Crypto World

XRP death cross warning puts $1.20 resistance in focus

XRP traded near $1.13 on July 5, according to crypto.news market data. The token was down 1.04% over 24 hours but remained up 7.79% over seven days. Its market cap stood near $70.26 billion, while 24-hour volume was about $1.67 billion.

Summary

- XRP’s current price near $1.13 keeps the token below the key $1.20 weekly average.

- A weekly death cross could turn the 200-week SMA from support into future resistance.

- Crypto.news analysis keeps $1.10, $1.20 and $1.40 as key levels for XRP traders.

The price remains close to a key technical zone after a short recovery from the $1 area. XRP has moved back above short-term support, but it has not reclaimed the higher resistance area near $1.20.

A post from ChartNerd warned that XRP is close to printing a weekly 20 EMA and 200-week SMA death cross. The analyst said the 200-week SMA near $1.20 may turn from a support floor into a supply ceiling.

That level now matters because price remains below it. A weekly close above $1.20 would weaken the bearish case. Failure to reclaim it may keep sellers active during future rallies.

Weekly death cross keeps traders cautious

A death cross happens when a shorter moving average falls below a longer moving average. In this case, the focus is on the weekly 20 EMA and the 200-week SMA.

The signal does not confirm an instant drop by itself. It shows that medium-term momentum has weakened against the long-term trend. Traders often watch how price reacts after the cross appears.

ChartNerd said “the 200-week SMA ($1.20) now has the potential to flip from a historical support floor into a supply ceiling.” The analyst added that XRP must reclaim that area to reject the bearish setup.

The analyst also pointed to two past examples. In 2022, XRP formed a bottom shortly after a similar signal. In the 2018 to 2020 bear market, the final low came months later after repeated failures near the 200-week SMA.

Daily chart shows short-term recovery

The XRP/USDT daily chart still shows a broader downtrend, with lower highs from May into late June. The token recently bounced from the lower Bollinger Band near $1 and moved back above the middle band.

The latest candle is red near $1.1325, showing a pullback after the rebound. Price remains between the middle Bollinger Band near $1.1064 and the upper band near $1.2094.

Holding above $1.1064 keeps the short-term recovery alive. A drop below that level would weaken the bounce and bring the $1.00 to $1.03 area back into focus.

The MACD has improved, with the MACD line above the signal line and a positive histogram. Still, both lines remain below zero. That means momentum is recovering, but the wider trend has not fully turned.

Source: TradingView

Crypto.news data keeps $1.20 in focus

Crypto.news reported on July 3 that XRP climbed to a three-day high after Ripple’s European expansion and a fresh Supertrend buy signal. The report said XRP moved from around $1.02 on July 1 to an intraday high near $1.11.

A separate crypto.news analysis said XRP needed to reclaim $1.20 to $1.25 to support a stronger rebound. It also placed $1.10 as a key support level and warned that wider weakness could bring $0.90 and $0.80 back into view.

The same report said a monthly close above $1.40 would help confirm a stronger double-bottom case. Until then, XRP remains in a cautious zone, even after the recent rebound.

At press time, traders are watching three levels. XRP must hold $1.10 to protect the short-term bounce, reclaim $1.20 to weaken the death cross warning, and clear $1.40 to improve the larger structure.

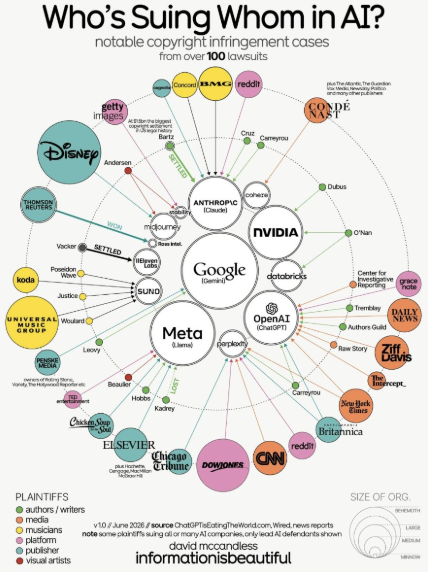

Anthropic faces a new $75 million lawsuit from authors who claim the company pirated copyrighted books to train Claude. The fresh case adds to mounting legal pressure on the AI developer.

The suit signals that the fight between authors and AI companies remains far from over across the industry.

What the New Anthropic Copyright Lawsuit Alleges

A copyright lawsuit is a legal action claiming someone used protected creative work without permission, licensing, or fair compensation. The new complaint accuses Anthropic of copying books from pirate libraries to train Claude. Furthermore, it seeks $75 million in damages.

The authors argue that Anthropic sourced their works from well-known shadow libraries. These sites host copyrighted material without any consent from the original creators, according to The New York Post.

Moreover, the plaintiffs say the company never sought licensing or offered payment before ingesting the books.

The case rests on a specific legal distinction. A previous ruling found that training AI on legally acquired books qualifies as fair use.

However, downloading pirated copies was deemed a separate act of infringement. As a result, the piracy claim remains the central legal battleground.

The plaintiffs believe existing settlements undervalue their works. Copyright law allows statutory damages of up to $150,000 per willfully infringed work.

The authors argue that smaller per-book payouts fail to reflect the true scale of the alleged infringement.

Follow us on X to get the latest news as it happens.

Why the Legal Pressure on Anthropic Keeps Building

The new lawsuit does not stand alone. Anthropic already faces a separate class action filed in June over its Claude Max subscription plans. That case targets the company on a completely different front, adding to the broader legal strain.

In that earlier suit, plaintiff Karl Kahn alleged the advertised 5x and 20x usage boosts collapsed under hidden caps.

Furthermore, the complaint targeted the $100 Max 5x and $200 Max 20x tiers. It sought refunds for subscribers since the plans launched in 2025.

The copyright case carries far heavier financial stakes. Anthropic previously settled a landmark class action for roughly $1.5 billion. That deal paid authors around $3,000 each for an estimated 500,000 pirated books covered under the agreement.

Some authors chose to opt out of that settlement. As a result, they retained the right to pursue their own individual claims.

The new $75 million lawsuit reflects exactly that strategy, allowing plaintiffs to seek far larger per-work damages.

Anthropic maintains a strong financial position despite the pressure. The company is valued at hundreds of billions of dollars following recent funding rounds. However, repeated legal challenges could reshape how AI firms source training data and market their subscription products going forward.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights.

The post Anthropic Faces a New $75 Million Lawsuit for Pirating Books to Train Claude AI appeared first on BeInCrypto.

Key Takeaways

- Shares of AXP are currently changing hands around $351.96, posting a 1.42% daily gain with a market capitalization approaching $240 billion

- First-quarter 2026 earnings per share reached $4.28, surpassing analyst expectations of $4.01; revenues climbed 11.4% from the prior year to $14.21 billion

- The company maintained its full-year 2026 EPS outlook of $17.30 to $17.90; Wall Street projects $17.65 on average

- Younger demographics, particularly Millennials and Gen Z, represent the company’s most rapidly expanding customer base

- Analyst consensus stands at Moderate Buy with a mean price objective of $366.95; Goldman Sachs has set a $400 target

American Express (AXP) stock is currently priced near $351.96, drawing renewed attention following a series of positive analyst revisions and increased institutional accumulation. Trading approximately 9% beneath its 52-week peak of $387.49, the stock remains comfortably above its yearly low of $288.34.

K.J. Harrison & Partners established a fresh stake worth $1.21 million during the first quarter, acquiring 4,003 shares. Multiple other institutional players also expanded their positions throughout the period. Institutional ownership of AXP stock now represents 84.33% of shares outstanding.

The first-quarter financial performance exceeded expectations. The credit card giant delivered earnings per share of $4.28, topping the Street consensus of $4.01 by $0.27. Total revenues reached $14.21 billion, representing an 11.4% year-over-year increase. The company achieved a net profit margin of 15.13% and posted a return on equity of 33.95%.

Executives reaffirmed their full-year 2026 earnings guidance range of $17.30 to $17.90 per share. The analyst community currently projects $17.65 for the complete fiscal year.

Analyst sentiment has strengthened noticeably. Goldman Sachs elevated its price target from $360 to $400 while maintaining a Buy recommendation. Truist increased its objective from $360 to $375, also with a Buy stance. Piper Sandler launched coverage with an Overweight rating and a $396 price target. The collective average price target among all covering analysts stands at $366.95, implying approximately 4% upside from current levels.

The overall analyst rating is Moderate Buy, comprising two Strong Buy ratings, nine Buy recommendations, eleven Hold positions, and one Sell rating among the 23 analysts providing coverage.

Younger Demographics Fueling Expansion

A particularly compelling narrative involves shifting customer demographics. Millennials and Gen Z members have emerged as the fastest-growing segment within Amex’s cardholder base. This demographic shift aligns perfectly with spending patterns focused on experiential purchases — travel, dining, entertainment — categories where the company’s premium card offerings deliver maximum rewards and benefits.

Capturing younger cardholders with premium products early in their financial journey tends to create lasting relationships. As significant wealth transfers occur from older generations over the next several decades, this early-established brand affinity could generate substantial long-term value for the company.

Equity analysts project earnings expansion of 13% to 14% per year over the next three to five years. Even applying a more conservative 10% growth assumption to account for potential economic headwinds, combined with the current 1.1% dividend yield, investors could reasonably expect total annual returns around 11%. Using the rule of 72, this pace would double an investment approximately every six to seven years.

Valuation Metrics and Shareholder Returns

AXP currently trades at less than 20 times projected 2026 earnings. This valuation appears reasonable given the company’s growth trajectory. The price-to-earnings-growth ratio sits at 1.45, while the beta coefficient of 1.04 indicates volatility roughly matching the broader market.

The company recently announced its quarterly dividend of $0.95 per share, scheduled for payment on August 10 to shareholders of record as of July 2. This equates to an annualized payout of $3.80, generating a yield of approximately 1.1%.

The stock is trading above both its 50-day moving average of $322.50 and its 200-day moving average of $333.27.

The upcoming earnings release will provide critical insight into whether the first-quarter outperformance represents an isolated event or the beginning of sustained momentum.

Crypto World

Market Preview: SpaceX (SPACEX) Nasdaq 100 Debut Highlights Busy Week of Earnings and Fed Minutes

Key Highlights

- SpaceX makes its Nasdaq 100 index debut on Tuesday, July 8, following significant price swings since its June public offering

- Financial institutions can now issue initial coverage on SpaceX as the post-IPO analyst restriction period concludes

- PepsiCo and Delta Air Lines unveil second-quarter financial results, spotlighting consumer behavior and operational expenses

- Federal Reserve publishes its June policy meeting transcript on Wednesday, potentially revealing rate adjustment plans

- Tech and media industry leaders converge at the Allen & Company Sun Valley Conference throughout the week

PepsiCo reduced pricing during the winter months after elevated inflation caused shoppers to seek alternatives to premium-priced products. Delta described travel appetite as “really great” in March while implementing fare increases to offset rising operational expenses. These quarterly reports will provide investors with valuable insight into current consumer spending patterns.

Fed Meeting Transcript Release Takes Center Stage

The Federal Reserve publishes its June policy meeting minutes on Wednesday at 2 p.m. ET. During that session, fifty percent of voting members indicated they anticipated at least one rate increase before the calendar year concludes. New Federal Reserve Chair Kevin Warsh has demonstrated a more restrictive monetary policy stance, prompting market participants to scrutinize the document for additional clarity on future policy direction.

The weekly unemployment claims figures and the New York Federal Reserve’s consumer inflation expectations report are also scheduled for release. The previous week’s employment statistics registered below analyst projections, which temporarily reduced speculation about imminent rate increases.

Levi Strauss announces its fiscal second-quarter financial performance on Wednesday. The apparel company exceeded analyst estimates in the previous quarter and upgraded its full-year guidance. Management attributed the positive results to enhanced direct-to-consumer channel performance and expanded product offerings beyond traditional denim.

Costco will publish its highly anticipated monthly sales data during the week.

SpaceX Joins Elite Nasdaq 100 Index

SpaceX becomes a Nasdaq 100 constituent prior to Tuesday’s market opening. The benchmark index comprises the 100 largest non-financial corporations listed on the Nasdaq stock exchange and serves as a performance reference for numerous institutional investment portfolios. Index membership is anticipated to generate increased buying pressure as passive index funds establish positions.

SpaceX equity has experienced substantial price fluctuations since the company’s June 12 market debut. The shares commenced trading at a reduced valuation, briefly surged above $225 — temporarily positioning SpaceX’s market capitalization ahead of Amazon — before retreating to a low of $147. The stock concluded last week’s trading session at $162. Market observers anticipate continued price volatility in the near term.

This week simultaneously marks the conclusion of the mandatory analyst quiet period that followed SpaceX’s initial public offering. Investment research firms are now authorized to distribute their inaugural analysis and recommendations on the company. These professional assessments could significantly influence share price movement.

The Allen & Company Sun Valley Conference commences this week. Senior executives from Apple, Amazon, Meta, Google, Netflix, Disney, and Warner Bros. Discovery are scheduled to participate. Concurrently, the Raise Summit AI conference convenes in Paris, showcasing thought leaders from Google, Broadcom, Anthropic, and OpenAI.

The three primary U.S. equity indexes concluded the second quarter with percentage gains in the double digits. The previous week featured abbreviated trading due to the Independence Day holiday, and all three major benchmarks registered positive returns.

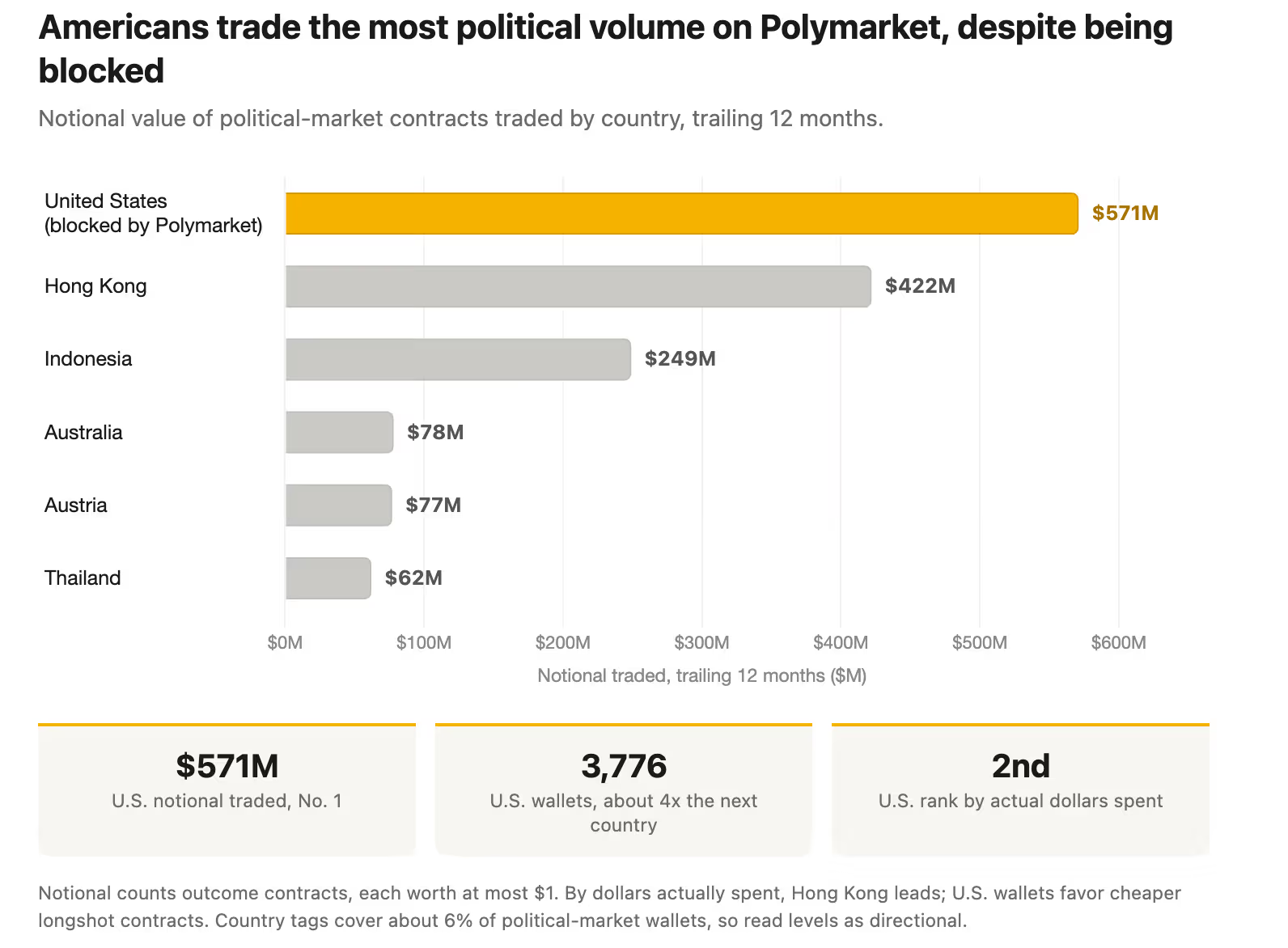

As such, Allium can tie only about 6% of Polymarket’s political-market wallets to a country – so the firm says the figures should be read as directional rather than exact.

Polymarket did not immediately respond to request for comments ahead of U.S. market hours.

Meanwhile, a further interesting bit is what Americans bet on. Geopolitics made up 46% of U.S. notional against 36% for the platform as a whole, while elections drew 16% from U.S. wallets against 32% platform-wide, meaning the American crowd trades foreign wars at nearly three times the rate it trades the elections everyone else favors.

Of U.S. cohort’s twelve biggest markets, five were bets on the Iran war. Its single largest, at $20.8 million, was a novelty market on whether Ukrainian President Volodymyr Zelenskyy would wear a suit.

Those are largely the markets regulated U.S. venues do not carry. Kalshi and Polymarket’s compliant U.S. arm stick mostly to economic data, rate decisions and elections, so the demand flows to the offshore version that lists regime change and ceasefires.

The pattern regulators might fear is the one the data does not show.

On markets that have resolved, U.S. wallets backed the winner 81.9% of the time against 80.3% for everyone else, effectively no edge, and returns if held were nearly identical.

Key Takeaways

- Taiwan Semiconductor posted first-quarter 2026 revenue of $35.9 billion, marking a 40.6% annual increase with a net margin of 50.5%

- Second-quarter guidance projects $39–$40.2 billion in revenue, while full-year expectations call for growth exceeding 30%

- The chipmaker commands approximately 70% of the worldwide market for cutting-edge semiconductor production

- TSMC’s $165 billion U.S. manufacturing initiative in Arizona is progressing ahead of projections, with the initial facility already generating $514 million in profits

- Trading near $434.70 per share, TSM carries a market capitalization close to $2.25 trillion — Wall Street’s average price target stands at $449.38

Taiwan Semiconductor Manufacturing Company currently maintains a market valuation around $2.25 trillion, with shares changing hands at $434.70 on the New York Stock Exchange. The distance to a $3 trillion milestone represents roughly a 34% climb — a threshold the company’s financial performance indicates may arrive sooner than conventional wisdom suggests.

Taiwan Semiconductor Manufacturing Company Limited, TSM

The first quarter of 2026 delivered impressive results. Revenue totaled $35.9 billion, representing a 40.6% jump from the prior-year period. Net income climbed 58.3% year-over-year. Gross margin reached 66.2%, while the net profit margin settled at 50.5% — effectively meaning the company retains half of every revenue dollar as profit.

Executive leadership provided second-quarter revenue guidance ranging from $39 billion to $40.2 billion. For the complete 2026 fiscal year, growth is projected to surpass 30% when measured in U.S. currency, positioning annual revenue comfortably above the $150 billion threshold.

The equity trades with a price-to-earnings multiple of 36.17 and a PEG ratio of 1.09. Over the past year, shares have fluctuated between $223.70 and $479.00. Analyst consensus leans toward a “Buy” recommendation, with the mean price objective at $449.38. Barclays maintains an overweight stance with a $470 price target, while Needham carries a buy rating with a $480 projection.

TSMC recently lifted its quarterly dividend payment to $1.1136 per share from the previous $0.95. The current annualized yield hovers around 1.0%.

TSMC’s Central Role in Artificial Intelligence Infrastructure

Nvidia designs the graphics processing units that drive AI computation centers, but manufacturing isn’t handled in-house. The same applies to AMD and Apple. Each advanced processor from these technology giants originates in TSMC facilities. The semiconductor manufacturer holds approximately 70% of global advanced chip production capacity, with no meaningful competition at the most sophisticated production nodes.

Advanced process technologies at 7 nanometers and smaller now represent 74% of TSMC’s wafer-level revenue. This product composition carries significance — more advanced nodes command premium pricing and deliver superior profitability. As artificial intelligence applications drive requirements toward 3nm and eventually 2nm manufacturing processes, TSMC captures higher revenue per wafer produced.

Every major cloud infrastructure provider deploying GPU arrays — Amazon, Alphabet, Microsoft — relies on TSMC-manufactured semiconductors. Nvidia’s Blackwell architecture, Google’s tensor processing units, and Amazon’s Trainium chips all originate from its production facilities.

United States Expansion Reshapes Geopolitical Risk Profile

The persistent concern surrounding Taiwan Semiconductor centered on geographic concentration — nearly all manufacturing capacity resided in Taiwan. This exposure created what market observers labeled a “Taiwan discount” embedded in the stock price.

That discount is diminishing. TSMC has allocated $165 billion toward its Arizona manufacturing complex, spanning more than 2,000 acres with six fabrication plants in the development pipeline. The inaugural Arizona facility generated $514 million in operating profit during its first year of commercial operation. The second phase, utilizing 3nm process technology, remains on schedule for 2027 completion — running a full year ahead of initial timelines.

Expanded domestic U.S. production capacity provides institutional capital allocators who previously maintained distance a compelling rationale to establish positions.

Regarding institutional ownership, Montrusco Bolton reduced its TSM holdings by 27% during the first quarter, disposing of approximately 188,725 shares. Conversely, FUKOKU Mutual Life Insurance expanded its position by more than 2,500% in the identical timeframe. Institutional investors collectively hold 16.51% of outstanding shares.

Two company insiders also acquired stock in late June at prices ranging from $76.64 to $79.19 per American Depositary Receipt equivalent, adding a combined $155,830 to their personal holdings.

Key Takeaways

- On June 12, 2026, SpaceX launched its IPO at $135 per share, starting trading at $150 and finishing the inaugural session at $160.95 — establishing a valuation exceeding $2 trillion

- The company achieved $18.67 billion in revenue during 2025, marking a 33% annual increase, with Starlink contributing approximately 60% of total sales

- Financial results showed a $4.94 billion net loss for 2025, a dramatic shift from the $791 million profit recorded the previous year

- CEO Elon Musk projects SpaceX could generate $1 trillion in yearly revenue by decade’s end

- By early July, short-sellers had established positions against SPCX, even while nursing substantial losses from the initial price surge

When SpaceX (SPCX) made its debut on the Nasdaq exchange June 12, 2026, the company set its initial offering price at $135 per share. Trading commenced at $150 before settling at $160.95 by market close, catapulting the firm’s market capitalization beyond the $2 trillion threshold in what Reuters characterized as the most significant public offering in history.

Space Exploration Technologies Corp., SPCX

This represents substantial market optimism embedded in the opening price.

Financial reports showed SpaceX brought in $18.67 billion during 2025, reflecting a 33% jump compared to the previous twelve months. Its Starlink satellite internet service represented approximately 60% of these revenues. The constellation currently provides connectivity to about 10.3 million subscribers via roughly 9,600 operational satellites.

This transformation is significant. The company has evolved beyond its identity as solely a space transportation provider — Starlink is rapidly emerging as its primary commercial revenue driver. The predictable income stream from internet subscriptions fundamentally alters the company’s financial structure compared to relying exclusively on launch services.

The rocket business remains crucial. SpaceX’s reusable launch technology serves both private sector clients and government agencies, while simultaneously deploying its own Starlink satellite network. This internal ecosystem reduces operational expenses and maintains schedule control — delivering substantial competitive advantages.

Financial Performance Reveals Complexity

Notwithstanding impressive top-line expansion, SpaceX recorded a $4.94 billion net loss throughout 2025. This marks a substantial departure from the $791 million in profits generated during 2024.

The organization is evidently allocating significant capital toward expanding Starlink and related infrastructure. Long-term shareholders must evaluate whether these investments will ultimately translate into sustainable profitability — and the timeline for achieving it.

Elon Musk has publicly stated SpaceX could reach $1 trillion in annual revenues by 2030. While this represents an ambitious projection, it demonstrates the scale of expansion the company envisions.

Market Sentiment Shows Sharp Division

Stock performance following the IPO has demonstrated significant volatility. Reuters coverage from June 23 highlighted dramatic price fluctuations in SPCX, reflecting intense debate between bullish and bearish investors.

Short-sellers had already established positions against the stock by July 2, despite experiencing paper losses from the post-IPO price appreciation. Early short interest in newly public companies isn’t uncommon — though it indicates skepticism about whether current valuations can be sustained.

With a market cap above $2 trillion, SpaceX is being valued as though its most ambitious objectives are virtually guaranteed.

The optimistic perspective is clear: industry-leading launch capabilities, an expanding internet service business, and exceptional vertical integration. For those investing with extended time horizons, these represent genuine and sustainable competitive strengths.

As of July 2, 2026, short-sellers maintained their bearish positions on SPCX, while post-IPO price volatility keeps the stock under intense Wall Street scrutiny.

Crypto World

5 Key Stocks Commanding Wall Street’s Attention This Week: SpaceX, Delta (DAL), PepsiCo (PEP), Nvidia (NVDA), and TSMC (TSM)

Key Takeaways

- SpaceX becomes part of the Nasdaq-100 index, prompting purchases from passive investment vehicles

- Delta Air Lines begins the Q2 reporting cycle with insights into travel demand and consumer behavior

- PepsiCo’s quarterly report will reveal whether pricing power remains intact for consumer packaged goods

- Nvidia continues attracting investor scrutiny amid evolving sentiment around artificial intelligence capital expenditures

- Taiwan Semiconductor draws attention before its upcoming report due to its critical position in the chip supply chain

The second-quarter reporting period has commenced, and market participants are closely monitoring five companies that stand out this week. Here’s what’s driving investor interest.

SpaceX Makes Its Nasdaq-100 Entry

SpaceX becomes an official component of the Nasdaq-100 Index during the current week. This addition will prompt mandatory purchases from passive funds and exchange-traded products tracking the benchmark, potentially enhancing trading volume and expanding ownership.

Space Exploration Technologies Corp., SPCX

Market observers continue monitoring Starlink’s global rollout, government launch agreements, and ongoing Starship development initiatives. Share price fluctuations have characterized the stock since going public, with volatility expected to persist.

Analysts anticipate SpaceX will maintain its position among closely followed growth equities throughout 2026.

Delta Air Lines Launches Reporting Season

Delta Air Lines takes center stage as earnings season begins in earnest this week. Airline financial reports provide early indicators of spending patterns across consumer and corporate segments.

Key metrics under examination include fare pricing dynamics, reservation volumes, and cross-border travel activity. Declining fuel costs have reduced a major expense category, potentially improving operating margins.

Positive forward guidance from Delta could generate optimism throughout the broader hospitality and tourism industries.

PepsiCo Provides Consumer Spending Snapshot

PepsiCo delivers quarterly results this week, offering critical visibility into worldwide consumer purchasing patterns. Analysts are questioning whether customers continue accepting elevated price points or beginning to resist.

The company’s diversified portfolio spanning beverages and packaged snacks positions it as a comprehensive barometer of consumer behavior. Management commentary regarding raw material expenses and profitability could influence forecasts for comparable companies reporting subsequently.

Nvidia Maintains Relevance Without Reporting

Nvidia isn’t scheduled to announce results this week, yet it continues exerting significant influence across equity markets. Investment activity surrounding artificial intelligence infrastructure keeps the stock at the forefront, with Nvidia dominating the GPU and AI accelerator landscape.

Following recent semiconductor sector volatility, market watchers are assessing whether institutional capital flows back toward AI frontrunners or continues diversifying. Developments concerning hyperscaler capital expenditure or processor demand could trigger rapid price movements.

Taiwan Semiconductor Draws Attention Before Earnings

Taiwan Semiconductor releases financial results in the coming week, but strategic positioning is already underway. As the foundry partner for Nvidia, Apple, AMD, and Qualcomm, the company serves as a premier indicator of worldwide semiconductor appetite.

Robust projections from TSMC would validate continued strength in AI-related infrastructure spending. Conversely, cautious commentary could pressure valuations across chip manufacturers broadly.

South Africa’s Revenue Service has published draft guidance on how crypto assets should be taxed under the country’s current tax laws. The proposal seeks public feedback until August 31, 2026, before SARS moves toward a final version.

Summary

- SARS says crypto is not currency, keeping digital assets inside income and capital gains rules.

- The draft treats trades, swaps and crypto payments as possible tax events under current law.

- Public comments remain open until August 31 as South Africa clarifies crypto tax reporting.

The draft does not create a new crypto tax law. It explains how current rules under theIncome Tax Act, 1962 may apply to people who buy, sell, swap, spend, mine, stake or receive crypto assets.

SARS says the guide covers selected income tax and capital gains tax issues linked to crypto. It also says the draft does not deal with value-added tax, meaning VAT treatment remains outside the scope of this document.

Crypto treated as an asset, not money

The draft repeats SARS’ long-held position that crypto assets are not legal tender or foreign currency. Instead, SARS treats them as intangible assets for tax purposes.

The agency said “crypto assets are not ‘currency’ and, consequently not ‘foreign currency’.” That wording matters because it places crypto inside current income and capital gains rules rather than foreign exchange rules.

Crypto.news previously reported that SARS had already viewed crypto as an asset of an intangible nature. The new draft expands that position into a more detailed guide for taxpayers.

The draft says tax treatment depends on the facts of each case. A person who trades often may face income tax treatment, while a long-term holder may fall under capital gains tax if the facts support that view.

Trades, swaps and spending may trigger tax

The draft guide says selling crypto for fiat may create a tax event. It also covers crypto-to-crypto swaps, crypto payments for goods or services, mining, staking, airdrops, hard forks and decentralized finance activity.

SARS places strong weight on the taxpayer’s intention. It says officials may assess why a person bought the asset, how long they held it, how often they traded and what they planned to do with it.

The agency said “a taxpayer’s intention regarding an asset may change over time.” This means a person may start as a long-term holder but later act more like a trader if their behavior changes.

The draft also says donations tax may apply because crypto can fall within the meaning of property. That may matter when a person gives crypto away without receiving payment in return.

Reporting pressure grows as adoption rises

SARS already says normal income tax rules apply to crypto assets. Taxpayers must declare crypto gains or losses in the tax year in which they receive or accrue them.

The tax authority also says failure to declare taxable crypto income can lead to interest and penalties. It has broad legal powers to collect third-party financial data during tax checks.

South Africa has also adopted theCrypto-Asset Reporting Framework. Under CARF, crypto service providers must collect and report selected user and transaction data to SARS.

The first CARF reporting period runs from March 1, 2026, to February 28, 2027. SARS says individual taxpayers do not file CARF reports directly, but they must still declare crypto transactions in their income tax returns.

The draft arrives as South Africa remains one of Africa’s larger crypto markets.Chainalysis said South Africa received about $26 billion in crypto value over a one-year period covered in its 2024 regional report.

The public comment window gives users, tax advisers and crypto firms time to respond. For now, SARS is seeking clearer treatment under existing law, not a separate tax system for digital assets.

Key Takeaways

- Micron’s Q3 results showed revenue of $41.46 billion, representing a 346% year-over-year surge, with earnings per share of $25.11 crushing expectations by more than $4.

- CEO Sanjay Mehrotra explained to Jim Cramer that the memory chip supply crisis is structural rather than cyclical, with new manufacturing facilities delayed until 2027–2028.

- Both HBM3E and HBM4 memory products are completely sold out through 2027, supported by $22 billion in advance customer deposits from hyperscalers.

- The company has delivered over $1 billion in HBM4 shipments and asserts technological superiority over competitors SK Hynix and Samsung in DRAM and NAND sectors.

- MU shares are currently trading around $970, retreating from their 52-week peak of $1,255, while maintaining approximately 244% gains year to date.

Micron Technology (MU) shares are hovering near $970, having pulled back from the 52-week high of $1,255 reached on June 25, yet the stock maintains impressive gains of approximately 244% year to date. Despite the recent decline, the fundamental narrative remains robust — a point CEO Sanjay Mehrotra emphasized during his appearance on Jim Cramer’s Mad Money on June 30.

Cramer posed the question dominating investor sentiment: what’s the timeline for resolving the memory shortage? Mehrotra’s response was unambiguous.

“The industry requires greenfield capacity. This means brand new construction of clean rooms. Those clean rooms require substantial time from initial groundbreaking to producing the first wafers.”

The company’s initial Idaho fabrication facility will begin wafer production by mid-2027, with full-scale manufacturing ramping predominantly throughout 2028. A secondary Idaho fab becomes operational by late 2028. The New York manufacturing site follows subsequently. Translation: the supply constraints persist for years.

Cramer previously highlighted Micron’s Q3 performance as among the most impressive earnings surprises he’s witnessed. The figures validate that assessment. Revenue totaled $41.46 billion, representing a 346% year-over-year increase from $9.30 billion. Non-GAAP earnings per share reached $25.11, surpassing the $20.78 consensus estimate. Free cash flow climbed to a company record of $18.30 billion.

The Q4 outlook is equally remarkable: $50 billion in projected revenue, approximately 86% gross margins, and anticipated EPS of $31.00.

HBM4 Technology Breakthrough

Both HBM3E and HBM4 memory products are entirely sold out through the end of calendar year 2027, with order backlogs already stretching into 2028. Major hyperscalers have deposited $22 billion in advance payments to guarantee future supply.

During the earnings conference call, Mehrotra revealed that Micron had already delivered over $1 billion worth of HBM4 products. This milestone transcends simple revenue metrics — it represents a technological achievement. HBM4 ranks as the most sophisticated memory product globally to manufacture, and Micron stands as the sole U.S.-based producer delivering it at commercial scale.

When Cramer directly questioned whether Micron had overtaken SK Hynix and Samsung, Mehrotra responded definitively: “Regarding DRAM and NAND technology, we maintain clear technology leadership.” The company currently holds approximately 65,000 patents.

Cramer also highlighted the valuation opportunity. Despite the substantial rally, MU shares trade at less than eight times earnings.

Domestic Manufacturing Expansion

Micron has pledged $200 billion toward U.S.-based manufacturing and research and development initiatives, targeting the creation of over 90,000 jobs. Additionally, the company is investing $300 million in developing a domestic semiconductor workforce through apprenticeship programs, community college partnerships, and university collaborations.

Cramer mentioned Morris Chang’s assertion that U.S. chip production costs exceed Taiwan’s by 50%. Mehrotra countered by referencing Micron’s current Manassas, Virginia facility, which already manufactures advanced memory solutions for automotive, defense, medical, and aerospace applications.

Addressing the consumer segment, Mehrotra acknowledged that surging AI data center demand is constraining availability for smartphone and PC memory, driving up consumer device prices. He noted that Micron maintains approximately 40% of its business in consumer markets to preserve portfolio diversification.

MU trades at $970 as of July 2, with fourth-quarter guidance projecting $50 billion in revenue and EPS of $31.00 approaching.

“If we don’t have a euro on the blockchain, the banks will use the dollar because it’s there, it’s available and it has a lot of liquidity,” Sell told CoinDesk. Rather than each bank issuing its own euro stablecoin, Qivalis is encouraging them to work together in a single shared network.

Sell said Qivalis is not trying to compete directly with USDC. Its goal is to give European banks, businesses and payment firms a regulated euro alternative as tokenized finance expands. That would allow institutions to settle in euros rather than converting assets into dollars and back again.

As more banks join, the consortium also benefits from the same network effects driving USDC’s adoption. “The more banks we have in the consortium, the better. Our network has stronger network effects,” Sell said.

Investing in infrastructure

Agant’s MacKenzie said he sees the same trend emerging in the U.K.

Banks are no longer focused only on digital assets, he said. Instead, they are investing in the infrastructure needed to connect stablecoins with traditional finance for payments, treasury operations and settlement. Businesses generally prefer settling obligations in their own currencies, he said, rather than converting into U.S. dollars first.

That may be the impetus for introducing non-dollar stablecoins, such as Societe Generale’s EUR CoinVertible (EURCV), Credit Agricole’s EURXT and Qivalis’ impending offering. But existing is insufficient. It’s how the bank deploys the stablecoin to its customers that will determine its success.

Novak Djokovic vs Roman Safiullin LIVE: Wimbledon 2026 fourth round latest score and updates

Tesla Model Y Dominates as Top Selling EV in US 2026 So Far with Strong Sales Lead Over Rivals

Anthropic Faces a New $75 Million Lawsuit for Pirating Books to Train Claude AI

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: High Hopes

-

Politics2 days ago

Politics2 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Crypto World6 days ago

Crypto World6 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

News Videos7 days ago

News Videos7 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

News Videos5 days ago

News Videos5 days agoHow to Build INSANE Live Financial Dashboards With Claude

-

Tech6 days ago

Tech6 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Business6 days ago

Business6 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

NewsBeat11 hours ago

NewsBeat11 hours agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Business6 days ago

Business6 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

-

Sports4 days ago

Sports4 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

NewsBeat5 days ago

NewsBeat5 days agoPresenter Caroline Flack’s brother Paul Flack dies aged 55

-

Crypto World3 days ago

Crypto World3 days agoBinance stock trading tops $1B in first month after launch

-

Crypto World4 days ago

Crypto World4 days agoAlibaba-affiliate Ant Group enters the humanoid robot market with 12 deals

-

NewsBeat3 days ago

NewsBeat3 days agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

Crypto World4 days ago

Crypto World4 days agoAirdrop Registration Becomes Key Focus For Remittix As RTX Launch Updates Approach

-

Business4 days ago

Business4 days agoMeta Platforms Stock Jumps 7% Today as Bloomberg Reports Company Plans to Enter the Cloud Business

-

Business2 days ago

Business2 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Crypto World3 days ago

Crypto World3 days agoBinance Re-Enters Philippines As EU MiCA Rules Restrict Access

-

Tech4 hours ago

Tech4 hours agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

Crypto World2 days ago

Crypto World2 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

You must be logged in to post a comment Login