Crypto World

Drift Protocol Rebrands to Velocity DEX Ahead of Relaunch

Solana perpetuals exchange Drift Protocol has rebranded to Velocity DEX, the protocol's official X account announced on Wednesday. Solana's own account confirmed the switch shortly after, posting "FYI: @driftprotocol is now @VelocityDEX." Velocity DEX said the new name reflects "a cleaner… Read the full story at The Defiant

Meta Q2 earnings beat Wall Street on revenue but missed on profit, as AI infrastructure spending, legal charges, and severance costs pushed the operating margin down to 31% from 43%.

Shares fell 5.06% to $556 in after-hours trading on Wednesday, according to Benzinga, as investors weighed a higher capital spending outlook against shrinking free cash flow.

Meta Q2 Earnings Beat Hides a Margin Squeeze

Revenue reached $60.80 billion, up 28% year over year and ahead of the roughly $59.50 billion analysts expected. Diluted earnings landed at $6.18 per share, down 13% from $7.14.

Costs told the other half of the story. Total expenses jumped 55% to $42.03 billion, including $2.40 billion in legal charges and $1.18 billion in severance tied to a May headcount reduction.

Operating income fell 8% to $18.78 billion. Ad demand stayed healthy, with impressions up 14% and average price per ad up 12%, yet neither was enough to hold the margin.

User growth also held up. Family daily active people averaged 3.60 billion in June, a 3% rise from a year earlier.

Filings across the sector had already flagged AI capex draining cash before this week’s reports.

Capex Guidance Climbs Toward $145 Billion

Meta raised the floor of its 2026 capital expenditure range to $130 billion from $125 billion and kept the ceiling at $145 billion. Full-year expense guidance now starts at $165 billion.

The quarter shows why. Capital expenditures hit $31.08 billion, and operating cash flow of $31.86 billion left only $784 million in free cash flow, against $8.55 billion a year ago.

Most of that money is going into data centers. Meta and BlackRock unveiled a $14 billion data center venture in El Paso, Texas, this week.

The tax outlook tightened as well. Meta now expects a rate of 15% to 17% for the rest of 2026, up from a prior 13% to 16%.

“AI is accelerating our core business today, powering our next generation of products, and opening the door to entirely new enterprise opportunities,” read an excerpt in the release, citing Mark Zuckerberg, Meta founder and chief executive.

Follow us on X to get the latest news as it happens

Will the Stock Surge From Here?

META stock dropped by over 7% after market after market to $543.54 after closing Wednesday at $585.61.

The bull case rests on guidance. Meta expects third-quarter revenue of $61 billion to $64 billion and still projects full-year operating income above the 2025 result.

The bear case rests on the balance sheet. Long-term debt grew to $83.66 billion from $58.74 billion in December, and Reality Labs lost another $4.62 billion.

Legal risk sits on top of that. Meta flagged youth-related trials in the United States this year that may ultimately produce a material loss.

Sentiment across the sector is split. Microsoft’s Azure growth beat landed the same evening, a sign that investors will still fund AI spending when revenue follows it.

Crypto traders track these reports because the AI trade sets risk appetite. A Big Tech selloff hit crypto in June, and Bitcoin (BTC) traded near $63,409 on Thursday, down 0.7% over 24 hours.

Apple reports Thursday. Its spending commentary should show whether Meta’s margin squeeze is company specific or the price every large cloud operator now pays.

The post Meta Revenue Beats, But AI Spending Crushes Profit Margins: Will the Stock Surge? appeared first on BeInCrypto.

Robinhood reported $100 million in second quarter cryptocurrency transaction revenue, topping the $86.6 million analyst consensus even as the line fell 38% from a year earlier.

The beat landed inside a record quarter. Total net revenues rose 32% to $1.31 billion, while diluted earnings per share climbed 48% to $0.62.

Robinhood Crypto Revenue Cleared a Bar That Had Already Dropped

Expectations were modest going into Wednesday’s release. Crypto revenue had already fallen 47% in the first quarter to $134 million.

The second quarter figure slipped another 25% from that level. Trading activity accounts for most of the decline.

Robinhood App crypto notional volumes fell 35% year over year to $18 billion. Bitstamp contributed $22 billion, taking the combined total to $40 billion.

The wider market has not recovered. Bitcoin trading near $63,559 sits roughly 46% below its level a year ago.

Robinhood opened a crypto stock earnings week that also brings Coinbase and Strategy results on Thursday.

Prediction Markets Carried the Record Print

Transaction based revenues rose 44% to $776 million. Event contracts delivered $156 million, more than 10 times the year ago figure.

Options revenue climbed 29% to $342 million. Equities revenue nearly doubled to $129 million.

Crypto now supplies under 8% of total net revenues. Two years ago it was one of the company’s headline growth stories.

The customer base kept widening behind those numbers. Funded customers reached 28.4 million and Robinhood Gold subscribers hit a record 4.8 million.

“The business is firing on all cylinders. We delivered record revenues and drove new highs across equity, option, and event contract volumes, as we continue to win market share,” Shiv Verma, Chief Financial Officer of Robinhood, in the earnings release.

Follow us on X to get the latest news as it happens

HOOD Slipped Even as the Numbers Beat

Robinhood shares closed Wednesday at $89.84, down 3.15% on the day. The stock eased further to $87.00 in after hours trading.

Earnings quality may explain some of the hesitation. The $0.62 diluted EPS included $0.14 of gains tied to the deconsolidation of Robinhood Ventures Fund I.

Management is still funding crypto regardless. The quarter brought the public mainnet launch of Robinhood Chain, an Ethereum Layer 2 built for tokenized real world assets.

That network has already climbed the fee tables, with Robinhood Chain application fees reaching $25 million in a single week this month.

Robinhood also debuted Robinhood Earn, its first onchain lending product, rolled out stock tokens across more than 120 countries, and closed the WonderFi acquisition in Canada.

Perpetual futures went live in the European Union during the quarter. The company flagged plans for a crypto offering in the United Kingdom.

The company lowered its 2026 adjusted operating expense and share based compensation outlook to a range of $2.675 billion to $2.775 billion.

Whether the crypto line stabilizes may matter less to the share price than whether event contract volumes keep compounding at this pace.

The post Robinhood Crypto Revenue Tops Estimates Despite 38% Drop, How Will Stock React? appeared first on BeInCrypto.

Crypto markets are moving into what ARK Invest analyst Lorenzo Valente describes as the industry’s “biggest consolidation phase yet,” driven by investor selectivity and a shift in where application revenues flow. In an X post on Wednesday, Valente argued that only a small set of protocols and platforms with clear product-market fit are capturing a growing share of demand—while weaker projects face closures or forced restructuring.

Valente pointed to concentration in crypto application revenue as a key signal. He cited Hyperliquid and Pump.fun as together accounting for about 67% of total crypto application revenue, and said that adding Ethena brings the top three’s combined share to nearly 80%, describing this as record-high concentration.

Key takeaways

- Revenue concentration is rising: Valente estimates Hyperliquid and Pump.fun make up ~67% of crypto application revenue, with the top three nearing ~80% when Ethena is included.

- Capital is getting more selective: Valente says it’s increasingly harder for exchanges and projects without strong product-market fit to attract funding.

- Industry shakeout is likely to intensify: He expects more mergers and acquisitions, shutdowns, and restructuring, including Chapter 11 filings.

- Exchange closures are already reinforcing the theme: Recent operational wind-down plans from multiple venues align with consolidation pressures.

Why investors are picking winners

Valente’s core argument is that investor behavior is changing alongside market maturity. As capital becomes more discerning, projects that fail to demonstrate sustained usage or a defensible niche are finding it increasingly difficult to secure financing or maintain growth. In his view, this accelerates attrition: weaker products either shut down or get absorbed, leaving a smaller set of dominant protocols behind.

While consolidation is not a new pattern in crypto, Valente framed the current period as unusually pronounced—especially when measured by application revenue share. By emphasizing top platforms’ increasing dominance, he suggested that the sector is not merely pruning inefficient competitors, but also concentrating economic returns into fewer hands.

Revenue concentration and the “record-high” claim

To make the case, Valente highlighted specific platforms and their estimated contribution to crypto application revenue. According to his post, Hyperliquid and Pump.fun account for roughly 67% of total crypto application revenue. When Ethena is added, the top three approach nearly 80% combined.

The practical implication for users and builders is straightforward: if revenue is increasingly concentrated, liquidity, incentives, partnerships, and developer attention may also cluster around the same dominant venues and protocols. That can create a reinforcing cycle—success brings more of the ecosystem’s resources—making it harder for new entrants to gain traction.

Valente also described the consolidation he expects ahead as “extremely bullish” for crypto, implying that a cleaner market structure could improve resilience and investor confidence, even if the transition is disruptive for teams that don’t survive the competitive narrowing.

Source: Lorenzo Valente

Exchange wind-downs add pressure from the infrastructure layer

Valente’s consolidation thesis comes as several exchanges have recently announced plans to wind down operations or end services, underscoring the broader challenge of sustaining activity in an increasingly competitive environment.

Last week, BitMEX said it would shut down its exchange in September following a strategic review by owner HDR Global Trading. The exchange cited insufficient trading interest and noted that it had accelerated delisting of trading pairs and derivative contracts ahead of the closure. Earlier coverage details the shutdown decision and the delisting rationale: BitMEX shut down its exchange.

Days later, BitMart announced it would end trading services on Aug. 26 and then wind down completely in January 2027. The exchange attributed the decision to an evaluation of operating conditions, the market environment, and its future strategic direction. This plan is described in earlier reporting: BitMart wind-down timeline.

Together, these announcements illustrate consolidation occurring not only through market share at the application level, but also at the venue level—where competitive pressures can force even established names to reduce offerings or exit entirely.

Mergers and acquisitions show consolidation can be strategic

Alongside closures, acquisitions are also contributing to industry consolidation. Valente’s expectations for more mergers and acquisitions are consistent with how some players are expanding rather than withdrawing.

Earlier this month, Bybit launched a locally operated exchange in Indonesia after acquiring a majority stake in digital asset firm NOBI. The move expands Bybit’s footprint in one of Asia’s largest crypto markets, illustrating a different pathway for consolidation: larger operators absorbing or partnering with local entities to gain access and scale.

Related coverage: Bybit launches in Indonesia after NOBI acquisition

What to watch next

As consolidation pressures build, the next signal to monitor is whether revenue concentration keeps widening toward a small set of dominant applications while more exchanges restructure or exit. Valente expects that pattern to accelerate—so investors, traders, and builders should pay close attention to which platforms keep attracting usage as the industry prunes weaker competitors.

Crypto World

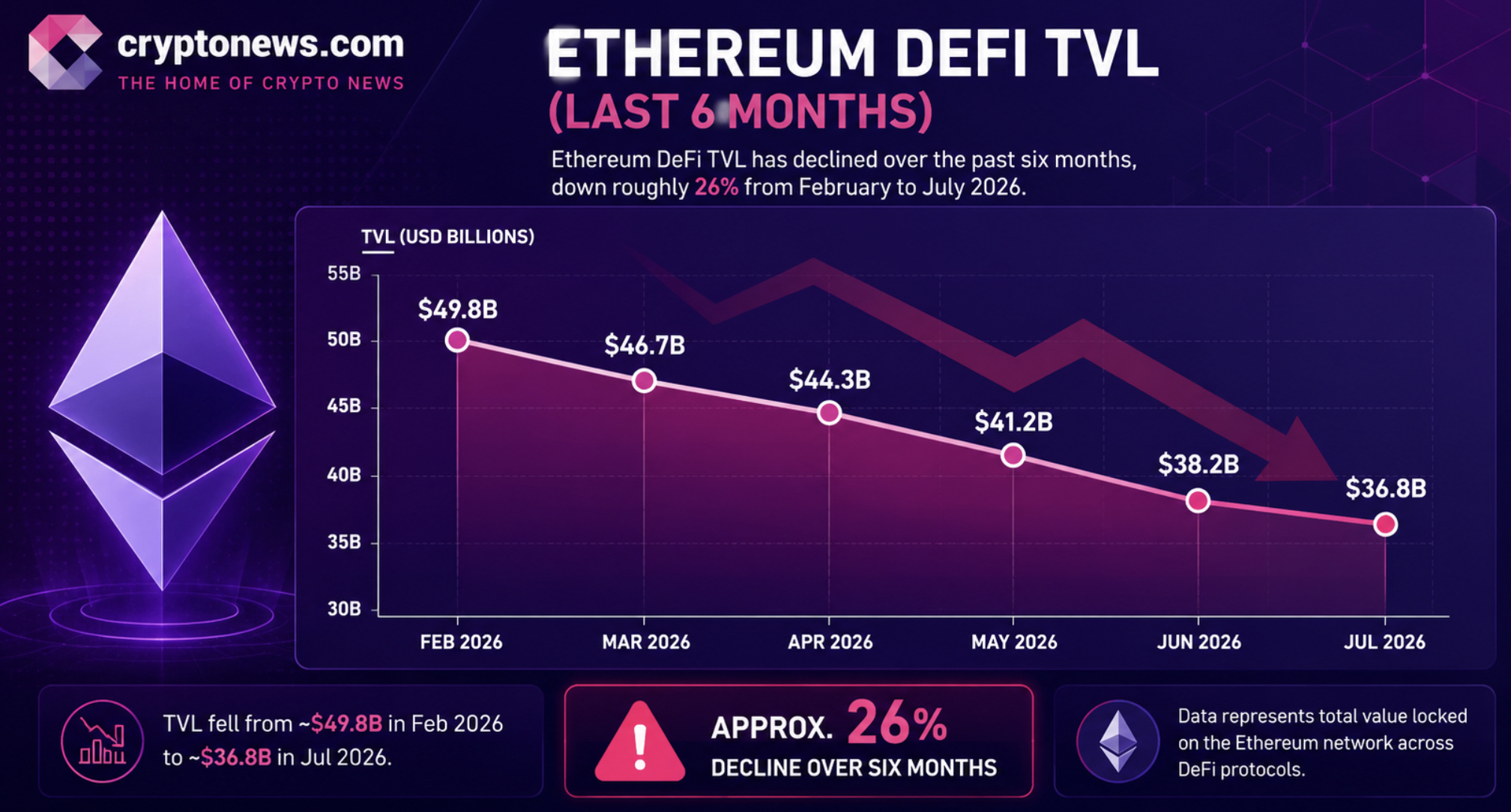

Ethereum Price Prediction: L2 Ecosystems Lose Their TVL as Robinhood Chain Activity Drops

Ethereum is trading at $1,920, but while price action remains relatively calm, the underlying picture looks more complicated for its prediction. Total value locked across Ethereum Layer 2 networks has slipped to roughly $5 billion, wiping out much of the 2024 expansion and returning to levels last seen in 2023. If L2s were meant to drive Ethereum’s next growth phase, that slowdown raises fresh questions.

The Robinhood Chain story captures that tension. The Arbitrum-based Layer 2 bridged roughly $141 million in ETH during its first two weeks. It also briefly overtook Ethereum L1 and Base in 24-hour DEX volume, reaching about $877.6 million. However, the network returned only around $4,000 in fees to Ethereum during its first week, fueling debate over how much value L2s actually sends back.

Some analysts argue Robinhood Chain’s $4.5 billion in DEX volume during its first week reflects activity shifting away from Ethereum’s base layer. Meanwhile, Optimism, Base, and Arbitrum still account for about $4.8 billion, or 96%, of the remaining Layer 2 TVL. Even so, the steady decline in total TVL remains difficult to ignore.

Meanwhile, the Ethereum Foundation has lost several senior leaders this year. At the same time, institutions including DTCC and JPMorgan continue expanding tokenization efforts across multiple blockchains instead of focusing only on Ethereum. ETH also remains range-bound, while derivatives positioning has cooled, suggesting traders still lack conviction for a decisive breakout.

Discover: The Best Crypto to Diversify Your Portfolio

Ethereum Price Prediction: Reclaim $2,050 Resistance This Week?

At $1,920, ETH is trading slightly above the $1,850 to $1,900 short term demand zone that many analysts identified as key support. The latest session ranged between $1,880 and $1,930, highlighting continued price compression. Meanwhile, derivatives positioning remains subdued, reflecting limited conviction from both bulls and bears.

The first resistance zone sits around $2,036 to $2,050. A decisive move above that could expose the 0.236 Fibonacci level near $2,134. Beyond that, $2,377 and $2,572 remain the next technical milestones. On the downside, $1,780 remains the key support, while $1,742 is the next major level if sellers regain control.

The bullish case remains straightforward. Holding above $1,900, improving derivatives sentiment, and stronger institutional activity on Layer 2 networks could support a move toward $2,050 and eventually $2,134. However, buyers still need fresh momentum before that scenario gains traction.

The base case still favors consolidation between $1,850 and $2,050. Layer 2 TVL remains a headwind, while no clear catalyst has emerged to break the current range. A daily close below $1,780 would weaken the short-term outlook and shift attention toward $1,742.

Robinhood’s prediction markets add another perspective. Only 22% of participants expect ETH to finish above $3,500 this year, while 54% anticipate a move below $1,500 at some point. That split highlights genuine uncertainty rather than one-sided bearish sentiment. Macro conditions also remain capable of reshaping the technical picture with little warning.

Trade Ethereum on Bybit and Get a Chance to Win Our $1,000 USDT Airdrop

LiquidChain Targets Early Mover Upside as Ethereum Tests Key Levels

ETH hovering below key resistance while L2 value leakage accelerates is exactly the environment where infrastructure capturing cross-chain activity, rather than betting on a single chain’s dominance, becomes a more interesting allocation question. The L2-versus-L1 value capture debate is real, and it does not resolve neatly in Ethereum’s favor in the short term. That dynamic is worth watching for rotation setups.

LiquidChain is positioning directly against the fragmentation problem at the root of this debate. The project is a Layer 3 infrastructure play, and its core proposition is fusing Bitcoin, Ethereum, and Solana liquidity into a single execution environment through what it calls a Unified Liquidity Layer.

The view is different from the third layer. — LiquidChain (@getliquidchain) July 27, 2026

You’ll understand soon. pic.twitter.com/P2WOELSTjI

With Liquid, developers only deploy once and access all three ecosystems; settlement is verifiable; execution is single-step. The presale is currently priced at $0.01484, with $920K raised to date.

Features like Deploy-Once Architecture address the exact developer fragmentation that the Robinhood Chain / Arbitrum / Base proliferation keeps making worse. Ethereum’s own infrastructure consolidation trends underscore why cross-chain abstraction has a credible thesis here.

Research LiquidChain further here.

Discover: The Best Token Presales

The post Ethereum Price Prediction: L2 Ecosystems Lose Their TVL as Robinhood Chain Activity Drops appeared first on Cryptonews.

Law enforcement groups backed by key Democrats have suggested some changes to the CLARITY Act that would make it easier to prosecute some crypto software developers.

However, White House officials still feel like the suggestions made fall short of what they want.

Trump’s Crypto Adviser Rejects Proposal

Trump’s crypto adviser, Patrick Witt, dismissed the proposal, saying claims that they were the result of “productive negotiations” with the White House and Treasury were far from the truth. He added that the administration had made its position clear to Sen. Catherine Cortez Masto for weeks and that the latest revision was “not even close” to meeting its expectations.

A report from Politico shows that two major groups representing U.S. prosecutors have submitted fresh changes to the White House, aiming to break months of deadlock over the CLARITY Act.

“Newest language is the culmination of productive negotiations with law enforcement, the White House, and Treasury, and we feel good about the chance to resolve this issue once and for all,” said Masto in a statement.

The proposal focuses on the Blockchain Regulatory Certainty Act (BRCA), with the new language removing provisions that could protect developers from criminal prosecution in some cases. At the heart of the dispute is whether law enforcement should hold crypto developers responsible for crimes committed on the platforms they build.

The Trump administration says that the authorities should protect builders who do not hold customer funds to encourage innovation. On the other side, critics and law enforcement groups disagree, warning that the current language could make it easier for financial crimes to go unchecked.

New York Attorney General Letitia James also shares the sentiment, having recently said that the CLARITY Act could weaken state enforcement against crypto fraud. According to her, this is because the legislation would limit the state’s ability to hold digital asset firms accountable for crimes.

Police Groups and Security Officials Rally Behind Clarity Act

Not everyone seems to be against the latest revision, though. The Fraternal Order of Police, the largest police organization in the U.S., recently dropped its objections and backed the crypto bill after previously raising concerns about the BRCA.

The report also says several other groups have backed the legislation, including the National Organization of Black Law Enforcement Executives and the Federal Law Enforcement Officers Association.

Last month, over 160 former national security, intelligence, and other officials also wrote a letter to the Senate in support of the bill, arguing that it would strengthen efforts to combat illicit finance in the crypto space.

The post Trump’s Crypto Adviser Rejects CLARITY Act Developer Proposal appeared first on CryptoPotato.

U.S. Federal Reserve Chairman Kevin Warsh holds a press conference following a two-day meeting of the Federal Open Market Committee (FOMC), as the Federal Reserve holds interest rates steady, at the Federal Reserve, in Washington, D.C., U.S. July 29, 2026.

Evelyn Hockstein | Reuters

The Federal Reserve on Wednesday followed through on expectations for no interest rate change, and Chairman Kevin Warsh offered little direction in his news conference. The meeting was notable for a surge in dissenting votes, while Warsh looked to provide some clarity on the board’s thought process.

Here are the five biggest takeaways from this week’s Fed actions:

- The “family fight” returns: Three voters on the Federal Open Market Committee voted against the hold, favoring instead a quarter percentage point hike. “I asked for a good family fight, and I got one. That’s the purpose. That’s the design feature,” Warsh said. “There was a lot more interaction between and among my colleagues. It was a real family fight.” All the “no” votes came from regional presidents: Lorie Logan of Dallas, Neil Kashkari of Minneapolis and Beth Hammack of Cleveland, none terribly surprising given previous statements they made.

- Another short and sweet statement: Other than detailing the “no” votes the statement was unchanged and still dramatically shorter than the Fed norm. “As before, the policy statement conveys just the facts. It’s steering clear of forecasting, a choice we consider especially prudent at these uncertain times,” Warsh said. “Uncertainty, however, does not mean a lack of clarity.”

- Dedication to slaying inflation, but …: Warsh again stated the Fed’s resolve to keep inflation under control, but braced markets and the public that it won’t be an easy fight nor will it end soon. “We’ve got no magic wand,” he said. “This isn’t something that we’re going to be able to carry out in days or weeks.”

- Revolt in the market: Despite the chairman’s tough talk on inflation, markets weren’t having it. Treasury yields at the long end of the curve soared, even as the policy-sensitive 2-year dipped. Translation: We think you’re going to keep short-term policy rates in check, and it’s going to create a ton of inflation later. The 30-year bond was the biggest gainer, roaring higher by 11.5 basis points to 5.211%, its highest yield since 2007 and seemingly undercutting Warsh’s inflation warrior credentials.

- No clues on September: Investors looking to get any further hints on whether the Fed will hike at the Sept. 15-16 FOMC meeting were largely out of luck. The statement offered no clues, either on forward guidance or even on the reaction function, and Warsh was at best cryptic on which way he will push. “So I take seriously that the pullback of forward guidance requires some transition. Reform isn’t easy, but our general judgment is going to help us make better decisions, and in so doing, satisfy our remit,” Warsh said.

They said it

“No doubt, in some of your commentaries today, you’ll talk about a divided Federal Reserve. Well, that’s not the feeling I felt the last couple of days and the couple days before. What I felt was a group of professionals, all the different perspectives, different views, different judgments, but eager to roll up their sleeves and have a family fight, and eager to reform the way in which the Fed does policy.” — Warsh, commenting on the tenor of the two meetings he’s chaired so far.

“We have long argued that September not July is when Warsh faces a binding credibility test/trap. If inflation and/or the war and energy run relatively hot over the summer he will have to hike in order to preserve his credibility. The key difference is that September is in a broad sense data-dependent while July was Warsh preferences dependent.” — Krishna Guha, head of global policy and central bank strategy at Evercore ISI.

“[T]he Warsh Fed seems to be turning a blind eye to the message the bond market’s higher yields are sending about the inflation risks. Stay tuned. The reform-oriented Federal Reserve under Chair Warsh is looking like a bust. The bond market wants answers, but is getting nothing in return.” — Chris Rupkey, chief economist at Fwdbonds.

DoubleLine Capital CEO Jeffrey Gundlach said the Treasury market is signaling that the Federal Reserve will need to do more than talk tough if policymakers are serious about reaching their 2% inflation target.

“If you really want to get to 2%, I think you have to raise interest rates,” Gundlach said on CNBC’s “Closing Bell” Wednesday after the Fed’s latest policy decision. “I think getting 2% is going to take a long time. We might not get there over the course of the next couple of years.”

The Fed left its benchmark interest rate unchanged at a range of 3.5% to 3.75%, a decision that was widely expected. The move was not approved unanimously, however, with three policy members dissenting in favor of raising rates by a quarter percentage point.

Gundlach said the divergent moves across the Treasury curve following the announcement showed investors’ skepticism that the Fed will ultimately follow through.

“The two-year Treasury rallied today because it thinks the Fed is taking its time,” he said. “And the long bond yield went up significantly after the press conference, because the bond market vigilantes are saying, ‘If you really want us to believe your rhetoric, you’ve got to start acting.’”

The benchmark 10-year Treasury yield rose more than 7 basis points to 4.681%, while the 30-year bond yield surged to 5.213% for its highest level since 2007. Meanwhile, the policy-sensitive two-year Treasury yield fell 3 basis points to 4.244%.

The long end is generally tied to expectations for inflation and deficits, while the short end is closely related to interest-rate expectations in the shorter run.

Fed Chairman Kevin Warsh stressed that the Fed will take necessary steps to meet its 2% inflation goal.

“I understand the desire for rolling forecasts and commentary from this committee, but for our part, we need to observe market reaction to developments direct and unfiltered,” Warsh said. “I want to stress, of course, that decisions by this committee matter a great deal, and where necessary and appropriate, we will not hesitate to act.”

A federal judge has rejected the CFTC’s request to stop Wisconsin from enforcing state gambling laws against federally regulated prediction market platforms.

Summary

- Judge William Griesbach denied the CFTC’s request for a preliminary injunction against Wisconsin.

- The court found sports event contracts may fall within Wisconsin’s commercial gambling laws.

- Wisconsin is pursuing cases against Kalshi, Polymarket, Crypto.com, Robinhood, and Coinbase.

- The CFTC plans to appeal the ruling and continue defending its claimed jurisdiction.

Wisconsin court rejects CFTC injunction

Judge William Griesbach of the U.S. District Court for the Eastern District of Wisconsin denied the Commodity Futures Trading Commission’s attempt to block Wisconsin from applying its gambling laws to prediction market operators.

The CFTC filed the federal case in April after Wisconsin sued Kalshi, Polymarket, Crypto.com, Robinhood, and Coinbase. Wisconsin alleges that sports event contracts offered through these platforms amount to unlicensed sports betting.

Griesbach found that the CFTC had not shown that it was likely to succeed on the merits, face irreparable harm, or benefit from the balance of equities required for a preliminary injunction.

The court also rejected requests from Kalshi and Crypto.com to intervene and seek preliminary relief in the federal dispute.

The CFTC argued that sports event contracts qualify as swaps under the Commodity Exchange Act and therefore fall under its exclusive federal authority. However, Griesbach concluded that the agency had not shown that sports contracts meet the law’s definition of swaps.

That finding alone was enough to deny the injunction, according to the court’s reasoning.

State gambling laws may cover sports contracts

Griesbach also rejected the CFTC’s argument that the Commodity Exchange Act prevents Wisconsin from applying its gambling statutes to CFTC-regulated platforms.

“Wisconsin’s gambling statutes do not conflict with federal commodities regulations and are not preempted by them,” the judge wrote.

The decision suggests that federal registration does not automatically shield a platform from state gambling enforcement when its contracts are tied to sporting outcomes.

Wisconsin Attorney General Josh Kaul has described these contracts as sports bets presented as financial products.

“Thinly disguising unlawful conduct doesn’t make it lawful,” Kaul said when the state announced its lawsuits in April. “These companies’ alleged facilitation of sports betting in Wisconsin should be shut down.”

Legal analyst Daniel Wallach said the five state cases are likely to return to Wisconsin courts because the federal statute does not completely preempt state law. State judges could then consider injunctions preventing the platforms from offering sports contracts in Wisconsin.

CFTC faces pressure from 44 states

The ruling adds to a wider challenge to the CFTC’s attempt to establish national control over prediction markets.

Attorneys general from 44 states have urged the regulator to withdraw and rewrite proposed amendments to Rule 40.11. Their letter argues that the framework exceeds the CFTC’s authority under the Commodity Exchange Act and intrudes into gambling oversight traditionally handled by states.

Ohio Attorney General Andy Wilson led the coalition, which submitted its objections as the public comment period closed. The states argued that Congress had not clearly authorized the CFTC to assume control over sports betting markets.

“States have long regulated gambling—including sports bets. The federal government has not,” the letter stated, according to the filing covered by crypto.news.

The dispute matters for US users because platform access may increasingly depend on where they live. If state laws apply alongside federal commodities rules, Kalshi, Polymarket, and similar operators could face different licensing requirements or restrictions across the country.

Conflicting rulings leave prediction markets uncertain

Wisconsin’s decision contrasts with a ruling issued in Minnesota earlier this week.

U.S. District Judge Katherine Menendez temporarily blocked Minnesota’s new prediction market ban after finding that the CFTC, Kalshi, and Polymarket were likely to succeed in their federal preemption challenge. The injunction allows the platforms to continue operating in Minnesota while the case proceeds, according to the Associated Press.

The different outcomes leave the industry without a consistent national standard. Courts in Wisconsin and New York have favored state authority, while Minnesota’s ruling supports the CFTC’s claim that some event contracts fall under exclusive federal oversight.

A CFTC spokesperson said the agency was disappointed with the Wisconsin decision and would appeal. The next stage could determine whether Wisconsin’s lawsuits proceed in state court and whether the affected platforms must stop offering sports contracts there.

Dogecoin is trading near $0.07, up 0.3% over the past day after another quiet session. However, the muted move hides a weaker weekly trend. Billy Markus just reminded the market why people embraced DOGE in the first place. The full context offers another look at Dogecoin’s real-world utility.

Markus, posting as Shibetoshi Nakamoto on X, replied to a prompt from crypto retirement platform iTrustCapital about the most crypto thing he had done. He answered, “I bought a ride in the Vegas Loop with Dogecoin.” He added it was not that weekend, but it remained his favorite crypto experience. The comment referenced The Boring Company’s 2022 decision to accept DOGE through BitPay.

At launch, a single ride cost about $1.50, while a day pass cost $2.50. Elon Musk also backed the payment option, saying he would support Dogecoin wherever possible. Markus, still pointing to that purchase years later, says more about DOGE’s everyday appeal than many marketing campaigns.

Meanwhile, the post arrived during another difficult stretch for crypto markets. The Senate delayed further consideration of the Clarity Act before the August recess. At the same time, roughly $604 million in crypto positions were liquidated during a sharp market selloff. That combination kept pressure on risk assets, including Dogecoin.

Discover: The Best Crypto to Diversify Your Portfolio

Can Dogecoin Price Break Back Above $0.10 Before the Clarity Act Deadline?

At $0.07064, DOGE is holding just above the $0.07 floor, but only by a slim margin. The session low reached about $0.0693, showing sellers are still pressing that support. A decisive break below $0.07 could expose the $0.064 to $0.068 range, where buyers previously stepped in.

Futures open interest has eased alongside the recent price decline, suggesting leveraged longs continue leaving the market. That points to more than a simple spot weakness. Still, price has not confirmed a breakdown, leaving the current support level in focus for the next move.

The previous reference to $0.40 VWAP support is no longer relevant at current prices. Instead, analysts are watching whether DOGE can reclaim $0.08 before discussing a stronger recovery. Until then, the market remains well below major resistance, and momentum still favors caution.

If the Clarity Act advances before the August recess, sentiment could improve. Fresh catalysts from Elon Musk or renewed payment integrations may also help. In that case, a move back above $0.08 could reopen the path toward $0.10.

The base case remains a consolidation between $0.07 and $0.08 as traders weigh regulation and macro risks. However, a daily close below $0.07 with rising volume would strengthen the bearish outlook. Until DOGE creates a clear distance from that level, the utility story remains stronger than the chart.

Trade Dogecoin on Bybit and Get a Chance to Win Our $1,000 USDT Airdrop

Maxi Doge Targets Early Mover Upside as DOGE Tests Key Levels

DOGE at $0.07 with a multi-billion-dollar market cap means the math on a 10x from here requires a full bull cycle and sustained retail inflows. Traders rotating capital for higher-asymmetry exposure are looking earlier in the lifecycle, which is exactly where Maxi Doge ($MAXI) sits.

The Clarity Act delay and broader risk-off pressure are squeezing established meme coins hardest; early-stage presales carry their own risks but aren’t subject to the same open-interest unwind dynamics.

$MAXI is a meme token built on Ethereum (ERC-20) positioned around a 240-lb canine mascot embodying 1000x leverage trading culture, think gym-bro meets trading desk, which lands well with the retail demographic that drives meme coin volume.

The presale has raised $4.8 million at a current price of $0.0002831, with dynamic staking APY live for holders. Features include holder-only trading competitions with leaderboard rewards and a Maxi Fund treasury earmarked for liquidity and partnerships. DYOR applies harder here than on listed assets.

Discover: The Best Token Presales

The post Dogecoin Co-Founder Billy Markus Revives Viral Vegas Loop Payment Memory appeared first on Cryptonews.

Microsoft delivered another blockbuster quarter, beating Wall Street expectations on revenue, earnings, and operating income as Azure cloud services and artificial intelligence continued to drive growth.

The stronger-than-expected results reinforced investor confidence that massive AI infrastructure investments are translating into accelerating revenue, a closely watched trend across technology and crypto markets alike.

Microsoft Crushes Q4 as Azure Growth Fuels AI Boom

The software giant reported fiscal fourth-quarter revenue of $90.0 billion, surpassing analysts’ expectations of $87.7 billion. Adjusted earnings per share came in at $4.74, well above the consensus estimate of $4.25, while operating income reached $40.6 billion, also topping forecasts.

Azure Emerges as the Standout Performer

The biggest surprise came from Microsoft’s Intelligent Cloud business.

Revenue from the segment climbed 32% year over year to $39.3 billion, while Azure and other cloud services revenue surged 43%, comfortably ahead of prior company guidance that had pointed to growth closer to the high-30% range.

Microsoft Cloud generated $59.3 billion in quarterly revenue, up 27% from a year earlier. Meanwhile, commercial remaining performance obligations—a key measure of future contracted revenue—jumped 84% to $678 billion, highlighting sustained enterprise demand.

CEO Satya Nadella credited Microsoft’s AI strategy for the performance.

“We are advancing the frontier on the cost-to-outcome curve, ensuring every customer can turn tokens into business results,” Nadella said.

He also revealed that Azure generated more than $100 billion in annual revenue for the first time during fiscal 2026, while Microsoft 365 Copilot surpassed 30 million paid seats, demonstrating growing enterprise adoption of generative AI.

AI Spending Continues to Accelerate

Microsoft’s earnings also showed that its aggressive AI investments remain substantial.

Operating cash flow reached $55.4 billion during the quarter, while capital expenditures continued climbing as the company expanded data center capacity to support AI workloads.

Property and equipment spending reached nearly $35.8 billion during the quarter and almost $116 billion for the full fiscal year, underscoring Microsoft’s commitment to building AI infrastructure despite investor scrutiny over rising costs.

The company also returned $10.2 billion to shareholders through dividends and share repurchases during the quarter.

Why Crypto Investors Are Watching

Although Microsoft’s earnings are not directly tied to digital assets, the results carry important implications for crypto markets.

Bitcoin miners, AI-related blockchain projects, decentralized infrastructure networks, and tokenized computing platforms all benefit from continued enterprise investment in cloud infrastructure and artificial intelligence.

Strong demand for AI services also reinforces the broader investment narrative that has fueled capital flows into technology stocks and AI-linked crypto assets throughout 2026.

Microsoft’s results arrive as investors increasingly evaluate whether enormous AI infrastructure spending is generating sustainable returns. This quarter’s performance suggests demand continues to outpace supply, easing concerns that cloud providers may be overbuilding capacity.

What’s Next?

Attention now turns to Microsoft’s earnings conference call, where executives are expected to provide guidance on Azure growth, capital expenditures, operating margins, and fiscal 2027 expectations.

For investors across both traditional finance and crypto markets, Microsoft’s latest results offer another indication that enterprise AI adoption continues accelerating. Whether that momentum remains strong through the remainder of the year could influence sentiment across technology stocks, AI infrastructure providers, and digital asset sectors closely tied to the expanding artificial intelligence ecosystem.

The post Microsoft Crushes Q4 as Azure Growth Fuels AI Boom, How Should Traders Position? appeared first on BeInCrypto.

LIV on verge of canceling Team Championship amid funding concerns

Why The Slate Truck Made A Last Minute Change To Its Battery Tech

CFA !! | Is it worth it ??? | #cfa Reality?? | #1cr #finance #cfaexam #salary #money #interview

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Brooks Brothers

-

Sports3 days ago

Sports3 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Tech3 days ago

Tech3 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Crypto World7 days ago

Crypto World7 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

Politics2 days ago

Politics2 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Crypto World4 days ago

Crypto World4 days agoRipple bought a bank in pieces. The $4 billion audit

-

Entertainment5 days ago

Entertainment5 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

News Videos3 days ago

News Videos3 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Politics2 days ago

Politics2 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Sports6 days ago

Sports6 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Fashion6 days ago

Fashion6 days ago16 Dresses for the High Summer Event

-

News Videos6 days ago

News Videos6 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Business17 hours ago

Business17 hours agoMajor shareholder moves on Canyon

-

Crypto World4 days ago

Crypto World4 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Politics3 days ago

Politics3 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

Business2 hours ago

Business2 hours agoWhy Trees Belong on the Risk Register

-

Crypto World6 days ago

Crypto World6 days agoUniswap (UNI) pushes deeper into tokenized RWAs with permissioned trading pools

-

Entertainment1 day ago

Entertainment1 day ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Crypto World7 days ago

SEC Agrees to Overhaul Recordkeeping After Settling Coinbase Lawsuit Over Gensler’s Lost Texts

-

Tech5 days ago

Tech5 days agoAnthropic launches Claude Opus 5, a cheaper AI model for coding, agents and enterprise workflows

You must be logged in to post a comment Login