Business

Night Watch Investment Management Q2 2026 Investor Letter

Jacob Wackerhausen/iStock via Getty Images

Performance

During the second quarter of 2026, Night Watch Investment Management LP appreciated by 12.80% net of fees.

Last quarter, we mentioned that our shareholding in Marex (MRX) had grown to be an outsized position in our portfolio, at 14.5%. This paid off this quarter, with the stock up 37% in the quarter and 230% since we bought our first shares around the IPO two years ago. The company is benefitting from high market volatility, while simultaneously showing great execution on their M&A playbook, most notably by continuing to grow their prime brokerage business. At 10x 2026 P/E and >30% ROE, this remains a compelling long.

Performance this quarter was further aided by strong performance of names such as Watches of Switzerland Group (WOSG LN) and Silicon Motion (SIMO). We owned two noticeable detractors: FUTU (FUTU) and Sanuwave (SNWV). We have been adding aggressively to FUTU while we are waiting for improving data points before risking more capital on SNWV.

Portfolio

Night Watch manages a global value strategy that differentiates on the following points:

Catalyst – We predominantly buy value companies with an identifiable catalyst for a rerating. Catalysts can include industry tailwinds or company-specific events (e.g., earnings inflection, CEO changes, refinancing).

Inside Ownership – We aim to find companies where management has considerable ownership in the company. We consider this alignment of interest to be an important determinant of share price performance.

Unique Names – To differentiate from a long list of other value strategies, we seek unique portfolio holdings that have little overlap with a typical wealth management portfolio. We aim to provide our LPs with diversification from their other investments in addition to strong performance.

The portfolio as of June 30th, 2026, is as follows:

Largest positions:

- Marex (13.7%)

- AAR Corp (7.3%)

- Remitly (6.2%)

- Distribution Solutions Group (5.8%)

- Universal Technical Institute (5.8%)

- Adyen (5.6%)

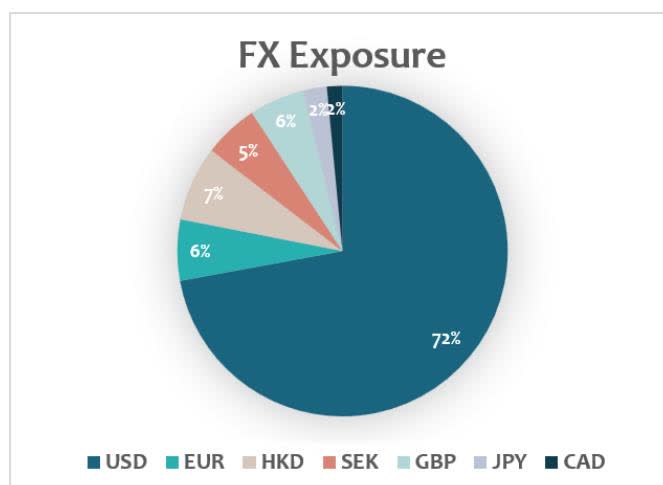

FX Exposure

Pie chart showing FX Exposure by currency: USD (72%), EUR (6%), HKD (7%), SEK (5%), GBP (6%), JPY (2%), CAD (2%).

Market Update

The first half of the year has been unusually volatile, and the market has been even more bifurcated than usual. On the one hand, you have got businesses that touch AI, whose stocks keep going up daily to what we believe to be unsustainable levels. We are not complaining. We were early on Western Digital Corp (WDC) and we still own Silicon Motion (SIMO). Both benefitted from the shortage in memory caused by strong demand from AI data centers. But we are not blind to the cyclical nature of those businesses, and we have been early in taking some chips off the table.

On the other hand, you have got everything that is not AI. If your business is a quality compounder with a decade-long history of providing your shareholders with 10-15% earnings growth, your stock got sold off because why would anyone care about 15% per year if you can earn that in a day by holding AI stocks!?

Naturally, we are buyers of such businesses. If we can find low-risk ways to lock in 15% earnings growth, and if we might even get some multiple expansion on top when markets normalize, we are happy to move up on the quality spectrum. We added quality names including Stryker (SYK), Adyen (ADYEN NA)(ADYYF) and Booking.com (BKNG).

Finally, there were the companies that, rightly or wrongly, were viewed as AI losers. We were reminded once again that valuation in today’s market does not provide a floor to stock prices. Especially software and payment related companies saw their shares freefall during the first half of 2026.

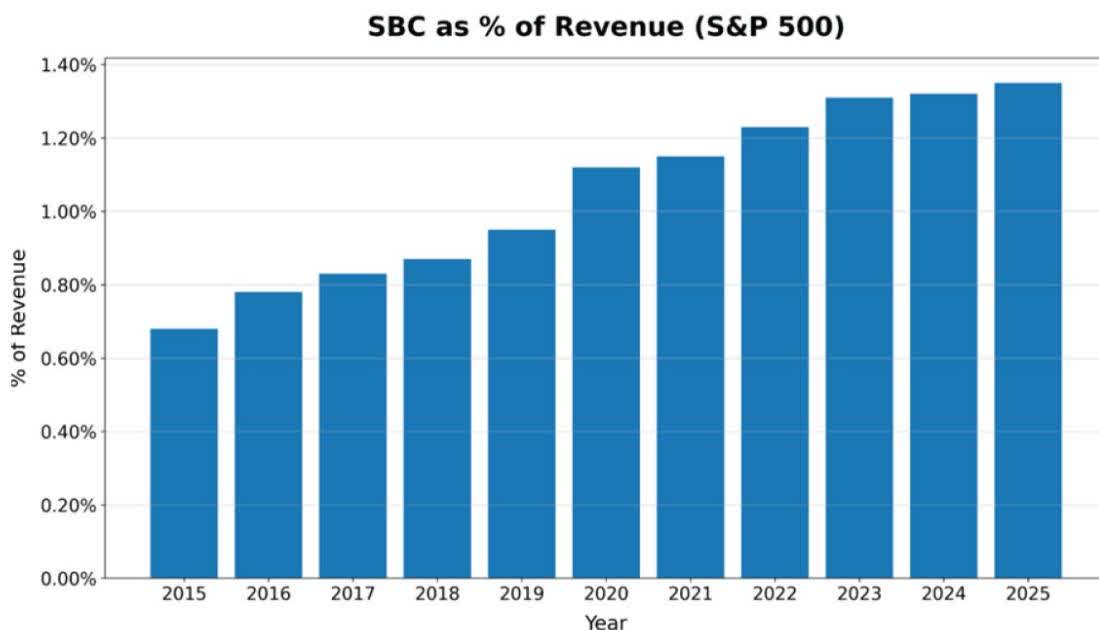

We have a differentiated view on this sell-off. Over the last few years, we have seen an increasing reliance of companies on Stock-Based Compensation (SBC). Growing a business requires capital. Wall Street’s greatest trick was to convince the markets that this growth could be funded without running the costs through the P&L. If you simply paid employees through stock options or stock grants, they argued, it’s not a real expense, and analysts ought to exclude it from their model.

For some reason, Wall Street obliged. SBC took on excessive levels as companies were keen to exploit this newly found loophole.

Source: KEDM.com – Companies taking Wall Street for a ride by excluding from earnings all salaries paid out in options and stock grants.

It isn’t hard to see the reflexive nature of this setup. Paying in SBC and excluding those costs is all fun and games when share prices go up. But when share prices go down, the dilution caused by the SBC goes up. 3% dilution per year can quickly become 10% dilution. On top of that, your employees are seeing the value of their stock options dwindle and might be quick to start thinking about updating their resumes.

Now that the market has finally started caring about SBC, it seems wise to buy companies with real earnings.

Historically, Dutch companies have paid out little to no SBC. This is not by accident. Stock options or grants in The Netherlands are taxed excessively, making this not a viable option for companies. While that’s a shame for Dutch employees, it benefits shareholders of those companies.

Companies with international operations, who have a large portion of their employees in places like Amsterdam, have a comparative advantage. BKNG and ADYEN fit that bill. For the first time since inception, Night Watch is going Dutch. We added BKNG and ADYEN to the portfolio.

Position Highlights

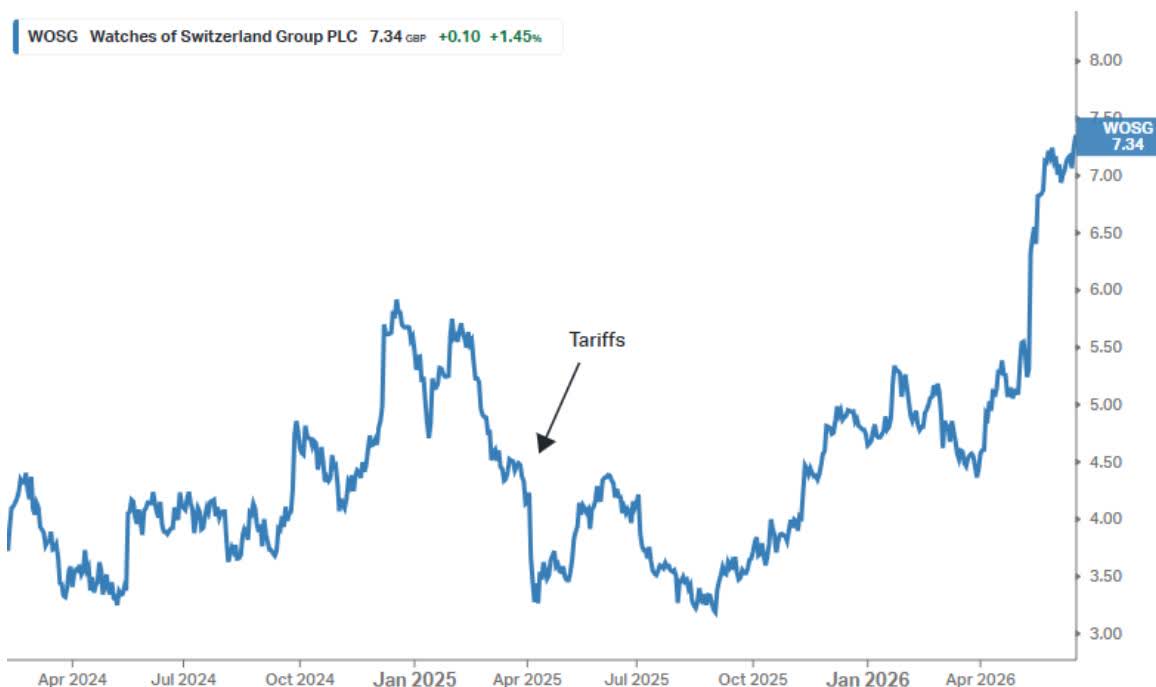

Watches of Switzerland Group (WOSG LN)(WOSGF) has been a core position since our inception in 2024. It has been a somewhat frustrating investment for the first two years, but more recently the stars have started to align.

WOSG is a retailer of luxury watches, most notably an authorized dealer of Rolex and Patek Philippe. This business is considerably higher quality than ordinary retailing because it is supply-constrained rather than demand-constrained. Prospective buyers often have to join waiting lists for popular models, and the number of watches a retailer sells is determined largely by the allocation it receives from Rolex rather than by end-market demand. Rolex, in turn, is owned by the Hans Wilsdorf Foundation, a non-profit organization that appears to be at least as interested in preserving its Swiss legacy as it is in maximizing profits.

The business model over the last few decades has been straightforward. Rolex consolidated the sale of its watches among a small group of trusted partners with the financial strength to invest millions in dedicated Rolex stores and the ability to provide a consistent customer experience across locations.

WOSG was the consolidator in the UK. In exchange for accepting slightly lower gross margins, it received larger allocations from Rolex. Higher volumes per store more than offset the lower margins.

Following its success in the UK, WOSG replicated the model in the United States, which today accounts for roughly 50% of revenue.

Luxury watch sales peaked in 2021, and demand for brands other than Rolex and Patek Philippe slowed. We initiated a position in early 2024 after the resulting decline in the share price.

Unfortunately, WOSG faced another setback when the United States imposed 39% tariffs on Swiss imports. We feared the economics of the business could deteriorate sharply. Rolex boutiques are difficult to repurpose, and passing through a 39% price increase, even in the luxury segment, seemed like a tall order.

We were patient. Switzerland was unlikely to be singled out as the root-cause of the US trade imbalance forever. And in a worst case, the tariffs would likely accelerate the consolidation in the industry, benefiting the strongest players.

With tariffs now finally in the rear-view mirror, WOSG is finally back to executing its proven playbook. US growth re-accelerated to 24%. The UK is steady at 5% growth. The balance sheet is underleveraged. Despite the strong move-up, shares are trading at 13x next year’s earnings. WOSG remains a conviction long.

Conclusion

The market has become a one-trick pony with many quality companies being sold off in favor of anything that touches the AI trade. We are happy to buy quality companies at depressed valuations. Meanwhile we are doing our own thing, allocating to sectors with structural tailwinds that are largely overlooked, including the aerospace aftermarket, futures commission merchants, and various payment companies.

By following this disciplined strategy, we have been compounding capital at well over 20% since inception while providing good diversification to anyone who is invested in the major indices. This has also resulted in very low volatility, and we have not seen any major drawdowns in our portfolio to date.

On behalf of the Night Watch team,

Roderick van Zuylen, Chief Investment Officer

Eileen Ke, Chief Operating Officer

Night Watch Investment Partners LP – Net Performance (in USD)

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Harbour Energy: Second Chance

OPINION: The government may discover that using a sledgehammer to crack a nut can have undesirable consequences.

Business

Spain Coach Luis de la Fuente Backs Lamine Yamal’s Bold ‘Unstoppable’ World Cup Claim Ahead of Austria Clash

INGLEWOOD, Calif. — Spain coach Luis de la Fuente said Wednesday he “loves” teenage star Lamine Yamal‘s declaration that the reigning European champions will be “almost unstoppable” once they hit their stride at the 2026 World Cup, backing his young winger’s bold proclamation ahead of Thursday’s round of 32 match against Austria at SoFi Stadium.

De la Fuente’s endorsement came after Yamal set tongues wagging with comments made in a radio interview earlier this week, in which the 17-year-old Barcelona winger suggested Spain had yet to show their true colors and predicted a dominant run once the team clicked.

“Once we hit our stride … we’ll be almost unstoppable,” Yamal said in the radio interview, adding that Spain are “the only national team expected to play really well” at the tournament.

The comments prompted questions about whether Yamal’s confidence bordered on arrogance, particularly given Spain’s uneven group stage showing. The team drew 0-0 with Cape Verde in their opener, a result that drew widespread criticism given Cape Verde’s status as one of the tournament’s rank outsiders. Spain subsequently beat Saudi Arabia 4-0 and edged Uruguay 1-0 to top Group B, but neither performance fully dispelled the sense that the side was operating well below the level that had made them European champions in 2024.

De la Fuente, speaking at his prematch news conference Wednesday at SoFi Stadium, was asked directly about Yamal’s bold claims and offered an enthusiastic defense of his youngest star’s mindset.

“I think he’s an optimistic player, confident about his possibilities and those of his teammates,” De la Fuente said. “We know what our potential is. We know how far we can go. His words, in their context, seem very positive to me. He transmits optimism, confidence, security, and I love that.”

Yamal himself has had an uneven tournament, in part due to a pre-tournament injury that curtailed his preparation and limited his early availability. He played only 19 minutes in the Cape Verde draw before contributing a goal in 45 minutes against Saudi Arabia. He was on the pitch for 76 minutes against Uruguay but found it harder to impact the game against tighter, more organized defensive opposition. De la Fuente addressed questions about whether Yamal will be capable of completing 90 minutes against Austria and struck an optimistic note.

“Lamine can now play whatever we ask of him,” De la Fuente said. “We’ve been, as always, very careful with all the players’ recovery. It isn’t the same playing a very demanding game, very intense and fast, where you might only be able to play half an hour, and other games that are more comfortable and you can play 70 minutes. Lamine is really good. You’ve seen how excited he is to play.”

Austria’s coach Ralf Rangnick offered an interesting counterpoint to Yamal’s confidence, acknowledging the teenager’s generational talent while framing his team’s approach in purely practical terms. Rangnick stopped well short of dismissing the claims, instead expressing something closer to admiration tempered by the pragmatic language of a coach who needs his players focused on nullifying a threat rather than being distracted by it.

“He is an excellent player, and he will be for the next 12, 13, 14 years or even longer if he stays healthy and keeps a good head on his shoulders,” Rangnick said. “If you look at Lionel Messi, you can see he could play a lot of matches. He’s one of the players we’ll watch very closely tomorrow. We’ll try not to give him space when he starts dribbling. He’s a player all fans love to watch, but it’s our task to make sure he has the ball as little as possible.”

De la Fuente also delivered an upbeat injury report on two wingers who picked up knocks during the Uruguay match. Yéremy Pino, who initially appeared to suffer a serious collarbone injury, has made a faster-than-expected recovery and returned to full training, with De la Fuente describing the turnaround as near miraculous given how serious the initial assessment appeared.

“Yeremy’s recovery has been miraculous,” De la Fuente said. “After the game it looked like a fracture and it wasn’t. With his character and his courage, he’s back training completely normally.”

Nico Williams, another key attacking player who sustained what was feared to be a significant injury late in the Uruguay match, has been ruled out of Thursday’s match but is expected to be available for the round of 16 if Spain advance.

“Nico got a big shock, he thought he had an important injury after the game, but it wasn’t like that,” De la Fuente said. “It’s moderate discomfort that prevents him from playing tomorrow, but we’re optimistic he’ll be there for the next game, if we go through.”

Víctor Muñoz, who has yet to feature at all during the tournament, is also back in full training according to De la Fuente, though the coach noted that a lack of recent competitive minutes makes his selection for Thursday’s match a more complex decision.

Spain are widely considered among the tournament’s top three or four favorites despite their uninspiring group stage performances, with the depth of their squad, their tactical flexibility under De la Fuente and the frightening individual quality of players like Yamal, Pedri, Williams and Álvaro Morata giving them a ceiling that most analysts still rate among the highest of any remaining team. The question throughout the group stage has been not whether Spain have that potential but when, and against whom, it will finally manifest in sustained, 90-minute dominance.

De la Fuente closed his news conference with a declaration of growing confidence that mirrored his young star’s own self-belief.

“As the days pass, I believe even more in this team,” De la Fuente said. “I’ve always believed in this team. For me they’re the best in the world. As the tournament evolves, there’s equality with the results we’re seeing. I’m still just as demanding, still just as realistic, but also more optimistic every day.”

Thursday’s round of 32 match kicks off at SoFi Stadium in Inglewood with a place in the round of 16 on the line for both sides.

Business

Wayne Rooney Warns England Are ‘In Big Trouble’ After Dismal Congo Win With Mexico Looming at the Azteca

ATLANTA — Wayne Rooney delivered a blunt and damaging assessment of England’s World Cup prospects Wednesday night, warning that Thomas Tuchel’s side faces a serious crisis of structure and cohesion that could bring their tournament to an abrupt end unless the coaching staff makes urgent changes before Sunday’s round of 16 clash against Mexico in Mexico City.

England’s narrow 2-1 victory over the Democratic Republic of Congo at Mercedes-Benz Stadium, secured only through two Harry Kane goals in the final 15 minutes of a match they were widely expected to win comfortably, prompted Rooney to pull no punches in his post-match analysis for the BBC.

“For me there are big concerns,” Rooney said. “We are all delighted England have gone through but in particular when England lose the ball they are so open. Against a better team I think we are in big trouble if we don’t sort that out.”

The former England captain and all-time leading scorer continued with a pointed breakdown of where specifically he sees the problems manifesting across the pitch.

“The connection isn’t great between the backline and midfield, the full-backs are struggling, Madueke struggled,” Rooney said. “There are just no connections and big gaps in the middle of the pitch and that is a big worry for me. He really needs to look at that otherwise we will go out.”

Those are not the words of a pundit looking for attention. Rooney earned 120 caps for England and has spent years analyzing the international game, and his concerns mirror those expressed by numerous technical observers who watched Wednesday’s performance with mounting anxiety. England were disorganized, unable to maintain defensive shape when out of possession and alarmingly open down the flanks for long stretches of a match against a side ranked considerably below them in the global standings.

Congo DR’s Brian Cipenga scored an early goal in the seventh minute that Rooney described as the product of poor decision-making at the heart of the England backline. He had been critical of center backs Marc Guehi and Ezri Konsa before his post-match comments, accusing both of “poor judgement” for allowing Cipenga to arrive completely unmarked at the back post and finish unopposed.

The right back position drew particular attention from Rooney, who singled out Djed Spence’s uncomfortable display as symptomatic of a structural vulnerability that could be exposed in a far more damaging way by Mexico, whose forward unit is in outstanding form. Spence was exposed multiple times by Congo’s attack and was eventually replaced by Eberechi Eze, with Declan Rice dropping into a makeshift right back role for a portion of the match, an arrangement that highlighted just how exposed England are at that position.

Rooney went as far as to advocate for an emergency recall of retired right back Kyle Walker, making the case that the cost of ignoring the problem is greater than the awkwardness of making an unconventional late tournament phone call.

“We’ve seen it before where players have come out of retirement,” Rooney said. “I think the minute Tino Livramento got injured, they should have been straight on the phone to Kyle Walker. Kyle’s still more than good enough and more than capable of playing in this England team. I would have been on the phone to him and saying, ‘Listen, we need you here so can you come out and help us,’ because that could really cost us. I’m worried on that.”

Walker has not featured for England since retiring from international football, but Rooney’s point reflects a view that seems to be gaining some traction among pundits and supporters who watched Wednesday’s performance and are already dreading how a more clinical attack than Congo’s would have punished the same defensive vulnerabilities. Whether Tuchel would seriously consider an out-of-retirement recall in the middle of a World Cup is another matter entirely.

Rooney’s concerns are rooted in what happened Wednesday and in what lies directly ahead. Mexico, England’s opponents on Sunday at the Estadio Azteca, are arguably the most difficult possible round of 16 opponent in the bracket at this stage of the tournament. Co-hosts who have played every match at home, Mexico have yet to concede a single goal across their four games, won all four of those matches and most recently dismantled Ecuador 2-0 in a first half performance that was as close to perfect as any team has produced in this tournament. Raúl Jiménez and Julián Quiñones are in exceptional form, the crowd at the Azteca is among the loudest and most intimidating in international football, and Mexico’s home record in World Cup play spans more than a decade without a loss.

The potential path beyond Mexico only intensifies the stakes. Should England navigate the Azteca, a quarterfinal meeting with Brazil, who beat Japan 2-1 in their round of 32 fixture, could await. And beyond that, a potential semifinal against defending champions Argentina, led by Lionel Messi in what may be the greatest individual scoring tournament of any player’s career, looms as the prize for getting that far.

None of those opponents would have allowed England the defensive lapses that Congo exploited repeatedly. Kane’s brilliance in the closing stages saved England on Wednesday, but relying on a single player’s individual class to rescue a structurally disorganized team in late minutes is not a sustainable model against opponents of the caliber England will face from the round of 16 onward.

Tuchel’s tactical adjustments Wednesday, including the substitutions that introduced Eze and Anthony Gordon in the 60th minute, changed the game’s momentum and ultimately produced the winning platform from which Kane finished. But the fundamental defensive connectivity problems Rooney identified were visible throughout, particularly in the first half when England struggled to organize themselves after going behind and passed the ball directly out of play on three separate occasions under minimal opposition pressure.

Whether Tuchel uses the days before Sunday’s match in Mexico City to address those structural concerns, and how England’s battered and injury-depleted defensive resources hold up against the pace and finishing quality of the Mexican attack, will go a long way toward determining whether Kane’s heroics on Wednesday extend further into the tournament or whether England’s World Cup ends against a side that simply doesn’t lose at home.

A dairy company had to pay almost $60,000 after the consumer watchdog issued notices for mislabelling its milk products, including one from Western Australia.

Astera Labs: A High-Risk, High-Reward Play On The AI Boom

Under the EES system, digital records linked to passports track when “third country” nationals – including British and American travellers – enter and leave the so-called Schengen free movement zone, which includes 29 European countries.

However, Airlines UK and Airlines for America said the EES rollout had been inconsistent.

They added “with peak summer travel approaching and the system not yet working as it should, airlines need the commission and member states to get serious about contingency measures and take a pragmatic look at whether the current timeline is realistic”.

Steve Heapy, chief executive of Jet2, said his airline found “the continued pursuit of a policy so baffling – in cases where it has clearly not been implemented in a robust manner”.

He said allowing EES checks to be paused where systems were not ready would “result in a much better experience for holidaymakers”.

Von Massenbach said there had been a “very high level meeting in Brussels” on Wednesday, “and we see now that they start to understand that this is a situation that is not bearable, not bearable over the summer”.

Airports lobby group, ACI Europe, have written to EC president Ursula Von Der Leyen, claiming wait times at border control had now reached up to five hours in peak traffic periods, and things could worsen as the busiest time of the year approached.

It warned “airlines face half-empty planes at gate closing time, while passengers are stuck in border control queues”.

Countries do have the ability to suspend EES checks under some circumstances.

However, ACI Europe argued states needed to be allowed to pro-actively suspend the system if high volumes of passengers are expected.

An EC spokesman said that “all efforts are being made to limit the impact [of EES] on travellers from outside the EU”.

He said the impact was “limited” in “most” EU airports and where there were issues, member states had not been able to provide sufficient numbers of border guards, appropriate infrastructure and automated equipment.

He said the EC continued to offer support with the new system, and was willing to do even more “in view of the coming summer period”.

Woodside Energy director Tony O’Neill has resigned after two years on the company’s board.

Business

Merck Shares Decline as Pharmaceutical Giant Faces Market Rotation and Pipeline Developments

NEW YORK — Merck & Co. Inc. shares fell more than 2 percent Tuesday, closing at $125.37 as investors rotated out of certain pharmaceutical names amid broader market shifts and company-specific considerations.

The 2.44 percent decline, or about $3.13 per share, reflected typical sector volatility as the pharmaceutical industry navigates patent cliffs, regulatory developments and pipeline investments. Merck, known for its oncology portfolio and vaccines, has maintained a strong position despite periodic pressures.

Keytruda, Merck’s flagship cancer treatment, continues driving significant revenue. The PD-1 inhibitor has achieved blockbuster status, with expanding approvals across multiple indications. However, eventual patent expiration remains a long-term focal point for investors.

The company’s recent performance has shown resilience in core areas. Oncology sales have provided stability, while vaccine franchises like Gardasil contribute to diversified revenue. Animal health operations through Merck Animal Health add further balance.

Tuesday’s trading occurred against a backdrop of sector rotation. Technology and growth stocks attracted capital, while some defensive healthcare names faced mild pressure. Merck’s movement aligned with peers experiencing similar dynamics.

Merck has pursued strategic acquisitions and licensing deals to bolster its pipeline. Recent transactions aim to complement existing strengths in oncology and expand into new therapeutic areas. Integration and development timelines influence investor sentiment.

Regulatory milestones remain critical. Approvals for new indications or formulations can drive upside, while clinical trial outcomes introduce variability. Merck’s research and development spending supports a robust pipeline addressing significant medical needs.

Analysts monitor Merck’s ability to offset potential revenue losses from maturing products. Diversification efforts and operational efficiency help mitigate risks associated with patent expirations.

The pharmaceutical sector faces ongoing policy debates around drug pricing and innovation incentives. Merck advocates for balanced approaches that support research while ensuring patient access.

Global operations expose Merck to currency fluctuations, supply chain dynamics and varying regulatory environments. Strong performance in key markets has helped offset challenges elsewhere.

Tuesday’s decline contributed to a mixed session for healthcare stocks. Broader indices showed varied performance as economic data and corporate earnings influenced sentiment.

Merck’s dividend remains attractive for income-focused investors. Consistent payouts reflect the company’s financial strength and commitment to shareholder returns.

Capital allocation priorities include research investment, strategic transactions and return of capital. Management balances growth initiatives with prudent financial management.

The company’s commitment to corporate responsibility encompasses access to medicines, environmental sustainability and diversity initiatives. These efforts align with stakeholder expectations in the healthcare industry.

Tuesday’s close at $125.37 left Merck shares in a range reflecting balanced views on near-term prospects. Valuation metrics incorporate growth projections and risk factors.

Longer-term, Merck’s pipeline and commercial execution will determine trajectory. Successful launches and label expansions could support revenue stability.

Industry analysts project continued demand for innovative therapies. Merck’s focus on oncology, vaccines and animal health aligns with global health priorities.

Competitive dynamics in pharmaceuticals require ongoing innovation. Merck invests significantly in research to maintain leadership positions.

Tuesday’s session highlighted typical market fluctuations. Merck’s fundamentals remain solid despite share price movement.

Investors will monitor upcoming earnings and clinical updates for additional insights. Guidance parameters often influence expectations in the sector.

Merck plays a vital role in addressing unmet medical needs. Its products impact millions of patients worldwide through treatments and preventive measures.

The company’s history of scientific advancement supports its reputation. Discoveries in multiple therapeutic areas have contributed to public health improvements.

As Merck navigates the evolving pharmaceutical landscape, focus remains on delivering value through innovation and execution. Tuesday’s trading reflected ongoing assessment by market participants.

Broader economic factors, including interest rates and healthcare policy, influence sector performance. Merck’s defensive characteristics provide some insulation from cyclical pressures.

The stock’s movement Tuesday contributed to sector narratives around rotation and valuation. Pharmaceutical companies with strong pipelines often command premiums.

Merck continues emphasizing patient-centric approaches and scientific rigor. These principles guide development and commercialization strategies.

Tuesday’s decline represents one session in a longer-term story. Merck’s trajectory depends on successful pipeline advancement and market conditions.

Investors maintain varied outlooks based on risk tolerance and time horizons. Dividend yield and growth potential appeal to different strategies.

The pharmaceutical industry remains essential to healthcare systems globally. Merck’s contributions through research and medicines support its strategic importance.

As markets assess opportunities, Merck stands as a established player with diversified operations and forward-looking investments.

Speaking to ET Now, Jain said the combination of stronger domestic fundamentals, improving external balances, and stable valuations has strengthened his outlook for Indian equities. While he remains optimistic about the broader market, he believes opportunities are emerging selectively across sectors, particularly in large-cap banking and information technology.

Macro environment turns supportive

Jain believes India has moved past the macro challenges that weighed on investor sentiment over the past few years. He pointed to a healthier balance of payments outlook, supportive measures taken by the Reserve Bank of India, and a shift in equity ownership from foreign investors to domestic institutional investors as key positives.”I am quite constructive on the markets. The macro challenges that India was facing are clearly behind us. The balance of payments in the current year should be materially positive because of both external factors and the steps the RBI has taken. Valuations are reasonable, and stocks have moved into very strong hands from foreigners to domestic institutional investors. Multiples are reasonable, so I am actually quite constructive on these markets,” he said.

IT sector presents value despite near-term challenges

The recent correction in IT stocks, particularly following weak guidance from some mid-tier companies, has created value, Jain said. While pricing pressures remain a concern, he does not expect Indian IT companies to witness a structural decline in business.

He believes the current pricing environment is cyclical and could improve as enterprises increase technology spending to adopt artificial intelligence.”There is value, in my opinion, and I do not think these businesses are going to melt away. Even in the current deflationary environment, toplines are not negative. They are holding on, maybe flattish or with very low growth. As enterprises adopt AI, they will need to spend more, and I do not think IT budgets are likely to degrow,” he said.

However, he cautioned that Indian IT stocks continue to face valuation pressure from cheaper global peers.

“The challenge is that similar businesses outside India are trading at 20-30% lower multiples. That will continue to pose a headwind for Indian IT stocks until there is some change in sentiment,” he said.

Potential triggers could revive IT sentiment

Despite the valuation gap with global peers, Jain believes several factors could unlock value in Indian IT stocks over time.

“When you are getting good value, it is very hard to forecast how that value will unlock itself. Maybe earnings turn out slightly better than expected, foreign selling stops, domestic investors continue to support these companies, or some companies announce buybacks. Any of these could become a trigger,” he said.

Avoids specific view on ER&D companies

Asked about engineering research and development companies, which have seen mixed commentary amid slowing European auto demand, Jain chose not to offer a stock-specific opinion.

“Let me not comment specifically on ER&D names. I do not think I would be able to do justice there,” he said.

Large private banks offer compelling value

Jain is particularly constructive on large private sector banks, arguing that the sector has been weighed down by prolonged foreign institutional selling despite improving fundamentals.

He noted that credit growth has strengthened, valuations have become attractive, and the unwinding of long-held foreign positions appears to be nearing completion.

“Over the last one or two years, value has clearly emerged in large private banks. Credit growth has inched up sharply, and as FCNR(B) dollars come in, it will be positive for banks. The sector has massively underperformed because foreigners have been reducing positions, but at current valuations I would be quite constructive,” he said.

Largecaps likely to outperform as foreign selling eases

While small and mid-cap stocks have staged a recovery from recent lows, Jain believes large-cap companies currently offer better value. He expects improving macro conditions and easing foreign selling to benefit the large-cap segment over time.

“As a category, largecaps are offering better value. They have borne the maximum brunt of foreign selling, and as macro conditions improve and foreign selling abates, largecaps should outperform smallcaps,” he said.

At the same time, he acknowledged that opportunities continue to exist in the broader market.

“After the correction in small and midcaps over the last two years, value is emerging on a stock-specific basis. It is going to be a stock picker’s market,” he said.

Strong economy could lift large-cap earnings

Jain dismissed concerns that earnings growth will remain confined to smaller companies, arguing that India’s underlying economy remains robust. He cited healthy demand conditions, strong credit growth, rising GST collections, and supportive nominal GDP trends as reasons why large-cap earnings could also accelerate.

“The underlying economy is doing extremely well. Credit growth, GST numbers and demand conditions point to a very robust economy. We could see some acceleration in earnings growth even in the large-cap space,” he said.

No clear view on real estate

While acknowledging that the real estate sector remains important, Jain said he does not track it closely enough to offer a meaningful opinion.

“It is a good space, but I do not track it very closely. So, let me not comment on that,” he said.

Consumer discretionary preferred over staples

Jain drew a clear distinction between consumer staples and consumer discretionary businesses, arguing that the former faces slower growth and increasing competitive pressures despite its strong business quality.

He believes discretionary consumption offers better long-term growth opportunities, although investors must remain disciplined on valuations.

“Consumer staples are highly penetrated and will continue to exhibit slow growth. They are also facing increasing competition from organised retail, D2C brands and private labels. The businesses are excellent, but valuations remain demanding relative to likely growth,” he said.

Instead, he prefers businesses linked to discretionary spending.

“I would be more inclined towards the consumer discretionary space than the consumer staples space,” he said.

He added that the discretionary universe is broad, covering automobiles, airlines, consumer durables, building materials, food delivery, cosmetics and apparel retail, making stock selection critical.

“It is a very diverse category. The attempt should be to have a realistic view of what growth is sustainable over the long term and what is already priced in. My preference would be to do more work in that space than in the staples space,” he said.

Outlook

Jain’s investment outlook remains firmly constructive. He believes improving macroeconomic conditions, healthier valuations and resilient domestic liquidity are creating an attractive backdrop for equities. While he sees selective opportunities across sectors, his preference currently lies with large-cap companies, private sector banks, and select consumer discretionary businesses, while viewing stock selection as the key driver of returns in the small- and mid-cap universe.

The remarkable moment DR Congo’s manager left stunned as press officer announces the death of his father in a press conference after England defeat

Harbour Energy: Second Chance

Bitcoin zooms above $61,000 as inflation fears soften

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics6 days ago

Politics6 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World2 days ago

Crypto World2 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics6 days ago

Politics6 days agoPotential 2028er World Cup attendee leaderboard

-

Business6 days ago

Business6 days agoAsia stock markets slide as tech shares slump

-

News Videos4 days ago

News Videos4 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech7 days ago

Tech7 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World7 days ago

Crypto World7 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World5 days ago

Crypto World5 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business2 days ago

Business2 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World5 days ago

Crypto World5 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports6 days ago

Sports6 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World6 days ago

Crypto World6 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech2 days ago

Tech2 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Tech4 days ago

Tech4 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech5 days ago

Tech5 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World6 days ago

Crypto World6 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World6 days ago

Crypto World6 days agoRTX holders must register wallets before token distribution begins

-

Sports22 hours ago

Sports22 hours agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Business3 days ago

Business3 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

You must be logged in to post a comment Login