Crypto World

SpaceX’s Bitcoin Trojan horse: what 18,712 BTC means

SpaceX went public in the largest IPO ever, and tucked inside its balance sheet are 18,712 bitcoin. Now every index fund and pension that buys the stock owns a sliver of BTC whether they meant to or not. Bulls call it a Trojan horse that could put a floor under Bitcoin. Here is what the holding actually does, and what it does not.

Summary

- SpaceX went public around June 12, 2026, in the largest IPO ever, priced at $135 a share, raising roughly $75 billion at about a $1.75 trillion valuation, with the stock spiking over 26% before sliding back below its opening price.

- The company disclosed 18,712 bitcoin, worth about $1.29 billion as of March 31, in its filing, so anyone who buys the stock gains indirect, passive exposure to Bitcoin.

- The bullish thesis is that index funds, pensions, and ETFs buying SpaceX for its aerospace and AI exposure will inherently and mechanically hold Bitcoin, creating price-insensitive demand and legitimizing BTC as a corporate treasury asset.

- The skeptical view is that the holding is a tiny fraction of a $1.75 trillion company, so the per-share Bitcoin exposure is minuscule, and that a giant risk-on IPO can drain capital from crypto in the near term rather than support it.

- The story also raises a Tesla-merger overhang that could concentrate roughly 30,000 BTC under Elon Musk, and a copycat question about whether other pre-IPO giants disclose Bitcoin to court crypto-correlated investors.

SpaceX went public around June 12, 2026, in the largest initial public offering in history, and inside the balance sheet of the most anticipated listing of the decade sits a detail that the crypto market has fixated on: the company holds 18,712 bitcoin. The offering priced at $135 a share, raised roughly $75 billion, and valued SpaceX at about $1.75 trillion, with the stock spiking more than 26% in early trading before sliding back below its opening price, a debut dramatic enough that reports described Elon Musk crossing into trillionaire territory on paper. For the broader market, the headline was the sheer scale of the raise and the arrival of a private giant on public markets. For crypto, the headline was the bitcoin.

With 18,712 BTC on its books, worth roughly $1.29 billion as of the end of March, SpaceX is now one of the larger corporate holders of the asset, and that holding has been folded, through the IPO, into a stock that thousands of funds will own. The argument that has spread across crypto social media is that this makes SpaceX a Trojan horse: a vehicle that smuggles Bitcoin exposure into the portfolios of investors who never set out to own any. That framing is catchy, and it points at something real, but it deserves to be examined rather than simply repeated, because the truth is more nuanced and more interesting than the slogan. The best version of the story is not that SpaceX suddenly controls Bitcoin’s price, but that Bitcoin has been made slightly more normal inside public-market infrastructure.

This article works through what the SpaceX bitcoin holding actually means for crypto, taking both the bullish and the skeptical cases seriously. It covers the IPO and the bitcoin inside it, the Trojan-horse thesis in its strongest form, why that thesis has genuine force, the math problem that cuts against it, the opposite argument that a giant IPO can pull capital out of crypto rather than feed it, the Tesla-merger overhang that could concentrate an enormous bitcoin position under one person, the question of whether other companies will copy the template, and a net read of what it all means. The forecasts and interpretations here are information, not advice. The goal is to let a reader walk away understanding both why the Trojan-horse idea caught fire and why the sober version of the story is more modest than the headline, because the gap between the two is where the real lesson about Bitcoin’s institutionalization lives.

The IPO and the bitcoin inside it

Start with the facts of the listing, because the scale is the context for everything else. SpaceX priced its IPO at $135 a share in a deal that raised roughly $75 billion, the largest public offering ever attempted, and valued the company at about $1.75 trillion, a figure lifted further by its earlier integration of Musk’s artificial-intelligence venture. The demand was extraordinary, with the offering reportedly several times oversubscribed and total interest running into the hundreds of billions of dollars, and the stock jumped more than a quarter in its first trading before giving much of that back and slipping below its opening price, a volatile debut that matched the hype around it. SpaceX’s business underneath the listing is real and large: 2025 revenue ran around $18.7 billion, driven heavily by Starlink, with rockets and the AI division making up the rest, though the company posted a substantial net loss for the year tied to the AI integration.

The bitcoin is the part that concerns crypto. SpaceX has held Bitcoin as a strategic reserve asset since 2021, viewing it, in Musk’s framing, as a long-term hedge, and its filing disclosed a position of 18,712 BTC with a fair value of roughly $1.29 billion as of March 31. Ahead of the listing, the company tidied up its holdings, consolidating legacy addresses into a single institutional custody arrangement, the kind of housekeeping a company does when it expects scrutiny of its balance sheet during an audit. For readers trying to understand how corporate BTC holdings work, this is the key difference between a private balance-sheet rumor and a public-market disclosure: the asset becomes visible, auditable, and part of the company’s reported financial picture.

What matters for the Trojan-horse argument is that this holding did not stay private. By going public, SpaceX wrapped its bitcoin inside a widely held stock, and the disclosure landed in the prospectus right alongside the Starlink revenue, which some observers read as a deliberate signal to bitcoin-friendly investors instead of an incidental footnote. The position is now a permanent, audited line on the balance sheet of one of the most important companies in the world, which is precisely what gives the next argument its appeal. SpaceX is not a Bitcoin treasury company in the Saylor sense; it is an operating giant with a crypto reserve attached, and that is exactly why the signal carries weight.

The Trojan-horse thesis in its strongest form

The bullish case is worth stating in its most compelling version before testing it. The argument runs like this. When a company the size of SpaceX lists on a major exchange, it becomes eligible for inclusion in the large stock indices, and inclusion in an index like a major large-cap benchmark means that every fund tracking that index must buy the stock, mechanically, regardless of any view on its components. Index funds, exchange-traded funds, pension funds, and other passive vehicles collectively command trillions of dollars and are required by their mandates to hold the constituents of the indices they track.

So once SpaceX enters the major indices, an enormous pool of capital will buy its shares not because those investors want aerospace, AI, or bitcoin, but simply because the stock is in the index. And because the stock carries 18,712 bitcoin on its balance sheet, every one of those passive buyers gains indirect exposure to Bitcoin whether they want it or not. That is the passive-buying mechanism explained in its simplest form: a mandate can create exposure without a fresh discretionary decision. The buyer thinks they are getting SpaceX, and buried inside that exposure is a tiny piece of BTC.

The thesis extends from there into a price argument and a legitimacy argument. On price, the claim is that this passive, mandate-driven buying creates a form of demand for Bitcoin that is insensitive to Bitcoin’s own price, because the funds are buying SpaceX for index reasons, not BTC reasons, and that this could function as a kind of structural floor under the asset, a layer of forced, ongoing exposure that does not sell on bad crypto news. On legitimacy, the claim is arguably more durable: by holding bitcoin as an audited treasury reserve inside a trillion-dollar public company, SpaceX validates Bitcoin as a serious corporate asset class, the same way earlier corporate treasuries did but at far greater scale and visibility. As one widely shared version of the argument put it, the bitcoin on SpaceX’s books is not a footnote but a balance-sheet argument, and every buyer of the stock gets passive Bitcoin exposure built in.

It is a genuinely clever observation, and it is not wrong. The problem is scale. A Trojan horse can be real while carrying a much smaller payload than the army imagines. The next sections separate the valid legitimacy signal from the much weaker claim that this creates a meaningful price floor.

Why the thesis has real force

Before puncturing anything, it is worth crediting what the Trojan-horse argument gets right, because parts of it are sound. The mechanical point about passive investing is accurate. Index funds really are required to hold index constituents, and the growth of passive investing means that a large share of all stock-buying is now done by vehicles that do not exercise discretion over individual holdings. If SpaceX enters the major indices, it is true that a great deal of capital will hold the stock automatically, and it is true that those holders thereby gain some exposure to the company’s bitcoin.

That exposure is real, it is ongoing, and it does not depend on anyone deciding they like Bitcoin. In that narrow sense, the Trojan horse is not a metaphor but a description: index inclusion would smuggle a measure of BTC exposure into portfolios indifferent to it. That matters because Bitcoin’s institutionalization is not only about people choosing Bitcoin directly. It is also about Bitcoin becoming part of financial products, company balance sheets, ETF structures, and public-market plumbing until investors encounter it without seeking it out.

The legitimacy argument is even stronger, and it may be the part that matters most. There is a meaningful difference between a smaller company holding bitcoin as a treasury bet and one of the most scrutinized companies on the planet carrying an audited, multibillion-dollar bitcoin position through the most high-profile IPO in years. The disclosure normalizes Bitcoin as a reserve asset at the highest tier of corporate America, and the fact that it sat in the prospectus next to the core business, instead of being downplayed, signals that SpaceX was comfortable presenting it to institutional investors. That normalization has a compounding quality: each major company that holds bitcoin and survives the scrutiny makes it easier for the next one to do the same, gradually shifting bitcoin from a speculative oddity on a balance sheet toward an accepted, if still volatile, treasury option.

For Bitcoin’s long-term institutional adoption, a trillion-dollar company carrying it through a landmark listing is a genuinely supportive data point. The Trojan-horse framing captures this real dynamic, which is why it resonated. The trouble is only that the price-floor version of the argument oversells the scale of what is happening. A signal can be important without being a demand engine.

The math problem with the thesis

Here is where the sober counterpoint enters, and it is decisive on the narrow price-floor claim. The bitcoin holding, while large in absolute terms, is tiny relative to the company that now contains it. SpaceX holds about $1.29 billion in bitcoin against a market valuation of roughly $1.75 trillion. That means the bitcoin represents well under one tenth of 1% of the company’s value.

For an investor buying SpaceX stock, the embedded bitcoin exposure per dollar invested is therefore minuscule: putting $1,000 into SpaceX shares buys, in effect, well under $1 of indirect bitcoin exposure. The passive, mandate-driven buying that the Trojan-horse thesis celebrates is real, but the slice of that buying which flows through to Bitcoin is a rounding error on the size of the position, not a meaningful new source of demand for an asset whose own market value runs well into the trillions. This matters because the price-floor claim depends on the indirect demand being large enough to move Bitcoin, and it is not. Index funds buying SpaceX are buying aerospace, satellite connectivity, and AI; the bitcoin is incidental ballast.

The dollars that reach BTC through this channel are a vanishingly small fraction of both the funds’ purchases and Bitcoin’s market capitalization. To put a real floor under Bitcoin, you would need sustained buying measured against Bitcoin’s own trillions, and the SpaceX channel simply does not supply that. The honest framing is that the Trojan horse delivers a legitimacy signal and a tiny sliver of passive exposure, not a structural price floor. Investors who bought the slogan expecting SpaceX index inclusion to meaningfully lift Bitcoin have mis-sized the effect by orders of magnitude.

The exposure is real; its impact on price is negligible. Both things are true at once, and conflating them is the central error in the bullish version of the story. That is why where BTC sits as this lands remains driven by Bitcoin’s own market structure, liquidity, macro backdrop, and flows, not by the tiny BTC line item embedded inside SpaceX stock. The IPO may matter for narrative; the chart still needs direct demand.

The other side: a giant IPO can drain crypto

There is a further argument that runs directly against the bullish read, and in the near term it may matter more than the Trojan horse. A listing of this size does not only add a sliver of bitcoin exposure to index portfolios; it also competes ferociously for investment capital, and crypto sits high on the list of assets that get sold to fund it. The SpaceX IPO was several times oversubscribed, drawing total demand reported in the hundreds of billions of dollars, and that demand had to come from somewhere. Because Bitcoin and other digital assets compete for the same risk-on dollars as high-growth equities and hot pre-IPO names, a generational listing approaching the market can pull money out of crypto as investors raise cash to chase the shares.

In the run-up to the SpaceX debut, that is exactly what some analysts observed, with crypto described as a potential first casualty of the IPO and high-beta tokens selling off as traders trimmed positions to fund their IPO allocations. The dynamic was visible in the tape. As the listing approached, Bitcoin slid toward $60,000 and high-beta tokens fell harder, with XRP and others dropping as the broader complex weakened in what looked like a rotation out of speculative crypto and into the IPO, a move made easier when one major brokerage cut its minimum account requirement for the SpaceX offering dramatically to widen retail access. In other words, the same event that the Trojan-horse thesis frames as bullish for Bitcoin acted, in the short term, as a drain on crypto, because the enormous appetite for SpaceX shares competed with crypto for the same pool of risk capital.

There is a longer-term wealth-effect counter to this, namely that the $75 billion raise unlocks an enormous amount of new wealth for early private investors, capital that tends over time to be redistributed down the risk curve into assets like high-cap cryptocurrencies, so the IPO could eventually feed crypto even as it drained it at the moment of listing. But for anyone weighing the immediate impact, the capital-competition effect is a serious and arguably larger near-term force than the trickle of indirect bitcoin exposure the Trojan horse delivers. The same IPO can be bearish for crypto today and supportive years from now, and both readings have evidence behind them. The mistake is assuming that because SpaceX owns BTC, every effect of the IPO must be bullish for BTC.

That is also why the stock’s own performance matters to crypto psychology. If an investor sees a SpaceX allocation outperform years of holding a major crypto asset, the capital-rotation argument becomes easier to understand emotionally as well as mechanically. A hot public-market listing can absorb the attention, liquidity, and risk appetite that might otherwise have gone into Bitcoin, Ethereum, or high-beta altcoins. The Trojan horse carries a sliver of BTC inside it, but the horse itself can still pull capital away from crypto.

The Tesla-merger overhang

Layered on top of the SpaceX story is a related question that could amplify everything: the possibility of a SpaceX and Tesla combination. Tesla already holds one of the larger corporate bitcoin treasuries among publicly traded companies, with a position reported at over 11,500 BTC, and Musk has at times explored the idea of combining his two largest companies. Neither company has announced a formal merger plan, so this remains speculative, but the arithmetic is striking. If SpaceX and Tesla were brought together, the combined entity would carry the sum of their bitcoin positions, roughly 18,712 plus over 11,500 BTC, which would place around 30,000 bitcoin under Musk’s control inside a single public company, one of the largest corporate bitcoin holdings in public markets.

A combined Musk bitcoin treasury of that size would sharpen both sides of the debate explored above. On the bullish side, it would deepen the legitimacy signal, concentrating a very large, audited bitcoin position inside an even more widely held and index-significant company, and it would extend the passive-exposure dynamic to an even broader base of investors. On the skeptical side, the same math problem would apply, only more so in absolute terms but still small relative to the combined company’s likely valuation, and it would introduce a concentration risk: a very large bitcoin position controlled by one individual, whose decisions about whether to hold, add to, or sell that position could move sentiment if not price. The merger is not on the table as an announced plan, and it may never happen, so it belongs in the analysis as an overhang and a scenario instead of a forecast.

But it is part of why the SpaceX listing drew such attention from crypto, because it hints at a future in which a single corporate vehicle, under a single famous owner, could hold one of the most significant bitcoin treasuries in the world. That prospect is worth watching precisely because it would magnify the dynamics this article describes instead of change them in kind. It would make the legitimacy signal louder and the concentration question sharper. It would not magically turn a corporate balance-sheet allocation into a guaranteed Bitcoin floor.

The copycat question

The final forward-looking thread is whether SpaceX has created a template that other companies will copy, which would matter far more than any single holding. The observation driving this is that SpaceX disclosed its bitcoin position prominently in its prospectus, alongside its core business, in a way some read as a deliberate pitch to bitcoin-correlated investors, the kind of allocators who might pay a slight premium for a stock that offers embedded crypto exposure. If that read is correct, then the bitcoin disclosure was partly a marketing decision, and a successful one could encourage other large private companies preparing to go public to do the same: hold some bitcoin, disclose it in the filing, and capture incremental demand from crypto-friendly investors during the listing. Some commentators speculated that other large pre-IPO technology and AI companies could adopt the template before long, disclosing bitcoin positions to court that pool of allocators.

This is the most speculative part of the story and should be treated as such, because it rests on inference about motives and on unconfirmed reports about other companies’ plans instead of on announced facts. It is entirely possible that SpaceX’s holding reflects nothing more than Musk’s long-standing personal conviction about Bitcoin, with no broader template intended, and that other companies will not follow because their leadership lacks the same view or sees no benefit. But the structural logic is real enough to watch: if disclosing a bitcoin treasury during an IPO measurably helps a company’s reception with a slice of investors, rational companies may do it, and a wave of large listings each carrying some bitcoin would, cumulatively, normalize the asset on corporate balance sheets far more than any single holding could. That cumulative legitimization, instead of the price-floor mechanics, is where the SpaceX precedent could matter most.

Whether other companies copy the template is the single most important thing to watch in the wake of this IPO. For now, it is a plausible hypothesis, not an established trend, and the honest framing keeps it in that category. The broader comparison is the corporate bitcoin-treasury meta, where companies are already being judged on whether their crypto holdings create value or financial stress. SpaceX may make the treasury idea more respectable, but Strategy shows how quickly the same theme can become fragile when market prices move against it.

What it actually means for crypto

Pulling the threads together, the SpaceX bitcoin story is real, important, and considerably more modest than its loudest framing, and holding all of that at once is the mark of understanding it. The Trojan-horse thesis is correct that index inclusion would mechanically give a vast pool of passive capital some indirect bitcoin exposure, and it is correct that a trillion-dollar company carrying audited bitcoin through a landmark IPO is a meaningful legitimacy milestone for the asset. Those points are sound and worth taking seriously, because the institutionalization of Bitcoin is a genuine, multiyear trend and SpaceX is a significant marker along it. Where the thesis overreaches is in the price-floor claim: the bitcoin is well under a tenth of 1% of the company’s value, so the demand that actually flows through to BTC via SpaceX is a rounding error against Bitcoin’s trillions, not a structural support for its price.

Set against that small positive is a real near-term negative, namely that an IPO of this magnitude competes for risk capital and can pull money out of crypto as investors fund their allocations, a dynamic that was visible in the weakness across Bitcoin and altcoins heading into the listing. The longer-term wealth-effect argument, that the raise will eventually redistribute capital down the risk curve toward crypto, cuts the other way but operates on a slower clock. The net read, then, is that the SpaceX IPO is best understood as a legitimization signal for Bitcoin instead of a demand engine, with a small structural exposure benefit, a real short-term capital-competition cost, and a more important open question about whether other companies copy the template and whether a Tesla combination concentrates an even larger position under Musk. For a crypto investor, the practical takeaway is to resist the slogan in both directions: SpaceX did not put a floor under Bitcoin, and it did not doom it either.

It made Bitcoin a little more normal as a corporate asset, took some capital out of the room on its way in, and set a precedent worth watching. That measured reading is less exciting than a Trojan horse, and far closer to the truth. It also leaves room for the other crypto angle of the IPO, where SpaceX exposure became part of the tokenized-stock race rather than only the corporate-treasury story. The IPO pulled crypto into the conversation from several directions at once: BTC on the balance sheet, capital rotation in markets, and tokenized equity products trying to package the shares on-chain.

Frequently asked questions

How much bitcoin does SpaceX hold?

SpaceX disclosed a holding of 18,712 bitcoin in its IPO filing, with a fair value of roughly $1.29 billion as of March 31, 2026. The company has held Bitcoin as a strategic reserve since 2021, viewing it, in Elon Musk’s framing, as a long-term hedge. Ahead of the listing, it consolidated its holdings into a single institutional custody arrangement, the kind of housekeeping done before balance-sheet scrutiny. The position makes SpaceX one of the larger known corporate holders of Bitcoin, and because the company is now public, that holding sits inside a widely held stock, which is the basis for the Trojan-horse argument that buyers of the shares gain indirect bitcoin exposure.

What is the SpaceX bitcoin Trojan-horse thesis?

It is the argument that because SpaceX holds bitcoin and is now a public company eligible for major stock indices, the index funds, pensions, and ETFs that must buy the stock will gain indirect, passive exposure to Bitcoin whether they want it or not. The bullish version claims this creates price-insensitive demand that could put a floor under Bitcoin and that it legitimizes BTC as a corporate treasury asset. The mechanical and legitimacy parts are sound: passive funds really would hold some bitcoin exposure through the stock, and a trillion-dollar company carrying audited bitcoin is a real validation. The price-floor part is where it overreaches, because the holding is too small relative to the company to move Bitcoin meaningfully.

Will the SpaceX IPO push Bitcoin’s price up?

Probably not in any meaningful, direct way, despite the Trojan-horse framing. The bitcoin holding is well under one tenth of 1% of SpaceX’s roughly $1.75 trillion valuation, so the demand that flows through to Bitcoin when funds buy the stock is a rounding error against Bitcoin’s multi-trillion-dollar market. In the near term, a giant IPO can actually weigh on crypto, because it competes for the same risk-on capital and investors sell crypto to fund share purchases, a dynamic visible in the weakness across Bitcoin and altcoins before the listing. The more durable effect is legitimization of Bitcoin as a corporate asset, which supports long-term adoption, instead of a direct price catalyst.

Could the SpaceX IPO actually hurt crypto?

In the short term, yes, and this is the underappreciated side of the story. An IPO of this size, several times oversubscribed with demand in the hundreds of billions, competes fiercely for investment capital, and crypto sits high on the list of assets sold to fund such allocations because it shares investors with high-beta tech and pre-IPO speculation. Heading into the SpaceX debut, Bitcoin slid and high-beta tokens like XRP fell harder, in what analysts described as crypto being a potential first casualty of the IPO drain. Over the longer term, the wealth unlocked by the raise could redistribute toward crypto, but the immediate capital-competition effect is a real headwind that runs opposite to the bullish Trojan-horse narrative.

What does a possible Tesla merger have to do with it?

Tesla already holds one of the larger corporate bitcoin treasuries, reported at over 11,500 BTC, and Musk has at times explored combining SpaceX and Tesla, though neither company has announced a formal plan. If they merged, the combined entity would hold roughly 30,000 bitcoin, around 18,712 from SpaceX plus over 11,500 from Tesla, placing one of the largest corporate bitcoin positions in public markets under Musk’s control. That would deepen the legitimacy signal and broaden the passive-exposure dynamic, while also concentrating a very large bitcoin holding under one individual. It remains a speculative overhang instead of an announced event, but it is part of why the SpaceX listing drew so much attention from the crypto market.

Will other companies copy SpaceX and disclose bitcoin?

It is a real possibility but unconfirmed. SpaceX disclosed its bitcoin prominently in its prospectus, which some read as a deliberate pitch to bitcoin-correlated investors who might favor a stock with embedded crypto exposure. If that helped its reception, other large pre-IPO companies, including major technology and AI firms, could adopt the same template, disclosing bitcoin positions to court those allocators. Some commentators have speculated exactly that. If it became a trend, a series of large listings each carrying bitcoin would normalize the asset on corporate balance sheets far more than any single holding. For now it is a plausible hypothesis based on inference instead of announced plans, and whether companies actually copy it is the most important thing to watch from here.

This article is information, not financial or investment advice. Figures on SpaceX’s bitcoin holding, valuation, IPO terms, and related companies reflect reporting available as of June 30, 2026, are point-in-time, and can change. References to a possible Tesla merger and to other companies disclosing bitcoin are speculative and unconfirmed. Cryptocurrency and equities are volatile and you can lose money. Do your own research and consult a qualified financial professional before making any decision.

Crypto World

Cardano Price Prediction: ADA Is Stuck in a Tight Range While the “Ghost Chain” Label Keeps Circulating

Cardano price is trading near $0.1448, down roughly 0.94% in 24 hours, the coin stuck in a tight consolidation band rather than anything directional.

The ghost chain label keeps surfacing in bear-cycle discourse, and with ADA rangebound for weeks, it’s worth examining whether the criticism holds or whether the chart is simply pausing before the next move. There’s a key resistance level that determines everything from here.

The “ghost chain” critique targets blockchains that are technically live but generate negligible real-world activity. Cardano has faced this charge repeatedly, given its deliberate, peer-reviewed development cadence, which critics read as stagnation.

The counterargument is in the on-chain data: the network continues to process transactions, its developer community remains active, and ecosystem upgrades have continued shipping.

Layer 1s don’t survive a decade on name recognition alone. Cardano has. The question is whether that’s enough to drive price.

Broader crypto sentiment is calm right now, which cuts both ways for ADA, no macro tailwind, but also no macro headwind shaking weak hands loose. The price action is a technical story, not a fundamental one, and the technicals are at a decision point.

Can Cardano Price Break $0.1489 Resistance This Week?

ADA is consolidating between $0.1366 and $0.1550 with the most actionable cluster sitting between $0.1489 and $0.1518 on the upside. CoinLore’s near-term ceiling sits at $0.1521 with a floor at $0.1344, a range tight enough that a single exchange-level catalyst resolves the trade in either direction.

Three support tiers sit below current price at $0.1428, $0.1395, and $0.1366. Price is holding above the first level, which is constructive but barely. Volume has been tepid with no confirmation of accumulation or distribution in either direction.

ADA clearing $0.1489 on volume compresses toward $0.1518 to $0.1550 and shelves the ghost chain narrative for another cycle.

Consolidation continuing in the $0.1395 to $0.1489 band through the near term makes CoinCheckup’s $0.1455 target for July 30 the soft ceiling for cautious models.

A break below $0.1366 brings the $0.1344 floor into play and makes Binance’s longer-range model at $0.09645 for 2027 look less like an outlier. Invalidation of the bull case is clean: a daily close below $0.1344.

Coinbase’s model diverges sharply bullish at $0.49 for 2026 and $0.59 for 2030. That is either a major unpriced catalyst or aggressive extrapolation. Treat it as a ceiling scenario, not a base case.

Maxi Doge Targets Early Mover Upside as Cardano Tests Key Levels

ADA’s range-bound structure makes patience the trade. Meaningful upside exists but it is conditional on a breakout that has not materialized yet. Traders who want crypto momentum without waiting on a technical resolution are rotating into earlier-stage plays where the entry price itself provides the asymmetry.

Maxi Doge is one presale drawing that rotation.

Built on Ethereum as an ERC-20 meme token, the project leans hard into gym-bro trading culture with a 240-lb canine mascot and the tagline “Never skip leg-day, never skip a pump.” The branding is intentionally loud but the mechanics underneath are more structured than the meme framing suggests.

Holder-only trading competitions with leaderboard rewards give the community something to compete for beyond price speculation. A Maxi Fund treasury is allocated to liquidity and partnerships. Dynamic staking APY rewards holders for staying in.

The presale is currently priced at $0.0002826 with $4.82 million raised to date. That number signals real capital commitment rather than a ghost project.

Meme tokens carry significant risk. Liquidity and post-launch price discovery are always the critical unknowns. But for traders looking for asymmetric exposure while ADA grinds sideways, the entry price here is doing a lot of the work.

For traders who’ve done the work, research Maxi Doge here.

The post Cardano Price Prediction: ADA Is Stuck in a Tight Range While the “Ghost Chain” Label Keeps Circulating appeared first on Cryptonews.

Strategy has received another Wall Street price target cut after Canaccord lowered its valuation on the company while maintaining that Bitcoin’s long-term investment case remains intact.

Summary

- Canaccord cut Strategy’s price target to $130 but said its long-term Bitcoin investment thesis remains unchanged.

- The brokerage believes Strategy’s Bitcoin-focused business model is still viable if Bitcoin posts moderate annual gains.

- Other analysts, including TD Cowen, Cantor Fitzgerald, and Benchmark, continue backing Strategy despite lowering or maintaining price targets.

Bitcoin outlook remains intact despite lower valuation

According to a research note from Canaccord, the brokerage reduced its price target for Strategy to $130 from $163, citing the company’s prolonged share price decline rather than any change in its long-term view on Bitcoin. The revision comes as Strategy stock has struggled for months, even though the firm said its underlying investment thesis for the cryptocurrency remains unchanged.

Strategy shares closed the previous trading session at $86.93, only slightly above their 52-week low of $81.81 and roughly 77% below where they traded a year ago. The stock later rebounded 8.12% to $93.96 after the company introduced its new Digital Credit Capital Framework.

Canaccord said Bitcoin continues to benefit from limited supply and growing adoption of blockchain technology. The brokerage added that the cryptocurrency has become more established within financial markets and is no longer facing the same uncertainty over whether it should be viewed primarily as a speculative asset or a long-term store of value.

The firm also maintained that Strategy’s Bitcoin-focused corporate model remains workable as long as Bitcoin delivers moderate annual appreciation. At the same time, Canaccord acknowledged that recent market performance has fallen short of those expectations.

“We think there is nothing broken here, either in the company’s model or in bitcoin, which suggests a pendulum swing back makes sense sometime over the medium term.”

Separately, data cited in the report showed Strategy’s Relative Strength Index has moved into oversold territory, while Fair Value analysis suggested the shares could be trading below their estimated intrinsic value.

Capital strategy continues to receive support from analysts

The latest revision follows another recent target cut from TD Cowen, which, as previously reported by crypto.news, lowered its price target on Strategy to $260 from $400 while keeping a “buy” rating. According to TD Cowen, the lower valuation was driven by a more conservative long-term Bitcoin price forecast rather than concerns about Strategy’s newly introduced Digital Credit Capital Framework.

TD Cowen said its revised target still implies roughly 200% upside from current trading levels. The brokerage also described the new capital framework as a constructive step that could improve Strategy’s financial flexibility, even after the stock surrendered part of its initial gains following the announcement.

In a regulatory filing dated June 29, Strategy disclosed that its Digital Credit Capital Framework allows the company to raise up to $1.25 billion through Bitcoin sales if needed. According to the filing, those proceeds may be used to maintain U.S. dollar reserves, fund preferred dividend payments, meet interest obligations, strengthen cash balances, and finance future share repurchases.

The same filing also authorized up to $1 billion in repurchases of the company’s Digital Credit Securities, including STRC, STRF, STRD, and STRK, when management determines buybacks would improve the firm’s capital structure. Strategy further disclosed that it has paused additional Bitcoin purchases while selling about $1.15 billion worth of MSTR shares as part of its capital management plan.

Elsewhere on Wall Street, Cantor Fitzgerald reaffirmed its Overweight rating and $212 price target, citing confidence in Strategy’s liquidity plans. Benchmark also reiterated its Buy rating and maintained its $570 price target, noting that although the company’s preferred shares have weakened in recent months, Strategy has continued adding Bitcoin to its balance sheet.

Crypto World

Ark Invest bought more than $75 million of COIN, CRCL, BLSH shares during June bloodbath

Ark Invest has a tendency to load up on shares in cryptocurrency companies when their prices are depressed, and June was no exception.

Bitcoin , the largest cryptocurrency, recorded its worst month in four years, and digital asset firms’ share prices suffered accordingly, which Ark read as a buying opportunity.

The St. Petersburg, Florida-based investment manager bought $44 million worth of shares in crypto exchange Coinbase (COIN), based on the closing prices of the days on which purchases were made. It purchased $25.25 million worth of equity in Circle Internet (CRCL), issuer of the world’s second-largest stablecoin USDC, and $8.2 million worth of crypto exchange Bullish (BLSH), the parent company of CoinDesk, according to emailed disclosures.

Shares of Circle slumped 40% in June, ending the month at $62.63. The decline included an 18% drop on June 30 following the debut of rival stablecoin Open USD, which is backed by more than 140 companies, including Coinbase, Stripe, Visa, Mastercard and BlackRock.

COIN ended June just under 20% lower at $146.19, while BLSH fell 27% to $23.43.

The Winklevoss twins have transferred about $67 million worth of Bitcoin and Ethereum to Gemini wallets, with Arkham Intelligence identifying the transactions as matching their usual selling pattern.

Summary

- Arkham Intelligence flagged the Winklevoss twins’ $67 million Bitcoin and Ethereum transfers to Gemini as matching previous selloff patterns.

- Bitcoin remains under pressure as Citigroup cuts its price target and ETF outflows continue weighing on market sentiment.

- Ethereum holds near key support despite continued treasury purchases from SharpLink and Bitmine failing to offset whale selling.

According to blockchain analytics firm Arkham Intelligence, Cameron and Tyler Winklevoss moved roughly $60 million in Bitcoin (BTC) and another $7 million in Ethereum (ETH) from custody to hot wallets linked to the Gemini crypto exchange on July 1. Arkham characterized the transfers as consistent with the twins’ previous selloff behavior, although the firm did not confirm that the assets had already been sold.

The latest transfers come as Bitcoin and Ethereum continue trading under pressure following quarter-end selling and persistent weakness in investor sentiment. Recent price declines have also coincided with reduced expectations that the CLARITY Act will pass this year after U.S. President Donald Trump disclosed a $1.4 billion crypto-related windfall, a development some market participants have linked to shifting legislative expectations.

Since accumulating Bitcoin in 2015, the Winklevoss twins have realized about $1.7 billion in profit, according to Arkham Intelligence. Despite the latest transfers, they still control more than $300 million worth of Bitcoin. The July movement also follows earlier transfers to Gemini, including about $67.5 million in Bitcoin during June and another $130 million moved in March.

Bitcoin continues to face selling pressure

Citigroup has turned more cautious on the two largest cryptocurrencies, lowering its 12-month Bitcoin price target to $82,000 from $112,000 while reducing its Ethereum forecast to $2,240 from $3,175.

Bitcoin fell as low as $57,747 over the past 24 hours before recovering to trade near $58,600. Trading volume rose about 9% during the same period, while June recorded roughly $4.5 billion in net outflows from U.S. spot Bitcoin exchange-traded funds, adding to the pressure on market sentiment.

Commenting on current market conditions, crypto analyst Ted Pillows wrote, “Sellers are still dominating, while Coinbase Bitcoin Premium is at its lowest level this cycle.” He added that losing the $57,000-$58,000 support region could expose Bitcoin to a deeper decline toward the $50,000 level.

Ethereum buyers continue accumulating despite weakness

Ethereum has also remained under pressure even as several companies continue adding the asset to their corporate treasuries. As previously reported by crypto.news, quarter-end selling, whale distribution, and weak institutional flows have kept Ether pinned near the $1,500 support area despite ongoing buying from public companies.

Corporate accumulation has nevertheless continued. SharpLink recently disclosed the purchase of another 10,000 ETH at an average price of $1,611, spending about $16.1 million to expand its treasury.

Separately, Bitmine acquired 27,084 ETH over the past week, increasing its holdings to more than 5.7 million ETH. According to crypto.news, those purchases have so far failed to offset continued selling by whales and institutional investors.

Ether was trading around $1,572 at the time of writing, down about 1% over the past 24 hours after moving between an intraday low of $1,549 and a high of $1,600. Trading volume also declined during the session.

Crypto.news reported earlier today that the $1,500-$1,510 region remains Ethereum’s most important support zone. A break below that level would invalidate the current consolidation structure and could open the door to declines toward $1,400 before attention turns to the $1,200 area identified by several market participants.

US spot Bitcoin ETFs continued to see money leaving the funds on June 30, as investors pulled out $223 million – for the last nine days in a row. In total, the ETFs saw $4.51 billion exit during June, their biggest monthly outflows since launching in January 2024.

Tim Sun, Senior Researcher at HashKey Group, said that while the ETF outflows certainly reflect a weakening of marginal buying pressure for Bitcoin, the core issue isn’t just that ETF funds are flowing out – it’s where those outgoing funds are actually headed.

Bitcoin ETF Exodus

In a statement to CryptoPotato, Sun said that if investors were simply moving their funds into cash or short-term bonds, it would indicate a temporary shift toward safer assets while markets waited for macroeconomic uncertainty to ease. Instead, the researcher said that fund flows since the beginning of the year suggest that institutional investors are reallocating capital to sectors such as artificial intelligence (AI), semiconductors, and the GPU supply chain.

“The market hasn’t completely lost its risk appetite; rather, it is re-selecting its preferred risk assets.”

Sun explained that Bitcoin and AI-related stocks share several characteristics, such as long duration, high volatility, and high narrative elasticity. However, institutional investors currently favor the AI supply chain because companies in that sector are able to turn revenue and capital spending into business results much faster than Bitcoin can deliver returns through its investment narrative.

As a result, he believes the current ETF outflows should be viewed as a sign that Bitcoin’s short-term appeal has weakened compared with AI and semiconductor investments, rather than evidence that the long-term investment case for crypto has disappeared. Sun described the trend as a “capital reallocation within risk assets: Bitcoin’s marginal attractiveness is temporarily weaker than that of AI and semiconductors.”

At the same time, he noted that Bitcoin could attract institutional capital again if the AI trade becomes overcrowded and experiences a correction or if macro liquidity improves.

The Strategy Crisis

ETF outflows aren’t the only headwind for Bitcoin. Strategy, the largest corporate holder of BTC, also faces growing challenges in maintaining its financing model. Sun acknowledged that downside risks remain significant. He said the market’s main concern is not any single development but the simultaneous weakening of the two major sources of marginal buying demand that previously supported Bitcoin’s rally.

On one side, ETFs have shifted from consistent inflows to outflows, while on the other, the market is re-pricing the financing capacity of Strategy. Even so, Sun stressed that the company’s biggest risk is not necessarily that it will trigger a broader market sell-off, but that its ability to keep purchasing BTC at the same pace could decline.

“What truly needs to be observed is whether it will be forced to alter its financing cadence, replenish cash reserves, slow down its buying pace, or even pause purchases altogether.”

If Strategy pauses its buying, Sun stated that it “might not necessarily be a bad thing, because it means the previous distortion of true supply and demand – caused by Strategy’s financial flywheel model – will be alleviated.” In that case, he added Bitcoin would have the opportunity to establish price support based on genuine market demand instead of relying primarily on ETF inflows and Strategy’s purchases.

The post The Vanishing Bitcoin Bid: Where Are the ETF Billions Going? appeared first on CryptoPotato.

Edel said it detected and contained the exploit, then paused all of its version-one contracts, which remain frozen, and warned users not to interact with them.

The team added it had traced the attacker’s transactions and is coordinating with exchanges, and that it has offered the attacker a whitehat settlement, a deal that lets a hacker return most of the funds in exchange for a fee and no legal pursuit, within a set window.

No depositor will take a loss, Edel noted, with the team absorbing the bad debt and restoring balances one for one. It is deploying a version two with a redesigned pricing setup meant to block this kind of manipulation, and promised a full technical breakdown to follow.

While the amount is small, the method sits in one of DeFi’s most persistent categories of exploit.

Manipulating the price a protocol reads, rather than breaking into it, ranks as the second most common smart-contract vulnerability in the OWASP Smart Contract Top 10 vulnerabilities for 2025, and security researchers at CertiK describe oracle price manipulation as one of the field’s most common attack vectors.

Alongside cross-chain bridges, which produced the year’s largest single thefts, including the $292 million drained from Kelp DAO in April, price manipulation is where much of the money keeps going, and in most of these, the code works as written.

Key Takeaways

- Shares of SanDisk tumbled 9.44% during Tuesday’s session even as Bank of America issued an optimistic price target increase

- Bank of America elevated its SNDK price objective from $2,100 to $2,500 while reiterating its Buy recommendation

- BofA’s Wamsi Mohan anticipates average selling prices could surge as much as 35%, while bit growth may increase 13% sequentially

- The memory maker has soared 800% in 2024 and an eye-popping 4,755% over the trailing year, reaching a $323 billion market capitalization

- Valuation concerns include a forward price-to-earnings ratio of 33 — exceeding both Nvidia and Micron — alongside troubling technical indicators

SanDisk shares experienced a steep decline on Tuesday, surrendering 9.44% of their value during the trading session. The selloff occurred paradoxically on the very day that Bank of America Securities announced an upward revision to its price target, moving from $2,100 to $2,500.

Bank of America’s equity analyst Wamsi Mohan maintained his Buy recommendation on the shares. His optimistic thesis centers on the persistent mismatch between NAND flash memory supply and demand, a condition he anticipates will persist through 2027.

Mohan’s research indicates SanDisk’s average selling prices could experience gains of up to 35%. Additionally, he projects bit growth — representing the total volume of memory units delivered — will expand by 13% on a sequential quarter basis.

Using these assumptions as a foundation, Bank of America now forecasts that SanDisk will report $9.1 billion in revenue for the June quarter alongside earnings per share of $37.01. These projections exceed the Street’s current consensus estimates of $8.35 billion in revenue and $34.26 in EPS.

For the subsequent quarter, BofA’s model anticipates revenue reaching $11.5 billion with EPS climbing to $48.55.

Multi-Year NAND Supply Deals Enhance Earnings Predictability

A critical element supporting Mohan’s optimistic outlook involves SanDisk’s strategic emphasis on securing long-term NAND supply agreements, referred to as NBMs. These multi-year commitments guarantee future revenue streams and provide greater clarity for investors modeling future profitability.

Bank of America anticipates widespread adoption of these contractual arrangements among cloud infrastructure providers and enterprise clients. The investment bank also highlighted that these agreements are designed to preserve gross margin levels within SanDisk’s established target parameters.

This strategic pivot has contributed significantly to SanDisk’s extraordinary market performance. The stock has skyrocketed 800% since the beginning of the year and an astonishing 4,755% over the past twelve months. This explosive growth has transformed what began as a Western Digital spinoff into a company valued at $323 billion.

The bullish sentiment extends beyond Bank of America. Mizuho Securities increased its target from $1,825 to $2,200. Cantor Fitzgerald established an even higher objective at $2,900. Susquehanna Financial Group represents the most aggressive bull case with a $3,250 price target.

The analyst community’s consensus rating stands at Strong Buy — featuring 14 Buy ratings, two Hold ratings, and zero Sell recommendations over the most recent three-month period. The mean price target across all analysts sits at $1,979.38, suggesting approximately 3% downside from present trading levels.

Growing Concerns About Valuation and Market Dynamics

Notwithstanding the widespread analyst enthusiasm, multiple risk factors deserve consideration — and Tuesday’s sharp decline serves as a cautionary reminder.

SanDisk’s forward price-to-earnings multiple has expanded to 33 times, surpassing Nvidia at 22 times and Micron Technology at 18 times. This valuation premium has begun attracting scrutiny from market participants.

Supply-side dynamics present another concern. Elevated memory pricing could incentivize rival manufacturers including Micron, Kingston Technology, and Kioxia Holdings to accelerate production capacity, which would ultimately exert downward pressure on pricing.

From a technical analysis perspective, the weekly chart reveals a bearish divergence in the Relative Strength Index. The RSI has been declining even as the stock price has continued advancing — a formation that frequently precedes price corrections.

The equity currently trades at $2,238, substantially above its 50-day moving average of $1,458.

Bitcoin has climbed back above $60,000 after Federal Reserve Chair Kevin Warsh declined to signal the direction of future interest rate decisions during an ECB policy discussion.

Summary

- Bitcoin rebounded above $60,000 after Fed Chair Kevin Warsh declined to signal the future path of interest rates.

- CME FedWatch shows markets still expect rates to remain unchanged in July despite lingering inflation concerns.

- Polymarket continues to price in a chance of a 2026 rate hike, while Morgan Stanley expects rates to stay on hold this year.

According to data from crypto.news, Bitcoin (BTC) traded around $60,175 at the time of writing after rebounding about 3% from an intraday low below the key $58,000 level. The move followed comments from Warsh, who again avoided offering forward guidance on monetary policy while reiterating that future decisions will depend on incoming economic data.

Bitcoin rebounds as Warsh avoids policy signals

Speaking during an ECB Forum panel, Warsh declined to say whether the Federal Reserve would raise interest rates at the July Federal Open Market Committee meeting. Instead, he repeated the position he adopted after taking office that the central bank would not pre-commit to future policy moves and would continue responding to economic data as it becomes available.

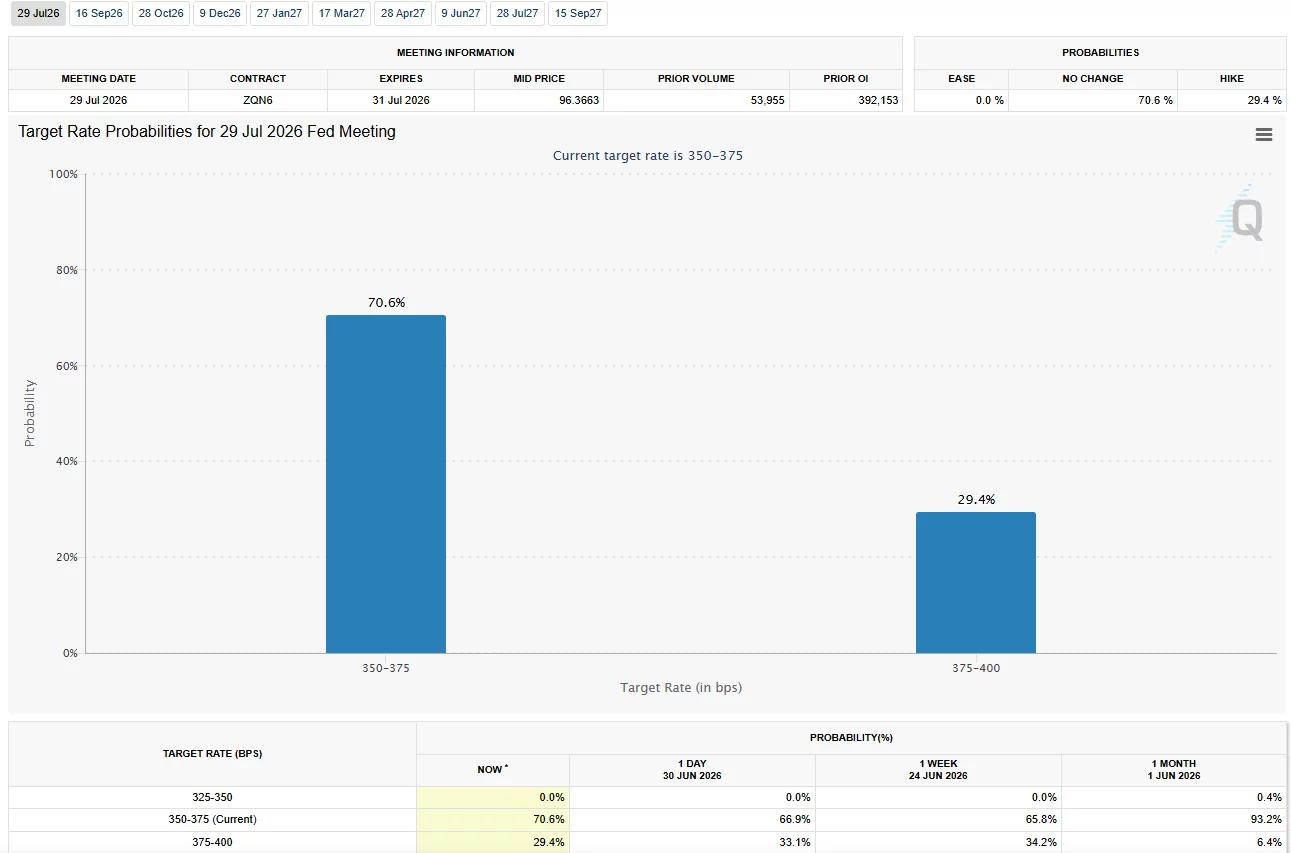

His remarks came as traders largely continued to expect no change in interest rates later this month. According to CME FedWatch data, markets currently assign a 70.6% probability that the Federal Reserve will leave rates unchanged at the July FOMC meeting.

Warsh also addressed inflation, saying expectations had declined during the first four weeks of the recent period despite concerns tied to the U.S.-Iran conflict. He added that inflation risks had eased while reaffirming the Federal Reserve’s commitment to returning inflation to its 2% target.

As crypto.news reported after the June FOMC meeting, Warsh also left rates unchanged at that gathering. Bitcoin fell to around $65,430 following the decision, while Ethereum traded near $1,770. The Federal Reserve’s updated projections at the time showed that nine policymakers expected at least one rate increase before the end of the year.

Those projections have continued to shape market expectations even after Warsh reiterated at the ECB Forum that future policy decisions would depend on incoming economic data.

Rate hike expectations continue to pressure crypto

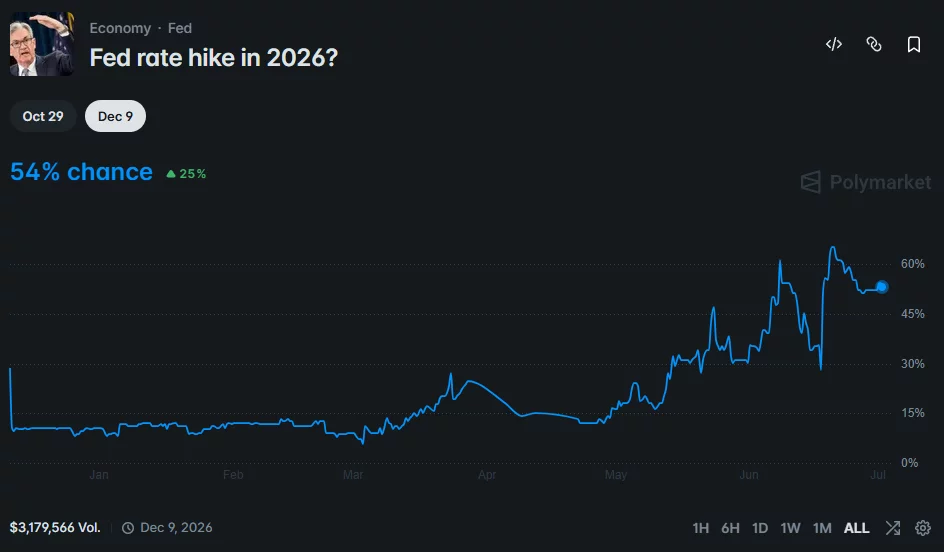

Although traders see little chance of a July rate increase, expectations for additional tightening later this year have not disappeared. According to Polymarket data, there is currently a 54% probability that the Federal Reserve will raise interest rates before the end of 2026.

Higher borrowing costs have generally remained a headwind for cryptocurrencies because elevated interest rates tend to support demand for cash and short-term fixed-income assets over riskier investments such as Bitcoin.

Separate reporting by crypto.news also noted that Morgan Stanley expects the Federal Reserve to keep rates unchanged through the rest of the year. The bank nevertheless warned that rate hikes could return if inflation remains persistent or if the unemployment rate falls further.

Outside monetary policy, another source of uncertainty for Bitcoin has come from corporate supply. As previously reported by crypto.news, the possibility that Strategy could sell as much as $1.25 billion worth of Bitcoin has remained one factor contributing to selling pressure in the market.

Political attention has also stayed on Federal Reserve policy. Before Warsh became chair, President Donald Trump repeatedly called for lower interest rates. After the June decision to keep rates unchanged, however, Trump responded without strong criticism and continued to praise the new Fed chair while receiving no timeline for future rate cuts.

The downgrade marks a sharp reversal from Citi’s previous outlook, which assumed passage of U.S. digital asset market structure legislation would spur adoption among financial advisors and traditional investors. The bank now believes that timeline has slipped, leaving the market without a meaningful catalyst.

Saunders said ETF flows continue to be the main force behind crypto prices, with recent demand turning negative as investors pulled back from risk.

According to the bank’s analyst, sentiment has also been hurt by concerns that digital asset treasury (DAT) companies could become net sellers of bitcoin. Recent corporate actions by Strategy amplified those fears despite involving relatively modest BTC sales.

The report noted that bitcoin and ether both remain below key technical levels, including their 200-day moving averages, while speculative capital has shifted toward AI-related investments.

The bank’s revised forecasts assume flat ETF flows in its base case. In its bull case, stronger retail and institutional adoption lifts bitcoin to $108,000 and ether to $2,932. Its bear case, based on recessionary macro conditions and continued ETF outflows, sees BTC falling to $53,000 and ETH to $1,094.

While the bank’s equity strategists have become more constructive on U.S. stocks, providing some support through crypto’s equity correlation, the report said that positive macro factors are insufficient to offset weakening flows.

A new independent non-profit, Ethereum Institutional, has launched with the goal of accelerating institutional adoption of Ethereum, its layer-2 networks and the broader ecosystem.

The organization is led by David Walsh, Marius Smith and Matthew Dawson. Walsh previously led the Ethereum Foundation’s enterprise efforts, while the organization said its leadership brings experience spanning institutional engagement, capital markets and Ethereum ecosystem development. It said its mission is to provide institutions with a neutral, independent point of contact as they evaluate Ethereum for tokenization, stablecoins and other onchain financial infrastructure.

In announcing the initiative on X, Ethereum Institutional said institutions need “a credible, independent front door” to the Ethereum ecosystem. While Ethereum’s neutrality is one of its defining strengths, the group argued, that neutrality has often left enterprises without a clear organization to engage as they make long-term infrastructure decisions.

The launch comes as the Ethereum Foundation continues to narrow its role to stewarding the core protocol, with ecosystem participants increasingly spinning up independent organizations focused on specific areas such as business development, institutional outreach and developer support. The shift follows broader changes at the foundation, including leadership restructuring and longstanding community calls for greater transparency.

Cardano Price Prediction: ADA Is Stuck in a Tight Range While the “Ghost Chain” Label Keeps Circulating

Inside the Royal Family Rift Divide Ahead of Harry’s Visit

Why isn't Donald Trump at the US match against Bosnia?

![BIS Just Gave XRP Holders Another Massive Clue! The XRP Connection Is Impossible To Ignore! [INSANE]](https://wordupnews.com/wp-content/uploads/2026/07/1782927079_maxresdefault-80x80.jpg)

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics5 days ago

Politics5 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World2 days ago

Crypto World2 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics6 days ago

Politics6 days agoPotential 2028er World Cup attendee leaderboard

-

Business5 days ago

Business5 days agoAsia stock markets slide as tech shares slump

-

News Videos3 days ago

News Videos3 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech6 days ago

Tech6 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World4 days ago

Crypto World4 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business2 days ago

Business2 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World5 days ago

Crypto World5 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports5 days ago

Sports5 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World6 days ago

Crypto World6 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech4 days ago

Tech4 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech4 days ago

Tech4 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World5 days ago

Crypto World5 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World5 days ago

Crypto World5 days agoRTX holders must register wallets before token distribution begins

-

Crypto World7 days ago

Crypto World7 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

-

Tech2 days ago

Tech2 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Sports5 hours ago

Sports5 hours agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

You must be logged in to post a comment Login