Crypto World

Would a Ripple IPO actually move XRP?

The assumption is simple: Ripple goes public, XRP moons. The reality is that Ripple equity and the XRP token are different assets, and the channels connecting them are weaker than the hype suggests.

Summary

- Ripple remains private with no S-1 on file, but a $750 million buyback fixed its valuation near $50 billion and private secondary shares have surged to about $136.90, keeping IPO speculation loud.

- Ripple equity and the XRP token are legally separate: owning XRP gives no claim on the company, and a public listing would not hand shareholders or token holders any automatic link between the two.

- The plausible transmission channels are sentiment, Ripple’s escrow and sell behavior, institutional validation, and value accrual, and each is weaker or more two-sided than the “IPO equals XRP moon” story assumes.

- There is a real counter-case that an IPO could pull capital away from XRP, by giving investors who want Ripple exposure a way to buy the stock instead of the token.

- The evidence so far is mixed: XRP briefly re-coupled to Ripple’s rising private valuation, yet the token is still down about 26% on the year, which points to weak, not strong, transmission.

The reflex in the XRP community is automatic. Ripple goes public, the story goes, and XRP rockets alongside it. The logic feels obvious, because Ripple and XRP are wrapped together in the same brand, the same headlines, and the same decade of shared history. But an initial public offering sells shares in a company, and XRP is a token that confers no ownership of that company.

Whether a Ripple listing would actually move the token is not a matter of sentiment or loyalty. It is a question of mechanism: through what channels, if any, would value flow from a Ripple equity event into the XRP price? This piece examines those channels one by one, and finds them thinner than the hype implies. The XRP holder payout question has already become a separate community obsession, but the XRP holder payout question is not the same as a price-transmission mechanism.

The starting point: Ripple equity and XRP are different assets

Everything begins with a distinction the excitement tends to blur. Ripple Labs is a private company. XRP is a digital asset that trades on public exchanges. There is no mechanism that entitles an XRP holder to Ripple shares, dividends, or any slice of the company’s profits, and a public listing would not create one.

If Ripple lists tomorrow, an XRP holder owns exactly what they owned the day before: a token, not a piece of the business. The one concrete link runs the other direction. Ripple is itself one of the largest holders of XRP, with tens of billions of tokens held in escrow that it releases on a schedule and uses, in part, to fund operations. So the company’s relationship to the token is that of a giant holder and periodic seller, not a value conduit that passes equity gains down to token holders.

That asymmetry matters for the whole analysis. When people say an IPO would help XRP, they are really claiming that something about Ripple becoming public would change demand for, or supply of, the token. The rest of this piece tests each version of that claim. Until then, Ripple equity and XRP should be treated as related but legally separate assets, not two versions of the same exposure.

Channel one: sentiment and attention

The first and most immediate channel is psychological. An IPO would be a media event, a wave of coverage, analyst notes, and credibility that reframes Ripple from a litigation-scarred crypto firm into a public company vetted by underwriters and public markets. In a market where attention is a real driver of price, that halo could spill onto XRP, lifting the token on narrative even without any mechanical connection. That is the channel the community understands instinctively, because XRP has always traded partly on Ripple headlines.

There is some evidence this channel is live. When Ripple’s private secondary shares surged, one analysis linked the move to XRP briefly re-coupling with the company’s rising valuation, as the market started treating the private-share price near $136.90 as a fundamental signal for the token. That is the sentiment channel working in real time: a Ripple equity data point moving XRP through association rather than mechanics. It is also why where XRP could go from here depends partly on whether traders treat corporate news as a catalyst or just another temporary headline.

The limit is that sentiment is fickle and shallow. It can lift a token into an event and drop it just as fast afterward, and it does not build the sustained demand that holds a price up. A narrative bump around an IPO is plausible. A durable re-rating on sentiment alone is not, which is why this channel, while real, is the weakest foundation for a lasting move.

Channel two: Ripple’s escrow and sell behavior

The most underappreciated channel runs through Ripple’s own balance sheet. Because Ripple holds a vast XRP escrow and sells tokens to help fund itself, anything that changes the company’s need to sell XRP changes the supply hitting the market. This is where an IPO could actually matter mechanically. A successful listing would raise cash and give Ripple a public currency, its own stock, to fund acquisitions and operations.

A cash-rich, publicly funded Ripple might lean less on programmatic XRP sales, easing a source of sell pressure that has weighed on the token for years. That is a genuine, if indirect, bullish path. Less selling from the single largest holder is a supply-side positive that does not depend on sentiment. It is the most concrete way an IPO could help XRP.

The two-sided catch is disclosure. Going public subjects Ripple to far heavier reporting requirements, which means the escrow, the sales, and the token’s role in Ripple’s finances would face new scrutiny from public-market investors and regulators. Greater transparency could reassure the market, or it could surface uncomfortable details about how much the company depends on token sales, which would cut the other way. The escrow channel is the strongest mechanical link, but its direction is not guaranteed.

Channel three: institutional access and validation

The third channel is legitimacy. A public Ripple would sit inside the regulated financial system in a way it does not today, and that validation could radiate outward to the whole XRP ecosystem. The backdrop already leans this way: XRP was recognized as a commodity in March, and seven spot XRP exchange-traded funds are trading with roughly $1.43 billion in cumulative inflows. A high-profile Ripple listing would add another layer of institutional acceptance, potentially making allocators more comfortable holding XRP through regulated products.

The argument is that validation compounds. Each step that moves XRP from contested asset toward accepted infrastructure lowers the barrier for the next institution, and a Ripple IPO would be a large step. In a world where the token already has ETF access, a public parent company strengthens the case that the ecosystem is durable. That is also why XRP’s regulatory status matters more than the IPO hype itself: institutions care less about community excitement than about whether the asset can be held cleanly under durable rules.

The weakness is that validation of the company is not the same as demand for the token. Institutions can conclude that Ripple is a fine investment and express that view by buying the stock, which does nothing for XRP. Legitimacy is a soft tailwind, helpful at the margin, but it does not force anyone to buy the token. For a durable move, validation has to become measurable token demand, not just a better story around the issuer.

Channel four: the value-accrual problem

This is the channel that breaks the simple story, and it is the most important. For an IPO to lift XRP durably, Ripple’s commercial success has to translate into demand for the token. But Ripple’s business and XRP’s value are only loosely coupled. Many of Ripple’s bank and payment partners use its software without touching XRP at all, and the company earns revenue from services, licensing, and acquisitions that do not route through the token.

Ripple can thrive as a company while XRP stagnates, because the token’s value depends on settlement usage and demand for XRP itself, instead of on Ripple’s profit and loss. This value-accrual gap explained is the reason a Ripple IPO is not the guaranteed catalyst holders imagine. An IPO rewards equity holders for the company’s success. It does not, by itself, create the on-chain demand that would lift the token.

Unless a listing changes how much XRP is actually used to move value, the mechanical link from Ripple’s public-market performance to the XRP price is faint. The token needs its own demand story, and the IPO does not write one. It may make Ripple more visible, more credible, and more valuable. None of that automatically makes XRP more scarce or more necessary.

The counter-case: an IPO could hurt XRP

The overlooked possibility is that a Ripple listing works against the token. For years, buying XRP was one of the only ways for a public investor to express a view on Ripple’s success. An IPO removes that constraint by offering the pure play: if you want exposure to Ripple, you buy the stock, which actually owns the business, the revenue, and the growth. The token, which owns none of that, becomes the inferior vehicle for a Ripple bet.

That substitution could siphon capital and attention away from XRP toward the equity. Some of the speculative demand that flowed into the token as a Ripple proxy would rationally rotate into shares once shares exist. In this reading, the IPO does not transmit value to XRP at all. It competes with it.

The very event the community treats as the catalyst could turn out to be a drain, redirecting the Ripple trade into a security that leaves the token behind. That does not mean XRP must fall on a Ripple IPO. It means the direction is not obvious, because the listing creates both a halo effect and a substitute asset. The market would have to decide whether XRP remains the best way to trade Ripple’s ecosystem once Ripple stock exists.

What the evidence shows so far

The cleanest test available is how XRP has behaved as Ripple’s private valuation has climbed. The answer is telling. Ripple’s secondary shares surged to about $136.90 and its valuation was fixed near $50 billion, and while XRP did briefly re-couple to that move on sentiment, the token still trades near $1, down roughly 26% on the year. If the transmission were strong, a 376% surge in Ripple’s private-share price should have dragged XRP sharply higher.

It did not. The token acknowledged the news and kept falling with the broader market. That is the empirical verdict: transmission exists, but it is weak. Ripple getting more valuable has not made XRP more valuable in any durable way, which is exactly what the value-accrual analysis predicts.

An actual IPO would be a bigger event than a private-share revaluation, so the sentiment bump could be larger. But the underlying mechanics that limited the private-market spillover would still apply to a public one. The stock would price Ripple’s business, while XRP would still need regulatory clarity, ETF flows, settlement usage, and broader market support. The link is real enough for traders to chase, but not strong enough to treat as automatic.

What would actually move XRP

If the IPO is a weak lever, what is a strong one? The catalysts that genuinely drive XRP are the ones that change token demand or supply directly. Regulatory outcomes rank first: whether crypto market-structure legislation codifies XRP’s status cleanly, which affects how freely institutions can hold it. ETF flows rank second, because sustained inflows into the seven XRP funds are real, measurable demand for the token.

Settlement usage ranks third: whether XRP is actually used to move value at scale, against the escrow supply that keeps entering the market. That is where XRP fits in settlement becomes more important than the IPO narrative. XRP needs recurring use as a bridge asset or liquidity tool, not just Ripple’s name in public-market headlines. And the direction of Bitcoin and the broader market ranks alongside all of them, since XRP rarely fights the tape.

Against those, a Ripple IPO sits at the edge of the picture. It could add a sentiment bump, it could ease Ripple’s XRP selling, and it could burnish the ecosystem’s legitimacy. Each is a real but modest channel, and at least one plausible effect points the wrong way. The honest conclusion is that a Ripple IPO would be a meaningful corporate event that most likely moves XRP far less than the community expects, and possibly not in the direction they assume.

The Coinbase and Circle precedent

The clearest way to test the transmission question is to look at crypto-adjacent companies that already trade publicly, because they show what happens when a company and the tokens around it are separated on public markets. Coinbase is the obvious case. Its stock gives investors exposure to the exchange’s revenue, which rises and falls with trading volume, but owning the stock is not the same as owning the assets that trade on it. When crypto rallies, Coinbase revenue tends to rise, so there is a loose correlation, yet the stock and the broader token market frequently move apart, because the equity is priced on the business and the tokens are priced on their own supply and demand.

Circle offers a sharper version of the lesson. Circle issues the USDC stablecoin, but USDC is a dollar-pegged token that does not float, so Circle equity captures the value of the issuing business, the reserves, the yield, the growth, while the token itself is designed to stay at a dollar. The company can be worth a great deal while the token it issues, by construction, accrues none of that equity value. That is the extreme illustration of the point: a token and its issuer’s stock can be almost entirely decoupled.

XRP sits somewhere between these cases. It is not a dollar peg, so it can appreciate, but it is also not an equity claim on Ripple, so it does not capture the company’s growth the way shares would. Even when Ripple-linked infrastructure appears in real capital-markets events, such as stablecoin settlement using RLUSD on the XRP Ledger, the immediate value still tends to accrue to the rails, the issuer, or the company before it accrues to XRP itself. The precedent from public crypto companies is that the market prices the business and the token separately, and a listing that rewards the equity does not automatically reward the associated token.

A Ripple IPO would most likely follow the same script, with the stock absorbing the value of the business while XRP continues to trade on its own drivers. That does not make the IPO irrelevant. It makes it indirect. The market would finally have a clean way to buy Ripple, and that could clarify how much demand for XRP was really token demand versus company-proxy demand all along.

What a realistic IPO scenario looks like for XRP

It helps to walk through how an actual Ripple listing would probably play out for the token, stage by stage, because the timeline reveals where the modest effects concentrate. In the announcement phase, when Ripple confirms an S-1 or a date, expect a sentiment spike: headlines, community excitement, and a short-term bid in XRP as traders position for the event. This is the sentiment channel firing, and it could produce a sharp but shallow move that fades as the news is absorbed.

In the run-up to the listing, attention would build, and XRP could trade with elevated volatility as speculation swings between the “IPO lifts XRP” and “IPO competes with XRP” theses. Some capital that had been using XRP as a Ripple proxy might already begin rotating toward the anticipated equity, capping the token’s upside even amid the excitement. The listing itself would be an equity event: shares price, the stock trades, and the value of Ripple’s business gets marked by the market. XRP would react mostly to the tone, a strong debut lifting sentiment, a weak one dampening it, rather than to any mechanical flow.

In the aftermath, the durable question resurfaces: does anything about a public Ripple change token demand or supply? If a cash-rich Ripple eases its XRP selling, that supply relief could support the token over time, the most concrete lasting benefit. If investors conclude the stock is the better Ripple bet, capital could keep rotating out of XRP into shares. The realistic net is a sentiment-driven spike around the event that mostly fades, a possible modest supply-side benefit if Ripple sells less XRP, and an ongoing competitive pull from the equity.

That is a meaningful corporate story with a muted and two-sided token effect, which is a long way from the moonshot the community pictures. The IPO could matter. It just would not erase the legal separation between the company and the token. XRP would still need its own demand engine.

Frequently asked questions

Does owning XRP give you a stake in Ripple?

No. XRP is a digital token that trades on public exchanges and confers no ownership of Ripple Labs, no shares, no dividends, and no claim on the company’s profits. Ripple the company and XRP the token are legally separate. A Ripple IPO would sell shares in the business, and holding XRP would give you no automatic right to those shares or their gains.

Has Ripple actually filed to go public?

Not as of late June 2026. Ripple remains private with no S-1 on file and no confirmed date, and executives have repeatedly downplayed the urgency of a listing. The speculation is driven by signals such as a $750 million share buyback that fixed the valuation near $50 billion and a surge in private secondary shares to about $136.90, not by an official filing. That distinction matters because IPO speculation can move sentiment long before any legal filing exists.

Could a Ripple IPO raise the XRP price?

It could, through weak and indirect channels. A listing could lift XRP on sentiment, could ease sell pressure if a cash-rich public Ripple relies less on XRP sales, and could add legitimacy to the ecosystem. None of these is a mechanical guarantee, and the evidence so far shows only faint transmission from Ripple’s rising valuation to the token. The stronger catalysts are still regulatory clarity, ETF flows, and actual XRP settlement usage.

How could an IPO hurt XRP?

By offering a substitute. An IPO would let investors who want Ripple exposure buy the stock, which actually owns the business, instead of the token, which does not. Some speculative capital that flowed into XRP as a Ripple proxy could rotate into the equity once it exists, redirecting demand away from the token rather than toward it. That is why a Ripple IPO is not automatically bullish for XRP.

What is the value-accrual problem?

It is the gap between Ripple’s success and XRP’s value. Many Ripple partners use its software without touching XRP, and much of its revenue does not route through the token. So Ripple can prosper as a company while XRP stagnates, because the token’s value depends on settlement usage and its own demand, not on Ripple’s profit and loss. This is why an IPO is not a guaranteed catalyst.

Did XRP move when Ripple’s private valuation rose?

Briefly and weakly. When Ripple’s secondary shares surged to about $136.90, one analysis linked it to XRP re-coupling with the valuation on sentiment. But XRP still trades near $1, down about 26% on the year, so a large rise in Ripple’s private-share price did not drag the token durably higher. That points to weak transmission between the two.

What actually drives the XRP price?

The strongest drivers are regulatory clarity on XRP’s status, sustained ETF inflows into the seven spot XRP funds, real settlement usage against the escrow supply, and the direction of Bitcoin and the broader market. These change token demand or supply directly. A Ripple IPO sits at the edge of that list, a modest and two-sided factor instead of a primary catalyst. The event may affect attention, but attention is not the same as recurring demand.

Would Ripple sell more or less XRP after an IPO?

Possibly less, which would be the most concrete bullish channel. A listing would raise cash and give Ripple a public stock to fund operations and deals, potentially reducing its need to sell XRP from escrow. The offsetting risk is that going public brings heavier disclosure of the escrow and token sales, which could reassure or unsettle the market depending on what it reveals. The direction depends on what the filings show and whether Ripple actually changes its sell behavior.

Disclaimer: This article is for information purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency prices are highly volatile, and corporate plans such as an IPO are speculative and can change. Nothing here is a recommendation to buy or sell any asset. Always do your own research and consider consulting a licensed professional before making financial decisions. Figures are accurate as of July 1, 2026, and will change.

Crypto World

Bitcoin (BTC) climbs toward $60,000 level after Fed Chair Warsh said inflation risks has come down

Bitcoin climbed back toward the $60,000 level on Wednesday after Federal Reserve Chair Kevin Warsh said inflation risks had eased while reaffirming the central bank’s commitment to returning inflation to its 2% target.

Warsh declined to provide guidance on the Federal Reserve’s next interest-rate decision, saying policymakers would debate incoming data at their meeting in four weekds, during a panel discussion at the European Central Bank’s annual forum in Sintra, Portugal.

Instead, he emphasized that the Fed remained focused on price stability.

“Inflation risks have come down,” Warsh said. “If there were people in households or the business sector, in the financial markets, who thought that this central bank was going to be comfortable with an inflation objective above 2%, well, I guess they’d be disappointed. We’re going to deliver price stability in the U.S.”

Bitcoin pared earlier losses to trade back around the $60,000 level, an increase of more than 2% over the past 24 hours, according to CoinDesk Data.

Christopher Alexander Delgado, the former CEO of Goliath Ventures, pleaded guilty to fraud and money laundering charges stemming from a crypto investment scheme prosecutors said stole at least $400 million from investors.

Delgado, a Florida resident, pleaded guilty Tuesday to conspiracy to commit wire fraud, wire fraud and money laundering, according to the U.S. Attorney’s Office for the Middle District of Florida.

He faces up to 20 years in prison for each fraud count and up to 10 years on the money laundering count.

Goliath Ventures, formerly Gen-Z Venture Firm, solicited investors from at least January 2023 through January 2026 with pitches for monthly payouts it claimed came from crypto liquidity pools, prosecutors said. Delgado admitted in his plea agreement to causing at least $250 million in investor losses.

Investor money was used to pay earlier investors, fund withdrawals and cover luxury spending, according to prosecutors. Delgado bought at least 6 residential properties worth between $1.15 million and $8.5 million each, plus Lamborghinis, Rolls-Royces, Rolex watches, dozens of Louis Vuitton bags and custom Tiffany jewelry, with the funds.

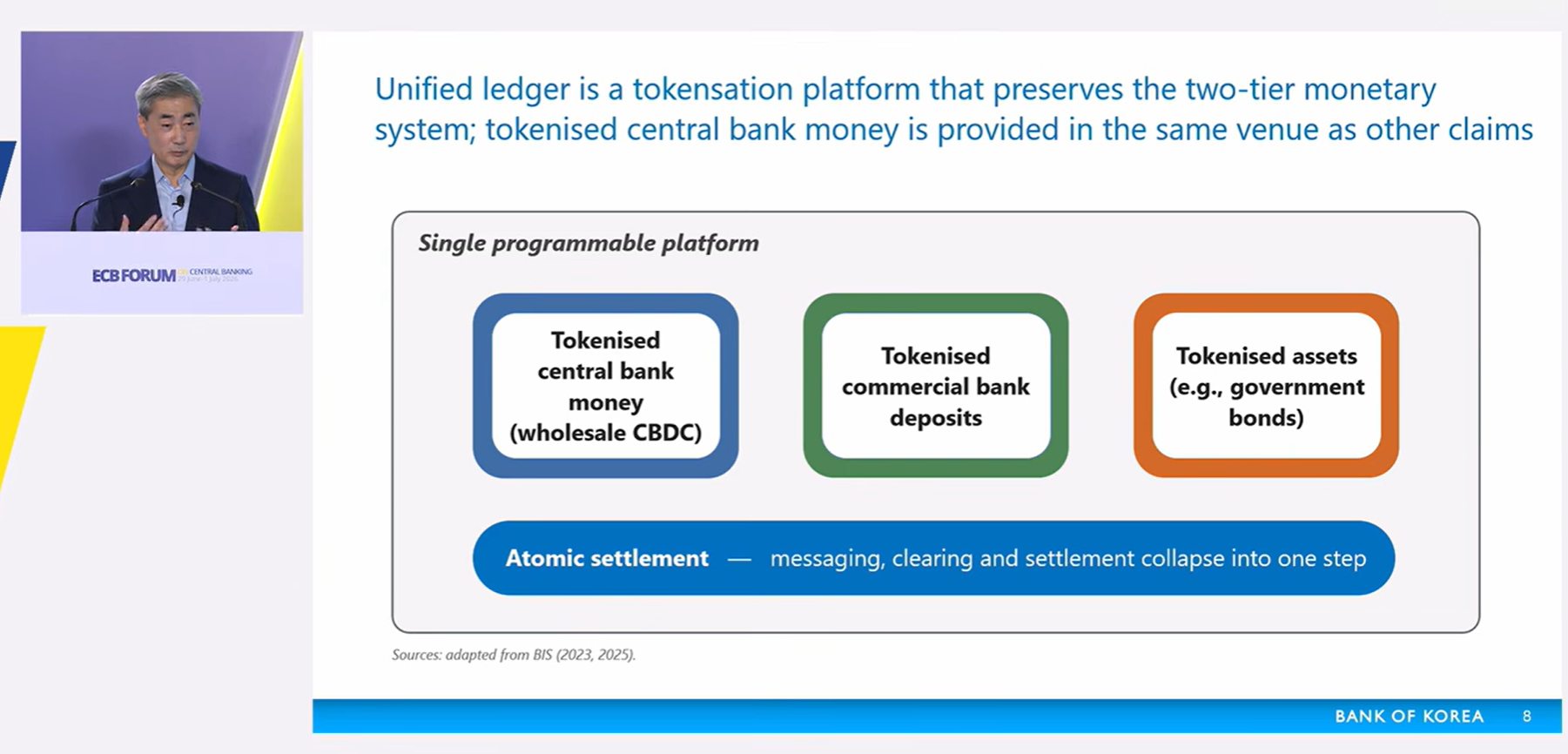

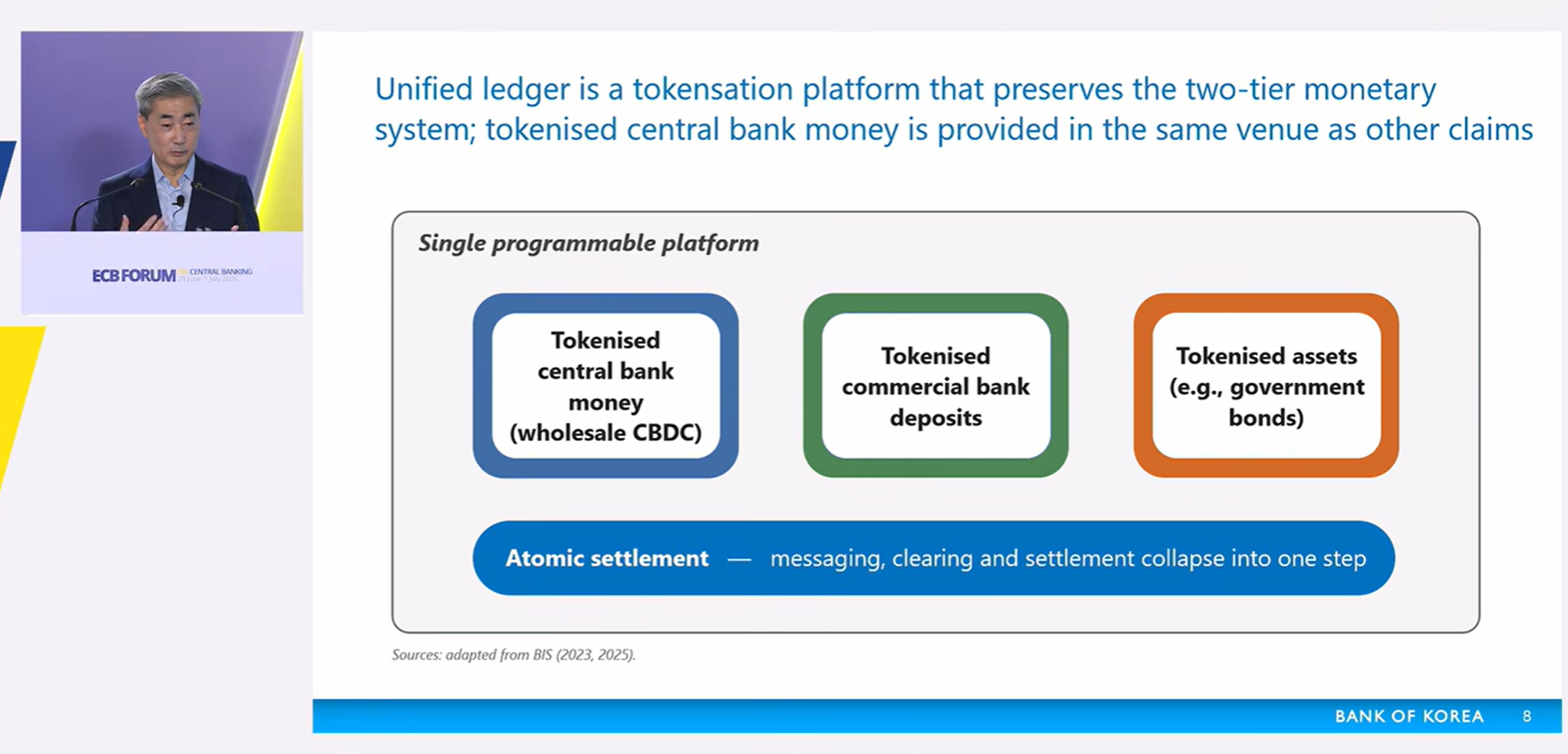

Hyun Song Shin, the governor of the Bank of Korea, praised tokenization for its ability to simplify the issuance and management of government bonds.

Shin said during a Wednesday panel discussion at the European Central Bank (ECB) Forum on Central Banking in Sintra, Portugal, that tokenized bonds would make it easier to verify collateral, credit the asset provider’s account and reverse transactions at the appropriate time.

“The big prize is tokenizing government bonds,” Shin said, adding that it is “much easier, much less prone to mistakes if you have everything tokenized.”

US Treasury debt is the largest tokenized real-world asset category, representing $14.6 billion, or about 46% of the $31.7 billion RWA market, according to data provider RWA.xyz.

Shin also outlined plans to bring tokenized government bonds, wholesale central bank digital currencies and tokenized commercial bank deposits on a unified ledger, as part of an extension to “Project Hangang,” a Bank of Korea-led pilot project testing a blockchain-based wholesale CBDC system.

Hyun Song Shin, governor of the Bank of Korea, speaks during a panel discussion at the ECB Forum on Central Banking. Source: YouTube

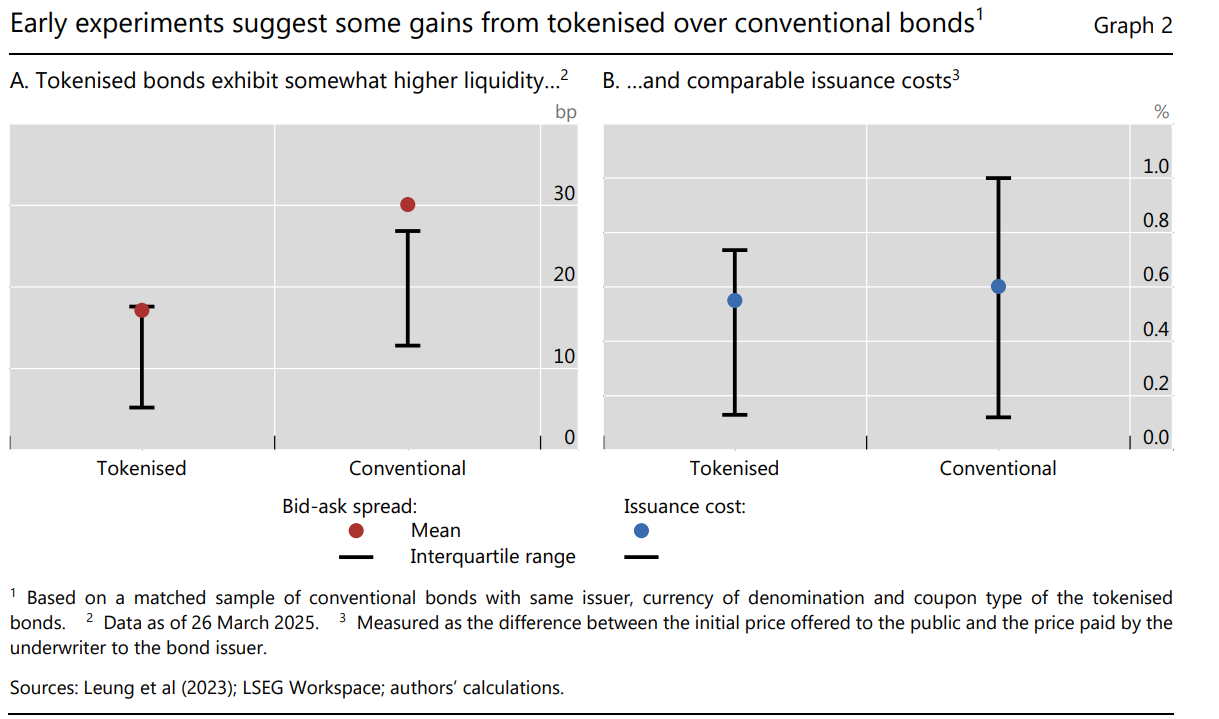

Tokenized government bonds may boost financial innovation: BIS

Government bond tokenization could improve market efficiency and support financial innovation, provided regulatory and infrastructure challenges are addressed, according to a July 2025 report by the Bank for International Settlements (BIS).

Related: Former BIS chief softens stance on stablecoins, backs coexistence with fiat

Government securities play a crucial role in the financial system, acting as a savings vehicle for households and firms and as collateral in a range of transactions, the report said, adding:

“By enabling the contingent execution of actions, tokenisation can help to enhance the efficiency of markets, reduce settlement risk, broaden investment access and spur the creation of new financial services.”

The report examined 39 tokenized bonds, including 24 issued by corporations and 15 by governments. Compared with traditional, non-tokenized bonds, the BIS found “suggestive evidence” of lower bid-ask spreads and comparable issuance costs and yields.

Tokenized bonds vs conventional, non-tokenized bonds, liquidity, issuance costs. Source: BIS

Magazine: Guide to the top and emerging global crypto hubs: Mid-2026

For now, most AI agents still live inside safe boxes. They summarize documents. Write code. Search databases. Help customer support teams move faster.

In finance, they are already creeping into fraud detection, compliance, research, and back-office workflows. Cambridge Judge Business School found this year that 52% of financial firms are actively adopting agentic AI, with 23% already scaling or transforming around it.

Bond Labs, a blockchain superapp network, is betting on the next step. It wants AI agents to trade, borrow, lend, move funds, and eventually spend money across crypto and traditional payment rails.

The company has launched on 0G, an AI-native blockchain network, with a DeFi platform designed for both humans and autonomous AI agents.

Bond says its platform combines

- A spot decentralized exchange,

- Perpetuals exchange

- Lending and borrowing markets,

And also a planned neobank layer with fiat on/off ramps, global transfers, on-chain IBAN access, Visa debit cards, and yield-bearing accounts.

That is a large promise. It also arrives at a moment when the financial industry is trying to work out how much autonomy it can safely give to software that can reason, plan, and act.

The Agent Needs a Wallet

The idea behind Bond is simple enough. If AI agents are going to become economic actors, they need financial infrastructure.

A chatbot can tell a user how to rebalance a portfolio. An agent could, in theory, do it. It could move idle funds into a yield account, borrow against collateral, hedge exposure, or route money across chains and payment systems.

That shift requires more than a prompt window. It needs liquidity, execution venues, credit markets, identity checks, payment access, and risk controls.

Bond is trying to put those pieces into one environment.

Its DeFi layer includes a spot DEX based on Uniswap V3-style automated market-making, a perpetual DEX using a central limit order book model, and lending markets with dynamic interest rates.

The company also plans to add a neobank layer within the next three months, bringing fiat access, global transfers, Visa card functionality, and accounts connected to 0G Chain.

Bond also says it will build a real-world asset division, giving users and agents exposure to tokenised assets for trading, settlement, and investment.

In plain terms, Bond wants to be the financial operating system for AI agents.

The Money Is Following the Thesis

The launch comes with direct ecosystem support from 0G Labs.

Bond is backed by a $10 million incentive programme from 0G Labs, a $3.5 million direct investment, and a stated $50 million TVL target. The incentive programme will run over 12 months and will be tracked on-chain. Bond says AI-agent trades will be included in the rewards structure.

The goal is liquidity. Without it, an agent-facing financial platform is just an interface. With it, agents can actually execute trades, access lending markets, and move value without waiting for a human to manually approve every step.

“The vision of AI agents managing someone’s finances has been held back by fragmented infrastructure,” said Bond Labs CEO Taweh Beysolow. “Bond provides the missing layer DeFi primitives and a neobank where agents can trade, borrow, spend, and earn, all within a single platform.”

Michael Heinrich, CEO of 0G Labs, framed Bond as part of a wider AI economy.

“0G is building the foundational infrastructure for an AI-native economy, and a core part of that vision is giving autonomous agents the ability to transact, manage assets, and access financial services as easily as any human,” Heinrich said. “Bond is the first platform to fully realize that vision, combining institutional-grade DeFi with a user-friendly neobank, all on a blockchain designed from the ground up for AI agents.”

The Pipes Behind the Platform

Bond has also lined up infrastructure and liquidity partners.

The company says Turtle will support liquidity and incentive distribution, Re7 will act as a DeFi vault curator, Midas will provide vault infrastructure, and Wormhole will support cross-chain interoperability.

It has also named Cicada Capital, Diffuse, GSR, and Flow Traders as liquidity providers.

Those names are important because AI-agent finance will not work without deep markets. An agent that manages capital needs execution quality, reliable settlement, and enough liquidity to avoid poor pricing.

Essi, CEO of Turtle Club, said the pre-deposit campaign had to work for different types of participants.

“Bond is building a superapp for an audience that spans retail and institutional. The pre-deposits campaign needed DeFi-native LPs who could underwrite both ends. We structured it with the Bond team until the economics held without compromising what Bond was committing to its users. Proud to be working alongside them.”

The Risk Is No Longer Theoretical

Deloitte’s 2026 enterprise AI survey found that 74% of companies expect to use AI agents at least moderately by 2027. In finance, Cambridge found agentic AI adoption is already further along among fintechs than traditional institutions.

Regulators are watching the same trend. The Financial Stability Board has warned that AI is spreading across AML, KYC, fraud detection, credit risk, cybersecurity, portfolio management, and compliance.

The Bank of England has gone further, warning that autonomous agents could eventually transact for consumers, execute trading strategies, and amplify market volatility if many systems behave in similar ways.

That makes security central to Bond’s pitch. The company says it has taken a security-first approach, including smart contract audits by Hashlock. That will matter as DeFi platforms remain exposed to exploits, oracle failures, bridge risk, liquidity shocks, and bad incentive design.

The harder question is governance. If an AI agent makes a trade, approves a payment, or borrows against collateral, the system needs clear rules for consent, limits, liability, and emergency shutdowns.

Bond’s launch is an early test of whether AI agents can move from assistants to financial actors. The infrastructure is starting to appear.

But the market now has to prove that autonomous finance can work without turning speed into fragility.

The post AI Agents are Starting to Handle Money. This Blockchain Wants to Build Their Bank appeared first on BeInCrypto.

Bitcoin’s battle around the $60K region is entering a decisive phase after sellers are forcing a breakdown below this major support area. With momentum still favoring the sellers, traders are now watching whether demand can prevent a deeper correction toward the mid-$50K region.

Bitcoin Price Analysis: The Daily Chart

On the daily timeframe, BTC has extended its bearish trend after losing several major support zones. The recent rejection by the 200-day moving average around $80K and the breakdown of the 100-day moving average near $ 74 K have reinforced the longer-term downtrend, with both moving averages now sloping lower and acting as dynamic resistance.

The price is currently trading around $58.7K after breaking slightly below the $60K demand zone. This indicates that buyers have struggled to defend one of the market’s most important psychological levels. The next significant support lies around the $55K region, while a deeper correction could expose the broader demand area near $52K.

On the upside, Bitcoin would first need to reclaim the $60K level quickly before challenging the $66K to $68K resistance zone. Beyond that, the $72K to $74K area remains the primary barrier, as it coincides with the long-term moving averages. The broader bearish structure would only begin to improve if BTC manages to reclaim this region.

BTC/USDT 4-Hour Chart

The lower timeframe presents a similarly bearish picture. Bitcoin continues to trade inside a descending structure, respecting both the upper and lower boundaries throughout the recent decline. Every recovery attempt has produced another lower high, confirming that sellers remain in control.

The latest rejection from the $66K to $68K supply zone pushed BTC back toward the lower boundary of the channel. Price is now hovering around $58.7K, slightly beneath the $60K support area, increasing the probability of another test of lower liquidity and a breakdown of the channel structure.

Meanwhile, the RSI has formed a modest bullish divergence, with momentum making slightly higher lows while price printed fresh lows. Although this divergence could trigger a short-term relief bounce, it has yet to receive confirmation through a decisive breakout above nearby resistance.

On-Chain Analysis

Bitcoin’s Net Unrealized Profit/Loss (NUPL) has fallen sharply to approximately 0.09, placing the metric deep within the low-profit region shown on the chart.

NUPL measures the aggregate unrealized profit or loss held across the Bitcoin network. Higher readings generally reflect widespread investor optimism and elevated profitability, while lower values indicate shrinking profits and deteriorating market sentiment.

The current reading suggests that the majority of holders have seen a significant reduction in unrealized gains compared to previous months. Historically, such depressed NUPL levels have been associated with periods of capitulation or late-stage bear market conditions, when weak hands are gradually flushed out of the market.

While this does not guarantee an immediate reversal, it indicates that much of the speculative excess has already been removed. If selling pressure begins to ease and long-term investors continue accumulating, these historically depressed profitability levels could eventually provide the foundation for a broader recovery. Until price reclaims key resistance zones, however, the technical structure continues to favor the sellers.

The post Bitcoin Price Prediction: BTC Risks Drop Toward $55K After $60K Breakdown appeared first on CryptoPotato.

Open USD (OUSD) launched on Tuesday with more than 140 corporate backers, raising a pointed question for anyone earning yield on USD Coin (USDC) through Aave.

The new token lets businesses mint and redeem for free and routes its reserve income to partners. That model aims at Circle, yet the effects could reach the decentralized finance (DeFi) markets where USDC earns its keep.

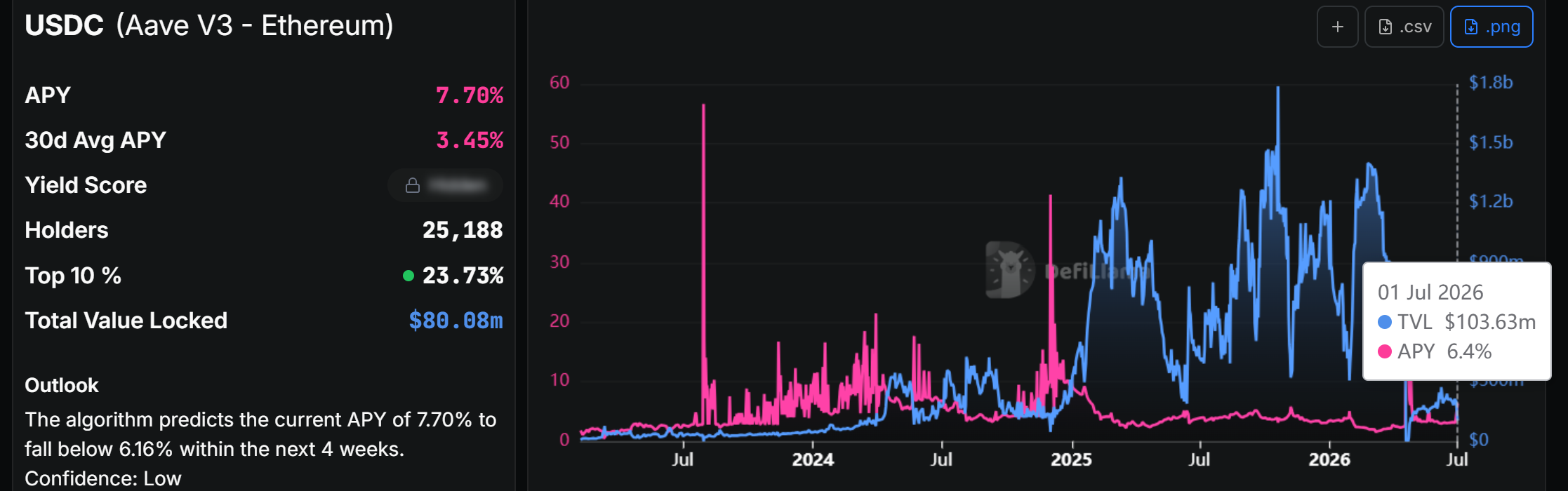

How USDC Earns Yield on Aave

Lenders who supply USDC to Aave do not pay interest to Circle. They earn from borrowers who pay to withdraw USDC from the pool.

Aave ties those rates to utilization, the share of supplied USDC that borrowers have taken out. Once utilization pushes past its optimal point, supply rates climb fast to pull in deposits.

That makes borrowing demand the number that matters. USDC suppliers on Aave’s main Ethereum market earn around 3.4%, according to DefiLlama data, though the rate fluctuates with demand.

The same market paid mid-single digits and climbed near 18% at times in 2024.

Federal law pushes savers onchain in the first place. The GENIUS Act, signed in July 2025, bars stablecoin issuers from paying holders interest.

That stablecoin yield limit leaves lending venues like Aave as the main route to a return. Aave has since opened an institutional lending market for tokenized assets.

Why Open USD Could Pressure Those Yields

Open USD targets the demand side. Its backers include Visa, Mastercard, Stripe, Coinbase, and BlackRock, the networks that route much of the world’s business payments.

The design gives them a reason to switch. Partners keep most of the interest Open USD earns on its reserves. That income generated 99% of Circle’s 2024 revenue, its filing shows.

Coinbase is the clearest test. Circle paid it $908 million in 2024 to distribute USDC. The exchange also keeps every dollar of reserve income on balances held there.

Now, Coinbase backs the rival, and its Circle deal is set to renew in August.

Stripe has gone further and tied its platform to the token.

“Open USD will be the default stablecoin for businesses running on Stripe,” Will Gaybrick, President of Technology and Business at Stripe, said in the announcement.

Follow us on X to get the latest news as it happens

Stripe’s weight is not theoretical. Zach Abrams, who now leads Open Standard, cofounded Bridge, the stablecoin firm Stripe bought in early 2025.

If those firms route settlement flows through Open USD, demand that once leaned on USDC could soften. Lower USDC borrowing on Aave means lower utilization, which pulls down supply yields.

Circle built its lead as USDC’s corporate transfer growth outpaced Tether (USDT). Many of those same rails now back the rival. The catch is timing, since Open USD is not fully live and no Aave market lists it yet.

Circle’s Defense and What DeFi Users Should Watch

Circle argues its lead is hard to copy. Chief Executive Jeremy Allaire says scale and liquidity, built over the years, protect USDC.

“Stablecoin networks are platform and network effect businesses that are established over a long period of time, tend towards winner-take-most market structures, and resemble other internet platform utility markets,” Allaire wrote in a post.

USDC still holds deep exchange liquidity and licenses across the US and Europe. It has kept its European regulatory standing even as USDT retreats from the region. Its supply sits near $73 billion, behind USDT at about $184 billion.

History also gives Circle a talking point. Visa, Mastercard, and Stripe once backed Facebook’s Libra project in 2019, then walked away within months as regulators pushed back.

The sharpest immediate damage hit Circle’s stock, not USDC. Circle Internet Group (CRCL) fell about 17% on Tuesday and roughly 40% over the past month.

Its removal from the five major Russell Growth indexes added rules-based selling at the same time.

For DeFi users, the near-term steps are practical. They can track Aave utilization and rates on live dashboards. Spreading deposits across protocols and chains can lower single-venue risk.

Newer onchain yield strategies may also emerge as Open USD rolls out.

The coming months will test one question. Can Open USD pull enough demand from USDC to move Aave’s rates, or will Circle’s head start hold?

The post Could Open USD Crush Aave’s USDC Yields? Here’s What DeFi Users Need to Know appeared first on BeInCrypto.

Crypto markets have struggled in recent months, with bitcoin falling more than 50% from its late-2025 peak after a sharp June selloff driven by persistent exchange-traded fund (ETF) outflows, elevated interest rates and weaker risk appetite.

Ether (ETH) and most major altcoins have underperformed bitcoin during the downturn, although a handful of sectors, including decentralized finance (DeFi) and tokenization, have shown relative resilience.

While crypto adoption is expanding across stablecoins, tokenized real-world assets, onchain credit and DeFi, the bank argued that usage alone does not drive token value. Instead, long-term winners will convert activity into sustainable cash flow or lasting monetary demand.

Cantor identified Hyperliquid as the clearest example of fee-driven token economics through HYPE buybacks and burns, while bitcoin remains the benchmark monetary asset and Ethereum the dominant collateral layer for onchain finance.

Solana, Sui, XRP and Zcash each have differentiated strengths, the report said, but still need to prove they can translate ecosystem growth into durable token demand.

The bank also highlighted digital asset treasury companies as an overlooked investment theme, arguing the strongest firms are evolving beyond passive crypto holders into active operators that generate yield, build infrastructure and provide institutional access to digital assets.

It initiated coverage of digital asset treasury companies Forward Industries (FWDI) and Cypherpunk Technologies (CYPH) with overweight ratings and price targets of $7.90 and $0.90, respectively.

New York Life Investment Management, a $807 billion asset manager, is putting a high-yield corporate bond strategy onchain for the first time. The firm partnered with tokenization platform Centrifuge to launch the NYLIM Anemoy U.S. High Yield Corporate Bond Segregated Portfolio, ticker HYB. The… Read the full story at The Defiant

Ripple remains one of the most discussed subjects in the crypto space as the company continues to advance its ecosystem and participate in major initiatives.

However, XRP has faced heavy pressure in the extended bear market, struggling to maintain momentum and hold above the $1 psychological barrier.

Joining the Giants

Several hours ago, Ripple announced that it is “proud to join” Open USD as a “day-one integration partner,” reinforcing its commitment to multichain infrastructure supporting institutional adoption across the crypto space.

Open USD (OUSD) is a new stablecoin designed for large-scale global payments. It is built by the independent organization Open Standard and aims to address several issues businesses face when using such financial products. OUSD is expected to go live later in 2026, and prominent backers include BlackRock, Visa, Mastercard, American Express, Coinbase, and others.

Just a few days ago, Ripple received approval from the Japanese Financial Services Agency (JFSA) to launch its own stablecoin (called RULSD) in the country. Shortly after, it revealed that last year it had committed $25 million in RLUSD to support underserved US small business owners and career programs for military veterans.

Despite these efforts, the stablecoin has lost some steam lately. Its market capitalization has dropped to roughly $1.4 billion, making it the 49th-biggest cryptocurrency.

The ETFs

The institutional interest in XRP remains solid. Over the past several weeks, ETF inflows have far exceeded outflows, signaling that pension funds, hedge funds, and other conservative market participants continue to increase their exposure to the asset.

Since day one, these products have generated a cumulative total net inflow of almost $1.5 billion. Recall that the first company to launch a spot XRP ETF in the USA was Canary Capital, while shortly after, Bitwise, Franklin Templeton, 21Shares, and Grayscale followed suit.

It is important to note that such investment vehicles with BTC and ETH as underlying assets have been bleeding heavily in recent months, underscoring a clear decline in institutional appetite.

XRP Price Outlook

Despite the aforementioned developments, XRP continues its fight to stay above $1. As of press time, it trades at around $1.04, representing a 20% plunge on a monthly scale.

Earlier this week, analyst Ali Martinez revealed that the Tom DeMark Sequential Indicator has flashed a buy signal on XRP and outlined the rising network activity. At the same time, though, he noted that whales have reduced their exposure to the asset, which can be interpreted as a bearish factor.

The post Ripple News and XRP Price Update Today: July 1 appeared first on CryptoPotato.

[PRESS RELEASE – Dubai, UAE, July 1st, 2026]

BNB Chain, one of the largest blockchain ecosystems worldwide, today announced the launch of BNB Agent Studio, a new platform that creates a category of AI agents that survive infrastructure failure, accept payments, and can be provably owned and transferred: deployed from a simple prompt in ~15 minutes.

BNB Agent Studio is a developer platform that enables engineers to define what they want inside Claude Code, Cursor, or any MCP-compatible development tool. By abstracting away the complexities of building onchain applications, the launch addresses three fundamental challenges that have prevented AI agents from operating truly autonomously: deployment, discoverability, and continuity.

Co-engineered with the AWS Generative AI Innovation Center, the solution includes an Infrastructure-as-Code generator that automatically provisions an agent’s cloud environment in accordance with current security and least-privilege best practices. It simply generates the code needed and deploys the agent to Amazon Bedrock AgentCore, Amazon’s managed agent runtime.

“Building an autonomous AI agent has typically meant assembling a fragile stack of four or more separate vendor integrations: a wallet, an identity layer, payments, an AI model, and hosting. We’re talking days and weeks of integration work. BNB Agent Studio replaces all of that with a single install, designed as one product from the ground up.” said Nina Rong, Executive Director of Growth at BNB Chain.

Key capabilities:

- BNB Agent Studio agents natively integrate LLM aggregators, allowing them to charge for their services and accept crypto payments for the work they perform. Those earnings allow the agent to fund its own operating costs, creating a self-sustaining cycle that keeps the agent running as long as it has work to do.

- BNB Agent Studio combines AWS AgentCore as the runtime with BNB Chain’s onchain infrastructure, so an agent’s core intelligence is simultaneously hosted on AWS and persisted onchain. The agent can be paused, resumed, migrated, and passed to a new owner without losing any of its accumulated intelligence. Its existence is no longer contingent on any single environment.

- Each agent is issued a verifiable digital identity (ERC 8004) controlled by cryptographic keys that stay on the owner’s own machine: not held by BNB Chain, not stored with any third party.

‘’With Amazon Bedrock AgentCore as the runtime, BNB Chain will unlock an entirely new category: AI agents as owned, tradeable, persistent digital entities. This vision will enable agents to be paused, resumed, migrated, recovered, and transferred, including through tokenisation.” Nina continued.

Today’s launch builds on BNB Chain’s recently announced BNB Agent SDK, which established a modular standard for identity (ERC8004), commerce (ERC8183), payment, and memory in AI agents. BNB Agent Studio is designed to be the fastest path from concept to a fully operational agent.

This is the initial release of BNB Agent Studio. Financial decisions have always demanded human time and attention to find the right yield, compare options, and act before an opportunity closes. When agents can do all of this autonomously, and when those agents are owned assets that persist, earn, and compound, the way people interact with their money changes fundamentally. BNB Chain intends to ship new capabilities on a fortnightly basis, with each update expanding the platform’s tooling for developers building in the agentic economy.

About BNB Chain

BNB Chain is the leading community-driven decentralized blockchain ecosystem powering Web3 applications across DeFi, AI, gaming, and consumer use cases. Its multi-chain architecture spans BNB Smart Chain (BSC), opBNB, and BNB Greenfield, providing the infrastructure for builders deploying onchain applications at scale. For more information, visit the official website.

The post BNB Chain Launches BNB Agent Studio: The AI Agent Infrastructure Behind Smart Money appeared first on CryptoPotato.

England-DR Congo live: Three Lions face World Cup underdogs for place in last 16

Venice AI becomes a unicorn with $65M Series A as its privacy-first AI platform takes off

‘GLOBAL FINANCIAL CRASH’: Central Bank Issues DIRE WARNING About NEW GREAT DEPRESSION!! | Kyle

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics5 days ago

Politics5 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World2 days ago

Crypto World2 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics6 days ago

Politics6 days agoPotential 2028er World Cup attendee leaderboard

-

Business5 days ago

Business5 days agoAsia stock markets slide as tech shares slump

-

News Videos3 days ago

News Videos3 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech6 days ago

Tech6 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World4 days ago

Crypto World4 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business2 days ago

Business2 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World4 days ago

Crypto World4 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports5 days ago

Sports5 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World6 days ago

Crypto World6 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech4 days ago

Tech4 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech4 days ago

Tech4 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World5 days ago

Crypto World5 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World5 days ago

Crypto World5 days agoRTX holders must register wallets before token distribution begins

-

Crypto World6 days ago

Crypto World6 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

-

Tech2 days ago

Tech2 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Sports3 hours ago

Sports3 hours agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

You must be logged in to post a comment Login