Crypto World

Hyperliquid HIP-3 and HIP-4 Explained: Perps to Predictions

Two protocol upgrades turned Hyperliquid from a crypto perpetuals exchange into something closer to an operating system for markets. HIP-3 lets anyone with enough staked HYPE launch a perpetuals exchange for stocks, oil, or gold. HIP-4 adds prediction markets that settle without a token vote. Here is how both work, what they have built so far, and where the risks sit.

Hyperliquid spent its first two years being described as the fastest decentralized perpetuals exchange in crypto. The description was accurate and incomplete. Since late 2025, the network has been executing a more ambitious plan: turning its core trading infrastructure into a platform that other builders deploy markets on top of, the way developers deploy apps on cloud infrastructure. Grayscale Research made the comparison explicit in a June 2026 note, writing that Hyperliquid now looks less like a stock exchange and more like Amazon Web Services.

Two upgrades carry that transformation. HIP-3, live on mainnet since October 13, 2025, opened perpetual futures listing to outside builders and brought tokenized stocks, commodities, and indices onto the platform at scale. HIP-4, live since May 2, 2026, added a second market primitive built for prediction markets and other event contracts. Together they explain why seven of the top ten markets by volume on a crypto exchange are now things like Nvidia stock and gold, and why the platform is picking a direct fight with Polymarket and Kalshi.

This guide walks through what each proposal does, how the mechanics work, what has happened since launch, and what can still go wrong.

First, the basics: what a HIP is

Hyperliquid is a layer 1 blockchain built around a fully on-chain central limit order book. Its core engine, HyperCore, processes around 200,000 orders per second and handles matching, margining, and liquidations for every market on the chain. A separate component, the HyperEVM, runs Ethereum-style smart contracts on the same consensus layer. The native token, HYPE, secures the network through staking, pays fees, and absorbs most protocol revenue through a continuous buyback program. Cumulative protocol revenue passed $1 billion in late June 2026, with an annualized run rate near $840 million.

Changes to the protocol arrive through Hyperliquid Improvement Proposals, or HIPs, which the community debates and HYPE stakers weigh in on before the core contributors ship the code. The first two set the pattern. HIP-1 created the standard for launching spot tokens, with ticker slots sold through recurring Dutch auctions, so listing a token became a market process instead of an application form. HIP-2 added a protocol-native liquidity mechanism that seeds order books for new tokens automatically, solving the empty-book problem that kills most new listings on other venues. Both dealt with spot markets, and both introduced ideas that return later: auctions as the allocation mechanism for scarce listing slots, and protocol-level guarantees standing behind builder-created markets. The third and fourth proposals took those ideas after the two bigger prizes: perpetual futures on everything, and event contracts on anything.

HIP-3: builder-deployed perpetuals

Before HIP-3, listing a new perpetual market on Hyperliquid worked the way it works on most exchanges: the core team decided. That created a bottleneck and a gatekeeper, two things the platform’s own community had complained about as the asset universe stayed narrow while demand for stock and commodity exposure grew.

HIP-3, called Builder-Deployed Perpetuals, removed the gatekeeper. Since October 2025, any builder who stakes 500,000 HYPE can deploy an independent perpetuals exchange on HyperCore, without core team approval. At current prices near $64, that stake represents roughly $32 million, a number that matters for reasons covered below.

The deployer controls nearly everything about their market. They choose the assets, the oracle that sets the mark price, the collateral token, margin requirements, leverage limits, funding parameters, and the front-end experience. The first three assets in any HIP-3 exchange deploy without an auction. Additional assets go through a Dutch auction shared across all HIP-3 deployers, similar to the HIP-1 ticker auctions.

What the deployer does not control is the plumbing. HIP-3 markets inherit the full HyperCore stack: the same matching engine, the same order types, the same margining and liquidation logic, and the same solvency guarantees as the validator-operated markets. A trader interacting with a builder-deployed market gets the same execution quality as on the flagship crypto perps.

The economic design has three pillars:

- The stake is a bond, not just a ticket. The 500,000 HYPE can be slashed if the deployer misbehaves, for example by manipulating an oracle or breaking market rules, and the requirement holds for 30 days even after a deployer halts all markets.

- Fees split down the middle. HIP-3 markets charge users twice the fee of validator-operated perps, and the deployer keeps 50%. The protocol collects the same revenue per trade either way, so builder markets grow the pie without cannibalizing it.

- Cross margin has eligibility standards. Validators only allow cross margin on HIP-3 assets with sufficient observable liquidity, a reliable external oracle, and resistance to price manipulation, and any 50% intraday move in the reference price triggers a review.

The design goal is alignment: builders with $32 million at stake and a 50% revenue share have every reason to run clean, liquid, well-oracled markets, and a slashing mechanism waits for the ones who do not.

What HIP-3 actually built

The proposal would be a footnote if nobody used it. The opposite happened. The first market, a synthetic Nasdaq-style index called XYZ100, went live within days of activation. Its deployer, TradeXYZ, then built out United States equities including Nvidia, Tesla, Google, and Amazon, plus gold and silver contracts benchmarked to COMEX front-month futures, and later secured official licensing rights to the S&P 500 ticker, a landmark moment for a DeFi protocol.

The numbers followed. Open interest across HIP-3 markets passed $1.43 billion within months of launch. By spring 2026, seven of Hyperliquid’s top ten markets by volume were tokenized equities or commodities, not crypto pairs. During the West Asia crisis earlier this year, when traditional commodity venues closed for the weekend, traders moved to Hyperliquid to trade oil, gold, and silver around the clock, and HIP-3 markets drove up to 40% of the platform’s total volume. Non-crypto assets showed 60% trader retention in late March, a signal that around-the-clock access to traditional markets is a durable product, not a novelty. At peak HIP-3 activity the platform generated $2.3 million in daily fees, funding $11 million in HYPE buybacks.

Other deployers took different angles. Kinetiq built around its liquid staking token. Liminal used HIP-3 markets to run fully on-chain delta-neutral yield strategies across equities, FX, and commodities, including markets collateralized with yield-bearing assets like Ethena’s USDe. In June, Hyperliquid and TradeXYZ launched the FOMO app, a single interface for trading equities, pre-IPO stocks, crypto, indices, and commodities. Access also spread through consumer wallets: HIP-3 markets can be traded through any Hyperliquid-compatible front end, including Phantom.

The listing economics also flipped in a way worth pausing on. Under the old model, and on centralized exchanges generally, a new asset waits for an exchange’s business development calendar, and projects have long complained about the cost and opacity of the process. Under HIP-3, listing latency collapsed from a governance or negotiation timeline to a deployment transaction plus an auction, and the gatekeeping moved from relationships to capital. A pre-launch project that wants a perpetual market for hedging no longer needs a major venue’s blessing; it needs a deployer willing to run the market. Comparable systems show how unusual this is: dYdX v4 still routes every new market through a governance vote with a week or two of latency, and GMX listings run through its core team. Hyperliquid is the first chain-level implementation where market creation itself carries no approval step.

The concentration is the caveat. TradeXYZ accounts for more than 90% of all HIP-3 open interest, and Blockworks Research has flagged the deployer economics as a structural risk: with a roughly $30 million lockup, auction costs, and stiff competition, a smaller deployer’s break-even period can stretch to four years. Blockworks has proposed lowering the stake for small builders and letting them keep 100% of revenue until they recover their costs. Hyperliquid’s own documentation says the 500,000 HYPE threshold is expected to fall as the infrastructure matures. Until it does, HIP-3 is permissionless in principle and an oligopoly in practice.

HIP-4: outcome markets

HIP-3 covered continuous markets, things with a price that moves all day. It could not cleanly handle discrete events. A perpetual future needs an oracle that updates continuously with limits of roughly 1% deviation per update, a design suited to leveraged trading on a live price and incompatible with questions that jump from uncertainty to a hard answer in one instant, like an election call or an inflation print.

HIP-4, announced on February 2, 2026 and live on mainnet since May 2, added a purpose-built primitive for exactly that. Outcome markets are fully collateralized contracts that settle to exactly 0 or 1 at expiry. Each market has two sides, typically Yes and No, and the order books for the two sides are merged: an order to buy Yes at a price of 0.62 is the same order as one to sell No at 0.38, so all liquidity concentrates in one book. Positions are collateralized in USDH, the network’s native stablecoin, and because every position is fully backed, there is no liquidation risk.

The market lifecycle has a distinctive opening. Each new outcome market starts with a single-price clearing auction lasting around 15 minutes, during which traders submit limit orders but nothing executes. The auction clears at the price that matches the most volume, and unfilled orders roll into continuous trading on the standard order book. The mechanism exists to concentrate early liquidity and produce a fair opening price instead of a thin, gappy first print. It borrows a page from how traditional exchanges open trading each morning, which is fitting for a protocol that keeps hiring ideas from the market structure it wants to replace.

The architecture runs natively inside HyperCore, sharing the matching engine, order types, and throughput of every other market on the chain. That matters for one under-discussed reason: liquidity providers can quote prediction markets with the same tooling and speed they use on perps, instead of the bespoke market-making setups that thinner prediction venues require. Deep books were always the missing ingredient on long-tail event markets, and Hyperliquid’s bet is that professional liquidity follows familiar infrastructure.

The fee structure is openly aggressive. Opening or minting an outcome position costs nothing. Fees apply only on closing, burning, or settling, and makers pay zero. That pricing targets Polymarket and Kalshi, which processed a combined $44.8 billion in June on the back of the World Cup, and the community reaction at announcement made the intent plain. When the proposal dropped in February, crypto.news covered the market pricing in exactly that ambition, with traders framing HIP-4 as Hyperliquid trying to house all of finance.

Initial markets are curated and validator-deployed, starting with recurring daily Bitcoin price threshold contracts that reset each day, run by the prediction platform Outcomexyz. Planned categories include politics, sports, macro data releases, crypto events, and entertainment. A later phase opens permissionless deployment: builders will stake 1,000,000 HYPE per market slot, slashable and burned if validators find oracle manipulation, invalid state transitions, or prolonged downtime. One slot supports rolling and recurring markets, recycling after each settlement.

Settlement without a token vote

The deepest difference between HIP-4 and the incumbent on-chain prediction markets is not fees. It is how truth gets decided.

Polymarket outsources contested resolutions to UMA’s optimistic oracle, where token holders vote on disputed outcomes, an architecture that has produced repeated controversies in 2026, including a $60 million market on a Strategy Bitcoin sale that resolved against the documented facts. The full mechanics and failure modes of that system are covered in our companion guide to how prediction markets resolve.

HIP-4 replaces the token vote with the chain itself. Settlement runs through Hyperliquid’s validator set executing automated resolution against pre-specified, objective data sources. There is no dispute window, no escalation, and no path for a token holder with a position in the market to also vote on its outcome. The trade-off is scope: deterministic settlement works for objective questions with a clean data source, which is why the first markets are price thresholds. Ambiguous questions, the kind that generate the worst oracle disputes elsewhere, are exactly the kind HIP-4’s design avoids listing.

What all of this looks like from the trader’s side

For a user, the machinery above mostly disappears. HIP-3 markets sit in the same interface as the flagship crypto perps, trade through the same API, and settle against the same margin account. A trader shorting gold on a builder-deployed market places the order the same way they would short Ethereum, and the differences show up in three places worth knowing.

Fees are higher on builder markets. The headline rate on a HIP-3 perp is twice the validator-operated rate, which at base tiers works out to roughly 3 and 9 basis points for makers and takers before discounts, with the deployer keeping half. Staking discounts, referral rebates, and collateral-based reductions still apply on top, so an active HYPE staker narrows the gap considerably.

Oracle quality varies by deployer. On validator-operated markets, the network itself maintains the price feed. On a HIP-3 market, the deployer chooses and operates the oracle, which is why the mark price on a weekend oil contract can drift from where Monday’s COMEX open eventually prints. During the West Asia crisis, Hyperliquid’s oil market traded on its own oracle through days when no traditional reference price existed at all. That independence is the product and the risk in one feature.

Collateral differs by market. Most markets margin in stablecoins, but HIP-3 supports alternative collateral where the deployer enables it, including yield-bearing assets, and HIP-4 outcome positions collateralize in USDH. Settlement demand for outcome markets flows through the stablecoin into the same fee-and-buyback loop that already routes nearly all protocol revenue toward HYPE, which is why analysts treat HIP-4 volume as a direct token catalyst rather than a side business.

The practical entry points have multiplied too. Beyond the native app, HIP-3 and HIP-4 markets surface through Phantom, through the FOMO app for the equities lineup, and through any front end built on the public API, since every builder market shares the unified HyperCore order flow.

The risk column

Every part of the story above has a counterweight, and an honest explainer lists them.

Deployer concentration is the loudest one. A permissionless system where one builder holds 90% of open interest has recreated a gatekeeper one level up, and the $32 million entry stake keeps it that way for now. Regulatory exposure is the second. Hyperliquid operates without KYC in most of the world, the United Kingdom’s FCA has declared the platform unauthorized, and pending United States market structure legislation could either validate or constrain synthetic stock perpetuals, a product category regulators have barely begun to examine. Institutional ceilings are the third: a June JPMorgan report saw limited institutional demand for perpetual futures generally, citing unbounded basis risk and missing clearing protections, which matters for a token whose valuation leans on volume growth. And the products themselves are dangerous instruments. Leveraged perpetuals on any underlying can liquidate a position in minutes, and cross margin across markets adds its own failure modes.

There is a subtler risk in the oracle layer that the slashing design only partially covers. A deployer’s oracle is a single point of interpretation for its markets, and unusual conditions expose the gap: when traditional venues close and a HIP-3 commodity market keeps trading, the mark price is whatever the deployer’s methodology says it is, with no external reference to check against until markets reopen. Validators review any 50% intraday reference move and slashing punishes proven manipulation, but a subtly mispriced weekend, honest or otherwise, transfers money between longs and shorts without tripping any threshold. Traders in builder markets are underwriting oracle methodology whether they think about it or not.

None of that has slowed the platform yet. Hyperliquid controls an estimated 70% of on-chain perpetuals volume, spot HYPE ETFs drew $111 million in inflows in late June while Bitcoin and Ethereum funds bled, and the ecosystem is spending on the long game, including a $29 million policy center in Washington. Whether the moat holds is a different question from whether it exists.

The bigger picture for L1 competition

HIP-3 and HIP-4 also reframe what layer 1 blockchains compete on. Ethereum and Solana fight over DeFi liquidity, users, and fees, a race with its own 2026 scoreboard. Hyperliquid opted out of the general-purpose contest and vertically integrated one thing: markets. The bet is that an exchange-shaped blockchain with permissionless market creation captures more value than a general-purpose chain hosting exchange apps. dYdX tried a dedicated appchain with governance-gated listings. GMX built on someone else’s layer 2. Hyperliquid is the first to make market creation itself permissionless at the chain layer, and the early evidence, an order of magnitude expansion in what can be traded on-chain, suggests the design space was bigger than the industry assumed.

What to watch from here

Three markers will tell the story over the next year. First, whether the HIP-3 stake requirement drops and the deployer set widens beyond one dominant builder. Second, whether HIP-4 volume becomes measurable against Polymarket and Kalshi once permissionless deployment opens and categories expand past crypto prices. Third, whether regulators treat builder-deployed stock perpetuals as an innovation to license or a loophole to close. The upgrades themselves are shipped and working. The open question, as always in this industry, is what survives contact with scale.

Frequently asked questions

What is Hyperliquid HIP-3?

HIP-3, called Builder-Deployed Perpetuals, is a Hyperliquid protocol upgrade live since October 13, 2025. It lets any builder who stakes 500,000 HYPE deploy an independent perpetual futures exchange on HyperCore, choosing the assets, oracle, collateral, and fee capture, while inheriting Hyperliquid’s matching engine, margining, and liquidation systems. It moved market listing from a core team decision to a permissionless, stake-secured process.

What is Hyperliquid HIP-4?

HIP-4 is the outcome markets upgrade, announced February 2, 2026 and live on mainnet since May 2, 2026. It adds fully collateralized event contracts that settle to exactly 0 or 1 at expiry, with merged Yes and No order books, USDH collateral, no liquidation risk, and zero fees to open a position. It is Hyperliquid’s entry into prediction markets.

How much does it cost to deploy a HIP-3 market?

A deployer must stake 500,000 HYPE, worth roughly $32 million at current prices near $64. The stake is slashable for misconduct and must be held for 30 days even after all of the deployer’s markets are halted. The first three assets deploy without an auction; additional assets go through a shared Dutch auction. Documentation says the threshold should fall over time.

What can you trade on HIP-3 markets?

Builder-deployed markets cover tokenized United States equities such as Nvidia, Tesla, Google, and Amazon, index products including a licensed S&P 500 contract and the Nasdaq-style XYZ100, commodities such as gold, silver, and oil benchmarked to COMEX and other references, FX, and long-tail crypto assets. Seven of Hyperliquid’s top ten markets by volume are now non-crypto assets.

How does HIP-4 settlement differ from Polymarket?

Polymarket resolves contested markets through UMA’s optimistic oracle, where token holders vote on disputed outcomes. HIP-4 settlement is deterministic: Hyperliquid’s validator set resolves each contract against a pre-specified objective data source, with no dispute window and no token vote. The design avoids governance attacks but limits markets to questions with clean, objective answers.

Who is TradeXYZ?

TradeXYZ is the dominant HIP-3 deployer, accounting for more than 90% of builder-deployed open interest. It launched the first HIP-3 market, the XYZ100 index, built out the equities and commodities lineup, secured S&P 500 ticker licensing, and co-launched the FOMO trading app with Hyperliquid in June 2026. Its dominance is also the center of the deployer concentration debate.

Is trading on Hyperliquid safe?

The protocol has strong solvency engineering and a clean track record on its core markets, but the products are high-risk by nature. Leveraged perpetuals can liquidate quickly, HIP-3 markets depend on each deployer’s oracle quality, the UK’s FCA lists the platform as unauthorized, and synthetic stock perpetuals sit in a regulatory gray zone. Position sizing and jurisdiction checks matter.

Does HIP-4 have liquidation risk?

No. Outcome positions are fully collateralized in USDH at purchase, so the maximum loss is the amount paid for the position and no liquidation engine is involved. That distinguishes outcome markets from perpetuals, where leverage means positions can be forcibly closed. The risk in outcome markets is being wrong about the event, or holding through a settlement data error.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Always do your own research. Information current as of July 3, 2026.

Bitget, the world’s largest Universal Exchange (UEX), has published CEO Gracy Chen’s mid-year address, outlining the company’s long-term vision for a more connected financial system powered by tokenization, artificial intelligence, and universal market access.

The leadership’s insights come as trading behavior continues to evolve beyond crypto alone. During the first half of 2026 the platform witnessed the shift, about 52% Bitget users now hold both stocks and crypto, 35% hold gold and other precious metals while 51% users use AI-powered tools. This highlights the growing demand for platforms that bring global markets together leveraging emerging tech.

Rather than becoming an “asset supermarket,” Bitget aims to remove the friction that separates financial markets. The letter outlines four principles guiding that strategy: improving capital efficiency, delivering global assets through a crypto-native experience, expanding financial access through products such as tokenized assets and pre-IPO investing, and simplifying trading through AI-powered automation.

“Our focus has pivoted from being a crypto exchange to a holistic universal provider,” said Gracy Chen, CEO of Bitget. “Our platform removes barriers that divided financial markets for decades. Users can now access crypto, stocks, CFDs, gold and do more with their capital 24/7.”

Bitget’s conviction on tokenization reshaping capital markets is based on Chen’s 10% tokenization vision, while highlighting products such as Stock+ and Reality as early examples of how blockchain infrastructure can make investing more accessible and efficient.

Artificial intelligence forms the second major pillar of the vision. As AI evolves from analysis toward execution, Chen described a future where users define investment goals and risk parameters while intelligent systems handle market monitoring and trade execution. Bitget now serves more than one million AI trading users alongside more than one million copy trading users, following the rollout of products including GetClaw and the GetAgent Playbook.

Closing the address, Chen described Bitget’s broader mission as extending financial opportunity beyond traditional institutional channels, calling it the shift from banking the unbanked to brokering the unbrokered.

Read the full “Break the Unbreakables” address here, or watch the address on Bitget’s X.

About Bitget

Bitget is the world’s largest Universal Exchange (UEX), serving over 125 million users and offering access to over 2M crypto tokens, 500+ tokenized stocks, ETFs, commodities, FX, and precious metals such as gold. The ecosystem is committed to helping users trade smarter with its AI agent, which co-pilots trade execution. Bitget is driving crypto adoption through strategic partnerships with LALIGA and MotoGP™. Aligned with its global impact strategy, Bitget has joined hands with UNICEF to support blockchain education for 1.1 million people by 2027. Bitget currently leads in the tokenized TradFi market, providing the industry’s lowest fees and highest liquidity across 150 regions worldwide.

For more information, visit: Website | X | Telegram | LinkedIn | Discord

Risk Warning: Digital asset prices are subject to fluctuation and may experience significant volatility. Investors are advised to only allocate funds they can afford to lose. The value of any investment may be impacted, and there is a possibility that financial objectives may not be met, nor the principal investment recovered. Independent financial advice should always be sought, and personal financial experience and standing carefully considered. Past performance is not a reliable indicator of future results. Bitget accepts no liability for any potential losses incurred. Nothing contained herein should be construed as financial advice. For further information, please refer to our Terms of Use.

The post Bitget CEO Gracy Chen Shares H1 2026 Remarks Highlight Company’s Strategy appeared first on BeInCrypto.

The European Securities and Markets Authority (ESMA) has warned that many prediction market contracts may already fall under existing restrictions on binary options, saying companies cannot avoid financial regulations simply by marketing them as “event contracts.”

In a public statement on Friday, the regulator reminded companies that event contracts meeting the definition of financial instruments are already prohibited from being marketed, distributed or sold to retail investors under national measures implementing ESMA’s 2018 binary options restrictions.

ESMA said the assessment depends on a contract’s characteristics rather than how it is marketed, adding that event contracts with binary outcomes and fixed payouts are likely to qualify as financial instruments subject to the restrictions.

The regulator also told companies that offering qualifying event contracts to professional or institutional clients still requires authorization under the EU’s Markets in Financial Instruments Directive, or MiFID II, regardless of whether retail investors are excluded.

Excerpt from ESMA’s July statement on event contracts. Source: ESMA

The statement does not introduce new restrictions. ESMA said it issued the reminder after observing increased offerings of event contracts and the rapid growth of prediction markets, noting that qualifying binary options have already been subject to national restrictions across the EU since 2018.

Related: StanChart joins ESMA’s first MiCA register update since deadline

US prediction markets face growing legal battle

In the United States, a regulatory battle over prediction markets is unfolding, pitting state gaming regulators against the Commodity Futures Trading Commission (CFTC) over whether event contracts should be treated as gambling or federally regulated derivatives.

By March, authorities in 11 states had taken legal or regulatory action against platforms including Kalshi and Polymarket. Nevada became the first state to temporarily block Kalshi’s operations, while Arizona brought criminal charges alleging the company was operating an illegal gambling business.

The following month, the CFTC asserted “exclusive jurisdiction” over prediction markets, saying Congress had entrusted the agency with sole authority to regulate commodity derivatives markets, including event contracts. The regulator also said it had sued several states and filed court briefs supporting platforms, including Kalshi.

The CFTC’s April announcement defending its authority over prediction markets. Source: CFTC.gov

The legal battle has continued to escalate. On June 30, a Massachusetts judge allowed state authorities to file an amended complaint against Kalshi in an ongoing lawsuit alleging that the company’s sports-event contracts constitute illegal gambling under state law.

The dispute has also prompted calls for congressional action. Last month, the Indian Gaming Association and American Gaming Association, joined by tribal and labor groups, urged lawmakers to amend the CLARITY Act to explicitly prohibit sports-related event contracts on prediction market platforms, arguing they fall outside the CFTC’s authority and should remain subject to state gambling laws.

Some legal experts believe the growing conflict between federal and state regulators over prediction markets could ultimately be decided by the US Supreme Court.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

Crypto World

Bittensor and Render Already Had Their Nvidia Moment, Stargate LLM is the Next 1000x AI Crypto Opportunity

Everyone who bought Nvidia in 2023 remembers why it felt like a leap of faith at the time. The AI story was still new, the chart hadn’t caught up yet, and most people waited for proof before buying in. That proof arrived, and the trade that followed became one of the biggest of the decade. Stargate LLM‘s presale sits in that same early window right now. Batch 1 just opened at $0.0005 per token, well ahead of any launch or listing.

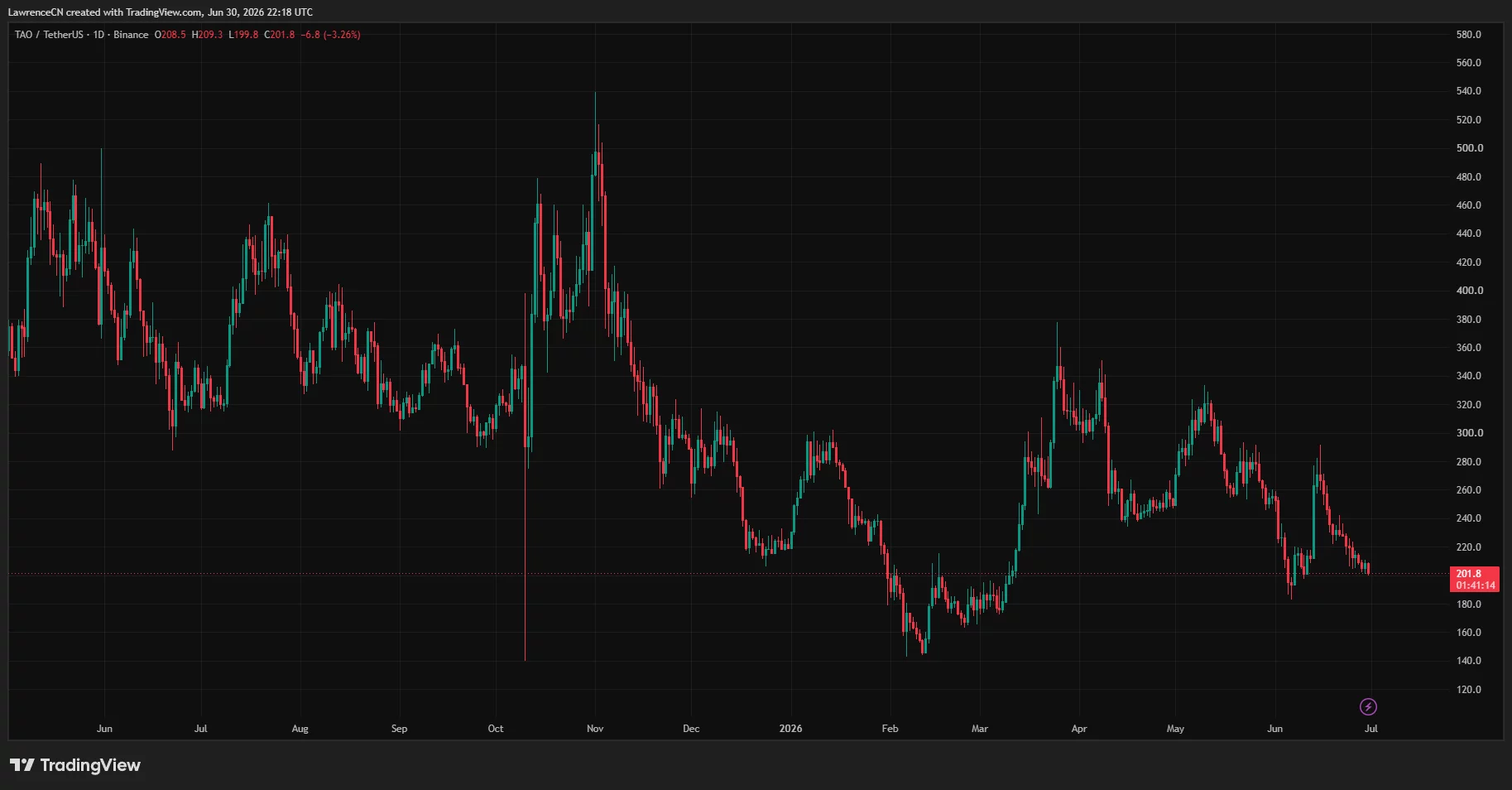

Bittensor and Render, two of the AI sector’s most established names, show what that same trade looks like once the proof has already arrived. TAO trades near $250 with a market cap close to $3 billion. TAO trades near $250 as of late June 2026, ranked around #27 to #37 with a market cap close to $3 billion. And Render is holding through a broader market pullback this week.

Stargate LLM: Getting In Before the Chart Exists

Global AI spending is on track to grow from roughly $391 billion in 2025 to more than $1.2 trillion by 2030. That kind of growth tends to reward the people who position early, and Stargate LLM is built to be one of the platforms through which growth flows. It’s not a wrapper riding on top of someone else’s model. It’s a full AI platform in its own right, offering conversational chat, image generation, video generation, private search, and its own agent marketplace, built to stand alongside names like OpenAI’s ChatGPT and Anthropic’s Claude rather than orbit around them.

The presale is structured in 10 batches, with the price stepping up at each stage. Batch 1 is open right now at $0.0005 per token, a 50x discount to the confirmed $0.025 launch price. The earlier a batch is bought into, the larger the theoretical multiple to launch, and Batch 1 alone carries a 50x path to listing, 9 batches ahead of where the presale eventually closes. That structure mirrors exactly what early infrastructure investors couldn’t get in 2023: a seat at the table before the breakout moment, not after it.

Token supply is fixed at 150 billion, with no additional minting planned after launch, and only 1% of that supply is set aside for the team. The rest flows to presale participants and to the community that will actually use the platform once it’s live. It’s the kind of allocation that signals a project built around its users first. This is exactly the kind of early window people are searching for when they look for the next 1000x AI crypto, a token priced before the market has had any real chance to weigh in.

Bittensor: A Mature Project Built Around Scarcity

Bittensor has spent the past year building its case around supply. The network capped its total token count at 21 million and completed its first halving in December 2025, cutting new token issuance in half. Bittensor ran its first halving on Dec. 12, 2025, cutting daily emissions from 7,200 to 3,600 TAO against a fixed 21 million cap, the same hard-cap design Bitcoin uses.

TAO daily price chart — June 30 | Source: crypto.news

Roughly 70% of the circulating supply is staked, locking away a large share of the tokens in circulation. It’s a well-established, actively used decentralized machine learning network, and TAO remains one of the most recognized names in AI crypto. Like most projects with a multi-year track record, its price today reflects a market that has already had time to study it closely.

Render: Real Infrastructure, Growing By the Week

Render connects people who need computing power for AI and rendering work with people who have GPUs sitting idle. The network recently expanded its capacity significantly, adding roughly 60,000 GPUs through a new partnership with Salad Technologies, approved through the project’s own governance process. It’s a genuine, functioning piece of AI infrastructure with real usage behind it.

Prices across the AI token sector dipped together this week amid a broader market pullback. A detailed market piece describes native DeFi, AI, and privacy tokens, including FET, TAO, RENDER, ZEC, and XMR, all falling as risk appetite faded across the board. which is normal for an established asset trading through short-term market cycles.

The Bottom Line

Bittensor and Render are two of the strongest, most established names building AI infrastructure on-chain today, and both are worth understanding on their own terms. Stargate LLM offers something different: a chance to get positioned at the very start of a project’s story, at Batch 1 pricing, before the market has set the price at all.

For anyone comparing the two paths, established infrastructure with a known track record or an early presale window still ahead of its own chart, both are real ways to be part of the AI crypto trade. They’re just at different points on the same road, and Stargate LLM is at the very beginning of its own.

Explore Stargate LLM:

Website: stargate.org

Buy: own.stargate.com

Telegram: https://t.me/StargatellmOfficial

Twitter/X: https://x.com/stargatellm

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Key Highlights

- PEG stock advanced 1.68% amid PSE&G’s weekend storm preparations.

- PSE&G deployed crews and equipment ahead of heat wave and thunderstorm threats.

- Extreme heat warning remained in effect as severe weather loomed over New Jersey.

- Residents advised to prepare emergency supplies and stay away from fallen power lines.

- Elevated air conditioning demand highlighted grid reliability concerns for PSE&G.

Shares of Public Service Enterprise Group (PEG) moved higher as its utility subsidiary PSE&G mobilized resources ahead of extreme heat and potential weekend storms. PEG advanced 1.68% to close at $81.62 during the trading session. The uptick followed the utility’s announcement regarding outage preparedness and anticipated surges in power consumption.

Public Service Enterprise Group Incorporated, PEG

PSE&G Mobilizes Resources Ahead of Weather Threats

PSE&G announced enhanced staffing levels throughout its service area as the holiday weekend approached. The company strategically deployed crews and stockpiled repair materials for rapid response capabilities. The operational strategy prioritized both heat-related strain and potential storm-induced infrastructure damage.

The National Weather Service maintained an Extreme Heat Warning through Saturday evening while simultaneously issuing storm alerts for Friday through Sunday. High winds accompanying thunderstorms posed significant risks to trees and electrical infrastructure across the region.

PSE&G indicated that repair teams would evaluate damage systematically and prioritize restoration efforts. The utility’s strategy focuses on repairing infrastructure that restores electricity to the greatest number of customers initially. Concurrently, customer service operations prepared for increased call volumes.

Public Service Enterprise Group Stock Advances on Operational Readiness

Public Service Enterprise Group equity appreciated as investors responded favorably to the utility’s proactive weather response strategy. The stock movement signaled market confidence in the company’s operational preparedness during peak summer electricity demand periods. Nevertheless, shares retreated modestly in after-hours trading.

PSE&G functions as the state’s premier electric and gas distribution utility serving New Jersey. Public Service Enterprise Group, its parent entity, maintains close ties to grid dependability and energy consumption patterns. Consequently, severe weather developments frequently influence operational performance metrics.

The company has committed substantial capital to electric infrastructure enhancements over recent months. These investments target improved reliability during extreme weather events including storms and prolonged heat episodes. Additionally, the utility maintains that system modernization enables faster crew response following service interruptions.

Residents Advised to Ready Households for Power Disruptions

PSE&G encouraged customers to fully charge mobile phones, essential medical equipment and backup power sources before storm systems arrive. The utility recommended securing patio furniture and loose objects outdoors. Furthermore, it suggested keeping flashlights and fresh batteries readily accessible.

The utility emphasized that all downed electrical wires must be presumed energized. Residents should maintain a minimum distance of 30 feet from any fallen conductor. They should immediately report hazardous conditions to PSE&G while contacting emergency services when imminent danger exists.

PSE&G cautioned against operating gasoline-powered generators indoors, within garages or any confined areas. The company stressed that incorrect generator operation creates serious carbon monoxide poisoning risks. Customers relying on electrically-powered medical devices should enroll in PSE&G’s registry and maintain alternative contingency arrangements.

Heat Wave Intensifies Concerns Over Electricity Consumption

Prolonged extreme heat forces air conditioning systems to operate continuously, substantially increasing electrical draw. PSE&G recommended that customers adjust thermostats to higher settings during absences from residences. The utility also suggested utilizing ceiling fans, closing window coverings, and maintaining clean HVAC filters.

The company directed customers toward available energy conservation programs and consumption monitoring resources. The MyMeter platform enables customers to monitor electricity usage via online accounts or smartphone applications. Accordingly, households can modify consumption patterns before receiving elevated utility statements.

The impending weekend storm threat compounds challenges for an already taxed electrical grid infrastructure. However, PSE&G affirmed that personnel and equipment remain positioned for forecasted conditions. The announcement maintained emphasis on service reliability, public safety, and seasonal power demand management.

Ethereum News: Grayscale Investments filed a Form 8-K for its Grayscale Ethereum Staking Mini ETF on July 2, 2026, disclosing the departure of CFO Edward McGee after seven years and his replacement by co-CFOs Kathryn Masci and Daniel Plourde on an interim basis, a governance shift at one of the most structurally sophisticated crypto ETF products currently listed in the U.S. market.

Discover: The Best Token Presales

Ethereum News: What the 8-K Actually Says, and What It Doesn’t

The 8-K filed with the SEC falls under the category covering departures, elections, and appointments of directors or certain officers, along with compensatory arrangements.

That category requires disclosure of the event but does not mandate full detail on circumstances, severance terms, or strategic rationale in the initial filing itself.

Kathryn Masci signed the filing as Co-Chief Financial Officer and Principal Financial and Accounting Officer of Grayscale Investments Sponsors, LLC.

Her background runs through Ernst & Young and Garrison Capital before she joined Grayscale in May 2020. Daniel Plourde, the second interim co-CFO, brings institutional ETF operations experience from SPDR ETF Trusts at State Street and Gabelli Funds – a combination that reads more like deliberate succession planning than an emergency scramble.

The structural significance of this governance event is modest in isolation. McGee’s exit does not appear to implicate fund strategy, staking policy, or custody operations.

What it does add to is a pattern of active corporate housekeeping at the sponsor level throughout 2025 and 2026, including the creation of a new Board of Managers for the Sponsor on May 4, 2026 – a context that makes the July filing look like a continuation of planned restructuring rather than a reactive disclosure.

Discover: The Best Crypto to Diversify Your Portfolio

The Fund Itself: Numbers That Matter More Than the Filing

The leadership change is the headline event, but the operational data behind the spot Ethereum ETF is where the real story sits.

The fund held over 861,000 Ethereum as of Q1 2026, up from roughly 734,000 ETH at the start of the year, net creations of approximately 218,500 ETH during the quarter, which translated to around $337 million in net inflows and ranked the fund as the top U.S. Ethereum ETP by Q1 inflows as reported by most news.

The staking yield mechanics are straightforward but worth quantifying precisely. Approximately 67% of the fund’s ETH is actively staked on Ethereum’s proof-of-stake network, generating a gross staking reward rate of approximately 2.88% annualized – the trailing 60-day figure Grayscale cited in January 2026.

Q1 2026 staking income came in at $8.38 million, with net investment income of $7.41 million after the fund’s 0.15% management fee. Total staking rewards generated since October 2025 have crossed $15 million.

That 2.88% gross yield against a 0.15% fee is a genuinely competitive structure. Non-staking spot ETH products capture price exposure only; holders of those funds absorb the fee drag without the partial offset that staking rewards provide.

The question for competing issuers is whether regulatory clarity on staking in registered fund structures,still evolving as of mid-2026, will allow them to match this product’s architecture or whether Grayscale’s first-mover position in staked Ethereum ETPs hardens further.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The post Ethereum News: Grayscale’s Ethereum Staking ETF Just Had Its CFO Resign appeared first on Cryptonews.

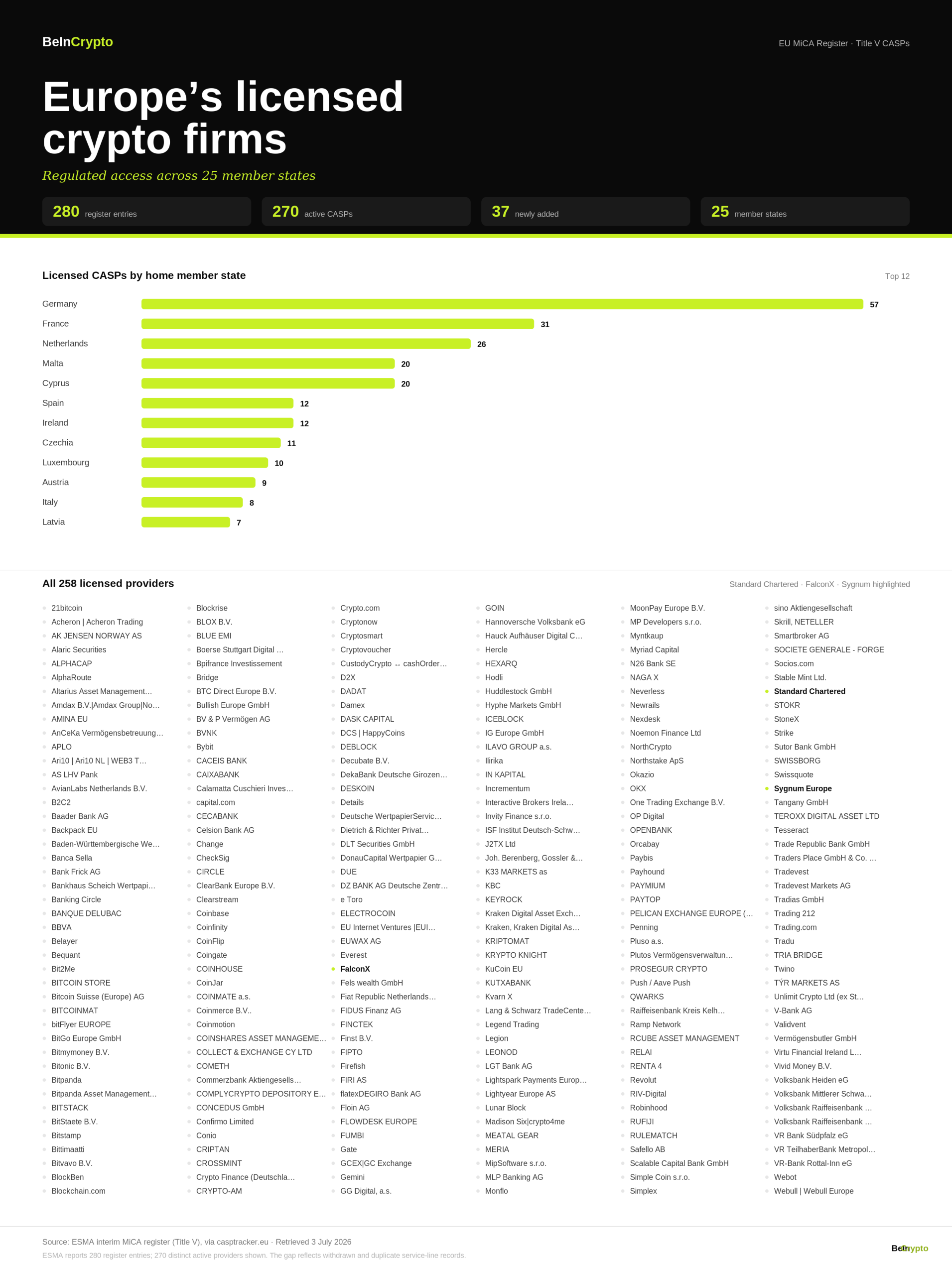

Standard Chartered secured its MiCA license, joining 37 firms added to the latest register update from the European Securities and Markets Authority (ESMA). Licensed crypto providers in the EU now total 280.

The batch is the first major licensing wave since MiCA’s transitional period closed on July 1. Grandfathered firms that missed the deadline can no longer serve EU clients under national rules.

First MiCA License Wave After the Transition Deadline

ESMA refreshes its interim register weekly. The latest update lists 280 authorized crypto-asset service providers (CASPs), 37 more than the previous file.

The timing explains the jump. MiCA’s Article 143 grandfathering clause let firms keep operating under national rules only until July 1, so this update captures the deadline scramble.

The new entrants also span both sides of finance. Crypto-native firms such as US prime broker FalconX and Sygnum Europe won CASP status, while Crédit Agricole’s CACEIS entered the register for e-money token issuers.

The MiCA transition period had already redrawn parts of the market before the register caught up. Most visibly, Tether’s EU delistings handed stablecoin ground to Circle.

Standard Chartered Swaps National Rules for an EU Passport

Standard Chartered announced both a MiCA authorization and an Electronic Money Institution (EMI) license through Standard Chartered Luxembourg S.A.

The bank opened that entity in 2025 to bring its digital asset custody business into the EU. Until now, however, it operated under the CSSF’s national virtual asset service provider regime, confined to Luxembourg.

Full MiCA status lifts that ceiling. The bank plans a phased rollout across the EU, with passporting subject to further approvals, extending custody launches already live in Asia and the Middle East.

“We are delighted to have obtained our MiCA and EMI licences, which enables us to progressively expand services to clients across Europe. This landmark authorisation reflects our strategic choice of Luxembourg…” Laurent Marochini, CEO of Standard Chartered Luxembourg, said in the statement.

Follow us on X to get the latest news as it happens

Luxembourg has meanwhile become a favored MiCA gateway. Coinbase houses its EU license there, and Ripple secured a preliminary MiCA CASP license in the Grand Duchy.

Web3 Users Question the Banking Embrace

The approval did not draw universal praise, however, with some users welcoming the bank’s Web3 build-out but highlighting the contradiction in its treatment of crypto-earning customers contradictory.

BeInCrypto could not independently verify the account details.

The contrast leaves an open question for MiCA’s next phase. Banks now hold licenses to serve crypto businesses across Europe, yet their retail risk policies may decide whether that access reaches the industry’s own participants.

The post Standard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms appeared first on BeInCrypto.

Quick Overview

-

Tesla activates robotaxi operations in Miami following delays past initial timeline.

-

TSLA shares gain momentum in after-hours trading following Miami announcement.

-

Miami marks the first of several postponed 2026 robotaxi cities to go live.

-

Waymo’s existing Miami presence intensifies competitive dynamics for Tesla.

-

Cybercab development continues as cornerstone of Tesla’s autonomous strategy beyond Model Y.

Tesla (TSLA) activated its autonomous ride-hailing service in Miami on Friday, refocusing attention on the company’s postponed geographic expansion strategy. This deployment extends Tesla’s robotaxi footprint into Florida following setbacks in meeting previously announced schedules. TSLA shares finished Friday’s session at $393.45, down 7.49%, before climbing modestly to $394.40 in extended trading.

Miami Deployment Highlights Schedule Challenges

Tesla confirmed the Miami service activation via its dedicated robotaxi social media channel, releasing details of the operational boundaries. The designated coverage zone encompasses sections of western Miami-Dade County, including West Miami, Doral, and Coral Gables. Notably absent from initial coverage are downtown Miami and Miami Beach.

This Florida entry represents Tesla’s inaugural robotaxi deployment beyond Texas and California’s San Francisco Bay Area. Miami also becomes the first among five cities that missed the company’s original first-half 2026 launch window. While the activation demonstrates forward momentum, it simultaneously highlights execution challenges.

Tesla’s announced first-half 2026 expansion list included Miami, Orlando, Tampa, Dallas, Houston, Phoenix, and Las Vegas. Only Dallas and Houston met that timeframe, leaving the remaining cities behind schedule. Miami’s activation now breaks through that logjam as the first delayed location to commence operations.

Rollout Timeline Shows Significant Gaps

Tesla initiated its autonomous ride service in Austin on June 22, 2025, deploying modified Model Y vehicles for passenger transport. Operations subsequently grew throughout Austin before extending into Dallas and Houston. The company has progressively removed safety personnel from certain trips as confidence in system performance increased.

California operations follow a distinct model because state regulations mandate specific permits for fully autonomous commercial rides. Tesla has not pursued these authorizations, resulting in Bay Area service that relies on human operators. Florida thus offers Tesla a more direct pathway for driverless commercial expansion.

Waymo’s established paid autonomous service in Miami amplifies competitive pressure on Tesla’s deployment speed. Tesla conducted Model Y testing in Miami starting August 2025. However, fare-paying passenger service only materialized after the company’s self-imposed first-half deadline had passed.

Cybercab Development Central to Investment Thesis

Tesla’s strategic robotaxi vision centers on Cybercab, a vehicle engineered specifically for autonomous operation. The design eliminates traditional steering wheels and pedals, making full autonomy a functional requirement rather than an option. Tesla currently operates its commercial robotaxi network exclusively with adapted Model Y vehicles.

Production began at Giga Texas in February when the first Cybercab exited the assembly line. Tesla has initiated public road validation in Austin using production-spec Cybercabs. Nevertheless, no jurisdiction has yet authorized the vehicle for commercial driverless passenger transport.

The Miami activation provides Tesla with momentum following notable TSLA stock weakness. However, substantial challenges remain including fleet expansion, geographic penetration, and regulatory clearances. Orlando, Tampa, Phoenix, and Las Vegas now represent critical milestones for validating the broader 2026 expansion blueprint.

BTSE Group has launched BTSE Indonesia, marking its official entry into Indonesia’s regulated crypto market. The platform began operations after the rebranding of NVX, a local digital asset exchange, into BTSE Indonesia.

The company announced the launch on July 3 through a joint venture with PT Aset Kripto Internasional. Under the arrangement, BTSE Group provides the exchange technology, trading engine, and liquidity, while the Indonesian entity manages local growth, partnerships, marketing, and sales.

BTSE Indonesia Enters Regulated Market

BTSE Indonesia operates under a license from Indonesia’s Financial Services Authority, known as OJK. The license allows the platform to act as a Digital Financial Assets and Crypto Assets Trading Operator, or PAKD, in the country.

That approval permits BTSE Indonesia to offer regulated crypto trading services while following anti-money laundering rules and customer asset protection standards. It also places the exchange among the approved platforms allowed to serve Indonesian crypto users under local supervision.

The license also allows the platform to work with Indonesian banks and payment gateways. As a result, users can access Indonesian rupiah deposits, withdrawals, conversions, and IDR-denominated trading pairs.

Joint Venture Combines Global Technology and Local Operations

BTSE Group said it will support the platform with trading infrastructure, liquidity, and technical systems. Meanwhile, BTSE Indonesia will use its domestic market knowledge to expand customer access and build business relationships.

Jeff Mei, Chief Operating Officer of BTSE Group, said Indonesia has the population, demand, and regulatory framework needed to become a major crypto hub in Asia. He added that the joint venture brings together global infrastructure and local expertise.

Stephanie Kusnadi, Chief Strategy Officer of BTSE Indonesia, said the integration with BTSE gives the platform access to global exchange technology while keeping its focus on local compliance and Indonesian users.

Indonesia Tightens Crypto Oversight

The launch comes as Indonesia continues to expand its rules for digital assets. In June, OJK issued Financial Services Authority Regulation No. 6 of 2026, which introduced new requirements for crypto promotion.

Under the rule, social media influencers who recommend crypto assets must obtain competency certification unless they already hold another qualifying license. They may also promote only assets listed on authorized exchanges.

The regulation also requires promotional campaigns to run through licensed financial services businesses. These businesses remain responsible for the content. For BTSE Indonesia, the launch places the platform inside a market where regulatory compliance now plays a central role in crypto expansion.

Find the original press release here.

While the market argues about XRP price levels, the ledger underneath it is assembling something more ambitious: a full stack of compliance-native DeFi rails aimed at banks, funds, and treasury desks. Here is what is already live, what is in validator voting right now, and why the whole bet could still fail.

Summary

- XRP Ledger is expanding its institutional DeFi infrastructure with compliance focused features including a permissioned DEX, native lending, and tokenized asset support.

- XRPL contributors are advancing XLS 65 and XLS 66 through validator voting to introduce fixed term lending designed for regulated financial institutions.

- Ripple’s RLUSD and more than $3 billion in tokenized real world assets are strengthening XRPL’s push to become a compliance ready blockchain for institutional finance.

The XRP Ledger has spent most of its fourteen-year life being described as a payments chain. Fast, cheap, boring. The description was accurate for a long time, and it also missed what has been happening on the ledger over the past eighteen months. Piece by piece, amendment by amendment, XRPL contributors and Ripple have been laying down infrastructure for something the rest of the industry mostly talks about in conference keynotes: DeFi that regulated institutions can actually use.

The phrase itself, institutional DeFi, tends to produce eye rolls among crypto natives. It sounds like a contradiction, a way of saying decentralized finance with the decentralization filed off. But the buildout on XRPL is concrete enough, and far enough along, that it deserves a serious look. As of this week, the two amendments that would bring native fixed-term lending to the ledger, XLS-65 and XLS-66, are in active validator voting following the Rippled v3.1.0 release in late January. Tokenized real-world assets on XRPL have passed $3 billion. Ripple’s stablecoin RLUSD crossed $1 billion in supply and ranks among the fastest-growing stablecoins in the market. A permissioned exchange layer with protocol-level compliance controls has gone live. None of this made much noise. That is partly the point.

The core bet: compliance at the protocol layer

Every major smart contract chain has tried to court institutions, and almost all of them have run into the same wall. Banks and asset managers cannot deploy client capital into open pools where the counterparty might be a sanctioned entity, a mixer, or a teenager with a hardware wallet. The standard industry answer has been to bolt compliance on afterward: whitelisted front ends, wrapped permissioned versions of open protocols, off-chain legal agreements draped over on-chain positions.

XRPL made the opposite bet. Instead of adding compliance on top, its contributors embedded identity and access controls into the protocol itself. Three primitives do most of the work.

Credentials, linked to decentralized identifiers, let trusted issuers attest on-chain that a wallet belongs to a KYC-verified entity, an accredited investor, or a firm with a specific regulatory permission. The attestation lives on the ledger. The underlying documents do not.

Permissioned Domains, which went live under the XLS-80 amendment with 91% validator support, use those credentials to gate access to specific markets. A domain can require that every participant holds a valid credential from an approved issuer. Anyone outside the domain simply cannot trade inside it.

The Permissioned DEX extends the ledger’s native order book exchange, which has existed since 2012, into these controlled environments. Regulated firms can run foreign exchange or tokenized asset markets with full AML and KYC enforcement while settlement still happens on a public blockchain. Activation followed within weeks of validator consensus earlier this year.

Alongside those three sit the supporting pieces: Multi-Purpose Tokens, a standard that embeds metadata and transfer rules at the asset layer so structured financial instruments do not need custom smart contracts; Batch Transactions for atomic delivery-versus-payment, the settlement pattern institutions use for cross-asset swaps; and Token Escrow support extended to IOUs and MPTs.

The design philosophy separates XRPL from nearly everything else in the market. On Ethereum or Solana, an institution wanting a compliant venue has to build one out of general-purpose parts and hope the auditors sign off. On XRPL, the compliance tooling is the venue.

The lending protocol is the real test

Infrastructure is necessary but not sufficient. The feature that will decide whether institutional DeFi on XRPL is a real business or a well-documented ghost town is the lending protocol, defined in the XLS-65 and XLS-66 specifications.

The two amendments work as a pair. XLS-65 introduces Single Asset Vaults, which aggregate liquidity from depositors and issue vault shares that can be transferable or locked depending on configuration. XLS-66 builds the actual credit machinery on top: fixed-term, fixed-rate loans with preset amortization schedules, issued through on-ledger contracts between lenders and borrowers.

The design choices are telling. Where open DeFi lending runs on overcollateralization and instant liquidations, the XRPL protocol supports uncollateralized loans with off-chain underwriting. Borrower evaluation, credit scoring, and risk management stay where institutions already have mature models, while issuance, repayment, and default records live on the ledger. First-loss capital structures add a protection layer familiar to anyone who has looked at securitization. Vault operators can restrict participation to KYC and AML compliant entities at the protocol level, which is precisely the feature that separates this from open DeFi.

Doppler Finance, a tokenized capital markets infrastructure firm, put the honest caveat on record this week: a protocol can define how lending activity is recorded and executed on-chain, but it cannot, by itself, create an institutional credit market. Underwriting, treasury management, portfolio monitoring, and regulatory oversight all need operational layers that no amendment can ship. XLS-66 provides the rails. Someone still has to run trains on them.

There is at least one committed passenger. Evernorth, one of the largest XRP treasury firms, has said it will make the lending protocol a core pillar of its digital asset strategy, describing it as a potential fundamental shift in how institutional liquidity moves on-chain and pointing to what it called a multi-billion-dollar annual yield opportunity for the XRP community. Treasury firms holding large XRP positions have an obvious incentive here: idle tokens earn nothing, and a native, compliance-gated lending market is the most direct way to change that.

The amendments are testable on devnet now, and developers can integrate against the lending stack ahead of mainnet activation. The open question is the validator vote. XRPL amendments require sustained support above the 80% threshold for two weeks before activation, and that process can stretch for months with no guarantee of passage. The framework is credible. The activation path is not automatic.

How amendments actually pass, and why it takes forever

Because so much of the XRPL story now hangs on validator votes, it is worth understanding the machinery, which differs from every other major chain’s governance.

XRPL has no token voting and no foundation decree. Protocol changes ship as amendments inside validator software releases, and each amendment activates only after more than 80% of trusted validators signal support continuously for two full weeks. Dip below the threshold for an hour and the clock resets. The validator set doing the voting is defined by Unique Node Lists, the curated rosters of validators that operators choose to trust, populated by exchanges, universities, infrastructure firms, and long-time community operators across jurisdictions.

The design makes XRPL upgrades slow, conservative, and hard to capture, three adjectives that read as insults on crypto Twitter and as compliments in a bank’s vendor-risk review. It also means every roadmap date in this article carries an implicit asterisk. Permissioned Domains cleared activation with 91% support, a comfortable margin. The lending amendments face a more complicated vote because they change the ledger’s risk surface in ways some conservative operators have historically resisted; earlier programmability proposals spent long stretches stuck below threshold while operators debated attack surface. The voting is live now following the v3.1.0 release, testable code is on devnet, and the realistic activation window stretches from weeks to quarters depending on how fast the holdouts move.

For traders, this creates a strange information asymmetry. Amendment support percentages are public, on-chain, and updated continuously, yet almost nobody prices them. Watching XLS-66 support climb toward 80% is about as close to a scheduled, verifiable catalyst as this market offers, and it sits in plain sight.

The competition is building the same thing with different parts

XRPL is not the only chain that noticed institutions want compliant rails, and an honest assessment has to place the ledger against the two ecosystems actually holding the money.

Ethereum remains the default venue for tokenized institutional product, full stop. BlackRock’s tokenized fund complex, Franklin Templeton’s on-chain money market operation, and the JPMorgan digital asset stack all touched Ethereum first, and the chain holds roughly 68% of global DeFi deposits along with about 70% of stablecoin supply. Its institutional DeFi answer is assembled from general-purpose parts: permissioned pool deployments of Aave, KYC-gated hooks on Uniswap V4, wrapper tokens with transfer restrictions, and off-chain agreements binding it together. The approach works, and its weakness is exactly what XRPL is betting on: every assembled solution is bespoke, every audit is novel, and the compliance burden lands on the builder instead of the protocol.

Solana has moved fastest recently. Token-2022 extensions gave issuers protocol-adjacent controls, transfer hooks, confidential amounts, and interest-bearing logic, and the Solana Developer Platform launched in March with Mastercard, Worldpay, and Western Union attached. Solana’s pitch is throughput plus tooling; its gap is that compliance remains a token-level option instead of a market-level guarantee, and its validator economics and outage history still appear in institutional risk memos even after the Firedancer-era reliability turnaround.

XRPL’s differentiation survives the comparison in one specific sense: it is the only major venue where identity, market access, and settlement controls are native ledger objects that no application can misconfigure. The cost of that purity is a smaller developer surface, a shallower liquidity base, and no general-purpose composability on mainnet. Institutions choosing between the three are effectively choosing which risk they prefer: Ethereum’s complexity, Solana’s history, or XRPL’s emptiness.

Three billion dollars of quiet traction

Skeptics can reasonably ask whether any of this is being used. The answer, increasingly, is yes, though the numbers remain small next to the giants.

Over $3 billion in tokenized real-world assets currently sit on XRPL, which places the ledger inside the top ten chains for RWA value. The most striking single data point came from a pilot earlier this year in which Ripple and JPMorgan processed a tokenized U.S. Treasury redemption in under five seconds, settling on XRPL what normally crawls through legacy market plumbing. The ledger also recorded its first month with more than $1 billion in stablecoin volume, and RLUSD passed the $1 billion supply mark while expanding into consortium settlement arrangements.

On the payments and FX side, XRP itself does structural work that most native assets do not. The ledger routes trades through XRP automatically whenever doing so improves pricing, a mechanism called autobridging. If there is no direct liquidity between two stablecoins or two tokenized currencies, the trade hops through XRP. The mechanism works inside the new permissioned environments as well as on the public DEX, though trades cannot bridge between the two. Every account reserve, every transaction fee, and a growing share of FX routing runs through the native asset, which ties institutional adoption of the ledger back to demand for the token in a way that is mechanical instead of narrative.

That linkage matters for anyone holding XRP, which trades near $1.08 at the time of writing after spending weeks pinned around the psychologically loaded $1.00 level. The token is still down more than 50% over twelve months, and the gap between infrastructure progress and price performance has become one of the more uncomfortable facts in the ecosystem. Readers who want the market-structure side of that story can find it in our coverage of why the broader market has been trading risk-off since the spring.

The gap XRPL still has to close

For all the compliance tooling, XRPL remains a shallow DeFi venue by the numbers that crypto natives actually check. Chain TVL sits far below rivals: Solana holds roughly $9 billion in DeFi deposits and BNB Chain about $6.5 billion, while XRPL’s locked value is a fraction of either. Deep liquidity attracts deep liquidity, and the ledger has not had it.

Part of the problem is technical, and it is being addressed with unusual candor. XRPL’s native automated market maker, live since 2024, launched with only a constant product curve at a time when roughly 60% of AMM volume across major ecosystems runs through concentrated liquidity designs. In late May, a draft amendment titled AMM Swappable Curves was filed on the XRPL standards repository, proposing three pluggable curve types: constant product, concentrated liquidity, and StableSwap, with a fully programmable Smart AMM reserved for a follow-up specification. Existing pools would stay untouched. If it passes, the ledger’s biggest capital-efficiency gap starts to close. If it stalls in the amendment process, XRPL keeps asking institutions to trade on 2024 infrastructure.

The other gap is programmability. XRPL mainnet deliberately avoids general-purpose smart contracts, which keeps the attack surface small and the behavior predictable, qualities institutions like, but it also means builders who need full flexibility have to go elsewhere. The ecosystem’s answer is a dual track: measured programmability on mainnet through Smart Escrows, which let developers write custom release conditions into the existing escrow primitive, and a live EVM sidechain bridged via Axelar for teams that want Solidity and full composability. Whether liquidity follows that split or gets fragmented by it remains an open question.

Privacy is the next frontier, and the strangest one

The roadmap item that best captures XRPL’s institutional positioning is also the one that sounds least like crypto: confidential transfers. Multi-Purpose Tokens are getting zero-knowledge-proof-based encryption of transaction amounts and balances, letting institutions move tokenized assets and manage positions without broadcasting their book to every competitor running a block explorer, while preserving selective disclosure for regulators and auditors.

Full transparency, it turns out, is a bug for professional money, not a feature. No trading desk wants its inventory legible in real time. The XRPL community has moved past exploration into prototyping ZKP integrations with research and compliance teams, with confidential MPT transfers slated as the first milestone. Privacy with accountability is the stated frame: encrypted by default, provable on demand.

Put the pieces in sequence and the shape of the strategy becomes clear. Identity first, through credentials. Access control second, through domains and the permissioned DEX. Assets third, through MPTs and tokenization. Credit fourth, through the lending protocol. Confidentiality fifth, through ZKPs. It reads less like a crypto roadmap and more like someone rebuilding the back office of a mid-sized bank, one amendment at a time.

The sidechain wildcard

One more piece complicates the tidy mainnet story: the XRPL EVM sidechain, live and bridged through Axelar, running on eXRP as gas. Its job is to catch the builders mainnet’s minimalism turns away, Solidity teams who want full composability with a route into XRPL liquidity and identity features. The dual-track design is defensible, mainnet stays lean while experimentation happens next door, but it imports the exact problem Ethereum has spent years managing: liquidity and users split across environments with a bridge in between, and bridges remain the industry’s most reliably exploited component. If institutional flows land on mainnet while DeFi innovation concentrates on the sidechain, XRPL ends up running two half-ecosystems instead of one whole one. The optimists’ version is that the sidechain functions as a proving ground, with successful patterns graduating into mainnet amendments the way ZKP research moved from prototype toward the confidential transfer roadmap alongside partners such as Hidden Road, the prime broker Ripple acquired to give institutional clients a familiar front door. Which version plays out is a 2027 question; the split exists today.

RLUSD is the demand engine hiding in plain sight

If the lending protocol is the supply side of XRPL’s institutional buildout, the stablecoin is the demand side, and it deserves more attention than it usually gets.

RLUSD launched under a New York trust charter, which put it in the small club of stablecoins that compliance departments can approve without a fight, and its growth since has outpaced nearly every peer on a percentage basis: past $1 billion in supply, expanding into multi-issuer consortium arrangements, and increasingly the settlement leg in XRPL’s FX corridors. The strategic logic is circular by design. Stablecoin corridors generate ledger volume, ledger volume generates XRP fee burn and autobridge demand, and a trusted on-ledger dollar makes every other institutional product viable, because tokenized Treasuries need something to trade against and vaults need a funding currency.

The lending protocol makes the loop explicit. The first wave of XLS-66 vaults is widely expected to be RLUSD-funded, with institutional borrowers taking fixed-term dollar credit against off-chain underwriting. If that market reaches even single-digit billions, XRPL hosts a native short-term credit curve denominated in a regulated stablecoin, which is the kind of boring financial primitive that payments desks, market makers, and treasury managers actually budget for. Whether regulated entities deploy capital into RLUSD-funded vaults at scale is, in one sentence, the whole question the next two quarters will answer.

The watchlist for the next two quarters

For readers who want to track the buildout instead of the discourse, the roadmap compresses to a short list of verifiable checkpoints.

• XLS-65 and XLS-66 validator support crossing and holding the 80% threshold, the single highest-signal event on the board.

• Confidential MPT transfers shipping in the stated first-quarter window, XRPL’s first production zero-knowledge feature.

• Permissioned DEX volume and domain creation after activation, the difference between compliance theater and used infrastructure.

• MPT integration with the native DEX, scheduled alongside Smart Escrows, which lets tokenized instruments trade against XRP and IOUs directly.

• The AMM Swappable Curves amendment advancing from draft to vote, closing the concentrated liquidity gap.

• Follow-through from Evernorth and any second public institutional commitment to the lending protocol, because one anchor tenant is a pilot and two is a market.

Each item is public, dated, and falsifiable, which is more than can be said for most crypto roadmaps.

What could still go wrong

The bear case does not require much imagination, because pieces of it are already visible.

• Validator activation risk is real and immediate. XLS-65 and XLS-66 need sustained supermajority support, and amendment votes have stalled before. Every month of delay is a month rival chains spend courting the same institutions.

• Infrastructure is not demand. XRPL has built the rails ahead of proven appetite, and outside Evernorth’s stated intent, no regulated lender has committed capital publicly. The chain could end up with the best-documented empty credit market in crypto.

• The competition is not standing still. Ethereum remains the default for tokenized funds from BlackRock and Franklin Templeton, and Solana launched a developer platform this spring with Mastercard, Worldpay, and Western Union as early adopters. XRPL’s compliance-native design is a differentiator, not a moat.

• Regulatory frameworks cut both ways. The same clarity that lets institutions touch permissioned DeFi also lets them demand terms, and there is no assurance the economics of on-ledger credit will beat what prime brokers already offer off-chain.

There is also a subtler risk: that permissioned DeFi succeeds and simply fails to matter for XRP. If activity concentrates in gated domains trading tokenized Treasuries against RLUSD, the native asset’s role could shrink to fees and reserves, a payments-era footprint under an institutional-era ledger. Autobridging and escrow denominated in XRP push against that outcome, but the tension is real and worth watching in the data rather than the marketing.

A ledger playing a long game

Step back far enough and the XRPL story inverts the usual crypto sequence. Most chains launch permissionless, attract speculation, and then spend years retrofitting the controls institutions require. XRPL is running the film backward: build the controls first, accept years of looking sleepy next to memecoin casinos, and wait for the moment when regulated capital decides it finally wants on-chain settlement, credit, and FX.

That moment may be closer than the price chart suggests. Tokenization has become the fastest-growing corner of the industry, stablecoin legislation has unlocked bank participation across several jurisdictions, and the first generation of tokenized funds is now large enough to need somewhere to borrow, lend, and hedge. The chains that win that flow will be the ones where a compliance officer can sign off without a novel-length risk memo.

Whether XRPL becomes one of them comes down to two things it does not fully control: an 80% validator threshold, and the willingness of institutions to move from pilots to production. The infrastructure argument has been made, and made well. The adoption argument is still being written, one vault and one loan at a time. For a network that has been declared irrelevant more times than any other top-ten asset, quietly shipping the plumbing while nobody watches might be the most on-brand strategy available.

For readers newer to the mechanics referenced here, our explainers on Ripple Prime and institutional brokerage, consortium stablecoins, and the earlier lending and escrow roadmap cover the building blocks in more depth.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Always do your own research. Information current as of July 3, 2026.

Crypto World

Sandisk Corporation (SNDK) Stock Falls 14% Despite Major NAND Manufacturing Breakthrough

Key Takeaways

-

Sandisk shares fell 14.13% even as manufacturing milestone was achieved.

-

Kioxia partnership launches 10th-generation 3D Flash at Japanese production site.

-

K2 manufacturing facility increases cutting-edge NAND production for AI applications.

-

Partnership extension through 2034 provides sustained NAND development framework.

-

After-hours recovery modest following significant intraday selling pressure.

Sandisk Corporation (SNDK) experienced a steep 14.13% decline, closing at 1,745.00, even as the company achieved significant progress with its Kioxia NAND manufacturing collaboration. After-hours trading saw a modest recovery to 1,762.07, representing a 0.98% gain. Nevertheless, the trading session revealed substantial downward pressure that overshadowed positive manufacturing developments.

Next-Generation 3D Flash Manufacturing Commences at K2 Plant