Crypto World

What is a stock buyback? How repurchases affect price

A stock buyback is a company spending its own cash to buy back its own shares. In crypto, it has become the move Bitcoin treasury companies reach for when the premium that powered them runs out.

Summary

- A stock buyback, or share repurchase, is when a public company uses cash to buy its own shares on the open market, reducing the number of shares outstanding.

- Fewer shares means each remaining share represents a larger claim on the company’s earnings and assets, which mechanically lifts earnings per share and can support the stock price.

- Companies buy back stock to return capital to shareholders, to signal that they see the shares as undervalued, and to offset the dilution created by issuing stock to employees.

- In crypto, buybacks have become central to Bitcoin treasury companies: when their shares stop trading at a premium to their coins, issuing new stock no longer works, so they turn to repurchasing instead.

- Buybacks differ from crypto token burns in one key way: repurchased shares are usually held in the treasury and can be reissued, while burned tokens are destroyed forever.

A stock buyback is one of the most common tools in corporate finance, and it has quietly become one of the most important levers in crypto. The basic idea is simple: a company uses its own cash to buy back its own shares from the market, shrinking the number of shares that exist. That reduction changes the math for every remaining shareholder. In the crypto world, buybacks have moved from a background technicality to a front-page issue because the Bitcoin treasury companies that dominate corporate crypto now lean on them when their main growth engine stalls. This guide explains how buybacks work, why companies use them, how they affect the price, why crypto treasuries have embraced them, and how they differ from the token burns they are often compared to.

What a stock buyback is

A stock buyback, also called a share repurchase, happens when a company that issued stock uses its cash to buy those shares back on the open market at the prevailing price. The purchased shares are absorbed by the company, which reduces the count of shares outstanding, the total number of shares held by all investors. There is no obligation for any shareholder to sell; the company simply buys from whoever is willing to sell at market, so a buyback is open to the market rather than targeted at specific holders.

The effect is a transfer of value expressed through arithmetic. A company’s ownership is divided into shares, and its earnings and assets are spread across those shares. Remove some shares from existence, and everything the company owns and earns is now divided among fewer of them. Each surviving share represents a slightly larger slice of the whole. That is the mechanical heart of a buyback, and everything else, the price effect, the signaling, the criticism, flows from it.

A buyback is one of two main ways a company returns cash to shareholders, the other being a dividend. A dividend pays cash directly to shareholders. A buyback returns value indirectly by increasing each holder’s proportional stake instead of sending them money. The choice between them shapes how the market reads a company’s use of its cash.

How buybacks are carried out

Companies repurchase shares through a few standard methods, and the method affects the pace and signal. The most common is an open-market repurchase, where the company buys its shares gradually over time on the exchange, just like any other buyer, often under a board-authorized program with a maximum dollar amount. This is flexible: the company can buy more when the price is attractive and pause when it is not, and the authorization is a ceiling, not a commitment to spend the full amount.

A tender offer is more direct: the company offers to buy a set number of shares from existing holders at a specified price, usually at a premium to the market, within a fixed window. Shareholders choose whether to accept. An accelerated share repurchase is faster still, with the company buying a large block of shares immediately through an investment bank and settling the details later. For most crypto treasury companies, the relevant form is the open-market program, authorized by the board up to a dollar cap, which the company then executes at its discretion depending on conditions.

The authorization is worth understanding clearly, because it is often misread. When a board authorizes a buyback of, say, up to $1 billion, it is granting permission to spend up to that amount, not promising to spend it. The company may buy the full amount, a fraction, or none, depending on the share price and its capital needs. A buyback authorization is a tool the company has armed, not a check it has written.

Why companies buy back stock

The motivations cluster into three main groups. The first is returning capital. A profitable company that generates more cash than it needs to run and grow the business has to do something with the surplus, and a buyback is one way to hand that value back to owners, as an alternative or complement to dividends. Rather than let cash sit idle, the company uses it to concentrate ownership among remaining shareholders.

The second is signaling. When a company buys back its own shares, especially aggressively, it communicates that management believes the stock is undervalued, worth more than the market is paying. A buyback is management putting the company’s money where its conviction is, and markets often read it as a vote of confidence. The signal is strongest when the company buys into weakness, purchasing shares while they trade below what leadership judges to be fair value.

The third is offsetting dilution. Companies routinely issue new shares to employees as compensation, which increases the share count and dilutes existing holders. Buybacks can counteract that, mopping up the newly issued shares to keep the total roughly stable. In this use, the buyback is less about returning capital and more about maintenance, preventing the slow erosion of each shareholder’s stake that stock-based pay would otherwise cause.

How buybacks affect the price

The price effect works through several channels at once. The most direct is supply and demand: a buyback removes shares from the market and adds a large, steady buyer, which can support the price simply through the purchasing itself. When a company is buying its own stock in size, it is one more source of demand competing for a now-smaller supply of shares.

The second channel is earnings per share. Because a company’s profit is divided across its shares, cutting the share count raises earnings per share even if total profit is unchanged. Since many investors value a stock as a multiple of its earnings per share, a higher figure can support a higher price. This is the arithmetic that makes buybacks attractive to management, though it is worth noting the improvement comes from a smaller denominator, not from the business earning more.

The third channel is sentiment. The signal of confidence a buyback sends can lift how investors feel about a stock, independent of the mechanical effects. Put together, reduced supply, higher earnings per share, and improved sentiment tend to support the price, which is why buybacks are generally received as shareholder-friendly. But the effect is not guaranteed. A buyback cannot rescue a company whose business is deteriorating, and a poorly timed one, buying shares at inflated prices, can destroy value rather than create it.

A worked example

Concrete numbers show the mechanism. Imagine a company with 100 million shares trading at $10, giving a market capitalization of $1 billion, and suppose it earns $100 million a year, which is earnings per share of $1. The company has surplus cash and authorizes a buyback, then repurchases 10 million shares at around $10 each, spending roughly $100 million.

After the buyback, the share count falls from 100 million to 90 million. If the company still earns $100 million, earnings per share rises from $1.00 to about $1.11, an increase of roughly 11%, without the business earning a single extra dollar. If investors keep valuing the stock at the same multiple of earnings, the price rises in step. And during the repurchase itself, the company’s buying supported the share price by adding demand. Every remaining shareholder now owns a slightly larger fraction of the same company.

The example also shows the catch. The company spent $100 million of real cash to achieve that arithmetic. If it had a more valuable use for the money, investing in growth, paying down expensive debt, the buyback might be the worse choice. And if the shares were overvalued at $10, the company overpaid to retire them, transferring value from the company to the shareholders who sold. The math always works; whether it creates value depends on price and alternatives.

Buybacks in Bitcoin treasury companies

This is where buybacks have become a live crypto issue. Bitcoin treasury companies are public companies whose main purpose is to hold Bitcoin or another crypto on their balance sheet, letting investors gain exposure through a stock. Their growth engine is issuing new shares at a premium to the value of their coins and using the proceeds to buy more crypto, which increases crypto per share. That engine works only while the stock trades above the value of its holdings, a condition often measured by a ratio called mNAV.

When the premium compresses toward the value of the coins, issuing new shares stops being accretive, because selling stock at or below the worth of the underlying crypto dilutes existing holders instead of enriching them. At that point, the growth lever jams, and the companies turn to the opposite move: buying back their own shares. A buyback becomes most attractive precisely when the stock trades near or below the value of its assets, because the company can retire shares cheaply and increase the crypto backing of each remaining share. The largest treasury companies have authorized buyback programs measured in billions, and some smaller ones have said they would repurchase shares if their stock kept trading below the value of its coins.

The signal is double-edged. A treasury company turning to buybacks is defending its stock and using capital sensibly at a discount, which is constructive. But it is also a tacit admission that the premium-issuance model that powered its rise has stopped working. When a company that grew by selling shares starts buying them back, the market reads it as the accretive era ending, which is why buybacks in this corner of crypto carry more meaning than a routine corporate repurchase.

Stock buyback versus crypto buyback-and-burn

Because crypto projects run their own version of buybacks, the comparison is worth drawing carefully. A crypto buyback-and-burn has a project purchase its own token on the market and then destroy it by sending it to a burn address, permanently removing it from supply. A stock buyback purchases shares and absorbs them into the company treasury, where they are removed from the trading float but not necessarily destroyed.

The difference is permanence and reissuance. Treasury shares from a buyback can be brought back later, reissued for acquisitions, compensation, or fresh capital, so the supply reduction can be undone. Burned tokens are gone for good, with no path back into circulation. There is also a difference in certainty: many crypto burns run automatically on smart contracts with fixed rules, while corporate buybacks are discretionary decisions management can start, pause, or stop. In short, both shrink supply to support value, but the token burn is absolute and often automatic, while the stock buyback is reversible and always discretionary. Understanding that distinction keeps the two mechanisms, which look similar on the surface, from being confused.

The case against buybacks

For balance, buybacks draw real criticism, and the objections are worth knowing. The first is that they can be financial engineering: lifting earnings per share by shrinking the share count rather than by growing the business creates the appearance of improvement without the substance. A company can report rising earnings per share while its actual profit stagnates, purely because there are fewer shares.

The second objection is timing. Companies have a poor track record of buying their own shares at the right price, often repurchasing heavily when the stock is high and flush times make cash plentiful, then stopping when the stock is cheap, and cash is tight, the opposite of buying low. Debt-funded buybacks sharpen the concern because borrowing money to retire shares adds leverage and risk in pursuit of a higher share price. Critics also argue that buybacks can enrich executives whose pay is tied to earnings per share or the stock price, and that money spent on repurchases is money not invested in research, wages, or growth.

None of this makes buybacks inherently bad. A well-timed buyback of an undervalued stock, funded from genuine surplus cash, can be an excellent use of capital. The critique is really about discipline: buybacks reward companies that repurchase cheaply from real surplus and punish those that overpay with borrowed money to flatter a metric. As with the crypto version, the mechanics are neutral; the judgment lies in the price, the funding, and the alternatives.

Buybacks, dilution, and the share-count treadmill

A detail that often gets lost in buyback coverage is how much of the activity simply offsets dilution instead of shrinking the share count on net. Many companies, especially in technology, pay employees heavily in stock, which issues new shares every year and dilutes existing holders. A large share of corporate buybacks goes toward mopping up those newly issued shares just to hold the total roughly flat. The buyback is real, but the net reduction is far smaller than the gross amount spent suggests.

This is the share-count treadmill. A company can announce billions in repurchases and still see its share count barely fall, because stock-based compensation is issuing shares out the other side at nearly the same pace. For shareholders, the important number is not how much a company spent on buybacks but how much the diluted share count actually changed. A buyback that only neutralizes dilution keeps ownership from eroding, which has value, but it is not the same as a buyback that genuinely concentrates ownership by cutting the count on net.

The distinction matters for how you read a company’s capital return. Gross buyback figures can look impressive while net share count is flat or even rising, if compensation-driven issuance outruns the repurchases. The honest way to judge is to track the diluted share count over several years and see whether it is falling, holding, or climbing. A steadily falling count shows buybacks are outpacing dilution and returning real value. A flat count shows the buyback is running on the treadmill, spending cash to stand still.

For Bitcoin treasury companies, this interacts with the model in a specific way. Their whole pitch is increasing crypto per share, so anything that quietly increases the share count works against that goal. A treasury company issuing stock for compensation while buying back shares needs the buybacks to more than offset the issuance, or crypto per share stalls even as the company appears to be returning capital. Watching net share count, not just the buyback headline, is how holders tell whether crypto backing per share is actually growing.

None of this makes buybacks that offset dilution pointless. Preventing erosion is a legitimate use of cash, and a company that did not repurchase would see its holders diluted year after year. The point is to read buybacks and issuance together. A repurchase program means little in isolation; paired against the shares a company is handing out, it reveals whether ownership is concentrating, holding, or slowly leaking away. The treadmill is invisible if you look only at the buyback side of the ledger.

Frequently Asked Questions

What is a stock buyback in simple terms?

A stock buyback is when a public company uses its own cash to buy back its own shares from the market. The repurchased shares are absorbed by the company, reducing the total number of shares outstanding. With fewer shares, each remaining share represents a larger portion of the company’s earnings and assets, which is the core effect a buyback produces.

How does a buyback affect the share price?

A buyback can support the price through three channels. It removes shares from the market while adding a large buyer, which is demand pressure. It raises earnings per share by dividing profit across fewer shares. And it signals management confidence that the stock is undervalued. These effects tend to support the price, but they are not guaranteed and cannot offset a deteriorating business.

Is a buyback the same as a dividend?

No. Both return value to shareholders, but differently. A dividend pays cash directly to shareholders. A buyback returns value indirectly by reducing the share count, so each remaining share represents a larger stake. Buybacks are more flexible, since a company can adjust or pause them, whereas cutting a dividend sends a strongly negative signal, so companies treat dividends as more of a commitment.

Why do Bitcoin treasury companies use buybacks?

Because their growth model depends on issuing shares at a premium to the value of their crypto. When that premium disappears and the stock trades near or below the worth of its coins, issuing new shares dilutes holders instead of helping them. Buybacks become attractive at that point, letting the company retire cheap shares and increase the crypto backing of each remaining share.

Does a buyback authorization mean the company will spend the money?

No. When a board authorizes a buyback of up to a certain amount, it is granting permission to spend up to that ceiling, not promising to spend it. The company may repurchase the full amount, a portion, or none, depending on the share price and its capital needs. An authorization is a tool the company has armed, not a guaranteed expenditure.

How is a stock buyback different from a crypto token burn?

A stock buyback absorbs repurchased shares into the company treasury, where they can be reissued later, so the reduction can be reversed. A crypto buyback-and-burn destroys the purchased tokens permanently at a burn address, so the cut is absolute. Many crypto burns also run automatically on smart contracts, while stock buybacks are discretionary decisions management can change.

Are buybacks good or bad for investors?

It depends on execution. A buyback of an undervalued stock, funded from genuine surplus cash, can be an excellent use of capital that benefits remaining shareholders. A poorly timed buyback that overpays for shares, or one funded with borrowed money, can destroy value. The mechanics are neutral; the outcome hinges on the price paid, the funding source, and whether the cash had a better use.

Can a buyback raise earnings per share without more profit?

Yes, and this is a common criticism. Because earnings per share divides profit by the share count, reducing the share count raises earnings per share even if total profit is unchanged. A company can report a higher figure purely from a smaller denominator. That is why analysts look at whether the underlying business is actually growing, not just at the reported per-share number.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or trading advice. Company share prices and crypto assets are volatile, and buybacks do not guarantee any price outcome. Nothing here is a recommendation to buy or sell any security or asset. Always do your own research and consider consulting a licensed professional before making financial decisions. Information is accurate as of July 1, 2026, and may change.

Tradeweb has carried out an onchain trade that pairs tokenized US Treasuries with tokenized cash, using Franklin Templeton as the seller of a tokenized Treasury security and Virtu Financial as the buyer. The execution reportedly took place over the Canton Network, with the companies saying settlement was completed in real time.

The deal is positioned as an industry milestone because it settles a tokenized Treasury against USDCx, a USDC-backed stablecoin issued on Canton. While the parties did not disclose the trade size, the firms framed the transaction as a practical step toward broader tokenized Treasury market infrastructure—particularly as major back-office plumbing, including DTCC’s planned tokenization services, moves closer to launch later this year.

Key takeaways

- Tradeweb executed a real-time onchain purchase-and-sale of a tokenized US Treasury settled against USDCx on the Canton Network.

- Franklin Templeton transferred the tokenized Treasury to Virtu Financial in exchange for tokenized cash, with Canton Network handling settlement synchronization.

- The trade is described as the first real-time purchase and sale of a tokenized US Treasury against USDCx, according to a Tradeweb spokesperson.

- The timing matters ahead of DTCC’s planned Tokenization Services rollout later this year.

- The transaction underscores how tokenized government bonds are moving from pilots toward production-style workflows.

A tokenized Treasury trade, settled in real time

According to the companies involved, Tradeweb served as the execution venue and source of price discovery for the transaction. Canton Network, meanwhile, coordinated settlement between the tokenized Treasury security and the tokenized cash leg of the trade.

Tradeweb and its counterparties said the trade settled in real time, though the exact notional amount was not released. Execution and settlement roles are often separated in traditional market structure; this type of workflow highlights how tokenization can compress those steps—at least within a controlled network environment—by linking asset and payment rails directly to the same settlement layer.

In a statement provided to Cointelegraph, a Tradeweb spokesperson said the transaction marked what they described as the industry’s first real-time purchase and sale of a tokenized US Treasury settled against USDCx, a USDC-backed stablecoin issued on Canton. Participants included Blockdaemon, Digital Asset, Societe Generale, Franklin Templeton, Tradeweb, and Virtu Financial.

Why the USDCx pairing is meaningful

The stablecoin used for settlement is not a minor detail. In tokenized Treasury markets, the “cash leg” is where many of the operational and compliance questions tend to concentrate: liquidity management, settlement finality, and how the payment instrument fits existing controls.

By explicitly citing settlement against USDCx on Canton, the firms are signaling that tokenized Treasuries can be paired with a stablecoin payment instrument on-chain—without requiring the buyer and seller to rely solely on separate off-chain cash processing. That matters for investors and trading desks because it can reduce settlement friction and shorten the path between trade execution and cash/asset finality, which are often decisive factors in institutional adoption.

At the same time, it remains important to watch how broadly these rails can scale beyond a limited set of participants. Real-time settlement claims are most meaningful when replicated across more counterparties, varied liquidity conditions, and larger volumes. The transaction size was not disclosed, leaving market participants to interpret the operational significance rather than the economic scale.

DTCC tokenization services as the next infrastructure milestone

The onchain trade also arrives ahead of a separate but related development: DTCC’s planned Tokenization Services later this year. DTCC has said the offering will enable participants to tokenize select stocks, exchange-traded funds (ETFs), and US Treasury securities while maintaining “the same investor protections and ownership rights as traditional assets,” according to DTCC’s published materials.

In practice, DTCC’s role is often associated with standardizing and simplifying settlement and custody workflows across the industry. If DTCC’s services deliver interoperable tokenization capabilities, they could help bridge the gap between isolated tokenization efforts and wider market participation. That makes Tradeweb and Canton’s transaction more than a standalone experiment—it can be read as preparation for a future where more participants can connect through shared tokenization infrastructure.

What remains uncertain is how DTCC’s approach will interact with existing tokenized Treasury ecosystems, including the specific stablecoin-based cash rails used for settlement. The Tradeweb/Canton transaction shows one functional pathway; the industry will likely be watching whether DTCC supports similar settlement models and whether cash and asset tokenization can be standardized across networks and venues.

Franklin Templeton’s wider tokenization push

This latest transaction fits into Franklin Templeton’s ongoing expansion of tokenized financial assets. Earlier this year, the asset manager partnered with Binance to let institutions use tokenized money market fund shares as trading collateral while keeping the underlying assets in regulated custody. Franklin Templeton has also partnered with Ondo Finance to bring tokenized ETFs onto blockchain networks, pointing to a broader strategy of onboarding institutional use cases through established market counterparties and custody frameworks.

The Treasury segment has been gaining attention alongside money markets and tokenized funds, in part because sovereign debt is often viewed as a foundational asset class for stable, yield-bearing tokenization strategies. While this does not automatically mean tokenized Treasuries will displace traditional Treasuries in size, each successful onchain settlement test reduces uncertainty about whether tokenized ownership can be operationally viable.

Governments and market data: tokenized sovereign debt keeps growing

Tokenized government bond efforts are not limited to the private sector. Several jurisdictions have launched blockchain-based initiatives to test issuance, settlement, and market infrastructure for sovereign debt.

Hong Kong was among the early movers, launching an inaugural digital green bond in 2023 and completing its third digital green bond issuance in November 2025, according to Hong Kong Monetary Authority announcements. Separately, the HKMA has said it will build a digital asset platform to support issuance and settlement of tokenized bonds, with plans to expand the infrastructure to other digital assets and connect with tokenization platforms across the region.

In the UK, the government appointed HSBC Orion to support its Digital Gilt Instrument pilot, designed to test blockchain-based issuance, settlement, and secondary trading of government bonds.

Meanwhile, on-chain Treasuries have reached significant scale in tokenized form. Data from RWA.xyz cited in the announcement places the tokenized US Treasury market at $14.6 billion, spanning 84 on-chain products and representing the largest segment within the tokenized real-world assets market.

Taken together, the picture that emerges is one of gradual maturation: policy pilots are exploring the mechanics of tokenized sovereign debt, while institutional market players are running increasingly production-like trades that validate execution and settlement workflows. The Tradeweb–Franklin Templeton–Virtu Financial transaction adds a concrete “cash + asset” settlement example—one that is particularly relevant for traders and custodians who need clarity on how stablecoin-based settlement can function alongside tokenized Treasuries.

Next, investors and market participants should watch for how DTCC’s forthcoming Tokenization Services change the connectivity and standardization of tokenized Treasuries settlement, and whether real-time USDCx-based settlement models prove replicable across more counterparties and larger volumes.

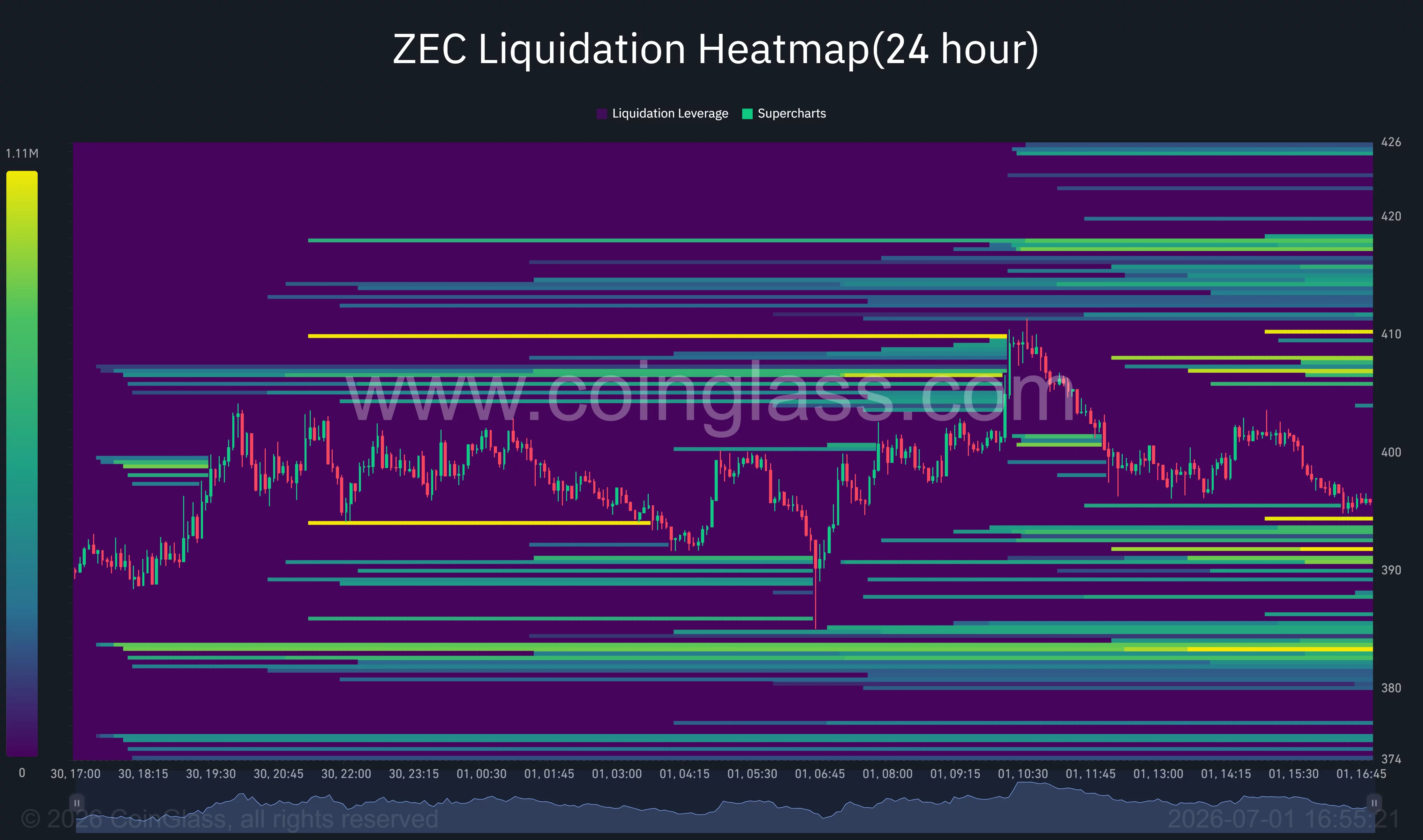

Zcash price has remained pinned below the $400 level after last month’s Orchard security scare, persistent overhead supply, and cautious derivatives positioning offset signs of improving buying pressure.

Summary

- Zcash price remains below $400 as sellers continue defending key resistance after June’s security-driven selloff.

- Technical charts show $410 as the breakout level, with $440 and $490 emerging as the next upside targets.

- Liquidation data and macro uncertainty keep downside risks alive unless buyers reclaim the descending trendline.

According to data from crypto.news, Zcash (ZEC) traded around $396 at the time of writing, little changed over the past week despite a relief bounce across several large-cap altcoins.

The privacy coin continues to recover from its violent early June collapse, when a critical flaw in the Orchard zero-knowledge proof circuit briefly raised double-spending concerns before developers deployed an emergency network upgrade. Although no funds were stolen, the event triggered a wave of liquidation and institutional selling that continues to weigh on price.

The fallout extended beyond the technical fix. Arthur Hayes exited his ZEC position during the panic, while the earlier 50% crash from roughly $624 to $309 left a large concentration of trapped holders at higher prices. That supply continues to emerge whenever ZEC approaches the $400-$420 region, limiting follow-through buying despite the stabilization seen during the past several sessions.

Descending trendline keeps Zcash trapped below key Fibonacci resistance

The daily chart shows ZEC trading just beneath the 61.8% Fibonacci retracement level near $419, a zone that rejected multiple recovery attempts following the June breakdown. Price also remains below a descending trendline that has defined the lower-high structure since the post-crash rebound peaked near $530 in mid-June.

Momentum indicators remain mixed. The daily RSI sits near 41, leaving room for another recovery attempt without entering overbought territory, while the MACD remains below its signal line despite the bearish histogram steadily shrinking. Together, the indicators suggest selling pressure has eased but buyers have yet to regain control of the longer-term trend.

The 4-hour chart presents a slightly more constructive picture. ZEC has begun testing the descending resistance line that has capped every rally over the past two weeks, while the Chaikin Money Flow has climbed back above zero, suggesting fresh capital has started entering the market. Even so, the Aroon indicator continues to favor the prevailing downtrend, showing that bullish momentum has not yet replaced the existing market structure.

According to analyst Team LAMBO, a decisive move through the immediate ceiling could change the short-term outlook. “ZEC can breakout above 410 to target 440 and 490 again,” the analyst wrote in a recent market update, identifying $410 as the trigger level that could expose the next resistance areas near $440 and $490.

Derivatives positioning also shows why the current range remains difficult to escape. CoinGlass liquidation heatmaps reveal dense clusters of leveraged short positions concentrated around $405-$410 and again near $418-$420. A sustained break through those zones could force short liquidations and accelerate upside momentum. On the downside, another significant concentration of long liquidations sits between roughly $392 and $385, creating an area where volatility could increase if sellers regain control.

Macro risks continue to challenge the recovery thesis

Several external risks continue to limit appetite for privacy-focused cryptocurrencies despite improving technical conditions. Crypto market sentiment remains fragile after weeks of elevated volatility, while investors continue to monitor U.S. inflation data, interest-rate expectations, and geopolitical tensions that have reduced demand for higher-risk digital assets.

Regulatory uncertainty also remains a headwind unique to the privacy coin sector. European compliance initiatives and tighter scrutiny of anonymous digital assets continue to discourage institutional participation, reducing the amount of fresh capital available to absorb the overhead supply left behind by June’s selloff.

The bullish setup would weaken if ZEC fails to hold support around $390, with a break below that level exposing the stronger demand zone near $380 and potentially the 78.6% Fibonacci retracement around $345.

A confirmed close above $410, however, would invalidate the current lower-high sequence and increase the probability of a move toward the $440 resistance area, with $490 becoming the next upside objective if buying momentum accelerates.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Solana perpetuals exchange Drift Protocol has rebranded to Velocity DEX, the protocol's official X account announced on Wednesday. Solana's own account confirmed the switch shortly after, posting "FYI: @driftprotocol is now @VelocityDEX." Velocity DEX said the new name reflects "a cleaner… Read the full story at The Defiant

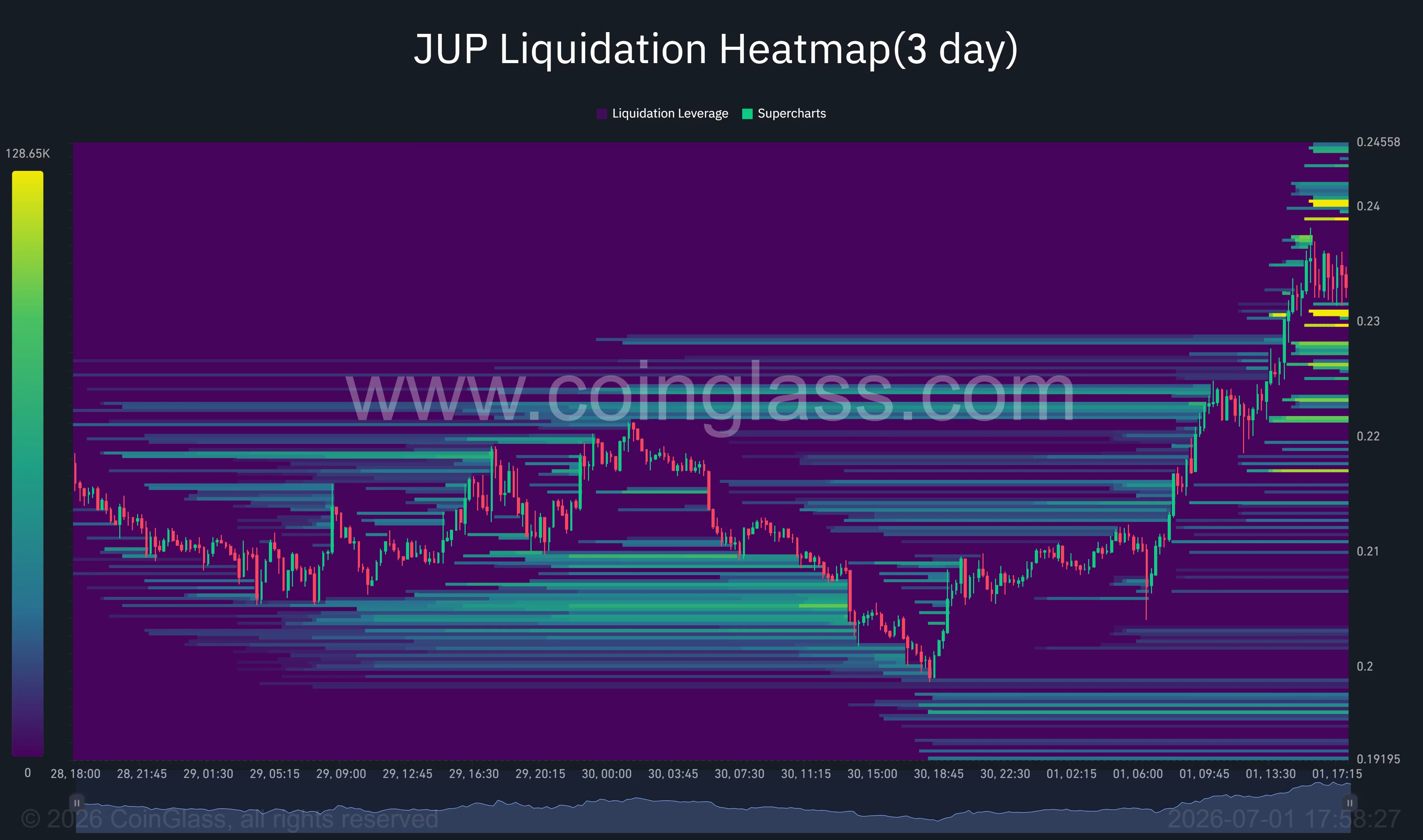

Jupiter has surged more than 15% after a sharp rebound in June protocol revenue revived bullish sentiment despite persistent risk-off conditions across the crypto market.

Summary

- Jupiter jumped more than 15% after June protocol revenue climbed to a three-month high.

- Technical indicators show JUP has reclaimed its 200-day EMA as open interest and funding rates strengthened.

- Bulls now target the $0.24-$0.26 range, while losing $0.218 support could revive selling pressure.

According to data from crypto.news, Jupiter (JUP) traded around $0.233 at the time of writing after briefly touching an intraday high near $0.238, extending its weekly gain to almost 30%.

The token’s rally followed a sharp improvement in protocol activity during June. Data from DeFiLlama showed Jupiter generated 261,909 SOL in user fees and 76,257 SOL in protocol revenue during the month, reversing three consecutive months of weakening network activity.

Because a portion of protocol revenue feeds Jupiter’s staking and governance model, the jump in cash flow quickly translated into renewed demand for the token.

The move also arrived while risk appetite across digital assets remained subdued. The Crypto Fear & Greed Index has continued to hover in Extreme Fear territory near 11 as macro uncertainty and tighter liquidity conditions keep investors selective toward altcoins. Jupiter nevertheless outperformed most large-cap tokens, suggesting traders have prioritized protocol-specific fundamentals over macro headwinds.

Derivatives traders joined the advance rather than fading it. Open interest climbed roughly 11% to $58.7 million, while funding rates stayed positive near 0.0021%, showing leveraged traders have continued paying a premium to maintain long exposure instead of aggressively hedging the rally. That combination generally supports sustained momentum as long as fresh buying continues to absorb profit-taking.

Bulls have reclaimed the long-term trend while momentum targets higher resistance

The daily chart shows JUP has reclaimed its 200-day exponential moving average around $0.219, a level that repeatedly rejected advances during the previous decline. Price has also remained comfortably above the daily Supertrend indicator near $0.169, preserving the bullish structure established after June’s recovery.

Momentum indicators continue to favor buyers. The daily MACD remains above its signal line despite a modest slowdown in histogram expansion, suggesting upside momentum has eased but has not reversed. On the four-hour chart, RSI has climbed to about 63 without entering overbought territory, while the MACD has completed another bullish crossover as price pushes back toward the recent swing high.

The 4-hour structure also shows JUP trading above an ascending trendline that has supported higher lows since early June. Fibonacci retracement levels place immediate resistance near $0.238, followed by the psychological $0.24 region. A decisive close above that zone could expose the May peak around $0.26, while the 0.786 Fibonacci level near $0.218 now serves as the first important support during any pullback.

CoinGlass liquidation data reinforces those technical levels. The largest concentration of short liquidations sits between roughly $0.238 and $0.245, creating a potential liquidity pocket if buyers force another breakout. Below the market, notable long liquidation clusters have formed around $0.22 and $0.21, areas that could attract buyers if price retraces before attempting another advance.

Failure to hold support could revive the previous bearish trend

The bullish outlook would weaken if JUP loses the ascending trendline and falls back below the former breakout zone around $0.218. Such a move would place the 200-day EMA under pressure again and increase the probability of a decline toward the $0.20-$0.19 region, where the 0.5 Fibonacci retracement aligns with previous consolidation.

Macro risks also remain in place despite Jupiter’s strong fundamentals. Persistent risk-off sentiment, reduced liquidity across crypto markets, or renewed weakness in Solana ecosystem tokens could limit follow-through buying. Without continued growth in protocol revenue and sustained derivatives participation, the latest breakout could lose momentum before challenging the next major resistance zone above $0.24.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

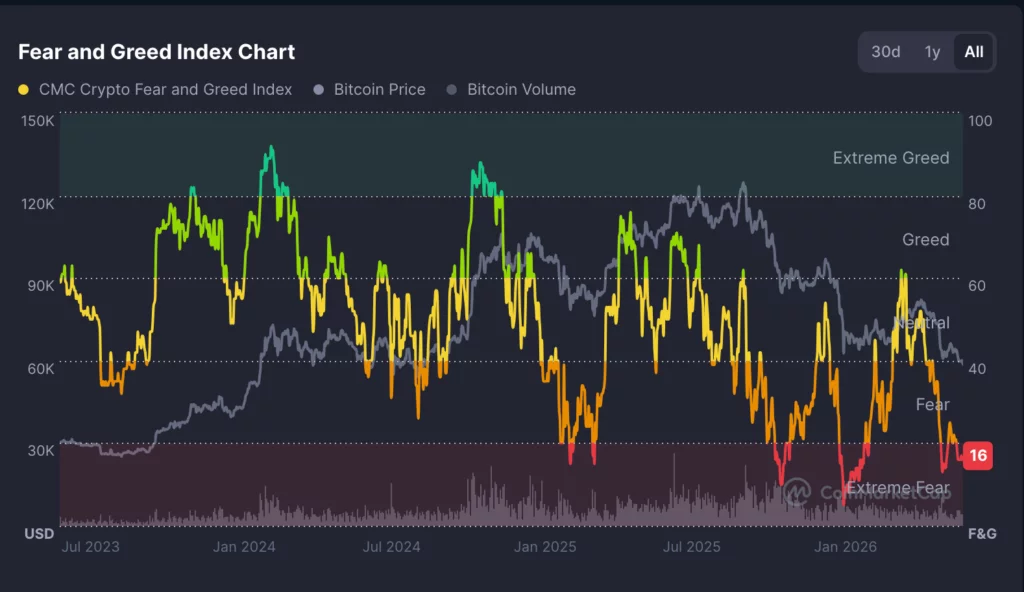

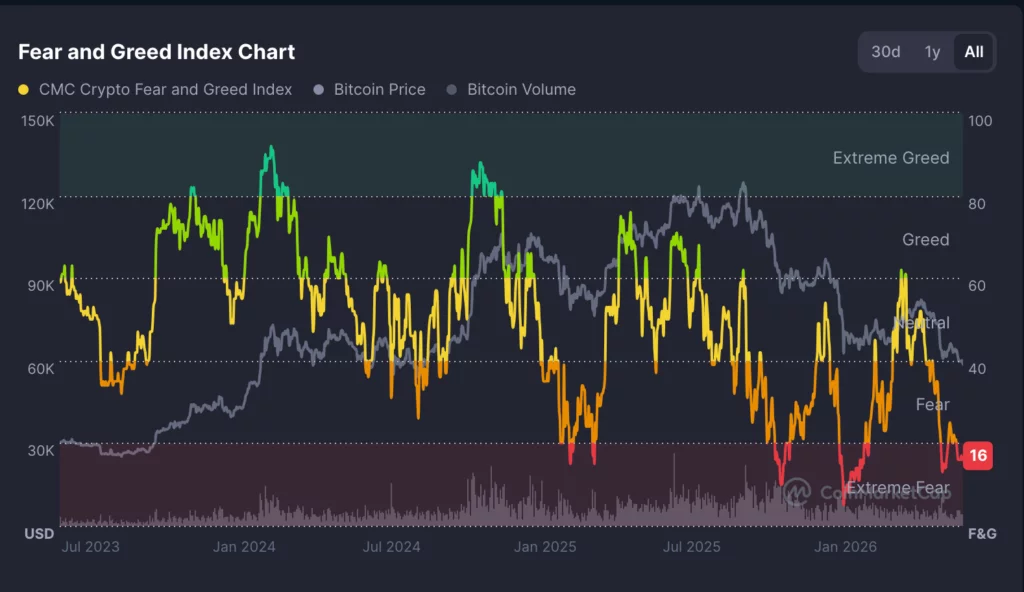

Bitcoin sits near $58,000 to $60,000 with the Fear and Greed Index buried in extreme fear. History says washed-out sentiment often precedes bottoms, but fear is a signal, not a floor. Here are the gauges traders are actually watching.

Summary

- Bitcoin trades near $58,000 to $60,000 as of July 1, 2026, down about 53% from its October 2025 record of $126,198, after back-to-back quarterly losses to open the year.

- The Fear and Greed Index sits around 12 to 16, deep in extreme fear, a zone that has historically appeared near local bottoms but is not a timing tool on its own.

- Bullish positioning signals are stacking up: open interest has collapsed from over $90 billion to about $44.5 billion, leverage is flushed, and coins are leaving exchanges in a pattern that suggests accumulation.

- The bearish counterweight is real: spot Bitcoin ETFs posted a record $4.5 billion of outflows in June, the Fed is hawkish with a likely December rate hike priced in, and one cycle model points to a bottom only around mid-October.

- The signals that would confirm a turn are concrete: reclaiming the 20-day and longer moving averages, a flip back to ETF inflows, open interest rebuilding alongside price, and the fear gauge lifting off its extremes.

Extreme fear is one of the most misread conditions in markets. When the Fear and Greed Index drops into the low teens, the crowd reads it as a reason to run, and the contrarian reads it as a reason to buy. Both are oversimplifying. Sentiment this low tells you that positioning is stretched and conviction is gone, which is often the raw material of a bottom, but “often” is not “now,” and fear can always get more extreme before it breaks.

The useful move is not to treat the fear gauge as a signal by itself, but to read it alongside the harder data on positioning, flows, and price. This piece walks through the signals traders are watching, lays out the bullish and bearish readings of each, and identifies what would actually confirm that the turn has arrived. The key point is simple: fear tells traders to pay attention, not to assume the bottom is already in.

What the Fear and Greed Index is saying

Start with the gauge everyone quotes. The Fear and Greed Index compresses several inputs, volatility, momentum, volume, and social signals, into a single 0 to 100 reading, and the latest chart still shows the market deep in extreme fear. Historically, readings this low have clustered near local bottoms, because they mark the point where sellers have largely exhausted themselves and the marginal holder is fearful rather than greedy. That is the contrarian appeal: when nobody wants the asset, much of the selling may already be done.

The caution is that the index is a description of the present, not a prediction of the future. Extreme fear can persist for weeks, and it can deepen. During genuine downtrends, the gauge has sat in fear for long stretches while price kept falling, so treating a low reading as an automatic buy signal has burned plenty of traders. The right way to use it is as context: it tells you the emotional backdrop is washed out, which raises the odds that other bottoming signals are meaningful, without confirming anything on its own.

That is why how the index works matters before using it as a trading signal. The number is useful because it summarizes the market mood, but it is not a floor under price. For confirmation, traders still need price levels, ETF flows, leverage data, and macro conditions to line up.

Signal one: positioning has reset

The most constructive signal under the surface is what happened to leverage. Open interest in Bitcoin derivatives has collapsed from above $90 billion to roughly $44.5 billion over recent weeks, less than half its peak. That drop reflects long liquidations, profit-taking, and traders reducing speculative exposure. In plain terms, the leverage that builds up in a rally and makes a market fragile has been flushed out.

Why this matters for a turn is mechanical. A market loaded with leveraged longs is vulnerable, because small drops trigger liquidations that cascade into larger drops. A market where that leverage has been cleared is sturdier, because the forced-selling fuel is gone. Resets like this often precede bottoms, since they remove the overhang that drags price lower and leave room for fresh positioning to push the other way.

The bearish reading is that falling open interest also signals fading demand and cautious participation, not just healthy deleveraging. Traders stepping back can mean they see no reason to buy, and a market with thin conviction can drift lower on light volume. The reset is a necessary condition for a durable bottom, but it is not sufficient by itself, because clean positioning can still sit under a price that keeps grinding down.

Signal two: exchange flows and accumulation

The second signal comes from where the coins are moving. Through the drawdown, Bitcoin has seen exchange outflows exceed inflows, meaning more coins are leaving exchanges than arriving. That pattern is typically read as accumulation: holders pulling coins into self-custody or long-term storage rather than keeping them on exchanges ready to sell. When supply leaves the venues where selling happens, it thins the pool of coins available to hit the market.

The bullish interpretation is that long-term holders are quietly buying weakness while short-term traders panic, a divergence that has marked accumulation phases before. Steady outflows during extreme fear suggest conviction underneath the fear, the kind of hands that absorb selling and set the base for a recovery. That is the constructive version of the on-chain story, and it fits with the broader idea that the market is moving from forced selling toward accumulation.

The counterpoint is that exchange flows are noisy and can reflect custody shifts, institutional plumbing, or one-off moves rather than genuine accumulation. Outflows are encouraging, but they are a soft signal, easily overstated. On their own they confirm that some holders are unbothered, not that the bottom is in. They matter most when they line up with stronger evidence from ETF flows and price.

Signal three: the ETF bid

The third signal is the one cutting against the bulls, and it is the most important on the bearish side. Spot Bitcoin ETFs recorded about $4.5 billion of net outflows in June 2026, their worst month since launching, removing the steady institutional bid that had cushioned earlier declines. The funds that were supposed to represent durable, price-insensitive demand instead became a source of selling, and their flows have tracked the drawdown closely.

This matters because the ETF bid was a structural change in how Bitcoin traded. When it was flowing in, it provided a floor of consistent demand. When it reverses, that floor becomes a headwind, and the market has to find other buyers to absorb the redemptions. For sentiment to turn convincingly, this is the signal that most needs to flip.

A return to sustained ETF inflows would tell the market that institutions are stepping back in, which would validate the bullish reading of the other signals. Continued outflows would keep the pressure on regardless of how washed out the fear gauge looks. That is why the ETF bid that reversed deserves more weight than a sentiment reading alone. In this cycle, flows are not a side detail; they are one of the main channels moving the market.

Signal four: oversold technicals

The fourth signal is on the chart. The relative strength index has dropped near 30, the oversold threshold, indicating that momentum has fallen far and fast and that the move may be stretched to the downside. Price sits near support in the $58,000 area, below the 20-day exponential moving average around $62,450, and well beneath the longer-term moving averages, the 200-day near $65,200 and the 50-month near $65,600, that mark the bull-bear boundaries.

The bullish read is that oversold conditions at support are where reversals begin, and a bounce off the high $50,000s that reclaims the moving averages would signal the downtrend is weakening. The bearish read is that oversold can stay oversold in a strong downtrend. Until price actually reclaims those moving averages, the path of least resistance points lower, with a break below support opening the door toward the mid-$50,000s. The technicals frame the levels, but they do not resolve the direction until price picks one.

That is why the level-based bottom question matters alongside sentiment. Bitcoin does not bottom because the index is low; it bottoms when buyers defend levels, reclaim resistance, and force trend-followers to change position. The fear gauge tells traders the market is stretched. The chart tells them whether the stretch is becoming a reversal.

The bull read: capitulation precedes bottoms

Put the constructive signals together and a coherent bottoming case emerges. Extreme fear, flushed leverage, steady accumulation, and oversold momentum are the classic ingredients of capitulation, the moment when the last weak hands sell and stronger hands absorb the supply. In prior cycles, this combination has marked the exhaustion of a downtrend, the point where selling pressure runs out because everyone inclined to sell already has. In this reading, the current setup looks less like the start of a new collapse and more like the late stage of a forced reset.

The bull case also treats the record ETF outflows as a lagging sign of the same capitulation instead of a fresh catastrophe. Institutions derisked into weakness, leverage was cleared, and sentiment collapsed into extreme fear. If that selling has already happened, the market may be closer to a base than the headline fear suggests. The reset positioning and the accumulation on-chain suggest a foundation is forming under the panic.

If that is right, the setup favors a recovery once a catalyst arrives to flip sentiment, and the extreme fear reading becomes, in hindsight, the marker of the low. This is the contrarian thesis, and the data gives it real support. The key caveat is timing: a market can be in a bottoming zone before the actual bottom is printed. Bulls still need confirmation before calling the turn.

The bear read: fear can deepen

The opposing case is equally grounded, and it starts with the fact that Bitcoin is down about 53% from its high with back-to-back quarterly losses, a genuine bear market instead of a shallow dip. Deep drawdowns can extend, and washed-out sentiment can get more washed out. The macro backdrop offers no relief: the Fed is hawkish under its current chair, markets are pricing a strong chance of a December rate hike as inflation drifts back toward 4%, and a key jobs report looms, all of which pressure risk assets like Bitcoin, which trades as high-beta risk far more than as a haven.

There is also a timing argument. One cycle model notes that bear-market corrections have averaged about 12 months, which, measured from the October 2025 record, points to a bottom only around mid-October 2026. By that reading, the current fear could be a stop along the way instead of the destination, with more downside and more time required before a durable low. The record ETF outflows, in this frame, are an active headwind, not a capitulation tail.

Fear is a signal, not a floor, and it can persist far longer than the impatient expect. The chart can stay oversold, ETF flows can stay negative, and macro can keep forcing risk assets lower. That does not invalidate the bottoming signals; it simply means they are conditions, not confirmations. The bear case is strongest as long as price remains below the key moving averages and the ETF bid stays absent.

What would confirm a turn

The way to cut through the debate is to watch for confirmation instead of guessing at the bottom. Four signals would mark a genuine turn. The first is price reclaiming the 20-day EMA near $62,450 and then the heavier resistance around $64,000, which would break the pattern of lower highs and put buyers back in control. The second is ETF flows flipping from outflows back to sustained inflows, the clearest sign the institutional bid has returned.

The third is open interest rebuilding alongside a rising price, which would show fresh capital coming in with conviction instead of a low-volume drift. The fourth is the Fear and Greed Index lifting off its extremes, confirming that the emotional backdrop is normalizing. Until several of those align, the constructive signals remain a setup instead of a trigger. Extreme fear, reset leverage, and accumulation describe a market that could turn, not one that has.

The discipline is to treat washed-out sentiment as a reason to watch closely, while waiting for price and flows to confirm before concluding the low is in. That is how experienced traders use a reading in extreme fear: not as a buy button, but as a cue to track the signals that actually mark the turn. The lower the fear gauge falls, the more important confirmation becomes, because the emotional temptation to act early grows stronger.

How this fear compares with past bottoms

Extreme fear is not new, and prior episodes offer a rough guide to how it tends to resolve, with a large caveat. In earlier cycles, the deepest fear readings have often clustered near major lows, appearing when a drawdown was closer to its end than its beginning, precisely because fear peaks when selling has run far. The pattern that has marked durable bottoms combines washed-out sentiment with flushed leverage and steady accumulation by long-term holders, the same three ingredients visible now. On that template, the current setup rhymes with past bottoming conditions.

The caveat is that the template has failed often enough to demand humility. Extreme fear has also appeared in the middle of downtrends, not just at their ends, and readers who bought every low reading in a bear market bought too early more than once. The difference between a fear reading that marks a bottom and one that marks a pause is usually not visible in the sentiment gauge itself. It shows up later, in whether price reclaims key levels and whether the institutional bid returns.

There is also a structural change that makes the comparison imperfect. The presence of spot ETFs has altered how Bitcoin trades, adding a large, flow-driven institutional participant that did not exist in earlier cycles. That means past bottoming patterns, built in a market without ETFs, may not map cleanly onto this one. The ETF flows can amplify moves in both directions, which is why the record June outflows matter so much and why this cycle’s bottom may look different from the ones the historical template describes.

The macro calendar that matters

Because Bitcoin is trading as a high-beta risk asset, the signals most likely to flip or deepen sentiment are macroeconomic, and the calendar is crowded. The nearest is the monthly jobs report, a read on labor-market strength that feeds directly into rate expectations: a hot number would reinforce the case for the Fed staying tight, pressuring risk assets, while a soft number could revive hopes for easier policy and lift them. Traders watching for a sentiment turn are watching that print closely. It is not a crypto-native signal, but it can decide whether crypto-native bottoming signals actually matter.

Further out sits the Fed itself. With markets pricing a meaningful chance of a December rate hike as inflation drifts back toward 4%, each inflation report and each Fed meeting becomes a potential catalyst. A hawkish surprise would deepen the risk-off mood that has weighed on Bitcoin, while any sign the tightening is ending could mark the macro turn that a sentiment-driven bottom needs. The path of rates, more than any crypto-native signal, is the backdrop against which the fear gauge will either normalize or sink further.

The practical point is that a durable turn in Bitcoin sentiment probably requires a shift in the macro wind, not just an oversold chart. The internal signals, reset leverage, accumulation, extreme fear, describe a market primed to respond, but the trigger is likely to come from outside crypto: a softer labor market, a friendlier inflation path, or a Fed that signals the end of tightening. Until the macro calendar delivers one of those, the constructive crypto signals remain a coiled setup waiting for a catalyst, which is why traders track the economic data as closely as the order book right now.

The one signal that matters most

With so many gauges flashing at once, it helps to rank them, and in this cycle one signal outranks the rest: the ETF bid. Before spot Bitcoin funds existed, a bottom was mostly a story about on-chain holders, leverage, and sentiment, the classic signals. Those still matter, but the arrival of ETFs added a large, flow-driven institutional participant whose buying and selling now sets much of the marginal price. When that participant is buying, it provides a steady floor. When it is selling, as it was through the record June outflows, it becomes a persistent drag that the other signals cannot easily overcome.

That is why the ETF flow number deserves more weight than the fear gauge or the RSI. Extreme fear can mark a bottom, reset leverage can prime one, and accumulation can build a base, but none of them forces the institutional bid to return. The flows do that directly. A market can sit at extreme fear with clean positioning and still grind lower if the funds keep redeeming, because the redemptions are real selling that has to be absorbed.

Conversely, a decisive flip back to sustained inflows would validate every other constructive signal at once, confirming that the capitulation the other gauges describe has actually ended. The practical takeaway is a hierarchy. Treat the ETF flows as the primary confirmation, the signal that most reliably separates a real turn from a false one. Treat reset leverage and on-chain accumulation as supporting evidence that the setup is favorable. Treat extreme fear and oversold technicals as context that raises the odds without confirming anything.

The macro calendar is the likely trigger that moves the flows one way or the other. Reading the signals in that order, flows first, positioning second, sentiment last, is how to avoid the classic trap of buying extreme fear too early. The gauge in extreme fear tells you the market is primed. The ETF flows will tell you when it has actually turned.

Frequently asked questions

What does a Fear and Greed reading near 16 mean?

It means the index sits deep in extreme fear, its lowest zone, reflecting washed-out sentiment across volatility, momentum, volume, and social signals. Historically, readings this low have appeared near local bottoms because much of the selling may be exhausted. But it is a description of the present, not a prediction, and extreme fear can persist or deepen during a real downtrend.

Is extreme fear a reliable buy signal?

Not on its own. Low readings raise the odds that a bottom is near, but sentiment can stay fearful for weeks while price keeps falling. It is best used as context alongside harder data on positioning, flows, and price, instead of as a standalone trigger. Treating a low reading as an automatic buy has repeatedly caught traders too early.

Why does falling open interest matter?

Open interest dropping from over $90 billion to about $44.5 billion means leverage has been flushed out through liquidations and derisking. That makes the market sturdier, because the forced-selling fuel that drives cascading drops is gone, which often precedes bottoms. The caveat is that falling open interest can also signal fading demand, so it is a necessary but not sufficient condition for a turn.

What are exchange outflows telling us?

More Bitcoin has been leaving exchanges than arriving, a pattern typically read as accumulation, with holders moving coins into storage instead of keeping them ready to sell. It suggests conviction underneath the fear. But exchange flows are noisy and can reflect custody or institutional shifts, so they are a soft signal that some holders are unbothered, not proof the bottom is in.

Why are the ETF outflows so important?

Spot Bitcoin ETFs posted a record $4.5 billion of outflows in June 2026, turning the steady institutional bid that once cushioned drops into a headwind. Because that bid was a structural support, its reversal is the signal that most needs to flip for a convincing turn. A return to sustained inflows would validate the bullish case, while continued outflows keep pressure on regardless of sentiment.

Where is Bitcoin’s key support and resistance?

Support sits near the $58,000 area, and reclaiming the 20-day EMA around $62,450 is the first upside test, followed by heavier resistance near $64,000 and the longer-term moving averages around $65,200 to $65,600. RSI near 30 shows oversold momentum. A break below support opens the door toward the mid-$50,000s, while reclaiming the moving averages would signal the downtrend is weakening.

Could Bitcoin fall further from here?

Yes. Bitcoin is down about 53% from its record with back-to-back quarterly losses, and deep drawdowns can extend. A hawkish Fed, a likely December rate hike, and looming jobs data pressure risk assets, and one cycle model points to a bottom only around mid-October 2026. Extreme fear is a signal, not a floor, and it can persist longer than expected.

What would confirm that Bitcoin has turned?

Four signals: price reclaiming the 20-day EMA near $62,450 and then resistance around $64,000, ETF flows flipping back to sustained inflows, open interest rebuilding alongside a rising price, and the Fear and Greed Index lifting off its extremes. Until several align, the constructive signals describe a market that could turn instead of one that has, so confirmation should come before conviction.

Disclaimer: This article is for information purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency prices are highly volatile, and technical and sentiment analysis is speculative and may not predict actual movements. Nothing here is a recommendation to buy or sell any asset. Always do your own research and consider consulting a licensed professional before making financial decisions. Figures are accurate as of July 1, 2026, and will change.

Shares in the Trump family-backed American Bitcoin (ABTC) sank to an all-time low on Wednesday after the crypto miner set a date for a 1-for-15 reverse stock split in a bid to stay listed on the Nasdaq.

American Bitcoin said its reverse stock split will go into effect after the market closes Thursday and will begin trading on a split-adjusted basis when the market opens Monday. It would continue to trade under the ticker ABTC.

It said every 15 shares of the company’s Class A and B common stock will be reclassified as one share. The company expects its common stock to be reduced from more than 1 billion outstanding shares to about 73 million.

American Bitcoin is the only public crypto company tied to the Trump family’s sprawling interests in the sector, and a reverse stock split is typically seen as a negative, as it indicates the company is in distress and is looking to artificially boost its share price.

American Bitcoin said the split aims to prop up its shares to maintain compliance with Nasdaq’s minimum bid requirements, which allow the exchange to delist the company if it trades below a $1 closing price for 30 consecutive trading days.

Shareholders had approved the reverse stock split on June 22.

American Bitcoin shares hit all-time low

Shares in American Bitcoin dropped nearly 8.4% to close trading Wednesday at an all-time low of 62 cents. The stock saw a slight lift after-hours, rising 4.5% to 65 cents.

American Bitcoin’s stock tumbled to an all-time closing low of 62 cents on Wednesday. Source: Google Finance

American Bitcoin’s stock is down more than 63% so far this year and has fallen more than 92% since the brand started trading on the Nasdaq on Sept. 3.

The company was co-founded early last year by US President Donald Trump’s sons, Donald Trump Jr. and Eric Trump.

American Bitcoin merged with the Nasdaq-listed Gryphon Digital Mining to go public, with the Trump brothers and crypto miner Hut 8 together owning around 98% of the newly formed company.

Related: Bitcoin miners need billions to fund AI ambitions, led by IREN’s $21B gap

The company’s falling share price comes amid a wider downturn in the crypto market. American Bitcoin reported in May that it lost $81.7 million in the first quarter.

Other crypto companies have also turned to reverse stock splits to prop up their share price. Bitcoin financial services company Nakamoto completed a 1-for-40 reverse stock split in May in a bid to stay listed on the Nasdaq after it reached a low of 16 cents in April.

Bitcoin (BTC) was trading at around $60,000 early Thursday, down 32% so far this year and having more than halved from its peak of more than $126,000 in October, according to CoinGecko.

Magazine: Clarity Act risks repeat of Europe’s mistakes, crypto lawyer warns

American Bitcoin (ABTC) is set to complete a 1-for-15 reverse stock split as it tries to remain listed on Nasdaq, a move that arrives as the company’s shares sink to fresh lows. The miner said the split becomes effective after the market closes on Thursday and will be reflected in trading on a split-adjusted basis when the market opens Monday, with the stock continuing to trade under the ABTC ticker.

Under the plan, every 15 shares of the company’s Class A and Class B common stock will be consolidated into a single share. American Bitcoin expects that its share count will fall from more than 1 billion outstanding shares to about 73 million. According to the company’s release, shareholders approved the reverse split on June 22, and the company now aims to satisfy Nasdaq’s minimum bid rules.

Key takeaways

- ABTC’s 1-for-15 reverse stock split takes effect after Thursday’s market close and begins trading on a split-adjusted basis on Monday.

- American Bitcoin expects its outstanding shares to drop from over 1 billion to roughly 73 million while keeping the ABTC ticker.

- The company’s stated reason is to maintain compliance with Nasdaq’s requirement that the stock not trade below $1 for 30 consecutive sessions.

- Shares fell to an all-time low of 62 cents on Wednesday, down nearly 8.4% on the day, before a modest after-hours rebound.

- The move reflects a broader pattern among crypto-related public companies using reverse splits to address prolonged weakness in share prices.

Reverse split scheduled to protect Nasdaq listing

Reverse stock splits are often viewed by investors as a sign that a company is struggling to keep its stock above exchange listing thresholds. In American Bitcoin’s case, the company explicitly tied the action to Nasdaq’s minimum bid requirements, which can lead to delisting if a stock closes below $1 for 30 consecutive trading days.

American Bitcoin said it is implementing the consolidation to support its share price and maintain compliance with those rules. The company also confirmed that it would continue trading under the ABTC ticker through the process.

Shares hit a record low as crypto equities remain under pressure

Wednesday’s trading brought another sharp decline for ABTC. Shares fell nearly 8.4% to close at an all-time low of 62 cents. After the close, the stock reportedly edged higher by about 4.5% to 65 cents in after-hours trading.

The stock’s broader performance has been weak. American Bitcoin is down more than 63% year-to-date and has fallen more than 92% since it began trading on Nasdaq on Sept. 3, when the company launched through a merger process involving a publicly listed crypto mining entity.

American Bitcoin was founded earlier this year by Donald Trump Jr. and Eric Trump, according to the company’s background described in the reporting. The business merged with Nasdaq-listed Gryphon Digital Mining to go public, with the Trump brothers and crypto miner Hut 8 together holding roughly 98% of the combined company.

Financial results and market turbulence weigh on the stock

American Bitcoin’s share weakness is unfolding amid a wider downturn affecting parts of the crypto market and the equities that trade as proxies for it. In May, the company reported that it lost $81.7 million in the first quarter, with the figure cited in earlier coverage from Cointelegraph.

Reverse splits can help companies avoid immediate delisting pressures, but they do not address underlying business fundamentals. For traders, that means investors may still be exposed to the same operational risks—especially in a sector where revenue can be influenced by factors such as mining economics, digital asset prices, and cost structures.

Bitcoin itself was trading around $60,000 in early Thursday trading, down 32% so far this year and more than halved from its October peak of above $126,000, according to CoinGecko.

Broader trend: crypto firms use reverse splits to stay listed

American Bitcoin is not alone in turning to reverse stock splits to manage listing compliance. Another example cited in the reporting is Bitcoin treasury company Nakamoto, which completed a 1-for-40 reverse stock split in May after its shares reached a low of 16 cents in April, also in an effort to remain on Nasdaq.

The pattern is notable because it highlights a recurring tension for crypto-linked equities: when digital assets or mining sentiment deteriorate, smaller-cap listed firms can quickly slip below exchange price floors. Reverse splits can temporarily alter the math of share price—though they leave investors’ proportional exposure unchanged in most cases—while companies work to stabilize operations or regain market confidence.

For ABTC holders, the immediate practical impact is timing. With the split scheduled to take effect after Thursday’s close and begin reflecting on Monday’s open, investors will want to watch how the market recalibrates around the new share count and whether trading volume or liquidity dynamics change after the adjustment.

Going forward, the key unknown is whether the company can sustain its share price long enough to satisfy Nasdaq’s ongoing $1 minimum-bid condition. The next few trading weeks will be the real test: the exchange compliance clock runs on consecutive closing prices, so investors should track ABTC’s daily closes after the effective date to see whether the reverse split achieves its intended listing protection.

dYdX Labs launched Arcus on Wednesday, a decentralized exchange that combines tokenized stock trading with perpetual futures. Founder Antonio Juliano announced the launch on X, built jointly with Robinhood Crypto. Arcus runs on Robinhood Chain, the EVM-compatible layer 2 that Robinhood opened to… Read the full story at The Defiant

LINE NEXT has opened developer pre-registration for Unifi Pay ahead of a planned global launch in the third quarter, with the payment infrastructure set to support USDT, JPYC and IDRP through its Unifi stablecoin wallet.

Summary

- LINE NEXT has opened developer pre-registration for Unifi Pay ahead of its planned global launch in the third quarter.

- Unifi Pay will support USDT, JPYC and IDRP, with users in Japan and Indonesia able to top up local stablecoins directly from bank accounts after identity verification.

- The service offers zero payment fees, an average settlement of about one second, and an SDK that lets developers create payment pages in about 10 minutes.

According to a CoinPost report, LINE NEXT, the U.S.-based affiliate of LINE Yahoo, announced on June 30 that Unifi Pay will be launched globally after a beta phase that handled 100 billion Korean won in cumulative payments and settlements over the past year.

The company, which has access to LINE Yahoo’s 300 million users, is building the service on its Unifi stablecoin wallet and has started accepting pre-registrations from global developers before the official rollout.

Unifi Pay will support Tether’s USDT, the Japanese yen-denominated JPYC and the Indonesian rupiah-denominated IDRP at launch. In Japan and Indonesia, users will be able to complete online identity verification and directly top up JPYC or IDRP from their bank accounts. LINE NEXT also said it plans to add local stablecoins in more countries, depending on what each market’s regulations allow.

Unifi Pay offers wallet-based settlement with zero payment fees

Using a wallet-based structure, Unifi Pay directly connects users and suppliers and removes payment fees from the transaction process, according to the announcement. LINE NEXT said the service offers an average settlement speed of about one second.

The company will also provide a function that allows settlement funds to be sent directly to bank accounts through connected crypto exchanges and blockchain remittance solutions. This gives suppliers and developers a path to move stablecoin payments into bank accounts after receiving funds through the wallet.

For developers, AI builders, and creators, LINE NEXT is introducing the Unifi Pay SDK to simplify the process of adding global payments. The company said the SDK uses an A2A, or Agent-to-Agent, task execution method for AI agents, allowing a payment page to be created in about 10 minutes through a single command input.

Developer companies that keep payment proceeds in the wallet may receive annual rewards of up to 5%, depending on the type of stablecoin used. LINE NEXT said the reward model is tied to stablecoin holdings inside the wallet.

The beta version of Unifi Pay recorded 100 billion Korean won in cumulative payment and settlement volume over the past year, equal to about 10 billion Japanese yen based on the announcement’s conversion rate of 1 won to 0.1 yen. LINE NEXT CEO Youngsu Ko said the company plans to establish Unifi Pay as a payment infrastructure that connects developers, creators, and users around the world through its developer tools.

The planned launch also follows LINE NEXT and Kaia’s earlier stablecoin work through Project Unify, which was announced during Korea Blockchain Week in September 2025. Kaia described Project Unify as a stablecoin super-app designed to bring payments, yield, on/off-ramps and access to more than 100 decentralized apps into LINE Messenger, which the company said had nearly 200 million monthly active users across Japan, Taiwan, Thailand and Indonesia.

Kaia said at the time that Project Unify would support USD, JPY, KRW, THB, IDR, PHP, MYR and SGD at launch, while offering developers and issuers a Unify SDK with a focus on regulatory compliance, especially in South Korea. The project followed the 2024 merger of LINE’s Finschia and Kakao’s Klaytn into Kaia, which has described itself as Asia’s stablecoin orchestration layer.

Diplomatic discussions between the United States and Iran gained fresh momentum after new comments from President Donald Trump. The latest developments supported gains across several financial markets while crude oil prices moved lower. Meanwhile, traders assessed the possibility of a longer negotiation period as discussions continued in Qatar.

US-Iran Negotiations Advance as Diplomatic Efforts Continue

The United States and Iran continued negotiations in Qatar with support from regional mediators. The latest round followed earlier diplomatic contacts aimed at reducing tensions between both countries. As a result, market participants responded quickly to signs of continued engagement.

President Donald Trump described recent diplomatic progress as positive during remarks on Wednesday. He also indicated that efforts surrounding Iran’s nuclear program continued moving in the intended direction. However, he stopped short of confirming that both sides had reached a final agreement.

US representatives Jared Kushner and Steve Witkoff remained involved in the talks held in Doha. Qatar and Pakistan continued supporting communication between both governments throughout the negotiations. Their involvement reflected ongoing regional efforts to maintain dialogue and reduce geopolitical risks.

Oil Declines While Gold and Crypto See Stronger Demand

Financial markets reacted soon after reports highlighted progress in the diplomatic discussions. West Texas Intermediate crude oil dropped more than two percent during the trading session. Consequently, the benchmark price slipped below the important $70 level.

Lower oil prices reflected expectations that supply disruptions could become less likely. Earlier tensions had increased concerns about energy exports across the Middle East region. Therefore, easing diplomatic risks encouraged selling pressure across crude oil markets.

Gold also attracted fresh demand during the same trading period. Market data indicated that the precious metal added more than $74 billion in value within one day. At the same time, digital assets recorded gains, with several major altcoins outperforming Bitcoin.

Earlier reports had linked geopolitical uncertainty with increased volatility across digital asset markets. Market analysts had already warned that diplomatic developments could influence short-term price movements. The latest positive headlines supported stronger buying activity across several cryptocurrency sectors.

Ceasefire Extension Expectations Increase as Talks Continue

Prediction platform Polymarket showed rising expectations for an extension of the current negotiation period. The platform estimated a 62% probability that discussions would continue beyond the existing 60-day framework. That reading reflected improving confidence that both sides would maintain diplomatic engagement.

Despite stronger expectations, negotiations still face several important stages before reaching a formal agreement. Diplomatic discussions often require additional meetings before both governments finalize key commitments. Therefore, current progress does not guarantee a lasting resolution.

The latest developments followed previous diplomatic activity involving Iran and Oman. Both countries had established a joint committee to discuss the Strait of Hormuz and broader ceasefire matters. Those earlier efforts created additional channels for communication before the current Doha meetings.

The Strait of Hormuz remains one of the world’s most important energy shipping routes. Any improvement in regional stability can influence global oil prices and broader financial markets. Consequently, diplomatic developments continue affecting commodity and digital asset trading activity.

Current negotiations have strengthened expectations that dialogue may continue beyond the initial timeline. However, any setback during future meetings could quickly change market sentiment across several asset classes. The coming diplomatic sessions may determine whether recent gains receive additional support or reverse in the near term.

Silicon Valley elite drop record cash to build Florida’s tech capital

Tradeweb Completes Real-Time Tokenized US Treasury Trade on Canton

MLB Roundup: Orioles avoid sweep with win over White Sox

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics6 days ago

Politics6 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World2 days ago

Crypto World2 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics6 days ago

Politics6 days agoPotential 2028er World Cup attendee leaderboard

-

Business6 days ago

Business6 days agoAsia stock markets slide as tech shares slump

-

News Videos3 days ago

News Videos3 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech6 days ago

Tech6 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World4 days ago

Crypto World4 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business2 days ago