Crypto World

ETF Outflows, Liquidations Leave Crypto Thinner for Q3

Cryptocurrency markets entered the third quarter of 2026 with less leverage but thinner liquidity after a wave of liquidations cleared speculative positions while major sources of demand weakened during the second quarter.

According to a market update from institutional data provider Talos, Bitcoin (BTC) and Ether (ETH) long liquidations totaled $8.35 billion in Q2. The data provider pointed out that the deleveraging coincided with spot Bitcoin exchange-traded fund (ETF) outflows, reduced Bitcoin buying by Strategy and a contraction in stablecoin supply.

While the reset left the market more stable heading into Q3, Talos said reduced order-book depth weakened its ability to absorb renewed selling pressure. This means the market could be less vulnerable to a chain reaction of forced selling, but prices may still swing sharply because there’s less trading activity to absorb large orders.

Cross-asset performance chart. Source: Talos

At last look on Wednesday, Bitcoin was trading hands at $58.656, after trading earlier in the day to $57,742, its lowest price since Sept. 17, 2024.

Talos said the liquidation wave reduced the amount of leveraged money in the market. Bitcoin open interest, which measures the value of outstanding derivatives contracts, fell to $33.5 billion, down 32% from its Q2 peak, while Ether open interest dropped to $16.2 billion, a 40% decline, according to the data provider.

Related: Swan’s Cory Klippsten sees record Bitcoin holder supply revealing early bottom

To be sure, the market became less liquid: Bitcoin’s 2% order-book depth, the value of buy and sell orders close to its market price, fell to between $35 and $40 million by late June from about $70 million in early May. Spot exchange volume also declined 28% quarter-over-quarter to $2.32 trillion, according to Talos.

ETF outflows and Strategy slowdown weigh on demand

Weakening demand was evident before the end of Q2. US spot Bitcoin ETFs recorded $696.3 million in net outflows in a single day on June 25. In total, June recorded about $4.5 billion in outflows, pushing year-to-date totals to $5.5 billion.

Strategy also purchased roughly 3,600 BTC in June, down from about 25,000 BTC in May and more than 50,000 BTC in April, according to company disclosures. The company also recorded a net sale of 32 BTC earlier in June and ended the month with 847,363 Bitcoin in its treasury, purchased at an average price of $64,103 apiece.

Magazine: Japanese pension fund tips 1% in crypto, G7 urges action on NK hackers: Asia Express

Binance has been hit with a £150 million ($200 million) lawsuit, accusing it of offering illegal derivative products, just one day before the exchange is due to exit EU markets.

Almost 1,700 British investors joined together to file the lawsuit in London’s High Court yesterday, claiming it offered risky derivative products without permission from the UK’s financial regulator, the FCA.

Investors claim to have lost tens of thousands, and in some cases millions, on derivatives offered between 2019 and 2020 while the exchange was under the leadership of its former CEO and founder, Changpeng Zhao.

A KP Law partner told the Financial Times, “Our clients are ordinary people, many of whom committed significant savings and who have suffered real financial harm. We are determined to hold Binance and its founder, Changpeng Zhao, to account.”

The exchange said it will “defend against these claims through the appropriate legal process in due course. Binance remains committed to its obligations to users and to operating in accordance with applicable law.”

Defendants in the lawsuit include Zhao, Binance’s Cayman Islands entity, the UAE-registered Nest Exchange, and unknown persons operating the Binance Trading Platform.

Time’s up for Binance in the EU

The lawsuit was filed just one day before Binance has to remove its operations from EU territories today, due to its failure to secure a license under the bloc’s Markets in Crypto-Assets Regulation (MiCA).

Binance had originally been earmarked to secure a license from Greece and believed it was compliant with MiCA regulations. It then withdrew its application on June 26 and claimed it would pursue a different EU member state.

According to The Block’s Gareth Jenkinson, European Central Bank President, Christine Lagarde, “directly ordered Greece to reject Binance’s MiCA license application.”

Jenkinson’s undisclosed source claimed Binance had “essentially been given the green light by Greece’s regulator, before the ECB stepped in.”

Read more: Binance probed by DoJ, files lawsuit against WSJ

Zhao claimed in an interview with Jenkinson that two EU countries were vying for Binance’s application until political forces intervened.

Despite the setback, Binance Head of Europe and the UK, Gillian Lynch, boldly claimed, “Binance is not leaving Europe.”

Binance CEO Richard Teng also said the company is committed to securing a license “in the coming months.”

However, it appears Binance has failed to find another welcoming EU country in time for the July 1 MiCA deadline, which it’s had six years to prepare for.

The exchange has stressed that any impacted users will still have access to withdraw their funds.

Teng added today, “Please know that we are working hard behind the scenes, including in close engagement with regulators, to navigate this transition responsibly and to continue serving our users in the best way possible.”

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

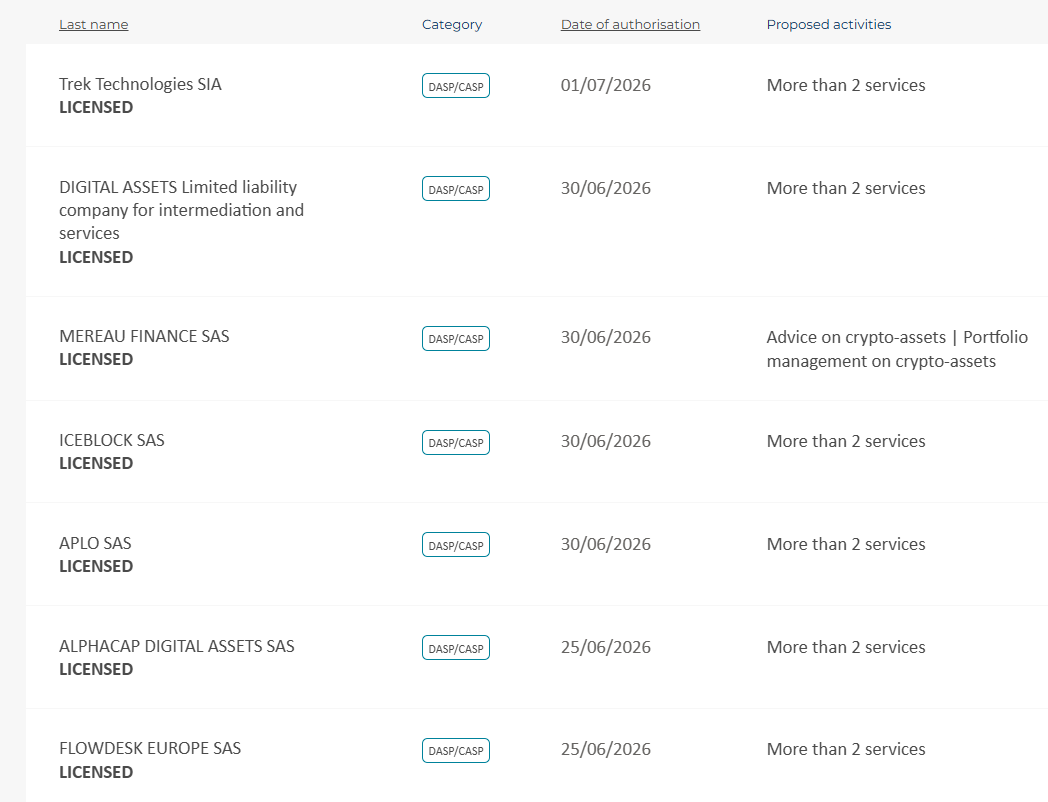

A slew of last-minute licenses were issued to cryptocurrency companies in Europe as Wednesday marked the end of the transitional period under the Markets in Crypto-Assets Regulation (MiCA).

Four companies were authorized in Italy this week, including asset management platform Hodlie, crypto exchange Young Platform, trading platform CryptoSmart and crypto service provider Hercle, bringing Italy’s total to eight authorized crypto asset service providers (CASPs), according to a Tuesday announcement from the Bank of Italy. The central bank said the country’s financial regulator, Consob, approved the licenses in coordination with it.

The French financial markets regulator, Autorité des marchés financiers (AMF), also added three new companies on Tuesday, including crypto investment platform Mereau Finance, blockchain infrastructure provider Iceblock and crypto service provider Aplo, bringing the total number of licensed CASPs to 31.

In Malta, digital asset prime broker FalconX announced Monday that it had received a MiCA license, while Venga announced on Wednesday that it had received CASP authorization from Spain.

The licenses were issued during the final stretch of MiCA’s 18-month transitional period, which ended on Wednesday. By Friday, the European Securities and Markets Authority’s (ESMA) interim register showed 244 authorized CASPs across the European Union and European Economic Area.

France’s whitelist includes newly licensed CASPs. Source: AMF

Related: Polish president vetoes crypto bill for third time ahead of MiCA deadline

Largest MiCA-authorized exchanges emerge as transition ends

Binance, the world’s largest crypto exchange by trading volume, remains unlicensed under MiCA. The exchange applied for authorization in Greece but later withdrew its application, saying it will seek authorization in another member state.

Greece is among the EU member states that have yet to issue a MiCA license.

On June 23, the European Securities and Markets Authority (ESMA) said crypto service providers that remain unauthorized by the deadline must take “immediate” steps to wind down their EU activities.

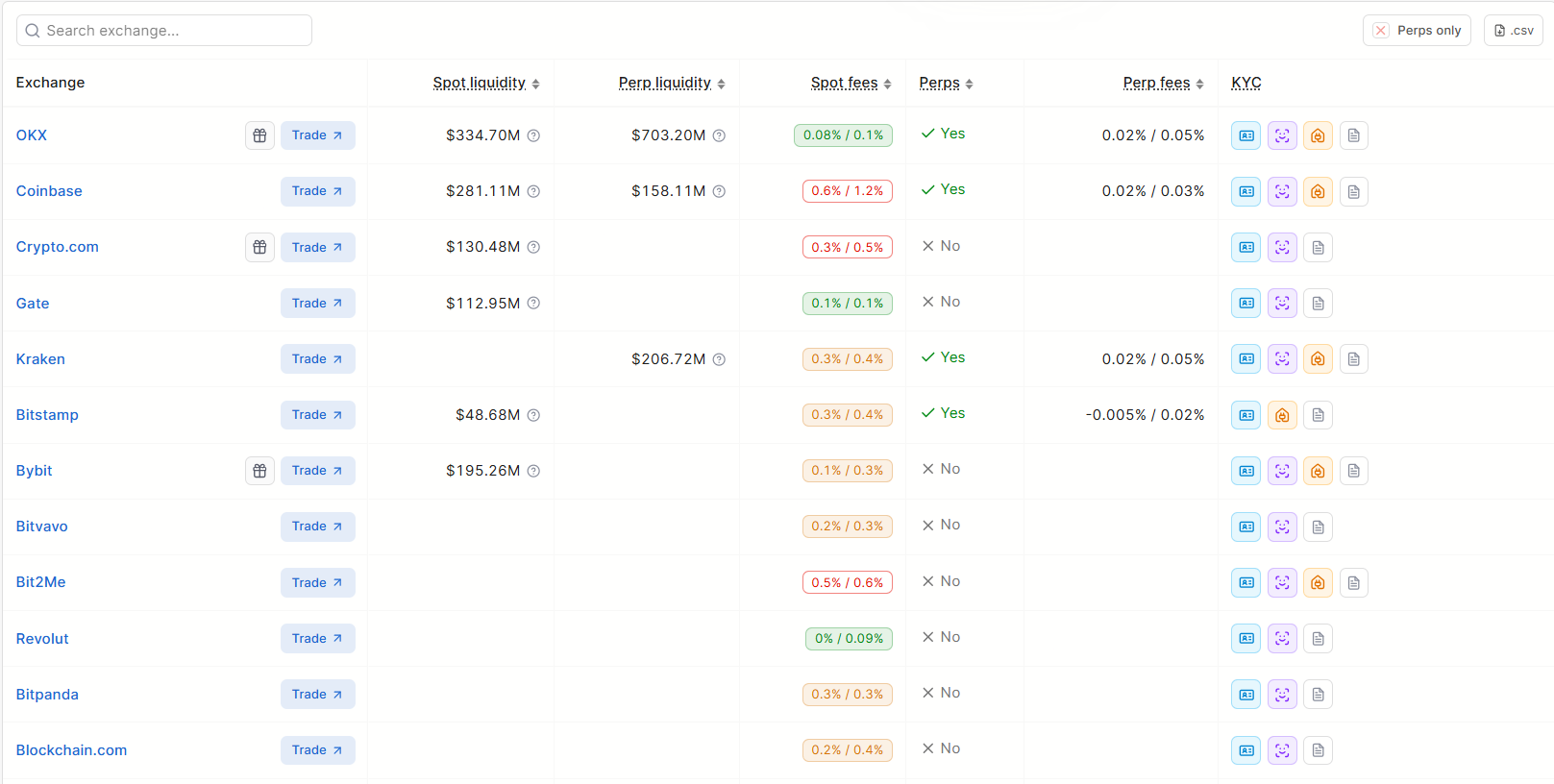

With Binance remaining unlicensed under MiCA, the largest MiCA-authorized exchanges by spot orderbook liquidity include OKX, Coinbase, Bybit, Crypto.com, Gate and Bitstamp, according to DefiLlama data.

MiCA-regulated cryptocurrency exchanges in Europe. Source: DefiLlama

Magazine: Crypto wanted to overthrow banks, now it’s becoming them in stablecoin fight

The assumption is simple: Ripple goes public, XRP moons. The reality is that Ripple equity and the XRP token are different assets, and the channels connecting them are weaker than the hype suggests.

Summary

- Ripple remains private with no S-1 on file, but a $750 million buyback fixed its valuation near $50 billion and private secondary shares have surged to about $136.90, keeping IPO speculation loud.

- Ripple equity and the XRP token are legally separate: owning XRP gives no claim on the company, and a public listing would not hand shareholders or token holders any automatic link between the two.

- The plausible transmission channels are sentiment, Ripple’s escrow and sell behavior, institutional validation, and value accrual, and each is weaker or more two-sided than the “IPO equals XRP moon” story assumes.

- There is a real counter-case that an IPO could pull capital away from XRP, by giving investors who want Ripple exposure a way to buy the stock instead of the token.

- The evidence so far is mixed: XRP briefly re-coupled to Ripple’s rising private valuation, yet the token is still down about 26% on the year, which points to weak, not strong, transmission.

The reflex in the XRP community is automatic. Ripple goes public, the story goes, and XRP rockets alongside it. The logic feels obvious, because Ripple and XRP are wrapped together in the same brand, the same headlines, and the same decade of shared history. But an initial public offering sells shares in a company, and XRP is a token that confers no ownership of that company.

Whether a Ripple listing would actually move the token is not a matter of sentiment or loyalty. It is a question of mechanism: through what channels, if any, would value flow from a Ripple equity event into the XRP price? This piece examines those channels one by one, and finds them thinner than the hype implies. The XRP holder payout question has already become a separate community obsession, but the XRP holder payout question is not the same as a price-transmission mechanism.

The starting point: Ripple equity and XRP are different assets

Everything begins with a distinction the excitement tends to blur. Ripple Labs is a private company. XRP is a digital asset that trades on public exchanges. There is no mechanism that entitles an XRP holder to Ripple shares, dividends, or any slice of the company’s profits, and a public listing would not create one.

If Ripple lists tomorrow, an XRP holder owns exactly what they owned the day before: a token, not a piece of the business. The one concrete link runs the other direction. Ripple is itself one of the largest holders of XRP, with tens of billions of tokens held in escrow that it releases on a schedule and uses, in part, to fund operations. So the company’s relationship to the token is that of a giant holder and periodic seller, not a value conduit that passes equity gains down to token holders.

That asymmetry matters for the whole analysis. When people say an IPO would help XRP, they are really claiming that something about Ripple becoming public would change demand for, or supply of, the token. The rest of this piece tests each version of that claim. Until then, Ripple equity and XRP should be treated as related but legally separate assets, not two versions of the same exposure.

Channel one: sentiment and attention

The first and most immediate channel is psychological. An IPO would be a media event, a wave of coverage, analyst notes, and credibility that reframes Ripple from a litigation-scarred crypto firm into a public company vetted by underwriters and public markets. In a market where attention is a real driver of price, that halo could spill onto XRP, lifting the token on narrative even without any mechanical connection. That is the channel the community understands instinctively, because XRP has always traded partly on Ripple headlines.

There is some evidence this channel is live. When Ripple’s private secondary shares surged, one analysis linked the move to XRP briefly re-coupling with the company’s rising valuation, as the market started treating the private-share price near $136.90 as a fundamental signal for the token. That is the sentiment channel working in real time: a Ripple equity data point moving XRP through association rather than mechanics. It is also why where XRP could go from here depends partly on whether traders treat corporate news as a catalyst or just another temporary headline.

The limit is that sentiment is fickle and shallow. It can lift a token into an event and drop it just as fast afterward, and it does not build the sustained demand that holds a price up. A narrative bump around an IPO is plausible. A durable re-rating on sentiment alone is not, which is why this channel, while real, is the weakest foundation for a lasting move.

Channel two: Ripple’s escrow and sell behavior

The most underappreciated channel runs through Ripple’s own balance sheet. Because Ripple holds a vast XRP escrow and sells tokens to help fund itself, anything that changes the company’s need to sell XRP changes the supply hitting the market. This is where an IPO could actually matter mechanically. A successful listing would raise cash and give Ripple a public currency, its own stock, to fund acquisitions and operations.

A cash-rich, publicly funded Ripple might lean less on programmatic XRP sales, easing a source of sell pressure that has weighed on the token for years. That is a genuine, if indirect, bullish path. Less selling from the single largest holder is a supply-side positive that does not depend on sentiment. It is the most concrete way an IPO could help XRP.

The two-sided catch is disclosure. Going public subjects Ripple to far heavier reporting requirements, which means the escrow, the sales, and the token’s role in Ripple’s finances would face new scrutiny from public-market investors and regulators. Greater transparency could reassure the market, or it could surface uncomfortable details about how much the company depends on token sales, which would cut the other way. The escrow channel is the strongest mechanical link, but its direction is not guaranteed.

Channel three: institutional access and validation

The third channel is legitimacy. A public Ripple would sit inside the regulated financial system in a way it does not today, and that validation could radiate outward to the whole XRP ecosystem. The backdrop already leans this way: XRP was recognized as a commodity in March, and seven spot XRP exchange-traded funds are trading with roughly $1.43 billion in cumulative inflows. A high-profile Ripple listing would add another layer of institutional acceptance, potentially making allocators more comfortable holding XRP through regulated products.

The argument is that validation compounds. Each step that moves XRP from contested asset toward accepted infrastructure lowers the barrier for the next institution, and a Ripple IPO would be a large step. In a world where the token already has ETF access, a public parent company strengthens the case that the ecosystem is durable. That is also why XRP’s regulatory status matters more than the IPO hype itself: institutions care less about community excitement than about whether the asset can be held cleanly under durable rules.

The weakness is that validation of the company is not the same as demand for the token. Institutions can conclude that Ripple is a fine investment and express that view by buying the stock, which does nothing for XRP. Legitimacy is a soft tailwind, helpful at the margin, but it does not force anyone to buy the token. For a durable move, validation has to become measurable token demand, not just a better story around the issuer.

Channel four: the value-accrual problem

This is the channel that breaks the simple story, and it is the most important. For an IPO to lift XRP durably, Ripple’s commercial success has to translate into demand for the token. But Ripple’s business and XRP’s value are only loosely coupled. Many of Ripple’s bank and payment partners use its software without touching XRP at all, and the company earns revenue from services, licensing, and acquisitions that do not route through the token.

Ripple can thrive as a company while XRP stagnates, because the token’s value depends on settlement usage and demand for XRP itself, instead of on Ripple’s profit and loss. This value-accrual gap explained is the reason a Ripple IPO is not the guaranteed catalyst holders imagine. An IPO rewards equity holders for the company’s success. It does not, by itself, create the on-chain demand that would lift the token.

Unless a listing changes how much XRP is actually used to move value, the mechanical link from Ripple’s public-market performance to the XRP price is faint. The token needs its own demand story, and the IPO does not write one. It may make Ripple more visible, more credible, and more valuable. None of that automatically makes XRP more scarce or more necessary.

The counter-case: an IPO could hurt XRP

The overlooked possibility is that a Ripple listing works against the token. For years, buying XRP was one of the only ways for a public investor to express a view on Ripple’s success. An IPO removes that constraint by offering the pure play: if you want exposure to Ripple, you buy the stock, which actually owns the business, the revenue, and the growth. The token, which owns none of that, becomes the inferior vehicle for a Ripple bet.

That substitution could siphon capital and attention away from XRP toward the equity. Some of the speculative demand that flowed into the token as a Ripple proxy would rationally rotate into shares once shares exist. In this reading, the IPO does not transmit value to XRP at all. It competes with it.

The very event the community treats as the catalyst could turn out to be a drain, redirecting the Ripple trade into a security that leaves the token behind. That does not mean XRP must fall on a Ripple IPO. It means the direction is not obvious, because the listing creates both a halo effect and a substitute asset. The market would have to decide whether XRP remains the best way to trade Ripple’s ecosystem once Ripple stock exists.

What the evidence shows so far

The cleanest test available is how XRP has behaved as Ripple’s private valuation has climbed. The answer is telling. Ripple’s secondary shares surged to about $136.90 and its valuation was fixed near $50 billion, and while XRP did briefly re-couple to that move on sentiment, the token still trades near $1, down roughly 26% on the year. If the transmission were strong, a 376% surge in Ripple’s private-share price should have dragged XRP sharply higher.

It did not. The token acknowledged the news and kept falling with the broader market. That is the empirical verdict: transmission exists, but it is weak. Ripple getting more valuable has not made XRP more valuable in any durable way, which is exactly what the value-accrual analysis predicts.

An actual IPO would be a bigger event than a private-share revaluation, so the sentiment bump could be larger. But the underlying mechanics that limited the private-market spillover would still apply to a public one. The stock would price Ripple’s business, while XRP would still need regulatory clarity, ETF flows, settlement usage, and broader market support. The link is real enough for traders to chase, but not strong enough to treat as automatic.

What would actually move XRP

If the IPO is a weak lever, what is a strong one? The catalysts that genuinely drive XRP are the ones that change token demand or supply directly. Regulatory outcomes rank first: whether crypto market-structure legislation codifies XRP’s status cleanly, which affects how freely institutions can hold it. ETF flows rank second, because sustained inflows into the seven XRP funds are real, measurable demand for the token.

Settlement usage ranks third: whether XRP is actually used to move value at scale, against the escrow supply that keeps entering the market. That is where XRP fits in settlement becomes more important than the IPO narrative. XRP needs recurring use as a bridge asset or liquidity tool, not just Ripple’s name in public-market headlines. And the direction of Bitcoin and the broader market ranks alongside all of them, since XRP rarely fights the tape.

Against those, a Ripple IPO sits at the edge of the picture. It could add a sentiment bump, it could ease Ripple’s XRP selling, and it could burnish the ecosystem’s legitimacy. Each is a real but modest channel, and at least one plausible effect points the wrong way. The honest conclusion is that a Ripple IPO would be a meaningful corporate event that most likely moves XRP far less than the community expects, and possibly not in the direction they assume.

The Coinbase and Circle precedent

The clearest way to test the transmission question is to look at crypto-adjacent companies that already trade publicly, because they show what happens when a company and the tokens around it are separated on public markets. Coinbase is the obvious case. Its stock gives investors exposure to the exchange’s revenue, which rises and falls with trading volume, but owning the stock is not the same as owning the assets that trade on it. When crypto rallies, Coinbase revenue tends to rise, so there is a loose correlation, yet the stock and the broader token market frequently move apart, because the equity is priced on the business and the tokens are priced on their own supply and demand.

Circle offers a sharper version of the lesson. Circle issues the USDC stablecoin, but USDC is a dollar-pegged token that does not float, so Circle equity captures the value of the issuing business, the reserves, the yield, the growth, while the token itself is designed to stay at a dollar. The company can be worth a great deal while the token it issues, by construction, accrues none of that equity value. That is the extreme illustration of the point: a token and its issuer’s stock can be almost entirely decoupled.

XRP sits somewhere between these cases. It is not a dollar peg, so it can appreciate, but it is also not an equity claim on Ripple, so it does not capture the company’s growth the way shares would. Even when Ripple-linked infrastructure appears in real capital-markets events, such as stablecoin settlement using RLUSD on the XRP Ledger, the immediate value still tends to accrue to the rails, the issuer, or the company before it accrues to XRP itself. The precedent from public crypto companies is that the market prices the business and the token separately, and a listing that rewards the equity does not automatically reward the associated token.

A Ripple IPO would most likely follow the same script, with the stock absorbing the value of the business while XRP continues to trade on its own drivers. That does not make the IPO irrelevant. It makes it indirect. The market would finally have a clean way to buy Ripple, and that could clarify how much demand for XRP was really token demand versus company-proxy demand all along.

What a realistic IPO scenario looks like for XRP

It helps to walk through how an actual Ripple listing would probably play out for the token, stage by stage, because the timeline reveals where the modest effects concentrate. In the announcement phase, when Ripple confirms an S-1 or a date, expect a sentiment spike: headlines, community excitement, and a short-term bid in XRP as traders position for the event. This is the sentiment channel firing, and it could produce a sharp but shallow move that fades as the news is absorbed.

In the run-up to the listing, attention would build, and XRP could trade with elevated volatility as speculation swings between the “IPO lifts XRP” and “IPO competes with XRP” theses. Some capital that had been using XRP as a Ripple proxy might already begin rotating toward the anticipated equity, capping the token’s upside even amid the excitement. The listing itself would be an equity event: shares price, the stock trades, and the value of Ripple’s business gets marked by the market. XRP would react mostly to the tone, a strong debut lifting sentiment, a weak one dampening it, rather than to any mechanical flow.

In the aftermath, the durable question resurfaces: does anything about a public Ripple change token demand or supply? If a cash-rich Ripple eases its XRP selling, that supply relief could support the token over time, the most concrete lasting benefit. If investors conclude the stock is the better Ripple bet, capital could keep rotating out of XRP into shares. The realistic net is a sentiment-driven spike around the event that mostly fades, a possible modest supply-side benefit if Ripple sells less XRP, and an ongoing competitive pull from the equity.

That is a meaningful corporate story with a muted and two-sided token effect, which is a long way from the moonshot the community pictures. The IPO could matter. It just would not erase the legal separation between the company and the token. XRP would still need its own demand engine.

Frequently asked questions

Does owning XRP give you a stake in Ripple?

No. XRP is a digital token that trades on public exchanges and confers no ownership of Ripple Labs, no shares, no dividends, and no claim on the company’s profits. Ripple the company and XRP the token are legally separate. A Ripple IPO would sell shares in the business, and holding XRP would give you no automatic right to those shares or their gains.

Has Ripple actually filed to go public?

Not as of late June 2026. Ripple remains private with no S-1 on file and no confirmed date, and executives have repeatedly downplayed the urgency of a listing. The speculation is driven by signals such as a $750 million share buyback that fixed the valuation near $50 billion and a surge in private secondary shares to about $136.90, not by an official filing. That distinction matters because IPO speculation can move sentiment long before any legal filing exists.

Could a Ripple IPO raise the XRP price?

It could, through weak and indirect channels. A listing could lift XRP on sentiment, could ease sell pressure if a cash-rich public Ripple relies less on XRP sales, and could add legitimacy to the ecosystem. None of these is a mechanical guarantee, and the evidence so far shows only faint transmission from Ripple’s rising valuation to the token. The stronger catalysts are still regulatory clarity, ETF flows, and actual XRP settlement usage.

How could an IPO hurt XRP?

By offering a substitute. An IPO would let investors who want Ripple exposure buy the stock, which actually owns the business, instead of the token, which does not. Some speculative capital that flowed into XRP as a Ripple proxy could rotate into the equity once it exists, redirecting demand away from the token rather than toward it. That is why a Ripple IPO is not automatically bullish for XRP.

What is the value-accrual problem?

It is the gap between Ripple’s success and XRP’s value. Many Ripple partners use its software without touching XRP, and much of its revenue does not route through the token. So Ripple can prosper as a company while XRP stagnates, because the token’s value depends on settlement usage and its own demand, not on Ripple’s profit and loss. This is why an IPO is not a guaranteed catalyst.

Did XRP move when Ripple’s private valuation rose?

Briefly and weakly. When Ripple’s secondary shares surged to about $136.90, one analysis linked it to XRP re-coupling with the valuation on sentiment. But XRP still trades near $1, down about 26% on the year, so a large rise in Ripple’s private-share price did not drag the token durably higher. That points to weak transmission between the two.

What actually drives the XRP price?

The strongest drivers are regulatory clarity on XRP’s status, sustained ETF inflows into the seven spot XRP funds, real settlement usage against the escrow supply, and the direction of Bitcoin and the broader market. These change token demand or supply directly. A Ripple IPO sits at the edge of that list, a modest and two-sided factor instead of a primary catalyst. The event may affect attention, but attention is not the same as recurring demand.

Would Ripple sell more or less XRP after an IPO?

Possibly less, which would be the most concrete bullish channel. A listing would raise cash and give Ripple a public stock to fund operations and deals, potentially reducing its need to sell XRP from escrow. The offsetting risk is that going public brings heavier disclosure of the escrow and token sales, which could reassure or unsettle the market depending on what it reveals. The direction depends on what the filings show and whether Ripple actually changes its sell behavior.

Disclaimer: This article is for information purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency prices are highly volatile, and corporate plans such as an IPO are speculative and can change. Nothing here is a recommendation to buy or sell any asset. Always do your own research and consider consulting a licensed professional before making financial decisions. Figures are accurate as of July 1, 2026, and will change.

Ripple has joined the OpenUSD (OUSD) consortium as a launch integration partner, placing itself inside a stablecoin initiative backed by more than 140 companies across payments, banking, fintech, and crypto.

However, according to crypto analyst WrathofKahneman, there’s a catch: OpenUSD will be launching on Solana, Stellar, Base, and Polygon, but not on the XRP Ledger, which has left traders asking what Ripple will actually get out of the deal and whether XRP could benefit at all.

Ripple Joins OpenUSD as Questions Swirl Around XRP

In a July 1 thread on X, WrathofKahneman described OpenUSD as a consortium-backed dollar stablecoin designed to solve pain points for businesses by enabling free minting and redemption and removing volume limits. It will also distribute reserve earnings to partners after deducting management fees.

According to Open Standard, the independent entity that will govern the token, OpenUSD, will go live later this year, with Visa, Mastercard, Stripe, Coinbase, BlackRock, Google, and Bybit among the companies backing it.

The analyst argued that the project is in part an anti-USDC play engineered by Stripe. Recall that Stripe bought Bridge earlier this year specifically for its OCC bank charter, and per WratheofKahneman, OpenUSD will let Stripe “get out from under Circle by creating neutral infrastructure and shared economics.”

They think that positioning makes OpenUSD dangerous for Circle’s margins, since a stablecoin where every partner feels like a co-owner is a hard thing to compete against with a traditional single-issuer model.

As for Ripple, the industry observer doesn’t think the company had much choice.

“Ripple doesn’t want to be absent from a massive payments-stablecoin consortium, even if OpenUSD is not issued on XRPL, because they sell payments infra,” they wrote.

They also noted that Ripple’s business would be fine, even if it lost some RLUSD profit to the new stablecoin. And speaking of RLUSD, the analyst said there is only a small overlap, given that OpenUSD is built for the broader economy, while RLUSD is primarily used for settlements within Ripple’s own stack.

On XRP, WrathofKahneman was a bit more uncertain, suggesting that the worth of the Ripple token requires value coming into the ledger, and it may only be affected if OpenUSD is eventually issued on XRPL.

“It would only help,” they explained. “But this is a big ‘if’ and likely why Ripple got in the consortium even if not yet issuing.”

The market watcher also flagged the presence of Coinbase in the group despite its deep USDC ties, saying it showed platforms are hedging against getting boxed into a single stablecoin economy.

Competition Moving Toward Shared Infrastructure

OUSD is entering a market where stablecoin issuers and payment firms are increasingly competing over infrastructure instead of individual tokens.

For instance, earlier this month, Mastercard expanded support for several stablecoins, including RLUSD and USDC, across networks such as XRPL, Ethereum, Solana, Arbitrum, and Base. According to the company, the move was to position itself as a neutral infrastructure provider rather than backing one issuer.

The post Ripple’s OpenUSD Move: Payment Infrastructure Push or XRP Value Catalyst? appeared first on CryptoPotato.

Crypto World

Europe is rewriting its landmark MiCA regulatory rulebook as hard July 1 deadline passes

Nevertheless, MiCA has achieved many of its original goals, according to Hansen. There are around 20 euro-denominated stablecoins that have been authorized by the regime, with adoption buoyed by their formal regulation.

It’s not perfect, though, he added, pointing to reserve rules that require minimum bank deposits. Attention is also shifting beyond domestic regulation to global oversight. The next phase of policymaking could focus on allowing tokens regulated in one jurisdiction to circulate in another through mutual recognition regimes.

“We could benefit from the global, internet-native nature of these assets instead of fragmenting their circulation through locally fragmented rulebooks,” he said.

The EU may have had something of a first-mover disadvantage with regard to regulating crypto assets, as there was no framework in major markets like the U.S or Hong Kong to work with like there is now.

Fortress Europe

Sebastian Barling, partner for financial institutions regulatory at Skadden, compared the EU’s approach to building a “fortress.”

“The consultation is clearly a serious review intended to make sure the European regime aligns internationally and remains competitive,” he told CoinDesk.

Barling and Legler explored the Commission’s pivotal shift toward evaluating a third-country equivalence regime and managing cross-border multi-issuance structures in a recent article. They highlighted that while MiCA currently lacks a mechanism to defer to foreign frameworks, an equivalence regime could transform the market by enabling mutual recognition and allowing globally circulating stablecoins to be listed on EU exchanges.

At the same time, he expects macroeconomic uncertainty to remain the dominant force across financial markets. Correlations among stocks, bonds, commodities and cryptocurrencies have risen in recent months, according to Kestrel data, suggesting investors are responding more to policy developments than to company-specific fundamentals.

“The rest of the year is going to be messy,” he said, arguing uncertainty around Federal Reserve policy and Treasury financing could keep markets volatile before financial conditions eventually improve.

Chris Sullivan, co-founder and portfolio manager at digital asset hedge fund Hyperion Decimus, sees a similar backdrop of elevated uncertainty but believes investors are paying too much attention to market narratives and not enough to market mechanics.

He argued that structural changes following the launch of U.S. spot bitcoin exchange-traded funds (ETFs), combined with institutional hedging activity in derivatives markets, have changed how bitcoin trades and weakened many of its historical relationships with broader macro indicators.

Bitcoin’s recent downturn has also challenged the idea that bitcoin had outgrown its traditional four-year cycle. Following the launch of U.S. spot bitcoin ETFs, some market participants argued institutional capital would smooth out bitcoin’s volatility and bring an end to its familiar boom-and-bust pattern. Sullivan disagrees, saying the current decline still fits within historical market cycles and that he is waiting for a final bottoming pattern before declaring the bear market over.

World, the mysterious Solana project that garnered millions of views on X with little more than a glowing globe, cryptic posts and the tagline “Trade Everything,” is now live as a fully onchain prediction market inside Phantom.

The platform is online at world.xyz and in the Phantom wallet on iOS, Android and desktop, with Chainlink serving as its primary oracle infrastructure for its data.

Users can trade event contracts tied to crypto prices and the 2026 FIFA World Cup, with additional markets on sports, geopolitics, and macroeconomics planned for the near future, according to an announcement shared with CoinDesk.

World’s world_xyz account has built attention throughsocial media posts offering scant product details, fueling speculation that the project could be a meme coin, trading app or broader Solana infrastructure play. Copycat WORLD-themed tokens have appeared on token launchpads, though those tokens are not official World assets.

The platform’s identity stayed hidden until late June, when a legal disclosure on Phantom’s site surfaced on X.

World is instead a non-custodial prediction market, with users being able to trade directly from their Solana wallets and funds moving only when they enter a market. Positions, settlement and redemptions happen onchain.

Circle CEO Jeremy Allaire argued that USDC’s decade-long network of integrations, liquidity and regulatory infrastructure gives it a structural advantage over new stablecoin entrants, while challenging key elements of Open USD’s proposed business model.

In a Wednesday X post, Allaire described stablecoin networks as platform businesses driven by network effects, saying sustained investment in integrations, liquidity, regulatory approvals, banking relationships and reserve management creates competitive advantages that are difficult to replicate.

He also questioned whether permanently offering free, unlimited minting and redemption would remain sustainable at scale and said returning nearly all reserve income to partners risks “starving an infrastructure.”

The comments highlight intensifying competition among stablecoin issuers as new entrants seek to challenge USDC and USDT by offering businesses a greater share of reserve income and influence over governance.

Open Standard announced Open USD (OUSD) on Tuesday, with support from over 140 payments, banking, technology and crypto companies, including Visa, Mastercard, Stripe, Coinbase, BlackRock and Google. The stablecoin is expected to go live later in 2026.

Circle’s stock performance in the last five days. Source: Yahoo Finance

Circle shares closed Tuesday at $62.63, down 17.55% from the previous session, before rising 2.44% to $64.18 in premarket trading as of 11 am UTC on Wednesday, according to Yahoo Finance data.

OUSD could challenge the Circle-Tether duopoly: Bernstein

In a research note, analysts at Bernstein said OUSD could become the “strongest and first new entrant to challenge the duopoly of Circle and Tether,” citing its reach across payments, banking, technology and commerce.

However, Bernstein said governance, operational architecture and the revenue-sharing formula remain open questions, as coordinating more than 140 partners will require substantial work. Bernstein said Circle spends close to $500 million on marketing, infrastructure, technology and compliance, highlighting the amount of resources needed to scale a stablecoin network.

Related: MetaMask launches stablecoin yield account with card spending

Lorenzo Valente, director of research at ARK Invest, took a more skeptical view. In a post on X, Valente said that OUSD still faces the cold-start problem created by USDC and USDT’s entrenched liquidity across the crypto ecosystem. He called the announcement a “giant” letter of intent and said that many participants also support competing stablecoins or operate their own infrastructure.

“The partners are backing rivals: Stripe owns Bridge and has its own stack, Coinbase is wedded to USDC, banks are building their own deposit tokens and the card networks support every token out there,” Valente wrote.

Magazine: Japanese pension fund tips 1% in crypto, G7 urges action on NK hackers: Asia Express

Remittix has moved into a busier launch window, and one update is now taking priority across the community: airdrop registration.

The registration page is live through the official Remittix site, giving RTX holders a clear step to complete before token distribution moves closer. For presale buyers, the focus is shifting from simply watching updates to taking action, registering wallets and preparing for the next stage of the Remittix rollout.

The timing is important. Remittix is currently building toward several major updates, including the RTX launch price reveal expected in 3 days, the extended 350% RTX bonus, the approaching public platform launch and the $32 million milestone expected to unlock the official launch date reveal.

Why Airdrop Registration Is Now In Focus

The Remittix airdrop is connected to the distribution of RTX tokens purchased during the presale. It is not being presented as a separate free-token campaign. Instead, it is part of the process for helping holders prepare for token distribution.

To register, holders need to visit the official Remittix site, connect their wallet, submit their wallet address and complete the registration page. Users can also add optional notification details so they can receive future updates linked to the airdrop, distribution and launch process.

Once the process is complete, the page confirms that the holder has successfully registered.

This has made registration one of the most practical updates for the community. While launch headlines continue to build, wallet submission is the step holders can complete now.

Launch Updates Are Starting To Stack Up

The next few updates could be important for Remittix. The RTX launch price reveal is expected in 3 days, giving holders a clearer view of how the token will be positioned heading into launch.

At the same time, the project is closing in on the $32 million milestone, which is expected to unlock the official launch date reveal. This has added more attention around the current registration period, especially as holders wait for clearer launch timing.

The extended 350% RTX bonus is also still active, adding another incentive for users watching the final stretch before launch activity increases.

Platform Launch Adds A Utility Angle

Beyond token distribution, Remittix is still building its wider crypto-to-fiat payments story.

The platform is designed to let users send crypto while recipients receive fiat directly into bank accounts. Multiple community members have reportedly received fiat payments through the Remittix system, giving the project practical proof as public platform access moves closer.

That is why the airdrop registration update matters beyond wallet submission alone. It arrives at the same time as launch price news, platform momentum, the 350% bonus extension and the $32 million milestone.

For RTX holders, the next step is straightforward. Register through the official Remittix site, submit wallet details and stay ready as the next Remittix launch updates approach.

Discover the future of PayFi with Remittix by checking out their project here:

Website: https://remittixpresale.io

Airdrop Registration: https://airdrop.remittixpresale.io

FAQ

Why is airdrop registration important for Remittix holders?

Airdrop registration allows RTX holders to submit their wallet address and prepare for the upcoming token distribution process.

What major Remittix updates are approaching?

The main updates include the RTX launch price reveal in 3 days, the $32 million milestone for the launch date reveal and the approaching public platform launch.

What is the Remittix platform designed to do?

The Remittix platform is designed to let users send crypto while recipients receive fiat directly into bank accounts.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Key Points

- Christopher Delgado admits guilt in $400M cryptocurrency fraud operation

- Federal prosecutors reveal Ponzi-style structure using new investor funds

- At least $250M in verified losses connected to the fraudulent scheme

- Agreement includes forfeiture of luxury properties, vehicles, and high-end goods

- Federal sentencing scheduled for October 8 in ongoing fraud prosecution

Christopher Alexander Delgado, former chief executive of Goliath Ventures, has entered a guilty plea in connection with a massive $400 million cryptocurrency fraud operation in Florida. Federal authorities allege that Goliath collected investor capital by promising substantial returns through digital asset liquidity pool investments. Instead, investigators claim the funds financed payouts to earlier investors, extravagant personal purchases, and corporate entertainment expenses.

Executive Acknowledges Involvement in Fraudulent Operation

According to the U.S. Attorney’s Office, Delgado entered guilty pleas on charges including conspiracy, wire fraud, and money laundering. Each wire fraud charge carries a potential sentence of up to 20 years behind bars. The money laundering charge adds an additional maximum penalty of 10 years in federal prison.

Delgado assumed leadership of Goliath Ventures following its earlier incarnation as Gen-Z Venture Firm. Federal prosecutors indicate that the Crypto Fraud scheme operated continuously from January 2023 until January 2026. Throughout this timeframe, the company marketed consistent monthly profits supposedly generated from cryptocurrency liquidity pool operations.

Federal authorities state that Delgado has acknowledged responsibility for investor losses totaling at least $250 million. Prosecutors further assert that Goliath collected approximately $400 million from defrauded victims. The executive now awaits his sentencing hearing scheduled for October 8.

Federal Investigation Reveals Luxury Asset Trail

Government prosecutors detail how Goliath employed incoming investor capital to satisfy withdrawal requests from previous participants. The organization simultaneously processed payouts and maintained outward appearances of legitimate investment activities. According to prosecutors, merely $1 million actually reached genuine cryptocurrency assets.

The Crypto Fraud investigation uncovered substantial luxury expenditures, based on federal court documents. Prosecutors documented purchases by Delgado including multiple residential properties, exotic automobiles, premium timepieces, designer handbags, upscale wallets, and fine jewelry. The spending spree encompassed Lamborghini and Rolls-Royce vehicles, Rolex watches, and custom-designed Tiffany & Co. jewelry pieces.

The plea arrangement mandates that Delgado surrender eight real estate properties and eleven luxury vehicles. Additional forfeitures include 30 high-end watches and over 50 designer bags and wallets. Delgado has also consented to relinquish no fewer than 29 pieces of jewelry.

Fraud Investigation Raises Questions About Financial Oversight

The investigation attracted significant attention even before Delgado’s guilty plea. Affected investors initiated a proposed class-action complaint against JPMorgan Chase in March. The legal action accused the banking institution of permitting questionable Goliath transactions through its banking infrastructure.

The civil complaint asserted that approximately $253 million flowed through a JPMorgan business account. Plaintiffs additionally claimed that roughly $123 million subsequently transferred to Goliath-controlled wallets at Coinbase. Independent federal filings documented additional transaction flows involving Bank of America accounts and Coinbase wallet addresses.

The Crypto Fraud prosecution underscores the disconnect between promotional representations and verifiable blockchain transactions. While liquidity pools function as legitimate DeFi mechanisms, companies must demonstrate transparent on-chain evidence. In this instance, federal prosecutors contend that Goliath exploited the liquidity pool concept to facilitate an extensive Crypto Fraud enterprise.

Sneeze When You Go Outside? Experts Explain Why You Do This When You Walk Outside

The most controversial issue at the World Cup

Oppo’s Air 5s are AirPods 4 rivals with ANC

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics5 days ago

Politics5 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World1 day ago

Crypto World1 day agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics5 days ago

Politics5 days agoPotential 2028er World Cup attendee leaderboard

-

Business5 days ago

Business5 days agoAsia stock markets slide as tech shares slump

-

News Videos3 days ago

News Videos3 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech6 days ago

Tech6 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World4 days ago

Crypto World4 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business1 day ago

Business1 day agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World4 days ago

Crypto World4 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports5 days ago

Sports5 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech4 days ago

Tech4 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech4 days ago

Tech4 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World5 days ago

Hyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World6 days ago

Crypto World6 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

-

Crypto World5 days ago

Crypto World5 days agoRTX holders must register wallets before token distribution begins

-

Tech2 days ago

Tech2 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Business2 days ago

Business2 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

You must be logged in to post a comment Login