves.

Does Goldman’s exit mean XRP is a bad investment?

Not on its own, and the episode should not be over-read. One bank’s quarterly decision is not a referendum on XRP, especially since Goldman pulled back from altcoin ETFs broadly during a risk-off market and could re-enter later. The retail demand underpinning XRP ETFs has been persistent, holding through the drawdown, and the structural supports, regulated access, clearer legal status, and the potential of the CLARITY Act to unlock larger institutional buyers, remain in place. What the episode does establish is that the institutional-adoption narrative built on the original Goldman headline was premature, and that holders should treat such headlines cautiously. It is a caution about reading stale filings, not a verdict on the asset.

What does this mean for Ripple?

It reinforces the central tension in the Ripple and XRP story: the distinction between adoption of Ripple’s ecosystem and demand for the XRP token. Goldman rotating from XRP into crypto equities like Circle and Coinbase mirrors, at the portfolio level, the broader pattern in which value tends to accrue to companies and infrastructure instead of to the token. If institutions seeking crypto exposure increasingly prefer to own the businesses over the coins, that is the value-accrual question expressed through Wall Street’s choices. The counterweight is that the larger, more durable institutional money may still be waiting on statutory clarity from the CLARITY Act, which, if it passes, could change the calculus. For now, the episode is a reminder that institutional validation for XRP is thinner and more provisional than headlines suggest.

This article is information, not financial or investment advice. Details of Goldman Sachs’s filings, holdings, XRP ETF figures, and price levels reflect reporting available as of June 30, 2026, are point-in-time, and can change. 13F filings are delayed snapshots and may not reflect current positions. Cryptocurrency is volatile and you can lose money. Nothing here is a recommendation about XRP or any asset. Do your own research and consult a qualified financial professional before making any decision.

Inside Taylor Swift & Travis Kelce’s Wedding Strict Measures

Ariana Grande Reschedules Tour Dates Due To ‘Safety’ Concerns

Katie Taylor vs Flora Pili: full undercard announced for Irish icon’s retirement fight

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Renter of Home in Anne Heche Crash Denies Settlement With Son

Two goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

How To Earn Money Online 2026 | Learn This Skill Before Everyone Else | how to make money online

Crypto Gold Live Trading 29 JUNE | Market Trader | #goldtrading #cryptotrading #bitcoin

SMART Money Reads Market Movements Like a Pro?

-

Sports7 days ago

Two goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics4 days ago

Politics4 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics4 days ago

Politics4 days agoPotential 2028er World Cup attendee leaderboard

-

News Videos2 days ago

News Videos2 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Business4 days ago

Business4 days agoAsia stock markets slide as tech shares slump

-

Tech5 days ago

Tech5 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World6 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World5 days ago

Crypto World5 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World3 days ago

Crypto World3 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business6 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World3 days ago

Crypto World3 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports4 days ago

Sports4 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World4 days ago

Crypto World4 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech2 days ago

Tech2 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech3 days ago

Tech3 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World4 days ago

Crypto World4 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World4 days ago

Crypto World4 days agoRTX holders must register wallets before token distribution begins

-

Crypto World5 days ago

Crypto World5 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

You must be logged in to post a comment Login